Embed Size (px)

Citation preview

Due Diligence for

Mergers & Acquisitions

11/02/2015

-

AGENDA

Why Due Diligence is important for M&A;

Objective of Due Diligence; Types of Due Diligence

Overviews; When Due Diligence becomes

Relevant; Key Focus Area in Due

Diligence; Due Diligence Process; Common Due Diligence Issues in

India; Case Study; Summary; Conclusion .

DUE DILIGENCE : LEARN FROM THE PAST, BUT LOOK TOWARDS

THE FUTURE 2

WHY DUE DILIGENCE IS IMPORTANT BEFORE ANY

TRANSACTIONS

3

To investigate into the Affairs of Business as a prudent business person

To confirm all material facts related to the Business

To assess the Risks and Opportunities of a proposed transaction.

To reduce the Risk of post-transaction unpleasant surprises

To confirm that the business is what it appears.

Why Due Diligence is Important for M&A….??

4

To Create a Trust between two Unrelated Parties

To identify potential deal killers defects in the target and avoid a bad business transaction.

To gain information that will be useful for Valuing Assets Representations & Warranties for Indemnification Negotiating Price Concessions

Why Due Diligence is Important for M&A….Cont…

5

To verify that the transaction complies with investment or acquisition criteria.

To Investigate & Evaluate a Business Opportunity

It Involves an analysis carried out before acquiring a controlling interest in a company.

DUE DILIGENCE IS NOT THE JUDGEMENT MAKING IT IS JUST BRING OUT ALL FACT TO FORE

Why Due Diligence is Important for M&A….Cont…

6

OBJECTIVE OF DUE

DILIGENCE

7

Objective of Due Diligence

To determine compliance with relevant laws and disclose any regulatory restrictions on the proposed transaction

To evaluate the condition of the physical plant and equipment; as well as other tangible and intangible Assets

To ascertain the appropriate purchase price & and the method of payment.

To determine details that may be relevant to the drafting of the acquisition agreement,

To discover liabilities or risks that may be

deal-breakers

To analyze any potential antitrust issues that may prohibit the proposed M&A

To evaluate the legal and financial risks of the transaction

8

TYPES OF DUE DILIGENCE OVERVIEWS

9

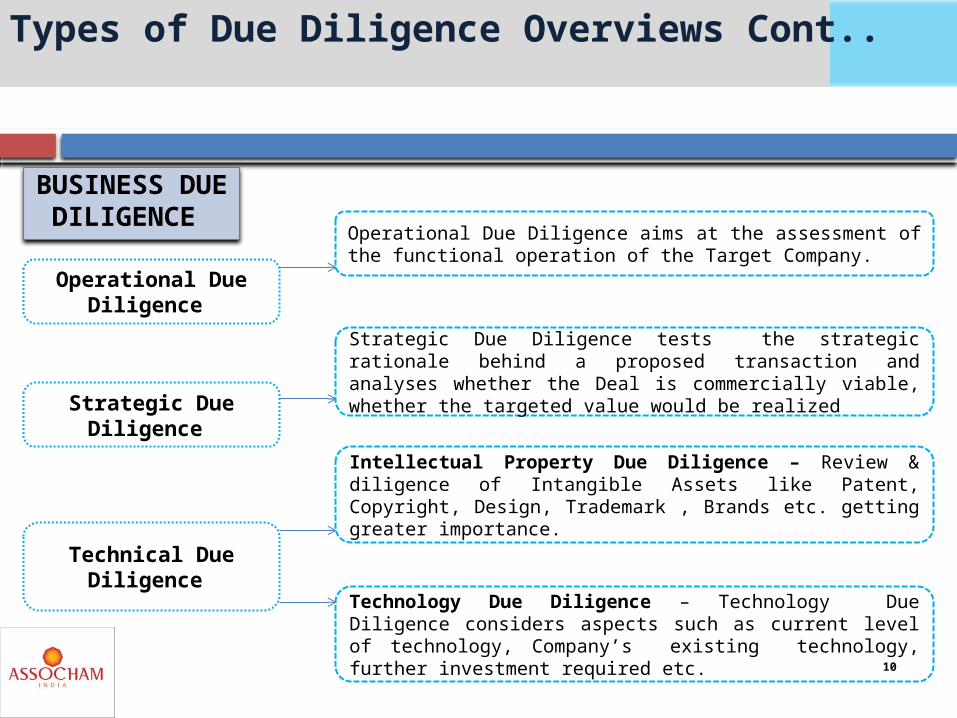

Types of Due Diligence Overviews Cont..

Operational Due Diligence

Operational Due Diligence aims at the assessment of the functional operation of the Target Company.

