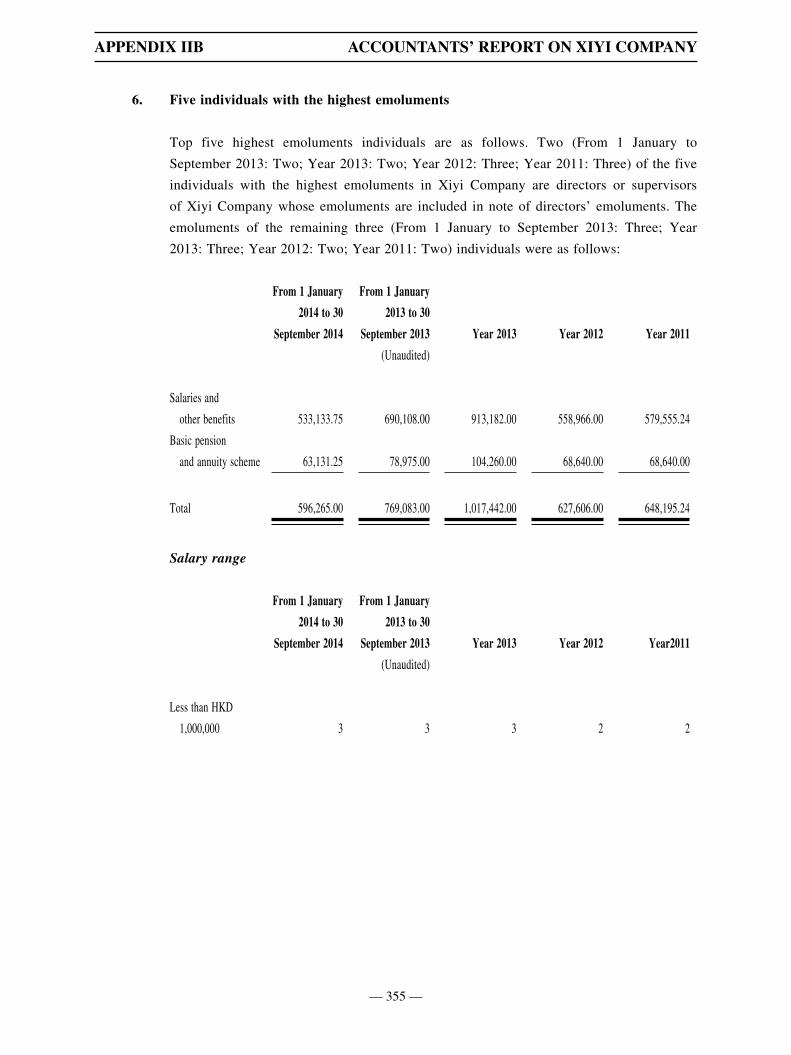

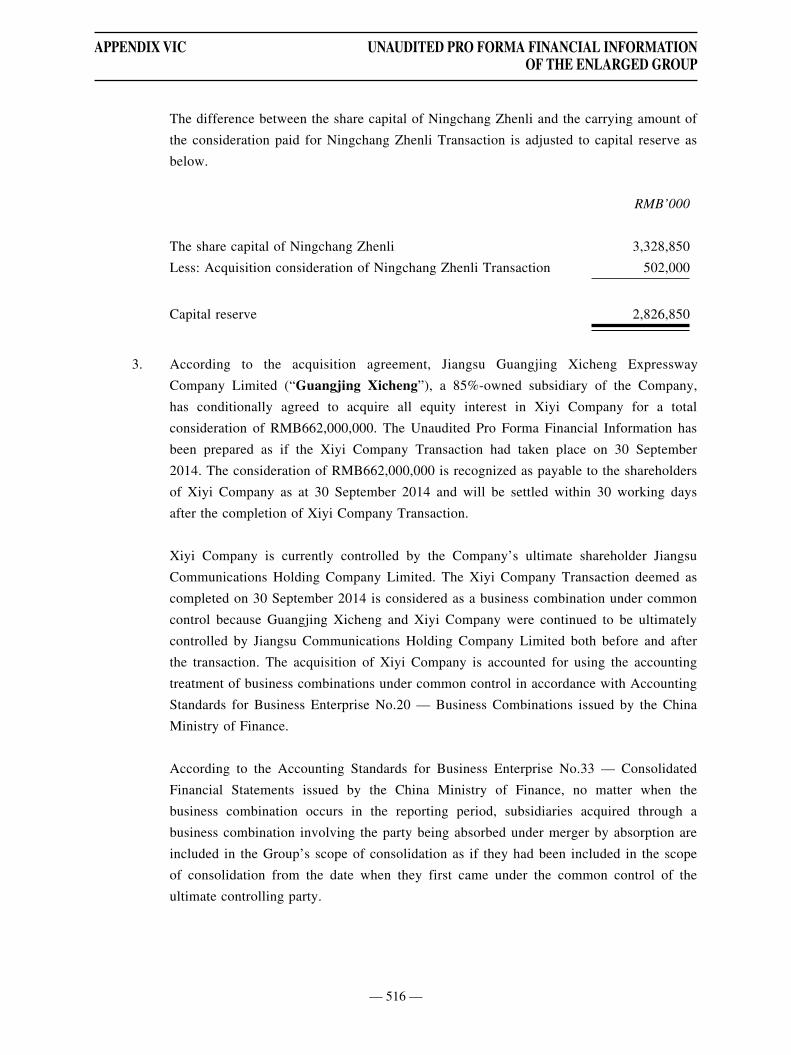

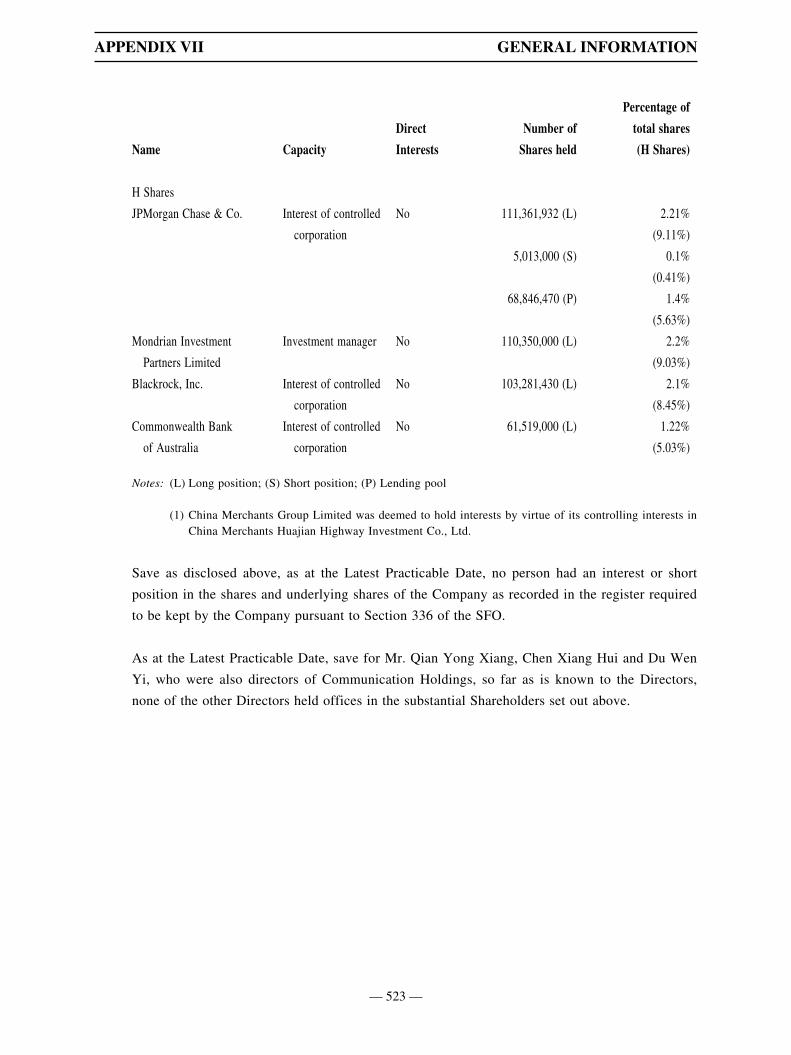

Embed Size (px)

Citation preview

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION

If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult your stockbroker or other registered dealer in securities, bank manager, solicitor, professional accountant or other professional advisers.

If you have sold all your H Shares in Jiangsu Expressway Company Limited, you should at once hand this circular and the accompanying form of proxy and confirmation slip to the purchaser or to the bank, stockbroker or other agent through whom the sale or transfer was effected for transmission to the purchaser.

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this circular, makes no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular.

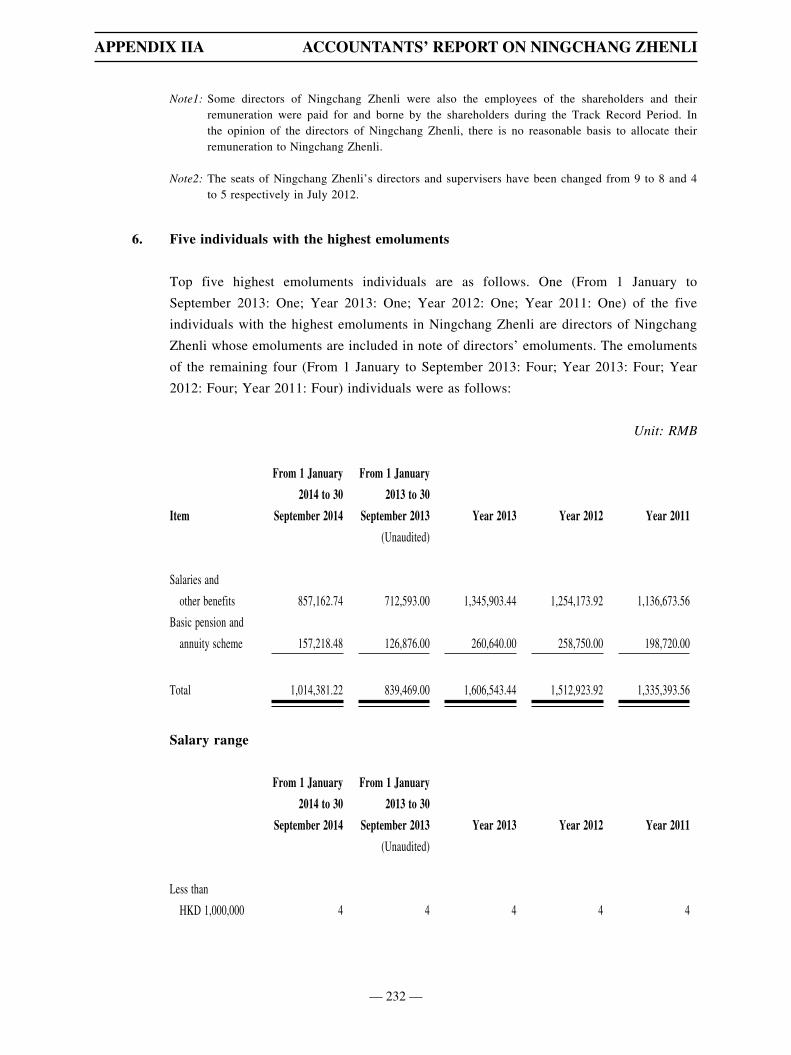

JIANGSU EXPRESSWAY COMPANY LIMITED 江蘇寧滬高速公路股份有限公司

(Incorporated in the People’s Republic of China as a joint-stock limited company) (Stock Code: 00177)

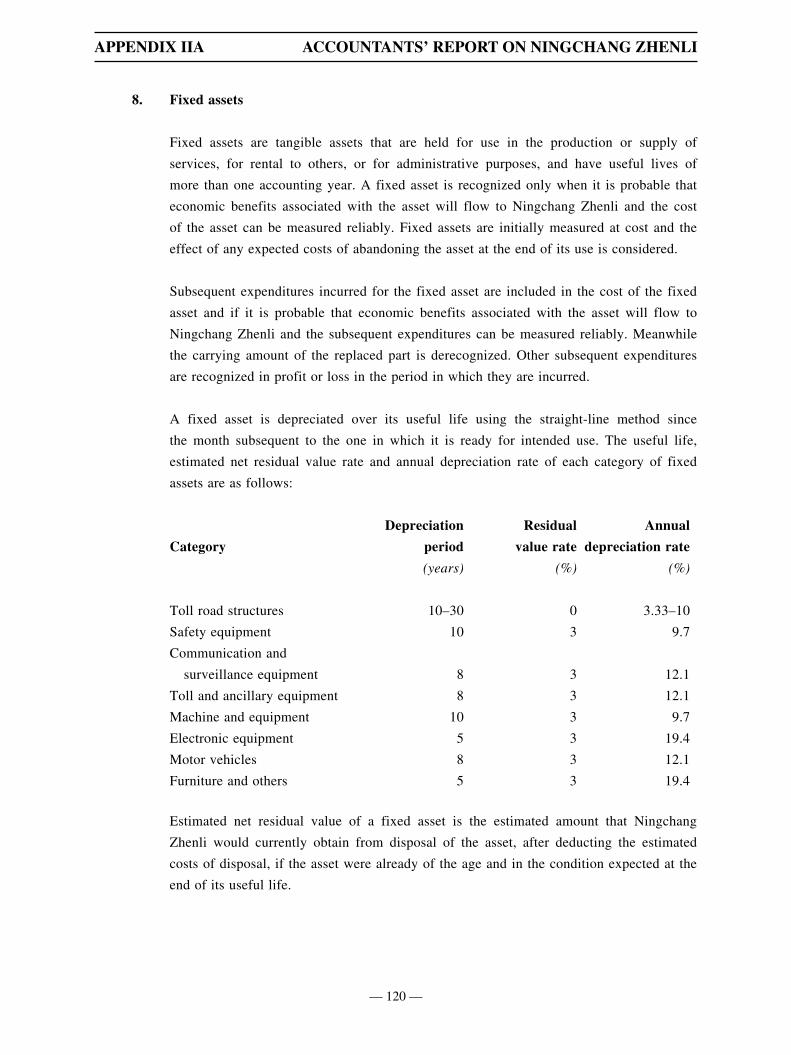

CONNECTED AND MAJOR TRANSACTION

Independent Financial Adviser to the Independent Board Committee

and the Independent Shareholders

Guotai Junan Capital Limited

A letter from the Board is set out on pages 1 to 47 of this circular and a letter from the Independent Board Committee is set out on pages 48 to 49 of this circular. A letter from Guotai Junan, the independent financial adviser to the Independent Board Committee and the Independent Shareholders, containing its advice to the Independent Board Committee and the Independent Shareholders in relation to the terms of the Transactions is set out on pages 50 to 92 of this circular.

A notice convening the 2015 First Extraordinary General Meeting to be held at the Conference Room, 6 Xianlin Avenue, Nanjing, the PRC on Thursday, 12 March 2015 at 2:30 p.m. is set out on page 529 to page 533 of this circular. Whether or not you are able to attend the meeting, you are requested to complete and return the accompanying form of proxy in accordance with the instructions printed thereon to the Company as soon as possible and, in any event, not less than 24 hours before the time appointed for the holding of the meeting. Completion and return of the form of proxy will not preclude you from attending and voting at the meeting should you so wish, in which case you will be deemed to have withdrawn the proxy you have appointed.

23 January 2015

— i —

CONTENT

Page

DEFINITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ii

LETTER FROM THE BOARD

I. Introduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1II. Summary of the connected and major transaction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2III. Information about the Company and parties to the Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8IV. Basic Information about the target companies of the Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . 13V. The general principle and method for determining price in affiliated transaction/ connected and major transaction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24VI. Details of the agreements dated 30 December 2014. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25VII. The purpose of the connected and major transaction and the effect on the Company . . . . . . . . . . . . 33VIII. The approval procedure for the performance of the Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . 41IX. Waiver from strict compliance with the Hong Kong Listing Rules . . . . . . . . . . . . . . . . . . . . . . . . . . 43X. The compensation undertaking letter from the related party . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44XI. Closure of register. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45XII. Extraordinary General Meeting. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46XIII. Recommendation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

LETTER FROM THE INDEPENDENT BOARD COMMITTEE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

LETTER FROM THE INDEPENDENT FINANCIAL ADVISER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

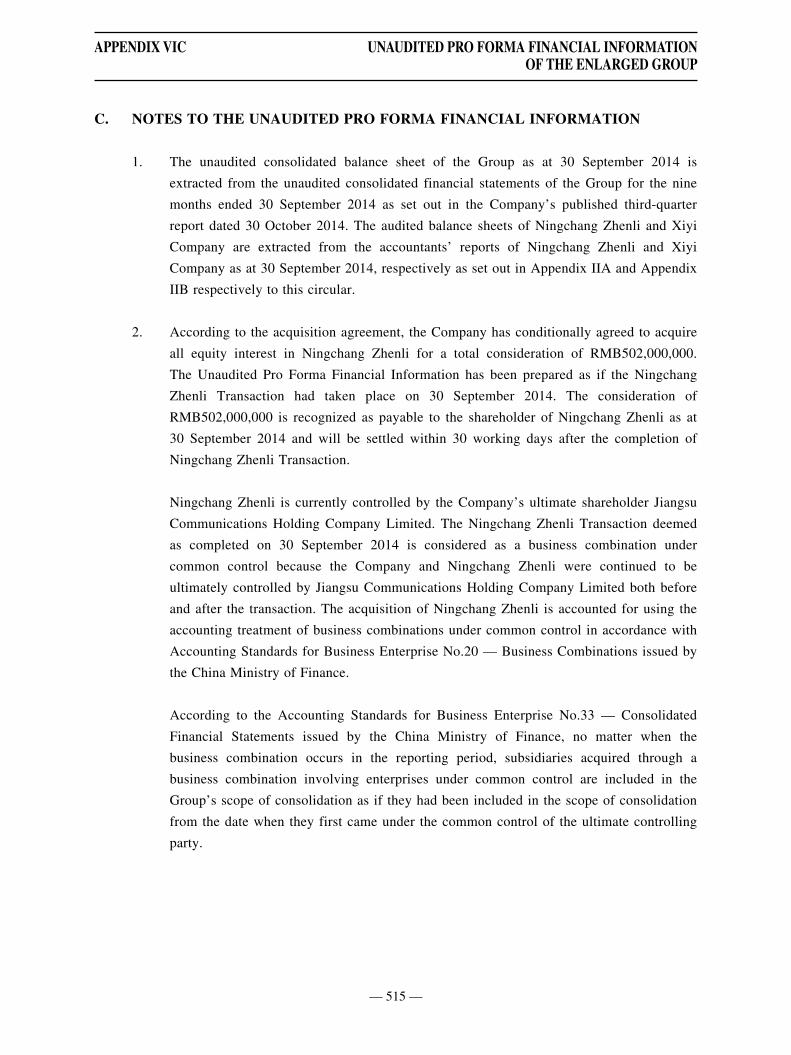

APPENDIX I — FINANCIAL INFORMATION OF THE GROUP. . . . . . . . . . . . . . . . . . . . . . 93

APPENDIX IIA — ACCOUNTANTS’ REPORT ON NINGCHANG ZHENLI . . . . . . . . . . . . . . 96

APPENDIX IIB — ACCOUNTANTS’ REPORT ON XIYI COMPANY . . . . . . . . . . . . . . . . . . . . 243

APPENDIX IIIA — MANAGEMENT DISCUSSION AND ANALYSIS OF NINGCHANG ZHENLI. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 365

APPENDIX IIIB — MANAGEMENT DISCUSSION AND ANALYSIS OF XIYI COMPANY. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 384

APPENDIX IVA — VALUATION REPORT OF NINGCHANG ZHENLI . . . . . . . . . . . . . . . . . . 403

APPENDIX IVB — VALUATION REPORT OF XIYI COMPANY . . . . . . . . . . . . . . . . . . . . . . . . 427

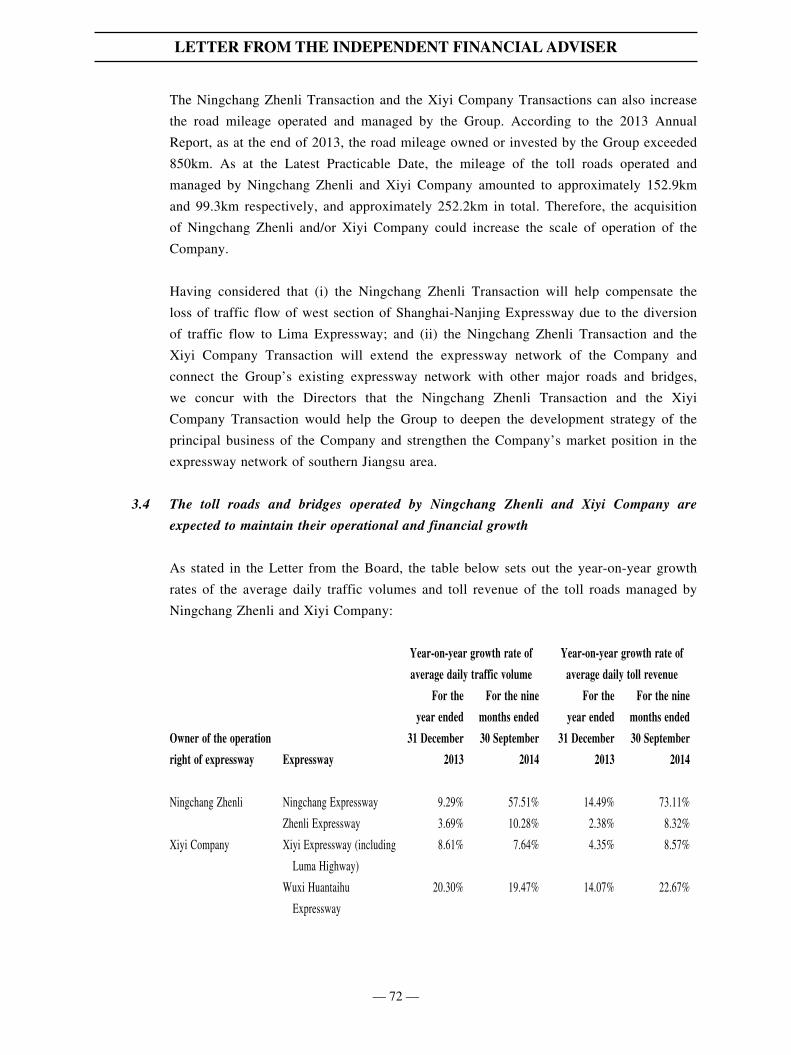

APPENDIX VA — TRAFFIC CONSULTANT’S REPORT IN RESPECT OF NINGCHANG ZHENLI . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 451

