Embed Size (px)

Citation preview

President

Vice President

Members (in alphabetical order)

Secretary & Chief Executive Officer :

Chairman

Members(in alphabetical order)

Editor & Publisher :

Consulting Editor :

Legal Correspondent :

Nesar Ahmad

S. N. Ananthasubramanian

Anil Murarka

Ardhendu Sen

Arun Balakrishnan

Ashok Kumar Pareek

Atul Hasmukhrai Mehta

Atul Mittal

B. Narasimhan

Gopalakrishna Hegde

Harish Kumar Vaid

Pradeep Kumar Mittal

Renuka Kumar (Ms.)

Sanjay Grover

Saroj Punhani (Ms.)

Sridharan R

Sudhir Babu C

U D Choubey (Dr.)

Umesh Harjivandas Ved

Vikas Yashwant Khare

N. K. Jain

S. Balasubramanian

Archana Shukla (Dr.)

D S Sengar (Prof.)

G R Bhatia

H S Siddhu

Harish K Vaid

K S Chalapati Rao (Dr.)

N V Narasimham (Prof.)

Pavan Kumar Vijay

Pradeep K Mittal

R S Nigam (Prof.)

Rakesh Chandra

Renu Budhiraja (Ms.)

S Chandrasekaran (Dr.)

Sanjeev Kumar (Dr.)

Sumant Batra

T V Narayanaswamy

V K Singhania (Dr.)

N. K. Jain

V. Gopalan

T. K. A. Padmanabhan

02

Inland : Rs. 750 (Rs. 300 for Students of the ICSI)Foreign : $75; £40 (surface mail) Single Copy : Rs. 75

‘Chartered Secretary’ is normally published in the first week of everymonth. Non-receipt of any issue should be notified within that month. Articles on subjects of interest to company secretaries are welcome. Views expressed by contributors are their own and the Institute doesnot accept any responsibility. The Institute is not in any wayresponsible for the result of any action taken on the basis of theadvertisement published in the journal. All rights reserved. No part ofthe journal may be reproduced or copied in any form by any meanswithout the written permission of the Institute. The write ups of thisissue are also available on the website of the Institute.

Edited, Printed & Published byN. K. Jain for The Institute of Company Secretaries of India, ‘ICSI House’, 22, Institutional Area, Lodi Road, New Delhi- 110 003. Phones : 41504444, 45341000, Grams : ’COMPSEC’Fax : 91-11-24626727 E-Mail : [email protected] Website : http://www.icsi.edu

Design & Printed at M. P. PrintersB-220, Phase II, Noida-201305Gautam Budh Nagar, U. P. - India

ISSN 0972-1983

[ Registered under Trade Marks Act, 1999 ]

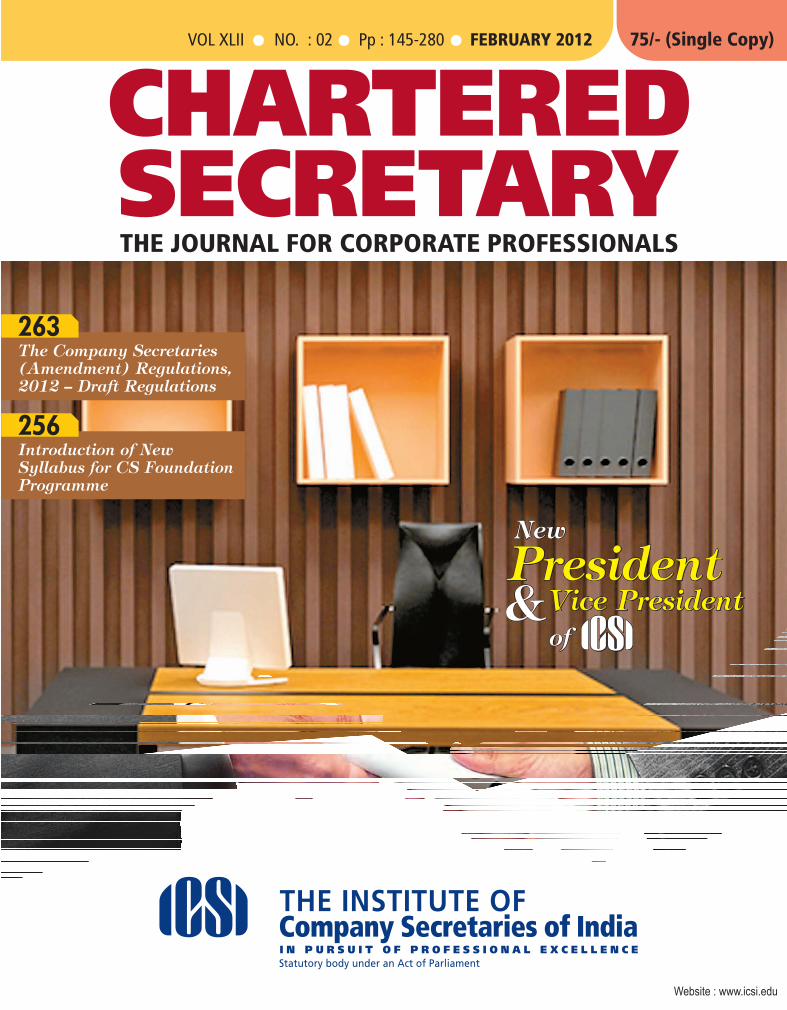

Vol. : XLII No. 2 Pp 145-280 February-2012

Legal

World192

(LW-15-24)

News from the

Institute224

From the

Government202

(GN-26-46)

Our

Members280

The Council

Editorial Advisory Board

Annual Subscription

152 From the

President

CHARTERED SECRETARYR

CHARTERED SECRETARY145February

2012

ARTICLES ( A 47- 84 )

Insider Trading: Duties of Insiders and Company Secretary 154

Refreshing Revisions in Schedule VI 161

Issue of Bonus Shares by a Public Limited Listed Company 166A Practical Approach

Impact of Gender Diversity: Women Participation in 169Boardroom and their Efficiencies

Corporate Criminal Liability Punishing the 175Directors or the Corporation

Of Anticipatory Bail Then & Now 182

Implications of Service Tax & Value Added 185Tax on Works Contract

ICSI-Feb-2012-4.qxd 2/1/2012 2:09 PM Page 1

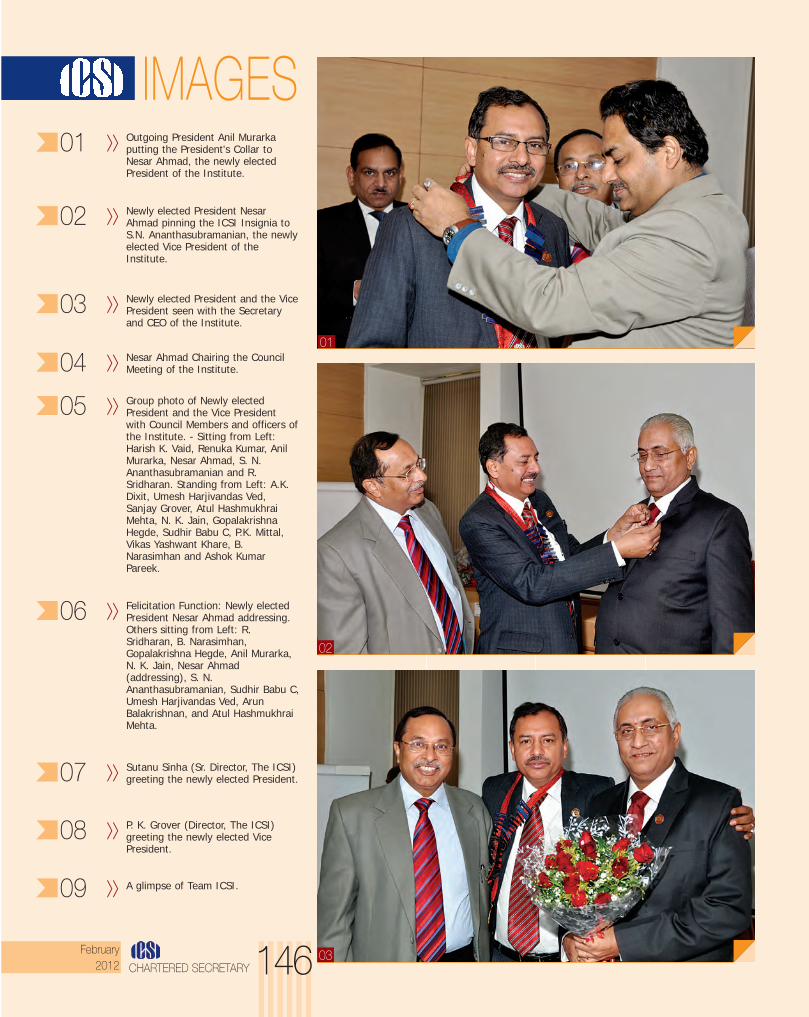

Outgoing President Anil Murarkaputting the President's Collar toNesar Ahmad, the newly electedPresident of the Institute.

