Embed Size (px)

Citation preview

CHAPTER 6. RECOMMENDING LIFE AND HEALTH INSURANCE Reference: CPCU 553 Online 1st edition / Assignment 6

Unit 21. Term Life Insurance

Unit 22. Whole and Universal Life Insurance

Unit 23. Disability Income Insurance

Unit 24. Health Insurance Plans

151

Chapter 6. Recommending Life and Health Insurance

Unit 21. Term Life Insurance Reference: CPCU 553 Online 1st edition, Assignment 6. Module 1, 3

Unit 21.a. Characteristics of Term Life Insurance While the period during which term life insurance policies will compensate the

beneficiary in the event of the insured's death varies, policy coverage always ends after some specified duration or when the insured reaches a particular age. That is, term life insurance policies are temporary.

The primary purpose of term life insurance is to meet temporary life insurance needs—needs that are unlikely to continue throughout a client's life, such as to cover a long-term loan, redeem a mortgage, fund a child's education, or as an alternative to whole life insurance. Besides their temporary nature, other characteristics distinguish term life insurance policies:

Lower initial premium

The principal attraction of term life insurance coverage is its low initial premium cost. Insurers generally offer a rate guarantee for an initial multiyear period, after which premiums are either guaranteed at a relatively low (but increased) rate for an additional multiyear period or changed to yearly renewable term coverage at a current, nonguaranteed premium rate that is significantly increased.

Renewability Some term life insurance policies can be renewed at the end of the coverage period without evidence of insurability. So, the premium for a renewable term life insurance policy normally increases each renewal term period to reflect the insured’s increased age.

Convertibility In addition to being renewable, term life insurance policies are typically convertible to any kind of permanent life insurance the insurer is offering on the date of conversion. And as with renewals, the insured can convert the policy without having to provide evidence of insurability. Usually, conversions can be made only up to a maximum insured age.

152

Unit 21. Term Life Insurance

Unit 21.b. Level Term Life InsuranceUnder a level term life insurance policy, the initial rate guarantee period may

be as short as a single year—a term life insurance product known as yearly renewable term (YRT)—or as long as 30 years. Not surprisingly, the annual premium charged during the initial premium rate guarantee period is higher for longer rate guarantee periods than for shorter ones.

YRT life insurance is renewable each year, and the insurer charges its current premium rate, which must not exceed the guaranteed rate specified by the insurer in the policy. Similarly, a 5- or 10-year (or other duration) term life insurance policy, provided that it is renewable, may be renewed at the end of the term period. Although many insurers offer to renew the coverage for a period of identical length, other insurers offer renewal coverage on a yearly renewable basis at the conclusion of the (initially longer) term period.

Unit 21.c. Decreasing Term Life InsuranceUnlike the level death benefits of level term life insurance, the death benefits of

decreasing term life insurance decline over the life of the policy while the premium, which is less expensive because the death benefit decreases, remains the same. Decreasing term life insurance is classified as either straight line decreasing term life insurance or mortgage protection decreasing term life insurance.

In straight line decreasing term life insurance, the death benefit declines evenly over the term of the policy and is zero at the end of the period. For example, for a 20-year term period, the death benefit would decrease by 1/20th each year; for a 10-year term period, it would decrease by 1/10th each year; and so on. At the end of the policy term, the death benefit would be zero.

The death benefit under mortgage protection decreasing term life insurance, unlike the evenly decreasing benefits of straight line decreasing term life insurance, is meant to coincide with the decreasing principal balance of a mortgage as it’s paid down over time. Although insurers generally permit decreasing term life insurance coverage to be converted to permanent life insurance coverage, decreasing coverage is not normally renewable for additional periods.

153

Chapter 6. Recommending Life and Health Insurance

Unit 21.d. Term Life Insurance CaseLydia has just purchased a home for herself and her adult daughter, Ariel, to

live in. Ariel is employed, but she can’t afford to buy a home on her own. Lydia is in poor health and worries about Ariel's ability to pay the mortgage if Lydia passes away. Lydia calls her insurance agent and requests a term life insurance policy. What should the insurance agent advise Lydia?

Lydia's insurance agent may suggest that a mortgage protection decreasing term policy might be more appropriate. In a decreasing term life insurance policy, the death benefit decreases during the policy period, while the premium, which is lower because the death benefit decreases over time, remains level. This could ensure that Lydia’s mortgage is paid off if she dies prematurely.

Unit 21.e. Case: Selecting a Life Insurance Policy Nia and Zahara, a married couple with twin eight-year-old daughters, are

concerned about their family’s financial stability should Nia die prematurely. (1) Determining Assets Needed in the Event of Nia's Premature Death: To

determine which type of life insurance policy is most appropriate for Nia, you need to know more about what the family's financial needs would be if Nia died prematurely. The family's specific cash needs upon Nia’s premature death total $944,661.

(2) Determining the Family's Available Assets: Now that you know the amount of cash the family needs in the event of Nia’s premature death, you can determine the family’s liquid assets—those assets available to meet cash needs or produce income. In this case, the available assets total $225,000.

(3) Selecting an Appropriate Life Insurance Policy: Determining the total amount of life insurance needed for the family to achieve its insurance goals in the event of Nia’s premature death is straightforward. It involves simply subtracting the current liquid assets available to Zahara upon Nia’s death from the total cash needed at death: $944,661 − $225,000 = $719,661. The family will likely experience changes over time, however. They may accumulate assets, welcome more children, and so on. To account for these changes, they should regularly review their life insurance needs.

154

Unit 21. Term Life Insurance

Unit 21.1. Questions: Term Life Insurance

1. A typical term life insurance policy terminates without value at the end of the specified period of coverage.2. During the policy period, the death benefit decreases, but the premium

remains level in decreasing term life insurance3. A person designated in a life insurance policy to receive a death benefit is

referred to as the Beneficiary. 4. In a typical transaction for personal life insurance, The insured is the owner

of the policy.5. The renewability feature found in most level term life insurance policies is

that The policy is guaranteed continuable for an additional period without the insured needing to prove continuing insurability.6. Life insurance may be temporary or permanent. Term life insurance

provides temporary coverage.7. The policy is guaranteed continuable for an additional period without the

insured needing to prove continuing insurability, which describes the renewability feature found in most level term life insurance policies.8. Patrick is using the needs approach to help a couple determine an adequate

amount of life insurance based on the survivor's needs. They have determined that the total capital needed to meet the survivor's cash and income needs is $500,000. The amount of current life insurance owned should be subtracted from this number to determine the amount of new life insurance required.9. Jason recently purchased a term insurance policy that can be renewed at one

year intervals for an increasing premium, even though the death benefit remains constant. This policy is referred to as a Yearly renewable term policy.10. Serena recently took out a five-year loan to finance repairs on her elderly

parents' home, and she must make equal monthly payments during this period to repay the loan. She wants the loan to be paid off if she should die before its maturity. The purchase of Decreasing term life insurance would meet her objective in the most cost effective manner.

155

Chapter 6. Recommending Life and Health Insurance

Unit 22. Whole and Universal Life Insurance Reference: CPCU 553 Online 1st edition, Assignment 6. Module 2, 3

Unit 22.a. Whole Life InsuranceThe coverage provided under whole life insurance is permanent, and the

periodic premium is always the same. The significant guarantees of death benefits and cash value that whole life insurance offers make the individual premiums higher than for other types of life insurance. Over time, however, the total premium paid for a term life insurance policy can vastly exceed the total paid for a whole life insurance policy. So a client wishing to spend the least total amount for life insurance that is guaranteed for life is best served by a traditional whole life insurance policy.

As an insurer's perspective, a level death benefit plus increasing cash value, both of which whole life insurance provides, equals a net amount at risk (the difference between the cash value and the death benefit) that is constantly decreasing. And because the insurer’s amount at risk under a whole life insurance policy is constantly decreasing, the cost of insurance (COI) decreases over time.

Unit 22.b. Characteristics of Whole Life InsuranceUnlike term life insurance, whole life insurance never needs to be converted or

renewed, nor can it be canceled by the insurer (unless a material misrepresentation appears on the coverage application). And its death benefit is guaranteed to be paid upon the insured’s death at any age before the policy matures.

Additionally, the guaranteed cash values of whole life insurance policies can provide funds to help policyowners manage emergencies and take advantage of financial opportunities during the insured’s lifetime. It can also be used by the beneficiary when cash is needed at the time of the insured's death.

Another benefit of whole life insurance policies is that they allow policyowners to access a policy’s cash value tax free. Policyowners can normally borrow an amount up to a policy's cash value. Insurers charge interest, usually in arrears, on an outstanding policy loan until it is repaid. The policyowner may repay the loan at any time, but there is no scheduled repayment required. Any interest not paid when billed is added to the loan balance. If a policy is surrendered while a policy loan is outstanding, the outstanding loan balance at the time of surrender is deemed to have become part of the surrender proceeds and is treated as a distribution.

156

Unit 22. Whole and Universal Life Insurance

Unit 22.c. Universal Life InsuranceJust like whole life insurance policies, universal life insurance policies provide

permanent protection. However, in order for a universal life insurance policy to remain in force, the cash value must be sufficient to enable the insurer to make its monthly deductions from the policy’s cash value for mortality costs and expenses.

The appeal of a universal life insurance policy is flexibility. Although insurers typically require universal life insurance policyowners to pay premiums in the first year in an amount at least equal to minimum premiums, premiums are otherwise flexible, and the policyowner may pay more or less than billed. Death benefits are similarly flexible. When an applicant applies for a universal life insurance policy, he or she specifies the initial death benefit amount, generally referred to as the specified amount.

These are the universal life insurance death benefit options: (1) Option A: A level death benefit equal to the specified amount (2) Option B: A generally increasing death benefit equal to the specified amount plus the cash value (3) Option C: An increasing death benefit equal to the specified amount plus total premiums paid.

Unit 22.d. Examples of Situations for Universal Life InsuranceExamples of situations in which a universal life insurance policy might be

appropriate include someone considering starting a family or a new job, or someone for whom cash flow is uncertain. Most universal life insurance is sold through agents who are compensated by commissions. Those commissions and associated field marketing costs make up the largest portion of an insurer’s business-acquisition costs. Although insurers may deduct a premium expense charge in an effort to recover business-acquisition costs, these generally modest deductions require an extended period of time before business-acquisition costs can be fully recovered—which means that the insurer might not recover those costs if the policy is surrendered early.

Because of that risk, insurers impose surrender charges for a certain period of time called the surrender charge period. Surrender charges are deducted from a universal life insurance policy’s cash value if the policy is surrendered during the surrender charge period. The extent of surrender charges and the duration of the surrender charge period vary significantly by insurer.

