Embed Size (px)

Citation preview

KeitH McCulLoUghWITH RiCH BLAKE

McCullOUghBLake

KEITH MCCULLOUGH is the founder of Research Edge, a provider of independent securities markets research that has become the go-to source for analysis and trade recommendations among savvy money managers. He is also a Bloomberg TV Contributing Editor. McCullough started in the business in 1999 as an equity analyst at Credit Suisse First Boston. From there, he ran assets for Dawson-Herman Capital Management’s Millennium Fund, and then launched his own fund, Falcon Henge Partners LLC, which was integrated in to Magnetar Capital. He then moved on to become a portfolio manager at Carlyle–Blue Wave until 2007. McCullough is a graduate of Yale University and also former captain of the Yale hockey team.

RICH BLAKE was the cofounder and executive editor of Trader Monthly magazine. He frequently contributes to CNBC’s Power Lunch and to Alphaand Portfolio magazines. Prior to the launch of Trader Monthly, Blake wrote for Institutional Inves-tor. He is the author of two books, The Day Donny Herbert Woke Up and Talking Proud: Rediscovering the Magical Season of the 1980 Buffalo Bills.

J A C K E T D E S I G N : M I C H A E L J . F R E E L A N D

$29.95 USA / $35.95 CAN

Diary of a Hedge Fund Manager is an insider’s view of the high-stakes money management world. In a distinctly straightforward and, at times, humorous style, Keith McCullough

and Rich Blake take you on the journey of a young and successful hedge fund manager and former junior hockey player from Thunder Bay, Ontario, as he gets recruited to the Ivy League, stumbles onto the nexus of the hedge fund universe, and then gets a crack at running his own pile—becoming one of the best young portfolio managers on the Street.

But when the young portfolio manager fi nds himself working for one of the world’s most prestigious fi rms—helping to run their hedge fund operation just as the market is starting to crack in 2007—McCullough becomes a lonely voice of reason in a world that rewards groupthink and disregards the adage about past performance having no bearing on future results. When McCullough fi nds himself shown the door, the story takes a fascinating turn into the world of independent research and no-holds-barred criticism.

Page by page, this fast-paced ride through the world of hedge funds reveals the unvarnished truth of how Wall Street and hedge funds really operate and offers real-world investment lessons you can take away and put to good use.

Written with the authority of someone who knows how Wall Street and hedge funds work, yet accessible to even a casual follower of fi nance, Diary of a Hedge Fund Manager mixes a constructive critique of the investment industry with fundamental lessons that any investor will fi nd valuable.

O V E R A L L M A T T E F I N I S H

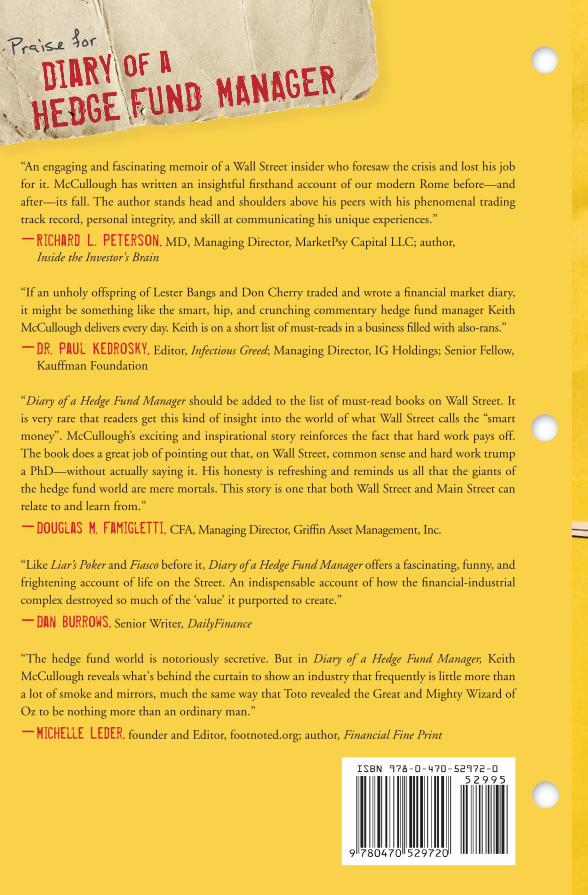

“An engaging and fascinating memoir of a Wall Street insider who foresaw the crisis and lost his job for it. McCullough has written an insightful fi rsthand account of our modern Rome before—and after—its fall. The author stands head and shoulders above his peers with his phenomenal trading track record, personal integrity, and skill at communicating his unique experiences.”

— Richard L. Peterson, MD, Managing Director, MarketPsy Capital LLC; author, Inside the Investor's Brain

“If an unholy offspring of Lester Bangs and Don Cherry traded and wrote a fi nancial market diary, it might be something like the smart, hip, and crunching commentary hedge fund manager Keith McCullough delivers every day. Keith is on a short list of must-reads in a business fi lled with also-rans.”

— Dr. Paul Kedrosky, Editor, Infectious Greed; Managing Director, IG Holdings; Senior Fellow, Kauffman Foundation

“Diary of a Hedge Fund Manager should be added to the list of must-read books on Wall Street. It is very rare that readers get this kind of insight into the world of what Wall Street calls the “smart money”. McCullough’s exciting and inspirational story reinforces the fact that hard work pays off. The book does a great job of pointing out that, on Wall Street, common sense and hard work trump a PhD—without actually saying it. His honesty is refreshing and reminds us all that the giants of the hedge fund world are mere mortals. This story is one that both Wall Street and Main Street can relate to and learn from.”

— Douglas M. Famigletti, CFA, Managing Director, Griffi n Asset Management, Inc.

“Like Liar’s Poker and Fiasco before it, Diary of a Hedge Fund Manager offers a fascinating, funny, and frightening account of life on the Street. An indispensable account of how the fi nancial-industrial complex destroyed so much of the ‘value’ it purported to create.”

—Dan Burrows, Senior Writer, DailyFinance

“The hedge fund world is notoriously secretive. But in Diary of a Hedge Fund Manager, Keith McCullough reveals what's behind the curtain to show an industry that frequently is little more than a lot of smoke and mirrors, much the same way that Toto revealed the Great and Mighty Wizard of Oz to be nothing more than an ordinary man.”

—Michelle Leder, founder and Editor, footnoted.org; author, Financial Fine Print

ffirs.indd iiffirs.indd ii 11/17/09 9:37:38 AM11/17/09 9:37:38 AM

i

Diary of a Hedge Fund Manager

ffirs.indd iffirs.indd i 11/17/09 9:37:37 AM11/17/09 9:37:37 AM

ffirs.indd iiffirs.indd ii 11/17/09 9:37:38 AM11/17/09 9:37:38 AM

iii

Diary of a Hedge Fund Manager

From the Top, to the Bottom, and Back Again

KEITH MCCULLOUGH WITH

RICH BLAKE

John Wiley & Sons, Inc.

ffirs.indd iiiffirs.indd iii 11/17/09 9:37:38 AM11/17/09 9:37:38 AM

Copyright © 2010 by Keith McCullough and Rich Blake. All rights reserved.

Published by John Wiley & Sons, Inc., Hoboken, New Jersey.Published simultaneously in Canada.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as permitted under Section 107 or 108 of the 1976 United States Copyright Act, without either the prior written permission of the Publisher, or authorization through payment of the appropriate per-copy fee to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, (978) 750-8400, fax (978) 750-4470, or on the web at www.copyright.com. Requests to the Publisher for permission should be addressed to the Permissions Department, John Wiley & Sons, Inc., 111 River Street, Hoboken, NJ 07030, (201) 748-6011, fax (201) 748-6008, or online at http://www.wiley.com/go/permissions.

Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best efforts in preparing this book, they make no representations or warranties with respect to the accuracy or completeness of the contents of this book and specifi cally disclaim any implied warranties of merchantability or fi tness for a particular purpose. No warranty may be created or extended by sales representatives or written sales materials. The advice and strategies contained herein may not be suitable for your situation. You should consult with a professional where appropriate. Neither the publisher nor author shall be liable for any loss of profi t or any other commercial damages, including but not limited to special, incidental, consequential, or other damages.

For general information on our other products and services or for technical support, please contact our Customer Care Department within the United States at (800) 762-2974, outside the United States at (317) 572-3993 or fax (317) 572-4002.

Wiley also publishes its books in a variety of electronic formats. Some content that appears in print may not be available in electronic books. For more information about Wiley products, visit our web site at www.wiley.com.

