Embed Size (px)

Citation preview

1

Developing the Knowledge Economy:

Trends and Indicators on

Regional Innovation-Based Development

and Science Parks in Europe

Anthony D’Andrea

ISSP Post-Doctoral Research Fellow, Project Coordinator

“Nomadic Work/Life in the Knowledge Economy”

Dept. Sociology, ISKS - University of Limerick

University of Limerick Sociology Seminar - April 14, 2010

Quoting is allowed - please cite author and sources

2

Developing the Knowledge Economy: Trends and Indicators on Regional Innovation-

Based Development and Science Parks in Europe

Anthony D’Andrea

Abstract: The knowledge economy is a key concept in the developmental agenda across

Europe and beyond. Meanwhile, due to EU supranational politics and global economy

processes, regions have emerged as another key unit of policy analysis and intervention. In

the meeting of innovation policy and cohesion policy, science parks have reemerged as a

catalyst tool for regional development, as indicated in the recent boom of science parks across

the developing world (China, India, Taiwan, Israel, Greece, etc.)

Based on EU policy reports, scholarship on science parks, and ethnographic research on

science parks in Ireland, this presentation provides an overview of the knowledge economy in

Ireland vis-à-vis the EU, and summarizes several national experiences with science parks.

The goal of this presentation is to identify the main factors and challenges affecting the

development of the knowledge economy at a regional level.

Keywords: smart economy, regional research-based clusters, regional innovation systems,

technology parks, RIPI

3

1. Knowledge economy in Ireland and EU

2. Regional development: integrating cohesion policy and innovation policy

3. Science parks: tools for regional (knowledge-based) development

4. Conclusion

Presentation Outline

4

Knowledge Economy

5

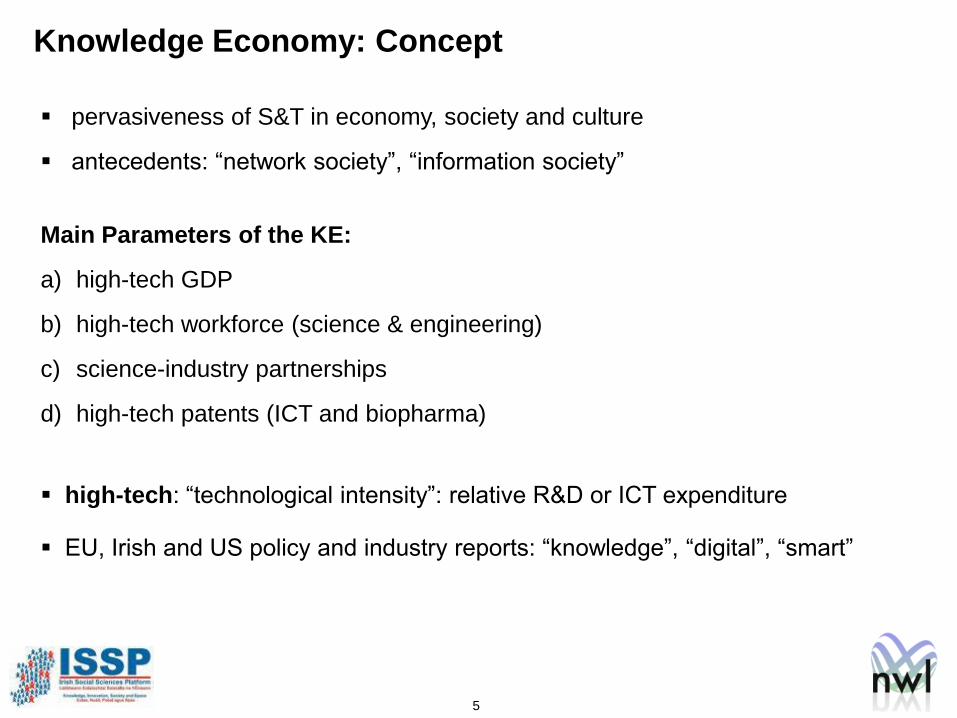

pervasiveness of S&T in economy, society and culture

antecedents: “network society”, “information society”

Main Parameters of the KE:

a) high-tech GDP

b) high-tech workforce (science & engineering)

c) science-industry partnerships

d) high-tech patents (ICT and biopharma)

high-tech: “technological intensity”: relative R&D or ICT expenditure

EU, Irish and US policy and industry reports: “knowledge”, “digital”, “smart”

Knowledge Economy: Concept

6

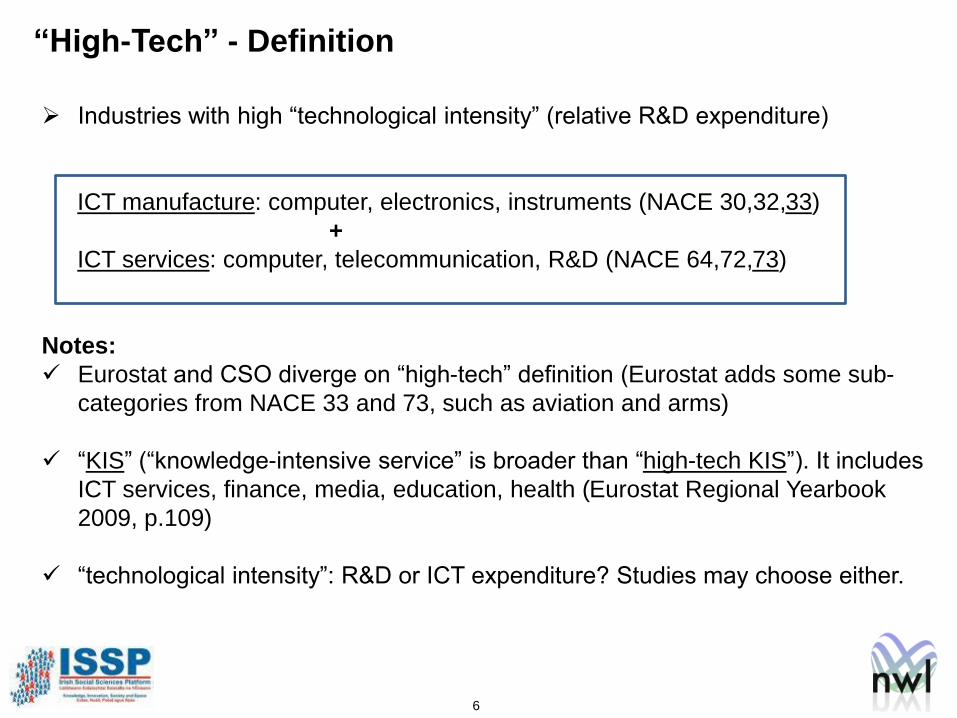

Industries with high “technological intensity” (relative R&D expenditure)

ICT manufacture: computer, electronics, instruments (NACE 30,32,33)

+

ICT services: computer, telecommunication, R&D (NACE 64,72,73)

Notes:

Eurostat and CSO diverge on “high-tech” definition (Eurostat adds some sub-

categories from NACE 33 and 73, such as aviation and arms)

“KIS” (“knowledge-intensive service” is broader than “high-tech KIS”). It includes

ICT services, finance, media, education, health (Eurostat Regional Yearbook

2009, p.109)

“technological intensity”: R&D or ICT expenditure? Studies may choose either.

“High-Tech” - Definition

7

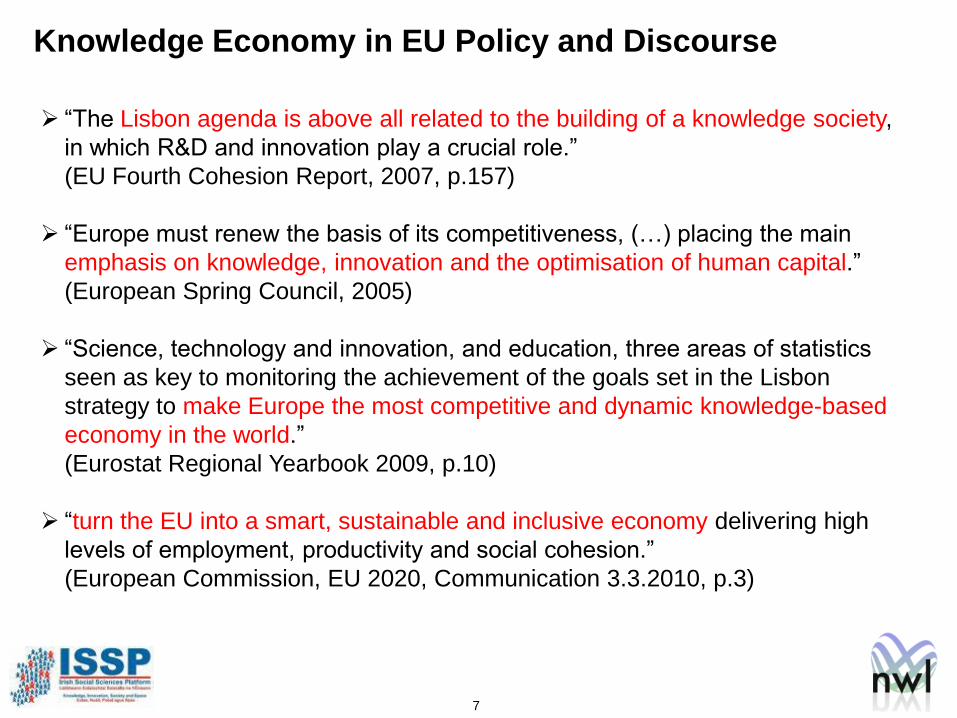

“The Lisbon agenda is above all related to the building of a knowledge society,

in which R&D and innovation play a crucial role.”