Finally, variable universal life (VUL) insurance is an important variation of universal life insurance. It differs from the previously discussed universal life insurance in how the interest credited to the cash value is determined. In other respects, it is virtually identical to a fixed universal life policy. Unlike fixed universal life insurance, the interest credited in a VUL policy is determined by the investment performance of the insurer’s separate account to which the policyowner has allocated premiums. The insurer’s separate account is normally made up of many variable subaccounts.

157

Chapter 6. Recommending Life and Health Insurance

Unit 22.e. Case: Selecting a Life Insurance Policy Although Nia earns a comfortable income, she sometimes goes a month or so

without any commission income at all. In addition, Nia and Zahara are willing to take risks to potentially increase the value of their investments, are contributing the maximum amounts to their tax-advantaged retirement plans, and welcome additional tax advantages.

Based on this information, the most suitable life insurance policy for Nia and Zahara would have these characteristics: (1) It should build tax-deferred cash value, which would offer the tax advantage of deferring taxes on gains. (2) The premium should be flexible to allow for Nia's irregular cash flow. (3) The death benefits should be flexible. The ability to increase and reduce the death benefit is important because the family’s death benefit needs are likely to change as the children mature and begin their own families and as Nia eventually retires. (4) The policy should facilitate access to its cash value that could be used to increase the couple’s retirement income. (5) The policy should enable the couple to potentially increase their cash value by taking on investment risk.

Because term life insurance does not build cash value, it is not appropriate for this family's needs. The suitability requirements of premium and death benefit flexibility, along with easy access to cash value, suggest that a universal life insurance policy is likely to be the most appropriate one for this family. Because Nia and Zahara are willing to take risks, a variable universal life insurance policy is the best recommendation because it will allow them to assume investment risk to increase cash values.

158

Unit 22. Whole and Universal Life Insurance

Unit 22.1. Questions: Whole and Universal Life Insurance

1. All life insurance premiums have three traditional elements, Mortality, expense, and interest.2. Fixed, level premiums is a characteristic of traditional whole life insurance. 3. Shifting of mortality and expense risk to the policyowner is a characteristic

of universal life insurance.4. The policyowner of a universal life insurance policy has flexibility with

respect to Death benefits. 5. Subaccounts may differ from one another by such factors as asset class and

risk in variable universal life insurance policies.6. Shifting of mortality and expense risk to the policyowner is a characteristic

of universal life insurance.7. An applicant for a universal life insurance policy specified an initial death

benefit and selected an option that provided for a benefit upon death equal to this specified amount plus the policy's cash value. This applicant elected a death benefit option that is referred to as Option B. 8. Withdrawals are considered partial surrenders and under certain

circumstances may be subject to a surrender charge, which describe the cash withdrawal feature of a universal life insurance policy. 9. Bruce and Sue are trying to decide how much additional life insurance is

needed if he should die. Currently, Sue does not work outside the home. They have come up with the following needs of Sue and the family as a result of Bruce's death: (1) Final expenses: $15,000, (2) Debt elimination: $340,000, (3) Family living expenses: $400,000, (4) Special needs: $25,000, (5) Sue's retirement needs: $350,000. Bruce and Sue currently have $10,000 in bank accounts. Bruce has $150,000 of employer provided life insurance, $300,000 of individually purchased life insurance, and a $50,000 death benefit in a pension plan. Sue is the beneficiary of all of these. The estimated Social Security survivors benefits upon Bruce's death are $230,000. Using the needs approach, how much additional life insurance should Bruce purchase? $390,000. 10. Fritz and Emma have determined that they should purchase more life

insurance on Fritz to meet their long-term needs, including retirement income and paying estate settlement costs. Because his income fluctuates, they want a premium that is flexible. They also want a policy that will build a cash value that they can borrow or withdraw. They are highly risk tolerant and are willing to take significant investment risk to potentially increase this cash value. In this case, Variable universal life insurance would be most appropriate.11. Paula is a successful business woman. She is married with three grown

children. Paula has always been very grateful for her college experience, and feels that it is responsible for much of her success. She has made a pledge of $50,000 to the college when she dies. She would like to fund this pledge through a life insurance policy. She should purchase a Whole life insurance policy to guarantee that the separate funds are available to satisfy this pledge.

159

Chapter 6. Recommending Life and Health Insurance

12. Linda is a single mother and is concerned about financial support for her daughter if she should die. Her sister will take care of the daughter, but Linda would like to provide at least $150,000 toward the cost of her care. Linda would also like to have an additional $100,000 to fund her daughter's college education. Linda estimates her final expense need would be $10,000. Currently, Linda expects that there would be $25,000 left over from the sale of her house and car after her death. She has $35,000 of employer-provided life insurance, but no other employee benefits that would provide income for her daughter. Linda also has $10,000 in savings. Finally, she expects Social Security survivors benefits to be $130,000. Using the needs approach, how much life insurance should Linda purchase? $60,000.

160

Unit 22. Whole and Universal Life Insurance

161

Chapter 6. Recommending Life and Health Insurance

Unit 23. Disability Income Insurance Reference: CPCU 553 Online 1st edition, Assignment 6. Module 4

Unit 23.a. Disability and Health-Related Personal Loss Exposures

1. Disability Loss Exposures

In addition to the loss of the disabled individual's wages, there are generally medical expenses to be paid (with or without health insurance), and the individual may incur costs for rehabilitation or for education so that he or she could qualify for another type of job.

2. Health-Related Loss Exposures

(1) Many lower-income, single-wage-earner families and elderly individuals do not purchase it due to the high cost and, often, lack of availability. (2) The cost of private health insurance for the benefits provided is significantly greater than the cost of group health insurance (as provided by an employer) because private plans lack the cost savings from economies of scale. (3) Associations offer group healthcare insurance plans with lower premiums. These plans might offer benefits only for lesser-quality medications and older treatment methods, often using outdated technology.

3. Long-Term Care Loss Exposures

Unexpected, high medical costs; disability costs; and long-term care costs can easily exhaust an individual's or a family's savings and retirement funds.

162

Unit 23. Disability Income Insurance

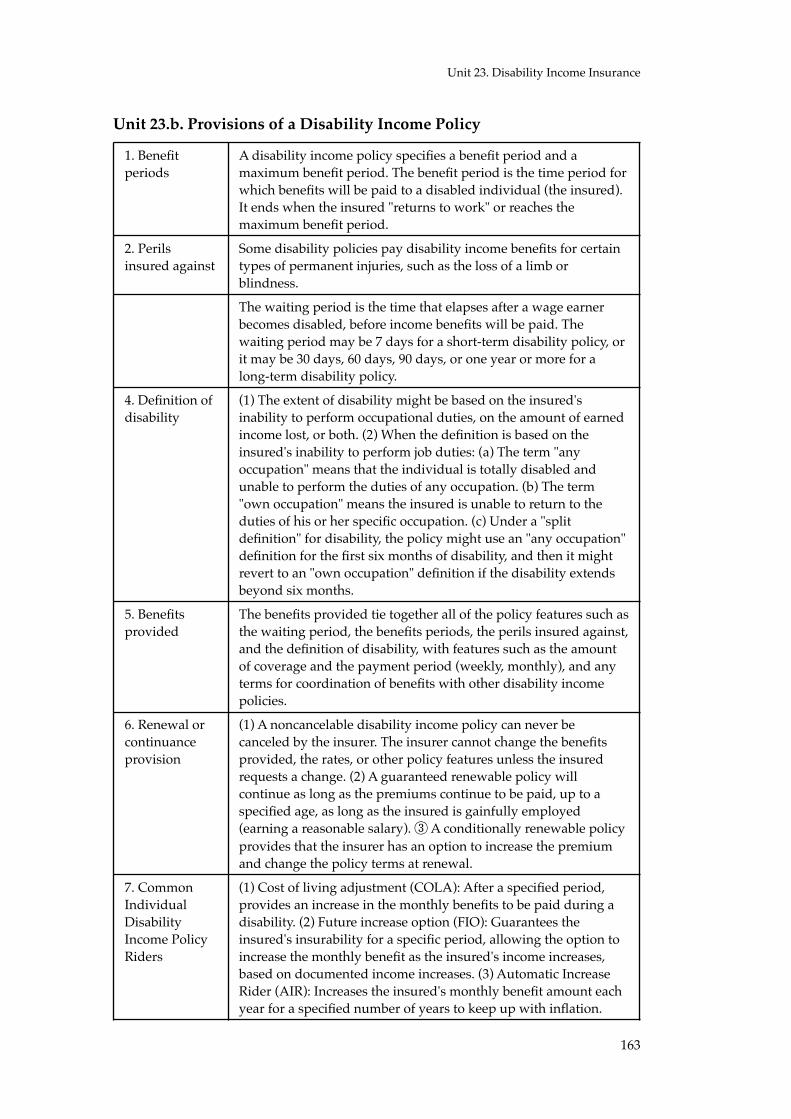

Unit 23.b. Provisions of a Disability Income Policy

1. Benefit periods

A disability income policy specifies a benefit period and a maximum benefit period. The benefit period is the time period for which benefits will be paid to a disabled individual (the insured). It ends when the insured "returns to work" or reaches the maximum benefit period.

2. Perils insured against

Some disability policies pay disability income benefits for certain types of permanent injuries, such as the loss of a limb or blindness.

3. Waiting period

The waiting period is the time that elapses after a wage earner becomes disabled, before income benefits will be paid. The waiting period may be 7 days for a short-term disability policy, or it may be 30 days, 60 days, 90 days, or one year or more for a long-term disability policy.

4. Definition of disability

(1) The extent of disability might be based on the insured's inability to perform occupational duties, on the amount of earned income lost, or both. (2) When the definition is based on the insured's inability to perform job duties: (a) The term "any occupation" means that the individual is totally disabled and unable to perform the duties of any occupation. (b) The term "own occupation" means the insured is unable to return to the duties of his or her specific occupation. (c) Under a "split definition" for disability, the policy might use an "any occupation" definition for the first six months of disability, and then it might revert to an "own occupation" definition if the disability extends beyond six months.

5. Benefits provided

The benefits provided tie together all of the policy features such as the waiting period, the benefits periods, the perils insured against, and the definition of disability, with features such as the amount of coverage and the payment period (weekly, monthly), and any terms for coordination of benefits with other disability income policies.