01

Sutanu Sinha (Sr. Director, The ICSI)greeting the newly elected President. 07

P. K. Grover (Director, The ICSI)greeting the newly elected VicePresident.

08

A glimpse of Team ICSI.09

Newly elected President NesarAhmad pinning the ICSI Insignia toS.N. Ananthasubramanian, the newlyelected Vice President of theInstitute.

02

Group photo of Newly electedPresident and the Vice Presidentwith Council Members and officers ofthe Institute. - Sitting from Left:Harish K. Vaid, Renuka Kumar, AnilMurarka, Nesar Ahmad, S. N.Ananthasubramanian and R.Sridharan. Standing from Left: A.K.Dixit, Umesh Harjivandas Ved,Sanjay Grover, Atul HashmukhraiMehta, N. K. Jain, GopalakrishnaHegde, Sudhir Babu C, P.K. Mittal,Vikas Yashwant Khare, B.Narasimhan and Ashok KumarPareek.

05

Felicitation Function: Newly electedPresident Nesar Ahmad addressing.Others sitting from Left: R.Sridharan, B. Narasimhan,Gopalakrishna Hegde, Anil Murarka,N. K. Jain, Nesar Ahmad(addressing), S. N.Ananthasubramanian, Sudhir Babu C, Umesh Harjivandas Ved, ArunBalakrishnan, and Atul HashmukhraiMehta.

06

Newly elected President and the VicePresident seen with the Secretaryand CEO of the Institute.

03

Nesar Ahmad Chairing the CouncilMeeting of the Institute. 04

CHARTERED SECRETARY 146February

2012

01

IMAGES

02

03

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 2

February

2012CHARTERED SECRETARY147

04

05

06 07

08

09

ICSI-Feb-2012-4.qxd 1/31/2012 10:57 PM Page 3

Insider Trading: Duties of Insiders and Company Secretary

Dr. K R Chandratre

Insider trading, as it involves misuse of confidentialinformation, is unethical amounting to breach of fiduciary

position of trust and confidence. Being fiduciaries towards thecompany, directors must act bona fide in the interests of thecompany and must not exercise their powers for any collateralpurpose. Further a director must not place himself in a positionwhere his duty to the company and his personal interestsconflict and he must not profit from his position as a director.This is equally true about company officers. The objective of theSecurities and Exchange Board of India (Insider Trading)Regulations, 1992 is to prevent and curb the menace of insidertrading in securities. In particular, the Regulations render insidertrading a criminal offence in certain circumstances, punishableunder the SEBI Act. The company secretary has onerousobligations in the matter of preventing insider trading bycompany directors, officers and others, in terms of disclosureand reporting.

Refreshing Revisions in Schedule VI Sriraman Parthasarathy

Schedule VI of the Companies Act, 1956 which defines thefinancial reporting framework for Indian Corporates has

been amended vide Notification dated 28 February 2011 whichis applicable for the financial statements prepared for allfinancial periods beginning on or after 1 April 2011. RevisedSchedule VI has been framed as per the existing non-convergedIndian Accounting Standards notified under the Companies(Accounting Standards) Rules, 2006. Revised Schedule VI hasintroduced several new concepts and disclosure requirementsfor financial reporting and it has also done away with severalredundant statutory disclosure requirements. This article isintended to discuss some of the key changes contained in theRevised Schedule VI, and their implications.

Issue of Bonus Shares by a Public Limited Listed Company A Practical Approach

P. Kesavulu Reddy

Issue of bonus shares by companies involves multifariouscompliances. In view of several restrictions and constraints,

the entire process of issue of bonus shares is required to bemeticulously planned with a view to avoid defaults andconsequent penalties. The step by step procedure for issue ofbonus shares is given in the article.

Impact of Gender Diversity:Women Participation in Boardroom and their Efficiencies

Komal Khilnani

In ancient times, women were considered as a symbol of love,purity, fertility, sacrifice. If we check the history of the Roman,

women were proved as good managers and played animportant role in the decision making process. Without anydoubt, women have proved their mettle. This article emphasiseswomen's participation in boardroom and examines what couldbe the productive results through their participation.

Corporate Criminal Liability Punishing the Directors or the Corporation

Manisha Chaudhary

For a very long time, common law countries like England andCanada did not generally let a corporation to be convicted of a

crime (as opposed to regulatory offences). There were exceptionsand these exceptions were usually based on the doctrine ofrespondeat superior (vicarious liability). However, the burden ofattributing mens rea to a non-human entity still remained a bighurdle in imposing criminal liability on corporations.The question ofimposing criminal liability to a corporation for criminal offencescommitted by its directors and officers while conducting corporateaffairs has gained a lot of importance in criminal jurisprudence.There is no impediment in the criminal jurisprudence whatsoever toimpose criminal sanction on a corporation since it can have a mindof its own and also an environment wherein crime is nurtured.Criminal jurisprudence in India has seen one exception in form ofdoctrine of strict liability in which one may be made liable in theabsence of any guilty state of mind.

Of Anticipatory Bail Then & NowShantimal Jain

The provision of anticipatory bail was inspired by Article 21ofthe Constitution of India.Ever since this provision was

brought on statute and subsequent to the celebrated discussionof the Constitution Bench in Gurbax Singh's case there have beenenough evolution of the concept of anticipatory bail. Unfortunatelysome amendment was proposed and passed which practicallytended to roast the objective of bringing this provision. However,unmindful of the development the different courts and evenSupreme Court interpreted the provision narrowly. Somedecisions were anomalous to the basic concept of anticipatorybail and some rulings even went beyond the confines of theprovision in favour of the expediency and distorted the legislativecontents of the provisions. In the recent case of Siddha RamSatlingappa Mhetre v. State of Maharashtra (2011) 1 SCC 694the Supreme Court has reiterated the fundamentals of GurbaxSingh's case and liberalised, enlarged, expanded and widenedthe scope of grant of anticipatory bail.This article analyticallyexamines the implication and impact of the decision.

Articles (A 47- 84) 154p- 169p-

175p-

182p-

154p-

161p-

166p-

CHARTERED SECRETARY 148February

2012

At a Glance

ICSI-Feb-2012-4.qxd 2/1/2012 2:20 PM Page 4

At a Glance

February

2012CHARTERED SECRETARY149

Legal World (LW 15-24)

Other Highlights

From the Government (GN 26 - 46) 202p-

224p-

uu LW 11.02.2012 Delhi High Court admits winding uppetition for non payment of admitted debt.

uu LW 12.02.2012 Mixing of polymer with bitumen is notmanufacture.[SC]

uu LW 13.02.2012 Incentive scheme encouraging theemployees to acquire additional qualifications is notdiscriminatory. [SC]

uu LW 14.02.2012 Based on the conduct of the workman, theDelhi High Court modifies the reinstatement with backwages order into payment of compensation. [Del]

uu LW 15.02.2012 Supreme Court recommends longer termof imprisonment for drunk driving.[SC]

uu LW 16.02.2012 In a cheque dishonour case, the trial courthas to decide the extent to which the cross examination ofthe complainant can be made by the accused. [Del]

uu LW 17.02.2012 Dishonour of cheques issued towardsrefundable security deposit under a lease deed is coveredunder section 138 of NIA.[Del]

uu LW 18.02.2012 When the No Claims Certificate wasissued after negotiation, the contractor cannot turn aroundand claim that it was issued under coercion.[Del]

uu LW 19.02.2012 Council of Architects is not empowered tolay down or prescribe minimum standards of education forqualifications other than recognized qualificationsmentioned in the Schedule of Architects Act. [Del]

uu LW 20.02.2012 Guarantor cannot take shelter underSec.37 of the Contract Act to avoid paying the guaranteedsum to the lender. [SC]

Implications of Service Tax & ValueAdded Tax on Works Contract

Nitesh Agarwal & Vinay Kumar Joshi

For entities engaged in works contract business, it iseconomically and procedurally beneficial to lay down an

efficient tax structure and implement an apt commercial taxplanning before undertaking a works project. There alreadyprevails a mystification in VAT and service tax aspects relatingto works contracts. An attempt has been made in this article toaddress certain issues faced by business entities andprofessionals concerned with works contract business.

u Fees Payable in terms of Regulations 29 and 30 of theCLB Regulations, 1991

u The Company Law Board (Amendment) Regulations,2012

u Eligibility criteria for qualified depository participant.u Composition of Arbitration Committeeu Investor Grievance Redressal Mechanism at Stock

Exchangesu Trade controls in Normal Trading Session for Initial Public

Offering (IPO) and other category of scripsu Call Auction in Pre-open session for Initial Public Offering

