Embed Size (px)

Citation preview

Stock Tales are concise, holistic stock reports across wider spectrum of sectors. Updates will not be periodical but based on significant events or change in price.

Stock_____

TALES

October 25, 2019

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

Stock T

ale

s

October 25, 2019

CMP: | 120 Target: | 160 (33%) Target Period: 12-14 months

months

Globus Spirits (GLOSPI)

BUY

Transition from ENA supplier to diversified business…

Globus Spirits (GSL) has a grain based manufacturing capacity of ~150

million bulk litre as on FY19, spanning across five integrated distilleries at

Vaishali (Bihar), Bardhaman (West Bengal), Behror (Rajasthan), Samalkha &

Hisar (Haryana). For FY19, IMIL contributed 47% to gross revenue while

ENA, others (animal feed, CO2, bottling, etc) formed 40%, 11%,

respectively. We expect 13%, 16%, 46% CAGR in revenue, EBITDA, PAT,

respectively, in FY19-21E driven by growth in IMIL, ethanol & bulk category.

ENA, ethanol, IMIL production to ensure utilisation stays high

For FY19, the company achieved extra neutral alcohol (raw material for IMIL,

IMFL) production at ~130 million litre (~85-90% utilisation) and is expected

to reach ~150-155 million litre (~95% utilisation of full capacity) in FY21E.

The capacity makes GSL self-sufficient in terms of captive utilisation of its

own ENA needs with low requirement of any incremental capex (~42%

captive utilisation of current capacity), residual being sold in open market,

which generated 43% (~| 427 crore) of net revenues in FY19. Going

forward, ethanol supply to OMC in the near term will further utilise ~22% of

the overall capacity, keeping utilisation in the 90-95% range.

Diversified business model positions GSL across value chain

GSL covers entire value chain of alcohol manufacturing undertaking an array

of operating activities from manufacturing of extra neutral alcohol (ENA) to

contract bottling of Indian made foreign liquor (IMFL), to marketing and

selling of IMIL and several by-products. IMIL dominates the share of captive

utilisation (~46% of FY19 revenue), with Rajasthan being the dominant

contributor (~75-80% of IMIL revenues, ~30% market share in the state).

Also, the company’s JV ‘Unibev’ (90% owned, 10% owned by former USL

MD Vijay Rekhi) has launched three IMFL liquor brands in Prestige and

Above category in a few pilot southern states. The management has been

slowly building up the franchise across key territories.

Valuation & outlook

We believe that initially newer capacities at Bihar and West Bengal will reach

optimal utilisation with bulk alcohol. Newer brands for IMIL (like “Goldee”

recently launched in West Bengal) and ethanol supply would lead to greater

captive usage of ENA. GSL saw a strong improvement in EBITDA margin

(~9% in FY19 from 8.1% in FY18). We expect margins in the range of 9-10%

for FY20E, FY21E, on the back of favourable hike in Rajasthan and negation

of rising input costs by higher bulk and ethanol realisation. We expect 13%,

16%, 46% CAGR in revenue, EBITDA, PAT, respectively, in FY19-21E.

Robust growth in the IMIL, ethanol & bulk category are expected to drive the

performance. Subsequently, RoCE is expected to move from 10% to ~14%

in FY21E. We have a BUY rating on the company with a target price of | 160,

valuing the business at 9x FY21E EPS.

Key Financial Summary

| crore FY18 FY19 FY20E FY21E CAGR

Net Sales 855.2 985.9 1,149.4 1,268.6 13.4%

EBITDA 68.2 88.3 102.3 119.2 16.2%

PAT 5.8 24.3 36.7 51.9 46.1%

P/E (x) 57.2 13.7 9.1 6.4

M.Cap/Sales (x) 0.4 0.3 0.3 0.3

RoCE (%) 6.0 9.5 11.3 13.5

RoE (%) 1.6 6.1 8.4 10.7

Source: ICICI Direct Research, Company

Particulars

Market Capitalisation (| cr) 337.7

52 Week High / Low (|) 182/92

Promoter Holding (%) 55.1

FII Holding (%) 0.4

DII Holding (%) 0.2

Dividend Yield (%) 0.0

Price Chart

0.0

50.0

100.0

150.0

200.0

250.0

0

1000

2000

3000

4000

5000

Aug-11

Aug-12

Aug-13

Aug-14

Aug-15

Aug-16

Aug-17

Aug-18

Aug-19

Nifty Smallcap 50

Globus Spirits (RHS)