6. Renewal or continuance provision

(1) A noncancelable disability income policy can never be canceled by the insurer. The insurer cannot change the benefits provided, the rates, or other policy features unless the insured requests a change. (2) A guaranteed renewable policy will continue as long as the premiums continue to be paid, up to a specified age, as long as the insured is gainfully employed (earning a reasonable salary). ③ A conditionally renewable policy provides that the insurer has an option to increase the premium and change the policy terms at renewal.

7. Common Individual Disability Income Policy Riders

(1) Cost of living adjustment (COLA): After a specified period, provides an increase in the monthly benefits to be paid during a disability. (2) Future increase option (FIO): Guarantees the insured's insurability for a specific period, allowing the option to increase the monthly benefit as the insured's income increases, based on documented income increases. (3) Automatic Increase Rider (AIR): Increases the insured's monthly benefit amount each year for a specified number of years to keep up with inflation.

163

Chapter 6. Recommending Life and Health Insurance

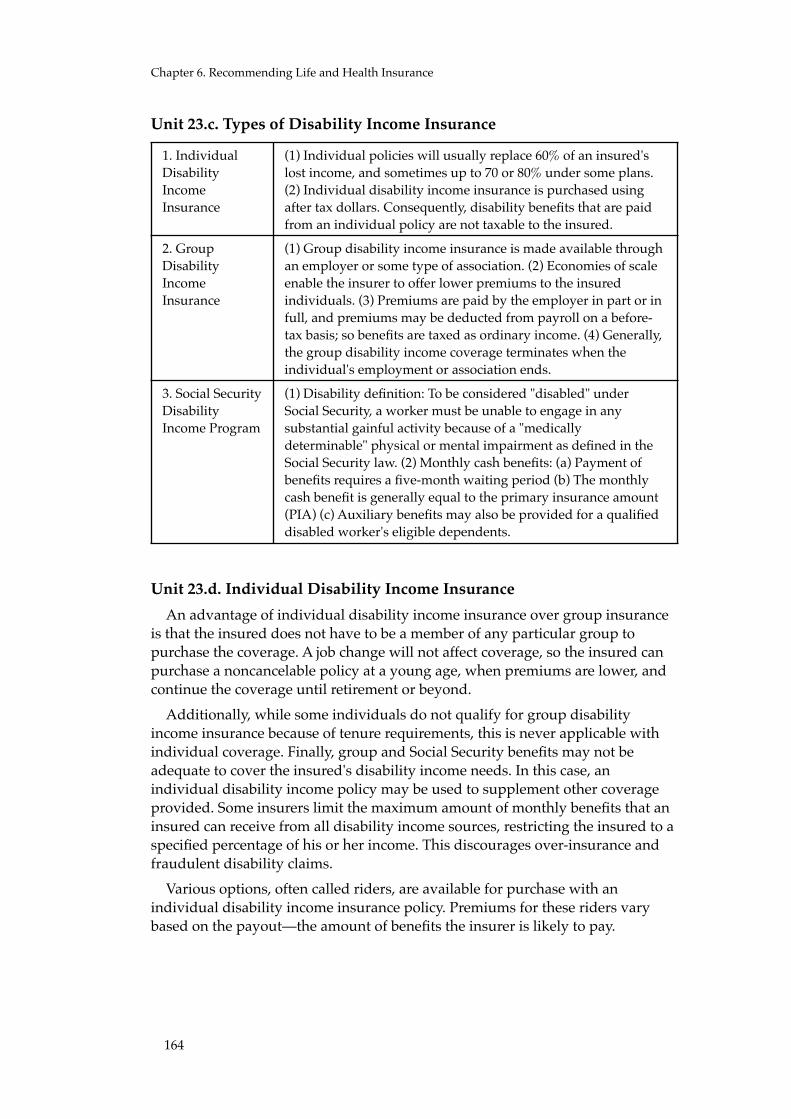

Unit 23.c. Types of Disability Income Insurance

Unit 23.d. Individual Disability Income Insurance An advantage of individual disability income insurance over group insurance

is that the insured does not have to be a member of any particular group to purchase the coverage. A job change will not affect coverage, so the insured can purchase a noncancelable policy at a young age, when premiums are lower, and continue the coverage until retirement or beyond.

Additionally, while some individuals do not qualify for group disability income insurance because of tenure requirements, this is never applicable with individual coverage. Finally, group and Social Security benefits may not be adequate to cover the insured's disability income needs. In this case, an individual disability income policy may be used to supplement other coverage provided. Some insurers limit the maximum amount of monthly benefits that an insured can receive from all disability income sources, restricting the insured to a specified percentage of his or her income. This discourages over-insurance and fraudulent disability claims.

Various options, often called riders, are available for purchase with an individual disability income insurance policy. Premiums for these riders vary based on the payout—the amount of benefits the insurer is likely to pay.

1. Individual Disability Income Insurance

(1) Individual policies will usually replace 60% of an insured's lost income, and sometimes up to 70 or 80% under some plans. (2) Individual disability income insurance is purchased using after tax dollars. Consequently, disability benefits that are paid from an individual policy are not taxable to the insured.

2. Group Disability Income Insurance

(1) Group disability income insurance is made available through an employer or some type of association. (2) Economies of scale enable the insurer to offer lower premiums to the insured individuals. (3) Premiums are paid by the employer in part or in full, and premiums may be deducted from payroll on a before-tax basis; so benefits are taxed as ordinary income. (4) Generally, the group disability income coverage terminates when the individual's employment or association ends.

3. Social Security Disability Income Program

(1) Disability definition: To be considered "disabled" under Social Security, a worker must be unable to engage in any substantial gainful activity because of a "medically determinable" physical or mental impairment as defined in the Social Security law. (2) Monthly cash benefits: (a) Payment of benefits requires a five-month waiting period (b) The monthly cash benefit is generally equal to the primary insurance amount (PIA) (c) Auxiliary benefits may also be provided for a qualified disabled worker's eligible dependents.

164

Unit 23. Disability Income Insurance

Unit 23.e. Group Disability Income Insurance An employer may offer both short- and long-term disability income insurance

plans. Short-term plans might offer weekly benefits, with waiting periods of one to seven days, and short maximum benefit periods. Long-term disability plans (often called LTDs) might have higher maximum benefit payouts, such as $5,000 per month or $60,000 per year. LTD policies usually replace around 60 percent of an insured's lost income. Premiums are paid by the employer in part or in full and may be deducted from the insured's payroll on a before-tax basis; consequently, benefits are taxed as ordinary income when they are paid to the insured during disability. Under an association's plan, premiums would be paid by the individual with after-tax dollars, so benefits are not taxable.

The waiting period under an LTD plan could be three or six months. Most group LTD plans use a split definition of disability, with which an "own occupation" definition applies for an initial disability period, such as two years, and then an "any occupation" definition applies for the remaining benefit period, until the maximum benefit period is reached. Because group policies are purchased in bulk, options are limited compared with those available in individual plans.

Under most LTD plans, when the individual's employment or association ends, the group disability income coverage terminates. The coverage also terminates if the employer fails to pay the premium for the employee or if the group policy is terminated by the employer or association. Most LTD plans do not have provisions enabling an insured to convert his or her plan to an individual disability income policy.

165

Chapter 6. Recommending Life and Health Insurance

Unit 23.f. Social Security Disability Insurance Program Rules to qualify under the Social Security Disability Insurance (SSDI) program

are strict compared with other disability plans. The program provides two protections for disabled workers: monthly cash benefits and establishment of a period of disability.

Disability definition: To be considered "disabled" under Social Security, a worker must be unable to engage in any substantial gainful activity because of a "medically determinable" physical or mental impairment as defined in the Social Security law. A substantial gainful activity is one that requires significant activities that are physical, mental, or a combination of the two, in work that is performed for profit, even if no profit is realized. This work qualifies whether it is full or part time. This disability definition is comparable to an "any occupation" definition. Additionally, the worker's impairment must be established by objective medical evidence and expected to last for at least 12 consecutive months or to result in the individual's death. Other, nonmedical criteria must also be met.

Establishment of a disability period: A "period of disability" under the Social Security law is a continuous period during which an individual is disabled. The established period of disability is not counted in determining either an individual's insured status under Social Security or the monthly benefit amount payable to the worker and his or her dependents. This period of disability is used to determine other types of Social Security benefits for the worker's family. A period of disability must be established during a worker's disability or within 12 months after the disability ends, assuming it lasted at least 5 consecutive months. Special exceptions exist to the 5-month waiting period; for example, the period is not required if the worker suffers a subsequent disability.

166

Unit 23. Disability Income Insurance

Unit 23.1. Questions: Disability Income Insurance

1. High costs associated with medical care, disability, and long-term care can force some individuals and families into bankruptcy.2. The average Social Security Disability Insurance SSDI benefit is only slightly

above the poverty line for a one-person household.3. A disability income policy has a rider that increases the monthly benefit

amount by 4 percent for each of the first five years the policy is in force, if benefits have not yet begun. This is an example of Automatic increase rider.4. Payment of benefits under the Social Security disability income program

requires a waiting period of Five months.5. The fewest number of people recognize The potential financial devastation

they could face if they or their spouse were to became disabled.6. Long term care insurance offers a way to help pay the costs of skilled

nursing facilities, adult daycare facilities, and home health care services for individuals suffering from serious medical conditions. 7. According to the Council for Disability Awareness, Musculoskeletal

disorders is the top cause of disabilities.8. Individual long-term disability income insurance plans may have a

provision that defines how disability income benefits from programs such as Social Security will affect benefits under the plan.9. Ed purchased an individual disability income policy several years ago and

continued to pay the annual premium with after-tax dollars. He recently was severely disabled and is not expected to ever return to work. His monthly benefit is $4,000, which represents 60 percent of his predisability earnings. The present value of his expected benefits is $240,000, and the aggregate premiums he has paid for the policy are $60,000. How much of each monthly benefit is subject to income taxation? Nothing.

