Embed Size (px)

Citation preview

VOLUME 9, NUMBER 2, 2011 1

Abstract: Capital investment projects with inherent flexibility provide valuable options for responding to changes in the business environment. While conventional investment appraisal methods fail to capture the value of this flexibility, real options analysis (ROA) has been proposed as a useful alternative, despite being challenging to implement.

This study examines how project flexibility is considered in practice. It focuses on local government organisations (LGOs), which typically have significant capital investment programmes that need to be responsive to changing operating conditions. A questionnaire (mailed to the financial directors of New Zealand LGOs) was combined with follow-up interviews to facilitate data triangulation.

The findings reveal that LGO managers recognize the value of project flexibility and take it into account to some extent. However, there was no evidence that formal ROA procedures are used in practice. These findings are of relevance to financial decision-makers concerned with assessing capital investment projects in the public sector.

Capturing the Value of Flexibility in Public Sector Capital Investment Projects: Evidence from New Zealand Local Government Organisations

ZAHIR AHMED THE AUCKLAND UNIVERSITY OF TECHNOLOGY

ALI ELHARIDY THE AUCKLAND UNIVERSITY OF TECHNOLOGY

KRISTINE FU THE AUCKLAND UNIVERSITY OF TECHNOLOGY

DERYL NORTHCOTT THE AUCKLAND UNIVERSITY OF TECHNOLOGY

Corresponding Author:

Professor Deryl Northcott, Department of Accounting, AUT Business School, The Auckland University of Technology, Private Bag 92006, Auckland 1142, New Zealand.

Email: [email protected]

Keywords: Capital investment; real options analysis; flexibility; public sector; local government organisations

INTRODUCTIONTraditional investment appraisal methods, such as Discounted Cash Flow (DCF) analysis, assume a static environment where the life of an investment is known and the cash-flows related to the investment can be estimated (Majd and Pindyck 1987). However, these methods have been criticised for neglecting to value the flexibility embedded in some capital investment projects (Adler 2000; Busby and Pitts 1998; Cheung 1993; Copeland and Howe 2002; Cotter, Marcum and Martin 2003; Hammer 2002; Myers 1984; Pike, Sharp and Price 1989; Slagmulder, Bruggeman and Wassenhove 1995).

NEW ZEALAND JOURNAL OF APPLIED BUSINESS RESEARCH 2

Where a capital investment project incorporates the possibility of flexibility, real options analysis (ROA) has been advocated as a means of addressing the limitations of traditional analysis methods because it both recognizes project flexibility and quantifies its value (Amram and Howe 2002; Anderson 2000; Barnett 2005; Benaroch and Kauffman 1999; Busby and Pitts 1998; Cheung 1993; Dixit and Pindyck 1994, 1995; Trigeorgis 1993, 1997). The concept of real options was initially derived from the financial options pricing model in 1973 (Black and Scholes 1973; Cox, Ross and Rubinstein 1979), although real options are associated with investments in real assets such as property, plant, equipment, production lines and machinery rather than investments in financial securities (Busby and Pitts 1998). ROA provides a means of valuing the flexibility, (that is, options) embedded in strategic projects, such as the potential to expand, defer, temporarily close down or abandon a capital project (Trigeorgis 1993). Such flexibility has value because it allows managers more scope to maximize future opportunities and minimize future losses as more information becomes available (Alkaraan and Northcott 2006; Barnett 2005; Schubert and Barenbaum 2007).

The use of real options analysis to value project flexibility has been investigated in private sector contexts such as the manufacturing, pharmaceutical, financial services and information technology (IT) industries (Adams 2004; Busby and Pitts 1997; Chen, Zhang and Lai 2009; Hartmann and Hassan 2006). However, there have been few studies of how real options analysis is used in public sector organisations, even through capital investment decisions are amongst the most important made in the public sector (Chan 2004; Kensinger and Crawford 2010; Schubert and Barenbaum 2007). Many public sector investment projects are strategic and long-term in nature, require large financial commitments and involve multiple sources of uncertainty such as changes in user demand, technology, public priorities and political agenda (Kensinger and Crawford 2010; Schubert and Barenbaum 2007).

This study focuses on local government organisations (LGOs) as examples of public sector organisations that face considerable uncertainty in their future operating environment. In New Zealand the LGO sector comprises regional, city and district councils. These autonomous organisations are funded largely by rates and are regulated by a series of local government acts. They are accountable to the communities they serve for the provision of a wide range of services including flood control, reserves management, rubbish collection, street lighting and local tourism (Guide to Local Government 2004). It is estimated that, in combination, New Zealand LGOs manage long-term assets worth $NZ32.5 billion and invest around $NZ800 million in capital assets each year (Guide to Local Government 2004), suggesting that capital investment decision-making is an important activity in this sector. The significant economic, demographic and political uncertainties confronting these organisations mean that, if flexibility exists in LGOs’ capital investment projects, its potential to maximise future project benefits or reduce future costs ought to be evaluated (Brealey, Cooper and Habib 1997; Schubert and Barenbaum 2007).

The aim of this study is two-fold: to explore how New Zealand LGO managers take account of flexibility when evaluating capital investment projects; and to investigate whether they use ROA-type principles or approaches in practice. This will be the first empirical study to examine this issue in the New Zealand public sector context.

The remainder of this paper is structured as follows. First, the significance of flexibility

VOLUME 9, NUMBER 2, 2011 3

and real options in capital investment projects is outlined via a brief literature review. The research method for this study is then described, followed by a presentation and discussion of the findings. Conclusions and reflections on implications for practice then follow.

FLEXIBILITY AND REAL OPTIONS IN CAPITAL INVESTMENT ANALYSISIf a capital investment project has inherent flexibility, there is greater potential for managers to change how the project takes shape rather than remaining locked into a decision made in the face of uncertainty (Busby and Pitts 1997, 1998; Copeland 2001; MacDougall and Pike 2003). Project flexibility can be defined as “situations where, for a time, we can avoid making irreversible commitments in the face of uncertainty” (Busby and Pitts 1998, p2) or more colloquially, “the ability to keep one’s options open”. Flexibility grants managers a degree of freedom to achieve better outcomes than were initially expected (Bengtsson 2001), or to observe future events, acquire further information and re-plan an investment before making an irreversible commitment to it (Copeland and Howe 2002; Cotter et al. 2003).

When a form of flexibility exists, a ‘real option’ arises (Brookfield 1995). Real options are defined as “manifestations of managerial flexibility, each enabling management to respond to changing business and economic conditions” (Busby and Pitts 1998, p 17). There are several forms that real options can take. These include the ability to: postpone a project while waiting to see how future events unfold; contract or expand a project; implement a project in stages; switch between outputs or inputs of products or materials; change the project’s technologies, products or markets; or abandon a project1.

Prior studies have identified that ‘managerial flexibility’ component – that is, the real options – can add significant value to an investment project (see for example: Brennan and Schwartz 1985; Ingersoll and Ross 1992; Paddock, Siegel and Smith 1988; Grinyer and Daing 1993; Myers and Majd 1990; Herath and Park 2002; Majid and Pindyck 1987; Kaplan 1986). Flexibility should, therefore, be taken into account in appraising a capital investment project; ignoring it may misdirect managerial decision-making by undervaluing projects that incorporate real options (Feinstein and Lander 2002). The advantage of ROA over traditional, DCF-based analysis techniques lies in its ability to incorporate the value of any ‘built-in’ flexibility (Busby and Pitts 1998; Trigeorgis 2005; Van Putten and MacMillan 2004). ROA also recognizes the effects of uncertainty: the higher the uncertainty during the economic life of a capital project and the higher the volatility of the project’s future cash flows, the more valuable the options, since they will add more value to the capital project (Cotter et al. 2003). ROA allows managers to exploit investment opportunities by exercising only those flexibility options it expects to have positive cash flow effects (Mills, Weinstein and Favato 2006). Therefore, their value always exceeds (or is at least equal to) zero (Gotze, Northcott and Schuster 2008).