(EU Fourth Cohesion Report, 2007, p.157)

“Europe must renew the basis of its competitiveness, (…) placing the main

emphasis on knowledge, innovation and the optimisation of human capital.”

(European Spring Council, 2005)

“Science, technology and innovation, and education, three areas of statistics

seen as key to monitoring the achievement of the goals set in the Lisbon

strategy to make Europe the most competitive and dynamic knowledge-based

economy in the world.”

(Eurostat Regional Yearbook 2009, p.10)

“turn the EU into a smart, sustainable and inclusive economy delivering high

levels of employment, productivity and social cohesion.”

(European Commission, EU 2020, Communication 3.3.2010, p.3)

Knowledge Economy in EU Policy and Discourse

8

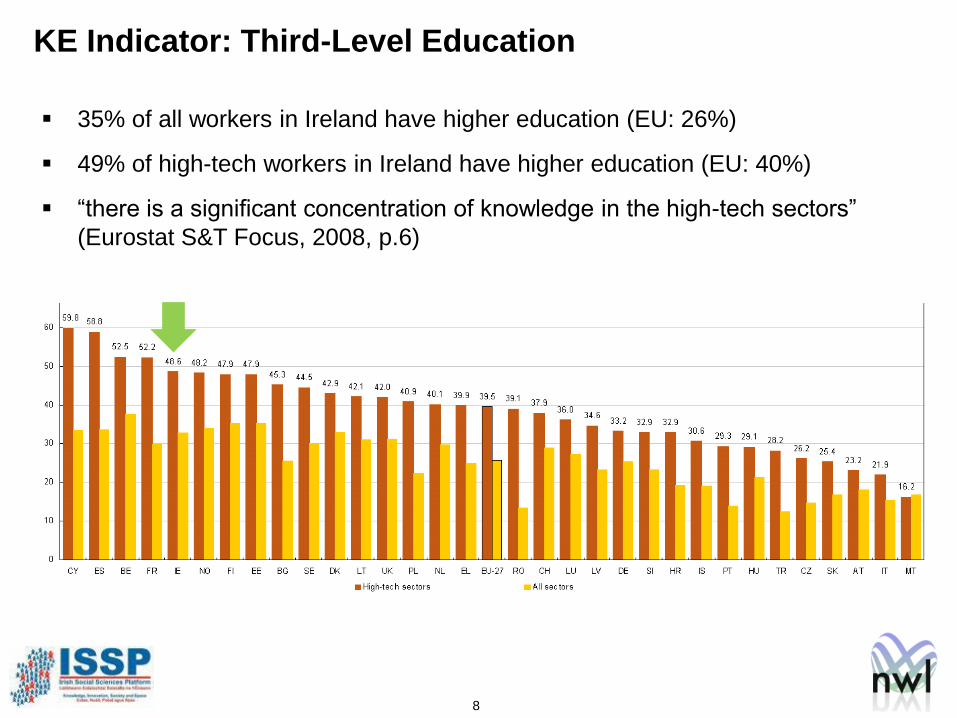

KE Indicator: Third-Level Education

35% of all workers in Ireland have higher education (EU: 26%)

49% of high-tech workers in Ireland have higher education (EU: 40%)

“there is a significant concentration of knowledge in the high-tech sectors”

(Eurostat S&T Focus, 2008, p.6)

9

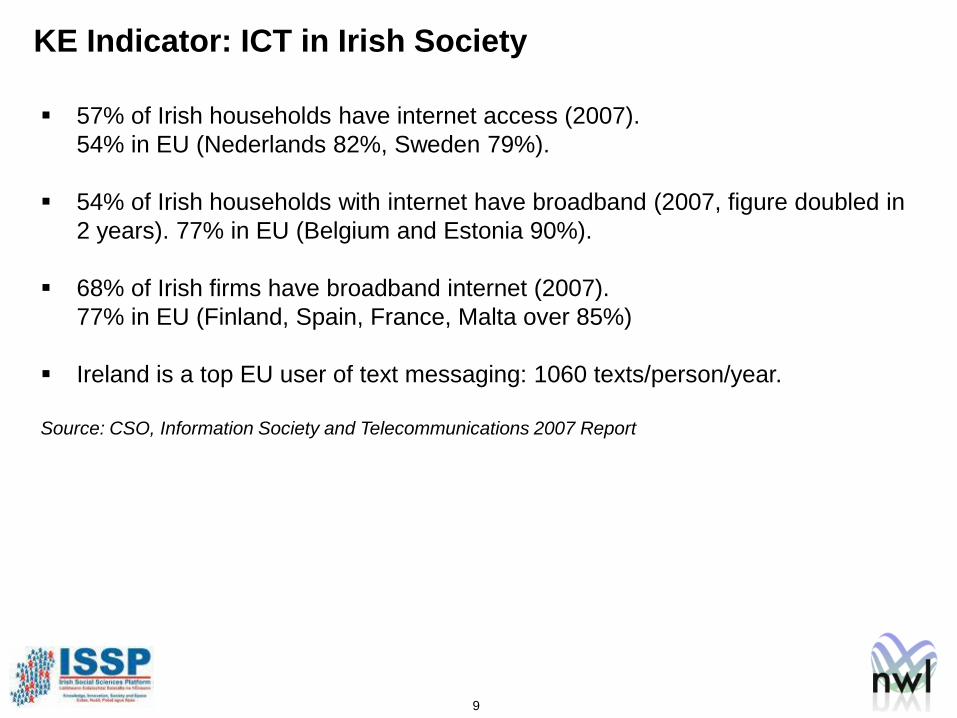

57% of Irish households have internet access (2007).

54% in EU (Nederlands 82%, Sweden 79%).

54% of Irish households with internet have broadband (2007, figure doubled in

2 years). 77% in EU (Belgium and Estonia 90%).

68% of Irish firms have broadband internet (2007).

77% in EU (Finland, Spain, France, Malta over 85%)

Ireland is a top EU user of text messaging: 1060 texts/person/year.

