Embed Size (px)

Citation preview

2019|Jan

2019|Feb

2019|Mar

2019|Apr

2019|May

2019|Jun

2019|Jul

2019|Aug

2019|Sep

2019|Oct

2019|Nov

2019|Dec

Volume: VIII

Issue: VI

Edition Focused on

Annuities under NPS

Pension Fund Regulatory and Development Authority

Chhatrapati Shivaji Bhawan, B-14/A,Qutab Institutional

Area, Katwaria Sarai New Delhi-110016

Annuities under

NPS

Index

Contents Section 1: Financial Literacy ............................................................................................................... 4

Section 2: NPS Quarterly Statistics .................................................................................................... 7

Section 3 : In The NEWS .................................................................................................................... 10

Section 4: Annuity under NPS .......................................................................................................... 13

Section 5 : NPS Statistics ................................................................................................................... 17

i. Sector wise growth(Yearly and Month wise) ............................................................................. 17

ii) Overall Status of State Governments .......................................................................................... 22

iii. UoS Sector (All citizens) in NPS .................................................................................................. 23

iv. Total amount of subscribers’ contribution under UoS (Tier-I & Tier II): ............................... 24

v. Total amount of AUM under UoS (Tier-I & Tier II) ................................................................... 25

vi. Total number of corporate, subscriber, contribution & AUM registered in Corp sec ......... 26

vii. Status of APY: ................................................................................................................................ 27

viii. PFM wise Total Assets on NPS schemes .................................................................................. 28

ix. PFM wise Return on NPS Schemes ............................................................................................. 29

x. Performance of NPS Schemes of Central Government & State Government Employees .... 29

xi. Performance of NPS schemes for Unorganized/Private Sector .............................................. 30

Section 6: Circulars ............................................................................................................................. 34

Circulars/Notices/Guidelines Issued/Advisory ........................................................................... 34

Section 7: International section ........................................................................................................ 35

Section 8: Events .................................................................................................................................. 38

Section 9: Macro-Economic Statistics .............................................................................................. 39

Graphical representation of Macro Economics Indicators: ........................................................... 40

Section 1: Financial Literacy

Retirement planning and taxation

Retirement usually refers to the end of an earning period. For retirees, making the best use of their retirement corpus that would help keep tax liability at bay and provide a regular stream of income is of prime importance. Building a retirement portfolio with a mix of fixed income and market-linked investments remains a big challenge for many. The challenge is not to outlive the retirement funds - one retires at 58 or 60, while the life expectancy could be 80.

Pre-Retirement Investment Products:

1) NPS: New Pension Scheme or NPS is an ideal retirement product open to all individuals across the country. NPS has delivered annualized returns of around 10% in the last 4 years. This scheme is mandatory for government employees. The fact that fund managers of NPS scheme can also take exposure to equity and equity related instruments is also a positive for the scheme in the long run. NPS provides tax benefit in the form of deduction under section 80C. Remember that it is mandatory to purchase annuity worth 40% of the corpus accumulated through NPS at the time of retirement. We can use Pension Calculators from Government of India to calculate basic pension, family pension and pension commuted. An additional tax deduction u/s 80 CCD (1A) is allowed to the extent of Rs. 50,000 contributed by an assesse to NPS. 2) EPF: Employee’s Provident Fund or EPF is the most popular retirement saving instrument in India. Though it was introduced as a retirement product, not many see it so. The current rate of return from EPF is fixed at 8.5% p.a. EPF offers deduction up to Rs. 150,000 limit under section 80C; interest from EPF is tax free and withdrawal is also tax free if there is continuous service of 5 years. Unlike NPS, EPF does not have any restrictions such as purchasing annuity. However, it is advisable to stay invested in this scheme by opting for EPF transfer whenever there is change of job. This would ensure that investor can reap the benefits of guaranteed returns along with power of compounding. 3) Equities: No matter how many financial instruments one picks, none of them can match the returns provided by equity related instruments such as Stocks and Mutual Funds. While investing in these instruments, make sure that we pick products for the long term i.e., at least 10 years or more. This doesn’t mean you have to stick to the product evening though it is not performing well. Review the products every year or switch to better products only is something has gone wrong fundamentally. Mutual funds also give you an option of monthly SIP, where you can invest in a disciplined manner for your retirement. Equity related products are also tax free after 1 year of investment. However, recent amendments have taxed long term capital gains from equity at the rate of 10%. 4) ETF: Exchange traded funds, popularly known as ETF’s are also a good option for accumulating corpus for retirement. In India, ETF can be done through Index or Gold. Index ETF tracks the index and Gold ETF invests in Gold. An investor can purchase units of ETF by purchasing Gold units every month. The investor would thus benefit from cost averaging rather than investing in bulk and entail the risk of timing the markets.

5) Bonds: Bond is a type of loan taken from investors, by a company or government and giving in return some interest for the loan. Some of these include: IIFCL tax free bonds, HUDCO bonds, inflation bonds, etc. Many of these bonds are for 10 and 15 year durations. Some of these bonds offer interest rates in excess of 10-12% p.a. It is crucial to verify the ratings of these bonds before investing in them.

Post-Retirement Investment Products:

1) Monthly Income Schemes: Post retirement, a person would require schemes which provide regular income. Such schemes are popularly known as Monthly Income Schemes (MIS). Various mutual funds provide these in the form of funds. Post office also provides MIS.

We usually invest a lump sum and the corpus is invested in various instruments to provide us monthly income. Post office offers interest rate of 8.4% p.a and the maturity period would be 5 years.

2) SCSS: Senior citizens saving scheme (SCSS) is just the kind of retirement product that is needed post retirement. This is the safest investment option for senior citizens. Investors can gain an interest of 9.2%p.a with a maturity period of 5 years. The account can be opened in post office or any nationalized banks.

3) Reverse Mortgage: Reverse mortgage is a wonderful option given to senior citizens for a regular source of income. One can pledge his/ her house with a bank to receive income from the bank regularly for a set period of time. The amount received will depend on the valuation of the house and the term opted. A recent ruling on this scheme has made the income received from house property under this scheme totally tax free.

4) Pension Plans: Pension plans are provided by insurance companies as well as mutual funds. They would invest a lump sum amount and provide us with monthly income just as in the case of SCSS or MIS. Charges from insurance company provided pension or annuity plans are usually higher than mutual fund provided ones.

5) Liquid Funds and FD’s: The investment options given above do not provide proper liquidity. As senior citizens, one might need to put some amount aside as an emergency. To make sure that this amount also earns decent returns, one can opt for liquid funds or fixed deposits of varying tenures. Liquid funds are also tax efficient.

Pension plans have two stages – the accumulation stage and the vesting stage. In the accumulation stage, the investors pay annual premiums until the time they reach the age of retirement. On reaching the retirement age; the second stage, the vesting stage begins. During this stage of the pension plan, the retiree will start receiving annuities until the time of their death or the death of their nominee.

The contributions that are made to a pension plan, under section 80CCC, are tax-exempt up to a maximum ceiling of INR 1 lakh. The withdrawals, however, are not tax-free. Only one-third of the corpus that is distributed to the retiree (soon after reaching the retirement age) by the pension plan is tax-free. The rest of the money is distributed as an annuity and is subject to taxation depending on the retiree’s tax rate at the time of retirement.

There are different kinds of pension plans which you can check below:

plans that are sponsored by an insurer where the investment is solely in debt and are best suited for

investors who are conservative.

plans that are unit linked and invest in both equity and debt.

the National Pension Scheme which invests in either in 100 percent government securities, 100 percent

debt securities (other than government securities) or in a maximum of 50 percent equity.

Author: Rakesh Singhi

Know your NPS (This section is about the knowledge of various entities, instruments, terms etc. forming part of NPS)

Who can join NPS

Any citizen of India, whether resident or non-

resident, who are aged between 18 – 65 years as on

the date of submission of his/her application. The

citizens can join NPS either as individuals or as an

employee-employer group(s) (corporates) subject to

submission of all required information and Know

your customer (KYC) documentation.

Section 2: NPS Quarterly Statistics

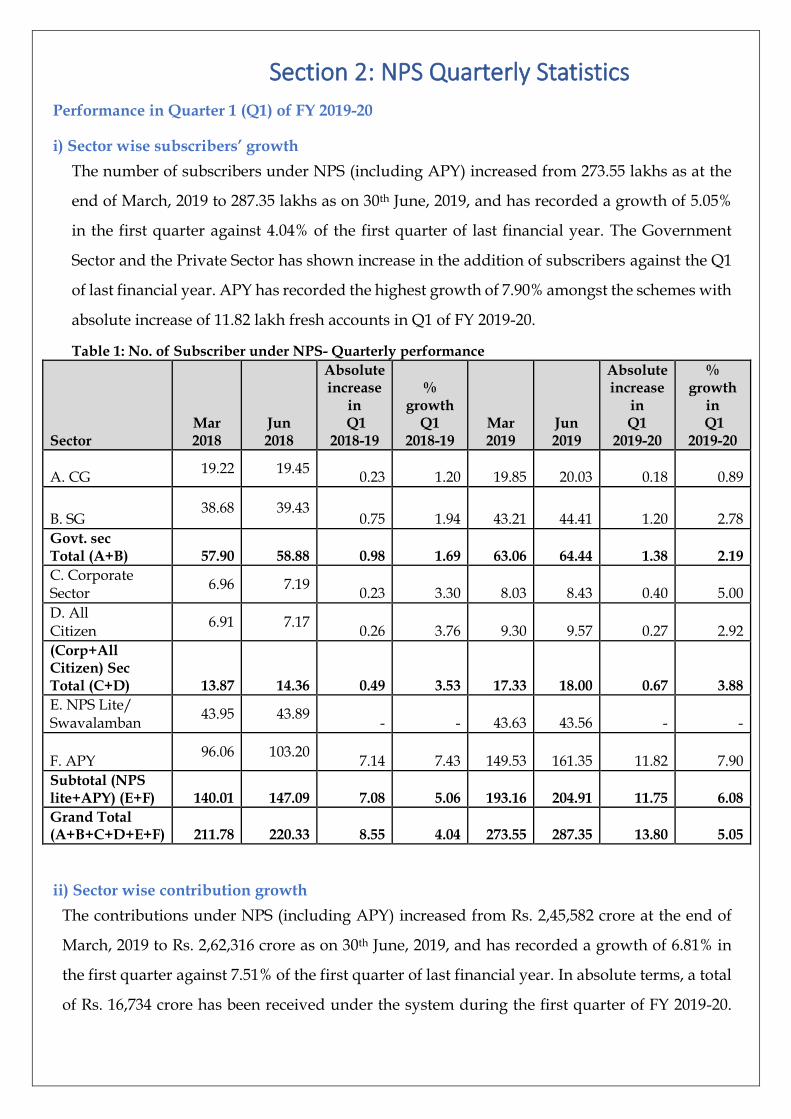

Performance in Quarter 1 (Q1) of FY 2019-20

i) Sector wise subscribers’ growth

The number of subscribers under NPS (including APY) increased from 273.55 lakhs as at the

end of March, 2019 to 287.35 lakhs as on 30th June, 2019, and has recorded a growth of 5.05%

in the first quarter against 4.04% of the first quarter of last financial year. The Government

Sector and the Private Sector has shown increase in the addition of subscribers against the Q1

of last financial year. APY has recorded the highest growth of 7.90% amongst the schemes with

absolute increase of 11.82 lakh fresh accounts in Q1 of FY 2019-20.

