Embed Size (px)

Citation preview

Finance UGC NET

2 Addarsh Basti Tonk Phatak,Jaipur, 8058195333, Study Material, Video classes, Online Test series, Notes by Jitendra Sharma Page 1

Finance MARKET REGULATION

The main legislation governing the Capital Market are :-

1. The SEBI Act, 1992 which establishes SEBI to protect investors and develop and regulate

securities market.

SEBI regulatory and statutory body

2. The Securities Contracts (Regulation ) Act, 1956, SC (R) A which regulates transactions

in securities through control over stock exchanges.(12Apr.1992)

3. The depositories Act, 1996 which provides for electronic maintenance and transfer of

ownership of demat securities.

4. The Companies Act, 2013, which sets out the code of conduct for the corporate sector

in relation to issue, allotment and transfer of securities and disclosures to be made in

public issues.

INVESTORS IN DEBT MARKET

Investors are the entities who invest in fixed income instruments. The investors in such instruments are generally Banks, Financial Institutions, Mutual Funds, Insurance Companies , Provident Funds etc. The individual investors invest to a great extent in Fixed Income products.

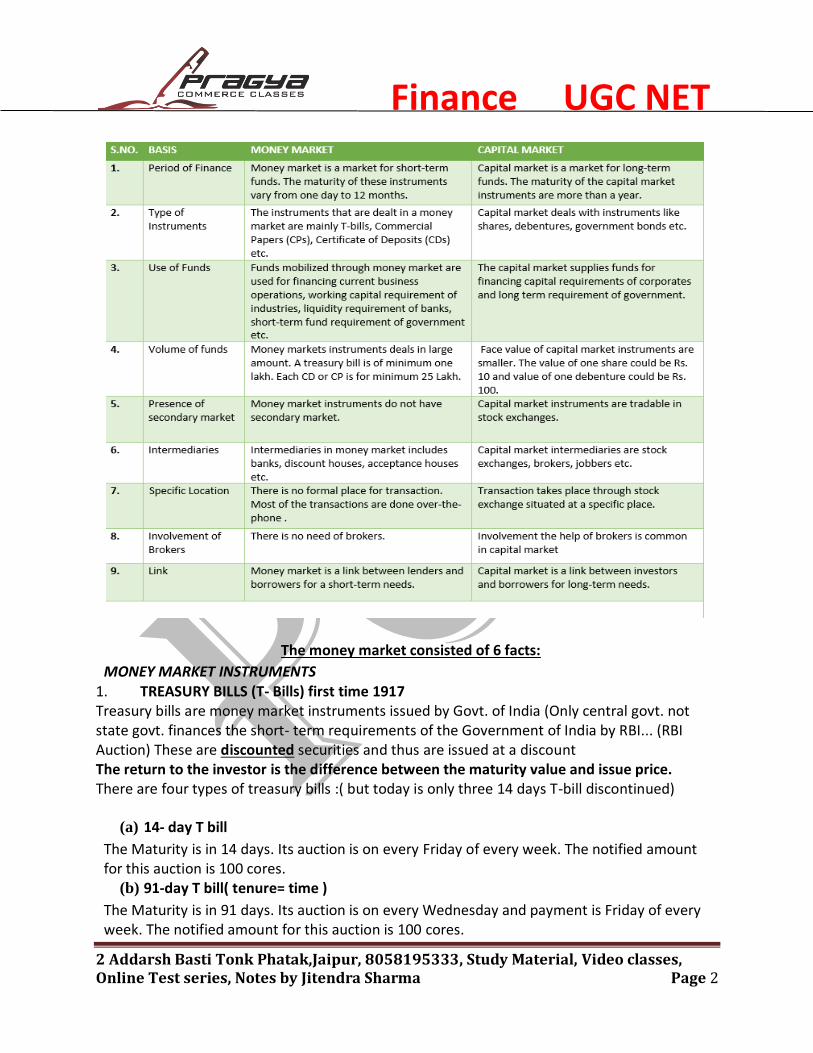

Deference between money market and capital market

Finance UGC NET

2 Addarsh Basti Tonk Phatak,Jaipur, 8058195333, Study Material, Video classes, Online Test series, Notes by Jitendra Sharma Page 2

