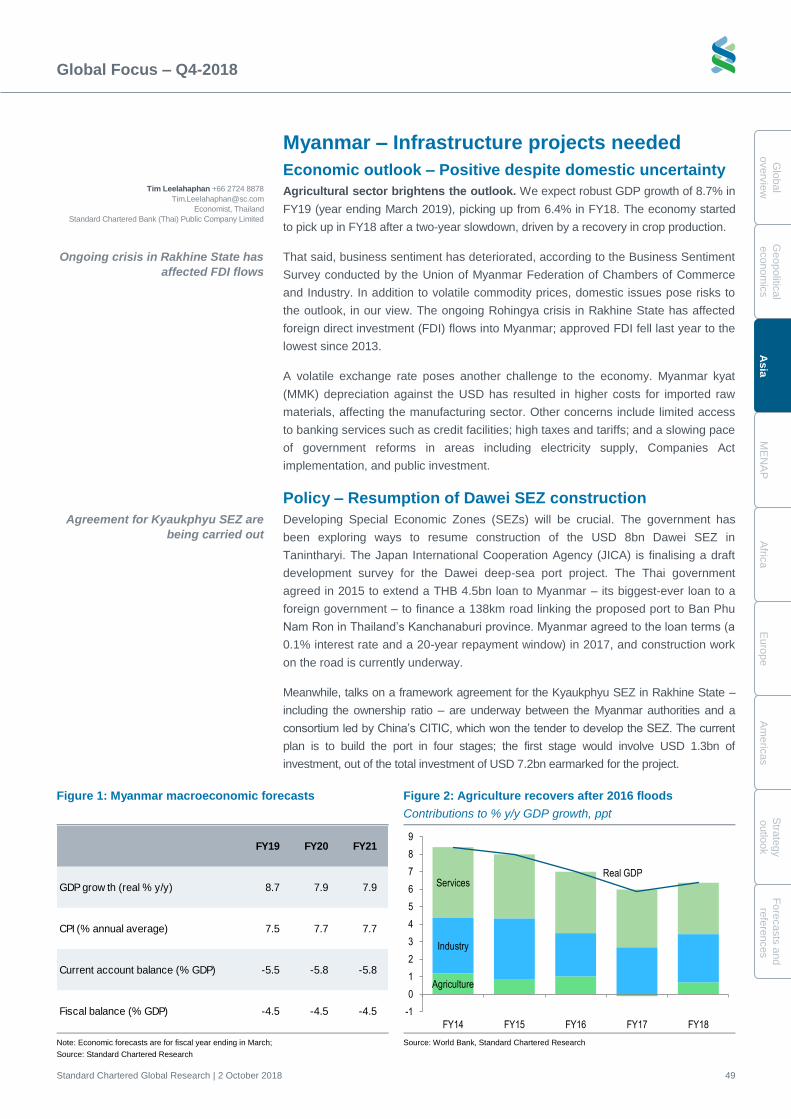

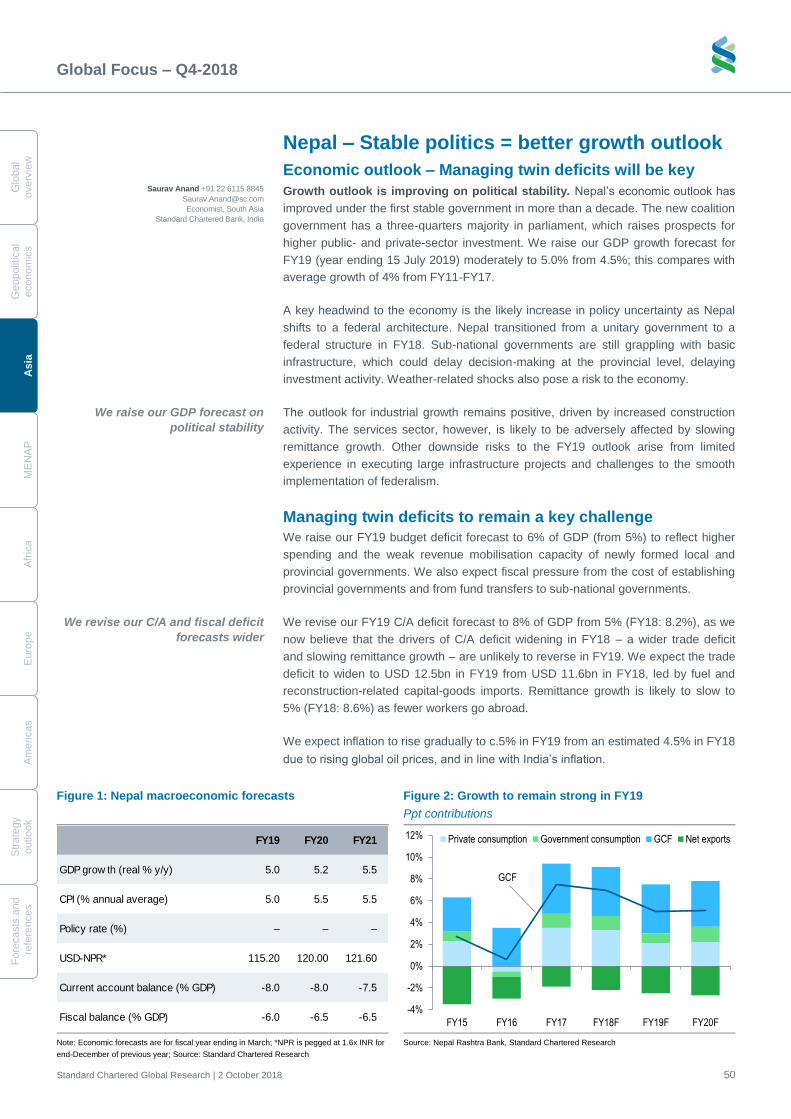

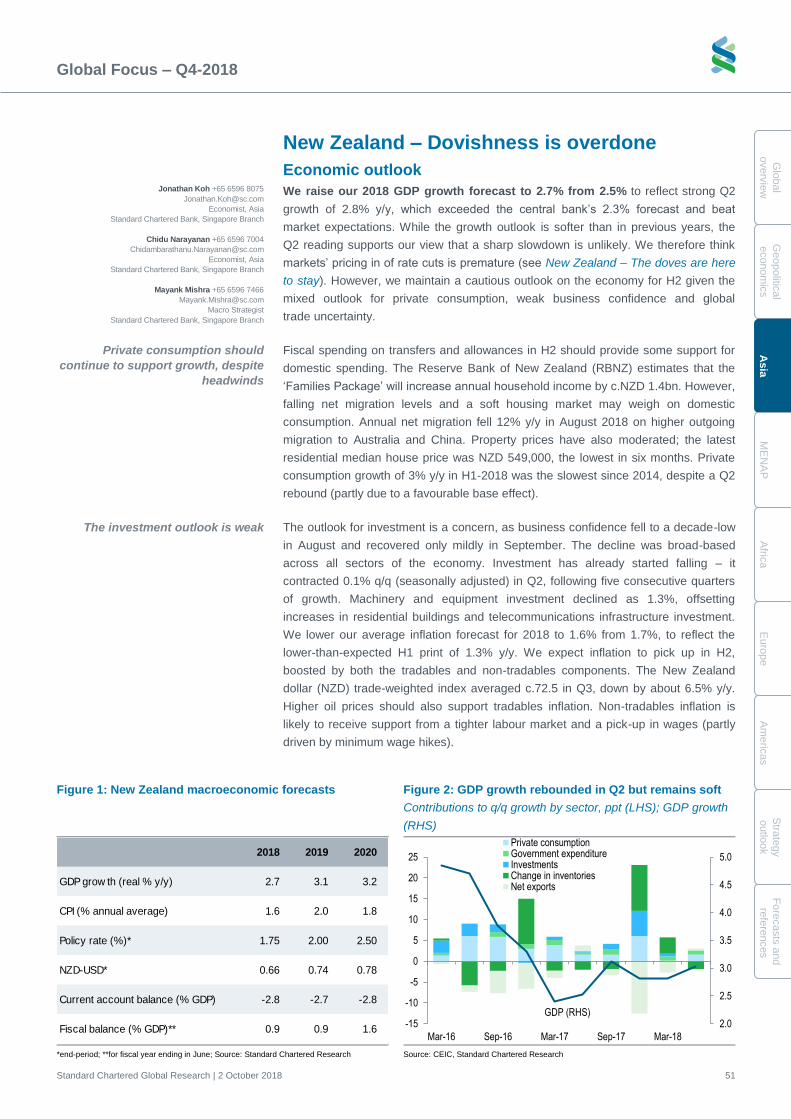

Embed Size (px)