Despite the theoretical advantages of using ROA to account for flexibility in capital investment projects, there are practical challenges in doing so. Since ROA is conceptually and mathematically complex, managers may find it difficult to understand and

1For discussions of these option types, see: Amran and Howe 2003; Anderson 2000; Bengtsson 2001; Bowe and Lee 2004; Brookfield 1995; Busby and Pitts 1997, 1998; Cheung 1993, Copeland and Keenan 1998; Cotter et al. 2003; Fichman, Keil and Tiwana 2005; Hammer 2002; McDonald and Siegel 1986; Trigeorgis 1993, 2005; Yeo and Qiu 2003.

NEW ZEALAND JOURNAL OF APPLIED BUSINESS RESEARCH 4

communicate the significance of ROA results (Block 2007; Busby and Pitts 1997). Also, Net Present Value (NPV) remains the preferred investment appraisal method because it is a proven and well-established technique (Alkaraan and Northcott 2006). Further, it has been suggested that using ROA may be perceived as encouraging risk-taking, since it attributes higher values to flexible projects, even (or especially) where the investment environment is uncertain (van Putten and MacMillan 2004). Reflecting these challenges, several international studies show that private sector managers still prefer conventional project analysis techniques over ROA (Alkaraan and Northcott 2006; Block 2007; Busby and Pitts 1997; Bowman and Moskowitz 2001; Cotter et al. 2003; MacDougall and Pike 2003).

Although ROA calculations are not widely employed in practice, some studies suggest managers understand the importance of identifying inherent flexibility in capital investment projects and do use real options-type heuristics to assess embedded flexibility in an intuitive or qualitative way (Busby and Pitts 1997; Howell and Jagle 1997; McGrath and Nerkar 2004). So, in studying how project flexibility is assessed in practice it is important to consider whether (and how) ROA-type concepts are employed, even where full ROA analysis is not used. This study examines this issue in the context of public sector organisations (LGOs). The research methods for doing so are outlined next.

RESEARCH METHODSThis study adopted a mixed methods approach, combining a survey questionnaire with follow-up interviews to examine LGO managers’ experiences and views on how project flexibility is captured in capital investment decision-making.

Questionnaire SurveyFirst, a questionnaire survey was used to collect data across the entire New Zealand LGO sector. Earlier studies on real option analysis and related themes have also used this approach to assess the use of ROA-type principles in evaluating capital investment projects (see for example: Alkaraan and Northcott 2006; Busby and Pitts 1997; Block 2007).

The questionnaire was mailed to all 86 New Zealand local government organisations2, including regional councils, city councils and district councils. It was addressed to the financial director, since he/she is the person in the organisation most likely to be involved in capital investment decision-making and is, therefore, the most knowledgeable and appropriate person to complete the questionnaire. Respondents were asked to answer 17 questions - a combination of structured and open-ended questions aimed at discovering their views and practices in regard to the assessment of capital investment project flexibility in their LGOs.

Respondents were given 17 days during April 2010 to complete and return the questionnaire. Since mail questionnaires typically suffer low response rates, three tactics were employed to address this. A cover letter was enclosed to explain the purpose of this research and to guarantee the confidentiality of the information provided by respondents. Follow-up emails were sent to non-respondents, the first three weeks after mailing out the questionnaire and the second two weeks later. A soft copy of the questionnaire was attached to the second reminder email in case the initial hard copy had been lost. 2There were 86 LGOs in New Zealand at the time this survey was conducted (April 2010).

VOLUME 9, NUMBER 2, 2011 5

Twenty-one LGOs returned their questionnaires, giving a response rate of 24.4%, which is consistent with some prior studies in this field (for example, Alkaraan and Northcott 2006; Block 2007). Sixteen non-respondents provided emailed explanations for their decisions not to participate. These reasons fell into three main categories: (i) their LGO was small with no major capital investment projects (n=5); (ii) they had no time to complete the questionnaire due to high workloads at the time (n=9) (iii) neither the financial decision-maker of their organisation nor any other person who could complete the questionnaire was available (n=2).

Follow-up Interviews

The aims of the follow-up interviews were to probe questionnaire responses in greater depth, provide the opportunity for respondents to expand on their survey answers, and to triangulate the findings against the survey results to improve their validity. The interviews also provided the opportunity to solicit actual examples of project flexibility assessment to illustrate the issues faced in practice.

Of the 21 LGO respondents, 14 indicated their willingness to participate in follow-up interviews; five were invited to do so during May 2010. These selected five had all indicated in their questionnaires that they used ROA-type approaches to evaluate capital investment projects in their LGOs. During the interviews, participants were asked to recall an example of a recent capital investment project that had elements of flexibility, and to describe how the project’s flexibility was considered. The interviewees were also encouraged to describe their own experience in dealing with capital investment projects where flexibility might be important and valuable. Interviewees were also asked their views on the need for analysis tools to assess the flexibility embedded in some capital investment projects.

All five interviews were conducted by telephone and lasted approximately 30 minutes each. A potential benefit of conducting telephone interviews rather than face-to-face interviews is that interviewees may feel more relaxed and comfortable if the interviewer is not present (Bryman 2008). However, possible limitations of this method are that non-verbal cues cannot be observed and people may not be willing to spend as much time on a phone interview. The interviews were tape-recorded with the interviewees’ permission, to allow the researcher to capture more data than would be possible by relying on memory (Bryman and Bell 2007). Interviewees’ statements were cross-checked with their questionnaire responses for triangulation purposes (Taylor and Bogdan 1998). After the five interviews, all tape-recorded responses were transcribed and analyzed.

FINDINGSThis section reports on the characteristics of the responding LGOs, the significant findings to emerge from the questionnaire survey and follow-up interviews, and the implications of these findings in relation to extant theory. This discussion is organised into key themes below.

The Responding LGOs

The 21 responding LGOs comprised 3 regional councils, 4 city councils and 14 district councils. Respondents included 12 Financial Managers and 5 Corporate Accountants

NEW ZEALAND JOURNAL OF APPLIED BUSINESS RESEARCH 6

(including a Financial Planner and a Controller), with the remaining 4 being Chief Executives, Chief Financial Officers, or General Managers. All respondents had an accounting background.

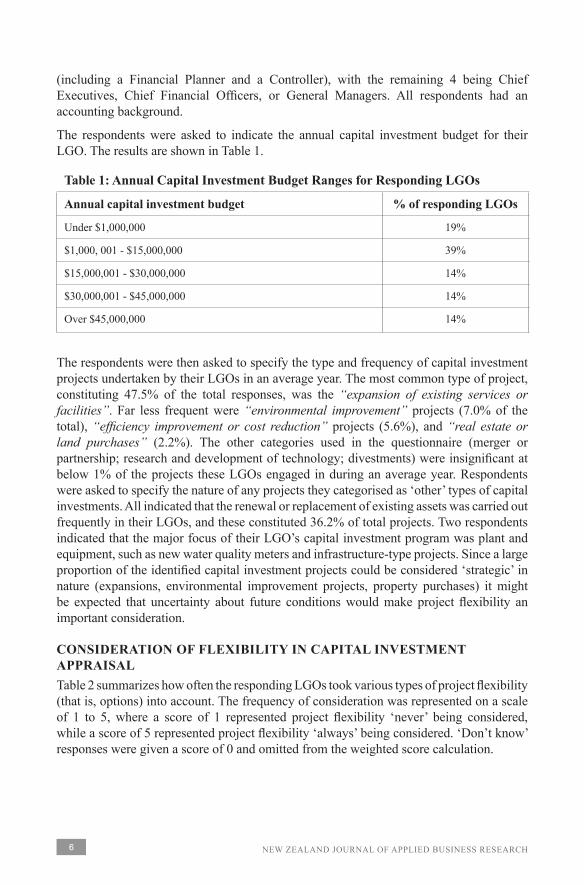

The respondents were asked to indicate the annual capital investment budget for their LGO. The results are shown in Table 1.

