Embed Size (px)

Citation preview

C.O.S.No.3/2020 1/25

IN THE COURT OF THE SPECIAL JUDGE FOR TRIAL AND DISPOSAL OFCOMMERCIAL DISPUTES, IBRAHIMPATNAM, VIJAYAWADA.

Present: Sri D.Yedukondalu,Special Judge for Trial and Disposal of Commercial Disputes,

Ibrahimpatnam, Vijayawada.

Thursday, this the 10th day of February, 2022.

C.O.S.No.3/2020

Between:

Sri Krishna Pharmaceuticals, Represented by its Proprietor Mr. K.V.K. Mohana Rao,S/o Purnachandra Rao, Hindu, aged about 47 years, Business, D.No.11-32-10B,Challamarajuvari Street, Vijayawada – 520 001.

... PlaintiffAND

1. M/s. Greenland Organics, Represented by its Partners, Having its place ofbusiness at D.No.6-174/1, Nuzvidu Road, Surampalli, Gannavaram – 521 212,Andhra Pradesh.

2. Vintha Vinod Reddy, S/o Prasad Reddy, Hindu, aged about – years, ManagingPartner, 6-174/1, Nuzividu Road, Surampalli, Gannavarm – 521 212, AndhraPradesh.

3. Vintha Seshidhar Reddy, Partner, S/o Prasad Reddy, 6-174/1, Nuzividu Road,Surampalli, Gannavarm – 521 212, Andhra Pradesh.

4. Vintha Prasad Reddy, S/o Koti Reddy, 6-174/1, Nuzividu Road, Surampalli,Gannavarm – 521 212, Andhra Pradesh.

... Defendants

This suit is coming on 03.01.2022 for final hearing before me in the presence of SriSk. Khadir, Advocate for plaintiff; Sri V.V.Varada Rajulu, Advocate for defendants; uponhearing and considering the material on record, and the matter having stood over forconsideration till this day, this court delivered the following:

// J U D G M E N T //

The plaintiff filed the suit against the defendants to: (a) declare that the

defendants are jointly and collectively liable to pay a sum of Rs.4,18,06,218/- to the

plaintiff including interest till date; (b) direct the defendants jointly and collectively to

pay a sum of Rs.4,18,06,218/- to the plaintiff including interest; (c) direct the

defendants jointly and severally to pay the plaintiff future interest at the rate of 24%

p.a., on a sum of Rs.2,59,66,595/-; and (e) for costs of the suit.

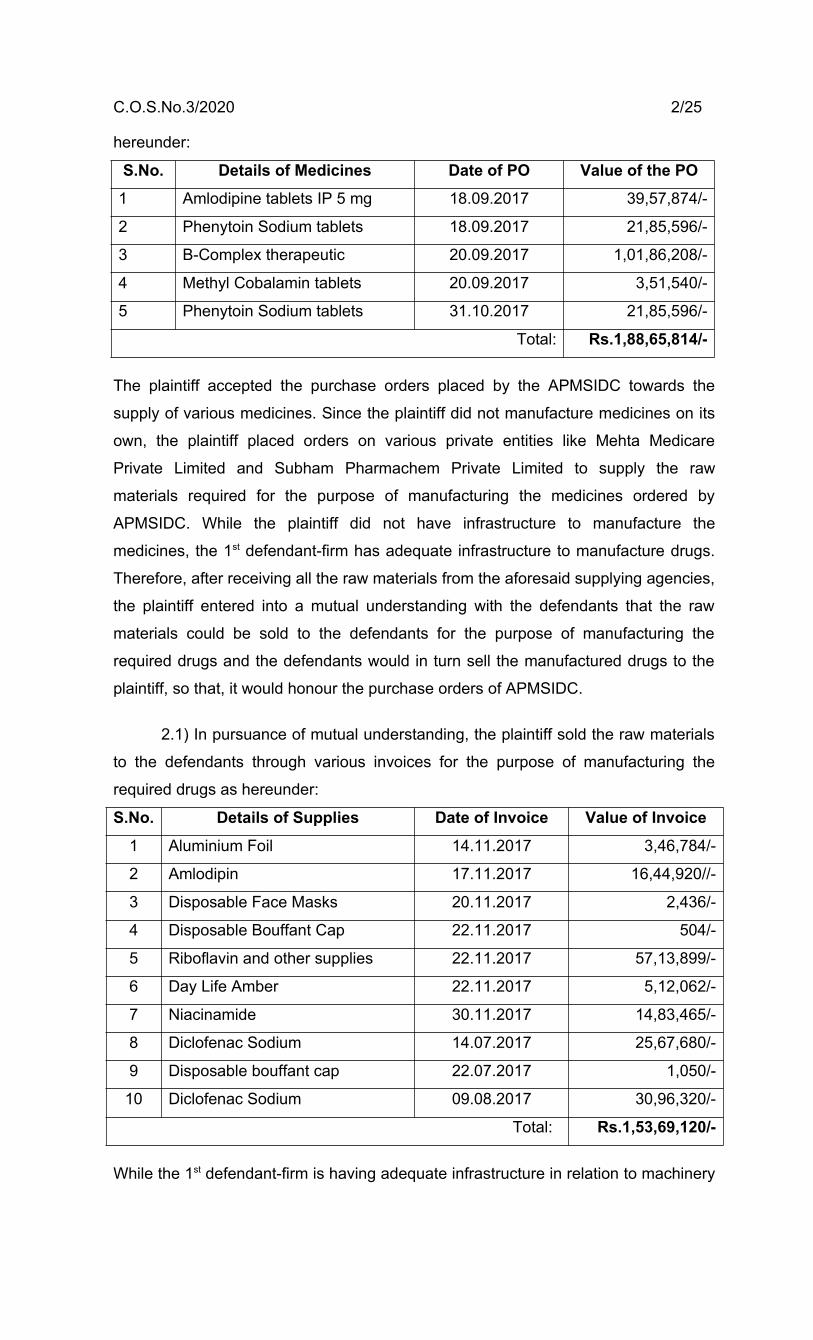

2) The brief averments in the plaint are as follows: The plaintiff is a proprietary

concern engaged in pharmaceutical business undertaking to supply various

medicines required by its clients including the Government Corporations. An

enterprise of Government of Andhra Pradesh viz., Andhra Pradesh Medical Services

and Infrastructure Development Corporation (in short APMSIDC) placed few

purchase orders on the plaintiff for the supply of various medicines tuning to the total

value of Rs.1,88,65,814/- in and around the month of September, 2017 as mentioned

C.O.S.No.3/2020 2/25

hereunder:

S.No. Details of Medicines Date of PO Value of the PO1 Amlodipine tablets IP 5 mg 18.09.2017 39,57,874/-

2 Phenytoin Sodium tablets 18.09.2017 21,85,596/-

3 B-Complex therapeutic 20.09.2017 1,01,86,208/-

4 Methyl Cobalamin tablets 20.09.2017 3,51,540/-

5 Phenytoin Sodium tablets 31.10.2017 21,85,596/-

Total: Rs.1,88,65,814/-

The plaintiff accepted the purchase orders placed by the APMSIDC towards the

supply of various medicines. Since the plaintiff did not manufacture medicines on its

own, the plaintiff placed orders on various private entities like Mehta Medicare

Private Limited and Subham Pharmachem Private Limited to supply the raw

materials required for the purpose of manufacturing the medicines ordered by

APMSIDC. While the plaintiff did not have infrastructure to manufacture the

medicines, the 1st defendant-firm has adequate infrastructure to manufacture drugs.

Therefore, after receiving all the raw materials from the aforesaid supplying agencies,

the plaintiff entered into a mutual understanding with the defendants that the raw

materials could be sold to the defendants for the purpose of manufacturing the

required drugs and the defendants would in turn sell the manufactured drugs to the

plaintiff, so that, it would honour the purchase orders of APMSIDC.

2.1) In pursuance of mutual understanding, the plaintiff sold the raw materials

to the defendants through various invoices for the purpose of manufacturing the

required drugs as hereunder:

S.No. Details of Supplies Date of Invoice Value of Invoice1 Aluminium Foil 14.11.2017 3,46,784/-

2 Amlodipin 17.11.2017 16,44,920//-

3 Disposable Face Masks 20.11.2017 2,436/-

4 Disposable Bouffant Cap 22.11.2017 504/-

5 Riboflavin and other supplies 22.11.2017 57,13,899/-

6 Day Life Amber 22.11.2017 5,12,062/-

7 Niacinamide 30.11.2017 14,83,465/-

8 Diclofenac Sodium 14.07.2017 25,67,680/-

9 Disposable bouffant cap 22.07.2017 1,050/-

10 Diclofenac Sodium 09.08.2017 30,96,320/-

Total: Rs.1,53,69,120/-

While the 1st defendant-firm is having adequate infrastructure in relation to machinery

C.O.S.No.3/2020 3/25

and equipment to manufacture the drugs, it lacks ancillary infrastructure, man power

and technology to run the laboratory to manufacture the drugs. Therefore, the

defendants requested the plaintiff to help the defendant-firm financing them in order

to run the laboratory to accomplish the project handed over to them by the plaintiff to

manufacture the drugs. Accordingly, the plaintiff financed the defendant-firm from

time to time to run their day-to-day activities for the purpose of manufacturing the

drugs. The plaintiff transferred money directly to the defendants bank account on

various occasions totaling to an amount of Rs.51,18,880/- and also paid in cash to

the defendants totaling to a sum of Rs.53,43,440/-. The plaintiff also sold the raw

materials worth of Rs.1,53,69,122/- and also paid income tax on behalf of the plaintiff

for a sum of Rs.1,23,460/- totaling to Rs.2,59,54,902/-. The plaintiff will get

Rs.17,074/- towards interest till the institution of the suit.

