Embed Size (px)

Citation preview

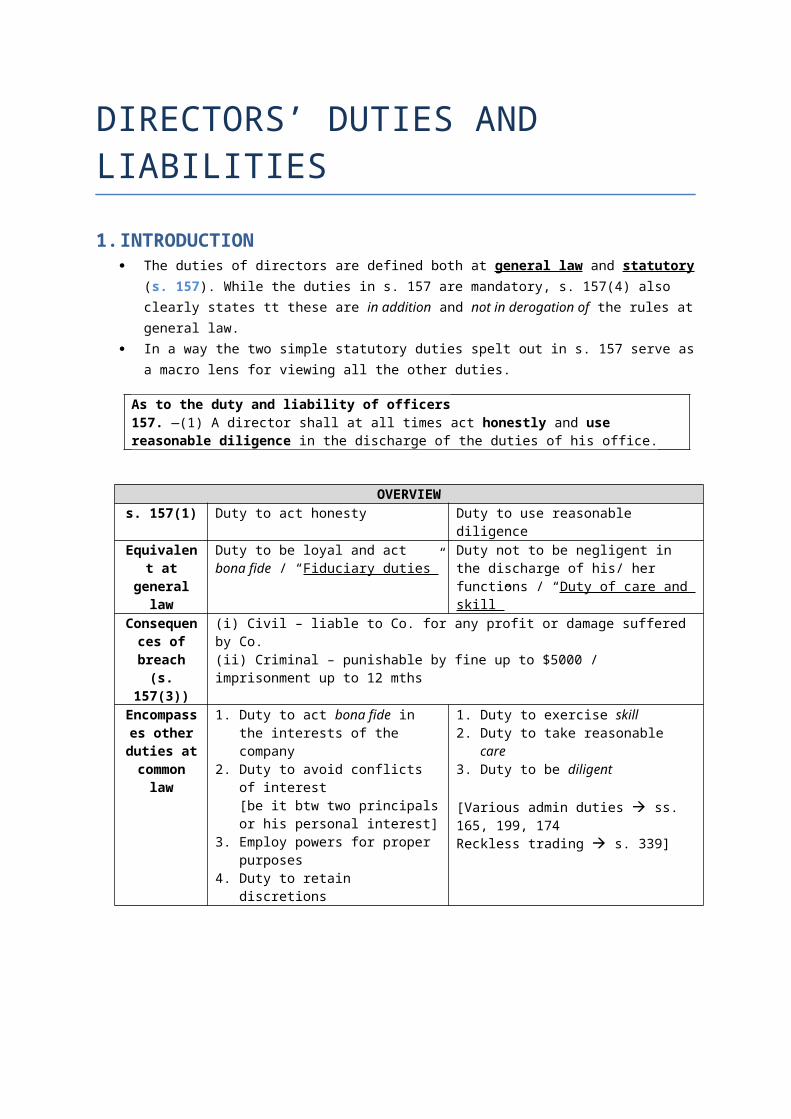

DIRECTORS’ DUTIES AND LIABILITIES1.INTRODUCTION

The duties of directors are defined both at general law and statutory(s. 157). While the duties in s. 157 are mandatory, s. 157(4) also clearly states tt these are in addition and not in derogation of the rules atgeneral law.

In a way the two simple statutory duties spelt out in s. 157 serve asa macro lens for viewing all the other duties.

As to the duty and liability of officers157. —(1) A director shall at all times act honestly and use reasonable diligence in the discharge of the duties of his office.

OVERVIEWs. 157(1) Duty to act honesty Duty to use reasonable

diligenceEquivalen

t atgenerallaw

Duty to be loyal and act bona fide / “Fiduciary duties”

Duty not to be negligent in the discharge of his/ her functions / “Duty of care and skill”

Consequences ofbreach(s.

157(3))

(i) Civil – liable to Co. for any profit or damage suffered by Co. (ii) Criminal – punishable by fine up to $5000 / imprisonment up to 12 mths

Encompasses otherduties atcommonlaw

1. Duty to act bona fide in the interests of the company

2. Duty to avoid conflicts of interest[be it btw two principalsor his personal interest]

3. Employ powers for proper purposes

4. Duty to retain discretions

1. Duty to exercise skill2. Duty to take reasonable

care3. Duty to be diligent

[Various admin duties ss. 165, 199, 174Reckless trading s. 339]

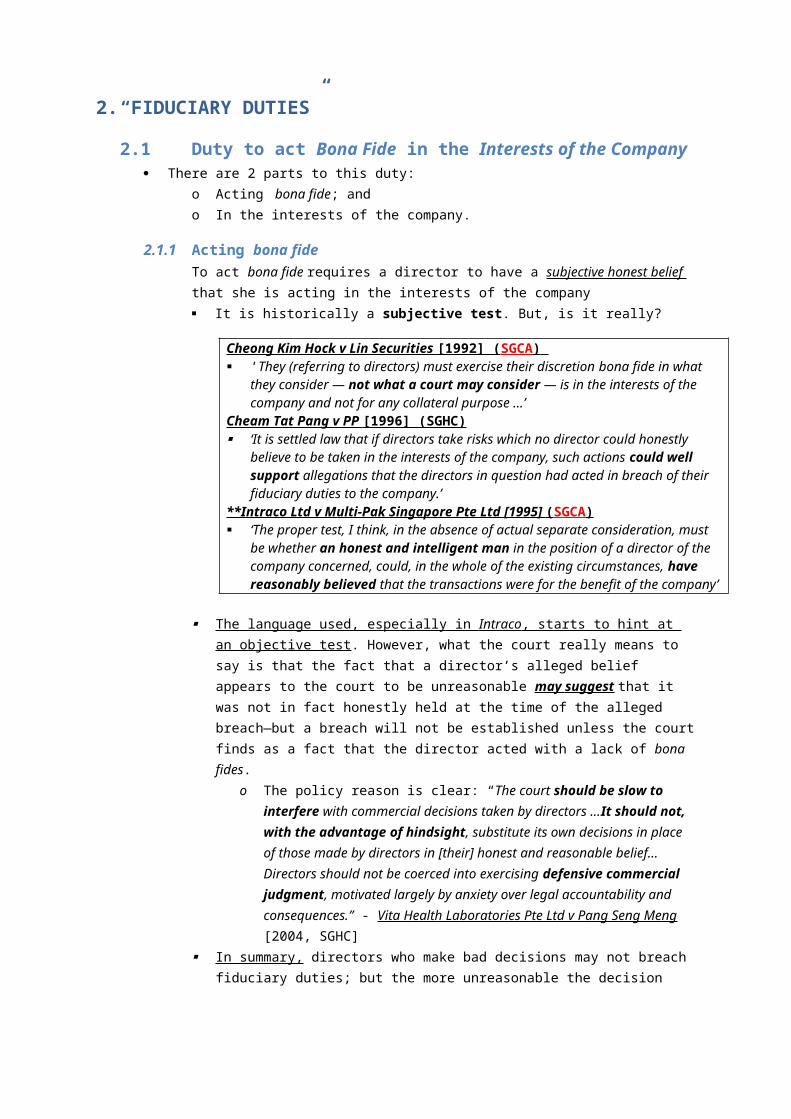

2.“FIDUCIARY DUTIES”

2.1 Duty to act Bona Fide in the Interests of the Company There are 2 parts to this duty:

o Acting bona fide; ando In the interests of the company.

2.1.1 Acting bona fideTo act bona fide requires a director to have a subjective honest belief that she is acting in the interests of the company It is historically a subjective test. But, is it really?

Cheong Kim Hock v Lin Securities [1992] ( SGCA ) ‘They (referring to directors) must exercise their discretion bona fide in what

they consider — not what a court may consider — is in the interests of the company and not for any collateral purpose …’

Cheam Tat Pang v PP [1996] (SGHC) ‘It is settled law that if directors take risks which no director could honestly

believe to be taken in the interests of the company, such actions could well support allegations that the directors in question had acted in breach of their fiduciary duties to the company.’

**Intraco Ltd v Multi-Pak Singapore Pte Ltd [1995] ( SGCA ) ‘The proper test, I think, in the absence of actual separate consideration, must

be whether an honest and intelligent man in the position of a director of the company concerned, could, in the whole of the existing circumstances, have reasonably believed that the transactions were for the benefit of the company’

The language used, especially in Intraco , starts to hint at an objective test. However, what the court really means to say is that the fact that a director’s alleged belief appears to the court to be unreasonable may suggest that it was not in fact honestly held at the time of the alleged breach—but a breach will not be established unless the courtfinds as a fact that the director acted with a lack of bona fides.

o The policy reason is clear: “The court should be slow to interfere with commercial decisions taken by directors ...It should not, with the advantage of hindsight, substitute its own decisions in place of those made by directors in [their] honest and reasonable belief…Directors should not be coerced into exercising defensive commercial judgment, motivated largely by anxiety over legal accountability and consequences.” - Vita Health Laboratories Pte Ltd v Pang Seng Meng [2004, SGHC]

In summary, directors who make bad decisions may not breach fiduciary duties; but the more unreasonable the decision

was, the more likely courts are going to infer that it was not made in good faith.