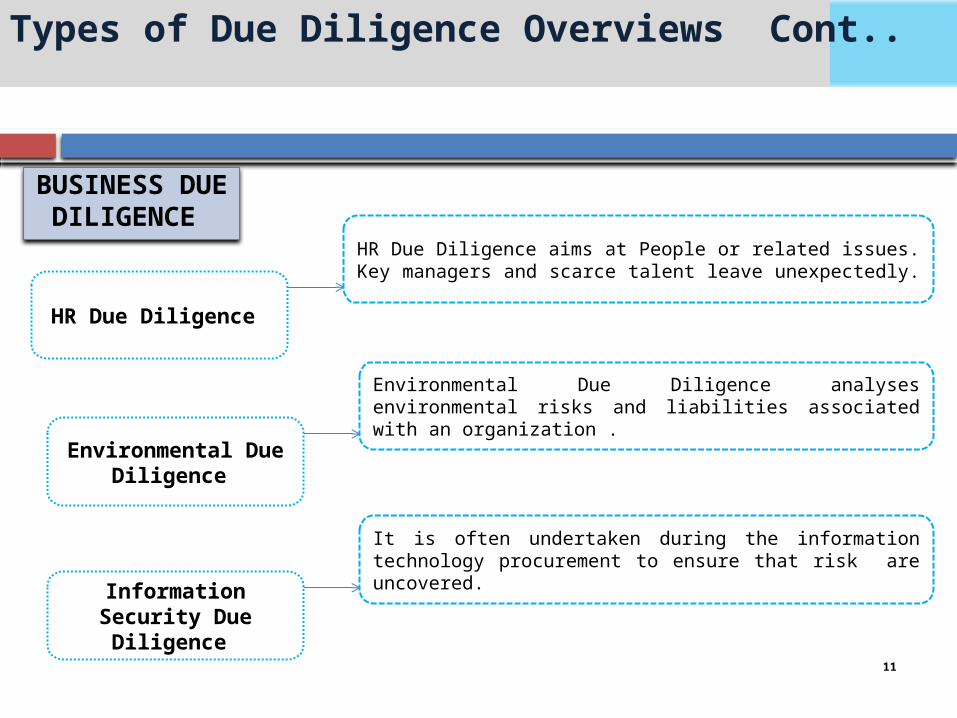

BUSINESS DUE DILIGENCE

Strategic Due Diligence

Technical Due Diligence

Strategic Due Diligence tests the strategic rationale behind a proposed transaction and analyses whether the Deal is commercially viable, whether the targeted value would be realized Intellectual Property Due Diligence – Review & diligence of Intangible Assets like Patent, Copyright, Design, Trademark , Brands etc. getting greater importance.

Technology Due Diligence – Technology Due Diligence considers aspects such as current level of technology, Company’s existing technology, further investment required etc. 10

HR Due Diligence

BUSINESS DUE DILIGENCE

HR Due Diligence aims at People or related issues. Key managers and scarce talent leave unexpectedly.

Environmental Due Diligence

Environmental Due Diligence analyses environmental risks and liabilities associated with an organization .

Information Security Due Diligence

It is often undertaken during the information technology procurement to ensure that risk are uncovered.

Types of Due Diligence Overviews Cont..

11

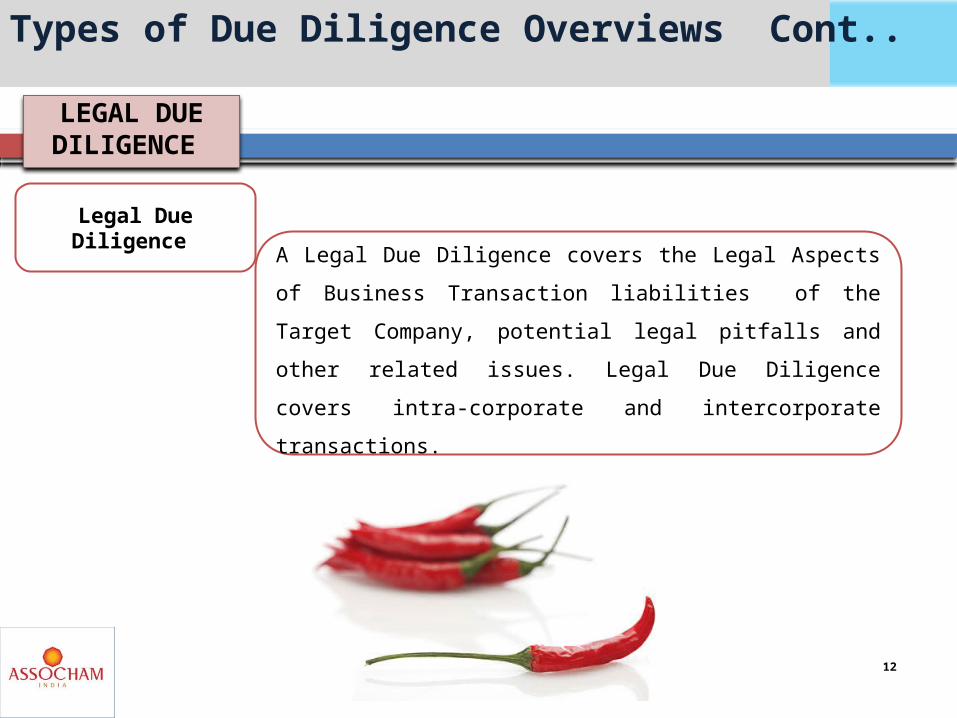

Legal Due Diligence A Legal Due Diligence covers the Legal Aspects

of Business Transaction liabilities of the Target Company, potential legal pitfalls and other related issues. Legal Due Diligence covers intra-corporate and intercorporate transactions.

LEGAL DUE DILIGENCE

Types of Due Diligence Overviews Cont..

12

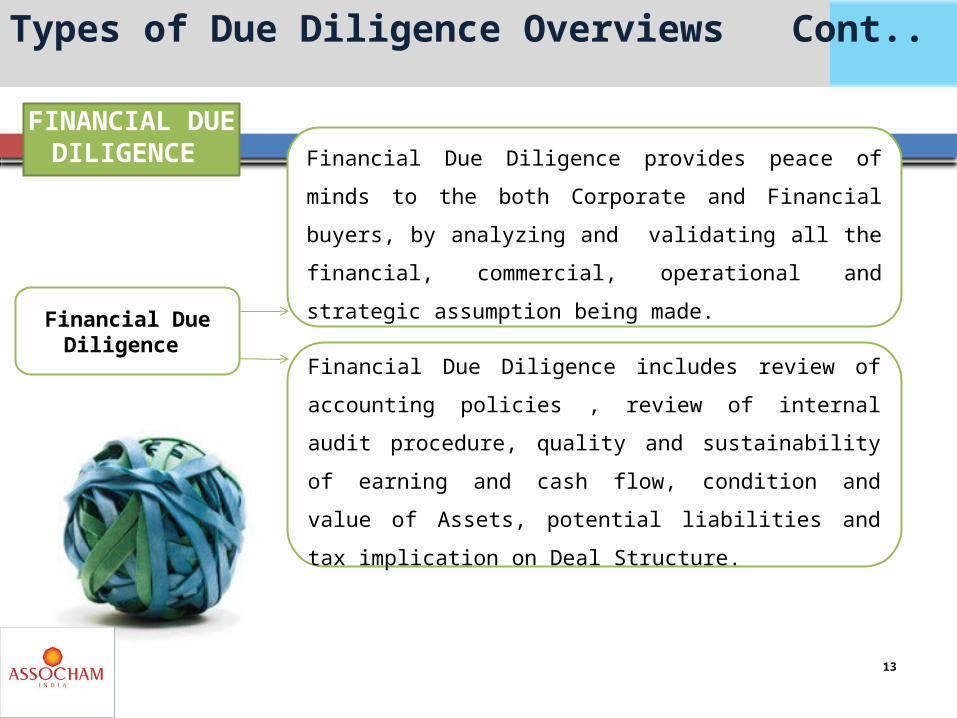

Financial Due Diligence provides peace of minds to the both Corporate and Financial buyers, by analyzing and validating all the financial, commercial, operational and strategic assumption being made.