Table 1: Annual Capital Investment Budget Ranges for Responding LGOs

Annual capital investment budget % of responding LGOs

Under $1,000,000 19%

$1,000, 001 - $15,000,000 39%

$15,000,001 - $30,000,000 14%

$30,000,001 - $45,000,000 14%

Over $45,000,000 14%

The respondents were then asked to specify the type and frequency of capital investment projects undertaken by their LGOs in an average year. The most common type of project, constituting 47.5% of the total responses, was the “expansion of existing services or facilities”. Far less frequent were “environmental improvement” projects (7.0% of the total), “efficiency improvement or cost reduction” projects (5.6%), and “real estate or land purchases” (2.2%). The other categories used in the questionnaire (merger or partnership; research and development of technology; divestments) were insignificant at below 1% of the projects these LGOs engaged in during an average year. Respondents were asked to specify the nature of any projects they categorised as ‘other’ types of capital investments. All indicated that the renewal or replacement of existing assets was carried out frequently in their LGOs, and these constituted 36.2% of total projects. Two respondents indicated that the major focus of their LGO’s capital investment program was plant and equipment, such as new water quality meters and infrastructure-type projects. Since a large proportion of the identified capital investment projects could be considered ‘strategic’ in nature (expansions, environmental improvement projects, property purchases) it might be expected that uncertainty about future conditions would make project flexibility an important consideration.

CONSIDERATION OF FLEXIBILITY IN CAPITAL INVESTMENT APPRAISAL Table 2 summarizes how often the responding LGOs took various types of project flexibility (that is, options) into account. The frequency of consideration was represented on a scale of 1 to 5, where a score of 1 represented project flexibility ‘never’ being considered, while a score of 5 represented project flexibility ‘always’ being considered. ‘Don’t know’ responses were given a score of 0 and omitted from the weighted score calculation.

VOLUME 9, NUMBER 2, 2011 7

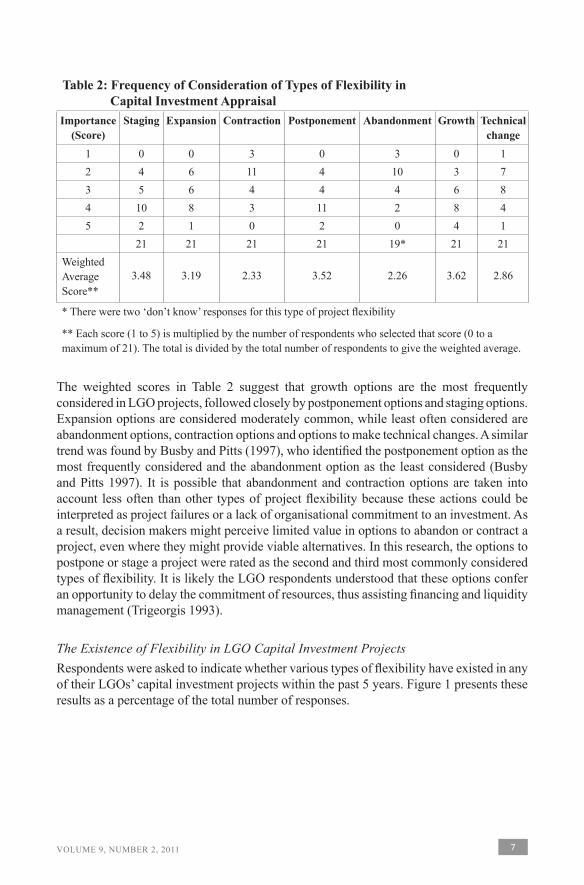

Table 2: Frequency of Consideration of Types of Flexibility in Capital Investment AppraisalImportance

(Score)Staging Expansion Contraction Postponement Abandonment Growth Technical

change1 0 0 3 0 3 0 12 4 6 11 4 10 3 73 5 6 4 4 4 6 84 10 8 3 11 2 8 45 2 1 0 2 0 4 1

21 21 21 21 19* 21 21Weighted Average Score**

3.48 3.19 2.33 3.52 2.26 3.62 2.86

* There were two ‘don’t know’ responses for this type of project flexibility

** Each score (1 to 5) is multiplied by the number of respondents who selected that score (0 to a maximum of 21). The total is divided by the total number of respondents to give the weighted average.

The weighted scores in Table 2 suggest that growth options are the most frequently considered in LGO projects, followed closely by postponement options and staging options. Expansion options are considered moderately common, while least often considered are abandonment options, contraction options and options to make technical changes. A similar trend was found by Busby and Pitts (1997), who identified the postponement option as the most frequently considered and the abandonment option as the least considered (Busby and Pitts 1997). It is possible that abandonment and contraction options are taken into account less often than other types of project flexibility because these actions could be interpreted as project failures or a lack of organisational commitment to an investment. As a result, decision makers might perceive limited value in options to abandon or contract a project, even where they might provide viable alternatives. In this research, the options to postpone or stage a project were rated as the second and third most commonly considered types of flexibility. It is likely the LGO respondents understood that these options confer an opportunity to delay the commitment of resources, thus assisting financing and liquidity management (Trigeorgis 1993).

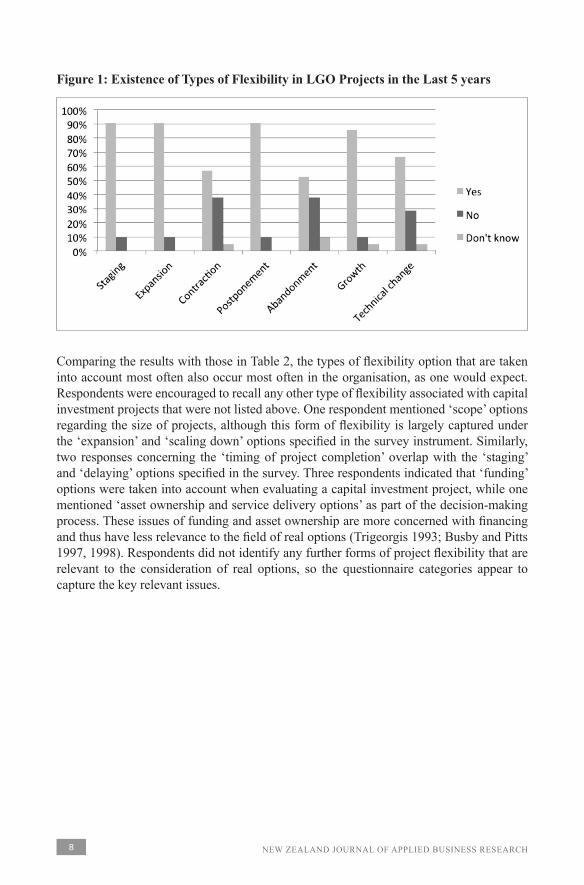

The Existence of Flexibility in LGO Capital Investment ProjectsRespondents were asked to indicate whether various types of flexibility have existed in any of their LGOs’ capital investment projects within the past 5 years. Figure 1 presents these results as a percentage of the total number of responses.