2.1.2 In the interests of the company In the “interests of the company” is a rather amorphous

concept. Exactly which stakeholder’s interests should be considered?

o Members / shareholderso Employeeso Creditorso Community/ customers?

2.1.2.1 Situation A: Company is solvent and not on the brink of insolvencyShareholders as a general body In normal circumstances, the Dirs have to consider the

interests of the shareholders as a general body:

Chip Thye Enterprises Pte Ltd (in liq) v Phay Gi Mo [2004 , SGHC] o “Street CJ said: ‘In a solvent company the propriety interests of the

shareholders entitle them as a general body to be regarded as the company’

This generally translates into the act being commercially justifiable or one that furthers the prosperity of the Co. as a whole.

Can a Co. do charity? “Charity, has no business to sit at boards of directors” – seemed to

be the conventional view; In Parke v. Daily News Ltd [1962, EWHC], a Co’s decision to philanthropically give out large sums of money to its employees prior to insolvency was found to be unjustified.

However, the law has relaxed in this regard. s. 24 hasbeen enacted to deal with the very case in Parke, and s. 23(1)(b) has granted companies a right to make donations for charitable purposes. Also, s. 159 charges companies with the responsibility of looking at employees’ interests when making business decisions.

How wide/ narrow should “commercially justifiable” be interpreted? In a modern context, commercially justifiable does not

mean profit maximization in all cases. Hence, doing

charity may been seen as a way to improve the image ofa Co.

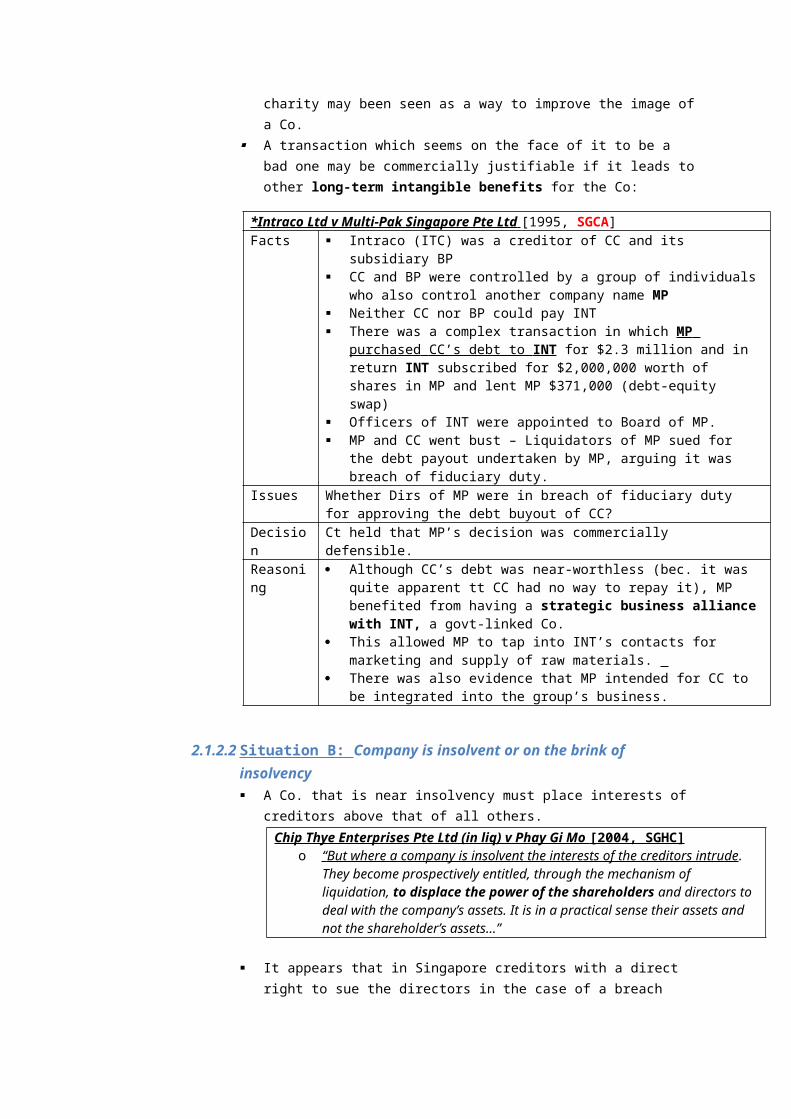

A transaction which seems on the face of it to be a bad one may be commercially justifiable if it leads toother long-term intangible benefits for the Co:

* Intraco Ltd v Multi-Pak Singapore Pte Ltd [1995, SGCA]Facts Intraco (ITC) was a creditor of CC and its

subsidiary BP CC and BP were controlled by a group of individuals

who also control another company name MP Neither CC nor BP could pay INT There was a complex transaction in which MP

purchased CC’s debt to INT for $2.3 million and in return INT subscribed for $2,000,000 worth of shares in MP and lent MP $371,000 (debt-equity swap)

Officers of INT were appointed to Board of MP. MP and CC went bust – Liquidators of MP sued for

the debt payout undertaken by MP, arguing it was breach of fiduciary duty.

Issues Whether Dirs of MP were in breach of fiduciary duty for approving the debt buyout of CC?

Decision

Ct held that MP’s decision was commercially defensible.

Reasoning

Although CC’s debt was near-worthless (bec. it was quite apparent tt CC had no way to repay it), MP benefited from having a strategic business alliancewith INT, a govt-linked Co.

This allowed MP to tap into INT’s contacts for marketing and supply of raw materials.

There was also evidence that MP intended for CC to be integrated into the group’s business.

2.1.2.2 Situation B: Company is insolvent or on the brink of insolvency A Co. that is near insolvency must place interests of

creditors above that of all others. Chip Thye Enterprises Pte Ltd (in liq) v Phay Gi Mo [2004, SGHC]

o “ But where a company is insolvent the interests of the creditors intrude . They become prospectively entitled, through the mechanism of liquidation, to displace the power of the shareholders and directors to deal with the company’s assets. It is in a practical sense their assets and not the shareholder’s assets…”

It appears that in Singapore creditors with a direct right to sue the directors in the case of a breach

(per Lai J. in Federal Express Pacific Inc v Meglis Airfreight Pte Ltd [1998, SGHC]).

o This is at odds with most other common law jurisdictions.

Duty is owed to both present and future creditors, hence Co. has to consider if decision will prejudice its ability to meet debts in future.

2.1.2.3 Situation C: Company is deeply divided among different factions When there is a distinct difference in the interest

between various shareholder factions in a solvent company the test is not a question of the interests ofthe company as a whole, but a question of what is fairas between different factions of shareholders .

Exception to the ‘interests of the Co. test’?

Tokuhon (Pte) Ltd v Seow Kang Hong (No 2) [ 2003, SGCA]o “In our judgment, the test of ‘the interest of the company’ would not be

the appropriate test to be applied in the present case....What we should be looking at is whether Mrs Seow had obtained any unfair advantage vis-à-vis the other two partners.”

2.1.2.4 Situation D: Company is part of a larger, legally-defined Group Theoretically, each company in a group is a separate

legal entity and therefore Dirs of that Co. is obligedto only consider how that Co. will benefit. But this position is practically untenable bec. the Dirs interests are often interwoven with the success of theGroup as a whole.

Hence, the SGCA’s answer is that directors may consider the interest of the group as a whole when making decisions as long as they do not sacrifice the interest of any company within the group .

Per Intraco : “Mr Bagnall for the bank contended that it is sufficient that the directors

of Castleford looked to the benefit of the group as a whole. Equally, I reject that contention. Each company in the group is a separate legal entity and the directors of a particular company are not entitled to sacrifice the interest of that company.”

Court found tt Dirs of MP had acted to benefit the Group as a whole and did not sacrifice MP in the process.

o The policy behind this is that if a parent Co. were tolet its subsidiary collapse, there could be grace repercussions for the entire Group.

Hence, it is possible for a parent to lend moneyto a subsidiary at nil interest or w no fixed repayment, in order to keep subsidiary afloat.

o Note that this is only for legally-defined groups ie. a holding Co. and its subsidiaries. Hence, even if Mr A is director of numerous companies, if they are not officially linked in a parent-subsidiary relationship,it would not hold.

How does one make a legally-recognised parent-subsidiary relationship??

2.2 Duty to Avoid Conflicts of interest The first thing that must be said is to note the wording of the

duty. It is not a duty to not conflict principal’s interest but a duty to avoid being in a position where there is a possibility of conflict.

The duty is strict (some have called it ‘inflexible’) and preventive in nature. (i) Strict

It is no excuse even if a company could not have or wouldnot have taken the transaction.

Even if Dir did not have any ulterior intention, he couldstill be liable if he was in a position where there was a possibility of conflict.

o Essentially, even the faintest whiff of improprietywill be censured.

Also, the Dir may be liable to indemnify the Co’s damageseven when Dir did not gain any profit or benefit from acting the way he did.