Key Highlights

Globus’ grain based ENA capacity

expected to reach ~150-155 million

litre (~95% utilisation of full capacity)

in FY21E

We expect 13%, 16%, 46% CAGR in

revenue, EBITDA, PAT, respectively,

in FY19-21E driven by growth in the

IMIL, ethanol & bulk category

Research Analyst

Bharat Chhoda

Harshal Mehta

ICICI Securities | Retail Research 2

ICICI Direct Research

Stock Tales | Globus Spirits

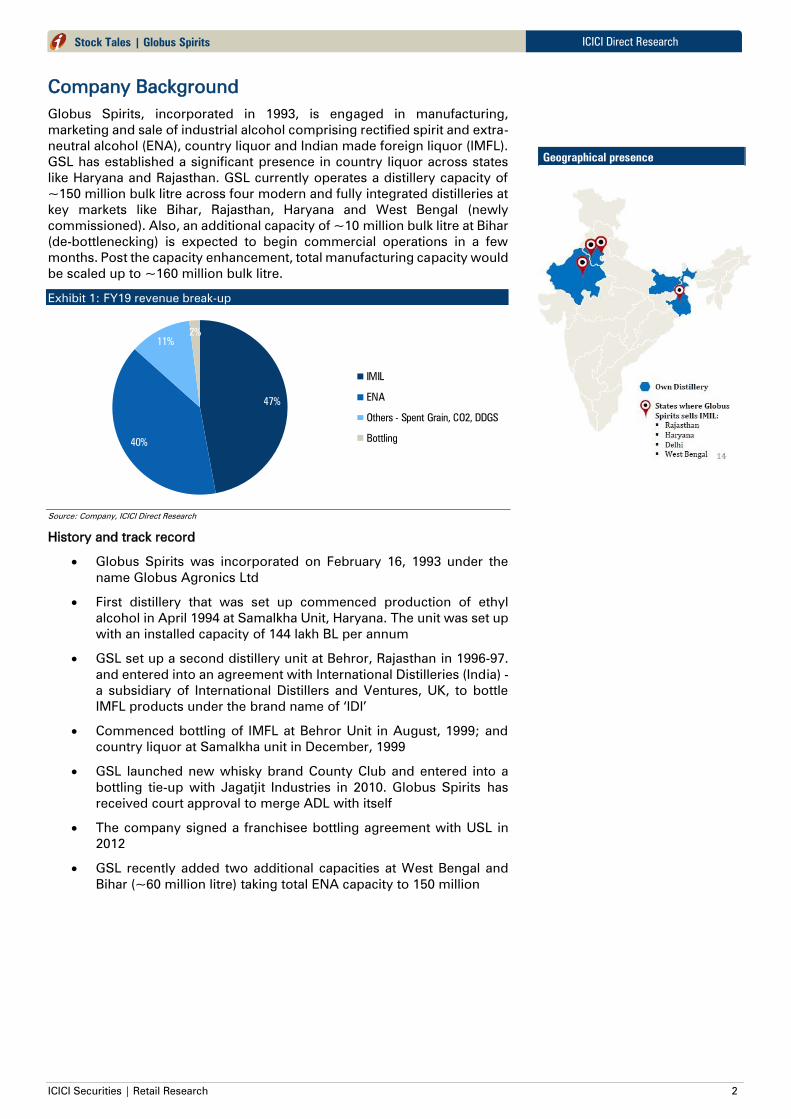

Company Background

Globus Spirits, incorporated in 1993, is engaged in manufacturing,

marketing and sale of industrial alcohol comprising rectified spirit and extra-

neutral alcohol (ENA), country liquor and Indian made foreign liquor (IMFL).

GSL has established a significant presence in country liquor across states

like Haryana and Rajasthan. GSL currently operates a distillery capacity of

~150 million bulk litre across four modern and fully integrated distilleries at

key markets like Bihar, Rajasthan, Haryana and West Bengal (newly

commissioned). Also, an additional capacity of ~10 million bulk litre at Bihar

(de-bottlenecking) is expected to begin commercial operations in a few

months. Post the capacity enhancement, total manufacturing capacity would

be scaled up to ~160 million bulk litre.

Exhibit 1: FY19 revenue break-up

47%

40%

11%

2%

IMIL

ENA

Others - Spent Grain, CO2, DDGS

Bottling

Source: Company, ICICI Direct Research

History and track record

Globus Spirits was incorporated on February 16, 1993 under the

name Globus Agronics Ltd

First distillery that was set up commenced production of ethyl

alcohol in April 1994 at Samalkha Unit, Haryana. The unit was set up

with an installed capacity of 144 lakh BL per annum

GSL set up a second distillery unit at Behror, Rajasthan in 1996-97.

and entered into an agreement with International Distilleries (India) -

a subsidiary of International Distillers and Ventures, UK, to bottle

IMFL products under the brand name of ‘IDI’

