Embed Size (px)

Citation preview

Debt Issuer: Credit Rating Agency Relations and the Trinityof Solicitude: An Empirical Study of the Role of Commitment

Angus Duff • Sandra Einig

Received: 24 April 2013 / Accepted: 7 April 2014

� Springer Science+Business Media Dordrecht 2014

Abstract Interest in credit ratings agencies and their role

in financial markets is at an all-time high. Concerns about a

lack of transparency concerning process, conflicts of

interest, and limited competition are frequently discussed

by politicians, regulators and other commentators. These

issues we term the credit ratings agency (CRA) trinity of

solicitude. We shed some light on this trinity by consid-

ering the unique relationship that exists between corporate

borrowers (debt issuers) and the CRAs they engage to rate

their securities. The exchange relationships literature is

used to create a model where commitment plays a central

role. Technical qualities, relationship qualities and depen-

dence are theorised as antecedents of commitment, which

is described by two constructs of affective commitment and

calculative commitment. The issuer’s intention to remain

with the CRA, their loyalty, is the consequence of com-

mitment. The model is operationalized by means of a

survey questionnaire administered to issuers of corporate

debt in the United Kingdom. As expected, perceptions of

the quality of the relationship and affective commitment

play an important role in CRA-issuer relations. However,

contrary to expectations, the technical quality of the rating

and issuer dependence on the CRA play little role in

determining commitment and continuance. The implica-

tions of these findings are discussed along with areas for

future research.

Keywords Credit rating agency � Trinity of solicitude �Conflict of interest � Transparency � Competition �Relationship quality � Technical quality � Calculative

commitment � Affective commitment

Introduction

A satisfactory credit rating from a reputable credit rating

agency (CRA) is required to enable the corporate borrower

to raise debt finance at an economic rate via the capital

markets. The borrower alone is responsible for selecting

the CRA, or multiple CRAs, used in evaluating the cred-

itworthiness of the debt issue. The ratings process is typi-

cally described by issuers of debt as onerous and expensive

in terms of fees and, especially, management time. Con-

sequently, the ratee is a forced participant in the ratings

process, being required to furnish the CRA with the nec-

essary information to secure an adequate rating for their

debt security, remunerate the CRA, and continue to supply

the rator with the necessary financial and strategic infor-

mation required for the CRA to continue to support or

enhance the rating provided at the primary issuance.

Relations between issuers and CRAs are frequently

described as adversary; for example, where the issuer is

unhappy with the initial rating, or subsequent downgrades

that adversely affect other areas of their business, or spe-

cific concerns with CRA staff (e.g. Duff and Einig 2007,

2009b; Langohr and Langohr 2008; Sinclair 2005).

The ratings process has been the subject of considerable

comment and censure on a global scale over the past

15 years. Concerns have been repeatedly raised about

CRAs in their inability to foresee the Asia crisis in 1997 or

the corporate reporting scandals of the early part of this

century typified by Enron, Parmalat and WorldCom.

A. Duff (&)

Management Centre, University of the West of Scotland, Craigie

House, Craigie Park, Ayr KA8 0SS, UK

e-mail: [email protected]

S. Einig

Business School, Oxford Brookes University, Wheatley Campus,

Oxford OX33 1HX, UK

e-mail: [email protected]

123

J Bus Ethics

DOI 10.1007/s10551-014-2175-y

Similarly, they have been implicated in the subprime

mortgage debacle in the United States (US) of 2007 and

subsequent current global credit crisis. Typically, three

major concerns have been levelled at CRAs; this we term

the CRA trinity of solicitude. Its three elements are: (i) the

lack of transparency related to methodologies and pro-

cesses which are not easily replicable (e.g. Duff and Einig

2009a; Vishwanath and Kaufmann 2001); (ii) an inherent

conflict of interest in the ‘issuer pays’ business model

whereby the entity being rated also remunerates the rator

(e.g. Cantor and Packer 1994; Palazzo and Rethol 2008;

Sinclair 2005; Wilson 1987); and (iii) an oligopolistic

market place where just two CRAs command 80 % of

ratings business (e.g. Langohr and Langohr 2008; White

2009).1

For the purposes of this paper, the ratings process

defines a gatekeeping relationship whereby a client enga-

ges an agent to act in the best interests of a third party. In

the case of credit ratings, the debt issuer employs a CRA to

supply a rating attesting to the relative creditworthiness of

the debt security to investors and other parties evaluating

the borrower. Coffee (2006, p. 2) defines a gatekeeper as ‘a

professional who is positioned so as to be able to prevent

wrongdoing by withholding the necessary cooperation or

consent’. Gatekeeping relations are considered significant

for three reasons. First, the client who remunerates the

gatekeeper is usually an involuntary participant for either

reasons of statute, of regulation, or of market needs (Coffee

2006). Second, the gatekeeper has little contact with the

third party for whom they perform an agency role. CRAs,

for example, generally do not communicate directly with

the investment community and the ratings process occurs

beyond the public gaze (Langohr and Langohr 2008).

Finally, client-gatekeeper relations are usually enduring

because of the considerable investment the client needs to

make to establish the relationship and educate the gate-

keeper in the organisation’s strategy and peculiarities (Duff

and Einig 2007). In the instance of the ratings game, a

client engaging a new CRA needs to supply the new rator

with a range of confidential financial and strategic infor-

mation and grant access to senior management.

A significant canon of literature documents the nature of

gatekeeping relations in audit (e.g. Beattie et al. 2000; Duff

2009; Singh 2013). However, much less work considers

CRAs. The omission of CRAs from the corpus of gate-

keeper literature partly reflects the finance literatures

interest in empirical matters such as the determinants of

corporate credit ratings (e.g. Adams et al. 2003; Bennell

et al. 2006); regulatory and risk issues (e.g. Dorn 2012;

Eling and Schmeiser 2010; Staikouras 2011); and issues of

split ratings (e.g. Alsakka and ap Gwilym 2010, 2011; Al-

Sakka and ap Gwilym 2010). Given the implication of

CRAs in the on-going global financial crisis (Alcubilla and

del Pozo 2012; Scalet and Kelly 2012), their role in the US

subprime mortgage crisis (Munoz et al. 2012; Rom 2009),

and the continuing demands by politicians for increased

regulation and monitoring of the agencies, the research

lacuna in rator and ratee relations is highly significant.

Specifically, this paper develops: first, a framework that

describes three related criticisms of the contemporary CRA

industry that we term the CRA trinity of solicitude; and

second, a theoretical model of the issuer–CRA relationship,

adapted from the exchange relationships literature. The

CRA trinity of solitude has three components: conflicts of

interest inherent in the buyer pays business model the

industry uses; a lack of transparency in how ratings deci-

sions are arrived at; and the lack of competition within the

CRA industry reducing buyer choice and the availability of

a range of ratings information to allow investors to make an

informed decision.

Constructs of commitment are central to the theoretical

model which predicts issuer intentions of maintaining

relations with their existing rating supplier, the CRA. Spe-

cifically, two commitment constructs are created: calcula-

tive commitment, whereby the issuer maintains the

relationship purely because it is expedient; and affective

commitment, where the ratee genuinely values relations

with the rator and values their business and inter-personal

interactions. A ratee’s desire to continue to be rated by their

current rator is at the heart of the trinity of solicitude. The

lack of competition in ratings markets highlights the issue

of calculative commitment, whereby the securities issuer

believes they have few viable alternatives to the status quo.

The concerns surrounding conflicts of interest and the buyer

pays business model place issues of affective commitment

into sharp relief. The lack of transparency regarding CRA

processes and methodologies motivates an issuer’s desire to

create affective relations to better understand how the CRA

views the organisation and consequently how the rator may

be manipulated by improving communication and changing

the organisation’s financial strategy.

Measures of ratings quality (Duff and Einig 2009a) and

a construct measuring dependence developed for the pur-

poses of this study provide the antecedents of commitment

in the issuer–CRA relationship. A number of hypotheses

are developed from the exchange relationship literature.

The model is operationalized by means of a survey ques-

tionnaire administered to corporate issuers of debt in the

United Kingdom (UK) and empirically tested by means of

a structural equation model.

The paper contributes to the on-going debate concerning

the role of CRAs in the corporate debt market and global

1 S&P and Moody’s account for 80 % of the market share. Fitch, the

third largest CRA only accounts for 15 % (Langohr and Langohr

2008).

A. Duff, S. Einig

123

financial markets in general. In particular, the paper offers

a theoretical contribution by the applied use of the rela-

tional exchange literature to credit ratings research and a

policy contribution by highlighting the significance of ra-

tee–rator relations which are implicated in core criticisms

of the ratings industry namely conflicts of interest, whereby

the ratee remunerates the rator; a lack of transparency,

involving confidential information exchange between ratee

and rator; and an oligopolistic market, where competition

is limited and switching CRAs is problematic, i.e. ratees

are largely dependent on their rators.