2.2) As per the mutual understanding, the plaintiff raised the credit sales bills

for the requisite raw materials to the 1st defendant-firm to follow the rules and norms

as per the Central Goods and Services Tax Act, 2017 and the Drugs and Cosmetics

Act, 1940. So that, the defendants would manufacture the required drugs for the

plaintiff and the plaintiff in turn purchase the same from the defendants and also

supply the same to APMSIDC. Though the defendants were required to clear the

amount within 30 days from the date of invoice, the defendants had not paid the

amount to the plaintiff and in turn, the defendants requested the plaintiff to finance

them for their day to day business activities in order to accomplish the project of

manufacturing the drugs for the plaintiff. The plaintiff was aware of the financial

difficulties of the defendants while entering into the contract and with good faith, the

plaintiff agreed for the project because the 1st defendant-firm requested by its

partners was having relationship for the last 10 years with the plaintiff and

categorically promised that all the invoices and the amount paid for running the

laboratory would be cleared with interest.

2.3) When the defendants failed to supply the drugs even after the

considerable period of time, the plaintiff started following up with the defendants for

the supply of drugs. When the defendants neither supplied the drugs nor returned

the total amount due, after admitting the liability, the defendants finally offered

cheques in favour of plaintiff towards clearing the dues as hereunder:

Cheque No. Date Amount Bank403766 06.12.2019 Rs.53,87,395/- IDBI Bank

144112 08.12.2019 Rs.1,50,00,000/- IOB

144114 30.11.2019 Rs.93,78,000/- IOB

Total: Rs.2,97,65,395/-

C.O.S.No.3/2020 4/25

To the utter shock and surprise of the plaintiff, the cheques were dishonored upon

presenting the same for encashment with an endorsement of insufficient funds. As a

result, the defendants became jointly and collectively liable to the plaintiff to the

admitted amount of Rs.2,97,65,395/- including interest. The transaction comes under

the definition of Sec.2(1)(c) of Commercial Courts Act, 2015. Hence, the plaintiff is

entitled for a sum of Rs.4,18,06,218/- including interest at the rate of 24% p.a.

Hence, the suit.

3) The defendants 1 & 2 filed written statement and the same was adopted by

the defendants 3 & 4. The defendants 1 & 2 denied the material allegations in the

plaint and submitted that they purchased raw materials from the plaintiff and

immediately after the said transaction, they repaid the amount to the plaintiff, but the

plaintiff intentionally suppressed the said fact. No business man would place the

orders for the firm which was not having any sort of capital to complete the work.

The defendants 1 & 2 repaid the amount within the stipulated time for supply of raw

materials which was purchased for their own business purpose. They never entered

into such an understanding of receiving raw material and supply of medicines after

manufacturing with the alleged material. The defendant 1 & 2 were having orders

directly from APMSIDC, and they were regularly supplying the medicines to the said

organization. It was impossible for them to enter into any transaction with the plaintiff

to purchase the raw material and could sell finished medicines to the plaintiff. The

defendants were having orders from the Government Organization and they fulfilled

the orders within time. Under those circumstances, entering into any transaction with

the plaintiff was nothing but a deliberate lie and the defendants were not having such

a capacity to entertain the work of the others, as they were busy with their work

which was directly entrusted by the said organization. They never issued any

cheques relating to the alleged transactions with the plaintiff, the cheques were given

only for security and the defendants repaid the amounts for every transaction and

purchase of raw material from the plaintiff immediately within 30 days.

3.1) According to the version of the plaintiff in the plaint, the plaintiff received

orders from APMSIDC for supply of medicines and in connection with that, the

plaintiff entered into the transaction with the defendants. But, as per the documents

filed by the plaintiff, the said version was proved as false. As the alleged order

obtained by the plaintiff from APMSIDC was relating to the month of September,

2017. As per the version of the plaintiff, after the said order from APMSIDC, the

plaintiff entered into the transaction with the defendants. But, as per the list of

documents filed by the plaintiff, the bill Nos.685, 707, 818 were dated 14.07.2017,

22.07.2017 and 09.8.2017 prior to the date of 18.09.2017. So, the bills were

C.O.S.No.3/2020 5/25

examples to prove that the plaintiff entered into transaction with the defendants

before obtaining the order from APMSIDC.

3.2) As per the version of the plaintiff, the plaintiff supplied the amount to the

defendants to fulfill the order placed by the defendants for manufacturing of the

medicines as the plaintiff obtained order from APMSIDC. The order was obtained on

18.09.2017 from the said organization. But, according to document No.13, the

vouchers were prior to the date of 18.09.2017. So, the version of the plaintiff that he

supplied the amount to the defendants for manufacturing the medicines for the orders

of the plaintiff was false. The defendants never entered into any such understanding

of supplying of medicines to the plaintiff at any point of time. They purchased the raw

materials for their own business purpose, and they repaid the amount within 30 days.

The plaintiff suppressed the true and correct facts and filed the suit for the reason

that the plaintiff came to know that several amounts were due by the said

Government Organization to the defendants and to get wrongful gain from the

defendants. Moreover, in order to get over the mandatory requirements under

Sec.12A of the Commercial Courts Act, 2015, the plaintiff filed false petition for

attachment of amounts lying with the said organization and absolutely belonging to

the defendants. The plaintiff did not file any paper to prove the understanding

between the plaintiff and defendants relating to supply of raw materials by the plaintiff

and supply medicines by the defendants to the plaintiff.

3.3) The plaintiff went to the extent of creating the stamp of the 1 st defendant-

firm for the alleged transaction of the purchase by the 2nd defendant, he signed only

in his individual capacity, but not as Managing Partner of the 1 st defendant-firm. The

stamp did not belong to the 1st defendant-firm, and it was created by the plaintiff. The

plaintiff intentionally tagged the personal transaction of the 2nd defendant with the 1st

defendant. The 4th defendant is no way concerned with the 1st defendant and the suit

is bad for mis-joinder of the 4th defendant. The plaintiff unnecessarily added the 4 th

defendant to the suit. The defendants were not due any amount to the plaintiff, and

they prayed the Court to dismiss the suit.

4) After filing the written statement, the defendants and plaintiff filed their

respective statements of admissions and denials of documents as required under

Order XI Rule 4 of the Code of Civil Procedure, 1908 as amended by the Commercial

Courts Act, 2015. After hearing the learned Counsel for the plaintiff and the learned

Counsel for the defendants in case management, the following issues were framed

for the purpose of trial:

1. Whether the plaintiff has business relationship with the 1st defendant-firm inrespect of suit transactions?

C.O.S.No.3/2020 6/25

1. Whether the bills and vouchers raised by the plaintiff are true, valid andbinding on the defendants?

2. Whether the defendants issued the cheques in favour of the plaintiff in respectof suit transactions?

3. Whether the 4th defendant is also partner of the 1st defendant-firm?4. Whether the plaintiff is entitled for recovery of suit amount with interest, as

prayed for?5. To what relief?

5) To substantiate the case of the plaintiff, the proprietor of the plaintiff viz., Sri

K.V.K. Mohana Rao gave evidence as PW1 and Exs.A1 to A38 were marked on

behalf of the plaintiff. (Exs.A20 to A38 were marked during the cross-examination of

DW1). On the other hand, the 2nd defendant viz., Sri Vintha Vinod Reddy gave

evidence as DW1 and Exs.B1 to B3 were marked on behalf of the defendants.

6) The learned Counsel for the defendants and the learned Counsel for the

plaintiff filed their respective written arguments. I heard the learned Counsel for the

defendants and the learned Counsel for the plaintiff.

7) Issue No.1: The plaintiff at Para No.3.1 of the plaint categorically pleaded

that the APMSIDC placed few purchase orders for a sum of Rs.1,88,65,814/-, the

details of which were furnished for 05 items, in the month of September, 2017.

During the evidence, PW1-K.V.K.Mohana Rao who was said to be the proprietor of

the plaintiff also deposed that APMSIDC placed purchase orders on 18.09.2017,

20.09.2017 and on 31.10.2017. The plaintiff further pleaded that after accepting the

purchase orders, the plaintiff placed orders on various private entities like Mehata

Medicare Private Limited and Shubham Pharmachem Private Limited to supply the

raw materials and as the plaintiff did not have infrastructure to manufacture the

medicines, and the 1st defendant-firm had adequate infrastructure, the plaintiff

entered into a mutual understanding with the defendants that the raw materials would

be sold to the defendants for the purpose of manufacturing the required drugs and

the defendants would in turn sell the manufactured drugs to the plaintiff, so that, the

plaintiff would honour the purchase order of APMSIDC. The said facts were clearly

pleaded by the plaintiff at Para No.3.2 of the plaint and also deposed by PW1-

K.V.K.Mohana Rao at Para No.3 of his chief affidavit. The plaintiff also pleaded that

it supplied the raw materials mentioned in Para No.3.3 of the plaint and also stated in

Para No.4 of the chief affidavit of PW1-K.V.K.Mohana Rao that the plaintiff supplied

raw materials worth Rs.1,53,69,120/- through various invoices. Though the

defendants admitted the earlier transactions with the plaintiff, they categorically

denied the transactions pleaded by the plaintiff especially basing on the purchase

orders placed by APMSIDC. Hence, this issue was framed placing the burden on the

C.O.S.No.3/2020 7/25

plaintiff to prove the business transaction of the plaintiff with the defendants.

7.1) In order to prove the version of the plaintiff, the plaintiff relied upon the

evidence of PW1-K.V.K.Mohana Rao coupled with Exs.A1 to A19 marked through

the PW1-K.V.K.Mohana Rao and Exs.A20 to A38 marked during the cross-

examination of DW1-Vintha Vinod Reddy. As argued by the learned Counsel for

defendants, the plaintiff shall prove his case as pleaded in the plaint and it cannot

travel beyond its pleadings. In this regard, the learned Counsel for the defendants

relied upon a decision of Hon’ble High Court of Andhra Pradesh in AllamGangadhara Rao v. Gollapalli Gangarao1, wherein at Para No.7, it was held as

hereunder:“It is trite to say that a party is expected and is bound to prove the case as alleged by

him and as covered by the issues framed. This is in accordance with the main

principle of practice that a party can only succeed according to what was alleged and

proved: secundum allegate et probata. He should not he allowed to succeed on a

case which he has failed to set up. He should not be permitted to change his case or

set up a case which is inconsistent with what he had himself alleged in his pleading

except by way of amendment of the plaint.”