Commenced bottling of IMFL at Behror Unit in August, 1999; and

country liquor at Samalkha unit in December, 1999

GSL launched new whisky brand County Club and entered into a

bottling tie-up with Jagatjit Industries in 2010. Globus Spirits has

received court approval to merge ADL with itself

The company signed a franchisee bottling agreement with USL in

2012

GSL recently added two additional capacities at West Bengal and

Bihar (~60 million litre) taking total ENA capacity to 150 million

Geographical presence

ICICI Securities | Retail Research 3

ICICI Direct Research

Stock Tales | Globus Spirits

Investment Rationale

Capacity utilisation to remain high

GSL has a manufacturing capacity of ~150 million bulk litre as on FY19,

which spans across five integrated distilleries at Bardhaman (West Bengal),

Behror (Rajasthan), Vaishali (Bihar) and Samalkha & Hisar (Haryana). Prior to

the 150 million bulk litre consolidated capacity, GSL had embarked on a

strategy, a few years ago, to add two additional capacities at WB and Bihar

(~60 million litre). However, the Bihar plant subsequently got entangled in

the changes of condition for issuance of distillery license in the state,

negatively impacting its P&L. The Bihar government, upon orders of the High

Court, later allowed manufacturing of ENA in the state implying that it can

now recommence the distillery and export ENA out of the state and country.

As on FY19, the plant has recommenced its operations, and along with ENA;

the ethanol supply is expected to drive its utilisation. The plant is expected

to further reach optimum capacity utilisation in the next six to 12 months

post de-bottlenecking at its Bihar plant. For FY19, GSL achieved extra neutral

alcohol (raw material for IMIL, IMFL) production at ~130 million litre (~85-

90% utilisation of current capacity) and is expected to reach ~150-155

million litre (~95% utilisation of full capacity) in FY21E. The capacity makes

GSL self-sufficient in terms of captive utilisation of its own ENA needs

(~42% captive utilisation of current capacity), residual being sold in open

market. Approximately 50% of ENA produced is sold in the open market,

which generated 43% (~| 427 crore) of net revenues in FY19.

Exhibit 2: ENA capacity

105.8

123.7

150.0160.0 160.0

0

40

80

120

160

200

FY17 FY18 FY19 FY20E FY21E

million litres

ENA Capacity

Source: Company, ICICI Direct Research

Diversified business model positions GSL across value chain

Over the years, GSL has successfully transformed from a grain-based bulk

alcohol manufacturer to a 360° alcohol beverage (alcobev segment) player.

GSL covers the entire value chain of alcohol manufacturing undertaking

array of operating activities from manufacturing of extra neutral alcohol

(ENA) to contract bottling of Indian made foreign liquor (IMFL), to marketing

and selling IMIL and several by-products. GSL utilised ~45% of existing

capacity for captive consumption in FY19. IMIL dominates the share of

captive utilisation (~46% FY19 revenue contribution), with Rajasthan being

the dominant contributor (~75-80% of IMIL revenues and ~30% market

share in the state). Major IMIL brands include Nimboo, Heer Ranjha,

Ghoomer and Goldee. New IMIL brands launched in West Bengal remain key

for the company’s growth in the IMIL category. GSL also offers contract

manufacturing for bottling brands like Officer’s Choice and McDowell's No.1

for leading IMFL players like United Spirits and Allied Blenders Distillers

(ABD). The company also markets its by-product distilled dried grains

soluble (DDGS), which provides an attractive animal feed in replacement for

soybean and maize. The diversified business model (360° approach) enables

GSL to manage optimum level of utilisation. Transition of the incremental

ENA produced towards captive utilisation would remain key for gaining

ICICI Securities | Retail Research 4

ICICI Direct Research

Stock Tales | Globus Spirits

higher realisation (ENA diverted towards IMIL yields ~2.5-3X realisation)

and also contributes to higher incremental margins.

Exhibit 3: Brand portfolio

Source: Company, ICICI Direct Research

Government fuel ethanol push to benefit ENA suppliers

Government of India has encouraged building additional ethanol production

capacity, to raise ethanol blending in petrol to 10% by 2022 from current 2-

3%. As per industry estimates for FY19E, 53% of alcohol demand (~3.3

billion litre) is expected to arise from production of ethanol and only 36%

(2.2 billion litre) will be from the potable alcohol sector. Also, going by the

recent BPCL E-procurement tender for supply of ~329 crore litre of ethanol,

it equated the bidding prices of grain based ethanol with B-heavy molasses

at ~| 47.1/litre. GSL bid and has been allocated 2.6 crore litre in the first

tender cycle. The management expects additional ethanol volumes in two

further allocation cycles. The management has enlisted its distilleries in

Haryana and Bihar to be utilised for production for ethanol from ENA (with

a | 10-12 crore capex). ENA from states such as Haryana and Bihar which

have over capacity situation garner lower realisation of ~| 39-40 /litre. Thus,

a diversion to ethanol production could raise the realisation by ~18-20%.