Table 1: No. of Subscriber under NPS- Quarterly performance

Sector Mar 2018

Jun 2018

Absolute increase

in Q1

2018-19

% growth

Q1 2018-19

Mar 2019

Jun 2019

Absolute increase

in Q1

2019-20

% growth

in Q1

2019-20

A. CG 19.22 19.45

0.23 1.20 19.85 20.03 0.18 0.89

B. SG 38.68 39.43

0.75 1.94 43.21 44.41 1.20 2.78

Govt. sec Total (A+B)

57.90

58.88 0.98 1.69 63.06 64.44 1.38 2.19

C. Corporate Sector

6.96 7.19 0.23 3.30 8.03 8.43 0.40 5.00

D. All Citizen

6.91 7.17 0.26 3.76 9.30 9.57 0.27 2.92

(Corp+All Citizen) Sec Total (C+D)

13.87

14.36 0.49 3.53 17.33 18.00 0.67 3.88

E. NPS Lite/ Swavalamban

43.95 43.89 - - 43.63 43.56 - -

F. APY 96.06 103.20

7.14 7.43 149.53 161.35 11.82 7.90

Subtotal (NPS lite+APY) (E+F)

140.01

147.09 7.08 5.06 193.16 204.91 11.75 6.08

Grand Total (A+B+C+D+E+F)

211.78

220.33 8.55 4.04 273.55 287.35 13.80 5.05

ii) Sector wise contribution growth

The contributions under NPS (including APY) increased from Rs. 2,45,582 crore at the end of

March, 2019 to Rs. 2,62,316 crore as on 30th June, 2019, and has recorded a growth of 6.81% in

the first quarter against 7.51% of the first quarter of last financial year. In absolute terms, a total

of Rs. 16,734 crore has been received under the system during the first quarter of FY 2019-20.

The Government Sector and the Private Sector has registered growth of 6.72% and 6.82% in the

Q1 of FY 2019-20 against 7.09% and 9.28% of respective sector in Q1 of FY 2018-19. APY has

recorded the highest growth in percentage term i.e. 11.79% amongst the schemes, however in

absolute terms highest contribution has been collected by State Government Sector.

Table 2: Contribution under NPS- Quarterly performance

Sector Mar 2018

Jun 2018

Absolute increase

in Q1

2018-19

% growth

Q1 2018-19

Mar 2019

Jun 2019

Absolute increase

in Q1

2019-20

% growth

in Q1

2019-20

A. CG

62351 66273 3922

6.29 78379 83,106 4,727 6.03

B. SG 92808 99884 7076

7.62 124191 1,33,084 8,893 7.16

Govt. sec Total (A+B)

155159

166157 10998

7.09 202570 2,16,190 13,620 6.72

C. Corporate Sector 17704 19211 1507

8.51 24437 25,955 1,518 6.21

D. All Citizen

5824

6501 677

11.62 9685 10,495 810 8.37

(Corp+All Citizen) Sec Total (C+D)

23528

25712 2184

9.28 34122 36,450 2,328 6.82

E. NPS Lite/ Swavalamban

2378

2441 63

2.65 2555 2,594 39 1.53

F. APY

3602

4220 618

17.16 6335 7,082 747 11.79

Subtotal (NPS lite+APY) (E+F)

5980

6661 681

11.38 8890 9,676 786 8.84

Grand Total (A+B+C+D+E+F) 184667

198530 13863 7.51 245582 2,62,316 16,734 6.81

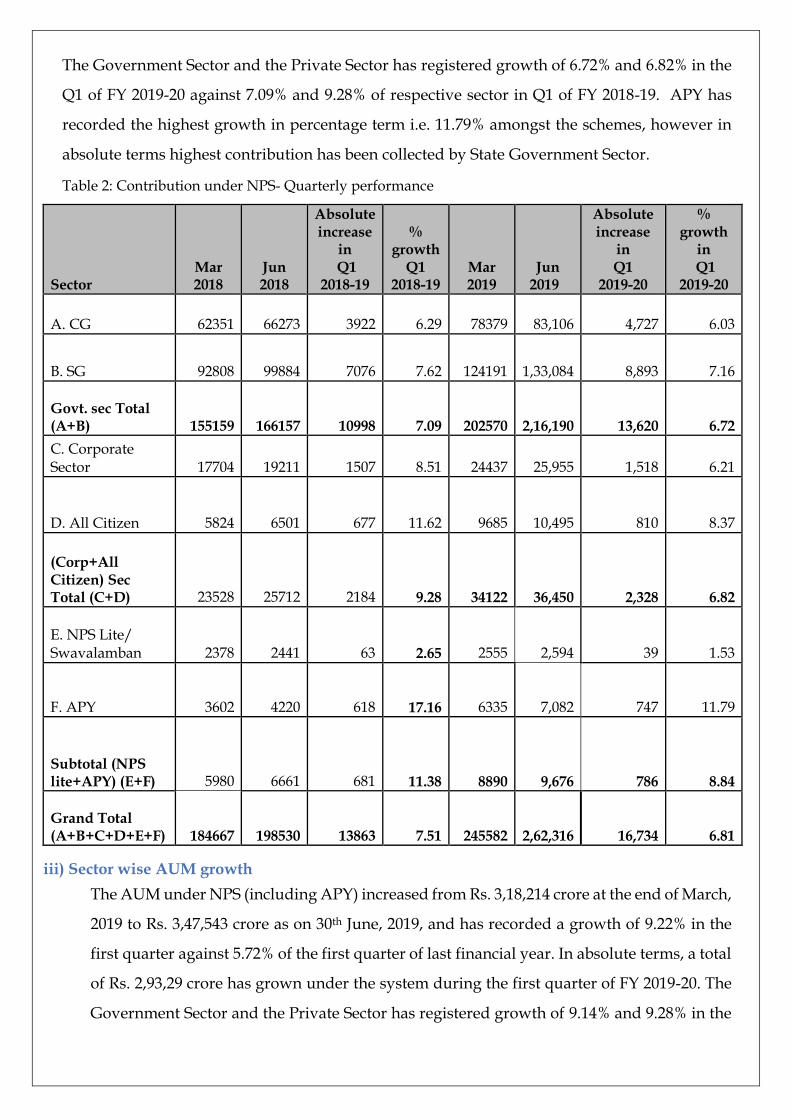

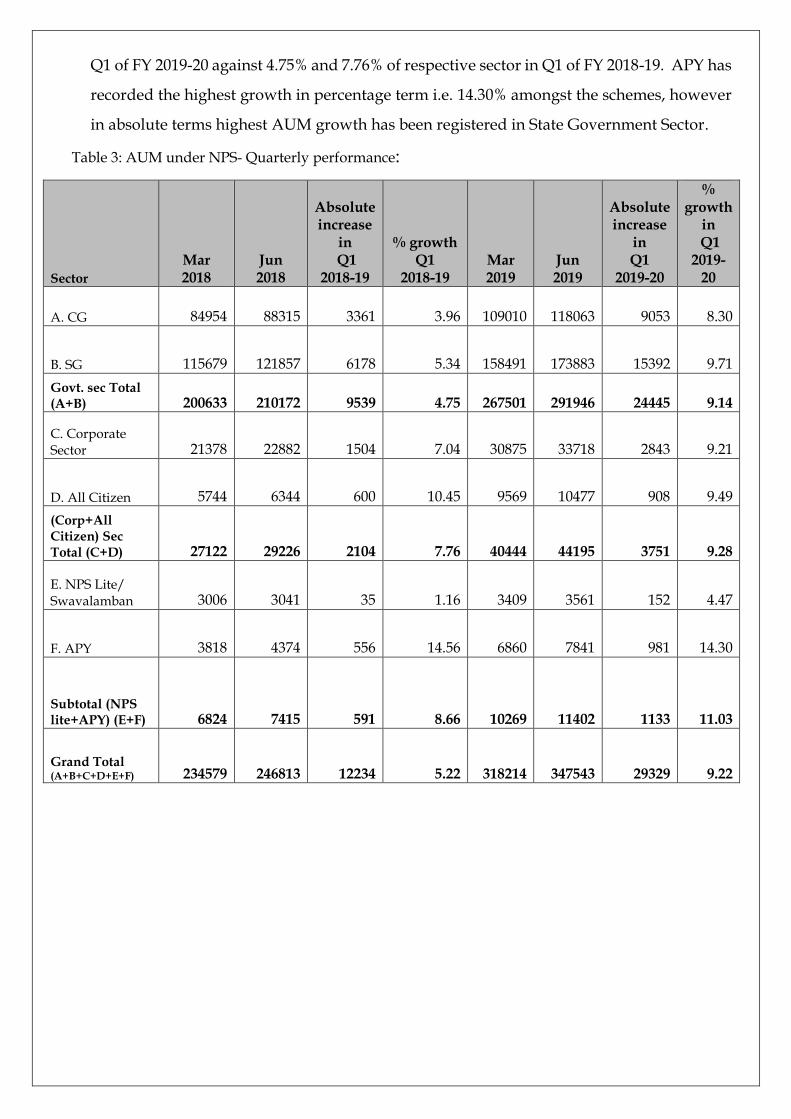

iii) Sector wise AUM growth

The AUM under NPS (including APY) increased from Rs. 3,18,214 crore at the end of March,

2019 to Rs. 3,47,543 crore as on 30th June, 2019, and has recorded a growth of 9.22% in the

first quarter against 5.72% of the first quarter of last financial year. In absolute terms, a total

of Rs. 2,93,29 crore has grown under the system during the first quarter of FY 2019-20. The

Government Sector and the Private Sector has registered growth of 9.14% and 9.28% in the

Q1 of FY 2019-20 against 4.75% and 7.76% of respective sector in Q1 of FY 2018-19. APY has

recorded the highest growth in percentage term i.e. 14.30% amongst the schemes, however

in absolute terms highest AUM growth has been registered in State Government Sector.

Table 3: AUM under NPS- Quarterly performance:

Sector

Mar 2018

Jun 2018

Absolute increase

in Q1

2018-19

% growth Q1

2018-19

Mar 2019

Jun 2019

Absolute increase

in Q1

2019-20

% growth

in Q1

2019-20

A. CG 84954 88315 3361 3.96 109010 118063 9053 8.30

B. SG 115679 121857 6178 5.34 158491 173883 15392 9.71

Govt. sec Total (A+B) 200633 210172 9539 4.75 267501 291946 24445 9.14

C. Corporate Sector 21378 22882 1504 7.04 30875 33718 2843 9.21

D. All Citizen 5744 6344 600 10.45 9569 10477 908 9.49

(Corp+All Citizen) Sec Total (C+D)

27122

29226 2104 7.76 40444 44195 3751 9.28

E. NPS Lite/ Swavalamban 3006 3041 35 1.16 3409 3561 152 4.47

F. APY 3818 4374 556 14.56 6860 7841 981 14.30

Subtotal (NPS lite+APY) (E+F)

6824

7415 591 8.66 10269 11402 1133 11.03

Grand Total (A+B+C+D+E+F)

234579

246813 12234 5.22 318214 347543 29329 9.22

Section 3 : In The NEWS

The PFRDA has also requested to

make the National Pension System

more tax-friendly by allowing tax

exemption for 60% of the corpus that

an investor withdraws on maturity,

instead of the current 40% limit

The Pension Fund Regulatory and Development Authority (PFRDA) has requested the Central Board of

Direct Taxes (CBDT) to allow companies and state governments to allocate 14% for employees’ pension

fund scheme, in-line with the change made for central government employees in April, the Times of

India said in a report. Government's contribution to central government employees' pension fund was

increased from 10% to 14% in April 2019.