(IPO) and other Category of Scripsu Disclosure of Track Record of the public issues managed

by Merchant Bankersu Changes in Re-Investment Period of FII Debt Limitu External Commercial Borrowings (ECB) Policy - Infrastructure

Finance Companies (IFCs)u External Commercial Borrowings - Simplification of procedureu Guidelines on Compensation of Whole Time Directors /

Chief Executive Officers / Risk takers and Control functionstaff, etc.

u Guidelines on Compensation of Whole Time Directors /Chief Executive Officers / Other Risk Takers

u Methodologies for risk and performance alignment ofremuneration

u Disclosure requirements for remunerationu Centralised Processing of Returns Scheme, 2011u Review of the policy on Foreign Direct Investment -

liberalization of the policy in Single - Brand Retail Trading

u Members Admitted/ Restoredu Certificate of Practice Issued/Cancelledu Licentiate ICSI Admittedu Company Secretaries Benevolent Fundu Payment of Annual Membership and Certificate of Practice Feeu News From the Regionsu ICSI-CCGRT NEWSu Foundation Programme New Syllabusu Online Services available to Membersu ICSI Knowledge Portal (ICSI-KP)u The Company Secretaries (Amendment) Regulations,

2012 - Draftu Contractual Engagement at MCA-21 for XBRL Worksu Book Reviewu Company Secretaries Benevolent Fundu Our Membersu Exposure Draftu The Standing and Other Committees/Boards of the Council

for the year 2012-2013u CS Quizu ICSI-WIRC Half-day Programme

185p-

192p-

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 5

CHARTERED SECRETARY 150February

2012

CG & CSR : WATCHThe Institute has always been in the frontline to promote good corporate governance and it has been theconstant endeavour of the Institute to raise awareness among the members and students in CorporateGovernance arena. This watch gives an update of the latest happenings in the area of CorporateGovernance and Corporate Social Responsibility.

NEW DEVELOPMENTS1.Financial Reporting Council (UK) reports high level of implementation of key

Corporate Governance provisions. The Financial Reporting Council (FRC) on 14th December, 2011 has published its first analysis of how the two UK Codesunder its supervision are being implemented i.e. the UK Corporate Governance Code for listed companies, revised in 2010,and the UK Stewardship Code for investors, launched in the same year.

The report reveals the high level of adherence to the new provisions announced last year. It shows that 80 per cent of FTSE350 boards have put all their directors up for annual re-election, demonstrating the value of the UK Corporate GovernanceCode in promoting behavioural change in the boardroom.

It also revealed that over 230 asset managers, asset owners and service providers signed up to the Stewardship Code in itsfirst year, including most of the major investors in UK equities. The report highlights evidence that the quality of engagementbetween investors and company boards is improving in certain areas, for example in discussions around corporate risk.The FRC has indicated that it will make limited changes to both the Codes during 2012 to promote further behaviouralchanges and to strengthen the dialogue between companies and their investors.

Copy of the report can be accessed at:http://www.frc.org.uk/press/pub2671.html

2. International Corporate Governance Network (ICGN) submitted its response to draftreport on corporate governance framework for European companiesOn 12th December 2011, International Corporate Governance Network (ICGN) submitted its response to draft report oncorporate governance framework for European Companies that was published by the Committee on Legal Affairs,EUROPEAN PARLIAMENT on 27.10.2011.ICGN has made its recommendations on the following areas of Corporate Governance:(a) Boards of directors

u Demarcation role Chair/CEOu Recruitment policiesu Remuneration policies

(b) Shareholdersu Voting chainu Shareholder identificationu Proxy advisory firms

Details can be accessed at:http://www.icgn.org/comment-letter.php?letter=5644

GREEN CORNERGREEN IDEA If: u You care about the environment.

u You want to save earth.

u Take green steps to make your contribution.

USE RECYCLED PAPER - "EVERY TON OF RECYCLED OFFICE PAPER SAVES 380 GALLONS(APPROX. 1438 LITRES) OF OIL"Avoid products with several layers of packaging when only one is sufficient. About 33% of what we throw away is packaging.By recycling half of our household waste, we can save 2,400 pounds of carbon dioxide annually.

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 6

February

2012CHARTERED SECRETARY151

Be bright about light/energy-u In one day, the sun provides more energy than our population could use in 27 years. Promote and make use of solar energy.u Artificial lighting accounts for 44 percent of the electricity use in office buildings.u Make it a habit to turn off the lights when you're leaving any room for 15 minutes or more and utilize natural light when you can.u Buy Energy Star-rated light bulbs and fixtures, which use at least two-thirds less energy than regular lighting, and install

timers or motion sensors that automatically shut off lights when they're not needed.

Something Good: OLD CLOTH VALUE CHAIN - by GOONJ…GOONJ is an acclaimed voluntary organization working on the issue of clothing need of poor. Started in 1998 with 67personal clothes, GOONJ is channelising over 70,000 kgs of material every month. Its key initiative includes VASTRA-SAMMAN, Cloth for work etc.

VASTRA-SAMMAN is a nationwide movement highlighting the importance of cloth as a basic need of poor. Theimplementation of VASTRA-SAMMAN takes place through Cloth for Work where clothes and other material are not providedas charity but as a motivational reward for village level development activities.

The idea behind Cloth for Work is to motivate Village communities to identify the pressing development needs of their ownarea and encourage them to do Shramdaan (Community Labour) for village development and they will get material in return,with dignity; as a reward.

To Remember:February 4 - World Cancer Day (WHO) February 20 - World Day of Social JusticeFebruary 21 - International Mother Language Day [UNESCO]

QUOTE OF THE MONTH

“Global market forces will sort out those companies that do not have sound corporate governance.”

- Mervyn King (Chairman: King Report)

FORTHCOMING EVENTSSEBI-OECD International Conference on Investor Education

An International Conference on Investor Education with the theme “Investor education: Towards a more inclusive andsecure financial world” is being co-hosted by the Securities and Exchange Board of India (SEBI) and Organisation forEconomic Co-operation and Development (OECD) on 3-4 February 2012, at the Goa Marriott Resort, Goa (India).

In the presence of the Honourable Finance Minister of India Pranab Mukherjee and Ambassador Richard A. Boucher, DeputySecretary-General of the OECD, the Conference will:u explore the specificities of investor education: the global context, rationale and research, main challenges, good practices

and programmes to reach out to targeted groups as well as innovative solutions u address international issues and analyse global trends, with a special attention to Asia and its investor education needsThe OECD contribution to this event is sponsored by the Government of Japan.

The details can be accessed at:http://www.oecd.org/dataoecd/60/7/49289024.pdf

FEEDBACK & SUGGESTIONSReaders may give their feedback and suggestions on this page to Mrs. Alka Kapoor, Joint Director, ICSI

Disclaimer:The contents under CG & CSR: Watch have been collated from different sources. Readers are advised to cross check fromoriginal sources.

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 7

CHARTERED SECRETARY 152February

2012

From the President

Dear Professional Colleagues,

The integrity of our perception andaction is perhaps the mostimportant trait that determines oursuccess in life - personal as well asthe professional. It is impossible tohave professional integrity withoutpersonal integrity and it has to comefrom within. Having said that I wishto say that there is no middle path tothe integrity. Either you are behavingwith integrity or you are not. Thereare innumerable studies thatindicate that convenience play spoilsport to the integrity.

Friends, you will appreciate that today's worldis entirely different than it was a decade agoand it will not remain the same in theimmediate future because of the speed atwhich changes are occurring. So we have tobe on learning curve, unlearn and relearn the

A dewdrop is a perfect integrity that has no filial memory of its parentage

nuances of emerging paradigm, to establishourselves in the dynamic market place. Inachieving this, the rich traditions, standardsand values of our profession should be ourguiding light, I am sure.

I am delighted and privileged to address myfirst communication to you after assuming theaugust office of the President of thisprestigious professional Institute. I would, atthe outset, like to express my heart-feltgratitude to my esteemed colleagues on theCouncil and all of you for having reposed thetrust and confidence in me. I accept thishonour with all my humility and wish to assureyou that it shall be my endeavour to furtherenhance the prestige of the Institute and theprofession.

The year 2011 has been an eventful year interms of adoption of ICSI Vision 2020, settingof top 10 goals for the Council, initiation ofprocess of syllabus review, strengthening ofinfrastructure, and several internationalnetworking initiatives, and also theintroduction of Companies Bill, 2011 inParliament by the Government. I am confidentthat with your support and wisdom, I shall beable to carry out the plans and tasks initiatedby my predecessors and devise strategies andaction plans for providing new dimensions tothe profession of Company Secretaries, in thecurrent business environment evolving out ofhighly contestable market dynamics.