Exhibit 4: IMIL gross revenues trend

400.4

479.6509.0

560.7

618.1

0

300

600

900

FY17 FY18 FY19 FY20E FY21E

| crore

IMIL gross revenues

Source: Company, ICICI Direct Research

Exhibit 5: ENA & ethanol revenue trend

205.1

349.2

427.1

543.9

610.6

0

150

300

450

600

750

FY17 FY18 FY19 FY20E FY21E

| crore

ENA & Ethanol revenues

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 5

ICICI Direct Research

Stock Tales | Globus Spirits

Building of IMFL franchise to add long term value

The company’s JV ‘Unibev’ (90% owned and 10% owned by former USL

MD Vijay Rekhi) has launched three IMFL liquor brands in Prestige and

Above category in a few pilot southern states. As on FY19, the geographic

presence includes Puducherry, Karnataka, Telangana, West Bengal and

Andhra Pradesh and the three brands include L’Affaire Napoleon Premium

French brandy, Governor’s Reserve whisky created with 12 Year old

matured scotch, Oakton Barrel Aged whisky created with 18 Year old

matured scotch. The premium brand portfolio has an age claim over

competitors (blended with aged scotch) and is expected to include two to

three more brands in the whisky and vodka segment. Rise in discretionary

spends, increasing number of aspiring consumers and limited competitors

and options for consumers makes the category particularly attractive.

However, the management is taking a cautious step in expansion and will

infuse | 15-20 crore each year in building up the JV business. It also intends

to launch IMFL in states such as Maharashtra in FY20 and would begin

exports in a while. Higher realisation from IMFL would push the asset

turnover for the company, with increased margins, thereby providing

healthy contribution to return ratios. However, we expect meaningful

contribution from the Unibev franchise from FY22 onwards.

ICICI Securities | Retail Research 6

ICICI Direct Research

Stock Tales | Globus Spirits

Financials

Net revenues expected to grow at 13% CAGR to | 1269 crore in FY19-21E

GSL’s blended revenues are expected to grow in grow double digits. IMIL

segment is expected to grow at CAGR of 10% over FY19-21E to | 498 crore,

on the back of 4% volume growth (low single digit volume growth mainly

led by management cautious stance on West Bengal IMIL market due delay

in the price hike by the state government). On the other hand, revenues from

bulk and ethanol sales are expected to clock 20% growth to | 611 crore

mainly led by the de-bottlenecking exercise at Bihar plant (would lead to an

incremental 10 million litre of ENA capacity) and commencement of ethanol

supply in FY20. Overall, others segment is expected to remain flat at | 129

crore. On an overall basis, we expect blended Globus revenues to grow at

13% CAGR to | 1269 crore in FY19-21E.

Exhibit 6: Net revenues expected to clock 13% CAGR in FY19-21 to | 1269 crore

789.1855.2

985.9

1149.4

1268.6

0

300

600

900

1200

1500

FY17 FY18 FY19 FY20E FY21E

| crore

Revenues

Source: Company, ICICI Direct Research

EBITDA margins expected to increase mere 40 bps due to COGS inflation

Liquor companies have been experiencing a rise in raw material inflation (i.e.

ENA and glass) since H2FY19. Being a grain ENA supplier itself, GSL has

also seen grain prices harden QoQ and YoY. However, ongoing stronger

growth in ENA realisation in key markets would, thus, negate higher inflation

and even result in a marginal gross margin expansion. Other expenses are

expected to stay range bound in the presence of a limited capex (| 30-40

crore) in the standalone and Unibev entity. Overall, we expect EBITDA

margins to expand 40 bps in two years, mainly led by expansion in gross

margins. Hence, absolute EBITDA is expected to grow 16% to | 119 crore.

Exhibit 7: EBITDA expected to grow 16% to | 119 crore

54.8

68.2

88.3

102.3

119.2

6.9

8.0

9.0 8.99.4

0.0

4.0

8.0

12.0

0

30

60

90

120

150

FY17 FY18 FY19 FY20E FY21E

%

| crore

EBITDA EBITDA margin (RHS)

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 7

ICICI Direct Research

Stock Tales | Globus Spirits

PAT expected to grow at 46% CAGR to | 52 crore in FY19-21E

Capex is expected to remain rangebound at | 30-40 crore each year in the

consolidated entity. The management also expects to further deleverage its

balance sheet from current debt level of | 200 crore by | 50-70 crore in two

years, which is expected to lower the interest expense from | 26 crore to

| 18 crore in FY21, which is expected to ramp up the profitability of the

company. Thus, PAT is expected to grow at 46% FY19-21 CAGR to | 52

crore, higher than the expected growth on the EBITDA front. Also lower tax

(decline of 200-300 bps) due to change in corporate tax rate is expected to

further aid the growth in net profit.