“This will be a win-win move for both the parties, as employees will get a tax break and employers will

account it as business expenditure,” the ToI report quoted PFRDA whole-time member (finance)

Supratim Bandopadhyay as saying. He added that a target of 65-75 lakh new subscribers to pension

funds has been set for the coming year.

(https://www.timesnownews.com/business-economy/economy/article/budget-2019-

pfrda-proposes-increase-in-state-govts-companies-contribution-to-pension-fund/430195)

Paytm Money to allow users to invest in National Pension System on its platform The company aims to offer NPS services (both Tier 1 and Tier 2 accounts) from all the

eight major Pension Fund Managers on the platform.

Online mutual fund investments platform, Paytm Money, which is a wholly owned subsidiary of One97

Communications Limited (the company that owns and operates Paytm), on Wednesday said that it has

received the approval to offer National Pension System (NPS) on its platform from the Pension Fund

Regulatory and Development Authority (PFRDA). With this service, investors registered

with Paytm Money will be able to invest in NPS within minutes. The company aims to offer NPS

services (both Tier 1 and Tier 2 accounts) from all the eight major Pension Fund Managers on the

platform. Paytm Money plans to offer end to end digital and paperless experience for NPS investing.

With NPS, investors on Paytm Money platform will be eligible for additional deduction of taxable

income up to Rs. 50,000 under Section 80 CCD (1B) over and above the ceiling of Rs. 1.5 lakh under

Budget 2019: PFRDA proposes increase in state govts', companies' contribution to pension fund

the Section 80C. “National Pension Scheme (NPS) is a perfect solution for retirement planning and we

are excited about bringing convenience of digital and paperless NPS investing to users of Paytm Money.

Investors can also avail additional annual tax benefits every year with this along with investing for

retirement. We expect to go live with NPS investing soon.” said Pravin Jadhav, Whole-time Director

of Paytm Money.

(https://yourstory.com/2019/06/paytm-money-national-pension-system-mutual-funds)

Viewpoint | NPS sets the example for retirement plans globally

Voluntary retirement plans can provide security and stability for older people who no longer have a

steady paycheck—and India's National Pension System (NPS) aims to do just that. Like most of the

world, India's population is aging, and lifespans are increasing. As a result of improved health and

sanitation conditions, the global life expectancy is forecast to increase from an average of 65 years in

1990 to 77 years by 2050.

For most people, living longer means more non-working years to enjoy. But for growing numbers of

people around the world, generating enough income to live comfortably during those non-working years

is expected to be a challenge. Not only are many older people no longer earning income, but as the years

advance, the cost of living and inflation continue to increase. As government leaders around the world

consider ways to help citizens prepare for retirement, they can look to India's NPS as a model for

boosting retirement savings and helping aging workers avoid poverty during old age.

(https://www.moneycontrol.com/news/business/personal-finance/nps-sets-the-example-for-

retirement-plans-globally-4092271.html )

Atal Pension Yojana online: Now subscribe to APY as an Airtel Payments Bank account holder Airtel Payments Bank has launched ‘Atal Pension Yojana’ for its

savings account holders and has become the first payments bank in

India to offer Government of India backed Atal Pension Yojana.

To join and contribute to the Atal Pension Yojana (APY), a government-sponsored pension plan is all

the more easier and simpler now. Airtel Payments Bank has launched ‘Atal Pension Yojana’ for its

savings account holders and has become the first payments bank in India to offer Government of India

backed Atal Pension Yojana. APY is administered by the Pension Fund Regulatory and Development

Authority (PFRDA). If you are already an Airtel Payments Bank savings account holder, then, according

to the company, the subscription to APY may be done through a simple, secure and paperless process

that will take only a few minutes at 50,000 banking points across India. Going forward, Airtel Payments

Bank aims to expand the availability of the scheme at 100,000 of its banking points.An initiative by the

Government of India; Atal Pension Yojana is primarily aimed at providing pension benefits and social

security for workers in the unorganized sector. To contribute towards APY, one needs to mandatorily

have a savings bank account as the future contributions need to be debited automatically from the

account.

(https://www.financialexpress.com/money/atal-pension-yojana-now-subscribe-to-apy-as-an-airtel-

payments-bank-account-holder/1613530/ )

How to avail up to Rs 2 lakh income tax deduction through National Pension System (NPS)

Over the last 10 years, NPS funds have delivered a higher return than

Employees' Provident Fund (EPF)

National Pension Scheme (NPS) was launched in January 2004 for Central government employees, with

the exception of armed forces. Most of the state governments also made this retirement saving available

for their new entrants. Later in 2009, this retirement savings scheme was made available to all sections

of the society, even for NRIs.In this scheme, a subscriber can contribute regularly during his working

life and withdraw 60% the corpus (tax-free) in lump sum after retirement and invest the remaining 40%

corpus to buy an annuity to create a regular source of income for him. The government has also been

making changes in the scheme regularly to make it more attractive for people. According to an earlier

report in the Hindu Business Line, government employees who opted for NPS are now better of than

Employees' Provident Fund (EPFO) subscribers as the schemes earmarked for Central (Scheme-CG) and

state government employees (Scheme-SG) have delivered a higher return than EPFO.

(https://www.timesnownews.com/business-economy/personal-finance/planning-

investing/article/how-to-avail-up-to-rs-2-lakh-income-tax-deduction-through-national-

pension-system-nps/444558 )

Section 4: Annuity under NPS

Annuity under NPS

NPS offers financial independence post retirement. It is a contributory pension scheme introduced

in 2004 for Central Government employees, replacing the old pension schemes. Subsequently, it was

opened up to corporate employees and unorganized sector. The scheme is designed in such a way

that subscribers can receive pension post exit from the scheme. This pension received is termed as

‘Annuity’. This section seeks to cover the following details regarding purchase of annuity from NPS.

1. Details pertaining to exit

2. Types of exits

3. Annuity Service Providers

4. Process for exit and application for annuity

5. Details of pension estimation

Annuity in the context of NPS refers to the payment that will be received by the subscriber from the

Annuity Service Provider after his exit from NPS. For government employees, the frequency of

annuity payment is monthly, while non-government sector (i.e. corporate and unorganized sectors)

have the flexibility to opt for half yearly, quarterly and annual mode of receipt of annuity in addition

to monthly mode.

At the time of exit, subscribers have the choice of deferment of annuity and lump sum withdrawal

subject to the below mentioned conditions.

1. Withdrawal of lump sum payout and deferment of annuity: In this case, subscribers can withdraw

the corpus amount as per eligibility and defer the pension from annuity service providers.

2. Initiation of annuity payouts and deferment of lump sum withdrawal: This scenario pertains to

cases where the lump sum withdrawal is being deferred to a certain age. However, there shall be no

deferment of annuity payments and subscribers shall be eligible to receive annuity immediately.

3. Initiation of lump sum withdrawal and annuity immediately: In this scenario, subscribers opt to

withdraw their lump sum and begin their annuity immediately

4. Deferment of annuity and lump sum withdrawal: Here, the subscribers opt to defer their annuity

as well as lump sum withdrawal and choose to continue investing in the scheme.

As notified in the Pension Fund Regulatory & Development Authority (PFRDA) Regulations, 2015

on Exit/Withdrawal from NPS, exit will happen under NPS upon retirement, resignation or death

of the subscriber (once the PRAN become an IRA compliant), as per details given below.

a. Upon normal superannuation (retirement): Minimum 40% of the accumulated pension wealth

of the subscriber needs to be utilized for purchase of an annuity providing monthly pension to the

subscriber and balance is paid as lump sum payment to the subscriber. However, in case of

superannuation, a subscriber can claim 100% withdrawal if the total accumulated pension wealth is

less than Rupees Two Lakhs at the time of Superannuation/attaining age of 60 years.

b. Exit from NPS before the age of normal superannuation (Pre-mature Exit): At least 80% of the

accumulated pension wealth of the subscriber needs to be utilized for purchase of an annuity

providing monthly pension to the subscriber and balance 20% is paid as lump sum payment to the

subscriber. If the accumulated pension wealth of the subscriber is equal to or less than Rupees One

Lakh, such subscriber shall have the option to withdraw the entire accumulated pension wealth

without purchasing any annuity and upon exercise of this option the right of the subscriber to

receive any pension or other amount under NPS shall extinguish.

c. Upon Death: At present, as per PFRDA circular dated March 10, 2016 (PFRDA/2016/5/Exits/01)

in case of Government subscribers upon death the entire accumulated pension wealth (100%) would

be paid to the nominee/ legal heir of the subscriber and there would not be any purchase of annuity

/ monthly pension.

I. As per the rules of the scheme, regardless of the type of exit, pension can be taken from any of the

annuity service providers.

Annuity Service Providers are IRDAI registered insurance companies empaneled by PFRDA for

providing of Annuity Services to NPS subscribers upon their exit from the system. ASPs will be

responsible for managing the funds (allocated for buying annuity) and payment of the pension.

Pension Fund Regulatory and Development Authority (PFRDA) has empaneled the following eight

IRDAI approved life insurance companies for providing annuity services to the subscribers of

National Pension System (NPS).

a. HDFC Standard Life Insurance Co. Ltd.

b. Life Insurance Corporation of India

c. SBI Life Insurance Co. Ltd.

d. ICICI Prudential Life Insurance Co. Ltd.

e. Star Union Dai-ichi Life Insurance Co. Ltd.

f. Edelweiss Tokio Life Insurance Company Limited

g. Bajaj Allianz Life Insurance

h. India First Life Insurance Company

Annuity Options : The following are the most common annuity options available to subscriber

under NPS.

a. Annuity for Life: The option pays annuity until for the life of annuitant.

b. Annuity for Life with return of purchase price on death

The option pays annuity (monthly pension) for the life of annuitant and the purchase price is

returned to the nominee.

c. Annuity payable for Life with 100% annuity payable to spouse on death of annuitant

Annuity / monthly pension are paid during the lifetime of Annuitant. On death of the Annuitant,

monthly pension is paid during the life span of Spouse of the Annuitant. On death of the Spouse,

the payment of annuity ceases

f. Annuity for life with a provision of 100% of the annuity payable to spouse during his/her lifetime

on death of the annuitant:

Payment of annuity ceases after death of the annuitant and full annuity is payable to the surviving

named spouse during his/her lifetime. If the spouse predeceases the annuitant, the annuity ceases

after death of the annuitant. It can be with or without return of purchase price.

g. NPS – Family Income Option :

Under this option, the annuity benefit would be payable in accordance with the regulations as

prescribed by Pension Fund Regulatory and Development Authority (PFRDA). As per current

regulations, the annuity benefit will be payable for life of the subscriber and his/her spouse as per

the annuity option “Joint Life Last Survivor with Return of Purchase Price”. In case, the subscriber

does not have a spouse, the annuity benefit will be payable for life of the subscriber as per the

annuity option “Life Annuity with Return of Purchase Price”. In case of demise of the subscriber

before the vesting of the annuity, the annuity benefits will be payable for life of the spouse as per

the annuity option “Life Annuity with Return of Purchase Price”. On death of the annuitant (s), the

annuity payment would cease and refund of the purchase price shall be utilized to purchase an

annuity contract afresh for living dependent parents (if any) as per the order specified below.

a) Living dependent mother of the deceased subscriber

b) Living dependent father of the deceased subscriber

However, the annuity amount would be revised and determined as per the annuity option “Life

Annuity with Return of Purchase Price” using the annuity rate prevalent at the time of purchase of

such annuity by utilizing the Purchase Price required to be refunded to the nominee under the

annuity contract. The annuity would continue until all such family members in the order specified

above are covered. After the coverage of all such family members, the Purchase Price shall be

returned to the surviving children of the subscriber and in the absence of the children, the legal heirs

of the subscriber, as may be applicable. In case no such family member exists upon the death of the

last survivor, there would be a refund of the Purchase Price to the nominee.