APPENDIX VB — TRAFFIC CONSULTANT’S REPORT IN RESPECT OF XIYI COMPANY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 472

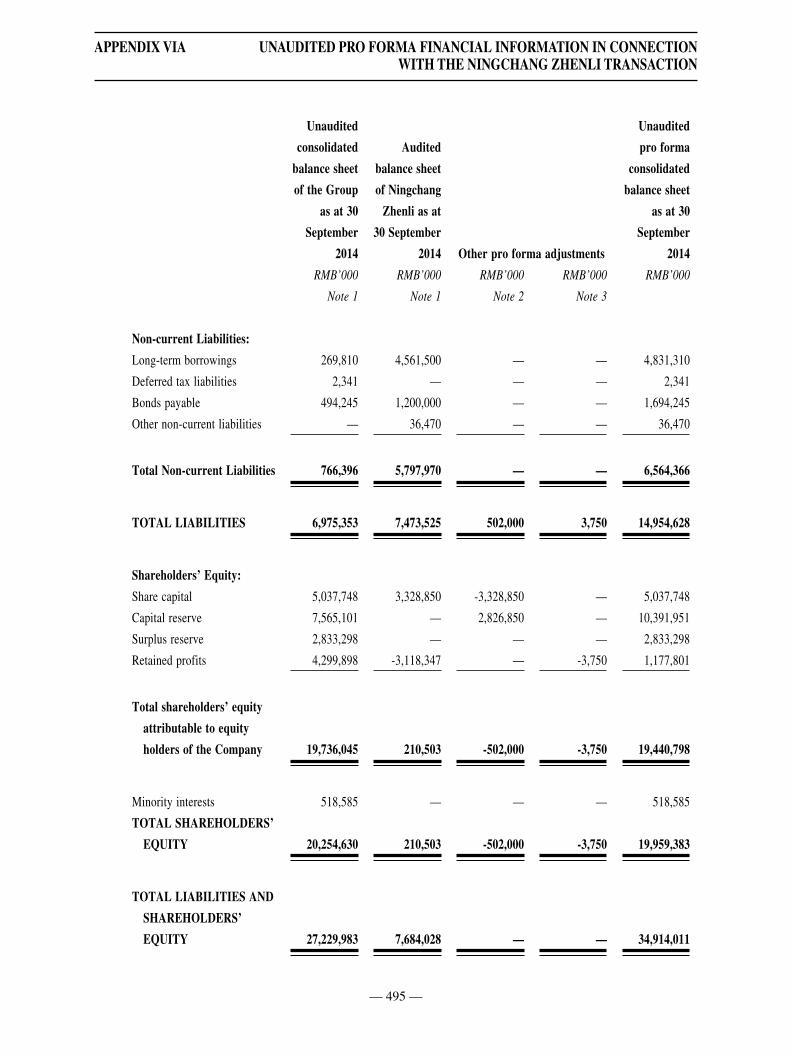

APPENDIX VIA — UNAUDITED PRO FORMA FINANCIAL INFORMATION IN CONNECTION WITH THE NINGCHANG ZHENLI TRANSACTION . . . . . . . . . . . . . . . . . . . . . . . . . . 491

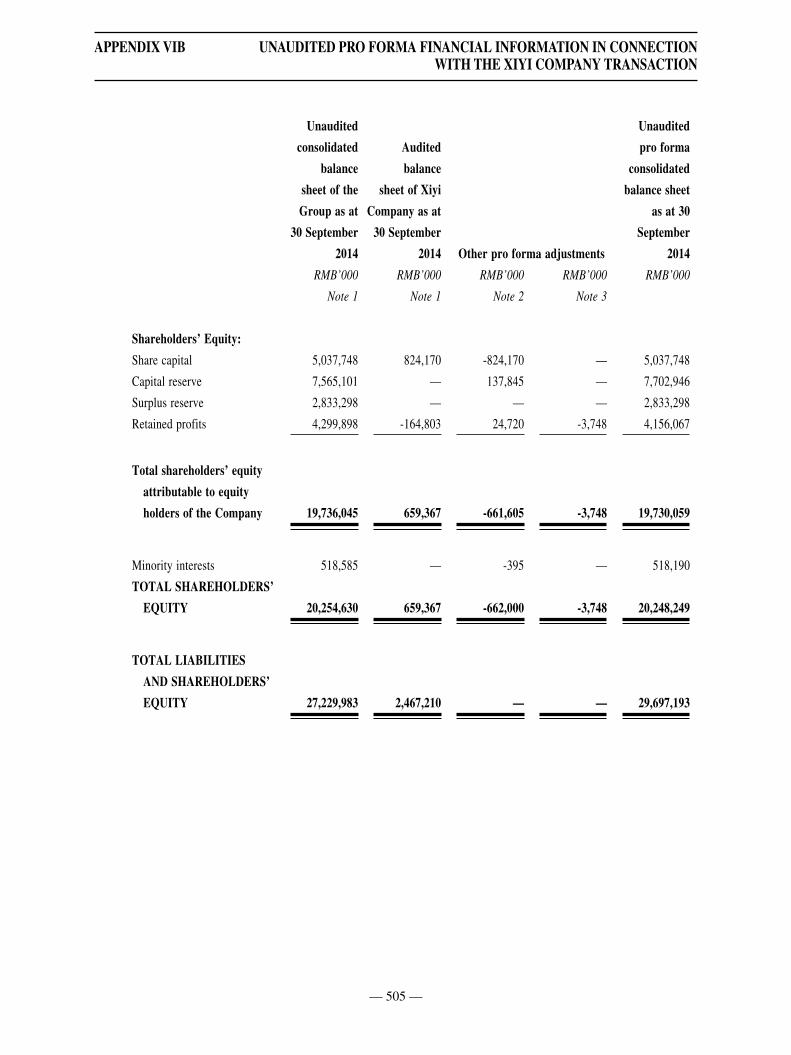

APPENDIX VIB — UNAUDITED PRO FORMA FINANCIAL INFORMATION IN CONNECTION WITH THE XIYI COMPANY TRANSACTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 501

APPENDIX VIC — UNAUDITED PRO FORMA FINANCIAL INFORMATION OF THE ENLARGED GROUP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 511

APPENDIX VII — GENERAL INFORMATION. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 521

NOTICE OF THE EXTRAORDINARY GENERAL MEETING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 529

— ii —

DEFINITIONS

In this circular, the following expressions have the meanings set out below unless the context requires

otherwise:

“Absorption and Merger

Agreement”

: has the same meaning as ascribed to it under the section headed “VI.

Details of the agreements dated 30 December 2014”

“Affiliated Transactions

Guidelines”

: The Guidelines for the Affiliated Transactions of Listed Companies of the

Shanghai Stock Exchange (《上海證券交易所上市公司關聯交易實施指引》)

“American Appraisal” : American Appraisal China Limited

“Announcement” : the announcement of the Company dated 31 December 2014 in respect of

the Transactions

“associates” : has the same meaning as defined in the Hong Kong Listing Rules

“Board” : the board of Directors

“Changzhou

Expressway”

: 常州高速公路投資發展有限公司 (Changzhou Expressway Investment

Development Company Limited*), a limited liability company established

in the PRC and an existing shareholder of Xiyi Company

“Communications

Holdings”

: 江蘇交通控股有限公司 (Jiangsu Communications Holdings Company

Limited*), a limited liability company established in the PRC and an

existing shareholder of Ningchang Zhenli and Xiyi Company

“Company” : 江蘇寧滬高速公路股份有限公司 (Jiangsu Expressway Company

Limited), a joint stock limited company established in the PRC with

limited liability and whose shares are listed on the Hong Kong Stock

Exchange (Stock Code of H Shares: 00177) and the Shanghai Stock

Exchange (Stock Code: 600377) and traded in the form of American

Depository Receipts on the OTC Markets Group Inc. in the United States

(Ticker: JEXYY)

“connected person” : has the same meaning as defined in the Hong Kong Listing Rules

“Debt Transfer

Agreement”

: has the same meaning as ascribed to it under the section headed “VI.

Details of the agreements dated 30 December 2014”

— iii —

DEFINITIONS

“Directors” : the directors of the Company

“Enlarged Group” : the Group as enlarged after the completion of the Transactions

“Enlarged Group

(inclusive of

Ningchang Zhenli)”

: the Group as enlarged after the completion of the transaction as referred

to under the section headed “II. Summary of the connected and major

transaction — (1) Main contents of the Transactions” of this circular

in respect of the Company’s acquisition of the entire equity interest in

Ningchang Zhenli from Communications Holdings and the transfer of all

the debts of Ningchang Zhenli to the Company and the capitalization of

such debts into equity in accordance with the applicable laws

“Enlarged Group

(inclusive of Xiyi

Company)”

: the Group as enlarged after the completion of the transaction as referred

to under the section headed “II. Summary of the connected and major

transaction — (1) Main contents of the Transactions” of this circular

in respect of Guangjing Xicheng’s acquisition and merger of Xiyi

Company from Communications Holdings, Changzhou Expressway, Wuxi

Expressway and Xiyi Company

“Extraordinary General

Meeting”

: the extraordinary general meeting of the Company to be held on 12

March 2015 to consider and, if thought fit, to approve, inter alia, the

Transactions

“Group” : the Company and its subsidiaries

“Guangjing Xicheng” : 江蘇廣靖錫澄高速公路有限責任公司 (Jiangsu Guangjing Xicheng

Expressway Company Limited*), a limited liability company established

in the PRC and a 85%-owned subsidiary of the Company

“Guotai Junan”,

“Independent

Financial Adviser”

: Guotai Junan Capital Limited, a licensed corporation authorised to

conduct Type 6 (advising on corporate finance) regulated activities

under SFO, the independent financial adviser to the Independent Board

Committee and the Independent Shareholders in relation to the terms of

the Transactions and the transactions contemplated thereunder

“H Shares” : overseas-listed foreign shares of RMB1.00 each, which are issued by the

Company in Hong Kong, subscribed in Hong Kong dollars and listed on

the Hong Kong Stock Exchange

— iv —

DEFINITIONS

“HKD” : Hong Kong Dollars, the lawful currency of Hong Kong

“Hong Kong” : the Hong Kong Special Administrative Region of the PRC

“Hong Kong Listing

Rules”

: The Rules Governing the Listing of Securities on The Stock Exchange of

Hong Kong Limited

“Hong Kong Stock

Exchange”

: The Stock Exchange of Hong Kong Limited

“Independent Board

Committee”

: the independent committee of the board of Directors comprising Mr.

Zhang Erzhen, Mr. Xu Chang Xin, Mr. Gao Bo and Mr. Chen Donghua,

being all the independent non-executive Directors, formed to advise the

Independent Shareholders in respect of the terms of the Transactions

“Independent

Shareholder(s)”

: Shareholders, but excluding Communications Holdings and its associates

“Jiangsu Weixin” : 江蘇緯信工程諮詢有限公司 (Jiangsu Weixin Engineering Consultants

Ltd.*), the traffic consultant

“Latest Practicable

Date”

: 16 January 2015, being the latest practicable date prior to the printing of

this circular for ascertaining certain information contained in this circular,

unless otherwise stated

“Ningchang Zhenli” : 江蘇寧常鎮溧高速公路有限公司 (Jiangsu Ningchang Zhenli

Expressway Company Limited*), a limited liability company established

in the PRC

“Ningchang Zhenli

Equity Transfer

Agreement”

: has the same meaning as ascribed to it under the section headed “VI.

Details of the agreements dated 30 December 2014”

“Ningchang Zhenli

Transaction”

: the transaction as referred to under the section headed “II. Summary

of the connected and major transaction — (1) Main contents of the

Transactions” of this circular in respect of the Company’s acquisition

of the entire equity interest in Ningchang Zhenli from Communications

Holdings and the transfer of all the debts of Ningchang Zhenli to the

Company and the capitalization of such debts into equity in accordance

with the applicable laws

— v —

DEFINITIONS

“Orient Appraisal” : Orient Appraisal Co., Ltd

“PRC” : the People’s Republic of China, which for the purpose of this circular

excludes Hong Kong, the Macao Special Administrative Region of the

PRC and Taiwan

“Profit Compensation

Agreement”

: has the same meaning as ascribed to it under the section headed “VI.

Details of the agreements dated 30 December 2014”

“RMB” : Renminbi, the lawful currency of the PRC

“SFO” : the Securities and Futures Ordinance, Chapter 571 of the Laws of Hong

Kong

“Shanghai Listing

Rules”

: The Rules Governing the Listing of Stocks on Shanghai Stock Exchange

“Shanghai Stock

Exchange”

: The Shanghai Stock Exchange

“Shareholders” : holders of shares of the Company

“Transactions” : the transactions as referred to under the section headed “II. Summary

of the connected and major transaction — (1) Main contents of the

Transactions” of this circular in respect of (1) the Company’s acquisition

of the entire equity interest in Ningchang Zhenli from Communications

Holdings and the transfer of all the debts of Ningchang Zhenli to the

Company; and (2) Guangjing Xicheng’s acquisition and merger of Xiyi

Company from Communications Holdings, Changzhou Expressway, Wuxi

Expressway and Xiyi Company

“Wuxi Expressway” : 無錫高速公路投資有限公司 (Wuxi Expressway Investment Company

Limited*), a limited liability company established in the PRC and an

existing shareholder of Xiyi Company

“Xiyi Company” : 江蘇錫宜高速公路有限公司 (Jiangsu Xiyi Expressway Company

Limited*), a limited liability company established in the PRC

— vi —

DEFINITIONS

“Xiyi Company

Equity Transfer

Agreement(s)”

: has the same meaning as ascribed to it under the section headed “VI.

Details of the agreements dated 30 December 2014”

“Xiyi Company

Transaction”

: the transaction as referred to under the section headed “II. Summary

of the connected and major transaction — (1) Main contents of the

Transactions” of this circular in respect of Guangjing Xicheng’s

acquisition and merger of Xiyi Company from Communications Holdings,

Changzhou Expressway, Wuxi Expressway and Xiyi Company

“%” : percentage

* for identification purpose only

— 1 —

LETTER FROM THE BOARD

JIANGSU EXPRESSWAY COMPANY LIMITED 江蘇寧滬高速公路股份有限公司

(Incorporated in the People’s Republic of China as a joint-stock limited company) (Stock Code: 00177)

Directors: Registered Office:Qian Yong Xiang 6 Xianlin AvenueZhang Yang Qixia DistrictChen Xiang Hui NanjingDu Wen Yi JiangsuCheng Chang Yung Tsung, Alice PRCFang Hung, KennethZhang Erzhen*Xu Chang Xin*Gao Bo*Chen Donghua*

* Independent non-executive Directors

23 January 2015

To the Shareholders of the Company

Dear Sir or Madam,

CONNECTED AND MAJOR TRANSACTION

I. INTRODUCTION

Reference is made to the Announcement dated 31 December 2014, pursuant to which the Board

of the Company announced that on 30 December 2014:

i. the Company and Communications Holdings entered into the Ningchang Zhenli Equity

Transfer Agreement pursuant to which the Company has agreed to acquire the entire

equity interest of Ningchang Zhenli held by Communications Holdings for a consideration

of RMB502,000,000 (equivalent to approximately HKD636,560,000). At the same time,

the Company and Ningchang Zhenli also entered into the Debt Transfer Agreement,

pursuant to which all of Ningchang Zhenli’s interest-bearing borrowings as at the

completion date shall be assigned to the Company (not exceeding RMB7,500,000,000

(equivalent to approximately HKD9,500,000,000)); and

— 2 —

LETTER FROM THE BOARD

ii. Guangjing Xicheng, a 85%-owned subsidiary of the Company, entered into a Xiyi

Company Equity Transfer Agreement with each of Communications Holdings, Changzhou

Expressway and Wuxi Expressway, respectively, pursuant to which Guangjing Xicheng

has agreed to acquire, in aggregate, the entire equity interest of Xiyi Company

for an aggregate consideration of RMB662,000,000 (equivalent to approximately

HKD839,450,000), and, at the same time, Guangjing Xicheng also entered into the

Absorption and Merger Agreement with Xiyi Company to merge with Xiyi Company and

to take over all its assets, liabilities, business and personnel.

The purpose of this circular is to provide, among other thing, the details of the Transactions and

other information in accordance with the Hong Kong Listing Rules. This circular also contains

the notice convening the Extraordinary General Meeting.

II. SUMMARY OF THE CONNECTED AND MAJOR TRANSACTION

(1) Main contents of the Transactions

The Transactions of the Company consist of the following two components:

1. Acquisition of all equity interest and interest-bearing borrowings of Ningchang

Zhenli

On 30 December 2014, the Company and Communications Holdings entered into

the Ningchang Zhenli Equity Transfer Agreement. The Company has agreed to

acquire 100% of the equity interest in Ningchang Zhenli held by Communications

Holdings for a consideration of RMB502,000,000 (equivalent to approximately

HKD636,560,000). At the same time, the Company and Ningchang Zhenli entered

into the Debt Transfer Agreement, pursuant to which all of Ningchang Zhenli’s

interest-bearing borrowings as at the completion date shall be assigned to the

Company (not exceeding RMB7,500,000,000). Following the assignment of such

interest-bearing borrowings of Ningchang Zhenli to the Company, the Company

shall capitalise such debts into equity in accordance with the applicable laws.

— 3 —

LETTER FROM THE BOARD

Pursuant to the applicable PRC law, the consideration payable for the disposal

of state-owned assets has to be made with reference to valuation of the assets

to be transferred as prepared by qualified valuer and hence the consideration

in respect of the entire equity interest in Ningchang Zhenli, which amounted to

RMB502,000,000 (equivalent to approximately HKD636,560,000), was determined

based on the assessment of value of the entire equity interest of Ningchang Zhenli

by the state-owned asset valuation method. Given the transaction contemplated

is a connected and major transaction under the Hong Kong Listing Rules, the

Company has commissioned an independent valuer to report on the valuation

of Ningchang Zhenli. In deciding the consideration payable by the Company,

the directors primarily took into account the preliminary valuation prepared by

American Appraisal and the other factors as disclosed in more detail in the section

VII below. The consideration in respect of the interest-bearing borrowings will

be based on the outstanding amount as at the completion date. The total amount

of the interest-bearing borrowings owed by Ningchang Zhenli as at 30 September

2014 amounted to RMB7,295,500,000. The relevant consideration (not exceeding

RMB7,500,000,000 (equivalent to approximately HKD9,500,000,000)) will be paid

out of the Company’s own fund or through the Company’s financing activities.

2. Acquisition and absorption and merger of Xiyi Company by Guangjing

Xicheng

On 30 December 2014, Guangjing Xicheng, a subsidiary of the Company, entered

into a Xiyi Company Equity Transfer Agreement with each of Communications

Holdings, Changzhou Expressway and Wuxi Expressway, respectively, pursuant to

which Guangjing Xicheng has agreed to acquire, in aggregate, 100% of the equity

interest of Xiyi Company. At the same time, the Company and Xiyi Company

entered into the Absorption and Merger Agreement. Guangjing Xicheng shall

merge with Xiyi Company when the former acquired the entire equity interest of

Xiyi Company. The consideration payable by Guangjing Xicheng pursuant to this

transaction is RMB662,000,000 (equivalent to approximately HKD839,450,000).