NEW ZEALAND JOURNAL OF APPLIED BUSINESS RESEARCH 8

Figure 1: Existence of Types of Flexibility in LGO Projects in the Last 5 years

Comparing the results with those in Table 2, the types of flexibility option that are taken into account most often also occur most often in the organisation, as one would expect. Respondents were encouraged to recall any other type of flexibility associated with capital investment projects that were not listed above. One respondent mentioned ‘scope’ options regarding the size of projects, although this form of flexibility is largely captured under the ‘expansion’ and ‘scaling down’ options specified in the survey instrument. Similarly, two responses concerning the ‘timing of project completion’ overlap with the ‘staging’ and ‘delaying’ options specified in the survey. Three respondents indicated that ‘funding’ options were taken into account when evaluating a capital investment project, while one mentioned ‘asset ownership and service delivery options’ as part of the decision-making process. These issues of funding and asset ownership are more concerned with financing and thus have less relevance to the field of real options (Trigeorgis 1993; Busby and Pitts 1997, 1998). Respondents did not identify any further forms of project flexibility that are relevant to the consideration of real options, so the questionnaire categories appear to capture the key relevant issues.

VOLUME 9, NUMBER 2, 2011 9

The five interviewees were encouraged to specify types of capital investment project launched during the past five years that had inherent valuable project flexibility. The following illustrative quotations reflect their experiences in taking flexibility into account when evaluating capital investment projects:

[1] We are building a new art gallery and museum building, but the project is deferred as the result of the global recession last year…we have flexibility on the start date and on how we are going to fund it. So there was a whole lot of flexibility we need to think about.

(Council Financial Director, Telephone Interview, 28th May 2010)

[2] We are doing an extension project which includes the provision of an ice rink. I think we had to abandon the ice rink because of the costing for it … we had to change the project in that respect in order to mitigate losses…. We don’t regularly abandon a project without a lot of consideration and discussion with the affected people. In this case, the ice rink would be nice to have if that could work financially, but in the end, we couldn’t make it work financially, so it just had to fall off the project.

(Council CFO, Telephone Interview, 26th May 2010)

[3] We have a project related to water supply. [But], if we can avoid wasting water that is in the network by making sure the network is maintained and the links are contained, and also modify consumer behaviour so they restrict their use in times of high demand, then we can put off the capital investment indefinitely.

(Council Financial Manager, Telephone Interview, 26th May 2010)

[4] We’ve got a big project which … incorporates improved technology for the treatment of waste water. The project provides a higher environmental standard... There is the opportunity to build into the project that we can add to the treatment plant and the waste water disposal fields when that additional capacity is required, so we make sure that we are keeping up with the increased demand.

(Council General Manager, Telephone Interview, 26th May 2010)

These examples reflect the importance of real options that can exist in LGO capital projects: postponement (examples 1 and 3); abandonment (example 2); future expansion and/or staging the project (example 4). The LGO managers’ recognition of these forms of real options accords with prior theory, which suggests that managers usually understand the potential advantages of project flexibility to the organisation (Busby and Pitts 1997; Howell and Jagle 1997; McGrath and Nerkar 2004). But how important is such project flexibility perceived to be?

Perceived Importance of Project Flexibility

Table 3 summarizes the perceived importance of each type of capital investment project flexibility. A score of 1 indicates that project flexibility is perceived as ’not at all important’ to the attractiveness of an investment opportunity, while a score of 5 indicates that project flexibility is perceived as ‘extremely important’. A score of 0 represents a ‘don’t know’ response and was omitted from the weighted score calculation.

NEW ZEALAND JOURNAL OF APPLIED BUSINESS RESEARCH 10

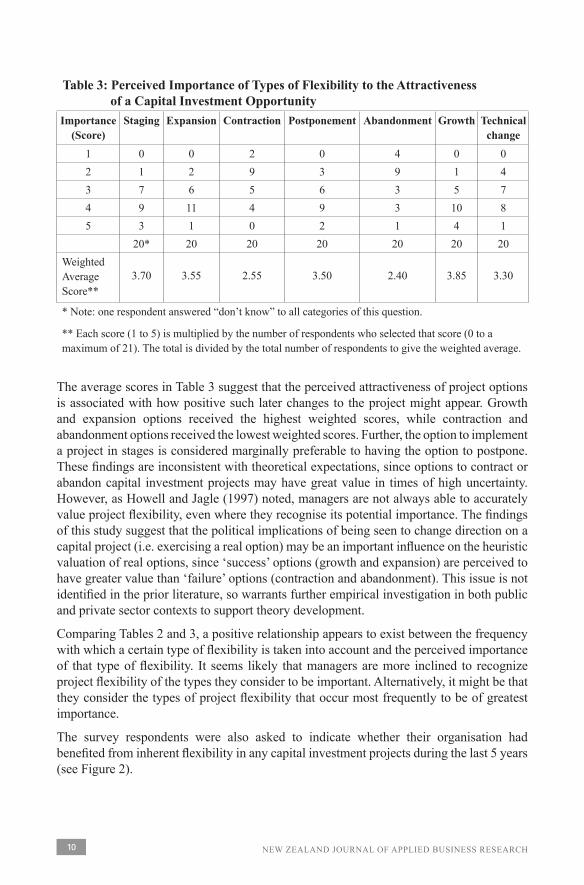

Table 3: Perceived Importance of Types of Flexibility to the Attractiveness of a Capital Investment Opportunity Importance

(Score)Staging Expansion Contraction Postponement Abandonment Growth Technical

change1 0 0 2 0 4 0 02 1 2 9 3 9 1 43 7 6 5 6 3 5 74 9 11 4 9 3 10 85 3 1 0 2 1 4 1

20* 20 20 20 20 20 20Weighted Average Score**

3.70 3.55 2.55 3.50 2.40 3.85 3.30

* Note: one respondent answered “don’t know” to all categories of this question.

** Each score (1 to 5) is multiplied by the number of respondents who selected that score (0 to a maximum of 21). The total is divided by the total number of respondents to give the weighted average.

The average scores in Table 3 suggest that the perceived attractiveness of project options is associated with how positive such later changes to the project might appear. Growth and expansion options received the highest weighted scores, while contraction and abandonment options received the lowest weighted scores. Further, the option to implement a project in stages is considered marginally preferable to having the option to postpone. These findings are inconsistent with theoretical expectations, since options to contract or abandon capital investment projects may have great value in times of high uncertainty. However, as Howell and Jagle (1997) noted, managers are not always able to accurately value project flexibility, even where they recognise its potential importance. The findings of this study suggest that the political implications of being seen to change direction on a capital project (i.e. exercising a real option) may be an important influence on the heuristic valuation of real options, since ‘success’ options (growth and expansion) are perceived to have greater value than ‘failure’ options (contraction and abandonment). This issue is not identified in the prior literature, so warrants further empirical investigation in both public and private sector contexts to support theory development.

Comparing Tables 2 and 3, a positive relationship appears to exist between the frequency with which a certain type of flexibility is taken into account and the perceived importance of that type of flexibility. It seems likely that managers are more inclined to recognize project flexibility of the types they consider to be important. Alternatively, it might be that they consider the types of project flexibility that occur most frequently to be of greatest importance.