Library of Congress Cataloging-in-Publication Data:

McCullough, Keith, 1975–

Diary of a hedge fund manager : from the top, to the bottom, and back again / Keith McCullough with Rich Blake. p. cm. Includes index. ISBN 978-0-470-52972-0 (cloth) 1. Hedge funds. 2. Investment advisors. I. Blake, Rich, 1968– II. Title. HG4530.M39 2010 332.64�524–dc22

2009035907

Printed in the United States of America

10 9 8 7 6 5 4 3 2 1

ffirs.indd ivffirs.indd iv 11/17/09 9:37:38 AM11/17/09 9:37:38 AM

For Jack

ffirs.indd vffirs.indd v 11/17/09 9:37:38 AM11/17/09 9:37:38 AM

ffirs.indd viffirs.indd vi 11/17/09 9:37:38 AM11/17/09 9:37:38 AM

vii

Contents

Introduction 1

Chapter 1: Catch a Wave 9Chapter 2: Shipping Out 17Chapter 3: Welcome to the Jungle 29Chapter 4: Snapshots from the Dot.Com Bubble 39Chapter 5: Discovery 61Chapter 6: Flying with the Giants 79Chapter 7: Shifting for Myself 97Chapter 8: Sucked In 115Chapter 9: Worlds Collide 123Chapter 10: Exile on Wall Street 139Chapter 11: Lifting the Curtain 157Chapter 12: The Great Squeeze 185

Epilogue 197Acknowledgments 205About the Authors 207Index 209

ftoc.indd viiftoc.indd vii 11/17/09 9:38:19 AM11/17/09 9:38:19 AM

ftoc.indd viiiftoc.indd viii 11/17/09 9:38:19 AM11/17/09 9:38:19 AM

1

Introduction

My fi nal day in the hedge fund business was Friday, November 2, 2007. I ’ d enjoyed nearly a nine - year run on Wall Street, fi rst as a junior analyst at Credit Suisse First Boston before landing on

the buyside, working for hedge fund pioneer Jon Dawson, and then eventually co - founding a hedge fund with my partner, Harry Schwefel. Our fund was later absorbed into multi - billion - dollar Magnetar Cap-ital. My last - ever hedge fund job was running money as a Portfolio Manager and Managing Director at Carlyle - Blue Wave Partners.

At the time I worked at Carlyle - Blue Wave (February through November of 2007), the Carlyle Group — already well known around the world for its private equity prominence — was pushing into the hedge fund business. Its new hedge fund arm, Blue Wave, a joint venture with two ex - Deutsche Bank executives, made me Partner and gave me a seat on the fund ’ s Investment Committee, represent-ing the Long/Short Equity side of the business.

On the morning of what would turn out to be my last day in the business, I ducked out of our Midtown offi ce right before noon

cintro.indd 1cintro.indd 1 11/17/09 9:36:38 AM11/17/09 9:36:38 AM

2

and walked down Fifth Avenue to buy a new pair of black loafers. The soles of the ones I had on weren ’ t exactly worn out and might have even lasted me another six months, but with my son Jack due to be born in the coming week, I felt it was time to start the next chapter of my life.

So did my bosses at Carlyle - Blue Wave. Later that afternoon I was told I was being let go. My days

trading a “ book ” for a hedge fund were over. I packed up my personal belongings, books, fi les, and notebooks into a couple of cardboard boxes, but I left my old shoes in the offi ce. When those dusty loafers were mailed to me a month later, I had already forgotten about them.

But I smiled.

■ ■ ■

During my brief time at Carlyle - Blue Wave, the fi rst cracks in private equity and in hedge funds — and in the fi nancial markets in general — were starting to manifest. The widening subprime mortgage crisis was starting to dominate the fi nancial press. It was clear, to me anyway, that a top had been reached and probably surpassed. My fi nal month of trading on Wall Street was a profi table one. My shorts were fi nally beginning to work out. But there was just no denying that I had turned in an unprofi table third quarter of 2007. Although the market took a nosedive in the early part of that August, it whipsawed right back up again later in the month and into September. In the end I ’ d been too bearish, too soon. Now I was being shown the door.

I had enjoyed the ride, made my eight fi gures, notched positive returns in 21 of 24 quarters. Still, unless you run the place, the hedge fund business is about being right each and every quarter. Being right early is called being wrong. But it seemed my last “ call, ” on the global market and on the asset management industry, was turning out to be right after all.

i n t r o d u c t i o n

cintro.indd 2cintro.indd 2 11/17/09 9:36:38 AM11/17/09 9:36:38 AM

3

As my hedge - fund trading days came to a close in the autumn of 2007, the seeds of a new type of real - time research fi rm — something akin to a virtual hedge fund — took root in a fi nancial blog I had begun writing. My audience at fi rst included a few friends and former colleagues from the Street, but I mostly wrote for myself. For years, I ’ d diarized all of my investment decisions, logging observations and data points meticulously into 10 × 7 7/8 inch collegiate style composition notebooks, marble covered, 100 sheets per notebook. With spare time no longer a scarcity, I started writing every day, often recalling my experiences as an analyst and as a fund manager.

And I kept making calls on markets, and wrote about them, to keep an on - the - record hand in the game. One day, when my son was old enough, I could show him that in the last game Dad ever played as a hedge fund manager he got kicked off the team when an MVP trophy would have been more appropriate.

Having closed on October 9, 2007, at a record high of 1565.15, * the S & P 500 reached 1576.09, intra - day, on October 11, before entering the initial stage of what would be a monumental decline. Convinced the worst was yet to come, I began sharing my market views with anyone who cared to read them. I published a blog, MCM Macro, my token attempt to bring some semblance of transparency to the investing world, starting with publishing every call I was making and articulating the reasons why. Every call is still up there on that site. I made short - term, and longer - term forecasts, always owning up to miscues, always an open book insofar as my rationale was concerned. Never that strong a writer, I was fi nding I enjoyed it, looked forward to it, and tried to improve. I wrote constantly. I wrote from a position of truth. I had no agenda other than to chronicle my process and thoughts. No such “ open book ” existed in the hedge fund world, or for that matter at the large

*According to FactSet Research Systems Inc.; all of the market and securities data contained in this book, in fact, came from FactSet.

Introduction

cintro.indd 3cintro.indd 3 11/17/09 9:36:38 AM11/17/09 9:36:38 AM

i n t r o d u c t i o n

4

banks and investment brokerage houses that sell research. In a market growing more perilous by the day, I was now giving former colleagues, family members, and friends full access to my portfolio management process. They saw every call in real time. In an industry that needed to creatively destruct before it could truly change, I felt like I would do my small part by being accountable in the meantime, even if I was merely a virtual Portfolio Manager.

On Tuesday, April 1, 2008, I posted a three - month perform-ance report for my MCM Macro model portfolio: +2.2 per-cent, compared to – 10 percent for the S & P 500 and – 14 percent for the Nasdaq. Along with a few partners, I offi cially opened the doors of Research Edge, my new fi rm, that month in New Haven, Connecticut, in a restored mansion once owned by hefty ex - U.S. President William Howard Taft, just a short walk from the Yale University campus.

As it turns out, my idea for a fresh approach to investment research had some heft of its own. I ’ ve since hired some 30 full - time employees, many of them former hedge fund analysts, including a few ex - Blue Wavers, at a time when the Street was laying off thou-sands. The roster of buyside fi rms that have regularly come to rely on our research has swelled from just a few to more than 100.

■ ■ ■

Why this book? Why now? Since leaving Wall Street to do real - time macro research, the

facts have largely played out on my side of the macro calls, calls that sorely needed to be made. I don ’ t think there was any remarkable genius to my viewpoints; oncoming fi nancial catastrophe was readily apparent to anyone who was allowed to be objective.

Unfortunately, the hedge fund business pays a higher multiple for short - term performance than it does long - term adherence to principles.

cintro.indd 4cintro.indd 4 11/17/09 9:36:38 AM11/17/09 9:36:38 AM

Introduction

5

We ’ re only now seeing the ugly side of that reality. Wall Street ’ s latest cycle of earnings gamesmanship and off - the - charts leveraging constituted an ambitious compensation mousetrap, not a sustainable business model.

When former Trader Monthly (now defunct) executive editor Rich Blake and I embarked on the early brainstorming for what would become this book, around December 2008, the timing and collaboration felt right. Wall Street was on its knees. Bernie Madoff was exposed. Rich and I both agreed our overriding goal would be to provide a stark, insider ’ s view of the hedge fund world, famously secretive and not well understood. Criticism would be meted out with context.

While the hedge fund industry has just gone through a signifi cant shakeout, we expect even more contraction going forward. Assets in hedge funds, once estimated to be as high as $ 2.9 trillion in the second quarter of 2008, dipped to $ 1.8 trillion as of the second quarter of 2009, according to HedgeFund.net . On average, hedge funds lost 18.3 percent in 2008, according to Hedge Fund Research. Many funds faced an onslaught of redemptions and requests for redemptions and, factoring in both outfl ows and investment losses, saw their assets cut in half during the fi nancial crisis. Looking at the deep end of the pool, some 268 U.S. - based hedge fund management companies had at least $ 1 billion in assets as of July 1, 2008, controlling a collective $ 1.68 trillion, according to Hedge Fund Intelligence. The number of U.S. - based management companies with at least $ 1 billion in hedge fund assets had, by the second quarter of 2009, dipped to 218 companies controlling a collective $ 1.13 trillion, according to HFI. HedgeFund.net ’ s database of individual funds with at least $ 100 million under management numbered 1,748 in June 2008; in June 2009, HFN said there were only 1,129 funds that big. At one point prior to the market meltdown, the total number of hedge funds was believed to have exceeded 10,000, according to HFN. Likely there were even more

cintro.indd 5cintro.indd 5 11/17/09 9:36:38 AM11/17/09 9:36:38 AM

i n t r o d u c t i o n

6

individual funds, or limited partnerships (LPs), than the estimates could capture when one considers enigmatic offshore vehicles. Hedge Fund Research says 1,471 hedge funds liquidated in 2008, with 778 of those happening in the fourth quarter alone. That ’ s a 15 percent lop off. Another 668 funds liquidated in the fi rst half of 2009, according to HFR. While performance seems to be turning around at some funds, and new vehicles are always starting up, I still would not be surprised if another 10 to 15 percent of all hedge funds shuttered over the next year or so. I would not be surprised if such a pace of hedge fund shuttering continues in 2010.