While the above are the most common options of annuity , subscribers can also check with the

empaneled Annuity Service Providers on other options which are approved for sale by PFRDA.

Exit formalities to be followed by subscribers:

On exit from NPS scheme, the subscribers are to submit relevant documentation to their Nodal

Officers or POPs with their choice of Annuity Service Providers. They have the choice of 2 modes of

completing the exit formalities:

1. Online mode: Subscribers can login to their NPS account through their CRA portal and complete

the exit formalities. The acknowledgement of the details post submission along with relevant

supporting documents has to be submitted to the Nodal Officers (for government sector) and POPs

(for all others)

2. Non online process: Hard copy of the withdrawal forms can be downloaded from the CRA’s

website and has to be submitted with all the details and supporting documents to the Nodal Officers

(for government sector) and POPs (for all others). In this case, the Nodal Officers / POPs shall

capture the request in the system on behalf of the subscribers. After their Nodal officers / POPs

authorize the request, the subscribers can approach the empaneled annuity service providers for

pension. Alternately, even the Annuity Service Provider chosen in the exit forms shall also be

intimated by the respective CRAs along with the subscribers’ details. Contact details of the Nodal

Offices / POPs can be obtained from the CRAs.

It is but natural to want to know the approximate pension which can be received post exit. At any

point of time, subscribers under NPS can refer to the Pension Calculator for an estimation of possible

pension. A Subscriber can calculate approximate pension receivable under NPS by using Pension

Calculator available on NPS Trust website (http://www.npstrust.org.in/content/pension-

calculator). This pension calculator illustrates the tentative Pension and Lump Sum amount an NPS

Subscriber may expect on maturity or 60 years of age based on regular monthly contributions,

percentage of corpus reinvested for purchasing annuity and assumed rates in respect of returns on

investment and annuity selected.

Subscribers can also visit website (https://cra-nsdl.com/CRAOnline/aspQuote.html) to know the

annuity rates of Annuity service providers.

However, since annuity rates are subject to change without any prior intimation and are at the

descriptions of the Annuity Service Providers, it is always advisable to check with the empaneled

annuity service providers for accurate quotes.

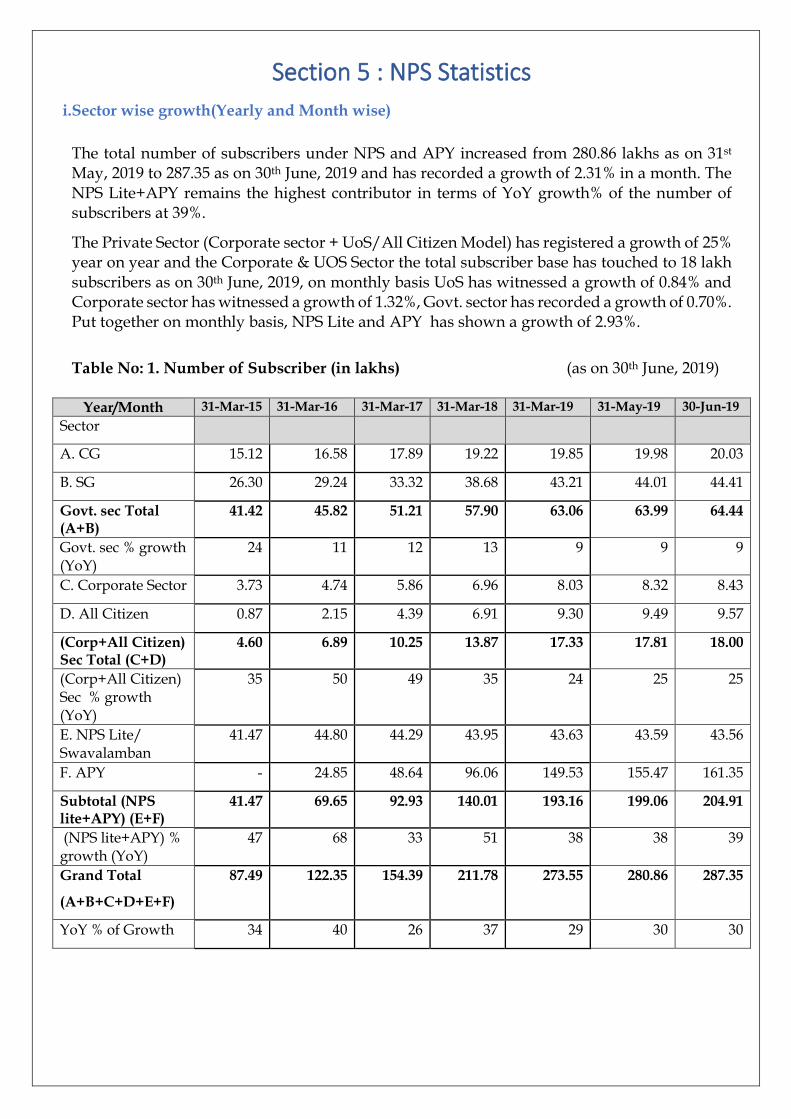

Section 5 : NPS Statistics

i.Sector wise growth(Yearly and Month wise)

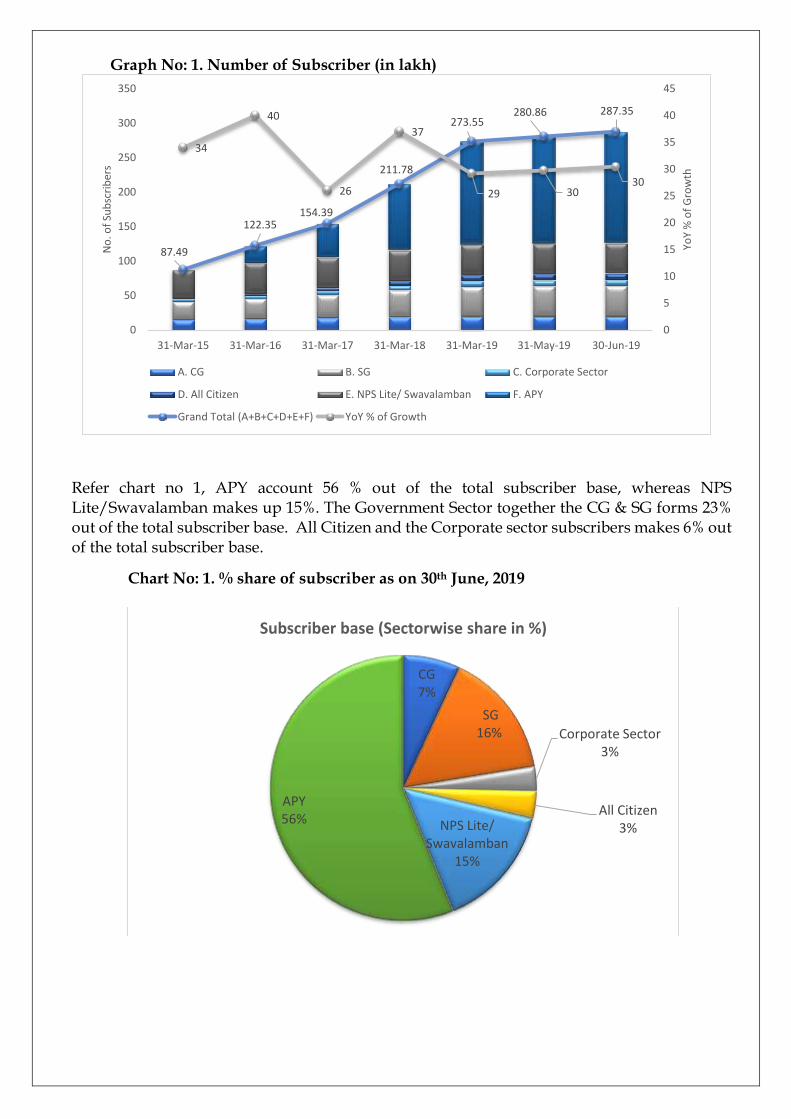

The total number of subscribers under NPS and APY increased from 280.86 lakhs as on 31st May, 2019 to 287.35 as on 30th June, 2019 and has recorded a growth of 2.31% in a month. The NPS Lite+APY remains the highest contributor in terms of YoY growth% of the number of subscribers at 39%.

The Private Sector (Corporate sector + UoS/All Citizen Model) has registered a growth of 25% year on year and the Corporate & UOS Sector the total subscriber base has touched to 18 lakh subscribers as on 30th June, 2019, on monthly basis UoS has witnessed a growth of 0.84% and Corporate sector has witnessed a growth of 1.32%, Govt. sector has recorded a growth of 0.70%. Put together on monthly basis, NPS Lite and APY has shown a growth of 2.93%.

Table No: 1. Number of Subscriber (in lakhs) (as on 30th June, 2019)

Year/Month 31-Mar-15 31-Mar-16 31-Mar-17 31-Mar-18 31-Mar-19 31-May-19 30-Jun-19

Sector

A. CG 15.12 16.58 17.89 19.22 19.85 19.98 20.03

B. SG 26.30 29.24 33.32 38.68 43.21 44.01 44.41

Govt. sec Total (A+B)

41.42 45.82 51.21 57.90 63.06 63.99 64.44

Govt. sec % growth (YoY)

24 11 12 13 9 9 9

C. Corporate Sector 3.73 4.74 5.86 6.96 8.03 8.32 8.43

D. All Citizen 0.87 2.15 4.39 6.91 9.30 9.49 9.57

(Corp+All Citizen) Sec Total (C+D)

4.60 6.89 10.25 13.87 17.33 17.81 18.00

(Corp+All Citizen) Sec % growth (YoY)

35 50 49 35 24 25 25

E. NPS Lite/ Swavalamban

41.47 44.80 44.29 43.95 43.63 43.59 43.56

F. APY - 24.85 48.64 96.06 149.53 155.47 161.35

Subtotal (NPS lite+APY) (E+F)

41.47 69.65 92.93 140.01 193.16 199.06 204.91

(NPS lite+APY) % growth (YoY)

47 68 33 51 38 38 39

Grand Total

(A+B+C+D+E+F)

87.49 122.35 154.39 211.78 273.55 280.86 287.35

YoY % of Growth 34 40 26 37 29 30 30

Graph No: 1. Number of Subscriber (in lakh)

Refer chart no 1, APY account 56 % out of the total subscriber base, whereas NPS Lite/Swavalamban makes up 15%. The Government Sector together the CG & SG forms 23% out of the total subscriber base. All Citizen and the Corporate sector subscribers makes 6% out of the total subscriber base.