— 4 —

LETTER FROM THE BOARD

Pursuant to the applicable PRC law, the consideration payable for the disposal

of state-owned assets has to be made with reference to valuation of the assets

to be transferred as prepared by qualified valuer and hence the consideration

in respect of the entire equity interest in Xiyi Company, which amounted to

RMB662,000,000 (equivalent to approximately HKD839,450,000), was determined

based on the assessment of value of the entire equity interest of Xiyi Company

the state-owned asset valuation method. Given the transaction contemplated

is a connected and major transaction under the Hong Kong Listing Rules, the

Company has commissioned an independent valuer to report on the valuation of

Xiyi Company. In deciding the consideration payable by Guangjing Xicheng,

the directors primarily took into account the preliminary valuation prepared by

American Appraisal and the other factors as more detailed disclosed in the section

VII below. In accordance to the respective equity interest held by Communications

Holdings, Changzhou Expressway and Wuxi Expressway in Xiyi Company, the

consideration to be paid by the Company to Communications Holdings, Changzhou

Expressway and Wuxi Expressway in relation to the acquisition of Xiyi Company

will be RMB519,010,000 (equivalent to approximately HKD658,130,000),

RMB31,910,000, (equivalent to approximately HKD40,460,000) and

RMB111,080,000 (equivalent to approximately HKD140,860,000), respectively.

Such consideration will be paid out of Guangjing Xicheng’s own fund or through

Guangjing Xicheng’s financing activities.

These two transactions are independent to each other, and shall be approved in

shareholders’ meeting separately.

(2) The Transactions constitute a significant affiliated transaction/connected and major

transaction

Significant affiliated transaction

Pursuant to the Shanghai Listing Rules and the Affiliated Transactions Guidelines,

as Communications Holdings which is a party to the Transactions, is the controlling

shareholder of the Company and is also the controlling shareholder of both Ningchang

Zhenli and Xiyi Company, the target companies of the Transactions, Communications

Holdings is an affiliated party and the Transactions constitute an affiliated transaction.

At the same time, as the transaction amount exceeds RMB30,000,000 and also exceeds

5% of the absolute value of the latest audited net asset of the Company, the Transactions

constitute a significant affiliated transaction. The Transactions do not constitute a

significant asset restructuring under the related regulations in Administrative Measures on

Significant Asset Restructuring of Listed Companies (《上市公司重大資產重組管理辦法》).

— 5 —

LETTER FROM THE BOARD

According to the Affiliated Transactions Guidelines and other relevant regulations issued

by the Shanghai Stock Exchange, given that the consideration for the entire equity

interests of Ningchang Zhenli is based on income approach, and exceeds its net book

value by over 100%, Communications Holdings has made profit guarantee in respect of

Ningchang Zhenli’s profit before tax and financial expenses after deducing non-recurring

gains and losses from 2015 to 2017.

Connected and major transaction

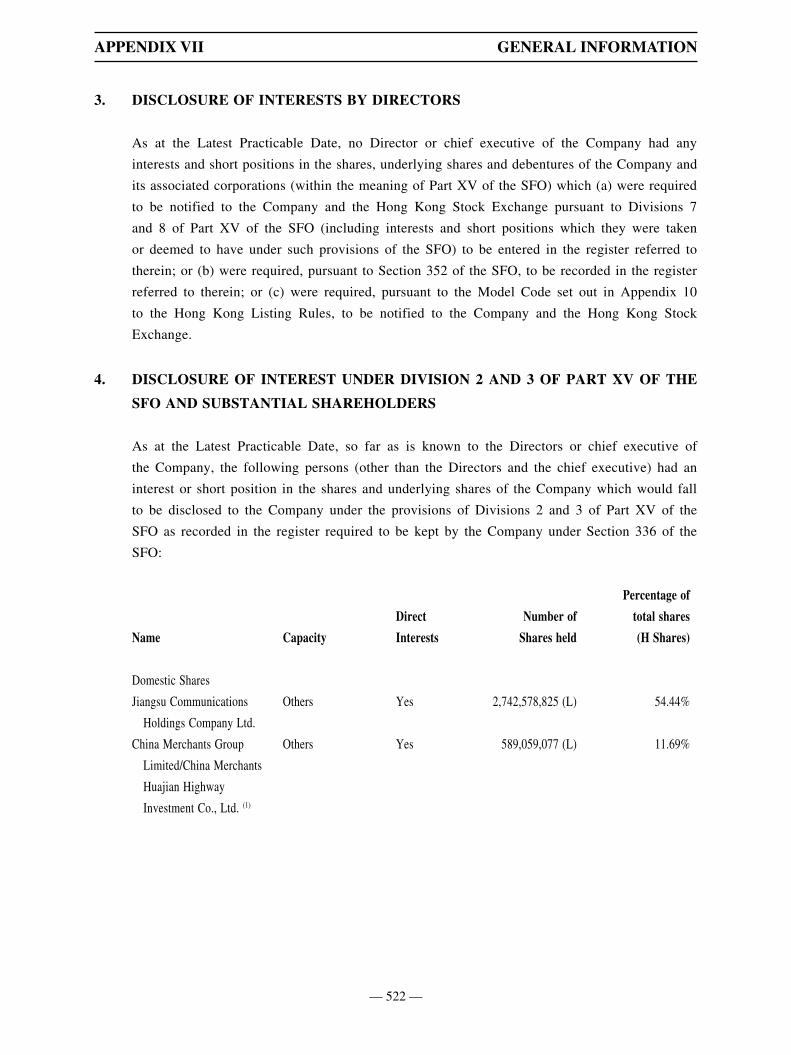

As at the Latest Practicable Date, Communications Holdings directly holds 2,742,578,825

shares of the Company, representing approximately 54.44% of the issued share capital

of the Company, and both Ningchang Zhenli and Xiyi Company are subsidiaries of

Communications Holdings. Therefore, Communications Holdings, Ningchang Zhenli

and Xiyi Company are connected persons of the Company and the Transactions together

constitute a connected transaction under Chapter 14A of the Hong Kong Listing Rules.

Given that the Transactions involve Communications Holdings or its associates as one

of the counterparties to the relevant agreements, the Directors of the Company are of

the view that the these Transactions should be aggregated pursuant to Rule 14.22 and

Rule 14A.81 of the Hong Kong Listing Rules. Upon aggregating the Transactions, given

that the asset ratio for these Transactions is approximately 37.28%, although all other

applicable ratios do not exceed 25%, the Transactions constitute a major transaction

pursuant to Chapter 14 of the Hong Kong Listing Rule. It is therefore subject to reporting,

announcement, circular and independent shareholders’ approval requirements under

Chapters 14 and 14A of the Listing Rules.