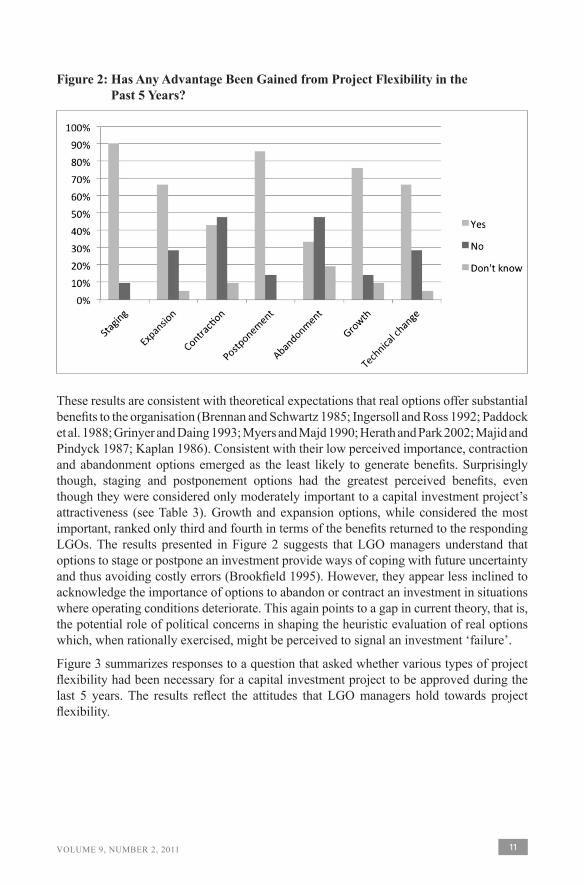

The survey respondents were also asked to indicate whether their organisation had benefited from inherent flexibility in any capital investment projects during the last 5 years (see Figure 2).

VOLUME 9, NUMBER 2, 2011 11

Figure 2: Has Any Advantage Been Gained from Project Flexibility in the Past 5 Years?

These results are consistent with theoretical expectations that real options offer substantial benefits to the organisation (Brennan and Schwartz 1985; Ingersoll and Ross 1992; Paddock et al. 1988; Grinyer and Daing 1993; Myers and Majd 1990; Herath and Park 2002; Majid and Pindyck 1987; Kaplan 1986). Consistent with their low perceived importance, contraction and abandonment options emerged as the least likely to generate benefits. Surprisingly though, staging and postponement options had the greatest perceived benefits, even though they were considered only moderately important to a capital investment project’s attractiveness (see Table 3). Growth and expansion options, while considered the most important, ranked only third and fourth in terms of the benefits returned to the responding LGOs. The results presented in Figure 2 suggests that LGO managers understand that options to stage or postpone an investment provide ways of coping with future uncertainty and thus avoiding costly errors (Brookfield 1995). However, they appear less inclined to acknowledge the importance of options to abandon or contract an investment in situations where operating conditions deteriorate. This again points to a gap in current theory, that is, the potential role of political concerns in shaping the heuristic evaluation of real options which, when rationally exercised, might be perceived to signal an investment ‘failure’.

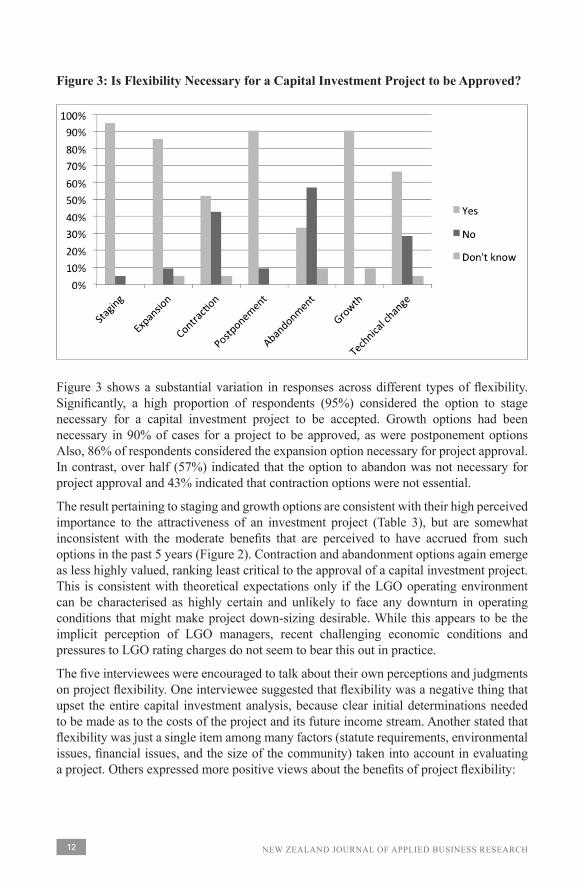

Figure 3 summarizes responses to a question that asked whether various types of project flexibility had been necessary for a capital investment project to be approved during the last 5 years. The results reflect the attitudes that LGO managers hold towards project flexibility.

NEW ZEALAND JOURNAL OF APPLIED BUSINESS RESEARCH 12

Figure 3: Is Flexibility Necessary for a Capital Investment Project to be Approved?

Figure 3 shows a substantial variation in responses across different types of flexibility. Significantly, a high proportion of respondents (95%) considered the option to stage necessary for a capital investment project to be accepted. Growth options had been necessary in 90% of cases for a project to be approved, as were postponement options Also, 86% of respondents considered the expansion option necessary for project approval. In contrast, over half (57%) indicated that the option to abandon was not necessary for project approval and 43% indicated that contraction options were not essential.

The result pertaining to staging and growth options are consistent with their high perceived importance to the attractiveness of an investment project (Table 3), but are somewhat inconsistent with the moderate benefits that are perceived to have accrued from such options in the past 5 years (Figure 2). Contraction and abandonment options again emerge as less highly valued, ranking least critical to the approval of a capital investment project. This is consistent with theoretical expectations only if the LGO operating environment can be characterised as highly certain and unlikely to face any downturn in operating conditions that might make project down-sizing desirable. While this appears to be the implicit perception of LGO managers, recent challenging economic conditions and pressures to LGO rating charges do not seem to bear this out in practice.

The five interviewees were encouraged to talk about their own perceptions and judgments on project flexibility. One interviewee suggested that flexibility was a negative thing that upset the entire capital investment analysis, because clear initial determinations needed to be made as to the costs of the project and its future income stream. Another stated that flexibility was just a single item among many factors (statute requirements, environmental issues, financial issues, and the size of the community) taken into account in evaluating a project. Others expressed more positive views about the benefits of project flexibility:

VOLUME 9, NUMBER 2, 2011 13

“There are things we can’t be 100% certain about, so we need to value flexibility to be able to respond to those uncertainties.”

(Council CFO, Telephone Interview, 26th May 2010)

“An assessment of flexibility benefits is generally done on a case by case basis using the experts that we have as staff.”

(Council Financial Manager, Telephone Interview, 28th May 2010)

The follow-up interviews revealed variation between individual perceptions of project flexibility and behaviour in dealing with it, which also matches with the variability in perceptions revealed by the survey findings. This result is consistent with Busby and Pitts (1997), who found wide variation between different managers’ views and practices regarding real options.

Understanding the Drivers of Real Options Value

The questionnaire examined respondents’ understanding of the concepts underlying real options valuation by soliciting their views on the impact four key factors have on the value of project flexibility. These factors are captured in four statements drawn from Busby and Pitts (1998, p33), who note that “these statements reflect the most basic predictions of theory”. The statements were included in the questionnaire as follows:

1. The more it costs to exercise project flexibility when it is needed, the less valuable that flexibility is

2. The longer the period for which project flexibility will remain available, the more valuable that flexibility is

3. The greater the uncertainty about future operating conditions, the more valuable project flexibility is

4. The higher current interest rates are, the more valuable project flexibility is.

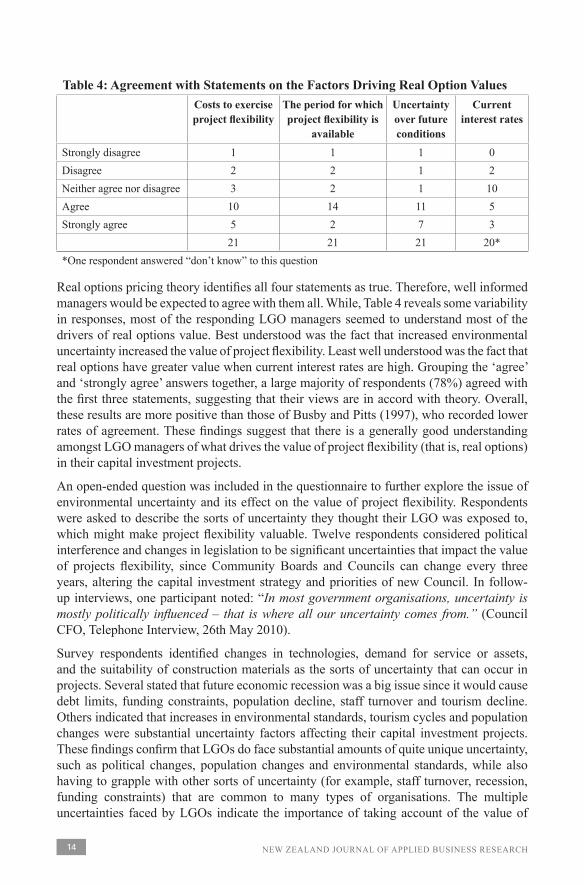

The first statement refers to the fact that the value of a real option is substantially determined by its settlement price (Gotze et al. 2008). Accordingly, the more it costs to exercise project flexibility when necessary, the less valuable it is. The second statement refers to the positive correlation between the life of options and their value (Gotze et al. 2008), while the third and fourth statements capture the relationship between uncertainty, economic conditions and option values. Table 4 summarizes the extent to which respondents agreed with these views and, thus, with the concepts underlying real options valuation methods.

NEW ZEALAND JOURNAL OF APPLIED BUSINESS RESEARCH 14

Table 4: Agreement with Statements on the Factors Driving Real Option ValuesCosts to exercise project flexibility

The period for which project flexibility is

available

Uncertainty over future conditions

Current interest rates

Strongly disagree 1 1 1 0Disagree 2 2 1 2Neither agree nor disagree 3 2 1 10Agree 10 14 11 5Strongly agree 5 2 7 3

21 21 21 20**One respondent answered “don’t know” to this question

Real options pricing theory identifies all four statements as true. Therefore, well informed managers would be expected to agree with them all. While, Table 4 reveals some variability in responses, most of the responding LGO managers seemed to understand most of the drivers of real options value. Best understood was the fact that increased environmental uncertainty increased the value of project flexibility. Least well understood was the fact that real options have greater value when current interest rates are high. Grouping the ‘agree’ and ‘strongly agree’ answers together, a large majority of respondents (78%) agreed with the first three statements, suggesting that their views are in accord with theory. Overall, these results are more positive than those of Busby and Pitts (1997), who recorded lower rates of agreement. These findings suggest that there is a generally good understanding amongst LGO managers of what drives the value of project flexibility (that is, real options) in their capital investment projects.

An open-ended question was included in the questionnaire to further explore the issue of environmental uncertainty and its effect on the value of project flexibility. Respondents were asked to describe the sorts of uncertainty they thought their LGO was exposed to, which might make project flexibility valuable. Twelve respondents considered political interference and changes in legislation to be significant uncertainties that impact the value of projects flexibility, since Community Boards and Councils can change every three years, altering the capital investment strategy and priorities of new Council. In follow-up interviews, one participant noted: “In most government organisations, uncertainty is mostly politically influenced – that is where all our uncertainty comes from.” (Council CFO, Telephone Interview, 26th May 2010).

Survey respondents identified changes in technologies, demand for service or assets, and the suitability of construction materials as the sorts of uncertainty that can occur in projects. Several stated that future economic recession was a big issue since it would cause debt limits, funding constraints, population decline, staff turnover and tourism decline. Others indicated that increases in environmental standards, tourism cycles and population changes were substantial uncertainty factors affecting their capital investment projects. These findings confirm that LGOs do face substantial amounts of quite unique uncertainty, such as political changes, population changes and environmental standards, while also having to grapple with other sorts of uncertainty (for example, staff turnover, recession, funding constraints) that are common to many types of organisations. The multiple uncertainties faced by LGOs indicate the importance of taking account of the value of

VOLUME 9, NUMBER 2, 2011 15

project flexibility. Indeed, Schubert and Barenbaum (2007), note the potential for public sector managers to employ ROA to assess the value of project flexibility and improve the efficacy of their capital investment decision-making.

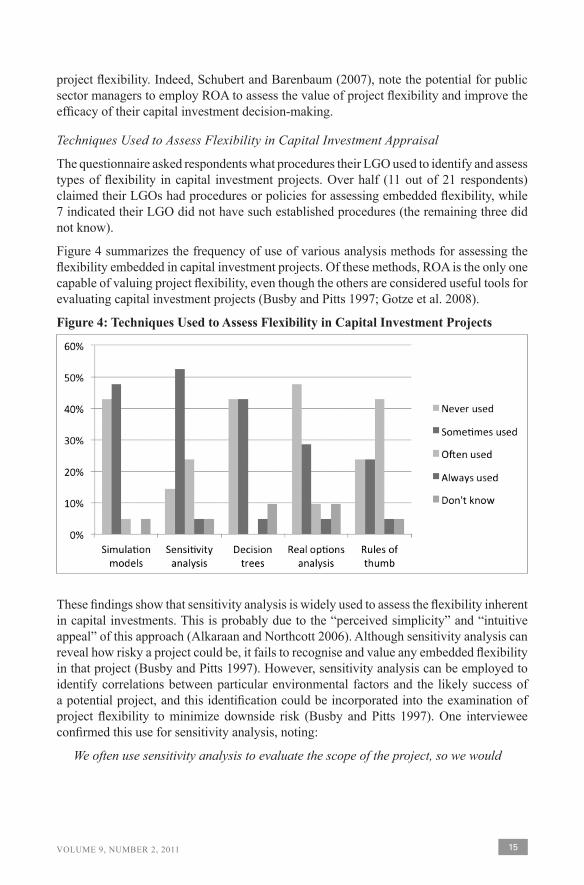

Techniques Used to Assess Flexibility in Capital Investment Appraisal

The questionnaire asked respondents what procedures their LGO used to identify and assess types of flexibility in capital investment projects. Over half (11 out of 21 respondents) claimed their LGOs had procedures or policies for assessing embedded flexibility, while 7 indicated their LGO did not have such established procedures (the remaining three did not know).

Figure 4 summarizes the frequency of use of various analysis methods for assessing the flexibility embedded in capital investment projects. Of these methods, ROA is the only one capable of valuing project flexibility, even though the others are considered useful tools for evaluating capital investment projects (Busby and Pitts 1997; Gotze et al. 2008).

Figure 4: Techniques Used to Assess Flexibility in Capital Investment Projects

These findings show that sensitivity analysis is widely used to assess the flexibility inherent in capital investments. This is probably due to the “perceived simplicity” and “intuitive appeal” of this approach (Alkaraan and Northcott 2006). Although sensitivity analysis can reveal how risky a project could be, it fails to recognise and value any embedded flexibility in that project (Busby and Pitts 1997). However, sensitivity analysis can be employed to identify correlations between particular environmental factors and the likely success of a potential project, and this identification could be incorporated into the examination of project flexibility to minimize downside risk (Busby and Pitts 1997). One interviewee confirmed this use for sensitivity analysis, noting:

We often use sensitivity analysis to evaluate the scope of the project, so we would

NEW ZEALAND JOURNAL OF APPLIED BUSINESS RESEARCH 16

look at whether we have a range of options that may deliver the outcome we want … we would look at what the cost is for all of those options of building it a certain size, building it bigger, etc. and … compare with what outputs we are going to get, and we do some sort of sensitivity analysis on what is the better option to run with.