So, the burden lies upon the plaintiff to prove its case as pleaded in the plaint. As I

earlier mentioned, the plaintiff relied upon as many as 19 documents marked through

PW1-K.V.K.Mohana Rao and other documents marked through DW1-Vintha Vinod

Reddy during his cross-examination. As argued by the learned Counsel for the

defendants, majority of the documents filed by the plaintiff were the electronic

records. On the other hand, the learned Counsel for the plaintiff argued that the

electronic records were placed before the Court by enclosing a certificate in

accordance with the provisions of Sec.65B of the Indian Evidence Act, 1872. But, as

it could be seen from the evidence of PW1-K.V.K.Mohana Rao, some of the

documents were marked subject to admissibility and subject to the provisions of

Sec.65B of the Indian Evidence Act, 1872. The said marking was given in the light of

a Three Judge Bench decision of Hon’ble Supreme Court of India in Bipin ShantilalPanchal v. State of Gujarat and Anr.2, wherein at Para No.14, it was held as

hereunder:“When so recast, the practice which can be a better substitute is this: Whenever an

objection is raised during evidence taking stage regarding the admissibility of any

material or item of oral evidence the trial court can make a note of such objection and

mark the objected document tentatively as an exhibit in the case (or record the

objected part of the oral evidence) subject to such objections to be decided at the last

stage in the final judgment. If the court finds at the final stage that the objection so

raised is sustainable the judge or magistrate can keep such evidence excluded from

1 AIR 1968 (AP) 291 2 2001 (3) SCC 1

C.O.S.No.3/2020 8/25

consideration. In our view there is no illegality in adopting such a course. (However,

we make it clear that if the objection relates to deficiency of stamp duty of a document

the court has to decide the objection before proceeding further. For all other

objections the procedure suggested above can be followed.)”

So, the documents marked subject to admissibility and the provisions of Sec.65B of

the Indian Evidence Act, 1872 shall be proved in accordance with the Law.

7.2) According to the evidence of PW1-K.V.K.Mohana Rao coupled with

Ex.A1, the plaintiff raised sale bills 10 in number in favour of the 1st defendant. As it

could be seen from Ex.A1 sale bills in the name of tax invoices 10 in number, they

are also electronic records attached with a declaration of PW1-K.V.K.Mohana Rao.

For better appreciation, the declaration on the back side of each tax invoice is

extracted as hereunder:“I, K.V.K. Mohana Rao S/o K. Poorna Chandra Rao, Proprietor of Sri Krishna

Pharmaceuticals, D.No.11-32-10B, Challamrajuvari street, Vijayawada – 520 001.

The invoice No.1363, dt.14.11.2017 was generated, stored and printed by me.

The Deponent knowledge, preparation, storage and issuance or receipt of

each such document of invoice or record on a computer resource including external

servers, details of ownership custody and access to such data on the computer or

computer resource and knowledge of contents and correctness of contents. And

further state that the computer or computer resource used for preparing or receiving

or storing such documents or data was functioning properly or in case of malfunction

that such malfunction did not affect the contents of the documents stored.”

At the time of marking Ex.A1 sale bills 10 in number, the learned Counsel for the

defendants did not make any objection as to admissibility of the documents

according to the provisions of Sec.65B of the Indian Evidence Act, 1872. So, Ex.A1

sale bills were admitted without any objection. But, as it could be seen from the

declaration, PW1-K.V.K.Mohana Rao stated that the data was generated, stored and

printed by him, and he had knowledge about the correctness of the contents and the

computer in question was functioning properly. A Three Judge Bench of Hon’ble

Supreme Court of India while answering a reference in Arjun Panditrao Khotkar v.Kailash Kushanrao Gorantyal3, at Para No.25 it was held as hereunder:

“Under Sub-section (4), a certificate is to be produced that identifies the electronic

record containing the statement and describes the manner in which it is produced, or

gives particulars of the device involved in the production of the electronic record to

show that the electronic record was produced by a computer, by either a person

occupying a responsible official position in relation to the operation of the relevant

device; or a person who is in the management of “relevant activities” – whichever is

appropriate.”

Further, the Hon’ble Supreme Court of India observed its previous decision in Anvar

3 2020 (7) SCC 1

C.O.S.No.3/2020 9/25

P.V v. P.K. Basheer and Ors (2014 10 SCC 473), at Para No.26, in which Para

No.15 of the decision with reference to the requirement of Sec.65B of the Indian

Evidence Act, 1872 was extracted as hereunder:“15. Under Section 65-B(4) of the Evidence Act, if it is desired to give a statement in

any proceedings pertaining to an electronic record, it is permissible provided the

following conditions are satisfied:

(a) There must be a certificate which identifies the electronic record containing the

statement;

(b) The certificate must describe the manner in which the electronic record was

produced;

(c) The certificate must furnish the particulars of the device involved in the production

of that record;

(d) The certificate must deal with the applicable conditions mentioned under Section

65-B(2) of the Evidence Act; and

(e) The certificate must be signed by a person occupying a responsible official

position in relation to the operation of the relevant device.”

Finally, the Hon’ble Apex Court of India at Para No.34 answered the reference with a

small modification omitting the words “under Section 62 of the Evidence Act” in Para

No.22 of the decision in Anwar P.V’s case referred supra. According to this decision,

the person producing the electronic record shall give the certificate identifying the

electronic record, describing the manner in which the electronic record was

produced, furnishing the particulars of the device involved in production of that

record, involving with the applicable conditions mentioned under Se.65B(2) of the

Indian Evidence Act, 1872 and affixing the signature by the person responsible

official position in relation to operation of the relevant device. But, as it could be seen

from the declaration given by PW1-K.V.K.Mohana Rao extracted supra though he

mentioned that he generated stored and printed certificate, and he had knowledge

about the preparation, storage and issuance or receipt of the document and also

correctness of the contents, he never mentioned in the certificate describing the

manner in which the electronic record was produced, and furnishing the particulars of

device involved in the production of the electronic record. In other words, the manner

of generating the documents and the identity of the computer in question were not

furnished by PW1-K.V.K.Mohana Rao. In such a case, the electronic record shall be

inadmissible by virtue of the express provisions mentioned under Sec.65B(1) of the

Indian Evidence Act, 1872.

7.3) But, as I earlier mentioned, the defendant did not raise any objection for

admission of the document at the time of marking Ex.A1. But, the learned Counsel

for the defendants argued that the defendant never received the goods under Ex.A1.

He had drawn my attention to the cross-examination of PW1-K.V.K.Mohana Rao

C.O.S.No.3/2020 10/25

wherein he deposed that he did not file the suit basing on the transactions taken

place between him and the defendants as per the orders placed by APMSIDC, but,

he mentioned in the plaint that he made transactions with the defendants to comply

the orders of APMSIDC. PW1-K.V.K.Mohana Rao also furnished the dates of

purchasing orders. It was an admitted fact that PW1-K.V.K.Mohana Rao also

purchased medicines once or twice during the last 10 years, and it was elicited from

the cross-examination of DW1-Vintha Vinod Reddy that he took stock, cash from the

plaintiff prior to the suit transactions. So, there were transactions between the plaintiff

and defendants prior to the purchase orders placed by APMSIDC. As I earlier

mentioned, this mutual understanding was especially entered by the plaintiff with the

defendants after APMSIDC had placed the purchase orders as pleaded by the

plaintiff and stated by PW1-K.V.K.Mohana Rao in his chief affidavit referred supra.

So, whatever the transactions between the plaintiff and defendant prior to the

purchase orders placed by APMSIDC were out of the cause of action contained in

this suit.

7.4) Apart from it, PW1-K.V.K.Mohana Rao, during his cross-examination, at

first instance deposed that he submitted documentary proof with respect to business

transaction with the defendants and at the second instance, he deposed that he did

not have any document to prove that he supplied raw material to the defendants, and

they supplied medicines to him. As argued by learned Counsel for defendants, Ex.A1

sale bills (tax invoices) did not contain the signatures of the defendants

acknowledging the receipts of the goods. Moreover, PW1-K.V.K.Mohana Rao gave

such fatal admission that he did not have any document to prove that he supplied the

raw material to the defendants. So, the plaintiff failed to prove that it supplied raw

materials to the defendants as pleaded at Para No.3.3 of the plaint with the evidence

of PW1-K.V.K.Mohana Rao. But, as argued by the learned counsel for the plaintiff,

the defendants while filing the statement of admissions and denials of the document

admitted the sale bills (tax invoices).

7.5) As I earlier mentioned, the plaintiff also pleaded that it purchased the raw

materials from Mehata Medicare Private Limited and Shubham Pharmachem Private

Limited, and supply the same to the plaintiff. In order to prove the said facts, the

plaintiff relied upon the evidence of PW1-K.V.K.Mohana Rao coupled with Exs.A2

and A3 tax invoices said to be issued by Mehata Medicare Private Limited and

Shubham Pharmachem Private Limited. These two documents were admitted in

evidence as Photostat copies containing the original signature and declaration of

plaintiff and subject to admissibility. Upon keen observation of Ex.A2 tax invoice

issued by Mehata Medicare Private Limited, it was signed by authorized signatory,

C.O.S.No.3/2020 11/25

but the Photostat copy of it was filed. Similarly, Ex.A3 Photostat copy of tax invoice

issued by Shubham Pharmachem Private Limited was filed even without the

signature of authorized person. But, these two documents contained the original

signatures and declarations of the plaintiff for the purpose of Sec.65B of the Indian

Evidence Act, 1872. When the tax invoices were computer outputs and electronic

records, a certificate shall be issued by the authorized persons of the respective

companies. But, for the reasons best known to the PW1-K.V.K.Mohana Rao, he

stamped, signed and attached his declaration to Exs.A2 and A3. Then, it shall be

deemed that these documents are also generated, stored and printed by him, though

they are issued by the said two companies. So, both the documents are inadmissible

in evidence for want of production of the originals and production of the Photostat

copies without complying the conditions mentioned under Sec.65 of the Indian

Evidence Act, 1872. Similarly, PW1-K.V.K.Mohana Rao is not competent to give

declaration/certificate for the purpose of Sec.65B (4) of the Indian Evidence Act,

1872 as they are third party documents. Hence, the plaintiff failed to prove that the

plaintiff purchased raw materials from the said two companies. It may not be out of

place to mention that the plaintiff had no raw materials of its own to supply the same

to the defendants.