Source: CSO, Information Society and Telecommunications 2007 Report

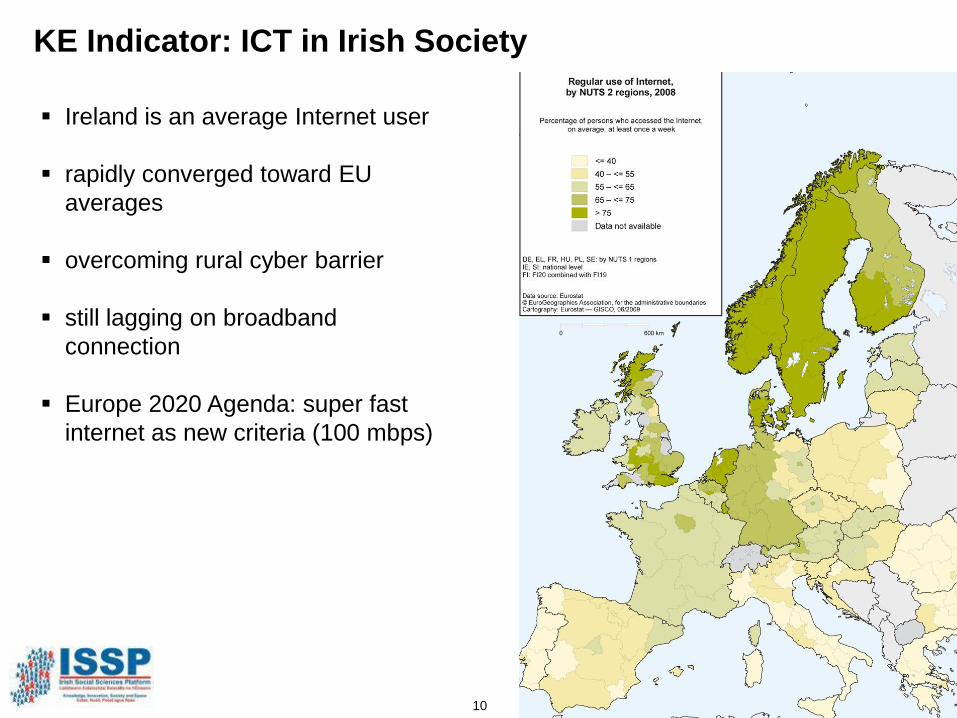

KE Indicator: ICT in Irish Society

10

KE Indicator: ICT in Irish Society

Ireland is an average Internet user

rapidly converged toward EU

averages

overcoming rural cyber barrier

still lagging on broadband

connection

Europe 2020 Agenda: super fast

internet as new criteria (100 mbps)

11

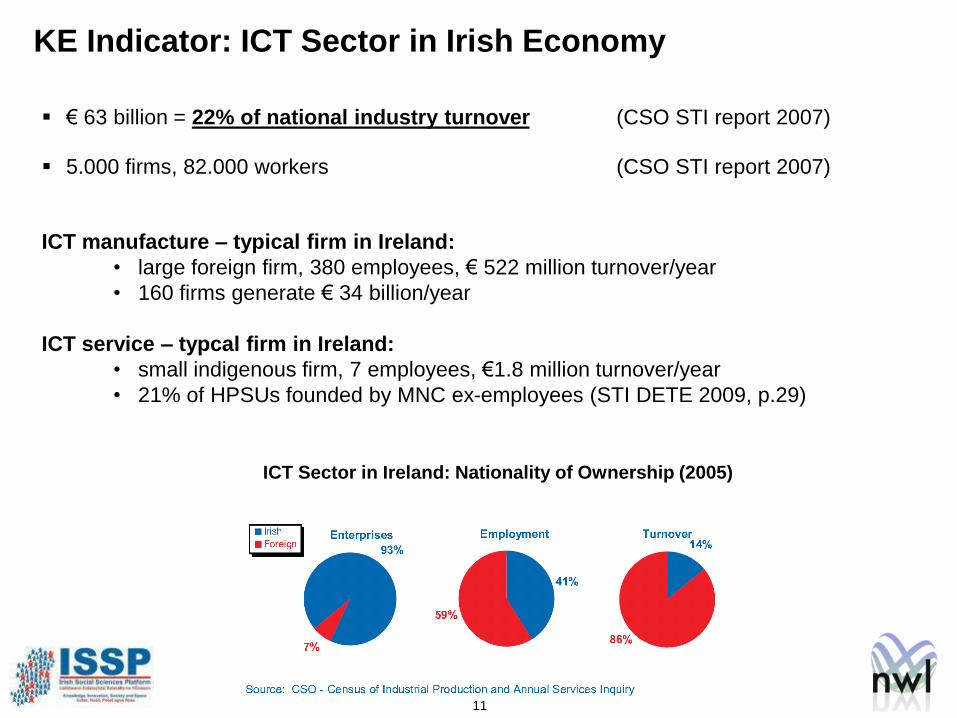

KE Indicator: ICT Sector in Irish Economy

€ 63 billion = 22% of national industry turnover (CSO STI report 2007)

5.000 firms, 82.000 workers (CSO STI report 2007)

ICT manufacture – typical firm in Ireland:

• large foreign firm, 380 employees, € 522 million turnover/year

• 160 firms generate € 34 billion/year

ICT service – typcal firm in Ireland:

• small indigenous firm, 7 employees, €1.8 million turnover/year

• 21% of HPSUs founded by MNC ex-employees (STI DETE 2009, p.29)

ICT Sector in Ireland: Nationality of Ownership (2005)

12

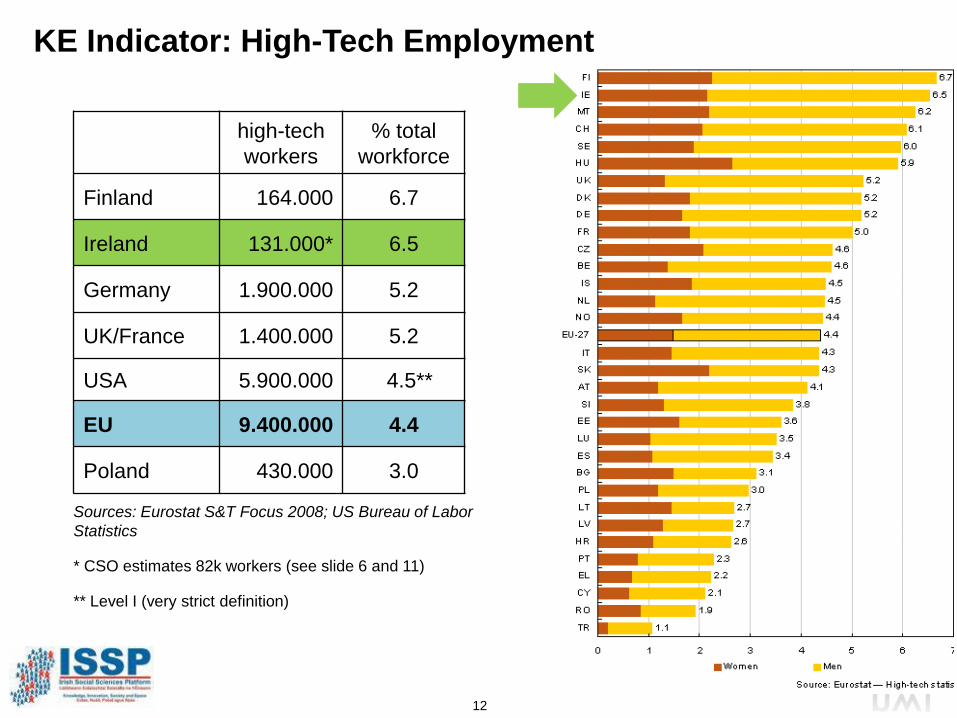

Sources: Eurostat S&T Focus 2008; US Bureau of Labor

Statistics

* CSO estimates 82k workers (see slide 6 and 11)

** Level I (very strict definition)

KE Indicator: High-Tech Employment

high-tech

workers

% total

workforce

Finland 164.000 6.7

Ireland 131.000* 6.5

Germany 1.900.000 5.2

UK/France 1.400.000 5.2

USA 5.900.000 4.5**

EU 9.400.000 4.4

Poland 430.000 3.0

13

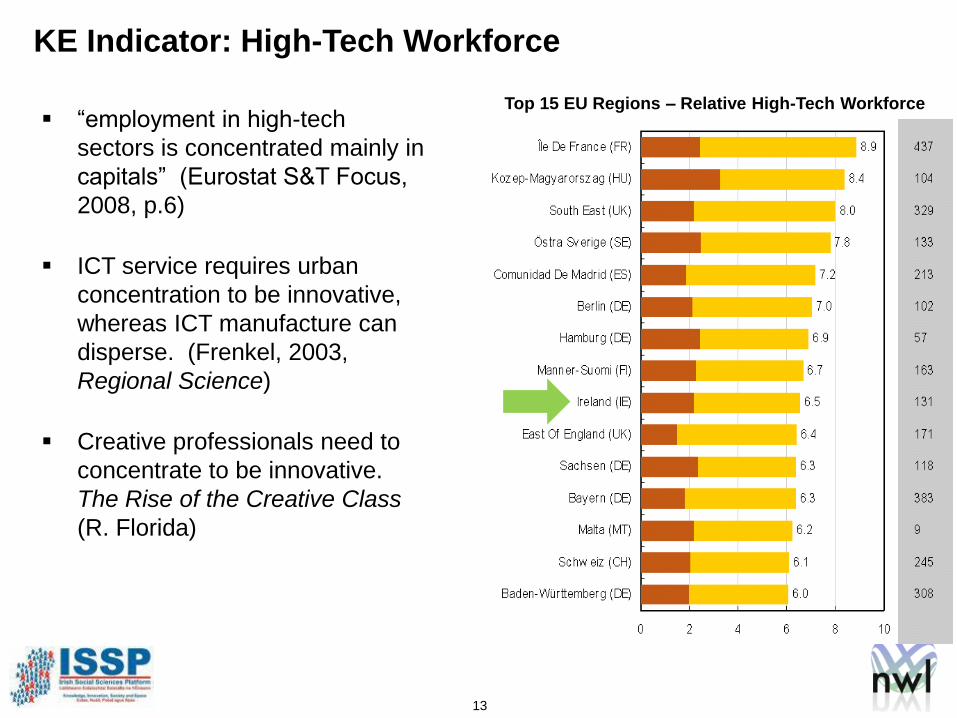

KE Indicator: High-Tech Workforce

“employment in high-tech

sectors is concentrated mainly in

capitals” (Eurostat S&T Focus,

2008, p.6)

ICT service requires urban

concentration to be innovative,

whereas ICT manufacture can

disperse. (Frenkel, 2003,

Regional Science)

Creative professionals need to

concentrate to be innovative.

