Embed Size (px)

Citation preview

➀➀

➀❷❸❹ 2003 Research Quarterly

Human Capital—The Elusive Asset

Measuring and Managing HumanCapital: A Strategic Imperative for HR

Leslie A. Weatherly, SPHR HR Content Expert

ResearchSHRM

S O C I E T Y F O R

H U M A N

R E S O U R C E

M A N A G E M E N T

HumanCapital

HUMAN CAPITAL IS ARGUABLY THE MOST VALUABLE

ASSET HELD BY AN ORGANIZATION TODAY. It is also

the most elusive asset to manage for a variety of rea-

sons. The primary purpose of this article is to describe

the terminology associated with human capital and its

context within an organization. Its secondary purpose is to

discuss the implications for the HR professional. HR prac-

tice leaders who are serious about making a difference

must be able to “measure” the business impact HR-driven

programs have on their organizations in order to demon-

strate the merit and worth of these programs. Only by

ensuring that HR metrics are recognized and valued on an

equal footing with other business metrics routinely used

by the CEO and management can the HR practice leader

be assured an equitable position as a key member of the

senior management team. These metrics must, of course,

measure the value and return on investment in human

capital to the organization. This is both a challenge and a

strategic imperative for today’s HR professional.

ResearchSHRM

Human Capital—The Elusive Asset 1

➀❷❸❹ 2003 SHRM®Research Quarterly

Calculating the value of human capital (HC)is not easy—because human capital is not

like other capital. With rare exception, HCsimultaneously represents the single greatestpotential asset and the single greatest poten-tial liability that an organization will acquire asit goes about its business. While there areother intangible assets, HC is the only intangi-ble asset that can be influenced, but nevercompletely controlled, invested in wisely, orwasted thoughtlessly, and still have tremen-dous value. These distinguishing features arewhat make HC unique, and also what makes itan elusive asset.

“Although we would agree that most CEOsare acutely aware of their investments intheir most valuable asset (salaries, benefits,training, recruitment programs and the like),almost none could tell you what their mostvaluable asset is worth.”1

Perhaps the best place to begin this discus-sion is to outline the business elements thatcreate value in an organization in order to laythe groundwork for understanding the contextwithin which human capital carries out itswork.

Organizational value is comprised of threemajor classes of assets that are integral to anorganization’s ability to produce goods andservices. These are:

� Financial Assets: Financial assets includeassets such as cash and marketable secu-rities, and may also be referred to as finan-cial capital;

� Physical Assets: Physical assets includesuch tangible assets as property, plant andequipment, and other furnishings; and

� Intangible Assets: Examples of intangibleassets, also called intangible capital,include intellectual capital (patent formulas,product designs, and process technology,i.e., the methods that delineate the stepsin a process), goodwill, and human capital.

Definition of Human Capital

Surprisingly, human capital is not the people ofan organization per se. That’s because peopleexercise control over their human capital andare free to invest it as they see fit in differentaspects of their lives: family, community inter-est groups, observance of religious beliefs,physical fitness pursuits, other outside inter-ests, and work. As such, the following defini-tion of human capital is offered:

A company’s human capital asset is the collective sum of the attributes, life experience, knowledge, inventiveness,energy, and enthusiasm that its peoplechoose to invest in their work.

Clarifying Intangible Capital

So, what is intangible capital, really? Intangiblecapital or intangible assets are as valuable asfinancial and physical assets; you just can’tdiscern them by touch, i.e., they are withoutphysical substance and are non-monetary.They are held by an entity to produce or supplygoods or services, to rent or lease to others,or for administrative purposes. For reasonsalready described, they can be difficult tomeasure and are not always addressed in con-crete terms in the typical public accountingdisclosure.