Chart No: 1. % share of subscriber as on 30th June, 2019

87.49

122.35154.39

211.78

273.55280.86 287.35

34

40

26

37

29 3030

0

5

10

15

20

25

30

35

40

45

0

50

100

150

200

250

300

350

31-Mar-15 31-Mar-16 31-Mar-17 31-Mar-18 31-Mar-19 31-May-19 30-Jun-19

YoY

% o

f G

row

th

No

. of

Sub

scri

ber

s

A. CG B. SG C. Corporate Sector

D. All Citizen E. NPS Lite/ Swavalamban F. APY

Grand Total (A+B+C+D+E+F) YoY % of Growth

CG7%

SG16% Corporate Sector

3%

All Citizen3%NPS Lite/

Swavalamban15%

APY56%

Subscriber base (Sectorwise share in %)

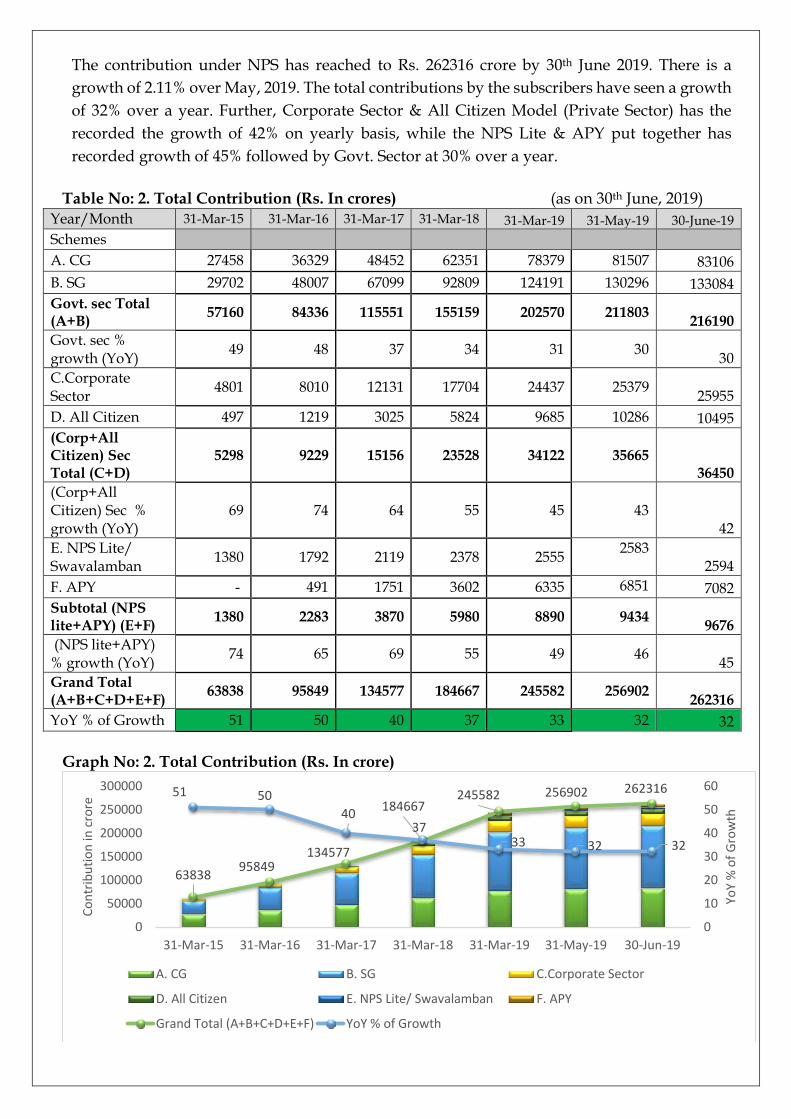

The contribution under NPS has reached to Rs. 262316 crore by 30th June 2019. There is a

growth of 2.11% over May, 2019. The total contributions by the subscribers have seen a growth

of 32% over a year. Further, Corporate Sector & All Citizen Model (Private Sector) has the

recorded the growth of 42% on yearly basis, while the NPS Lite & APY put together has

recorded growth of 45% followed by Govt. Sector at 30% over a year.

Table No: 2. Total Contribution (Rs. In crores) (as on 30th June, 2019)

Year/Month 31-Mar-15 31-Mar-16 31-Mar-17 31-Mar-18 31-Mar-19 31-May-19 30-June-19

Schemes

A. CG 27458 36329 48452 62351 78379 81507 83106

B. SG 29702 48007 67099 92809 124191 130296 133084

Govt. sec Total (A+B)

57160 84336 115551 155159 202570 211803 216190

Govt. sec % growth (YoY)

49 48 37 34 31 30 30

C.Corporate Sector

4801 8010 12131 17704 24437 25379 25955

D. All Citizen 497 1219 3025 5824 9685 10286 10495

(Corp+All Citizen) Sec Total (C+D)

5298 9229 15156 23528 34122 35665 36450

(Corp+All Citizen) Sec % growth (YoY)

69 74 64 55 45

43 42

E. NPS Lite/ Swavalamban

1380 1792 2119 2378 2555 2583

2594

F. APY - 491 1751 3602 6335 6851 7082

Subtotal (NPS lite+APY) (E+F)

1380 2283 3870 5980 8890 9434 9676

(NPS lite+APY) % growth (YoY)

74 65 69 55 49 46 45

Grand Total (A+B+C+D+E+F)

63838 95849 134577 184667 245582 256902 262316

YoY % of Growth 51 50 40 37 33 32 32

Graph No: 2. Total Contribution (Rs. In crore)

6383895849

134577

184667245582 256902 26231651 50

4037

33 32 32

0

10

20

30

40

50

60

0

50000

100000

150000

200000

250000

300000

31-Mar-15 31-Mar-16 31-Mar-17 31-Mar-18 31-Mar-19 31-May-19 30-Jun-19

YoY

% o

f G

row

th

Co

ntr

ibu

tio

n in

cro

re

A. CG B. SG C.Corporate Sector

D. All Citizen E. NPS Lite/ Swavalamban F. APY

Grand Total (A+B+C+D+E+F) YoY % of Growth

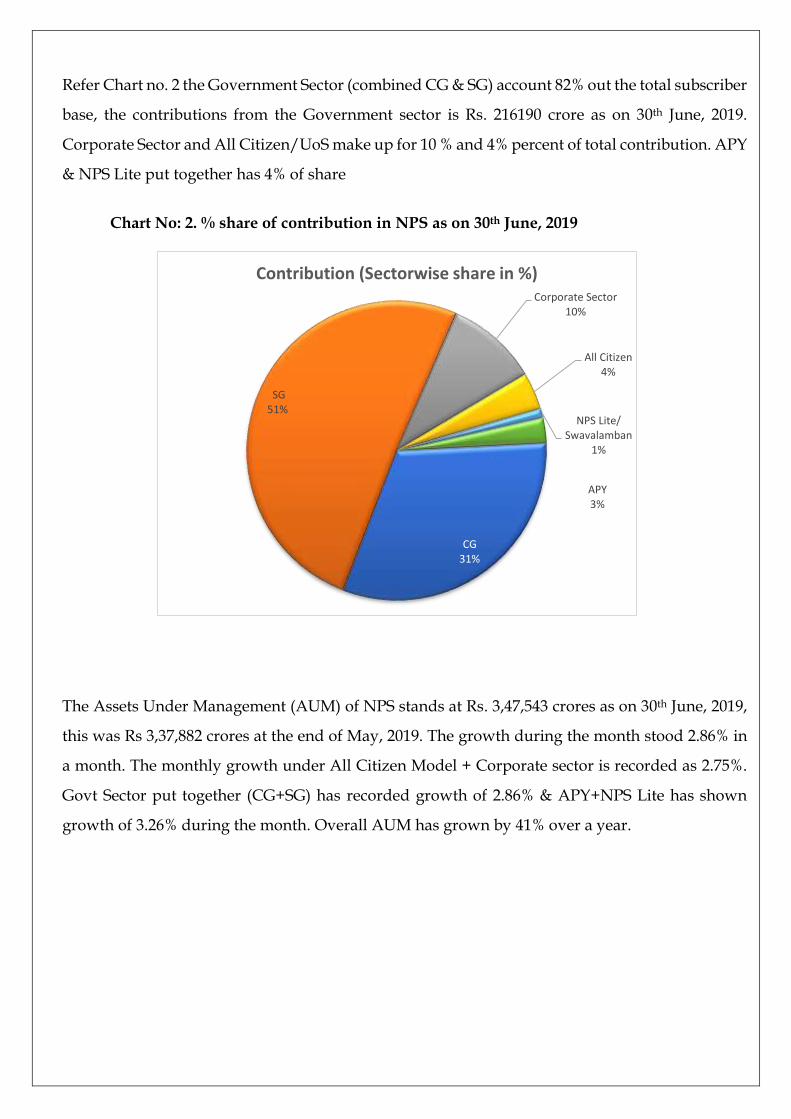

Refer Chart no. 2 the Government Sector (combined CG & SG) account 82% out the total subscriber

base, the contributions from the Government sector is Rs. 216190 crore as on 30th June, 2019.

Corporate Sector and All Citizen/UoS make up for 10 % and 4% percent of total contribution. APY

& NPS Lite put together has 4% of share

Chart No: 2. % share of contribution in NPS as on 30th June, 2019

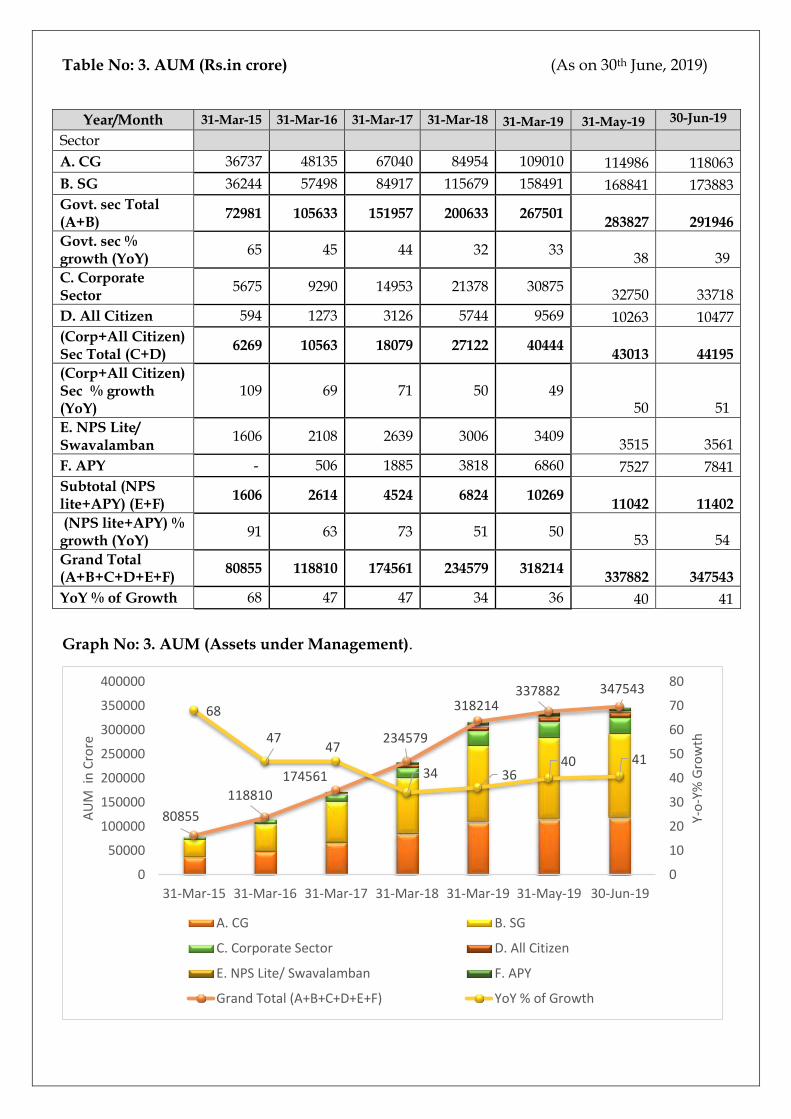

The Assets Under Management (AUM) of NPS stands at Rs. 3,47,543 crores as on 30th June, 2019,

this was Rs 3,37,882 crores at the end of May, 2019. The growth during the month stood 2.86% in

a month. The monthly growth under All Citizen Model + Corporate sector is recorded as 2.75%.