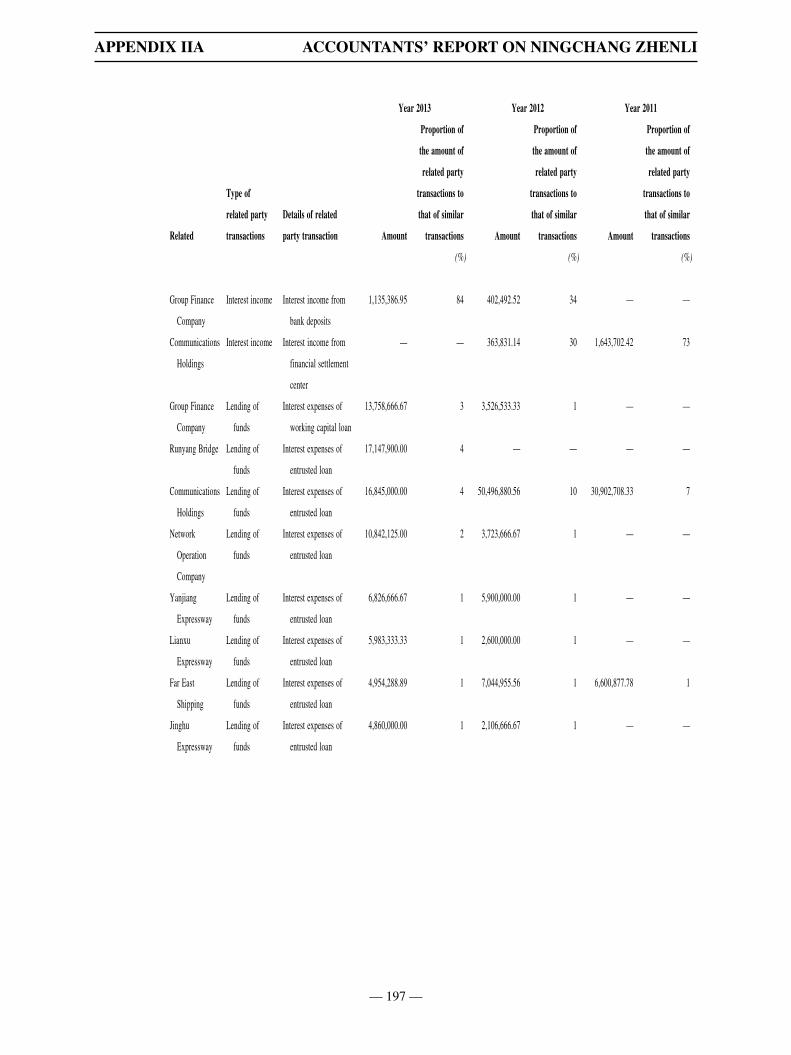

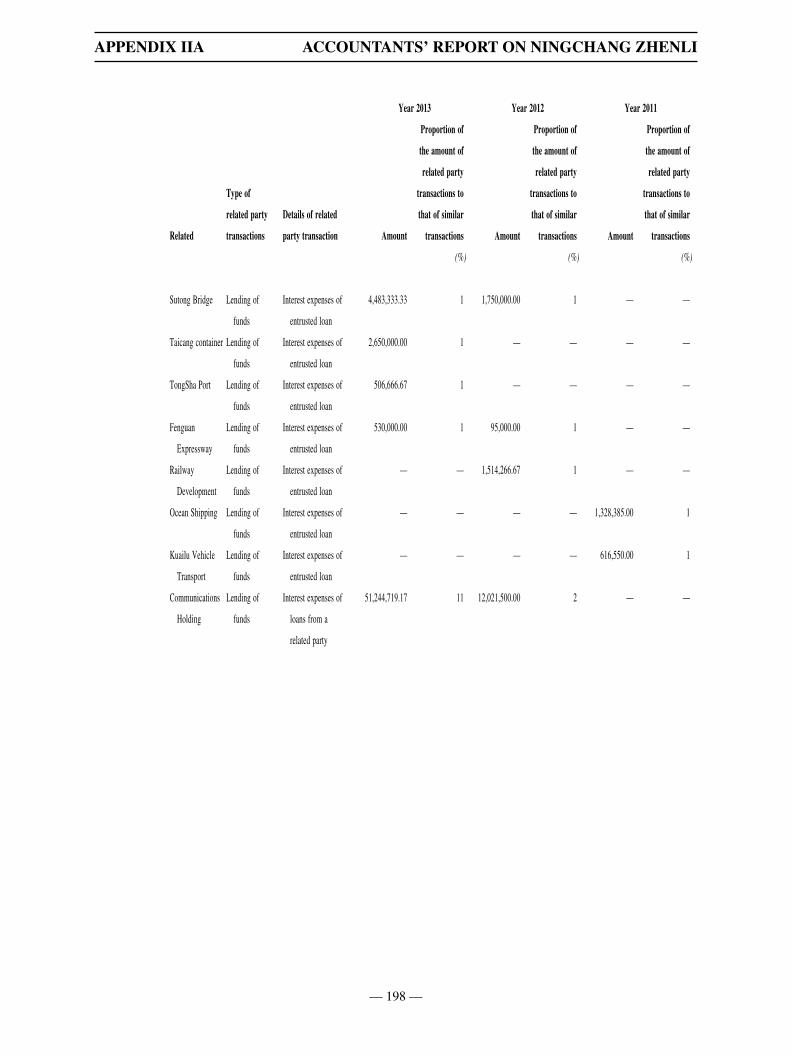

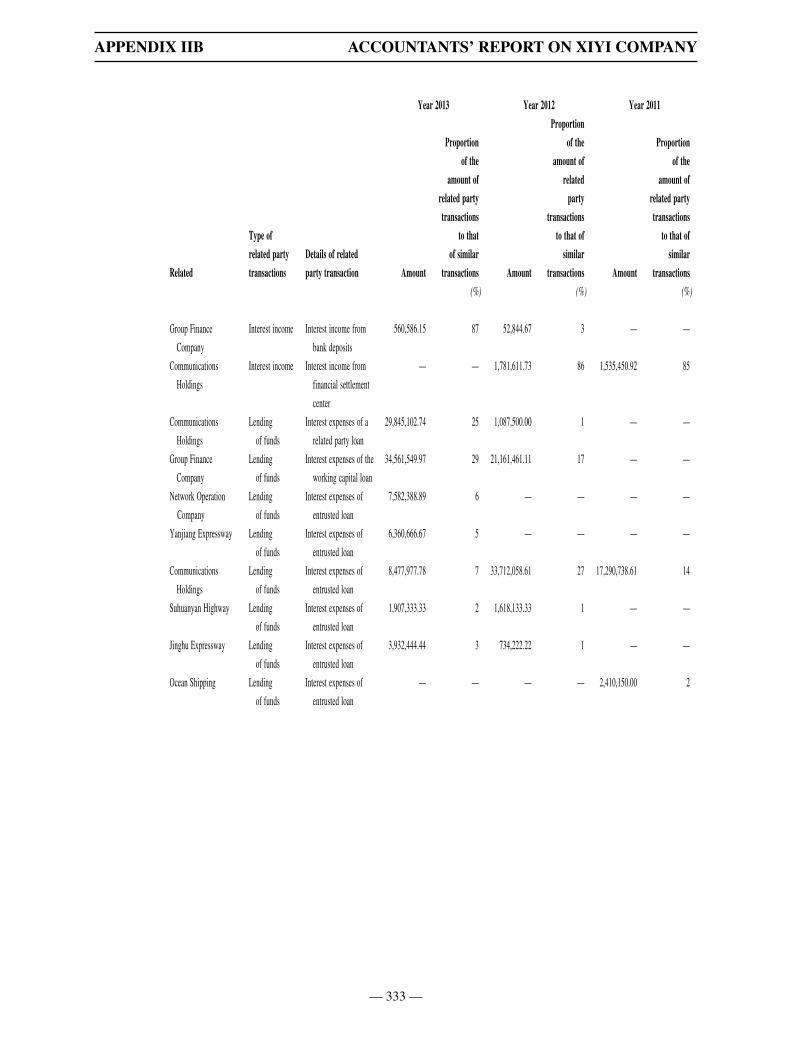

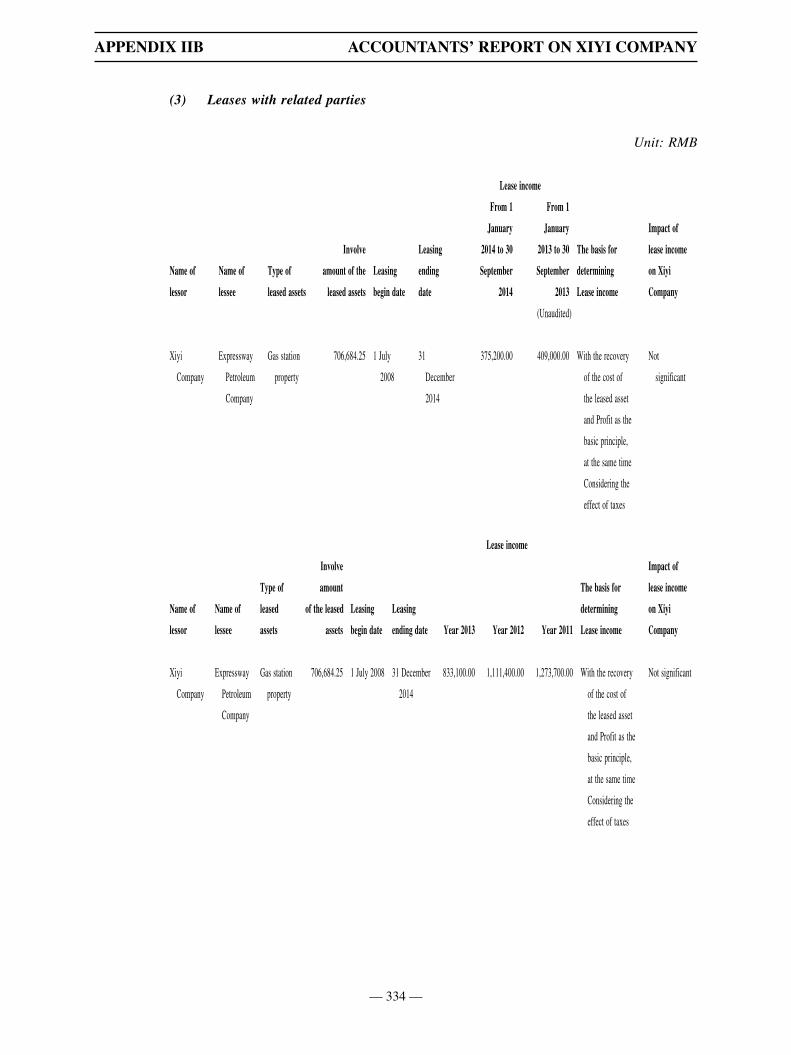

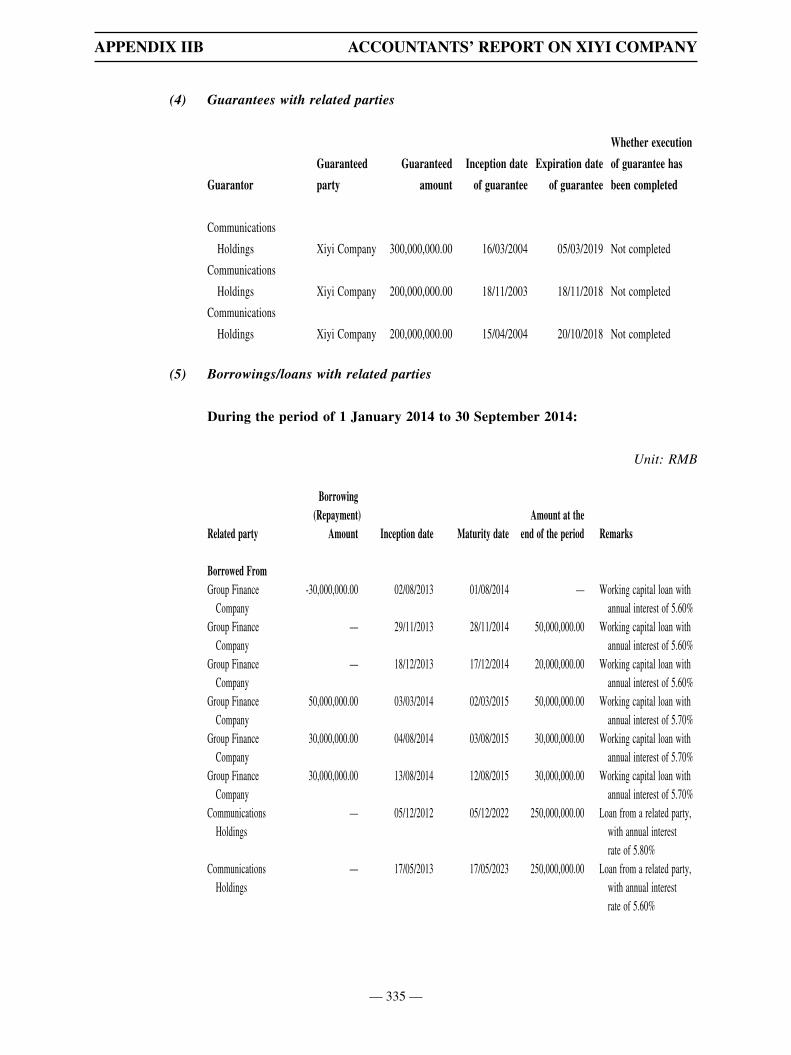

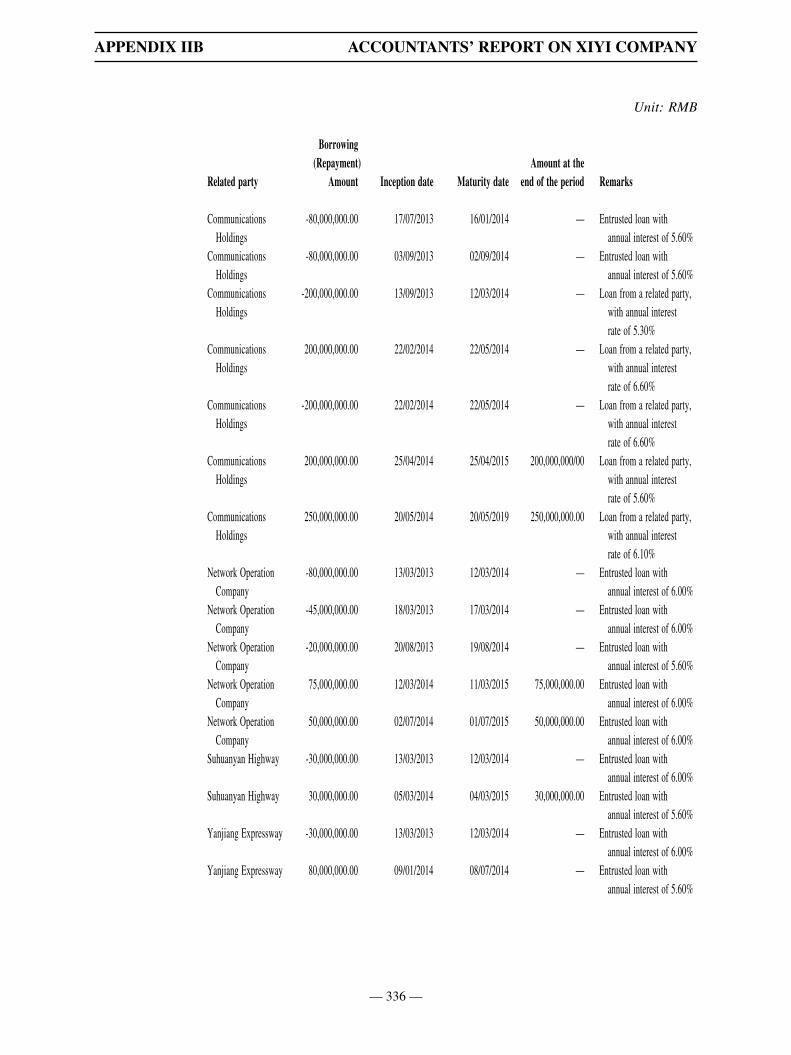

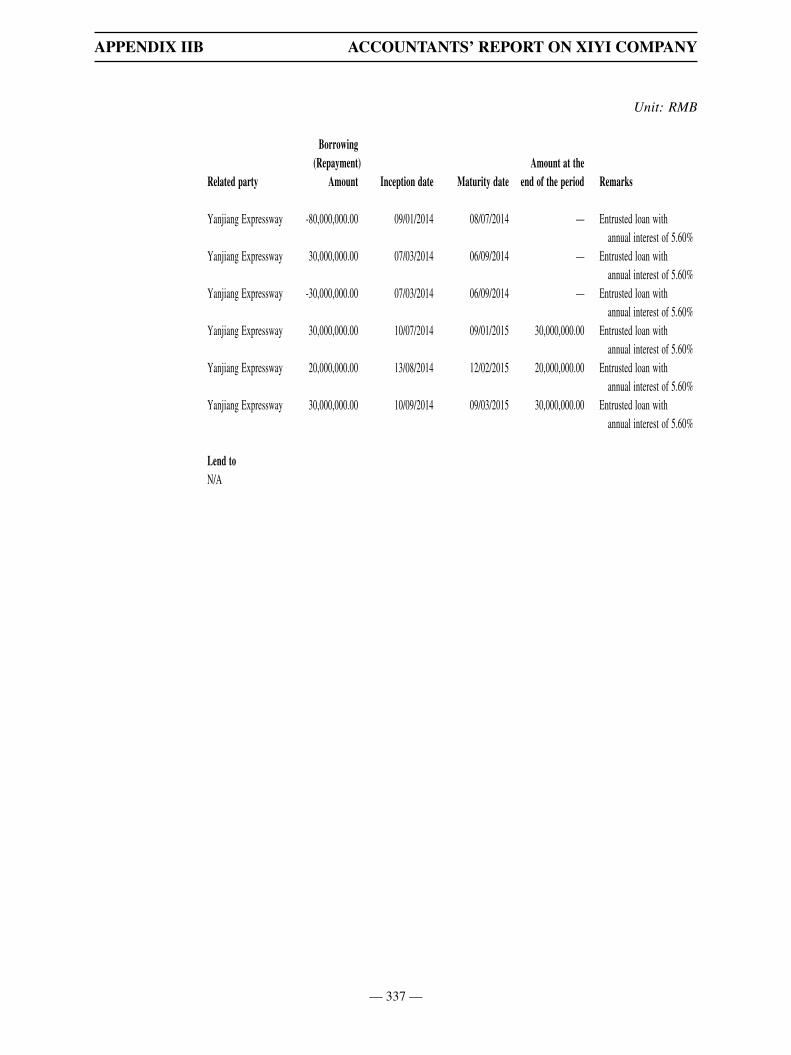

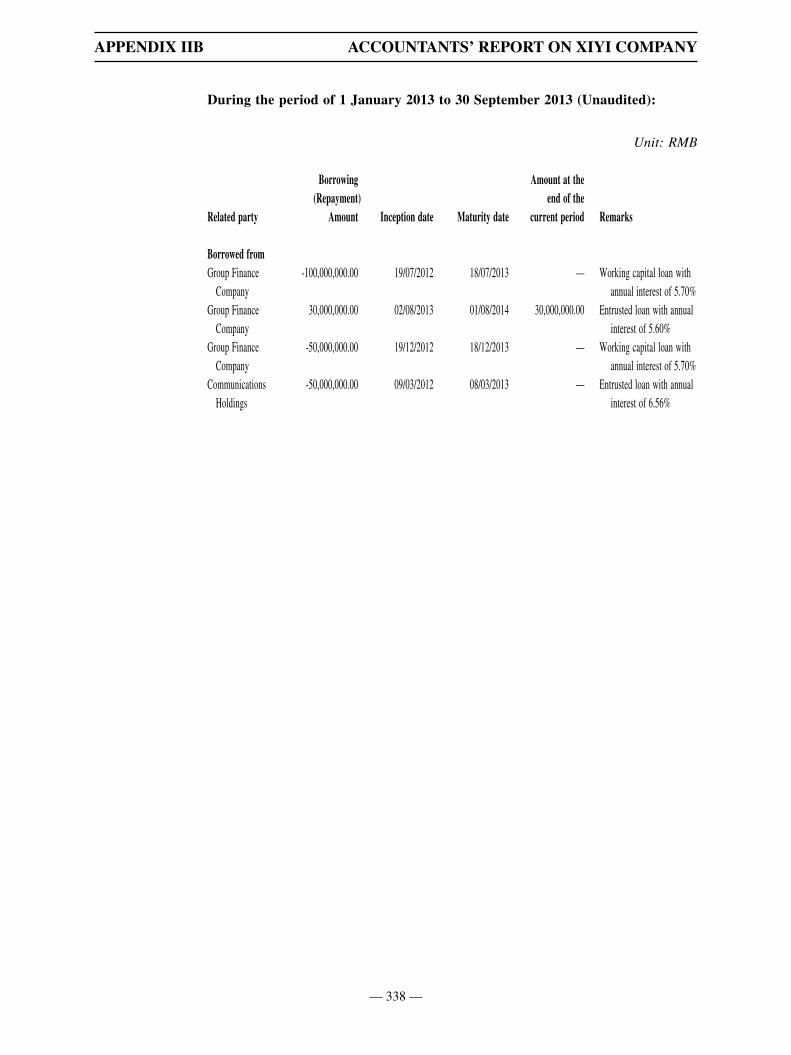

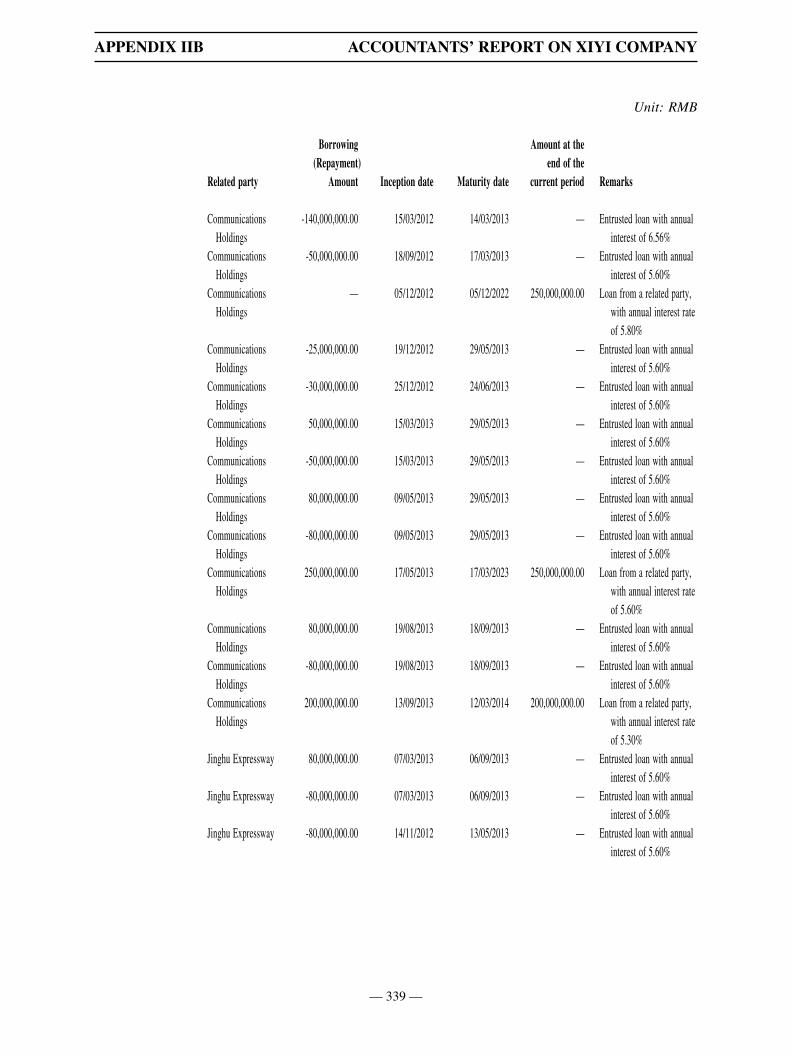

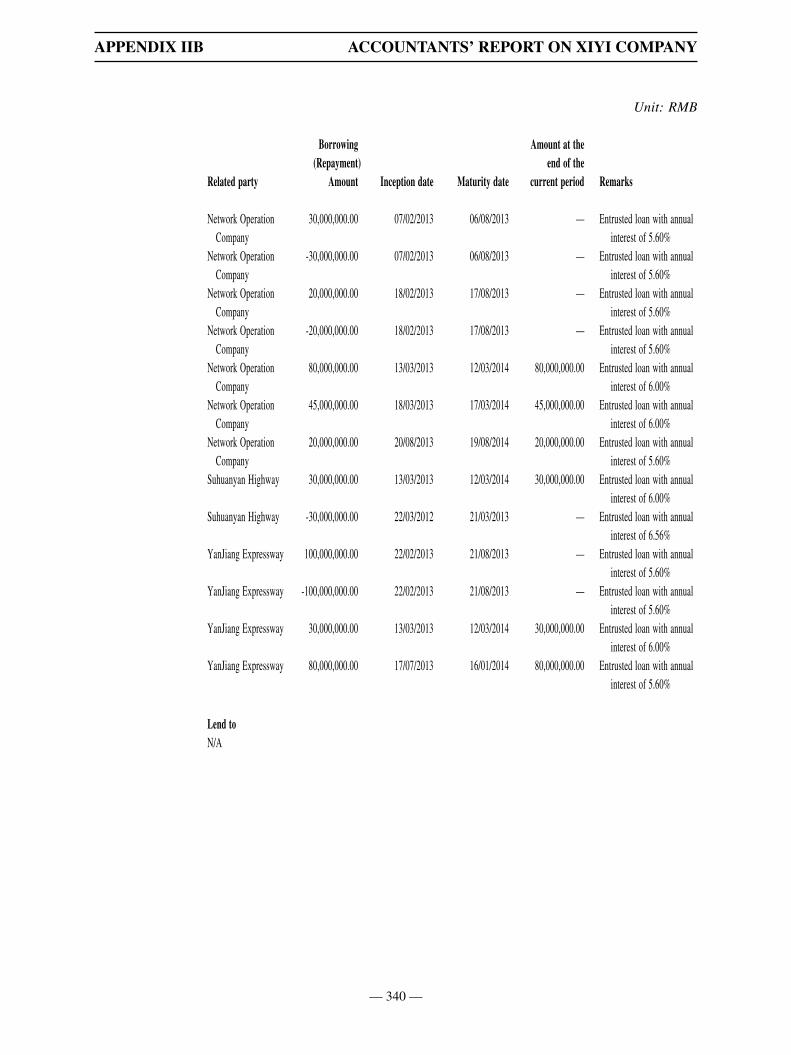

Continuing connected transaction

The interest-bearing borrowings owed by Ningchang Zhenli, which would be acquired

by the Company, include loans owed to Communications Holdings and its subsidiaries

(Jiangsu Communications Holding Group Financial Company Limited (hereinafter

“Communications Financial”) and Jiangsu Yanjiang Expressway Co., Ltd. (“Yanjiang

Expressway”), Jiangsu Runyang Bridge Development Company Limited (“Runyang

Bridge”), Jiangsu Expressway Network Operation & Management Co., Ltd. (“Network

Operation Company”), Jiangsu Jinghu Expressway Company Limited (“Jinghu

Expressway”), Nantong Tongsha Port Company Limited (“Tongsha Port”) and Taicang

Container Lines Company Limited (“Taicang Lines”)). Communications Holdings,

Communications Financial, Yanjiang Expressway, Runyang Bridge, Network Operation

Company, Jinghu Expressway, Tongsha Port and Taicang Line are connected persons of

the Company and the undertaking constitutes continuing connected transactions pursuant

to Chapter 14A of the Hong Kong Listing Rules. However, given that the loans with

— 6 —

LETTER FROM THE BOARD

Communications Financial are conducted on normal commercial terms or better terms

and are not secured by the assets of the Group, such connected transactions are exempted

from the reporting, announcement, circular and independent shareholders’ approval

requirements under Rule 14A.90 of the Hong Kong Listing Rules.

Ningchang Zhenli and Xiyi Company are shareholders of Network Operation Company.

Network Operation Company is the only company in the Jiangsu Province which provides

technical services for expressway inter-networked toll collection, and its equity interests

were held by various major expressway and bridge operators in the Jiangsu Province. Its

services include toll auditing and account settlements (including inter-provincial network

settlements in ETC East China region); electronic toll collection services; collection,

dispatch, coordination and management of expressways’ inter-network public information

in Jiangsu Province; procurement and distribution of On Board Unit (OBU) and Identity

Card which are used by expressway toll systems in Jiangsu Province; publicity and

promotion of the ETC system and the sale of OBU, as well as ancillary services such as

the setting up and marketing of the ETC customer service networks. The standard fee

rate chargeable by Network Operation Company for the provisions of operation-network

services to the member of the expressway networks shall be paid by Ningchang Zhenli

and Xiyi Company in cash based on the actual toll revenue and the service fee standards

under the Official Response of the Provincial Price Bureau on the Inter-network Service

Fee Standards of Expressways (Jiangsu Province Price Bureau Su Jia Fu [2008] No. 204)

(江蘇省物價局蘇價服[2008]204號《省物價局關於高速公路聯網服務費標準的批覆》), which is not more than 0.2% for cash revenue and not more than 2% for non-cash

revenue. The annual technical service fees paid by Ningchang Zhenli and Xiyi Company

for 2014 were estimated to be approximately RMB3,000,000 and RMB1,900,000,

respectively (as set out in the traffic consultant reports of Ningchang Zhenli and Xiyi

Company in Appendix VA and Appendix VB, respectively). Based on the fees paid for

2014 and the estimated toll revenues, the maximum annual technical service fees payable

by Ningchang Zhenli and Xiyi Company are calculated based on the assumption that all

toll revenues will be non-cash revenue, i.e. multiplying the maximum rate of 2% by the

estimated annual toll revenues of each of Ningchang Zhenli and Xiyi Company. Hence,

the maximum annual technical service fees payable by Ningchang Zhenli for 2015, 2016

and 2017 are expected to be approximately not more than RMB15,080,000 (equivalent

to approximately HKD19,120,000), RMB16,440,000 (equivalent to approximately

HKD20,850,000) and RMB17,160,000 (equivalent to approximately HKD21,760,000)

respectively, whereas the maximum annual technical service fees payable by Xiyi

Company for 2015, 2016 and 2017 are expected to be approximately not more than

RMB5,930,000 (equivalent to approximately HKD7,520,000), RMB6,430,000 (equivalent

to approximately HKD8,150,000) and RMB6,950,000 (equivalent to approximately

— 7 —

LETTER FROM THE BOARD

HKD8,810,000) respectively, representing less than 5% of the unaudited consolidated total

assets of the Company as at 30 September 2014, the audited consolidated total revenue

of the Company for the year 2013 and the current market capitalization of the Company,

the technical services arrangements constitute continuing connected transactions under

the Hong Kong Listing Rules, which are subject to the reporting and announcement

requirements but are exempt from the independent shareholders’ approval requirement.

The technical services transaction must comply with the requirements of annual review

under the Hong Kong Listing Rules. Network Operation Company is an affiliated person

of the Company and the provisions of technical services constitute affiliated transactions

under the Shanghai Listing Rules. As these transactions represent less than 5% of the net

assets of the Company, under the Shanghai Listing Rules, they are subject to the reporting

and announcement requirements but are exempt from independent shareholders’ approval

requirement.

As at the Latest Practicable Date, both Ningchang Zhenli and Xiyi Company have

(i) maintained various outstanding account receivables balances with associate(s) of

Communications Holdings; and (ii) entered into certain related party transactions in

relation to, among other, sale and purchase of goods, provision and receipt of services,

borrowings and leasing. Following completion of the Transactions, the above mentioned

related party transactions and the related account receivables are expected to continue, and

some of which (being transactions between the Group and Commutation Holdings (and/

or its associates)) would constitute continuing connected transactions under Chapter 14A

of the Hong Kong Listing Rules. In order to comply with the relevant requirements under

the Hong Kong Listing Rules, the Company, Ningchang Zhenli and Guangjing Xicheng

shall, upon completion of the Transactions, enter into a fresh set of written agreements

with Communications Holdings (and/or its associates) in respect of such transactions.

Further announcement(s) will be issued by the Company in compliance with the

relevant requirements under Chapter 14A of the Hong Kong Listing Rules as and when

appropriate. In respect of the other short term and long term borrowings of Ningchang

Zhenli and Xiyi Company which will not constitute continuing connected transactions (and

will therefore not be subject to the written agreements as mentioned above) and will not

be transferred pursuant to the Debt Transfer Agreement, the Company will repay the same

as they fall due, or make necessary arrangements with the aim of reducing the relevant

finance costs.

— 8 —

LETTER FROM THE BOARD

III. INFORMATION ABOUT THE COMPANY AND PARTIES TO THE

TRANSACTIONS

(1) The Company

The Company is principally engaged in the investment, construction, operation and

management of toll road and bridge within Jiangsu Province and the development and

operation of ancillary service areas along such toll road and bridges.

(2) Communications Holdings

Name of corporation Jiangsu Communications Holdings Company Limited (江蘇交通控股有限公司)

Nature of the corporation Limited liability company (state-owned)

Registered address 291 East Zhongshan Road, Nanjing, the PRC.

Legal representative Chang Qing (常青)

Registered capital RMB16,800,000,000

Scope of business Management and administration of state-owned

assets (within the provincial government’s mandate),

investment, construction, operation and management

of transportation infrastructure, transportation and

related industries, highway toll, real estate investment,

domestic trade. (Projects subject to the approval of the

relevant departments shall be approved by the relevant

departments before being carried out)

Shareholder(s) State-owned Assets Supervision and Administration

Commission of Jiangsu Province (100%)

Principal Business Communications Holdings, a wholly state-owned

company, is authorised by the government of Jiangsu to

be principally engaged in the investment, construction,

operations and management of the transport infrastructure,

transportation and related properties, and the principal

business has remained stable for the past 3 years.

— 9 —

LETTER FROM THE BOARD

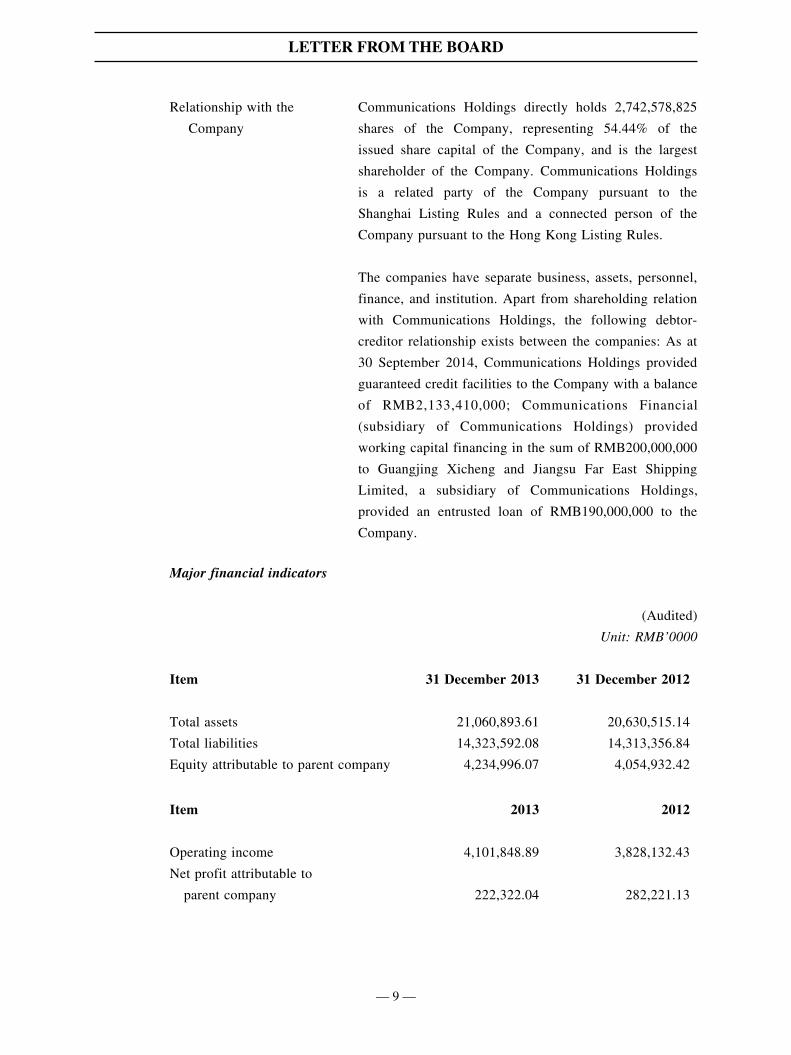

Relationship with the

Company

Communications Holdings directly holds 2,742,578,825

shares of the Company, representing 54.44% of the

issued share capital of the Company, and is the largest

shareholder of the Company. Communications Holdings

is a related party of the Company pursuant to the

Shanghai Listing Rules and a connected person of the

Company pursuant to the Hong Kong Listing Rules.