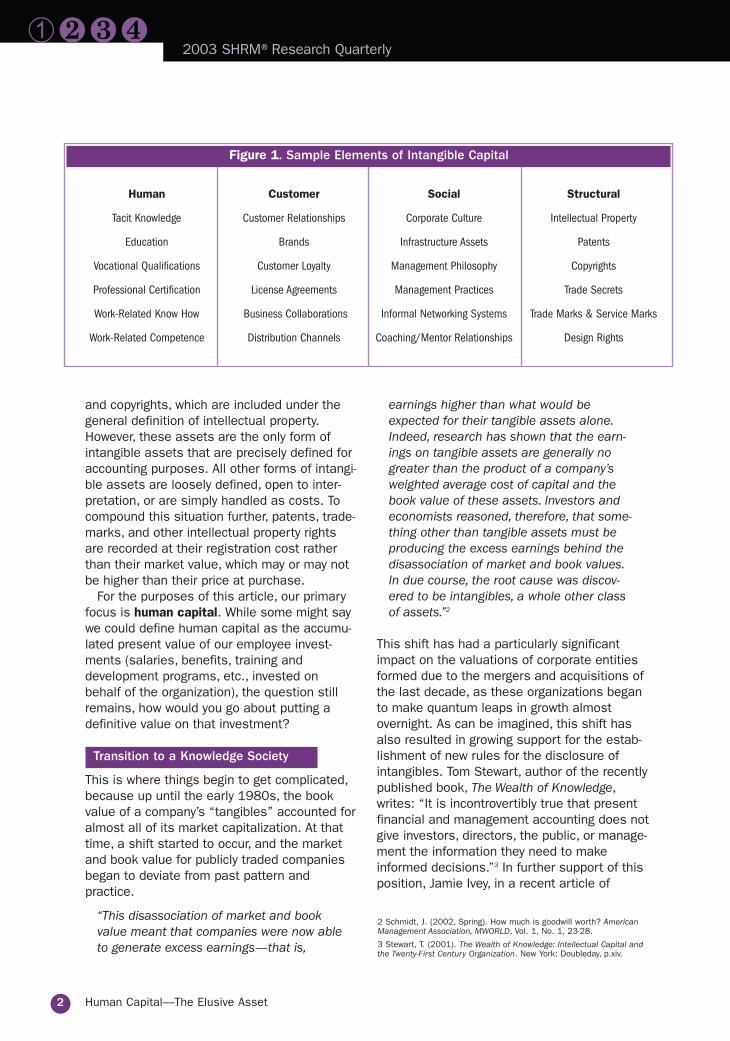

Intangibles also comprise other forms ofcapital (see Figure 1). From a pure accountingperspective, financial assets and physicalassets are generally easier to classify andvalue than intangible assets. For example,intellectual property is legally defined andincludes such things as patents, trademarks,

➀❷❸❹

Human Capital—The Elusive Asset

1 DiFrancesco, J. (2002, March). Managing human capital as a realbusiness asset. IHRIM Journal, Vol. VI, No. 2, 7-16.

2 Human Capital—The Elusive Asset

➀❷❸❹ 2003 SHRM®Research Quarterly

and copyrights, which are included under thegeneral definition of intellectual property.However, these assets are the only form ofintangible assets that are precisely defined foraccounting purposes. All other forms of intangi-ble assets are loosely defined, open to inter-pretation, or are simply handled as costs. Tocompound this situation further, patents, trade-marks, and other intellectual property rightsare recorded at their registration cost ratherthan their market value, which may or may notbe higher than their price at purchase.

For the purposes of this article, our primaryfocus is human capital. While some might saywe could define human capital as the accumu-lated present value of our employee invest-ments (salaries, benefits, training anddevelopment programs, etc., invested onbehalf of the organization), the question stillremains, how would you go about putting adefinitive value on that investment?

Transition to a Knowledge Society

This is where things begin to get complicated,because up until the early 1980s, the bookvalue of a company’s “tangibles” accounted foralmost all of its market capitalization. At thattime, a shift started to occur, and the marketand book value for publicly traded companiesbegan to deviate from past pattern and practice.

“This disassociation of market and bookvalue meant that companies were now ableto generate excess earnings—that is,

earnings higher than what would beexpected for their tangible assets alone.Indeed, research has shown that the earn-ings on tangible assets are generally nogreater than the product of a company’sweighted average cost of capital and thebook value of these assets. Investors andeconomists reasoned, therefore, that some-thing other than tangible assets must beproducing the excess earnings behind thedisassociation of market and book values.In due course, the root cause was discov-ered to be intangibles, a whole other classof assets.”2

This shift has had a particularly significantimpact on the valuations of corporate entitiesformed due to the mergers and acquisitions ofthe last decade, as these organizations beganto make quantum leaps in growth almostovernight. As can be imagined, this shift hasalso resulted in growing support for the estab-lishment of new rules for the disclosure ofintangibles. Tom Stewart, author of the recentlypublished book, The Wealth of Knowledge,writes: “It is incontrovertibly true that presentfinancial and management accounting does notgive investors, directors, the public, or manage-ment the information they need to makeinformed decisions.”3 In further support of thisposition, Jamie Ivey, in a recent article of

2 Schmidt, J. (2002, Spring). How much is goodwill worth? AmericanManagement Association, MWORLD, Vol. 1, No. 1, 23-28.

3 Stewart, T. (2001). The Wealth of Knowledge: Intellectual Capital andthe Twenty-First Century Organization. New York: Doubleday, p.xiv.