The money market consisted of 6 facts:

MONEY MARKET INSTRUMENTS 1. TREASURY BILLS (T- Bills) first time 1917 Treasury bills are money market instruments issued by Govt. of India (Only central govt. not state govt. finances the short- term requirements of the Government of India by RBI... (RBI Auction) These are discounted securities and thus are issued at a discount The return to the investor is the difference between the maturity value and issue price. There are four types of treasury bills :( but today is only three 14 days T-bill discontinued)

(a) 14- day T bill

The Maturity is in 14 days. Its auction is on every Friday of every week. The notified amount for this auction is 100 cores.

(b) 91-day T bill( tenure= time )

The Maturity is in 91 days. Its auction is on every Wednesday and payment is Friday of every week. The notified amount for this auction is 100 cores.

Finance UGC NET

2 Addarsh Basti Tonk Phatak,Jaipur, 8058195333, Study Material, Video classes, Online Test series, Notes by Jitendra Sharma Page 3

(c) 182- day T bill

The Maturity is in 182 days. Its auction is on every alternate Wednesday (which is not a reporting week= reporting week second or fourth, not reporting means first and third). The notified amount for this auction is 100 cores.

(d) 364- day T bill

The Maturity is in 364 days. Its auction is on every alternate Wednesday (which is a reporting week) . The notified amount for this auction is 500 cores.

BENEFITS OF INVESTMENT IN TREASURY BILLS (secured instruments)

(a) No tax deducted at source.

(b) Zero default risk being sovereign paper.

(c) Highly liquid money market instrument.

(d) Better returns especially in the short- term.

(e) Transparency

(f) Simplified settlement

FEATURES OF TREASURY BILLS

(a) Form The treasury bills are issued in the form of promissory note in physical form or by

credit to Subsidiary General Ledger (SGL) account or Gilt account in dematerialized

form.

(b) Minimum Amount of Bids Bids for treasury bills are to be made for a minimum amount

of 25000/- only and in multiples thereof.

(c) Eligibility All entities registered in India like banks, financial institutions , Primary

Dealers, firms, companies, corporate bodies, partnership firms, institutions, mutual

funds, Foreign Institutional Investors, State Governments, Provident funds, trusts,

research organization, Nepal Rashtra bank and even individuals are eligible to bid and

purchase Treasury bills

(d) Repayment The treasury bills are repaid at par on the expiry of their tenure at the office

of the Reserve Bank of India

(e) Availability All the treasury Bills are highly liquid instruments available both in the

primary and secondary market.

2. Commercial Papers (CP) A. Commercial paper is an unsecured, short-term debt instrument issued by a corporation( organization/ company), typically for the financing of accounts receivable, inventories and meeting short-term liabilities. Maturities on commercial paper rarely

Finance UGC NET

2 Addarsh Basti Tonk Phatak,Jaipur, 8058195333, Study Material, Video classes, Online Test series, Notes by Jitendra Sharma Page 4

range 7 to 364 days. Commercial paper is usually issued at a discount and high interest rate and mature at face value . B. Organization can issue through banks or merchant banker (called as dealers)C. Issue multiple of rs 5 lakh .

CPs is negotiable short- term unsecured promissory notes with maturities, issued by well rated Companies generally sold on discount basis. Companies can issue CPs either directly to the investors or through banks/ merchant banks ( called dealers) . These are basically instruments evidencing the liability of the issuer to pay the holder in due course a fixed amount i.e. face value of the instrument , on the specified due date. These are issued for a fixed period of time at a discount to the face value and mature at par.

