Embed Size (px)

Citation preview

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

COMMODITY EXCHANGE MARKETS AND ECONOMIC DEVELOPMENT

BY

Eleje, Edward Ogbonnia , Josaphat, U.J. Onwumere (Ph.D), Nwokeji, N. N. C. Department of

Banking and Finance, University of Nigeria, Enugu Campus, Enugu, Nigeria

ABSTRACT

The pursuit of economic development has remained a major issue of concern to economists,

government officials, and the interested public. Many countries have approached it from varying

perspectives, involving often, a package of policies/strategies. One of these has been the angle of

commodity exchange market. This work appraises commodity exchange markets and their

roles/challenges in economic development from local and global view points.

Key Words: Commodity exchange markets, economic development

1.0 Introduction

The concept „economic development‟ has been approached in various dimensions. It has in some

cases been used interchangeably with economic growth (Todaro and Smith, 2003). Unarguably,

however, economic growth has a narrower scope. Economic growth is a rise in the productive

capacity of a country on a per capita basis. It involves the expansion of the economy through a

simple widening process (Eleje and Emerole, 2010). It is the increase in the national output or

GDP of the nation (Hogendorn, 1992). Economic development on the other hand is broder. Idam,

(2007) argues that economic development involves economic growth plus sustained structural

changes that enhance the living standard of the wider segment of the society. According to Hla

and Krueger (2009) economic development is the increase in the standard of living in a nation's

population with sustained growth from a simple, low-income economy to a modern, high-income

economy. Also, if the local quality of life could be improved, economic development would be

enhanced. Its scope includes the process and policies by which a nation improves the economic,

political, and social well-being of its people (O'Sullivan & Steven; 2003).

The commodity markets espacially in developing countries have become such a crucial issue in

any discuss of the pace and pattern of economic development. It has moved from the periphery

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

of nations‟ growth mechanism to a potentially dominant position as an important engine of

economic transformation. In Nigeria for instance, increased emphasis on agricultural production

and improvement in the productive base of small and medium sized enterprises have come to

constitute the major driving force in the nation‟s development process. The post civil war era of

economic reconstruction offered an opportunity for the nation to correct past lapses in the

management of the industrial and commercial sectors. It also provided the avenue for putting the

nation‟s developmental programmes on a stronger and more rational basis. This is particularly

important because Nigeria is now moving away from the easier early phases of industrialization

to a more demanding second generation phase of basic structural change (Onwumere, 2000).

This calls for a proper conceptualization of the nature, roles and contributions of the commodity

market to economic development.

2.0 Meaning of Commodity Exchange Market (Comex)

A commodity market is a market were commodities are bought and sold (ASCE, 2006). It is the

only market that has existed almost throughout the history of mankind. Trading in commodities

has evolved from barter sessions organized on town marketplaces in absence of any monetary

vehicle to a commodity exchange; a contemporary sophisticated and more complex organization

of futures and other derivatives markets (Eleje and Okafor, 2010). The commodity exchange

markets are the organized markets of buyers and sellers of various specified commodities. Such

markets have specific locations, specific rules, regulations, and procedures.

According to the Abuja Securities and Commodities Exchange (2005), a commodity exchange is

any organization providing facilities for registered commodity brokers to trade in commodities,

financial instruments and their derivatives. The united state security and exchange commission,

posits that any organization, association, or group of persons whether incorporated or not which

constitute, maintains and provides a market place or facilities for bringing together buyers and

sellers of commodities is a commodity exchange. Onoh (2002) has argued that there are two

types of commodity exchange; the simple commodity exchange, where farm commodities,

minerals, metals, stocks, bonds, and all forms of financial derivatives are traded and paid for, and

the futures market where futures contracts are bought and sold. The simple commodity exchange

is a spot or cash market where transactions are for immediate payment and delivery. Good

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

examples of this type include the America Exchange (AMEX), the London International

Petroleum Exchange (LIPC) and the Abuja Securities and Commodity Exchange (ASCE).

3.0 Evolution of Commodity Exchange Markets

Commodities have in recent times become major asset instrument for individual investors,

pension funds and other institutional operators especially in the developed countries. The genesis

of this is often traced to the ancient days of the great Greek philosopher, Thales, as narrated by

Aristotle (Eleje, 2009). However, historians have traced the origin of commodity and futures

exchange to the trade fairs of medieval Europe at which, the medieval traders conceptualized the

use of a bill of exchange which was similar to a warrant but which was termed “fair letter”. The

fair letter represented the goods traded which would be settled at a later date upon delivery in the

city of residence of the seller (Gorton, 2004). The first remarkable centre for commodity and

futures trading in Europe developed in Antwerp in the early 16th

century. It later spread to other

European towns and cities including London which later turned out to be the meeting point of

commodity traders. Growth in business activities eventually led to the establishment of terminal

markets like Garro-Ways Coffee House and the London Commercial Sales Room in 1670 and

1811 respectively. The need for standardization of contracts and delivery terms, with the aim to

increase transaction, gave rise, in the next century, to the first two standard Exchanges namely:

the New York Cotton Exchange (1842) and the Chicago Board of Trade (1848). Further progress

in the development of terminal markets was made possible soon after the introduction of

standardized grades of certain commodities and the greater use of warrants. Overtime,

commodity exchanges have grown in number and volumes of transactions in Europe, South

America, North America, Asia, and currently in Africa.