My predecessors have set high expectationsin the minds of stakeholders through theircommendable performance. I undertake tocome upto the expectations of thestakeholders with the various initiatives in thechanging environment. The task is enormousand calls for proactive approach, spirit ofexcellence, healthy debate on vital issues andabove all, collective wisdom and coordinatedteam work. I seek your indulgence, guidanceand support in building upon the excellentwork already done for the healthy growth anddevelopment of the profession. I assure youthat I will use best of my time and energy tokeep up to the expectations and faith and trustreposed in me.

Members are the custodian of goodwill andreputation of the profession. The better are the

- Rabindranath Tagore

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 8

February

2012CHARTERED SECRETARY153

From the President

opportunities, the more there would be spaceto showcase the knowledge, the expertise andthe efficiency to our stakeholders. It will,therefore, be my endeavor to pursue theGovernment and the regulatory authorities tocarve out new areas for our members, bothin employment and in practice.

Students are the backbone of the sustainedgrowth and goodwill of the profession, andtheir capacity building to nurture them to meetthe challenges of ever evolving dynamicbusiness environment is a duty cast upon us.In that context, providing a contemporarysyllabus, strengthening of training structureand creating more infrastructure will be on thetop of agenda during the year. It will be myendeavour to ensure that our youngProfessionals are well equipped to face thechallenges of changing business expectationswith confidence.

The Syllabus Review Committee has alreadyformulated the syllabus for FoundationProgramme, Executive Programme andProfessional Programme. The Council hasapproved and implemented the new syllabusfor Foundation Programme w.e.f. February 1,2012. The first examination for FoundationProgramme under the new syllabus would beheld from December, 2012 session under theOptical Mark Recognition (OMR) system.There will be no negative marking under OMRSystem. It has also been decided that thestudents pursuing Foundation Programmeunder existing syllabus would be given optionto change over to new syllabus without anyexemption. Students would be provided twoattempts to complete the FoundationProgramme under the existing syllabus unlessthey switch-over to the new syllabus. The firstexamination for Foundation Programmeunder new syllabus will be held in two days,each day having two sessions of two hours,and the last examination for FoundationProgramme under the existing syllabus wouldbe in June, 2013. The Council hasdiscontinued the requirement of CoachingCompletion Certificate for FoundationProgramme under new syllabus.

The Council of the Institute has approved inprinciple the new syllabus for ExecutiveProgramme and Professional Programme and

decided to publish the same as ExposureDraft soliciting views and suggestions frommembers, students and all other stakeholders.The Exposure Draft is available on the websiteof the Institute. I invite all of you to send to theInstitute your considered views and suggestionson the proposed syllabus for Executive andProfessional Programmes, on or beforeFebruary 29, 2012.

Efforts at institution building and strengtheningof infrastructure at Regional and Chapter levelwould continue to receive added emphasis, asit is imperative to enhance the visibility and toprovide value added services to students andmembers to maintain the growth momentumof the profession.

The influence and the high purpose of ourprofession is being recognized andappreciated not only in India but across theborder. The Institute has been activelyengaged in creating brand 'CS' across thejurisdictions through engagement andinterface with its counterparts abroad. First,the International Federation of CompanySecretaries (IFCS) and now the CompanySecretaries International Association (CSIA) isthe recognition of our efforts towardsinternationalization of profession of CompanySecretaries. You are aware the Institute hasbeen making constant efforts towards creationof new sub-head for company/corporatesecretaries services under Services SectoralClassification of WTO. Much of the headwayhas been made, yet we have a long way to goto achieve the desired purpose. I wish toassure all of you that I will leave no stoneunturned to achieve our long cherished goal.

Let us look forward to a fruitful year ahead.

With kind regards,Yours sincerely,

New DelhiJanuary 31, 2012

(CS. NESAR AHMAD)[email protected]

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 9

CHARTERED SECRETARY 154February

2012

Articles

Dr K. R. Chandratre, FCS

Practising Company Secretary Pune.

Insider Trading:

Duties of Insiders andCompany Secretary

An International investment expert asreported by Associated Press from NewYork, Raj Rajaratnam, the hedge fundbillionaire at the center of the biggestinsider-trading case in U.S. history, wassentenced recently for 11 years thestiffest punishment ever handed out forthe crime. "His crimes and the scope ofhis crimes reflect a virus in our businessculture that needs to be eradicated,"U.S. District Judge Richard J. Holwellsaid, "Simple justice requires a lengthysentence."

The judge called it "an assault on the free marketsthat are a fundamental element of our democraticsociety. There may not be readily identifiablevictims, but when the playing field is not level, theintegrity of the marketplace is called into questionand the public suffers."Now it is the turn of Rajat Gupta, who will face trial

on the charge of tipping Rajaratnam insider informationconcerning some listed companies, which is an offence ofequal scale. It was said by an international investment experta few years ago that in the Indian capital market most listedcompanies' securities are traded on the basis of informationwhich is not on the public domain and in many casespromoters or people in control of management themselvesindulge, directly or indirectly, in insider trading.

The evil of insider tradingInsider trading causes injury or detriment to those who do notpossess such information and therefore do not and cannotdeal in the securities of the company to which the informationrelates. Insider trading, as it involves misuse of confidentialinformation, is unethical amounting to breach of fiduciaryposition of trust and confidence. The misuse of insideunpublished information is bad for several reasons, such as-a) it involves taking a secret, unfair advantage;b) it gives rise to potential conflicts of interests in which the

company's best interest may wrongfully take second placeto insider's self-interest; and

c) it brings the market into disrepute and may be adisincentive to investment.

In Lord Lane's view, the rationale behind the prohibition on

Insider trading is an evil by which any stock market is infected to cause grave damage to the common investor. It erodes the confidence of the investor and undermines itscredibility. Duties of the insiders as well as the companysecretary are outlined here.

(A -47)

* Past President, The Institute of Company Secretaries of India.

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 10

February

2012CHARTERED SECRETARY155

Articles

insider trading is "the obvious and understandableconcern……about the damage to public confidence whichinsider dealing is likely to cause and the clear intention toprevent so far as possible what amounts to cheating whenthose with inside knowledge use that knowledge to make aprofit in their dealing with others."1

Insider trading is an evil by which any stock market isinfected to cause grave damage to the common investor. Iterodes the confidence of the investor and undermines itscredibility. It is often said that insider trading is not as rampantin any other stock market in the world as in the Indian market.To remedy the malady of insider trading, the Regulationsprovide for various measures. In particular, the Regulationsrender insider trading a criminal offence in certaincircumstances, punishable under the SEBI Act. TheRegulations also clothe the SEBI with the powers ofinvestigation to unearth and prove the crime of insider trading,though the task is very arduous. All listed companies in Indiaare affected by the Regulations but any person or a companyoutside India may also be affected by the Regulations when

such person is accused of insider trading.Owing to its non-public and precise nature and its ability toinfluence the prices of financial instruments significantly,inside information grants the insider in possession of suchinformation an advantage in relation to all the other actors onthe market who are unaware of it. It enables that insider, whenhe acts in accordance with that information in entering into atransaction on the market, to expect to derive an economicadvantage from it without exposing himself to the same risksas the other investors on the market. The essentialcharacteristic of insider dealing thus consists in an unfairadvantage being obtained from information to the detriment ofthird parties who are unaware of it and, consequently, theundermining of the integrity of financial markets and investorconfidence. [ See Spector Photo Group NV and another v.Commissie voor het Bank Financie - en Assurantiewezen[2010] Bus LR 1416.]

What is 'insider trading'?In simple terms, insider trading implies illegal buying andselling of shares based on privileged information, which isknown only to a few who belong to a limited circle of 'insiders'in a company. Insider is a person in possession of corporateinformation not generally available to the public, as a director,an accountant, or other officer or employee of a corporation.This is clearly dealing in company securities with a view tomaking a profit or avoiding a loss while in possession ofinformation that, if generally known, would affect their price.The information is, of course, 'price-sensitive' as it is likely tohave an impact on the market price of the share. A classicexposition of the concept of insider trading is to be found in aWhite Paper that was prepared in the UK in 1977 on theConduct of Company Directors. That type of conduct was notthen subject of any legal sanctions, although it was causingserious concern in the country. The White Paper stated:

1] Attorney General's Reference No. 1 of 1988 (1988) BCC 765: (1989) 3WLR 195: (1989) 2 CLA 101 (CA) affirmed by the House of Lords asreported at (1989) BCC 625. Attorney General's Reference (No 1 of1988), [1989] 2 A11 ER 1

(A -48)

Insider Trading: Duties of Insiders and Company Secretary

Insider trading causes injury ordetriment to those who do notpossess such information andtherefore do not and cannotdeal in the securities of thecompany to which theinformation relates. Insidertrading, as it involves misuse ofconfidential information, isunethical amounting to breachof fiduciary position of trust andconfidence.

