Embed Size (px)

Citation preview

6 This chapter focuses on the importance of approaching economic edu-cation pedagogy as a whole-family learning process, especially in highimmigrant and culturally diverse neighborhoods.

Economic Inclusion and Financial Educationin Culturally Diverse Communities:Leveraging Cultural Capital andWhole-Family Learning∗

Barbara J. Robles

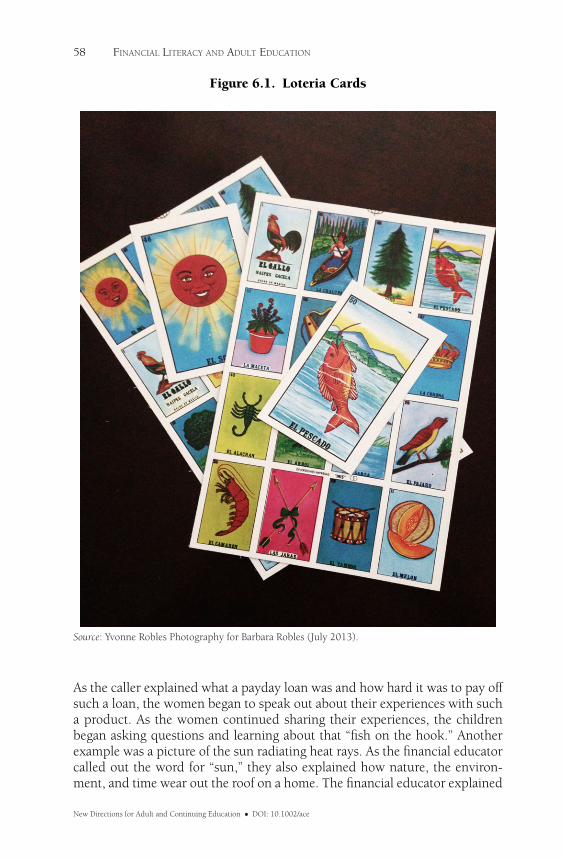

Financial education can happen in many contexts and can be especially effec-tive when the entire family is engaged. It can even happen at cultural festivalsand celebrations. For example, at a day-long festival celebrating the birthdayof Cesar Chavez, La Union del Pueblo Entero (LUPE) coordinated a series offamily-education booths displaying financial services and products for localresidents of a small southwestern border community. (La Union del Pueblo En-tero or “LUPE” is the social service organization for the Texas Farm WorkersUnion.) One of the family-oriented, financial education sessions was based onthe well-loved family game of Loteria. Loteria is a Spanish language form of theEnglish language Bingo board game played by many Mexican origin families; itis also the Spanish word for lottery/lotto. Instead of numbers being called out,pictures from a deck of cards are used to introduce children to various words(see Figure 6.1).

As in Bingo, the first person to line up a straight line or diagonal or fourcorners of the picture board game wins a prize. The person drawing cards andcalling out the word for the picture images was a financial educator. Each pic-ture represented a particular aspect of financial services or products that couldbe explained in a familiar manner. For example, a picture of a fish on a hookwas called out to the various family players. The players, mostly grannies, aun-ties, and mothers with children of various ages helping identify the pictureon the players’ boards, marked off the corresponding image on their boardgames. The fish on the hook represented getting “hooked” on payday loans.

∗This chapter does not necessarily reflect the views or opinions of the Board of Governorsof the Federal Reserve System.NEW DIRECTIONS FOR ADULT AND CONTINUING EDUCATION, no. 141, Spring 2014 © 2014 Wiley Periodicals, Inc.∗∗This article is a US Government work and, as such, is in the public domain in the United States of America.Published online in Wiley Online Library (wileyonlinelibrary.com) • DOI: 10.1002/ace.20085 57

58 FINANCIAL LITERACY AND ADULT EDUCATION

Figure 6.1. Loteria Cards

Source: Yvonne Robles Photography for Barbara Robles (July 2013).

As the caller explained what a payday loan was and how hard it was to pay offsuch a loan, the women began to speak out about their experiences with sucha product. As the women continued sharing their experiences, the childrenbegan asking questions and learning about that “fish on the hook.” Anotherexample was a picture of the sun radiating heat rays. As the financial educatorcalled out the word for “sun,” they also explained how nature, the environ-ment, and time wear out the roof on a home. The financial educator explained

New Directions for Adult and Continuing Education • DOI: 10.1002/ace

ECONOMIC INCLUSION AND FINANCIAL EDUCATION IN CULTURALLY DIVERSE COMMUNITIES 59

that having home insurance helps to pay for roof replacement and that homeinsurance saves families more money in the long run.