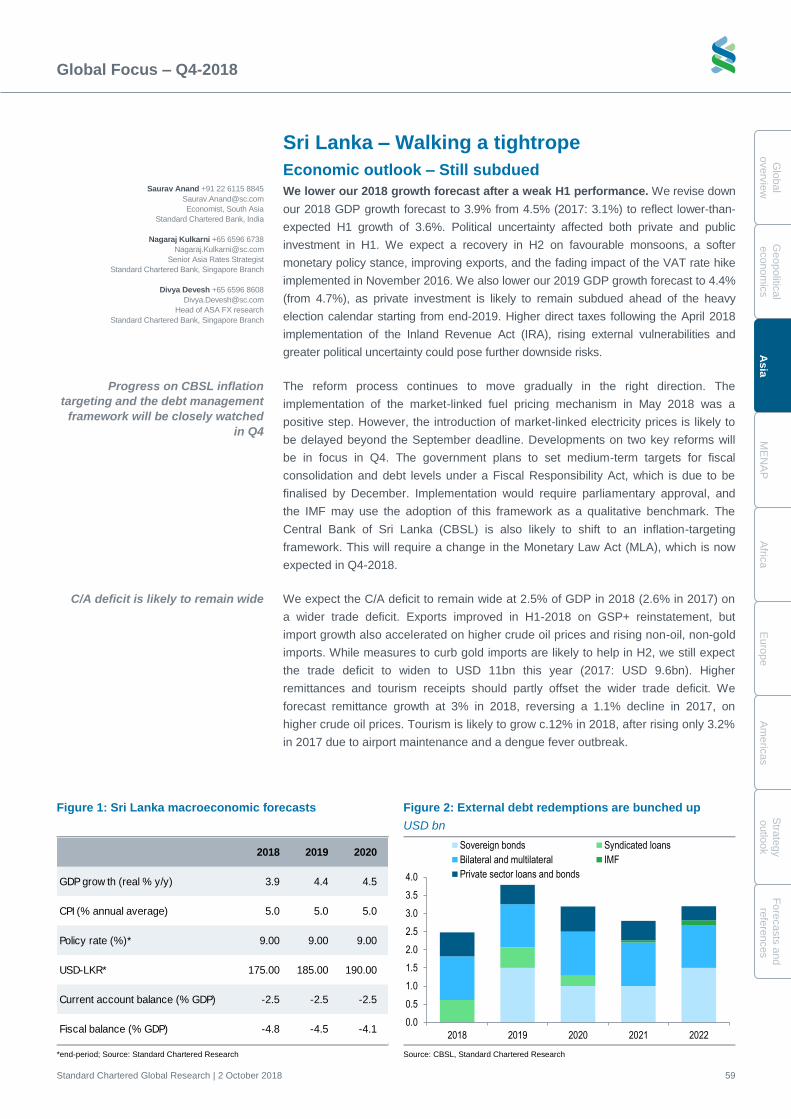

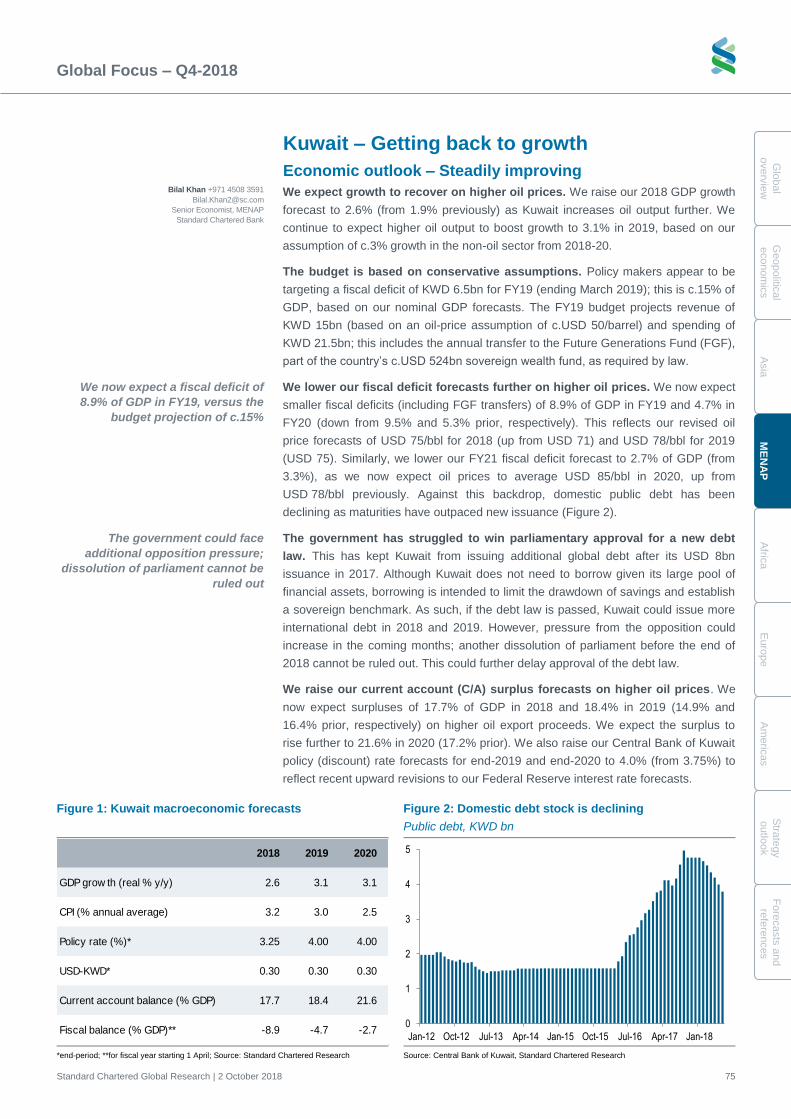

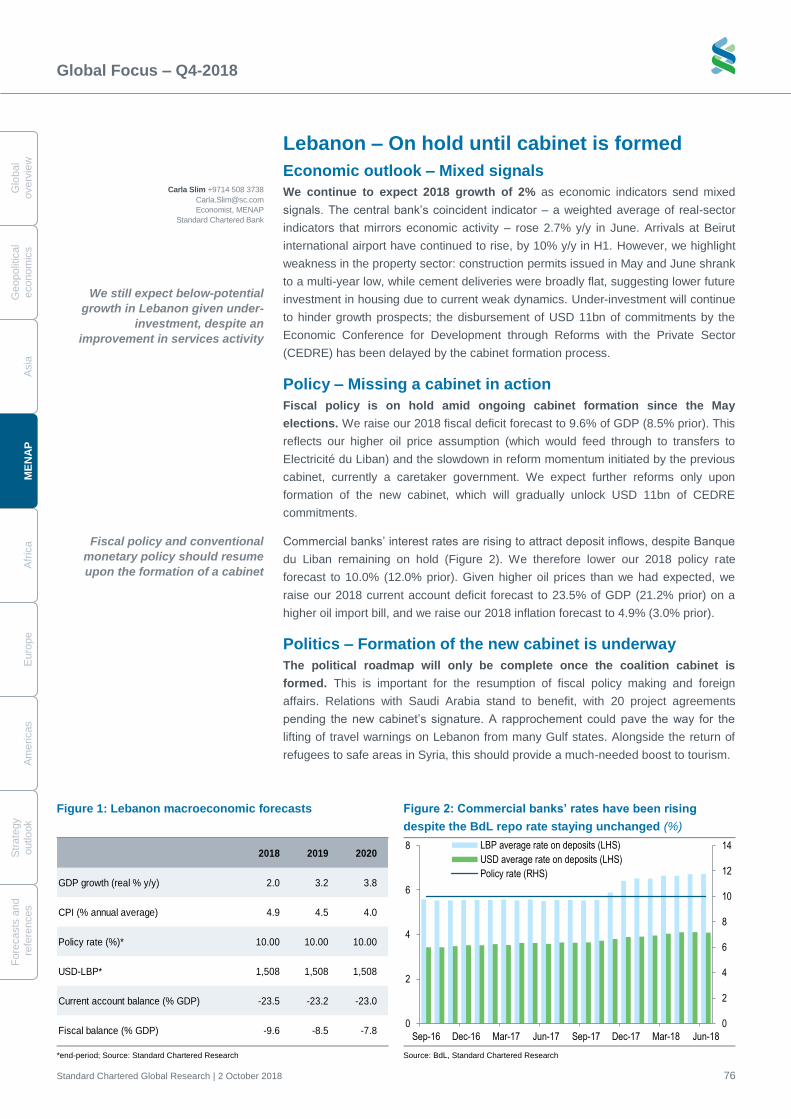

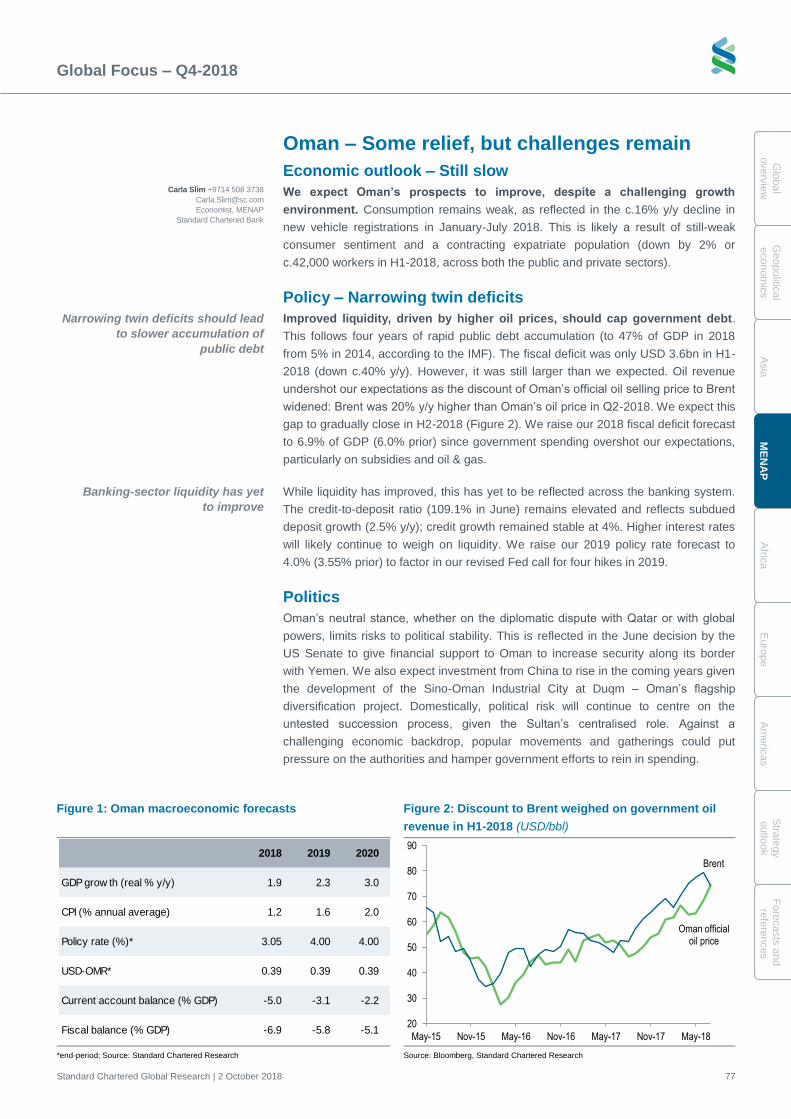

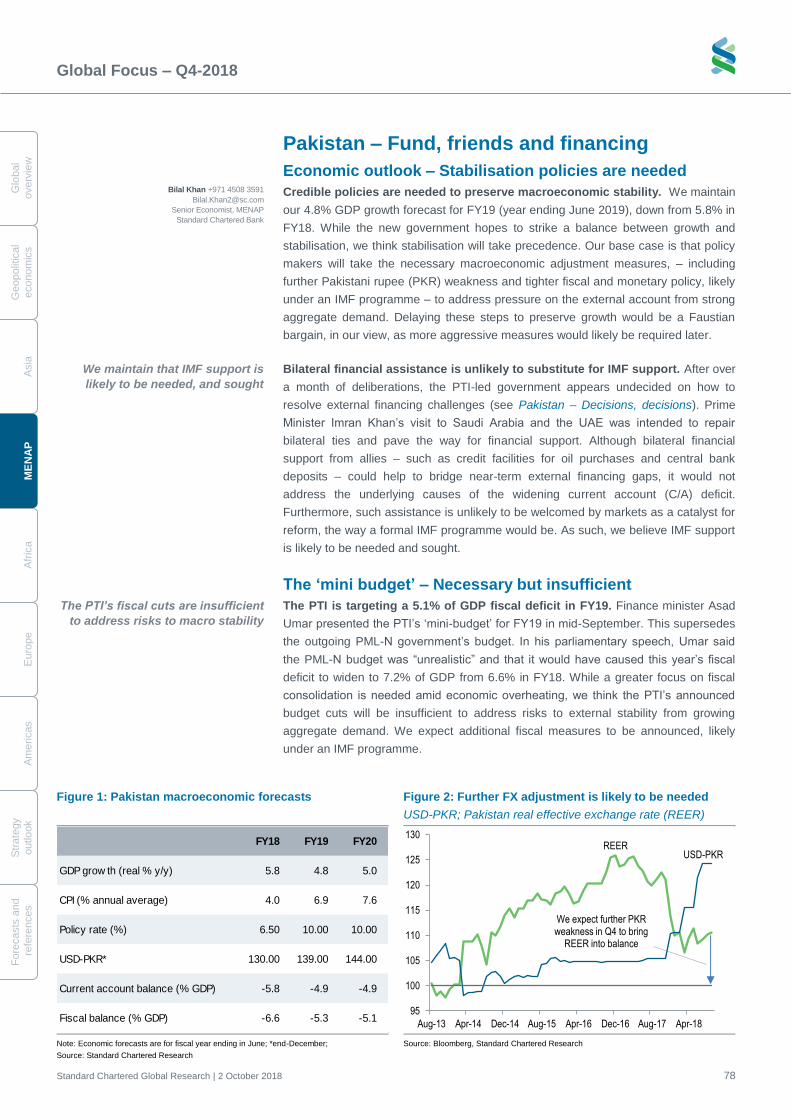

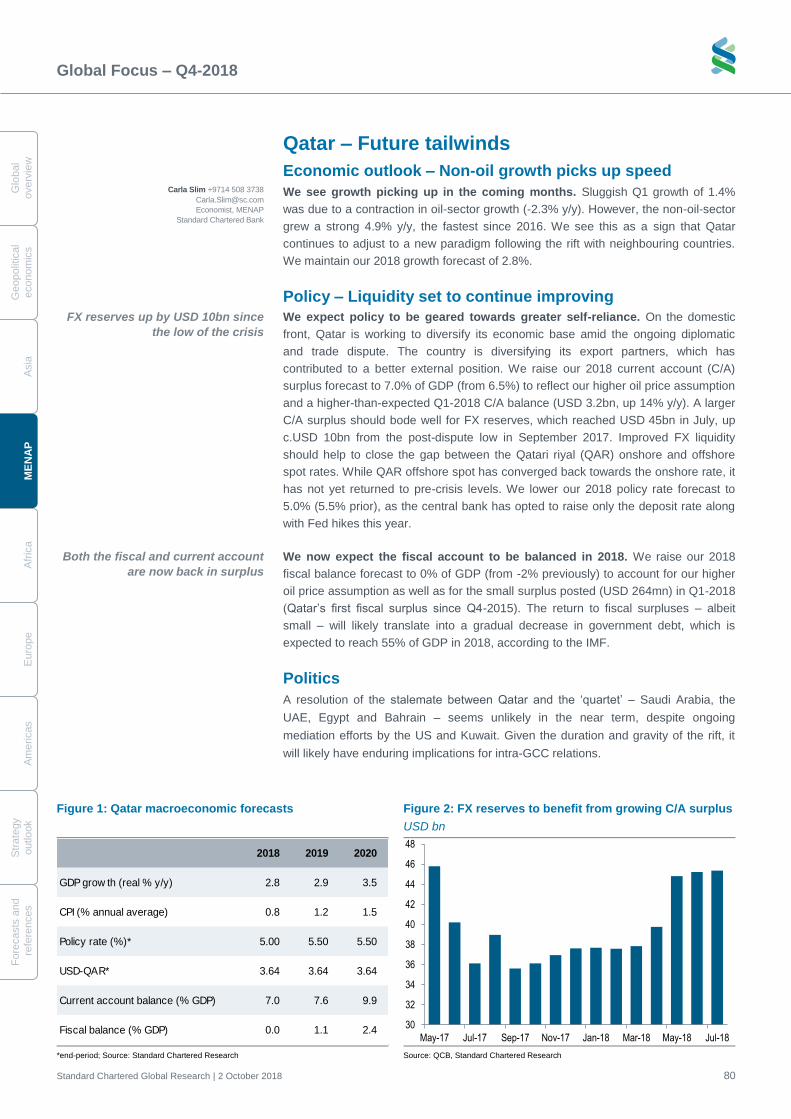

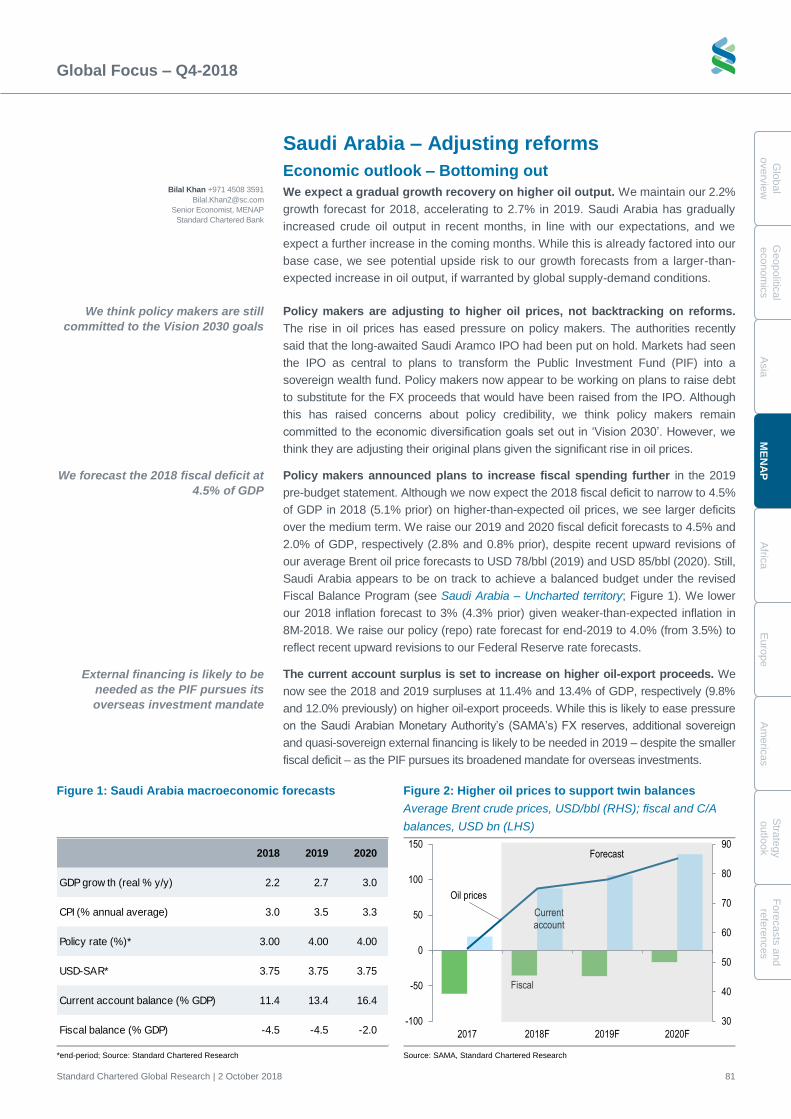

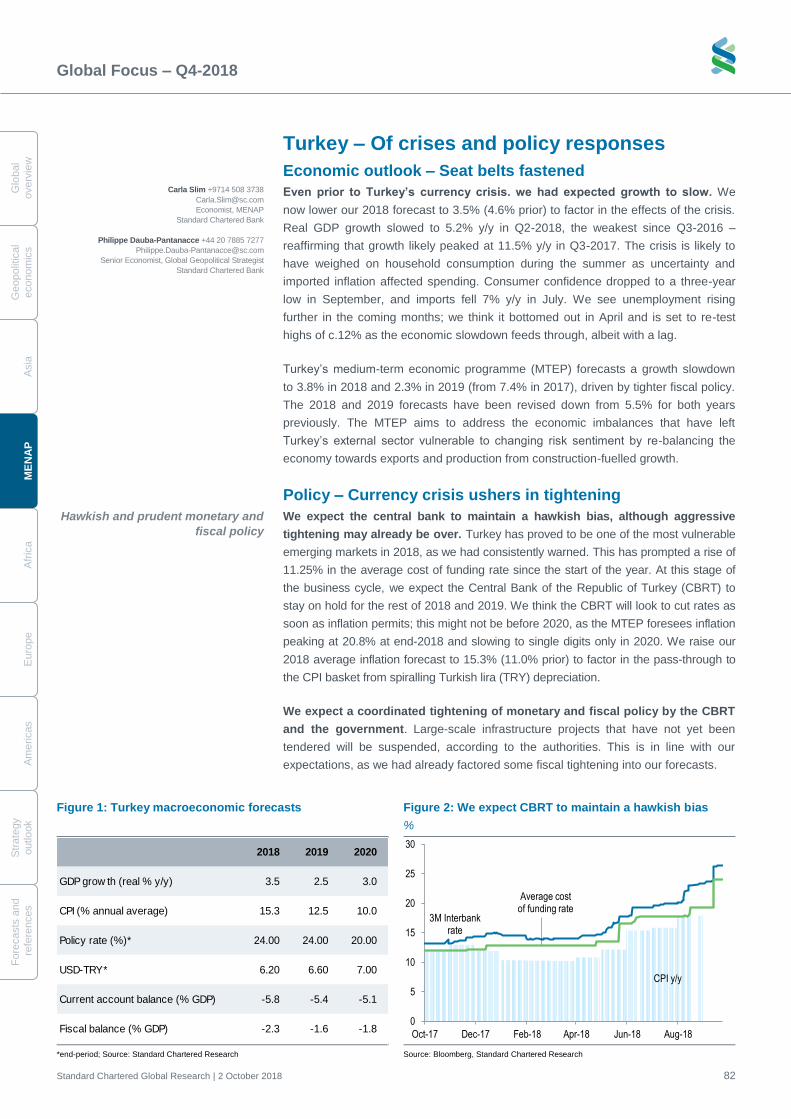

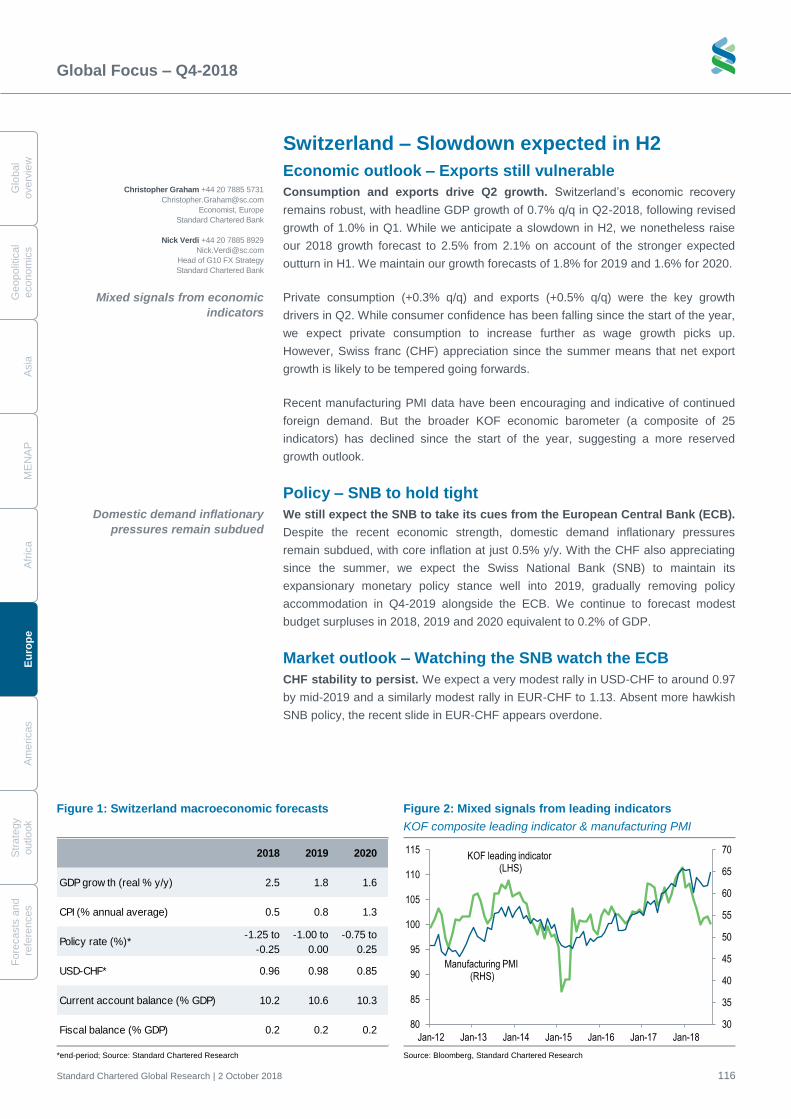

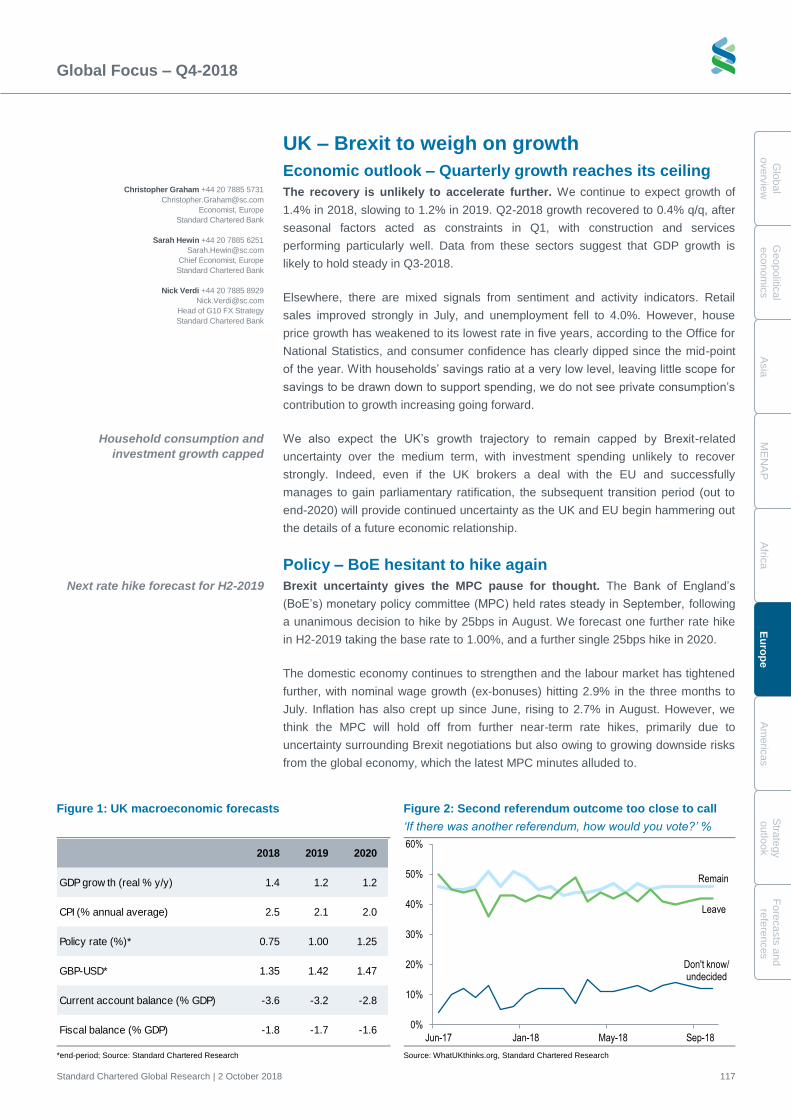

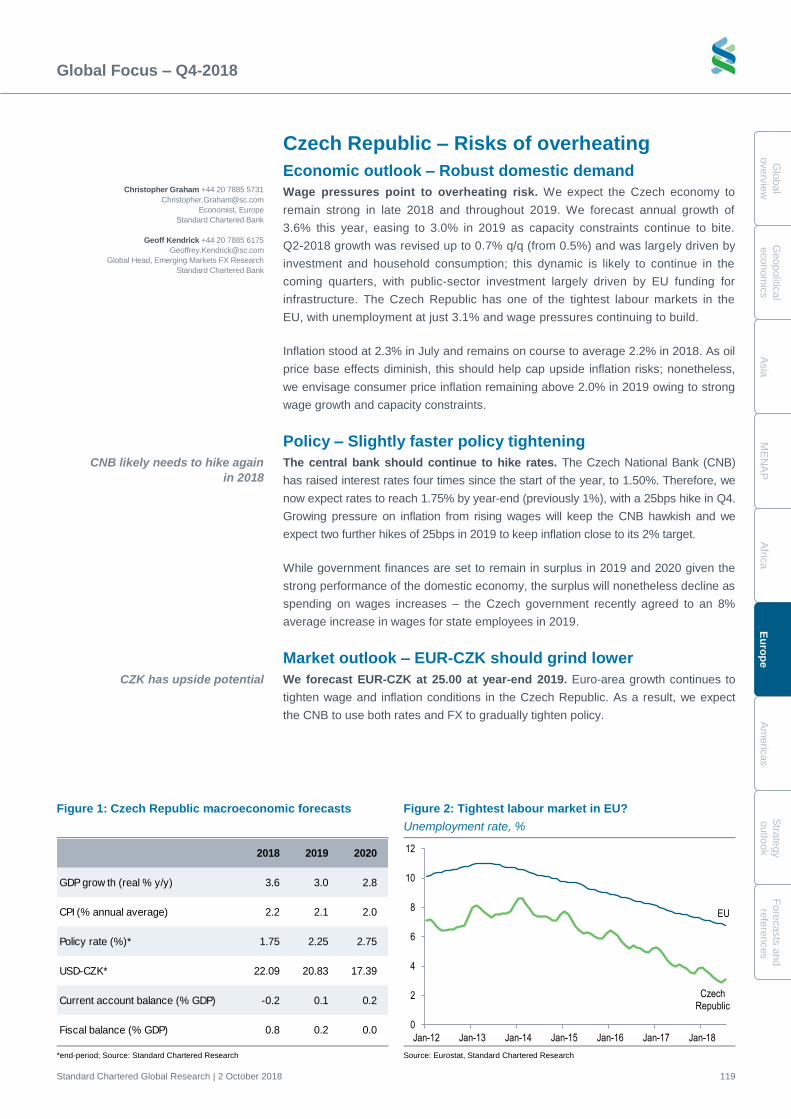

Citation preview

Global Research

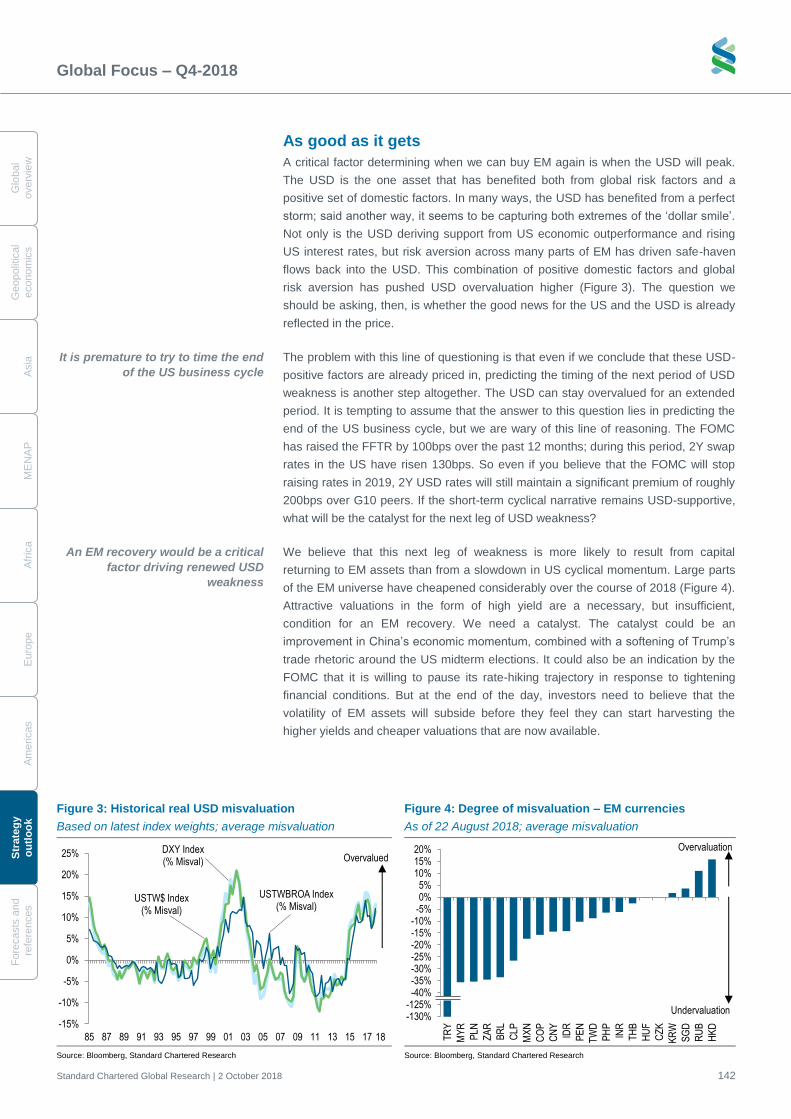

Issuer of Report Standard Chartered Bank, Singapore Branch

Important disclosures can be found in the Disclosures Appendix

All rights reserved. Standard Chartered Bank 2018 https://research.sc.com

Global Focus – Q4-2018

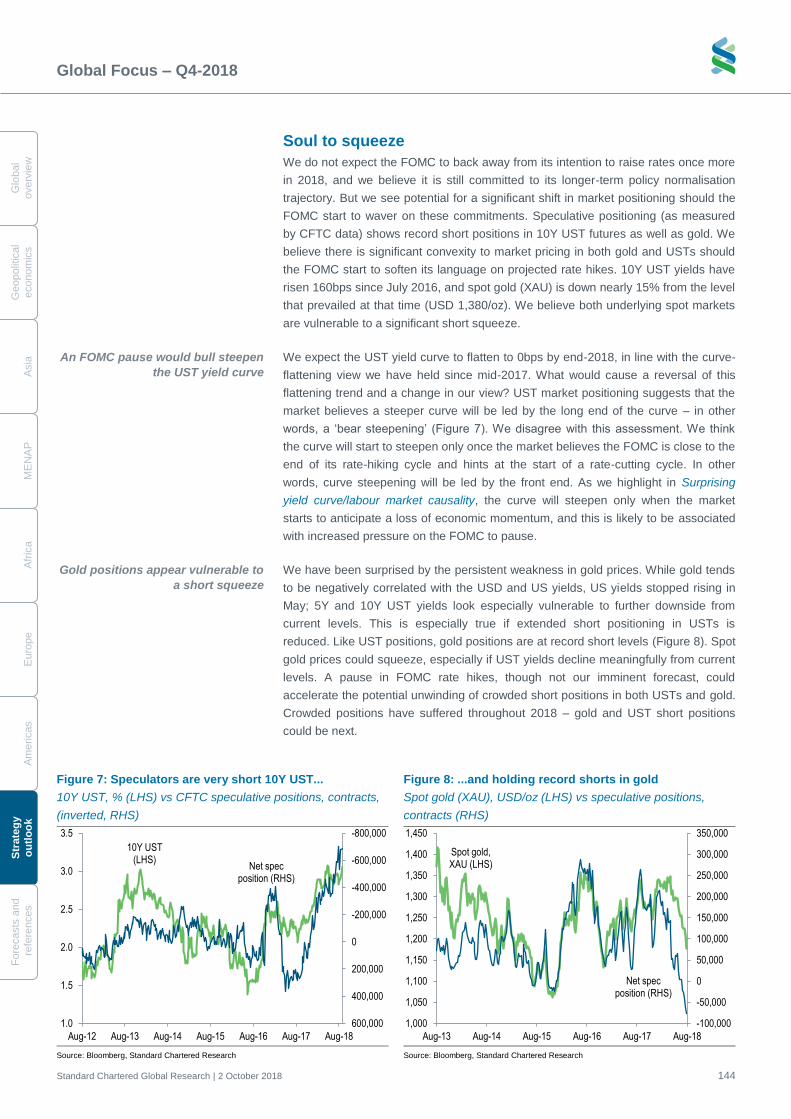

Beneath the surface

research.sc.com

Standard Chartered Global Research is available across all iOS and Android devices.

Our intuitive, accessible and customisable apps* allow you to receive our reports, forecasts, audio-visual presentations and

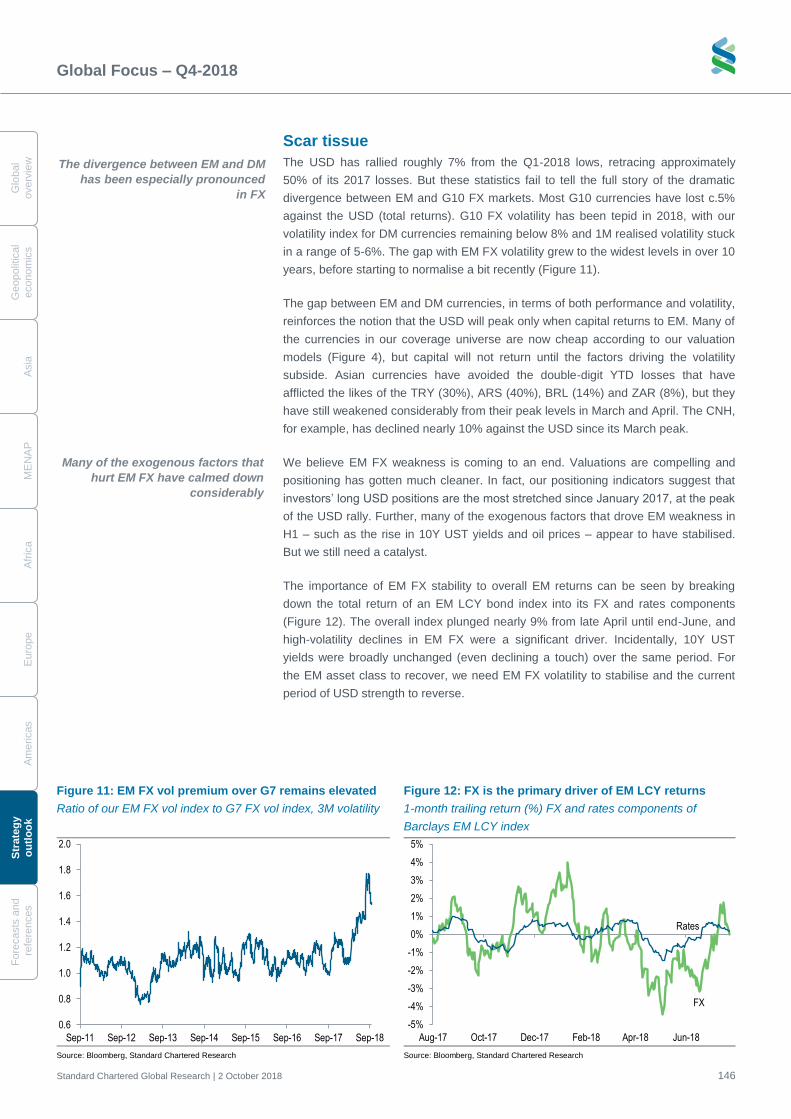

interactive data visualisation tools on-the-go.

* Click the icons to download or search ‘Standard Chartered Global Research’ in the app store.

If you are in scope for MiFID II and want to opt out of our Research services, please contact us.

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 2

Table of contents

Global overview 3

Executive summary 4 Distribution of world GDP growth 6 Global overview – Beneath the surface 10 Global charts 20

Geopolitical economics 22

US midterms – A looming risk for Trump 23

Economies – Asia 29

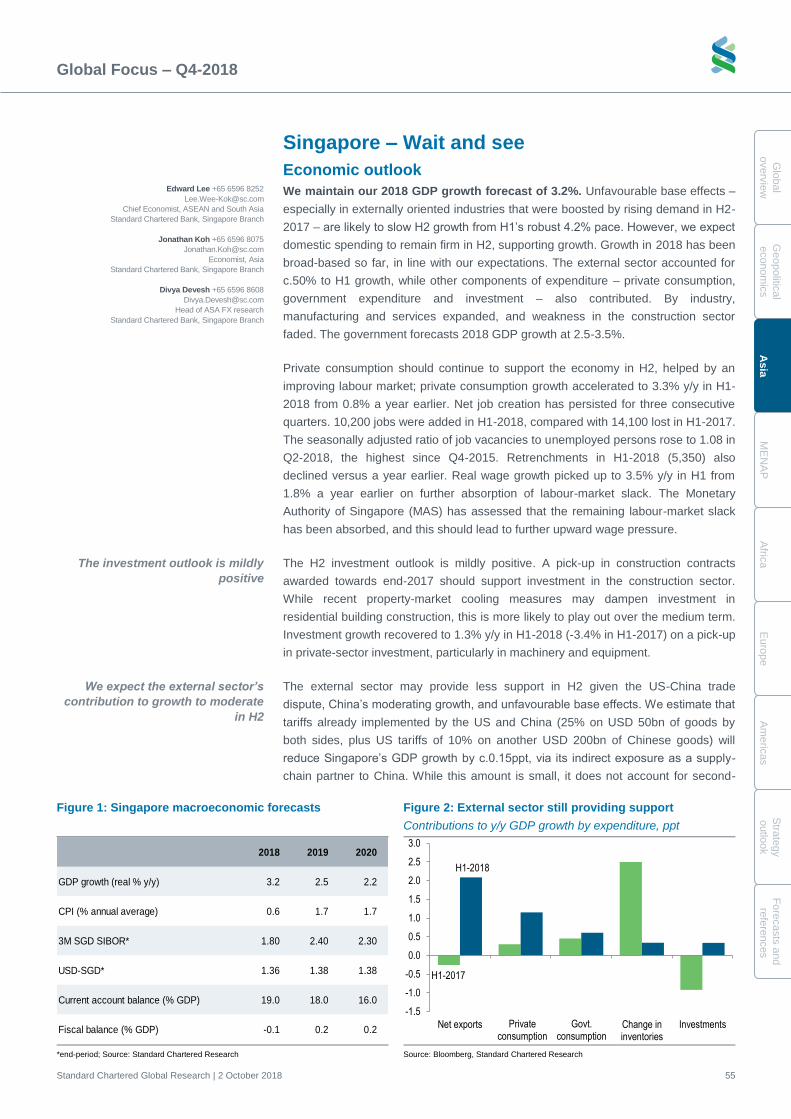

Asia – Top charts 30 Asia – Macro trackers 31 Australia – Boiling frog? 33 Bangladesh – A strong year likely; risks remain 35 China – Risks contained, despite downtrend 37 Hong Kong – A bumpier ride 39 India – Battling external headwinds 41 Indonesia – Playing defence 43 Japan – On a positive growth path 45 Malaysia – Will a single engine be enough? 47 Myanmar – Infrastructure projects needed 49 Nepal – Stable politics = better growth outlook 50 New Zealand – Dovishness is overdone 51 Philippines – More hikes to come 53 Singapore – Wait and see 55 South Korea – Between reality and ideals 57 Sri Lanka – Walking a tightrope 59 Taiwan – Growth momentum to slow 61 Thailand – About to move into election mode 63 Vietnam – Fast, not furious 65