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 11

CHARTERED SECRETARY 156February

2012

Articles

"Insider dealing is understood broadly to cover situationswhere a person buys or sells securities when he, but not theother party to the transaction, is in possession of confidentialinformation which affects the value to be placed on thosesecurities. Furthermore the confidential information inquestion will generally be in his possession because of someconnection which he has with the company whose securitiesare to be dealt in (e.g. he may be a director, employee orprofessional adviser of that company) or because someone insuch a position has provided him, directly or indirectly, with theinformation. Public confidence in directors and others closelyassociated with companies requires that such people shouldnot use inside information to further their own interests.Furthermore, if they were to do so, they would frequently be inbreach of their obligations to the companies, and could beheld to be taking an unfair advantage of the people with whomthey were dealing."

Insider trading is a systemic way of hoodwinking thecommon investors by the misuse of inside information by theprivileged few. It not only involves taking a secret, unfairadvantage of the inside information for persons gain, but alsogives rise to potential conflicts of interests in which thecompany's best interest may wrongfully take second place tothe insider's self interest. Moreover, it brings the market intodisrepute and may be a disincentive to investment.

Insider trading occurs where an individual or organizationbuys or sells securities while knowingly in possession of somepiece of confidential information which is not generallyavailable and which is likely, if made available to the generalpublic, to materially affect the price of these securities. Forexample, there is insider trading where a company directorknows that the company is in a bad financial condition andsells his shares in it knowing that in a few days time this newswill be made public together with an announcement of a cut individend payment. Likewise, the director would be chargedwith insider dealing if, on being informed before it was

generally known by the public, that the company hasdiscovered oil or gold on its own land, he bought more sharesin the company in the not unrealistic expectation of anincrease in their market value as a result of the subsequentpublic announcement.

An insider who knows that the company is in a financialmess may sell the company's shares knowing that shortlythere will be a public announcement of the news. Similarly, acompany director who is aware that the company has baggeda huge export order may buy more shares in anticipation of arise in the price of the shares.

Recently, the Court of Justice of the European Union heldin Spector Photo Group NV and another v. Commissie voor hetBank Financie-en Assurantiewezen [2010] Bus LR 1416, that"the purpose of the prohibition (of insider trading) is to ensureequality between the contracting parties in stock-markettransactions by preventing one of them who possesses insideinformation and who is, therefore, in an advantageous positionvis-à-vis other investors, from profiting from that information, tothe detriment of those who are unaware of it." Earlier, in theAdvocate General's Opinion in the case, it was said:

"... the prohibition on insider dealing imposed by thedirective is intended to ensure the integrity of ... financialmarkets and thus to enhance investor confidence in thosemarkets. ... A functioning integrated financial market requiresthe legitimate expectation of economic actors in full andproper market transparency. It is necessary to guaranteeequality of opportunity and to prevent individual market actorsbeing given preferential treatment through the use of insideknowledge to the detriment of the other market actors."

Regulation of insider trading in the USMost countries have now recognized insider trading to beobjectionable. The first country to tackle it effectively was theUSA. The Securities Exchange Act of 1934 imposes statutorycurbs on insider trading, requiring public disclosure of insiders'transactions in the shares and providing for recovery of'shortswing' profits made by them. The Act provides measuresfor protection of investors against sharp practices andfraudulent schemes by insiders in making short-term,

A classic exposition of theconcept of insider trading is tobe found in a White Paper thatwas prepared in the UK in1977 on the Conduct ofCompany Directors. That typeof conduct was not thensubject of any legal sanctions,although it was causing seriousconcern in the country.

(A -49)

Insider Trading: Duties of Insiders and Company Secretary

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 12

February

2012CHARTERED SECRETARY157

Articles

speculative profits. A corporation or issuer of a registeredsecurity can recover all profits realized by an insider, by unfairuse of information, which he may have obtained by reason ofhis relationship to the issuer, from any purchase and sale orvice versa of the security, within a period of 6 months. Thefederal court determines the quantum of compensation to theinjured shareholder.

One of the best-known cases of insider dealing in the UKconcerned an adviser to a company involved in a takeover.[SEC v. Collier]. Mr. Collier was head of securities at City ofLondon finance house Morgan Grenfell, which had beenretained by a client to advise on a takeover bid. When the bidwas about to be launched, Mr. Collier arranged the acquisitionin London, on his own behalf, of shares of the target company.He did so through a company registered in the CaymanIslands prior to the announcement of the bid. He wassubsequently convicted on pleading guilty to insider dealing,his prison sentence of twelve months being suspended for twoyears. He was fined £ 25,000, ordered to pay £7,000 in costsand was subsequently also expelled from membership of theStock Exchange in London. Apparently, he only stood to profitin the amount of £l5, 000 a result of what he did.

Another example, which achieved greater notoriety,involved Ivan Boesky who worked as a risk arbitrageur in theUSA. Risk arbitrageurs became prevalent in the last decade.They would acquire holdings of shares in companies in thehope that the market value of those shares would riseenabling them to turn a tidy profit on the disposal of theshares. A common scenario might again have involved theacquisition of shares in a company in anticipation of atakeover. If the takeover went ahead, the arbitrageur couldeither dispose of his shares or, alternatively, retain them in thehope of exercising influence over the company following thetakeover. Ivan Boesky was very active in this area. Incorporate terms, he was often in the right place at the righttime and many thought this was due to his superior marketanalysis. However, subsequently, in many cases it turned outto be due to the receipt of inside information from a number ofinformants. Boesky was convicted and sentenced toimprisonment for three years. He also paid over $100 millionin settlement to the Securities and Exchange Commission inthe USA. Approximately half that amount represented a finewhile the other half represented the return of ill-gotten gains.Mr. Boesky is alleged to have made a minimum profit frominsider dealing of $ 50 million over a period of five years or so.It was reported at the time that Mr. Boesky's estimated profitwas in the region of $200 million.

In Texas Gulf Sulphur Co. case, a test hole drilled by TexasGulf Sulphur Company in Ontario indicated a high copper andzinc concentration. Several of company's employees whoknew this discovery and their friends began to buy largequantities of the company's stock and, thereupon thecompany's management issued a press note stating that therumors of the discovery were exaggerated and stated thatthey were possibly misleading. Subsequently the news about

the success of the hole drilling became widespread and theprice of the stock soared to more than double their price whichprevailed before the success of the extremely profitable holedrilling operations came to the knowledge of the general bodyof shareholders and the investing public. The Court of Appealheld that the directors and insiders were liable to refund to thecompany the profits made by them and they were also liablein damages to the parties who had suffered loss. The pressnote issued by the management to the effect that the rumorswere exaggerated and misleading was also held to be false onthe facts admitted or proved.

Regulation in EU The relevant provision in the European Union Directive oninsider trading provides: "Any person who possesses insideinformation is prohibited from using that information byacquiring or disposing of, or trying to acquire or dispose of, forhis own account or for the account of a third party, eitherdirectly or indirectly, the financial instruments to which thatinformation relates or connected financial instruments."

SEBI's anti-insider tradingregulationsIt is undeniably indisputable that only a prohibition on insiderdealing which is effectively enforceable in practice can

(A -50)

Insider Trading: Duties of Insiders and Company Secretary

Insider trading is a systemic way ofhoodwinking the common investors by the

misuse of inside information by the privilegedfew. It not only involves taking a secret, unfair

advantage of the inside information forpersons gain, but also gives rise to potentialconflicts of interests in which the company's

best interest may wrongfully take secondplace to the insider's self interest.

guarantee the functioning of the financial markets in the bestway possible. Only if the prohibition on insider dealing allowsinfringements to be effectively sanctioned does it prove to bepowerful and encourage compliance with the rules by allmarket actors on a lasting basis.

In India, by the Securities and Exchange Board of India(Insider Trading) Regulations, 1992 ("the Regulations"), theSEBI has attempted to give a concrete shape, by a legislativemeasure, to one of the specific functions which section 11 ofthe Securities and Exchange Board of India Act, 1992 ("theSEBI Act") requires SEBI to discharge.

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 13

CHARTERED SECRETARY 158February

2012

Articles

a crime to tip UPSI as much the same as dealing in securities.Communication denotes the act of imparting or transmitting.To communicate means to transmit, pass on, transfer, impart,convey, relay spread, disseminate, make known, publish,broadcast, announce, report, divulge, disclose, let othersknow etc. To 'counsel' means to advise somebody to dosomething; to give professional advice to somebody;recommend; give one's opinion or suggestion. To 'procure'means to obtain; to persuade or cause somebody to dosomething; to cause something to happen. An insider whocounsels or procures some other person and that persondeals in securities, such person will be guilty of contraventionof this prohibition if the latter deals in securities.