167

Chapter 6. Recommending Life and Health Insurance

Unit 24. Health Insurance Plans Reference: CPCU 553 Online 1st edition, Assignment 6. Module 5

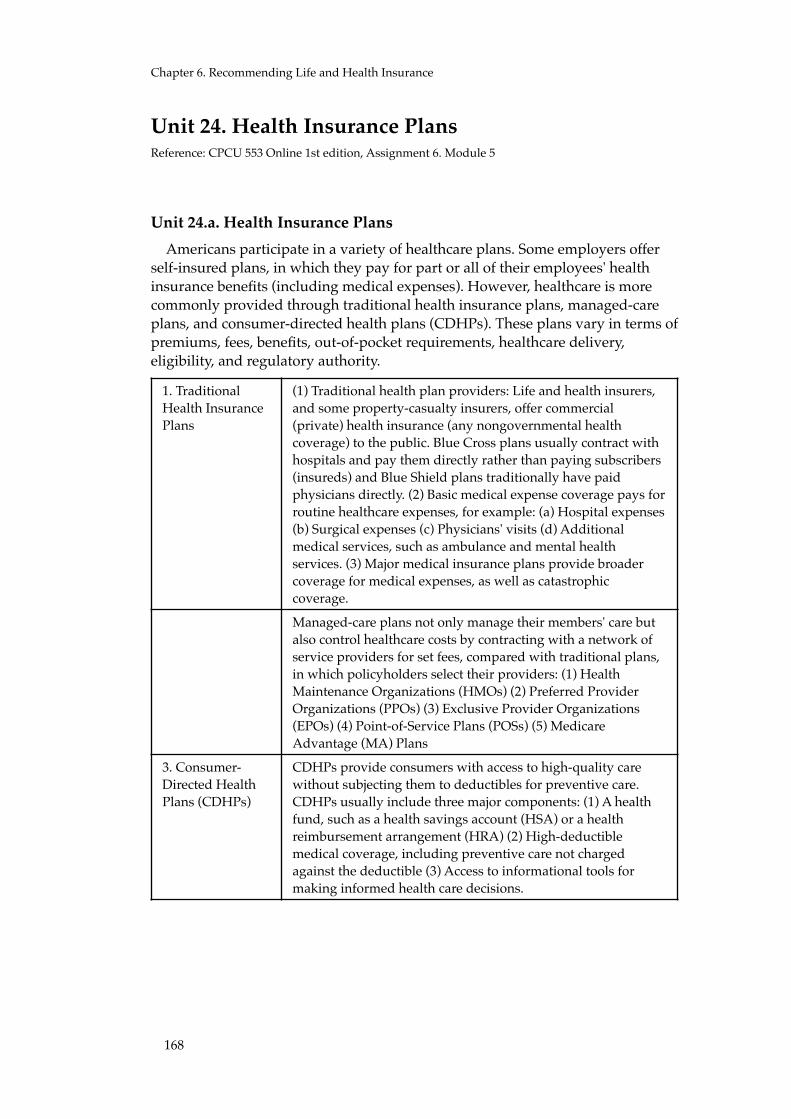

Unit 24.a. Health Insurance Plans Americans participate in a variety of healthcare plans. Some employers offer

self-insured plans, in which they pay for part or all of their employees' health insurance benefits (including medical expenses). However, healthcare is more commonly provided through traditional health insurance plans, managed-care plans, and consumer-directed health plans (CDHPs). These plans vary in terms of premiums, fees, benefits, out-of-pocket requirements, healthcare delivery, eligibility, and regulatory authority.

1. Traditional Health Insurance Plans

(1) Traditional health plan providers: Life and health insurers, and some property-casualty insurers, offer commercial (private) health insurance (any nongovernmental health coverage) to the public. Blue Cross plans usually contract with hospitals and pay them directly rather than paying subscribers (insureds) and Blue Shield plans traditionally have paid physicians directly. (2) Basic medical expense coverage pays for routine healthcare expenses, for example: (a) Hospital expenses (b) Surgical expenses (c) Physicians' visits (d) Additional medical services, such as ambulance and mental health services. (3) Major medical insurance plans provide broader coverage for medical expenses, as well as catastrophic coverage.

2. Managed-Care Plans

Managed-care plans not only manage their members' care but also control healthcare costs by contracting with a network of service providers for set fees, compared with traditional plans, in which policyholders select their providers: (1) Health Maintenance Organizations (HMOs) (2) Preferred Provider Organizations (PPOs) (3) Exclusive Provider Organizations (EPOs) (4) Point-of-Service Plans (POSs) (5) Medicare Advantage (MA) Plans

3. Consumer-Directed Health Plans (CDHPs)

CDHPs provide consumers with access to high-quality care without subjecting them to deductibles for preventive care. CDHPs usually include three major components: (1) A health fund, such as a health savings account (HSA) or a health reimbursement arrangement (HRA) (2) High-deductible medical coverage, including preventive care not charged against the deductible (3) Access to informational tools for making informed health care decisions.

168

Unit 24. Health Insurance Plans

Unit 24.b. Managed-Care Plans Providers

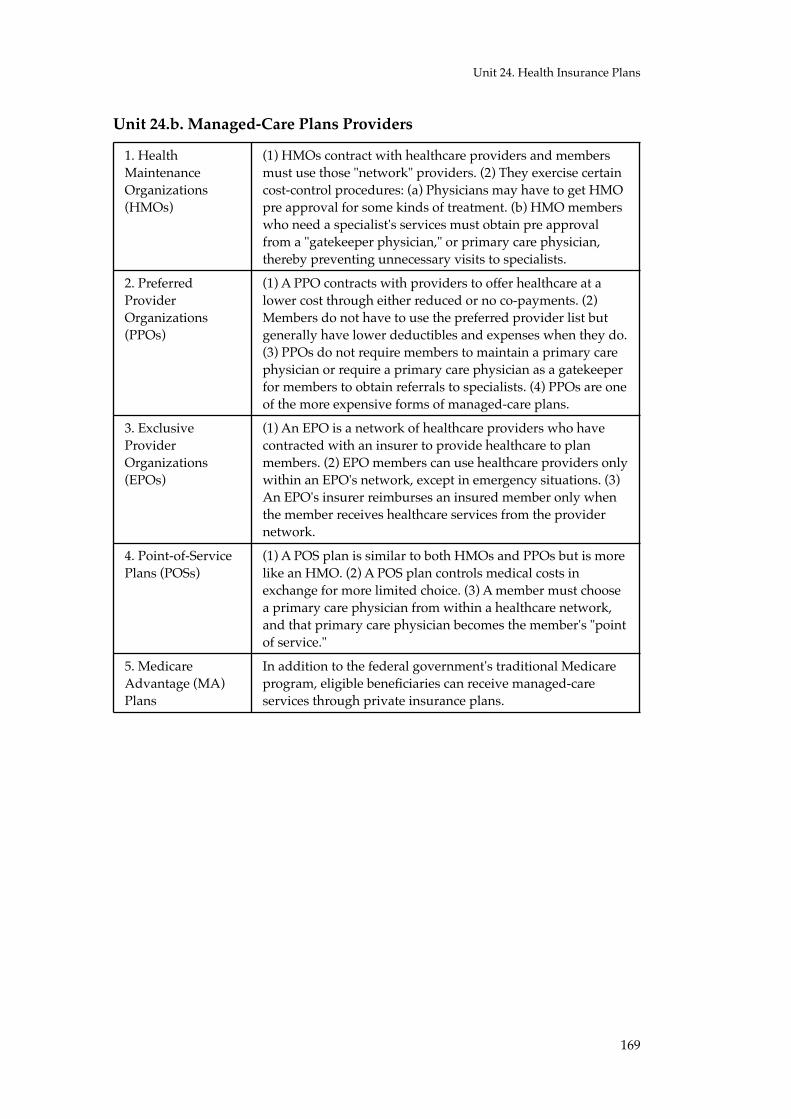

1. Health Maintenance Organizations (HMOs)

(1) HMOs contract with healthcare providers and members must use those "network" providers. (2) They exercise certain cost-control procedures: (a) Physicians may have to get HMO pre approval for some kinds of treatment. (b) HMO members who need a specialist's services must obtain pre approval from a "gatekeeper physician," or primary care physician, thereby preventing unnecessary visits to specialists.

2. Preferred Provider Organizations (PPOs)

(1) A PPO contracts with providers to offer healthcare at a lower cost through either reduced or no co-payments. (2) Members do not have to use the preferred provider list but generally have lower deductibles and expenses when they do. (3) PPOs do not require members to maintain a primary care physician or require a primary care physician as a gatekeeper for members to obtain referrals to specialists. (4) PPOs are one of the more expensive forms of managed-care plans.

3. Exclusive Provider Organizations (EPOs)

(1) An EPO is a network of healthcare providers who have contracted with an insurer to provide healthcare to plan members. (2) EPO members can use healthcare providers only within an EPO's network, except in emergency situations. (3) An EPO's insurer reimburses an insured member only when the member receives healthcare services from the provider network.

4. Point-of-Service Plans (POSs)

(1) A POS plan is similar to both HMOs and PPOs but is more like an HMO. (2) A POS plan controls medical costs in exchange for more limited choice. (3) A member must choose a primary care physician from within a healthcare network, and that primary care physician becomes the member's "point of service."

5. Medicare Advantage (MA) Plans

In addition to the federal government's traditional Medicare program, eligible beneficiaries can receive managed-care services through private insurance plans.

169

Chapter 6. Recommending Life and Health Insurance

Unit 24.c. Consumer-Directed Health Plans (CDHPs) CDHPs usually include three major components: (1) A health savings

account (HSA) or a health reimbursement arrangement (HRA) (2) High-deductible medical coverage with no charge for preventive care (3) Access to informational tools to make informed healthcare decisions

People covered by CDHPs pay lower premiums but higher deductibles. Using either an HSA or HRA, they set aside money that can be used to help satisfy the deductible. HSAs are funded by enrollees themselves—and the money within them can be rolled over for future use at year's end. No taxes are withheld from funds contributed to an HSA.

Money in an HRA, meanwhile, is contributed by the employer and not included in the employees’ income for tax purposes. The employer’s distributions to the employee are tax-deductible, and unused funds in HRA accounts can be rolled over from year to year for future use.

Participants set aside HSA and HRA funds for medical expenses before paying out-of-pocket costs. For example, if a consumer has an annual deductible of $2,000 and a $1,000 HSA or HRA fund, the consumer's first $1,000 of medical expenses could be paid from the corresponding fund, with the remaining $1,000 paid out of pocket. Medical coverage would absorb costs after that. However, the consumer can always choose to pay medical expenses out of pocket, rather than using HSA or HRA funds.

Unit 24.d. Case 1: Selecting Health Insurance Plans Bonita has a 10-year-old son, Ray, who has a number of medical conditions and

prefers to see certain specialists for his treatments. Bonita changed jobs, and her new employer offers two managed-care options, a PPO plan and an EPO plan. While Bonita would prefer a flexible plan with low deductibles and co-payments, Ray would like to continue treatments with his preferred specialists. Which option would best meet Bonita’s and Ray’s healthcare needs?