7.6) The plaintiff further relied upon the evidence of PW1-K.V.K.Mohana Rao

coupled with Exs.A4 & A5 computer generated statement of accounts relating to

Mehata Medicare Private Limited and Shubham Pharmachem Private Limited with

the declaration of the plaintiff. As I earlier mentioned, the declarations did not contain

the manner in which the electronic record was produced, and the particulars of the

electronic device involved in the production of the record. But, the learned counsel

for the defendants did not object the documents and at best Ex.A4 & A5 proved that

the plaintiff had some transactions with the said companies. Similarly, the plaintiff

produced two more statements of accounts relating to Sri Venkateswara Coil Mill

Private Limited marked as Ex.A6 and Feno Plast Limited marked as Ex.A7. As I

earlier mentioned, while dealing with Exs.A4 & A5, Exs.A6 & A7 also at best proved

the transactions of the plaintiff with the said companies. The plaintiff also filed one

more statement of account marked as Ex.A8 to prove that he had some monitory

transactions with the City Union Bank. As it could be seen from Ex.A8, it also

revealed the monitory transactions of the plaintiff with the City Union Bank. Ex.A9

was filed for the purpose of obtaining attachment before the judgment and the same

is not relevant to decide the issues in controversy in the main suit.

7.7) But, the plaintiff filed five purchase orders of APMSIDC pleaded by the

plaintiff at Para No.3.1 of the plaint and marked them as Ex.A10 through PW1-

C.O.S.No.3/2020 12/25

K.V.K.Mohana Rao. Ex.A10 is also an electronic record and marked subject to

admissibility and provisions of Sec.65B of the Indian Evidence Act, 1872. For the

reasons best known to the plaintiff, the plaintiff gave the same declaration to Ex.A10

without describing the manner in which the electronic record was produced, and

furnishing the particulars of the device. So, Ex.A10 is also inadmissible in evidence

according to Sec.65B (1) of the Indian Evidence Act, 1872. So, the plaintiff failed to

prove that APMSIDC placed purchase orders in the months of September and

October, 2017 as pleaded by the plaintiff and stated by PW1-K.V.K.Mohana Rao in

his chief affidavit.

7.8) The plaintiff further produced Photostat copies of income tax returns of

the plaintiff for the assessment years 2019-20 and 2018-19 marked as Exs.A11 and

A12 respectively. Obviously, the said documents marked as Ex.A11 and A12 are the

Photostat copies of the income tax returns of the plaintiff. But, for the reasons best

known to the plaintiff, the declaration of PW1-K.V.K.Mohana Rao was printed on the

back side of the 1st page of the document keeping the invoice number and date as

blank. Exs.A11 and A12 are inadmissible in evidence for want of primary evidence

and producing the secondary evidence without compliance of the provisions of

Sec.65 of the Indian Evidence Act, 1872. So, as it could be seen from the material

on record, the plaintiff pleaded that on receipt of the purchase orders from APMSIDC,

it entered into a mutual understanding with the defendants and supplied raw

materials worth Rs.1,53,69,120/-. But, it failed to prove the same except to the extent

of the documents admitted by the defendants in the statement of admissions and

denials of documents as the plaintiff failed to prove the purchase and supply of raw

materials by producing authenticated document.

7.9) The plaintiff also pleaded that as the defendants did not have sufficient

funds, the plaintiff transferred a sum of Rs.51,18,880/- to the bank account of the

defendants and paid cash of Rs.53,43,440/-, totaling a sum of Rs.1,05,85,780/-. The

plaintiff also pleaded that it paid income tax of Rs.1,23,460/- on behalf of the

defendants. The payment of income tax of Rs.1,23,460/- on behalf of the defendants

by the plaintiff was admitted by DW1-Vintha Vinod Reddy during his cross-

examination. The cash vouchers were admitted in evidence after collecting the stamp

duty and penalty. But, as it could be seen from the cash vouchers, those were filed

with supporting paper affixing 3 or 2 documents to each paper and the said paper

contained the same declaration as if they were also electronic records. The said

vouchers are not the electronic records, but those are issued in the names of Krishna

Mohan, S.K.P., K.Krishna Mohan and Sri Krishna Pharma. The name of PW1 is

‘K.V.K.Mohana Rao’ and the name of the plaintiff is ‘Sri Krishna Pharmaceuticals’.

C.O.S.No.3/2020 13/25

The vouchers were not issued either in the name of PW1-K.V.K.Mohana Rao or in

the name of the plaintiff. But, as argued by the learned Counsel for the plaintiff, the

DW1-Vintha Vinod Reddy admitted in the cross-examination that he mentioned in the

attachment that he received a sum of Rs.9,32,880/- i.e., a sum of Rs.3,00,000/- and

Rs.6,32,880/- through IOB RTGS and also admitted that he issued vouchers for

Rs.6,00,000/- on 06.07.2017, for Rs.14,00,000/- on 10.07.2017, for Rs.5,00,000/- on

26.07.2017 and for Rs.5,00,000/- on 31.07.2017. He categorically once again

admitted that he received cash of Rs.39,32,880/- in the year 2017 and issued

vouchers. He further also admitted that he received raw materials under 3 invoices

bearing Nos.685, 707 and 818 dated 14.07.2017, 22.07.2017 and 09.08.2017

respectively. But, for the reasons best known to PW1-K.V.K.Mohana Rao, he

categorically deposed that there were no monitory transactions between him and the

2nd defendant for the last 10 years. However, all these transactions were earlier to the

purchase orders placed by APMSIDC. But, as I earlier mentioned, the cause of

action started after purchase orders placed by the APMSIDC especially in view of a

mutual understanding pleaded by the plaintiff and stated by the PW1-K.V.K.Mohana

Rao. So, the admission of DW1-Vintha Vinod Reddy did not prove the contention of

the plaintiff as pleaded in the plaint.

7.10) The plaintiff further produced Ex.A14 computer generated statement of

account relating to the 1st defendant-firm with the declaration of PW1-K.V.K.Mohana

Rao. The said document was admitted in evidence without any objection though it

was also lack of information regarding the manner in which the electronic record was

produced and the particulars of device involved in the production of the record.

Though it is deemed to be proved, the debt under Ex.A14 statement of account was

not acknowledged by the defendants. As such, it cannot solely help the plaintiff in

getting the decree. Coming to Ex.A15 computer generated statement of account

issued by City Union Bank Limited, the plaintiff filed the same to prove RTGS transfer

in favour of the 1st defendant. But, the said document was admitted in evidence

subject to admissibility and provisions of Sec.65B of the Indian Evidence Act, 1872.

The document did not contain the certificate by the responsible person of the Bank,

but it contained the declaration of the plaintiff mentioned supra. Though the

document was not generated by the plaintiff, PW1-K.V.K.Mohana Rao declared as if

it was generated by him. So, the plaintiff further failed to prove that it transferred any

amount to the 1st defendant-firm for want of the authenticated document. The learned

Counsel for defendants also argued that Ex.A15 was not duly signed by the

authorized officer of the City Union Bank, and then it cannot be looked into. In this

regard, he relied upon a Division Bench decision of Hon’ble High Court of Andhra

C.O.S.No.3/2020 14/25

Pradesh at Hyderabad in Indian Bank, Chittor v. V.R.Venkataramana and Others4,wherein at Para No.20, it was held as hereunder:

“The question is whether the documents, which do not contain the endorsement as

required under Section 2(8) of the Bankers’ Book Evidence Act, can be treated as

certified copy or cannot be treated as certified copy within the meaning of the said

Section. The intention of the framers of the said Act is clear that whenever the

document is treated as certified copy it shall contain the endorsement. Mere mention

of true copy cannot lead to the conclusion that it is a certified copy. There is lot of

significance in insisting upon the endorsement due to the reason that originals are not

being produced into Court even for the purpose of comparison. The statue gives

exemption under the Bankers’ Books Evidence Act from production of the originals. It

lays down a particular procedure to produce the copies, which can be treated as

certified copies. Moreover, in the present case the certified copy does not contain the

seal and stamp of the bank. The statute has specified the nature of the certificate to

be endorsed. It is not the intention of the legislature to treat it as directory. It is

mandatory. It cannot be treated as certified copy, since endorsement mentioned by

the statute is not made. It is a safeguard placed on the extracts for acting on them as

evidence in truth.”

In the present suit, there is no endorsement of the authorized person as required

under Sec.2 (8) of the Bankers’ Book Evidence Act, 1891. Moreover, Sec.2-A of the

Bankers’ Book Evidence Act, 1891 was inserted by the Information Technology Act,

2000 making almost all the similar provisions under Sec.65B of the Indian Evidence

Act, 1872. So, the statement of account issued by the banker must be accompanied

by a certificate required under Sec.2(8) r/w Sec.2-A of the Bankers’ Book Evidence

Act, 1891. As the bank statement marked as Ex.A15 is not at all signed and certified

by the banker, the same is not admissible in evidence. So, the plaintiff failed to prove

the said RTGS money transaction.

7.11) Similarly, the plaintiff filed Ex.A16 computer generated copies of Form

GSTR-3B in order to prove the payment of integrated tax. But, those documents also

contained the declaration of the plaintiff. However, even if those documents are

regarded as proved, the plaintiff paid integrated tax to the concerned department, but

the name of the defendants was not found. Ex.A17 was computer generated sanction

letter issued by City Union Bank Limited with the signature, seal and declaration of

the plaintiff though the respective officer of the City Union Bank Limited ought to have

issued the certificate, the plaintiff attached his declaration for the reasons best known

to him. So, the said document is also inadmissible in evidence. Similarly, Ex.A18

sanction letter issued by City Union Bank Limited was also filed in the same manner

and it was also inadmissible evidence for want of certificate by proper person. So, as

it could be seen from the Exs.A1 to A18, the plaintiff failed to prove either the supply4 2004 (3) ALT 665 (D.B.)