The paper is structured as follows. The following section

describes credit ratings, the operation of the ratings

industry, and explains the trinity of solicitude to concep-

tualise contemporary concerns with the operation of the

credit rating industry. Then, we focus on the relational

exchange literature, and in particular the concept of com-

mitment, and its relevance to the ratings market and rela-

tions between CRAs (rators) and issuers (ratees). We then

report the results of a study that has examined empirically

the antecedents and consequences of different types of

commitment in rator–ratee relationships.

Literature Review and Development of Hypothesized

Commitment Model

Credit Ratings, the Ratings Industry and the Trinity

of Solicitude

Obtaining a rating is crucial for most borrowers in public

debt markets as it allows them access to a wide range of

investors. Unrated securities can only be placed privately,

so the investor base is much smaller. In addition, most

investors’ investment policies limit investment in unrated

debt securities. Ratings are most frequently used to estab-

lish minimum rating requirements for bond purchases, with

over 80 % of investors in Europe and the US using ratings

as part of their investment criteria (Cantor et al. 2007).

Ratings provide two important functions beyond the need

to fulfil investors’ internal investment guidelines. First, rat-

ings are used as a means of pre-selection. As debt markets are

global, most investors do not possess the resources to cover

the whole market. Therefore, ratings are used to preselect

potentially suitable bonds based on their ratings and subject

them to further analysis afterwards (Duff and Einig 2009b).

Without a rating, many securities would not be considered by

issuers, especially if the borrower is relatively unknown.

Second, rated securities usually achieve better pricing than

unrated securities (Hsueh and Liu 1993), a primary reason

for raising debt in capital markets compared to traditional

bank borrowing. Ratings are the most important determinant

of spreads (Gabbi and Sironi 2002).

The ratings industry has endured significant criticism as

a consequence of its role in the on-going global financial

crisis of 2008 and its antecedent the US subprime crisis of

2007. However, its role in other prominent financial

scandals has also been noted such as the Enron debacle of

2001 and the Asia crisis of 1997. Alcubilla and del Pozo

(2012), Langohr and Langohr (2008), Sinclair (2005) and

Sylla (2002) all provide compelling and authoritative his-

tories of the industry and its operation. Alongside these

histories sits significant journalistic, political, and regula-

tory debate concerning the role of CRAs and their ratings.

Three primary, and seemingly intractable, issues arise that

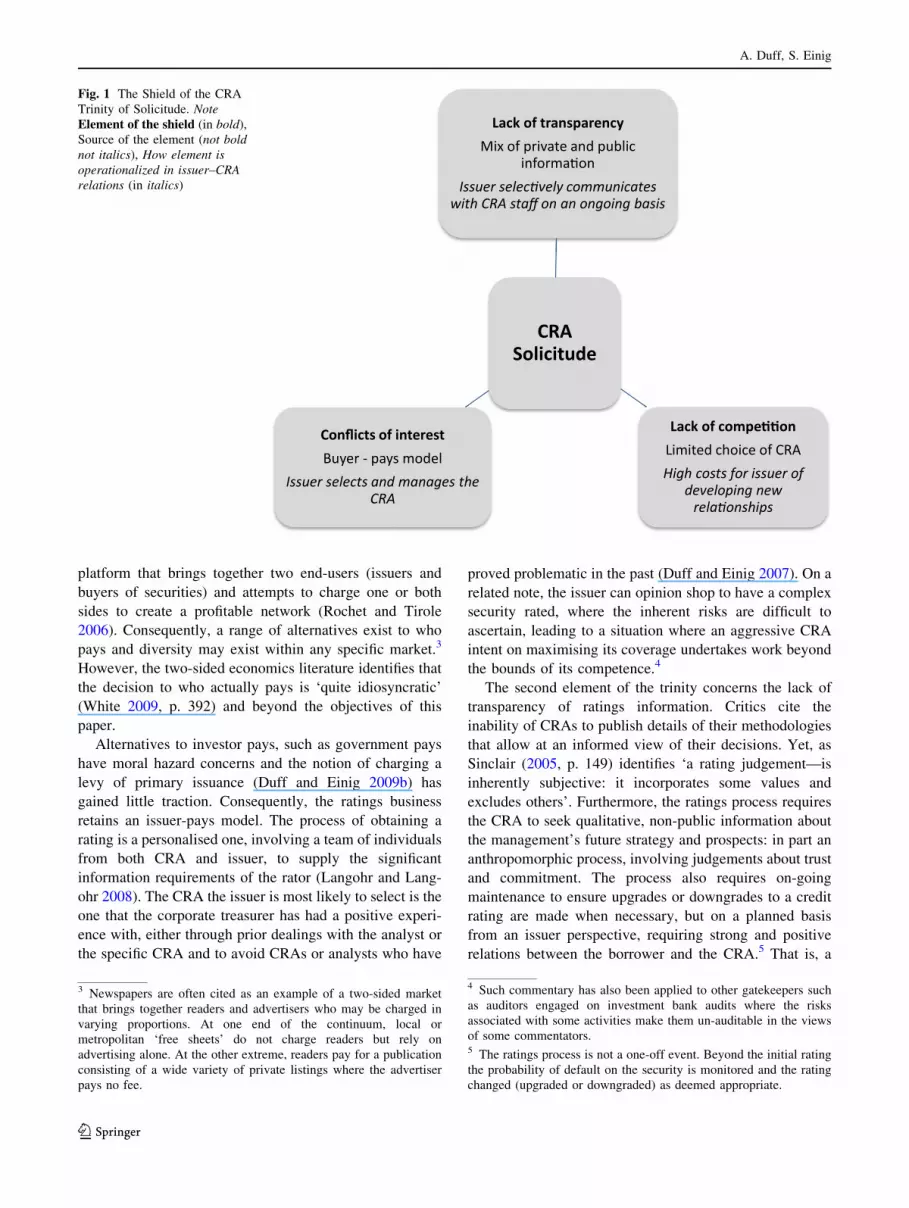

continually dog the ratings business.2 This is termed the

CRA Trinity of Solicitude, with Fig. 1 depicting the shield

of the trinity. In each of these issues, human relations that

exist between the personnel of the rate and the rator play a

pivotal role.

The first element concerns conflicts of interest, whereby

the issuer is responsible for appointing and remunerating

the CRA (see also Palazzo and Rethol 2008). This is

termed the buyer (issuer)-pays model. Specifically the

borrower’s treasurer selects a CRA they wish to rate their

security. Prior research (Duff and Einig 2007) indicate this

is on the basis of their prior experience with CRA per-

sonnel, where one agency or analyst may be preferred to

another for largely affective reasons. For example, Duff

and Einig (2009b, p. 114) quote an issuer thus:

The agency we chose I have dealt with in the past. I

was quite comfortable whereas in the previous role

I’ve had some fairly acrimonious discussions with the

other two. There are really just three agencies. So I

suppose it is logical that we used the one I was

happiest with.

The issuer-pays model is in contrast to the investor-pays

model that existed up until the 1970s (Sinclair 2005) where

investors paid a subscription to a CRA that effectively

published a book of corporate credit ratings. The ‘investor

pays’ model became redundant as the demand for ratings

grew from an institutional clientele and with changes in

news technology, more of this private information leaked

into the public market, the so-called ‘free-rider’ problem

(Sylla 2002). Essentially, the bond rating market is a two-

sided market whereby the ratings agencies create a

2 A fourth criticism is sometimes leveled at the ratings industry,

namely the competence of CRAs. However, this criticism was most

apparent at the time of the subprime bond crisis where rapid growth,

and subsequent failure, of the structured finance market—using

ratings labels akin the regular corporate and sovereign bonds—

resulting in significant censure and reputational loss for CRAs.

However, in the mainstream corporate and sovereign bond markets

CRAs have a longstanding track record of accurately predicting the

probability of failure (see Langohr and Langohr 2008, pp. 307–351

for a comprehensive analysis of the performance of credit ratings).

An Empirical Study of the Role of Commitment

123

platform that brings together two end-users (issuers and

buyers of securities) and attempts to charge one or both

sides to create a profitable network (Rochet and Tirole

2006). Consequently, a range of alternatives exist to who

pays and diversity may exist within any specific market.3

However, the two-sided economics literature identifies that

the decision to who actually pays is ‘quite idiosyncratic’

(White 2009, p. 392) and beyond the objectives of this

paper.