Communication/counselling/procurement by an insider ofany unpublished price-sensitive information to any person,whether he (the insider) has been requested to furnish suchinformation or not, will amount to contravention of theRegulations. Communication/counselling/procurement may bewritten or verbal. It should be noted thatcommunication/counselling/procurement of the information byan insider to any other person even without the latter asking forit would be sufficient to bring the insider within this prohibition.In such a case the person to whom the information has beencommunicated/counselled/procured may also become insiderand if he deals in the securities of the company to which suchinformation relates, while in possession of such information, theprohibition under clause (ii) shall apply.

While the person who communicates/counsels/procuresinformation must be an insider, the person to whominformation is communicated/counselled/procured need notbe an insider; consequently he need not be a 'connectedperson' or a 'person who is deemed to be connected' with thecompany within the scope of the definitions of thoseexpressions. The recipient of information who deals insecurities while in possession of the information acquired byhim will be liable for action, regardless of whether he is aninsider or not.

At first sight, one might think that the prohibition undersub-clause (ii) applies even to a pure and simple case of, inter alia, communication of unpublished price sensitiveinformation by an insider to another person (including acompany or other body corporate), without anything more. Itis, however, doubtful whether mere communication ofunpublished price sensitive information, without anythingmore, would give rise to the case of insider trading, for theessence of insider trading is make use of inside informationfor dealing in securities, either by the person who obtains anyunpublished price sensitive information.

Sub-clause (ii) ends with the words "who while inpossession of such unpublished price sensitive informationshall not deal in securities." These words are very crucial anddecisive as to whether communication of unpublished pricesensitive information by an insider attracts the prohibitionunder Regulation 3(ii) and creates a liability for contraventionthereof. The prohibition under Regulation 3(ii), in so far

( A -51)

Insider Trading: Duties of Insiders and Company Secretary

Where a person is an insider as per the criteria discussedbelow, he will be affected by the prohibitions contained inRegulation 3, which is the key provision for prohibition oninsider trading and creating it an offence punishable, onconviction, under section 24 of the SEBI Act.

What is prohibited?Dealing: The objective of the Regulations is banning insidertrading. Regulation 3 contains the main provision in thisregard. It prohibits an insider from dealing in listed securitieswhen he possesses any unpublished price sensitiveinformation (UPSI). It provides that no insider shall either onhis own behalf or on behalf of any other person, deal insecurities of a company listed on any stock exchange when inpossession of any unpublished price sensitive information.

The expression 'when in possession of any unpublishedprice sensitive information' when read with the expression 'noinsider shall deal in securities' indicates that merely havingknowledge of UPSI while dealing in securities is enough tocharge a person with the wrong of insider trading; actuallyusing the UPSI for or in relation to dealing in securities is notnecessary to be proved.

The expression 'dealing in securities' is defined as an act ofsubscribing, buying, selling or agreeing to subscribe, buy, sell ordeal in any securities by any person either as principal or agent.

Tipping: The prohibition under Regulation 3 doesn't end there;it has one more limb in its clause (ii). It also banscommunication, counselling and procuring, directly orindirectly, any UPSI to any person and also restrains suchperson, while in possession of UPSI from dealing insecurities. Communication of UPSI in the ordinary course ofbusiness or under any law is, however, not forbidden.

Insider trading occurs not only when a person in possession ofUPSI deals in the company's securities; it also occurs when sucha person tips or communicates UPSI to another person. Thus, it is

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 14

February

2012CHARTERED SECRETARY159

Articles

communication of information is concerned, cannot apply tothe case of mere communication of unpublished pricesensitive information. For that, the condition stipulated in theconcluding portion of the said Regulation, which is a sine quanon, has to be satisfied. In other words, even if an insider of alisted company communicates certain unpublished pricesensitive information to another person and that other personmerely keeps such information in his custody and doesnothing more, that alone would not bring the case within theambit of the prohibition under Regulation 3(ii). It needssomething more, and it is the dealing in securities of theconcerned listed company while that person is in possessionof unpublished price sensitive information. The expression"deal in securities" is defined in clause (d) of Regulation 2,which has already been considered earlier.

Who is 'insider'?: Under Regulation 2(e), any person who,is or was connected with the company or is deemed to havebeen connected with the company, and who is reasonablyexpected to have access to UPSI in respect of securities of acompany, or who has received or has had access to suchunpublished price sensitive information, is 'insider'. It will benoticed from this definition that an 'insider' must be aconnected person. The expression 'connected person' isdefined as follows:

Regulation 2(h) defines the expression 'connected person'and it embraces in its ambit directors, officers or employes ofthe company and every person who holds a position involvinga professional or business relationship between himself andthe company whether temporary or permanent and who mayreasonably be expected to have an access to unpublishedprice sensitive information in relation to that company.

According to the Explanation appended to the abovedefinition, any person who has been a connected person(according to the above definition) for a period of six monthsprior to an act of insider trading is also to be treated asconnected person.

Certain persons are deemed to be connected persons andthere is a list of such persons in Regulation 2(h).

Offence of insider trading andmens reaThe expression mens rea (criminal intent) is variouslydescribed, such as guilty mind, blameworthy mind, criminalintention, evil intent, guilty or wrongful purpose etc. Mens rea isone of the essentials of a crime. It means 'criminal intent', thatis the essential mental element that in theory has to be provedfor all crimes, although in practice some statutory offences arecrimes of absolute liability, regardless of criminal intent. Everycrime requires a mental element. Even in strict or absoluteliability some mental element is required. Mens rea or actusnon facit reum nisi mens sit rea (the intent and act must bothconcur to constitute the crime; the act itself does not make aman guilty unless his intention were so or his mind is alsoguilty) is considered a fundamental principle of penal liability.

Under the SEBI Regulations it is not necessary to prove thatthe insider was knowingly connected with the company or heknowingly indulged in insider trading. It would therefore primafacie seem that mens rea is not an essential ingredient of theoffence of insider trading. Consequently, a person may beconvicted of the offence regardless of whether he hascommitted it knowingly, deliberately or intentionally. He wouldbe liable to be convicted and punished once it is establishedthat he is an insider within the scope of the SEBI Regulationsand, further, that he has committed any one of the three actsprohibited by regulation 3. Thus, it will not be necessary toestablish mens rea, although it will be necessary to establishthat the insider did any of the prohibited acts on the basis ofunpublished price-sensitive information. There are no wordssuggesting the requirement of mens rea.

InvestigationChapter III of the SEBI Regulations, contains provisionsregarding SEBI's powers of investigation into insider tradingand matters incidental thereto. In UK the provisionsconcerning such investigation are contained in sections 177and 178 of the Financial Services Act, 1986. The SEBI Actcontains no provisions on this subject, nor does it confer onSEBI or any other authority, even general powers ofinvestigation or the power to appoint inspectors orinvestigators. The powers conferred on SEBI, and on theinvestigators appointed by it, are nothing different from thepowers of search, (although regulation 7(2) euphemisticallyuses the expression "reasonable access to premises")interrogation, examination on oath, etc. but they do not havethe necessary statutory backing as is found in all thosestatutes which confer such powers on the authoritiesconstituted thereunder.

The SEBI Regulations in regard to investigation aredistinct from the UK law in one respect. Under section 177(1)of the Financial Services Act of UK the Secretary of the Stateis empowered to appoint one or more competent inspectors tocarry out such investigations as are requisite to establishwhether or not any contravention of the provisions of theCompany Securities (Insider Dealing) Act has occurred, and

Under the SEBI Regulations it is not necessary to prove that the

insider was knowingly connected withthe company or he knowingly

indulged in insider trading. It wouldtherefore prima facie seem that mens

rea is not an essential ingredient ofthe offence of insider trading.

( A -52 )

Insider Trading: Duties of Insiders and Company Secretary

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 15

CHARTERED SECRETARY 160February

2012

Articles

to report the results of their investigations to him, and theinspectors so appointed are entitled to require "any person",whom they consider to be able to give information concerningany such contravention, to produce documents, to attendbefore them and otherwise give all assistance in connectionwith the investigation.

As opposed to this, under the SEBI Regulations, theinvestigation cannot go beyond an insider and, in certainrespects, his associates as specified in regulation 7. Theinvestigator cannot require 'any person' to do any of the thingsmentioned in regulation 7.In terms of regulation 5, the power of investigation may beinvoked by SEBI for the following two purposes:a) to investigate into the complaints received from investors,

intermediaries or any other person on any matter having abearing on the allegations of insider trading; and

b) to investigate suo-motu upon its own knowledge orinformation in its possession to protect the interest ofinvestors in securities against breach of these regulations.