For those who are still specifi cally working at hedge funds, and in the fi nancial industry in general, who survives and who thrives will depend on who among the pack most enthusiastically embraces principles and sound practices, old - fashioned concepts such as putting customers fi rst, no matter what. Now is the time to look in the mirror and rebuild the trust that has been destroyed. Work ethic and handshakes are important to me. I think they are to other people, too. Accountability and trust are transcending “ trends. ” I believe these trends are just now taking hold and that the U.S. fi nancial system is headed in a new direction.

Just as politics were transformed by YouTube and Twitter, so too will the fi nancial markets as they inevitably succumb to unprece-dented transparency. From Madoff to AIG, fi nancial cataclysm has drastically changed the way the industry is perceived. The barn door has been blown off its hinges, and the public at large continues to stare inside with disbelief.

Some 92 million Americans have money invested in mutual funds, according to the Investment Company Institute. Around 62 million Americans participate in some form of retirement plan, according to the Employee Benefi t Research Institute. An estimated 47 percent of American households, or 54.5 million households, have some form of ownership of stock or bonds, according to a joint study done by the ICI and the Securities Industry and Financial

cintro.indd 6cintro.indd 6 11/17/09 9:36:39 AM11/17/09 9:36:39 AM

Introduction

7

Markets Association. Has anyone from Wall Street told them any-thing about the fi nancial meltdown that they can understand? Or believe?

No matter what you glean from reading about my experiences, I trust you can see that the highs, lows, and lessons of a hedge fund manager are of no greater signifi cance than those of any other pro-fession. We all share the same intrinsic motivations, in work, and, for that matter, in life: to create; collaborate; meet challenges; take worthwhile risks, and avoid unnecessary ones. Money may or may not be the root of all evil, but we all crave validation. We all get up every morning hoping that everyone else is doing the right thing when nobody is looking. What follows is a glimpse, mine, of what hedge funds were doing during this past decade.

Keith R. McCullough CEO, Research Edge

New Haven, Connecticut Third Quarter 2009

cintro.indd 7cintro.indd 7 11/17/09 9:36:39 AM11/17/09 9:36:39 AM

cintro.indd 8cintro.indd 8 11/17/09 9:36:39 AM11/17/09 9:36:39 AM

9

Chapter 1

Catch A Wave

c01.indd 9c01.indd 9 11/17/09 9:38:56 AM11/17/09 9:38:56 AM

c01.indd 10c01.indd 10 11/17/09 9:38:56 AM11/17/09 9:38:56 AM

11

The recruiter ’ s message was garbled and vague: Large, well - known private equity player looking to launch multi - strategy hedge fund. It was late November 2006. I already worked for a large,

well - known hedge fund fi rm, Magnetar Capital. Magnetar was launched in April 2005 by a 39 - year - old numerical savant named Alec Litowitz, formerly the Head of Equities at Citadel Investment Group and considered to be a master of merger arbitrage. Litowitz had joined forces with ex - Glenwood Capital Partners president Ross Laser. Man Group Plc had acquired Glenwood in 2000, pro-ducing a nice windfall for Laser; Litowitz, meanwhile, had been producing handsome profi ts at Citadel. Together, the two set up headquarters in Evanston, Illinois, outside Chicago and not far from Northwestern University. Magnetar opened its doors for business with $ 1.7 billion in assets under management. At the time, it was one of the largest hedge fund startups ever. Less than two years later

c01.indd 11c01.indd 11 11/17/09 9:38:56 AM11/17/09 9:38:56 AM

d i a r y o f a h e d g e f u n d m a n a g e r

12

Magnetar ’ s assets neared $ 4 billion, it had expanded its reach to open offi ces in New York and London, and it was charging after numerous forms of portfolio strategies not limited to merger arb or equities.

Around the time Magnetar was forming, I launched, along with my partner Harry Schwefel, a hedge fund management com-pany called Falconhenge Partners, and a fl agship hedge fund of the same name. We put up some impressive numbers, which eventually came to the attention of Laser, who proposed folding our team into Magnetar. Laser wasn ’ t alone in his pursuit during the fi rst half of 2006. Dan Och of Och - Ziff Capital Management was also court-ing Harry and me. Deciding which offer to take put us in an envi-able position, although it was still a diffi cult choice. In May 2006, we chose Magnetar.

The recruiter called not long after I ’ d joined Magnetar ’ s New York offi ce, and I wasn ’ t looking to leave. So I ignored the message.

Most hedge fund portfolio managers (PMs), if they ’ re any good, can expect to hear from a headhunter now and again, perhaps every other month. In the latter half of 2006, with hedge fund mania spik-ing, it seemed like I was getting calls from PM - seeking recruiters every other week.

Later that same November afternoon, the recruiter called again, and I let her go to voice mail again. This time, she mentioned the name of the fi rm looking to get into the hedge fund business: The Carlyle Group.

After the close, I called her back.

■ ■ ■

In terms of sheer size and clout, few investment fi rms are on Carlyle ’ s level. Around the time it set out to conquer the hedge fund business, Carlyle ’ s total assets under management were nearing $ 60 billion, spread across 50 - plus funds, mainly in private equity vehicles, and via

c01.indd 12c01.indd 12 11/17/09 9:38:56 AM11/17/09 9:38:56 AM

Catch a Wave

13

those funds Carlyle controlled huge stakes in hundreds of companies all around the world. With alternative asset management rivals The Blackstone Group and Fortress Investment Group both preparing to go public, it was hardly a secret that Carlyle might be entertaining a similar course.

Based in Washington, DC, the fi rm was setting up its new hedge fund arm, Carlyle - Blue Wave Partners, in the heart of Midtown Manhattan, securing prime commercial real estate on the Avenue of the Americas just south of Central Park, the New Wall Street, post-9/11. I was told Carlyle was sparing no expense, setting a launch target of $ 1 billion. Considering the fi rm ’ s access to institutional channels, corporate and state pension funds, nonprofi t foundations, and university endowments, not to mention the world ’ s wealthiest individuals, such a goal did not seem like a stretch. To Carlyle, $ 1 billion was strategically nimble.

My curiosity suffi ciently aroused, and having apparently passed the recruiter ’ s smell test, I soon sat down with the two ex - Deutsche Bank executives who had been tapped by Carlyle CEO David Rubenstein to create Carlyle - Blue Wave. Rick Goldsmith and Ralph Reynolds had formed a joint venture along with Carlyle that August and promptly set about building one of the largest, most ambitious hedge fund startup teams yet created in an era marked by a series of sizable, noteworthy hedge fund startups.

Reynolds had been Deutsche Bank ’ s global head of proprietary trading and would serve as Carlyle - Blue Wave ’ s CIO; Goldsmith, who had been in charge of a highly profi table hedge fund division of Deutsche Bank, would be the Chief Executive. They teamed up on fundraising and recruiting fund managers. They made quite a pair — Reynolds reserved to the point of saying next to nothing but listening intently, Goldsmith doing all the talking, amiable and sharp. Following a second episode of the “ Rick and Ralph Show, ” I found myself on an impromptu tour of Blue Wave ’ s new digs, completely empty at the time except for some workers doing

c01.indd 13c01.indd 13 11/17/09 9:38:56 AM11/17/09 9:38:56 AM

d i a r y o f a h e d g e f u n d m a n a g e r

14

renovations. The trading fl oor would be top fl ight, ultramodern, and it would be enormous, taking up the offi ce tower ’ s entire 16th fl oor. The space previously had been occupied by Archipelago Holdings, the electronic trading platform which one year earlier merged with the New York Stock Exchange. Around the fl oor ’ s perimeter were several spotless glassed - off rooms, earmarked for various sector teams that were in the midst of being assembled. Carlyle - Blue Wave, I ’ d been told, was building a dream team, and I didn ’ t doubt it. A few months earlier, after hedge fund heavyweight Amaranth Advisors imploded, a number of hedge fund competitors scrambled to pick off the fi rm ’ s most talented traders not based in Calgary, Alberta. * Several of them, including long/short veteran John Bailey, would be joining.

I stared around the room at the rows of empty workspaces. Goldsmith said the fl oor plan had my group, Long/Short Global Consumer, situated in the dead center of it all.