Govt Sector put together (CG+SG) has recorded growth of 2.86% & APY+NPS Lite has shown

growth of 3.26% during the month. Overall AUM has grown by 41% over a year.

CG31%

SG51%

Corporate Sector10%

All Citizen4%

NPS Lite/ Swavalamban

1%

APY3%

Contribution (Sectorwise share in %)

Table No: 3. AUM (Rs.in crore) (As on 30th June, 2019)

Graph No: 3. AUM (Assets under Management).

80855

118810

174561

234579

318214337882 347543

68

4747

34 3640 41

0

10

20

30

40

50

60

70

80

0

50000

100000

150000

200000

250000

300000

350000

400000

31-Mar-15 31-Mar-16 31-Mar-17 31-Mar-18 31-Mar-19 31-May-19 30-Jun-19

Y-o

-Y%

Gro

wth

AU

M i

n C

rore

A. CG B. SG

C. Corporate Sector D. All Citizen

E. NPS Lite/ Swavalamban F. APY

Grand Total (A+B+C+D+E+F) YoY % of Growth

Year/Month 31-Mar-15 31-Mar-16 31-Mar-17 31-Mar-18 31-Mar-19 31-May-19 30-Jun-19

Sector

A. CG 36737 48135 67040 84954 109010 114986 118063

B. SG 36244 57498 84917 115679 158491 168841 173883

Govt. sec Total (A+B)

72981 105633 151957 200633 267501 283827 291946

Govt. sec % growth (YoY)

65 45 44 32 33 38 39

C. Corporate Sector

5675 9290 14953 21378 30875 32750 33718

D. All Citizen 594 1273 3126 5744 9569 10263 10477

(Corp+All Citizen) Sec Total (C+D)

6269 10563 18079 27122 40444 43013 44195

(Corp+All Citizen) Sec % growth (YoY)

109 69 71 50 49 50 51

E. NPS Lite/ Swavalamban

1606 2108 2639 3006 3409 3515 3561

F. APY - 506 1885 3818 6860 7527 7841

Subtotal (NPS lite+APY) (E+F)

1606 2614 4524 6824 10269 11042 11402

(NPS lite+APY) % growth (YoY)

91 63 73 51 50 53 54

Grand Total (A+B+C+D+E+F)

80855 118810 174561 234579 318214 337882 347543

YoY % of Growth 68 47 47 34 36 40 41

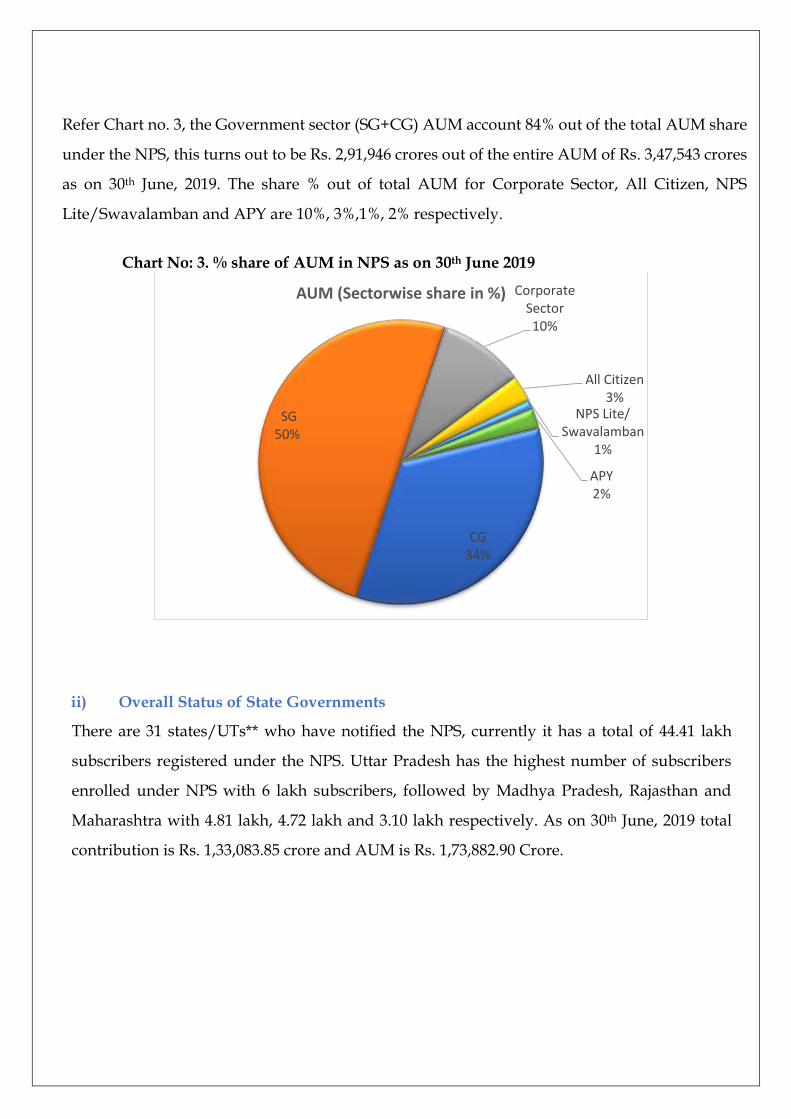

Refer Chart no. 3, the Government sector (SG+CG) AUM account 84% out of the total AUM share

under the NPS, this turns out to be Rs. 2,91,946 crores out of the entire AUM of Rs. 3,47,543 crores

as on 30th June, 2019. The share % out of total AUM for Corporate Sector, All Citizen, NPS

Lite/Swavalamban and APY are 10%, 3%,1%, 2% respectively.

Chart No: 3. % share of AUM in NPS as on 30th June 2019

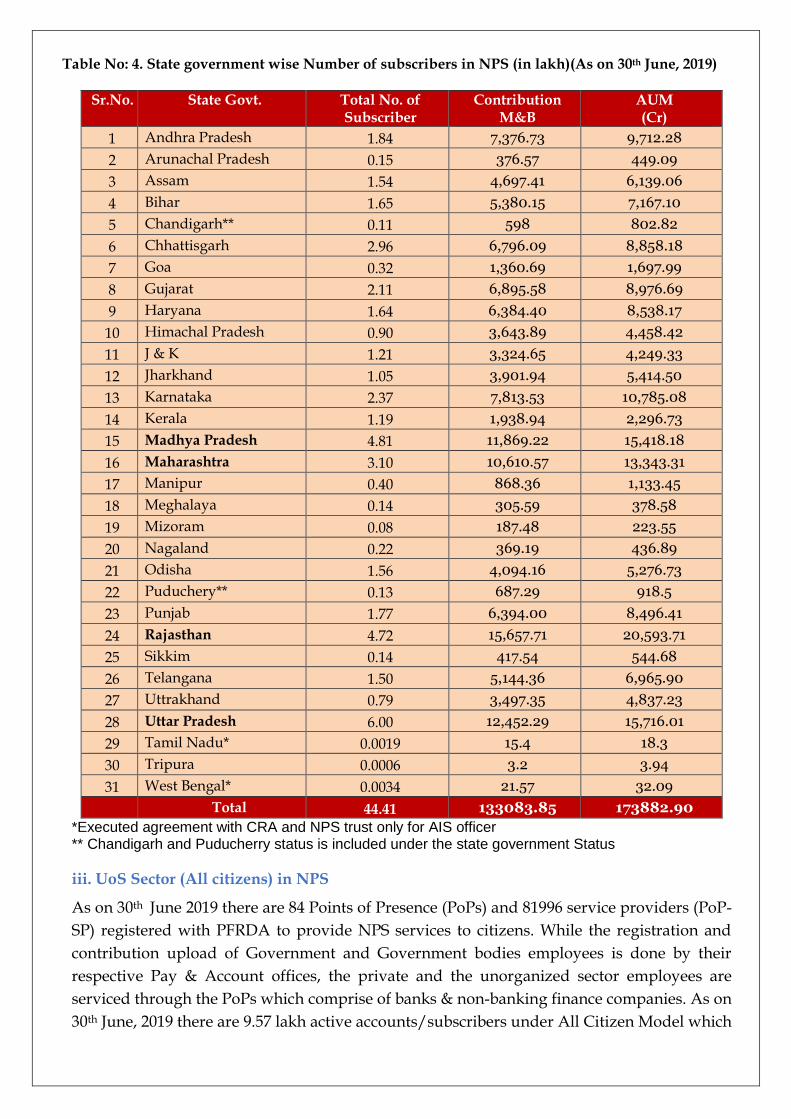

ii) Overall Status of State Governments

There are 31 states/UTs** who have notified the NPS, currently it has a total of 44.41 lakh

subscribers registered under the NPS. Uttar Pradesh has the highest number of subscribers

enrolled under NPS with 6 lakh subscribers, followed by Madhya Pradesh, Rajasthan and

Maharashtra with 4.81 lakh, 4.72 lakh and 3.10 lakh respectively. As on 30th June, 2019 total

contribution is Rs. 1,33,083.85 crore and AUM is Rs. 1,73,882.90 Crore.