(ii) Preventive / like a prophylactic medication It is meant to lean toward disclosure whenever there is

doubt. It covers a wide area of possible situations where there

may be conflict. o It aims to make directors conduct themselves in an

entirely aboveboard manner. The juridical basis is expediency, and not morality:

Bray v. Ford [1896, HL]o “It does not appear to me that this rule is … founded upon principles

of morality. I regard it rather as based on the consideration that, human nature being what it is, there is danger, in such circumstances, of the person…being swayed by interest rather than

by duty…It has therefore been deemed expedient to lay down this positive rule.”

Often, this duty to avoid conflict overlaps with the duty to act in best interest of Co.

o If you place yourself in a position of conflict, you are not placing the best interests of the Co. at the forefront.

This Duty is embodied in 3 rules:(i) No conflict rule(ii) No secret profit and corporate opportunities rule(iii) No misappropriation of company assets rules

2.2.1 No Conflict Rule Directors cannot place themselves in situation where there

is a conflict with:(a) Their personal interests (eg. Co. involved in a

deal with another Co. where Dir has a stake); or(b) Interests of another principal (ie. ‘the double

employment rule’)

The test is simply whether a reasonable person would think that conflict is possible.

Boardman v Phipps [1967] 2 AC 46 (House of Lords) (Per Lord Upjohn) “The phrase ‘possibly may conflict’ requires consideration. In my view it means that the reasonable man looking at the relevant facts and circumstances of the particular case would think that there was a real sensible possibility of conflict; not that you could imagine some situation arising which might, in some conceivable possibility in events not contemplated as real sensible possibilities by any reasonable person, result in a conflict”

(a) Conflict with personal interests s. 156(1), (2) specifies when that conflict arises:

o When director is directly or indirectly interested in a transaction of the Co.; but only if it is a material interest.

The section does not define this ‘material interest’ but it states which situations are insufficient to deem a director as being materially interested: s. 156(2), (3)

Yeo Geok Seng v PP [2000] 1 SLR 195 “It appeared to me that the amount of shareholding which constitutes a material interest under s 156(2) of the Act may vary according to the facts of each case. In most instances, a controlling interest in a company would be a material interest and

would require disclosure. In this case, even if the appellant’s 50% shareholding in Triple Star was not a controlling interest, it was clearly a substantial shareholding bywhich he could influence the decisions of the company and thus constituted a material interest under s 156(2).”

This duty is discharged:o At general law , when the director has disclosed the

potential conflict + the Co. (ie. S/Hs in general meeting) has given the go-ahead.

o Under statute, when the director has declared the nature and specifics of his interest in the transaction to a meeting of the Board (s. 156(4))

CONFORMING WITH THE STATUTORY REQUIREMENTS OF DECLARATION (ie. s156) ONLY ABSOLVES CRIMINAL LIABILITY.

(b) Conflict with interests of another principal (s. 156(5)) This could come in the form of a Director being a

director of more than one company; or Nominee directors appointed by their principals (Double

employment rule)o The Dir is minimally obliged to declare his holding

of such other office that may put him in conflict.o At other times, he may be required to abstain from

voting if the particular decision is one where the two Co’s positions are misaligned

o In extreme cases, he may be required to resign one position.

Nominee Directors o WOON claims tt the CA ignores the appointment of

nominee directors. However, seeing that many nominee directors are employees of their principalswho sit on investee companies, it may arguably be caught by the ‘holding such office’ ambit of s. 156(5).

o In any case, the law does not forbid nominee directors serving two masters per se, but he/she cannot sacrifice the interests of the investee Co. in favour of the interests of his principal.

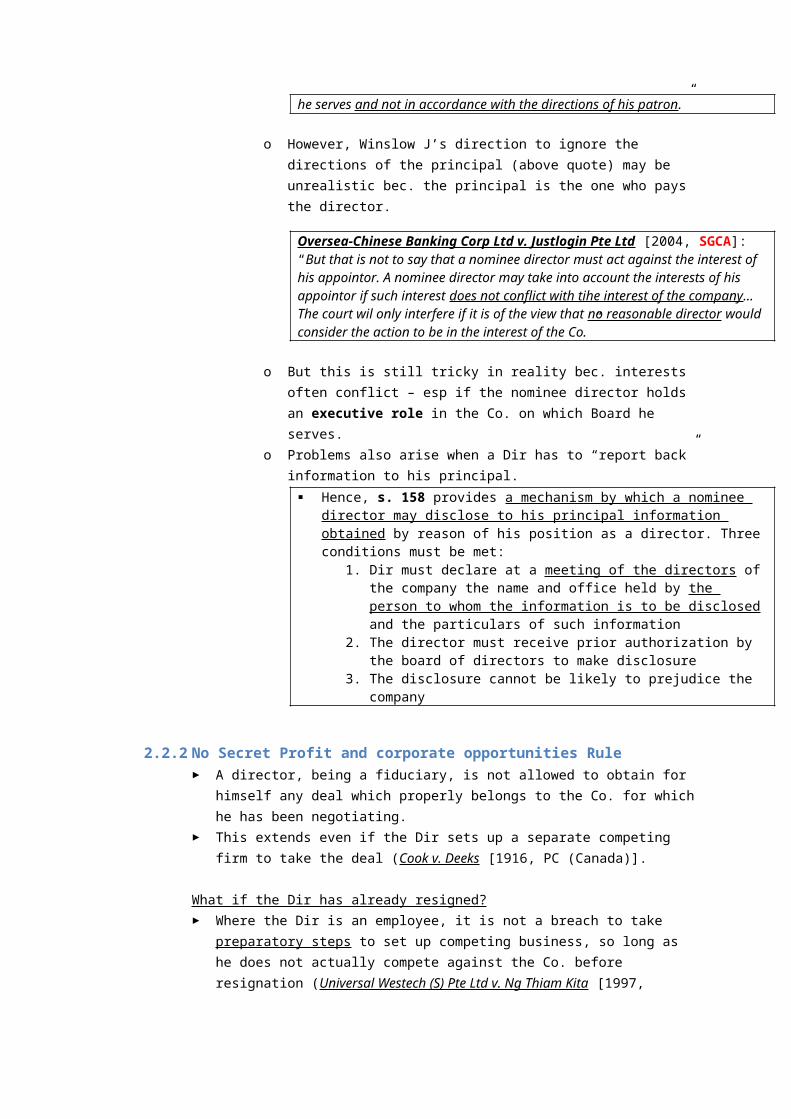

Raffles Hotel Ltd v. Rayner [1965, SGHC]: “A company is entitled to the undivided loyalty of its directors. A director who is a nominee…should exercise his best judgment in the interests of the company

he serves and not in accordance with the directions of his patron.”

o However, Winslow J’s direction to ignore the directions of the principal (above quote) may be unrealistic bec. the principal is the one who pays the director.

Oversea-Chinese Banking Corp Ltd v. Justlogin Pte Ltd [2004, SGCA]: “But that is not to say that a nominee director must act against the interest of his appointor. A nominee director may take into account the interests of his appointor if such interest does not conflict with tihe interest of the company…The court wil only interfere if it is of the view that no reasonable director would consider the action to be in the interest of the Co.”

o But this is still tricky in reality bec. interests often conflict – esp if the nominee director holds an executive role in the Co. on which Board he serves.

o Problems also arise when a Dir has to “report back”information to his principal.

Hence, s. 158 provides a mechanism by which a nominee director may disclose to his principal information obtained by reason of his position as a director. Threeconditions must be met:

1. Dir must declare at a meeting of the directors ofthe company the name and office held by the person to whom the information is to be disclosedand the particulars of such information

2. The director must receive prior authorization by the board of directors to make disclosure

3. The disclosure cannot be likely to prejudice the company

2.2.2 No Secret Profit and corporate opportunities Rule A director, being a fiduciary, is not allowed to obtain for

himself any deal which properly belongs to the Co. for whichhe has been negotiating.

This extends even if the Dir sets up a separate competing firm to take the deal (Cook v. Deeks [1916, PC (Canada)].