In Nigeria, early attempts to formalize commodity marketing dates back to the 1930s when

European companies including the United African Company (UAC), John Holt, Societe

Commerciale Occidentale Agency (SCOA) and Peterson Zochonis (PZ) were directly involved

in purchases and exports of Nigeria‟s major agricultural commodities which were essential raw

materials for overseas‟ industries (Eleje and Okafor, 2010). Government involvement in

organized commodity marketing started during the Second World War, when the West African

Produce Control Board (WAPCB) was established in 1942 to stabilize commodity prices. With

the scrapping of the Commodity Boards via the Structural Adjustment Programme (SAP) in

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

1986, the federal government of Nigeria took the first giant stride to establish a commodity

exchange and futures market in Nigeria. This followed the setting up of an inter-ministerial

technical committee at the behest of the Central Bank of Nigeria (CBN) in 1989 to study the

feasibility of establishing a Futures Exchange for agricultural commodities to frontally address

the agro-commodity marketing problems. Series of efforts were embarked upon thereafter. The

conversion of the short-lived and controversial Abuja Stock Exchange into a commodity and

futures exchange (Comex) on August 8, 2001 was a much-expected fillip to the promotion of the

non-oil exports for economic development. It was a decision widely lauded by industry experts.

The new Comex was subsequently brought under the supervision of the Federal Ministry of

Commerce and Industry. The conversion was premised on the need for an alternative

institutional arrangement that would manage the effect of price fluctuations in the marketing of

agricultural produce which has negatively affected the earnings of farmers since the abolition of

the Commodity Boards. The Comex commenced spot market trading on July 25, 2006. It has a

21-members council which was inaugurated, a day after the commencement of trading.

4.0 Structure and Grouping of Commodities in Commodity Exchange Markets

Commodity exchanges are similar in a way to the stock exchanges. They are the organized

trading floors for commodities just as the stock exchanges are the organized trading floors for

stocks and other financial instruments (Nwaneri; 2000). Commodity dealers are not individuals

but corporate citizen who must be duly registered by the Corporate Affair Commission (CAC)

and the Securities and Exchange Commission (SEC). Besides, the company‟s MEMART must

authorize it to engage in commodity trading and it‟s chief operating officer must be sufficiently

proficient in commodity business (ASCE, 2006). The company must have at least one qualified

commodity broker who must have passed qualifying examinations of a relevant examination

body. However, in countries where the commodity exchange is still novel like Nigeria, qualified

stockbrokers can be registered on the exchange to trade in commodities until such country

establishes her examining body. Farmers, commodity merchants, commodity processors like

food and beverages companies as well as others involved in commodity business often make use

of the commodity exchange. However, there are minimum contract sizes for transactions which

can be traded on the exchange. Commodity exchanges composed of member-traders authorized

to buy and sell spots and derivative contracts. These members could be categorized into three

namely:

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

Member–traders who trade for themselves;

Member–traders who trade for themselves and others; and,

Member–traders who trade for themselves and others for a commission or fee (i.e.

commodity brokers).

The trading floor of a commodity exchange is where buyers, sellers, and the exchange governing

board meet to set and enforce rules and regulations for orderly trading and delivery of

commodities. The trading floors and the trading pits are equally where actual trading occur and

as such, they constitute the most visible aspect of the exchange (CBOT; 1989). A very

significant but less visible component of commodity exchange is the communication network

which links brokers worldwide with traders in the pits. The commodity trading floor is a physical

location, but it represents a worldwide market. There is also subtle specialization in the various

commodity exchanges all over the world.

Commodity exchanges are closest to the theoretical perfectly competitive market. Evidence is

with respect to constant availability of daily price quotations of tradable assets both in the print

and in electronic media. An up-to date minute reports on exchange prices are also available in

the office of most commodity brokers and in Reuter services like commodities 2000 and

Equities 2000 (CFTC;2004). The commodity exchanges operate a 24hour market. At any point

in time, there are thousands of buyers and sellers of commodity contracts participating in the

market and establishing prices through open trading on the floor of the exchange. Clients‟

participation is via their brokers who report to them directly or through electronic media. It is

often very difficult if not impossible to manipulate contract prices in the exchanges. This is

because most information relating to contract prices are timely published and made to circulate

worldwide. Commodity exchanges have warehousing facilities. A warehouse is a building

constructed for storage of commodities such as manufactured goods, agricultural produce, and

metals. It may either be public or private depending on ownership and management.

In most exchange markets where commodity futures or spots are traded, certain specialization is

prevailing. For example, at the Chicago Board of Trade (CBOT), agricultural commodity futures

and options having as underlying wheat, corn, oat, rice, soyabeans, soyabeans meal, ethanol, as

well as metals like gold and silver are traded. At the New York Mercantile Exchange (NYMEX),

the agricultural commodities are represented by wheat, corn syrup, and Orange juice; metals are

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

represented by copper; while energy is represented by crude oil, heating gasoline, natural gas,

and electricity. The Chicago Mercantile Exchange (CME) trades futures on dairy products like

butter and several types of milk. Other commodities include pork bellies, live stocks, lean hogs,

ethanol and timber. In Europe, the London International Financial Future Exchange

(EURONEXT- LIFFE) trade futures and option on sugar, Cocoa, Coffee, wheat and corn. In

developing countries such as Nigerian, most spot transactions are with respect to primary

agricultural commodities including Benniseed, Cocoa, Coffee, Tea, Cotton, Groundnut, Ginger,

Palm Kernel, Palm Oil, Soya Bean, Rubber, Cashew nut, and Wheat (Eleje; 2008). Generally,

tradable commodities in commodity exchanges could be typologically classified into:

Commodity Type Commodity Group

Energy Crude oil, Heating oil, gasoline, Natural gas, Electricity

Metals Gold, Silver, Platinum, Copper, Aluminum

Forest products Timber, Pulp

Textiles Cotton

Food stuffs Cocoa, Coffee, Orange Juice, potatoes, Sugar

Livestock Pork, Beef

Oil and meal Soya Bean

Grains Corn, Oats, Rice, Wheat. Source: Department Matematica DMAD (2008)

5.0 Trading Process and Collateral Management in Commodity Exchange Markets

In every trade, there is a buyer and a seller operating in a market existing anywhere or

somewhere at every level of the society, at any point in time. Such is the same with trading in

Comex. The difference however is that in Comex, the buyer and the seller do not engage in

direct transaction. Instead, they initiate their trading decisions through agents called the

commodity brokers. The buyer will approach his broker with a „buy‟ instruction while the seller

will do same with a „sell‟ instruction (ASCE, 2005). Both agents (brokers) will strike the trading

deal unbehalf of their clients (buyer/seller) either physically in the trading floor of the exchange

or through electronic means.

In physical trading, both brokers will come to the floor of the exchange to trade base on the

instructions from their clients. The exchange‟s trading engine will match the trade on price-time

priority bases. If the trade is matched, the buyer and the seller have a firm obligation to honor

their commitments if they leave their positions open till maturity (MSPDD, 2005). In electronic

trading on the other hand, trading occurs through computer network facilities. A centralized

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

computer will proceed to Match bids and offers on price–time priority basis making it obligatory

for the buyer and the seller to exercise their position at maturity (UNCTAD; 2005). Compared to

the open outcry system (physical trading), electronic trading connotes two basic advantages. One

is that trading is not necessarily restricted to time Limit. Invariably, trading is continuous round-

the-clock. Another advantage is that brokers who are directly involved in trading need not be

physically present on the trading floor of the exchange, but anywhere in the world in-as-much–as

they are connected online. These two advantages encouraged Chicago Board of Trade (CBOT),

Chicago Mercantile Exchange (CME), and Reuters holding Plc to develop a 24-hour global

electronic automated transaction system for futures and options trading on September 2, 1987

(GLOBEX, 1989). Since then, several other exchanges have developed alternative systems.

One major disadvantage of electronic trading system is inadequate “locale” Opportunities.

Locales depend to a large extent on their ability to interpret what they hear and see around them

and on their relations with others in the trading ring. A computer-based system definitely makes

trading unattractive to locales. Since locales provide a large proportion of the intra-day liquidity

on commodity exchanges, their disappearance will likely result in traders having more problems

in closing deals and thus obliged to accept less attractive prices. Another major problem of

electronic trading is the tendency of manipulation. A 24-hour trading certainly will be

characterized by two periods of high and low trading activities. Hence, at that period when

trading activity and liquidity are low the market can be easily manipulated (Gorton; 2004). The

table below is a prototype of electronic commodity trading system:

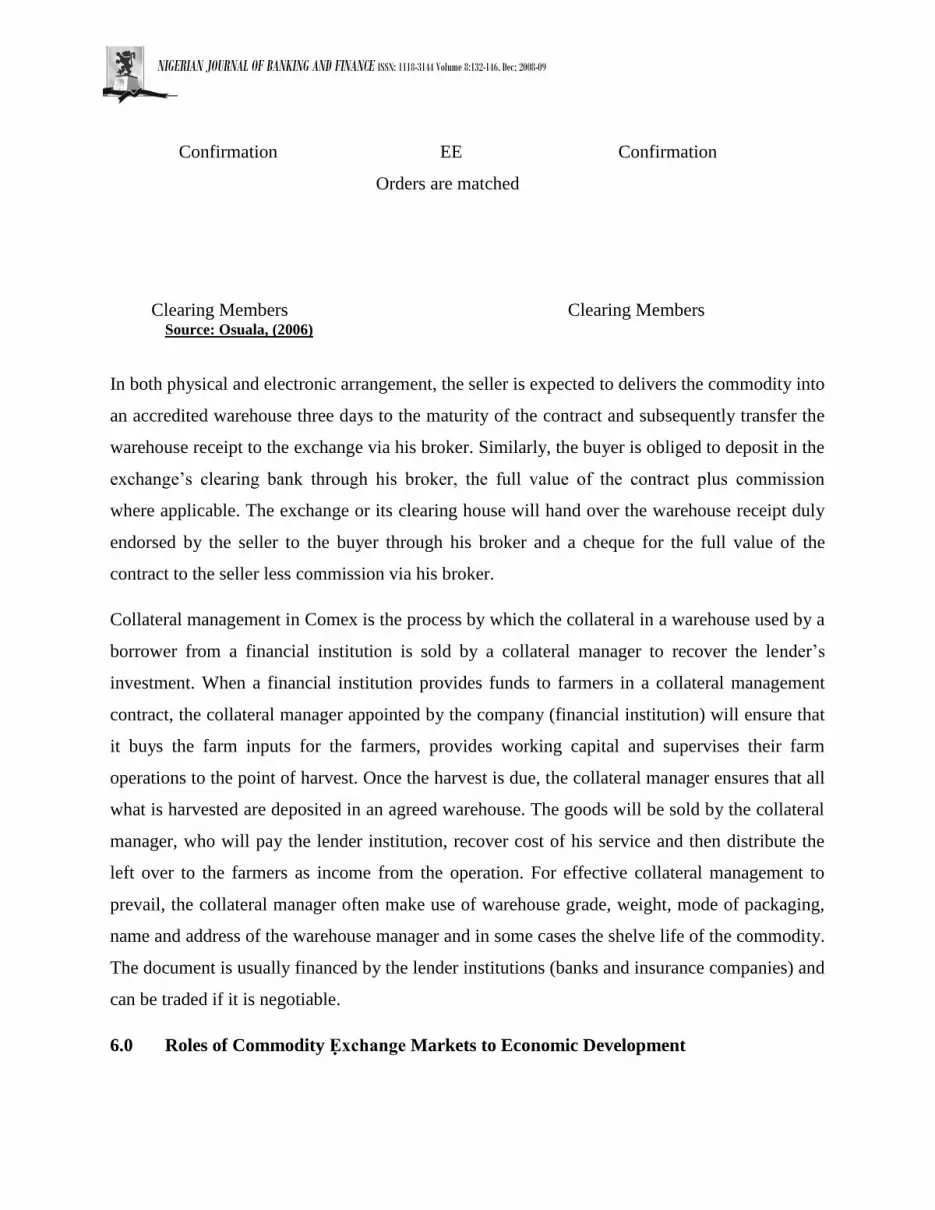

FIGURE 1: A COMPUTER–BASED COMMODITY TRADING SYSTEM

Order input Order input

Verification of order Verification of order

Legitimate Orders are Legitimate orders are

transferred transferred

Buyer Seller

Computer Computer

Check credit Risk Check credit Risk

Execution

Clearing House

Electronic

Trading

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

Confirmation EE Confirmation

Orders are matched

Clearing Members Clearing Members Source: Osuala, (2006)

In both physical and electronic arrangement, the seller is expected to delivers the commodity into

an accredited warehouse three days to the maturity of the contract and subsequently transfer the

warehouse receipt to the exchange via his broker. Similarly, the buyer is obliged to deposit in the

exchange‟s clearing bank through his broker, the full value of the contract plus commission

where applicable. The exchange or its clearing house will hand over the warehouse receipt duly

endorsed by the seller to the buyer through his broker and a cheque for the full value of the

contract to the seller less commission via his broker.

Collateral management in Comex is the process by which the collateral in a warehouse used by a

borrower from a financial institution is sold by a collateral manager to recover the lender‟s

investment. When a financial institution provides funds to farmers in a collateral management

contract, the collateral manager appointed by the company (financial institution) will ensure that

it buys the farm inputs for the farmers, provides working capital and supervises their farm

operations to the point of harvest. Once the harvest is due, the collateral manager ensures that all

what is harvested are deposited in an agreed warehouse. The goods will be sold by the collateral

manager, who will pay the lender institution, recover cost of his service and then distribute the

left over to the farmers as income from the operation. For effective collateral management to

prevail, the collateral manager often make use of warehouse grade, weight, mode of packaging,

name and address of the warehouse manager and in some cases the shelve life of the commodity.

The document is usually financed by the lender institutions (banks and insurance companies) and

can be traded if it is negotiable.

6.0 Roles of Commodity Ẹxchange Markets to Economic Development

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

Commodity exchange markets are integral part of the economic system. They constitute that part

of efficient capital market that allows users to invest on commodities including agricultural

products, petroleum, solid minerals, and other precious materials. Their roles in the economic

development of any nation are very significant. These roles are with respect to the following:

(a) Price discovery: Another major role of the commodity markets to economic development is

percieved from their price discovery function. Price discovery is the process of providing

equilibrium prices that reflects current and prospective demands on current and prospective

supplies and making these prices visible to all (Jorion, 1995). Commodity markets are important

not only in terms of the actual trading that takes place, but also because they guide the rest of the

economy to optimal production and consumption decisions. Higher future prices for storable

commodities signal the need for greater production and storage thus smoothing the supply of a

product over time and helping to avoid over-and under-supply conditions. In a survey on the

reaction of primary commodity dealers, Peck (1985) in Eleje (2008) documented that stocks of

Corn are quite responsive to changes in storage costs implicit in futures prices. Between 1971

and 1981, the United States, the only exporter with an active grain futures market, was the least

destabilizing major exporter in the world commodity market. Thus commodity futures markets

help to stabilize prices by facilitating optimal production and storage decisions of firms.

Price discovery process is equally beneficial in other respects. Miller (1991) documented

reduction in search costs, availability of reference prices for similar commodities, and volatility

discovery. By going to an exchange, one has direct access to centralized competitive trading,

which ensures that the price will be fair. Thus, costly searches are eliminated. Commodity

futures contracts, for example, cotton futures create one reference price. This price can be used to

derive the fair value of individual stocks of cotton thereby avoiding multitude of cash prices

arising from quality differences. Again, the traditional option pricing model (Black and Schole;

1973) can be used to recover an “implied” volatility from the option price (Eleje, 2010). This

volatility is the market assessment of the possible range of values for commodity price over the

life of the option. Hence, knowing the volatility of exchange rate will enable exporters to infer a

distribution of future exchange rates and access worst-case scenario to enable them decide

whether the risk should be hedged or not.

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

(b) Risk management: Commodity markets offer innovations in risk management, not in risk

itself. Risk exists because there is uncertainty in the world. Commodity markets are crucial

because while they provide platform for buying and selling of commodities, they also provide

the possibility of effective risk management through hedging (Eleje and Modebe, 2010). Hedgers

use derivatives contracts provided by the market to shift unwanted price risk to others just like

speculators who willingly assume risks in order to make profits or traders with different risk

profiles. The presence of the derivatives instruments in the commodity exchange markets makes

the management of trade risk easier and more efficient. One misconception about derivatives

however, needs clarification at this juncture. Commodity derivatives are sometimes associated

with gambling. This is misleading. Gambling entails the assumption of newly created risks while

derivatives contract involves speculations which entails the assumption of existing risks and

must be viewed as the necessary counterpart to hedging.