Eligible issuer of CP

A. tangible net worth not less than 4 cores B. the company has been sanctioned bank overdraft facility from bank and financial institution C. the borrowed accounts of the company is classified as a standard assets by financial bank and institution

Rating requirement

All eligible participants shall obtain credit rating for issuance of CP from any one of the SEBI registered Credit rating agencies the minimum credit rating shall be A3

Denomination CP can be issued in denominations of rs. 5 lakh and multiples thereof. The amount invested by a single investor should not be less than rs 5 lakh ( face value)

3. Certificates of Deposits (CDs)

After treasury bills, the next lowest risk category investment option is the certificate of deposit (CD) issued by banks and Financial Institutions. Introduced in 1989

Maturing 7 days to 364 days

Minimum amount 1 lakh and multiple of 1 lakh

CDs are issued by banks and FLs mainly to augment funds by attracting deposits from corporate, high net worth individuals , trusts ,etc. the foreign and private banks , especially , which do not have large branch networks and hence lower deposit base use this instrument to raise funds.

4. Call Money = Participants in the call money market are banks and related entities specified by the RBI. Scheduled commercial banks (excluding RRBs), co-operative banks (other than Land Development Banks) and Primary Dealers (PDs), are permitted to participate in call/notice money market both as borrowers and lenders.

a. Call = for 1 days

b. Call notice 1 to 14 days

Call / Notice money is an amount borrowed or lent on demand for a very short period. If the period is more than one day and up to 14 days it is called “ Notice Money” otherwise the amount is known as call money. No collateral security is required to cover these transactions. The call market enables the banks and institutions to even out their day to day deficits and

Finance UGC NET

2 Addarsh Basti Tonk Phatak,Jaipur, 8058195333, Study Material, Video classes, Online Test series, Notes by Jitendra Sharma Page 5

surpluses of money. Commercial banks, Co- operative Banks and primary dealers are allowed to borrow and lend in this market for adjusting their cash reserve requirements.

c. Terms Money Market

Inter – bank market for deposits of maturity beyond 14 days and upto three months (one year) is referred to as the term money market.

5. Inter- corporate Deposits

Inter-company deposit is the deposit made by a company that has surplus funds, to another company for a maximum of 6 months. It is a source of short-term financing.

6. Commercial Bills The commercial bills are issued by the seller (drawer) on the buyer (drawee) for the value of goods delivered by him. These bills are of 30 days, 60 days or 90 days maturity.

If the seller is in need of funds, he may draw a bill and send it to the buyer for seller is in need of funds, he may draw a bill and send it to the buyer for acceptance. The buyer accepts the bill and promises to make payment on the due date. He may also approach his bank to accept the bill.

capital market/security market Function Securities Market -

Is a link between investment & savings

Mobilizes & channelizes savings

Provides Liquidity to investors

Is a market place for purchase and sale of securities

Controlled by SEBI, long term market (more than one year)