Figure 1. Sample Elements of Intangible Capital

Human Customer Social Structural

Tacit Knowledge Customer Relationships Corporate Culture Intellectual Property

Education Brands Infrastructure Assets Patents

Vocational Qualifications Customer Loyalty Management Philosophy Copyrights

Professional Certification License Agreements Management Practices Trade Secrets

Work-Related Know How Business Collaborations Informal Networking Systems Trade Marks & Service Marks

Work-Related Competence Distribution Channels Coaching/Mentor Relationships Design Rights

Human Capital—The Elusive Asset 3

➀❷❸❹ 2003 SHRM®Research Quarterly

Corporate Finance states, “A balance sheetprovides a snapshot of a company’s assets atany one moment in time, but how useful issuch a snapshot when a company’s currency isits knowledge and that knowledge can betransported in a split second? Enron is anexample of the problem. An investor could havelooked at his balance sheet in late Novemberand have been perfectly satisfied as to thesecurity of his investment, but by December 2his investment had vanished in smoke.”4

Even still, the Financial AccountingStandards Board (FASB) has been reluctant toeffect a change to a system of accounting thatreflects the magnitude of this shift and pro-vides a clearly delineated standard method ofaccounting for human capital as an intangibleasset. The investment community appears tobe reluctant to initiate change as well, in partdue to the failure of so many new economy(dot-com) companies, coupled with concernsabout the interpretation and application of gen-erally accepted accounting principles (GAAP) bylarge corporations over the last year (e.g.,Arthur Andersen, Enron, WorldCom).Apparently, the feeling is that the dust should settle before reform takes place.

What we do know at this time is that it is notunusual for the value of a company’s intangibleassets to exceed its book (tangible) assets bytwo- or threefold. In extreme cases, this ratiocan be quite significant. For example, in 1996Microsoft’s ratio of intangible assets to book(tangible) assets exceeded 11 to one. 5

So what is the basis for this paradigm shift,i.e., the routine use of the phrase “intangibleassets” in a company’s vocabulary? In brief, wehave moved from an industrial society, wherethe primary source of wealth was machinery, toa knowledge society, where the primary sourceof wealth is human capital. In essence, we

have undergone a metamorphosis. “In the clos-ing years of the 20th century, management hascome to accept that people, not cash, build-ings, or equipment, are the critical differentia-tors of a business enterprise.”6

The reality of the situation today is that 60percent to 70 percent of a company’s expendi-tures on average are labor related. Data fromthe Brookings Institute will help to put theimportance of the measurement and manage-ment of human capital/knowledge assets intoperspective. In 1982, hard assets represented62 percent of a company’s market value onaverage. By 1992, this figure had dropped to38 percent.7 More recent studies place theaverage market value of hard assets in manycompanies as low as 30 percent.8 In otherwords, up to 70 percent of a company’sexpenses may be related to human capital. Itwould seem nothing less than a businessimperative, therefore, that the challenge of ataxonomy and a valuation of human capital bepursued.

The Dynamics of an Organization’s Total Capital Environment

It is important to note that a business is notjust a storehouse for knowledge, but a viable,dynamic environment. Vital relationships existthroughout an organization and interactionsoccur with varying degrees of intensity toensure that knowledge (the tacit knowledge ofthe group found in the form of organizationalculture, the explicit knowledge of an individual,or the structural knowledge of a data ware-house) gets converted from one form toanother through, perhaps, multiple transforma-tions, all for the purpose of adding value.These interactions result in the creation of newknowledge, organizational learning, and, onoccasion, innovation.

Whereas human capital represents theknowledge, experience, and attributes ofemployees, additional types of capital haveemerged in the literature. Structural capitalrepresents the codified knowledge that resideswithin an organization (policy and proceduremanuals, databases, corporate files, depart-mental and organizational processes). Socialcapital represents the value that can be foundamong the relationships within the organization

4 Ivey, J. (2002, March). Accounting for knowledge. Corporate Finance,Issue 208, 19-20.

5 Dzinkowski, Ramona, (2000, February). The measurement and man-agement of intellectual capital: An introduction. ManagementAccounting; London; Vol. 78, Issue 2, 32-36.

6 Fitz-enz, J. (2000). The ROI of Human Capital. New York: AmericanManagement Association, p. 1.

7 Dzinkowski, Ramona, (2000, February). The measurement and man-agement of intellectual capital: An introduction. ManagementAccounting; London; Vol. 78, Issue 2, 32-36.