(Council General Manager, Telephone Interview, 26th May 2010)

‘Rules of thumb’ (that is, less formal analytical methods developed for easy use in assessing project flexibility) were also used at least ‘sometimes’ by most respondents (71%). Despite the practical limitations of decision tree analysis in identifying project risk, Busby and Pitts (1998) suggested this technique can usefully reflect the range of outcomes provided by project flexibility. Therefore, it might be expected to have utility in assessing flexibility in practice. However this expectation was not supported by the survey findings, which suggest decision tree analysis is not widely used for assessing project flexibility.

Real options analysis emerged as the least used technique for assessing project flexibility, rated as ‘never used’ by nearly half of respondents (48%). This result is not surprising based on the findings of prior studies. Despite its theoretical superiority, the limited use of ROA is probably due to its mathematically complex nature (Block 2007). Moreover, it is not surprising that two respondents had never heard of this analysis tool, since ROA is still a relatively new approach (Block 2007). What is perhaps surprising is that nine respondents indicated that ROA was employed to assess project flexibility in their LGOs, rating it as ‘sometimes used’ (n=6) ‘often used’ (n=2) or ‘always used’ (n=1).

Five of these respondents were randomly selected for the follow-up interviews. They were asked to describe a situation where ROA was employed in evaluating the flexibility of a project. However, none could recall such a case. Therefore, this survey result does not appear to represent formal ROA use in LGOs, but perhaps some kind of ROA-type thinking is considered when evaluating flexibility in capital investment projects. This finding also cautions against taking survey results at face value where the aim is to examine the use of innovative new techniques whose associated procedures and nomenclature may not yet be well understood.

In the follow-up interviews, participants were asked whether they considered it necessary to employ formal methods to value project flexibility. None of them currently had such formal methods in their LGOs. Two agreed with the idea of introducing such a method to value project flexibility, while two disagreed. One was not sure, but expressed concern about whether such a method would be too complex in nature. The following quotes illustrate these varying views.

“Yes, definitely. We need ways to check we have enough flexibility to get over changes in the environment or changes in resources during the project.”

(Council CFO, Telephone Interview, 26th May 2010)

“If the method is sophisticated and complicated, it is not going to work in local government, because the variables are too uncertain.”

(Council Financial Director, Telephone Interview, 28th May 2010)

VOLUME 9, NUMBER 2, 2011 17

It is not necessary to employ an additional method to value project flexibility. In our industry we are not actually in most cases looking for a return as such. The community is actually asking us to provide a facility. So just working out the net present value or returns on that is not what we do.

(Council General Manager, Telephone Interview, 26th May 2010)

“We are satisfied with the current procedures used in our organisation, which seem to serve our needs at the moment.”

(Council Financial Manager, Telephone Interview, 28th May 2010)

These findings suggest varying attitudes amongst public sector managers to a ‘sophisticated’ technique such as ROA. While the first interviewee seems enthusiastic about the potential for formal analysis to inform capital investment decision-making in the face of uncertainty, the others remain less convinced. However, their reasons - uncertain variables and the lack of a financial decision imperative – seem inconsistent with a rational approach to decision making, since uncertainty is best dealt with via the use of appropriate analysis tools (one being ROA) and even not-for-profit organisations ought to be concerned with cost minimisation and best value. These results suggest that the introduction of ROA, while potentially beneficial in the public sector context, may be impeded by perceptions that the technique is too complex, overly focused on financial goals, and unnecessary.

CONCLUSIONSReal options analysis has been advocated as an appropriate analysis technique in capital investment appraisal, since it captures the value of inherent project flexibility. Although the theoretical ROA literature is well developed, the empirical investigation of this topic remains weak (MacDougall and Pike 2003). In particular, while some studies of ROA usage have been conducted in manufacturing and other private sector organisations, there have been very few in public sector contexts. This study aimed to address this gap by examining how public sector managers take account of inherent flexibility in capital investment appraisal, and whether ROA-type principles or approaches are employed. The findings offer the first empirical insights into this issue in the New Zealand public sector context.

This study had some limitations that should be noted. First, although the response rate for the questionnaire was similar to that found in many prior studies (for example, Alkaraan and Northcott 2006; Block 2007), it could be considered relatively low at 24.4%. The use of a mailed questionnaire, and the limited time allowed to respond to the questionnaire, may be two main reasons for this. This research used a small number of follow-up interviews to gather broader but deeper data to address the research questions, but future studies could usefully employ interviews or case studies to extend this approach. A second possible limitation is the focus on LGOs as a sub-set of the public sector, which may limit the generalization of the findings to public sector organisations more broadly. Third, the small number of survey respondents restricted our analysis to the interpretation of descriptive statistics and rendered the examination of correlations between variables less useful. To extend this first, exploratory study, future research within the broader public sector could seek larger samples to enhance the potential for generalization and statistical analysis.

NEW ZEALAND JOURNAL OF APPLIED BUSINESS RESEARCH 18

The results of this study indicate that LGOs face multiple forms of uncertainty in their operating environment. Political interference, legislative changes, population and tourism fluctuations, and environmental standard changes were identified as problematic, along with less sector-specific factors such as economic recession, funding constraints and changing technologies. Flexibility is a significant factor in LGO capital investment projects, therefore. Consistent with this, LGO managers noted the importance and benefits of options to postpone, stage, or expand investment projects. However, options to abandon or contract an investment were considered less important, despite their potential benefits in uncertain operating conditions. A possible explanation is that exercising these options might be viewed as failure, or as indicating a lack of organisational commitment to investment projects. The types of project flexibility that occurred most frequently were regarded by managers as the most important to a capital investment’s attractiveness, and also the most beneficial based on recent experience. But, it is possible that other, less favoured options (such as abandonment and contraction) may also benefit LGOs in adverse operating conditions, even though their political implications may seem less favourable. Improved recognition and assessment of the value of real options would likely help to reveal this potential.

An aim of this study was to examine whether public sector managers use ROA-type principles or approaches in evaluating capital investment projects. This could involve the formal use of ROA analysis, or the implicit application of ROA concepts when evaluating projects. The findings reveal that few of the responding LGOs used ROA as a formal procedure for assessing project flexibility, even though most felt that some form of flexibility is necessary for a project to be approved and many demonstrated a reasonable understanding of the factors driving the value of project flexibility. In terms of investment appraisal techniques, LGOs seemed to employ mainly sensitivity analysis and unspecified ‘rules of thumb’ as means of assessing project flexibility. These less mathematically challenging practices, along with LGO managers’ perceptions that project flexibility is relevant to capital investment decision-making, suggest that ROA-type concepts might be at play even where formal ROA analysis is absent. However, the findings of this study suggest that this ROA-type thinking could be further developed and exploited. A key implication for practice is that more rigorous forms of analysis could be used to improve the assessment of project flexibility in the public sector, where multiple forms of uncertainty impact the outcomes of capital investments and give rise to significant - but largely unrecognised - value in project flexibility.

VOLUME 9, NUMBER 2, 2011 19

REFERENCESAdams M 2004. Real options and customer management in the financial services sector. Journal of Strategic Marketing, 12: 3-11.

Adler R W 2000. Strategic investment decision appraisal techniques: The old and the new. Business Horizons, 43(6): 15-22.

Alkaraan F, Northcott D 2006. Strategic capital investment decision-making: a role for emergent analysis tools? A study of practice in large UK manufacturing companies. The British Accounting Review 38: 149-173.

Amram M, Howe K M 2002. Capturing the value of flexibility. Strategic Finance 84(6): 10-13.

Amram M, Howe K M 2003. Real-options valuations: taking out the rocket science. Strategic Finance 84(8): 10-13.