Using a whole-family learning activity by using a board game that is bothculturally familiar and engages all family members is an effective way to intro-duce difficult financial and economic concepts. Leveraging familiar game playalong with a festival, family-oriented atmosphere where children and youth arealso included in a whole-family activity creates a safe and memorable learningenvironment for financial and economic education in hard to reach commu-nities. It also acts as a form of culturally responsive financial education.

The Great Recession of 2007–2009 revealed that the average Americanconsumer was woefully unprepared for navigating increasingly complex eco-nomic and financial services and products. For culturally diverse, low-wealthcommunities, the recession erased family assets acquired with hard work thattook years, if not generations, to accumulate (Shapiro, Meschede, & Osoro,2013). Research on consumer behavior and cultural diversity indicates that in-dividuals and families experience daily economic activities and decision mak-ing in terms of multiple identities such as mother, daughter, sister, wife, aswell as situational socioeconomic class and racial/ethnic affiliations (Penaloza,1995; Stayman & Deshpande, 1989; Viramontez & Trask, 2009). In acknowl-edging this lived reality and multiple relationships over the life course, Tis-dell, Taylor, and Sprow Forte (2013) suggest that adult educators can leveragelearners’ cultural capital and family affiliations in curriculum and pedagogicalframing. This chapter goes one step further by considering not just the adultlearner as the student participant but also the entire family unit. When adulteducators leverage all foundational elements of the learners’ environment suchas cultural capital, socioeconomic class, and community environment (for low-income neighborhoods, this often means a cash economy), a whole-familylearning approach becomes comfortable, familiar, and most importantly, un-derstandable for low-wealth, culturally diverse families and communities.

The remainder of this chapter first presents insights into economic re-siliency and financial aspirational information collected from a study over afive-year period in the southwestern region of the United States (California,Arizona, New Mexico, and Texas). Next, some of the information and primaryfindings of the study are presented that highlight the importance of capturingcultural information and knowledge gaps. Third, the importance of attendingto the family in a cultural context as a way of increasing economic resiliencyis addressed.

Economic Inclusion: Economic Education and Cultural Capital

Economic education is promoted as a means to strengthen family financial ca-pabilities. Financial capabilities are defined as resilient behaviors that reflectmaking ends meet, planning for both the present and the future, and assetbuilding connected to economic mobility aspirations (short-run and long-run goal setting) and entrepreneurial activities. The information-gathering

New Directions for Adult and Continuing Education • DOI: 10.1002/ace

60 FINANCIAL LITERACY AND ADULT EDUCATION

methods (survey and open-ended responses) used for the study that is the basisfor the insights discussed here were designed to track financial capabilities andeconomic activities that reflect the daily lives and resiliencies of low-wealth,working families in culturally diverse communities and ethnic enclaves.

Most mainstream research on economic and financial education curriculaand campaigns generally focuses on understanding the decision making andliteracy of the individual, divorced from any family-oriented, joint financialdecision making or shared economic knowledge. Since the Great Recession,formation of intergenerational households appears to be escalating as a resultof the current fragile recovery (Kochhar & Cohn, 2011; Lofquist, 2012; Tayloret al., 2010). As more adult children move back into their parents’ households,two to three generations living under one roof to safeguard assets and minimizefinancial losses has become commonplace.

What is a “whole-family-learning-over-the-life-course” approach? As il-lustrated in the Loterıa vignette, it is allowing the family unit to interact withother family units in a space that is inclusive of children learning with parentsabout economic and financial concepts, markets, products, and services. In-deed, by having the entire family engaged in conversation with other families,no fear of the product or confusion or shame toward the economic or finan-cial concept is attached. In low-income, low-wealth, ethnic enclaves, learningto do more with less is part of the “making ends meet” capacity of the entirefamily unit. Given the orientation toward family, a learning environment in-troducing not only financial management but also economic markets is part ofconnecting the dots for high immigrant, transnational, and immigrant legacycommunities and ethnic/racial enclaves. By including children, and deliber-ately engaging the age 10–16 cohort, economic education and financial literacybecomes part of what the youth paraphrasers and translators can access wheninterpreting for immediate and extended family members (Orellana, Dorner,& Pulido, 2003; Valdes, 2003).