CG34%

SG50%

Corporate Sector10%

All Citizen3%

NPS Lite/ Swavalamban

1%

APY2%

AUM (Sectorwise share in %)

Table No: 4. State government wise Number of subscribers in NPS (in lakh)(As on 30th June, 2019)

Sr.No. State Govt. Total No. of Subscriber

Contribution M&B

AUM (Cr)

1 Andhra Pradesh 1.84 7,376.73 9,712.28

2 Arunachal Pradesh 0.15 376.57 449.09

3 Assam 1.54 4,697.41 6,139.06

4 Bihar 1.65 5,380.15 7,167.10

5 Chandigarh** 0.11 598 802.82

6 Chhattisgarh 2.96 6,796.09 8,858.18

7 Goa 0.32 1,360.69 1,697.99

8 Gujarat 2.11 6,895.58 8,976.69

9 Haryana 1.64 6,384.40 8,538.17

10 Himachal Pradesh 0.90 3,643.89 4,458.42

11 J & K 1.21 3,324.65 4,249.33

12 Jharkhand 1.05 3,901.94 5,414.50

13 Karnataka 2.37 7,813.53 10,785.08

14 Kerala 1.19 1,938.94 2,296.73

15 Madhya Pradesh 4.81 11,869.22 15,418.18

16 Maharashtra 3.10 10,610.57 13,343.31

17 Manipur 0.40 868.36 1,133.45

18 Meghalaya 0.14 305.59 378.58

19 Mizoram 0.08 187.48 223.55

20 Nagaland 0.22 369.19 436.89

21 Odisha 1.56 4,094.16 5,276.73

22 Puduchery** 0.13 687.29 918.5

23 Punjab 1.77 6,394.00 8,496.41

24 Rajasthan 4.72 15,657.71 20,593.71

25 Sikkim 0.14 417.54 544.68

26 Telangana 1.50 5,144.36 6,965.90

27 Uttrakhand 0.79 3,497.35 4,837.23

28 Uttar Pradesh 6.00 12,452.29 15,716.01

29 Tamil Nadu* 0.0019 15.4 18.3

30 Tripura 0.0006 3.2 3.94

31 West Bengal* 0.0034 21.57 32.09

Total 44.41 133083.85 173882.90

*Executed agreement with CRA and NPS trust only for AIS officer ** Chandigarh and Puducherry status is included under the state government Status

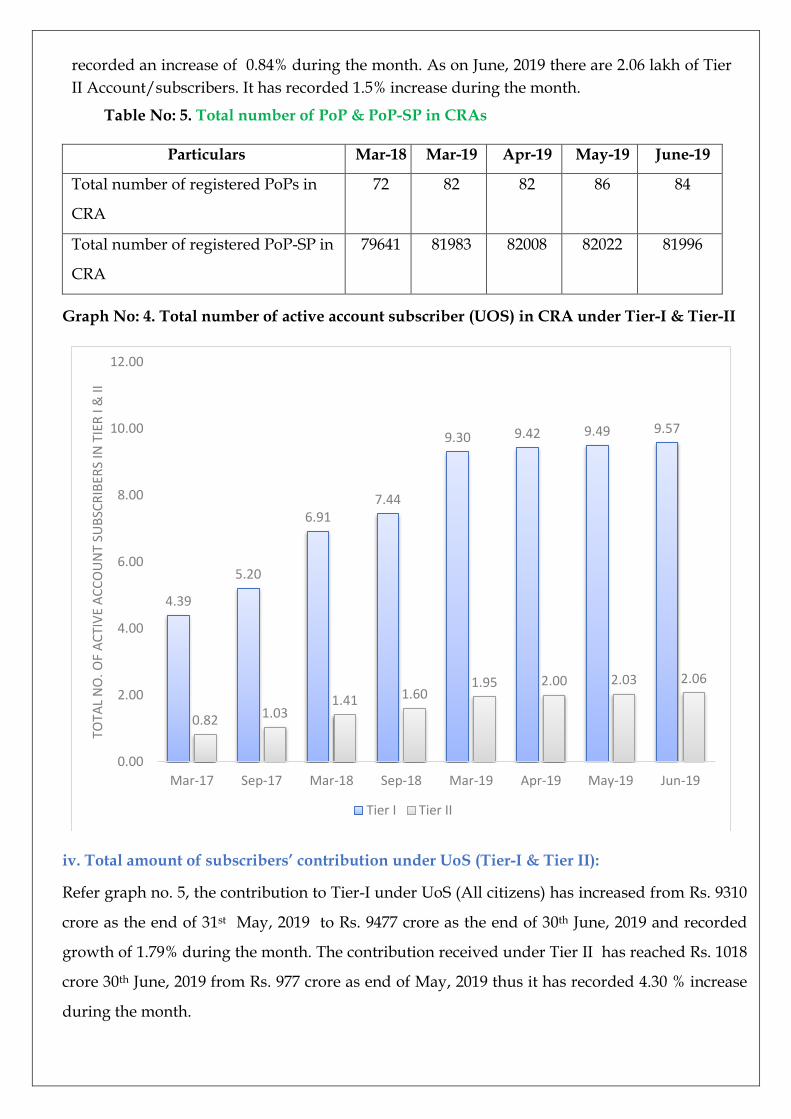

iii. UoS Sector (All citizens) in NPS

As on 30th June 2019 there are 84 Points of Presence (PoPs) and 81996 service providers (PoP-

SP) registered with PFRDA to provide NPS services to citizens. While the registration and

contribution upload of Government and Government bodies employees is done by their

respective Pay & Account offices, the private and the unorganized sector employees are

serviced through the PoPs which comprise of banks & non-banking finance companies. As on

30th June, 2019 there are 9.57 lakh active accounts/subscribers under All Citizen Model which

recorded an increase of 0.84% during the month. As on June, 2019 there are 2.06 lakh of Tier

II Account/subscribers. It has recorded 1.5% increase during the month.

Table No: 5. Total number of PoP & PoP-SP in CRAs

Particulars Mar-18 Mar-19 Apr-19 May-19 June-19

Total number of registered PoPs in

CRA

72 82 82 86 84

Total number of registered PoP-SP in

CRA

79641 81983 82008 82022 81996

Graph No: 4. Total number of active account subscriber (UOS) in CRA under Tier-I & Tier-II

iv. Total amount of subscribers’ contribution under UoS (Tier-I & Tier II):

Refer graph no. 5, the contribution to Tier-I under UoS (All citizens) has increased from Rs. 9310

crore as the end of 31st May, 2019 to Rs. 9477 crore as the end of 30th June, 2019 and recorded

growth of 1.79% during the month. The contribution received under Tier II has reached Rs. 1018

crore 30th June, 2019 from Rs. 977 crore as end of May, 2019 thus it has recorded 4.30 % increase

during the month.

4.39

5.20

6.917.44

9.30 9.42 9.49 9.57

0.82 1.031.41 1.60

1.95 2.00 2.03 2.06

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Apr-19 May-19 Jun-19

TOTA

L N

O. O

F A

CTI

VE

AC

CO

UN

T SU

BSC

RIB

ERS

IN T

IER

I &

II

Tier I Tier II

Graph No: 5. Contribution of subscribers under (UoS) in NPS under Tier-I &Tier-II (Rs. in crores)

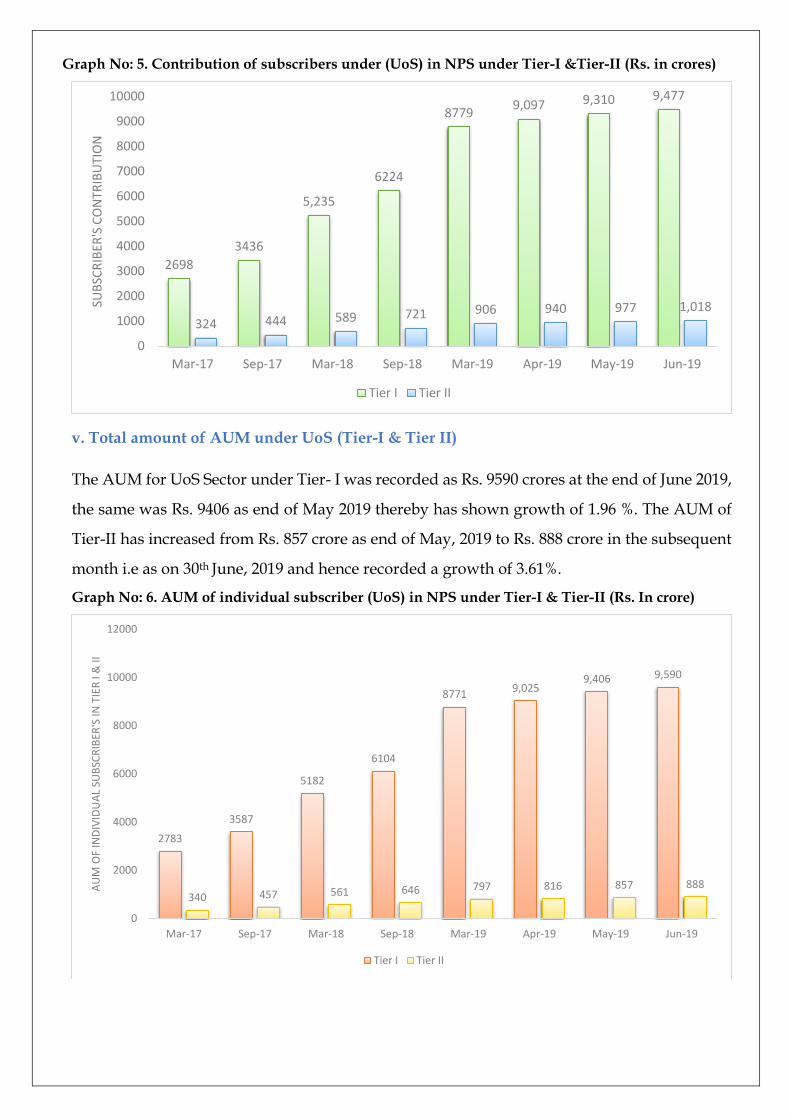

v. Total amount of AUM under UoS (Tier-I & Tier II)

The AUM for UoS Sector under Tier- I was recorded as Rs. 9590 crores at the end of June 2019,

the same was Rs. 9406 as end of May 2019 thereby has shown growth of 1.96 %. The AUM of

Tier-II has increased from Rs. 857 crore as end of May, 2019 to Rs. 888 crore in the subsequent

month i.e as on 30th June, 2019 and hence recorded a growth of 3.61%.

Graph No: 6. AUM of individual subscriber (UoS) in NPS under Tier-I & Tier-II (Rs. In crore)

2698

3436

5,235

6224

87799,097 9,310 9,477

324 444 589 721 906 940 977 1,018

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Apr-19 May-19 Jun-19

SUB

SCR

IBER

'S C

ON

TRIB

UTI

ON

Tier I Tier II

2783

3587

5182

6104

87719,025

9,406 9,590

340 457 561 646 797 816 857 888

0

2000

4000

6000

8000

10000

12000

Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Apr-19 May-19 Jun-19

AU

M O

F IN

DIV

IDU

AL

SUB

SCR

IBER

'S IN

TIE

R I

& II

Tier I Tier II

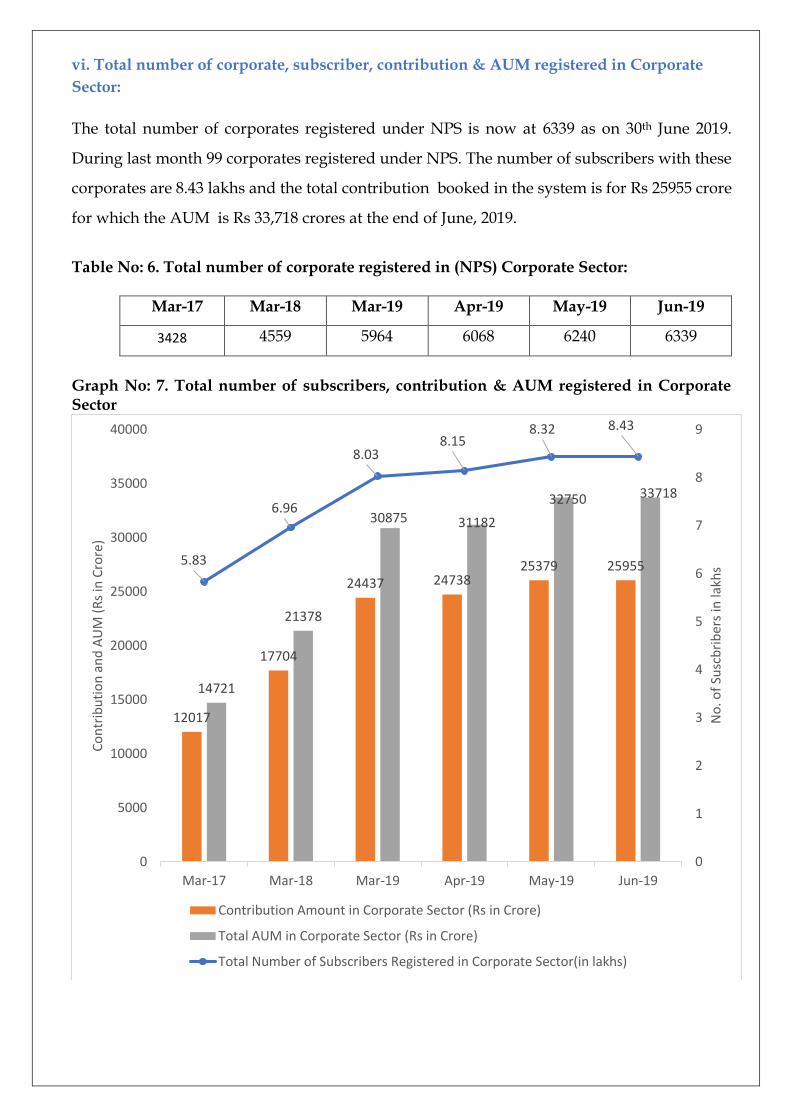

vi. Total number of corporate, subscriber, contribution & AUM registered in Corporate

Sector:

The total number of corporates registered under NPS is now at 6339 as on 30th June 2019.