At some point after that second meeting, Goldsmith was feel-ing me out for my “ number, ” which meant my compensation requirement — what would get me to leave my current employer? Thankfully, this wasn ’ t my fi rst negotiation rodeo. In the end, “ Rick and Ralph ” came back with an offer that would be very hard for me to turn down.

But I ’ d had some other requirements as well. I would get to handpick my own investment team, whomever I wanted. Of course . Additionally, I would need to attend any industry conference event anywhere on the planet — travel anywhere my research led me. Not a problem . As a kicker, and since I commuted into Manhattan

* Amaranth, based in Greenwich, was felled in September 2006 by one trader ’ s staggering losses—about $ 6 billion all told — linked to outsized, highly leveraged, long bets on the direction of natural gas prices. The aggressively bullish position, doubled down upon as prices were falling precipitously, was the handiwork of a 32 - year - old trader named Brian Hunter operating from a satellite offi ce in Calgary.

c01.indd 14c01.indd 14 11/17/09 9:38:56 AM11/17/09 9:38:56 AM

Catch a Wave

15

from Westchester County, I wanted to be put up one night a week in a four - star hotel, of my choosing, near the offi ce. Done.

That night, I talked over Carlyle ’ s offer with my wife Laura. She ’ d worked on Wall Street, too, and knew this was a rare opportu-nity. Few hedge fund jobs on the Street were of this magnitude. As a Carlyle - Blue Wave PM, my research team, my access to executives, my sphere of infl uence , would be scarcely matched. Corporate America was at my disposal.

“ This is what you ’ ve always wanted, isn ’ t it? ” she ’ d asked. I suppose. But the decision had come down to the money, the

title, and the prestigious platform versus the satisfaction of working with a close, collaborative team. That ’ s what I had with my exist-ing colleagues, particularly Harry, my thought partner of nearly four years. Money and title versus loyalty.

I took the money and the title.

■ ■ ■

That December, the Carlyle - Blue Wave gig largely secured, my bank balance about to reach a level I never dreamed possible, and the holidays approaching, I boarded a fl ight, along with my wife Laura, to Thunder Bay, Ontario. A snowy Christmas in Thunder Bay sur-rounded by family and friends had become an annual grounding rit-ual, no matter what was going on in my life. Certainly, I had come a long way.

In just under one year I ’ d gone from running a startup hedge fund with tens of millions, to overseeing hundreds of millions, to now, at age 31, becoming part of a group that was seeking to start off with $ 1 billion housed within a still larger group that managed north of $ 50 billion. My ascent through the hedge fund ranks had been a rocket ride at a time when the industry was erupting, in terms of numbers of funds, assets in them, and compensation totals for the guys in charge. Whether I realized it at the time — and in

c01.indd 15c01.indd 15 11/17/09 9:38:57 AM11/17/09 9:38:57 AM

d i a r y o f a h e d g e f u n d m a n a g e r

16

some ways I think I did — the apex of the hedge fund bubble was at hand. Sitting around the Christmas tree with my family, the Wall Street world, for the moment at least, did not exist. Apart from my dad and my younger brother Ryan, who asked me questions now and again about what it was that I actually did for a living, no one else back home knew much of anything about what I was up to in the Big City.

It ’ s not that people from Thunder Bay disliked hedge fund managers; they just didn ’ t give a hoot. Which was fi ne by me, and one of the main reasons why I always return there.

c01.indd 16c01.indd 16 11/17/09 9:38:57 AM11/17/09 9:38:57 AM

17

Chapter 2

Shipping Out

c02.indd 17c02.indd 17 11/17/09 9:39:20 AM11/17/09 9:39:20 AM

c02.indd 18c02.indd 18 11/17/09 9:39:21 AM11/17/09 9:39:21 AM

19

The city of Thunder Bay, actually an amalgamation of two cities, Fort William and Port Arthur, sits atop Lake Superior in northwestern Ontario, right smack in the middle of the continent.

It ’ s an hour ’ s drive from the U.S. – Canadian border, not far from Duluth, Minnesota. Actually one of North America ’ s earliest known trading hubs (Paleo - Indian, pelts, we ’ re talking 1,000 years ago), Thunder Bay has long been a gateway for freighters carrying lumber and wheat from Western Canada down through the Great Lakes and into the St. Lawrence Seaway. Towering steel grain elevators, black and gray, still mark the lake head to this day. The city maintains a viable forestry industry, and transportation sector manufacturer Bombardier has a plant here, too.

c02.indd 19c02.indd 19 11/17/09 9:39:21 AM11/17/09 9:39:21 AM

d i a r y o f a h e d g e f u n d m a n a g e r

20

To Canadians, though, Thunder Bay is best known for producing something far more valuable than timber or subway cars. Thunder Bay makes hockey players.

■ ■ ■

Growing up, kids get fi tted for ice skates around the time they learn to walk. I was skating at 3. My fi rst House League games were played as a 5 - year - old. I came of age following the exploits of a fellow Ontario kid named Wayne Gretzky at the dawn of his career, fi rst in the World Hockey Association and, after it folded, with the National Hockey League ’ s Edmonton Oilers. All of us kids idolized The Great One, and of course, we all watched the Toronto Maple Leafs on CBC ’ s Hockey Night in Canada , and we all dreamed of someday playing in the NHL.

For some of us, playing professionally wasn ’ t all that far - fetched a proposition. My hometown has produced a steady torrent of NHL players over the decades, and nine current players. The most famous are the Staal Brothers, Eric, Jordan, and Marc, who grew up on their dad ’ s sod farms about 20 minutes from my house. Bill “ Goldie ” Goldthorpe, a semi - pro legend and the inspiration for the Ogie Oglethorpe char-acter in Slapshot , lived and played in Thunder Bay. Though not in the same league as Slapshot , the 1986 Rob Lowe fl ick Youngblood con-tained an epic goon character, “ Racki, ” of the Thunder Bay Bombers.

Around the time Youngblood came out, I was one of Thunder Bay ’ s rising Squirt prospects in my age group. Aggressive and quick to the puck, I always led my teams and my leagues in scoring. My mom Vivianne, an elementary school principal, and dad John, a fi refi ghter who ’ d played competitive hockey in Thunder Bay, drilled it into my melon that if I worked hard, if I put in the ice time, I could one day make it to the NHL. Playing for the Leafs became my dream.

During the winter, I woke up at dawn to get in some extra ice time before school. I shot pucks in my basement and in the backyard.

c02.indd 20c02.indd 20 11/17/09 9:39:21 AM11/17/09 9:39:21 AM

Shipping Out

21

I shot pucks at the side of the garage and at my little brother. I hung around the outdoor rinks all day, skating with the older kids in the neighborhood — no referees, parents, or rules beyond “ be home in time for dinner. ” In a city teeming with hockey talent, I thought if I worked that much harder than everyone else, I would have an edge. Shivering in the front seat of my dad ’ s pickup truck at 5 a.m. on absurdly cold winter mornings, I might not have fully appreciated the value of prep-aration, but I ’ ve since found it trumps all else, in sports or business.

By the time I was a freshman in high school, I was playing for the top all - star team in the region, the Thunder Bay Kings. Only three teams mattered in the T - Bay feeder system when I was growing up, and they were the two Triple - A Kings teams (one for 13 - year - olds, the “ Pee Wee ” division, and one for 15 - year - olds, or “ Bantams ” ) and the Junior Hockey powerhouse Thunder Bay Flyers. In Canada, Junior Hockey is a big deal, and features numerous leagues and thousands of the best young players, between the ages of 17 and 20, battling for an invitation to the Junior - A leagues, such as the Ontario Hockey League, part of the Canadian Hockey League, a direct pipeline to the NHL. Important NCAA Division I scouts mine Canada ’ s Junior leagues for talent as well. *

I was determined to play for the Thunder Bay Flyers, and I couldn ’ t turn 17 fast enough. As a 14 - year - old I played on the Kings ’ 15 - year - old team, and I helped the team reach the Canadian Tire Cup tourna-ment where we lost in the provincial tournament to the Toronto Red

* A 1999 research paper “ The Chances of Making It in Pro Hockey for Ontario Minor Hockey Players ” by Jim Parcells of the Ontario Minor Hockey Association, which looks specifi cally at players born in Ontario in 1975 (McCullough ’ s birth year) found that out of approximately 22,000 play-ers active in either minor or junior level hockey, just 41 of them, including McCullough, played NCAA Division I hockey. The study also found that of Ontario players born in 1975, only 48 were drafted to the NHL; four others signed as free agents. At the time of the study, 35 players from the sample group had been signed to NHL contracts and 26 had seen NHL action, making 1975 Ontario ’ s best birth year ever in terms of players drafted to the NHL.

c02.indd 21c02.indd 21 11/17/09 9:39:21 AM11/17/09 9:39:21 AM

d i a r y o f a h e d g e f u n d m a n a g e r

22

Wings. At 16, I wanted to try out for the Thunder Bay Flyers, but the coach, Dave Siciliano, told me in no uncertain terms I wasn ’ t ready for the Flyers. My dad always told me “ don ’ t be the big fi sh in the small pond. ” He always prodded me to compete with the older kids. Instead of waiting another year and playing on the Kings within my age group, my dad convinced me that I had to compete in the big pond. In 1991, a Central Junior Hockey League team, the Brockville Braves, then coached by Rick Ladouceur, invited me to come to their train-ing camp. I made the team. I had my shot to play junior hockey, pretty much unheard of for a kid my age. No one I knew from Thunder Bay had ever left town at 16 to go play Junior - A hockey. If you did try to play outside the T - Bay system, you were pretty much blackballed from then on. I packed some clothes, my blow dryer and a boom box into a blue tickle trunk (with gold buckles) that my dad went out and bought for me, and just like that I was shipped down to Brockville, a 15 - hour drive to the southeastern part of Ontario.