Using a whole-family orientation when undertaking economic and finan-cial decision making has been a significant component of cultural capital indiverse, low-wealth, and high immigrant memory communities. For example,resource pooling in order to accumulate family assets is often viewed as part ofa deliberate assimilation and economic inclusion strategy; it is a means of as-piring to upward socioeconomic mobility. For ethnic enclaves, cultural capitalis not just knowledge of other languages or understanding cultural markers ofbehavior that language courses often do not teach. It is also youth interpretingfor elders; it is extended family members serving as substitute workers or childcare providers; cultural capital is also knowledge of how to make ends meetduring lean times for specific cultures, groups, or tribes. To know how to movefrom the formal economy to the informal economy seamlessly is another typeof cultural and class navigational capital. Ultimately, the intersection of cul-ture, social-economic class, ethno-racial, and gender characteristics combinesto create a very diverse learner pool.

New Directions for Adult and Continuing Education • DOI: 10.1002/ace

ECONOMIC INCLUSION AND FINANCIAL EDUCATION IN CULTURALLY DIVERSE COMMUNITIES 61

It is precisely the diversity of the learner pool that, if harnessed appro-priately, can anchor learning economic concepts and financial literacy in waysthat prepare the participants for a rapidly changing 21st-century economicreality. For low-wealth, high immigrant communities, we may want to re-assess the individualized financial education outreach campaigns to includeextended family, or at least, a multi-generational family perspective that pro-vides an introduction to economic education and financial services knowledgeas a “whole-family” initiative. Such an approach to economic education work-shops, curricula design, and pedagogy as part of family-oriented communityactivities and whole-family awareness campaigns may resonate more stronglywith communities of color (Guy, 1999; Tisdell et al., 2013).

Capturing Financial Knowledge and Gaps: Community Voices

The study that has generated much of the insights discussed here made use of acommunity-data-gathering process. Community data become a basis for com-munity self-advocacy and the role of culturally inclusive data collection createsan avenue to identify the cultural capital of low-wealth communities that oftenescape mainstream notice. Community data collection also sheds light on fam-ilies’ financial education knowledge as well as gaps along with their economicmobility aspirations. Given the increased incidence of distressed communitiesacross the United States, the information gathered from low-wealth, culturallydiverse communities in California, Arizona, New Mexico, and Texas createsthe opportunity to share insights with other community-based organizations(CBOs), researchers, and community stakeholders.

The Frontera Asset Building Network (FABN) is a coalition of community-based organizations partnering with university researchers, federal and localpublic sector agencies, as well as foundation and private sponsors to increasetax compliance and asset building awareness campaigns in the southwesternregion of the United States. The CBOs that participated in the study’s surveydesign crafted an instrument, which sought to be as noninvasive as possiblewhile capturing economic, financial, and tax decisions of individuals, families,and households. This respondent pool includes Latinos, Native Americans,Non-Hispanic Whites, African Americans, Asian Americans, and others. Inaddition, the survey sought to identify economic resiliency activities engagedin by respondents.

Culture and language play a large role in culturally diverse family eco-nomic security and financial resiliency behaviors and the community datacapture this aspect of diverse low-wealth communities (Robles, 2006, 2009;Yosso, 2005). The participating CBO members agreed to administer the sur-veys during tax seasons (January 15 to April 15). The data were collected at theparticipating CBOs offering either low-fee tax preparation services or free taxpreparation services affiliated with VITA (Volunteer Individual Tax Assistance)programs sponsored by the Internal Revenue Service. The surveys were admin-istered in English and Spanish. The response rates were generally high and

New Directions for Adult and Continuing Education • DOI: 10.1002/ace

62 FINANCIAL LITERACY AND ADULT EDUCATION

attributable to the long-term presence of the CBOs anchored in low-wealth,diverse communities. The data were collected over seven years after first beingpiloted in tax season 2004 (tax year 2003) through 2009 (tax year 2008).