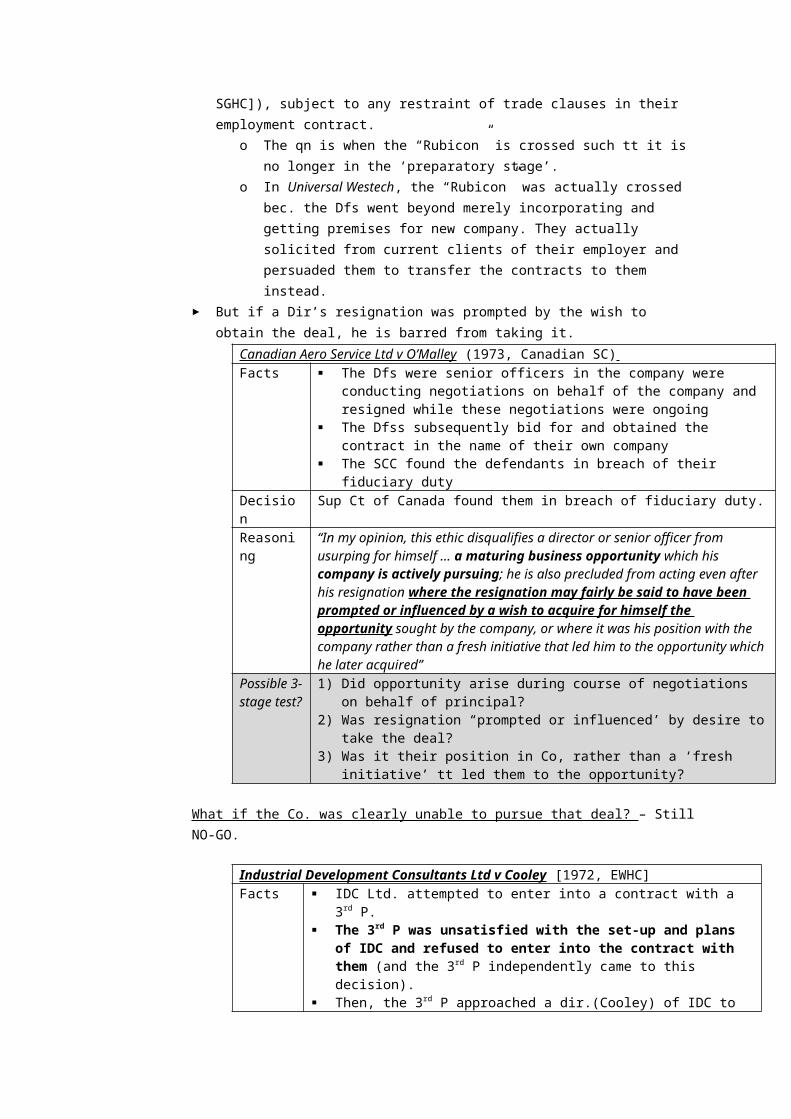

What if the Dir has already resigned? Where the Dir is an employee, it is not a breach to take

preparatory steps to set up competing business, so long as he does not actually compete against the Co. before resignation (Universal Westech (S) Pte Ltd v. Ng Thiam Kita [1997,

SGHC]), subject to any restraint of trade clauses in their employment contract.

o The qn is when the “Rubicon” is crossed such tt it is no longer in the ‘preparatory stage’.

o In Universal Westech, the “Rubicon” was actually crossed bec. the Dfs went beyond merely incorporating and getting premises for new company. They actually solicited from current clients of their employer and persuaded them to transfer the contracts to them instead.

But if a Dir’s resignation was prompted by the wish to obtain the deal, he is barred from taking it.

Canadian Aero Service Ltd v O’Malley (1973, Canadian SC) Facts The Dfs were senior officers in the company were

conducting negotiations on behalf of the company and resigned while these negotiations were ongoing

The Dfss subsequently bid for and obtained the contract in the name of their own company

The SCC found the defendants in breach of their fiduciary duty

Decision

Sup Ct of Canada found them in breach of fiduciary duty.

Reasoning

“In my opinion, this ethic disqualifies a director or senior officer from usurping for himself … a maturing business opportunity which his company is actively pursuing; he is also precluded from acting even after his resignation where the resignation may fairly be said to have been prompted or influenced by a wish to acquire for himself the opportunity sought by the company, or where it was his position with the company rather than a fresh initiative that led him to the opportunity which he later acquired”

Possible 3-stage test?

1) Did opportunity arise during course of negotiations on behalf of principal?

2) Was resignation “prompted or influenced’ by desire totake the deal?

3) Was it their position in Co, rather than a ‘fresh initiative’ tt led them to the opportunity?

What if the Co. was clearly unable to pursue that deal? – StillNO-GO.

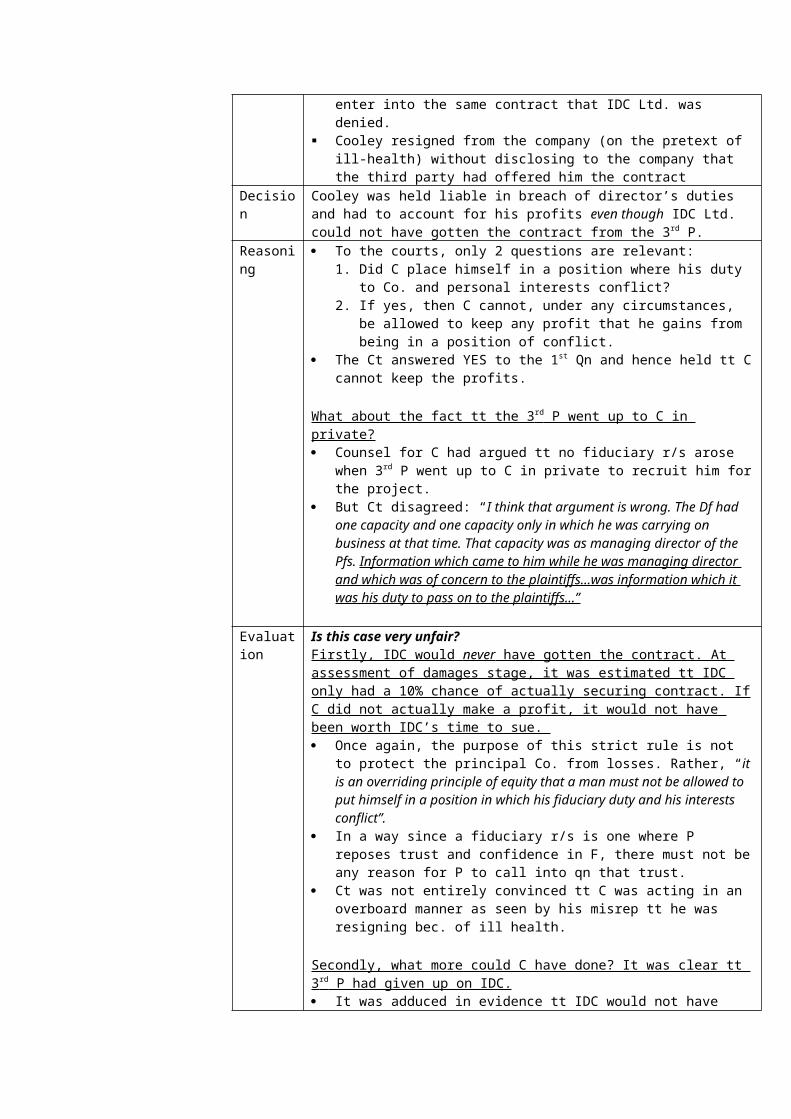

Industrial Development Consultants Ltd v Cooley [1972, EWHC]Facts IDC Ltd. attempted to enter into a contract with a

3rd P. The 3rd P was unsatisfied with the set-up and plans

of IDC and refused to enter into the contract with them (and the 3rd P independently came to this decision).

Then, the 3rd P approached a dir.(Cooley) of IDC to

enter into the same contract that IDC Ltd. was denied.

Cooley resigned from the company (on the pretext of ill-health) without disclosing to the company that the third party had offered him the contract

Decision

Cooley was held liable in breach of director’s duties and had to account for his profits even though IDC Ltd. could not have gotten the contract from the 3rd P.

Reasoning

To the courts, only 2 questions are relevant:1. Did C place himself in a position where his duty

to Co. and personal interests conflict?2. If yes, then C cannot, under any circumstances,

be allowed to keep any profit that he gains from being in a position of conflict.

The Ct answered YES to the 1st Qn and hence held tt Ccannot keep the profits.

What about the fact tt the 3 rd P went up to C in private? Counsel for C had argued tt no fiduciary r/s arose

when 3rd P went up to C in private to recruit him forthe project.

But Ct disagreed: “I think that argument is wrong. The Df had one capacity and one capacity only in which he was carrying on business at that time. That capacity was as managing director of the Pfs. Information which came to him while he was managing director and which was of concern to the plaintiffs…was information which it was his duty to pass on to the plaintiffs…”

Evaluation

Is this case very unfair?Firstly, IDC would never have gotten the contract. At assessment of damages stage, it was estimated tt IDC only had a 10% chance of actually securing contract. IfC did not actually make a profit, it would not have been worth IDC’s time to sue. Once again, the purpose of this strict rule is not

to protect the principal Co. from losses. Rather, “it is an overriding principle of equity that a man must not be allowed to put himself in a position in which his fiduciary duty and his interests conflict”.

In a way since a fiduciary r/s is one where P reposes trust and confidence in F, there must not beany reason for P to call into qn that trust.

Ct was not entirely convinced tt C was acting in an overboard manner as seen by his misrep tt he was resigning bec. of ill health.

Secondly, what more could C have done? It was clear tt 3 rd P had given up on IDC. It was adduced in evidence tt IDC would not have

given C their blessings if it was disclosed. Furthermore, since 3rd P was not happy with IDC’s

capability, perhaps C’s job was to spruce up that capability, rather than just leave. Maybe this strict duty imposes an obligation to improve your principal Co.