C.O.S.No.3/2020 15/25

of raw materials (except to the extent of admitted documents) or transfer of the

amount or payment of cash to the defendants, especially in view of the mutual

understanding after APMSIDC had placed the purchase orders.

7.12) But, the learned Counsel for plaintiff tried to elicit certain facts through

DW1-Vintha Vinod Reddy in order to prove business transactions between plaintiff

and defendants. During the cross-examination, he put a straight question and DW1-

Vintha Vinod Reddy answered that he did business with the plaintiff earlier, and he

did not have any business with the plaintiff connected to suit transaction. So, there

was no clear and categorical admission even on the part of the defendants. He made

one more attempt questioning DW1-Vintha Vinod Reddy whether he entered into any

business with the plaintiff prior to filing the suit. The learned Counsel for plaintiff

insisted him to say ‘yes or no’ and the witness said ‘no’. Once DW1-Vintha Vinod

Reddy gave a categorical statement that he did not do any business with the plaintiff

connected to the suit transaction, and he did business with the plaintiff earlier, it

could not be possible to him to say ‘yes or no’ to the same question once again. But,

the learned Counsel for plaintiff insisted him and the witness said ‘no’. So, there was

no admission on the part of the defendants in respect of business transaction of the

plaintiff with the defendants covered under the suit basing on the cause of action

arose after the APMSIDC placed its purchase orders, except in the form of statement

of admissions and denials of documents referred supra.

7.13) The learned Counsel for plaintiff tried to elicit several answers by

confronting several mails to DW1-Vintha Vinod Reddy during his cross-examination.

DW1-Vintha Vinod Reddy admitted in his cross-examination that he sent a mail to the

plaintiff marked as Ex.A20 on 04.08.2017. Ex.A21 is the attachment to the e-mail

marked as Ex.A20. In the said attachment, he mentioned that he received

Rs.9,32,880/- but the mail itself was dated 04.08.2017 prior to the date of placing the

orders by APMSIDC. Similarly, DW1-Vintha Vinod Reddy admitted that he also sent

e-mail marked as Ex.A22 on 06.07.2017 along with an attachment marked as Ex.A23

dated 05.07.2017. The e-mail was also relating to requirement of raw material and

placing the order of Diclofenac Sodium, but those two documents were also prior to

the date of order placed by APMSIDC. Similarly, DW1-Vintha Vinod Reddy admitted

about the sending of e-mail dated 05.07.2017 marked as Ex.A24 and e-mail dated

01.07.2017 with two purchase orders dated 27.06.2017 and 28.06.2017 which were

prior to the date of orders placed by APMSIDC. The defendant also sent a statement

along with e-mail marked as Ex.A25 dated 01.07.2017 in which it was mentioned that

the plaintiff had to receive a sum of Rs.1,15,56,159/-. The statement of account was

relating to the date of 01.07.2017 prior to the date of order placed by APMSIDC.

C.O.S.No.3/2020 16/25

7.14) Apart from it, the learned counsel for the plaintiff confronted one more

document marked as Ex.A27 which was a copy of list of firms black listed. According

to the contents of Ex.A27, several firms including the 1st defendant (Sl.No.2) were

blacklisted due to supply of not of standard quality of drugs, especially, the 1st

defendant was black listed from 05.02.2018. In spite of it, the plaintiff transacted with

the 1st defendant till 18.07.2018 according to Ex.A.14. Once the 1st defendant-firm

was blacklisted on 05.02.2018 for the reason that it was not supplying standard

quality of drugs, the plaintiff could have normally stopped his transactions and

demanded the amount. It could have occurred in normal course. But, the transaction

of the plaintiff with the 1st defendant even after the 1st defendant-firm was blacklisted

on 05.02.2018 was beyond the normal course of business. It may not be out of place

to mention that the plaintiff pleaded that it filed the suit as the defendants did not sell

the manufactured drugs, but not as the 1st defendant-firm was blacklisted. However,

the plaintiff failed to prove that it supplied the raw material except to the extent of

admission of documents referred supra or paid the amounts due to want of

authenticated documentary proof and the oral admission of PW1-K.V.K.Mohana Rao

with respect to monitory transactions for the last 10 years, referred supra.

7.15) However, the learned counsel for plaintiff further confronted one more

e-mail dated 03.01.2018 marked as Ex.A28 with attachment. As deposed by DW1-

Vintha Vinod Reddy, there were no transactions between him and the plaintiff with

respect to attachment sent with Ex.A28 e-mail. As it could be seen from the

attachment, the 1st defendant simply forwarded the said e-mail to the plaintiff with the

attachment stood in the name of the plaintiff. In other words, the attachment was

prepared in the name of the plaintiff along with the 05 Government purchase orders,

but it was not relating to any transaction between the plaintiff and defendants.

Similarly, Ex.A29 is copy of forwarded e-mail dated 20.08.2017. The said e-mail was

received by the 1st defendant from APMSIDC and the same was forwarded by the 1st

defendant to the plaintiff. It was also dated 20.08.2017 prior to the suit transaction.

Similarly, Ex.A30 is e-mail dated 20.08.2017 with attachment. The attachment

disclosed that it was addressed by the plaintiff to the APMSIDC mentioning the 05

purchase orders and signed by the Proprietor of the plaintiff. This e-mail was not

between the plaintiff and defendants.

7.16) The learned counsel for plaintiff further confronted a copy of non

conviction certificate in favour of the 1st defendant dated 01.06.2017, according to

which, the 1st defendant was having licence, and it was not convicted for the last 3

years. However, the said certificate was issued on 01.06.2017 for the purpose of

participating in tenders by the State Government Departments, and it was not in

C.O.S.No.3/2020 17/25

connection with any transaction between the plaintiff and defendants. Similarly,

Ex.A32 certificate was also issued certifying the 1st defendant that it was following

good manufacturing practices. Even it was not between the plaintiff and defendants.

As admitted by DW1-Vintha Vinod Reddy, he sent Ex.A33 e-mail with 03

attachments including Exs.31 and 32 which were not relating to the transactions

between the plaintiff and defendants. In other words, the plaintiff never pleaded or

gave evidence about the relevancy of those documents. Though the learned counsel

for plaintiff confronted certain invoices to DW1-Vintha Vinod Reddy and got an

admission that they belonged to the defendants, DW1-Vintha Vinod Reddy deposed

that they were not related to the suit products. There was no suggestion to DW1-

Vintha Vinod Reddy that those were relating to the suit products.

7.17) The learned counsel for plaintiff further confronted Ex.A34 e-mail dated

24.09.2017 with an attachment. According to the evidence of DW1-Vintha Vinod

Reddy, the plaintiff asked him to prepare a statement; he prepared a statement and

sent to the plaintiff. The attachment does not disclose any transaction between the

plaintiff and defendants. DW1-Vintha Vinod Reddy also admitted that he sent an e-

mail dated 03.10.2017 with attachment marked as Ex.A35, according to which, a

statement in the form of attachment was prepared by DW1-Vintha Vinod Reddy and

sent to the plaintiff. DW1-Vintha Vinod Reddy was not questioned about the details

of the statement and figures therein. DW1-Vintha Vinod Reddy also admitted that he

forwarded an e-mail dated 25.10.2017 marked as Ex.A36 received from Mehata

Medicare Private Limited with proforma invoice. This was also only a proforma which

did not disclose any transaction between the plaintiff and the defendants. Similarly,

DW1-Vintha Vinod Reddy sent an e-mail dated 03.10.2017 marked as Ex.A37 with

two attachments, according to those attachments Mehata Medicare Private Limited

issued proforma invoice in the name of the plaintiff. In other words, the transaction

was between the plaintiff and the said Mehata Medicare Private Limited. It may not

be an out of place to mention that the name of the 1st defendant was mentioned as

authorized signatory below the firm name of the plaintiff in one of the attachments

marked as Ex.A37. The plaintiff did not give satisfactory suggestion during the cross-

examination of DW1-Vintha Vinod Reddy. But, DW1-Vintha Vinod Reddy

categorically deposed that he did not purchase any raw materials from the plaintiff

after getting purchase orders by the plaintiff.

7.18) The learned counsel for plaintiff also suggested that the plaintiff paid the

1st defendant’s income tax of Rs.1,23,460/-, and according to the date of challan, it

was paid on 07.11.2017 after the date of placement of orders by APMSIDC. But,

DW1-Vintha Vinod Reddy categorically denied a suggestion immediately after

C.O.S.No.3/2020 18/25

marking Ex.A38 that he received raw materials from the plaintiff and sold the same to

the third parties whose names were mentioned in sales tax returns. The plaintiff

never pleaded that the 1st defendant sold the raw materials to the third parties.

7.19) So, if the oral and documentary evidence on record is scrutinized, the

admissions of DW1-Vintha Vinod Reddy proved that he had certain money

transactions in the year 2017 for a sum of Rs.39,32,880/- and he also received raw

materials under 03 invoices bearing Nos.685, 707 and 818 dated 14.07.2017,

22.07.2017 and 09.08.2017 respectively. But, for the reasons best known to PW1-

K.V.K.Mohana Rao, he categorically deposed that there were no monitory

transactions between him and the 2nd defendant for the last 10 years. This admission

of PW1-K.V.K.Mohana Rao washed away even the admitted liability of the 2nd

defendant in his cross-examination with respect to monetary transactions. Hence, I

can safely come to conclusion that the plaintiff failed to prove the business

relationship with the 1st defendant-firm in respect of the suit transactions especially by

virtue of the alleged mutual understanding after placement of the orders of APMSIDC

towards supply of medicines mentioned in the plaint, except to the extent of admitted

documents in the statement of admissions and denials of documents referred supra.

Hence, this issue is answered accordingly in favour of the defendants and against

the plaintiff.

8) Issue No.2: As I earlier mentioned while answering Issue No.1, DW1-

Vintha Vinod Reddy during his cross-examination admitted 03 invoices bearing

Nos.685, 707 and 818 dated 14.07.2017, 22.07.2017 and 09.08.2017 respectively.