Exhibit 8: PAT expected to grow 46% to | 52 crore

7.45.8

24.3

36.7

51.9

0

15

30

45

60

FY17 FY18 FY19 FY20E FY21E

| crore

PAT

Source: Company, ICICI Direct Research

Return ratios, free cash flows to remain strong, going ahead

GSL clocked RoE & RoCE of mere 6.1% & 9.5%, respectively, in FY19, led by

subdued grain ENA prices and excess capacity. With rising revenues and

profitability and lack of any major capex in the medium term, RoE and RoCE

are expected to remain healthy at 10.7% and 13.5%, respectively, in FY21.

Exhibit 9: Return ratios to remain stable

2.01.6

6.1

8.4

10.7

3.3

6.0

9.5

11.3

13.5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

FY17 FY18 FY19 FY20E FY21E

%

RoE RoCE

Source: Company, ICICI Direct Research

Similarly, with focus on priority states and better working capital

management and lower capex, cash flows are expected to remain strong.

ICICI Securities | Retail Research 8

ICICI Direct Research

Stock Tales | Globus Spirits

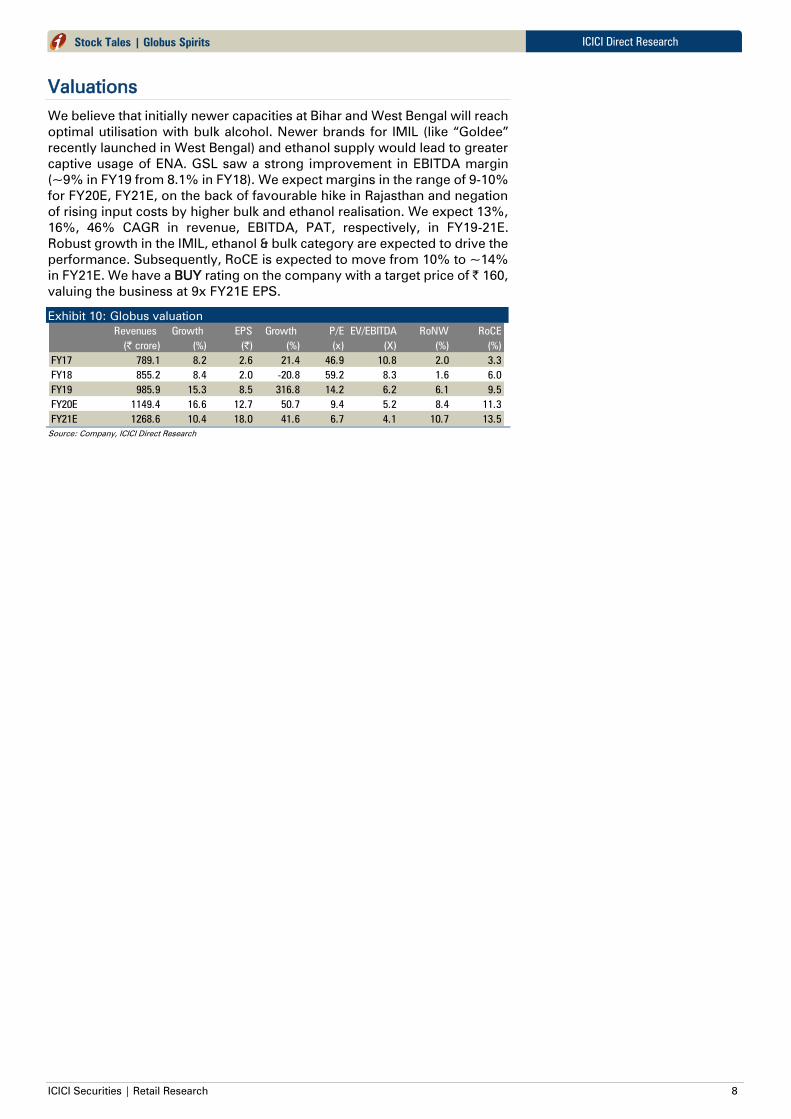

Valuations

We believe that initially newer capacities at Bihar and West Bengal will reach

optimal utilisation with bulk alcohol. Newer brands for IMIL (like “Goldee”

recently launched in West Bengal) and ethanol supply would lead to greater

captive usage of ENA. GSL saw a strong improvement in EBITDA margin

(~9% in FY19 from 8.1% in FY18). We expect margins in the range of 9-10%

for FY20E, FY21E, on the back of favourable hike in Rajasthan and negation

of rising input costs by higher bulk and ethanol realisation. We expect 13%,

16%, 46% CAGR in revenue, EBITDA, PAT, respectively, in FY19-21E.