8 Bassi, L. (2001, Spring). Human capital advantage: Developing met-rics for the knowledge era. Retrieved August 27, 2002, fromhttp://www.linezine.com/4.2/articles/lbhca.htm

4 Human Capital—The Elusive Asset

➀❷❸❹ 2003 SHRM®Research Quarterly

to facilitate the transfer of knowledge.Examples of social capital could include men-tor/mentee relationships, informal networks oflong-term interdepartmental work associates,and peer relationships. Finally, customer capital (also referred to as organizationaland/or relational capital) is the corporate mem-ory possessed by those who have relationshipswith suppliers, customers, and any other out-side entity that interacts with the firm for thepurpose of accomplishing the work of theorganization. It is the successful ameliorationof each of these forms of capital and theireffective blending that forms the basis forimproving organizational value. (see Figure 1.)

The predominant objective of any investmentis to minimize risk and maximize return. So,how should this statement be interpreted inrelation to human capital, the elusive asset?

What Gets Measured Gets Managed

What should be apparent at this point is thatthe measurement of human capital will neverbe as straightforward as calculating the valueof a tangible asset; there are simply too manyvariables involved to make this practical.However, it should also be obvious that we canno longer fail to recognize the importance ofseeking to develop, test, and refine appropriatemethodologies to measure the value of whathas become for all intents and purposes ourprimary asset. To give an old adage its due:“what gets measured gets managed.” Simplyput, what gets measured stands a betterchance of becoming successful within the con-text of an applied strategic business plan. If weare not capable of measuring the true value ofhuman capital in our organizations, then wecannot begin to appreciate in quantifiableterms its true potential. It would follow thenthat we are not able to envision and reap thefull measure of the benefits that this essentialasset can afford our organization(s). We cannotafford to let that happen.

Why is it Important to Know How to Value Human Capital?

Human resources, like other resources, arefinite. What makes them especially unique,however, is that they are intangible. Human

capital can be developed and cultivated, but itcan also decide to leave the organization,become sick, disheartened, and even influenceothers to behave in a way that may not be tothe advantage of an employer, thus usurping orsiphoning off resources intended for use else-where in the organization. In other words, theperformance of an organization’s human capi-tal is not always predictable and/or within thecontrol of the employer. So, the measurementand the management of human capitalbecomes part art and part science.

Senior management requires a referenceindex, therefore, for valuing human capitalwithin the organization. With the right tools andcontext, management will be in an enhancedposition to make decisions that will drive howthis resource, along with other finite financial,product, and customer resources can best beallocated.

What are the Implications for the Human Resources Function?