Alternatives to investor pays, such as government pays

have moral hazard concerns and the notion of charging a

levy of primary issuance (Duff and Einig 2009b) has

gained little traction. Consequently, the ratings business

retains an issuer-pays model. The process of obtaining a

rating is a personalised one, involving a team of individuals

from both CRA and issuer, to supply the significant

information requirements of the rator (Langohr and Lang-

ohr 2008). The CRA the issuer is most likely to select is the

one that the corporate treasurer has had a positive experi-

ence with, either through prior dealings with the analyst or

the specific CRA and to avoid CRAs or analysts who have

proved problematic in the past (Duff and Einig 2007). On a

related note, the issuer can opinion shop to have a complex

security rated, where the inherent risks are difficult to

ascertain, leading to a situation where an aggressive CRA

intent on maximising its coverage undertakes work beyond

the bounds of its competence.4

The second element of the trinity concerns the lack of

transparency of ratings information. Critics cite the

inability of CRAs to publish details of their methodologies

that allow at an informed view of their decisions. Yet, as

Sinclair (2005, p. 149) identifies ‘a rating judgement—is

inherently subjective: it incorporates some values and

excludes others’. Furthermore, the ratings process requires

the CRA to seek qualitative, non-public information about

the management’s future strategy and prospects: in part an

anthropomorphic process, involving judgements about trust

and commitment. The process also requires on-going

maintenance to ensure upgrades or downgrades to a credit

rating are made when necessary, but on a planned basis

from an issuer perspective, requiring strong and positive

relations between the borrower and the CRA.5 That is, a

Fig. 1 The Shield of the CRA

Trinity of Solicitude. Note

Element of the shield (in bold),

Source of the element (not bold

not italics), How element is

operationalized in issuer–CRA

relations (in italics)

3 Newspapers are often cited as an example of a two-sided market

that brings together readers and advertisers who may be charged in

varying proportions. At one end of the continuum, local or

metropolitan ‘free sheets’ do not charge readers but rely on

advertising alone. At the other extreme, readers pay for a publication

consisting of a wide variety of private listings where the advertiser

pays no fee.

4 Such commentary has also been applied to other gatekeepers such

as auditors engaged on investment bank audits where the risks

associated with some activities make them un-auditable in the views

of some commentators.5 The ratings process is not a one-off event. Beyond the initial rating

the probability of default on the security is monitored and the rating

changed (upgraded or downgraded) as deemed appropriate.

A. Duff, S. Einig

123

debt investor relations function needs to exist. The ability

of the issuer’s treasurer to communicate effectively with

CRA personnel becomes a significant issue in how the

rating is maintained and accurately reflects a borrower’s

credit profile (Duff and Einig 2007).

The final element of the trinity concerns competition. As

described previously, the ratings market is an oligopoly

where two main players account for 80 % of the business

(Langohr and Langohr 2008; Scalet and Kelly 2012).

Essentially, the ratings business has evolved as it has

because the industry is a natural monopoly where the

business of creating a comprehensive book of ratings

developed through statistical analysis and personalised

relations with issuers lends itself to a small number of

suppliers. In addition, the cost of seeking and maintaining a

rating is expensive, more so in senior management time

than in issuance and maintenance fees. Where an issuer

engages multiple CRAs, it will expect to deal with man-

agement on an independent basis, i.e. not be invited to a

corporate presentation where other CRAs are also involved

(Duff and Einig 2007). Thus, interpersonal relations

become highly significant or the issuer has limited alter-

natives if dissatisfied with a CRA (see Duff and Einig

2009b, p. 114). Furthermore, ratings work is necessarily

labour intensive with the quality of ratings decisions a

function of human analytic decision-making and the ability

to improve methodological insight (Langohr and Langohr

2008). CRAs compete with one another and, more impor-

tantly, other financial services organisations offering more

lucrative and prestigious positions (Duff and Einig 2007,

2009b). Enmeshed in the lack of competition element of

the trinity then is the intense competition CRAs face in

attracting the ‘brightest and the best’ human capital.

Although a considerable literature examines matters

such as the determinants of ratings, ratings changes, split

ratings, little prior research exists of CRA-issuer interac-

tions and relations. Using interview-based evidence, Duff

and Einig (2009b) identify a corporate issuer’s Treasurer as

the key decision-maker when engaging a CRA. When

selecting a new or additional CRA, the Treasurer often

selects the CRA on the basis of his or her past experience

with that CRA and its analytic staff. Consequently, the

affective relationship between an issuer’s Treasurer and

CRA staff may precede formal engagement. In addition,

the substantial investments in senior management time

associated with a successful solicited rating necessitate

commitment, particularly given the longevity of the rela-

tionship (Duff and Einig 2009b). Issuers also tend to view

the competence of CRA analytic staff as a key component

of ratings quality; when there was an issue with a particular

rating the problem tended to lie with individual staff rather

than the CRA’s methodology (Duff and Einig 2009b).

Furthermore, ratings decision-making relies on non-public

qualitative, and often subjective, information provided by

the debt issuer. The reliance the rator places on this

information reflects the affective relationship between

issuer and CRA. At the same time, affective commitment is

achieved at a cost to the borrower who needs to invest time

and resources in producing the necessary information to the

CRA on a timely basis.

Relational Exchange Literature

The origin of the exchange relationships literature is

located in social exchange theory (Blau 1964; Emerson

1976; Homans 1958; Thibaut and Kelley 1959) along with

Scanzoni’s (1979) work considering personal relationships.

Scanzoni (1979) considers personal relationships develop

in five discrete stages: awareness; exploration; expansion;

commitment; and dissolution. Commitment lies at the focal

point of this model as successful long-term business rela-

tions are characterised by a requirement for relational

continuity (Rylander et al. 1997; De Ruyter et al. 2001).

The nature of the bond rating process is naturally long-term

as corporate and sovereign debt may have a term of many

years and the CRA will continue to re-rate the security. The

three stages that precede commitment describe those pro-

cesses whereby each party develops awareness, explores,

and evaluates each other as a viable business party. The

final stage, dissolution, describes the process whereby one

party identifies their dissatisfaction with the relationship

and then enters into negotiations with the other to terminate

relations. In a ratings context, the natural dissolution of the

relationship would occur at the term of the bond. Issuers,

having established credibility in debt markets, usually

continue to issue debt securities, and continue to use a

relationship CRA who understands their business.

Commitment is considered an essential ingredient for

successful long-term business relationships (Tummala

et al. 2006). For example, committed partners are willing to

invest in valuable assets specific to an exchange (Anderson

and Weitz 1992). Commitment has a direct influence on

customer loyalty and retention (e.g. Dick and Basu 1994;

Hennig-Thurau and Klee 1997). Committed customers are

less likely to switch an organization than clients who lack

commitment to the organization (Wetzels et al. 1998;

Fullerton 2003).

Commitment is generally regarded as a complex con-

struct that has more than one dimension (Ozag 2006). Most

studies distinguish between two discrete forms of com-

mitment: affective commitment; and calculative commit-

ment. Morgan and Hunt (1994) define Affective

Commitment as an enduring desire to maintain a valued

relationship. Affective Commitment is rooted in identifi-

cation, shared values, belongingness, dedication, and sim-

ilarity (Achrol 1997; Bendapudi and Berry 1997; Pritchard

An Empirical Study of the Role of Commitment

123

et al. 1999). The essence of Affective Commitment is that

customers come to acquire an emotional attachment to their

partner in a consumption relationship. When consumers

come to like brands or service providers, they are experi-

encing the psychological state of Affective Commitment

(Fullerton 2003).

Unlike Affective Commitment that describes the emo-

tional attachment of a customer to their service provider,

Calculative Commitment measures the degree to which a

firm or individual experiences a need to continue a rela-

tionship due to the high costs of leaving. A consumer is

likely to be committed to a relationship if he or she faces

concrete switching costs (Sharma and Patterson 2000;

Yang and Petersen 2004), or if the benefits that he or she

receives from the partner are not easily replaceable from

other potential exchange partners (Geyskens et al. 1996).

Antecedents and Consequences of Commitment

Prior research identifies major antecedents of commitment

as being: (i) customer (issuer) orientation (Bejou et al.

1998; Saxe and Weitz 1982); (ii) service quality (Patterson

et al. 1996; Woodside et al. 1992) (iii) shared values and

norms (Morgan and Hunt 1994; Dwyer et al. 1987); and

(iv) trust (Granovetter 1985; Geyskens and Steenkamp

1995). In a recent study considering users’ perceptions of

the qualities required of a CRA, Duff and Einig (2009a)