Robust growth in the IMIL, ethanol & bulk category are expected to drive the

performance. Subsequently, RoCE is expected to move from 10% to ~14%

in FY21E. We have a BUY rating on the company with a target price of | 160,

valuing the business at 9x FY21E EPS.

Exhibit 10: Globus valuation

Revenues Growth EPS Growth P/E EV/EBITDA RoNW RoCE

(| crore) (%) (|) (%) (x) (X) (%) (%)

FY17 789.1 8.2 2.6 21.4 46.9 10.8 2.0 3.3

FY18 855.2 8.4 2.0 -20.8 59.2 8.3 1.6 6.0

FY19 985.9 15.3 8.5 316.8 14.2 6.2 6.1 9.5

FY20E 1149.4 16.6 12.7 50.7 9.4 5.2 8.4 11.3

FY21E 1268.6 10.4 18.0 41.6 6.7 4.1 10.7 13.5

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 9

ICICI Direct Research

Stock Tales | Globus Spirits

Risks and concerns

Geographic concentration

The company derives 75% of its IMIL revenues (52% of FY18 topline) from

Rajasthan. Any disruption (on the supply or demand side) in the state, could

lead to revenue and profitability decline for the company.

JV related costs

The company will invest | 20-25 crore each year in developing brands in

the IMFL category, dominated by Diageo and Pernod Richard. It is yet to be

seen how that avenue pans out

Highly regulated sector

Liquor distribution business in India is subject to strict regulations. The rules

and regulation vary in different states. Any change in policies by the

respective state governments with regard to production, distribution or

marketing of IMFL can impact the operational performance of the company.

Also, changes in taxes and other levies by the state government can impact

the financial performance of the company.

Increase in raw material costs

The prices of grains (which is one of the primary raw materials for

manufacture of IMFL) and packaging material have been hardening since

H2FY19, which has impacted the margins of liquor companies. Any further

significant and sustained increase in their prices can impact the profitability

of the company.

Slowdown in volume growth

Any significant slowdown in volume growth could impact the operation and

financial performance of the company in a negative manner.

Inability to take price hikes

In majority of the states, price hikes are decided by the government. If the

company is not granted price hikes or the price hike is insufficient to cover

for increased input cost, it can impact the margins of the company.