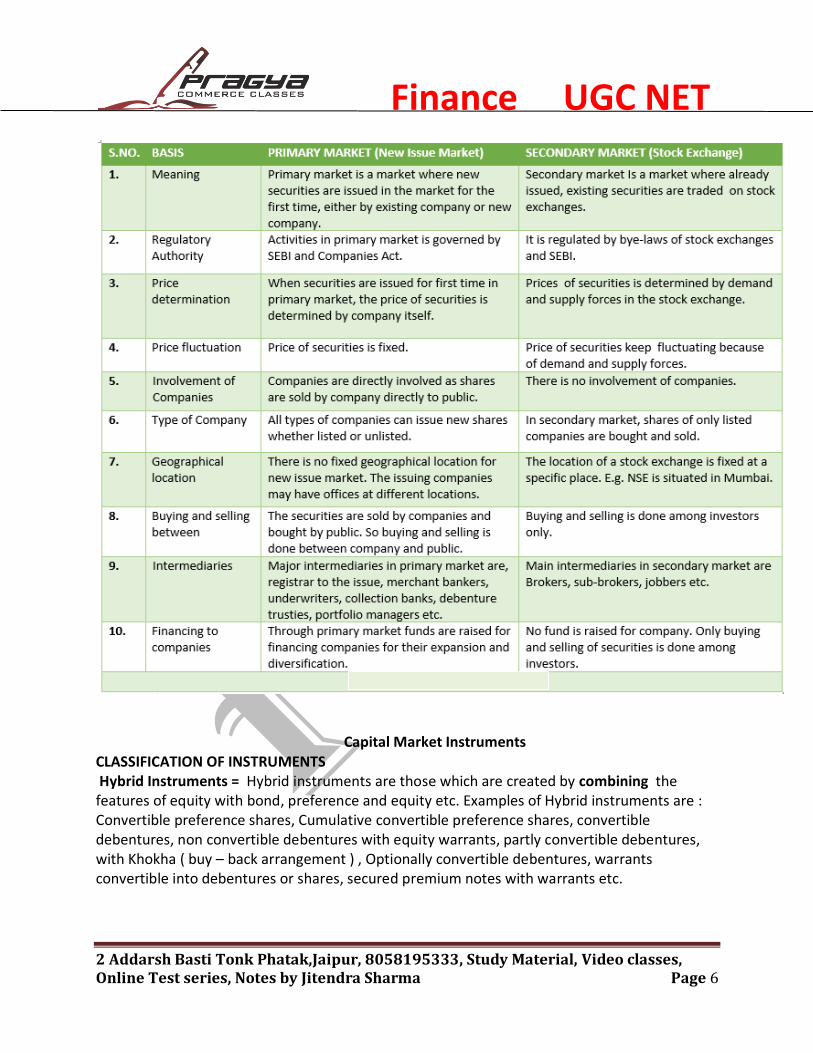

These are two types 1. Primary market and 2. secondary market

In primary market issue new security (i.e. IPO), transaction between company to

investor, and In secondary market issue previously issued by company, transaction

between investors to inventors, through stock exchange from stock broker

The Securities Market refers to the markets for those financial instrument / claims /

obligations that are commonly and readily transferable by sale.

Finance UGC NET

2 Addarsh Basti Tonk Phatak,Jaipur, 8058195333, Study Material, Video classes, Online Test series, Notes by Jitendra Sharma Page 6

Capital Market Instruments CLASSIFICATION OF INSTRUMENTS Hybrid Instruments = Hybrid instruments are those which are created by combining the features of equity with bond, preference and equity etc. Examples of Hybrid instruments are : Convertible preference shares, Cumulative convertible preference shares, convertible debentures, non convertible debentures with equity warrants, partly convertible debentures, with Khokha ( buy – back arrangement ) , Optionally convertible debentures, warrants convertible into debentures or shares, secured premium notes with warrants etc.

Finance UGC NET

2 Addarsh Basti Tonk Phatak,Jaipur, 8058195333, Study Material, Video classes, Online Test series, Notes by Jitendra Sharma Page 7

Pure Instruments = Equity shares, preference shares and debentures/ bonds which were issued with their basic characteristics intact without mixing features of other classes of instruments are called Pure instruments Derivatives Instruments = Derivatives are contracts which derive their values from the value of one or more of other assets (known as underlying assets.) The derivatives itself is merely a contract between two or more parties. Its value is determined by fluctuations in the underlying assets. The most common underlying assets include stocks, bonds, commodities, currencies, interest rates and market indexes. Some of the most commonly traded derivatives are futures, forward, options and swaps. EQUITY SHARES = Equity shares , commonly referred to as ordinary share also represents the form of fractional ownership in which a shareholder, as a fractional owner , undertakes the maximum entrepreneurial risk associated with a business venture. The holder of such shares is the member of the company and has voting rights. PREFERNCE SHARES=In simple terms , the preference shares are those shares which have rights of preference over equity shares in the case of distribution of dividend and distribution of surplus in the case of winding up. They generally carry a fixed rate of dividend and redeemable after specific period of time. Cumulative preference shares

Non – cumulative preference shares

Convertible preference shares

Redeemable preference shares

Participating preference shares

Non participating preference shares

DEBENTURES Section 2 ( 30) of the Companies Act, 2013 defines debentures, “Debenture” includes debenture stock, bonds or any other instrument of a company evidencing a debt, whether constituting a charge on the assets of the company or not ; Debenture is a document evidencing a debt or acknowledging it and any document which fulfills either of these conditions is a debenture. SWEAT EQUITY SHARES Section 2 (88) of the Companies Act , 2013 defines “ sweat equity shares “ means such equity shares as are issued by a company to its directors or employees at a discount or for consideration , other than cash, for providing their know – how or making available rights in the nature of intellectual property rights or value additions , by whatever name called. According to Section 54 of the Companies Act, 2013 a company may issue sweat equity shares of a class of shares already issued, if the following conditions are fulfilled:

(a) The issue is authorized by a special resolutionpassed by the company in the general

meeting.