Well, it took me a while to adjust to being away from home. I missed my mom and my younger sister Cheryl more than they ’ ll ever know, although I didn ’ t miss my little brother quite as much, not at fi rst anyway, because growing up we shared a room and that arrangement had run its course. But soon enough I ended up missing him too. I lived with a billet , or “ host ” family, ” Roz and Eric Verbrughe, terrifi c people, and hell - bent on feeding me humongous plates of food. Coming up through the T - Bay hockey system, I was 5 ' 7 " , 150 pounds, so as a 14 - year - old, coaches thought I was going to have some size when I got older. But I never grew any more. When I arrived in the CJHL, I suppose I was considered something of a runt, but I chased after the puck with a vengeance. The guys on the team naturally called me “ Mucker. ” * I remember the feeling

* Old mining camp term referring to the lowest - paying, least desirable job — that of sifting through rocks, mud, and muck, shoveling ore into buckets, and loading them onto conveyor belts.

c02.indd 22c02.indd 22 11/17/09 9:39:21 AM11/17/09 9:39:21 AM

Shipping Out

23

when I stepped on to the ice for my fi rst game, hearing my dad in the back of my head saying that it was better to be the small fi sh in the big pond and realizing in the seconds before my fi rst shift that all my prior accomplishments on the ice back home had absolutely no bearing on the moment at hand.

Hockey is a violent sport. If you consistently put the puck in the net, opposing teams will come after you, and come after you hard. I learned to take a beating, which would be invaluable to me years later on Wall Street.

In my playing days, I ’ d had my throat slit open by a skate blade and my cranium split by a slapshot. I ’ ve lost teeth, broken my wrist, my hand, and multiple fi ngers. I ’ d also generally been subjected to miscellaneous beatings. During my rookie season in Brockville, playing in a game on the border of Quebec against the Hawkesbury Hawks, I “ snowed ” the opposing goalie, using my momentum, skate blade, and the surface to spray him with a coating of ice shavings. It was a rookie move, not lost on a burly, 6�3� Hawks defenseman named Dan McGillis who crosschecked me as payback. On instinct, I turned around and took a swipe at him with my glove. McGillis ripped the face cage off of my helmet, plastic and screws snap-ping, and then proceeded to use me as his personal speed bag as a French - Canadian deejay at the Hawkesbury arena provided a disco soundtrack to the entire spectacle. McGillis would go on to play in the NHL.

During my second season with the Braves, I blew out my knee, badly, after colliding with another player. Now in my second season, I was, at only 17, one of the top players a third of the way through the 1992 – 1993 season. But it didn ’ t matter. Playing hurt, I was noticeably wobbly. I ’ d lost a stride. The Braves coach, Fred Parker, who had arrived in 1992 to replace Ladouceur, told me one dark December day after practice to head up to the General Manager ’ s offi ce, tucked above the stands, almost in the catwalk of the Brockville arena. Parker was kind of a meathead type. He never

c02.indd 23c02.indd 23 11/17/09 9:39:21 AM11/17/09 9:39:21 AM

d i a r y o f a h e d g e f u n d m a n a g e r

24

liked me; I wasn ’ t his guy, and I didn ’ t suck up to him. The rink was dim, quiet, as I hobbled up to the cramped offi ce, hockey photos and memorabilia strewn everywhere. Parker was sitting inside drinking a coffee or something with the GM, a grizzly old timer with white hair and a red face named Mac MacLean. “ We ’ re trading you, ” MacLean informed me with all the emotion of a butcher weighing a half pound of ground chuck.

I was stunned, and angry. Traded? Traded where? I ’ m fairly certain I told them both to shove off, except I think

I used much harsher phrasing. I left the rink feeling lost and alone. It was freezing cold, a few days before Christmas. I was real homesick. It was, literally, at the time, anyway, the worst moment of my life.

I phoned my mom from the Verbrughes ’ kitchen. “ I ’ m coming home, ” I told her. “ Hockey ’ s fi nished. ” “ For the season? ” she ’ d asked. “ No, ” I replied. “ Forever. ”

■ ■ ■

I fl ew home the next day, really glad to be back in Thunder Bay, eat-ing my mom ’ s food, seeing friends, although immediately I could tell there were some people in my hometown who were pleased I had failed. Or rather, they were pleased I did not succeed.

Over the Christmas break my knee healed up and I began skating again, spending hours alone with my thoughts, and feeling guilty about quitting. Out there on the outdoor rinks, the hockey bug bit me all over again. I started going to Thunder Bay Flyers games with my friends. Sitting in the stands, watching, I observed the players I grew up with, more as a scout than a fan, picking up strengths and weaknesses. I knew in my heart that I could skate with them. I always had. Late in December, the Flyers gave me a tryout of sorts, and I skated well, but it was brutal. No one on the team wanted me there (the players saw me as a threat to their ice time

c02.indd 24c02.indd 24 11/17/09 9:39:21 AM11/17/09 9:39:21 AM

Shipping Out

25

and the coaches disliked that I ’ d gone outside their system) and, in the end, once again, the coach told me I wasn ’ t quite Thunder Bay Flyers material.

As it turned out, right around the same time, that old battle - ax Mac MacLean wound up arranging another trade, one that shipped me 17 hours southeast to Pembroke, Ontario, to play Center for the Pembroke Lumber Kings. I jumped at the offer and vowed to my dad and myself not to let it go to waste.

In my fi rst games with the Lumber Kings I was still a half - stride slower than before, but I learned how to grind and help the team win. The Brockville Braves were in our division, so we must have played them a half - dozen times a year, and I think we beat them fairly consistently. Whenever I put one in the net, I ’ d skate by the Braves bench and yell to Coach Parker some profane instruction on what he might do with each puck. In hockey that ’ s called chirping. I liked to chirp.

Playing for the Lumber Kings, my game excelled. That ’ s where I came into my own as a player again, as a winner. When I was named team captain in 1994 it was one of the proudest days of my life. I felt blessed to have been given a second chance to play the game I loved. Playing for the Lumber Kings taught me the impor-tance of believing in myself. It gave me confi dence. It ’ s how I ended up going to Yale.

■ ■ ■

My fi rst day walking around the Yale University campus in New Haven, Connecticut, I kept looking around thinking to myself the whole time: Wow, these are the top students in the world; what am I doing here ? Most likely many of these same students stared back at me wondering why is that guy wearing cutoff denim shorts ?

I was assigned to the third fl oor of Vanderbilt Hall on the Old Campus. Most Yale students, even the upperclassmen, tended to live

c02.indd 25c02.indd 25 11/17/09 9:39:21 AM11/17/09 9:39:21 AM

d i a r y o f a h e d g e f u n d m a n a g e r

26

on campus. I quickly made friends with a couple of the guys in the four - man suite next to mine, one of whom was an easy - going tennis player from North Carolina named Reid Lerner, and the other, Michael Blum, the Hong Kong – Montreal - Cologne — reared son of a German textile industry executive. Hockey practice started up right away, so between classes, ice time, weight training, and a tutor, I stayed busy. I majored in Economics only because it sounded like it had something to do with business. I wanted to learn something here that might help me start a small business one day. Back home, in the summertime, when I wasn ’ t playing hockey, I ran a six - man landscaping - contracting company, called the College Gophers.

My dream to play professionally led me to play an extra year of junior hockey, trying to make up for my lost season in Brockville. When I was recruited to Yale by the team ’ s assistant coach, C.J. Marottolo, I was a 20 - year - old freshman, and I had lived much of the time on my own since age 16. I remember pledging a fraternity those fi rst few weeks of school and realizing midway through the second pledge ritual that frats were not for me; I didn ’ t do groupthink, and I didn ’ t bow down to anyone. Plus, I was swamped. Hockey dominated my life. I was at ease in the locker room. We had one of college hockey ’ s greatest coaches, Tim Taylor. Taylor seemed to be in a soul - searching phase of his career, having just wrapped up a disappointing stint as coach of the U.S. Olympic Hockey Team, which had not fared well during the Lillehammer Winter Games in 1994. His program ’ s mantra seemed to be relegated at the time to “ just being competitive. ” I think the general attitude around Yale (which had competed in the fi rst collegiate hockey game ever played, a century earlier) was that the Bulldogs simply were never going to be an elite NCAA program but should at least be able to compete. In the previous two seasons the Bulldogs had fi nished in last or second - last place. But I looked around the locker room. I saw we had a stellar freshman goalie, Alex “ Westy ” Westlund. He was a ridiculous competitor who would not settle for

c02.indd 26c02.indd 26 11/17/09 9:39:21 AM11/17/09 9:39:21 AM

Shipping Out

27

backup status very long. My fi rst season, 1995 – 1996, Yale had one of its single worst years ever, losing 23 games, a school record at the time. I played every game that year. When Coach Taylor would say after a loss, “ Hey, you guys competed right there with those guys — you should feel proud. ” I ’ d look at Westy and see he had the same look on his face I did, a perplexed grimace that said I don ’ t just want to compete, I want to win.