Economies – Middle East, North Africa and

Pakistan 67

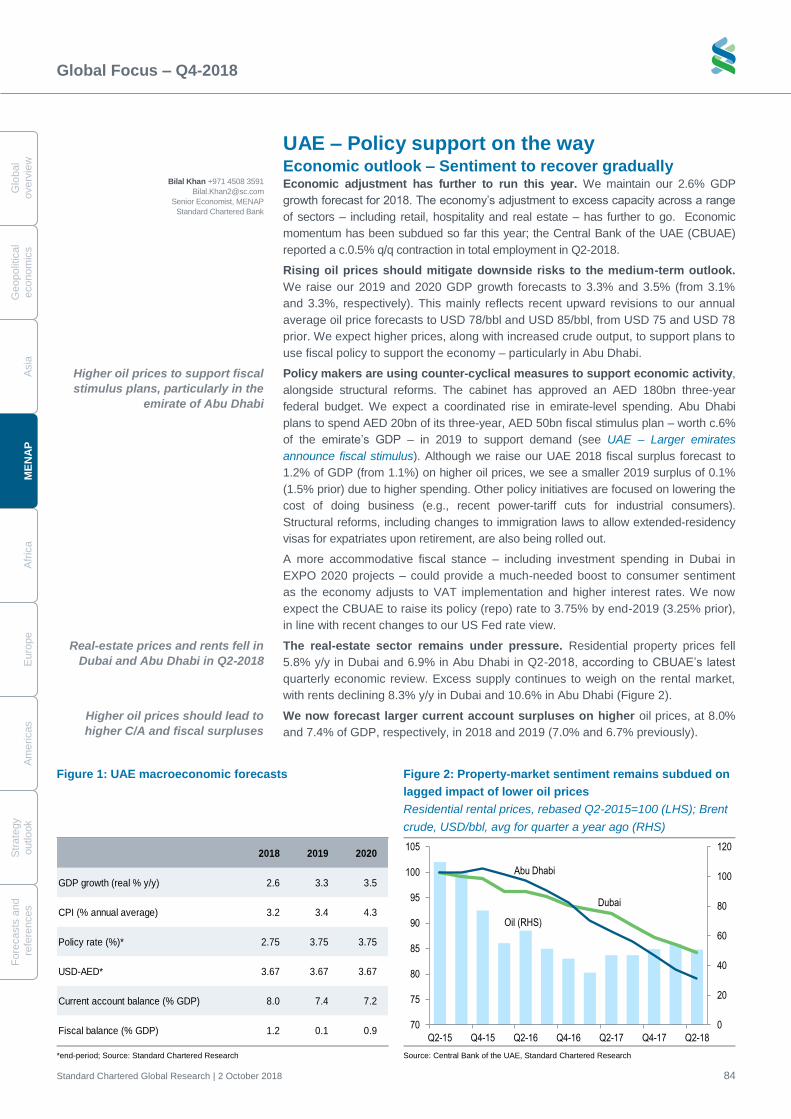

MENAP – Back to the future? 68 MENAP – Top charts 70 Bahrain – Funding for reform 71 Egypt – Steady progress 72 Iraq – Catching a break 73 Jordan – Just getting by 74 Kuwait – Getting back to growth 75 Lebanon – On hold until cabinet is formed 76 Oman – Some relief, but challenges remain 77 Pakistan – Fund, friends and financing 78 Qatar – Future tailwinds 80 Saudi Arabia – Adjusting reforms 81 Turkey – Of crises and policy responses 82 UAE – Policy support on the way 84

Economies – Africa 85

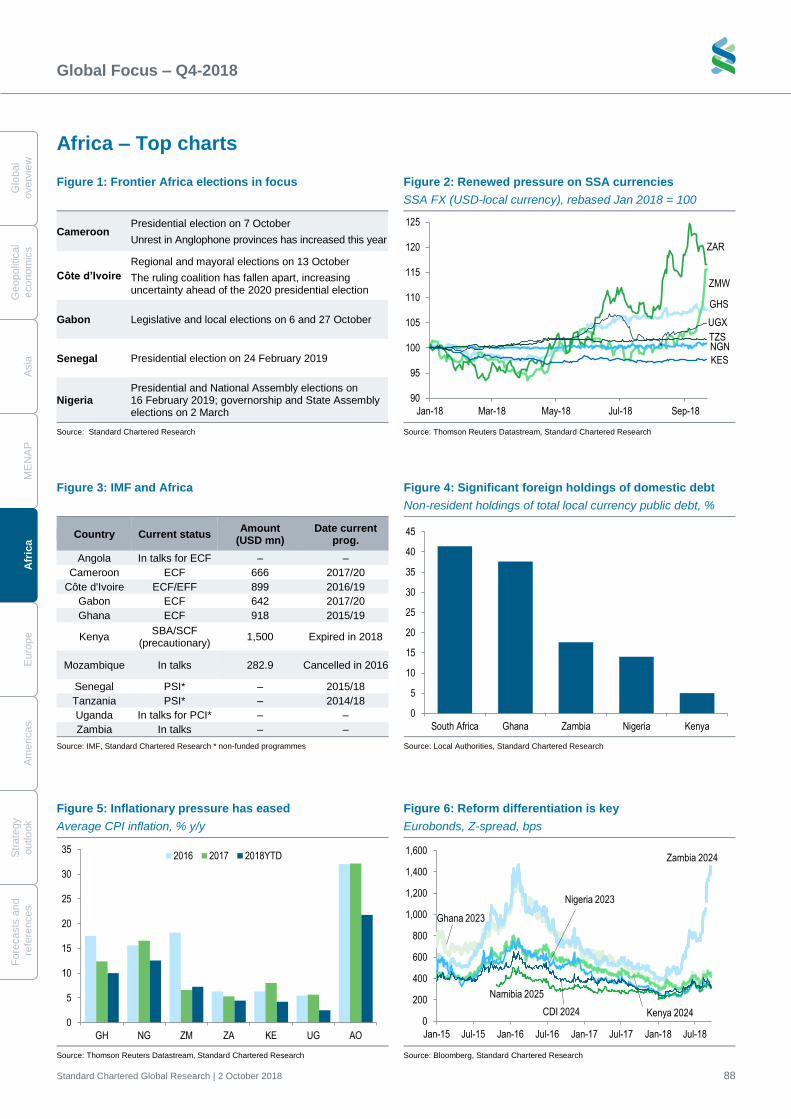

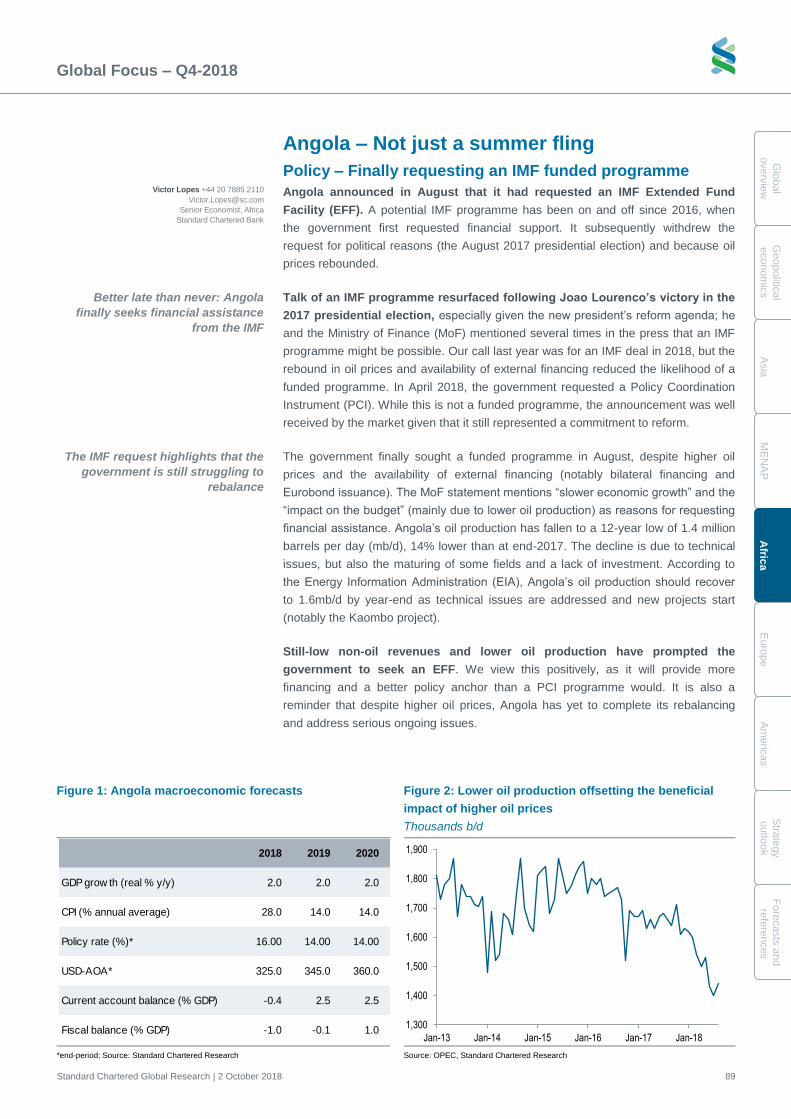

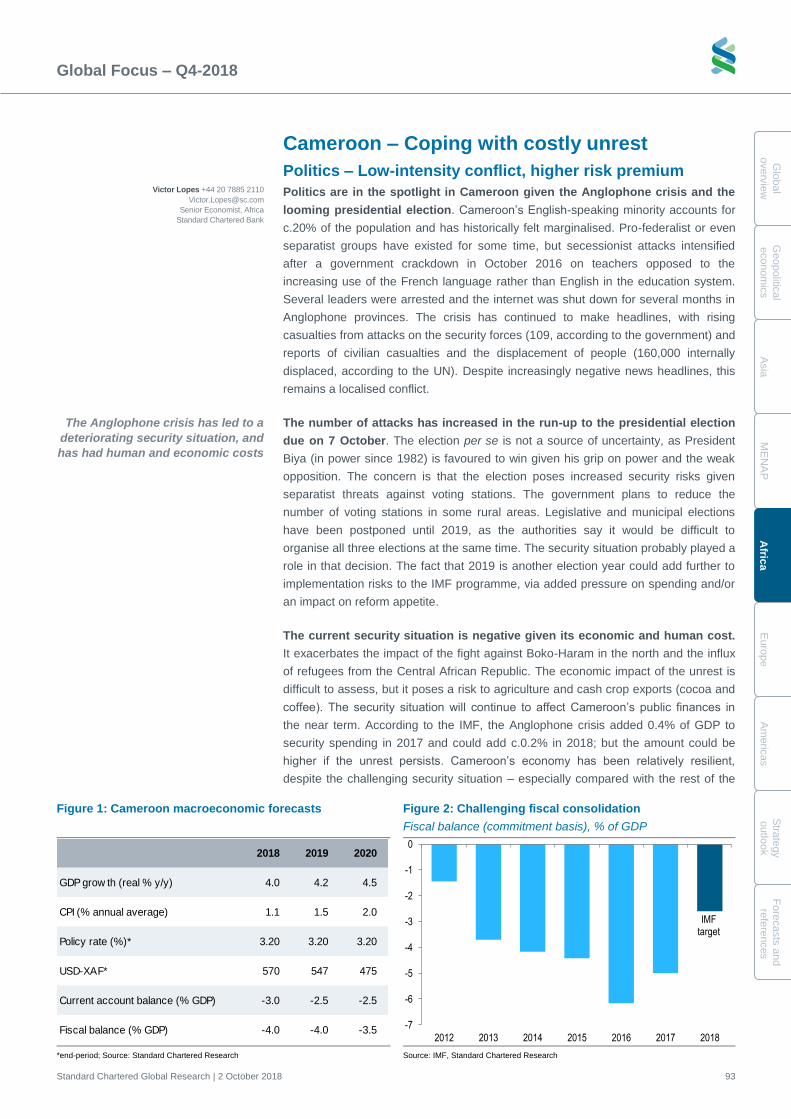

Africa – Navigating troubled waters 86 Africa – Top charts 88 Angola – Not just a summer fling 89 Botswana – A mining recovery 91

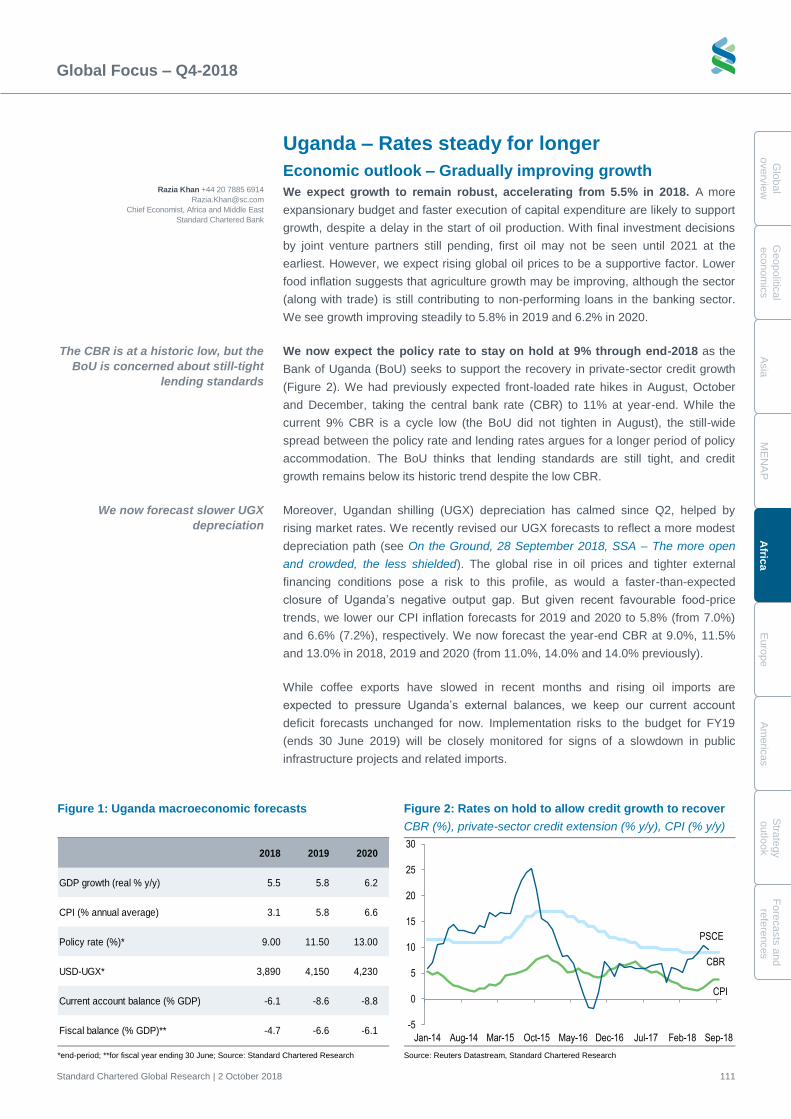

Cameroon – Coping with costly unrest 93 Côte d’Ivoire – Tomorrow is now 95 Ethiopia – New opportunities, old challenges 96 Gabon – Not there yet 97 Ghana – 25% bigger with recent rebasing 99 Kenya – Not such taxing times 101 Mozambique – Untying the Gordian knot 103 Nigeria – Politics, politics 105 Senegal – Losing its shine? 107 South Africa – Fears are overdone 108 Tanzania – Subdued outlook 110 Uganda – Rates steady for longer 111

Economies – Europe 112

Europe – Top charts 113 Euro area – Ending QE 114 Switzerland – Slowdown expected in H2 116 UK – Brexit to weigh on growth 117 Czech Republic – Risks of overheating 119 Hungary – Growth has likely peaked 120 Poland – Private consumption is key 121 Russia – Recovery remains intact 122

Economies – Americas 123

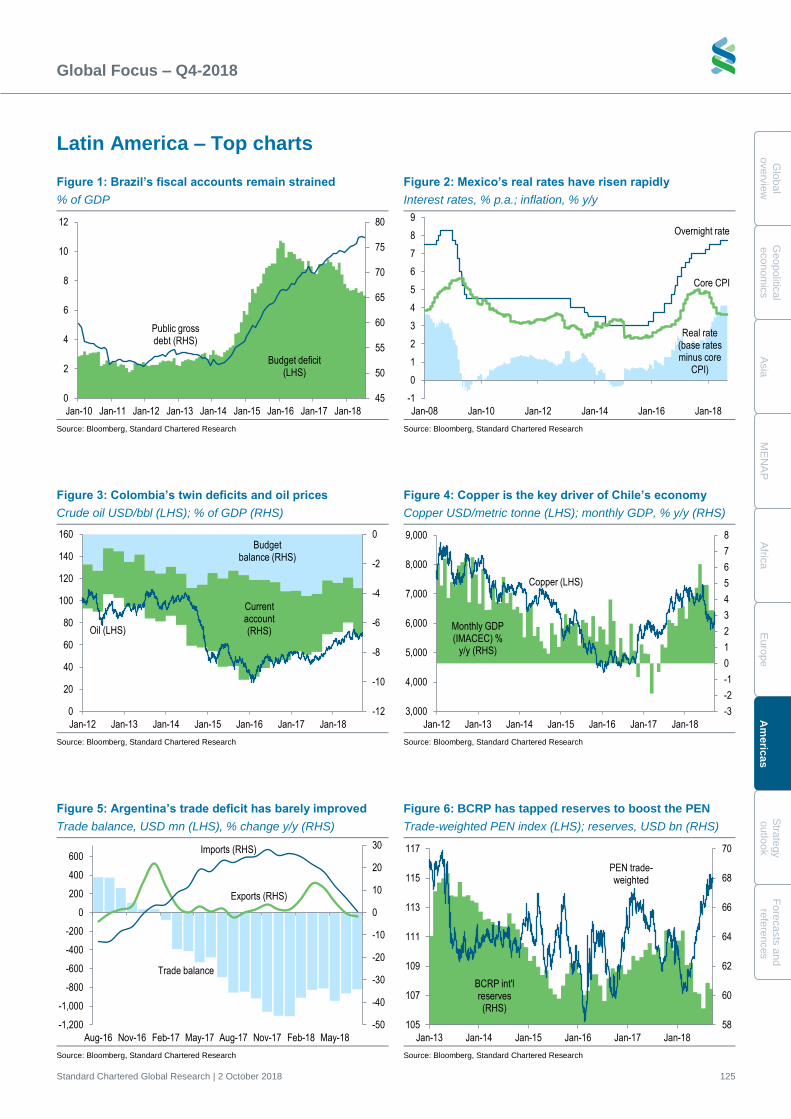

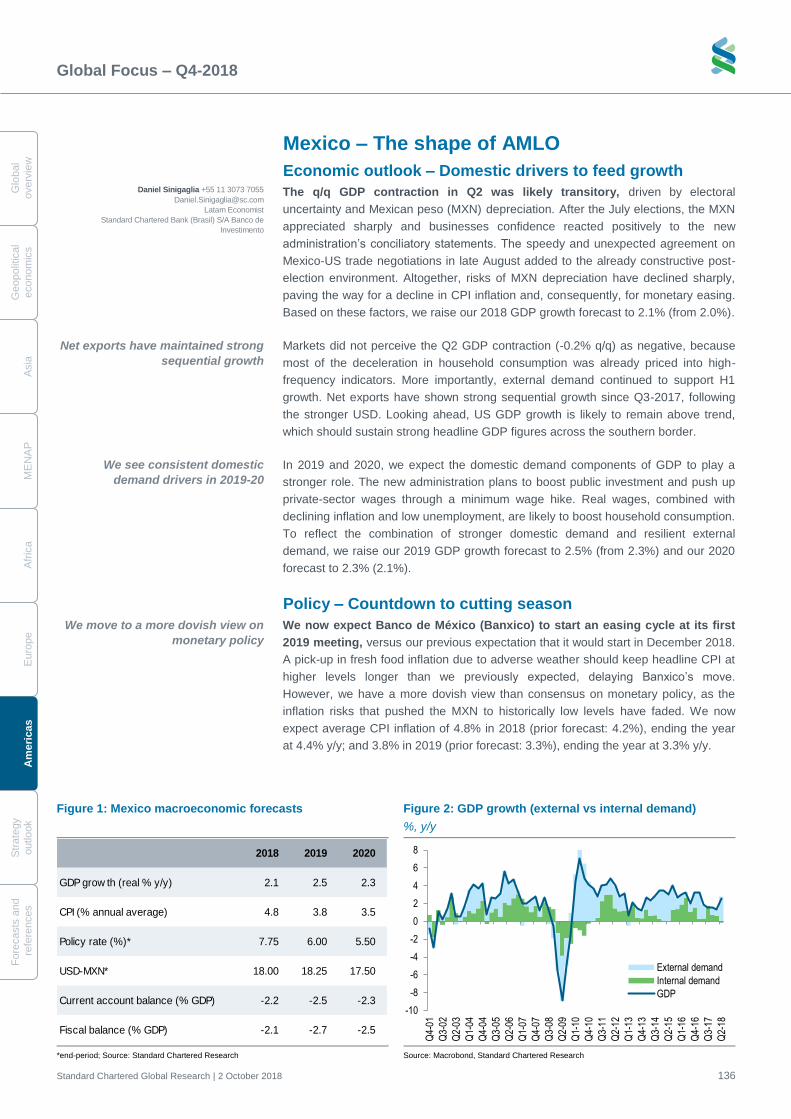

US and Canada – Top charts 124 Latin America – Top charts 125 US – Outlook remains positive 126 Canada – Internally solid, externally vulnerable 129 Brazil – Post-election hangover 130 Chile – Causes for concern 132 Colombia – Smells like animal spirits 134 Mexico – The shape of AMLO 136 Peru – Solid growth, fluid political backdrop 138