Financial Due Diligence includes review of accounting policies , review of internal audit procedure, quality and sustainability of earning and cash flow, condition and value of Assets, potential liabilities and tax implication on Deal Structure.

FINANCIAL DUE DILIGENCE

Financial Due Diligence

Types of Due Diligence Overviews Cont..

13

WHEN DUE DILIGENCE BECOMES

RELEVANT???

14

Deal Strategy Validation

Value Driver Identification

Identifying black holes

Valuation

Identifying Deals

Evaluating Deals

Executing Deals

Making Deals

SuccessfulHarvesting

Deals

• Structuring and Negotiating issues

• Matters to be included in Shareholders / other agreement

• Representation and warranties / indemnities involved

• Design tax efficient structures for acquisitions and disposals

• Planning exit strategies

When does Due Diligence become relevant?

15

KEY FOCUS AREA IN DUE DILIGENCE

16

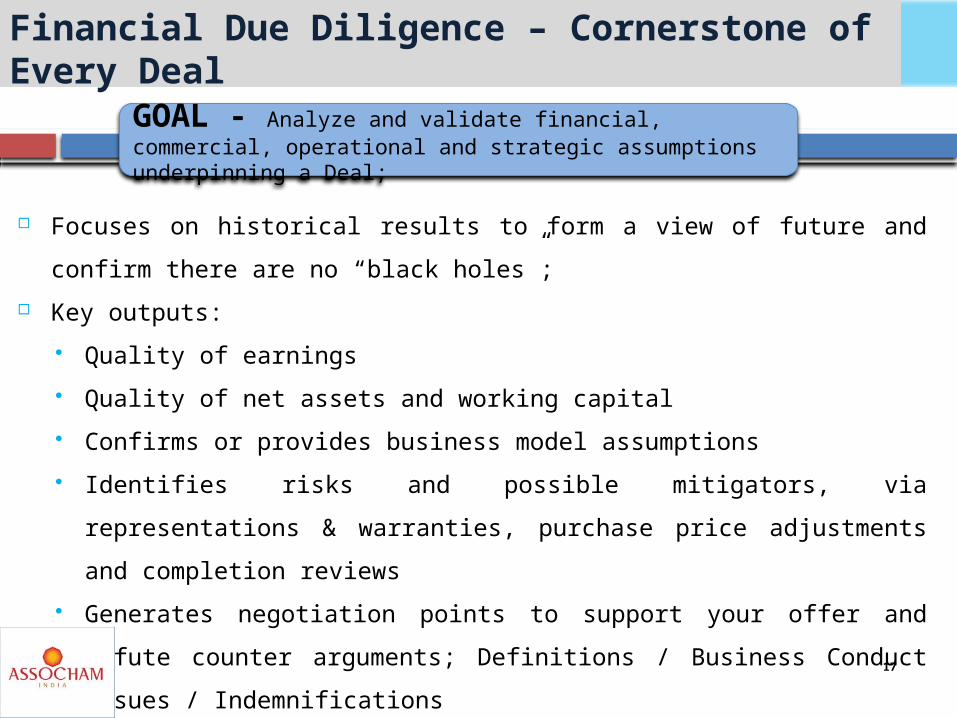

Focuses on historical results to form a view of future and confirm there are no “black holes”;

Key outputs: Quality of earnings Quality of net assets and working capital Confirms or provides business model assumptions Identifies risks and possible mitigators, via representations & warranties, purchase price adjustments and completion reviews

Generates negotiation points to support your offer and refute counter arguments; Definitions / Business Conduct Issues / Indemnifications

Financial Due Diligence – Cornerstone ofEvery Deal

GOAL - Analyze and validate financial, commercial, operational and strategic assumptions underpinning a Deal;

17

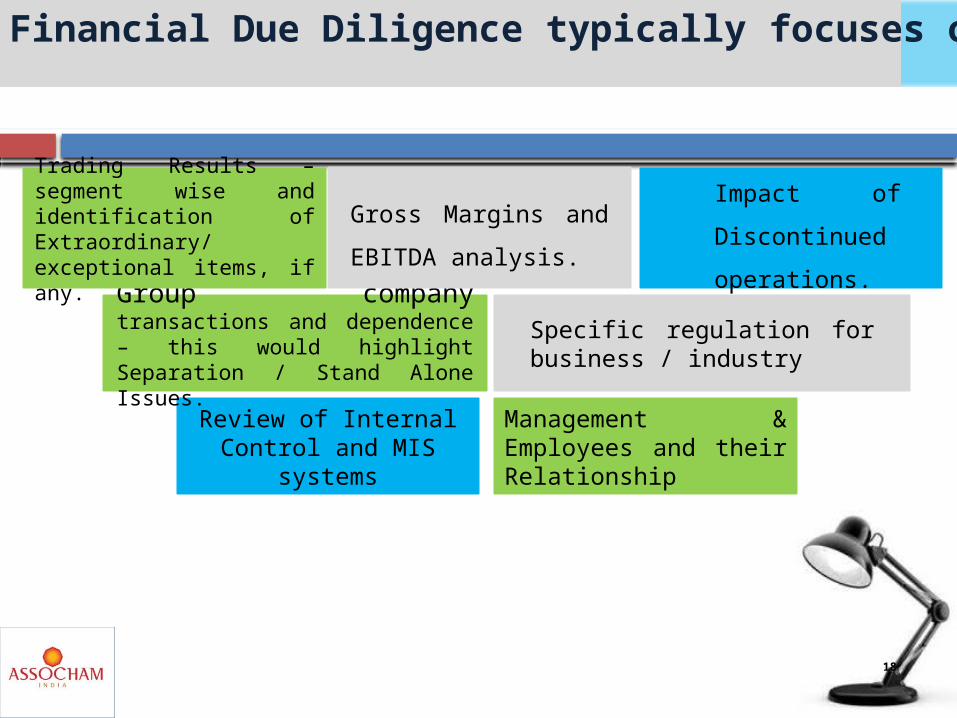

Financial Due Diligence typically focuses on….