In my sophomore season (1996 – 1997) we played better, and improved to 10 wins, 19 losses, and 3 ties. I led the team in scoring and penalty minutes that season. The next season, my junior year, we did more than compete. The team registered the winningest sea-son in the history of Yale hockey, an honest - to - goodness Cinderella story. With a 23 – 9 – 3 record, the Bulldogs notched the most wins in the history of the program at that time and won the school ’ s fi rst - ever regular season Eastern Collegiate Athletic Conference (ECAC) Championship. Our team Captain, Ray Giroux, was named ECAC player of the year; Westy brought home the Dryden trophy for the league ’ s best goalie. We were the toast of New Haven — students and people affi liated with the university were ecstatic about the pro-gram ’ s newfound glory, including alumni and former Yale hockey players. One of those former players wound up offering me an internship at his securities trading fi rm in the summer of 1998 prior to the start of my senior year. His name was David Williams, but everyone knew him by his nickname, Tiger. Thanks to him I was about to earn my fi rst stripes on Wall Street.

c02.indd 27c02.indd 27 11/17/09 9:39:21 AM11/17/09 9:39:21 AM

c02.indd 28c02.indd 28 11/17/09 9:39:21 AM11/17/09 9:39:21 AM

29

Chapter 3

Welcome to The Jungle

c03.indd 29c03.indd 29 11/17/09 9:39:52 AM11/17/09 9:39:52 AM

c03.indd 30c03.indd 30 11/17/09 9:39:53 AM11/17/09 9:39:53 AM

31

On the fi rst day of my summer internship at Williams Trading, I strolled in at 7 a.m., fi guring I was way early. Turned out, I was a half - hour late. Meanwhile, I ’ d decided to wear the nicest set of

clothes I owned at the time — a black silk dress shirt, and my lone tie, maroon, adorned with bald eagles. Both were gifts from my mom. When I walked into the Rockefeller Center offi ce, * one of the traders, Ray “ Razor ” Letourneau, a former equities trader at J.P. Morgan Securities and also a former Yale hockey player, looked me over, incredulous. “ What the hell are you wearing ? ” he asked.

Here I was, at what some might consider the nexus of the hedge fund universe, and yet I was about as oblivious as Forrest Gump at a Black Panther meeting. I ’ ve always thought of my career trajectory on Wall Street as having something of a Forrest Gump - type quality

* Williams Trading is currently located in Stamford, Connecticut.

c03.indd 31c03.indd 31 11/17/09 9:39:53 AM11/17/09 9:39:53 AM

d i a r y o f a h e d g e f u n d m a n a g e r

32

to it, intersecting with historical turning points and major fi gures now and again. But even Gump would have had the good sense not to show up on a trading fl oor wearing a shirt that looked like something purchased at Chess King. * Later that summer I bought two suits — one blue, one gray — which I rotated every other day. The Williams crew wore ties, but they looked low key, like their trading setup. In fact, the whole operation was just four guys, an administrative assistant, and some computers set up in a small room. But man, did these guys have discipline, and a process.

Williams had launched his fi rm one year prior, in 1997. The captain of the 1983 – 1984 Yale hockey team during his senior season, Williams started out on Wall Street in 1987 as a fl oor clerk for E.F. Hutton. He was trading on the fl oor of the New York Stock Exchange on “ Black Monday, ” October 19, 1987. Williams then became an equity sales trader for CS First Boston, which was created in 1988 when Credit Suisse took a controlling stake in the First Boston Corporation. Eventually, Williams became a Vice President and Senior Equity Trader at Donaldson Lufkin and Jenrette, before it merged with Credit Suisse as well. Williams’ big break came in 1993 when he joined up with an iconic hedge fund manager named Julian Robertson, Jr.

At that time, Robertson ’ s fi rm, Tiger Management was (and while closed to new money it remains) among the most storied money management operations of all time. The fact that David “ Tiger ” Williams wound up joining a fi rm called Tiger Management was pure happenstance — the Tiger moniker had already stuck to him during his hockey playing days as a kid growing up north of Boston, on account of Williams’ sharing the same fi rst and last name as the infamous NHL brawler (and the league ’ s all - time

* Chess King was a retailer of quintessentially cheesy 1980s clothing particularly popular on Long Island and in New Jersey. It was acquired in 1993 by Merry Go Round, which entered Chapter 11 bankruptcy one year later.

c03.indd 32c03.indd 32 11/17/09 9:39:53 AM11/17/09 9:39:53 AM

Welcome to the Jungle

33

career penalty minutes leader with 3,966 minutes over 15 seasons, the equivalent of nearly three days in the penalty box) Dave “ Tiger ” Williams. The fact that Tiger Management produced hedge fund managers the way Thunder Bay produced hockey players was no coincidence. Robertson picked and mentored the best analysts and traders in the business. Several former Tiger employees wound up leaving to launch their own funds in the early - to mid - 1990s, students of Robertson such as Lee Ainslie of Maverick Capital, John Griffi n of Blue Ridge Capital, and Stephen Mandel of Lone Pine Capital; several more of Robertson ’ s brightest pupils, such as Dwight Anderson, Paul Touradji, and Andreas Halvorsen, all also would go on to launch sizable hedge fund companies in the decade to come. Collectively, they were called the “ Tiger Cubs. ” Seeded by Robertson, these new funds began life with tens of millions in assets, fairly puny on a relative basis. They were modestly staffed and usually sublet offi ce space from larger trading fi rms or money managers, which gave rise to the whole concept of hedge fund hotels. But because smaller money managers with their smaller orders tended to get relegated to the bulge bracket ’ s pay - no - mind - list, these new hedge fund fi rms needed help and expertise executing their trading strategies. That ’ s where Williams came in.

He had a vast network of potential trading counterparts, all over the Street. He ’ d been Tiger Management ’ s Associate Director responsible for trading the Domestic Equity portfolio at a time when Robertson ’ s hedge fund fi rm saw its assets grow from $ 3 billion when Williams joined up in 1993 all the way to $ 15 billion by the time he left in March 1997. Williams Trading, formed the following June, was not a hedge fund; it was created to be the execution - only, outsourced - trading - desk - of - choice for startup hedge funds.

In addition to Williams, who functioned as captain, coach, and head trader, there was “ Razor ” Letourneau, who was pretty much Williams’ right - hand man, and Rob “ Laffer ” Laferriere, who ’ d played hockey at Boston College and Princeton, and the

c03.indd 33c03.indd 33 11/17/09 9:39:53 AM11/17/09 9:39:53 AM

d i a r y o f a h e d g e f u n d m a n a g e r

34

one non - hockey guy, the operations/compliance chief, Danny “ the Dirty Dog ” Dispigna who handled reconciling all the trades, a mundane but critical function known on the Street as the “ back offi ce. ” There was also Elodie Fielding, the administrative assistant. She held her own and kept things running smoothly.

As the intern, I had four mundane tasks of my own to worry about: Collect the Buy/Sell tickets that were manually written out with every single trade (black ones for Longs, red for Shorts); fi le the tickets with Dispigna, who entered them into a computer; open the mail; and order lunch. I came to learn that of these four jobs, the failure to properly carry out a timely, well - executed lunch order was the gravest of infractions, although if I inadvertently mismarked a ticket that wasn ’ t a good thing either because it caused headaches for Dispigna. No one likes to get yelled at. But when I screwed up and he had to stay late to fi x my error, I felt terrible that I had let down a teammate. Williams ran his fi rm like a hockey team. The environment was intensely competitive, every minute. Some trading fl oors may have stories of guys having hilarious side bets ( hundred bucks says you can ’ t eat 72 Chicken McNuggets ) and ribald rituals, but the Williams crew was strictly business. For one thing, they were always busy, taking orders and calling around the Street to get them carried out. My fi rst week there was the most intimidating period of my life, because I was out of my element. I didn ’ t know the securities market jargon — I didn ’ t understand the game. I couldn ’ t see it being played in front of me. Not at fi rst anyway.