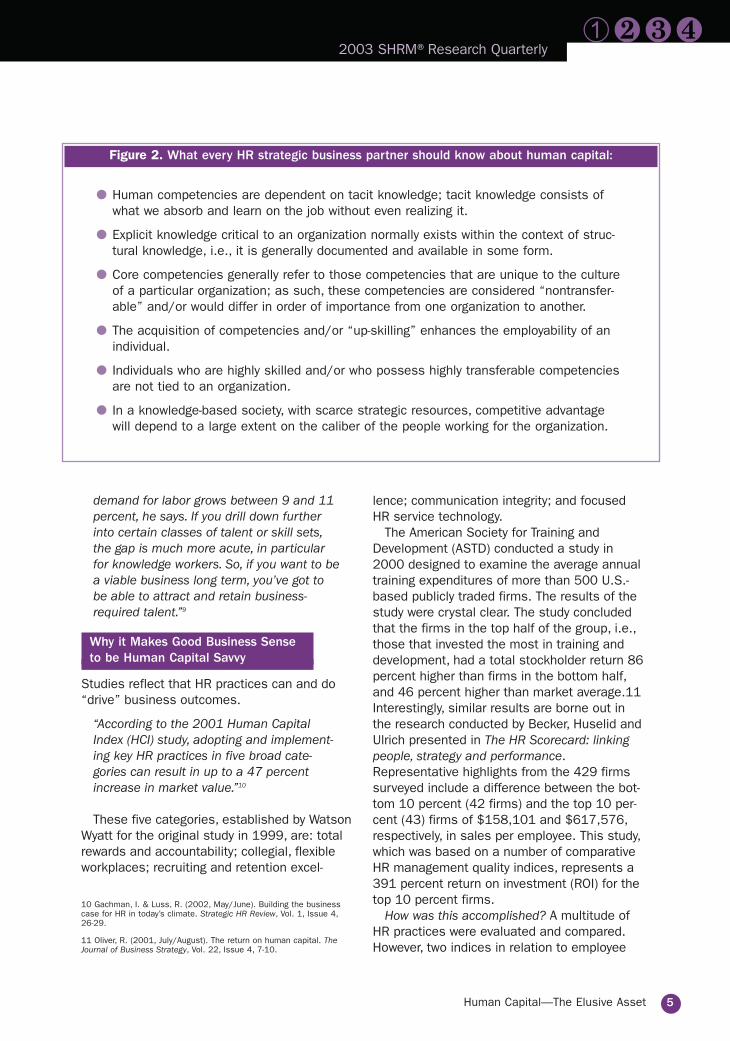

It is incumbent upon HR professionals today tobe familiar with not only HR operations, i.e.,core competencies, but also those aspects ofHR that will have the most significant impacton long-term business growth and develop-ment. These aspects include organizationaldevelopment and organizational effectiveness.As such, it is critical that HR strategic businesspartners become conversant in these areas.An example of information every HR strategicbusiness partner should know about humancapital is provided in Figure 2.

This, combined with the fact that humanresources are simply becoming scarce shouldgive each of us pause to carefully consider ourstaffing, retention, and succession planningstrategies.

“The war for talent will continue over thenext decade or so, asserts Richard Kleinert,global practice leader for the HumanResources Strategies Group at DeloitteTouche Tohmatsu, the professional servicesfirm. The supply of labor is projected to growbetween 6 and 7 percent, while the

9 Woods, B. (2001, July). Harvesting your human capital. Chief Executive. Available from http://www.chiefexecutive.net/ceoguides/july2001/p12.html

Human Capital—The Elusive Asset 5

➀❷❸❹ 2003 SHRM®Research Quarterly

demand for labor grows between 9 and 11percent, he says. If you drill down furtherinto certain classes of talent or skill sets,the gap is much more acute, in particularfor knowledge workers. So, if you want to bea viable business long term, you’ve got tobe able to attract and retain business-required talent.”9

Why it Makes Good Business Sense to be Human Capital Savvy

Studies reflect that HR practices can and do“drive” business outcomes.

“According to the 2001 Human CapitalIndex (HCI) study, adopting and implement-ing key HR practices in five broad cate-gories can result in up to a 47 percentincrease in market value.”10

These five categories, established by WatsonWyatt for the original study in 1999, are: totalrewards and accountability; collegial, flexibleworkplaces; recruiting and retention excel-

lence; communication integrity; and focusedHR service technology.

The American Society for Training andDevelopment (ASTD) conducted a study in2000 designed to examine the average annualtraining expenditures of more than 500 U.S.-based publicly traded firms. The results of thestudy were crystal clear. The study concludedthat the firms in the top half of the group, i.e.,those that invested the most in training anddevelopment, had a total stockholder return 86percent higher than firms in the bottom half,and 46 percent higher than market average.11 Interestingly, similar results are borne out inthe research conducted by Becker, Huselid andUlrich presented in The HR Scorecard: linkingpeople, strategy and performance.Representative highlights from the 429 firmssurveyed include a difference between the bot-tom 10 percent (42 firms) and the top 10 per-cent (43) firms of $158,101 and $617,576,respectively, in sales per employee. This study,which was based on a number of comparativeHR management quality indices, represents a391 percent return on investment (ROI) for thetop 10 percent firms.

How was this accomplished? A multitude ofHR practices were evaluated and compared.However, two indices in relation to employee

Figure 2. What every HR strategic business partner should know about human capital:

� Human competencies are dependent on tacit knowledge; tacit knowledge consists ofwhat we absorb and learn on the job without even realizing it.

� Explicit knowledge critical to an organization normally exists within the context of struc-tural knowledge, i.e., it is generally documented and available in some form.

� Core competencies generally refer to those competencies that are unique to the cultureof a particular organization; as such, these competencies are considered “nontransfer-able” and/or would differ in order of importance from one organization to another.

� The acquisition of competencies and/or “up-skilling” enhances the employability of anindividual.

� Individuals who are highly skilled and/or who possess highly transferable competenciesare not tied to an organization.

� In a knowledge-based society, with scarce strategic resources, competitive advantagewill depend to a large extent on the caliber of the people working for the organization.

10 Gachman, I. & Luss, R. (2002, May/June). Building the businesscase for HR in today’s climate. Strategic HR Review, Vol. 1, Issue 4,26-29.