Review of Internal Control and MIS

systems

Group company transactions and dependence – this would highlight Separation / Stand Alone Issues.

Trading Results – segment wise and identification of Extraordinary/ exceptional items, if any.

Gross Margins and EBITDA analysis.

Management & Employees and their Relationship

Specific regulation for business / industry

Impact of Discontinued operations.

18

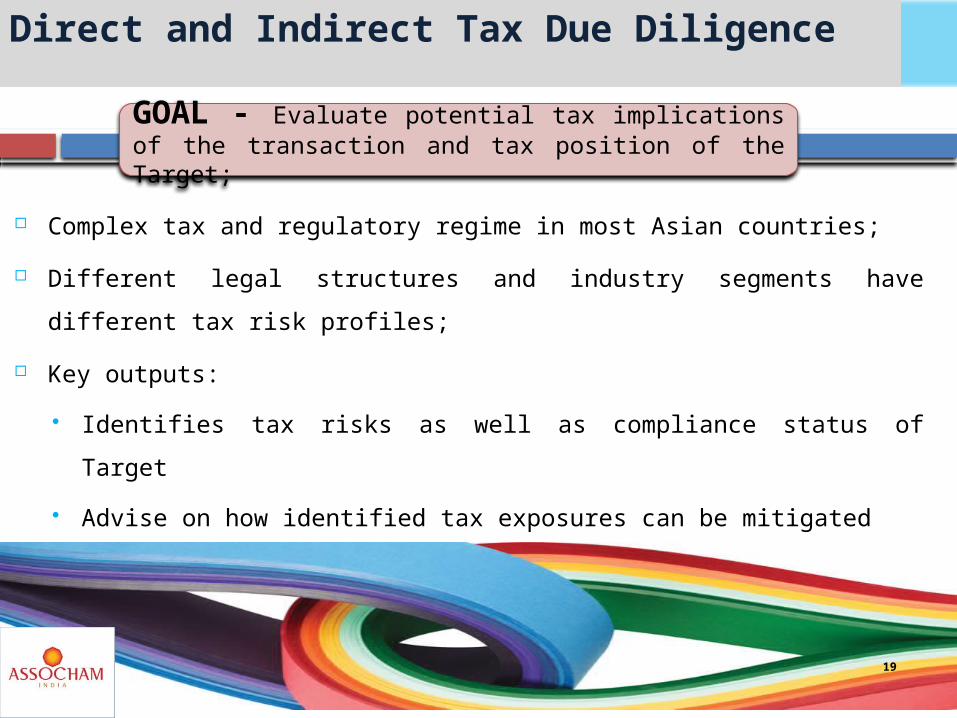

Complex tax and regulatory regime in most Asian countries; Different legal structures and industry segments have

different tax risk profiles; Key outputs:

Identifies tax risks as well as compliance status of Target

Advise on how identified tax exposures can be mitigated Provides optimal financial and tax structure for the proposed deal

Direct and Indirect Tax Due Diligence

GOAL - Evaluate potential tax implications of the transaction and tax position of the Target;

19

Tax Due Diligence Typically Focuses On..

Status of Direct and Indirect tax assessments.

Review of audits carried out by the respective tax authorities

Review of the claims made by the tax authorities and the responses made.

20

Typically involves a combination of desk research, interviews with target management team, key trading partners and industry experts;

Key outputs: Issues in respect of achievability of business plan projections

Target’s positioning and competitiveness Target specific market and industry related issues Identifies strategic value creating opportunities Highlights Exit risks and opportunities

Market Due Diligence

GOAL - Assist in understanding the condition and prospects of the market a Company wishes to enter in;

21

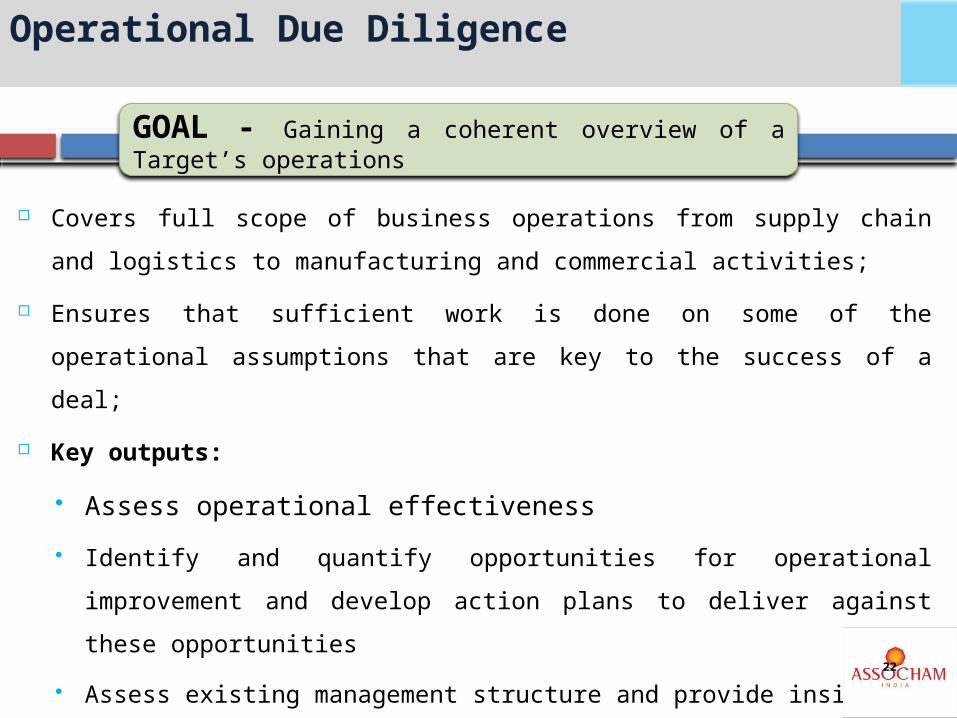

Covers full scope of business operations from supply chain and logistics to manufacturing and commercial activities;

Ensures that sufficient work is done on some of the operational assumptions that are key to the success of a deal;

Key outputs:

Assess operational effectiveness Identify and quantify opportunities for operational improvement and develop action plans to deliver against these opportunities

Assess existing management structure and provide insight on personnel related issues