Strategy outlook 140

The return of the VaR shock 141

Forecasts and reference tables 148

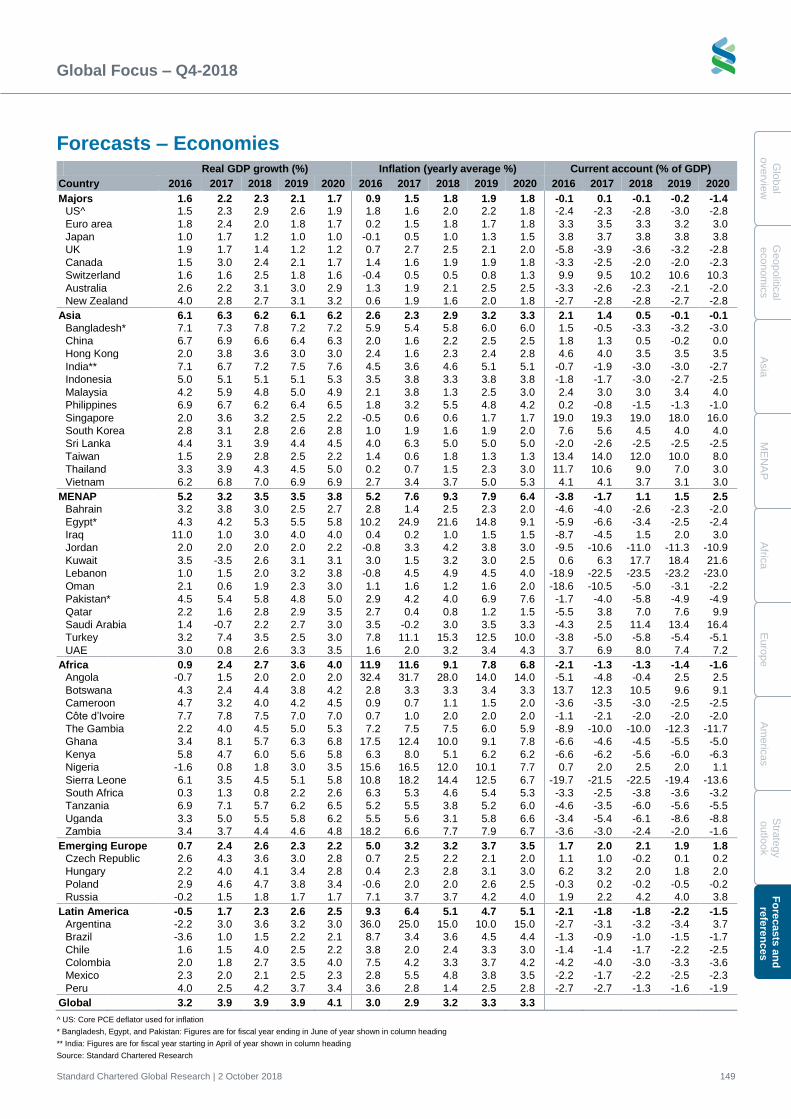

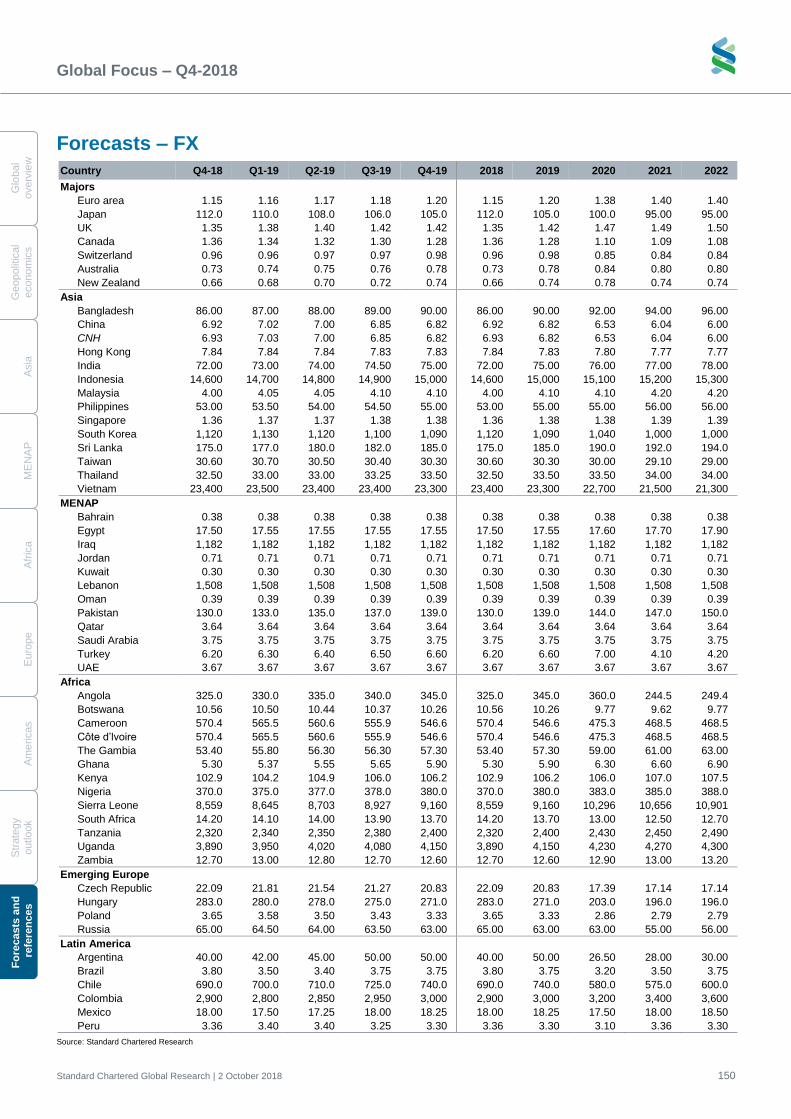

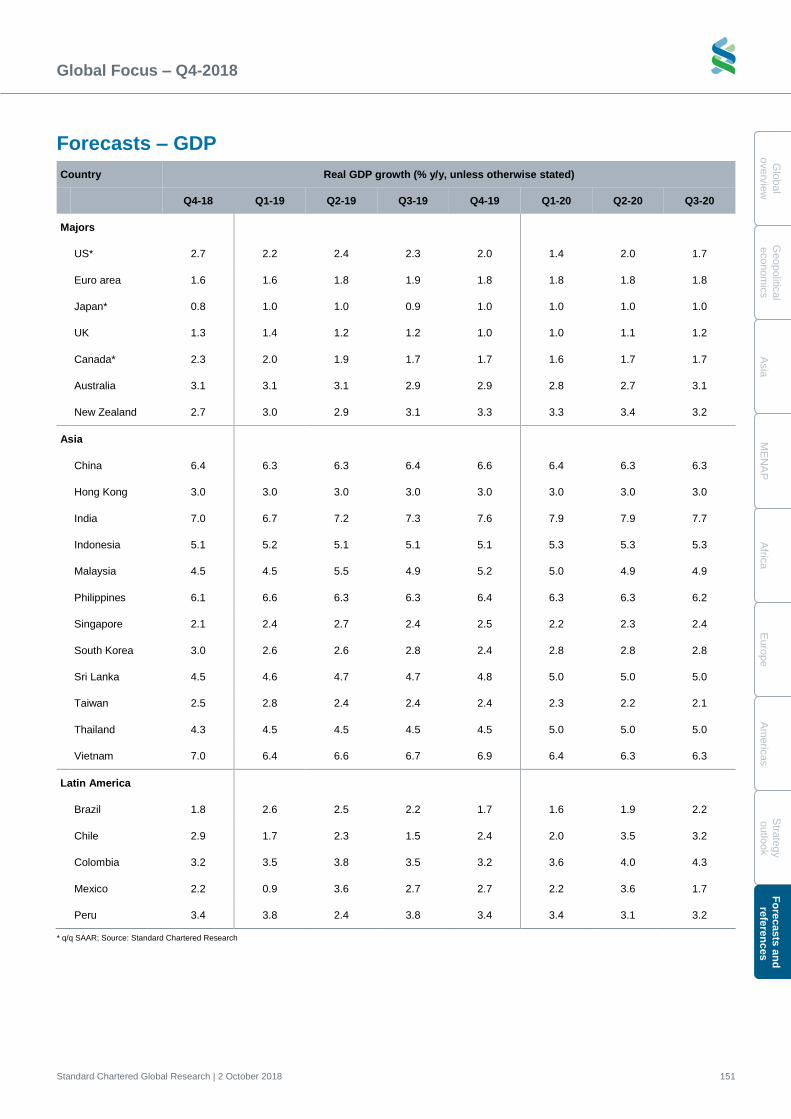

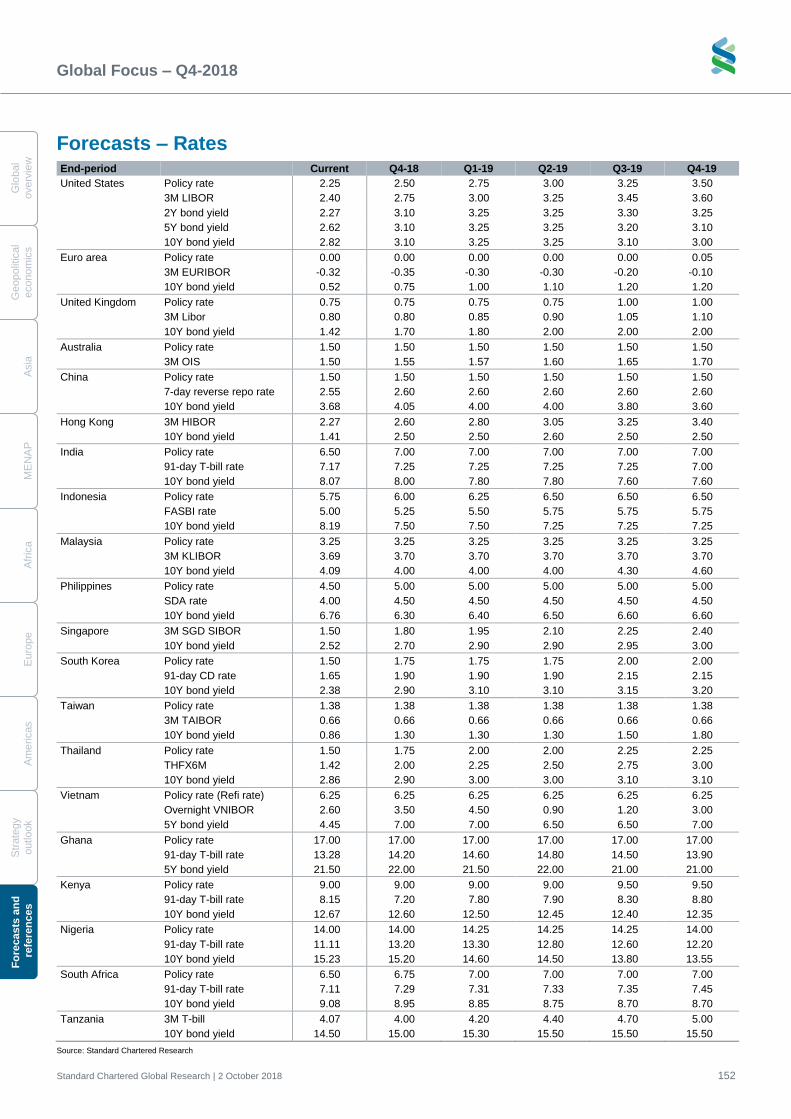

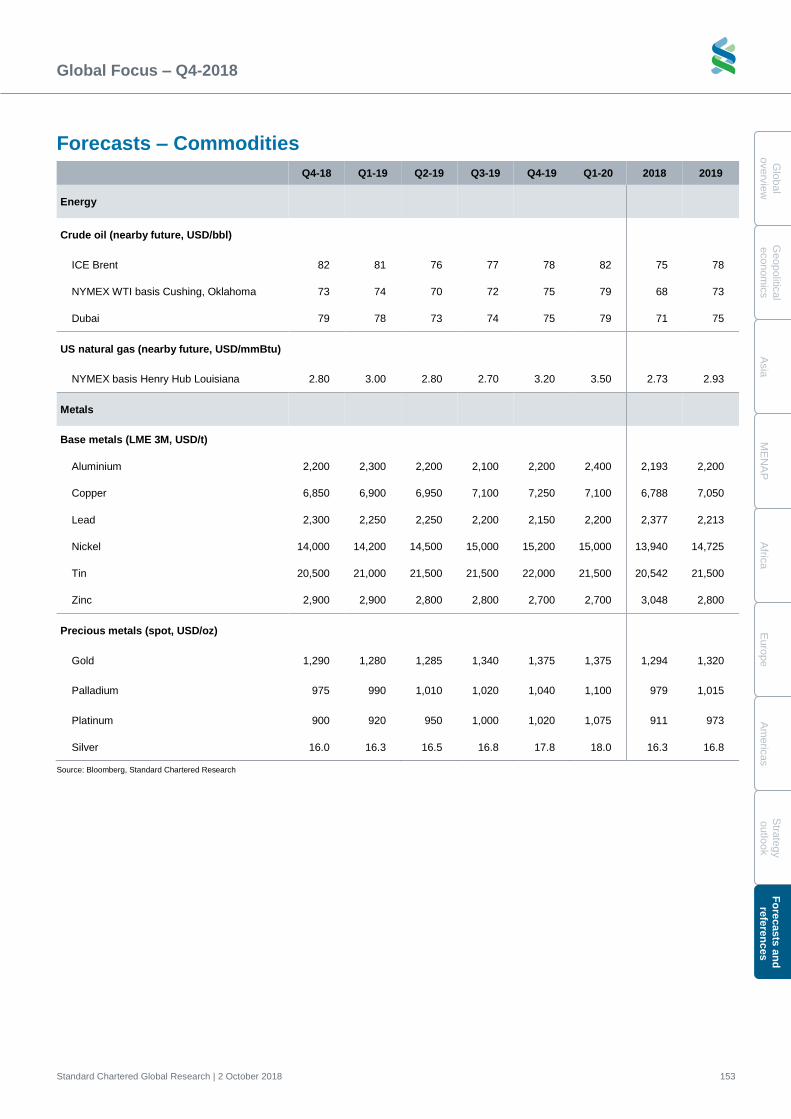

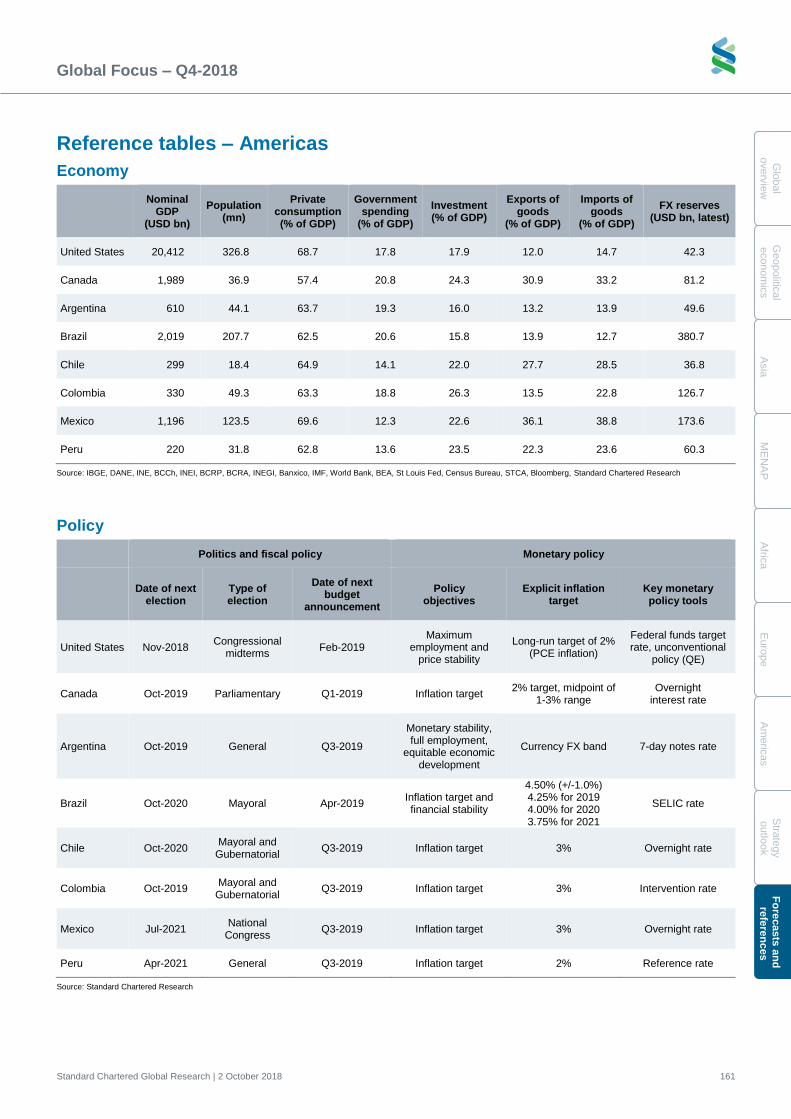

Forecasts – Economies 149 Forecasts – FX 150 Forecasts – GDP 151 Forecasts – Rates 152 Forecasts – Commodities 153 Forecasts – Long-term 154 Forecasts – Selected interbank rates by tenor 156 Reference tables – Asia 157 Reference tables – MENAP 158 Reference tables – Africa 159 Reference tables – Europe 160 Reference tables – Americas 161

Authors 162

Global overview

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 4

G

lob

al

o

verv

iew

Geopolit

ical

econom

ics

A

sia

M

EN

AP

A

fric

a

E

uro

pe

A

me

ricas

S

trate

gy

o

utlo

ok

Fo

recasts

and

re

fere

nces

Executive summary

Beneath the surface

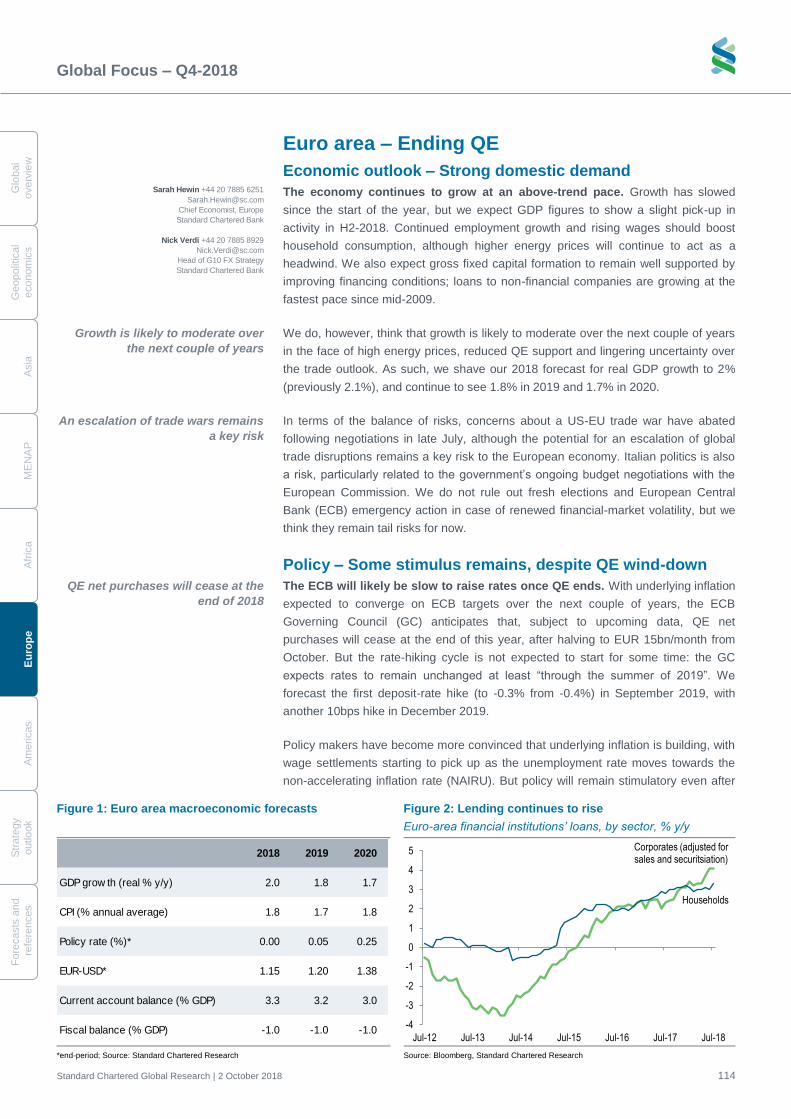

Global growth has been strong so far this year, and we maintain our 2018 global

growth forecast of 3.9%. We expect the same robust pace to be maintained in 2019.

The improved global outlook is largely premised on our upgraded US forecasts,

driven by the ‘sugar rush’ from fiscal stimulus.

But while global growth has been resilient so far, risks bubbling beneath the surface

have increased since the start of 2018. These include the escalating US-China trade

war; a break higher in oil prices; and tightening global liquidity conditions due to the

end of the QE era, trends in the USD, and US monetary tightening. These factors

have led to mounting external pressure on emerging markets with twin deficits,

resulting in more aggressive monetary tightening in these economies.

Emerging markets with twin deficits

are having to tighten monetary

policy more aggressively

China: China’s economy is likely to lose further momentum in the coming months

amid rising trade tensions with the US and slowing housing-market growth. The

government is committed, however, to achieving its 6.5% growth target for 2018,

using more proactive fiscal policy via tax cuts and infrastructure spending to boost

domestic demand. We see limited room to loosen monetary policy further. On the

Chinese yuan (CNY), we expect more efforts by the authorities to slow depreciation

and prevent USD-CNY breaking above 7.0 this year.

ASEAN: Slowing growth in China and worries about escalating US-China trade

tensions are already beginning to affect export growth sentiment in ASEAN countries.

However, the growth outlook remains benign and ASEAN economies have been more

resilient to EM risk aversion than those in EMEA or Latin America. Domestic demand –

especially government infrastructure spending – should support growth in Indonesia, the

Philippines and Thailand. The inflation picture is mixed in ASEAN. The Philippines

central bank has hiked rates aggressively to counter strong inflationary pressure.

Indonesia’s inflation is comparatively manageable; while Bank Indonesia has also

tightened policy aggressively, Indonesian rupiah (IDR) stability has been the main driver.

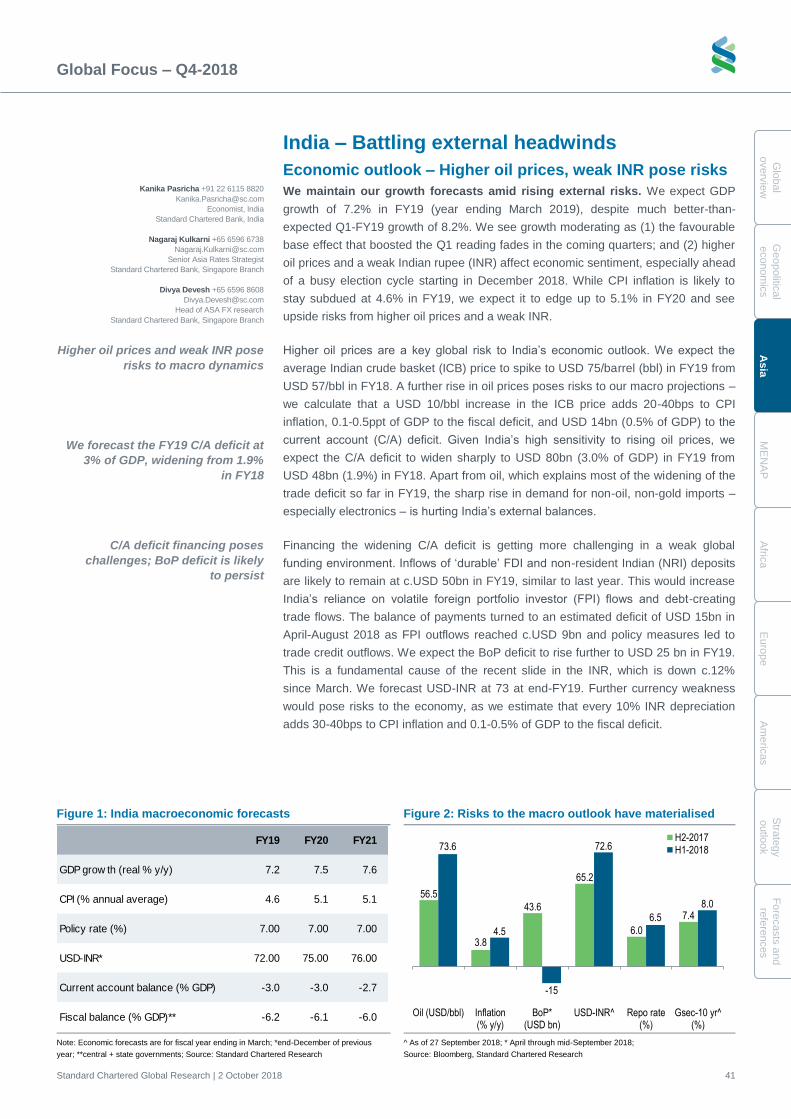

India: India is one of the fastest-growing EM economies. However, higher oil prices

are a key global risk to India’s economic outlook. Policy makers are likely to stay

focused on managing external headwinds through monetary policy tightening, direct

measures to narrow the deficit, and fiscal prudence.

US monetary policy is likely to

remain relatively benign despite

four more rate hikes in 2019

US: The near-term economic outlook has strengthened further on fiscal stimulus,

and we recently raised our 2018 GDP growth forecast to 2.9%. Given the strength of

real growth and the tight labour market, we have raised our expectation of the

terminal federal funds target rate to 3.50%. Despite pencilling in a higher terminal

rate, we expect the policy stance to remain relatively benign. The US midterm

elections in November are increasingly becoming the focus for investors, who view it

as a ‘practice run’ for the 2020 presidential race. The House appears more

vulnerable than the Senate to a Democratic takeover.

Europe: The euro-area economy continues to grow at an above-trend pace,

supported by household consumption and investment spending. Growth is likely to

moderate over the next couple of years, however, in the face of high energy prices,

reduced QE support and an uncertain trade outlook. Concerns about Italy’s fiscal

position are likely to persist, especially as QE ends. While the European Central

Bank is on track to end QE, it is likely to be slow to raise rates. Brexit negotiations will

continue to dominate sentiment in the UK, with rising concerns about a ‘hard’ Brexit.

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 5

Glo

ba

l

ov

erv

iew

Geopolitic

al

econom

ics

Asia

ME

NA

P

Afric

a

Euro

pe

Am

eric

as

Stra

tegy

outlo

ok

Fo

recasts

and

refe

rences

Africa: Commodity prices are key to the outlook. Higher oil prices have benefited

Nigeria and have been crucial in avoiding deeper economic crises in Angola and

Gabon. Among oil importers, Senegal’s fundamentals may deteriorate the most.

Further Fed tightening, trade-war concerns and EM vulnerabilities will shape the

external environment for Sub-Saharan Africa. Commitment to IMF programmes in

several countries will be crucial to maintaining investor confidence.

IMF programmes are important for

continued investor confidence for

several countries in SSA and

MENAP

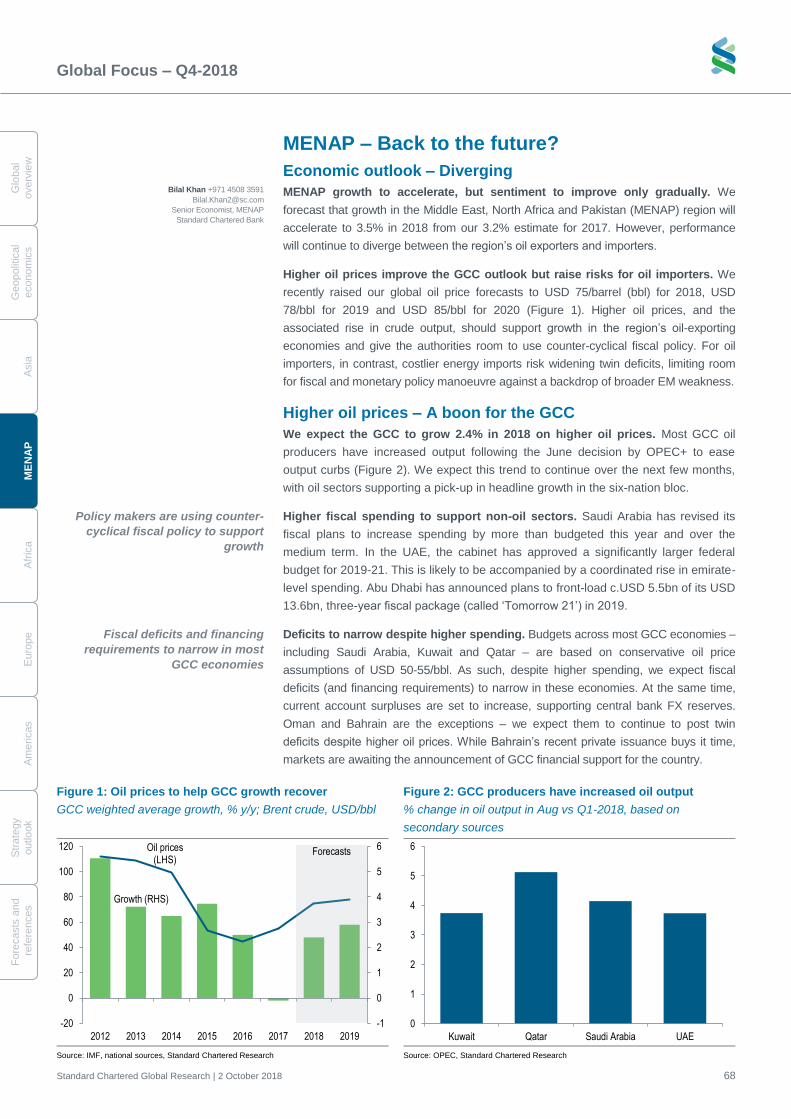

MENAP: Higher oil prices improve the outlook for the GCC but raise risks for oil

importers. We forecast that growth in the Middle East, North Africa and Pakistan

(MENAP) region will accelerate to 3.5% in 2018 from our 3.2% estimate for 2017. For

GCC countries, higher oil prices will allow lower budget deficits despite an increase in

fiscal spending. We expect monetary policy to tighten across MENAP. Due to external

vulnerabilities, Egypt, Jordan and Iraq are in IMF programmes; Pakistan is likely to follow.

Latin America: Growth is diverging across economies. Peru, Colombia and Chile

are benefiting from increasing business confidence as incoming administrations try to

move to a pro-business reform agenda. Growth in Brazil and Argentina, on the other

hand, has underperformed Latam peers due to election-related risks (in Brazil) and a

currency crisis driven by a collapse in confidence over macro adjustment (Argentina).

Intensifying trade tensions and a stronger USD have affected local currencies.

Consequently, monetary policy is taking on a more explicit tightening bias, although

underlying inflation pressures are under control.

Where we differ from consensus

US: We see one more FOMC hike in 2018 (in December) and four in 2019, versus

the consensus call of three more hikes between now and end-2019. Our view is

premised on a strong US labour market and a positive output gap.

China: We forecast a faster deterioration in China’s current account (C/A) balance

than consensus. We expect the C/A surplus to turn to a deficit of 0.2% of GDP in

2019 from a surplus of 0.5% in 2018 as trade tariffs start to hurt exports.

Korea: We expect the BoK to hike rates in 2019, unlike the market consensus. Concerns

about rising wealth inequality and financial stability are likely to drive this decision.

Indonesia: We expect a wider current account deficit than market consensus, driven

by unfavourable commodity price movements.

MENAP: Egypt’s central bank is unlikely to cut rates, despite falling inflation, as it

seeks to protect against capital outflows. In Pakistan, we still think markets are

under-pricing monetary tightening. Pakistani rupee (PKR) adjustment amid higher oil

prices is likely to pressure CPI inflation higher. We expect the central bank to

respond with another 150bps of hikes.

Latin America: We think economic activity has already peaked in Chile, as it is

vulnerable to the current global combination of high oil prices and low metal prices. In

Mexico, we expect more aggressive rate cuts than consensus, as we see inflation

sharply undershooting consensus from Q2-2019. In Colombia, we expect growth to

be stronger than consensus, supported by domestic demand and higher oil prices.