(c) Transactional efficiency: The work of Fabozzi et al (1994) shows two components of

transactional efficiency in the commodity markets. They include low cost of operations, and

absence of bureaucratic arrangement. These factors are expanded in Jorion (1995) under cost

savings and liquidity functions. By reducing cost of transacting in real cash markets, commodity

derivatives markets could induce cost savings to traders and other investors in the market.

Besides, liquidity measures the ease and speed with which transactions can be executed in a

market situation. Hence, eliminating undue conditionalities and bureaucratic arrangements

guarantees a more liquid market where customers who have positions can feel confident that they

can exit the market anytime.

(d) Allocation of capital: Commodity markets also have a positive effect on capital allocation.

A fully developed commodity exchange as earlier emphaszed incorporates the derivatives market

where commodity risks can be hedged against market uncertainties. A dealer in commodity

exports who envisages a bounty supply of profitable products in the near future is faced with

market price risk. In addition, such investor faces substantial financial risk due to movement in

inflation, movement in future interest payment on borrowed fund, and the possibility of foreign

exchange rate changes. Commodity derivatives can increase the willingness of such investor to

invest under the above risky conditions. This is possible since the market mechanism will

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

provide him opportunity to be protected against the commodity price risk and the other market

uncertainties.

(e) Accumulation of capital: Commodity derivatives market also has a positive effect on

accumulation of capital. By reducing the firms cost of financial distress, commodity derivatives

market induces firms to increase debt capacity and interest tax shield. Such inducement boosts

firms‟ capability to carry its investment and financing functions effectively. Besides, the

economic growth of a country is driven by improvement in productivity resulting from

investment in the diverse sector of the economy. In a closed economy, the total pool of

investment derives from national savings. In such scenario, investment will be less than savings

because of frictions, or costs, in the financial system. Reducing these frictions, leads to a higher

level of investment and ultimately, of economic growth (Glen, 1993). In an open economy,

commodity markets may increase the inflows of foreign capital, given that some market risks can

be easily hedged, resulting in higher investment level.

7.0 Relevance of Commodity Exchange Markets to Economic Development

Commodity exchange markets provide numerous benefits to many societies most expecially, in

the developed societies where the values have been properly harnessed. Their relevance to

economic development cannot be overemphasized. They include among others the following:

(i) Efficiency of production decisions and diversification: A long range of empirical

studies including Hatakeda (Undated), Lensink, et al (1999/2000), Sarkar (2000) and Onwumere

and Eleje (2008/2010) documented that uncertainty has a negative impact on productivity and

therefore reduces growth. In agriculture, the main effect of price uncertainty is to reduce

production of the risky crop and to diversify (Newbery and Stiglitz, 1981). In some cases,

farmers may be able to diversify into other cash crops, but because different crops are suited to

different soils, altitudes, and other conditions, these possibilities can be limited. More often,

diversification is directed to subsistence crops and animal products (Reardon, 1994). One major

consequence of diversification is that farmers fail to exploit their comparative advantage, trading

lower average incomes for reduced income volatility (Collier and Gunning, 1999). Farmers who

hedge directly or indirectly through a floor price guarantee scheme would know their minimum

revenue in advance, given an expected level of production. They can then adjust their time and

resource inputs accordingly.

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

(ii) Enhanced access to credit and financing: Better access to funding has been driving

demand for commodity price hedging in the developed market economies. The same should be

true for developing countries like Nigeria in the nearest future. Improved accessibility of funding

will level the playing ground. Local traders at the moment in many developing countries find

themselves at a competitive disadvantage with their multinational counterparts who have

international links that can enable them obtain credit on good terms and hedge their positions

through their parent affiliate (Gilbert and Tollens, 1999). The disadvantaged position of local

firms squeezes them out of the commodity industries, even though they are not less efficient than

their international affiliated competitors. Better access to commodity risk management can level

the playing ground by allowing indigenous firms to compete on closer to equal terms.

(iii) Good policy environment and macroeconomic stability: In Nigeria, and other

developing economies, government and her parastatals have exposure to commodity price

changes in various different ways:

Tax revenue may depend on prices, generally, for energy and metals, where there is often

a substantial rent element in government taxed prices.

Like Nigeria, most developing countries are major importer of oil and cereals. Some

government parastatals import directly. In other cases, particularly in fuels, governments

may impose import taxes. If government aims to smooth changes in domestic prices, it

will hedge risk exposure to price fluctuations.

Where export prices affect government tax revenues, price volatility may seriously affect

the attainability of sustainability ratios (debt-GDP, debt to exports), a potentially serious

problem for heavily indebted poor countries (HIPCs).

With the above prevailing senario, developing countries like Nigerian could benefit from

commodity price insurance provided by the commodity exchange. For oil and metals, hedging

anticipated tax revenues could make government budgets more predictable, enabling more

tightly defined policies and greater accountability. Where governments are exposed to

commodity price risk and can hedge this position, perceived country risk should be lower and

better budgetary control would improve debt management. This effect if large would manifest in

faster growth. Moreover, better access to commodity price insurance can improve food security

for countries dependent on staple food imports from the world markets. This will be possible if

the concerned government purchase ceiling price guarantees to insure against sharp increase in

import prices.