The Rise of the Creative Class

(R. Florida)

Top 15 EU Regions – Relative High-Tech Workforce

14

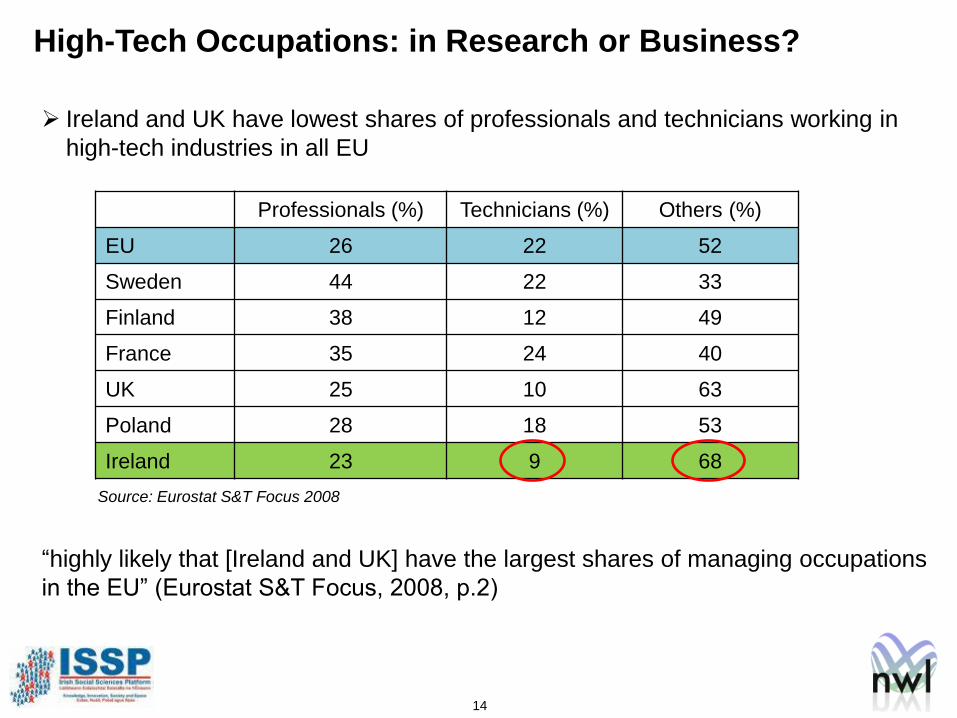

High-Tech Occupations: in Research or Business?

Professionals (%) Technicians (%) Others (%)

EU 26 22 52

Sweden 44 22 33

Finland 38 12 49

France 35 24 40

UK 25 10 63

Poland 28 18 53

Ireland 23 9 68

Ireland and UK have lowest shares of professionals and technicians working in

high-tech industries in all EU

“highly likely that [Ireland and UK] have the largest shares of managing occupations

in the EU” (Eurostat S&T Focus, 2008, p.2)

Source: Eurostat S&T Focus 2008

15

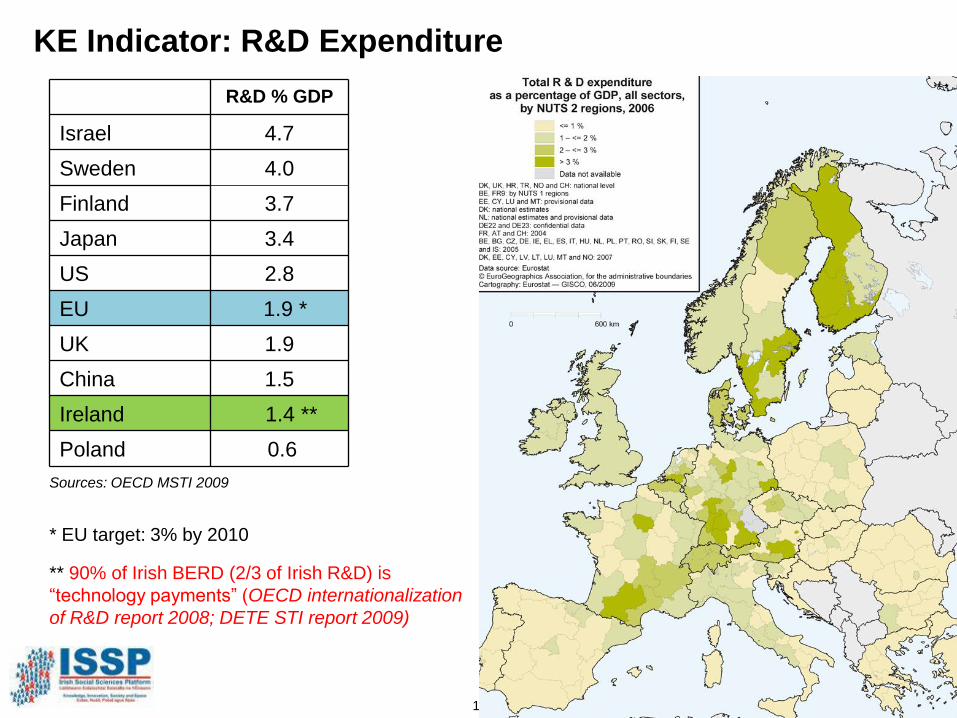

KE Indicator: R&D Expenditure

Sources: OECD MSTI 2009

* EU target: 3% by 2010

** 90% of Irish BERD (2/3 of Irish R&D) is

“technology payments” (OECD internationalization

of R&D report 2008; DETE STI report 2009)