Operational Due Diligence

GOAL - Gaining a coherent overview of a Target’s operations

22

Particularly important for M&A in the IT services sector; Key outputs:

Assess existing IT infrastructure and future needs Provides inputs for planning integration of systems and applications

Highlight key business process issues, such as in purchases & payables cycle, revenues & receivables cycle

Assess security & controls to ensure data integrity, availability and confidentiality

IT Due Diligence

GOAL - Evaluation of IT security & controls and business process issues

23

Typically covers pension and employee liability valuation, payroll costs validation, employment termination costs, compensation and benefit alignment costs

Key outputs: Assess existing levels of employee proficiency against industry standards

Highlight redundancy issues Assess potential for redeployment of staff Analyses of industrial relations Assess employee compensation, including retirement benefits

HR Due Diligence

GOAL - Qualitative evaluation of existing staff including HR policies

24

Buy Side Diligence(For ascertain what buyer are buying )

Sell Side Diligence(Issues on which buyers can negotiate)

v/s

Types of Due Diligence Reviews – Purpose

25

Financial analysis to support opinions and conclusions. Identification of hidden value in the target. Highlighting post-acquisition / integration / separation

issues. Using expert resources in the target country to identify

local risks and issues. Identifying areas that may impact the exit strategy of the

equity provider. Analysing the sustainability of earnings and cash flows.

Buy side Due Diligence

26

Assists the vendor by providing an upfront independent review.

Highlights sale and purchase agreement issues early that may become negotiating points or areas for warranties/indemnities.

Ensures a level playing field by providing all potential purchasers with objective information.

Reduces the level of due diligence procedures that potential purchasers need to perform.

Expedites the deal timetable by avoiding lengthy negotiations and disruption to the vendor.

Reduces the risk of last minute value erosion and avoid lengthy re-negotiations.

Sell side Due Diligence

27

Full AccessFull access to the target management, staff, accounting, financial and legal data.

Limited AccessLimited access to the target management, staff, accounting, financial and legal data.

No AccessStrictly controlled environment, typically based on publicly available data.

Carve OutStrictly limited to the part of business proposed to be sold.

Types of Due Diligence Reviews – Access Levels

28

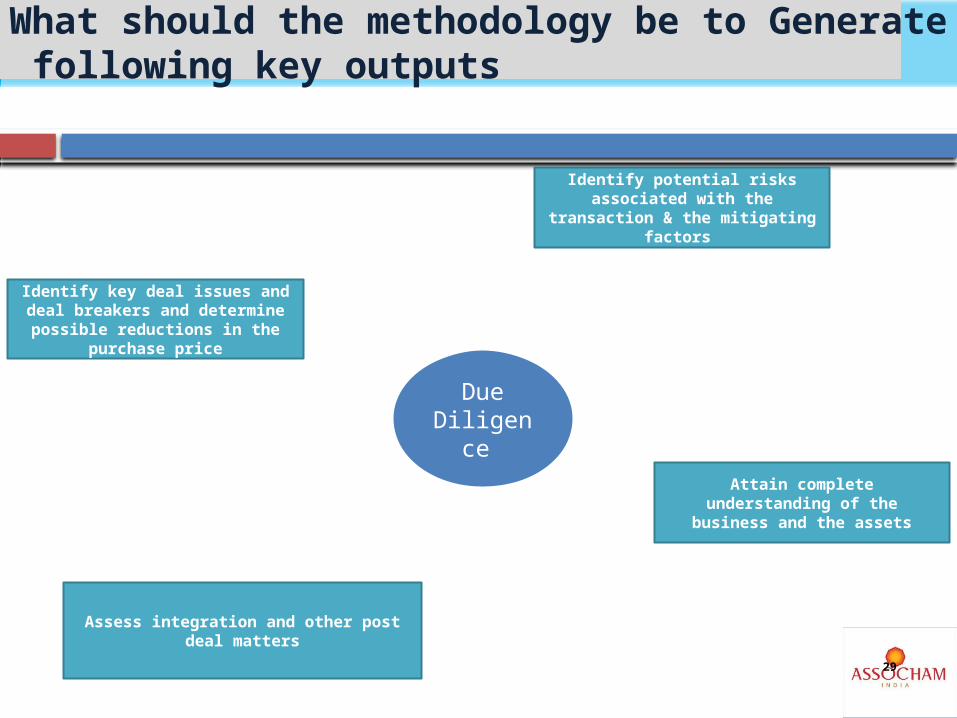

Due Diligen

ce

What should the methodology be to Generate following key outputs

Attain complete understanding of the

business and the assets

Identify potential risks associated with the

transaction & the mitigating factors

Identify key deal issues and deal breakers and determine possible reductions in the