Anderson T J 2000. Real options analysis in strategic decision making: an applied approach in a dual options framework. Journal of Applied Management Studies 9(2): 235-255.

Barnett M L 2005. Paying attention to real options. R&D Management 35(1): 61-72.

Benaroch M, Kauffman R J 1999. A case for using real options pricing analysis to evaluate information technology project investments. Information Systems Research 10(1): 70-86.

Bengtsson J 2001. Manufacturing flexibility and real options: a review. International Journal of Production Economics 74: 213-224.

Black F, Scholes M 1973. The pricing of options and corporate liabilities. The Journal of Political Economy 81(3): 637-654.

Block S 2007. Are “real options” actually used in the real world? The Engineering Economist 52(3): 255-267.

Bowe M, Lee D L 2004. Project evaluation in the presence of multiple embedded real options: evidence from the Taiwan high-speed rail project. Journal of Asian Economics, 15(1): 71-98.

Bowman E H, Moskowitz G T 2001. Real options analysis and strategic decision making. Organisation Science 12(6): 772-777.

Brealey R A, Cooper I A, Habib M A 1997. Investment appraisal in the public sector. Oxford Review of Economic Policy, 13(4): 12-28.

Brennan M J, Schwartz E S 1985. Evaluating natural resource investments. Journal of Business, 58: 135-157.

Brookfield D 1995. Risk and capital budgeting: avoiding the pitfalls in using NPV when risk arises. Management Decision 33(8): 56-59.

Bryman A 2008. Social research methods. 3rd Ed.. Oxford University Press: New York.

Bryman A, Bell E 2007. Business research methods. 2nd Ed. Oxford University Press: Oxford.

NEW ZEALAND JOURNAL OF APPLIED BUSINESS RESEARCH 20

Busby J S, Pitts C G C 1997. Real options in practice: an exploratory survey of how finance officers deal with flexibility in capital appraisal. Management Accounting Research 8(2): 169-186.

Busby J S, Pitts C G C 1998. Assessing flexibility in capital investment. The Chartered Institute of Management Accountants, London.

Chan Y L 2004. Use of capital budgeting techniques and an analytic approach to capital investment decisions in Canadian municipal governments. Public Budgeting & Finance Summer, 40-58.

Chen T, Zhang J, Lai K 2009. An integrated real options evaluating model for information technology projects under multiple risks. International Journal of Project Management 27: 776-786.

Cheung J K 1993. Managerial flexibility in capital investment decisions: insights from the real-options literature. Journal of Accounting Literature 12: 29-66.

Copeland T 2001. The real-options approach to capital allocation. Strategic Finance 83(4): 33-37.

Copeland T, Howe K M 2002. Real options and strategic decisions. Strategic Finance 83(10): 8-11.

Copeland T E, Keenan P T 1998. How much is flexibility work. The McKinsey quarterly 2: 38-49.

Cotter J F, Marcum B, Martin D R 2003. A cure for outdated capital budgeting techniques. The Journal of Corporate Accounting & Finance 14(3): 71-80.

Cox J C, Ross S, Rubinstein M 1979. Option pricing: a simplified approach. Journal of Financial Economics 17(2): 145-160.

Dixit A, Pindyck R S 1994. Investment under uncertainty. Princeton University Press: New Jersey.

Dixit A K, Pindyck R S 1995. The options approach to capital investment. Harvard Business Review May-June: 105-115.

Feinstein S P, Lander D M 2002. A better way of understanding why NPV undervalues managerial flexibility. The Engineering Economist 47(4): 418-435.

Fichman R G, Keil M, Tiwana A 2005. Beyond valuation: “options thinking” in IT project management. California Management Review 47(2): 74-96.

Gotze U, Northcott D, Schuster P 2008. Investment Appraisal methods and models. Springer: Verlag Berlin Heidelberg.

Grinyer J R, Daing N I 1993. The use of abandonment values in capital budgeting – a research note. Management Accounting Research 4: 49-62.

Guide to Local Government 2004. Local government, local governance, local decision-making. Retrieved 30 August, 2011, from http://guide.localgovt.co.nz/tbp/localgov/html.

Hammer H 2002. Is the real options method better than the net present value rule? EBS Review 14: 5-11

VOLUME 9, NUMBER 2, 2011 21

Hartmann M, Hassan, A 2006. Application of real options analysis for pharmaceutical R&D project valuation – empirical results from a survey. Research Policy 35: 343-354.

Herath H S B, Park C S 2002. Multi-stage capital investment opportunities as compound real options. The Engineering Economist 47(1): 1-27.

Howell S D, Jagle A J 1997. Laboratory evidence on how managers intuitively value real growth options. Journal of Business Finance & Accounting 24(7/8): 915-935.

Ingersoll J E, Ross S A 1992. Waiting to invest: investment and uncertainty. Journal of Business 65(1): 1-29.

Kaplan R S 1986. Must CIM be justified by faith alone? Harvard Business Review March-April: 87-95.

Kensinger J W, Crawford T 2010. Managing real options in non-for-organisations: the case of shell space. Research in Finance 26: 33-50.

MacDougall S L, Pike R H 2003. Consider your options: changes to strategic value during implementation of advanced manufacturing technology. Omega 31(1): 1-15.

Majd S, Pindyck R S 1987. Time to build, option value, and investment decisions. Journal of Financial Economics 18: 7-27.

McDonald R, Siegel D 1986. The value of waiting to invest. Quarterly Journal of Economics 101: 707-727.

McGrath R G, Nerkar A 2004. Real options reasoning and a new look at the R&D investment strategies of pharmaceutical firms. Strategic Management Journal 25(1): 1-21.

Mills R W, Weinstein B, Favato G 2006. Using scenario thinking to make real options relevant to managers: a case illustration. Journal of General Management 31(3): 49-74.

Myers S C 1984. Finance theory and financial strategy. Interfaces 14(1): 126-137.

Myers S C, Majd S 1990. Abandonment value and project life. Advances in Futures and Options research 1-21.

Paddock J L, Siegel A, Smith J L 1988. Option valuation of claims on real assets: the case on offshore petroleum leases. Quarterly Journal of Economics 103(3): 479-508.

Pike R H, Sharp J, Price D 1989. AMT investment in the large UK firm. International Journal of Operations and Production Management 9 (2): 13-26.

Schubert W, Barenbaum L 2007. Real options and public sector capital project decision-making. Journal of Public Budgeting, Accounting & Financial management 19(2): 139-152.

Slagmulder R, Bruggeman W, Wassenhove L 1995. An empirical study of capital budgeting practices for strategic investments in CIM technologies. International Journal of Production Economics 40: 121-152.

Taylor S J, Bogdan R 1998. Introduction to qualitative research methods: A guidebook and resource. 3rd Ed.. John Wiley: New York.

Trigeorgis L 1993. Real options and interactions with financial flexibility. Financial Management 22(3): 202-224.

NEW ZEALAND JOURNAL OF APPLIED BUSINESS RESEARCH 22

Trigeorgis L 1997. Real options: managerial flexibility and strategy in resource allocation. 2nd Ed.. MIT Press: Cambridge MA.

Trigeorgis L 2005. Making use of real options simple: an overview and applications in flexible/modular decision making. The Engineering Economist 50: 25-53.

Van Putten A B, MacMillian I C 2004. Making real options really work. Harvard Business Review 82(12): 134-141.

Yeo K T, Qiu F 2003. The value of management flexibility – a real option approach to investment evaluation. International Journal of Project Management 21: 243-250.

Copyright of New Zealand Journal of Applied Business Research (NZJABR) is the property of Manukau

Institute of Technology and its content may not be copied or emailed to multiple sites or posted to a listserv

without the copyright holder's express written permission. However, users may print, download, or email

articles for individual use.