create a conceptual and empirical model that includes these

four key antecedents of commitment. Specifically Duff and

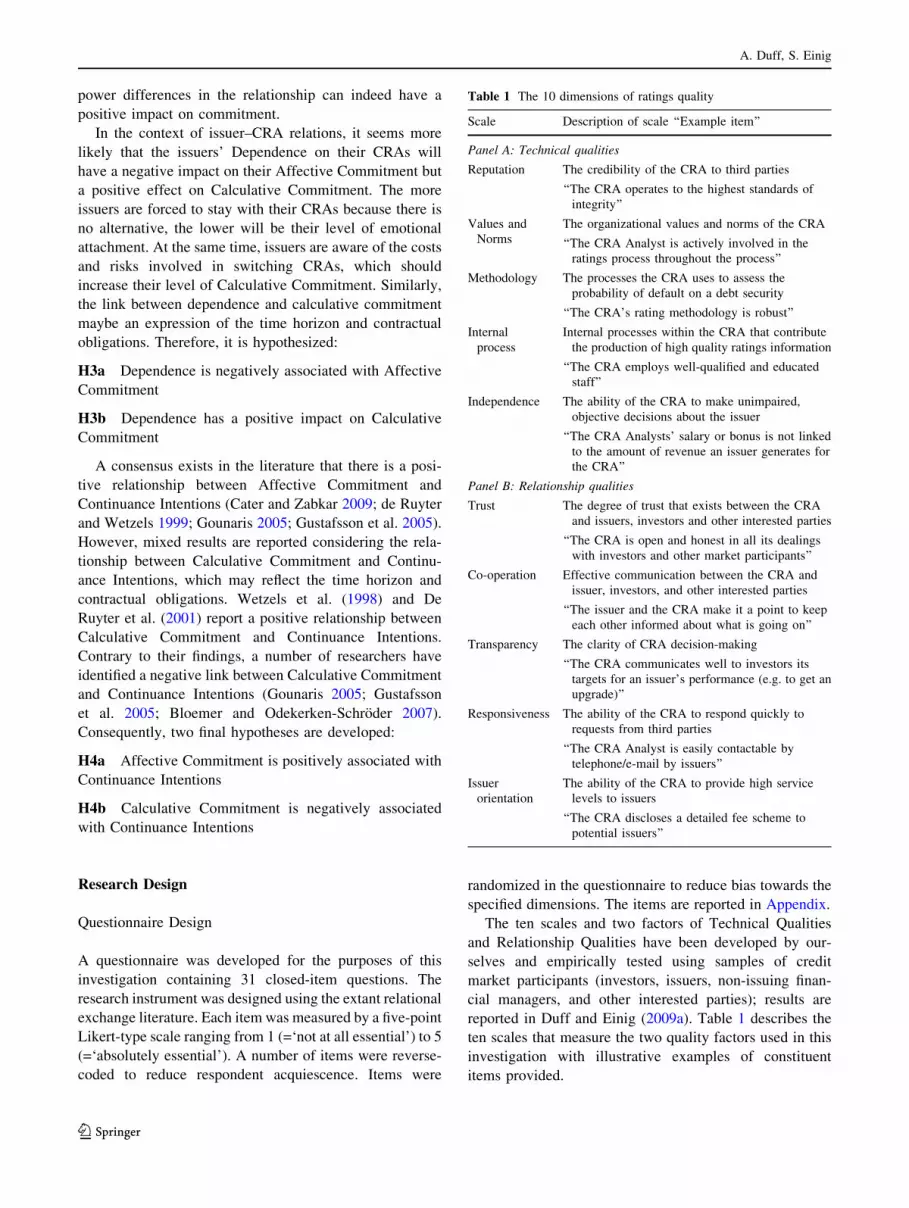

Einig (2009a) develop ten dimensions of ratings quality.

Five relate to relationship qualities, i.e. those factors rele-

vant to CRA-issuer relations. These they label: (i) cooper-

ation; (ii) issuer orientation; (iii) service quality; (iv)

transparency; and (v) trust. Alongside relationship qualities

sit technical qualities that describe the competence of the

ratings team, i.e. the appropriateness of the CRA’s meth-

odologies and their ability to arrive at a frank assessment of

the probability of default. Technical qualities are defined

by five dimensions that do not feature significantly as

antecedents of commitment in the exchange relationships

literature but which are major features of the credibility of

a CRA in debt markets (Duff and Einig 2009a, b). These

five technical qualities are labelled: (i) independence; (ii)

internal processes; (iii) methodology; (iv) reputation; and

(v) shared values and norms.

Dependence refers to a firm’s need to maintain an

exchange relationship with another firm to achieve desired

goals (Andaleeb 1995; Razzaque and Boon 2008).

Buchanan (1992, p. 65) defines Dependence as ‘‘the extent

to which a trade partner provides important and critical

resources for which there are few alternative sources of

supply’’. Dependence is a distinct construct to Calculative

Commitment, as Dependence refers to the structure of the

relationship by measuring structural elements that bind the

firm to the partner (Geyskens et al. 1996). By contrast,

Calculative Commitment measures the firm’s motivation to

maintain relations with a partner because of these structural

ties. Geyskens et al. (1996) provide empirical evidence that

a firm’s Calculative Commitment and its Dependence on

the channel partner are distinct constructs.

The proposed empirical model includes technical and

relationship qualities, dependence, two forms of commit-

ment, and continuance intentions—see Fig. 2.

In terms of technical qualities, independence is an

essential feature of CRAs. If the CRA, remunerated by the

issuer of the debt security, is not seen to be independent of

the issuer then the concerns regarding the buyer-pays

model are crystallised, and the rating becomes worthless.

Internal processes relate to the mechanisms the CRA

employs to ensure hat the staff engaged in ratings decisions

are competent to assess the probability of default on a

security (e.g. are well educated and trained, have an

appropriate workload, are regularly appraised) as ratings

work is essentially labour intensive. Methodology relates to

the meaning and robustness of a CRA’s methods, which

form the basis of their decision-making. Reputation

describes how the CRA is perceived in the market; in a

ratings decision, CRAs are effectively pledging their rep-

utational capital and the value of that rating is a function of

that capital. Finally, shared norms and values describe the

match in ethical standards between the CRA and the issuer

and the active willingness of CRA analytic staff engaged in

the rating to understand the idiosyncrasies of the ratee’s

business. Shared norms and values have also been empir-

ically associated with the fostering of affective commit-

ment (Morgan and Hunt, 1994; Gundlach et al. 1995).

In terms of relationship qualities, trust is an essential

component of relationship qualities, and is considered by

many researchers a central aspect of successful business

relationships (Morgan and Hunt 1994). Trust reflects a

belief in the reliability of a third party, particularly when

there is an element of personal risk (Arnott 2007). For

example, in a ratings contest, issuers need to provide CRAs

with timely, market-sensitive, and confidential information

for the rating to be accurate. Without trust, i.e. a willing-

ness to lay bare their future plans and strategy allowing an

honest appraisal of their prospects, ratings are likely to be

misleading and the CRA be more conservative in its credit

assessment, to the detriment of the borrower. However,

close relations between issuers and CRAs may also be

perceived as sweethearting (e.g. Brady et al. 2012)

whereby investors may be suspicious of this relationship

fuelling criticism of the buyer pays business model.

For the purpose of this study, Dependence measures the

degree of dependence in the CRA-issuer relationship. A

high level of Dependence is usually caused by a lack of

A. Duff, S. Einig

123

suitable alternatives or when highly specified services are

provided by the supplier. As the ratings market is domi-

nated by two major players, it can be assumed that there is

a high level of dependence in this market. Consequently, a

relatively high level of power imbalance between the

CRAs and issuers exists (cf., Weitz and Jap 1995).

Researchers investigating buyer decisions to remain

with a supplier have examined constructs such as propen-

sity to stay (Rutherford et al. 2006); expectation of conti-

nuity (Crosby et al. 1990; Doney and Cannon 1997); and

continuance (Anderson and Sullivan 1993). For the pur-

poses of this study, the factor Continuance Intentions is

defined as the issuers’ willingness to continue the rela-

tionship with their existing CRAs and invest in this rela-

tionship with a long-term view.

We develop eight hypotheses to assess the causal rela-

tionships of our exchange relationship model of issuer–

CRA relations. There is relatively little conceptual or

empirical evidence in the literature considering the rela-

tionships between Technical Qualities or Relationship

Qualities and commitment. Conceptually, Wetzels et al.

(1999) propose that both Technical Qualities and Rela-

tionship Qualities are positively related to Affective

Commitment and Calculative Commitment. Conceptual

support is found linking individual dimensions of technical

quality to Affective Commitment (e.g. Shared Values and

Norms: Dwyer et al. 1987; Morgan and Hunt 1994;

Gundlach et al. 1995). Furthermore, the gatekeeping nature

of CRAs and the unique nature of the market they operate

in, described in part by the trinity of solicitude, means that

we rely on our prior work considering determinants of

ratings quality (Duff and Einig 2009a, b) in our concep-

tualisation of the antecedents of commitment in CRA—

issuer relations.

De Ruyter and Wetzels (1999) found in their study of

auditor–client commitment that both Service Quality and

Trust were positively related to Affective Commitment.

Wetzels et al. (1998) studying a Dutch manufacturer report a

positive significant relationship between Technical Qualities

and Affective Commitment, but no significant relationship

between Technical Qualities and Calculative Commitment.

As the outcome of the present study cannot be predicted, it is

hypothesized that there is a positive relationship between

Technical Qualities and Relationship Qualities and both

forms of commitment as originally hypothesized by De

Ruyter and Wetzels (1999) and Wetzels et al. (1998). This

discussion leads to the following hypotheses:

H1a Technical Qualities have a positive impact on

Affective Commitment

H1b Technical Qualities have a positive impact on Cal-

culative Commitment

H2a Relationship Qualities have a positive impact on

Affective Commitment

H2b Relationship Qualities have a positive impact on

Calculative Commitment

Empirical studies in the field of business have found that

dependence in relationships has a negative impact on

Affective Commitment (Anderson and Weitz 1989; Kumar

et al. 1995), and a positive influence on Calculative

Commitment (Ganasan 1994). Parties who are dependent

on some other party are typically less emotionally involved

in the relationship (Anderson and Weitz 1989). However,

Calculative Commitment increases with a higher level of

Dependence as it becomes more costly for the dependent

party to terminate the relationship (Anderson and Weitz

1989).