Finance UGC NET

2 Addarsh Basti Tonk Phatak,Jaipur, 8058195333, Study Material, Video classes, Online Test series, Notes by Jitendra Sharma Page 8

(b) The resolution specifies the number of shares, current market price , consideration if

any and the class or classes or directors or employees to whom such equity shares are

to be issued.

(c) Not less than one year has elapsed at the date of the issue, since the date on which the

company was entitled to commence business.

(d) The sweat equity shares of a company whose equity shares are listed on a recognized

stock exchange are issued in accordance with the regulations made by SEBI in this

regard and id they are not listed the sweat equity shares are to be issued in accordance

with the rule 8 of Companies (Share Capital and Debenture) Rules, 2014.

SECURED PREMIUM NOTES ( spn) = These instruments are issued with detachable warrants and are redeemable after a notified period say 4 to 7 years. The warrants enable the holder to get equity shares allotted provided the secured premium notes are fully paid. The holder has an option to sell back the SPN to the company at par value after the lock in period. If the holder exercise this option, no interest / premium is paid on redemption, in case the holder keeps it further, he is repaid the principal amount along with the additional interest / premium on redemption Qu. Financial instruments which are issued with detachable warrants and are redeemable after certain period is known as:

(1) Deep Discount Bonds

(2) Secured Premium Notes

(3) Bunny Bonds

(4) Junk Bonds

Extendable notes = maturity that can be extended by mutual agreement between the issuer

and investors. Extendable notes are issued for 10 years with flexibility to the issuer to review

the interest rate every two years.

Zero coupon bond = it is issued at a discount to face value. No interest is paid during the period. But at the time maturity full payment or bullet payment of the face value would be done. (Not fixed but general 5 to 10 year after deep discount bond) ZERO COUNPON CONVERTIBLE NOTES = These are debt convertible into equity shares of the issuer. If investors choose to convert, they forgo all the accrued and unpaid interest. These convertibles are generally issued with put option to the investors. The advantage to the issuer is the raising of convertible debt without heavy dilution of equity. Since the investors give up acquired interest by exercise of conversion option, the conversion option may not be exercised by many investors.

Finance UGC NET

2 Addarsh Basti Tonk Phatak,Jaipur, 8058195333, Study Material, Video classes, Online Test series, Notes by Jitendra Sharma Page 9

DEEP DISCOUNT BOND A zero-coupon bond (also discount bond or deep discount bond) is a bond where the face value is repaid at the time of maturity. Note that this definition assumes a positive time value of money. It does not make periodic interest payments, or have so-called "coupons", hence the term zero-coupon bond. DISASTER BONDS = These are issued by companies and institutions to share the risk and expand the capital to link investors return with the size of insurer losses. The bigger the losses, the smaller the return and vice - versa. The coupon rate and the principal of the bonds are decided by the occurrence of the casualty of disaster and by the possibility of borrower defaults. OPTION BONDS = This instrument covers those cumulative and non – cumulative bonds where interest is payable on maturity or periodically and redemption premium is offered to attract investors. EASY EXIT BONDS = This instrument covers both bonds which provide liquidity and an easy exit route to the investor by way of redemption or buy back where investors can get ready enchantment in case of need to withdraw before maturity. PAY IN KIND BONDS = This refers to bonds wherein interest for the first three to five years is paid through issue of additional bonds , which are called baby bonds as they are derived from parent bond. DERIVED INSTRUMENTS A derivative is an instrument whose value is derived from the value of one or more underlying, which can be commodities, precious metals, currency, bonds, stocks, stocks indices, etc. Four most common examples of derivative instruments are Forwards, Futures, Options and Swaps. Mortgage bond = Mortgage backed bonds is collateralize term- debt offering. Every issue of such bonds is backed by pledged collateral. Property that can be pledged as security for mortgage bonds is called eligible collateral. The terms of these bonds are like bonds floated in the capital market, semi- annual or quarterly payments of interest and final bullet payment of principal. Pass Through Certificates = When mortgages are pooled together and undivided interest in the pool is sold, pass- through securities are created. The pass through securities promise that the cash flow from the underlying mortgages would be passed through to the holders of the securities in the form of monthly payments of interest and principal Participation Certificates BENCH MARKED INSTRUMENTS = There are certain debt instruments wherein the fixed income earned is based on a bench mark. For instance, the Floating interest rate Bonds bench-marked to either the LIBOR, MIBOR etc