purchase price

Assess integration and other post deal matters

29

DUE DILIGENCE PROCESS

30

Consider Preliminary Structure

Visit Data room Review Background Material

Review Audit Work Paper

Assist with letter of Intent

Visit Target Company and Interview

Management Develop workmen and info Request

List Review financial model of Target

Company

Preparation of Report

Finalize Structure

Support Integration Plan

Read and Comment on Sale Agreement

Pre-Fieldwork Fieldwork Post-Fieldwork

Typical Diligence Process

31

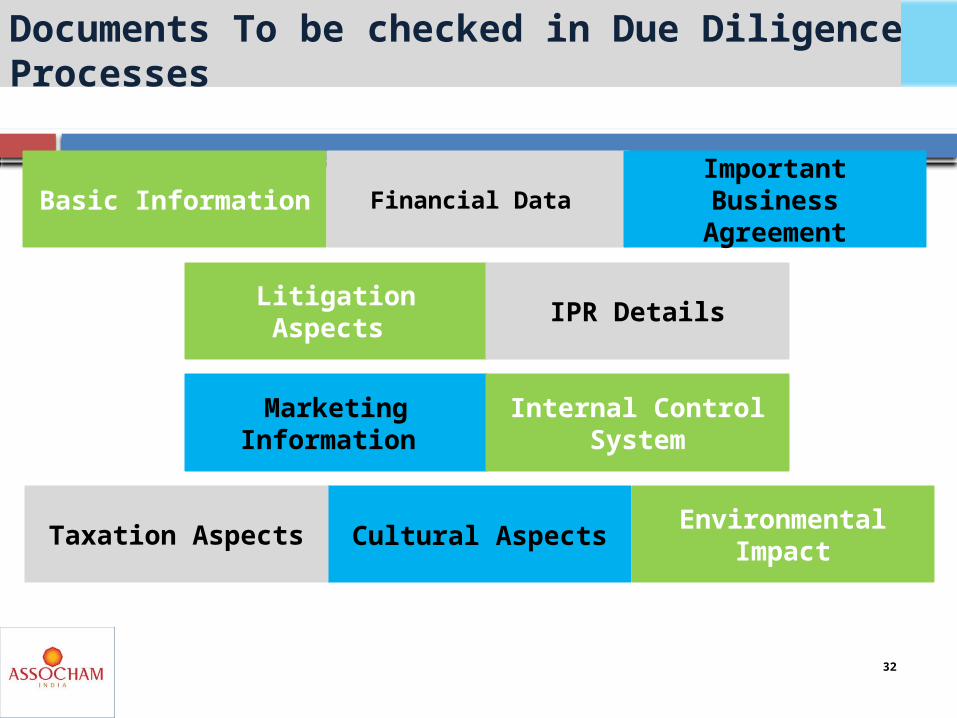

Cultural AspectsTaxation Aspects

Marketing Information

Litigation Aspects

Basic Information Financial Data

Environmental Impact

Internal Control System

IPR Details

Important Business Agreement

Documents To be checked in Due Diligence Processes

32

COMMON DILIGENCE ISSUES IN INDIA

33

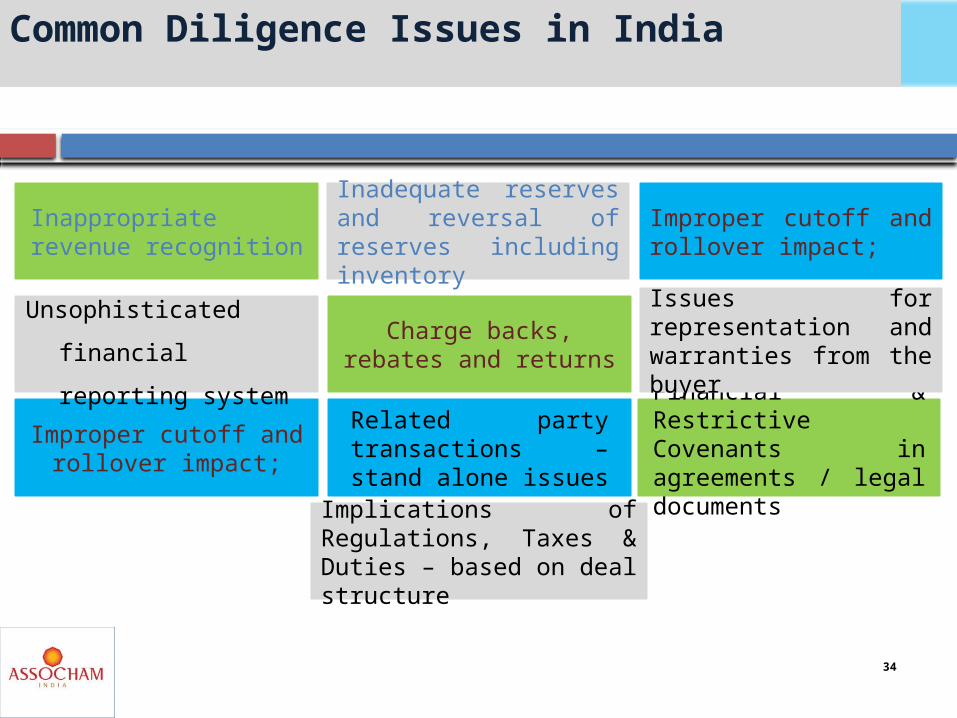

Common Diligence Issues in India

Charge backs, rebates and returns

Inappropriate revenue recognition

Inadequate reserves and reversal of reserves including inventory

Improper cutoff and rollover impact;

Financial & Restrictive Covenants in agreements / legal documents

Improper cutoff and rollover impact;

Unsophisticated financial reporting system

Issues for representation and warranties from the buyer

Related party transactions – stand alone issues

Implications of Regulations, Taxes & Duties – based on deal structure

34

35

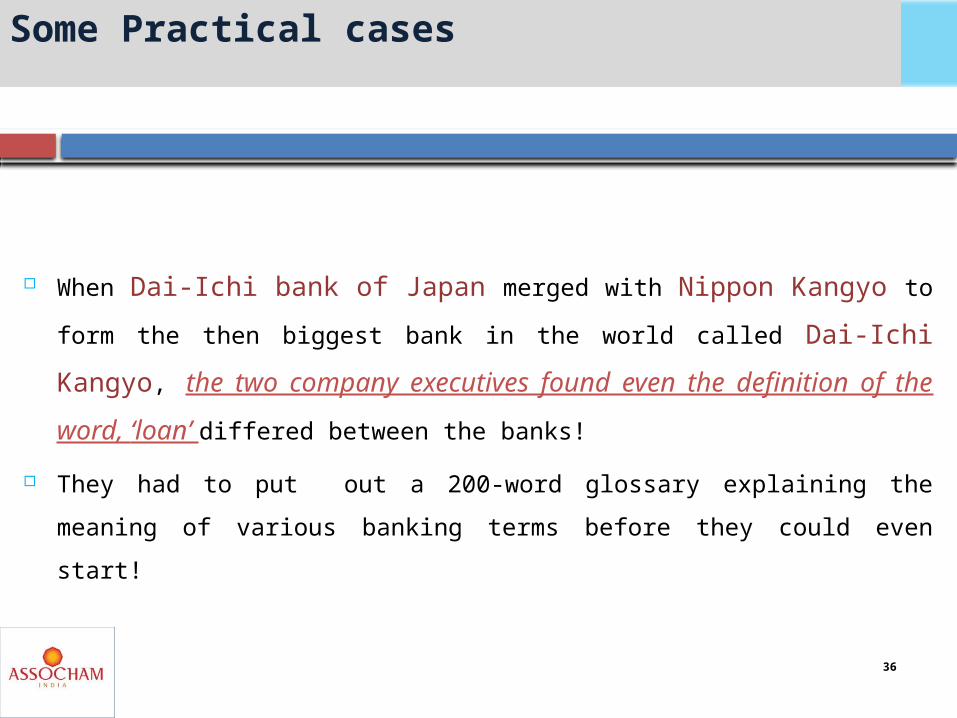

Some Practical cases

When Dai-Ichi bank of Japan merged with Nippon Kangyo to form the then biggest bank in the world called Dai-Ichi Kangyo, the two company executives found even the definition of the word, ‘loan’ differed between the banks!