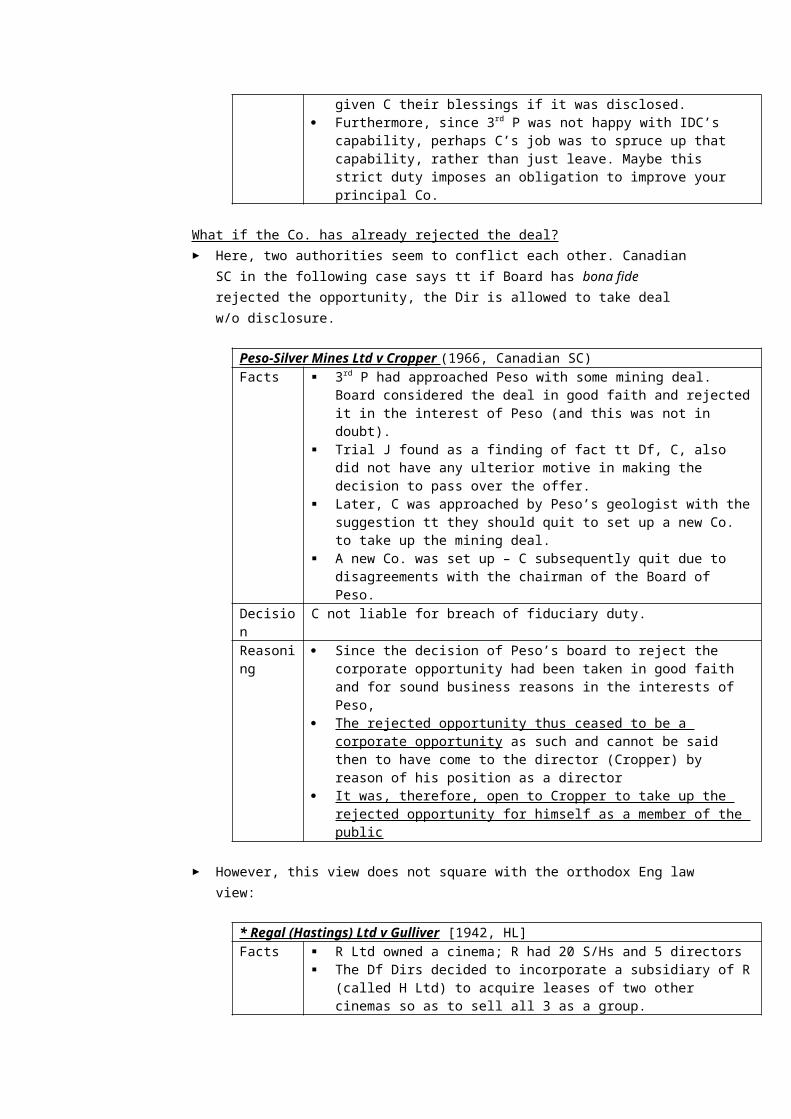

What if the Co. has already rejected the deal? Here, two authorities seem to conflict each other. Canadian

SC in the following case says tt if Board has bona fide rejected the opportunity, the Dir is allowed to take deal w/o disclosure.

Peso-Silver Mines Ltd v Cropper (1966, Canadian SC)Facts 3rd P had approached Peso with some mining deal.

Board considered the deal in good faith and rejectedit in the interest of Peso (and this was not in doubt).

Trial J found as a finding of fact tt Df, C, also did not have any ulterior motive in making the decision to pass over the offer.

Later, C was approached by Peso’s geologist with thesuggestion tt they should quit to set up a new Co. to take up the mining deal.

A new Co. was set up – C subsequently quit due to disagreements with the chairman of the Board of Peso.

Decision

C not liable for breach of fiduciary duty.

Reasoning

Since the decision of Peso’s board to reject the corporate opportunity had been taken in good faith and for sound business reasons in the interests of Peso,

The rejected opportunity thus ceased to be a corporate opportunity as such and cannot be said then to have come to the director (Cropper) by reason of his position as a director

It was, therefore, open to Cropper to take up the rejected opportunity for himself as a member of the public

However, this view does not square with the orthodox Eng lawview:

* Regal (Hastings) Ltd v Gulliver [1942, HL]Facts R Ltd owned a cinema; R had 20 S/Hs and 5 directors

The Df Dirs decided to incorporate a subsidiary of R(called H Ltd) to acquire leases of two other cinemas so as to sell all 3 as a group.

The owner of the two cinemas required that the paid-up capital of H to be at least 5000 pounds

R had invested 2000 pounds in H and could not affordmore

Four of the Df Dirs therefore subscribed for 500 pounds in shares each--with the remainder being taken up by R’s lawyer and some outsiders

Three weeks after the directors subscribed for the H’s shares, all of the shares of R and H were sold to a new owner

The directors made a huge profit on their H shares The directors of Regal were replaced by directors

representing the new owners and the new directors had Regal sue the old Regal directors (one of which was Gulliver)

The claim was that the old Regal directors had breached their duty and the profit that they made ontheir Hastings shares belonged to Regal

Decision

HL held the Df Dirs liable.

Reasoning

HL found that the defendant directors were all acting honestly and further that Regal did not have the money to invest in Hastings.

However, the directors breached their duty (of conflict) as the opportunity had come to them in their capacity as fiduciaries and they therefore could not take a secret profit or corporate opportunity

Lord Russell in obiter opined that if the defendant directors had wished to protect themselves they could have ratified the breach by a vote at the general meeting

“The rule of equity which insists on those, who by use of a fiduciary position make a profit, being liable to account for that profit, in no way depends on fraud, or absence of bona fides …or whether the plaintiff has infact been damaged or benefited by his actions. The liability arises from the mere fact of a profit having, in the stated circumstances, been made. The profiteer, however honest and well-intentioned, cannot escape the risk of being called upon to account”

“It is, however, not true that such a person is absolutely barred, because hecould by obtaining the assent of the shareholders have secured his freedom to make the profit for himself. Failing that, the only course open isto let the opportunity pass.”

Evaluation

Seems even more onerous than the Industrial Development case bec. the Dirs here probably did all this just so tt R could get a slice of the deal. They risked their buck so tt R could potentially profit.

Also, this was not a case where a 3rd P came to offer

a deal to the Co.; the Dirs thought up this deal to prosper the Co.

But perhaps the strictness is to ensure there is no excuse for disclosure, especially when it is only after the event tt Cts find the Dirs exercised bona fidein rejecting deals. Since, Dirs control whether the Board passes over the deal, perhaps too much power is vested if they are not required to disclose to S/Hs in general meeting?

o Then again, the facts of Regal suggest tt the directors had control over the majority of shares in the Co. anyway.

One last note: these cases show tt the No Conflict Rule is at times a different duty from the duty to place best interests of Co. first. In these cases, theDirs had the interests of the Co. first, yet they werefound liable. Arguably this is a stricter duty that the duty to place Co. foremost.

2.2.3 No Misappropriation of company assets Rule A director cannot use company property or take a corporate

opportunity for her own personal advantage or for the benefit of any third party

It is not open to the company in general meeting to ratify the misdeed and excuse the director from liability where thedirector has misappropriated corporate assets or opportunities from the company

This distinguishes “secret profit” from “misappropriation” cases

Cook v. Deeks – to be confirmed…

2.3 Duty to Employ Powers for proper purposes Directors are obligated to exercise the powers that they are given

and to use the company’s assets for the purpose they were intendedo It is no defence for a director to assert that she acted

bona fide in the interests of the company or was ignorant of the law if his actions were for “an improper purpose”

Most commonly arises in a hostile takeover situation in which directors via the M&A have been given a wide scope of authority toissue shares

o But this is somewhat limited by s 161 in Sgp (S/Hs in gen meeting must approve issuing of new shares)

A two part test may be used to establish a breach of the duty. Thecourt must

(1) Determine the limits within which the power can be exercised

(2) Decide whether the substantial purpose for which the power was exercised fell within those limits

In considering the purpose (or limits of the power) credit may be given to the bona fide opinion of the directors

Where there are two or more competing purposes underlying the exercise of a power, there will be a breach of duty if the impermissible purpose was causative in the sense that but for its presence the power would not have been exercised

o ie. the improper purpose was the cause for the power to be exercised.

Any decision concerning a particular exercise of a power will be in part a value judgment as to the “propriety” of a particular action in a particular context. This approach is not usually appropriate in company law, where we say that we do not second guess the decisions of the board of directors. It is a means to control fiduciary power.

*Howard Smith Ltd v Ampol Petroleum Ltd [1974, PC on appeal fr NSW]Facts M Ltd was a Co. caught in a takeover bid by both HS Ltd

and AM Ltd. Dirs of M believed it would be in the best interest of M

to be taken over by HS rather than AM. However, AM controlled sufficient shares in M to block

HS’s takeover bid. Thus, the Dirs of M decided to issue new shares to HS,

thereby diluting AM’s holdings to the pt where it could no longer block the takeover.

At trial, M’s Dirs testified tt they issued shares so asto raise capital for M; however trial J. found tt this was not their sole purpose.

Issue Was the power of the Dir’s to issue shares exercised for the proper purpose?

Decision

PC held tt the proper purpose for issuing shares was for raising money, but the Dirs had used it here to forestall atakeover bid instead. DECLARED the issue of new shares a nullity.

Reasoning

The factors that titled the court against the directors claim were Events leading up to the board meeting in question that

demonstrated the directors concern about the takeover The urgency with which the board meeting was called and

the shares were allotted The lack of information given to the board about the

capital needs of the company

The boards failure to consider the tax consequences of ashare issue versus a loan

The absence of a reason for why the rights issue was made to a particular party rather than all shareholders if the purpose was to raise capital

The PC accepted tt Dirs had an honest belief that control by the party whom shares were allotted was indeed in the company’s best interests. However, this serves as no defence to a claim of improper purpose.

Quare: What is the penalty for applying power for improper purpose? In the Howard Smith case, since Co. did not suffer loss and Dirs did not profit; what remedy is there?

2.4 Duty to Retain Discretions As fiduciaries, directors are required to actively exercise their

discretion before coming to a decision that they can honestly say is in the company’s interests

Therefore, directors cannot bind or fetter themselves to decide inany particular manner

E.g., agreeing to vote at board meetings in accordance with the direction of some other person

This duty is most relevant in the case of nominee directors Section 158 provides conditions for nominee or multiple directors

to disclose to his principal or other company information obtainedby reason of his position as a director.

3.“NEGLIGENCE DUTIES”/ DUTY OF CARE AND SKILL The second large component of Dir’s duties is the duty to not be

negligent. Insofar as the large component above calls into question the character of a director, this component pertains to the competence of a director.

o As such, it is natural tt the law looks at a host of factors, the more common ones being: (1) the nature of the Co. and S/Hs expectation of directors; (2) executive or non-executive director and (3) particular skill of that person.

First comparison: Traditional view vs. Modern view

TRADITIONAL MODERN

No. of duties

Treated as a single component

Treated as comprising 3 distinct components

Standard Purely subjective – Dirs.had to merely display only such competence as they themselves were capable of

Minimum objective standards—which is made more stringent (but not lowered) based on a director’s particular expertise and/or position in the company

Industrialattitude to directorship

Directors were commonly seen as mere figureheads of the company

Dirs. have a direct hand in management and even NEDs are seen as critical monitors of management

Second comparison: Executive vs. non-executive director.

EXCUTIVE DIRECTORS NON-EXEC DIRECTORSExpertise/Qualifications

Usually hired bec. they possess certain qualification or experience in the industry

No particular expertise or atleast they are very diverselyqualified. – Many are appointed bec. they are reputable names in commercialcircles.

Expectations from public andS/Hs

Hired to actually improveand direct management direction

Expected to be a “second pairof eyes” – esp. so for the Audit Committee.

Knowledge of Co’s affairs

Works for Co. and shd be familiar with day-to-day operations.

NEDs of many years’ appointment may still lack intimate knowledge of the CO’s affairs; Usually dependent on management to keep them informed.

Locus Classicus: The birth of negligence duties and traditional view

*Re City Equitable Fire Insurance Co Ltd. [1925, ECA] – Note tt this decision was before Donoghue v. Stevenson, hence tort of negligence wasn’t formally in existence then. Facts Co. lost £1.2m (which was unthinkable at that time),

owing to the frauds of the chairman of the Board, a one Bevan.

Liquidator sought to make the entire Board liable for (1) giving the chairman free rein to wreck such mischiefand (2) for allowing securities to be retained by the brokers.

Decision

HELD tt Dirs not liable bec. of provision in Articles tt exempts liability unless losses were caused by ‘their own willful neglect or default’.

Reasoni o While the court did not consider it as 3 distinct

ng duties, we see the standard expected of the traditional equivalent of the 3 modern duties:

1. Duty to exercise skill “A director need not exhibit in the performance of his duties a greater degree of skill than may reasonably be expected from a person of his knowledge and experience…[D]irectors are not liable for mere errors of judgment.”

2. Duty to take care “In respect of all duties that…may properly be left to some other official, a director is…justified in trusting that official to perform such duties honestly.”

How do Dirs. know whether they are justified in delegating?“It is the duty of each director [to see to the business of the Co.] except in sofar as the company’s articles of association may justify him in delegating that duty to others…That Bevan and Mansell were persons enjoying the highest reputation is beside the mark. If the shareholders had desired to leave hundreds of thousands of pounds of the Co’s money under the sole control of Bevan, they would have done so.”

3. Duty to be diligent “A director is not bound to give continuous attention to the affairs of his company. His duties are of an intermittent nature to be performed at periodical board meetings”

3.1 Duty to be skilful Must a director share his knowledge or use his particular skill-

sets in discharging his duty? From the outset, it was clear that the standard would differ btw

executive and non-exec directors:o Executive Dir. – obliged to share his skill or expertise

because he is usually under a contract of employment where he has promised to do so.

Held to standard of the objective body of knowledge and expertise possessed by those in the same calling (Permanent Building Society (in liq) v Wheeler (1994, SC of Western Aus).

o Non-Exec Dir – need not have any particular skill to be appointed.

Held only to the level of competence (or incompetence)that he really has.

Re Brazilian Rubber Plantations and Estates Ltd [1911, EWHC]“[A director] is, I think, not bound to bring any special qualifications to his office. He may

undertake the management of a rubber company in complete ignorance of everything connected with rubber, without incurring responsibilities for the mistakes which may result from such ignorance; while if he is acquainted with the rubber business he must give the company the advantage of his knowledge when transacting the company’s business.”

However, the law now seems to be a bit more strict toward NEDs. While the standard for them remains largely subjective, they are expected to at least take reasonable effort to become familiar with the affairs of the company.

o Does that mean tt NEDs have a duty to ensure they have the requisite skill to understand the Co’s business?

Commonwealth Bank of Australia v Frierich (1991) “[T]he stage has been reached when a director is expected to be capable of understanding his company’s affairs to the extent of actually reaching a reasonably informed opinion of its financial capacity…I think it follows that he is required by law to be capable of keeping abreast of the company’s affairs, and sufficiently abreast of them to act appropriately”

3.2 Duty to take care The question of standard of care has changed over the times.

Traditionally, the law employs a subjective standard – that of the level of knowledge and expertise possessed by that particulardirector.

However, the modern approach now subjects director to a minimum objective standard expected of a person discharging the responsibilities that the director has assumed. Of course, what that standard is depends on the structure of the Co. and what the Dir. Has held himself out to possess.

Daniels v Anderson [1995, NSW CA]“That duty will vary according to the size and business of the particular company and the experience or skills that the director held himself or herself out to have in support of appointment to the office.”

Lim Weng Kee v PP [2002,SGHC] – (Dir. of pawnshop allowed redemptionbef. Cheque cleared)“The law hence stands as thus: the civil standard of care and diligence expected of a director is objective , namely, whether he has exercised the same degree of care and diligence as a reasonable director found in his position. This standard is not fixed but a continuum depending on various factors such as the individual’s role in the company, thetype of decision being made, the size and the business of the company. However, it is important to note that, unlike the traditional approach, this standard will not be loweredto accommodate any inadequacies in the individual’s knowledge or experience. The standard will however be raised if he held himself out to possess or in fact possesses some special knowledge or experience.”

This duty to take care usually plays out in two areas: 1) Director must discover what his rights and obligations are

under the Arts and at law. – Ignorantia juris non excusat – While Dirdoes not need to be a legal expert, he is required to have general familiarity with what the law requires of him.

2) Directors may delegate their powers and can trust their delegates to do work properly in the absence of circumstances that would arouse the suspicion of a reasonable man. o Re National Bank of Wales [1899, ECA] – “Business cannot be carried on

upon principles of distrust. Men in responsible positions must be trusted by those above them…until there is reason to distrust them.”

o Directors are also entitled to trust their fellow directors.

Huckerby v. Elliot [1970, EWHC] – H charged with negligencefor failing to obtain gaming license for Co. tt ran agaming club – H knew little of the business and left the running to her co-director – Acquitted bec. she was entitled to trust her fellow director in the absence of any reason to doubt.

o Once a Dir. Has reason to suspect his delegate, he must make reasonable inquiries. In considering whether a Dir. ought to have suspected, once again we must look at the level of skill and experience tt the Dir. has and whether areasonable Dir. in the same position would have enquired.

Thus means tt the standard for Exec Dir. and NED may be quite different.

*Daniels v Anderson [1995, NSW CA]Facts AWA Ltd manufactured electronic products.

To manage their exposure, they set up an FX operation which was run by a single person (“Koval”) who combined the functions of trading, recording and settlement

K was effectively unsupervised and ran up massive liabilities

The board was concerned about the FX operations. In response to these concerns, the board was assured by management and by the auditor that all was well

It turned out that K was in fact losing money and concealing this fact from his supervisors and his activities caused substantial losses toAWA

The company sued its auditor for negligence. The auditor pleaded that the company had been contributorily negligent

Decisio HELD tt the non-executive directors had not been

n negligent under the circumstances but that the chairman/CEO was negligent

Reasoning

o Chairman of Board, H, was liable because he hadbasically lost control of his subordinates and left them to their own devices.

o This case illustrates quite plainly how the executive Dir was liable but not the NEDs.

3.3 Duty to be diligento This pertains to how much work directors are expected to put in. o The standard is objective, but different for executive directors

and NEDso Executive directors are expected to attend all meetings

(unless there is a good reason not to) and to give continuous attention to the affairs of the company

o NEDs are only expected to provide intermittent attention to the company

o The articles of most companies automatically disqualify directors if they are absent, without permission, from board meetings for a specific period (often six months).

o Another question is how this duty should be applied considering ttmany NEDs rely on subordinates to keep them informed of what is going on.

o WOON contends tt there is a significant different between not knowing because one’s subordinates kept the information back and not knowing because one was too busy to pay attention to what was going on.

s. 157 – Diligence only? o S. 157 states tt Dirs. are required to use “reasonable diligence”.

Does this refer to all 3 negligence duties above or only to the duty to be diligent?

o IN Lim Weng Kee v. PP, the CJ. was making reference to standardof “care and diligence” and didn’t’ seem to restrict it to any particular sub-duty.

o But in Byrne v Baker [1964, Aus SC], The Supreme Court of Victoria considered a provision

that was the predecessor to the provision on which s 157 is based. The court expressed the view that as theprovision only included the term ‘diligence’ and not care or skill that “what the legislature by the subsection is demanding of honest directors is diligence only”

o This position has not been adopted (but also has not been expressly rejected) in Singapore.

4.EFFECT OF A BREACH OF DIRECTOR’S DUTIESo Effect on transactions – (a) with 3rd P and (b) with that director

himself. o Liability of 3rd Ps o Remedies available to a Co.

4.1 Transactions with Dirs. who breach their fiduciary dutieso Transactions are voidable but not void. The Co. has the option of

affirming the contract, otherwise it can set aside the contract. o Also, there is no way the offending Dir. can get specific

performance. o Equitable principle tt a court will not assist a Dir. when he is

himself in breach of fiduciary duty (One who comes into equity must come with clean hands).

4.2 Transactions with 3rd Ps by Dirs. who breach their fiduciary dutyo Whether a Co. can set aside the transaction with a 3rd P depends on

whether 3rd P knew or ought to have known of the Dir’s breach of duty.

*Cheong Kim Hock v. Lin Securities (Pte) Ltd [1992, SGCA]A vendor was offered 3 times the mkt price for his property – CAheld tt he had notice (actual or constructive) of the breach of FD by the Dir. of the purchasing Co. bec. the vendor knew tt prop mkt was depressed and there was no way his prop could have fetched that price.He wilfully closed his eyes to the obvious suspicion tt the Dir.was cheating his Co.

o The basis for notice entitling the Co. to set aside the contract: Agency law Rogue Dir. has apparent authority until 3rd P has

or ought to have notice of the breach of authority. Otherwise, what is a breach of FD is a matter btw the Dir. and the Co.

Undue Influence A Dir. who breaches FD is akin to one who exerts undue influence on the Co. A 3rd P is entitled to assume that there is no UI until and unless he has notice (actual or constructive) of the UI.

o But the decision in Cheong Kim Hock does not stand for the principlett simply because I am getting a good deal, I should suspect a breach of fiduciary duty on the part of my counterpart. Such a position is commercially unfeasible.

o D & C Property Pte Ltd v. Four Seas Constructions Pte Ltd [1997, SGHC] – “As a general rule, commercial transactions cannot be property conducted on the basis that a person who is dealing with a company’s agent is, without more, obliged to take steps to convince himself that the agent in question is not breaching his fiduciary duty”

o This would penalise contracting parties for driving a hard bargain.

From Cheong Kim Hock: Liability is only attached where aperson “knows of circumstances sufficient to put him on inquiry”.

4.3 ‘Recipient liability’/ ‘Accessory liability’ of 3rd Pso Recipient liability – 3rd P is liable for receiving property

subject to a trust or fiduciary obligation and then passing it on,provided he knew that he was in possession of trust property OR heknew that he would be assisting someone pass on trust property.

o If prop is still in his hands, he is deemed to hold prop as constructive trustee. If passed on, 3rd P has to compensate the Co.

o Accessory liability 3rd P assisted or participated in the breachof duty by a fiduciary.

o Not dependent on receipt of trust property but so long as 3rd

P is deemed to act dishonestly. o He would either compensate Co. for losses or disgorge

profits.

Royal Brunei Airlines Sdn Bhd v. Tan Kok Ming [1995, PC (Brunei)]Elements to establish dishonest assistance:

(a)that there has been a disposal of his assets in breach of trust or fiduciary duty;

(b)in which the defendant has assisted or which she/he has procured;

(c)the defendant has acted dishonestly;(d)resulting loss to the claimant.

How is ‘dishonesty’ definedo Defendant must himself appreciate that what he was doing was

dishonest by the standards of honest and reasonable men. o Law will not find a defendant 'dishonest' in assisting in a

breach of trust if he knew of the facts which created the trust and its breach but had not been aware that what he was

doing would be regarded by honest men as being dishonest.

o “[t]he standard of what constitutes honest conduct is not subjective. Honesty is not an optional scale, with higher or lower values according to the moral standards of each individual"

4.4 Remedies available to a Co. 3 remedies available:i. Sue for damages (in case of negligence of breach of FD) /

return of a specific property (where there has beenmisapplication of Co property)

ii. Force Dir. to disgorge any secret profit (if any)iii. Declaration (in cases where Dir.’s exercise of power was not

for proper purpose) The choice btw (i) and (ii) is entirely the Co’s choice.

Generally, where the damage done is greater than any profit theDir. might have made, Co will sue for damages. Where there islittle damage done, then Co. will want Dir. to account for profitsinstead. Choice need only be made when time comes for judgement tobe entered in Co’s favour.

Proper Plaintiff (more in next topic) Per Foss v. Harbottle, members generally cannot sue Dir. for damage.

This is because a Co. is a separate entity from the members(theoretical reason) and also because usually the member suffersno additional damage other than the damage that the Co. suffers(practical reason).

Interlocutory remedies In the course of proceedings, s. 409A of CA allows Co. to apply to

court to restrain an ongoing transaction on the basis tt it wasentered into in breach of fiduciary duties.

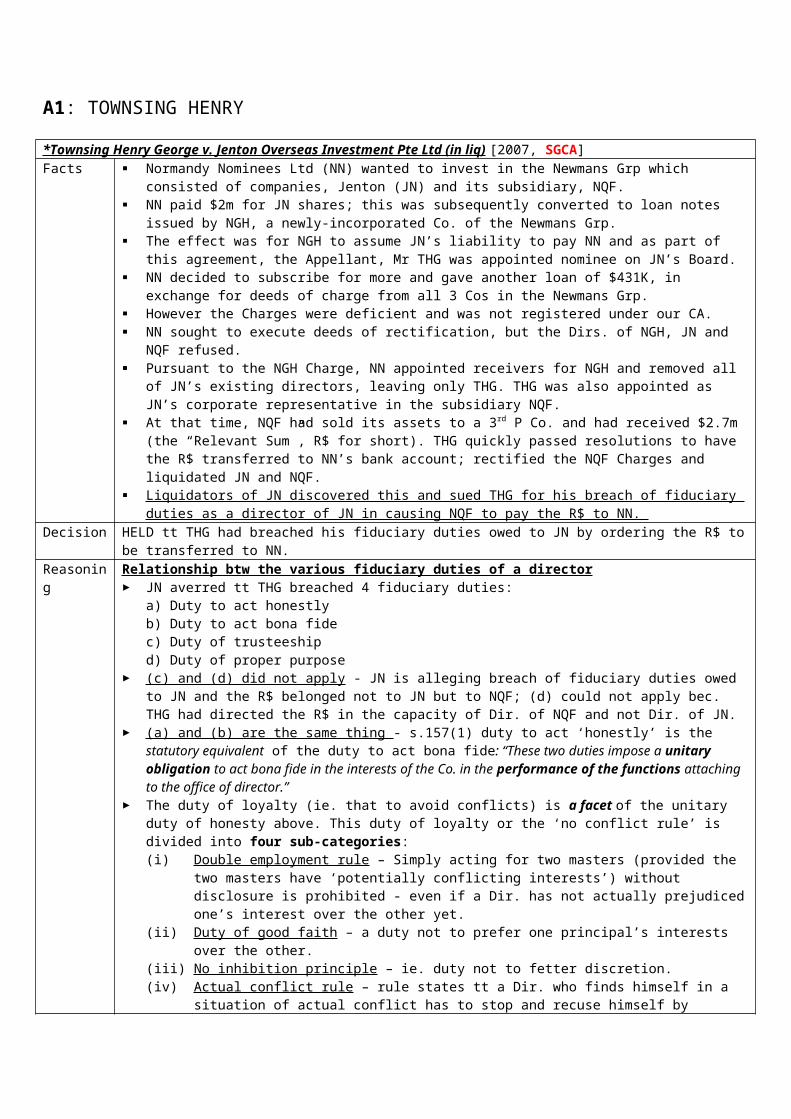

A1: TOWNSING HENRY

*Townsing Henry George v. Jenton Overseas Investment Pte Ltd (in liq) [2007, SGCA]Facts Normandy Nominees Ltd (NN) wanted to invest in the Newmans Grp which

consisted of companies, Jenton (JN) and its subsidiary, NQF. NN paid $2m for JN shares; this was subsequently converted to loan notes

issued by NGH, a newly-incorporated Co. of the Newmans Grp. The effect was for NGH to assume JN’s liability to pay NN and as part of

this agreement, the Appellant, Mr THG was appointed nominee on JN’s Board. NN decided to subscribe for more and gave another loan of $431K, in

exchange for deeds of charge from all 3 Cos in the Newmans Grp. However the Charges were deficient and was not registered under our CA. NN sought to execute deeds of rectification, but the Dirs. of NGH, JN and

NQF refused. Pursuant to the NGH Charge, NN appointed receivers for NGH and removed all

of JN’s existing directors, leaving only THG. THG was also appointed as JN’s corporate representative in the subsidiary NQF.

At that time, NQF had sold its assets to a 3rd P Co. and had received $2.7m (the “Relevant Sum”, R$ for short). THG quickly passed resolutions to have the R$ transferred to NN’s bank account; rectified the NQF Charges and liquidated JN and NQF.

Liquidators of JN discovered this and sued THG for his breach of fiduciary duties as a director of JN in causing NQF to pay the R$ to NN.

Decision HELD tt THG had breached his fiduciary duties owed to JN by ordering the R$ tobe transferred to NN.

Reasoning

Relationship btw the various fiduciary duties of a director JN averred tt THG breached 4 fiduciary duties:

a) Duty to act honestlyb) Duty to act bona fidec) Duty of trusteeshipd) Duty of proper purpose

(c) and (d) did not apply - JN is alleging breach of fiduciary duties owed to JN and the R$ belonged not to JN but to NQF; (d) could not apply bec. THG had directed the R$ in the capacity of Dir. of NQF and not Dir. of JN.

(a) and (b) are the same thing - s.157(1) duty to act ‘honestly’ is the statutory equivalent of the duty to act bona fide: “These two duties impose a unitary obligation to act bona fide in the interests of the Co. in the performance of the functions attaching to the office of director.”

The duty of loyalty (ie. that to avoid conflicts) is a facet of the unitary duty of honesty above. This duty of loyalty or the ‘no conflict rule’ is divided into four sub-categories:(i) Double employment rule – Simply acting for two masters (provided the

two masters have ‘potentially conflicting interests’) without disclosure is prohibited - even if a Dir. has not actually prejudicedone’s interest over the other yet.

(ii) Duty of good faith – a duty not to prefer one principal’s interests over the other.

(iii) No inhibition principle – ie. duty not to fetter discretion. (iv) Actual conflict rule – rule states tt a Dir. who finds himself in a

situation of actual conflict has to stop and recuse himself by

ceasing to act for one or preferably both parties. On the facts, (i) and (iii) were not breached bec. THG had JN’s consent

and knowledge that he was working for Newmans Grp and NN + THG did not act as if he was only acting in interest of JN or NQF.

However, he had breached (ii) and (iv).

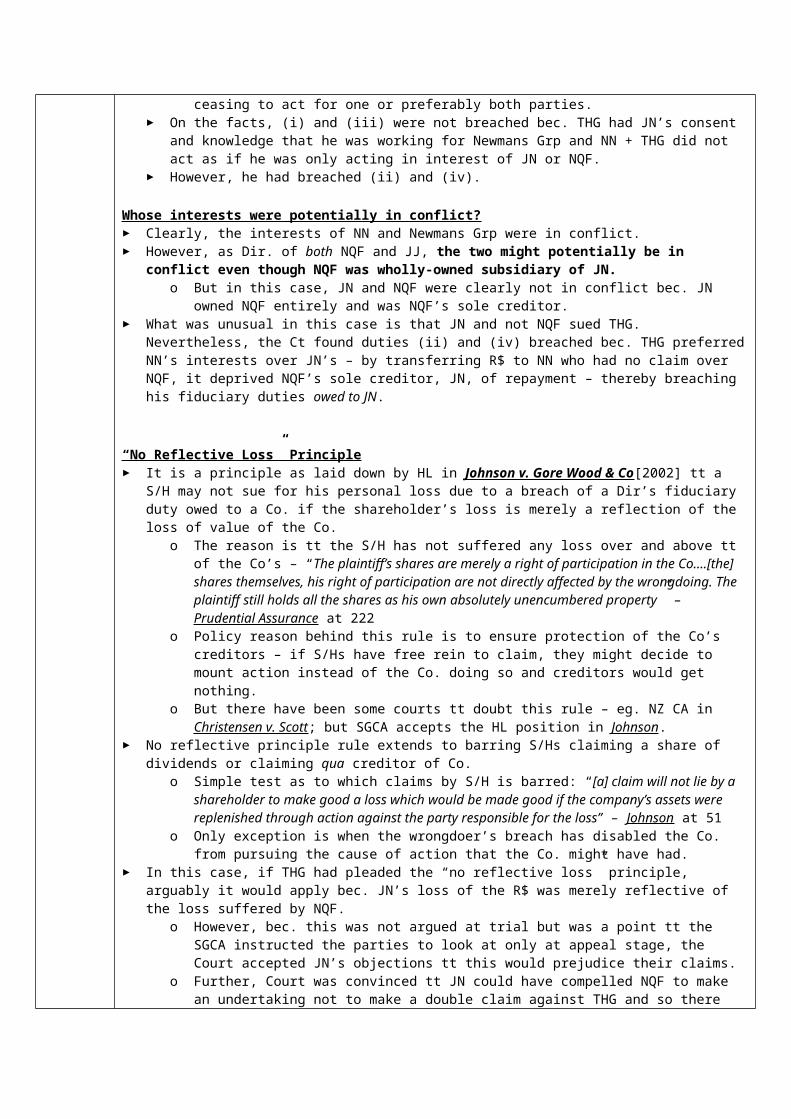

Whose interests were potentially in conflict? Clearly, the interests of NN and Newmans Grp were in conflict. However, as Dir. of both NQF and JJ, the two might potentially be in

conflict even though NQF was wholly-owned subsidiary of JN. o But in this case, JN and NQF were clearly not in conflict bec. JN

owned NQF entirely and was NQF’s sole creditor. What was unusual in this case is that JN and not NQF sued THG.

Nevertheless, the Ct found duties (ii) and (iv) breached bec. THG preferredNN’s interests over JN’s – by transferring R$ to NN who had no claim over NQF, it deprived NQF’s sole creditor, JN, of repayment – thereby breaching his fiduciary duties owed to JN.

“No Reflective Loss” Principle It is a principle as laid down by HL in Johnson v. Gore Wood & Co[2002] tt a

S/H may not sue for his personal loss due to a breach of a Dir’s fiduciary duty owed to a Co. if the shareholder’s loss is merely a reflection of the loss of value of the Co.

o The reason is tt the S/H has not suffered any loss over and above tt of the Co’s – “The plaintiff’s shares are merely a right of participation in the Co….[the] shares themselves, his right of participation are not directly affected by the wrongdoing. The plaintiff still holds all the shares as his own absolutely unencumbered property” – Prudential Assurance at 222

o Policy reason behind this rule is to ensure protection of the Co’s creditors – if S/Hs have free rein to claim, they might decide to mount action instead of the Co. doing so and creditors would get nothing.

o But there have been some courts tt doubt this rule – eg. NZ CA in Christensen v. Scott; but SGCA accepts the HL position in Johnson.

No reflective principle rule extends to barring S/Hs claiming a share of dividends or claiming qua creditor of Co.

o Simple test as to which claims by S/H is barred: “[a] claim will not lie by a shareholder to make good a loss which would be made good if the company’s assets were replenished through action against the party responsible for the loss” – Johnson at 51

o Only exception is when the wrongdoer’s breach has disabled the Co. from pursuing the cause of action that the Co. might have had.

In this case, if THG had pleaded the “no reflective loss” principle, arguably it would apply bec. JN’s loss of the R$ was merely reflective of the loss suffered by NQF.

o However, bec. this was not argued at trial but was a point tt the SGCA instructed the parties to look at only at appeal stage, the Court accepted JN’s objections tt this would prejudice their claims.

o Further, Court was convinced tt JN could have compelled NQF to make an undertaking not to make a double claim against THG and so there

was no chance of double-recovery. There was thus no reason to strike out the claim and force NQF to mount the action instead

Hence, “no reflective loss” principle was not applied. Impt points

A parent and its subsidiary’s interests are usually aligned but not always so. A Dir. of both will be in breach if he sacrifices one’s interests over the other, even if it may be in the best interest of the entire Group.

A2: REGAL HASTINGS

* Regal (Hastings) Ltd v Gulliver [1942, HL]Facts Facts above, at p. 9Reasoning

Ratification

Impt points