A small number of studies report findings contrary to the

majority of business research in this area. For example, De

Ruyter et al. (2001) reported a positive link between

Dependence and Affective Commitment in their study on

relationship commitment in high technology markets.

Geyskens et al. (1996) also concluded in their study of the

effects of trust and interdependence on commitment that

Fig. 2 The issuer-commitment

model

An Empirical Study of the Role of Commitment

123

power differences in the relationship can indeed have a

positive impact on commitment.

In the context of issuer–CRA relations, it seems more

likely that the issuers’ Dependence on their CRAs will

have a negative impact on their Affective Commitment but

a positive effect on Calculative Commitment. The more

issuers are forced to stay with their CRAs because there is

no alternative, the lower will be their level of emotional

attachment. At the same time, issuers are aware of the costs

and risks involved in switching CRAs, which should

increase their level of Calculative Commitment. Similarly,

the link between dependence and calculative commitment

maybe an expression of the time horizon and contractual

obligations. Therefore, it is hypothesized:

H3a Dependence is negatively associated with Affective

Commitment

H3b Dependence has a positive impact on Calculative

Commitment

A consensus exists in the literature that there is a posi-

tive relationship between Affective Commitment and

Continuance Intentions (Cater and Zabkar 2009; de Ruyter

and Wetzels 1999; Gounaris 2005; Gustafsson et al. 2005).

However, mixed results are reported considering the rela-

tionship between Calculative Commitment and Continu-

ance Intentions, which may reflect the time horizon and

contractual obligations. Wetzels et al. (1998) and De

Ruyter et al. (2001) report a positive relationship between

Calculative Commitment and Continuance Intentions.

Contrary to their findings, a number of researchers have

identified a negative link between Calculative Commitment

and Continuance Intentions (Gounaris 2005; Gustafsson

et al. 2005; Bloemer and Odekerken-Schroder 2007).

Consequently, two final hypotheses are developed:

H4a Affective Commitment is positively associated with

Continuance Intentions

H4b Calculative Commitment is negatively associated

with Continuance Intentions

Research Design

Questionnaire Design

A questionnaire was developed for the purposes of this

investigation containing 31 closed-item questions. The

research instrument was designed using the extant relational

exchange literature. Each item was measured by a five-point

Likert-type scale ranging from 1 (=‘not at all essential’) to 5

(=‘absolutely essential’). A number of items were reverse-

coded to reduce respondent acquiescence. Items were

randomized in the questionnaire to reduce bias towards the

specified dimensions. The items are reported in Appendix.

The ten scales and two factors of Technical Qualities

and Relationship Qualities have been developed by our-

selves and empirically tested using samples of credit

market participants (investors, issuers, non-issuing finan-

cial managers, and other interested parties); results are

reported in Duff and Einig (2009a). Table 1 describes the

ten scales that measure the two quality factors used in this

investigation with illustrative examples of constituent

items provided.

Table 1 The 10 dimensions of ratings quality

Scale Description of scale ‘‘Example item’’

Panel A: Technical qualities

Reputation The credibility of the CRA to third parties

‘‘The CRA operates to the highest standards of

integrity’’

Values and

Norms

The organizational values and norms of the CRA

‘‘The CRA Analyst is actively involved in the

ratings process throughout the process’’

Methodology The processes the CRA uses to assess the

probability of default on a debt security

‘‘The CRA’s rating methodology is robust’’

Internal

process

Internal processes within the CRA that contribute

the production of high quality ratings information

‘‘The CRA employs well-qualified and educated

staff’’

Independence The ability of the CRA to make unimpaired,

objective decisions about the issuer

‘‘The CRA Analysts’ salary or bonus is not linked

to the amount of revenue an issuer generates for

the CRA’’

Panel B: Relationship qualities

Trust The degree of trust that exists between the CRA

and issuers, investors and other interested parties

‘‘The CRA is open and honest in all its dealings

with investors and other market participants’’

Co-operation Effective communication between the CRA and

issuer, investors, and other interested parties

‘‘The issuer and the CRA make it a point to keep

each other informed about what is going on’’

Transparency The clarity of CRA decision-making

‘‘The CRA communicates well to investors its

targets for an issuer’s performance (e.g. to get an

upgrade)’’

Responsiveness The ability of the CRA to respond quickly to

requests from third parties

‘‘The CRA Analyst is easily contactable by

telephone/e-mail by issuers’’

Issuer

orientation

The ability of the CRA to provide high service

levels to issuers

‘‘The CRA discloses a detailed fee scheme to

potential issuers’’

A. Duff, S. Einig

123

The questionnaire was piloted through two processes.

First, officers from two professional bodies with an interest

in the activities of CRAs inspected the questionnaire to

comment on the appropriateness of the wording of the

questionnaire. Second, the questionnaire was reviewed by

six of the eleven interview participants reported in Duff

and Einig (2009b). At each stage, the content of the

questionnaire was revised accordingly.

Conduct of Survey

The questionnaire was mailed to 950 Corporate Treasurers.

Questionnaires were sent to Treasurers as they are the

individual most likely to hold the relationship with the

CRA or be a key individual in financing decision-making.

Participants were selected in two ways: first, all companies

who issued fixed-income securities at the London Stock

Exchange (N = 284) were identified using the LSE data-

base. The Association of Corporate Treasurer’s (ACT)

Directory was used to identify the exact contact details for

these organizations. When this was not possible, the

questionnaires were addressed to ‘The Treasurer’. Second,

666 additional Treasurers were chosen at random from the

ACT Directory. This second group enabled identification of

additional issuers who exclusively issue in non-UK mar-

kets. Inclusion of the second group allows greater coverage

of issuers as conceivably some borrowers may chose to

issue non-sterling denominated debt outside the UK.6

The questionnaire was accompanied by a personalised

explanatory covering letter describing the purpose of the

study, and provided assurances of the confidentiality of

responses. A post-paid University-addressed return enve-

lope was also provided. Two follow-ups were administered

to non-respondents after 14 days (reminder letter), and

28 days (replacement questionnaire). Finally, respondents

were given the option of receiving a summary report of the

results of the investigation as an incentive to respond.

Response Rate and Response Bias

From the sample of 950 Treasurers, 74 parties were elim-

inated from the sample because the company no longer

existed or the named individual had left the company. Of

the 198 useable responses were returned, 67 responses

were eliminated from the sample because the organization

did not use the services of a CRA. This was done to ensure

that only knowledgeable respondents with current experi-

ence of working with a CRA were included in the sample.

Our final sample consisted of 131 respondents and a

response rate of 24.5 %. Tests for response bias indicated it

is unlikely that response bias will challenge the validity of

the results of the present investigation.7

Of the 131 respondents, 21 respondents engaged only

one CRA, 62 engaged two CRAs, 43 commissioned rat-

ings from three CRAs, and four respondents used four

CRAs.

Results

Measurement Model

To evaluate the fit of the hypothesized model to the data, the

standardized root mean square residual (SRMR) is used in

tandem with the root mean square error of approximation

(RMSEA) as recommended by Hu and Bentler (1999) and

MacCallum and Austin (2000).8 Residuals and modification

indices were used to identify misspecifications (Byrne

2001). Any detected misspecifications were followed up

and the model re-specified when possible. Some items were

deleted because they cross-loaded on other factors and

therefore deteriorated the model fit. Scales were then

retested for internal consistency reliability to ensure that

they remained homogenous. Model re-specification was

completed when the model was deemed a close fit with the

data (v2 = 1016; d.f. = 766; SRMR = .0784;

RMSEA = .050). Browne and Cudeck (1993) confirm that

RMSEA values of .05 or below and SRMR values of .08

and below indicate excellent model fit.

Table 2 reports the scale means, standard deviations,

correlations, and the Cronbach-alphas (in bold setting).

Ultimately, all remaining scales achieved an acceptable

level of internal consistency—see Table 2. Five of the ten

alpha coefficients exceed .7, a widely-cited and conserva-

tive threshold for instruments intended to be used in a wide

range of applied settings (Nunnally and Bernstein 1994).

The other five dimensions exceed .6 as required. In sum,

6 Multinational businesses may seek to issue debt wherever they

believe there is the greatest appetite for the issue. Depending on the

profile of the organisation this may be outside the UK.