R&D % GDP

Israel 4.7

Sweden 4.0

Finland 3.7

Japan 3.4

US 2.8

EU 1.9 *

UK 1.9

China 1.5

Ireland 1.4 **

Poland 0.6

16

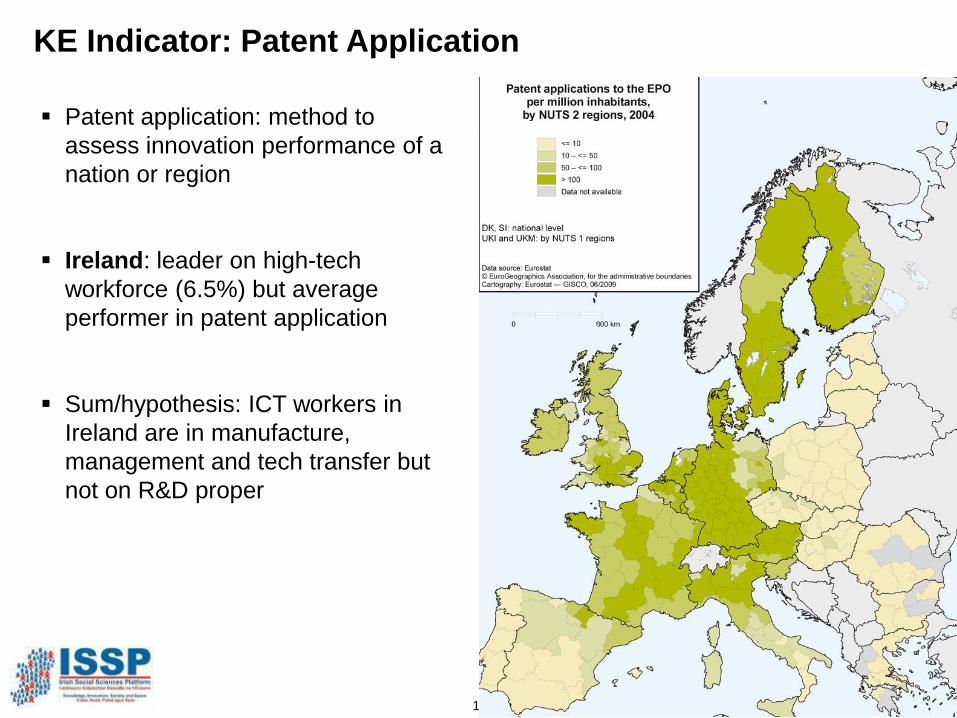

KE Indicator: Patent Application

Patent application: method to

assess innovation performance of a

nation or region

Ireland: leader on high-tech

workforce (6.5%) but average

performer in patent application

Sum/hypothesis: ICT workers in

Ireland are in manufacture,

management and tech transfer but

not on R&D proper

17

Regions

18

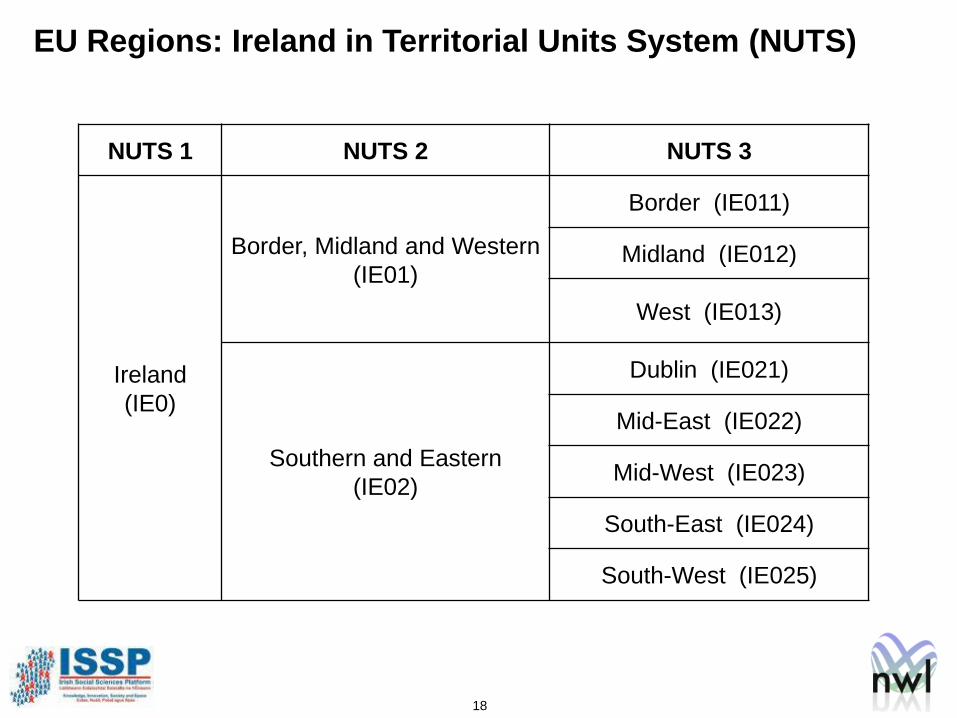

EU Regions: Ireland in Territorial Units System (NUTS)

NUTS 1 NUTS 2 NUTS 3

Ireland

(IE0)

Border, Midland and Western

(IE01)

Border (IE011)

Midland (IE012)

West (IE013)

Southern and Eastern

(IE02)

Dublin (IE021)

Mid-East (IE022)

Mid-West (IE023)

South-East (IE024)

South-West (IE025)

19

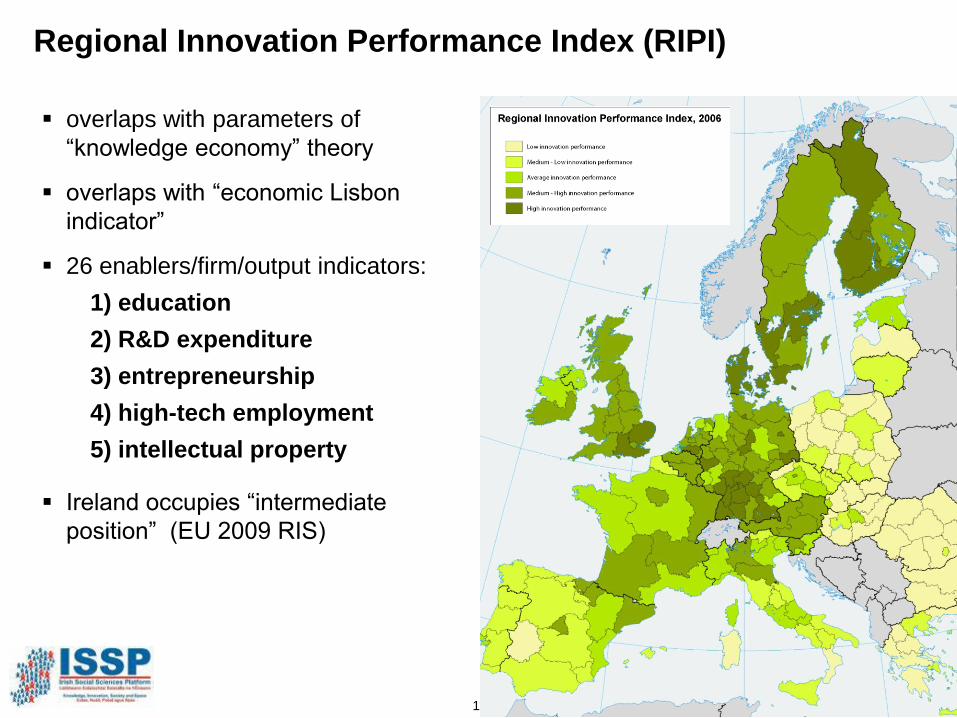

Regional Innovation Performance Index (RIPI)

overlaps with parameters of

“knowledge economy” theory

overlaps with “economic Lisbon

indicator”

26 enablers/firm/output indicators:

1) education

2) R&D expenditure

3) entrepreneurship

4) high-tech employment

5) intellectual property

Ireland occupies “intermediate

position” (EU 2009 RIS)

20

Context:

economic globalization

EU system decentralization

Regions in EU Policy:

economic growth: derives from “more weight to local level resources”

integrating Cohesion and Innovation:

• Integrating “smart” and “inclusive” growth (EU 2020 Strategy)

• “Regions should focus on the integration of R&D and innovation into regional

development strategies”

multi-level governance

Rise of Regions in the EU:

21

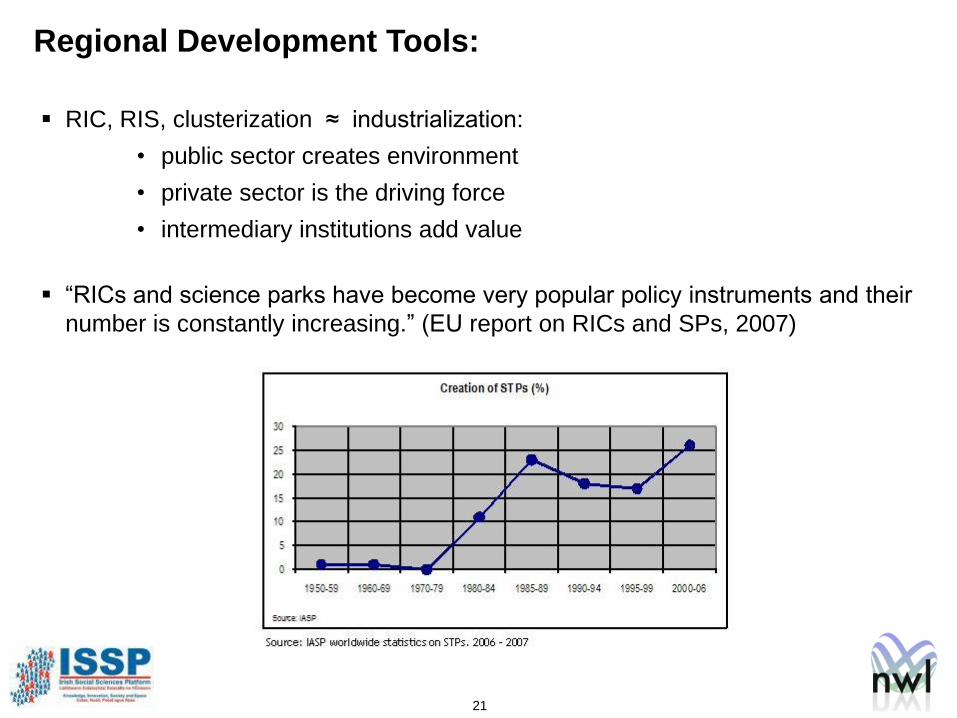

RIC, RIS, clusterization ≈ industrialization:

• public sector creates environment

• private sector is the driving force

• intermediary institutions add value

“RICs and science parks have become very popular policy instruments and their

number is constantly increasing.” (EU report on RICs and SPs, 2007)

Regional Development Tools:

22

1. Strong science base

2. Above-average entrepreneurial culture

3. Generates ‘gazelles’ and RDTI absorption by SME

4. Attractive to talent professionals and students

5. Skilled workforce

6. Financial resources: seed and venture capital

7. Business support services

8. Good location for research centers and MNCs (life quality, transport)

9. Effective and informal networks

10. Support to international/transnational networks

Ten Characteristics of Successful RICs (by EURADA)

23

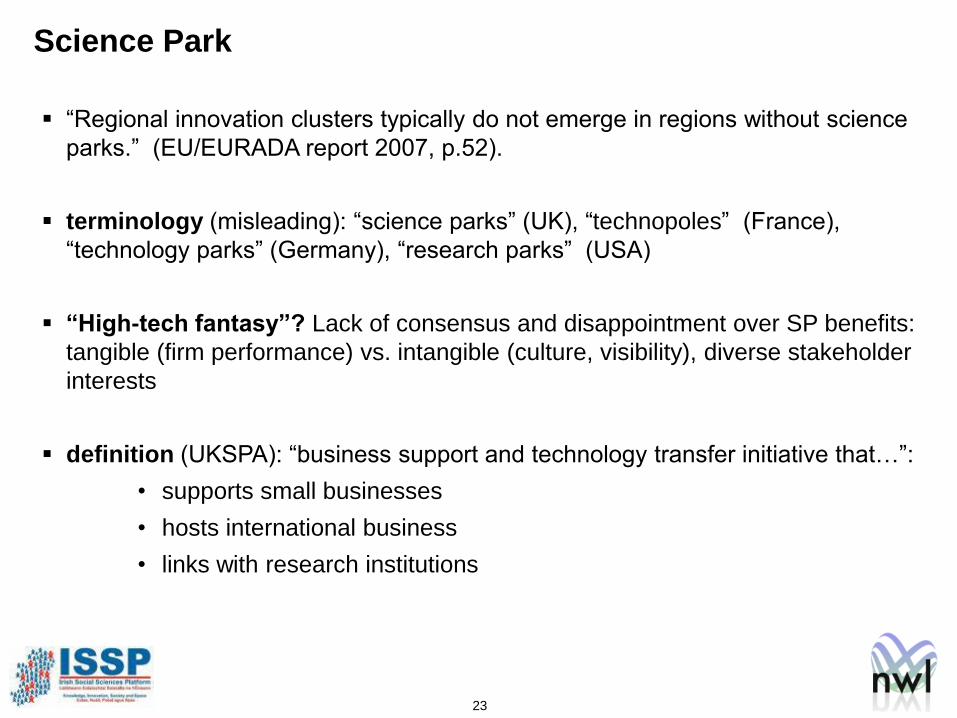

“Regional innovation clusters typically do not emerge in regions without science

parks.” (EU/EURADA report 2007, p.52).

terminology (misleading): “science parks” (UK), “technopoles” (France),

“technology parks” (Germany), “research parks” (USA)

“High-tech fantasy”? Lack of consensus and disappointment over SP benefits:

tangible (firm performance) vs. intangible (culture, visibility), diverse stakeholder

interests

definition (UKSPA): “business support and technology transfer initiative that…”:

• supports small businesses

• hosts international business

• links with research institutions

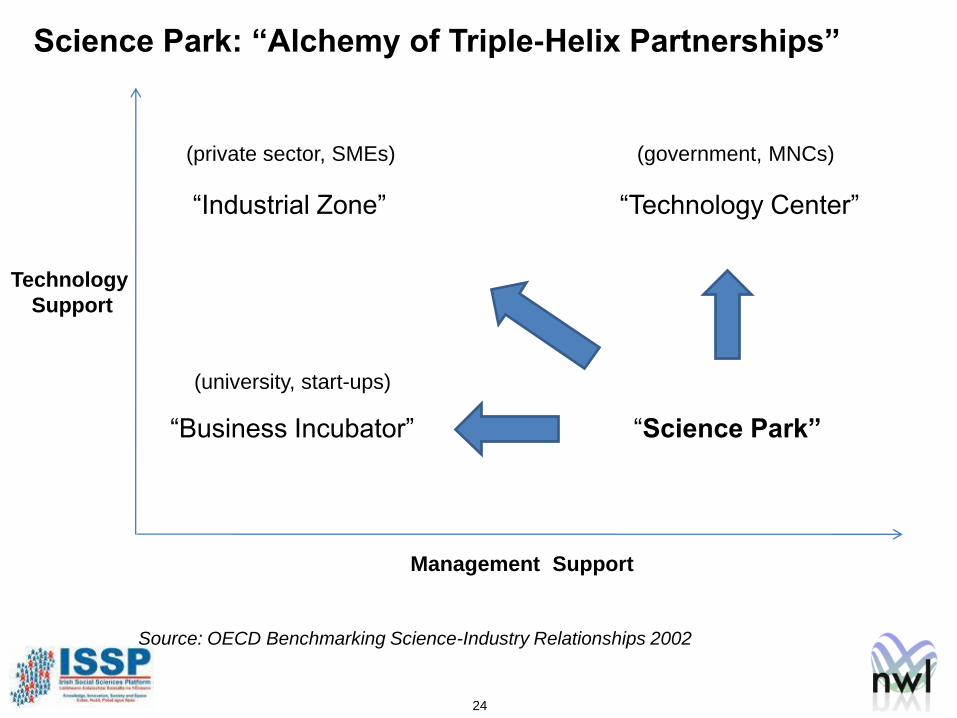

Science Park

24

“Industrial Zone” “Technology Center”

Science Park: “Alchemy of Triple-Helix Partnerships”

Management Support

“Business Incubator” “Science Park”

Technology

Support

(private sector, SMEs)

(university, start-ups)

(government, MNCs)

Source: OECD Benchmarking Science-Industry Relationships 2002

25

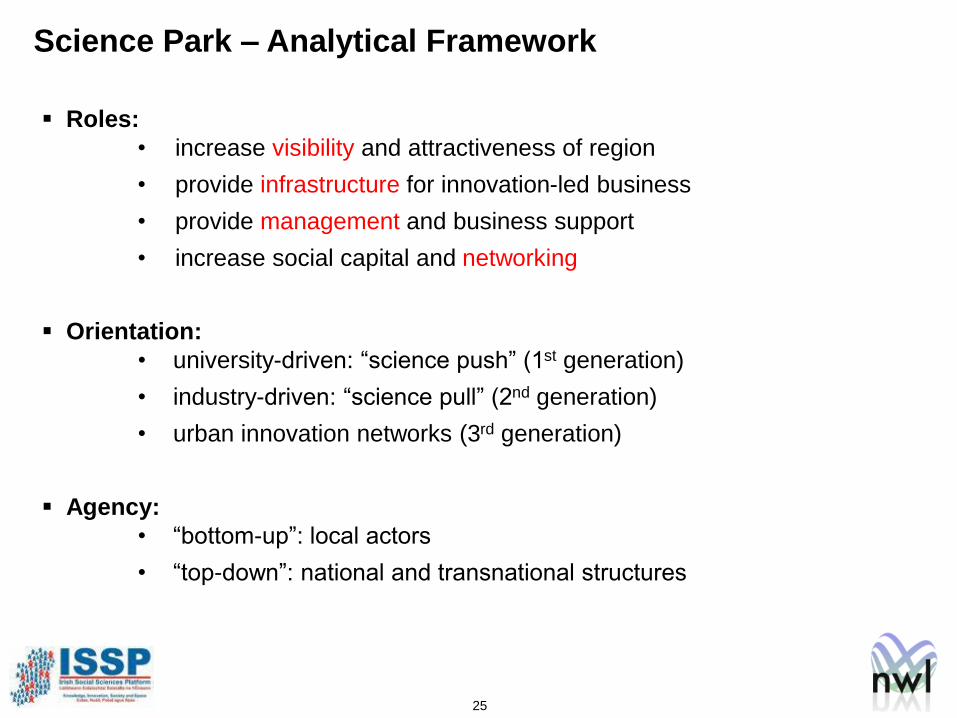

Roles:

• increase visibility and attractiveness of region

• provide infrastructure for innovation-led business

• provide management and business support

• increase social capital and networking

Orientation:

• university-driven: “science push” (1st generation)

• industry-driven: “science pull” (2nd generation)

• urban innovation networks (3rd generation)

Agency:

• “bottom-up”: local actors

• “top-down”: national and transnational structures

Science Park – Analytical Framework

26

Science Parks: International Cases

27

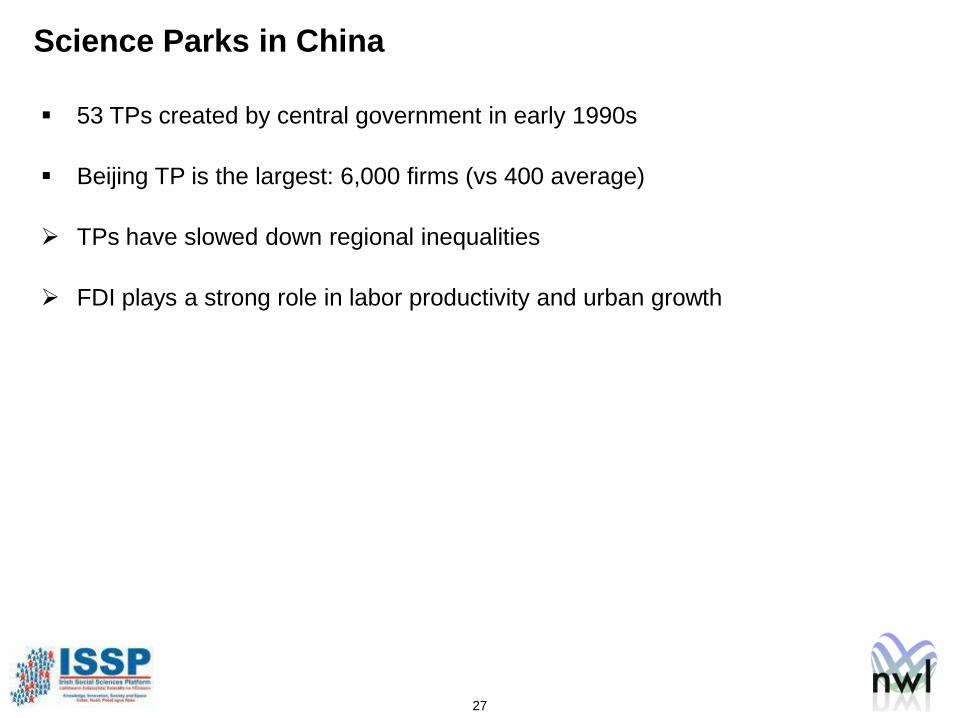

53 TPs created by central government in early 1990s

Beijing TP is the largest: 6,000 firms (vs 400 average)

TPs have slowed down regional inequalities

FDI plays a strong role in labor productivity and urban growth

Science Parks in China

28

Background: Japanese and US manufacture capital into Export Platforms

(Taiwan, S. Korea, Thailand)

Hinschu Science-Based Industrial Park (300 firms, 96.000 workers)

High level of vertical integration and internal competition: industrialization,

clusterization

Losing HR and infrastructure: investments into China: transnational connections

Science Parks in Taiwan

29

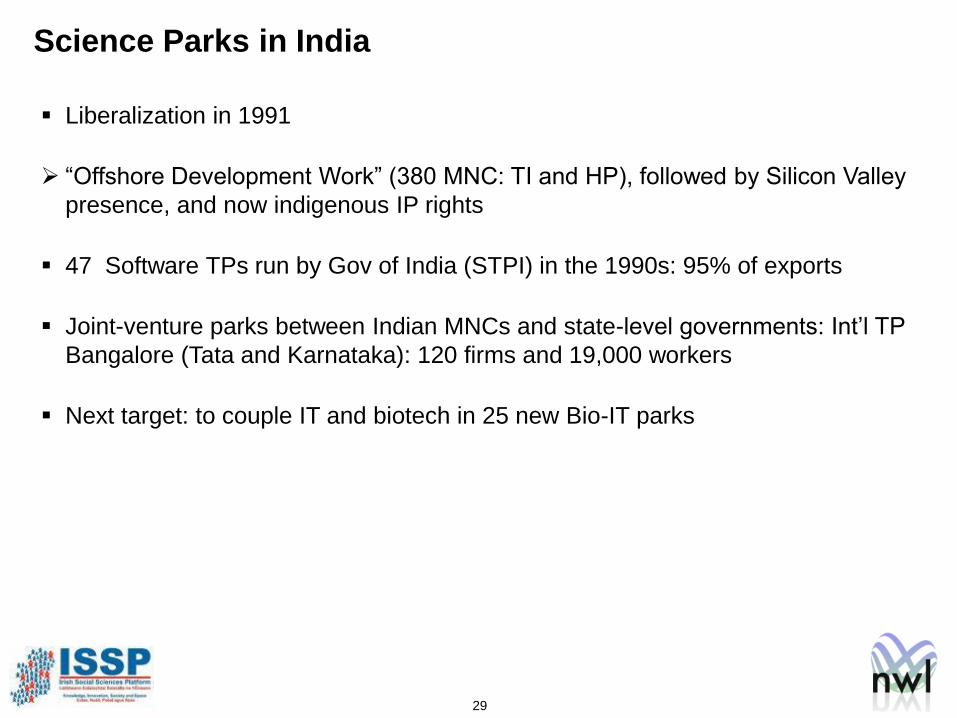

Liberalization in 1991

“Offshore Development Work” (380 MNC: TI and HP), followed by Silicon Valley

presence, and now indigenous IP rights

47 Software TPs run by Gov of India (STPI) in the 1990s: 95% of exports

Joint-venture parks between Indian MNCs and state-level governments: Int’l TP

Bangalore (Tata and Karnataka): 120 firms and 19,000 workers

Next target: to couple IT and biotech in 25 new Bio-IT parks

Science Parks in India

30

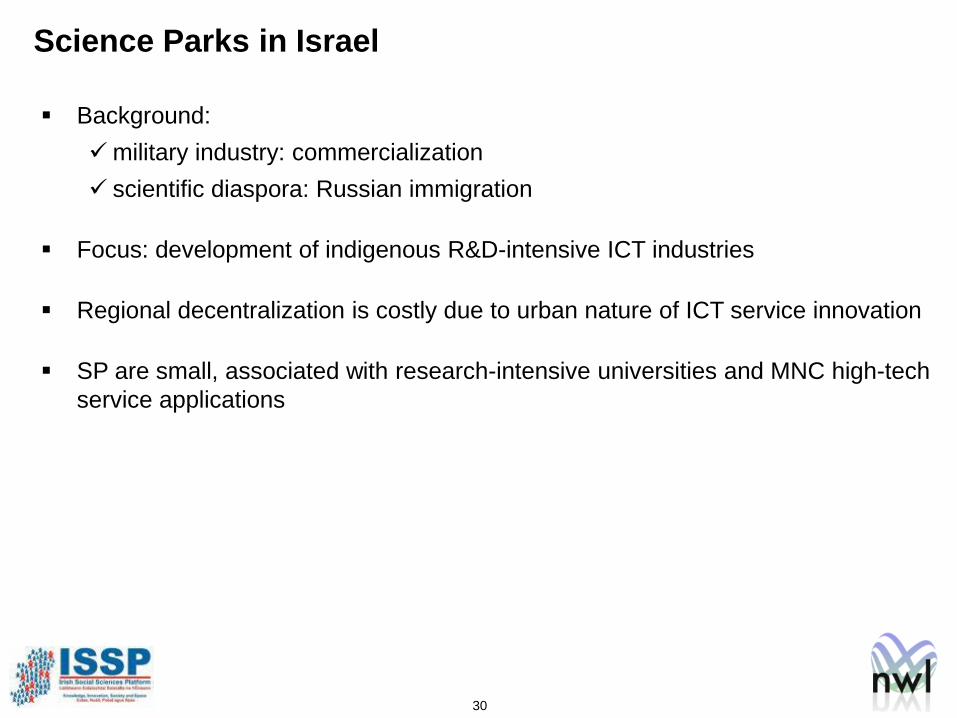

Background:

military industry: commercialization

scientific diaspora: Russian immigration

Focus: development of indigenous R&D-intensive ICT industries

Regional decentralization is costly due to urban nature of ICT service innovation