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

(iv) Poverty reduction: Although small farmers are not necessarily the poorest members of

their communities, their economic situation is precarious. Their current self insurance strategy,

through diversification, is potentially expensive one as it reduces their ability to exploit their

comparative advantage. Where diversification is from a cash crop to subsistence crops, as is

often the case, peasant holders‟ families may still remain vulnerable to income shortfalls. Access

to price insurance offered by the commodity exchange will raise the welfare of poor families and

improve the prospects for their children to move into a wider variety of economic activities.

(v) Fair pricing: Commodity price insurance offered by the commodity exchange markets

might increase production. But since commodity demand is fairly insensitive to prices, the

increase in production could reduce prices, potentially off setting some benefits of risk

management to producers (1TF 1999).

(vi) Effect on farmers: Again, with better market information embedded in the price insurance

contracts provided by the commodity exchange markets, farmers will reduce their production in

some years, and increase it in others. Such a substitution will be based on relative profitability

expected for such commodities. Better information that helps coordinate production with

anticipated demand should increase adjustment of production towards comparative advantage

and thus induce efficiency of resource allocation.

(vii) Risk integration and management: Better access to commodity price insurance will

also allow entities in developing countries to transfer unwanted price risk to those who are more

able or willing, to bear it in established international commodity exchanges. The scheme could

also create new opportunities for global investment managers to „package‟ developing country

„commodity risk‟ as part of their investment portfolio, or to hedge commodity exposure in an

existing portfolio. Such could increase liquidity of the commodity risk management markets.

8.0 Global Commodity Market Problems

An impressive amount of empirical evidence has shown that commodity markets problem is a

combination of declining terms of trade, producers income volatility, price volatility and

exchange rate volatility. Studies on long term decline in prices were conducted by Prebisch

(1950) and, Singer (1950). Both concluded that in the long run, the price of primary commodities

often decline more relative to manufactured goods. This hypothesis has been repeatedly tested

and found valid in later studies such as Spraos (1983) as well as Bloch and Sapsford (2000). In a

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

theoretical analysis, DFID (2004) has equally supported the above findings. Their analysis

suggest that agricultural commodity prices fall more relative to other products due to relatively

inelastic demand and lack of differentiation among producers.

In addition to the long term decline in commodity prices, many primary commodity exports have

revealed a high degree of price fluctuation. Gilbert (1999) has found that the characteristics

behaviour of commodity price cycle is one of the `flat bottoms punctuated by occasional sharp

peaks‟. This means that the period of low prices endures far longer than the period of price

spikes. The implication is that producers often face the dual problems of low returns and high

risk. Cashin and Pattillo, (2000) conducted a similar study on commodity price fluctuation.

Their study reveals the existence of two types of commodity price fluctuations - short-term and

long term. Those fluctuations whose shock effects dissipate in less than four years were

classified as short term whereas; those with permanent shock effects were classified as long term

fluctuations (Eleje and Okafor; 2010). Their distinctions have been lauded by policy makers for

its significance in informing policy responses. While short term shocks can be dealt with through

savings or borrowing from both private and public sector, or managed through market-based risk

management mechanisms, long term shocks will require permanent change in the economy

(Page and Hewitt, 2001). Kwanashie, et al (1994) earlier had established that the degree of

fluctuation in prices is a major determinant of changes in earnings given the trend in output over

the years. The vulnerability of the poor to price fluctuations has increased over the recent period

due to Liberalization which has shifted price risk from governments to small producers and

consumers. Phasing out some preferential trade agreement, may further expose producers

especially, small holder and government agencies to the high price volatility in international

commodity markets.

9.0 Factors Affecting the Development of Efficient Commodity Exchange Markets In

Developing Economies

In considering the creation of a commodity exchange to foster economic development, it is

important to build on the collective wisdom in market development acquired globally. Important

lessons emerge from international experience concerning the problems that hindered the

development of most exchanges, around the world. The problems are legion. Eleje and Okafor

(2010) empirically identified six of such major factors to include:

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

(i) Commodities problem: Commodity exchanges are not necessarily useful or viable in all

countries. A careful evaluation of specific country circumstances is often needed when

conceiving the idea of establishing an exchange. Generally, exchanges are considered less viable

when goods are not easily standardized; when commodities are not storable; when trade is highly

decentralized with no central hub of market flows; and when there is weak volume of trade

(Eleni, et al, 2005). Another major commodity problem associated with commodities is the

inadequate quality certification arrangement and the absence of accurate data on annual

production quantity (Al-Faki, Undated).

(ii) Weak infrastructure: One major infrastructural problem is the weak access by small

holders‟ farmers to viable transportation and storage infrastructure. inadequate transport facility

could result in high cost of transportation and other physical marketing costs such as storage,

handling amongst others. Limited telecommunication is another major factor affecting the

development of efficient commodity market in developing nations. Poor telecommunication

impact directly on costs such as the cost of searching for and screening a trading partner; the cost

of obtaining information on prices, qualities, and quantities of goods; the cost of negotiating a

contract; the cost of monitoring contract performance; and the cost of enforcing contracts.

Although these costs are in most cases overlooked because they are difficult to identify and

measure, they however offer powerful explanation of the persistence of market failures.

(iii) Inadequate support markets and reference delivery points: Large domestic market

existing alongside multiple reference locations and delivery points is critical to the development

of viable commodity exchange market. This has accounted for the growth of notable exchanges

like South Africa Futures Exchange with 130 reference points as well as Chicago Board of

Trade, the largest commodity exchange in the world. Inadequate markets will definitely delay

exchange transactions and in the long-run, affect growth and development.

(iv) Inadequate support institutions: The most important supporting institution for commodity

exchange market is the clearing house. The clearing house should be party to all transactions in

other to offset the buy-and-sell orders. Second to clearing house is the banking institutions.