Not only was I learning that teamwork existed on Wall Street (which I ’ d presumed was every man for himself ), I was beginning to understand how markets functioned. Mega, long - only, tax - free retirement asset - laden mutual fund companies, such as Janus, Fidelity, Putnam, T. Rowe Price, et al., carried enormous clout in the market, and these were household names across America with the S & P 500 cranking out a fourth straight year of double - digit returns

c03.indd 34c03.indd 34 11/17/09 9:39:53 AM11/17/09 9:39:53 AM

Welcome to the Jungle

35

and the Nasdaq soaring. * Hedge funds held sway in the market, too, increasingly so, but most people outside of the clubby Wall Street set had zero clue hedge funds existed. When I came to Williams Trading in June 1998, there were, according to various industry estimates, somewhere between 3,000 and 4,000 hedge funds totaling roughly between $ 300 billion and $ 400 billion. I ’ d barely even ever heard the term “ hedge fund ” and neither had most Americans, but nevertheless by the late 1990s there were many established hedge funds managers that had asserted themselves as world - class investors, taking up some of the highest rungs of the sellside pecking order. There were the Godfathers of the Game, guys like Julian Robertson, George Soros, and Michael Steinhardt; and next generation traders, or so - called gunslingers, such as Paul Tudor Jones and Steve Cohen; expertly trained ex - Goldmanites, such as Leon Cooperman, Richard Perry, and Dan Och; research intensive stalwarts such as Art Samberg and Jon Dawson; and statistically driven Big Brains, such as Jim Simons and David Shaw. These latter types, the so - called “ quants, ” were really starting to rise to the fore amidst technological and academic advancements. One of the largest, most talked about funds that summer, Long Term Capital Management, had been started a few years earlier in Greenwich by an ex - Salomon Brothers bond trader, John Meriwether, along with esteemed economics professors Myron Scholes and Robert Merton who matched up cutting - edge mathematical theory with sophisticated computer models.

During my junior year I ’ d gotten a taste of the highest academic echelons, taking an Economics course taught by Professor Robert Shiller, who would become famous for the housing price index he helped create, the S & P Case - Shiller Home Price Index. Economics didn ’ t mean jack to me before I took his class. He was the fi rst pro-fessor who made economics seem relevant, practical. Everything I ’ d

* The Nasdaq Composite Index fi nished 1997 at 1570.35. It ended 1998 at 2192.69.

c03.indd 35c03.indd 35 11/17/09 9:39:53 AM11/17/09 9:39:53 AM

d i a r y o f a h e d g e f u n d m a n a g e r

36

learned in the classroom had been statistical, theoretical, hermeti-cally sealed concepts: supply, demand, infl ation, defl ation, stagfl ation. Shiller used real - world illustrations and historical examples, and he always had decades of data to illuminate how market forces behaved, how patterns tended to repeat. Except, of course, when they don ’ t repeat, which is why that giant quant fund co - created by those economics professors wound up getting into serious trouble * later that summer of 1998, and why for the fi rst time millions of people around the world fi rst realized hedge funds existed and the extent to which they could impact the world ’ s fi nancial machine.

That summer at Williams Trading, I came to begin to realize the true scope, depth, and dynamics of this vast expanse of money fl owing in and out of securities, around the world, in different ways, to achieve different outcomes, by way of often drastically different approaches. Once I understood that, okay, sure, people were either buying shares of something or selling them, building a Long position or covering a Short one, I started to pick up how certain participants traded. Some money managers were fading the market; other ones were chasing. I saw how the surge in the morning between 9:30 a.m. and 11 a.m. forestalled a lunchtime lull (it ’ s a wildly simple phenomenon: traders eat lunch). It didn ’ t all make perfect sense to me, but I liked the buzz and camaraderie. I knew for the fi rst time that if my professional hockey aspirations didn ’ t come to fruition,

* Hurt badly in August of 1998 by wrong way derivative bets on bond yield spreads amidst a global currency crisis sparked by Russian bond defaults and widening to Asia, and compounded by the $ 10 billion fund ’ s use of leverage on top of leverage leading to approximately $ 100 billion in balance sheet exposure, LTCM was in September of that year forced into a form of liquidation. This outcome involved a consortium of creditors, 14 institutions in all, including almost all the major investment banks at that time, infusing the fund with $ 3.6 billion in capital (i.e., a private bailout) at the emergency prompting of the Federal Reserve Bank of New York, which at the time feared that total failure of the fund would jeopardize the stability of the fi nancial system.

c03.indd 36c03.indd 36 11/17/09 9:39:53 AM11/17/09 9:39:53 AM

Welcome to the Jungle

37

perhaps this Wall Street thing could be an option. But my hockey playing days weren ’ t over just yet.

■ ■ ■

My senior season at Yale, 1998 – 1999, I was named captain. We still had a great team, so there were a few NHL scouts coming to our games. We turned in another solid campaign, winning 8 of our last 13 games to win a share of the Ivy League crown along with Princeton, even though our best player, Ray Giroux, possibly the single best player in Yale history, had graduated. Off the ice I was crafting my senior thesis, in which I was attempting to identify key traits common to successful entrepreneurs. I struggled to write the paper, although I enjoyed the research part of it. Keep in mind that the very fi rst English Literature composition I turned in my fresh-man year had come back to me marked “ ungradable. ” The school gave me a tutor, but writing remained a struggle. Still, I embraced my thesis. I built upon some themes I had developed writing an ear-lier paper about my Grampa Alphonse, one of 19 children from the French - Canadian logging town of Long Lac and who wound up starting a string of successful small businesses, including a restaurant, a general store, and a ladies clothing store. I started thinking about the all - time greatest businessmen and naturally arrived at Warren Buffett as the focus of my thesis. To understand what made Buffett so great, I examined his early years. Buffett ’ s autobiography, The Making of an American Capitalist , provided the bulk of my source material. Both my Grampa and The Oracle of Omaha, as far as I could tell, believed in themselves and cared little about what others may have thought of them. If I could redo the thesis today I ’ d keep it simple. What makes a really successful entrepreneur? Drive, hard work, and a mind of your own.

As my time at Yale wound down, the hockey season dwindling to the last 10 games, it was clear there were no scouts waiting to

c03.indd 37c03.indd 37 11/17/09 9:39:53 AM11/17/09 9:39:53 AM

d i a r y o f a h e d g e f u n d m a n a g e r

38

talk to me outside the locker room. I began to face up to the fact that my hockey - playing days were coming to an end. In the locker room after my last game, March 13, 1999, a crushing 7 – 2 loss at home in the ECAC playoffs to Colgate, I hit a wall of despondency. I ’ d suffered a groin injury and didn ’ t have the greatest game. When it was over, the game, my career, was over, really over , the idea that I would no longer be a hockey player rolled over me like a Zamboni. I wouldn ’ t take my equipment off. My boom box cranked out a song by Garth Brooks, “ The River. ”

I just sat there playing the cassette tape over and over. I think I played “ The River ” nine times in a row. The tune is about someone who follows his dreams as far as they can take him, until his “ river runs dry. ” I wasn ’ t crying, because much like baseball, there ’ s no crying in hockey. But I was empty inside. I was 24, and didn ’ t quite know who I was, or what I was supposed to do next. This was the low point of my entire life. As for where the “ river ” would take me next I was not exactly sure, maybe back to Thunder Bay for one last summer landscaping with the Gophers and hanging at the Lake.

But it wouldn ’ t be long before the path ahead of me took shape. I mean, I was about to be a Yale graduate, captain of the hockey team. Wall Street came knocking. And I answered.

c03.indd 38c03.indd 38 11/17/09 9:39:53 AM11/17/09 9:39:53 AM

39

Chapter 4

Snapshots From The Dot.Com Bubble

c04.indd 39c04.indd 39 11/17/09 9:40:17 AM11/17/09 9:40:17 AM

c04.indd 40c04.indd 40 11/17/09 9:40:17 AM11/17/09 9:40:17 AM

41

D o you have a ball? ” The Lehman Brothers executive met my question with a blank stare. He either didn ’ t expect a lowly member of the

Class of 1999 to ask him a question — he was, after all, interviewing me — or he didn ’ t appreciate it, because the guy looked at me like I had just made a rude comment about his wife. We were seated across from one another in a New York City hotel during the investment brokerage house ’ s spring “ Super Saturday ” recruiting event. Lehman had invited me and around two dozen other graduating, mostly Ivy League, seniors to compete for about six entry - level positions. Most of the banks put on a “ Super Saturday ” event, part junket, part steeplechase. I refused to be intimidated.

“ A ball? ” he asked. “ What do you mean? ” “ A ball, ” I said, smiling, cocky. “ That thing you throw. Tennis

ball, soccer ball, any ball. Do you have one? ”

“

c04.indd 41c04.indd 41 11/17/09 9:40:17 AM11/17/09 9:40:17 AM

d i a r y o f a h e d g e f u n d m a n a g e r

42

“ What ’ s your point? ” This whole exchange had started with him, somewhat condes-

cendingly, asking me why I believed I was Lehman material. What set me apart?

I told him: “ If you took every college recruit here, put us all in a room, and then shut the doors and turned off the lights, so it was pitch black, and then threw a ball in the room for us to chase around . . . I can guarantee you . . . that I ’ d be the one coming out of there with that ball. ”

The Lehmanite, trim, jockish, and in his early 30s, fl ashed me a smile as the bewilderment vacated his eyes. Extending his arm in a handshake, he practically shouted: “ That ’ s the best answer I have ever heard! ”

Although the dot.com era was well underway, Wall Street still had its pick of the roughly one million or so college seniors who graduate every May. But they were more vigorously pursuing the best and the brightest in 1999 now that they had to compete with Silicon Valley. I ended up getting an offer from Lehman, but wound up taking another job. I was going to work for Credit Suisse First Boston (CSFB). * It was the summer of 1999 and there was no hotter fi rm on Wall Street than CSFB.

