Embed Size (px)

Citation preview

Financial Planning and Forecasting

Financial PlanningThe projection of sales, income, and assets based on alternative production and marketing strategies, as well as the determination of the resources needed to achieve these projection is called financial planning.Financial planning is assessing your business' financial situation, determining its objectives and formulating financial strategies of how to achieve them. Financial planning should become a continuous activity where the plan is reviewed regularly and performance measured against specific devised targets.

Financial Planning Types1. Long-Term (Strategic) Financial Plans: An investment plan or

strategy with a term of usually longer than one year. A long-term financial plan involves more uncertainty than anything short-term because, typically, market trends are more easily predictable in the short term.

2. Operating (Short-Term) Financial Planning: A financial plan outlining investment and other financial goals for the coming fiscal year. Short-term financial plans involve less uncertainty than long-term financial plans because, generally speaking, market trends are more easily predictable in the short term. Short-term financial plans usually invest in short-lived securities, such as T bills. A short-term financial plan aims to achieve goals that would be beneficial for one's long-term financial plan.

Long-term (Strategic) Financial PlansLong-term (strategic) financial plans lay out a company’s planned financial actions and the anticipated impact of those actions over periods ranging from 2 to 10 years.These plans are one component of a company’s integrated strategic plan (along with production and marketing plans) that guide a company toward achievement of its goals.Long-term financial plans consider a number of financial activities including:

Proposed fixed asset investments Research and development activities Marketing and product development Capital structure Sources of financing

These plans are generally supported by a series of annual budgets and profit plans.

Short-Term (Operating) Financial PlansShort-term (operating) financial plans specify short-term

financial actions and the anticipated impact of those actions and typically cover a 1- to 2-year operating period.

Key inputs include the sales forecast and other operating and financial data.

Key outputs include operating budgets, the cash budget, and pro forma financial statements.

short-term financial planning begins with a sales forecast. From this sales forecast, production plans are developed that

consider lead times and raw material requirements. From the production plans, direct labor, factory overhead,

and operating expense estimates are developed. From this information, the pro forma income statement and cash

budget are prepared—ultimately leading to the development of the pro forma balance sheet.

Cash Planning: Cash Budgets

The cash budget is a statement of the firm’s planned inflows and outflows of cash.

It is used to estimate short-term cash requirements with particular attention to anticipated cash surpluses and shortfalls.

Surpluses must be invested and shortfalls must be funded.

The cash budget is a useful tool for determining the timing of cash inflows and outflows during a given period.

Typically, monthly budgets are developed covering a 1-year time period.

Cash Planning: Cash Budgets….

The cash budget begins with a sales forecast, which is simply a prediction of the sales activity during a given period.

A prerequisite to the sales forecast is a forecast for the economy, the industry, the company, and other external and internal factors that might influence company sales.

The sales forecast is then used as a basis for estimating the monthly cash inflows that will result from projected sales—and outflows related to production, overhead and other expenses.

Steps in Financial Forecasting

Forecast salesProject the assets needed to support salesProject internally generated fundsProject outside funds neededDecide how to raise fundsSee effects of plan on ratios and stock

price

Depreciation Depreciation: The systematic charging of a portion of the costs of fixed assets against annual revenues over time is called Depreciation. This is a historical cost of fixed assets over time.Depreciable life of an Asset :The time period over which an asset is depreciated is called depreciable life of that asset.

Depreciable Value of an asset

Under the basic MACRS procedures, the depreciable value of an asset (the amount to be depreciated) is its full cost, including outlays for installation. No adjustment is required for expected salvage value.Example: Orin Corporation acquired a new machine at a price of $38000 and installation costs of $2000. What is the depreciable value of the machine?Now, the Depreciable Value is: $38000

$ 2000 $40000

MACRS: What is it?One of the depreciation methods is MACRS which stands for Modified Accelerated Cost Recovery System. It is used to determine the depreciation of assets for tax purpose.Some other depreciation methods are: Straight-line; Double-Declining balance and sum-of-the-year-digits.

3 years: Research equipment and certain special tools.5 years: Computers, typewriters, copiers, duplicating equipment, cars, light duty trucks, qualified technological equipment, and similar assets.7 years: Office furniture, fixtures, most manufacturing equipment, railroad track, and single-purpose agricultural and horticultural structures.10 years Equipment used in petroleum refining or in the manufacture of tobacco products and certain food products.

First Four Property Classes Under MACRS

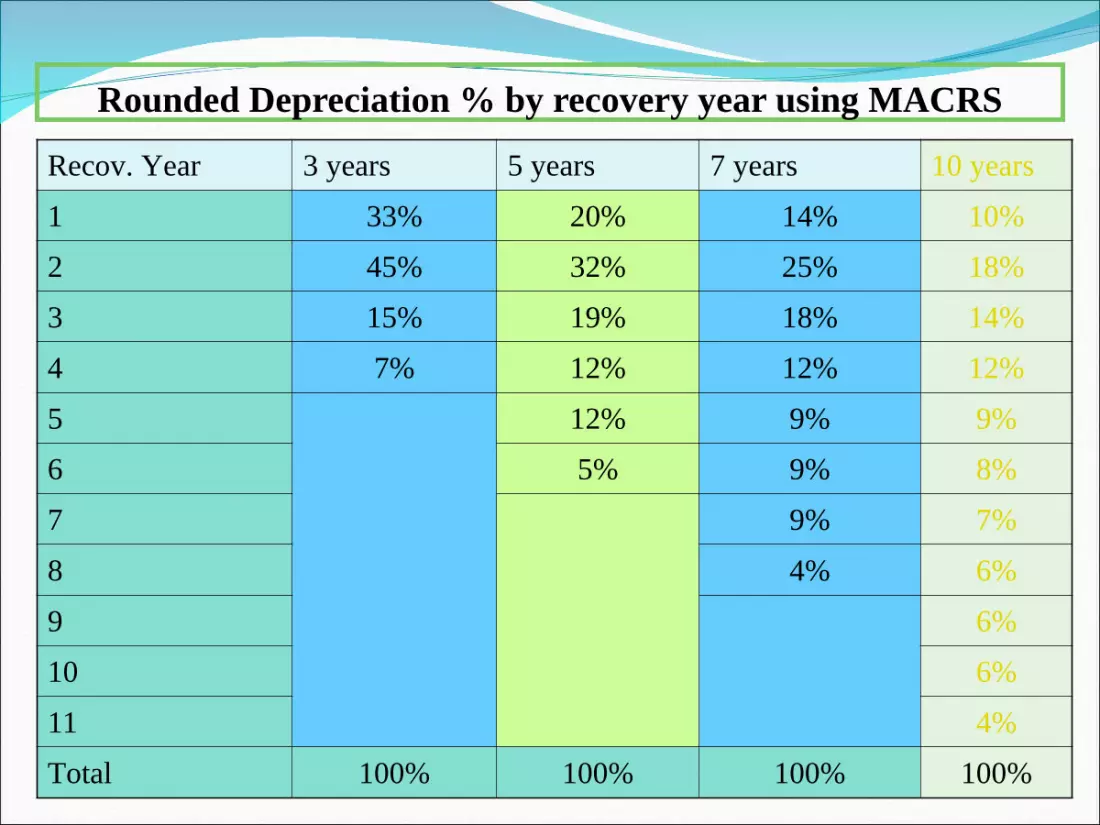

Rounded Depreciation % by recovery year using MACRS

Recov. Year 3 years 5 years 7 years 10 years

1 33% 20% 14% 10%

2 45% 32% 25% 18%

3 15% 19% 18% 14%

4 7% 12% 12% 12%

5 12% 9% 9%

6 5% 9% 8%

7 9% 7%

8 4% 6%

9 6%

10 6%

11 4%

Total 100% 100% 100% 100%

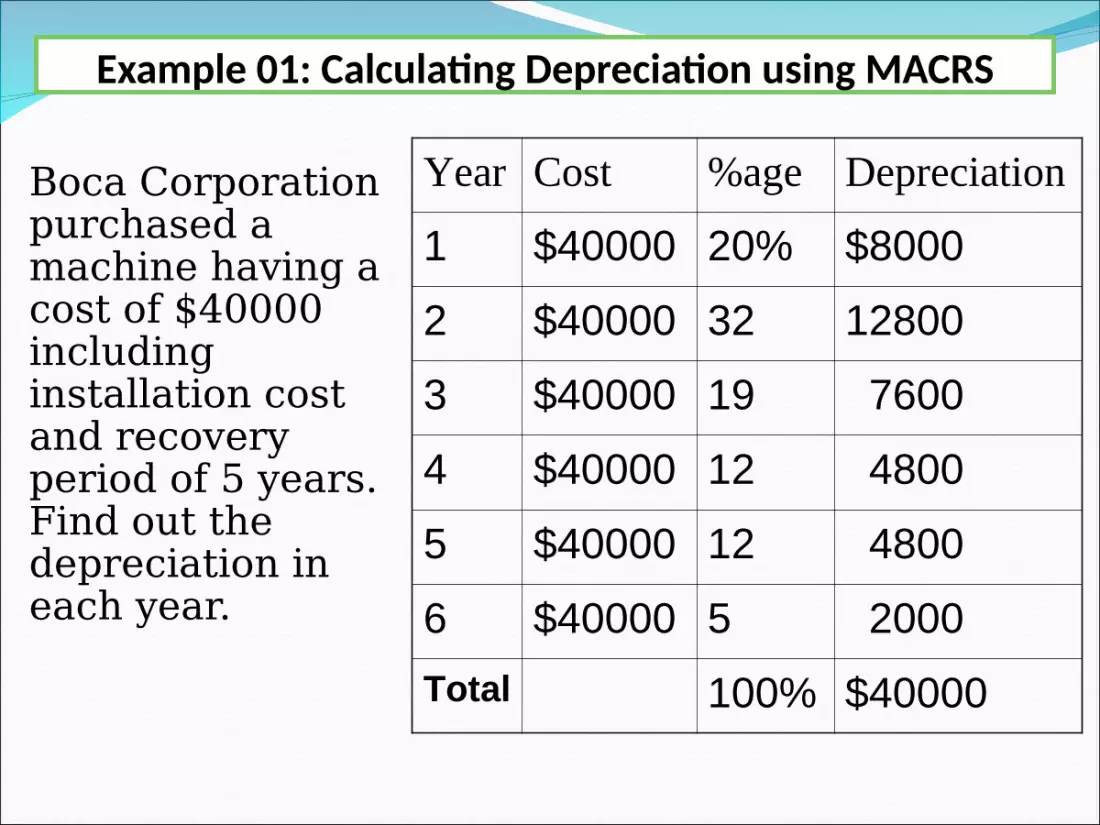

Example 01: Calculating Depreciation using MACRS

Boca Corporation purchased a machine having a cost of $40000 including installation cost and recovery period of 5 years. Find out the depreciation in each year.

Year Cost %age Depreciation

1 $40000 20% $8000

2 $40000 32 12800

3 $40000 19 7600

4 $40000 12 4800

5 $40000 12 4800

6 $40000 5 2000Total 100% $40000

Practice 01: Calculating Depreciation

On March 20, 2007, Norton Systems acquired two new assets. Asset A was research equipment costing $17000 and having a 3-year recovery period. Asset B was duplicating equipment having an installed cost of $45000 and a 5-year recovery period. Using MACRS depreciation percentages, prepare a depreciation schedule for each of these assets.

Firm’s Cash Flows1. Operating Cash Flow

Cashflow directly related to sale and production of the firm’s products and services.

2. Investment Cash FlowCashflow associated with purchase and sale of both fixed assets and business interests.

3. Financing Cash FlowsCashflows that result from debt and equity financing transactions; includes incurrence and repayment of debt, cash inflow from the sale of stock, and cash outflows to pay cash dividends or repurchase stock.

4. Free cash flowsThe amount of cashflow available to investors after the firm has met all operating needs and paid for investments in net fixed assets and not current assets.

Baker Corporation Income Statement, 2008

Sales revenue $ 1700Less: Cost of Goods Sold (1000)Gross Profit $ 700Less: Operating Expenses:

Selling Expenses ($ 110)Lease exp ($120)Depreciation exp ($100)

Total Operating Exp ($ 330)Earnings Before Interest and Taxes (EBIT) $ 370Less Interest Exp ($ 70)Earnings Before Taxes (EBT) $ 300Less: Taxes @ 40% ($ 120)Net Profit After Taxes $180Less: Preferred stock dividend ($ 10)Earnings Available to Common stockholders $170

Example 01: Calculating Operating Cashflow

Calculate Baker Corporation’s Operating cashflow for 2008 from the given income statement.Solution: OCF = EBIT – Taxes + DepreciationOCF = $370 – $120 + $100OCF = $350

A firm’s operating cash flow (OCF) is the cash flow it generates from its normal operations—producing and selling its output of goods or services

Free cash Flows

FCF = OCF – NFAI – NCAIHere, NFAI = Net Fixed Asset InvestmentNCAI = Net Current Asset InvestmentNFAI = Change in net fixed Assets +

Depreciation NCAI = Change in Current Assets – Change in

(Accounts payable + Accruals)

The firm’s free cash flow (FCF) represents the amount of cash flow available to investors—the providers of debt (creditors) and equity (owners)—after the firm has met all operating needs and paid for investments in net fixed assets and net current assets. It represents the summation of the net amount of cash flow available to creditors and owners during the period.

Example 02: Calculating NFAI

The Baker Corporations 2007 fixed asset was $1000 and 2008 fixed asset was $1200 and the depreciation for 2008 was $100. Find out the Baker’s NFAI.Solution:Fixed Assets in 2008 = $ 1200Fixed Assets in 2007 = $ 1000 Change in Net Fixed Asset = $200So,NFAI = Change in net fixed Asset + Depreciation

= $ 200 + $ 100= $ 300

Example 03: Calculating NCAIThe following information is available for Baker Company’s 2008 and 2007 Balance Sheet statement.

2008 2007

Current Asset $2000 $1900

Accounts Payable $700 $500

Accruals $100 $200

NCAI = Change in Current Assets – Change in (Accounts payable + Accruals)

NCAI = $ 100 - $ 100= $ 0

Example 04: Calculating FCF

From the previous example 01, 02 and 03, calculate the Free Cash Flow for Baker Company.Solution: FCF = OCF – NFAI – NCAIFCF = $350 - $ 300 - $ 0FCF = $ 50

2008 2007Sales $1500 $1435

Cost of goods sold (1230) (1176.7)Depreciation (50) (40)

Earnings before interests and Taxes (EBIT) 130 133.3EBT 90 98.3

Taxes (40%) (36.0) (39.3)Net income 54.0 59.0Total Current Assets $465.0 400.0Total Fixed Assets 380.0 350.0

Total Assets $845.0 $750.0===== =====

Accounts payable $70.0 $60.0Accruals 60.0 55.0Long term bonds 300.0 255.0

Calculate FCF from the following information:

The Bangla-Longla Company has purchased an asset which cost Taka 50000 and an installation charge of Taka 10,000 in the year of 2005 with five years of working life. The following information are given for Bangla-Longla Company. Calculate the FCF from the given information for 2007.

2007 2006EBIT Tk 27500 ------------Depreciation Tk ?????? ------------Current Assets Tk 8200 Tk 6800Fixed Assets Tk 14800 Tk 15000Accounts Payable Tk 1600 Tk 1500Accruals Tk 200 Tk 300Taxes Tk 933 ------------Net Profit Tk 1400 ------------

Preparation1. Try to answer all of the Self-Test

question within the chapter given in your text book.

2. Try to understand the difference between Accounting Cashflow and Financing Cashflow.

3. Try to prepare a Pro-forma Income statement.

4. Try to solve following relevant types of problem from the end chapter: Depreciation, OCF, NFAI, NCAI and FCF.