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 6

G

lob

al

o

verv

iew

Geopolit

ical

econom

ics

A

sia

M

EN

AP

A

fric

a

E

uro

pe

A

me

ricas

S

trate

gy

o

utlo

ok

Fo

recasts

and

re

fere

nces

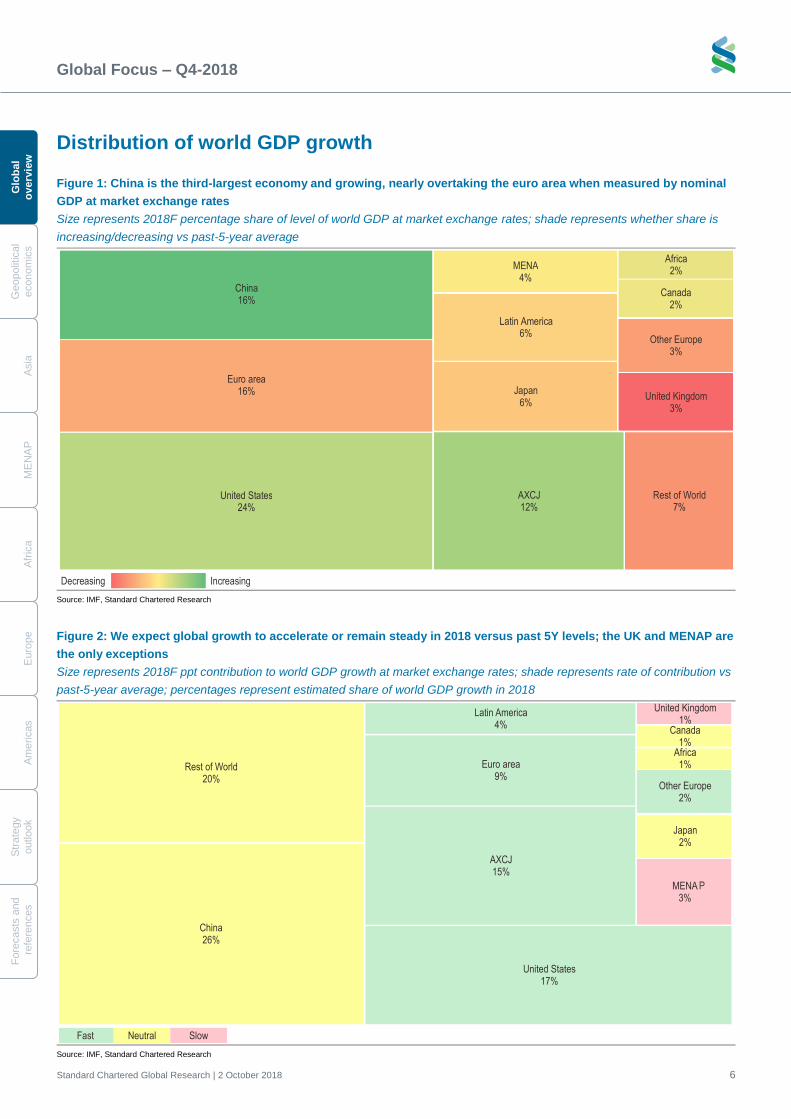

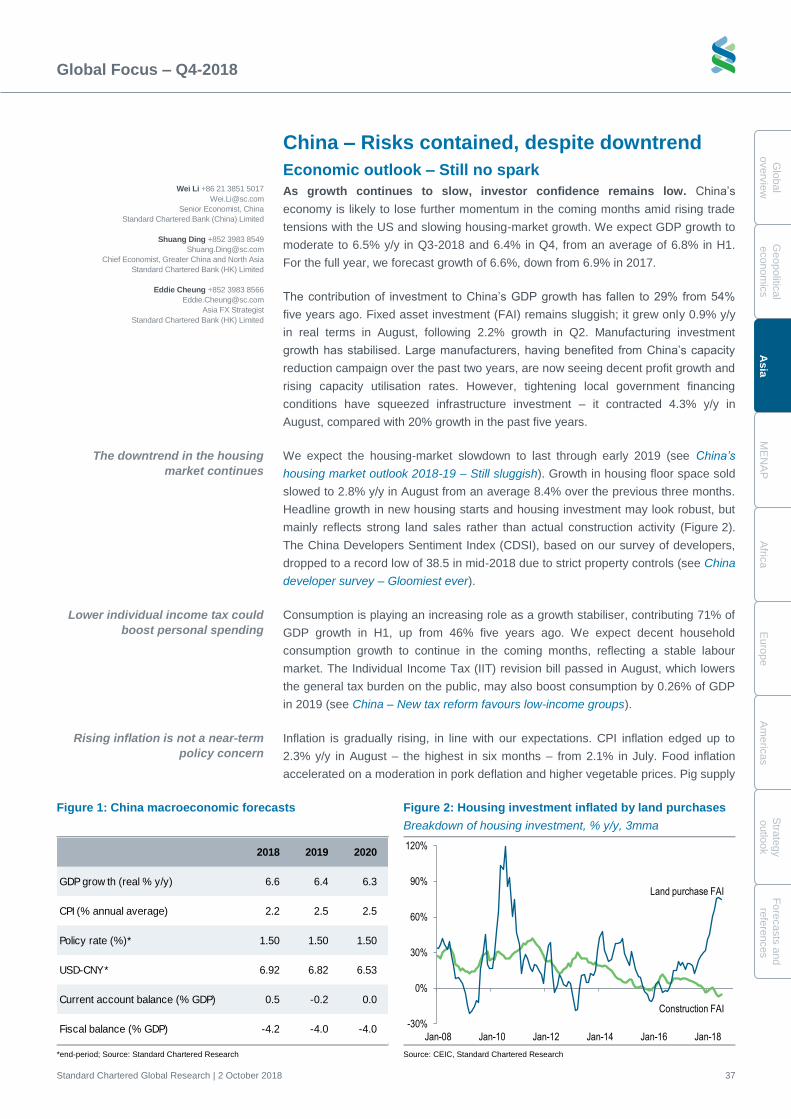

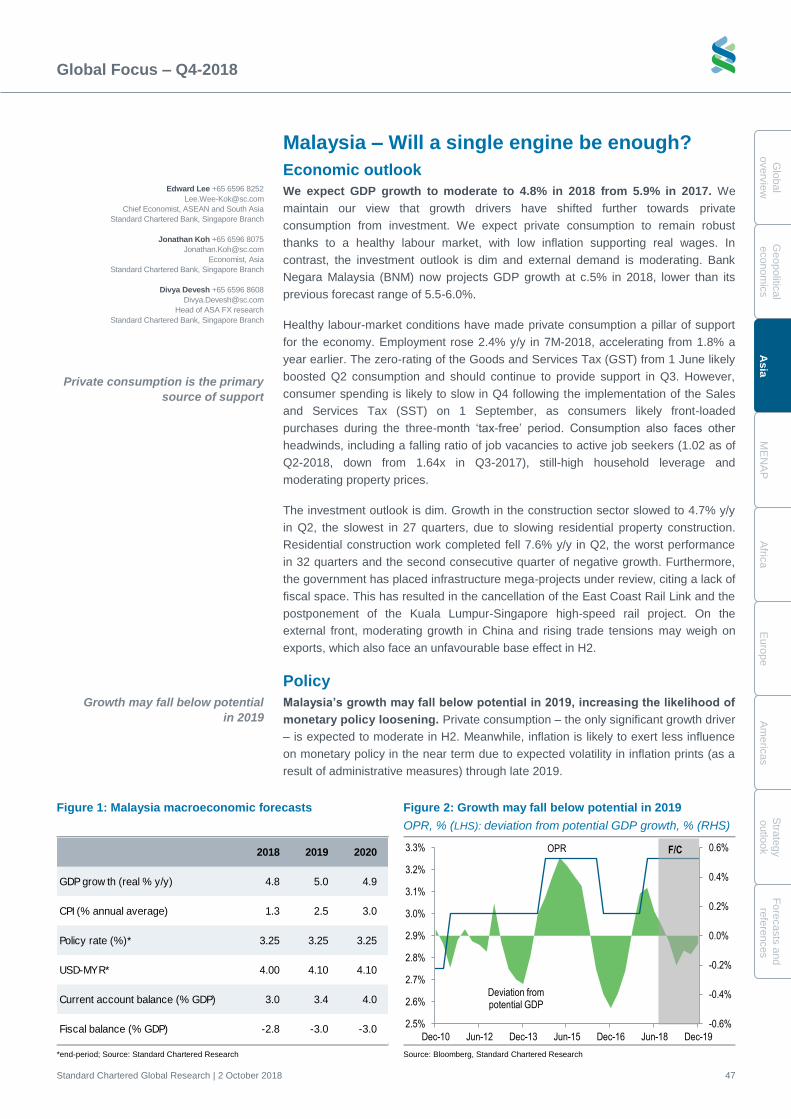

Distribution of world GDP growth

Figure 1: China is the third-largest economy and growing, nearly overtaking the euro area when measured by nominal

GDP at market exchange rates

Size represents 2018F percentage share of level of world GDP at market exchange rates; shade represents whether share is

increasing/decreasing vs past-5-year average

Source: IMF, Standard Chartered Research

Figure 2: We expect global growth to accelerate or remain steady in 2018 versus past 5Y levels; the UK and MENAP are

the only exceptions

Size represents 2018F ppt contribution to world GDP growth at market exchange rates; shade represents rate of contribution vs

past-5-year average; percentages represent estimated share of world GDP growth in 2018

Source: IMF, Standard Chartered Research

China26%

Euro area9%

United States17%

AXCJ15%

Japan2%

Latin America4%

MENA3%

Africa1%Rest of World

20%

United Kingdom1%

Canada1%

Other Europe2%

Fast Neutral Slow

P

China 16%

Euro area 16%

United States 24%

AXCJ 12%

Japan 6%

Latin America 6%

MENA 4%

Africa 2%

Rest of World 7%

United Kingdom 3%

Canada 2%

Other Europe 3%

Decreasing Increasing

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 7

Glo

ba

l

ov

erv

iew

Geopolitic

al

econom

ics

Asia

ME

NA

P

Afric

a

Euro

pe

Am

eric

as

Stra

tegy

outlo

ok

Fo

recasts

and

refe

rences

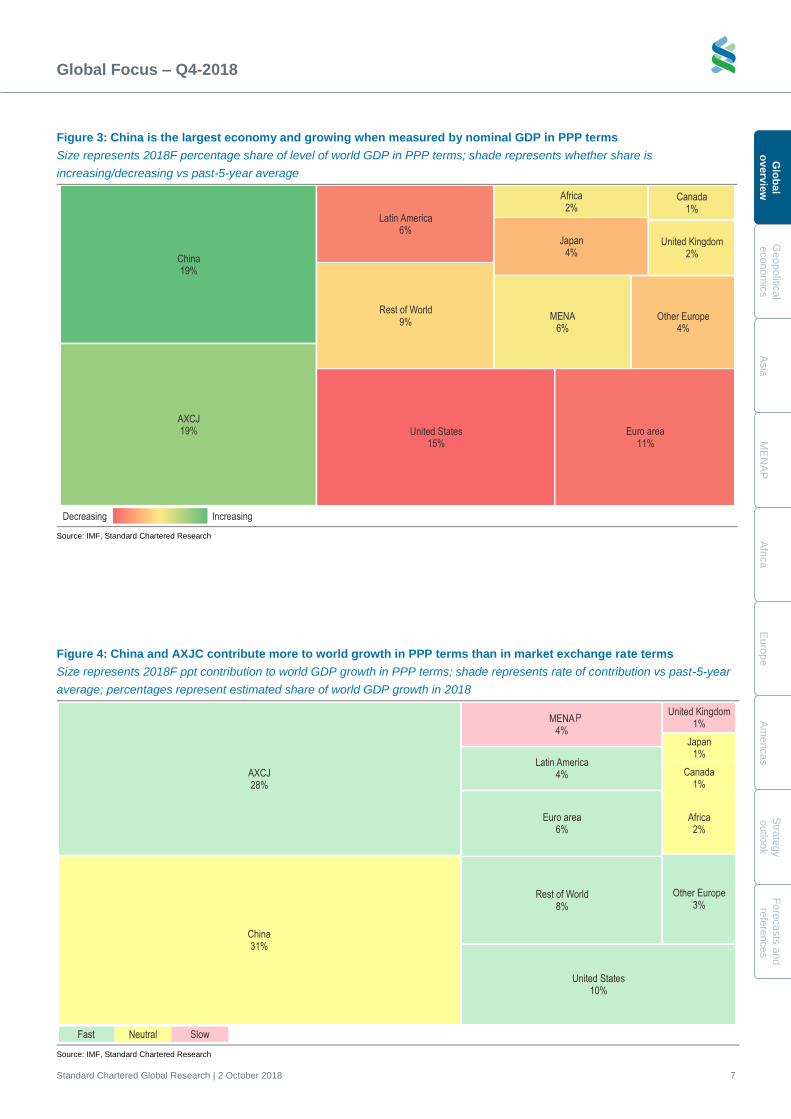

Figure 3: China is the largest economy and growing when measured by nominal GDP in PPP terms

Size represents 2018F percentage share of level of world GDP in PPP terms; shade represents whether share is

increasing/decreasing vs past-5-year average

Source: IMF, Standard Chartered Research

Figure 4: China and AXJC contribute more to world growth in PPP terms than in market exchange rate terms

Size represents 2018F ppt contribution to world GDP growth in PPP terms; shade represents rate of contribution vs past-5-year

average; percentages represent estimated share of world GDP growth in 2018

Source: IMF, Standard Chartered Research

China31%

Euro area6%

United States10%

AXCJ28%

Japan1%

Latin America4%

MENA4%

Africa2%

Rest of World8%

United Kingdom1%

Canada1%

Other Europe3%

Fast Neutral Slow

P

China 19%

Euro area 11%

United States 15%

AXCJ 19%

Japan 4%

Latin America 6%

MENA 6%

Africa 2%

Rest of World 9%

United Kingdom 2%

Canada 1%

Other Europe 4%

Decreasing Increasing

Glo

bal F

oc

us

– Q

4-2

01

8

Sta

nd

ard

Charte

red

Glo

bal R

esea

rch | 2

Octo

ber 2

018

8

Global overview

Geopolitical economics

Asia

MENAP

Africa

Europe

Americas

Strategy outlook

Forecasts and references

Figure 5: Global economic trackers – Our indicators suggest that inflation has picked up globally

Selection of our preferred economic indicators for economies in the region

Indicator CN IN ID KR MY PH TH TW VN HK SG AU JP NZ US DE UK BR MX ZA TR

Economy

GDP (% y/y) 6.7↓ 8.2↑ 5.3↑ 2.8 4.5↓ 6.0↓ 4.6 3.3↑ 7.1 3.5 3.9↓ 3.4↑ 1.3↓ 2.8 2.9↑ 2.3↑ 1.3 1.0↓ 2.6↑ 0.4↓ 5.2↓

Credit growth (% y/y 3mma) 32.3↑ 9.5 10.7↑ 5.1↑ 17.7↓ 7.6↓ 5.2↑ 16.9↓ 5.6↑ 4.7↓ 2.1↑ 19.4↑ 1.9↓ 4.0↓ 2.5↑ 5.2↓ 11.9↓

MCI Tracker ↑ ↓ ↑ ↑ ↓ ↑ ↓ ↓ ↓ ↓ ↑ ↓ ↑ ↑ ↑ ↑

Stock market performance (% y/y 3mma) -14.0↓ 17.3↑ 1.3↓ -3.0↓ 0.0↓ -4.6↓ 5.3↓ 4.9↓ 24.1↓ 5.4↓ -0.3↓ 9.5↑ 13.6↓ 17.5↑ 14.5↑ 2.7 3.2↑ 14.5↓ -3.4 7.6↓ -10.0↓

Domestic

Manufacturing PMI (3mma) 51.3 52.4↑ 50.9 49.3 50.1↑ 51.9 50.1 53.5↓ 54.8↑ 48.1↓ 52.5↓ 52.6↓ 59.9↑ 55.5↓ 53.6↓ 50.5↓ 51.6↓ 47.4↓

Industrial production (% y/y 3mma) 6.0↓ 5.8 4.6↓ 0.6↑ 2.2↓ 12.0 3.5 2.2↓ 13.3↑ 1.6↑ 6.0↓ 3.5↓ 1.8↓ 4.1↑ 2.3↓ 1.1↓ 0.3↓ 0.6 1.5↑ 5.8↓

Capital goods imports (% y/y 3mma) 2.0↑ 26.7↑ 30.6↑ -15.7↓ 5.6↑ 32.1↑ -1.8↑ 16.2↑ 8.8↑ 13.0↑ 8.0 5.7 16.3↓ 8.0↓ 0.0↑ -9.3↑ 151.8↑ 14.0 -3.2↓

Retail sales (% y/y 3mma) 8.9 2.7 6.3 9.8↑ 7.1↑ 3.0↓ 11.0↑ 10.9↓ -0.1↓ 2.7 1.3 3.8↑ 6.5↑ 2.7↓ 5.7↑ 4.1 3.5↑ 2.0↓ 4.2↓

Inflation (% y/y 3mma) 2.1 4.3↓ 3.2↓ 1.5 0.6↓ 5.8↑ 1.5↑ 1.6↓ 4.4↑ 2.4 0.6↑ 2.1↑ 1.0 1.5↑ 2.8↑ 2.0↑ 2.5 4.4↑ 4.8 4.9↑ 16.4↑

Property market index (% y/y 3mma) 17.0 7.6 2.1↑ 1.9 4.1↓ 2.1↓ 5.7↓ 1.1↓ 16.3↑ 9.1↑ -0.6↓ 1.6↓ 5.2↑ 7.2↑ 2.2↓ -0.6↑ 10.1↑

External

Exports (% y/y 3mma) 12.1↑ 25.1↑ 21.4↑ 3.1↑ 7.0 5.9↑ 6.2↑ 6.3↓ 12.8 8.8 5.5 13.7↑ 6.0 9.8↑ 9.6↑ 4.6 5.2↑ 38.1↑ 17.8↑ 7.6↑ 39.3↑

Exports broadness index (destination) ↑ ↓ ↓ ↓ ↓ ↓ ↑ ↑ ↑ ↓ ↓ ↑ ↓ ↑ ↓ ↑ ↑ ↑ ↑

Tourist arrivals (% y/y 3mma) 4.4 11.8 26.6↑ -1.7↑ 7.4↓ 5.6↓ 3.3 14.9↓ 8.6↓ 8.3↑ 5.7↑ 8.1↓ -0.2↓ 2.8↓ 1.3↓ -2.5↓ 21.2↓

↓ Slower ↑ Faster

Fast Neutral Slow

Cell colours (medium-term performance): Metrics growing ‘fast’ compared to their 3-year average are coloured green; those growing ‘slow’ versus the 3-year average are red. Our threshold for ‘fast’ and ‘slow’ is the 3-year average +/- 0.5 standard deviations.

Arrows (near-term performance): Metrics growing faster than their 6mma are identified with an upward arrow (↑); those growing slower than the 6mma are marked with a downward arrow (↓); thresholds for ‘faster ()’ and slower ()’ are 6mma +/- 0.5 standard deviations.

*Thresholds for cell colours for GDP and the GDP tracker are 5-year average +/- 0.5 standard deviations, and for arrows are 6-quarter average +/- 0.5 standard deviations. Vietnam’s GDP growth tracker is YTD, as reported. We show Q2 GDP growth data here, as

it is already available.

^The Exports Broadness Index by destination indicates how ‘broad’ or ‘narrow’ exports are by destination of exports. If a few destinations account for a large share of exports, it is ‘narrow’. If exports are well diversified by destination, it is ‘broad’. ‘Broad’ is indicated

by a green cell and ‘Narrow’ by a red cell. The more diversified the exports, the better. Arrows indicate near term-performance versus the 6mma – for example, if exports are currently broad but getting narrower, this is indicated by a ↓ in a green cell. If exports are

currently narrow (highly concentrated on a few destinations) but getting broader, this is indicated by a ↑ in a red cell.

#The Monetary Conditions Index (MCI) indicates the ‘tightness’ or ‘looseness’ of monetary conditions. ‘Tighter’ is growth-negative, ‘looser’ is growth-positive. An upward arrow (↑) indicates loosening, and a downward arrow (↓) indicates tightening.

All indicators use the most recent publicly available data at the time of publication.

Source: Bloomberg, CEIC, Standard Chartered Research

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 9

Glo

ba

l

ov

erv

iew

Geopolitic

al

econom

ics

Asia

ME

NA

P

Afric

a

Euro

pe

Am

eric

as

Stra

tegy

outlo

ok

Fo

recasts

and

refe

rences

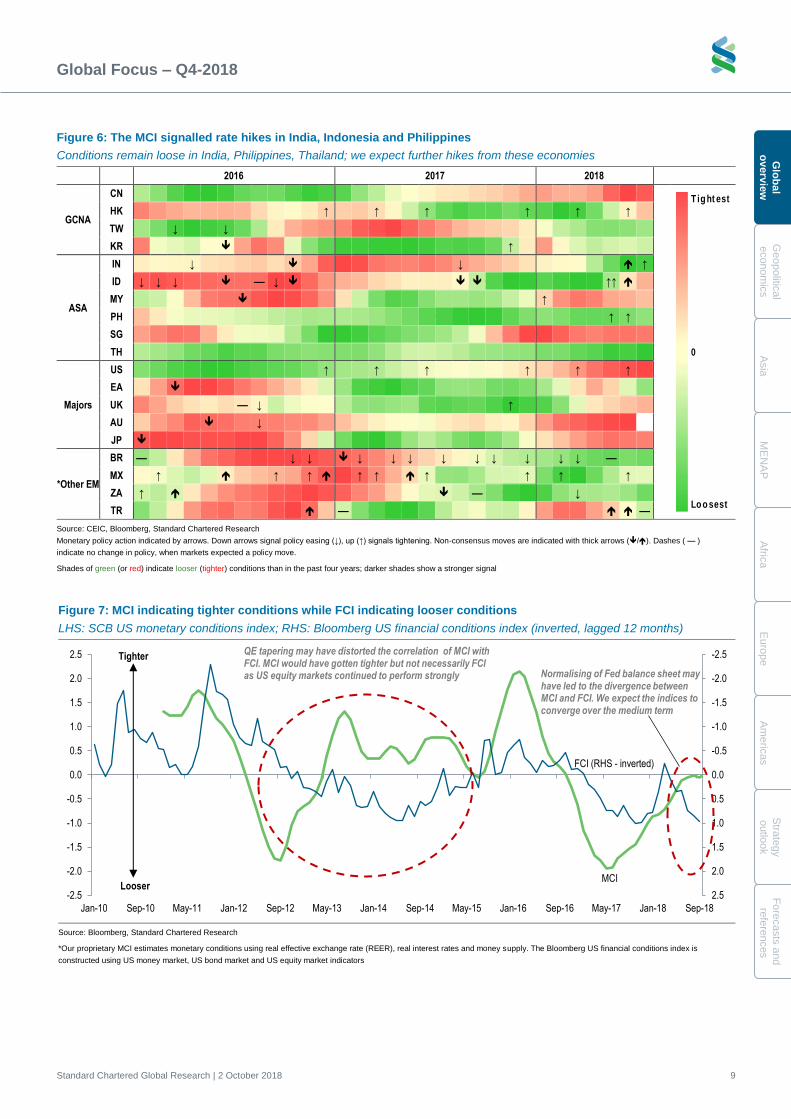

Figure 6: The MCI signalled rate hikes in India, Indonesia and Philippines

Conditions remain loose in India, Philippines, Thailand; we expect further hikes from these economies

2016 2017 2018

GCNA

CN

HK ↑

↑

↑

↑

↑

↑

TW ↓

↓

KR

↑

ASA

IN ↓

↓

↑

ID ↓ ↓ ↓

— ↓

↑↑

MY

↑

PH ↑ ↑

SG

TH

Majors

US ↑

↑

↑

↑

↑

↑

EA

UK — ↓

↑

AU

↓

JP

*Other EM

BR —

↓ ↓

↓

↓ ↓

↓

↓ ↓

↓

↓ ↓

—

MX ↑

↑

↑

↑ ↑

↑

↑

↑

↑

ZA ↑

—

↓

TR

—

—

Source: CEIC, Bloomberg, Standard Chartered Research

Monetary policy action indicated by arrows. Down arrows signal policy easing (↓), up (↑) signals tightening. Non-consensus moves are indicated with thick arrows (/). Dashes ( — )

indicate no change in policy, when markets expected a policy move.

Shades of green (or red) indicate looser (tighter) conditions than in the past four years; darker shades show a stronger signal

Figure 7: MCI indicating tighter conditions while FCI indicating looser conditions

LHS: SCB US monetary conditions index; RHS: Bloomberg US financial conditions index (inverted, lagged 12 months)

Source: Bloomberg, Standard Chartered Research

*Our proprietary MCI estimates monetary conditions using real effective exchange rate (REER), real interest rates and money supply. The Bloomberg US financial conditions index is

constructed using US money market, US bond market and US equity market indicators

T ig ht est

0

Lo o sest

MCI

FCI (RHS - inverted)

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

Jan-10 Sep-10 May-11 Jan-12 Sep-12 May-13 Jan-14 Sep-14 May-15 Jan-16 Sep-16 May-17 Jan-18 Sep-18

QE tapering may have distorted the correlation of MCI with FCI. MCI would have gotten tighter but not necessarily FCI as US equity markets continued to perform strongly Normalising of Fed balance sheet may

have led to the divergence between MCI and FCI. We expect the indices to converge over the medium term

Tighter

Looser

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 10

G

lob

al

o

verv

iew

Geopolit

ical

econom

ics

A

sia

M

EN

AP

A

fric

a

E

uro

pe

A

me

ricas

S

trate

gy

o

utlo

ok

Fo

recasts

and

re

fere

nces

Global overview – Beneath the surface

Global growth remains robust... for now

Our 2018 global growth forecast of 3.9% is unchanged since the start of the year,

despite mostly negative news flow. We expect the same robust pace to be

maintained in 2019. Downgrades to our growth forecasts in Africa and Latin America

have been countered by our upgraded US forecasts, which are premised on the

‘sugar rush’ from fiscal stimulus. The euro-area economy is on track to keep growing

above trend (2.0% in 2018). We expect China’s policy response to help its economy

weather the US-China trade war, growing 6.6% in 2018 and 6.4% in 2019. But while

global growth and trade have been resilient so far, negative tail risks to our forecasts

have increased since the start of 2018 – when we were already cautioning to

‘Beware of the Dog’. A number of risks are bubbling beneath the surface.

Global growth resilience so far contrasts with a steady flow of negative news for

longer-term growth: the escalating US-China trade war; a break higher in oil prices;

and mounting external pressure on emerging markets with twin deficits, which has

forced more aggressive monetary tightening in these economies. The end of the QE

era is also part of the story this year, but trends in the USD and US monetary policy

are just as important for emerging markets with twin (fiscal and current

account) deficits.

Given the stronger cyclical performance of the US economy, we recently raised our

forecast for the terminal federal funds target rate (FFTR) to 3.5% at end-2019 (from

3.0%). We expect this to be reached at the current gradual pace of +25bps per

quarter. US labour-market tightness has reached a point where it should start leading

to higher wage pressure and inflation, bolstered by fiscal stimulus. But even as

FOMC policy rate expectations have moved higher, US financial conditions (shown in

Figure 1) have loosened – in contrast with tightening elsewhere, notably EM Asia.