He also admitted that he issued vouchers for Rs.6,00,000/- on 06.07.2017, for

Rs.14,00,000/- on 10.07.2017, for Rs.5,00,000/- on 26.07.2017 and for Rs.5,00,000/-

on 31.07.2017. So far as the other invoices and vouchers are concerned, as I earlier

mentioned in Issue No.1, none of the invoices contained the signature of any of the

defendants acknowledging the receipts of the goods. The learned counsel for plaintiff

argued that since the invoices were raised on the computer, the signatures of the

defendants were not found. As it could be seen from Ex.A1 invoices, the computer

was used for generating Ex.A1 invoices and admittedly Ex.A1 invoices were

electronic records, but after getting the printouts (computer out puts), the proprietor of

the plaintiff signed each invoice. If the goods were dispatched to the 1st defendant,

the authorized person of the 1st defendant could have signed Ex.A1 invoices

acknowledging the receipt of the goods. But, the learned counsel for plaintiff argued

that the defendant admitted the invoices during the cross-examination and in the

statement of admissions and denials of the documents filed by the defendants. As I

earlier mentioned, 03 invoices with particular numbers and dates were admitted by

C.O.S.No.3/2020 19/25

DW1-Vintha Vinod Reddy during his cross-examination. Apart from the 03 invoices,

the defendant also admitted bill No.1363, dated 14.11.2017; bill No.1391, dated

17.11.2017; bill No.1397, dated 20.11.2017; bill No.1414, dated 22.11.2017; bill

No.1415, dated 22.11.2017; bill No.1417, dated 22.11.2017; bill No.1468, dated

30.11.2017 in the statement of admissions and denials of documents. The other 03

bills which were shown as admitted in the statement of admissions and denials of

documents were also admitted during the cross-examination of DW1-Vintha Vinod

Reddy. So, irrespective of the nature of the bill/tax invoice or irrespective of

signature of the authorized person of the 1st defendant, since the said documents 10

in number were admitted in the statement of admissions and denials of documents, I

can safely come to conclusion that those are true, valid and binding on the

defendants.

8.1) Coming to the cash vouchers marked as Ex.A13, the contention of the

defendants was that it contained the signature of the 2nd defendant, but the firm seal

was fabricated. As it could be seen from the vouchers, as I earlier mentioned while

answering Issue No.1, the vouchers were in the names of Krishna Mohan, S.K.P.,

K.Krishna Mohan and Sri Krishna Pharma signed by the 2nd defendant/DW1-Vintha

Vinod Reddy with the seal of the 1st defendant-firm. But, the 2nd defendant denied

the seal and admitted the signature on the vouchers. But, the vouchers were issued

in the name of the person/s or firm referred supra. The plaintiff is Sri Krishna

Pharmaceuticals and represented by K.V.K.Mohana Rao. The plaintiff nowhere

pleaded anything about the name of Krishna Mohan, or S.K.P., or K.Krishna Mohan,

or Sri Krishna Pharma. But, as I earlier mentioned, DW1-Vintha Vinod Reddy during

the cross-examination admitted that he issued 05 vouchers. He was not questioned

in respect of the person or the firm in whose favour the vouchers were issued in spite

of the specific admission that he received cash of Rs.39,32,880/- in the year 2017

and issued the vouchers. In other words, he was never asked that the vouchers

were issued either in the name of the plaintiff or in the name of the proprietor of the

plaintiff. Moreover, PW1-K.V.K.Mohana Rao categorically admitted that there were

no monitory transactions between him and the 2nd defendant for the last 10 years. In

view of the said admission, I cannot come to conclusion that the vouchers are

binding on the defendants, but I can come to conclusion that the 05 vouchers

admitted by DW1-Vintha Vinod Reddy are true and valid. This issue is answered

accordingly.

9) Issue No.3: The contention of the plaintiff is that the defendant issued

cheques in respect of suit transactions. In order to prove the said fact, PW1 produced

Ex.A19 Notary attested copies of cheques with cheque return memos along with

C.O.S.No.3/2020 20/25

declarations of the plaintiff. The defendants admitted the signature in the cheque,

but set up a case that the defendants signed on the blank cheque and as such,

denied the contents of the cheques. As it could be seen from Ex.A19 cheques with

cheque return memos, those were the Photostat copies of the cheques attested by

Notary. But, the plaintiff attached the declaration referred supra as if those were

electronic records by keeping invoice number and date as blanks. So, I cannot come

to a conclusion whether Ex.A19 was electronic record or the Photostat copies

attested by the Notary. However, as originals were not filed and in view of ambiguity

as to the Photostat copies or the electronic records, I cannot come to conclusion that

the cheques were issued in favour of the plaintiff in respect of suit transactions

especially when the plaintiff failed to prove the total suit transaction except the

transactions admitted by the defendants. This issue is answered accordingly.

10) Issue No.4: The defendants contended that the 4th defendant is not

partner of the 1st defendant-firm. In order to prove the same, the defendants filed

Ex.B1 copy of Incorporation Certificate. As it could be seen from Ex.B1, it was

issued as acknowledgment of registration of firm by the Registrar of Firms.

According to it, the defendants 2 & 3 were the partners and the 4 th defendant was not

partner. However, Exs.B2 and B3 were filed in respect of immovable property

standing in the name of the 2nd defendant and his wife, and also in the name of the 4th

defendant, and they are not relating to the partnership concern. On the other hand,

the plaintiff did not file any document to prove that the 4 th defendant is also a partner

of the 1st defendant-firm. Hence, this Court can safely come to conclusion that the

defendants 2 & 3 are only the partners of the 1st defendant-firm and the 4th defendant

is not the partner of the 1st defendant-firm. This issue is answered accordingly in

favour of the defendants and against the plaintiff.

11) Issue No.5: In view of my findings in Issue Nos.1 & 2, I came to

conclusion that the plaintiff had no business transactions with the defendants after

the orders placed by APMSIDC. It was an admitted fact by the plaintiff and the

defendants that there were previous business transactions between the plaintiff and

defendants and those were also proved during the cross-examinations of the

respective witnesses and also not-proved statement of account filed by the plaintiff

relating to the defendants marked as Ex.A14. Once the plaintiff set up a cause of

action that the plaintiff entered into mutual understanding with the defendants after

the purchase orders placed by APMSIDC, the transactions between the plaintiff and

defendants shall be from the date of the said mutual understanding. The date of

mutual understanding was not pleaded by the plaintiff. But the date of first purchase

order was mentioned by the plaintiff as 18.09.2017. So, the transactions between

C.O.S.No.3/2020 21/25

the plaintiff and defendant should have started after 18.09.2017 and the plaintiff can

make a claim relating to those transactions only especially when there was no

pleading in respect of the previous transactions. As I earlier mentioned, DW1-Vintha

Vinod Reddy admitted 03 previous transactions vide invoice Nos. 685, 707 and 818

dated 14.07.2017, 22.07.2017 and 09.08.2017 respectively, for which, the plaintiff

shall not be entitled for recovery of any amount as it was beyond the pleadings. But,

the defendants denied the rest of the transactions after placement of orders by

APMSIDC in the written statement and in the evidence of DW1-Vintha Vinod Reddy.

But, as argued by the learned Counsel for the plaintiff, the defendants admitted

certain vouchers issued by the plaintiff after placement of orders by APMSIDC while

filing the statement of admissions and denials of documents as required under Order

XI Rule 4 of the Code of Civil Procedure, 1908 as amended by the Commercial

Courts Act, 2015. As the defendants admitted 07 bills/invoices raised in the month of

November, 2017 after placement of orders by APMSIDC, they were liable to pay the

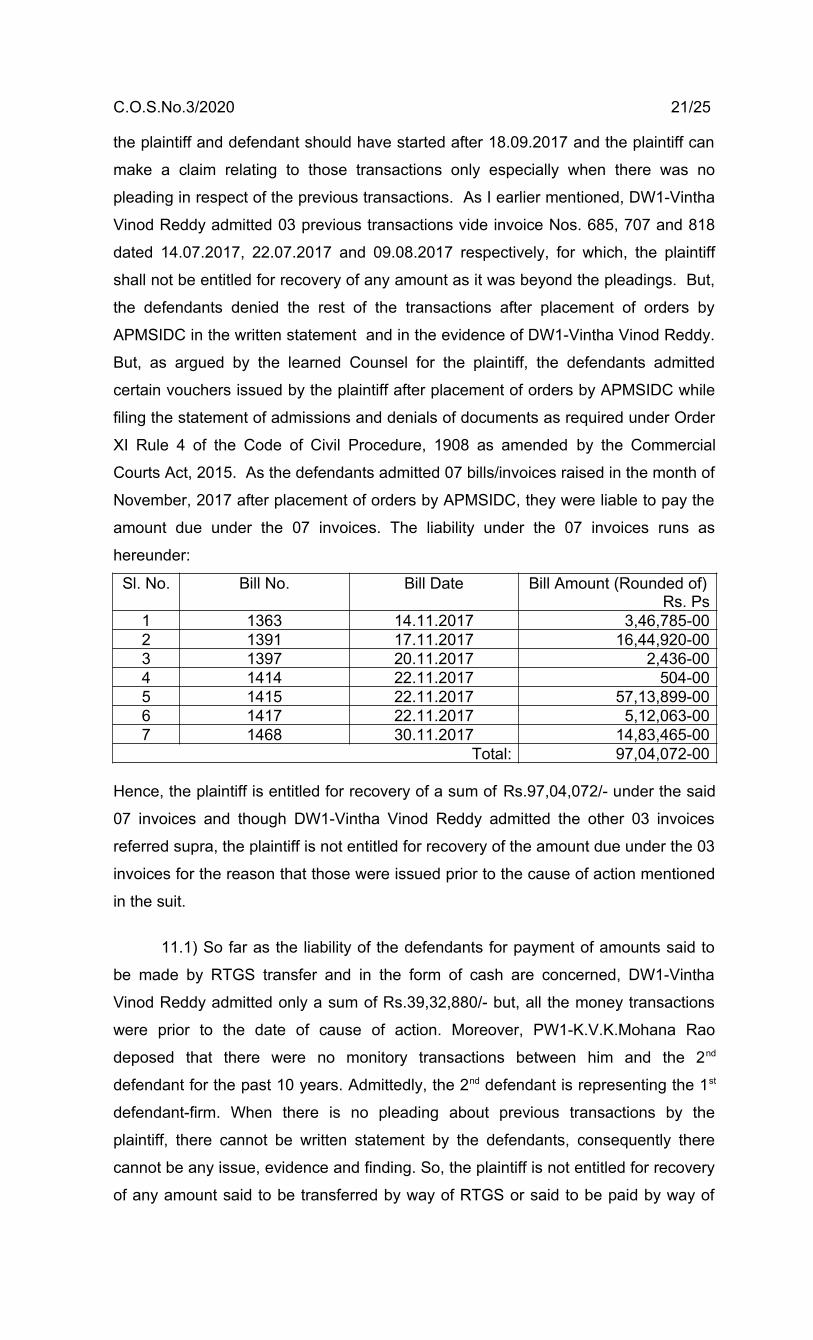

amount due under the 07 invoices. The liability under the 07 invoices runs as

hereunder:

Sl. No. Bill No. Bill Date Bill Amount (Rounded of)Rs. Ps

1 1363 14.11.2017 3,46,785-002 1391 17.11.2017 16,44,920-003 1397 20.11.2017 2,436-004 1414 22.11.2017 504-005 1415 22.11.2017 57,13,899-006 1417 22.11.2017 5,12,063-007 1468 30.11.2017 14,83,465-00

Total: 97,04,072-00

Hence, the plaintiff is entitled for recovery of a sum of Rs.97,04,072/- under the said

07 invoices and though DW1-Vintha Vinod Reddy admitted the other 03 invoices

referred supra, the plaintiff is not entitled for recovery of the amount due under the 03

invoices for the reason that those were issued prior to the cause of action mentioned

in the suit.

11.1) So far as the liability of the defendants for payment of amounts said to

be made by RTGS transfer and in the form of cash are concerned, DW1-Vintha

Vinod Reddy admitted only a sum of Rs.39,32,880/- but, all the money transactions

were prior to the date of cause of action. Moreover, PW1-K.V.K.Mohana Rao

deposed that there were no monitory transactions between him and the 2nd

defendant for the past 10 years. Admittedly, the 2nd defendant is representing the 1st

defendant-firm. When there is no pleading about previous transactions by the

plaintiff, there cannot be written statement by the defendants, consequently there

cannot be any issue, evidence and finding. So, the plaintiff is not entitled for recovery

of any amount said to be transferred by way of RTGS or said to be paid by way of

C.O.S.No.3/2020 22/25

cash. But, as I earlier mentioned, DW1-Vintha Vinod Reddy admitted in the cross-

examination that the plaintiff paid income tax of the 1st defendant of Rs.1,23,460/-.

The said payment was made on 07.11.2017 after the cause of action arose. So, the

plaintiff is entitled for recovery of the said amount of Rs.1,23,460/- apart from the

amounts of Rs.97,04,072/- covered under the 07 bills/invoices.

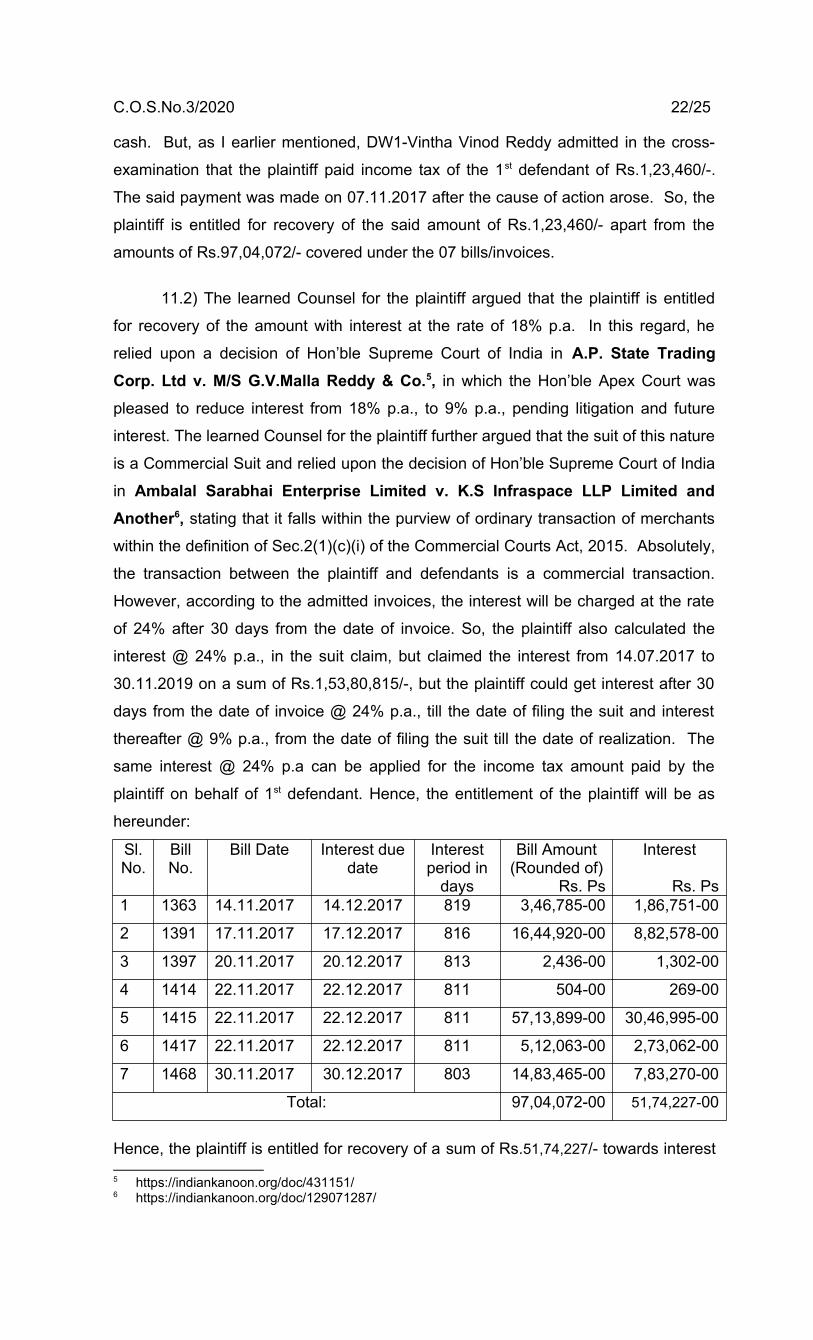

11.2) The learned Counsel for the plaintiff argued that the plaintiff is entitled

for recovery of the amount with interest at the rate of 18% p.a. In this regard, he

relied upon a decision of Hon’ble Supreme Court of India in A.P. State TradingCorp. Ltd v. M/S G.V.Malla Reddy & Co.5, in which the Hon’ble Apex Court was

pleased to reduce interest from 18% p.a., to 9% p.a., pending litigation and future

interest. The learned Counsel for the plaintiff further argued that the suit of this nature

is a Commercial Suit and relied upon the decision of Hon’ble Supreme Court of India

in Ambalal Sarabhai Enterprise Limited v. K.S Infraspace LLP Limited andAnother6, stating that it falls within the purview of ordinary transaction of merchants

within the definition of Sec.2(1)(c)(i) of the Commercial Courts Act, 2015. Absolutely,

the transaction between the plaintiff and defendants is a commercial transaction.

However, according to the admitted invoices, the interest will be charged at the rate

of 24% after 30 days from the date of invoice. So, the plaintiff also calculated the

interest @ 24% p.a., in the suit claim, but claimed the interest from 14.07.2017 to

30.11.2019 on a sum of Rs.1,53,80,815/-, but the plaintiff could get interest after 30

days from the date of invoice @ 24% p.a., till the date of filing the suit and interest

thereafter @ 9% p.a., from the date of filing the suit till the date of realization. The

same interest @ 24% p.a can be applied for the income tax amount paid by the

plaintiff on behalf of 1st defendant. Hence, the entitlement of the plaintiff will be as

hereunder:

Sl.No.

BillNo.

Bill Date Interest duedate

Interestperiod in

days

Bill Amount(Rounded of)

Rs. Ps

Interest

Rs. Ps 1 1363 14.11.2017 14.12.2017 819 3,46,785-00 1,86,751-00

2 1391 17.11.2017 17.12.2017 816 16,44,920-00 8,82,578-00

3 1397 20.11.2017 20.12.2017 813 2,436-00 1,302-00

4 1414 22.11.2017 22.12.2017 811 504-00 269-00

5 1415 22.11.2017 22.12.2017 811 57,13,899-00 30,46,995-00

6 1417 22.11.2017 22.12.2017 811 5,12,063-00 2,73,062-00

7 1468 30.11.2017 30.12.2017 803 14,83,465-00 7,83,270-00

Total: 97,04,072-00 51,74,227-00

Hence, the plaintiff is entitled for recovery of a sum of Rs.51,74,227/- towards interest

5 https://indiankanoon.org/doc/431151/6 https://indiankanoon.org/doc/129071287/

C.O.S.No.3/2020 23/25

from the date of eligibility of bills till the date of filing of the suit on 31.01.2020 @ 24%

p.a., and interest thereafter @ 9% p.a., till the date of realization. The plaintiff is also

entitled for interest of Rs.69,489/- on the amount of Rs.1,23,460/- paid towards

income tax of the defendants from 07.11.2017 till the date of filing the suit on

31.01.2020 and interest thereafter @ 9% p.a., till the date of realization, with

proportionate costs. This issue is answered accordingly.