Floating Interest Rate = Floating rate of interest simply means that the rate of interest is variable. Periodically the interest rate payable for the next period is set with reference to a benchmark market rate agreed upon by both the lender and the borrower. The benchmark market rate is the State Bank of India Prime Lending Rate in domestic markets and LIBOR or US Treasury Bill Rate in the over as markets.

Finance UGC NET

2 Addarsh Basti Tonk Phatak,Jaipur, 8058195333, Study Material, Video classes, Online Test series, Notes by Jitendra Sharma Page 10

Inflation Linked Bonds = A bond is considered indexed for inflation if the payments on the instruments are indexed by reference to the change in the value of a general price or wage index over the term of the instrument. The options are that either the interest payments are adjusted for inflation or the principal repayment or both.

Securities Market Intermediaries The role of intermediaries makes the market vibrant, and to function smoothly and continuously.

The following market intermediaries are involved in the Securities Market

PRIMARY MARKET INTERMEDIARIES

The following market intermediaries are involved in the primary market:

1.Merchant Bankers/Lead Managers 2.Registrars and Share Transfer Agents. 3.Underwriters 4.Bankers to issue. 5.Debenture Trustees

The following market intermediaries are involved in the secondary market

1)Stock brokers 2)Portfolio managers 3)Custodians 4)Foreign Institutional Investors

5)Investment Adviser 6. Depository participant 7.Jobbers

This secondary market has further two components, 1. The spot market (cash market) = where securities are traded for immediate delivery and payment, (t+2 basis) 2. Future market (derivatives market) = where contract entered today but executed a future date. Future market divided in to two parts A. future and B. Option A. FUTURE = future contract and forward contract B. OPTION = call option and put option DIFFEREANCE BETWEEN CASH AND DERIVATES MARKET

cash market

Derivatives market

1. the settlement of contract is delivery based 1. delivery not required the settlement is done by paying or receiving the difference between the contract rate and the closing rate on the expiry of contract

2.no margin is required full payment on

contract date itself

2, only margin money required

Finance UGC NET

2 Addarsh Basti Tonk Phatak,Jaipur, 8058195333, Study Material, Video classes, Online Test series, Notes by Jitendra Sharma Page 11

3. contract can be done is desired quantity 3. specific lot of size

FUTURES Futures is a contract between two parties to buy or sell a underlying asset of standardized quantity and quality for a price at agreed upon today with delivery and payment occurring at a specified future date. Underlying assets for the purpose include equities, foreign exchange, interest bearing securities and commodities. The idea behind financial futures contract is to transfer future changes in security prices from one party in the contract to the other.

DIFFERENCE BETWEEN FORWARD CONTRACH AND FUTURE CONTRACT

Basis of Diff FORWARD CONTRACT FUTURE CONTRACT

Trading Forward contracts are traded

on personal basis or on

telephone or otherwise.

Future contracts are traded

in a competitive arena.(on

markets)

Size of Contract Forward contracts are

individually tailored and have

no standardized size

Futures Contracts are

standardized in terms of

quantity or amount as the

case may be

Organized exchanges Forward contract are traded

in an Over the Counter

Market

Future contracts are traded

on organized exchanges with

a designated physical

location

Settlement Forward Contract are

settlement takes place on the

date agreed upon between

the parties

Future contracts settlement

are made daily via exchange

clearing house

Delivery Forward contracts may be

delivered on the dates

agreed upon and in terms of

actual delivery

Future contracts delivery

dates are fixed on cyclical

basis and hardly takes place.