This makes us more comfortable with the view that the FOMC will continue to tighten.

Meanwhile, emerging economies have had to tighten monetary policy to counter

external market pressure from a stronger USD and widening rate spreads versus the

US. This poses longer-term risks to their growth outlook.

Figure 1: Financial conditions loosen in the US but tighten in AXJ

Bloomberg financial conditions index

Source: Bloomberg, Standard Chartered Research

US

EA

AXJ

-4

-3

-2

-1

0

1

2

Jan-12 Feb-13 Mar-14 Apr-15 May-16 Jun-17 Jul-18

In the US, a tight labour market and

positive output gap should allow

the Fed to keep hiking throughout

2019

Global growth is still solid, despite

bad news on global trade, oil prices

and US policy rates

David Mann +65 6596 8649

Global Chief Economist

Standard Chartered Bank, Singapore Branch

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 11

Glo

ba

l

ov

erv

iew

Geopolitic

al

econom

ics

Asia

ME

NA

P

Afric

a

Euro

pe

Am

eric

as

Stra

tegy

outlo

ok

Fo

recasts

and

refe

rences

China – A pause in the deleveraging push

At the start of 2018, we saw China’s deleveraging agenda as the main driver of

weaker sentiment among domestic investors. We are now less concerned about a

slowdown in China’s growth as the authorities scale back the pace of deleveraging

and the policy mix shifts towards fiscal policy as a growth stabiliser.

The recent Politburo meeting pledged more proactive fiscal policy via tax cuts and

infrastructure spending to boost domestic demand, along with a measured pace of

deleveraging. We now see room for fiscal policy to play a much bigger role without a

revision of the 2018 budget. According to our calculation, if the budget is fully

implemented, the fiscal deficit will be 0.9% of GDP (or CNY 1.1tn) higher than last

year (see China – Growth likely to beat target with fiscal expansion).

While the People’s Bank of China (PBoC) has removed its tightening bias, we see

limited room to loosen monetary policy further. The PBoC has already provided

ample liquidity to the interbank market via reserve requirement ratio (RRR) cuts and

the medium-term lending facility. Recent remarks by PBoC officials suggest a

preference for total social financing to grow at a similar pace to nominal GDP. The

challenge, however, is to unclog the transmission mechanism in order to channel

financing to the real economy. We maintain our call that the PBoC will lower the RRR

by another 2.5ppt in total before end-2019 to prevent a tightening of the

monetary stance.

Our confidence that China’s growth will remain robust throughout 2018-19 reflects

how important the growth target currently is for policy makers. Once the 2020 target

of doubling real GDP versus 2010 levels has been achieved, there may be less

emphasis on this target and more on broader social goals such as environmental

protection and tackling systemic risks from prior leverage excesses. Given that China

is the top trading partner for most EM economies in Asia and accounts for more than

30% of global growth (using PPP exchange rates), this makes us less optimistic on

longer-term growth.

Figure 2: US growth has been the biggest positive

surprise since the start of 2018

Revisions to growth forecasts since end-2017, ppt

Figure 3: US unemployment rate has fallen below NAIRU,

but participation rate remains low

Source: Bloomberg, Standard Chartered Research Source: Bloomberg, Standard Chartered Research

Consensus

-0.4

-0.2

0

0.2

0.4

0.6

0.8

US CN EU IN ID US CN IN EU ID

2018F 2019F

Our forecast

U3 unemployment

rate

NAIRU

Participation rate (RHS)

62

63

64

65

66

67

0

2

4

6

8

10

12

Sep-02 Sep-06 Sep-10 Sep-14 Sep-18

China’s monetary policy is likely to

remain neutral

We have long expected China’s

growth to slow in the 2020s

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 12

G

lob

al

o

verv

iew

Geopolit

ical

econom

ics

A

sia

M

EN

AP

A

fric

a

E

uro

pe

A

me

ricas

S

trate

gy

o

utlo

ok

Fo

recasts

and

re

fere

nces

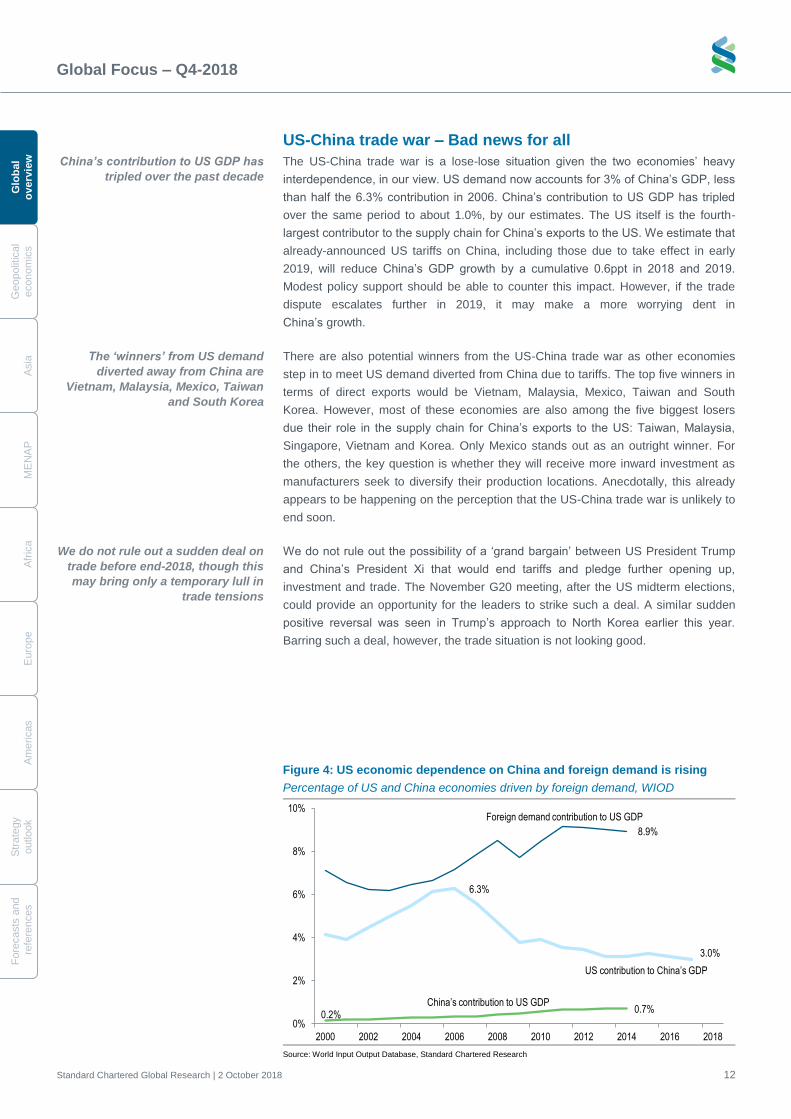

US-China trade war – Bad news for all

The US-China trade war is a lose-lose situation given the two economies’ heavy

interdependence, in our view. US demand now accounts for 3% of China’s GDP, less

than half the 6.3% contribution in 2006. China’s contribution to US GDP has tripled

over the same period to about 1.0%, by our estimates. The US itself is the fourth-

largest contributor to the supply chain for China’s exports to the US. We estimate that

already-announced US tariffs on China, including those due to take effect in early

2019, will reduce China’s GDP growth by a cumulative 0.6ppt in 2018 and 2019.

Modest policy support should be able to counter this impact. However, if the trade

dispute escalates further in 2019, it may make a more worrying dent in

China’s growth.

There are also potential winners from the US-China trade war as other economies

step in to meet US demand diverted from China due to tariffs. The top five winners in

terms of direct exports would be Vietnam, Malaysia, Mexico, Taiwan and South

Korea. However, most of these economies are also among the five biggest losers

due their role in the supply chain for China’s exports to the US: Taiwan, Malaysia,

Singapore, Vietnam and Korea. Only Mexico stands out as an outright winner. For

the others, the key question is whether they will receive more inward investment as

manufacturers seek to diversify their production locations. Anecdotally, this already

appears to be happening on the perception that the US-China trade war is unlikely to

end soon.

We do not rule out the possibility of a ‘grand bargain’ between US President Trump

and China’s President Xi that would end tariffs and pledge further opening up,

investment and trade. The November G20 meeting, after the US midterm elections,

could provide an opportunity for the leaders to strike such a deal. A similar sudden

positive reversal was seen in Trump’s approach to North Korea earlier this year.

Barring such a deal, however, the trade situation is not looking good.

Figure 4: US economic dependence on China and foreign demand is rising

Percentage of US and China economies driven by foreign demand, WIOD

Source: World Input Output Database, Standard Chartered Research

6.3%

3.0%

0.2%0.7%

8.9%

0%

2%

4%

6%

8%

10%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

US contribution to China’s GDP

Foreign demand contribution to US GDP

China’s contribution to US GDP

China’s contribution to US GDP has

tripled over the past decade

The ‘winners’ from US demand

diverted away from China are

Vietnam, Malaysia, Mexico, Taiwan

and South Korea

We do not rule out a sudden deal on

trade before end-2018, though this

may bring only a temporary lull in

trade tensions

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 13

Glo

ba

l

ov

erv

iew

Geopolitic

al

econom

ics

Asia

ME

NA

P

Afric

a

Euro

pe

Am

eric

as

Stra

tegy

outlo

ok

Fo

recasts

and

refe

rences

Risk of an oil price shock

Sustainable spare capacity declines

Our Commodities Research team recently revised up its oil price forecasts to reflect

expectations of a decline in sustainable spare capacity by end-2018 (see Oil Notes –

This house is haunted; raising forecasts). This is partly due to the decline in supply

from Iran and Venezuela. We still see a risk that prices may overshoot the new

forecasts. We see upside risks to our average Brent price forecasts – USD 82/barrel

(bbl) for Q4-2018 and USD 78/bbl for 2019 – from the likely reduction in Iran’s

exports, other geopolitical issues, and our forecast slowdown in US supply growth.

Risks to growth beyond 2019

We see several risks that could emerge by 2019, slowing global growth.

1. Oil prices could rally beyond our expectations if supply tightens and demand

holds up better than expected. The negative growth impact would take about a

year to affect growth, according to our estimates (see Quantifying the impact of

an oil shock, 12 June 2018).

2. By 2020, China’s policy makers may feel less pressure to keep GDP growth at

today’s levels. The authorities have often repeated their commitment to double

GDP by 2020 versus the 2010 level. If this is achieved ahead of schedule, other

priorities – including tackling systemic debt-related risks or other qualitative

objectives – may be prioritised over growth, leading to a sharper slowdown than

we currently expect. Our current long-term assumption is that China’s growth will

slow to an average 5.5% in the 2020s.

3. We expect the growth boost from US fiscal stimulus to fade by 2020. This is

already reflected in our forecasts, which see US growth slowing to 1.9% in 2020.

The US-China trade war, which could potentially raise the cost of all imports

from China, poses a downside risk to growth in 2020 and beyond.

Figure 5: Reduction in spare capacity implies upside oil price risks

OPEC spare capacity, % of global demand (LHS); Brent price, USD (RHS)

Source: EIA, Standard Chartered Research

OPEC spare capacity, LHS, % of

global demand

Brent price, USDbbl, RHS

0

20

40

60

80

100

120

140

160

0.0

1.0

2.0

3.0

4.0

5.0

6.0

03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

OPEC cuts output after start of GFC

Start of OPEC/non-OPEC production deal

Our Commodities Research team

sees upside risks to oil prices due

to tightening sustainable spare

capacity and doubts about 2019 US

supply growth

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 14

G

lob

al

o

verv

iew

Geopolit

ical

econom

ics

A

sia

M

EN

AP

A

fric

a

E

uro

pe

A

me

ricas

S

trate

gy

o

utlo

ok

Fo

recasts

and

re

fere

nces

Where we differ from consensus and why

US – We expect 25bps FOMC hikes every quarter through end-2019

We see one more FOMC hike in 2018 (in December) and four in 2019, versus the

consensus call of three more hikes between now and end-2019. The strong US

labour market and the positive output gap support this call. We believe the Phillips

curve framework (the reverse relationship between unemployment and inflation/wage

growth) still features prominently in the FOMC’s assessment of the economy, and the

consensus view on the committee is that the Phillips curve has flattened compared to

previous cycles. But a ‘kink’ – an acceleration in wage growth below a certain

unemployment level – is possible. The FOMC is likely to want to avoid this for

financial stability reasons, as it would necessitate a more forceful policy response to

contain inflation expectations. A gradual but steady pace of tightening in 2019 should

help to accomplish that aim.

China – We expect the current account to turn to a deficit in 2019

We forecast a faster deterioration in China’s current account (C/A) balance than

consensus. China reported a C/A deficit of USD 28.3bn in H1-2018, the first half-year

deficit in 18 years. The US-China trade dispute is putting the export sector under

pressure. We estimate that additional US tariffs announced so far on China-made

goods will cause China’s exports to the US (currently c.USD 520bn per year) to fall

by 10% over the next 12 months. In contrast, China’s import growth is supported by

high oil prices, reduced import tariffs on consumer goods, and policies aimed at

boosting domestic demand. As a result, we expect the C/A surplus to turn to a deficit

of 0.2% of GDP in 2019 from a surplus of 0.5% in 2018.

We see substantial room for expansionary fiscal policy this year, without requiring a

revision of the budget. We calculate a broad budget deficit of 4.6% of GDP in 2018,

higher than the actual deficit of 3.7% in 2017. (Our deficit calculations, which are based

on international standards, combine the general public budget and the government

funds budget; we think this more accurately reflects the fiscal stance than the official

budget numbers.) In other words, if the 2018 budget is fully implemented, we think the

actual deficit will be 0.9% of GDP higher than in 2017. This is equivalent to fiscal

stimulus of CNY 1.1tn. We believe the authorities are under pressure to utilise this fiscal

headroom via tax cuts and accelerated infrastructure spending. As a result, we think

the 2018 GDP growth target of 6.5% is likely to be exceeded. (Based on China’s fiscal

track record, we assume that the budget will be mostly implemented and forecast an

actual deficit of 4.2% of GDP for 2018.)

Korea – Consensus underestimates Bank of Korea’s hawkish stance

We expect the Bank of Korea (BoK) to tighten policy in November and again in 2019.

For now, the market is only focused on this year’s expected hike, with not much

expected for next year. Some market participants believe that the BoK may not be

able hike at all, since key economic indicators peaked in Q2-2018. We think this view

underestimates the BoK’s hawkish stance and is based too narrowly on weak job-

market data and low inflation. Inequality and financial stability also need to be taken

into account when assessing the BoK’s policy stance, in our view. Apartment prices

in the Seoul area have risen rapidly this year, increasing wealth inequality. The ruling

party has attributed this to low interest rates and abundant liquidity. It appears to

believe that macro-prudential policies in the mortgage market would merely divert

flows into other assets, and that liquidity therefore needs to be controlled. This is

likely to put pressure on the BoK to tighten policy. The central bank will also want to

reduce the risk of sudden capital outflows triggered by US rate hikes in order to

preserve financial stability. We expect these considerations to override concerns

about the slowing economy.

We expect two more 25bps FOMC

hikes than consensus by end-2019

China’s current account is likely to

turn to a mild deficit in 2019

Fiscal policy may provide important

support to China’s growth

We do not think the peak in Korea’s

economic indicators in mid-2018

means the end of the BoK hiking

cycle

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 15

Glo

ba

l

ov

erv

iew

Geopolitic

al

econom

ics

Asia

ME

NA

P

Afric

a

Euro

pe

Am

eric

as

Stra

tegy

outlo

ok

Fo

recasts

and

refe

rences

Indonesia – BI likely to hike more in response to widening C/A deficit

We expect the C/A deficit to surprise the market to the upside. We forecast that the

2018 deficit will widen to 3.0% of GDP, versus the consensus forecast of 2.7%.

Unfavourable commodity price movements (higher crude oil and lower palm oil

prices) are likely to weigh on the commodity trade balance. The oil and gas trade

deficit widened to USD 1.6bn in August, the highest monthly figure since 2014.

Government measures to boost the trade balance may not be implemented

immediately or have a significant short-term impact, in our view. Plans to delay

infrastructure projects, for instance, are unlikely to affect projects that are already

underway. The effectiveness of some fiscal measures – such as the higher biofuel

requirement and import taxes on selected consumer goods – will depend on the

readiness of domestic industry to substitute for imports. We believe that Bank

Indonesia (BI) will have to respond to pressure on the exchange rate with higher

interest rates – particularly with the Fed now expected to hike throughout 2019. We

now forecast 25bps rate hikes every quarter from Q4-2018 through Q2-2019.

Egypt – CBE likely to delay easing

Markets are converging with our non-consensus view that the Central Bank of Egypt

(CBE) is unlikely to respond to slowing inflation with rate cuts in 2018. Although the

CBE’s CPI inflation target for Q4-2018 (13% +/- 3ppt) remains within reach, Egypt

has seen capital outflows from its LCY government debt market amid broader EM

weakness. This is likely to be a concern for policy makers given the rise in yields and

implications for the balance of payments. As such, we expect the CBE to delay the

next 100bps cut to Q2-2019. While the CBE’s strong FX reserves have helped to

preserve Egyptian pound (EGP) stability so far, we do not rule out a reversal of

previous easing should capital outflows intensify.

Pakistan – We expect more tightening than consensus and markets

The State Bank of Pakistan (SBP) has delivered the 200bps of hikes we expected for

Q3-2018, surprising consensus expectations. However, we still think markets are

under-pricing monetary tightening ahead. We expect policy makers to agree to an

IMF programme in Q4-2018. Conditions for a potential programme are likely to

include further Pakistani rupee (PKR) depreciation to address external imbalances, in

our view. PKR adjustment amid higher oil prices is likely to pressure CPI inflation

higher. We expect the SBP to respond with another 150bps of hikes, taking the policy

rate to 10% by Q2-2019.

Chile – We think economic activity has already peaked

Economic activity data picked up strongly in H1-2018, causing the consensus growth

forecast for the year to rise. Meanwhile, Banco Central de Chile (BCCh) has recently

turned hawkish as the output gap has closed faster than expected; this has led the

market to expect the start of a tightening cycle in late 2018. We are more downbeat

on the pace of economic recovery, as we see mounting headwinds. In our view, the

factors that cushioned Chile’s growth against the decline in copper prices in H1-2018

are likely to fade in the next few months: loose monetary policy, a favourable base

effect and an election-driven boost to business confidence. We expect Chile to return

to a lacklustre growth trend, in line with increasing slack in the labour market, which

has driven down wage inflation despite high headline GDP figures. Chile is

vulnerable to the current global combination of high oil prices and low metal prices.

Given increasing downside risks to growth, we think the central bank’s inflation

concerns are exaggerated.

Higher oil and lower palm oil prices

are likely to weigh on Indonesia’s

trade balance

The consensus is moving towards

our call for no monetary easing in

Egypt in 2018

We expect Pakistan’s policy rate to

rise to 10% by mid-2019

We expect Chile’s economy to

return to softer growth amid higher

oil and subdued metal prices

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 16

G

lob

al

o

verv

iew

Geopolit

ical

econom

ics

A

sia

M

EN

AP

A

fric

a

E

uro

pe

A

me

ricas

S

trate

gy

o

utlo

ok

Fo

recasts

and

re

fere

nces

Mexico – We see the monetary policy consensus as too hawkish

We are more dovish than the consensus on monetary policy expectations for Mexico.

We think the inflation uptick is driven by higher oil prices and Mexican peso (MXN)

depreciation, which are short-term factors. Underlying inflation measures have eased

consistently (although they remain above target). Still-elevated real rates provide further

support for the MXN. Base effects and fresh food inflation pressure may prevent a

sharp slowdown in inflation in the short term, but we expect it to significantly undershoot

consensus expectations from Q2-2019 onwards. This also implies that rate cuts will be

more aggressive than consensus expectations, in our view.

Colombia – We are turning bullish

We think the market is underestimating Colombia’s growth prospects. Robust

domestic demand drove H1-2018 growth, as reflected in strong activity in the

manufacturing, construction and financial sectors. Looking ahead, the lagged impact

of the recent monetary easing cycle should provide an additional boost to domestic

demand. At the same time, we think Colombia is better positioned than Andean

peers in the current risk-off global environment. Sustainably high oil prices should

mitigate the twin deficits, a key risk to the country. The new administration has

announced a technocratic staff and a pro-business reform agenda aimed at

encouraging productivity gains and accelerating potential GDP. The ruling coalition’s

ample majority in Congress should facilitate faster approval of tax and social security

reform proposals, allowing the government to address long-standing regulatory

hurdles to investment in key sectors such as natural gas.

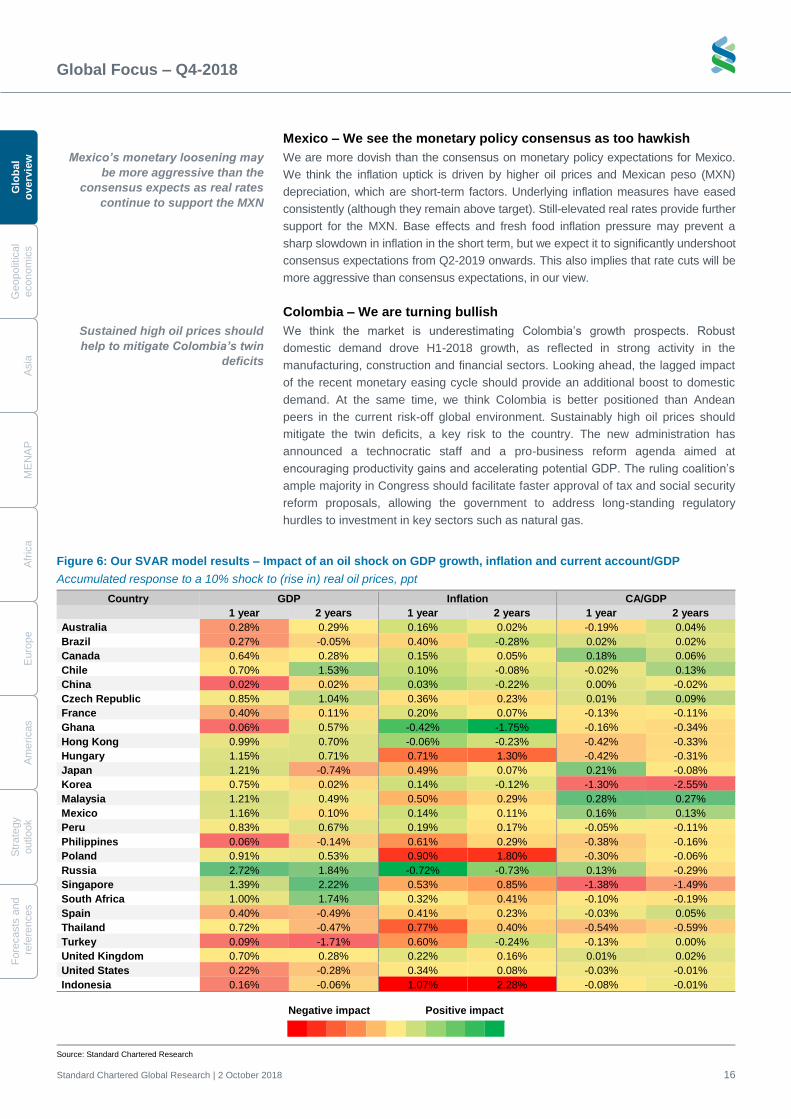

Figure 6: Our SVAR model results – Impact of an oil shock on GDP growth, inflation and current account/GDP

Accumulated response to a 10% shock to (rise in) real oil prices, ppt

Country GDP Inflation CA/GDP

1 year 2 years 1 year 2 years 1 year 2 years

Australia 0.28% 0.29% 0.16% 0.02% -0.19% 0.04%

Brazil 0.27% -0.05% 0.40% -0.28% 0.02% 0.02%

Canada 0.64% 0.28% 0.15% 0.05% 0.18% 0.06%

Chile 0.70% 1.53% 0.10% -0.08% -0.02% 0.13%

China 0.02% 0.02% 0.03% -0.22% 0.00% -0.02%

Czech Republic 0.85% 1.04% 0.36% 0.23% 0.01% 0.09%

France 0.40% 0.11% 0.20% 0.07% -0.13% -0.11%

Ghana 0.06% 0.57% -0.42% -1.75% -0.16% -0.34%

Hong Kong 0.99% 0.70% -0.06% -0.23% -0.42% -0.33%

Hungary 1.15% 0.71% 0.71% 1.30% -0.42% -0.31%

Japan 1.21% -0.74% 0.49% 0.07% 0.21% -0.08%

Korea 0.75% 0.02% 0.14% -0.12% -1.30% -2.55%

Malaysia 1.21% 0.49% 0.50% 0.29% 0.28% 0.27%

Mexico 1.16% 0.10% 0.14% 0.11% 0.16% 0.13%

Peru 0.83% 0.67% 0.19% 0.17% -0.05% -0.11%

Philippines 0.06% -0.14% 0.61% 0.29% -0.38% -0.16%

Poland 0.91% 0.53% 0.90% 1.80% -0.30% -0.06%

Russia 2.72% 1.84% -0.72% -0.73% 0.13% -0.29%

Singapore 1.39% 2.22% 0.53% 0.85% -1.38% -1.49%

South Africa 1.00% 1.74% 0.32% 0.41% -0.10% -0.19%

Spain 0.40% -0.49% 0.41% 0.23% -0.03% 0.05%

Thailand 0.72% -0.47% 0.77% 0.40% -0.54% -0.59%

Turkey 0.09% -1.71% 0.60% -0.24% -0.13% 0.00%

United Kingdom 0.70% 0.28% 0.22% 0.16% 0.01% 0.02%

United States 0.22% -0.28% 0.34% 0.08% -0.03% -0.01%

Indonesia 0.16% -0.06% 1.07% 2.28% -0.08% -0.01%

Negative impact

Positive impact

Source: Standard Chartered Research

Mexico’s monetary loosening may

be more aggressive than the

consensus expects as real rates

continue to support the MXN

Sustained high oil prices should

help to mitigate Colombia’s twin

deficits

Glo

bal F

oc

us

– Q

4-2

01

8

Sta

nd

ard

Charte

red

Glo

bal R

esea

rch | 2

Octo

ber 2

018

17

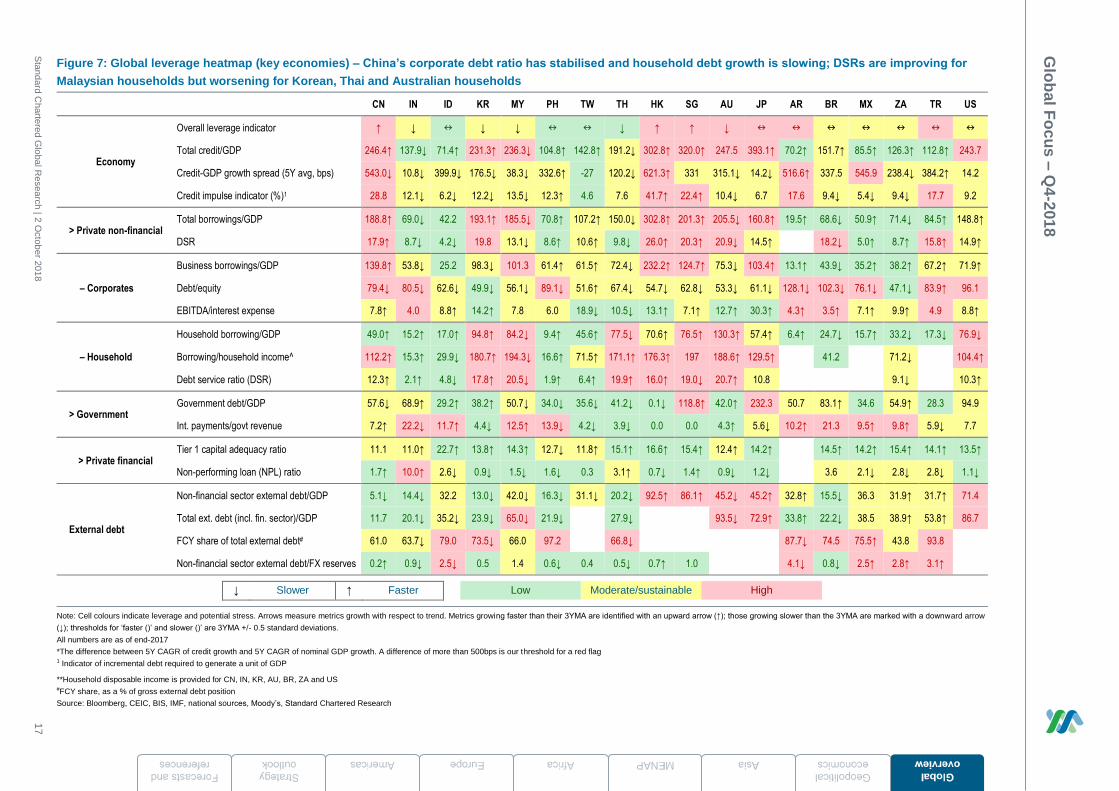

Figure 7: Global leverage heatmap (key economies) – China’s corporate debt ratio has stabilised and household debt growth is slowing; DSRs are improving for