The PPO plan offered by Bonita's new employer would best meet their healthcare needs because it would allow them to seek medical care from their current physicians and specialists and offer decreased costs for in-network providers. If one of their providers is out-of-network, they could still see that provider—although they would pay higher costs, co-payments, and deductibles for such treatments.

170

Unit 24. Health Insurance Plans

Unit 24.e. Case 2: Selecting Health Insurance Plans Brian’s employer offers two healthcare plan options: an HMO and a PPO.

Brian and his husband, Karl, are both in their late 20s and have no known health issues. They would prefer a plan with low premiums and out-of-pocket expenses. But they are new to the area and not familiar with area physicians or other medical care providers. Which one of the healthcare options would best meet the couple’s needs?

An HMO would best meet Brian and Karl’s needs. It would offer lower premiums and low, fixed, prepaid fees with small co-payments for routine visits. Because the two are in good health but not familiar with area physicians and other medical care providers, they are less likely to want or require the services of out-of-network providers. A PPO plan would be a more costly solution in terms of premiums and co-payments but would provide more flexibility for treatment from out-of-network providers, which does not suit the couple’s current needs.

171

Chapter 6. Recommending Life and Health Insurance

Unit 24.1. Questions: Health Insurance Plans

1. Amelia’s employer offers a point-of-service (POS) healthcare plan. A POS plan is a hybrid healthcare plan that has characteristic of A health maintenance organization (HMO) and a preferred provider organization (PPO).2. The use of a health savings account (HSA) or a health reimbursement

arrangement (HRA) is a major characteristic of a consumer-directed health plan. 3. Blue Cross and Blue Shield plans are often administered by for-profit

organizations.4. The basic provisions of the Affordable Health Care Act of 2010 requires

insurers to spend set percentages of premiums received on direct medical care or improvements in the quality of care provided.5. Chris and Bill have their family insured under a plan that allows them to

select their own health care provider without any restrictions. The plan then reimburses them for a percentage of their medical expenses after the satisfaction of a deductible. This is an example of An indemnity plan.

172

CHAPTER 7. FUNDING RETIREMENT Reference: CPCU 553 Online 1st edition / Assignment 7

Unit 25. The Retirement Planning Process and Retirement Savings Needs

Unit 26. Employer-Sponsored Retirement Plans

Unit 27. Individual Retirement Accounts (IRA)

Unit 28. Retirement Plan Taxes

Unit 29. Social Security Retirement Benefits and Individual Annuities

173

Chapter 7. Funding Retirement

Unit 25. The Retirement Planning Process and Retirement Savings NeedsReference: CPCU 553 Online 1st edition, Assignment 7. Module 1, 2

Unit 25.a. The Retirement Planning Process One of the most significant factors in maintaining financial security in

retirement is effective planning. This planning involves estimating the living expenses that will arise after income from full-time employment ceases and the anticipated length of retirement. Some individuals mistakenly assume that overall expenses will decrease in retirement. And while housing expenses, for example, may be lower if a mortgage is paid in full, expenses such as healthcare costs usually increase as people age. Planning should also consider the potential costs of long-term care and increased expenses related to hobbies, recreational activity, or travel. Failure to accurately plan for retirement needs such as these can result in a lower standard of living in retirement or the need to continue working past a planned retirement age.

1. Determining Retirement Goals

Individuals must determine their desired standard of living during retirement before they are able to set their retirement goals. Retirement goals should be stated clearly and objectively in writing.

2. Analyzing Financial Needs

The next step turns an individual’s retirement goals into an accumulation goal. (1) the amount of income needed at retirement (2) Estimated length of retirement (3) Anticipated Social Security retirement benefits (4) Estimated value of existing retirement resources (401K, Pension, and so on) at retirement date (5) Calculation of the annual retirement savings amount required to meet retirement goals (6) Estimated retirement income shortfall

3. Arranging Financial and Control Techniques

After identifying the annual retirement savings amount required in the previous step, the individual (and his or her financial professional) must determine the types of financial products needed to accumulate that sum. Retirement savings funding vehicles fall into these four categories: (1) Both tax-deductible and tax-deferred (2) Tax-free (3) Tax-deferred (4) Currently taxable

4. Monitoring and Revising the Plan

Most retirement plans need to be revised as an individual’s financial situation changes. Financial professionals should therefore monitor plans annually. But if a significant event occurs that could affect a person’s financial situation, such as the death of a spouse or loss of a job, the plan should be revised sooner. Any of these factors could also warrant a plan revision: (1) Changes in tax laws (2) Increased or decreased performance of retirement assets (3) New investments.

174

Unit 25. The Retirement Planning Process and Retirement Savings Needs

Unit 25.b. Determining Retirement Goals Alva, a single, 45-year-old woman, earns $90,000 per year in her current job

and can put $15,000 per year into a retirement investment. Her disabled daughter is her dependent and requires daily assistance with medical and personal care. Alva would like to have all of her outstanding financial obligations, including her mortgage, paid in full when she retires. She would like to be able to travel twice a year in her first five years of retirement, and because her daughter doesn’t travel, Alva needs to pay a professional to care for her daughter during those trips. Except for the added travel, Alva would like to maintain her current lifestyle after she retires at age 65. Based on these facts, assemble a list of financial goals that should be in her retirement plan.

Each of these factors becomes a financial goal in Alva’s retirement plan: (1) Having enough retirement income to maintain her current lifestyle and to support her daughter, including providing the daily medical and personal care her daughter requires (2) Paying to travel twice a year for five years (3) Paying a professional to care for her daughter while she travels (4) Paying off her mortgage and other outstanding financial obligations before she retires.

175

Chapter 7. Funding Retirement

Unit 25.c. Arranging Financial and Control Techniques 1. Both tax-deductible and tax-deferred: Retirement funding vehicles that are

tax-deductible (before-tax contributions) and offer investment gains that are tax-deferred (taxes paid at a future date) are generally considered qualified retirement plans. Examples of these plans include traditional individual retirement accounts (IRAs), Section 401(k) plans, Section 403(b) plans (other than designated Roth accounts), and Section 457 deferred compensation plans. Qualified retirement plans can lower an individual’s taxable income because the amount a person contributes to them is exempt from current federal income taxes. Also, because the contributions to these plans are made on a before-tax basis, the contributions are worth more. However, these plans often impose certain limitations, such as having maximum annual contributions, limiting access to funds before retirement or termination of employment, and having required minimum distribution rules and dates.

2. Tax-free: Tax-free retirement funding vehicles offer investors nontaxable earnings, but the downside is that contributions to them are made with after-tax funds. Two types of funding vehicles that offer tax-free distributed income for qualified distributions are municipal bonds, which are debt obligations of a state or local government entity, and Roth IRAs. Unlike funds contributed to tax-deductible and tax-deferred funding vehicles, contributions made to these vehicles may be withdrawn without penalty (in most cases) or taxes.

3. Tax-deferred: Tax-deferred funding vehicles delay the taxation of investment earnings until the earnings are distributed. Unlike tax-deductible and tax-deferred investment vehicles, contributions to tax-deferred funding vehicles are made with after-tax funds, such as with a nonqualified annuity. No contribution limitations or lifetime required minimum distribution (RMD) rules apply to nonqualified annuities, but withdrawals may subject the owner to surrender charges; unfavorable last-in, first-out (LIFO) tax treatment; and tax penalties (if withdrawals are made before age 59.5).

4. Currently taxable: Currently taxable funding vehicles are financial products in which after-tax investments are made, and their earnings are taxable in the year credited. So, when calculating income for tax purposes each year, an individual must include—and pay taxes on—any earnings from the investment product. In short, currently taxable funding vehicles offer individuals no accumulation tax advantages. Currently, taxable funding vehicles include certificates of deposit (CDs), regular savings accounts, money market accounts, and money market mutual funds. The principal benefit of these funding vehicles is that they make it easy to access funds.

176

Unit 25. The Retirement Planning Process and Retirement Savings Needs

Unit 25.d. Determining Retirement Savings Needs Individuals can determine their retirement income needs by using the income

replacement ratio method or the expense method. Those needs must be converted to an annual savings requirement that the individual can fulfill by contributing funds to assorted investment vehicles. At retirement, the annual income required to supplement traditional pension and Social Security benefits is taken from the individual's savings as periodic annuity payments or through annual withdrawals.

Unit 25.e. Methods for Determining Retirement Income NeedsDetermining an individual’s corresponding income needs in retirement is

based on certain assumptions—so, although the estimated results may not be precise, they provide a starting point in retirement income planning. (1) Income replacement ratio method: The individual's estimated earned income in the final three years of employment is averaged together. A specified percentage (generally 60 percent to 80 percent) is then applied to that figure to approximate the amount of income that person will need in the first retirement year. (2) Expense method: Estimates needed retirement income by considering the retiree’s anticipated total expenses in the first year of retirement. Because a retiree's expense estimate is particularly speculative when retirement is many years away, the financial planning professional and the individual should estimate the needed income and revise it regularly.

As part of the retirement income needs calculation, any income provided by traditional pension and Social Security benefits is subtracted from the income needs. This difference is the retirement income shortage, or the amount of income that the retiree will require from personal retirement savings. After this deduction, the annual savings requirement is determined and annual individual contributions begin. In most cases, less income is needed once a person retires because many expenses decline (such as mortgage payments, college costs, and work clothing). However, other types of expenses may increase, such as those for healthcare, additional travel and vacationing, and hobbies.

177

Chapter 7. Funding Retirement

Unit 25.f. Determining What Is Needed From Annual SavingsTo determine the annual savings needed for retirement goals, a person must

complete two calculations, likely with help from a financial planning professional: retirement income shortfall and annual retirement funding contribution necessary to counteract this shortfall.

First, however, the financial planner and individual must make assumptions about these factors: (1) The amount of annual income needed during retirement (2) The length of time the retirement income will be provided (3) The amount of income that will be provided by Social Security and defined-benefit pension plans (4) The projected value of existing retirement assets at retirement (5) Anticipated inflation and investment return rates.

After determining an individual's retirement income needs, the financial planning professional and individual can calculate the current annual savings needed and determine the funding vehicles to use during the accumulation period. Retirement savings can accrue through investments in funding vehicles that are tax deductible, tax free, tax deferred, and/or currently taxable.

The second phase of retirement planning, the distribution period, begins when the person retires. He or she may choose to receive funds through annual withdrawals from the supplemental fund or through an annuity providing fixed or variable periodic payments.

178

Unit 25. The Retirement Planning Process and Retirement Savings Needs

Unit 25.g. Case 1: Determining What Is Needed From Annual SavingsBill is a 45-year-old corporate manager earning an annual salary of $100,000.