7 To test for response bias, a comparison was applied to early (first

33 %) and late (last 33 %) of respondents using the Wilcoxon–Mann–

Whitney non-parametric test. This assumes late respondents are

similar to non-respondents (Dillman 1978). Statistically significant

differences between early and late respondents were fund for only one

item (a = .05).8 A number of authors (Hu and Bentler 1998; Marsh et al. 1998; Hu

and Bentler 1999) warn against the use of more common goodness-of-

fit indices such as the goodness-of-fit index (GFI) and adjusted

goodness-of-fit index (AGFI) which are widely used in the structural

equation modelling literature. Hu and Bentler (1999, p. 26) indicate

for samples N \ 500, the combinational rule SRMR \ .11 and

RMSEA \ .08 is ‘‘extremely sensitive in detecting model with

misspecified factor covariances’’.

An Empirical Study of the Role of Commitment

123

the instrument yields scores of satisfactory internal con-

sistency reliability.9,10

Structural Model and Hypothesis Testing

Table 3 shows the standardized regression weights mea-

suring the causal relationship between the respective fac-

tors. Statistical significance of relationships was established

using two-tailed significance tests (a = .05).

Hypotheses H1a and H1b are rejected on the basis of a

negative relationship between Technical Qualities and

Affective Commitment (SRW = -2.57), and Technical

Qualities and Calculative Commitment (SRW = -2.83),

respectively. Although these findings are unexpected, they

might be explained by considering the importance of

Technical Qualities for the rating. Technical Qualities are

highly valued by investors and other users of ratings

information but not necessarily so by issuers who seek a

rating to ensure a market for their debt and reduce their

cost of debt. An alternative explanation might be that

issuers have a good understanding of CRAs’ methodolo-

gies and an ability to manage the non-public information

available to the CRA. Therefore, the assignment of a rating

is unlikely to provide any surprises to an issuer’s Treasurer

who is knowledgeable of the mechanics of the CRA’s

quantitative methodology that heavily influences the final

decision.

Hypothesis 2 predicts that a positive relationship exists

between Relationship Qualities and Affective Commitment

(H2a) and Calculative Commitment (H2b). Issuers should

be more committed to a CRA that provides a higher level

of relationship qualities. Results indicate that a significant

positive relationship between Relationship Qualities and

Affective Commitment exists. The relationship between

Relationship Qualities and Calculative Commitment is also

positive and significant. Consequently, both H2a and H2b

are supported.

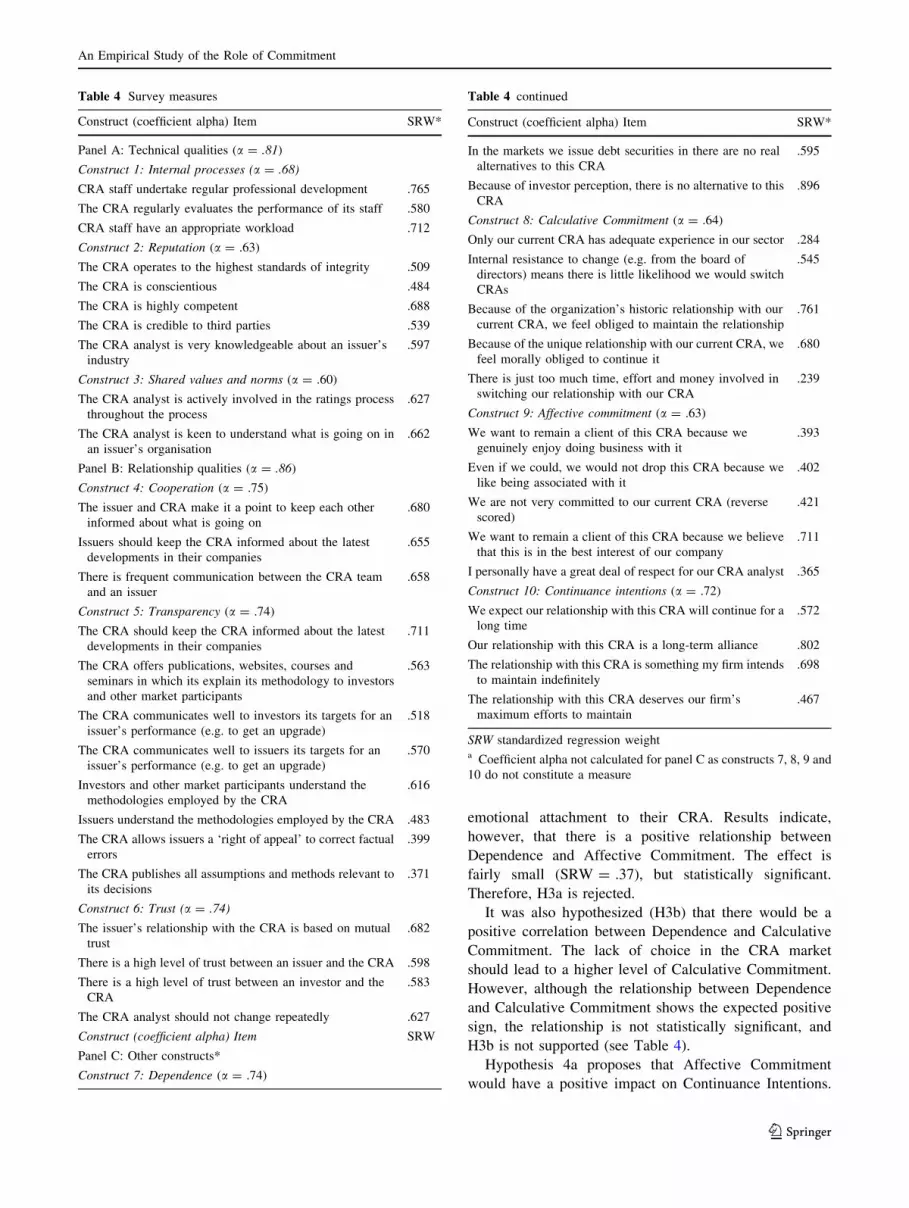

Hypothesis 3a proposes that Dependence would be

negatively related to Affective Commitment. The more

issuers are forced to stay with their CRAs, because of a

lack of suitable alternatives, the lower will be their level of

Table 2 Data distribution and

correlations

r [ .16 p \ .05; r [ .2 p \ .01

(two-tailed)

Scale Mean SD 1 2 3 4 5 6 7 8 9 10

Internal process 3.97 .84 .68

Reputation 4.71 .51 .60 .63

Shared values 4.38 .73 .58 .54 .60

Cooperation 4.11 .76 .51 .39 .62 .75

Transparency 4.03 .85 .47 .34 .47 .50 .74

Trust 4.13 .85 .64 .55 .62 .60 .63 .74

Dependence 3.18 1.18 -.09 -.06 -.06 -.05 .11 -.09 .74

Affective commitment 3.12 .59 .04 .11 .11 .14 .12 -.01 .26 .64

Calculative commitment 2.21 .61 .00 -.09 -.09 .16 .18 .00 .47 .31 .63

Continuance intentions 3.50 .69 .11 .11 .25 .28 .11 .13 .21 .35 .36 .72

Table 3 Parameter estimates

and results of hypotheses tests

a Standardized regression

weights (SRW) (i.e. factor

loadings)

Hypothesis Estimatea p value Results

H1a Positive effect of TQ on ACO -2.57 \.05 Not supported

H1b Positive effect of TQ on CCO -2.83 \.05 Not supported

H2a Positive effect of RQ on ACO 2.69 \.05 Supported

H2b Positive effect of RQ on CCO 2.66 \.05 Supported

H3a Negative effect of DEP on ACO .37 \.001 Not supported

H3b Positive effect of DEP on CCO .94 n.s. Not supported

H4a Positive effect of ACO on CON 1.09 \.001 Supported

H4b Positive effect of CCO on CON -.27 \.05 Not supported

9 Some alternatives were considered to the hypothesised model

including tests for mediation of Affective Commitment and Calcu-

lative Commitment on Dependence and Continuation as a direct

effect on Continuation. Bootstrapping, per the recommendations of

Chung and Lau (2009), identifies that Affective Commitment and

Calculative Commitment have a net mediated effect on Continuation.10 The discriminant validity of: (i) technical qualities versus

relationship qualities; and (ii) dependence and calculative commit-

ment by setting the correlation to zero and comparing it to a model

where this was not constrained (Segars 1997). The findings:

(i) Dv2 = .407, 1 d.f. p \ .001; and (ii) Dv2 = .404, 1 d.f.

p \ .001); respectively suggest each are distinct constructs.

A. Duff, S. Einig

123

emotional attachment to their CRA. Results indicate,

however, that there is a positive relationship between

Dependence and Affective Commitment. The effect is

fairly small (SRW = .37), but statistically significant.

Therefore, H3a is rejected.

It was also hypothesized (H3b) that there would be a

positive correlation between Dependence and Calculative

Commitment. The lack of choice in the CRA market

should lead to a higher level of Calculative Commitment.

However, although the relationship between Dependence

and Calculative Commitment shows the expected positive

sign, the relationship is not statistically significant, and

H3b is not supported (see Table 4).

Hypothesis 4a proposes that Affective Commitment

would have a positive impact on Continuance Intentions.