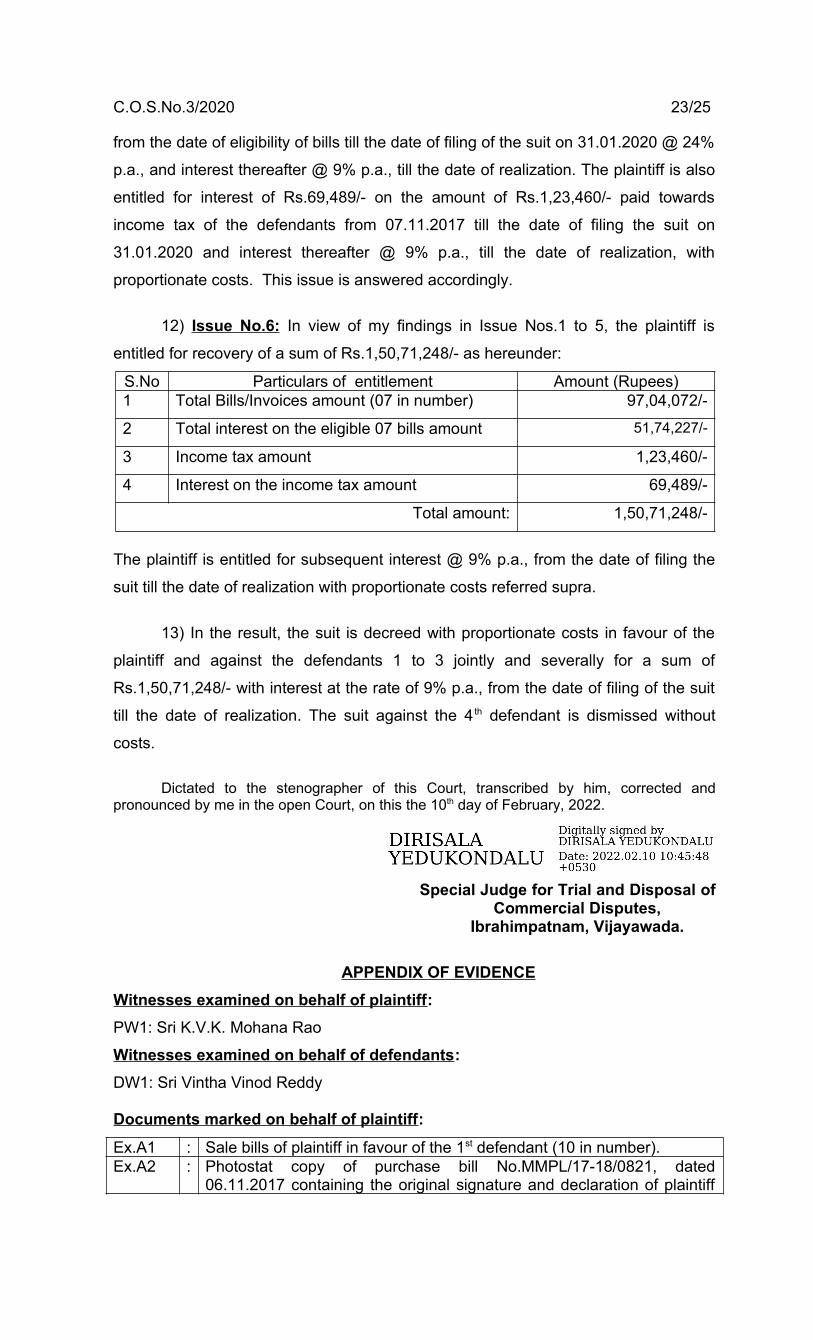

12) Issue No.6: In view of my findings in Issue Nos.1 to 5, the plaintiff is

entitled for recovery of a sum of Rs.1,50,71,248/- as hereunder:

S.No Particulars of entitlement Amount (Rupees)1 Total Bills/Invoices amount (07 in number) 97,04,072/-

2 Total interest on the eligible 07 bills amount 51,74,227/-

3 Income tax amount 1,23,460/-

4 Interest on the income tax amount 69,489/-

Total amount: 1,50,71,248/-

The plaintiff is entitled for subsequent interest @ 9% p.a., from the date of filing the

suit till the date of realization with proportionate costs referred supra.

13) In the result, the suit is decreed with proportionate costs in favour of the

plaintiff and against the defendants 1 to 3 jointly and severally for a sum of

Rs.1,50,71,248/- with interest at the rate of 9% p.a., from the date of filing of the suit

till the date of realization. The suit against the 4 th defendant is dismissed without

costs.

Dictated to the stenographer of this Court, transcribed by him, corrected andpronounced by me in the open Court, on this the 10th day of February, 2022.

Special Judge for Trial and Disposal of Commercial Disputes,

Ibrahimpatnam, Vijayawada.

APPENDIX OF EVIDENCEWitnesses examined on behalf of plaintiff:PW1: Sri K.V.K. Mohana Rao

Witnesses examined on behalf of defendants:DW1: Sri Vintha Vinod Reddy

Documents marked on behalf of plaintiff:Ex.A1 : Sale bills of plaintiff in favour of the 1st defendant (10 in number).Ex.A2 : Photostat copy of purchase bill No.MMPL/17-18/0821, dated

06.11.2017 containing the original signature and declaration of plaintiff

C.O.S.No.3/2020 24/25

(Marked subject to admissibility).Ex.A3 : Photostat copy of purchase bill No.2201, dated 14.11.2017 containing

the original signature and declaration of plaintiff (Marked subject toadmissibility).

Ex.A4 : Computer generated statement of account relating to Mehata MedicarePrivate Ltd., with declaration of plaintiff.

Ex.A5 : Computer generated statement of account relating to Shubam PharmaPrivate Ltd., with declaration of plaintiff.

Ex.A6 : Computer generated statement of account relating to Sri VenkateswaraCoil Mill Private Ltd., with declaration of plaintiff.

Ex.A7 : Computer generated statement of account relating to Feno Plast Ltd..,with declaration of plaintiff.

Ex.A8 : Computer generated statements of account relating to City Union Bank,Special Loan Account with declaration of plaintiff (Two statements).

Ex.A9 : Printout of electronic record of Encumbrance certificate with declarationof plaintiff (Marked subject to admissibility and provisions of Sec.65B ofIndian Evidence Act, 1872).

Ex.A10 : Copies of 5 orders of APMISIDC in 14 pages with URL address at thetop of each page containing the signatures and declaration of plaintiff(Marked subject to admissibility and provisions of Sec.65B of IndianEvidence Act, 1872).

Ex.A11 : Photostat copy of Income Tax Returns of plaintiff with the stamp andsignature of plaintiff for the assessment year 2019-20 with declaration ofplaintiff (Marked subject to admissibility).

Ex.A12 : Photostat copy of Income Tax Returns of plaintiff with the stamp ofplaintiff (without signature) for the assessment year 2018-19 withdeclaration of plaintiff (Marked subject to admissibility).

Ex.A13 : Original cash voucher 17 in number with declaration of plaintiff (Markedafter collecting stamp duty and penalty).

Ex.A14 : Computer generated statements of account from 01.04.2017 to31.03.2018 and 01.04.2018 to 31.03.2019 relating to the 1st defendantalong with declarations of plaintiff.

Ex.A15 : Computer generated statements of account in 9 pages issued by CityUnion Bank Ltd., with the declarations of plaintiff (Marked subject toadmissibility and provisions of Sec.65B of Indian Evidence Act, 1872).

Ex.A16 : Computer generated copies of Form GSTR-3B with the declarations ofthe plaintiff (3 pages).

Ex.A17 : Computer generated sanction letter issued by City Union Bank Ltd.,dated 10.11.2017 with the signature and seal of plaintiff along withdeclaration of plaintiff (Marked subject to admissibility and provisions ofSec.65B of Indian Evidence Act, 1872).

Ex.A18 : Computer generated sanction letter issued by City Union Bank Ltd.,dated 21.12.2017 with the signature and seal of plaintiff along withdeclaration of plaintiff (Marked subject to admissibility and provisions ofSec.65B of Indian Evidence Act, 1872).

Ex.A19 : Notary attested copies of cheques with Check return memos along withdeclarations of plaintiff (Marked subject to admissibility).

Ex.A20 : Copy of email dated 04.08.2017.Ex.A21 : Attachment to email dated 04.08.2017.Ex.A22 : Copy of email dated 06.07.2017.Ex.A23 : Copy of attachment dated 05.07.2017.Ex.A24 : Copy of email dated 05.07.2017.Ex.A25 : Copy of email dated 01.07.2017 with two purchase orders dated

27.06.2017 and 28.06.2017.Ex.A26 : Copy of statement.Ex.A27 : Copy of list of firms blacklisted.Ex.A28 : Copy of email dated 03.01.2018 with attachment.

C.O.S.No.3/2020 25/25

Ex.A29 : Copy of forwarded email dated 20.08.2017.Ex.A30 : Copy of email dated 20.08.2017 with attachment.Ex.A31 : Copy of non-conviction certificate in favour of 1st defendant dated

01.06.2017.Ex.A32 : Copy of G.M.P Certificate dated 01.06.2017 in favour of 1st defendant.Ex.A33 : Copy of email dated 12.09.2017 with attachments in four pages.Ex.A34 : Copy of the email dated 24.09.2017 with attachment.Ex.A35 : Copy of the email dated 03.10.2017 with attachment.Ex.A36 : Copy of forwarded email dated 25.10.2017 with proforma invoice.Ex.A37 : Copy of email dated 03.10.2017 with two attachments.Ex.A38 : Copy of email with income tax challan. Documents marked on behalf of defendants:

Ex.B1 : Copy of certificate of incorporation of 1st Defendant-firm obtained throughMee-Seva.

Ex.B2 : Certified copy of registered sale deed dated 26.12.2009 vide documentNo.2832/2009 on the file of S.R.O., Gunadala, Vijayawada standing in thename of 2nd Defendant and his wife viz., Ch.Swathi.

Ex.B3 : Certified copy of registered sale deed dated 30.03.1998 vide documentNo.1441/1998 on the file of S.R.O., Gannavaram standing in the name of4th Defendant.

Special Judge for Trial and Disposal of Commercial Disputes,

Ibrahimpatnam, Vijayawada.