He plans to retire in 20 years, at age 65, and expects to need 75 percent of his earned income to maintain his lifestyle in retirement. Bill wants to accumulate a fund sufficient to provide retirement income for 25 years. His Social Security retirement and defined-benefit pension plan benefits will provide $45,000 per year, and with $440,153 of savings earmarked for retirement, his retirement income shortfall to be funded would be $30,000. He assumes 5 percent inflation, a 4 percent after-tax return before retirement, and a 3 percent after-tax return during retirement.

Because Bill will not be retiring for another 20 years, the retirement income shortfall will be subjected to an annual inflation rate of 5 percent. Using a financial calculator to determine the future value of this amount, he finds that his shortfall will be the equivalent of $79,599. The present value (at retirement) of the $79,599 retirement income shortfall for 25 years, discounted at 3 percent (the expected return), is $1,427,648. This is the value of the funds Bill needs to accumulate by the retirement date to produce an annual income equal to the shortfall for 25 years.

Bill's current retirement savings of $440,153 can be expected to grow at an annual after-tax rate of 4 percent for 20 years. Thus, the future value of Bill's savings is $964,421. The additional amount Bill needs to accumulate can be determined by subtracting $964,421 from the $1,427,648 required funds at retirement. To determine the amount Bill must contribute each year to his supplemental retirement fund, assuming the fund will grow by 4 percent each year for 20 years, the future value of an annuity worth $463,227 must be found. The resulting annual required contribution is $15,556.

Unit 25.h. Case 2: Determining What Is Needed From Annual SavingsChloe, age 40, has no retirement savings and, after considering Social Security

and traditional pension benefits, needs to accumulate a retirement fund that will provide her with $20,000 of supplemental retirement income (in current dollars). Explain how Chloe could determine her annual saving need if she wants to retire at age 65 and expects annual inflation to be 4 percent, assumes a 25-year retirement period, and expects a 6 percent after-tax return before retirement and a 3 percent after-tax return on invested assets during retirement.

The first step in the calculation would be to convert Chloe's retirement income shortfall (in current dollars) to the anticipated shortfall at the time she retires in 25 years using the assumption of 4 percent inflation. Next, she would determine the amount needed at the beginning of her retirement and invested at a 3 percent after-tax return over her 25-year retirement period to find how much money she will need to save to meet her retirement income goals. Finally, Chloe would need to calculate the annual contribution that would be required by finding the future value of an annuity for that amount, assuming a 6 percent return on investment for the 25-year period before she retires.

179

Chapter 7. Funding Retirement

Unit 25.1. Questions: The Retirement Planning Process and Retirement Savings Needs

1. Financial needs analysis is part of the financial planning process. This analysis translates an individual's retirement goals into An accumulation goal that must be met.2. Traditional individual retirement accounts (IRAs) is categorized as both tax-

deductible and tax-deferred.3. Ease in which funds can be accessed, is the principal advantage of

accumulating retirement funds in a currently taxable funding vehicle. 4. Although many expenses typically decline in retirement, certain types of

expenses may increase. One type of expense that falls into this category is Travel.5. When determining annual savings needs for retirement, Anticipated

inflation must be taken into account.6. Tim and Peg has their retirement savings allocated in a variety of financial

products with differing tax treatments. Money market mutual fund would be considered currently taxable.7. Now that their children are grown, Timothy and Zoe feel they have the

resources to plan for their retirement, which they expect will be in about fifteen years. They are in good health and hope to have a long retirement to enjoy their hobbies and to travel. Over what period should they take into account the effect of inflation? During their current planning period and through their entire retirement years. 8. Jerry is considering two funding vehicles for retirement and will put the

same amount of money into either. His financial adviser has told him that one of the investments will actually leave him with more current spendable money. Contributions to only one of the funding vehicles are tax deductible, explains the adviser's comment?9. Eileen is planning her retirement and is using the income replacement ratio

method to determine her needed retirement income. She should start by averaging estimated earned income during The final three years of employment.10. Joel is a 50-year-old accountant who is earning an annual salary of

$150,000. He plans to retire at age 65, and expects to need 80 percent of his earned income to maintain the lifestyle that he desires for retirement. His Social Security retirement will provide an annual income of $30,000 and his defined-benefit pension will provide an annual income of $45,000. What is Joel's annual retirement income shortfall that needs to be funded? $45,000.

180

Unit 25. The Retirement Planning Process and Retirement Savings Needs

181

Chapter 7. Funding Retirement

Unit 26. Employer-Sponsored Retirement Plans Reference: CPCU 553 Online 1st edition, Assignment 7. Module 3

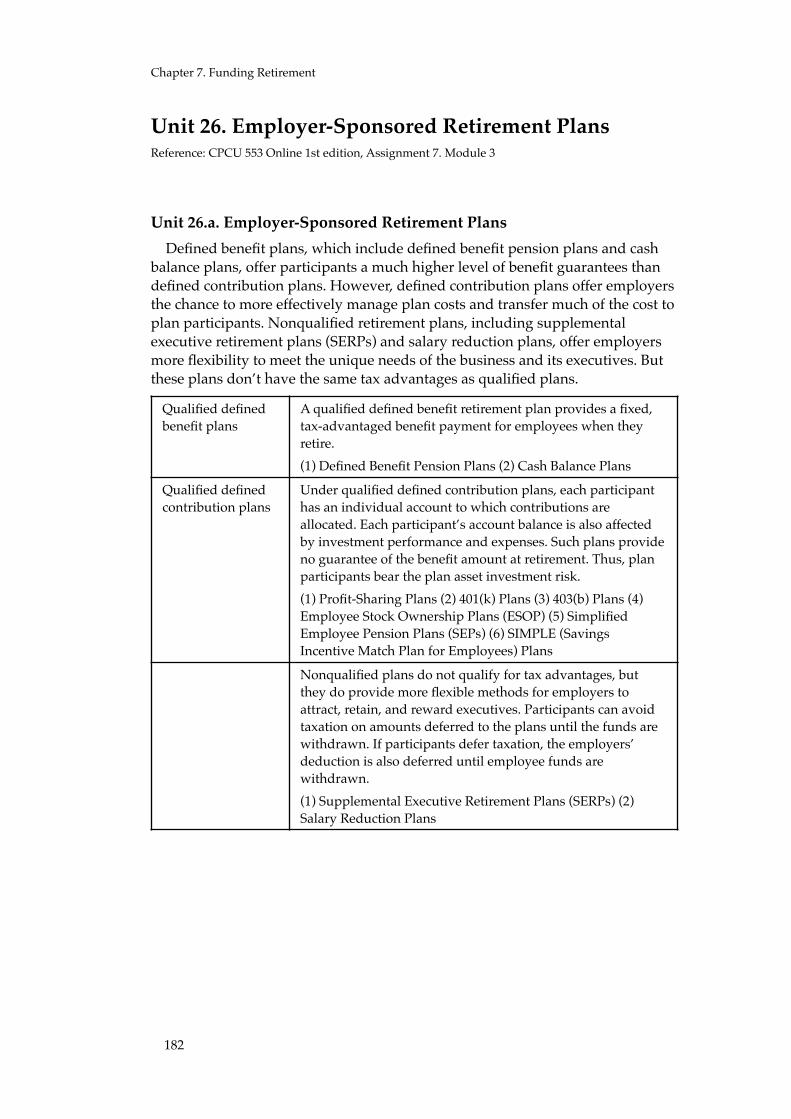

Unit 26.a. Employer-Sponsored Retirement Plans Defined benefit plans, which include defined benefit pension plans and cash

balance plans, offer participants a much higher level of benefit guarantees than defined contribution plans. However, defined contribution plans offer employers the chance to more effectively manage plan costs and transfer much of the cost to plan participants. Nonqualified retirement plans, including supplemental executive retirement plans (SERPs) and salary reduction plans, offer employers more flexibility to meet the unique needs of the business and its executives. But these plans don’t have the same tax advantages as qualified plans.

Qualified defined benefit plans

A qualified defined benefit retirement plan provides a fixed, tax-advantaged benefit payment for employees when they retire. (1) Defined Benefit Pension Plans (2) Cash Balance Plans

Qualified defined contribution plans

Under qualified defined contribution plans, each participant has an individual account to which contributions are allocated. Each participant’s account balance is also affected by investment performance and expenses. Such plans provide no guarantee of the benefit amount at retirement. Thus, plan participants bear the plan asset investment risk. (1) Profit-Sharing Plans (2) 401(k) Plans (3) 403(b) Plans (4) Employee Stock Ownership Plans (ESOP) (5) Simplified Employee Pension Plans (SEPs) (6) SIMPLE (Savings Incentive Match Plan for Employees) Plans

Nonqualified plans Nonqualified plans do not qualify for tax advantages, but they do provide more flexible methods for employers to attract, retain, and reward executives. Participants can avoid taxation on amounts deferred to the plans until the funds are withdrawn. If participants defer taxation, the employers’ deduction is also deferred until employee funds are withdrawn. (1) Supplemental Executive Retirement Plans (SERPs) (2) Salary Reduction Plans