Additionally, several survey questions were designed to capture the af-fordability and accessibility of financial services used by low-wealth diversefamilies. These questions included (a) Where do you cash your paycheck? (b)Do you use money orders to pay your bills? (c) Have you ever received yourtax refund the same day (or within the week) from a commercial tax preparer?(d) Do you lend to or borrow from family members in emergencies? (e) Doyou send money to family members not residing with you?

Such questions, which are intended to get at the cultural context of therespondents, reveal the types of financial transaction services used by low-wealth families living in predominantly cash-based economies. For example,even though a significant percentage of survey responders indicated that theycashed their paycheck at a mainstream financial institution (90%), they stillhad a high rate of using money orders to pay their bills (48%). In additionto these combined questions indicating that banking products may not beas easily accepted in a cash-based economy (e.g., landlords accepting moneyorders or cash only), they also indicate that low-wealth consumers do notemploy mainstream financial institution services and products in the samemanner as do middle-class and affluent consumers.

The findings indicate that family is far more flexible a definition amongculturally diverse communities where more grandparents raise grandchild-ren, aunts and uncles and fictive kin (e.g., kinship relationships establishedthrough religious ceremonies, godmother/godfather) predominate, and thesesocial networks may be substituting as the “savings” buffer for family emergen-cies. Survey respondents were also asked two structural questions: (a) Haveyou ever spent your tax refund on the following? (b) What would you liketo know more about? Both questions had a list of entries covering various fi-nancial services and products along with asset-building activities as well as anopen-ended text option. Some of the 15 tax refund items asked about includedsuch economic resiliency activities as house down payments, car, computer,and appliance purchases, as well as other types of payment fees, such as im-migration fees, medical bills, auto insurance, and payoff of payday loans.

The survey results provide evidence that asset building in communitieswith high immigrant, ethnic, and cultural legacies does not conform to the“individualized” consumer stereotype of the nuclear family unit but rather en-compasses a multi-generational and extended family orientation. For exam-ple, survey respondents indicated that they used their tax refunds to pay forfamily members’ green card immigration fees, for brother/sister/niece/nephewor grandchildren’s tuition and/or books, for family member funerals, to helpfamily members with bills, to pay back money borrowed from family mem-bers/fictive kin/friends, and to pay for a baptism, wedding, or quincenera(coming of age celebration). For the open-ended text responses for the sec-ond question (i.e., What would you like to learn more about?), respondents

New Directions for Adult and Continuing Education • DOI: 10.1002/ace

ECONOMIC INCLUSION AND FINANCIAL EDUCATION IN CULTURALLY DIVERSE COMMUNITIES 63

indicated future and family-oriented items such as helping with taking careof elderly parents, getting a GED, enrolling in ESL courses, how to save forschool expenses, and legal help with student loan repayment.

Finally, to better understand how culturally diverse, low-wealth familiesengage in asset building and savings behaviors, a survey question designed tocapture “informal savings circles,” (known as rotating savings and credit as-sociations [ROSCAS] in the development economic literature) was includedin the survey instrument. This particular question captures savings behaviorthat has a communal-trust component since it occurs outside mainstream fi-nancial institutions, does not have an interest rate attached to it, and relieson a high degree of social and cultural capital among the savings participants(Hernandez, Restler, & Peralta, 2010; Hevener, 2006; Robles, 2007, 2009).The evidence indicates that college-educated or some-college Latinas were thehighest participants in communal savings circles. This indicates that it is notknowledge of other savings products (mainstream financial institutions), butrather cultural capital, communal trust building, and “goal”-oriented savingsthat are drivers in low-wealth, high immigrant legacy communities. The sur-vey findings provide an evidence-based context for creating economic and fi-nancial education curricula and provide a blueprint for crafting pedagogicalapproaches that can potentially meet diverse low-wealth community memberswhere they “are.” These findings, along with those from other studies, high-light the importance of attending to cultural and communal issues in financialeducation (Cohen & Casper, 2002; Hatton & Leigh, 2011; Spader, Ratcliffe,Montoya, & Skillern, 2009).