■ ■ ■

Many corporations, blue - chip investment banks included, place their greenhorn university recruits into training programs designed to matriculate them through a series of temporary sojourns across divisions. A bank or investment brokerage house might rotate a new recruit through stints in sales, trading, and research. When I joined,

* Credit Suisse Group ’ s investment banking business, CS First Boston, was renamed Credit Suisse First Boston (CSFB) in 1996. One decade later, the franchise was renamed again, becoming simply Credit Suisse.

c04.indd 42c04.indd 42 11/17/09 9:40:17 AM11/17/09 9:40:17 AM

Snapshots from the Dot.Com Bubble

43

CSFB had exactly such a trainee rotation program. But these were not normal times.

Technology/dot.com fever reached epidemic proportions, partly fuelled by the growing awareness of the ubiquity and power of the Internet, and partly by massive amounts of spending connected to so - called Y2K concerns.

Under CEO Allen Wheat, CSFB, the New York – based global investment banking arm of Zurich - based Credit Suisse Group, was proving to be an epicenter of “ tech stock ” mania. One year earlier, in mid - 1998, Wheat snared Midas - touch investment banker Frank Quattrone and his entire Menlo Park, California – based technology group, recruiting them away from the Deutsche Morgan Grenfell unit of rival Deutsche Bank. Prior to Morgan Grenfell, Quattrone had worked at Morgan Stanley where he ’ d been a colleague of Mary Meeker, one of the technology sector ’ s best - known analysts and most vociferous boosters. By mid - 1999, Quattrone ’ s tech/dot.com IPO machine was cranking out shares at a breathtaking clip. In 1998 alone, Quattrone led 138 IPOs, according to BusinessWeek. Technology mutual fund managers from the Back Bay section of Boston to the Cherry Creek section of Denver contorted themselves to get dialed into the CSFB platform, and many of the funds and their investors were being treated to some of the lowest - hanging fruit ever harvested on Wall Street.

Instead of doing mini - stints in a series of varying departments, I was dispatched to Equity Sales. My immediate bosses, Steve Keller and Tom Ferraro, were two of CSFB ’ s most senior - ranking equity salesmen. I ’ d been assigned to support them as the junior member of their team, effectively doing whatever they told me. Title - wise I was an “ analyst, ” but my business card may as well have said “ Mucker. ” Our group was part of an equity sales group of around 150 persons around the world, part of the larger glo-bal equities division at CSFB. This division was headed up by a

c04.indd 43c04.indd 43 11/17/09 9:40:17 AM11/17/09 9:40:17 AM

d i a r y o f a h e d g e f u n d m a n a g e r

44

veteran derivatives trader, Brady Dougan, and employed more than 3,000 people in 1999.

My being included among those ranks owed to an Ivy League/jock connection. Keller, the captain of the 1990 – 1991 Yale basket-ball team, personally recruited me. He and Ferraro spearheaded CSFB ’ s equity sales effort, selling into the burgeoning hedge fund channels. They focused on the largest fi rms in New York and Connecticut. If Keller asked me for a spreadsheet of phone numbers of every hedge fund fi rm with more than $ 100 million in assets under management based in Greenwich and Stamford, I asked: How about e - mails, too?

I felt like a junior hockey rookie all over again, thrown right onto the ice, or in this case, into the fi re. I was no doubt a cog in the wheel, a foot soldier in a campaign that amounted to an ambitious sales effort, nothing more. Nevertheless, I made a pledge to myself: to be the best teammate I could be, to do the best job I possibly could — nothing half - assed, not too much partying, or at least not during the week. If I could make Keller and Ferraro look good, then maybe I might get paid a nice bonus at the end of the year to go with my mid - fi ve - fi gure base salary.

Dougan had made a pledge of his own. He set an almost mythical goal in 1996 when he took over as CSFB ’ s global head of equities, determining that the division would produce pretax, pre - bonus profi ts of $ 1 billion by 2000. This target, if met, would represent a 17 - fold increase from CSFB ’ s 1995 pretax, pre - bonus profi ts. Dougan and his disciples called it “ sticking to the program. ”

As programs go, mine wasn ’ t too terrible. I settled into the job, future shock gave way to an agreeable routine. I lived in a high - rise apartment on 34th Street, between Park and Lexington Avenues, in the Murray Hill section of Manhattan. I decided to bite the bullet and pay up for a location just blocks from my offi ce. I ’ d moved in with my old Yale buds, Reid Lerner and Francois “ Frenchy ” Magnant (a Bulldog defenseman), who were working as bankers.

c04.indd 44c04.indd 44 11/17/09 9:40:17 AM11/17/09 9:40:17 AM

Snapshots from the Dot.Com Bubble

45

I walked to work every day. The CSFB offi ces were located in the Flatiron District on Madison Avenue at 28th Street, in an impressive art deco building that originally belonged to MetLife.

Inspired by the Williams Trading experience, I was, without fail, at my desk by 6:30 a.m., which at CSFB meant I was among the fi rst handful of people in the door. If one of our roughly four dozen or so hedge fund clients rang the equity sales desk at sunrise expecting to get Keller or Ferraro ’ s voice mail, I ’ d pick up the phone to let him or her know that the message would be delivered personally. This allowed me to get know the hedge fund people, sometimes PMs or analysts, sometimes their junior counterparts. Quickly I realized that I knew some of those junior voices on the other end of the line — junior buyside analysts who had been peers of mine at Yale. I could skate with them, I thought, I could be the one placing orders, not taking orders.

Still, I enjoyed what I did. My daily work environment was boisterous, exciting, like being in the infi eld of a horse race, with this exception — you couldn ’ t actually see the horses. Rather, you could only hear the raised, hurried voices of those who were placing bets. You heard the action, and soon it was obvious to me which funds on the other end of the line were running at a gallop and which ones were content to trot. I did not see hedge funds start to break ahead of the fi eld, I heard and sensed them. And due to the massive volume of trading hedge funds did on the Street, we jumped at the chance to do their bidding.

To understand the distinction between an equity sales trader and an equity salesman, look a little more closely at how an investment bank such as CSFB functions, how it ’ s organized. In 1999 and into 2000, CSFB primarily existed as a factory manufacturing and distrib-uting shares of new companies. CSFB “ brought ” these “ startups ” to the public equities markets. Once those companies began trad-ing, usually on the Nasdaq, CSFB provided money managers with “ coverage, ” ongoing research, crucial, and not so crucial, nuggets of

c04.indd 45c04.indd 45 11/17/09 9:40:17 AM11/17/09 9:40:17 AM

d i a r y o f a h e d g e f u n d m a n a g e r

46

information, often gleaned (or spoon fed) directly from manage-ment. Bankers such as Quattrone, working with a network of “ ven-ture capitalists, ” found the startups, deemed them worthy of public consumption, structured the IPO deals, and, key to the whole pro-gram, lined up big institutional buyers for the newly minted shares. CSFB analysts followed these companies ’ every move, guiding the institutional owners of the shares as to where revenues, earnings, and share prices might be heading. Nailing the quarterly earnings per share or revenue number before it was released was the invest-ment and trading industry ’ s Holy Grail. Our analysts were closely followed, not so much for reports and recommendations but for reliable, almost to the penny estimates. Much of Wall Street ’ s “ research ” from this era has been characterized as confl icted and thus unreliable for investors, but such a broad stroke critique, while in some ways accurate, still misses a more nuanced picture of what was taking place, at least with respect to my employer. Believe me, institutions hung on our analysts ’ every update.

Although I sat amidst our sales traders, the ability to be effective in my job hinged on keeping communication lines open with the research analysts upstairs, so as to not miss even a single new crumb of information coming in the door from the various analysts, many of whom were out on the road or jammed up with meetings. I fi gured out fairly quickly that as a junior analyst barely through the Series 7, my access to CSFB analysts was nonexistent. I could not expect to get a major CSFB analyst such as telecom all - star Dan Reingold or our software industry stalwart Wendell Laidley to call me up with the latest guidance on WorldCom or Veritas. But if I befriended the junior analysts in each sector, then my access to information increased many - fold. So I sidled up to as many of the junior analysts as I could, any chance I could, in the CSFB cafeteria or in its gym. I made it my mission to make friends. Keller told me that clients told him I was doing well, which was motivational. “ Keith gets it, ” one client had said. Keller began to let me call more

c04.indd 46c04.indd 46 11/17/09 9:40:17 AM11/17/09 9:40:17 AM

Snapshots from the Dot.Com Bubble

47

and more clients directly, because I could hold my own and because sometimes I had the scoop fi rst.

My workstation was right on the equity trading fl oor, or rather directly adjacent to it, down a ramp from an elevated group of equity sales traders, which, it should be pointed out, are a different species of Wall Street animals than my brethren in equity sales.