182

Unit 26. Employer-Sponsored Retirement Plans

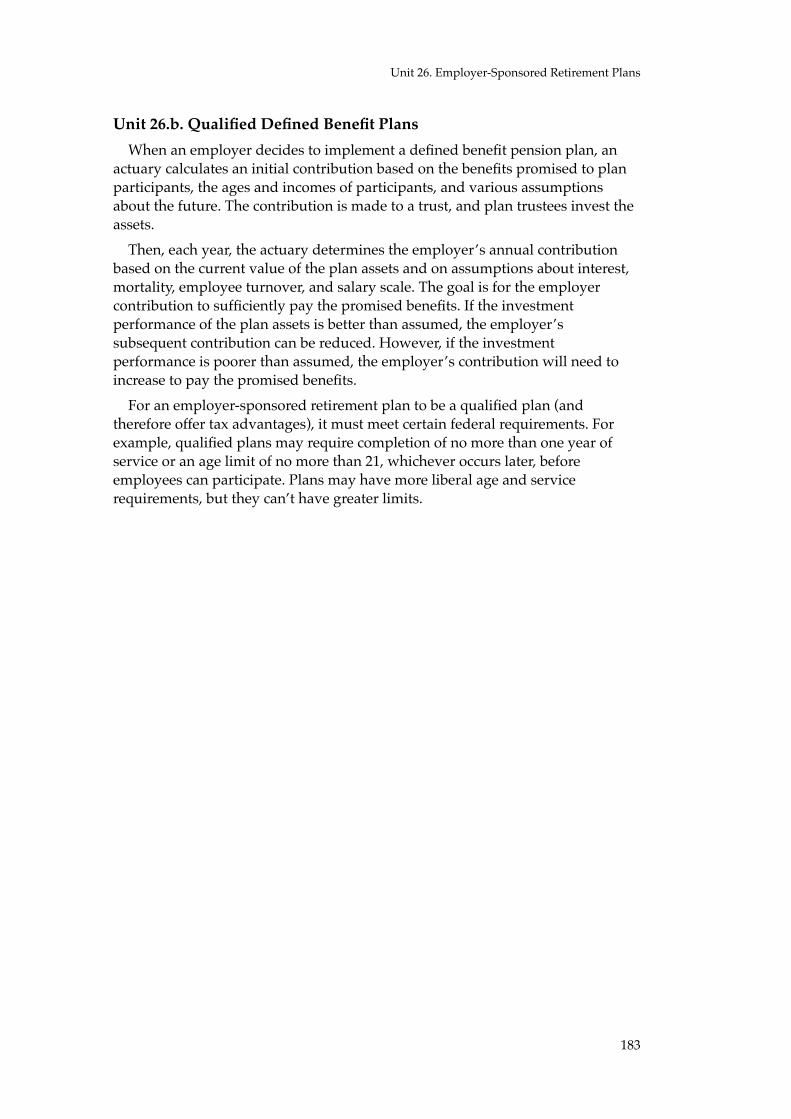

Unit 26.b. Qualified Defined Benefit Plans When an employer decides to implement a defined benefit pension plan, an

actuary calculates an initial contribution based on the benefits promised to plan participants, the ages and incomes of participants, and various assumptions about the future. The contribution is made to a trust, and plan trustees invest the assets.

Then, each year, the actuary determines the employer’s annual contribution based on the current value of the plan assets and on assumptions about interest, mortality, employee turnover, and salary scale. The goal is for the employer contribution to sufficiently pay the promised benefits. If the investment performance of the plan assets is better than assumed, the employer’s subsequent contribution can be reduced. However, if the investment performance is poorer than assumed, the employer’s contribution will need to increase to pay the promised benefits.

For an employer-sponsored retirement plan to be a qualified plan (and therefore offer tax advantages), it must meet certain federal requirements. For example, qualified plans may require completion of no more than one year of service or an age limit of no more than 21, whichever occurs later, before employees can participate. Plans may have more liberal age and service requirements, but they can’t have greater limits.

183

Chapter 7. Funding Retirement

Unit 26.c. Defined Benefit Pension Plans and Cash Balance Plans A qualified defined benefit retirement plan may be a defined benefit pension

plan or a cash balance plan. 1. Defined Benefit Pension PlansA defined benefit pension plan is often referred to as a traditional pension

plan. A person’s promised benefits under this type of plan are stated as life income that is paid out starting at normal retirement age—which is typically calculated based on age and years of employment. The promised life income can be calculated using various formulas. Flat benefit and unit benefit formulas are the most common.

Under a flat benefit formula, the life income payable at retirement is based solely on the participant’s salary. A typical flat benefit formula might provide a monthly pension benefit equal to 45 percent of the participant’s final average monthly salary. Under a unit benefit formula, both income and years of service are taken into consideration. For example, the plan may provide a benefit equal to 1.5 percent of a person’s final average monthly salary multiplied by years of service (capped at 30 years).

2. Cash Balance PlansA cash balance plan is a defined benefit plan that looks and operates similar to

a defined contribution plan. Rather than using a formula that’s based on age, salary, or years of service to calculate a person’s benefit payments, a cash balance plan uses an individual’s account balance. But as with any defined benefit plan, the employer is required to make an actuarially determined annual contribution sufficient to pay the promised benefit.

Under a cash balance plan, every plan participant has a hypothetical account. Each year, the account statement is published showing both benefit and interest credits to the account. Benefit credits may be a fixed percentage of earnings for all participants or a percentage of earnings that varies based on age or length of service. Despite their popularity with employees, defined benefit plans are steadily being replaced by defined contribution plans, which shift the financial burden of funding retirement plans from employers to employees.

184

Unit 26. Employer-Sponsored Retirement Plans

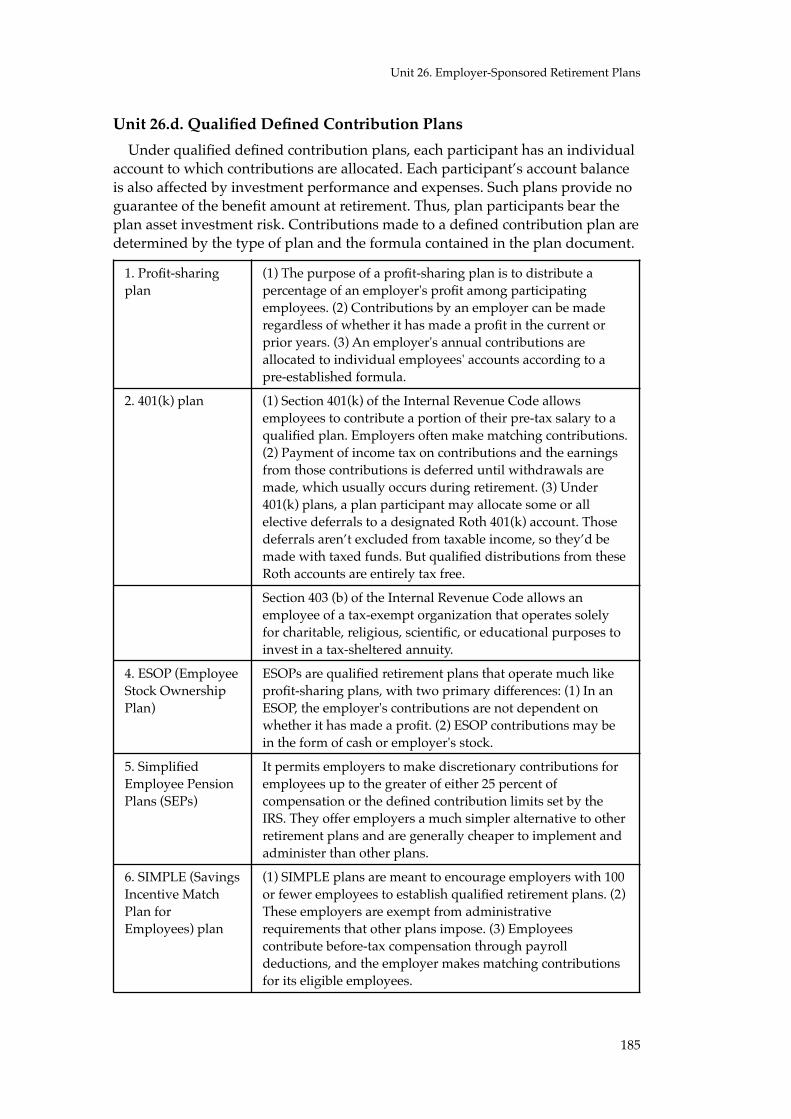

Unit 26.d. Qualified Defined Contribution Plans Under qualified defined contribution plans, each participant has an individual

account to which contributions are allocated. Each participant’s account balance is also affected by investment performance and expenses. Such plans provide no guarantee of the benefit amount at retirement. Thus, plan participants bear the plan asset investment risk. Contributions made to a defined contribution plan are determined by the type of plan and the formula contained in the plan document.

1. Profit-sharing plan

(1) The purpose of a profit-sharing plan is to distribute a percentage of an employer's profit among participating employees. (2) Contributions by an employer can be made regardless of whether it has made a profit in the current or prior years. (3) An employer's annual contributions are allocated to individual employees' accounts according to a pre-established formula.

2. 401(k) plan (1) Section 401(k) of the Internal Revenue Code allows employees to contribute a portion of their pre-tax salary to a qualified plan. Employers often make matching contributions. (2) Payment of income tax on contributions and the earnings from those contributions is deferred until withdrawals are made, which usually occurs during retirement. (3) Under 401(k) plans, a plan participant may allocate some or all elective deferrals to a designated Roth 401(k) account. Those deferrals aren’t excluded from taxable income, so they’d be made with taxed funds. But qualified distributions from these Roth accounts are entirely tax free.

3. 403(b) plan Section 403 (b) of the Internal Revenue Code allows an employee of a tax-exempt organization that operates solely for charitable, religious, scientific, or educational purposes to invest in a tax-sheltered annuity.

4. ESOP (Employee Stock Ownership Plan)

ESOPs are qualified retirement plans that operate much like profit-sharing plans, with two primary differences: (1) In an ESOP, the employer's contributions are not dependent on whether it has made a profit. (2) ESOP contributions may be in the form of cash or employer's stock.

5. Simplified Employee Pension Plans (SEPs)

It permits employers to make discretionary contributions for employees up to the greater of either 25 percent of compensation or the defined contribution limits set by the IRS. They offer employers a much simpler alternative to other retirement plans and are generally cheaper to implement and administer than other plans.

6. SIMPLE (Savings Incentive Match Plan for Employees) plan

(1) SIMPLE plans are meant to encourage employers with 100 or fewer employees to establish qualified retirement plans. (2) These employers are exempt from administrative requirements that other plans impose. (3) Employees contribute before-tax compensation through payroll deductions, and the employer makes matching contributions for its eligible employees.

185

Chapter 7. Funding Retirement

Unit 26.e. Nonqualified PlansNonqualified plans do not qualify for tax advantages, but they do provide

more flexible methods for employers to attract, retain, and reward executives. Participants can avoid taxation on amounts deferred to the plans until the funds are withdrawn. If participants defer taxation, the employers’ deduction is also deferred until employee funds are withdrawn. An employer may choose to include only one or several executives in a nonqualified plan. The executives chosen obtain the benefits of the nonqualified plan as well as those of any qualified plan sponsored by the employer.

A plan can be funded or unfunded, which has implications for participant taxation and security. In a funded plan, the employer sets aside funds in a trust to pay the promised benefits. These funds are safe from the company’s general creditors but are taxable to an executive once they are either contributed to the plan or the executive becomes vested in the benefit. Because of this, nonqualified retirement plans are usually designed to be unfunded. A nonqualified plan is considered unfunded and not subject to adverse tax consequences if it is not backed by a reserve or if an established reserve is subject to the claims of a creditor.

Unit 26.f. Supplemental Executive Retirement Plans and Salary Reduction Plans

Nonqualified retirement plans are available as supplemental executive retirement plans (SERPs) and salary reduction plans. The difference relates to whether the employer or the participant pays for the benefit.