The companies have separate business, assets, personnel,

finance, and institution. Apart from shareholding relation

with Communications Holdings, the following debtor-

creditor relationship exists between the companies: As at

30 September 2014, Communications Holdings provided

guaranteed credit facilities to the Company with a balance

of RMB2,133,410,000; Communications Financial

(subsidiary of Communications Holdings) provided

working capital financing in the sum of RMB200,000,000

to Guangjing Xicheng and Jiangsu Far East Shipping

Limited, a subsidiary of Communications Holdings,

provided an entrusted loan of RMB190,000,000 to the

Company.

Major financial indicators

(Audited)

Unit: RMB’0000

Item 31 December 2013 31 December 2012

Total assets 21,060,893.61 20,630,515.14

Total liabilities 14,323,592.08 14,313,356.84

Equity attributable to parent company 4,234,996.07 4,054,932.42

Item 2013 2012

Operating income 4,101,848.89 3,828,132.43

Net profit attributable to

parent company 222,322.04 282,221.13

— 10 —

LETTER FROM THE BOARD

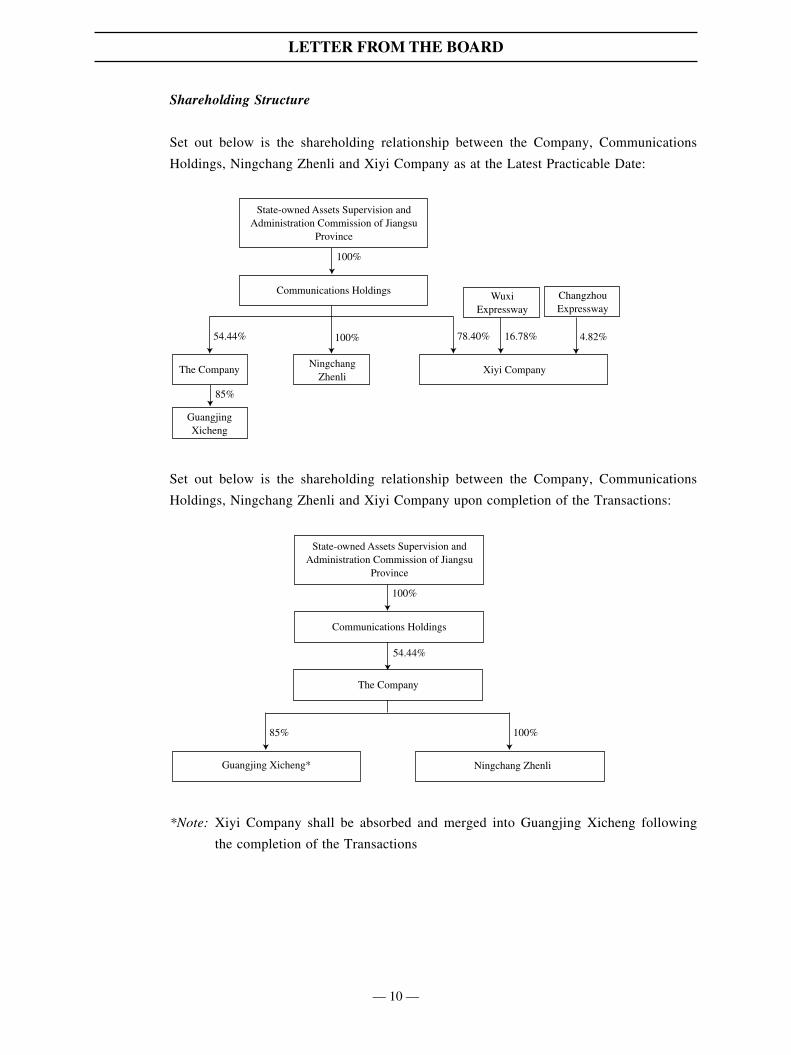

Shareholding Structure

Set out below is the shareholding relationship between the Company, Communications

Holdings, Ningchang Zhenli and Xiyi Company as at the Latest Practicable Date:

100%

100%

54.44%

85%

78.40%

State-owned Assets Supervision and Administration Commission of Jiangsu

Province

Communications Holdings

The CompanyNingchang

ZhenliXiyi Company

Guangjing Xicheng

16.78% 4.82%

Changzhou Expressway

WuxiExpressway

Set out below is the shareholding relationship between the Company, Communications

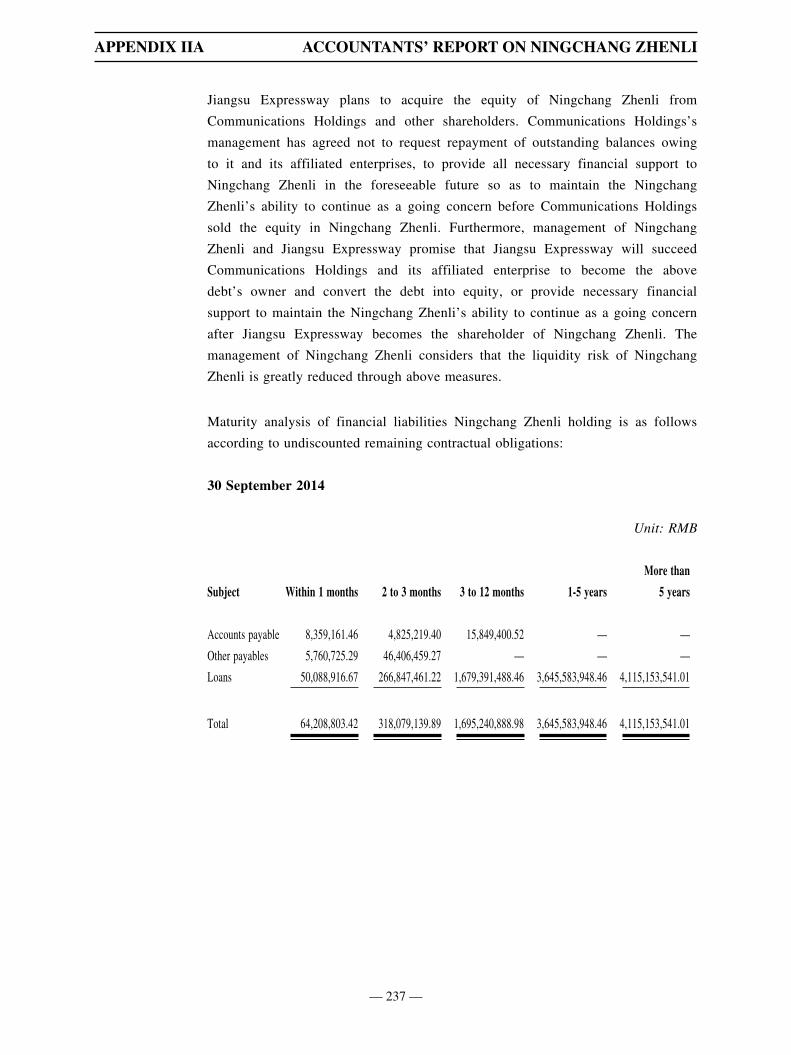

Holdings, Ningchang Zhenli and Xiyi Company upon completion of the Transactions:

54.44%

100%

85% 100%

State-owned Assets Supervision and Administration Commission of Jiangsu

Province

Communications Holdings

The Company

Ningchang ZhenliGuangjing Xicheng*

*Note: Xiyi Company shall be absorbed and merged into Guangjing Xicheng following

the completion of the Transactions

— 11 —

LETTER FROM THE BOARD

(3) Wuxi Expressway

Name of corporation Wuxi Expressway Investment Company Limited (無錫高速公路投資有限公司)

Registered capital RMB270,000,000

Registered address 100 East Yunhe Road, Wuxi, the PRC

Legal representative Xue Jun (薛軍)

Principal business Wuxi Expressway is principally engaged in the

investment, operation and management of expressway

and other regional highway projects, and the principal

business has remained stable for the past three years

Date of establishment 21 January 2001

As at the Latest Practicable Date, to the best of the Directors’ knowledge, information

and belief having made all reasonable enquiries, Wuxi Expressway and its ultimate

beneficial owners are third parties independent of and not a connected person (as defined

in the Hong Kong Listing Rules) of the Company.

(4) Changzhou Expressway

Name of corporation Changzhou Expressway Investment Development

Company Limited (常州高速公路投資發展有限公司)

Registered capital RMB200,000,000

Registered address Building 8, 583 Tongjiang Avenue, Changzhou, the PRC

Legal representative Ye Jun (葉軍)

Principal business Changzhou Expressway is principally engaged in the

construction, operation and management of highways,

roads, bridges and other infrastructure, and the principal

business has remained stable for the past three years

Date of establishment 11 May 2000

— 12 —

LETTER FROM THE BOARD

As at the Latest Practicable Date, to the best of the Directors’ knowledge, information

and belief having made all reasonable enquiries, Changzhou Expressway and its ultimate

beneficial owners are third parties independent of and not a connected person (as defined

in the Hong Kong Listing Rules) of the Company.

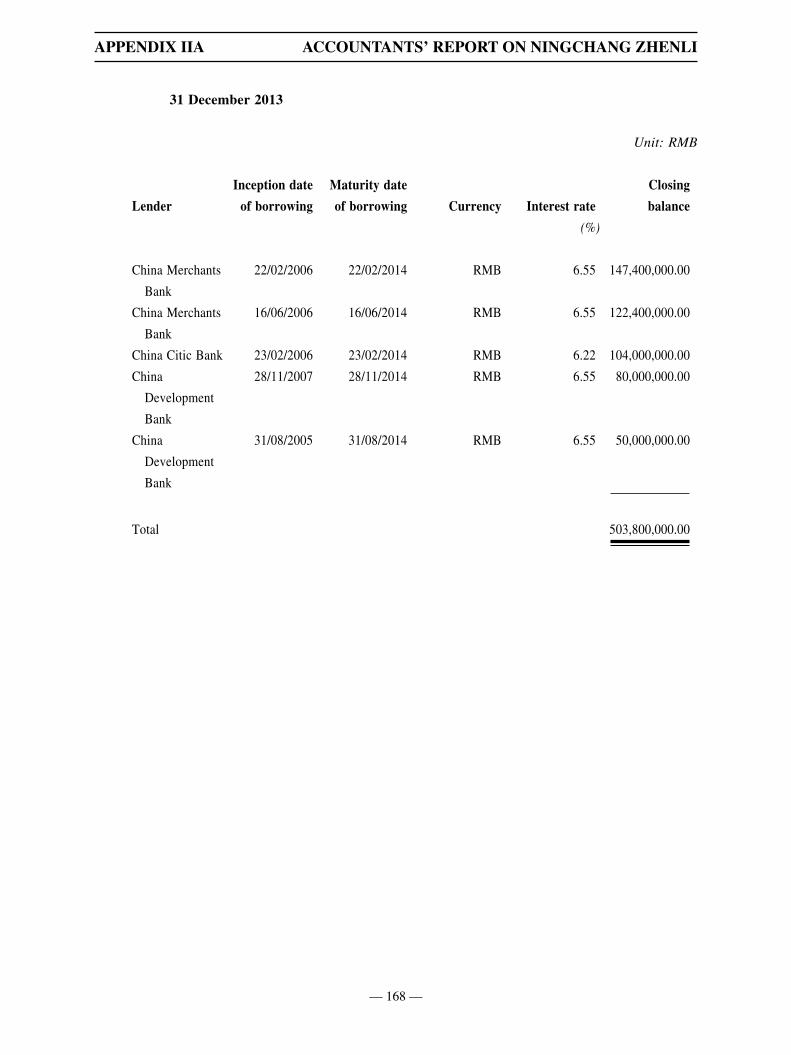

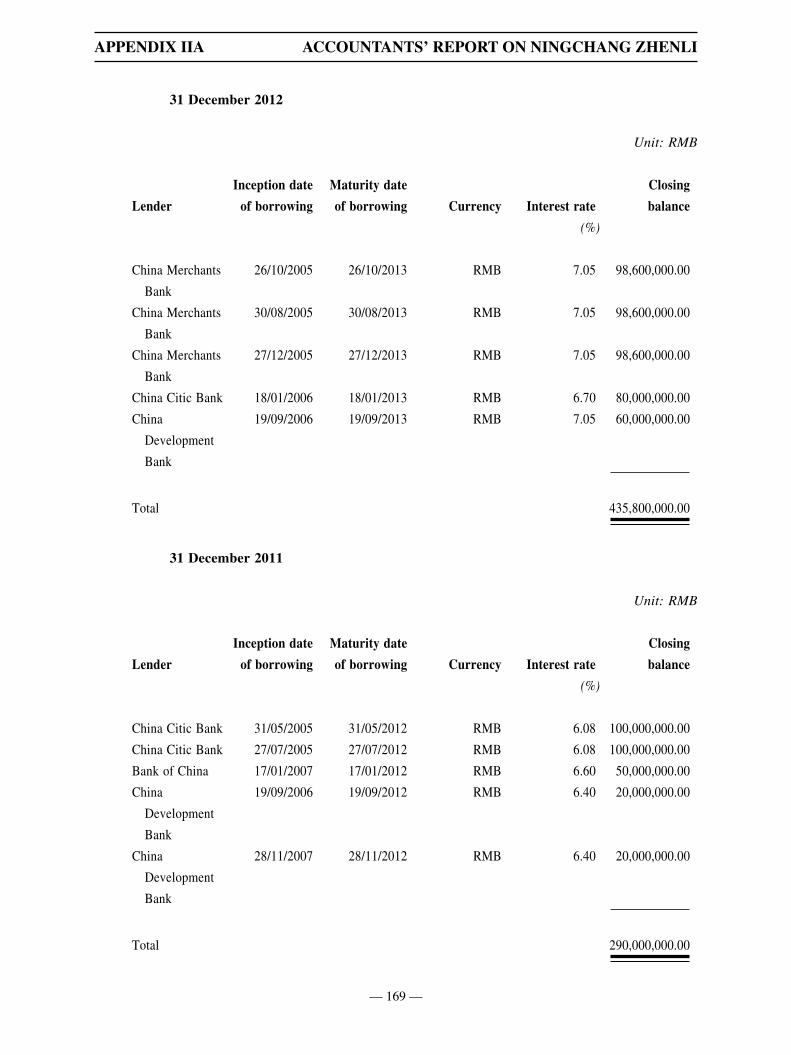

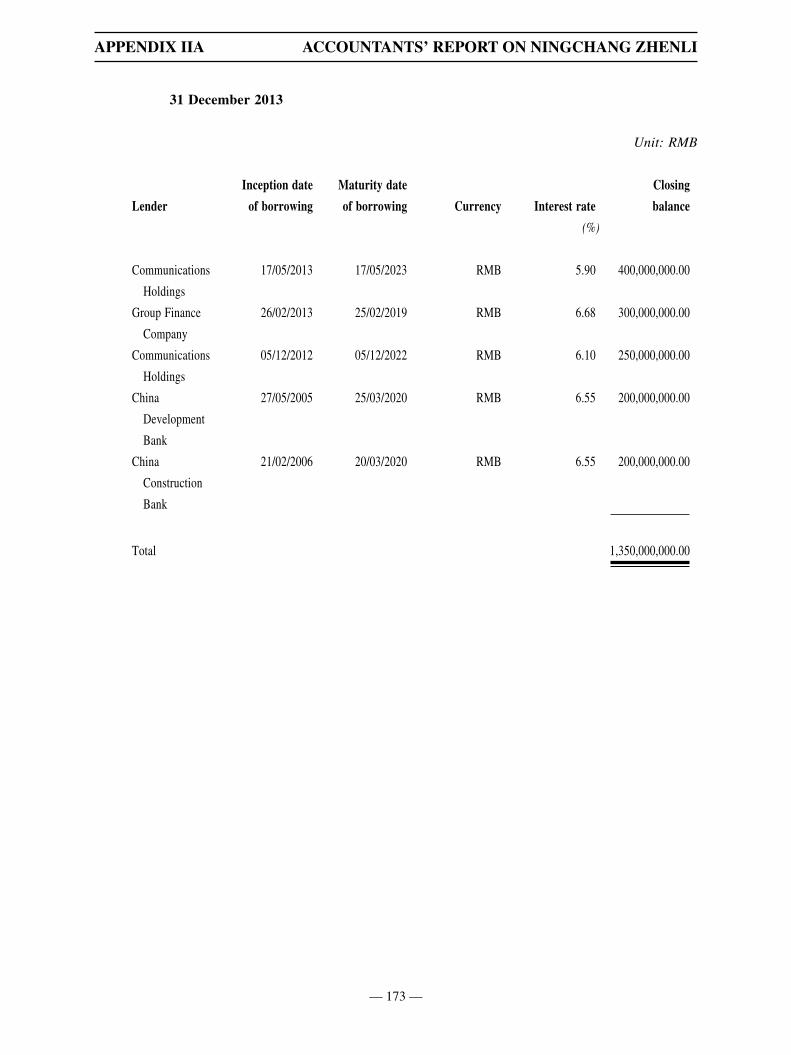

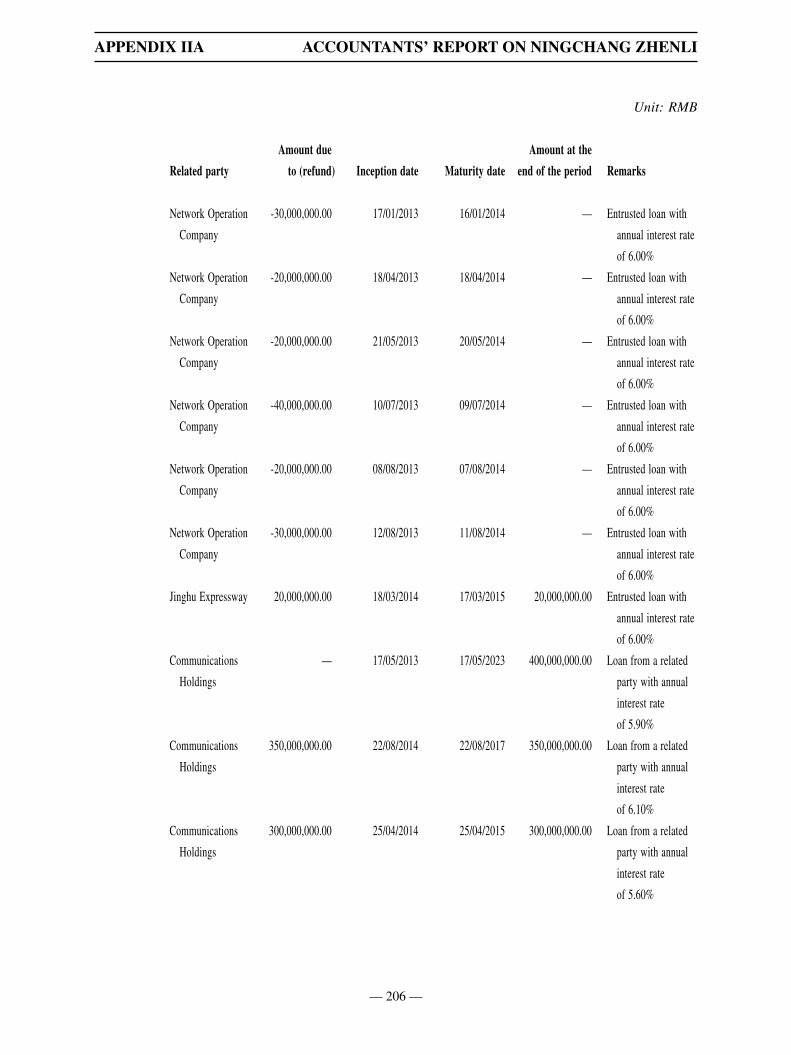

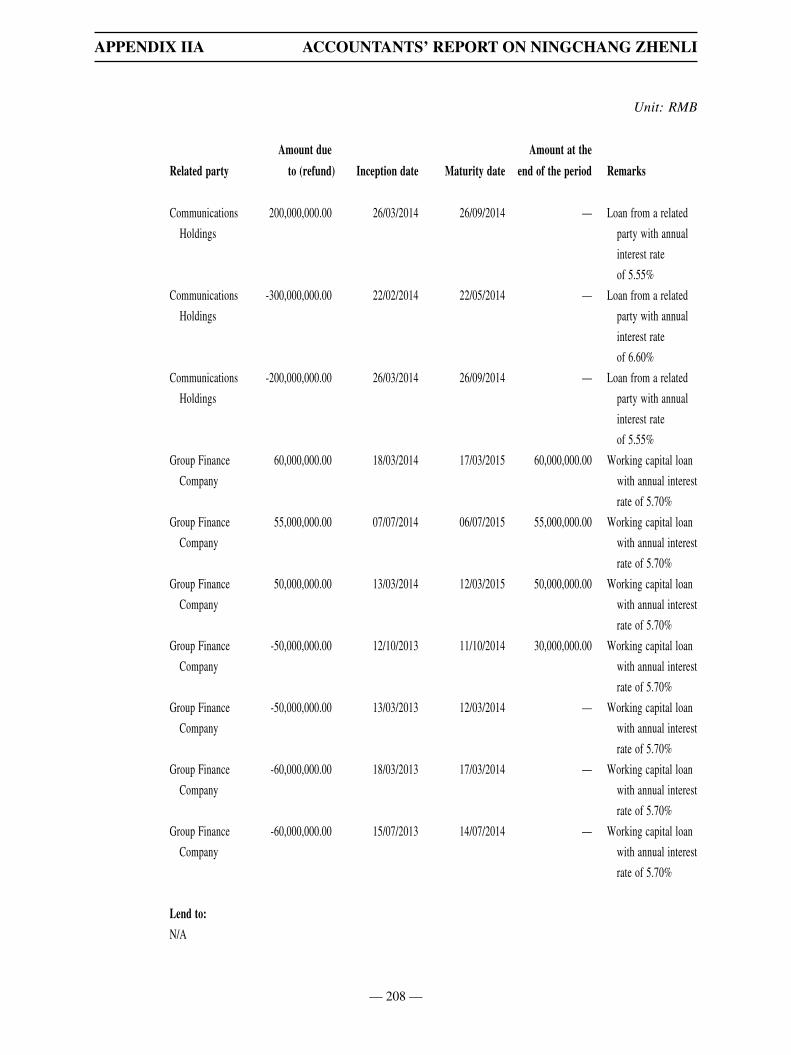

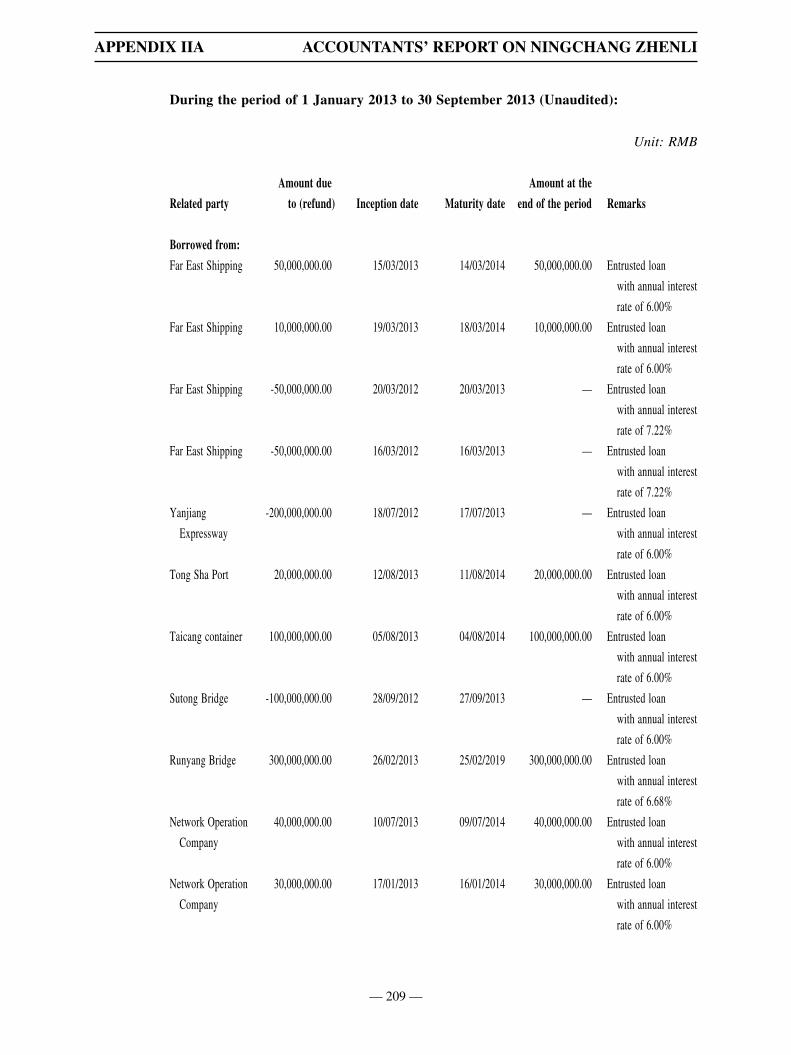

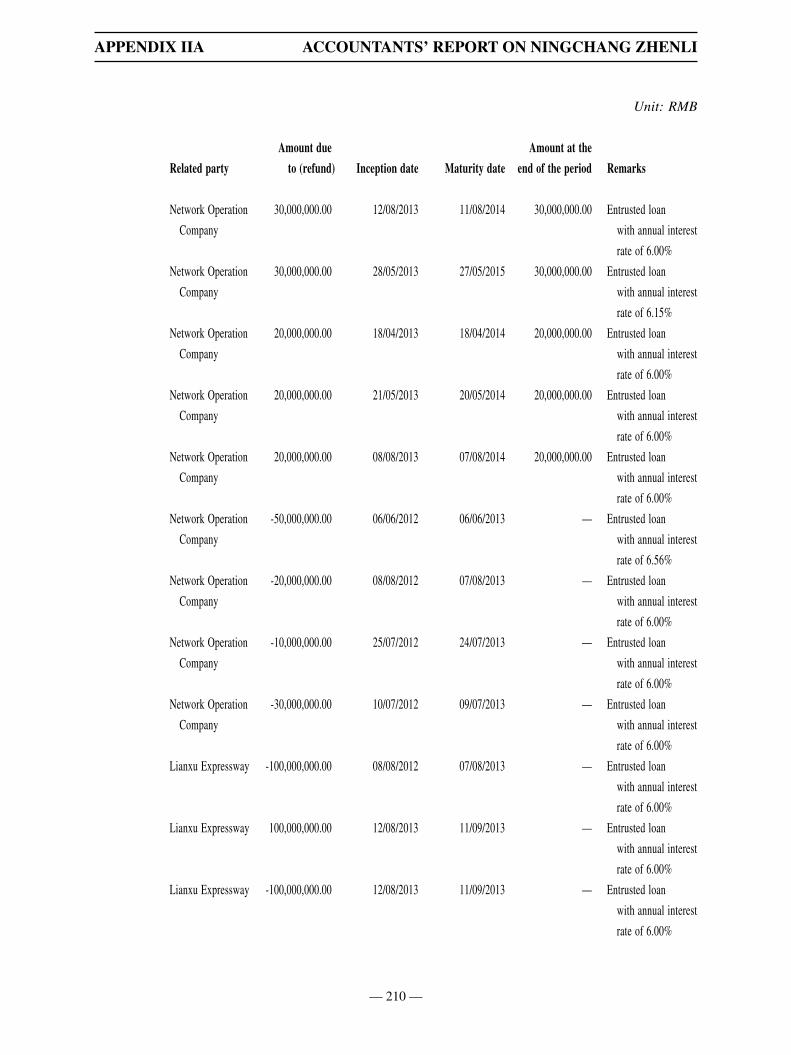

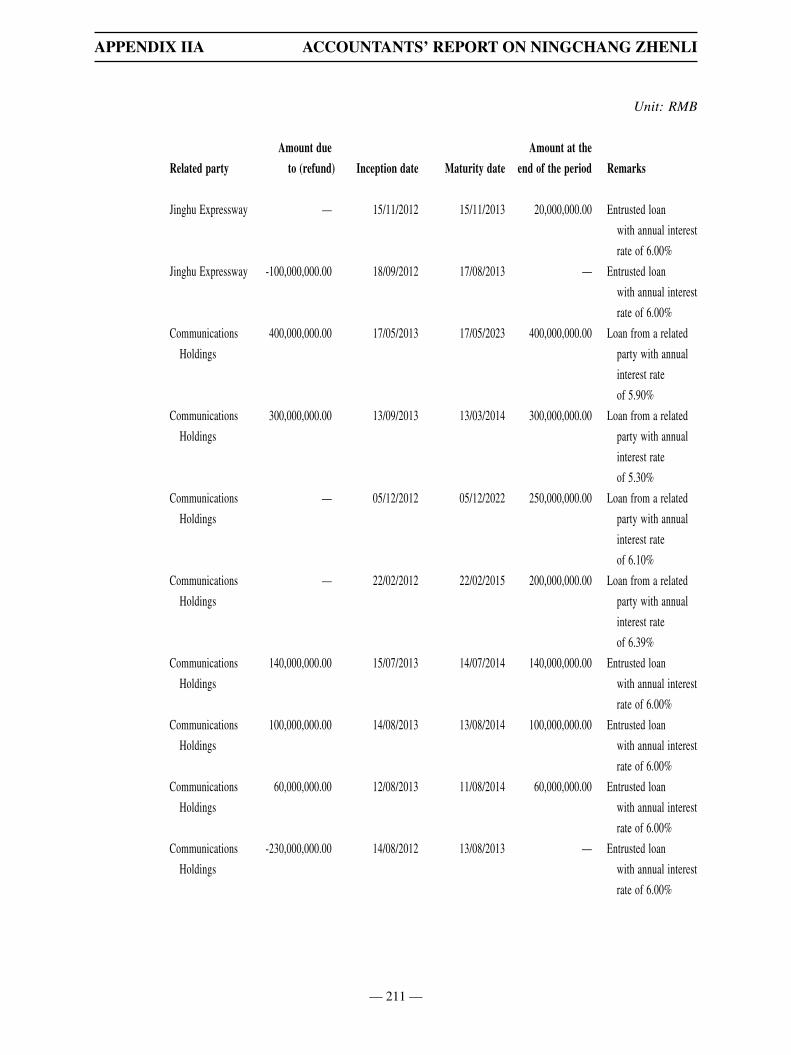

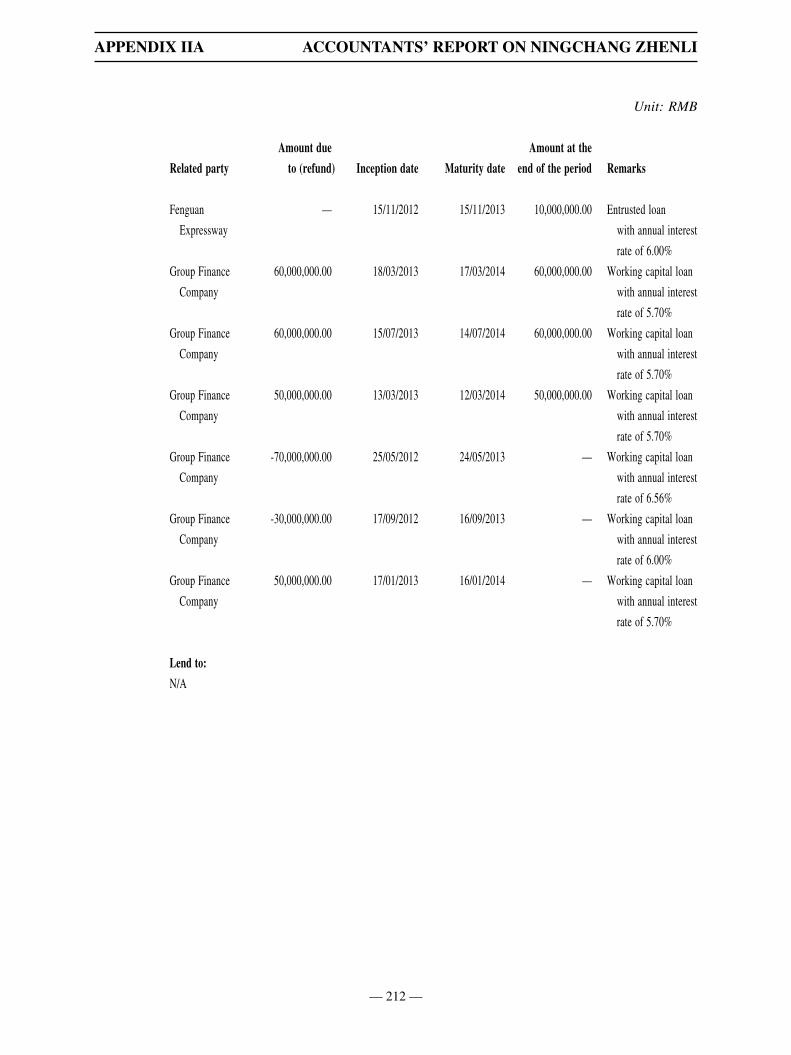

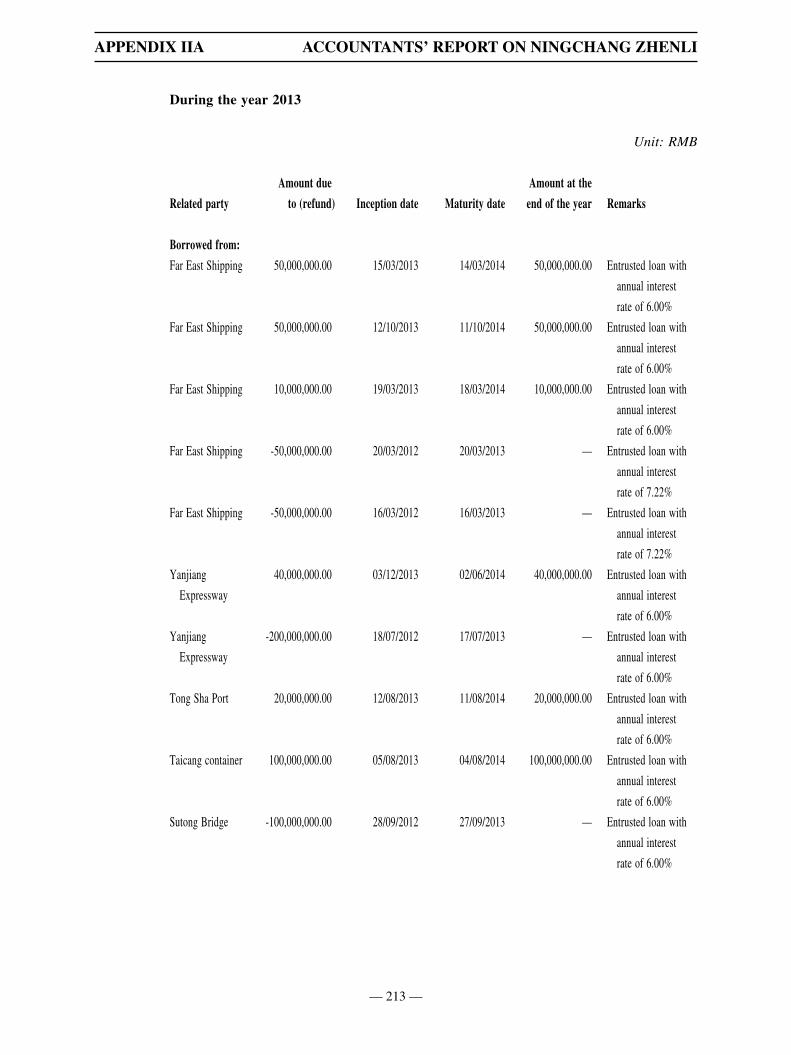

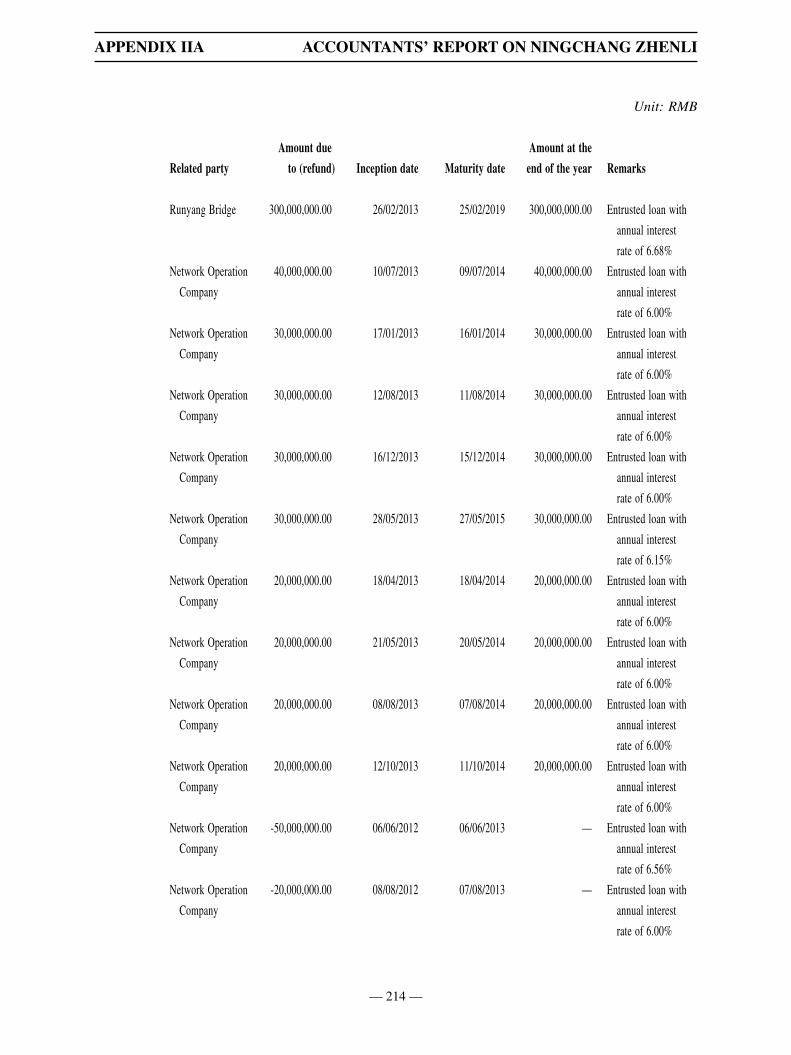

(5) Creditors of the interest-bearing borrowings of Ningchang Zhenli as at 30 September

2014

For the list of creditors of the interest-bearing borrowings of Ningchang Zhenli as at

30 September 2014, please refer to the section “IV. Basic information about the target

companies of the Transactions — (1) Ningchang Zhenli — v. Interest-bearing borrowings

proposed to be transferred in the transaction” in this letter.

At the Latest Practicable Date, after making all reasonable enquiries, according to the

Directors’ knowledge, information and belief, the connected relationships between the

creditors and the Company are as follows:

Debtor Connected relationship with the Company

Jiangsu Runyang

Bridge Development

Company Limited

Connected person: a subsidiary of a substantial shareholder

of the Company, Communications Holdings

Jiangsu Expressway

Network Operation

& Management

Company Limited

Connected person: a subsidiary of a substantial shareholder

of the Company, Communications Holdings

Jiangsu Communications

Holding Group

Financial Company

Limited

Connected person: a subsidiary of a substantial shareholder

of the Company, Communications Holdings

Jiangsu Jinghu

Expressway Company

Limited

Connected person: a subsidiary of a substantial shareholder

of the Company, Communications Holdings

Jiangsu Yanjiang

Expressway Co., Ltd

Connected person: a subsidiary of a substantial shareholder

of the Company, Communications Holdings

Nantong Tongsha Port

Company Limited

Connected person: a subsidiary of a substantial shareholder

of the Company, Communications Holdings

Taicang Container Lines

Company Limited

Connected person: a subsidiary of a substantial shareholder

of the Company, Communications Holdings

Communications

Holdings

Connected person: a substantial shareholder of the Company

— 13 —

LETTER FROM THE BOARD

Save as the aforementioned creditors, all other creditors are commercial banks with PRC

bank operating licenses. As at the Latest Practicable Date, to the best of the Directors’

knowledge, information and belief having made all reasonable enquiries, all other

creditors (China Development Bank (Jiangsu Branch), China Construction Bank (Jiangsu

Branch), Wangfu Nanjing Branch of CITIC Bank and Bank of China (Jiangsu Branch))

and their ultimate beneficial owners are third parties independent of and not a connected

person of the Company.

IV. BASIC INFORMATION ABOUT THE TARGET COMPANIES OF THE

TRANSACTIONS

The Transactions concern: the Company acquiring 100% of the equity interest of Ningchang

Zhenli and Xiyi Company from Communications Holdings and other parties by cash, and

merging with Xiyi Company; and also carrying out debt restructuring in respect of Ningchang

Zhenli at the same time (through acquiring all the interest-bearing borrowings of Ningchang

Zhenli and capitalising such debts).

The relevant category of these affiliated transactions is asset acquisition and debt restructuring.

(1) Ningchang Zhenli

i. Basic Information

Name of corporation Jiangsu Ningchang Zhenli Expressway Company Limited

(江蘇寧常鎮溧高速公路有限公司)

Nature of corporation Limited liability company

Registered capital RMB3,328,850,000

Registered address 291 East Zhongshan Road, Nanjing, the PRC

Legal representative Chen Xianghui (陳祥輝)

— 14 —

LETTER FROM THE BOARD

Business scope Approved business scopes: (the following areas are

operated by branch organizations as regulated by the

respective business licenses): car maintenance and repair,

catering service, sales of food and beverage, cigarettes

(cigar), sales of refined oil products, accommodation,

sales of publications.

General business scope: highway construction,

management, repair and related technical consultation, toll

for traffic access, sales of goods, textile products, daily

commodities, hardware, electrical equipment, chemicals

and water product, design of, production of, agent for

and outdoor distribution of advertisements, prints and gift

advertisements.

Date of incorporation 10 June 2004

ii. Description on ownership

As at the Latest Practicable Date, Ningchang Zhenli was 100% owned by

Communications Holdings. The total investment cost of Communications Holdings

in Ningchang Zhenli, which is Communications Holdings’ original purchase cost of

its equity interest in Ningchang Zhenli, is RMB3,328,850,000.

Note: Since the consideration for the acquisition of Ningchang Zhenli is based on a valuation, the historic acquisition costs of Communications Holdings is not relevant.

The ownership concerning the equity interest of Ningchang Zhenli is transparent

without any charge or mortgage. Ningchang Zhenli is not involved in any

significant litigation, arbitration or other circumstances which will impede the

transfer of ownership.

— 15 —

LETTER FROM THE BOARD

iii. Description of operations of relevant assets

Ningchang Zhenli is principally engaged in the operation, maintenance and

management of Ningchang Expressway and Zhenli Expressway, which operations

are normal. The main revenue of the business of Ningchang Zhenli is its toll

income. A brief summary of the basic information of Ningchang Expressway and

Zhenli Expressway is as follows:

Name of road Starting point Ending point Kilometers No. of lanes Concession period

Ningchang Expressway Lishui Duzhuang Hub South of Changzhou

Interchange

87.26 6 lanes in the entire expressway Sep 2007 to Sep 2032

Zhenli Expressway Dantu Hub Liyang Qianma Hub 65.658 6 lanes in the entire expressway Sep 2007 to Sep 2032

Set out below is a geographic diagram showing Jiangsu Section of the Huning

Expressway (“Shanghai-Nanjing Expressway”), the major road assets of the

Company and the major road assets of Ningchang Zhenli:

Taihu Lake

Ma’anshan

Nanjing

ZhenJiang

Hanjiang Yangzhou

Runzhou

Jintan

Lishui

Gaochun

Liyang

Yixing

Wujin

YanjiangExpressway

South Connectionof Runyang Bridge

Runyang Bridge

Lima Expressway

LiguangExpressway

Shanghai-NanjingExpressway

NingchangExpresswayZhenli

Expressway

North Connectionof Runyang Bridge

DanyangJurong

Changzhou

— 16 —

LETTER FROM THE BOARD

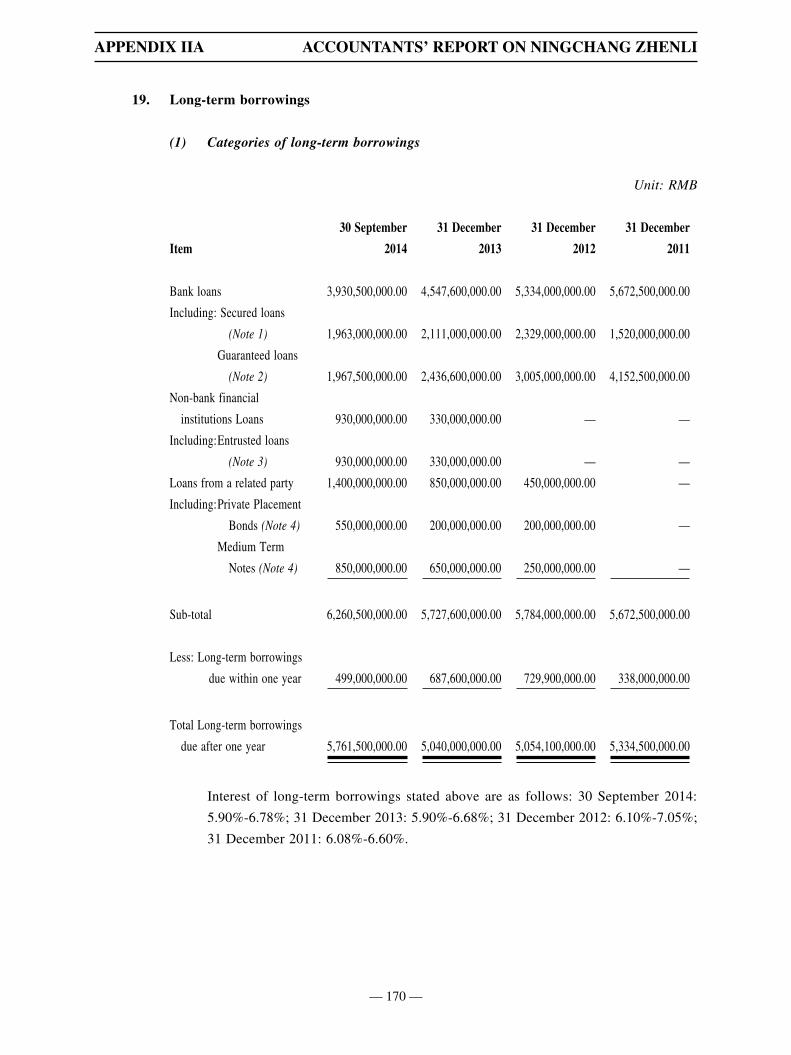

iv. Major financial data (Two years and nine months ended 30 September 2014)

In accordance of the audit report De Shi Bao (Shen) Zi No. S0211 (specific audit

report) (standard unqualified opinion) of Ningchang Zhenli (on consolidated basis)

as prepared by Deloitte Touche Tohmatsu Certified Public Accountants LLP, a

licensed corporation to carry out equity and futures activities, the major financial

data of Ningchang Zhenli for the years 2012 and 2013 and the nine months ended

30 September 2014 is as follows:

Unit: RMB’0000

(Audited)

Item

30 September

2014

31 December

2013

31 December

2012

Total assets 768,402.75 788,804.08 815,563.78

Total liabilities 747,352.44 743,691.41 725,451.57

Shareholders’ equity 21,050.31 45,112.67 90,112.21

Item Jan to Sep 2014 2013 2012

Income 49,165.21 45,613.98 42,289.80

Financial expenses 35,449.96 46,744.00 48,851.06

Profit –24,107.27 –45,130.88 –46,467.70

Net profit* –24,062.36 –44,999.54 –46,663.12

* Net profit before deduction of tax and non-recurring items = net profit after deducting taxes and non-recurring items

The concession rights of Ningchang Expressway and Zhenli Expressway

represented over 90% of the assets of Ningchang Zhenli. These concession rights

had a book value of RMB7,018 million as at 30 September 2014, and the aggregate

amortization was RMB908 million. In 2013 the annual amortization was RMB185

million. The amortization from January to September 2014 was RMB200 million.

After the completion of the Transactions, Ningchang Zhenli shall be consolidated

into the consolidated financial statements of the Company. The Company has not

provided any guarantee for Ningchang Zhenli or appointed Ningchang Zhenli to

manage assets. No fund of the Company has been used by Ningchang Zhenli.

— 17 —

LETTER FROM THE BOARD

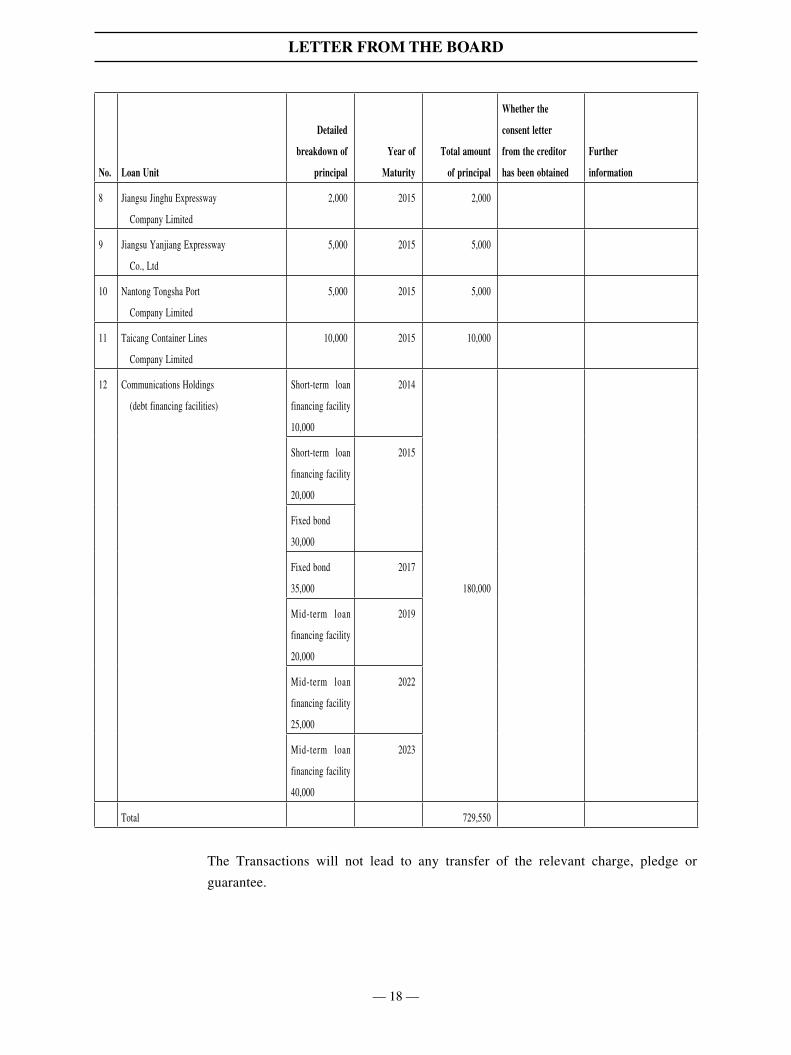

v. Interest-bearing borrowings proposed to be transferred in the Transactions

The Company intends to acquire all interest-bearing borrowings of Ningchang

Zhenli as at the completion date of the transfer of equity interest. As at 30

September 2014, the details of interest-bearing borrowings of Ningchang Zhenli is

as follows:

Unit: RMB’0000

No. Loan Unit

Detailed

breakdown of

principal

Year of

Maturity

Total amount

of principal

Whether the

consent letter

from the creditor

has been obtained

Further

information

1 Jiangsu Branch of

China Development Bank

10,000 2017 127,000 Yes Pledge of concession

right of Ningchang

Expressway

102,000 2020

15,000 2022

2 Jiangsu Branch of

China Construction Bank

50,750 2019 109,750 Yes Guaranteed by

Communications Holdings59,000 2020

3 Jiangsu Branch of Bank of China 69,300 2020 69,300 Yes Pledge of

concession right

of Zhenli

Expressway

4 Wangfu Nanjing Branch of

CITIC Bank

87,000 87,000 Fully repaid

on 28 November

2014

Guaranteed by

Communications

Holdings

5 Jiangsu Runyang Bridge Development

Company Limited

30,000 2019 90,000

60,000 2023

6 Jiangsu Expressway Network Operation

& Management Company Limited

5,000 2014 25,000

20,000 2015

7 Jiagnsu Communications Holding

Group Financial Company

Limited

19,500 2014 19,500

— 18 —

LETTER FROM THE BOARD

No. Loan Unit

Detailed

breakdown of

principal

Year of

Maturity

Total amount

of principal

Whether the

consent letter

from the creditor

has been obtained

Further

information

8 Jiangsu Jinghu Expressway

Company Limited

2,000 2015 2,000

9 Jiangsu Yanjiang Expressway

Co., Ltd

5,000 2015 5,000

10 Nantong Tongsha Port

Company Limited

5,000 2015 5,000

11 Taicang Container Lines

Company Limited

10,000 2015 10,000

12 Communications Holdings

(debt financing facilities)

Short-term loan

financing facility

10,000

2014

180,000

Short-term loan

financing facility

20,000

2015

Fixed bond

30,000

Fixed bond

35,000

2017

Mid-term loan

financing facility

20,000

2019

Mid-term loan

financing facility

25,000

2022

Mid-term loan

financing facility

40,000

2023

Total 729,550

The Transactions will not lead to any transfer of the relevant charge, pledge or

guarantee.

— 19 —

LETTER FROM THE BOARD

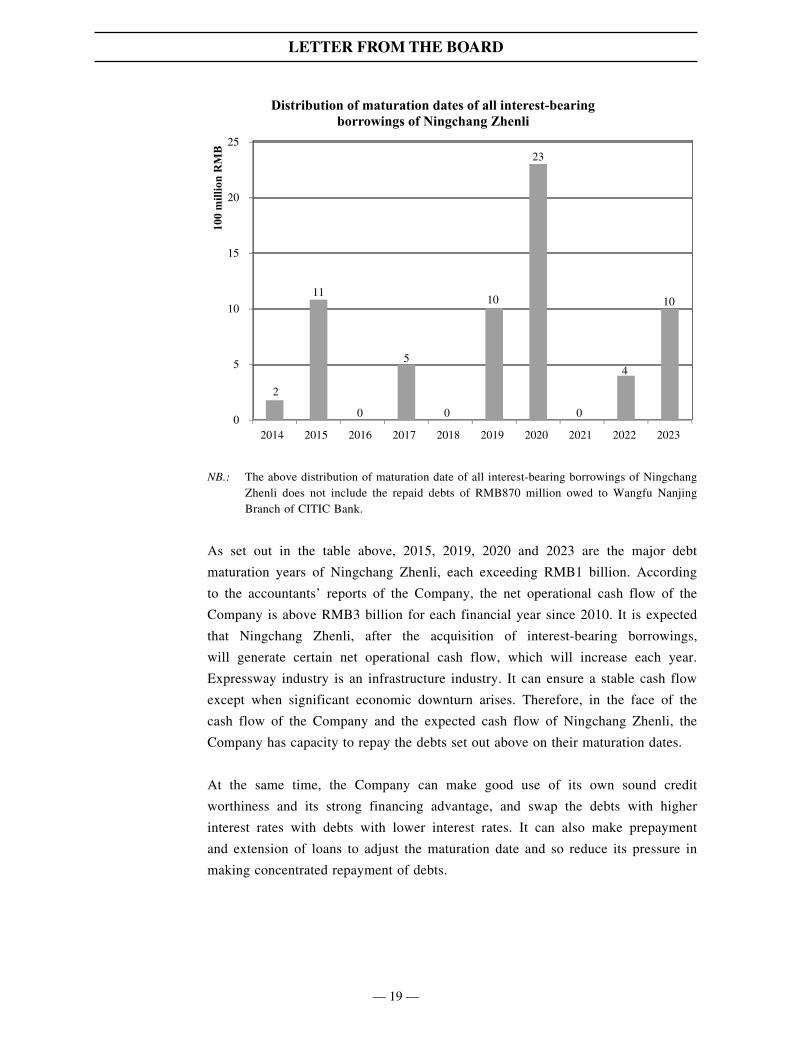

2

11

0 0 0

5

10

23

4

10

0

5

10

15

20

25

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

100

mill

ion

RM

B

Distribution of maturation dates of all interest-bearing borrowings of Ningchang Zhenli

NB.: The above distribution of maturation date of all interest-bearing borrowings of Ningchang Zhenli does not include the repaid debts of RMB870 million owed to Wangfu Nanjing Branch of CITIC Bank.

As set out in the table above, 2015, 2019, 2020 and 2023 are the major debt

maturation years of Ningchang Zhenli, each exceeding RMB1 billion. According

to the accountants’ reports of the Company, the net operational cash flow of the

Company is above RMB3 billion for each financial year since 2010. It is expected

that Ningchang Zhenli, after the acquisition of interest-bearing borrowings,

will generate certain net operational cash flow, which will increase each year.

Expressway industry is an infrastructure industry. It can ensure a stable cash flow

except when significant economic downturn arises. Therefore, in the face of the

cash flow of the Company and the expected cash flow of Ningchang Zhenli, the

Company has capacity to repay the debts set out above on their maturation dates.

At the same time, the Company can make good use of its own sound credit

worthiness and its strong financing advantage, and swap the debts with higher

interest rates with debts with lower interest rates. It can also make prepayment

and extension of loans to adjust the maturation date and so reduce its pressure in

making concentrated repayment of debts.

— 20 —

LETTER FROM THE BOARD

(2) Xiyi Company

i. Basic Information

Name of corporation Jiangsu Xiyi Expressway Company Limited (江蘇錫宜高速公路有限公司)

Nature of corporation Limited liability company

Registered capital RMB824,170,000

Registered address 100 East Yunhe Road, Wuxi, the PRC

Legal representative Yang Fei (楊飛)

Business scope Approved business scopes: (Limited to operations by

branch organizations): transport of passengers and

goods, warehousing; sales of petroleum products; car

maintenance; accommodation, catering service; sales of

non-staple and other food; sales of tobacco; sales and

renting of publications.

General business scope: construction, maintenance and

management of Xiyi Expressway, collection of toll for

traffic access. (the following areas are limited to branch

organizations) design of, production of, agent for and

distribution of national advertisements; sales of textile

products, daily commodities (excluding explosives),

hardware, electrical equipment, chemicals (excluding

hazardous products) and car spare parts; sales of goods;

provision of enterprise management service.

**(For business scope which requires special approval,

approval should be obtained prior to operation)**

Date of incorporation 11 September 2000

— 21 —

LETTER FROM THE BOARD

ii. Description on ownership

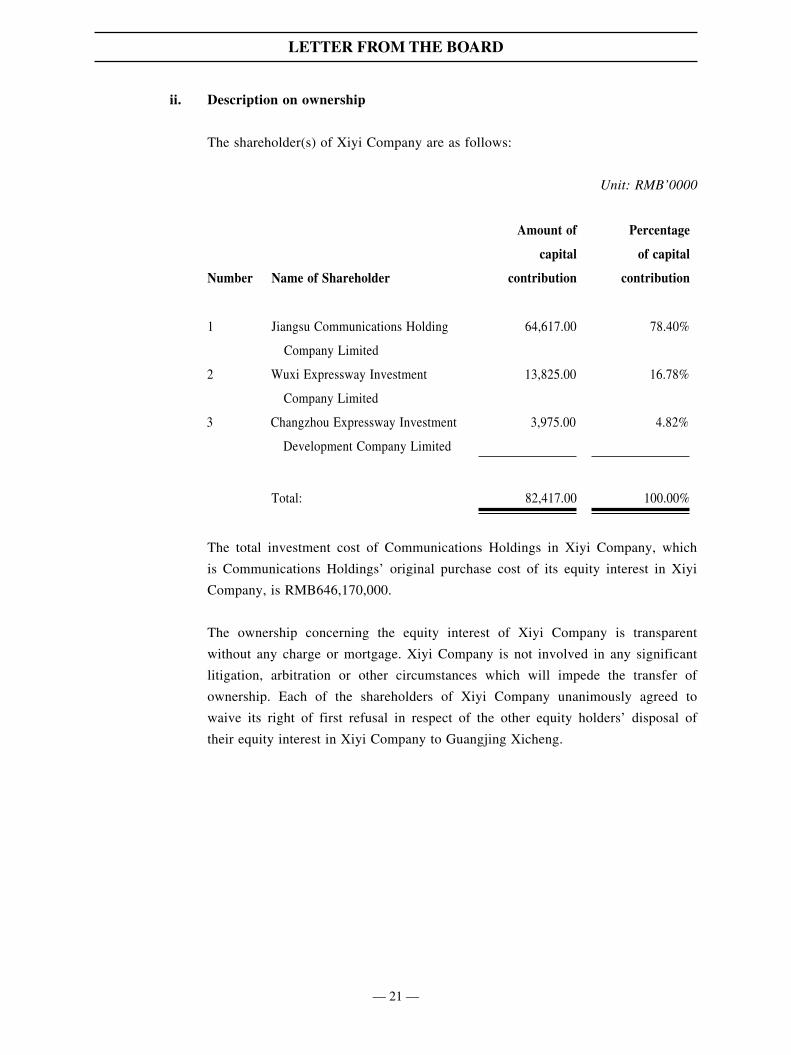

The shareholder(s) of Xiyi Company are as follows:

Unit: RMB’0000

Number Name of Shareholder

Amount of

capital

contribution

Percentage

of capital

contribution

1 Jiangsu Communications Holding

Company Limited

64,617.00 78.40%

2 Wuxi Expressway Investment

Company Limited

13,825.00 16.78%

3 Changzhou Expressway Investment

Development Company Limited

3,975.00 4.82%

Total: 82,417.00 100.00%

The total investment cost of Communications Holdings in Xiyi Company, which

is Communications Holdings’ original purchase cost of its equity interest in Xiyi

Company, is RMB646,170,000.

The ownership concerning the equity interest of Xiyi Company is transparent

without any charge or mortgage. Xiyi Company is not involved in any significant

litigation, arbitration or other circumstances which will impede the transfer of

ownership. Each of the shareholders of Xiyi Company unanimously agreed to

waive its right of first refusal in respect of the other equity holders’ disposal of

their equity interest in Xiyi Company to Guangjing Xicheng.

— 22 —

LETTER FROM THE BOARD

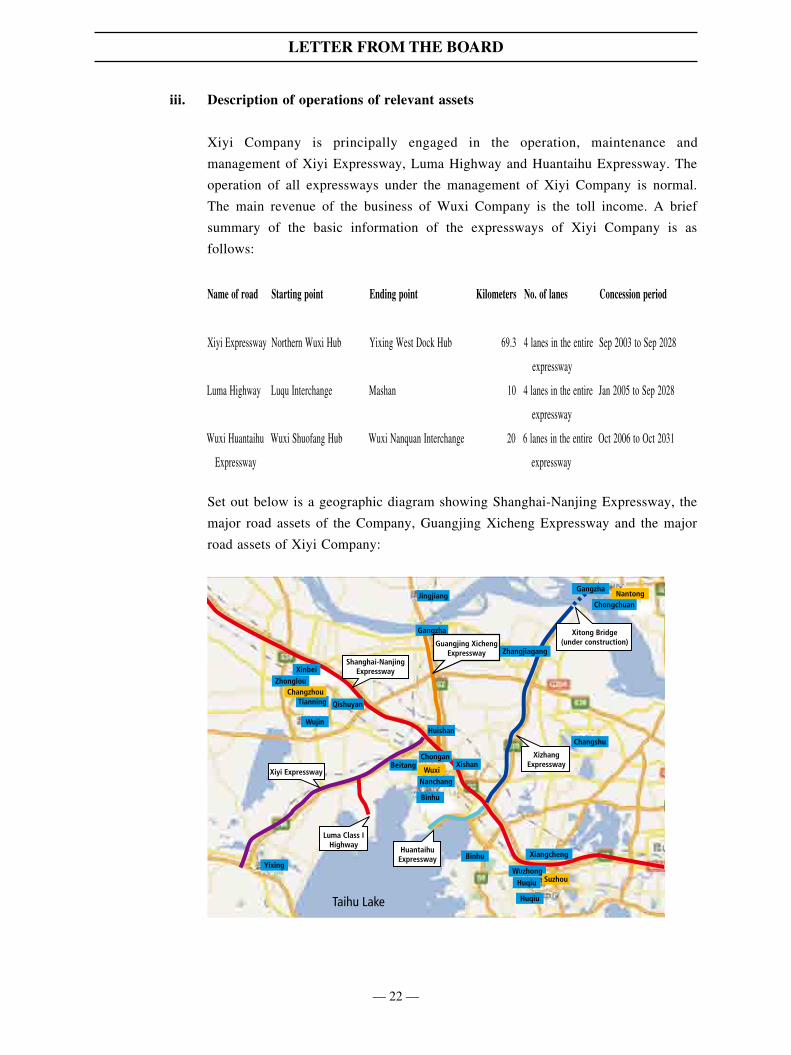

iii. Description of operations of relevant assets

Xiyi Company is principally engaged in the operation, maintenance and

management of Xiyi Expressway, Luma Highway and Huantaihu Expressway. The

operation of all expressways under the management of Xiyi Company is normal.

The main revenue of the business of Wuxi Company is the toll income. A brief

summary of the basic information of the expressways of Xiyi Company is as

follows:

Name of road Starting point Ending point Kilometers No. of lanes Concession period

Xiyi Expressway Northern Wuxi Hub Yixing West Dock Hub 69.3 4 lanes in the entire

expressway

Sep 2003 to Sep 2028

Luma Highway Luqu Interchange Mashan 10 4 lanes in the entire

expressway

Jan 2005 to Sep 2028

Wuxi Huantaihu

Expressway

Wuxi Shuofang Hub Wuxi Nanquan Interchange 20 6 lanes in the entire

expressway

Oct 2006 to Oct 2031

Set out below is a geographic diagram showing Shanghai-Nanjing Expressway, the

major road assets of the Company, Guangjing Xicheng Expressway and the major

road assets of Xiyi Company:

Taihu Lake

Xinbei

Tianning

Binhu

Binhu

Nanchang

XishanChongan

Huishan

Beitang

Zhonglou

Qishuyan

Gangzha

Gangzha

Chongchuan

Zhangjiagang

Jingjiang

Changshu

Xiangcheng

Huqiu

Huqiu

Wuzhong

Xiyi Expressway

Shanghai-NanjingExpressway

Guangjing XichengExpressway

XizhangExpressway

HuantaihuExpressway

Luma Class IHighway

Xitong Bridge(under construction)

Yixing

Wujin

Changzhou

Wuxi

Nantong

Suzhou

— 23 —

LETTER FROM THE BOARD

iv. Major financial data (Two years and nine months ended 30 September 2014)

In accordance of the audit report De Shi Bao (Shen) Zi No. S0210 (specific audit

report) (standard unqualified opinion)(on consolidated basis) of Xiyi Company

as prepared by Deloitte Touche Tohmatsu Certified Public Accountants LLP, a

licensed corporation to carry out equity and futures activities, the major financial

data of Xiyi Company for the years 2012 and 2013 and the nine months ended 30

September 2014 is as follows:

Unit: RMB’0000

(Audited)

Item

30 September

2014

31 December

2013

31 December

2012

Total assets 246,721.00 250,763.66 261,135.21

Total liabilities 180,784.32 184,485.86 192,057.14

Shareholders’ equity 65,936.68 66,277.80 69,078.07

Items Jan to Sep 2014 2013 2012

Income 20,762.84 26,274.31 25,214.53

Financial expenses 8,324.93 11,957.57 12,495.45

Profit –283.81 –2,798.29 –2,011.86

Net profit* –341.12 –2,800.27 –2,123.15

* Net profit before deduction of tax and non-recurring items = net profit after deducting taxes and non-recurring items

The concession rights of the expressways under the management of Xiyi Company,

with a book value of RMB2,300 million represented over 90% of the assets of

Xiyi Company as at 30 September 2014. The aggregate amortization was RMB482

million. In 2013, the annual amortization was RMB52 million. The amortization

during January to September 2014 was RMB50 million.

After the completion of the Transactions, Xiyi Company shall be consolidated

into the consolidated financial statements of the Company. The Company has not

provided any guarantee for Xiyi Company, and the Company has not appointed

Xiyi Company to manage its assets. No funds of the Company has been used by

Xiyi Company.

— 24 —

LETTER FROM THE BOARD

V. THE GENERAL PRINCIPLE AND METHOD FOR DETERMINING PRICE IN

AFFILIATED TRANSACTION/CONNECTED AND MAJOR TRANSACTION

i. The principle of price determination of the affiliated transactions

As the Transactions involve the disposal of state-owned assets, the prices of 100% equity

interests of Ningchang Zhenli and 100% equity interests of Xiyi Company have to be

determined based on the valuation prepared by Orient Appraisal, which is qualified to

advise on securities and futures transactions and the consideration will be determined upon

assessment after registration by the state-owned assets administrative departments. Orient

Appraisal has adopted the income approach in the valuation. It is finally determined that

the prices of 100% equity interests of Ningchang Zhenli is RMB502,000,000, and the

price of 100% equity interests of Xiyi Company is RMB662,000,000. On 8 January 2015,

the relevant transfers concerning state-owned assets were approved by the State-owned

Assets Supervision and Administration Commission of Jiangsu Province.

ii. Valuation for Connected and Major Transaction

Given the Transactions constitute a connected and major transaction and involve the

acquisition interests of infrastructure companies, the Company has instructed American

Appraisal to conduct an independent business valuation. American Appraisal has formed

a valuation opinion using the income approach (also known as discounted cash flow

approach) and the fair market value of the entire equity interest in business enterprise of

Ningchang Zhenli as at the valuation date (30 September 2014) was preliminarily valued

at approximately RMB522,000,000, whereas the fair market value of the entire equity

interest in business enterprise of Xiyi Company as at the valuation date (30 September

2014) was preliminarily valued at approximately RMB669,000,000. Pursuant to the Hong

Kong Listing Rules, such valuation reports will be regarded as profit forecasts and such

reports have been incorporated in this circular as Appendix IVA and Appendix IVB,

respectively. The key assumptions of the relevant valuation are as follows:

• no major changes are expected in the political, legal and economic conditions in

the PRC;

• industry trend and market conditions for toll road industry in the PRC will continue

to develop according to prevailing market expectations;

• there will be no major changes in the current taxation law and/or taxation rates

applicable to the relevant companies;

— 25 —

LETTER FROM THE BOARD

• the operation of the relevant companies will not be constrained by the availability

of finance;

• future exchange rates and interest rates movement will not differ materially from

prevailing market expectations; and

• the relevant companies will retain competent management, key personnel and

technical staff to support its ongoing operations.

Having considered that the underlying assumptions adopted in the valuation reports issued

by American Appraise are in line with the actual circumstances and are normally used in

valuing toll road projects, the Board considers that the use of such assumptions are fair

and reasonable. The Board further confirms that the relevant profit forecasts contained in

the valuation reports incorporated as Appendices IVA and IVB of this circular were made

after due and careful enquiry by the Board.

VI. DETAILS OF THE AGREEMENTS DATED 30 DECEMBER 2014

(1) Principal terms of the equity transfer agreement (the “Ningchang Zhenli Equity

Transfer Agreement”) between the Company and Communications Holdings and the

relevant arrangements on performance of the agreement:

Signatories Party A: the Company

Party B: Communications Holdings

Consideration and method

of payment

The Company shall pay a sum of RMB502,000,000 to

Communications Holdings as the consideration for the

acquisition of the entire shareholding of Ningchang Zhenli

that was held by Communications Holdings. The Company

shall pay the share transfer payment to Communications

Holdings by way of cash within 30 working days after this

equity transfer agreement becomes unconditional.

Profit and loss and

arrangements during the

transitional period

The period between the date immediately following the

valuation date of Ningchang Zhenli (30 September 2014) in

relation to this transfer of equity interest and the completion

date of the transfer of such equity shall be the transitional

period.

— 26 —

LETTER FROM THE BOARD

The transaction price of this transfer of equity interest shall

be the asset valuation results of Ningchang Zhenli using the

income approach. In light of this, the parties confirm that

the profit and loss of Ningchang Zhenli arising during the

transitional period will be enjoyed or borne by the Company.

Conditions precedent (1) This agreement and the transaction and transaction

price contemplated hereunder having been approved

by the shareholders in the general meeting of the

Company.

(2) The transaction under this agreement having been

approved or registered by the state-owned assets

management department.

(3) All conditions precedent under the Debt Transfer

Agreement between the Company and Ningchang

Zhenli having been satisfied.

Liability of Breach Upon this agreement becomes unconditional, the parties

shall actively perform their obligations. Any action in breach

of a provision of this agreement will constitute a default.

Defaulting party shall compensate the non-defaulting party

accordingly.

(2) The principal terms of the debt transfer agreement (the “Debt Transfer Agreement”)

between the Company and Ningchang Zhenli:

Signatories Party A: the Company

Party B : Ningchang Zhenli

Completion date of

the transfer of debts

The date of registration of the relevant business registration

procedures as stipulated under the Ningchang Zhenli Equity

Transfer Agreement entered into between the Company and

Communications Holdings shall be the completion date of

the transfer of debts under this agreement.

— 27 —

LETTER FROM THE BOARD

Debts to be transferred The parties confirm that, at the completion date, all the

interest-bearing borrowings of Ningchang Zhenli shall be

transferred to the Company. These do not include interest-

bearing borrowings and interest accrued that became due but

remained unpaid at the completion date. The due but unpaid

borrowings and interest accrued as at the completion date

shall continue to be borne by Ningchang Zhenli.

Arrangement during the

transitional period

(1) The parties confirm that, the period between the date

immediately following 30 September 2014 and the

completion date shall be the transitional period.

(2) The amount of debt to be transferred between the

parties shall be the actual amount of all interest-

bearing borrowings of Ningchang Zhenli at the

completion date. The interest-bearing borrowings

which are voluntarily repaid by Ningchang Zhenli

during the transitional period shall not to be borne

by the Company; whereas any new interest-bearing

borrowings incurred by Ningchang Zhenli during the

transitional period shall be borne by the Company in

accordance with this agreement.

(3) Before the completion date, apart from the existing

creditors, Ningchang Zhenli shall not borrow any

loans from third parties.

(4) During the transitional period, Ningchang Zhenli

shall carry out financing according to the principle of

reasonableness and appropriateness, and shall ensure

that the total amount of interest-bearing borrowings

shall not exceed RMB7,500 million.

(5) The parties shall confirm the principal amount of

all interest-bearing borrowings to be transferred by

written confirmation on the completion date.

— 28 —

LETTER FROM THE BOARD

Method of Transfer

of debts and

limitation period

The parties confirm that, at the completion date, the

Company shall enter into loan agreements and related

supplementary agreements with the creditors in respect of

the transfer of all interest-bearing borrowings pursuant to

the terms of this agreement. The terms and conditions of

the loan agreements shall be determined through amicable

negotiations between the Company and the creditors. At such

time, the loan agreements between Ningchang Zhenli and the

creditors shall cease to have effect simultaneously.

Arrangements for charge,

pledge and guarantee

Ningchang Zhenli undertakes that, in respect of the pledges

of the concession right for the subsisting debts to be

transferred, to the extent that they are provided by Ningchang

Zhenli and remain effective, Ningchang Zhenli shall continue

to bear its obligation concerning such pledge in favour of

the creditors in accordance with the original agreements. In

respect of guarantees provided by Communications Holdings,

so long as the guarantee periods subsist, Communications

Holdings shall continue its obligations and comply with the

terms under the original guarantee documents and continue

to provide the guarantees.

Conditions precedent (1) This agreement, the transfer of debts and the amount

to be transferred as contemplated under this agreement

having been approved by the shareholders in the

general meeting of the Company.

(2) All conditions precedent under the Ningchang Zhenli

Equity Transfer Agreement between the Company and

Communications Holdings having been satisfied.

Liability of Breach Upon this agreement becomes unconditional, the parties

shall actively perform their obligations. Any action in breach

of a provision of this agreement will constitute a default.

Defaulting party shall compensate the non-defaulting party

accordingly.

— 29 —

LETTER FROM THE BOARD

(3) The principal terms of the profit compensation agreement (the “Profit Compensation

Agreement”) between the Company and Communications Holdings in respect of the

affiliated transaction of Ningchang Zhenli:

Signatories Party A: the Company

Party B: Communications Holdings

Compensation Period Given that the acquisition of Ningchang Zhenli is expected

to be completed within year 2015, Communications Holdings

agreed that the compensation period and period of guarantee

of responsibility shall be three accounting years, from 2015

to 2017.

Profit forecast and

computation of amount

According to the Affiliated Transactions Guidelines and

other relevant regulations issued by the Shanghai Stock

Exchange, given that the consideration for the entire equity

interests of Ningchang Zhenli is based on the valuation

result using the income approach, and exceeds its net book

value by over 100%, within the three accounting years after

the completion of the current transactions, Communications

Holdings is required to compensate the Company for the

shortfall of the actual profit from the profit forecast. Orient

Appraisal has issued Hu Dong Zhou Zi Ping Bao Zi [2014]

No. 0922044 “Asset Valuation Report” to project the net

profit of Ningchang Zhenli after deducting non-recurring

gains and losses in years 2015, 2016 and 2017.

Given that after the completion of the acquisition, the

Company shall bear all interest-bearing borrowings of

Ningchang Zhenli, this will cause major changes between the

actual operations of Ningchang Zhenli and the assumptions

in the abovementioned Asset Valuation Report and therefore

lead to a major difference in the actual net profit of

Ningchang Zhenli and the predicted net profit income tax

and financial expenses set out in Asset Valuation Report.

— 30 —

LETTER FROM THE BOARD

The parties confirm that, Communications Holdings

shall, in respect of the compensation period, guarantee

Ningchang Zhenli’s profit before tax and financial expenses

after deducing non-recurring gains and losses, such that

it shall not be less than RMB230,434,300 in 2015, not

less than RMB269,083,700 in 2016 and not less than

RMB299,931,100 in 2017. Such guaranteed amounts are

consistent with the projected profits before tax and financial

expenses after deducting non-recurring gains and losses set

out in the Asset Valuation Report.

Computation of

compensation amount

After the end of each accounting year during the

compensation period, the Company shall instruct an

accounting firm with securities qualification to carry out

annual auditing of the Company and at the same time, issue

specific audited report to confirm the actual profit before tax

and financial expenses after deducting non-recurring gains

and losses achieved by Ningchang Zhenli.

Compensation method and

arrangement

If Communications Holdings is required to make any profit

compensation, Communications Holdings shall compensate

the Company such shortfall amount in the profit in cash,

within 30 days after the specific audit report is issued.

Conditions precedent (1) All conditions precedent under the agreement on

which the transaction and the transaction price are

based having been satisfied, which means that the

Ningchang Zhenli Equity Transfer Agreement between

the Company and Communications Holdings having

taken effect and the Debt Transfer Agreement between

the Company and Communications Holdings becomes

unconditional.

(2) The relevant business registration in respect of the

capitalisation of the debt against Ningchang Zhenli as

a result of the transfer of interest-bearing borrowings

to the Company from Ningchang Zhenli having been

completed.

— 31 —

LETTER FROM THE BOARD

Liability of Breach Upon this agreement becomes unconditional, the parties

shall actively perform their obligations. Any action in breach

of a provision of this agreement will constitute a default.

Defaulting party shall compensate the non-defaulting party

accordingly.

(4) The principal terms of the three equity transfer agreements (collectively, the “Xiyi

Company Equity Transfer Agreements”) entered into between Guangjing Xicheng, a

subsidiary of the Company, and Communications Holdings, Changzhou Expressway

and Wuxi Expressway, respectively, in relation to the acquisition of Xiyi Company:

Signatories Party A: Guangjing Xicheng

Party B: Communications Holdings,

Changzhou Expressway, Wuxi Expressway

Consideration Guangjing Xicheng shall pay a sum of RMB519,010,000

to Communications Holdings as the consideration for

the transfer of the 78.40% of the equity interest of Xiyi

Company held by Communications Holdings, a sum

of RMB31,910,000 to Changzhou Expressway as the

consideration for the transfer of the 4.82% of the equity

interest of Xiyi Company held by Changzhou Expressway

and a sum of RMB111,080,000 to Wuxi Expressway as the

consideration for the transfer of the 16.78% of the equity

interest of Xiyi Company held by Wuxi Expressway.

Guangjing Xicheng shall pay Communications Holdings,

Changzhou Expressway and Wuxi Expressway the relevant

consideration by way of cash within 30 working days after

these agreements become unconditional.

Arrangements during

the transitional period

The period between the date immediately following the

valuation date of the target company (30 September 2014) in

relation to this transfer of equity interest and the completion

date of the transfer of such equity shall be the transitional

period.

The transaction price of this transfer of equity interest

has adopted the results from the asset valuation on Xiyi

Company using the income approach. In light of this, the

parties confirm that the profit and loss of Xiyi Company

arising within the transitional period will be enjoyed or

borne by Guangjing Xicheng.

— 32 —

LETTER FROM THE BOARD

Conditions precedent (1) As part of the significant affiliated transaction of the

Company, these agreements and the transactions and

the transaction prices contemplated hereunder having

been approved by the shareholders in the general

meeting of the Company.

(2) The transaction contemplated under these agreements

having been approved or registered by the state-owned

assets management department.

Liability of Breach Upon these agreements become unconditional, the parties

shall actively perform their obligations. Any action in breach

of a provision of these agreements will constitute a default.

Defaulting party shall compensate the non-defaulting party

accordingly.

(5) The principal terms of the absorption and merger agreement (the “Absorption and

Merger Agreement”) entered into between Guangjing Xicheng, a subsidiary of the

Company and Xiyi Company in relation to the merger:

Signatories Party A: Guangjing Xicheng

Party B: Xiyi Company

Method of absorption and

merger

Guangjing Xicheng shall transfer all assets, liabilities,

business and personnel of Xiyi Company to Guangjing

Xicheng. Upon the absorption and merger, Guangjing

Xicheng, as the absorber, will continue to exist and Xiyi

Company, as the absorbee, will cease to exist.

Arrangement of credit and

debt

After approvals have been obtained from the board of

directors and the shareholders of Xiyi Company, Xiyi

Company shall carry out notification and announcement

procedures in respect of the creditors according to the legal

requirements. With effect from the date of deregistration

of Xiyi Company with the relevant State Administration

of Industry and Commerce, Guangjing Xicheng shall be

responsible for those debts which creditors fails to petition

for early repayment or provision of guarantee by Xiyi

Company within statutory period.

— 33 —

LETTER FROM THE BOARD

Conditions precedent (1) As part of the significant affiliated transaction of the

Company, this agreement and the transaction and the

transaction price contemplated hereunder having been

approved by the shareholders in the general meeting