The SEBI may appoint an investigating authority where it hasordered investigation under this Regulation. Before orderingan investigation the SEBI must form an opinion that it isnecessary to investigate and inspect books of account, otherrecords and documents of an insider for any of the aforesaidpurposes.Such formation of the opinion must be based on"written information in its possession". Thus, to be inpossession of written information leading to the formation ofthe opinion is the sine qua non for ordering an investigation.An investigation may be ordered to be conducted by aninvestigator, either suo motu i.e., upon its (SEBI's) ownknowledge or information or upon receiving a complaint offacts which constitute contravention of the Regulations, if

SEBI is of opinion that there are circumstances suggestingthat there has been a contravention of the Regulations.Regulation 5 is unclear and ambiguous.The SEBI's Regulations on insider trading appear to havebeen made in a hurry and haste. They are overduecomprehensive review and revision for they are inadequate toeffectively deal with the menace of insider dealing. There isindeed a need to have a separate statute on this subject. Ifnot, at least the SEBI Act should be amended to insert aChapter dealing with the subject, backed by more teeth toSEBI. But what really is required is to deal harshly with thosewho are responsible to spread the evil of insider trading.Corporate governance codes alone cannot eradicate thisplague, not surely in the Indian capital market.

Company Secretary's DutiesCompany secretaries of listed companies are in almost allcases compliance officers under the Insider Trading Coderecommended by SEBI under the Regulations. There areseveral compliances of administrative nature that a companysecretary has to ensure compliance with in order to get theCode implemented in the company. The company secretaryis, however, responsible not only for implantation of the Code,but also for creating awareness among the people in andoutside the company who have or likely to have access toUPSI to make it known to them the SEBI Regulations and theCode and dissuade them from indulging in insider trading ortipping insider information to other people.The definition of 'insider' under the Insider Trading Code isvery wide which is not contemplated by the SEBI's modelCode. It need not include persons who are notdirectors/officers/designated employees of the Company. Thedefinition of 'insider' as given in the SEBI Regulations neednot be adopted and incorporated in the Code because thatdefinition is very wide and covers many people who are not(and not expected to be) covered by the Code. For example, ifunder the company's Code all insiders are required to reportcertain details relating to the company's securities to thecompany, this will be almost impossible to be implementedand, moreover, the Code doesn't apply to outsiders. The Codeis for the company's directors, officers and few selectedemployees (called 'designated employees') who are expectedto be governed by the Code.

However, making people connected with the company(directly or indirectly) about the SEBI Regulations andconsequences of breach is an important duty of companysecretary as a compliance officer.

Only a prohibition on insider dealing which is effectively enforceable inpractice can guarantee the functioning of the financial markets in the best waypossible. Only if the prohibition on insider dealing allows infringements to beeffectively sanctioned does it prove to be powerful and encourage compliancewith the rules by all market actors on a lasting basis.

( A -53 )

Insider Trading: Duties of Insiders and Company Secretary

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 16

February

2012CHARTERED SECRETARY161

Articles

INTRODUCTION

India is a unique country where the Governmentstipulates and defines the format for the financialreporting for corporates though in an internationalarena, generally, no defined format for financialreporting is suggested by the Regulators. Schedule VIof the Companies Act, 1956 which defines the financialreporting framework for Indian companies has beenamended last year by the Government vide Notificationdated 28 February 2011 which is applicable for thefinancial statements prepared for all financial periodsbeginning on or after 1 April 2011.

The Revised Schedule VI has been framed as per the existingnon-converged Indian Accounting Standards notified underthe Companies (Accounting Standards), Rules, 2006 and hasno direct connection with the converged Indian AccountingStandards. This comprehensive revision in the Schedule VIhas come after a long time and was infact overdue.

GLOBAL ACCOUNTINGENVIRONMENTThe Global Accounting Environment in the recent past hastaken a new dimension with emphasis on the "Theory ofTransparency" necessitating more and more disclosures inthe financial statements of Corporates. Needless to add thatthe extent of disclosures in the financial statements needs totake into account the business sensitivities and there shouldbe a fine balance between the disclosure requirements tofacilitate greater transparency vis-à-vis businessconfidentiality and the need for maintaining the cutting edge ina cut throat competitive environment. The changes made bythe Government in the Schedule VI have attempted tomaintain this balance. Hence, though on the one side, new

Sriraman Parthasarathy, ACS

Partner, Delloitte Haskins and SellsChennai.

Refreshing Revisions inSchedule VI The Revised Schedule VI has introduced several new conceptsand disclosure requirements for financial reporting and it hasalso done away with several redundant statutory disclosurerequirements. This article is intended to discuss some of thekey changes proposed in the Revised Schedule VI, itsimplications and the related background.

( A -54 )

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 17

CHARTERED SECRETARY 162February

2012

Articles

disclosure requirements have been mandated, on the otherend, certain information which was required to be mandatorilydisclosed in the financial statements in the past has beendone away with. In addition, several procedural relaxationshave also been made in the recent past relating to certaindisclosure items which simplifies the process of takingdecisions as regards disclosures based on the "principle ofself-evaluation".

FUNDAMENTAL CHANGES MADEIN REVISED SCHEDULE VIThe key and fundamental changes that dictate the format /disclosure requirement of financial reporting under theRevised Schedule VI are given below:

Acceptance of the Supremacy of AccountingStandards and Companies ActThe most important change in the Revised Schedule VI isdefining the authority level for the disclosures. It hascategorically spelt out that the disclosure requirements of theAccounting Standards and the provisions of the CompaniesAct would prevail and, hence, the additional disclosures /modifications to the Revised Schedule VI as may be requiredon account of the same would be applicable and the ScheduleVI would stand modified to that extent automatically.Further, itclearly states that for the purposes of the Revised ScheduleVI, the terms used therein will carry the meaning as defined

by the applicable Accounting Standards. This is a significantchange in the mind set /approach wherein the supremacy ofthe Accounting Standards and the provisions of theCompanies Act has been clearly accepted/established.

Aligning the Financial Statements Presentationas per Global ExpectationsAs per the earlier Schedule VI, the break-up of amountsdisclosed in the main Balance Sheet and Profit and LossAccount was given in the form of Schedules and onlyadditional information, wherever required, was furnished inthe Notes to Accounts. The Revised Schedule VI haseliminated the concept of Schedules and such information willnow be provided in the Notes to Accounts. This is in line withthe practice followed under global financial reporting. It alsostipulates that all the information relating to a particular item ofBalance Sheet and Profit and Loss Account disclosed in thenotes is required to be cross-referred to that item on the faceof the Balance Sheet/ Profit and Loss Account.

Setting the Tone for Disclosure Expectations

The expectations of the disclosure requirements of thefinancial statements are clearly spelt out in the RevisedSchedule VI. It categorically states that the stipulateddisclosures on the face of the financial statements or in thenotes represent the minimum requirements/expectations onlyand the entities have to consider the requirements of Industry,Sector, Accounting Standards, Companies Act etc.foradditional/modified disclosure on the face of the financialstatements.

Clarity in Formats/Presentation

The erstwhile Schedule VI did not provide any format for thepresentation of the Profit and Loss Account, though itprovided a format for the Balance Sheet. Part II of Schedule

The most important change in theRevised Schedule VI is defining theauthority level for the disclosures. Ithas categorically spelt out that thedisclosure requirements of theAccounting Standards and theprovisions of the Companies Actwould prevail and, hence, theadditional disclosures / modificationsto the Revised Schedule VI as maybe required on account of the samewould be applicable and theSchedule VI would stand modified tothat extent automatically.

( A -55 )

Refreshing Revisions in Schedule VI

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 18

February

2012CHARTERED SECRETARY163

Articles

contained only requirements relating to the Profit and LossAccount.This dichotomy in the approach has been removed inthe Revised Schedule VI wherein a stipulated format has beenpresented for the Profit and Loss Account as well to makesure that the intention of setting the basic disclosureexpectation is fulfilled in totality.Similarly, as per the erstwhile Schedule VI, both horizontal andvertical forms were allowed for presenting the Balance Sheetdefeating in a way the ultimate objective of ensuringstandardized presentation of the financial statements. This hasbeen addressed in the Revised Schedule VI, wherein, only avertical form of the Balance Sheet has been specified.Further, there is an explicit requirement in the RevisedSchedule VI to use the same unit of measurement with respectto the figures uniformly throughout the financial statements.

Current v. Non-Current Classification

As per Revised Schedule VI, Assets and Liabilities are to bebifurcated into Current and Non-Current and are to be shownseparately. Hence, Net Working Capital will not be appearingin the Balance Sheet. This is a significant change as regardsthe presentation of the items in the Balance Sheet keeping inmind the principle of liquidity which is also in line with theglobal financial reporting framework.

Drastic Disclosure Shifts in Presentation ofCertain Items

There are certain drastic disclosure shifts in the financialstatements which are indicated in the Revised Schedule VI.Some of the key ones are highlighted below:

Presentation of Proposed DividendAs against the previous requirement of making anadjustment to the financial statements for the proposeddividend, the new Schedule VI stipulates that theproposed dividend needs to be disclosed in the Notes toAccounts as a commitment.