However , it does not mean

that there is no actual

delivery

Transaction costs Cost of forward contracts is

based on bid ask spread

Future contracts entail

brokerage fees for buy and

sell orders

Marketing to Market Forward Contracts are not Future Contracts are subject

Finance UGC NET

2 Addarsh Basti Tonk Phatak,Jaipur, 8058195333, Study Material, Video classes, Online Test series, Notes by Jitendra Sharma Page 12

subjects to marking to

market

to marking to market in

which loss of profit is debited

or credited in the margin

account on daily basis due to

change in price

Margins Margins are not required in

forward contract

In future contracts every

participant is subject to

maintain margin as decided

by exchange authorities

Credit Risk Credit risk is borne by each party and therefore every party has to evaluate the credit worthiness of other party ( default = yes) Rule regulation = low Purposegenerally= hedging

Liquidity = low

The transaction is a two way transaction through exchange and hence the parties need not bother for the risk ( default = no) High Speculation

high

Qu. Assertion (A) : A futures contract specifies in advance the exchange rate to be used , but it is not as flexible as a forward Contract. Reason (R) : A futures contract is for specific currency amount and a specific maturity date. Codes:

(A) (R) is a correct explanation of (A)

(B) (R) is not a correct explanation of (A)

(C) (A) and (R) are not related with each other.

(D) (R) is irrelevant for (A)

Qu. Which of the following most appropriately describes the meaning of the term “Option Forward’ ?

(A) Forward contract entered into along with buying a call option.

(B) Forward contract entered into for buying or selling at a future date.

(C) Forward contract entered into for buying or selling over a period of time.

(D) Forward contract entered into with writing a put option.

option

Finance UGC NET

2 Addarsh Basti Tonk Phatak,Jaipur, 8058195333, Study Material, Video classes, Online Test series, Notes by Jitendra Sharma Page 13

OPTIONS ARE TWO TYPES 1. Call option and 2. Put option) An option contract conveys the right, but not the obligation, to buy or sell a specific security or commodity at specified price within a specified period of time. The right to buy is referred to as a call option whereas the right to sell is known as a put option. An option contract comprise of its type a put or call , underlying security or commodity expiry date, strike price at which it may be exercised. Option provides the investor with the opportunity to hedge investments in the underlying shares and share portfolios and can thus reduce the overall risk related to the investments significantly. Generally two type of options namely: European option- an option can be excised only on a specified date American option – An option exercised anytime within a specified time period KEY WORDS

Option is right but not obligation

In option loss only for premium amount but profit in unlimited

Call option (right to purchase) at this point investor see market are going upper side

Put option (right to sale) at this point investor see market are going to lower side

Terms one should know Long Position = A position showing a purchase or a greater number of purchases than sales in anticipation of a rise in prices. A long position can be closed out through the sale of an equivalent amount. Short Position – in futures, the short has sold the commodity or security for future delivery, in options, the short has sold the call or put and is obligated to take a future position if he or she is assigned for exercise. Qu. In case a farmer in India buys a wheat option on future:

(a) The farmer must accept a wheat futures contract and not take physical possession of

wheat.

(b) The farmer must accept delivery of the wheat at a higher price.

(c) The farmer has the right to delivery of the wheat and will do so only if the price is

favorable.

(d) The farmer must deliver the wheat at market price.

Codes:

Finance UGC NET

2 Addarsh Basti Tonk Phatak,Jaipur, 8058195333, Study Material, Video classes, Online Test series, Notes by Jitendra Sharma Page 14

(1) (a) and (d)

(2) (d) only

(3) (c) only

(4) (b) and (c)

Qu. Following statements are related to futures contracts. Choose the statements that are not true:

(A) Purchase of a futures contract is called short position.

(B) Currency futures are traded on an exchange in standardized form and in fixed quantity.

(C) Default risk in futures contract is high compared to forward contract.

Codes

(1) Only (a) and (b)

(2) Only (a) and (c)

(3) (a) , (b) and (c)

(4) Only (b)