Table 4 Survey measures

Construct (coefficient alpha) Item SRW*

Panel A: Technical qualities (a = .81)

Construct 1: Internal processes (a = .68)

CRA staff undertake regular professional development .765

The CRA regularly evaluates the performance of its staff .580

CRA staff have an appropriate workload .712

Construct 2: Reputation (a = .63)

The CRA operates to the highest standards of integrity .509

The CRA is conscientious .484

The CRA is highly competent .688

The CRA is credible to third parties .539

The CRA analyst is very knowledgeable about an issuer’s

industry

.597

Construct 3: Shared values and norms (a = .60)

The CRA analyst is actively involved in the ratings process

throughout the process

.627

The CRA analyst is keen to understand what is going on in

an issuer’s organisation

.662

Panel B: Relationship qualities (a = .86)

Construct 4: Cooperation (a = .75)

The issuer and CRA make it a point to keep each other

informed about what is going on

.680

Issuers should keep the CRA informed about the latest

developments in their companies

.655

There is frequent communication between the CRA team

and an issuer

.658

Construct 5: Transparency (a = .74)

The CRA should keep the CRA informed about the latest

developments in their companies

.711

The CRA offers publications, websites, courses and

seminars in which its explain its methodology to investors

and other market participants

.563

The CRA communicates well to investors its targets for an

issuer’s performance (e.g. to get an upgrade)

.518

The CRA communicates well to issuers its targets for an

issuer’s performance (e.g. to get an upgrade)

.570

Investors and other market participants understand the

methodologies employed by the CRA

.616

Issuers understand the methodologies employed by the CRA .483

The CRA allows issuers a ‘right of appeal’ to correct factual

errors

.399

The CRA publishes all assumptions and methods relevant to

its decisions

.371

Construct 6: Trust (a = .74)

The issuer’s relationship with the CRA is based on mutual

trust

.682

There is a high level of trust between an issuer and the CRA .598

There is a high level of trust between an investor and the

CRA

.583

The CRA analyst should not change repeatedly .627

Construct (coefficient alpha) Item SRW

Panel C: Other constructs*

Construct 7: Dependence (a = .74)

Table 4 continued

Construct (coefficient alpha) Item SRW*

In the markets we issue debt securities in there are no real

alternatives to this CRA

.595

Because of investor perception, there is no alternative to this

CRA

.896

Construct 8: Calculative Commitment (a = .64)

Only our current CRA has adequate experience in our sector .284

Internal resistance to change (e.g. from the board of

directors) means there is little likelihood we would switch

CRAs

.545

Because of the organization’s historic relationship with our

current CRA, we feel obliged to maintain the relationship

.761

Because of the unique relationship with our current CRA, we

feel morally obliged to continue it

.680

There is just too much time, effort and money involved in

switching our relationship with our CRA

.239

Construct 9: Affective commitment (a = .63)

We want to remain a client of this CRA because we

genuinely enjoy doing business with it

.393

Even if we could, we would not drop this CRA because we

like being associated with it

.402

We are not very committed to our current CRA (reverse

scored)

.421

We want to remain a client of this CRA because we believe

that this is in the best interest of our company

.711

I personally have a great deal of respect for our CRA analyst .365

Construct 10: Continuance intentions (a = .72)

We expect our relationship with this CRA will continue for a

long time

.572

Our relationship with this CRA is a long-term alliance .802

The relationship with this CRA is something my firm intends

to maintain indefinitely

.698

The relationship with this CRA deserves our firm’s

maximum efforts to maintain

.467

SRW standardized regression weighta Coefficient alpha not calculated for panel C as constructs 7, 8, 9 and

10 do not constitute a measure

An Empirical Study of the Role of Commitment

123

Issuers who are more committed to their CRAs should be

more likely to continue their relationship with their CRAs.

A significant positive relationship was found between

Affective Commitment and Continuance Intentions, sup-

porting H4a.

It was also hypothesized that Calculative Commitment

would have a positive impact on Continuance Intentions

(H4b). A significant negative relationship between Calcu-

lative Commitment and Continuance Intentions is found,

and H4b is not supported.

Discussion

The aim of this study was to explore issuer–CRA relations

from the perspective of what motivates an issuer to remain

with their present relationship CRA. It set out to achieve

this by the development and empirical testing of a struc-

tural equation model using the relational exchange litera-

ture. The constructs of commitment are predictors of issuer

intentions to remain with a ratings supplier. In turn,

affective and calculative commitment can be predicted by

two form of ratings quality and the degree of dependence

an issuer has on its CRAs. Figure 3 summarises results.

An unexpected finding was that Technical Qualities are

shown to have a negative effect on both Affective and

Calculative Commitment. One interpretation of this finding

could be that ‘less is more’, whereby issuers would be more

committed to their relationship with a CRA that offered a

lower level of Technical Qualities. Essentially, issuers seek

a rating to gain access to public debt markets. Without a

rating there is either: no demand for the bond; or the bond

is priced at a higher level. Assuming the rating is what the

issuer expected, the degree of due diligence that went into

the rating is perhaps of less concern to the borrower but a

significant issue to buyers and other users of ratings

information. This result differs from Wetzels et al. (1998)

who found a positive relationship between Technical

Qualities and Affective Commitment and an insignificant

relationship between Technical Qualities and Calculative

Commitment. Therefore, our findings suggest that the

CRA-issuer relationship and the CRA market are distinct

from other financial gatekeeper relationships.

As anticipated, the results indicate that Relationship

Qualities lead to client commitment. Relationship Qualities

have a substantial effect on Affective Commitment, the

form of commitment that is most beneficial for the business

relationship, and a, statistically somewhat weaker, impact

on Calculative Commitment. The positive expected rela-

tionship between Relationship Qualities and Affective

Commitment accords with De Ruyter and Wetzel’s (1999)

findings considering auditor–client commitment.

An unexpected finding was that Dependence was shown

to have a small positive effect on Affective Commitment,

indicating that some degree of dependence on the business

partner does not have to be problematic. A similar effect

has also been reported by De Ruyter et al. (2001) who

suggests dependence contributes to a positive attitude

towards the business partner. This could be expected as

issuers invest substantial resources in terms of management

time in educating the CRA about their organization’s future

strategy and prospects. This is particularly true for frequent

issuers who rely heavily on their ratings.

An important finding is that Affective Commitment has

the strongest effect on continuance intentions. Issuers who

feel emotionally attached to their CRAs are much more

likely to continue the relationship. This finding is supported

by a number of studies that also found strong links between

Affective Commitment and continuance intentions (e.g.

Cater and Zabkar 2009; Wetzels et al. 1998; De Ruyter and

Wetzels 1999). The idea that issuers have an affective

identification with their CRAs is not one captured in the

literature. Prior work suggests the relationship with an

agency is onerous, time-consuming, and one in which the

Fig. 3 The issuer-commitment

model: empirical findings. Note:

Relationships between latent

factors without an indicated

direction (?ve/-ve) are not

statistically significant

A. Duff, S. Einig

123

CRA holds an excessive degree of power (Duff and Einig

2007; Langohr and Langohr 2008; Sinclair 2005). So our

finding provides an interesting angle on CRA-issuer rela-

tions. Calculative Commitment, however, was shown to

have a negative effect on continuance intentions. This

result is as hypothesized, supporting prior research

(Gounaris 2005; Gustafsson et al. 2005).

The findings of this research contrast with the findings

of related exchange relationship studies. In particular the

negative relationship between Technical Qualities and the

two forms of Commitment suggest that the nature of the

issuer–CRA relationship is unusual. The continuing focus

by regulators and critical market commentators on the need

for CRAs to improve their methodologies may fall on deaf

ears as issuers are solely responsible for the CRA selection

decision. This study therefore provides new insights into a

research area that, to date, has received little attention.

An important finding of our study is that an issuer’s

intention to remain with a relationship CRA is dependent

on the degree of Affective Commitment they feel towards

the CRA. This contrasts with the finding that Affective

Commitment is determined by the quality of the ratings

process (Relationship Qualities), rather than the quality of

the ratings themselves (Technical Qualities). Relationship

Qualities are composed of attributes of trust, co-operation,

and transparency. The key then to CRAs to develop an

effective relationship with corporate issuers is to secure the

issuers trust, maximize opportunities for co-operation, and

be transparent in their actions. Affective relations provide a

precondition for an effective relationship having important

consequences for both parties. Borrowers deliberately seek

a solicited rating, rather than passively allow themselves to

be rated on an unsolicited basis, and suffer potentially a

lower rating and adverse pricing. Therefore, the issuer

should ensure the preconditions for an affective commit-

ment are met to allow the CRA to confidently incorporate

as much soft, non-public information as possible.