11 Oliver, R. (2001, July/August). The return on human capital. TheJournal of Business Strategy, Vol. 22, Issue 4, 7-10.

6 Human Capital—The Elusive Asset

➀❷❸❹ 2003 SHRM®Research Quarterly

training and development stood out. The firstinvolved the number of hours devoted to thetraining of employees during their initial year ofemployment; 35.02 hours for the bottom 10percent versus 116.87 hours for the top 10percent. The second involved the number ofhours devoted to employee training annually,i.e., after their first year of employment; 13.4hours for the bottom 10 percent of firms and72 hours for the top 10 percent of firms.12

Clearly, the continuous investment in trainingand education by the top 10 percent is provid-ing a substantial ROI.

Optimizing the Human Capital Return on Investment (ROI)

Following are what some of the top HR strate-gic business partners and their organizationsare doing to build and maintain their humancapital investment:

1. Management’s stance in relation to continu-ing education and on-the-job training foremployees is the single most influential fac-tor in the success of workplace learningprograms; the president/CEO holds the keyin this regard, i.e., if the CEO is convincedthat the return on investment (ROI) justifiesthe expense and stands firmly behind a pro-gram, the rest of the management team willfollow.

RECOMMENDATIONS: Get your CEO firmlybehind your workplace learning programs byfocusing awareness on the development ofpeople (management and employees alike)as a major source of obtaining and main-taining competitive advantage; fully substan-tiate the ROI for any program endorsed byHR; this means knowing upfront the keyresults areas (KRAs) for your business, i.e.,what to measure and understanding whatthe ongoing measures of success will be. Inother words, once the training programshave been put in place, how will the criticalsuccess factors related to these programsbe monitored over the long term and/orreported to senior management? A compre-hensive reporting and evaluation programwill be required.

2. Executives have long argued that superior“people management practices” will resultin “superior business profits.” The questionremains, however, how do you go aboutmeasuring progress? Thousands of texts,theories, articles, and working papers havebeen put forward and the best thought lead-ers of the past decade have offered theiropinions on this subject. The good news isthat it appears that we are making progress.The answer has to do, in part, with the uni-versal acceptance of the “language of num-bers.” This is a language that can be readilyunderstood across organizational and func-tional lines and, as importantly, is universal-ly understood outside the organization aswell, i.e., within a “global context.”

RECOMMENDATIONS: Get acquainted withthe business metrics that are relied uponby your CEO and management team to runthe business. Establish associated HR busi-ness metrics that are aligned with the goalsand objectives of your organization; thisincludes establishing an initial baseline foreach measurement, as well as industrybenchmarks for comparative purposes.Ensure that the metrics established are notsimply based on transactions, but are clear-cut, indisputable measures of the success,failure, improvement, or decline of any pro-gram or function for which HR provides over-sight; frame recommendations related tothese programs based on the qualitativeand quantitative information obtained fromthis measurement process.

3. Technology-based learning tools, such asaudiocasts, Webcasts, computer-basedlearning software, and simulated job train-ing models enhance the opportunity for indi-vidual and group learning in remote set-tings. These tools are especially useful fornew hire orientation, new job or task certifi-cation, and safe work practices trainingwhere the communication of substantial

12 Becker, B. E., Huselid, M. A., & Ulrich, D. (2001). The HR Scorecard: linking people, strategy and performance. Boston, Massachusetts:Harvard Business School Press, p. 16-17.

Human Capital—The Elusive Asset 7

➀❷❸❹ 2003 SHRM®Research Quarterly

information in a consistent format is impor-tant and cost is a consideration.

RECOMMENDATIONS: Introduce and/oroptimize the use of HR e-technologies, suchas HR self-service options on the corporateintranet, distance learning opportunities,regional staff meetings, etc., in order toimprove staff interaction and networkingopportunities, convenience, and to reducethe cost of employee learning opportunitiesat the same time.

4. Human resource development is responsi-ble for anticipating and preparing the work-force of the future; at the same time, thisfunction cannot lose sight of the fact that itmust maintain the competencies of theexisting staff. This is a double-edged swordand requires balance and perspective.

RECOMMENDATIONS: Develop continuingeducation and training programs designedto maintain core competencies; partner withuniversities, colleges, and other learninginstitutions to supplement in-house trainingefforts when economically feasible and/ortime constraints make this a requirement;encourage active participation by interestedparties in setting objectives and design andimplementation processes to increase thelikelihood of program success.