ICICI Securities | Retail Research 10

ICICI Direct Research

Stock Tales | Globus Spirits

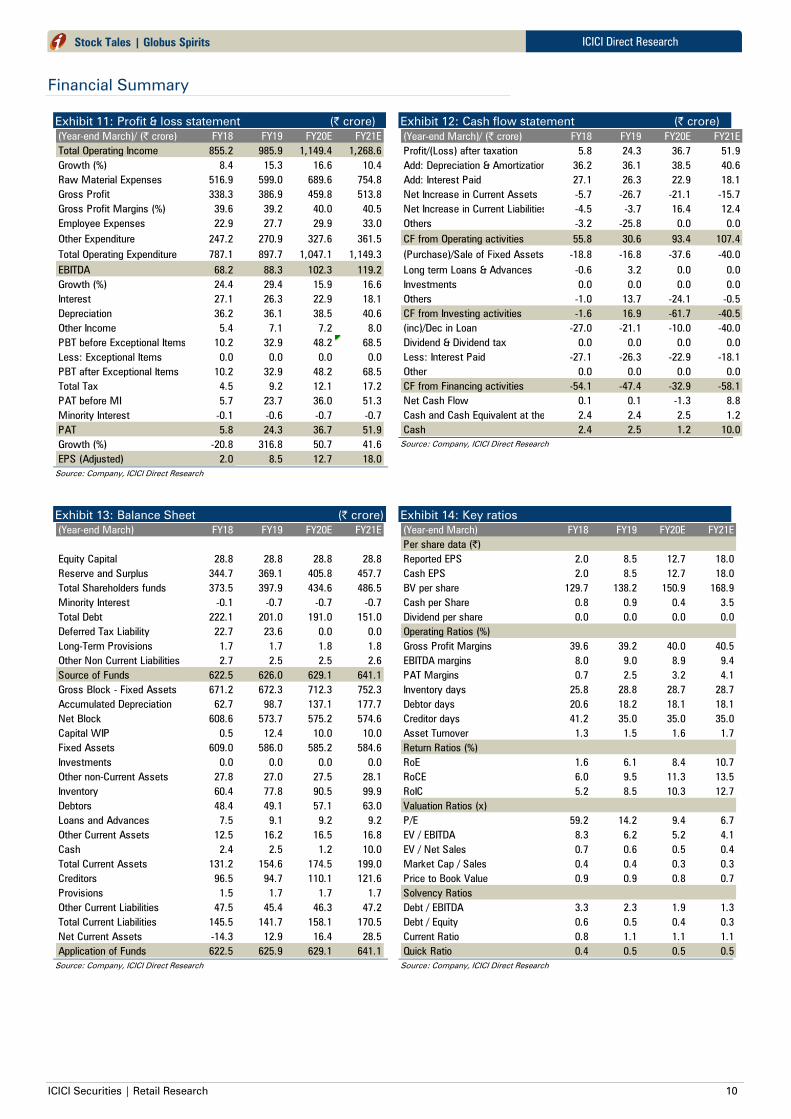

Financial Summary

Exhibit 11: Profit & loss statement (| crore)

(Year-end March)/ (| crore) FY18 FY19 FY20E FY21E

Total Operating Income 855.2 985.9 1,149.4 1,268.6

Growth (%) 8.4 15.3 16.6 10.4

Raw Material Expenses 516.9 599.0 689.6 754.8

Gross Profit 338.3 386.9 459.8 513.8

Gross Profit Margins (%) 39.6 39.2 40.0 40.5

Employee Expenses 22.9 27.7 29.9 33.0

Other Expenditure 247.2 270.9 327.6 361.5

Total Operating Expenditure 787.1 897.7 1,047.1 1,149.3

EBITDA 68.2 88.3 102.3 119.2

Growth (%) 24.4 29.4 15.9 16.6

Interest 27.1 26.3 22.9 18.1

Depreciation 36.2 36.1 38.5 40.6

Other Income 5.4 7.1 7.2 8.0

PBT before Exceptional Items 10.2 32.9 48.2 68.5

Less: Exceptional Items 0.0 0.0 0.0 0.0

PBT after Exceptional Items 10.2 32.9 48.2 68.5

Total Tax 4.5 9.2 12.1 17.2

PAT before MI 5.7 23.7 36.0 51.3

Minority Interest -0.1 -0.6 -0.7 -0.7

PAT 5.8 24.3 36.7 51.9

Growth (%) -20.8 316.8 50.7 41.6

EPS (Adjusted) 2.0 8.5 12.7 18.0

Source: Company, ICICI Direct Research

Exhibit 12: Cash flow statement (| crore)

(Year-end March)/ (| crore) FY18 FY19 FY20E FY21E

Profit/(Loss) after taxation 5.8 24.3 36.7 51.9

Add: Depreciation & Amortization 36.2 36.1 38.5 40.6

Add: Interest Paid 27.1 26.3 22.9 18.1

Net Increase in Current Assets -5.7 -26.7 -21.1 -15.7

Net Increase in Current Liabilities -4.5 -3.7 16.4 12.4

Others -3.2 -25.8 0.0 0.0

CF from Operating activities 55.8 30.6 93.4 107.4

(Purchase)/Sale of Fixed Assets -18.8 -16.8 -37.6 -40.0

Long term Loans & Advances -0.6 3.2 0.0 0.0

Investments 0.0 0.0 0.0 0.0

Others -1.0 13.7 -24.1 -0.5

CF from Investing activities -1.6 16.9 -61.7 -40.5

(inc)/Dec in Loan -27.0 -21.1 -10.0 -40.0

Dividend & Dividend tax 0.0 0.0 0.0 0.0

Less: Interest Paid -27.1 -26.3 -22.9 -18.1

Other 0.0 0.0 0.0 0.0

CF from Financing activities -54.1 -47.4 -32.9 -58.1

Net Cash Flow 0.1 0.1 -1.3 8.8

Cash and Cash Equivalent at the beginning2.4 2.4 2.5 1.2

Cash 2.4 2.5 1.2 10.0

Source: Company, ICICI Direct Research

Exhibit 13: Balance Sheet (| crore)

(Year-end March) FY18 FY19 FY20E FY21E

Equity Capital 28.8 28.8 28.8 28.8

Reserve and Surplus 344.7 369.1 405.8 457.7

Total Shareholders funds 373.5 397.9 434.6 486.5

Minority Interest -0.1 -0.7 -0.7 -0.7

Total Debt 222.1 201.0 191.0 151.0

Deferred Tax Liability 22.7 23.6 0.0 0.0

Long-Term Provisions 1.7 1.7 1.8 1.8

Other Non Current Liabilities 2.7 2.5 2.5 2.6

Source of Funds 622.5 626.0 629.1 641.1

Gross Block - Fixed Assets 671.2 672.3 712.3 752.3

Accumulated Depreciation 62.7 98.7 137.1 177.7

Net Block 608.6 573.7 575.2 574.6

Capital WIP 0.5 12.4 10.0 10.0

Fixed Assets 609.0 586.0 585.2 584.6

Investments 0.0 0.0 0.0 0.0

Other non-Current Assets 27.8 27.0 27.5 28.1

Inventory 60.4 77.8 90.5 99.9

Debtors 48.4 49.1 57.1 63.0

Loans and Advances 7.5 9.1 9.2 9.2

Other Current Assets 12.5 16.2 16.5 16.8

Cash 2.4 2.5 1.2 10.0

Total Current Assets 131.2 154.6 174.5 199.0

Creditors 96.5 94.7 110.1 121.6

Provisions 1.5 1.7 1.7 1.7

Other Current Liabilities 47.5 45.4 46.3 47.2

Total Current Liabilities 145.5 141.7 158.1 170.5

Net Current Assets -14.3 12.9 16.4 28.5

Application of Funds 622.5 625.9 629.1 641.1

Source: Company, ICICI Direct Research

Exhibit 14: Key ratios

(Year-end March) FY18 FY19 FY20E FY21E

Per share data (|)

Reported EPS 2.0 8.5 12.7 18.0

Cash EPS 2.0 8.5 12.7 18.0

BV per share 129.7 138.2 150.9 168.9

Cash per Share 0.8 0.9 0.4 3.5

Dividend per share 0.0 0.0 0.0 0.0

Operating Ratios (%)

Gross Profit Margins 39.6 39.2 40.0 40.5

EBITDA margins 8.0 9.0 8.9 9.4

PAT Margins 0.7 2.5 3.2 4.1

Inventory days 25.8 28.8 28.7 28.7

Debtor days 20.6 18.2 18.1 18.1

Creditor days 41.2 35.0 35.0 35.0

Asset Turnover 1.3 1.5 1.6 1.7

Return Ratios (%)

RoE 1.6 6.1 8.4 10.7

RoCE 6.0 9.5 11.3 13.5

RoIC 5.2 8.5 10.3 12.7

Valuation Ratios (x)

P/E 59.2 14.2 9.4 6.7

EV / EBITDA 8.3 6.2 5.2 4.1

EV / Net Sales 0.7 0.6 0.5 0.4

Market Cap / Sales 0.4 0.4 0.3 0.3

Price to Book Value 0.9 0.9 0.8 0.7

Solvency Ratios

Debt / EBITDA 3.3 2.3 1.9 1.3

Debt / Equity 0.6 0.5 0.4 0.3

Current Ratio 0.8 1.1 1.1 1.1

Quick Ratio 0.4 0.5 0.5 0.5

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 11

ICICI Direct Research

Stock Tales | Globus Spirits

RATING RATIONALE

ICICI Direct endeavors to provide objective opinions and recommendations. ICICI Direct assigns ratings to its

stocks according to their notional target price vs. current market price and then categorizes them as Buy, Hold,

Reduce and Sell. The performance horizon is two years unless specified and the notional target price is defined as

the analysts' valuation for a stock

Buy: >15%

Hold: -5% to 15%;

Reduce: -15% to -5%;

Sell: <-15%

Pankaj Pandey Head – Research [email protected]

ICICI Direct Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities | Retail Research 12

ICICI Direct Research

Stock Tales | Globus Spirits

ANALYST CERTIFICATION

I/We, Bharat Chhoda, MBA; Harshal Mehta MTech (Biotech) , Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views

about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. It is also confirmed that above

mentioned Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months and do not serve as an officer, director or employee of the companies mentioned in

the report

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities Limited is a Sebi registered

Research Analyst with SEBI Registration Number – INH000000990. ICICI Securities Limited Sebi Registration is INZ000183631 for stock broker. ICICI Securities is a subsidiary of ICICI Bank which is India’s largest private sector bank

and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on

www.icicibank.com

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship

with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the

securities or derivatives of any companies that the analysts cover.

Recommendation in reports based on technical and derivative analysis centre on studying charts of a stock's price movement, outstanding positions, trading volume etc as opposed to focusing on a company's fundamentals and, as

such, may not match with the recommendation in fundamental reports. Investors may visit icicidirect.com to view the Fundamental and Technical Research Reports.

Our proprietary trading and investment businesses may make investment decisions that are inconsistent with the recommendations expressed herein.

ICICI Securities Limited has two independent equity research groups: Institutional Research and Retail Research. This report has been prepared by the Retail Research. The views and opinions expressed in this document may or may

not match or may be contrary with the views, estimates, rating, target price of the Institutional Research.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected

recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would

endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI

Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in

circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein

is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers

simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting

and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who

must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient.

The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities

whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks

associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-

managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any compensation or other

benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts and their relatives have any material conflict of

interest at the time of publication of this report.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of

the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this

report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or

use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in

all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.