However, these findings have significant consequences

for third parties such as investors, regulators and myriad

individuals who directly, or indirectly, rely on ratings to

inform the credit marketplace. How desirable are qualities

of affect between ratees and rators? Consider the gover-

nance era in which Enron, and other corporate reporting

scandals, occurred at the turn of this century when relations

between audit firm and company were largely between the

auditor’s engagement partner and the auditee’s finance

director: a similar position to that of the credit market

today. Where issues of affect become central to a gate-

keeping relationship, how sure can external parties be of

the gatekeeper’s role in withholding consent to lobbying

for an upgrade or managing financial communications to

postpone downgrades? Thus, when CRAs meet regularly

with their remunerating issuers to discuss the issuer’s

future strategy and prospects what use does the CRA make

of this information? Consider a situation where an issuer,

with a longstanding relationship with a CRA analyst, is

faced with a difficult trading environment but presents this

as a temporary situation along with a credible and coherent

story about the future prospects on the organisation. This

research has conceptualised the relationship qualities

inherent in the CRAs service offering as trust, cooperation,

and transparency. The nature of relationships is that these

qualities are to some degree reciprocal so that the coop-

erative, transparent, and responsive issuer who furnishes

the CRA with regular and reliable information enjoys a

position of trust and potentially higher status with the CRA

in its assessment of its prospects. The subjective element of

ratings decisions, largely attributable to the private infor-

mation made available to the CRA, sits uneasily with these

affective relations uncovered by this study.

Arguably the strength of any research work reflects an

identification of its limitations. Specifically, the investiga-

tion has four limitations which are suggestive of future

research. First, the study samples UK corporate issuers of

debt. Although debt issuance and the ratings industry are

by their nature pan-national, it is plausible that conceptions

of commitment and dependence could be different in other

geographic locations, as a consequence of different market

practices and regulatory frameworks. For example, the US

was the first regime to implement formal regulation of

CRAs and ratings have long been an established part of

debt markets. By contrast, in continental Europe ratings are

generally considered less important and CRAs have

struggled to gain a foothold in the market. Future research

might thus wish to examine issuers’ perceptions in other

countries or economic areas.

Second, feelings of commitment, particularly Affective

Commitment, might differ between specific CRAs, e.g.

issuers might feel emotionally attached to Moody’s

because they offer an excellent client service, but do not

feel the same level of attachment to S&P. By contrast,

issuers may believe S&P offer a higher level of technical

ratings quality, but without the positive affective element

that other CRAs are believed to possess. The research

design used for this study did not allow testing for these

differences as most issuers used more than one CRA and

data was not collected separately for these agencies. Future

research could attempt to establish whether issuer percep-

tions differ between individual CRAs and whether specific

CRAs are more successful in securing their clients’ com-

mitment than others. It would be particularly interesting to

see whether smaller CRAs are more successful in achiev-

ing this than the larger CRAs.

Third, this study used the constructs of Technical

Qualities and Relationship Qualities. However, it is plau-

sible given significant environmental upheaval in debt

An Empirical Study of the Role of Commitment

123

markets and the ratings industry that there might be dif-

ferent or additional antecedents that can provide further

insight into the issuer–CRA relationship. Examples of

other antecedents used in other industrial marketing related

studies have included factors such as satisfaction (Wetzels

et al. 1998), power structure (Brown et al. 1995), tie

strength (Stanko et al. 2007) and age of relationship

(Anderson and Weitz 1989).

Fourth, the investigation considers issuer perspectives of

the relationship. Yet, it is axiomatic that a relationship

involves at least two parties. As Cater and Zabkhar (2009,

p. 794) observe, there is a need to broaden the scope of

research to include views from the other side of the dyad.

We would argue that, from a governance perspective, the

raison d’etre of the ratings industry, that future research

could consider the views of third parties such as investors,

regulators, and users of ratings information, who may not

directly observe issuer–CRA interactions, that by their very

nature operate behind closed doors.

Conclusion

The CRA trinity of solicitude is described by three per-

vasive concerns regarding the operation of the ratings

industry. This paper provides another angle on the deter-

minants of the trinity of solicitude: relations and concom-

itant commitment between the ratee and rator. In particular,

the investigation by its novel application of the exchange

relationship literature to the credit ratings process has

highlighted how committed issuers feel in their relations

with CRAs. In turn, this provides a perspective on each of

the three elements of the CRA trinity of solicitude. Given

the scrutiny the ratings industry has encountered, and

continued discussion of the politics of creditworthiness (cf.

Sinclair 2005) to face, we believe a consideration of the

dyadic relationship offers another perspective on the

somewhat elusive nature of ratings quality and a fecund

area for future research.

In particular, the finding that Affective Commitment is

induced by Relationship Qualities, which in turn lead to

Continuance Intentions has important consequences for

corporate governance and regulatory work in the ratings

arena. CRAs are typically described as gatekeepers to

capital markets (Coffee 2006) and the loyal agents of

investors (Sinclair 2005; Langohr and Langohr 2008). The

findings of this research suggest that affective relations

between the issuer’s Treasurer and the CRA’s Lead Ana-

lyst have a significant effect on the longevity of the rela-

tionship. It also suggests the connexion between the two

parties is closer than is often described, which may

potentially threaten the independence of the CRA. Prior

work suggests that issuers select CRAs on the basis of

analysts or agencies with whom they have worked suc-

cessfully in the past (Duff and Einig 2007). For regulators

concerned to improve ratings quality our findings suggest

that CRA selection might be improved if each issuer

established an Independent Ratings Committee, established

as a committee of the board of directors with delegated

responsibility from the board for overseeing the ratings

process. Such committees have been adopted for the

external audit function within companies in North America

since the 1970s and have become widely established in

many parts of the world. While the inherent conflict of

interest remains, the increasing governance of the ratings

process from the side of the ratee should add to investor

and other stakeholder perspectives.

This study highlights the significance of relationships to

the ratings process and emphasises that the ratings process

is not just one of number-crunching financial analysis, with

opaque methodologies, and varying degrees of due dili-

gence. Rather it is a relationship whereby effective com-

munication relates to matters of affect rather than wholly

matters of cognition or calculative appraisal. The search

for, acquisition, and maintenance of a meritorious rating is

not solely a reporting-driven exercise. The need for careful

and reciprocal communications between the issuer and the

CRA mean that it is unlikely that the ratings process will

ever be truly transparent. If borrowers were forced to

publicly disclose non-public information as a matter of

course, then they would lose competitive advantage to

unrated rivals, essentially ending their access to public debt

markets.

The research also sheds some light on why the ratings

market suffers from a lack of competition. The dependence

of ratees on their rator, the highlighting of affective com-

mitment and the limited concern for technical qualities

indicate borrowers are unlikely to welcome new suppliers

of credit information to the market. The sheer cost of

developing and maintaining a relationship makes such

work prohibitive. Our research suggests that issuers are a

powerful obstacle to be overcome in the regulatory mission

to make the ratings game more open to new suppliers. If

regulators seriously wish to improve competition, they may

wish to consider alternatives such as mandatory inclusion

of smaller agencies, alongside the largest two CRAs, for

larger issuers.

Commentators’ interest in the trinity of solicitude has

been largely driven by the CRAs’ role in the current eco-

nomic crisis. It is important to understand that the lack of

confidence in CRAs’ ability is due to the rapid expansion of

securitised debt markets and their concomitant role. The

structured finance products accompanying these markets

owe their provenance to the ratings provided to the tranches

of debt of varying creditworthiness. Ratings agencies were

traditionally autonomous, almost academic, publishing

A. Duff, S. Einig

123

organisations whose hallmark was their independent and

impartial opinion. The growth of structured finance markets

along with the lure of providing ratings advisory and con-

sulting services created a position whereby the culture of the

CRAs changed from the quasi-academic to the commercial.

New financial products represented new financial markets

and an opportunity for growth and enlarged market capi-

talisation. This new culture when combined with the trinity

of solicitude of conflicts of interest, poor transparency and

lack of competition creates a dangerous cocktail. Our study

highlights in particular the paradoxical role of affective

relations between CRA and issuer personnel. On the one

hand, proactive CRAs who elicit real-time information from

issuers by the development of constructive working rela-

tionships have the capacity to enhance actual ratings quality,

i.e. the ability to accurately predict the probability of default

on a timely basis. On the other hand, creating affective

relations combined with the spectre of commercialised

CRAs viewing issuers as clients has a detrimental effect on

public confidence in ratings and the CRAs themselves.

Appendix

Measures

A Note on Scale Development

Initially, three additional factors were hypothesized:

(i) Normative commitment measuring to which degree

issuers felt morally obliged to remain with their CRAs; (ii)

Opportunistic behaviour measuring to what extent issuers

behave opportunistically and try to find better alternatives

or use the existence of other CRAs to negotiate more

favourable terms; and (iii) additional CRAs measuring

what factors would cause issuers to engage additional

CRAs. However, these scales failed to achieve acceptable

levels of internal consistency reliability (a\ .6) and were

thus removed from the model. Some of the items relating to

these scales could be successfully included in other con-

structs; the remaining items were deleted from the model.

References

Achrol, R. (1997). Changes in the theory of interorganizational

relations in marketing: Toward a network paradigm. Journal of