They had to put out a 200-word glossary explaining the meaning of various banking terms before they could even start!

36

Some Practical cases Cont…

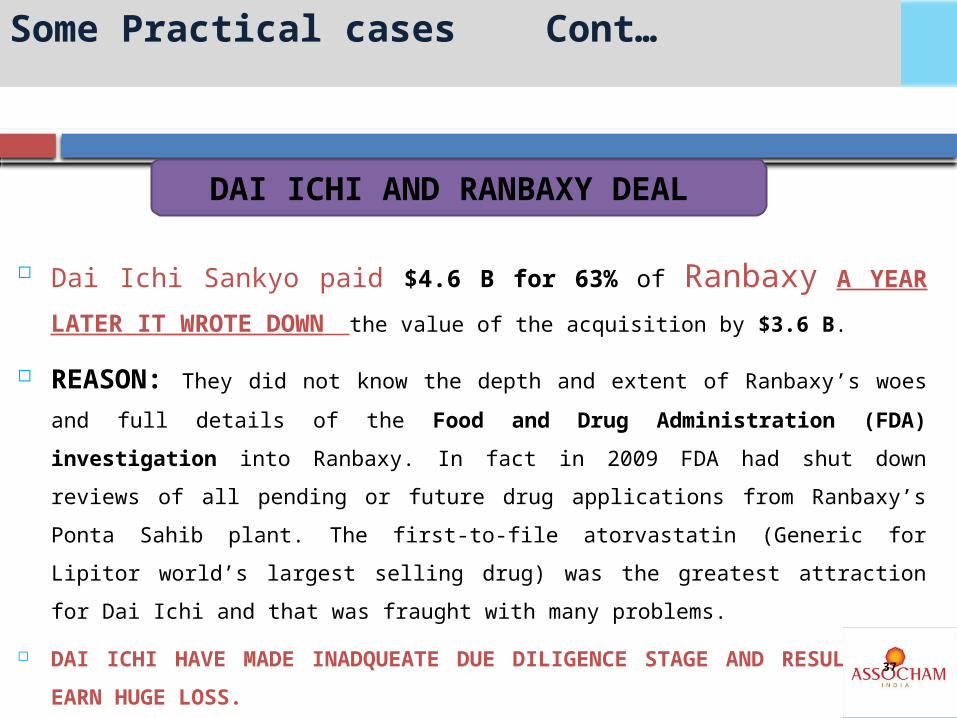

Dai Ichi Sankyo paid $4.6 B for 63% of Ranbaxy A YEAR LATER IT WROTE DOWN the value of the acquisition by $3.6 B.

REASON: They did not know the depth and extent of Ranbaxy’s woes and full details of the Food and Drug Administration (FDA) investigation into Ranbaxy. In fact in 2009 FDA had shut down reviews of all pending or future drug applications from Ranbaxy’s Ponta Sahib plant. The first-to-file atorvastatin (Generic for Lipitor world’s largest selling drug) was the greatest attraction for Dai Ichi and that was fraught with many problems.

DAI ICHI HAVE MADE INADQUEATE DUE DILIGENCE STAGE AND RESULT THEY EARN HUGE LOSS.

DAI ICHI AND RANBAXY DEAL

37

Some Practical cases Cont…

HCL AND AXON DEAL Infosys and HCL bid for Axon in Sep 08, HCL countered

Infosys bid of 600 pence with an aggressive offer of 650 pence; INFOSYS WITHDREW AND HCL TOOK IT OVER

NOTE: HCL did make the acquisition work by doing all the right things –main one –by eating the ego!

They reverse merged HCL teams into AXON as AXON was a high performance team and they were better than HCL –thus HCL Axon was born.

HCL DURING HR DUE DILIGENCE UNDERSTOOD THE FACTS THAT AXON TEAM HAS HUGE POTENTIAL AND DEAL CREATE SYNERGEY FOR HCL-AXON.

38

39

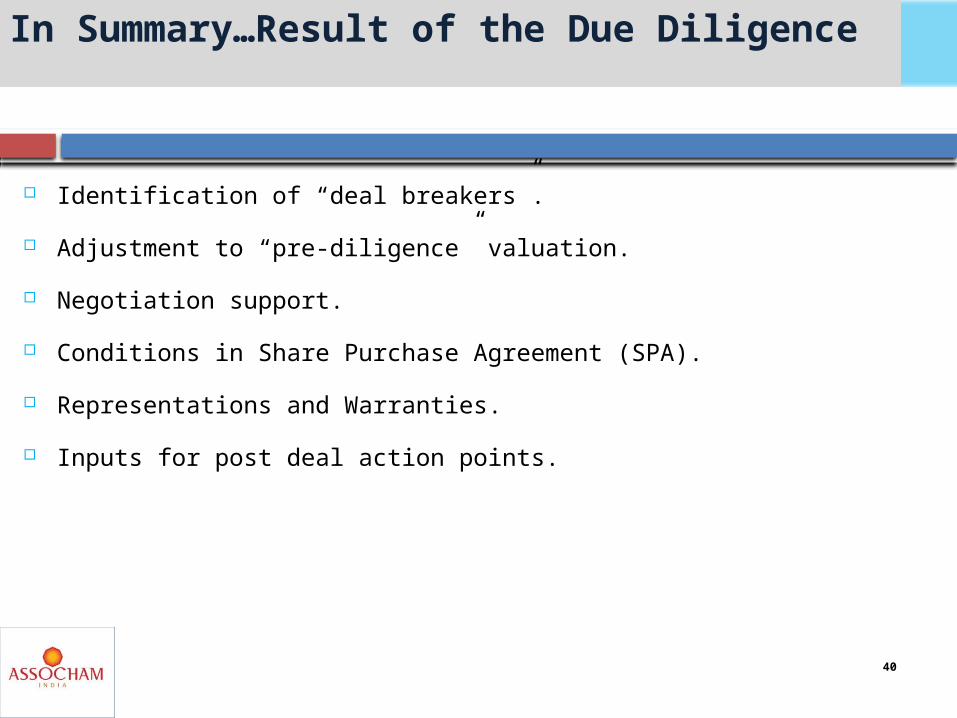

Identification of “deal breakers”. Adjustment to “pre-diligence” valuation. Negotiation support. Conditions in Share Purchase Agreement (SPA). Representations and Warranties. Inputs for post deal action points.