SP are small, associated with research-intensive universities and MNC high-tech

service applications

Science Parks in Israel

31

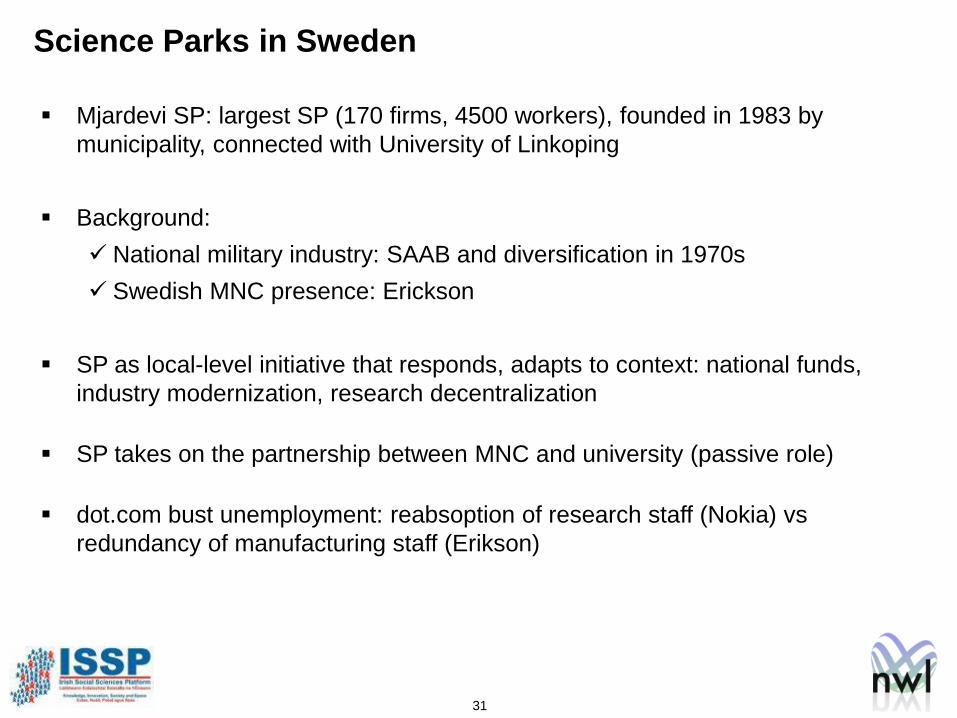

Mjardevi SP: largest SP (170 firms, 4500 workers), founded in 1983 by

municipality, connected with University of Linkoping

Background:

National military industry: SAAB and diversification in 1970s

Swedish MNC presence: Erickson

SP as local-level initiative that responds, adapts to context: national funds,

industry modernization, research decentralization

SP takes on the partnership between MNC and university (passive role)

dot.com bust unemployment: reabsoption of research staff (Nokia) vs

redundancy of manufacturing staff (Erikson)

Science Parks in Sweden

32

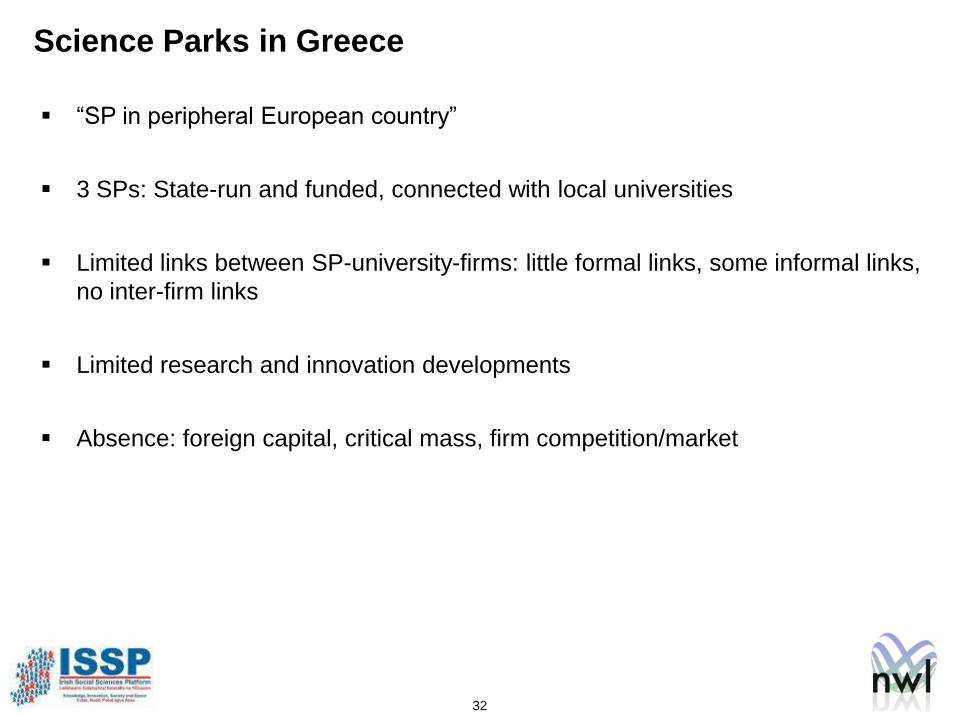

“SP in peripheral European country”

3 SPs: State-run and funded, connected with local universities

Limited links between SP-university-firms: little formal links, some informal links,

no inter-firm links

Limited research and innovation developments

Absence: foreign capital, critical mass, firm competition/market

Science Parks in Greece

33

Conclusions

34

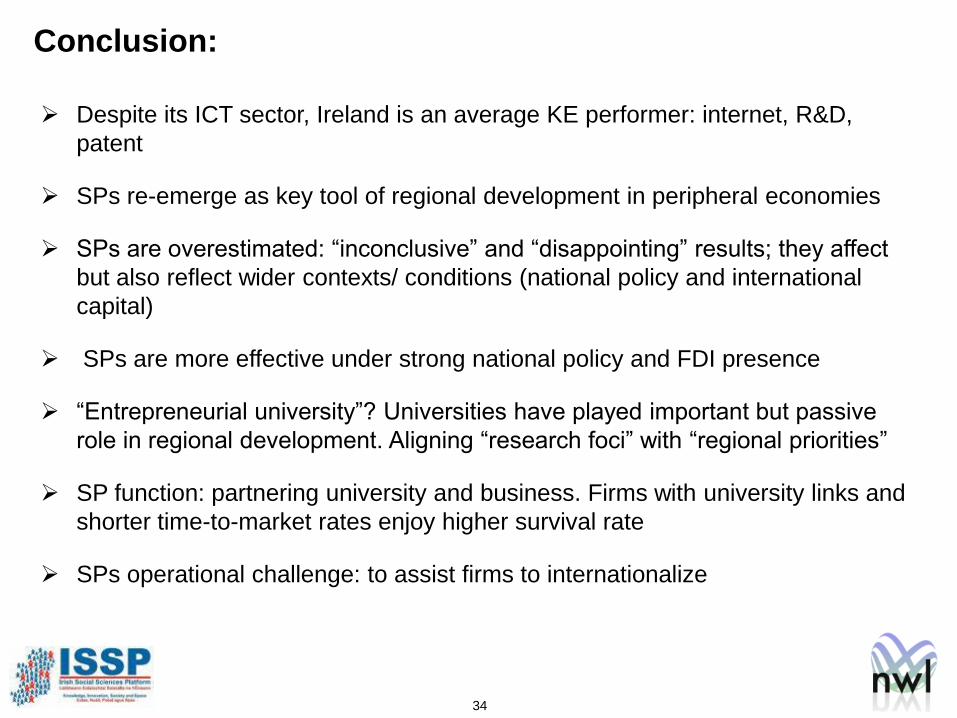

Despite its ICT sector, Ireland is an average KE performer: internet, R&D,

patent

SPs re-emerge as key tool of regional development in peripheral economies

SPs are overestimated: “inconclusive” and “disappointing” results; they affect

but also reflect wider contexts/ conditions (national policy and international

capital)

SPs are more effective under strong national policy and FDI presence

“Entrepreneurial university”? Universities have played important but passive

role in regional development. Aligning “research foci” with “regional priorities”

SP function: partnering university and business. Firms with university links and

shorter time-to-market rates enjoy higher survival rate

SPs operational challenge: to assist firms to internationalize

Conclusion: