Embed Size (px)

Citation preview

This article was downloaded by: [University of Lethbridge]On: 24 July 2014, At: 11:43Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH,UK

International Economic JournalPublication details, including instructions for authorsand subscription information:http://www.tandfonline.com/loi/riej20

Are We Sure That the RealExchange Rate Follows a RandomWalk? A ReexaminationBaizhu Chen a & Kien C. Tran ba The Claremont Graduate Schoolb University of Western OntarioPublished online: 28 Jul 2006.

To cite this article: Baizhu Chen & Kien C. Tran (1994) Are We Sure That the RealExchange Rate Follows a Random Walk? A Reexamination, International EconomicJournal, 8:3, 33-44

To link to this article: http://dx.doi.org/10.1080/10168739400000004

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all theinformation (the “Content”) contained in the publications on our platform.However, Taylor & Francis, our agents, and our licensors make norepresentations or warranties whatsoever as to the accuracy, completeness, orsuitability for any purpose of the Content. Any opinions and views expressedin this publication are the opinions and views of the authors, and are not theviews of or endorsed by Taylor & Francis. The accuracy of the Content shouldnot be relied upon and should be independently verified with primary sourcesof information. Taylor and Francis shall not be liable for any losses, actions,claims, proceedings, demands, costs, expenses, damages, and other liabilitieswhatsoever or howsoever caused arising directly or indirectly in connectionwith, in relation to or arising out of the use of the Content.

This article may be used for research, teaching, and private study purposes.Any substantial or systematic reproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in any form to anyone is expresslyforbidden. Terms & Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

INTERNATIONAL ECONOMIC JOURNAL Volume 8, Number 3, Autumn 1994

ARE WE SURE THAT THE REAL EXCHANGE RATE FOLLOWS A RANDOM WALK? A REEXAMINATION

BAIZHU CHEN The Claremont Graduate School

KIEN C. TRAN* University of Western Ontario

This paper reexamines whether the real exchange rate follows a random walk. We test the null hypothesis of a unit root against the alternative of stationarity and also the null hypothesis of stationarity against the alternative of a unit root. The test proposed by Kwiatkowski, Phillips, Schmidt and Shin (KPSS, 1992) is modified and applied to the monthly and annual data. While our monthly series suggest somewhat mixed results, the results of annual data favor the stationarity hypothesis in our both tests. We conclude that the real exchange rate may have a long mean-reversion component that the conventional unit root tests are not powerful C w g h to detect in a short span sample. [F 3 11

1. INTRODUCTION

That the real exchange rate follows a random walk has almost become a paradigm in the international finance literature for a long time. However, this conclusion has been subject to increasing debate recently. On one side, many continue to find evidence supporting this conclusion. Corbae and Ouliaris (1988) find evidence for the random walk hypothesis of the real exchange rate for the post-1973 data except for the Canada-U. S. case. Enders (1988) applying cointegration tests and error correction model provides mixed support for the random walk hypothesis. Fisher and Park (1991) also find evidence for the nonstationarity of the real exchange rate. However, as Hakkio (1984, 1986) points out, the conventional tests used to test the unit root of the real exchange rate may suffer the deficiency of low power. Using cross-country tests, he has found some evidence for the stationarity of the real exchange rate in the 1970s. Recently, there emerge increasing challenges to the random walk hypothesis of the real exchange rate. Abuaf and Jorion (1990), Diebold, Husted and Rush (1991), Liu and He (1991). Grilli and Kaminsky (1991), and Whitt (1992) all find evidence

*We are very grateful to Robin Carter, Bruce Hansen, Alfred Haug, John Knight, Alan Stockman and the participants in the Econometrics Workshop at the University of Western Ontario for their valuable comments and suggestions. We also thank an anonymous referee and the editor of the Journal for their useful comments. However, they are not responsible for any errors. Baizhu Chen thanks the University of Saskatchewan for providing a starting research grant.

Dow

nloa

ded

by [

Uni

vers

ity o

f L

ethb

ridg

e] a

t 11:

43 2

4 Ju

ly 2

014

34 B. CHEN AND K. C. TRAN

that a substantial transitory component exists in the long horizon time series of the real exchange rate.

Whether the real exchange rate follows a stationary process has some important implications in international finance. First of all, the real exchange rate measures the deviation from purchasing power parity (PPP). A finding that the real exchange rate follows a random walk or a nonstationary process suggests that the deviation from purchasing power parity is not transitory but permanent. This implies that purchasing power parity as a long run relation between the exchange rate and the relative price level of two countries does not hold. If this is true, then there is absolutely no tendency to return to purchasing power parity and one country's price can get out of line from another's without any limit. On the other hand, a finding that the real exchange rate is stationary indicates that purchasing power parity can still be a valid equilibrium proposition in the long run. Secondly, that the real exchange rate follows a random walk or the change of the real exchange rate is permanent is often used as a test against the disequilibrium theory of the exchange rate (Dornbusch, 1976). According to the disequilibrium approach, a change in the real exchange rate occurs in response to changes in the nominal exchange rate because of sticky nominal good price. As prices adjust eventually toward the new equilibrium levels, the real exchange rate should adjust back toward its new equilibrium value. A disequilibrium model of exchange rate implies that changes of the real exchange rate are transitory. Finally, the random walk behavior of the real exchange rate is not inconsistent with an equilibrium model. Stockman and Dellas (1989) show that in an equilibrium model, the relative price of the nontraded goods and thus the real exchange rate is a martingale under certain conditions.' However the conditions for a random walk behavior of the real exchange rate are stringent, and require that shocks to the economy are of a permanent nature and are dominantly the real shocks because monetary shocks are widely believed to have only a transitory real effects.' To determine whether the real exchange rate in fact follows a random walk can help to shed light on the nature of the shocks to the economy.

This study joins the debate on the stationarity versus nonstationarity of the real exchange rate. Apart from the conventional unit root tests on the real exchange rate, we perform the tests on the stationarity of the real exchange rate. Specifically, we test the null hypothesis of stationarity against the alternative of nonstationarity. We modify the stationarity test proposed by Kwiatkowski, Phillips, Schmidt and Shin (1992, hereafter KPSS). Instead of using Barlett's window as suggested by them, we use the automatic bandwidth estimator with Quadratic Spectral kernel as suggested by Andrew (1991) in calculating the test statistics. This simple modification enables us to avoid the drawbacks of the original test. The modified KPSS test is applied to our real exchange rate series. We use both monthly and annual data. Our main findings

'They show that the relative price of nontraded goods is a martingale if (1) real disturbances are permanent, and (2) the utility function is isoelastic.

2See Obstfeld (1985), and Cambell and Clarida (1987).

Dow

nloa

ded

by [

Uni

vers

ity o

f L

ethb

ridg

e] a

t 11:

43 2

4 Ju

ly 2

014

REAL EXCHANGE RATE 35

are as follows. First, the standard Augmented Dickey-Fuller tests can not reject the null hypothesis of nonstationarity for all the monthly data, but reject it for all the annual data except the real exchange rate of pound. Second, the KPSS tests suggest that we can only reject in the monthly data the null hypothesis of stationarity for yen. Particularly we can not reject the null hypothesis of stationarity for the annual data. Thus though the random walk hypothesis is not completely rejected for the monthly data, it is rejected in favor of the stationarity hypothesis for the annual data. We conclude that there may be a long mean-reversion transitory component in the change of the real exchange rate that the conventional unit root tests are not powerful enough to detect in a short span sample.

Section 2 provides a little background on the real exchange rate and PPP, and discusses the data construction. Section 3 introduces the econometric methods used to test our hypothesis. Results are explained in section 4. Section 5 concludes.

2. THE REAL EXCHANGE RATE AND THE DATA

The real exchange rate is defined as

where q, is the time t real exchange rate, e, is the nominal foreign exchange rate per domestic currency, and p, andp: are the domestic and foreign price levels. The real exchange rate is simply the relative price of the domestic good in terms of the foreign good.

If q, = 1, (1) is called absolute purchasing power parity (PPP) which states that the

same currency should have the same purchasing power in the two countries. If q, equals any constant number, (1) is the so called relative purchasing power parity, or in an equivalent form:

where I'I, and I'Ihre the inflation rates in the domestic and foreign countries. Relative PPP states that the depreciation of the foreign exchange rate should equal the inflation rate differential between the foreign and domestic countries.

Generally the empirical evidence supports neither absolute PPP nor relative PPP as a short-run proposition. Provided that the conditions under which PPP holds are often violated in the real world, e.g., the existence of nontraded good, it is understandable why purchasing power parity as a short-run proposition does not hold (Kravis and Lipsey, 1983). The question that remains is whether PPP can still be a long run equilibrium proposition. If PPP holds in the long run, then the parity relation between

Dow

nloa

ded

by [

Uni

vers

ity o

f L

ethb

ridg

e] a

t 11:

43 2

4 Ju

ly 2

014

36 B. CHEN AND K. C. TRAN

countries will be re-established eventually even if there are deviations from purchasing power parity in the short run. In this case, the deviation from PPP is only transitory. On the other hand, if PPP as a long run equilibrium relation does not hold, then the deviation from purchasing power parity is not transitory and will not disappear even in the long run. Thus, whether PPP holds in the long run is equivalent to whether the deviation from PPP is transitory. Since the real exchange rate measures the deviation from PPP, the same question translates to whether the real exchange rate is stationary or nonstationary. If the real exchange rate follows a nonstationary process, then the deviation from purchasing power parity is permanent and PPP does not hold in the long run. On the other hand, if the real exchange rate follows a stationary process, then the deviation from pu;chasing power parity is only transitory and will disappear in the long run eventually. In this case, the parity condition will eventually be restored.

We construct the log real exchange rates per dollar using (1) for four countries: Canada, France, Japan, and United K ingd~m.~ Since we want to test long run PPP, we need the data which span as long as possible. The monthly data is from the first month of 1957 to the last month of 1988. We also construct the annual real exchange rates for these countries from 1900- 1990, except for canadian dollar (1 875-1 900). The wholesale price indices are used to calculate the real exchange ratesU4

The countries studied here have gone through many different exchange rate systems over these long periods of time, and have switched from the fixed exchange rate system to the floating exchange rate system in 1973. However the measure of the real exchange rate is not affected by the change of exchange rate system and thus neither is the test of stationarity versus nonstationarity of the real exchange rate.

3. LM STATISTICS FOR THE STATIONARY HYPOTHESIS

As mentioned in the introduction, the standard Augmented Dickey-Fuller tests for the null hypothesis of unit root tend to have low power against the alternative hypothesis of stationarity (Diehold, Husted and Rush, 1991; Diebold and Rudebusch, 1989; Schwert 1989). Thus, in deciding whether economic data are integrated or not based on the Augmented Dickey-Fuller tests may be inadequate. This inadequacy leads researchers to find alternative methods. There are many various alternatives in recent unit root literat~re,~ however one particular method that attracts our attention is one proposed by Kwiatkowski, Phillips, Schmidt and Shin (1992). They provide tests

3We have also run tests on the cross real exchange rates per pound which lead us to the same conclusions of this paper. To save space, we do not report the results here.

W e have also used CPI for monthly and annual data. Annual data of CPI before 1914 were not compiled. Our results are similar to those using the wholesale price indices.

5For Bayesian approaches, see DeJong and Whiteman (1991). For other classical approaches, see Park and Choi (1990), Rudebusch (1990), DeJong, Nankervis, Savin and Whiteman (1992).

Dow

nloa

ded

by [

Uni

vers

ity o

f L

ethb

ridg

e] a

t 11:

43 2

4 Ju

ly 2

014

REAL EXCHANGE RATE 37

complement to the Augmented Dickey-Fuller tests for unit root by testing the null hypothesis of stationarity. In particular, by testing both the unit root hypothesis and the stationarity hypothesis, researchers can distinguish economic series that appear to be unit root, series that appear to be stationary, and series for which data are not sufficiently informative to be sure whether the series are integrated or stationary.

Because the test statistics used in this paper for the stationarity test are described fully in Kwiatkowski, Phillips, Schmidt and Shin (1992), we shall give here only a brief summary with some modifications of the tests. The tests are derived as a special case of the statistics developed by Nabeya and Tanaka (1988). They are easy to implement and flexible to deal with either trended or nontrended series. We consider the regression model:

u, is i.i.d.(0, 0;). E, is assumed to be stationary. Combining ( 3 ) and (4 ) , we can rewrite the above regression model as fol10w.~

Here the initial value of x, is assumed to be fixed and plays the role of an intercept. Thus, the null hypothesis of stationarity is simply, H,:G: = O (or equivalently 0; =0). Since E is assumed to be stationary, under the null hypothesis, y, is trend stationary if a # 0 while y, is level stationary if a = 0 .

KPSS's (1992) approach yields two types of statistics. The f ir statistic is based on the null of trend stationary, and is given by

where S, = CI=,C, ,Ci is the residual from regression (5). ~ ' ( 1 ) is the consistent estimator

of the "long run variance" o2 = limT,_ T-'E(s;). It is given by

w(s, 1) is the weighting function that corresponds to the choice of a spectral window. KPSS (1992) considers only the integer valued lag truncation parameters.

"Here no assumption is being made about the process E,

Dow

nloa

ded

by [

Uni

vers

ity o

f L

ethb

ridg

e] a

t 11:

43 2

4 Ju

ly 2

014

38 B. CHEN AND K. C. TRAN

Specifically, they used Barlett's window of the form w(s, 1) = 1 - sl(1 + 1). However, with this choice of weighting function, the estimation S2(l) and hence the test statistic, f i , suffers some drawbacks. First, the values of test statistic, f i , are fairly sensitive to the choice of the lag truncation parameter, I. Therefore, the ability to reject the hypothesis of stationarity depend crucially upon the choice of 1. Secondly, there is no systematic way or guidance to tell how one can choose I . Therefore, to avoid these problems, we propose to use Andrew's (1991) automatic bandwidth estimator with the Quadratic Spectral (QS) kernel as the weighting function.' Andrew (1991) compared various kernel estimators of heteroskedasticity and autocorrelation consistent variance-covariance matrices. He also compared several methods to truncate the lag length. He found that the automatic bandwidth estimator with the QS Kernel was optimal in terms of the bias, mean squared error, and true confidence levels. The quadratic spectral kernel is given by

with the automatic plug - in bandwidth estimator

where n= 3.1415 and b,denotes the first-order autorgressive coefficient estimate of p by regressing G, against G,-,.' Thus, the consistent estimator of the "long-run variance." 0 2 now becomes:

I

Thus, the f i , statistics can be calculated by

The f i , statistic is shown to be distributed asymptotically I;v;(r)dr, where V,(r) is the second-level Brownian bridge and the upper tail critical values are given in KPSS (1992).

The second type of statistic, fi,, is based on the null hypothesis of level stationary which in (3, we set a = 0 so that the residuals C, are now from a regression of y, and

'The advantages of choosing this particular type of weighting function are discussed in Andrew (1991), Ogaki and Park (1990).

8About the general form of this weighting function, see Andrew (1991). Also see Hansen (1991) for the conditions of M for s'(M) to be consistent.

Dow

nloa

ded

by [

Uni

vers

ity o

f L

ethb

ridg

e] a

t 11:

43 2

4 Ju

ly 2

014

REAL EXCHANGE RATE 39

intercept only. The test statistic fi, is computed as in (11) but its asymptotic distribution is now j;v(r)'dr where V(r) is the standard Brownian bridge. The critical values are also tabulated in KPSS (1992).9

These two statistics, fir and fip, are calculated using the real exchange rate time series. The statistics are used to test the null hypothesis of stationarity against the alternative of unit root of the real exchange rate.

4. EMPIRICAL RESULTS

A. Test the Null Hypothesis of Unit Root

We first use the Augmented Dickey-Fuller method to test the null hypothesis of a unit root against the alternative of stationarity for the real exchange rate time series. The equation tested is the following

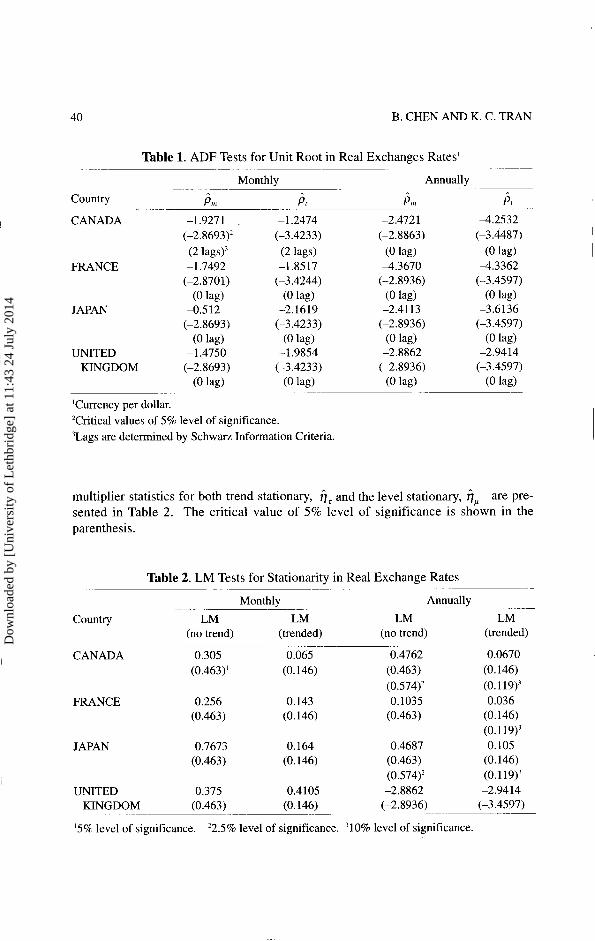

where y, is the log real exchange rate, and A is the first difference. If y, contains a unit rdot, a test for the null hypothesis that the coefficient p = 0 will not be rejected. The results of the test are presented in Table 1 for the monthly and annual data. The br and b, statistics are the 't-statistics' for the null hypothesis that p is zero with and without a trend in the regression respectively. The critical value of 5% level of significance is reported in the parenthesis. The number of lags is determined according to Schwarz's information criterion (SIC = -2 In likelihood + 1nT [# of parameters], where T is the sample size).

The Augmented Dickey-Fuller test indicates that for the monthly data, we can not reject the null hypothesis of unit root in all the real exchange rate series. The results for the annual data show a mixed picture. The test rejects the unit root hypothesis for the real exchange rate of franc. It rejects the random walk hypothesis for the canadian dollar and yen if trends are taken into account.'O The unit root hypothesis is not rejected only marginally for pound.

B. Test the Null Hypothesis of Stationarity

We next perform the test on the null hypothesis of stationarity against the alternative of nonstationarity. The modified KPSS test described in section 3 is applied to the real exchange rates using the monthly and annual data. The Lagrange

9The asymptotic distribution of both f i , andj , are unaltered when different weighting function is used provided that the estimate of s'(M) is consistent.

''We have plotted out these time series. The real exchange rates of the canadian dollar and yen display clear trends over the whole sample.

Dow

nloa

ded

by [

Uni

vers

ity o

f L

ethb

ridg

e] a

t 11:

43 2

4 Ju

ly 2

014

B. CHEN AND K. C. TRAN

Table 1. ADF Tests for Unit Root in Real Exchanges Rates1 -- - - --

Monthly - - -

Annually --

Country --

P m - -

bt b m bt -

CANADA -1.927 1 -1.2474 -2.4721 4.2532 (-2.8693)2 (-3.4233) (-2.8863) (-3.4487)

(2 lags)' (2 lags) (0 lag) (0 lag) FRANCE -1.7492 -1 3517 4.3670 4.3362

(-2.8701) (-3.4244) (-2.8936) (-3.4597) (0 1%) (0 lag) (0 1%) (0 1%)

JAPAN -0.512 -2.1619 -2.4113 -3.6136 (-2.8693) (-3.4233) (-2.8936) (-3.4597)

(0 lag) (0 1%) (0 1%) (0 1%) UNITED -1.4750 -1.9854 -2.8862 -2.9414

KINGDOM (-2.8693) (-3.4233) (-2.8936) (-3.4597) (0 lag) (0 lag) (0 lag) (0 lag)

'Currency per dollar. 'Critical values of 5% level of significance. 'Lags are determined by Schwarz Information Cntena.

multiplier statistics for both trend stationary, f i r and the level stationary, fi, are pre- sented in Table 2. The critical value of 5% level of significance is shown in the parenthesis.

Table 2. LM Tests for Stationarity in Real Exchange Rates - - - -

Monthly - - - -- - --

Annually

Country LM LM LM LM (no trend) (trended) (no trend) (trended)

- - - - --

CANADA 0.305 0.065 0.4762 0.0670 (0.463)' (0.1 46) (0.463) (0.146)

(0.574)' (0.1 19)' FRANCE 0.256 0.143 0.1035 0.036

(0.463) (0.146) (0.463) (0.146) (0.119)3

JAPAN 0.7673 0.164 0.4687 0.105 (0.463) (0.146) (0.463) (0.146)

(0.574)' (0.119)3 UNITED 0.375 0.4105 -2.8862 -2.9414

KINGDOM (0.463) (0.146) (-2.8936) (-3.4597)

'5% level of significance. 22.5% level of significance. '10% level of significance.

Dow

nloa

ded

by [

Uni

vers

ity o

f L

ethb

ridg

e] a

t 11:

43 2

4 Ju

ly 2

014

REAL EXCHANGE RATE 4 1

For the monthly data, we can reject neither the level stationary nor the trend stationary for canadian dollar and french franc. We can not reject the level stationary for pound at 5 percent level of significance. We reject both level stationary and trend stationary for yen. For the annual data, the evidence strongly favors the stationarity for franc and pound. The evidence also supports trend stationary for canadian dollar and yen but marginally rejects level stationary at 5% level. However at 2.5% level, the level stationary hypothesis for Canadian dollar and yen can't be rejected. Overall, we conclude that the evidence using the annual data favors the null hypothesis of stationarity of the real exchange rates.

C. Discussion

Our Augmented Dickey-Fuller test for unit root and KPSS test both show that the annual time series of real exchange rates of canadian dollar, franc and yen over a long period of time are stationary, while pound shows a unit root in our Augmented Dickey-Fuller test but passes our KPSS stationarity test. These results are consistent with the findings of Grilli and kaminsky (1991), and Diebold et al. (1991). These papers use long span time series (often more than one hundred years) to conclude that the real exchange rate may in fact be stationary. Diebold et al. (1991) argue that in testing PPP as a long run proposition, longer horizon samples rather than larger samples should be used.

Using monthly data, our tests provide mixed results. On the one hand, the standard unit root tests imply a unit root for all the monthly series. On the other hand, using the KPSS test, we can only reject the null hypothesis of stationarity for yen. However, due to the fact that the standard Augmented Dickey-Fuller tests tend to have low power in detecting a long mean-reversion component in a short span sample, it is not too surprising that the Dickey-Fuller tests do not reject the unit root hypothesis for the monthly data. In fact, many economists recently have found that using more powerful alternative tests, the unit root hypothesis is often rejected even for the monthly real exchange rate. For example, using a heteroscedasticity-consistent variance-ratio test. Liu and He (1991) provide evidence rejecting the unit root hypothesis for monthly data. Whitt (1992) applies both Dickey-Fuller test and Baysian approach, and finds somewhat mixed results; while he can not reject random walk by the Dickey-Fuller test, he clearly rejects it by the Baysian approach. Abuaf and Jorion (1990) increase statistical power by using a multivariate generalized least squares version of the Dickey-Fuller test, and provide evidence against random walk using monthly data. Our results are also in line with the findings of these authors. Contrary to the Dickey-Fuller results, our KPSS test results using monthly data generally can not reject the null hypothesis of stationarity.

5. CONCLUSION

There have been emerging challenges to the view that the real exchange rate

Dow

nloa

ded

by [

Uni

vers

ity o

f L

ethb

ridg

e] a

t 11:

43 2

4 Ju

ly 2

014

42 B. CHEN AND K. C. TRAN

follows a random walk. Two recent papers, Grilli and kaminsky (1991), and Diebold et al. (1991) find some evidence of stationarity of the real exchange rate using data of long spans. In addition, using more powerful tests, Abuaf and Jorion (1990), Liu and He (1991), and Whitt (1992) also reject the random walk hypothesis for the monthly real exchange rate. These findings all suggest that the conventional unit root test may not be powerful enough to detect the stationarity of the real exchange rate.

This p'aper tests the null hypothesis of unit root against the alternative of stationarity of the real exchange rate. Unlike other studies, we also reverse the null. We test the null hypothesis of stationarity against the alternative of nonstationarity. We modify the test proposed by Kwiatkowski, Phillips, Schmidt and Shin (1992) and apply the modified test on the real exchange rate. Our results suggest that the random walk hypothesis can be clearly rejected in the annual data and that moderate support for the stationarity hypothesis can also be found in the monthly real exchange rate.

I We conclude that PPP may still be a valid long run proposition and that the real exchange rate may have a long mean-reversion component that standard Augmented Dickey-Fuller unit root tests are not powerful enough to detect in a short sample.

APPENDIX: DATA SOURCES

Monthly

The exchange rates and wholesale price indices of all countries from 1957 to 1988 are taken from International Financial Statistics (IFS) data tape.

Annual data

The exchange rate and wholesale price indices from 1900 to 1975 are taken from The Purchasing Power Parity, by Moon H . Lee, New York: M. Dekker, 1975. The canadian exchange rate and wholesale price index from 1875 to 1900 are from Historical Statistics of Canada, First Edition (1963). Ottawa, Statistics Canada. The U. S. Wholesale price index from 1875 to 1900 is the quarterly average of the series from "Historical Data" by Nathan Balke and Robert Gordon, in The American Business Cycles: Continuity and Change, University of Chicago Press.

REFERENCES

Abuaf, Niso and Jorion, Philippe, "Purchasing Power Parity in the Long Run," Journal of Finance, March 1990, 157-176.

Andrew, Donald, "Heteroskedesticity and Autocorrelation Consistent Covariance Matrix Estimation," Econometrica, May 1991, 817-858.

Cambell, J. and Clarida, Richard, "The Dollar and the Real Interest Rate," in Karl Brunner and Allan Meltzer, eds., Empirical Studies of Ve loc i~ , Real Exchange

Dow

nloa

ded

by [

Uni

vers

ity o

f L

ethb

ridg

e] a

t 11:

43 2

4 Ju

ly 2

014

REAL EXCHANGE RATE 43

Rates, Unemployment, and Productivity, Carnegie-Rochester Conferences Series on Public Policy, 1987.

Corbae, Dean and Ouliaris, Sam, "Cointegration and Tests of Purchasing Power Parity," Review of Economics and Statistics, August 1988,508-5 11.

DeJong, David and Whiteman, Charles, "Trends and Random Walks in Macroeco- nomic Time Series; A Reconsideration Based on Likelihood Principle," Journal of Monetary Economics, October 1991,221-254.

DeJong, David N., Nankervis, John C., Savin, N. E. and Whiteman, Charles, "Inte- gration versus Trend Stationarity in Time Series," Econometrica, March 1992, 423-433.

Diebold, Francis, Husted, Steven and Rush, Mark, "Real exchange rate under gold Standard," Journal of Political Economy, December 1991, 1252-127 1.

Diebold, Francis and Rudebusch, Glenn D., "Long Memory and Persistence in Aggregate Output," Journal of Monetary Economics, September 1989, 189-209.

Dornbusch, Rudiger, "Expectations and exchange rate," Journal of Political Economy, December,l976. 1161-1 176.

Enders, Walter, "ARIMA and Cointegration Tests of PPP Under Fixed and Flexible Exchange Rate Regimes," Review of Economics and Statistics, August, 1988, 504- 508.

Fisher, Eric and Park, Joon Y., "Testing Purchasing Power Parity Under the Null Hypothesis of Cointegration," Economic Journal, November 1991, 1476- 1484.

Grilli, Vittrio and Kaminsky, Graciela, "Nominal Exchange Rate Regimes and the Real Exchange Rate: Evidence from the United States and Great Britain, 1885- 1986," Journal of Monetary Economics, April 1991, 191-212.

Hakkio, Craig, "A Reexamination of Purchasing Power Parity: Multi-Country and Multi-Period Study," Journal of International Economics, November 1984, 265- 277.

, "Does the Exchange Rate Follow a Random Walk? a Monte Carlo Study of Four Tests for a Random Walk," Journal of International Money and Finance, June 1986,221-229.

Hansen, Bruce, "Tests for Parameter Nonstability in Regressions with I(1) Processes," University of Rochester, August 1991.

Kravis, Irvine and Lipsey, Richard, "Toward an Explanation of National Price Levels," Princeton Studies in International Finance, No. 52, 1983.

Kwiatowski, Denis, Phillips, Peter C. B., Schmidt, Peter and Shin, Yoogcheol, "Testing the Null Hypothesis of Stationality Against the Alternative of a Unit Root: How Sure are we that Economic Time Series have a Unit Root?" Journal of Econometries, October 1992, 159- 178.

Liu, Christina Y. and He, Jia, "Do Real Exchange Rate Follow Random Walks? a Heteroscedasticity-Robust Autocorrelation Test," International Economic Journal, Autumn 1991, 39-48.

Nabeya, Seiji and Tanaka, Katsuto, "Asymptotic Theory of a Test for the Constancy of Regression Coefficients Against the Random Walk Alternative," Annuals of

Dow

nloa

ded

by [

Uni

vers

ity o

f L

ethb

ridg

e] a

t 11:

43 2

4 Ju

ly 2

014

B . CHEN AND K. C. TRAN

Statistics, 1988,218-234. Obstfeld, Maurice, "Floating Exchange Rates: Experience and Prospects," Brookings

Paper in Economic Activity, 1985, 369-450. Ogaki, Masao and Park, Joon Y., "Inference in Cointegrated Models Using VAR,"

Rochester Center of Economic Research Working Paper 21 8- 1991. Park, Joon Y. and Choi, Buhmsoo, "A New Approach to Testing for a Unit Root,"

Working Paper No. 88-23, Center for Analytical Economics, Cornell University, 1991.

Rudebusch, Glenn D., "Trends and Random Walks in macroeconomic Time Series: A Reexamination," Working Paper Series, Number 105, Economic Activity Section, Board of Governors of the Federal Reserve System, 1991.

Schwert, William G., "Tests for Unit Roots: a Monte Carlo Investigation," Journal of Business and Economic Statistics, 1989, 147- 159.

Stockman, Alan and Dellas, Harris, "International Portfolio Nondiversification and Exchange Rate Variability," Journal of International Economics, May 1989, 271- 289.

Whitt, Joseph, "The Long-Run Behavior of the Real Exchange Rate," Journal of Money, Credit and Banking, February 1992,72-82.

Mailing Address: Professor Baizhu Chen, Department of Economics, The Claremont Graduate School, Claremont, CA 91 711, U. S. A. Mailing Address: Professor Kien C. Tran, Department of Economics, University of Western Ontario, London, Ontario, N6A 5C2, CANADA.

Dow

nloa

ded

by [

Uni

vers

ity o

f L

ethb

ridg

e] a

t 11:

43 2

4 Ju

ly 2

014