Banks and other financial intermediaries are required by exchanges to perform such

intermediation roles and further help provide risk management instruments for hedging of

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

commodity risks (Cordia, 1998). Inadequacy of these institutions in most developing nations

have dampened the growth of viable commodity exchanges.

(v) Government regulations: Inconsistent government policies hinder private sector

participation in the commodity market. Also, the lack of legal backing for the use of warehouse

receipts and warrants in physical commodities contracts pose great danger to the development of

a commodity exchange in developing economies.

(vi) Inadequate trained personnel: Financial market is a market where professionals interact

to facilitate the exchange process (Nnanna et al 2004). A commodity exchange is an integral

component of the financial market and as such, requires the service of professionals. The reason

is the sophisticated nature of the instruments traded therein such as derivative contracts.

Inadeqate trained personnel such as qualified commodity brokers accounts for why exchanges in

many developing economies including Nigeria are still battling to take off.

10.0 Summary and Recommendations

Despite its numerous contributions to economic development, the commodity exchange market

is still an emerging investment area in many of the developing countries today including Nigeria.

The reasons are not far from the factors discussed above. For a commodity exchange market to

be successful therefore, concerted efforts are needed by stakeholders including the governments,

private organizations, financial intermediaries, price insurance providers, commodity producers

amongst others. Governments and other stakeholders should speed up the development of a

viable commodity exchange market espacially in Nigeria to help reduce trading risks and secure

better prices for primary commodity exports. As part of the strategies to achieving this objective,

this paper hereby recommend that:

A functional warehouse with legal mandate to issue transferable receipts be established to

curb the problem of inelasticity of primary commodity exports. Functional warehouse

facility is expected to guarantee product standardization, quality certification, and stable

prices for primary export products. This in turn will increase the liquidity of primary

commodity trade flows in Nigeria and other developing countries.

Secondly, a well developed infrastructure including sound railway system, good network

of roads, and accessible seaports, will in no small measure ease the mobility of primary

commodity exports. Besides, governments should provide adequate incentives such as

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

modern farm machineries, chemicals, fertilizers as well as loans and subsidies to motivate

farmer and to boost their productivity.

Furthermore, governments should also review major regulations and policies that

impinge on the primary commodities sectors including the oil, agriculture, and solid

mineral. Among such regulations that need immediate reforms are tax systems and

practices which negatively affect agriculture and agro-allied industries; land use act; and

other necessary fiscal policy measures.

The benefits of deregulation and trade liberalization cannot be underestimated.

Competition has been found to impact positively and significantly on economic growth of

most economies due to its emphasis on quality and offering. The positive impact of

competition on large domestic market as well as multiple reference delivery points has

also been proven. This work therefore recommends a private sector led commodity

exchanges espacially for Nigeria with government being the enabler.

The take-off and speedy growth of a commodity exchange market is not impossible. A

robust spot market and supporting institutions like clearing house as well as banks are

sine quo non for its operational efficiency. The government should set the pace for the

robustness of the market by establishing more supporting credit institutions. Besides, the

call for the re-invention of the scrapped commodity boards to serve as procurement

points for trading on the commodity exchange should be supported by all stakeholders.

Lastly, commodity exchange and futures market is still a new capital market innovation

espacially in Nigeria. To exploit the gains therein, strong enlightenment and sensitization

campaign must be employed to teach the populace the „Dos‟ and „Don‟ts‟ of the market.

Above all, stakeholders should join hands in sponsorship training for prospective

commodity market operators.

References

Al-Faki, S. (Undated), “Regulatory Framework for Commodity and Futures Markets Operations in

Nigeria” ASCE Interactive Session Paper Abuja

ASCE, (2005), “Abuja Commodities Exchange; Brief History and Mode of Operations”

www.nigerianbusinessinfo.com

ASCE, (2006), “Abuja Commodity Exchange Commences Trading” www.abujacomex.com

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

Black, Fisher and Merton, Scholes (1973) “The Pricing of Option and Corporate Liabilities”,

Journal of Political Economy, Volume 18, Issue 3; 637-654.

Bloch H. and Sapsford, D. (2000) “Whither the Terms of Trade? An Elaboration of the Prebisch

Singer Hypothesis” Cambridge Journal of Economics 24: 461.

Cashin P. and Pattillo, C. (2000) “Terms of Trade Shocks in Africa: Are they Short-Lived or Long

-Lived?” IMF Working Paper

CBOT, (1989), “Chicago Board of Trade, Commodity Trading Manual”,

www.cbot.commtrading.com

CFTC, (2004) The Economic Purpose of Futures Market Federal Register”, Publication of

Commodity Futures Trading Commission, Retrieved 10/08/08 www.cftc.gov/foia/fedreg04

Collier P. and Gunning, J. W. (1998) “Explaining African Economic Performance”, Journal of

Economic Literature, 37; 64-111

Cordier, J. E (1998), “Importance of Commodity Risk Management for Producers of the European

Union” UNCTAD Publication

DFID (2004) “Rethinking Tropical Agricultural Commodities” UK Agriculture and Natural

Resources Team Research Paper, 3

Eleje, Edward O (2008) “Development of Commodity Derivatives Market in Nigeria: Issues,

Problems and Prospects” M.Sc. Dissertation Submitted to the Department of Banking and

Finance, University of Nigeria, Enugu.

Eleje, Edward O. (2009), “Global Economic System Recovery: How Far Has Nigeria Gone with

the Prevailing Turmoil in Her Financial Market,” Journal of the Chartered Institute of

Bankers of Nigeria, Vol.5, No.1: 19-25

Eleje, Edward O. (2010), “Risk Asset Market and Derivatives: Some Lessons for Emerging

Markets Like Nigeria,” Nigerian Journal of Banking, Finance and Management, Vol.11,

No.2

Eleje, Edward O. and Emerole, Gideon A. (2010), Development Financing for Growth in

Developing Countries of West Africa: Empirical Evidence from Nigerian, Accepted;

Journal of Entreprenurship and Development

Eleje, Edward O. and M. J. Modebe (2010), “Empirical Evidence on Uncertainty and Corporate

Risk Hedging in Nigeria,” Abuja Journal of Administration and Management, University of

Abuja

Eleje, Edward O. and Okafor, F.O. (2010), “Development of Commodity Derivatives Market in

Nigeria: An Empirical Assessment”, African Journal of Contemporary Issues, Vol.10 No.1

Eleni, Z Gabre-Madhin and Ian Goggin (2005), “Does Ethiopia Need a Commodity Exchange? An

Integrated Approach to Market Development, EDRI-ESSP Policy Working Paper No. 4

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

Fabozzi, F. J, Modigliani, F. & Ferri, M. G (1994) Foundation of Financial Market and

Institutions, New Jersey; Prentice-Hall

Gilbert C (1999) “Commodity Risk Management for Developing Countries”, Working Paper No

6. ITF 3rd

Meeting, Geneva. 23 – 24 June.

Gilbert, C. L. and Tollens, E. (1999) “Commodity Risk Management in Cameroon”, Vrije

Universities, Amsterdam FEWEC

Glen, J. (1993), “How Firms in Developing Countries Manage Risk” International Finance

Corporation Discussion Paper, No. 17

GLOBEX, (1989) “The Logical Extension of the Financial Futures Revolution”, GLOBEX

Brochure Chicago; Publication of Chicago Mercantile Exchange

Gorton G. et al (2004) “The Facts and the Fantasies about Commodity Futures”, Yale ICF;

Working Paper No. 04-20

Hatakeda, T. (Undated) “How do we Account for the Relationship between Investment and

Uncertainty”, Nihon University College of Economics Research Paper 101-8360

Hla Myint and Anne O. Krueger (2009) "Economic development," Encyclopædia Britannica

Hogendorn, J. S. (1992), Economic Development 2nd

Edition, New York, Collins Publisher

Idam, L. (2007) “Micro-Finance Institution As Instrument for Economic Development in

Nigeria”, Journal of Banking, Finance, and Development Vol. 1 No. 1

ITF (1999) “Dealing with Commodity Price Volatility in Developing Countries: A Proposal for a

Market-Based Approach”, Washington D.C, Discussion Paper – 33632

Jorion, P. (1995), Importance of Derivative Securities Markets to Modern Finance, Chicago,

Illinois: Irwin

Kwanashie, et al (1994) “The Nigerian Economy Response of Agriculture to Adjustment Policies”

AERC Research Paper 19

Lensink, R. Bo, H. and Sterken E. (1999) “Does Uncertainty Affect Economic Growth?”

Weltwitschaftiches Archieve 135, 379-396

Miller, M. (1991) Financial Innovations and Market Volatility, Cambridge, Massachusetts:

Blackwell Publisher

MSPDD,(2005), “Agricultural Commodity Futures Exchange Market”

www.dit.go.th/English/market2.htm.

Newbery, D.M.G and Stiglitz, J. E (1981) The Theory of Commodity Price Stabilization, Oxford:

Clarence Press.

Nnanna, O. J, Edoko, F. O. & Englama, A. (2004), Financial Markets in Nigeria, Abuja, A

Central Bank of Publication

NIGERIAN JOURNAL OF BANKING AND FINANCE ISSN: 1118-3144 Volume 8:132-146, Dec; 2008-09

Nnanna, O. J., Englama, A. and Odoko, F. O. (2004), “Finance, Investment & Growth in Nigeria”,

A Central Bank of Nigeria Publication

Nwaneri, Vitalis (2000) “Commodity Markets and the Interface with Stock Exchanges”, Abuja;

Conference of African Stock Exchanges Association Paper

O'Sullivan, Arthur & Steven M. Sheffrin (2003), Economics: Principles in Action. Upper Saddle

River, New Jersey 07458: Pearson Prentice Hall. pp. 471

Onoh, J. K. (2002), Dynamics of Money and Banking in Nigeria: An Emerging Market, Aba;

Astral Meridian Publishers

Onwumere J. U. (2000) „The nature and relevance of SMEs in Economic Development‟ The

Nigerian Banker July -December 2000

Page S. and Hewitt, A. (2001) “World Commodity Prices: Still a Problem for Developing

Countries?” Overseas Development Institute

Peck, A. (1985) Futures Markets; Their Economic Roles, Washington, D. C: American Enterprise

Institute for Public Policy Research.

Prebisch, P. (1950) “The Economic Development of Latin America and its Principal Problem”

Santiago: UNECLA

Reardon, T. et al, (1994) “Is Income Diversification Agriculture-Led in the West African Semi-

Arid Tropics?” Nairobi, African Economic Research Consortium

Singer, H.W. (1950) “The Distribution of Gains between Investing and Borrowing Countries”

American Economic Review, Papers and Proceedings 40: 473-85

Spraos, J. (1983) Inequalising Trade? A Study of Traditional North/South Specialization in the

Context of Terms of Trade Concept, Oxford: Clarendon Press.

Torado, M.P. and Smith, S.C.(2003), Economic Development, 8th

Edition, Delhi, Pearson

Education Inc.