Whole-Family Economic Education Over the Life Cycle:Crossing Into New Territory

Given that many culturally diverse communities are very family oriented, apart of culturally responsive financial education should seek to leverage familycultural capital by including the family unit in economic and financial educa-tion curriculum. Social policy and education researchers generally define cul-tural capital as the diverse linguistic and racial/ethnic traditions in geographi-cally anchored communities (Robles, 2006, 2009; Yosso, 2005). In economicsresearch, cultural capital is often defined as cultural infrastructure and activ-ities of a locale such as the number of visits to museums and revenue gener-ated from tourist destinations. For example, social capital is often a functionof human capital: where we go to university and the discipline or field that westudy often dictates our social capital connections, their depth and breadth.What is important to recognize about cultural capital in creating a “whole-family-over-the-life-course” economic education curriculum and pedagogy isthat it contains the seeds for leveraging human capital across all the other eco-nomic sectors families and communities will be required to navigate in the21st century.

New Directions for Adult and Continuing Education • DOI: 10.1002/ace

64 FINANCIAL LITERACY AND ADULT EDUCATION

One example of infusing economic education into a whole-family per-spective is sharing information that credit scores (a consumer certification con-cept) have cascading and interconnecting impacts on several economic sectorsof family well-being over the life cycle. For example, credit scores impact jobapplications (labor markets), securing auto loans (consumer market and trans-portation security), insurance rates and costs (asset building and wealth pro-tection), and opportunities for entrepreneurial entry and expansion (incomesecurity and wealth accumulation).

The Great Recession alerted us to the increasing complexity of economicsector connectedness and the significance of economic events—both local andglobal—that impact our daily lives. Creating opportunities to understand fam-ily economic inclusion and financial security over the life cycle becomes cru-cial to family and community well-being. Such basic family economic activ-ities that leverage cultural capital include elders caring for grandchildren asparents and older siblings work, youth translators for immigrant extended-family members as they engage in consumption decisions, home-based eco-nomic and entrepreneurial activities that require rotating family memberparticipation, pooling of family transportation resources, financial decisionmaking based on whole-family mobility aspirations, and communal savingscircles, to name a few. Using new understanding of geographic and culturallyanchored traditions in diverse low-wealth communities can provide an inclu-sive economic education pedagogy that requires all family members to bringtheir daily economic activities and multiple affiliations to the learning process(Ruwanpura, 2008; Thornton & White-Means, 2000). This allows for inter-generational transmission of survival and sustainability knowledge directedat navigating economic markets as part of the economic education learningprocess without creating age or experience silos.

Conclusion

Current economic and financial education curricula have identified the need totarget specific groups and populations that have traditionally been neglected inpedagogical approaches: adult learners, English as a Second Language learners,recently arrived/immigrants, and the working poor. In culturally diverse andimmigrant legacy communities, family orientation is paramount: family andextended family are generally both young and elder care-givers, lenders of firstresort, and often the only source of advice for financial and economic emergen-cies. To create financial and economic educational courses, workshops, andmaterials that acknowledge and include the family unit would cultivate in-creased trust and would contribute to word-of-mouth marketing. In addition,such an approach would expand participation rates among working adultsprecisely because economic and financial literacy would be offered as a familyactivity. Preparing consumers to understand financial products and servicescontinues to be a fundamental learning goal addressed by adult education re-searchers and practitioners. Preparing the entire family unit to better navigate

New Directions for Adult and Continuing Education • DOI: 10.1002/ace

ECONOMIC INCLUSION AND FINANCIAL EDUCATION IN CULTURALLY DIVERSE COMMUNITIES 65

rapidly changing financial and economic markets using culturally responsiveapproaches serves as an additional communication tool in hard to reach di-verse, low-wealth communities.

References

Cohen, P., & Casper, L. (2002). In whose home? Multigenerational families in the UnitedStates, 1998–2002. Sociological Perspectives, 45(1), 1–20.

Guy, T. C. (1999). Culture as context for adult education: The need for culturally relevantadult education. In T. C. Guy (Ed.), New Directions for Adult and Continuing Education:No. 82. Providing culturally relevant adult education: A challenge for the twenty-first century(pp. 5–18). San Francisco, CA: Jossey-Bass.

Hatton, T., & Leigh, A. (2011). Immigrants assimilate as communities, not just as individ-uals. Journal of Population Economics, 24, 389–410. doi:10.1007/s00148-009-0277-0

Hernandez, R., Restler, L., & Peralta, G. (2010). Understanding financial behavior amongDominicans in New York city. New York, NY: Dominican Studies Institute, CUNY.

Hevener, C. C. (2006, November). Alternative financial vehicles: Rotating savingsand credit associations (ROSCAS) (Working Paper). Philadelphia, PA: CommunityDevelopment Division of the Federal Reserve Bank of Philadelphia. Retrievedfrom http://www.philadelphiafed.org/community-development/publications/discussion-papers/discussionpaper-ROSCAs.pdf

Kochhar, R., & Cohn, D. (2011). Fighting poverty in a tough economy, Americans movein with their relatives. Pew Social and Demographic Trends Publication. Retrieved fromwww.pewsocialtrends.org/files/2011/10/Multigenerational-Households-Final1.pdf

Lofquist, D. A. (2012, October). Multigenerational households: 2009–2011. Ameri-can Community Survey Briefs, ACSBR/11-03, U.S. Census Bureau. Retrieved fromhttp://www.census.gov/prod/2012pubs/acsbr11-03.pdf

Orellana, M., Dorner, L., & Pulido, L. (2003). Accessing assets: Immigrant youth’s work asfamily translators or “para-phrasers.” Social Problems, 50(4), 505–524.

Penaloza, L. (1995). Immigrant consumers: Marketing and public policy considerations inthe global economy. Journal of Public Policy and Marketing, 14(1), 83–94.

Robles, B. (2006). Wealth creation in Latino Communities: Latino families, communityassets and cultural capital. In J. G. Nembhard & N. Chiteji (Eds.), Wealth accumulationand communities of color in the United States: Current issues (pp. 241–266). Ann Arbor:University of Michigan Press.

Robles, B. (2007). Tax refunds and microbusinesses: Expanding family and communitywealth building in the borderlands. The Annals of the American Academy of Political andSocial Sciences, 612, 178–191.

Robles, B. (2009, September). U.S. Latino families, heads of household, and the elderly: Emerg-ing trends in financial services and asset-building behaviors. Madison, WI: Filene ResearchInstitute.

Ruwanpura, K. N. (2008). Multiple identities, multiple-discrimination: A critical review.Feminist Economics, 14(3), 77–105.

Shapiro, T., Meschede, T., & Osoro, S. (2013, February). The roots of the widen-ing racial wealth gap: Explaining the Black-White economic divide. Waltham,MA: Institute on Assets and Social Policy, Brandeis University. Retrieved fromhttp://iasp.brandeis.edu/pdfs/Author/shapiro-thomas-m/racialwealthgapbrief.pdf

Spader, J., Ratcliffe, J., Montoya, J., & Skillern, P. (2009). The bold and the bankable: Howthe Nuestro Barrio telenovela reaches Latino immigrants with financial education. TheJournal of Consumer Affairs, 43(1), 56–79.

Stayman, D. M., & Deshpande, R. (1989). Situational ethnicity and consumer behavior.Journal of Consumer Research, 16, 361–371.

New Directions for Adult and Continuing Education • DOI: 10.1002/ace

66 FINANCIAL LITERACY AND ADULT EDUCATION

Taylor, P., Passel, J., Fry, R., Morin, R., Wang, W., Velasco, G., & Dockterman, D. (2010,March 18). The return of the multi-generational family household (PEW Research Center,A Social & Demographic Trends Report). Retrieved from http://www.pewsocialtrends.org/files/2010/10/752-multi-generational-families.pdf

Thornton, M. C., & White-Means, S. I. (2000). Race versus ethnic heritage in models offamily economic decisions. Journal of Family and Economic Issues, 21(1), 65–86.

Tisdell, E., Taylor, E., & Sprow Forte, K. (2013). Community-based financial literacy ed-ucation in a cultural context: A study of teacher beliefs and pedagogical practice. AdultEducation Quarterly, 63(4), 338–356.

Valdes, G. (2003). Expanding definitions of giftedness: The case of young interpreters from im-migrant communities. Educational Psychology Series. Mahwah, NJ: Lawrence ErlbaumAssociations.

Viramontez, R., & Trask, B. (2009). Intersections: Family and consumer sciences and cul-tural diversity. Family and Consumer Sciences Research Journal, 37(3), 247–252.

Yosso, T. (2005). Whose culture has capital? A critical race theory discussion of communitycultural wealth. Race, Ethnicity and Education, 8(1), 69–91.

BARBARA J. ROBLES works in the Division of Consumer and Community Affairs forthe Board of Governors of the Federal Reserve System.

New Directions for Adult and Continuing Education • DOI: 10.1002/ace