5. In an environment where mergers andacquisitions are commonplace, and “right-sizing and downsizing” are a natural by-product of these transactions, many employ-ers are beginning to assume responsibilityfor employee career development opportuni-ties, in addition to “on-the-job” training anddevelopment. Career pathing and/or “com-petency enhancement” is based on thepremise that individuals should be planningtheir next career move while they are stillemployed and “stress-free.” The benefitsthat accrue to an employer under thisstrategic concept are: enhanced employeemorale and loyalty, a more competent work

force prepared for future internal growth,and reduced expenditures associated withthe cost of employees in transition (i.e., thecost of outplacement, unemployment insur-ance, etc.) in the event the employmentrelationship must come to an end. This isdue to the fact that the departing employ-ee(s) in this scenario should possess skillsets and competencies that give them acompetitive edge in the marketplace.

RECOMMENDATIONS: Develop continuingeducation and training programs with afocus on career planning and competencyenhancement; establish career ladderswhen feasible; conduct cost benefits analy-sis and determine ROI on a periodicbasis—adjust programs based on businesscase; openly communicate why the programis mutually beneficial to the organizationand its employees.

Conclusion

If we believe that “people are our greatestasset,” then we must also believe that organi-zations compete for business through the peo-ple they employ. If this is the case, then it is tothe organization’s advantage to ensure that itsgreatest asset, albeit its most elusive one,human capital, is utilized to its best and highest use.

This cannot and will not happen of its ownaccord. By now, it should be evident that noth-ing can happen until and unless a humanbeing makes a decision to act, and a plan isdeveloped and put into motion. For its part,the HR function has finally come into its ownand has the opportunity to move from thebackground to the forefront of the businessequation. HR practice leaders, who are trulyserious about making a difference, need to“measure” the business impact HR-driven pro-grams have on their organizations as a meansof demonstrating the merit and credibility ofany program that they endorse. After all, does-n’t it simply make good business sense to do so? �

8 Human Capital—The Elusive Asset

➀❷❸❹ 2003 SHRM®Research Quarterly

Bassi, L. (2001, Spring). Human capital advantage:Developing metrics for the knowledge era. RetrievedAugust 27, 2002, from http://www.linezine.com/4.2/articles/lbhca.htm

Bates, S. (2002, October). Accounting for people. HRMagazine, Vol. 47, No. 10, 30-37.

Becker, B. E., Huselid, M. A., & Ulrich, D. (2001). The HRScorecard: linking people, strategy and performance.Boston, Massachusetts: Harvard Business School Press.

Berkowitz, S. (2001, Fall). Measuring and reportinghuman capital. The Journal of Government FinancialManagement, Vol. 50, Issue 3, 13-17.

Bontis, N. & Fitz-enz, J. (2002). Intellectual capital ROI: Acausal map of human capital antecedents and conse-quents. Journal of Intellectual Capital, Vol. 3, Issue 3,223-247.

Boudreau, J. & Ramstad, P. (2002, August). StrategicHRM Measurement in the 21st Century: From JustifyingHR to Strategic Talent Leadership. Center for AdvancedHuman Resource Studies/Cornell University, WorkingPaper Series, Working Paper 02-15. Available fromhttp://ilr.cornell.edu/CAHRS/

Boudreau, J. (1996, February). Human Resources andOrganization Success. Center for Advanced HumanResource Studies/Cornell University, Working PaperSeries,Working Paper 96-03. Available fromhttp://www.ilr.cornell.edu/CAHRS/

Clark, R. & Morgan, B. (2001). Becoming measurement-managed. Strategy & Leadership, Vol. 29, No. 5, 26-30.

Davenport, Tom (1997, February). Secrets of successfulknowledge management. Knowledge, Inc. Available fromhttp://webcom.com/quantera/Secrets.html

DiFrancesco, J. (2002, March). Managing human capitalas a real business asset. IHRIM Journal, Vol. VI, No. 2,7-16.

Dzinkowski, R. (2000, February). The measurement andmanagement of intellectual capital: An introduction.Management Accounting; London; Vol. 78, Issue 2, 32-36.

Fitz-enz, J. (2000). The ROI of Human Capital. (New York:American Management Association.

Gachman, I. & Luss, R. (2002, May/June). Building thebusiness case for HR in today’s climate. Strategic HRReview, Vol. 1, Issue 4, 26-29.

Galvin, T. (2002, March). The 2002 training top 100.Training, Vol. 39, Issue 3, 20-68.

Garavan, T., Morley, M., Gunnigle, P., & Collins, E. (2001).Human capital accumulation the role of human resourcedevelopment. Journal of European Industrial Training,Vol. 25, Issue 2, 48-68.

Fitz-enz, J. & Phillips, J. (1998). A New Vision for HumanResources. Menlo Park, California: Crisp Learning.