Malaysian households but worsening for Korean, Thai and Australian households

CN IN ID KR MY PH TW TH HK SG AU JP AR BR MX ZA TR US

Economy

Overall leverage indicator ↑ ↓ ↓ ↓ ↓ ↑ ↑ ↓

Total credit/GDP 246.4↑ 137.9↓ 71.4↑ 231.3↑ 236.3↓ 104.8↑ 142.8↑ 191.2↓ 302.8↑ 320.0↑ 247.5 393.1↑ 70.2↑ 151.7↑ 85.5↑ 126.3↑ 112.8↑ 243.7

Credit-GDP growth spread (5Y avg, bps) 543.0↓ 10.8↓ 399.9↓ 176.5↓ 38.3↓ 332.6↑ -27 120.2↓ 621.3↑ 331 315.1↓ 14.2↓ 516.6↑ 337.5 545.9 238.4↓ 384.2↑ 14.2

Credit impulse indicator (%)1 28.8 12.1↓ 6.2↓ 12.2↓ 13.5↓ 12.3↑ 4.6 7.6 41.7↑ 22.4↑ 10.4↓ 6.7 17.6 9.4↓ 5.4↓ 9.4↓ 17.7 9.2

> Private non-financial Total borrowings/GDP 188.8↑ 69.0↓ 42.2 193.1↑ 185.5↓ 70.8↑ 107.2↑ 150.0↓ 302.8↑ 201.3↑ 205.5↓ 160.8↑ 19.5↑ 68.6↓ 50.9↑ 71.4↓ 84.5↑ 148.8↑

DSR 17.9↑ 8.7↓ 4.2↓ 19.8 13.1↓ 8.6↑ 10.6↑ 9.8↓ 26.0↑ 20.3↑ 20.9↓ 14.5↑ 18.2↓ 5.0↑ 8.7↑ 15.8↑ 14.9↑

– Corporates

Business borrowings/GDP 139.8↑ 53.8↓ 25.2 98.3↓ 101.3 61.4↑ 61.5↑ 72.4↓ 232.2↑ 124.7↑ 75.3↓ 103.4↑ 13.1↑ 43.9↓ 35.2↑ 38.2↑ 67.2↑ 71.9↑

Debt/equity 79.4↓ 80.5↓ 62.6↓ 49.9↓ 56.1↓ 89.1↓ 51.6↑ 67.4↓ 54.7↓ 62.8↓ 53.3↓ 61.1↓ 128.1↓ 102.3↓ 76.1↓ 47.1↓ 83.9↑ 96.1

EBITDA/interest expense 7.8↑ 4.0 8.8↑ 14.2↑ 7.8 6.0 18.9↓ 10.5↓ 13.1↑ 7.1↑ 12.7↑ 30.3↑ 4.3↑ 3.5↑ 7.1↑ 9.9↑ 4.9 8.8↑

– Household

Household borrowing/GDP 49.0↑ 15.2↑ 17.0↑ 94.8↑ 84.2↓ 9.4↑ 45.6↑ 77.5↓ 70.6↑ 76.5↑ 130.3↑ 57.4↑ 6.4↑ 24.7↓ 15.7↑ 33.2↓ 17.3↓ 76.9↓

Borrowing/household income^ 112.2↑ 15.3↑ 29.9↓ 180.7↑ 194.3↓ 16.6↑ 71.5↑ 171.1↑ 176.3↑ 197 188.6↑ 129.5↑ 41.2 71.2↓

104.4↑

Debt service ratio (DSR) 12.3↑ 2.1↑ 4.8↓ 17.8↑ 20.5↓ 1.9↑ 6.4↑ 19.9↑ 16.0↑ 19.0↓ 20.7↑ 10.8

9.1↓

10.3↑

> Government Government debt/GDP 57.6↓ 68.9↑ 29.2↑ 38.2↑ 50.7↓ 34.0↓ 35.6↓ 41.2↓ 0.1↓ 118.8↑ 42.0↑ 232.3 50.7 83.1↑ 34.6 54.9↑ 28.3 94.9

Int. payments/govt revenue 7.2↑ 22.2↓ 11.7↑ 4.4↓ 12.5↑ 13.9↓ 4.2↓ 3.9↓ 0.0 0.0 4.3↑ 5.6↓ 10.2↑ 21.3 9.5↑ 9.8↑ 5.9↓ 7.7

> Private financial Tier 1 capital adequacy ratio 11.1 11.0↑ 22.7↑ 13.8↑ 14.3↑ 12.7↓ 11.8↑ 15.1↑ 16.6↑ 15.4↑ 12.4↑ 14.2↑ 14.5↑ 14.2↑ 15.4↑ 14.1↑ 13.5↑

Non-performing loan (NPL) ratio 1.7↑ 10.0↑ 2.6↓ 0.9↓ 1.5↓ 1.6↓ 0.3 3.1↑ 0.7↓ 1.4↑ 0.9↓ 1.2↓ 3.6 2.1↓ 2.8↓ 2.8↓ 1.1↓

External debt

Non-financial sector external debt/GDP 5.1↓ 14.4↓ 32.2 13.0↓ 42.0↓ 16.3↓ 31.1↓ 20.2↓ 92.5↑ 86.1↑ 45.2↓ 45.2↑ 32.8↑ 15.5↓ 36.3 31.9↑ 31.7↑ 71.4

Total ext. debt (incl. fin. sector)/GDP 11.7 20.1↓ 35.2↓ 23.9↓ 65.0↓ 21.9↓

27.9↓

93.5↓ 72.9↑ 33.8↑ 22.2↓ 38.5 38.9↑ 53.8↑ 86.7

FCY share of total external debt# 61.0 63.7↓ 79.0 73.5↓ 66.0 97.2

66.8↓

87.7↓ 74.5 75.5↑ 43.8 93.8

Non-financial sector external debt/FX reserves 0.2↑ 0.9↓ 2.5↓ 0.5 1.4 0.6↓ 0.4 0.5↓ 0.7↑ 1.0

4.1↓ 0.8↓ 2.5↑ 2.8↑ 3.1↑

↓ Slower ↑ Faster

Low Moderate/sustainable High

Note: Cell colours indicate leverage and potential stress. Arrows measure metrics growth with respect to trend. Metrics growing faster than their 3YMA are identified with an upward arrow (↑); those growing slower than the 3YMA are marked with a downward arrow

(↓); thresholds for ‘faster ()’ and slower ()’ are 3YMA +/- 0.5 standard deviations.

All numbers are as of end-2017

*The difference between 5Y CAGR of credit growth and 5Y CAGR of nominal GDP growth. A difference of more than 500bps is our threshold for a red flag 1 Indicator of incremental debt required to generate a unit of GDP

**Household disposable income is provided for CN, IN, KR, AU, BR, ZA and US #FCY share, as a % of gross external debt position

Source: Bloomberg, CEIC, BIS, IMF, national sources, Moody’s, Standard Chartered Research

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 18

G

lob

al

o

verv

iew

Geopolit

ical

econom

ics

A

sia

M

EN

AP

A

fric

a

E

uro

pe

A

me

ricas

S

trate

gy

o

utlo

ok

Fo

recasts

and

re

fere

nces

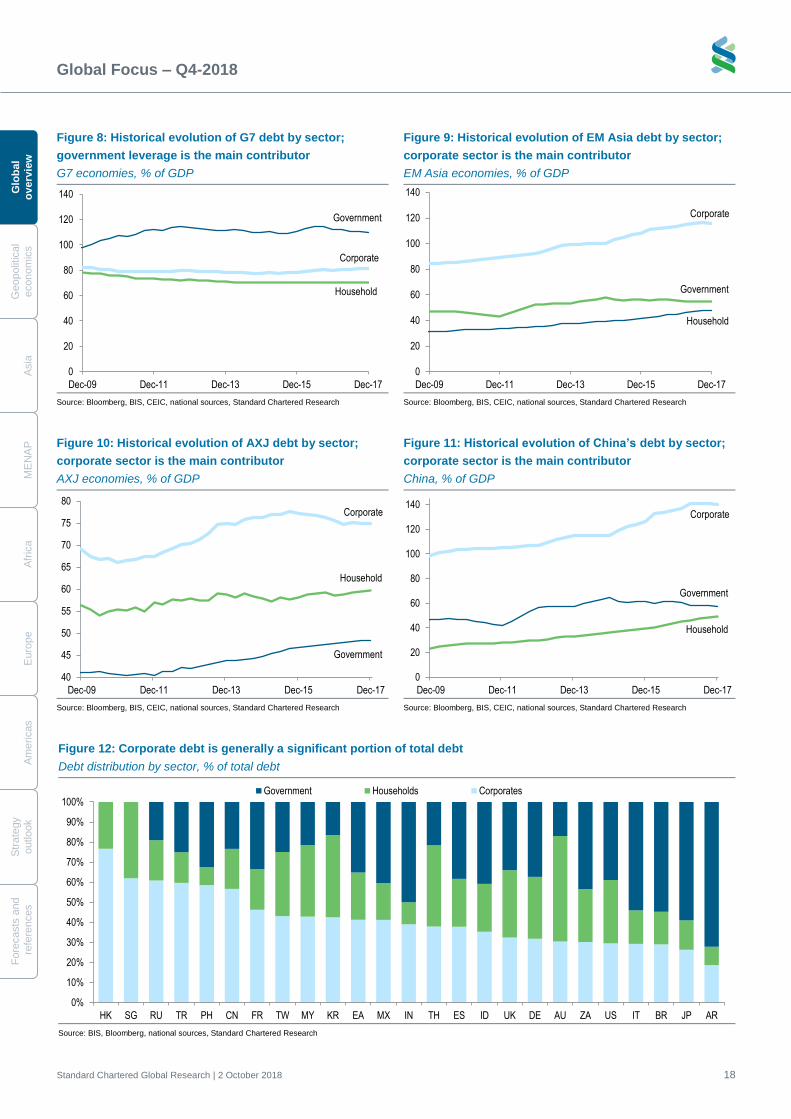

Figure 8: Historical evolution of G7 debt by sector;

government leverage is the main contributor

G7 economies, % of GDP

Figure 9: Historical evolution of EM Asia debt by sector;

corporate sector is the main contributor

EM Asia economies, % of GDP

Source: Bloomberg, BIS, CEIC, national sources, Standard Chartered Research Source: Bloomberg, BIS, CEIC, national sources, Standard Chartered Research

Figure 10: Historical evolution of AXJ debt by sector;

corporate sector is the main contributor

AXJ economies, % of GDP

Figure 11: Historical evolution of China’s debt by sector;

corporate sector is the main contributor

China, % of GDP

Source: Bloomberg, BIS, CEIC, national sources, Standard Chartered Research Source: Bloomberg, BIS, CEIC, national sources, Standard Chartered Research

Figure 12: Corporate debt is generally a significant portion of total debt

Debt distribution by sector, % of total debt

Source: BIS, Bloomberg, national sources, Standard Chartered Research

Corporate

Household

Government

0

20

40

60

80

100

120

140

Dec-09 Dec-11 Dec-13 Dec-15 Dec-17

Corporate

Government

Household

0

20

40

60

80

100

120

140

Dec-09 Dec-11 Dec-13 Dec-15 Dec-17

Corporate

Household

Government

40

45

50

55

60

65

70

75

80

Dec-09 Dec-11 Dec-13 Dec-15 Dec-17

Corporate

Household

Government

0

20

40

60

80

100

120

140

Dec-09 Dec-11 Dec-13 Dec-15 Dec-17

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

HK SG RU TR PH CN FR TW MY KR EA MX IN TH ES ID UK DE AU ZA US IT BR JP AR

Government Households Corporates

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 19

Glo

ba

l

ov

erv

iew

Geopolitic

al

econom

ics

Asia

ME

NA

P

Afric

a

Euro

pe

Am

eric

as

Stra

tegy

outlo

ok

Fo

recasts

and

refe

rences

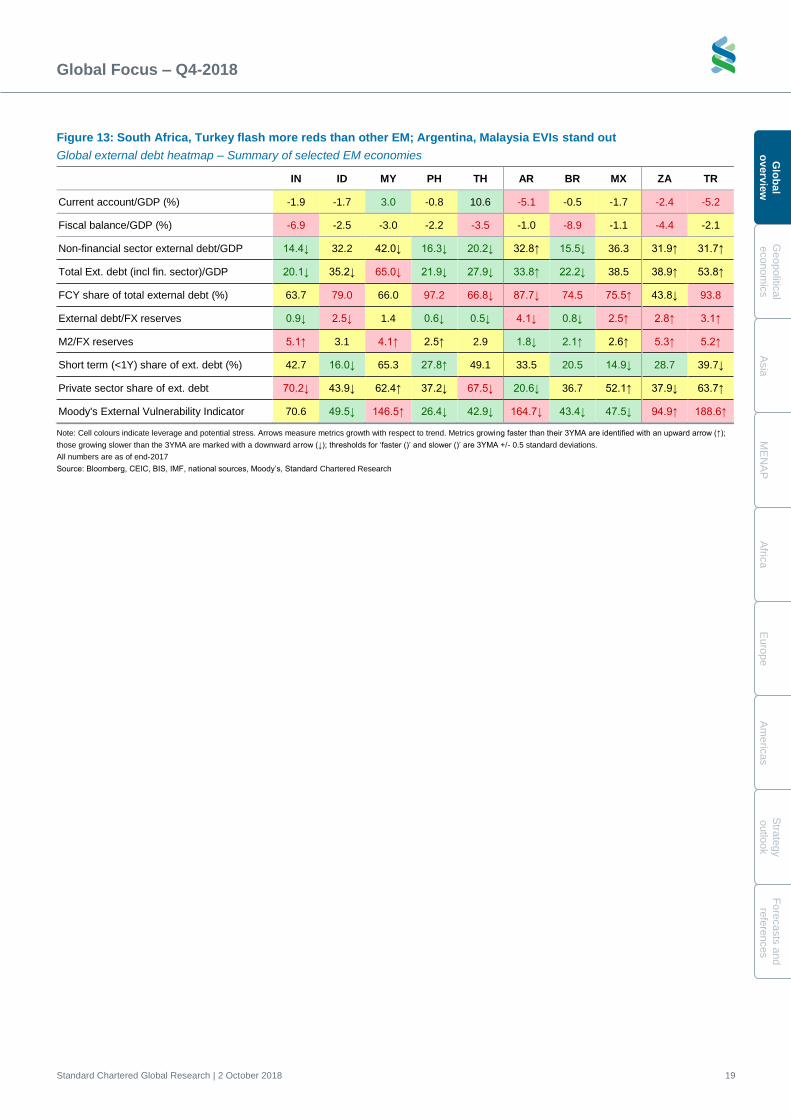

Figure 13: South Africa, Turkey flash more reds than other EM; Argentina, Malaysia EVIs stand out

Global external debt heatmap – Summary of selected EM economies

IN ID MY PH TH AR BR MX ZA TR

Current account/GDP (%) -1.9 -1.7 3.0 -0.8 10.6 -5.1 -0.5 -1.7 -2.4 -5.2

Fiscal balance/GDP (%) -6.9 -2.5 -3.0 -2.2 -3.5 -1.0 -8.9 -1.1 -4.4 -2.1

Non-financial sector external debt/GDP 14.4↓ 32.2 42.0↓ 16.3↓ 20.2↓ 32.8↑ 15.5↓ 36.3 31.9↑ 31.7↑

Total Ext. debt (incl fin. sector)/GDP 20.1↓ 35.2↓ 65.0↓ 21.9↓ 27.9↓ 33.8↑ 22.2↓ 38.5 38.9↑ 53.8↑

FCY share of total external debt (%) 63.7 79.0 66.0 97.2 66.8↓ 87.7↓ 74.5 75.5↑ 43.8↓ 93.8

External debt/FX reserves 0.9↓ 2.5↓ 1.4 0.6↓ 0.5↓ 4.1↓ 0.8↓ 2.5↑ 2.8↑ 3.1↑

M2/FX reserves 5.1↑ 3.1 4.1↑ 2.5↑ 2.9 1.8↓ 2.1↑ 2.6↑ 5.3↑ 5.2↑

Short term (<1Y) share of ext. debt (%) 42.7 16.0↓ 65.3 27.8↑ 49.1 33.5 20.5 14.9↓ 28.7 39.7↓

Private sector share of ext. debt 70.2↓ 43.9↓ 62.4↑ 37.2↓ 67.5↓ 20.6↓ 36.7 52.1↑ 37.9↓ 63.7↑

Moody's External Vulnerability Indicator 70.6 49.5↓ 146.5↑ 26.4↓ 42.9↓ 164.7↓ 43.4↓ 47.5↓ 94.9↑ 188.6↑

Note: Cell colours indicate leverage and potential stress. Arrows measure metrics growth with respect to trend. Metrics growing faster than their 3YMA are identified with an upward arrow (↑);

those growing slower than the 3YMA are marked with a downward arrow (↓); thresholds for ‘faster ()’ and slower ()’ are 3YMA +/- 0.5 standard deviations.

All numbers are as of end-2017

Source: Bloomberg, CEIC, BIS, IMF, national sources, Moody’s, Standard Chartered Research

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 20

G

lob

al

o

verv

iew

Geopolit

ical

econom

ics

A

sia

M

EN

AP

A

fric

a

E

uro

pe

A

me

ricas

S

trate

gy

o

utlo

ok

Fo

recasts

and

re

fere

nces

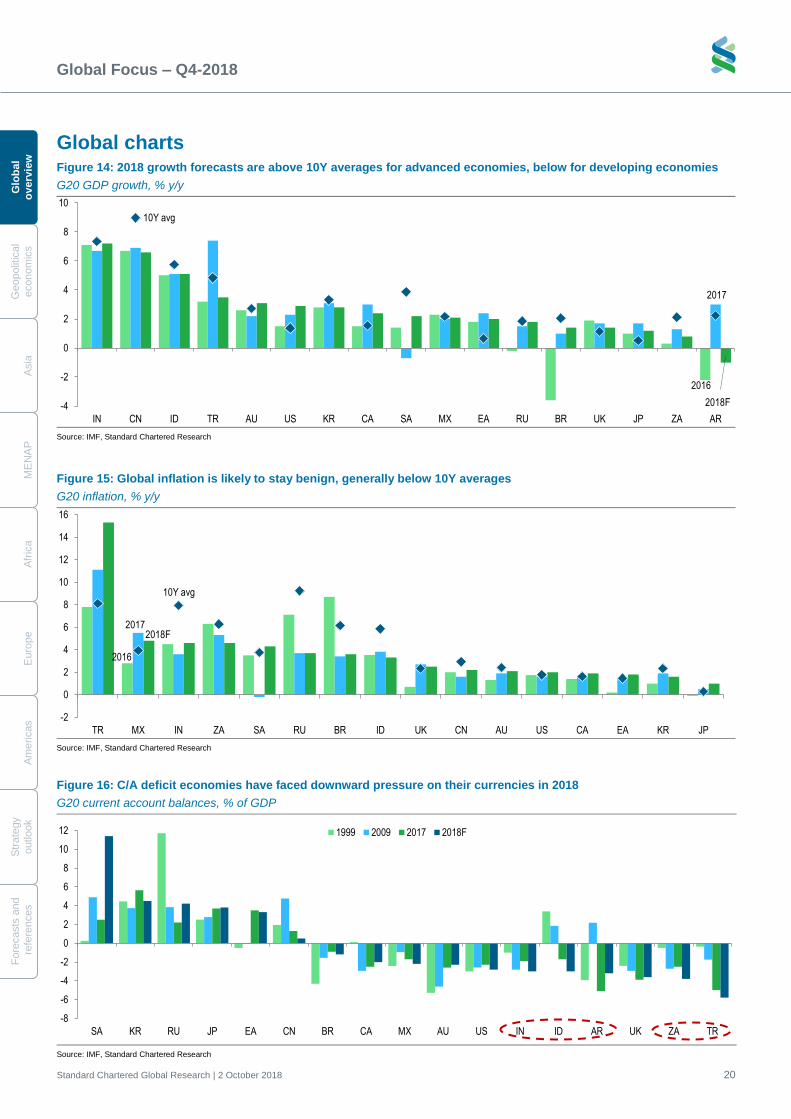

Global charts Figure 14: 2018 growth forecasts are above 10Y averages for advanced economies, below for developing economies

G20 GDP growth, % y/y

Source: IMF, Standard Chartered Research

Figure 15: Global inflation is likely to stay benign, generally below 10Y averages

G20 inflation, % y/y

Source: IMF, Standard Chartered Research

2016

2017

2018F

10Y avg

-4

-2

0

2

4

6

8

10

IN CN ID TR AU US KR CA SA MX EA RU BR UK JP ZA AR

2016

20172018F

10Y avg

-2

0

2

4

6

8

10

12

14

16

TR MX IN ZA SA RU BR ID UK CN AU US CA EA KR JP

Figure 16: C/A deficit economies have faced downward pressure on their currencies in 2018

G20 current account balances, % of GDP

Source: IMF, Standard Chartered Research

-8

-6

-4

-2

0

2

4

6

8

10

12

SA KR RU JP EA CN BR CA MX AU US IN ID AR UK ZA TR

1999 2009 2017 2018F

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 21

Glo

ba

l

ov

erv

iew

Geopolitic

al

econom

ics

Asia

ME

NA

P

Afric

a

Euro

pe

Am

eric

as

Stra

tegy

outlo

ok

Fo

recasts

and

refe

rences

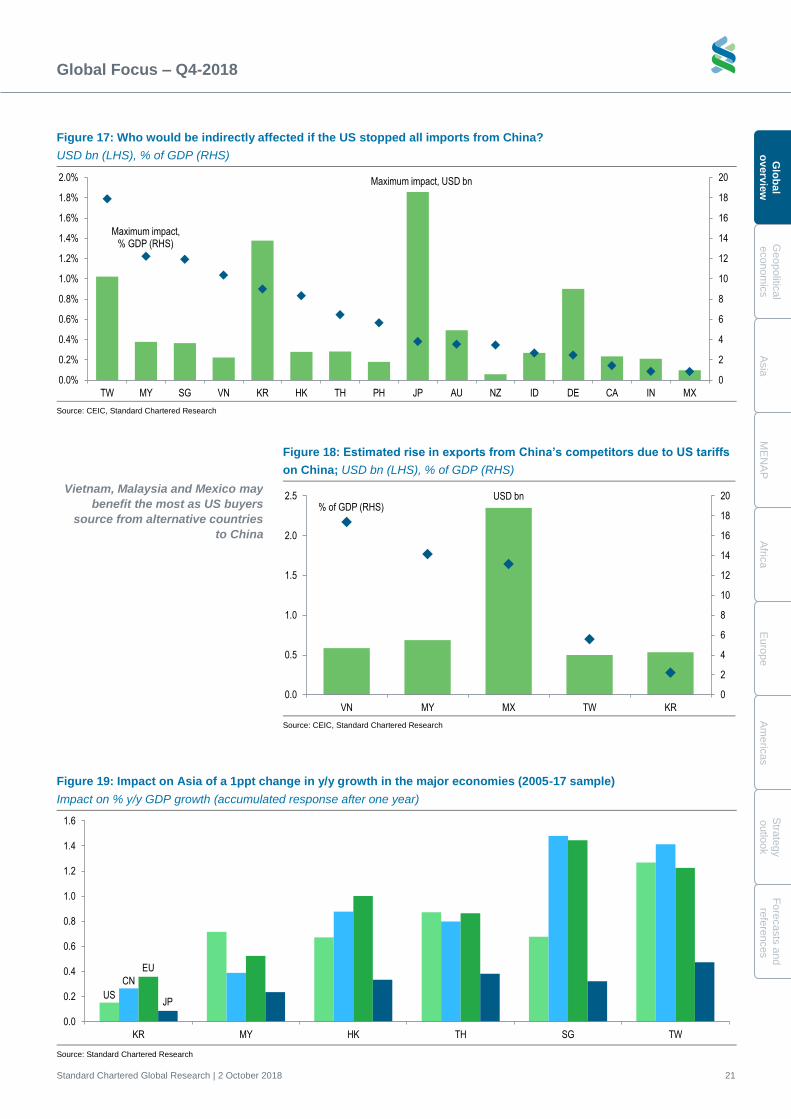

Figure 18: Estimated rise in exports from China’s competitors due to US tariffs

on China; USD bn (LHS), % of GDP (RHS)

Vietnam, Malaysia and Mexico may

benefit the most as US buyers

source from alternative countries

to China

Source: CEIC, Standard Chartered Research

USD bn% of GDP (RHS)

0

2

4

6

8

10

12

14

16

18

20

0.0

0.5

1.0

1.5

2.0

2.5

VN MY MX TW KR

Figure 17: Who would be indirectly affected if the US stopped all imports from China?