Presentation of Debit Balance in Profit and Loss AccountIn Schedule VI earlier the accumulated debit balance inthe Profit and Loss Account was required to be disclosedseparately in the Balance Sheet. However, as perRevised Schedule VI, debit balance in the Profit and LossAccount needs to be shown as a negative figure underthe head Surplus. Therefore, Reserves and Surplus canhave a negative balance.

Presentation of Profit and LossAppropriation AccountOpening surplus, proposed dividend and transfer to/fromreserves were shown in the Profit and Loss AppropriationAccount under the earlier Schedule VI. However, theRevised Schedule VI stipulates that transfer from/ toreserves have to be shown under the heading Reserves andSurplus only. Hence, there is no requirement for presentinga separate Profit and Loss Appropriation Account.

NEW /ADDITONAL DISCLOSURESIN THE FINANCIAL STATEMENTSThe Revised Schedule VI has introduced a number of additionaldisclosures. Some of the key disclosures are as under:

Shareholders' Fundsu Separate disclosure of Money Received Against Share

Warrantsu Number of shares held by each shareholder in excess of

5 % together with their namesu Number of bonus shares/ shares allotted without payment

being received in cash/ shares bought back during the 5years immediately preceding the date of the BalanceSheet

u Rights, preferences and restrictions attaching to eachclass of shares including restrictions on the distribution ofdividends and the repayment of capital

Reserves and Surplusu Share Option Outstanding Account to be shown under

Reserves and Surplus

( A -56 )

Refreshing Revisions in Schedule VI

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 19

CHARTERED SECRETARY 164February

2012

Articles

Borrowings - Long Term & Short Termu Long term borrowings to be shown under non-current

liabilities and short term borrowings to be shown undercurrent liabilities with separate disclosure of secured /unsecured loans

u Current maturities of long-term debt, interest accrued anddue on borrowings and interest accrued but not due onborrowings to be shown under Current Liabilities

u Terms of repayment of loansu Period and amount of continuing default as on the Balance

Sheet date in repayment of loans and interest, shall bespecified separately in each case

u Loans and advances taken from related parties

Fixed Assetsu Fixed assets to be shown under non-current assets and to

be bifurcated in to Tangible and Intangible assets.u Intangible assets under development

Investmentsu Current and non-current investments are to be disclosed

separately under current assets and non-current assets,respectively

u Under each class of investment, details regarding namesof the bodies corporate, indicating separately whethersuch bodies are (i) subsidiaries, (ii) associates, (iii) jointventures, or (iv) controlled special purpose entities, inwhom investments have been made and the nature andextent of the investment made in each such bodycorporate (showing separately partly-paid investments)

u Regarding investments in the capital of partnership firms,the names of the firms with the names of all their partners,total capital and the shares of each partner

u Aggregate provision for diminution in value of investments(separately for current and non-current investments)

Current / Non - Current Assetsu Stock-in-trade (in respect of goods acquired for trading

purposes) separately from other finished goodsu Goods in transit under relevant sub-head of inventoriesu Trade receivables.The term "Trade receivables" is defined

as dues arising only from goods sold or services renderedin the normal course of business. Hence, amounts due onaccount of other contractual obligations, which were earlierincluded under sundry debtors, can no longer be includedin the trade receivables

u Aggregate amount of trade receivables outstanding formore than six months from the date they became due tobe shown separately as against the past requirement ofdisclosing debtors outstanding for more than six monthsfrom the invoice date

u Long term trade receivables (including trade receivableson deferred credit terms) to be shown under Other Non-Current Assets

u Cash and cash equivalentsu Loans and advances provided to related parties - Long

term and short termu Capital advances to be shown under the head 'long term

loans and advances'u Security deposits to be disclosed as long term loans and

advances under the head non-current assets

Current /Non - Current Liabilitiesu Trade payablesu Short term provisions and long term provisions providing

details of provision for employee benefits and othersu Income received in advance

Statement of Profit and Lossu In respect of companies other than finance companies,

revenue from operations need to be disclosed separatelyas revenue from (a) sale of products, (b) sale of servicesand (c) other operating revenues

u Any item of income / expense which exceeds one per centof the revenue from operations or Rs. 1,00,000, whicheveris higher, to be disclosed separately

u Expenses in the Statement of Profit and Loss to beclassified on the basis of Nature of Expenses

u Expense on Employee Stock Option Scheme (ESOP) andEmployee Stock Purchase Plan (ESPP) to be shownseparately as part of Employee Benefits expense

u Net exchange gain/loss on foreign currency borrowings tothe extent considered as an adjustment to interest costneeds to be disclosed separately as a finance cost

u Finance cost shall be classified as interest expense, otherborrowing costs and gain / loss on foreign currencytransaction and translation

( A -57 )

Refreshing Revisions in Schedule VI

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 20

February

2012CHARTERED SECRETARY165

Articles

u Exceptional and extraordinary items need to be disclosedseparately on the face of the Statement of Profit and Loss.The details of the same as also of any prior period itemsshould be disclosed in the Notes to Accounts

u Profit / loss before and after tax from discontinuingoperations and the tax expense from discontinuingoperations need to be disclosed separately on the face ofthe Statement of Profit and Loss

Miscellaneousu In the erstwhile Schedule VI, details of capital

commitments were required to be disclosedUnder the Revised Schedule VI, all commitments needtobe disclosed

u Disclosure requirements relating to break-up in terms ofquantitative disclosures for significant items of Profit andLoss Account such as raw material consumption, stocks,purchases and sales have been simplified and replacedwith the disclosure of Purchases, Sales, Consumption ofRaw Materials, Gross Income from Services and Work inProgress under "broad heads" only.The determination andidentification of such broad heads needs to be done basedon materiality and presentation of true and fair view of thefinancial statements

DROPPED DISCLOSURES 1. Part IV Balance Sheet Abstract and

Company's General Business Profile Part IV of the erstwhile Schedule VI comprising detailsof company registration number, capital raised,Balance Sheet details, products etc. which wasrequired to be attached to the financial statements isno longer required under the Revised Schedule VI.Consequent to E-Filing of financial statements and theavailability of all the required information in theBalance Sheet and the Profit and Loss Account, PartIV is a redundant requirement, which has beenrightfully removed in the Revised Schedule VI.

2 Managerial RemunerationDisclosure requirements related to ManagerialRemuneration/Commission along with the detailedcalculation under section 198 of the Companies Acthas been removed from Schedule VI.This is also in linewith the procedural liberalization initiatives alreadytaken by the Government.

3. Tax Deducted on Interest,Royalty Received etc.There is no need for disclosure relating to the amountof tax deducted on the amount of Interest, Royalty etc,as per the Revised Schedule VI.

4. Information relating to Licensed Capacity,Installed Capacity and Actual ProductionDetails relating to the licensed capacity of the entity, itsinstalled capacity and the details of actual production inthe case of manufacturing companies were required tobe disclosed separately in the notes to the financialstatements as per the Erstwhile Schedule VI which hasbeen removed under the Revised Schedule VI.

5. Miscellaneous ItemFurther, disclosure required as per the ErstwhileSchedule VI for the following items has been removedunder the Revised Schedule VI:

u Details relating to Names / Balances/ MaximumAmount etc. in Non Scheduled Banks

u Information on Investments purchased and sold duringthe year

u Investments, Sundry Debtors and Loans & Advancespertaining to Companies under the Same Management.

u Commission, brokerage and non-trade discounts

CONCLUSIONThe extent of changes made in the Revised Schedule VI ispath breaking and is in the right direction. Better/ Greater /Qualitative disclosures in the financial statements are the needof the hour and the Regulator has taken the right step in thisdirection. In the global environment where the disclosure is adominant factor in the financial statements, greater andtransparent disclosures in the financial statements are not onlygoing to enhance the investors' confidence but also heightenthe level of comfort amongst the international community.Though the changes in the disclosure requirements are notintended to address the IFRS considerations in totality, theRegulator has taken a right and bold decision in this front. Theexperience gained in implementation of the Revised ScheduleVI would certainly help in fine tuning the disclosurerequirements in future and enhancing the quality of thefinancial reporting framework.

( A -58 )

Refreshing Revisions in Schedule VI

ICSI-Feb-2012-4.qxd 1/31/2012 10:43 PM Page 21

CHARTERED SECRETARY 166February

2012

Articles

( A -59 )

P. Kesavulu Reddy, FCS

President & Company SecretaryJOCIL Limited, Dokiparru, Guntur Distt.

Andhra Pradesh.

Issue of Bonus Shares by a Public Limited Listed Company

A Practical Approach Issue of bonus shares by a company involves a series ofprocedural compliances. Considerable and meticulousplanning is also required. A checklist of relevant compliancesis set out in this article.