Giannantonio, C. & Hurley, A. (2002). Executive insightsinto HR practices and education. Human ResourceManagement Review, Vol. 12, No. 4, 491-511

Ivey, J. (2002, March). Accounting for knowledge.Corporate Finance, Issue 208, 19-20.

Lepak, D. & Snell, S. (2002). Examining the humanresource architecture: The relationships among humancapital, employment, and human resource configurations.Journal of Management, Vol. 28, No. 4, 517-543.

Losey, M. (1999, Summer). Mastering the competenciesof HR management. Human Resource Management. Vol.38, No. 2., 99-102.

MacDonald, B. & Colombo, L. (2001, August). Creatingvalue through human capital management. The InternalAuditor, Vol. 58, Issue 4, 69-75.

Nerdrum, L. & Erikson, T. (2001). Intellectual capital: Ahuman capital perspective. Journal of IntellectualCapital, Vol. 2, Issue 2, 127-135.

Oliver, R. (2001, July/August). The return on human capi-tal. The Journal of Business Strategy, Vol. 22, Issue 4,7-10.

Schmidt, J. (2002, Spring). How much is goodwill worth?American Management Association, MWORLD, Vol. 1,No. 1, 23-28.

Schmidt, J. (2002, June). New tools for managing intangi-ble assets. Harvard Management Update, Vol. 5, No. 6,Guest Column.

Seibert, S., Kraimer, M. & Crant, M. (2001). What doproactive people do? A longitudinal model linking proac-tive personality and career success. PersonnelPsychology, Vol. 54, Issue 4, 845-874.

Stamps, D. (2000, May). Measuring minds. Training, Vol.37, Issue 5, 76-84.

Stewart, T. (2001). The Wealth of Knowledge:Intellectual Capital and the Twenty-First CenturyOrganization. New York: Doubleday.

Valance, N. (2001, January). Bright minds, big theories: Anew generation of thinkers offers new ideas aboutfinance, markets, and management. Retrieved 11/27/02from http://www.cfo.com/printarticle/0,5317,1899|,00.html

Walker, J. (2001). Human capital: Beyond HR. HumanResource Planning, Vol. 24, Issue 2, 4-5.

Woods, B. (2001, July). Harvesting your human capital.Chief Executive. Available from http://www.chiefexecu-tive.net/ceoguides/july2001/p12.html

Woolf, D. (2002, June). The long road to the executiveboardroom. Canadian HR Reporter, Vol. 15, Issue 12,7-10.

References

ABOUT THE AUTHORLeslie A. Weatherly, SPHR, is an HR Content Expert for the Society for HumanResource Management. Her responsibilities include identifying topics and focusareas in need of additional human resource management research and creatingHR products of strategic and practical value for HR target audiences. She is certified as a Senior Professional in Human Resource Management by theHuman Resource Certification Institute. Ms. Weatherly can be reached by email at [email protected].

ABOUT THE SHRM® RESEARCH DEPARTMENTThe SHRM Research Department researches and synthesizes the thoughts,practices and voices of today’s HR professional, business and academic leaderson various HR topics and focus areas, and creates products of strategic andpractical value for HR target audiences. The Research Department includes theSurvey Program, the Workplace Trends and Forecasting Program, and theDiversity Program. These programs provide SHRM members with a wide varietyof information and research pertaining to HR strategy and practices to bothserve the HR professional and advance the HR profession.

ABOUT SHRM®The Society for Human Resource Management (SHRM) is the world’s largestassociation devoted to human resource management. Representing more than170,000 individual members, the Society’s mission is both to serve humanresource management professionals and to advance the profession. Foundedin 1948, SHRM currently has more than 500 affiliated chapters within theUnited States and members in more than 120 countries. Visit SHRM Online at www.shrm.org.

This report is published by the Society for Human Resource Management(SHRM). The interpretations, conclusions, and recommendations in this reportare those of the author and do not necessarily represent those of SHRM. All content is for informational purposes only and is not to be construed as aguaranteed outcome. The Society for Human Resource Management cannotaccept responsibility for any errors or omissions or any liability resulting fromthe use or misuse of any such information.

© 2003 Society for Human Resource Management. All rights reserved. Printedin the United States of America.

This publication may not be reproduced, stored in a retrieval system, or trans-mitted in whole or in part, in any form or by any means, electronic, mechanical,photocopying, recording, or otherwise, without the prior written permission of theSociety for Human Resource Management, 1800 Duke Street, Alexandria, VA22314, USA.

For more information, please contact:

SHRM Research Department1800 Duke Street, Alexandria, VA 22314, USAPhone: +1.703.548.3440 Fax: +1.703.535.6473www.shrm.org/research

ResearchSHRM