USD bn (LHS), % of GDP (RHS)

Source: CEIC, Standard Chartered Research

Figure 19: Impact on Asia of a 1ppt change in y/y growth in the major economies (2005-17 sample)

Impact on % y/y GDP growth (accumulated response after one year)

Source: Standard Chartered Research

Maximum impact, USD bn

Maximum impact, % GDP (RHS)

0

2

4

6

8

10

12

14

16

18

20

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

TW MY SG VN KR HK TH PH JP AU NZ ID DE CA IN MX

US

CN

EU

JP

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

KR MY HK TH SG TW

Geopolitical economics

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 23

Glo

bal

overv

iew

G

eo

po

litical

eco

no

mic

s

Asia

ME

NA

P

Afric

a

Euro

pe

Am

eric

as

Stra

tegy

outlo

ok

Fo

recasts

and

refe

rences

US midterms – A looming risk for Trump

Potential stakes – Impeachment, paralysis, trade policy

US voters will choose members of both houses of Congress (Senate and House of

Representatives) in the midterm elections on 6 November. The midterms are

increasingly being framed as a referendum on President Donald Trump and the

Republican majority in Congress.

Midterm elections, which are held two years into the four-year presidential term, are

often a concern for the sitting president. The president’s initial ‘grace period’ has

ended and his party typically loses seats. The stakes in the upcoming midterms may

be the highest in decades given the growing polarisation of the US electorate and the

turmoil surrounding Trump during his first two years in office. In an August interview,

Trump himself hinted at the possibility of impeachment should the Democrats win

control of the House – possibly a tactic to motivate Republican voter turnout. A key

determinant of the election outcome will indeed be turnout, which is generally weak

for midterms.

Even if the Democrats win the House – they are currently leading in polls – we think

the chances of Trump’s removal from office through impeachment are low. But the

stakes for Trump’s presidency are still high. Should the Democrats regain control of

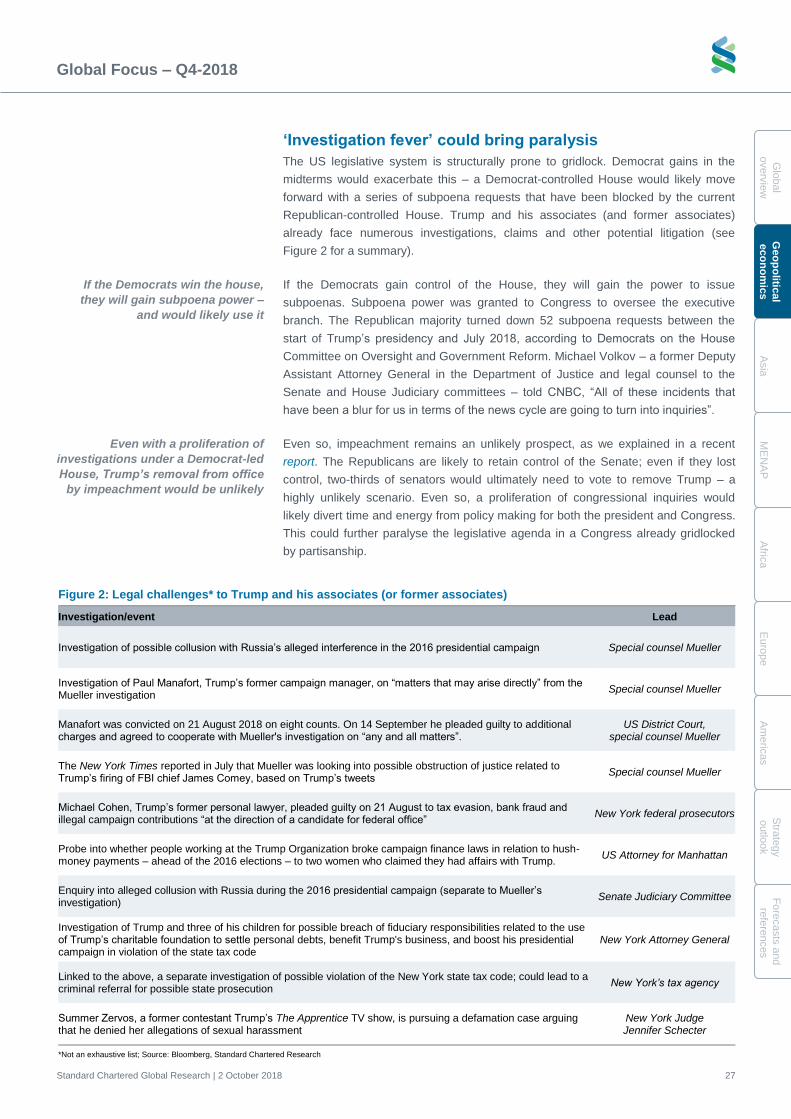

the House, we see two key outcomes: (1) Congress could open a series of

investigations into Trump and his associates, backed by the power to issue

subpoenas. This could consume the White House and its ability to efficiently conduct

policy; meanwhile, a split Congress would compound the traditional legislative

gridlock, potentially leading to further paralysis. (2) The president’s trade agenda

could be challenged – either directly through efforts by Congress to regain authority

over trade, or due to a changing cost/benefit analysis of trade wars.

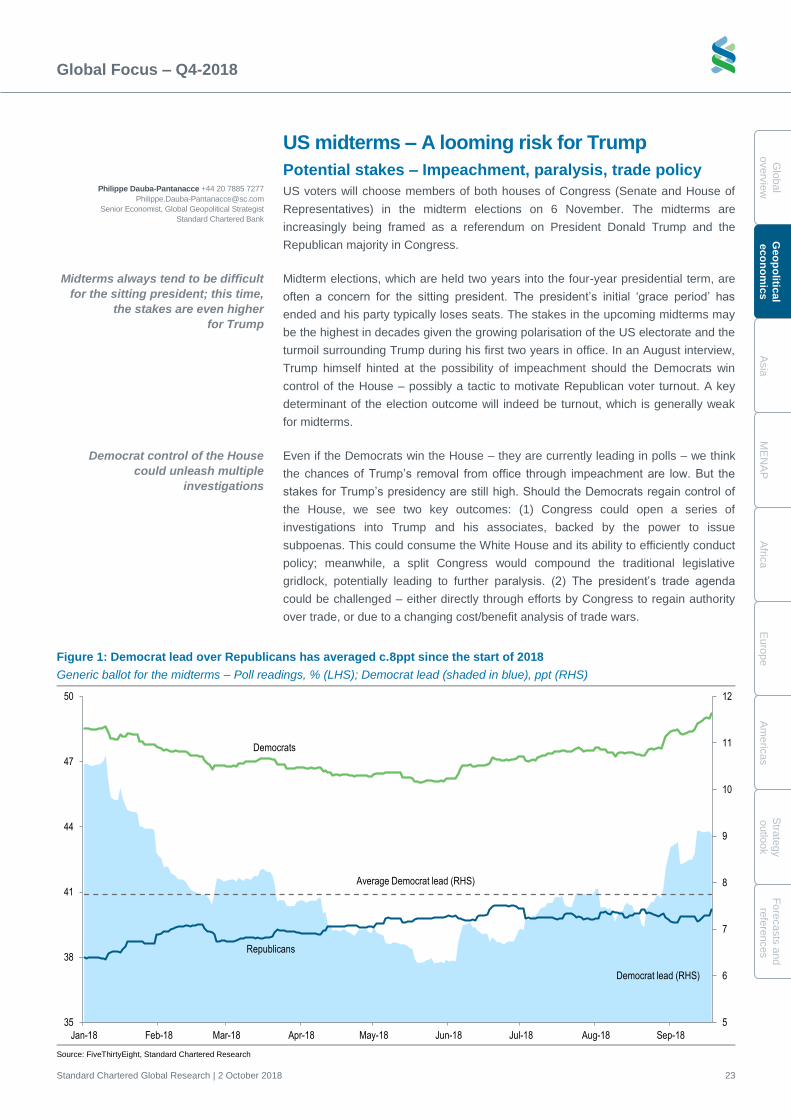

Figure 1: Democrat lead over Republicans has averaged c.8ppt since the start of 2018

Generic ballot for the midterms – Poll readings, % (LHS); Democrat lead (shaded in blue), ppt (RHS)

Source: FiveThirtyEight, Standard Chartered Research

Democrat lead (RHS)

Democrats

Republicans

Average Democrat lead (RHS)

5

6

7

8

9

10

11

12

35

38

41

44

47

50

Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18

Philippe Dauba-Pantanacce +44 20 7885 7277

Senior Economist, Global Geopolitical Strategist

Standard Chartered Bank

Midterms always tend to be difficult

for the sitting president; this time,

the stakes are even higher

for Trump

Democrat control of the House

could unleash multiple

investigations

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 24

G

lobal

overv

iew

Geo

po

liti

cal

eco

no

mic

s

A

sia

M

EN

AP

A

fric

a

E

uro

pe

A

me

ricas

S

trate

gy

o

utlo

ok

Fo

recasts

and

re

fere

nces

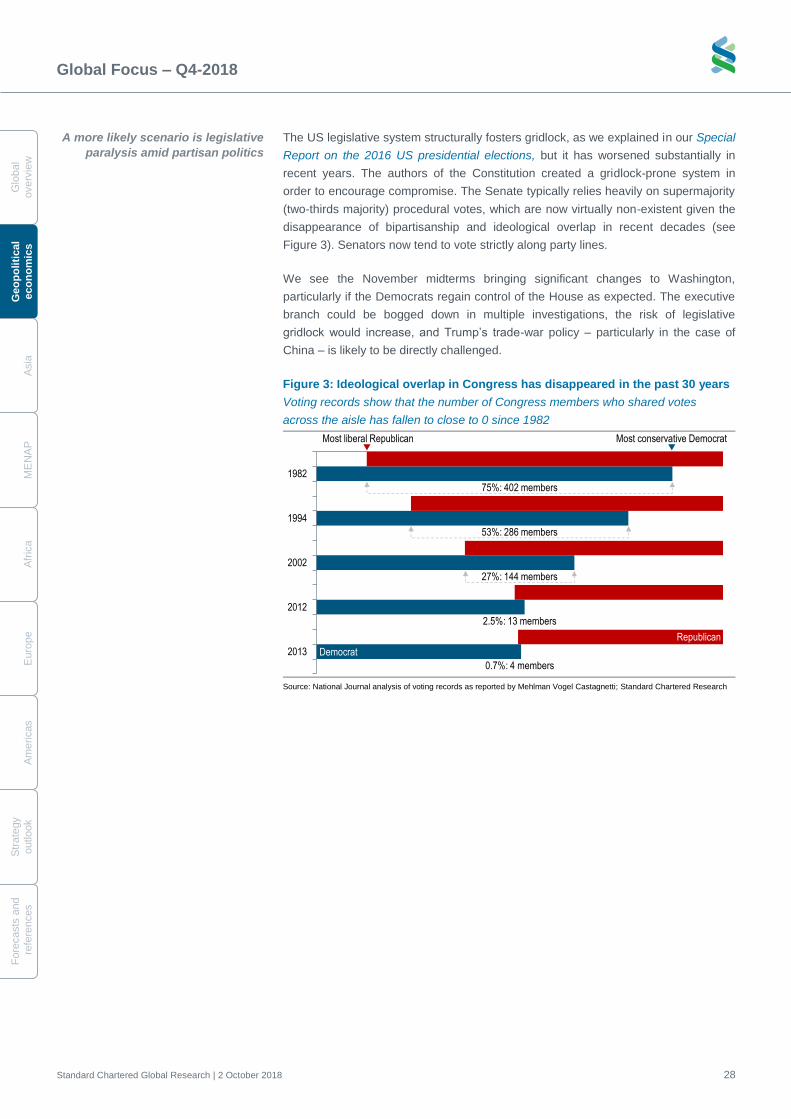

Midterms are never good for sitting presidents

The US midterms on 6 November will elect the full House of Representatives

(435 seats) and 34 of the Senate’s 100 seats.

The midterms are widely seen as a referendum on Trump and the Republican Party’s

majority in Congress. Republican voters’ support for Trump is consolidating. His approval

rating within the party has been hovering around 90%, and averaged 87% in September

(Gallup poll tracking). However, Republicans’ share of total voting intentions has eroded,

according to polls. Current polls suggest that the Democrats are likely to regain control

of the House, while the statistical odds favour the Republicans retaining control of

the Senate.

We think that turnout will be the decisive factor in these elections. The president’s party

typically loses seats in midterms, and this is likely to be the case in November; the

question is whether these losses will be enough for the Democrats to win control of either

chamber. The Democrats need to gain 24 seats to take the House (435 seats in total). In

the Senate (100 seats), of the 34 seats at stake, the Democrats are defending 26, while

the Republicans are defending eight; so the statistical risks are unfavourable for the

Democrats. Furthermore, of these 26 Democratic seats, 10 are in states that Trump won

in 2016, half of them by a wide margin.

The ‘generic ballot’ average of polls – which ask voters if they will vote for Democrats or

Republicans for Congress and is historically a good indicator of the House result – shows

an average Democrat lead of c.8ppt since the start of 2018 (Figure 1). As of 24

September, FiveThirtyEight, which specialises in analysing opinion polls, indicated 49.4%

for Democrats against 40.9% for Republicans.

In the current highly polarised political environment, turnout is likely to be a function of

how strongly Democrats seek to express their disapproval for Trump’s agenda, and

how strongly Republicans seek to express their approval. Which side can get more

supporters to polling stations on election day will be the key determinant of

the outcome.

US elections tend to have low turnout compared with other OECD countries. Just over

half (55%) of eligible voters cast ballots in the 2016 presidential election; on average,

turnout for midterms is about one-third lower than for presidential elections. The 2014

midterms had the lowest participation rate in 72 years, at 36%. A recent study by

FiveThirtyEight (‘Do Republicans Really Have a Big Turnout Advantage in Midterms?’)

showed that Republicans tend to have slightly higher turnout than Democrats in

midterms on average, although this advantage is less clear if the GOP already holds

the White House.

Could the midterms alter trade policy?

We think the midterms could weaken Trump’s trade agenda, regardless of who

controls Congress. There have already been some initiatives from within Congress –

including by Republican lawmakers – to restrain the president’s power on trade. We

think these efforts are likely to gain strength after the midterms. If Democrats take

control of the House, they might be able to push through legislation to curb Trump’s

trade powers. Meanwhile, Republican lawmakers who oppose Trump’s trade stance

are likely to be more emboldened to challenge it once the political exigencies of the

midterms are out of the way. This would increase the chances of a bipartisan effort to

rein in the Trump administration’s trade policies. We also think that as the economic

cost of trade wars increases, so will the political cost – incentivising lawmakers to

push for a change.

Polls have shown a consistent lead

for Democrats in the House since

the start of the year

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 25

Glo

bal

overv

iew

G

eo

po

litical

eco

no

mic

s

Asia

ME

NA

P

Afric

a

Euro

pe

Am

eric

as

Stra

tegy

outlo

ok

Fo

recasts

and

refe

rences

As part of his ‘America first’ approach, Trump has undermined the US’ most

important trade relationships and rejected the free-trade principles that have

traditionally been a cornerstone of Republican policy. Examples include imposing

tariffs on China and other trading partners; and withdrawing the US from the Trans-

Pacific Partnership (TPP), which was seen as a crucial element of US geopolitical

and commercial engagement with Asia.

While the president has the authority to negotiate international trade agreements,

Congress has sole constitutional authority over “the regulation of foreign commerce

and the imposition of tariffs”. In past decades, lawmakers have given presidents

special authority to negotiate trade deals within established parameters – notably in

the 1974 Trade Act. But the way this power is exercised by the president could be

challenged in courts, according to Jennifer Hillman, a Georgetown University law

professor and former WTO appellate judge.

Congressional pressure

Republicans have been at the forefront of initiatives to constrain Trump’s authority on

trade. The failure of these initiatives to gain traction may be partly explained by politics

– confronting Trump ahead of the midterms could anger his support base. This may

change after the midterms, given the conviction among many Republican lawmakers

that the party should continue to stand for free trade and that the president’s powers in

this sphere should be checked. In a recent media interview with Foreign Policy

magazine, Gary Hufbauer of the Peterson Institute for International Economics said, “I

think we’re getting closer to where Congress reasserts its authority on trade”.

In June, Bob Corker – a prominent Republican senator from Tennessee who has

been a vocal Trump critic and is not running for re-election – authored a bill that

would reform the 1974 Trade Act to remove the president’s unilateral authority on

trade and require congressional approval of all tariffs on national security grounds.

The Republican leadership did not bring the bill to a binding vote. In July, the Senate

backed another non-binding provision to give Congress more say on trade policy. It

was adopted with overwhelming bipartisan support of 88 votes to 11 (the Senate’s

current composition is 51 Republicans and 49 Democrats). Even if such a bill were to

pass, Trump could veto it; but it could precipitate a stand-off between the legislative

and executive branches.

Since the start of Trump’s presidency, there have been numerous calls – including

from Republicans – to roll back the delegation of trade powers to the president. Utah

Republican Senator Mike Lee, along with other senators from both parties, began

promoting The Global Trade Accountability Act in January 2017 to curb executive

authority on trade. The bill is supported by prominent Republican donors David and

Charles Koch; in March 2018, six Republican House representatives referred a

‘companion bill’ (which mirrored the Senate bill) to the House Committee on Ways

and Means and the House Committee on Rules for further review.

Economic cost, lobbying efforts could also bring change to the trade agenda

Against the backdrop of a booming US economy, corporate tax cuts and a strong

equity market, there has been little economic pressure on Trump to change his

confrontational trade policy, particularly with regards to China. This is likely to change

as corporate lobbying pressure and economic costs gradually rise. In response to

these pressures, we believe that the US will eventually reach a deal with China on

tariffs, defusing the trade war. However, we make a distinction between the issue of

Constitutionally, Congress has sole

authority over trade; but over the

years, it has delegated some of this

authority to the president

Senators have already taken

initiatives to restore Congress’

authority on trade

A deal with China could see a

‘rebalancing’ of the trade deficit;

resolving the IP issue would be

more difficult

Global Focus – Q4-2018

Standard Chartered Global Research | 2 October 2018 26

G

lobal

overv

iew

Geo

po

liti

cal

eco

no

mic

s

A

sia

M

EN

AP

A

fric

a

E

uro

pe

A

me

ricas

S

trate

gy

o

utlo

ok

Fo

recasts

and

re

fere

nces

tariffs and trade deficit ‘rebalancing’ on one side, and broader US-China differences

on intellectual property (IP) and technological transfers on the other. This second set

of issues is unlikely to be resolved imminently, and there is broad consensus – in US

political circles and beyond – that the US needs to be tough on China in these areas.

Concerns among US business groups are a source of mounting pressure on

Congress members to act against tariffs. Multiple organisations have criticised

Trump’s trade policy, including the National Retail Federation, the Consumer

Technology Association, the US Chamber of Commerce, the Business Roundtable,

the US-China Business Council and the National Association of Manufacturers. US

farmers have been negatively affected by China’s retaliatory tariffs on US exports of

soybeans, corn and other crops, prompting the Trump administration to announce a

USD 12bn bailout programme.

Farmers’ reaction was of particular concern to Republican lawmakers. Bloomberg

reported that “"the package has offended the sensibilities of many farmers who

supported both Trump and a party that historically champions small government and

free trade". Quoting Dave Struthers, a soy farmer affected by the tariffs, “we would

prefer trade, not aid.” In September, a coalition of the National Retail Federation and

150 organisations told the Trump administration in an open letter that “tit-for-tat tariffs

are counterproductive and so far have only produced increased costs for American

business, farmers, importers, exporters and consumers.”

Economic costs – in terms of both corporate profits and jobs – are likely to surface

gradually as tariffs remain in place. Companies may increase their lobbying efforts

before that happens; this was a theme of our recent conversations with US corporate

clients. Analysis of previous US tariff episodes shows that they have destroyed jobs

and incurred costs for the economy as a whole. A widely cited 2003 study by

consulting firm Trade Partnership Worldwide found that steel tariffs imposed by the

G.W. Bush administration in 2002 cost 200,000 US jobs (more than total US steel

industry employment at the time). One in four job losses was in the steel-making

industry itself, while there were many more in steel-consuming industries. The report

also mentioned USD 4bn in lost wages in only nine months. A 2012 study by the

Peterson Institute for International Economics showed that President Obama’s tariffs

on China-made tyres in 2009 saved 1,200 jobs at the distorted cost of USD 900,000

each, and caused 2,500 job losses in retail due to higher prices.

Trump’s tariffs may come at a higher economic cost than previous episodes. The Tax

Foundation – a public non-partisan US tax policy analysis institute – estimates that

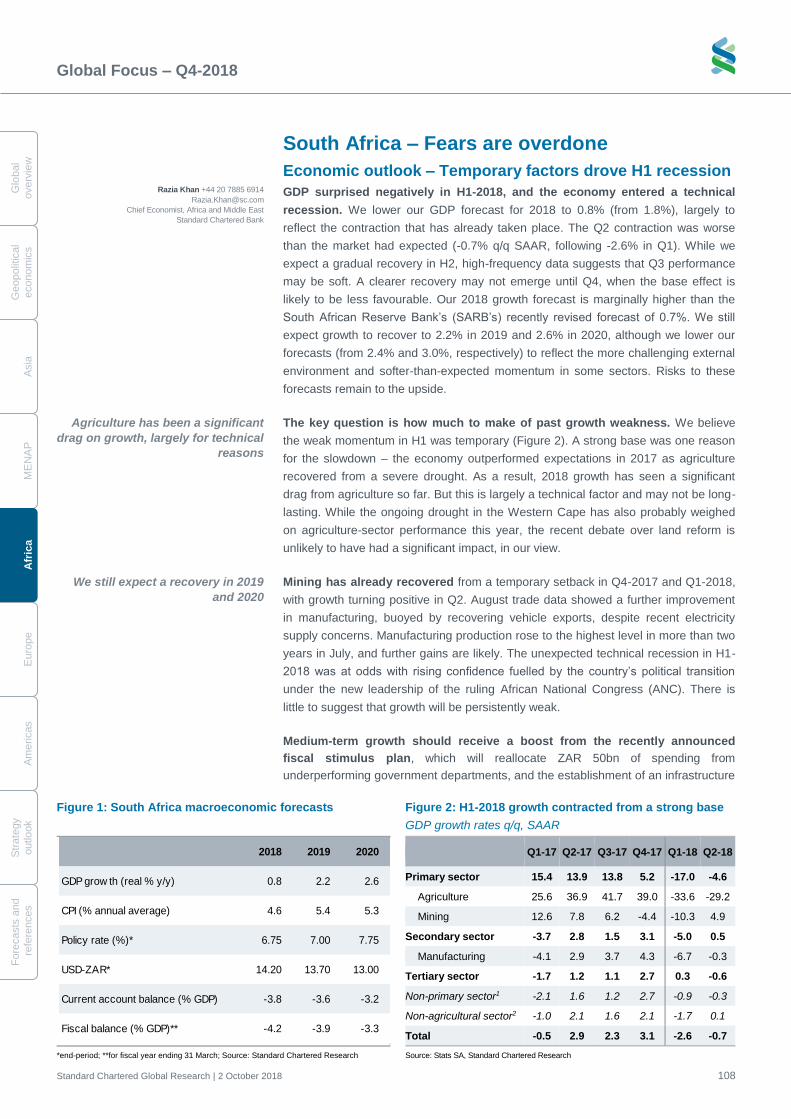

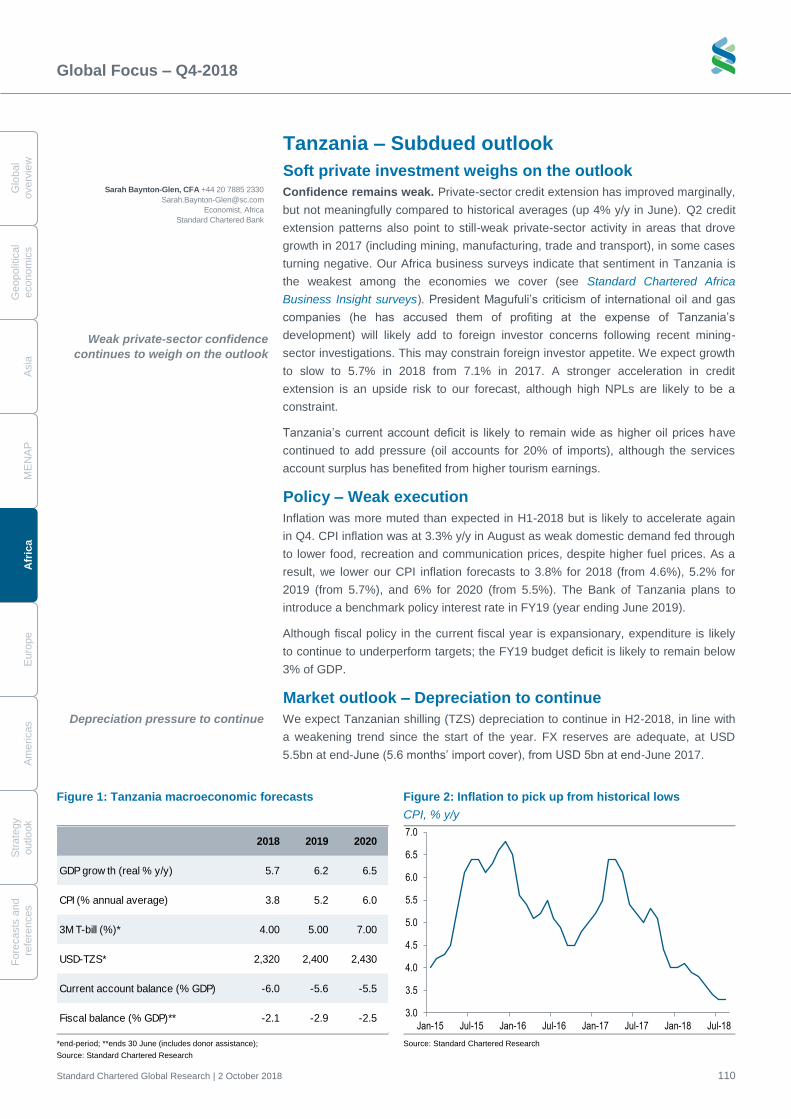

tariffs announced and enacted as of 18 September would eventually result in half a