1. Supplemental Executive Retirement PlansIn a SERP, the plan participant doesn’t defer any compensation to the plan. The

employer promises to pay the participant or a beneficiary a specified dollar amount for a period of years after the participant retires or dies, whichever comes first. SERPs often act as golden handcuffs, tying participants to employers by including forfeiture provisions for those who leave an employer’s service before a specified number of years, go to work for a competitor, or open a competing business.

2. Salary Reduction PlansSalary reduction plans are sometimes referred to as true deferred

compensation plans because plan participants defer compensation until they may be in a lower marginal income tax bracket—at retirement, for example. Although a salary reduction plan may appear to emulate a 401(k) plan, a significant difference between the two relates to the limits applied to the elective deferral amount: No dollar limit applies to funds deferred under salary reduction plans. And because the deferred funds are the participant’s earned money, deferrals are typically nonforfeitable.

186

Unit 26. Employer-Sponsored Retirement Plans

Unit 26.1. Questions: Employer-Sponsored Retirement Plans

1. Whether the employer or the participant pays for the benefits is the major distinction between a supplemental executive retirement plan (SERP) and a nonqualified salary reduction plan.2. Supplemental executive retirement plan is a non qualified retirement plan. 3. A qualified plan must have minimum vesting standards. Vesting refers to A

plan participant's nonforfeitable right to his or her accrued plan benefit.4. Automatic survivor benefits as appropriate, is a characteristic of a qualified

retirement plan.5. A retirement plan that guarantees a benefit of 50 percent of final salary after

30 years of service is an example of a Defined benefit plan.6. An employee stock ownership plan (ESOP) can serve as an estate planning

tool for closely held business owners.7. Samantha is covered by a 401 (k) plan at work. She contributes 8 percent of

her salary to the plan, and her employer makes a matching 4 percent contribution. Which one of the following statements about the federal income taxation associated with her participation in the plan is true? Plan income is deferred until distributed. 8. Herb and his wife are the sole stockholders of a small closely held

corporation. They have decided to establish an employee retirement plan that they can also use as an estate planning tool for their own retirement. Which one of the following types of qualified plan can be used for this purpose? Employee stock ownership plan.9. Brad is single and 50 years old. He recently had a promotion at work and

has decided to use some of his salary increase to fund additional retirement income. He participates in the 403(b) plan of his employer, but he contributes just enough to get the full employer matching contribution. He has not made any additional elective deferrals under the plan, even though he could do so. His adjusted gross income this year is such that he can only contribute to an IRA on an after-tax basis, and he is ineligible to establish a Roth IRA. He expects to be in a low income tax bracket after retirement, and his objective today is to minimize his current taxable income. Which one of the following would best meet Brad's objective? Additional elective deferrals under the 403(b) plan.

187

Chapter 7. Funding Retirement

Unit 27. Individual Retirement Accounts (IRA) Reference: CPCU 553 Online 1st edition, Assignment 7. Module 4

Unit 27.a. Comparing Individual Retirement Accounts Being able to advise clients on how to prepare for their perfect retirement

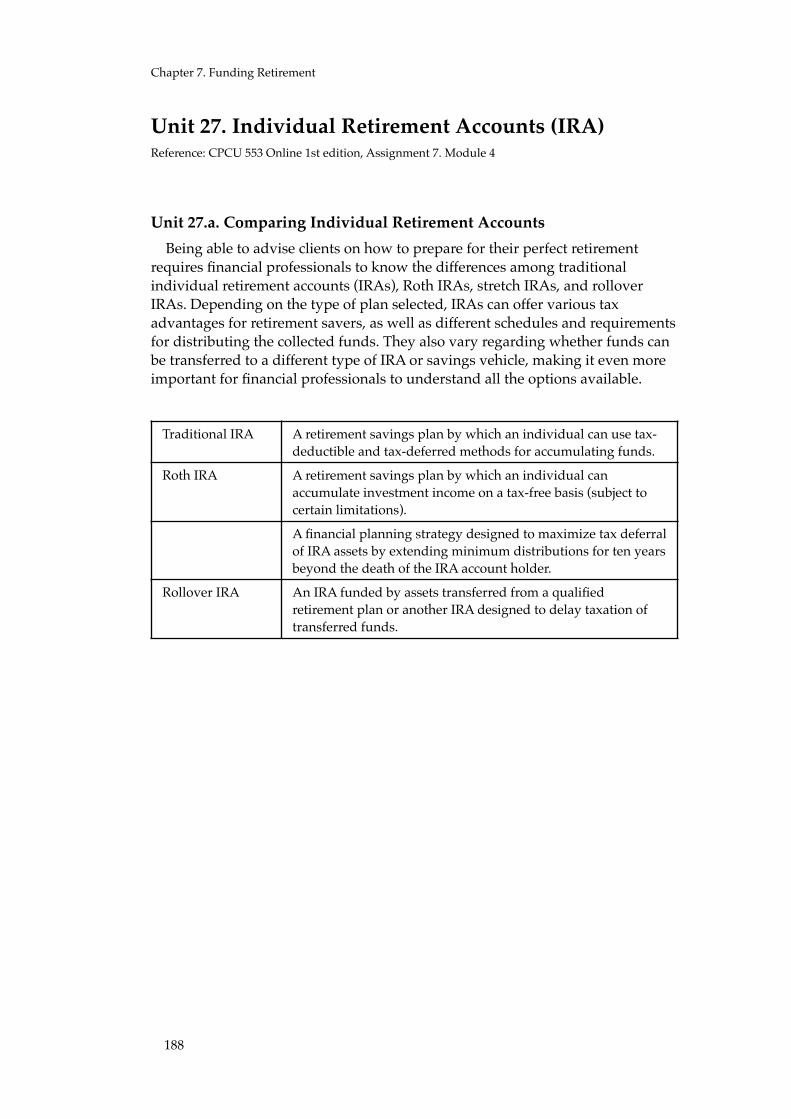

requires financial professionals to know the differences among traditional individual retirement accounts (IRAs), Roth IRAs, stretch IRAs, and rollover IRAs. Depending on the type of plan selected, IRAs can offer various tax advantages for retirement savers, as well as different schedules and requirements for distributing the collected funds. They also vary regarding whether funds can be transferred to a different type of IRA or savings vehicle, making it even more important for financial professionals to understand all the options available.

Traditional IRA A retirement savings plan by which an individual can use tax-deductible and tax-deferred methods for accumulating funds.

Roth IRA A retirement savings plan by which an individual can accumulate investment income on a tax-free basis (subject to certain limitations).

Stretch IRA A financial planning strategy designed to maximize tax deferral of IRA assets by extending minimum distributions for ten years beyond the death of the IRA account holder.

Rollover IRA An IRA funded by assets transferred from a qualified retirement plan or another IRA designed to delay taxation of transferred funds.

188

Unit 27. Individual Retirement Accounts (IRA)

Unit 27.b. Traditional IRATraditional individual retirement accounts (IRAs) allow owners to contribute

to retirement savings accounts with funds that, in most cases, can be deducted from their income for tax purposes. An eligibility rule that applies to all traditional IRAs, except for spousal IRAs, requires individuals to have received earned income in the year the contribution is made. For purposes of traditional IRA eligibility, earned income includes salary, fees, tips, bonuses, commissions, and alimony. Unearned income, such as royalties, rent, interest, dividends, and capital gains, doesn't count toward IRA eligibility.

While a spousal IRA doesn’t require the owner to have earned income, the owner (spouse) must be married and file a joint federal income tax return with his or her spouse. A spousal IRA established by a nonworking spouse cannot be combined with an IRA owned by the working spouse; a separate IRA must be established. Traditional IRA contributions are limited to the lesser of earned income or the yearly contribution limit established by the Internal Revenue Service (IRS). Individuals age 50 or older can make additional contributions (called catch-up contributions) up to the IRS limit. Both IRS limits may be adjusted based on inflation. Also, the maximum permitted contribution to a traditional IRA is reduced by any amount contributed to a Roth IRA for the same year.

A traditional IRA contribution can be deducted from taxable income. However, if an account owner is also an active participant in an employer-sponsored retirement plan, the amount that person is allowed to deduct may be reduced or eliminated, depending on his or her adjusted gross income (AGI) and tax-filing status. Nonetheless, even if the deductibility is reduced or eliminated, the participant can still make a nondeductible traditional IRA contribution. In a traditional IRA, pretax contributions and the earnings on them are taxed when they are distributed (withdrawn). When contributions are made on an after-tax basis, they (and the earnings from them) are not taxed again when they are distributed.

Traditional IRA distributions that are taxed are also subject to a 10 percent premature distribution tax penalty (unless a specific exception to the penalty applies) if they are withdrawn before age 59.5. The IRS requires owners of a traditional IRA to begin taking required minimum distributions (RMDs) each year once they reach age 72. This is because the IRS doesn’t want funds sitting in the account indefinitely. The IRS has a formula for determining an individual’s RMD.

189

Chapter 7. Funding Retirement

Unit 27.c. Roth IRAsRoth IRAs also permit owners to make contributions to retirement savings

accounts, but contributions are never tax-deductible because they are made with after-tax funds. In contrast to a traditional IRA, Roth IRA eligibility is affected by the person’s AGI but not age. In addition, a person needs to have earned income (except in the case of a spousal Roth IRA) and an AGI that does not exceed certain limits. (These limits can change annually.) An individual can establish a spousal Roth IRA if he or she is married and files a federal income tax return as married filing jointly. Like a spousal traditional IRA, a spousal Roth IRA cannot be combined with a working spouse’s IRA.

Roth IRA contributions are also limited to the lesser of earned income or the yearly contribution limit established by the IRS. And individuals age 50 or older can make catch-up contributions up to the IRS limit. The maximum permitted contribution to a Roth IRA is reduced by any amount contributed to a traditional IRA for the same year. Because all contributions to a Roth IRA are made on an after-tax basis, distributions are entirely tax free—but must be made after five taxable years (beginning with the year in which the person made the first contribution).

A Roth IRA distribution of earnings that doesn’t meet these criteria is known as a nonqualified distribution and is taxable as ordinary income. In addition, if a nonqualified distribution is made before the Roth IRA owner becomes 59.5, it is subject to a 10 percent premature distribution tax penalty on the amount of the distribution that is taxable. Unlike traditional IRA owners, Roth IRA owners aren’t required to make RMDs during the owner’s lifetime. This can be a big advantage for Roth IRAs because it helps the funds grow tax free.

Unit 27.d. Stretch IRAsIRAs are all subject to a “required beginning date.” This is the date by which