In Summary…Result of the Due Diligence

40

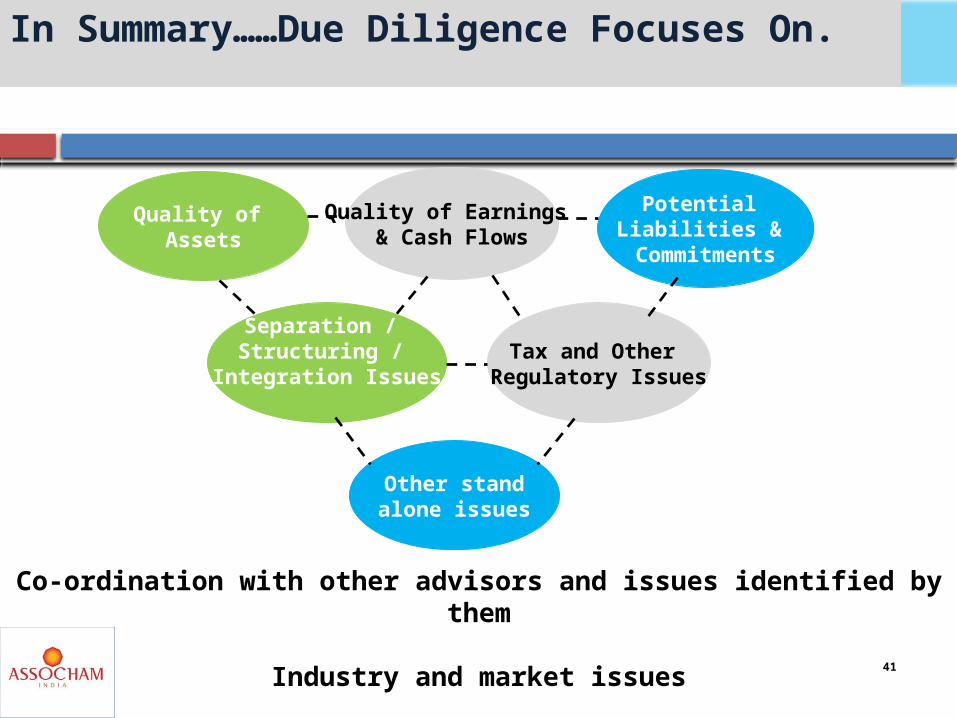

Quality of Assets

Quality of Earnings & Cash Flows

Potential Liabilities & Commitments

Separation / Structuring /

Integration IssuesTax and Other

Regulatory Issues

Other standalone issues

Co-ordination with other advisors and issues identified by them

Industry and market issues

In Summary……Due Diligence Focuses On.

41

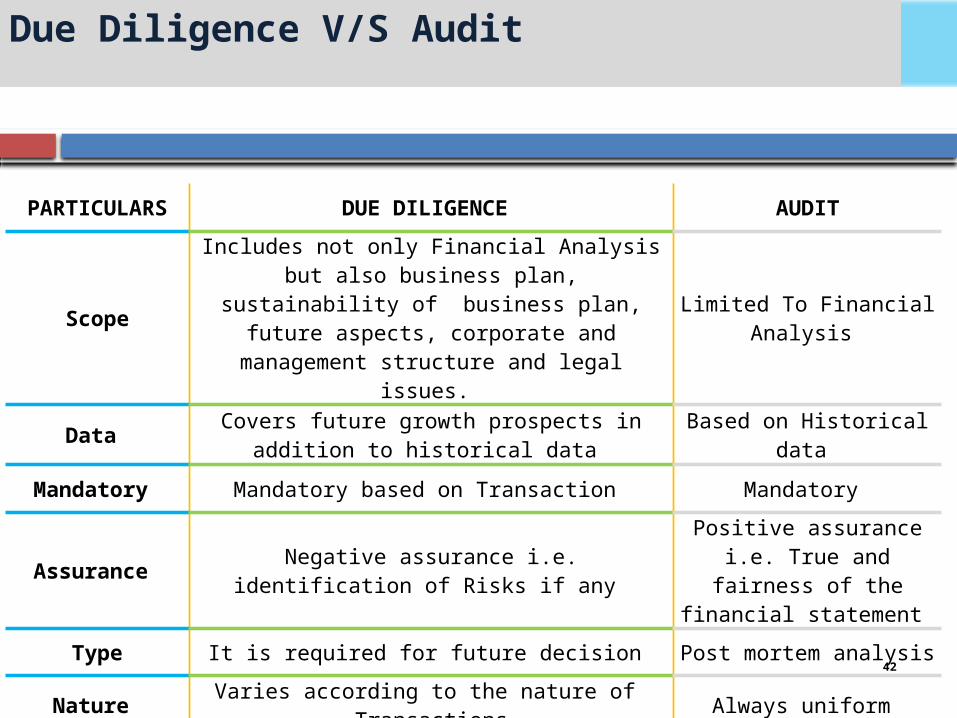

PARTICULARS DUE DILIGENCE AUDIT

Scope

Includes not only Financial Analysis but also business plan,

sustainability of business plan, future aspects, corporate and management structure and legal

issues.

Limited To Financial Analysis

Data Covers future growth prospects in addition to historical data

Based on Historical data

Mandatory Mandatory based on Transaction Mandatory

Assurance Negative assurance i.e. identification of Risks if any

Positive assurance i.e. True and fairness of the

financial statement Type It is required for future decision Post mortem analysis

Nature Varies according to the nature of Transactions Always uniform

Repetitiveness Occasional event Recurring event

Due Diligence V/S Audit

42

CONCLUSION

43

The goal of DUE DILIGENCE should be

DEAL MAKING

not

KILLING…

44

Corporate Professionals Capital Private Limited

D-28, South Extension –I, New Delhi-110 049Ph: +91.11.40622200; Fax: +91.11.40622201; E:

Pavan Kumar VijayManaging Director

45