During last month 99 corporates registered under NPS. The number of subscribers with these

corporates are 8.43 lakhs and the total contribution booked in the system is for Rs 25955 crore

for which the AUM is Rs 33,718 crores at the end of June, 2019.

Table No: 6. Total number of corporate registered in (NPS) Corporate Sector:

Mar-17 Mar-18 Mar-19 Apr-19 May-19 Jun-19

3428 4559 5964 6068 6240 6339

Graph No: 7. Total number of subscribers, contribution & AUM registered in Corporate Sector

12017

17704

24437 2473825379 25955

14721

21378

30875 31182

32750 33718

5.83

6.96

8.038.15

8.32 8.43

0

1

2

3

4

5

6

7

8

9

0

5000

10000

15000

20000

25000

30000

35000

40000

Mar-17 Mar-18 Mar-19 Apr-19 May-19 Jun-19

No

. of

Susc

bri

be

rs in

lakh

s

Co

ntr

ibu

tio

n a

nd

AU

M (

Rs

in C

rore

)

Contribution Amount in Corporate Sector (Rs in Crore)

Total AUM in Corporate Sector (Rs in Crore)

Total Number of Subscribers Registered in Corporate Sector(in lakhs)

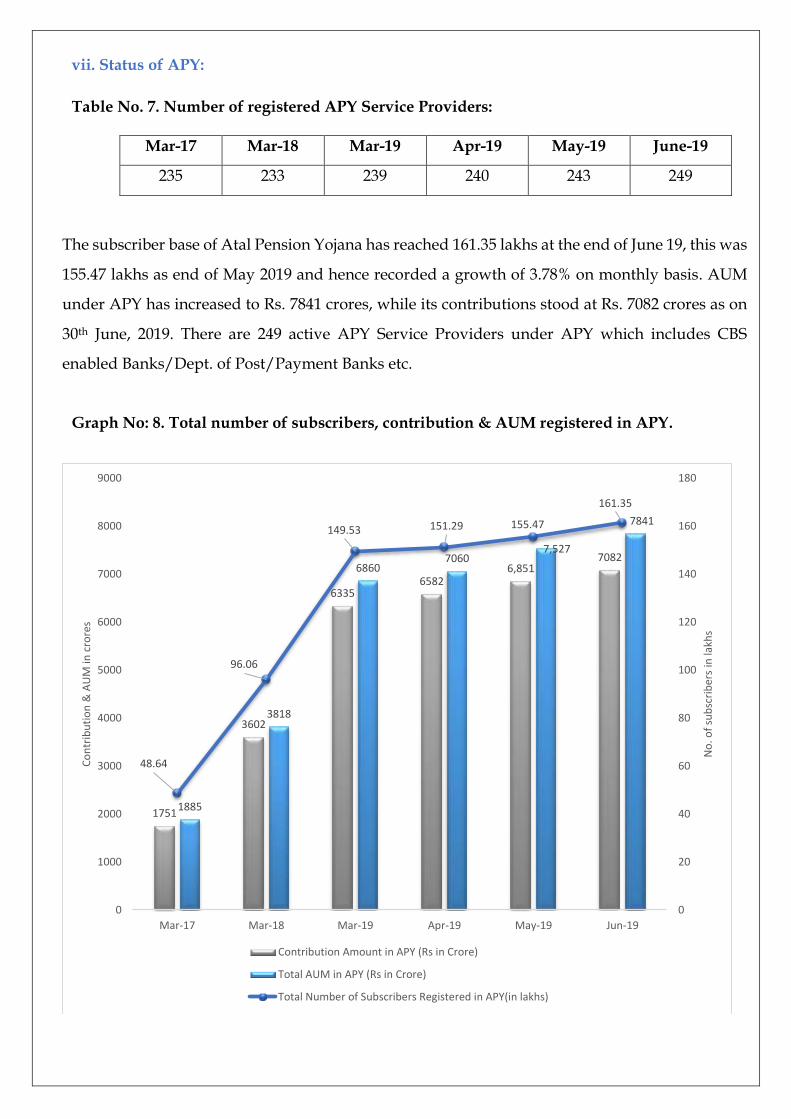

vii. Status of APY:

Table No. 7. Number of registered APY Service Providers:

Mar-17 Mar-18 Mar-19 Apr-19 May-19 June-19

235 233 239 240 243 249

The subscriber base of Atal Pension Yojana has reached 161.35 lakhs at the end of June 19, this was

155.47 lakhs as end of May 2019 and hence recorded a growth of 3.78% on monthly basis. AUM

under APY has increased to Rs. 7841 crores, while its contributions stood at Rs. 7082 crores as on

30th June, 2019. There are 249 active APY Service Providers under APY which includes CBS

enabled Banks/Dept. of Post/Payment Banks etc.

Graph No: 8. Total number of subscribers, contribution & AUM registered in APY.

1751

3602

63356582

6,8517082

1885

3818

68607060

7,527

7841

48.64

96.06

149.53 151.29 155.47

161.35

0

20

40

60

80

100

120

140

160

180

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

Mar-17 Mar-18 Mar-19 Apr-19 May-19 Jun-19

No

. of

sub

scri

ber

s in

lakh

s

Co

ntr

ibu

tio

n &

AU

M in

cro

res

Contribution Amount in APY (Rs in Crore)

Total AUM in APY (Rs in Crore)

Total Number of Subscribers Registered in APY(in lakhs)

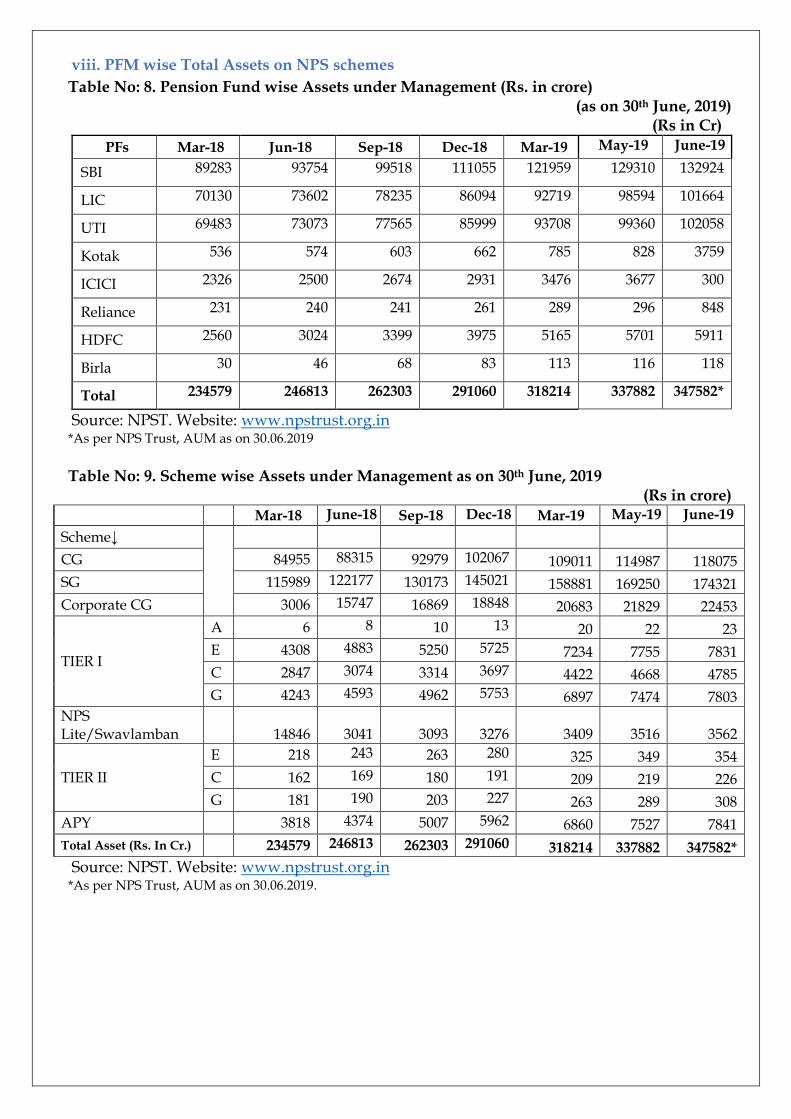

viii. PFM wise Total Assets on NPS schemes

Table No: 8. Pension Fund wise Assets under Management (Rs. in crore) (as on 30th June, 2019)

(Rs in Cr)

PFs Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 May-19 June-19

SBI 89283 93754 99518 111055 121959 129310 132924

LIC 70130 73602 78235 86094 92719 98594 101664

UTI 69483 73073 77565 85999 93708 99360 102058

Kotak 536 574 603 662 785 828 3759

ICICI 2326 2500 2674 2931 3476 3677 300

Reliance 231 240 241 261 289 296 848

HDFC 2560 3024 3399 3975 5165 5701 5911

Birla 30 46 68 83 113 116 118

Total 234579 246813 262303 291060 318214 337882 347582*

Source: NPST. Website: www.npstrust.org.in *As per NPS Trust, AUM as on 30.06.2019

Table No: 9. Scheme wise Assets under Management as on 30th June, 2019

(Rs in crore)

Mar-18 June-18 Sep-18 Dec-18 Mar-19 May-19 June-19

Scheme↓

CG 84955 88315 92979 102067 109011 114987 118075

SG 115989 122177 130173 145021 158881 169250 174321

Corporate CG 3006 15747 16869 18848 20683 21829 22453

TIER I

A 6 8 10 13 20 22 23

E 4308 4883 5250 5725 7234 7755 7831

C 2847 3074 3314 3697 4422 4668 4785

G 4243 4593 4962 5753 6897 7474 7803

NPS Lite/Swavlamban

14846

3041

3093

3276 3409 3516 3562

TIER II

E 218 243 263 280 325 349 354

C 162 169 180 191 209 219 226

G 181 190 203 227 263 289 308

APY 3818 4374 5007 5962 6860 7527 7841

Total Asset (Rs. In Cr.) 234579 246813 262303 291060 318214 337882 347582*

Source: NPST. Website: www.npstrust.org.in *As per NPS Trust, AUM as on 30.06.2019.

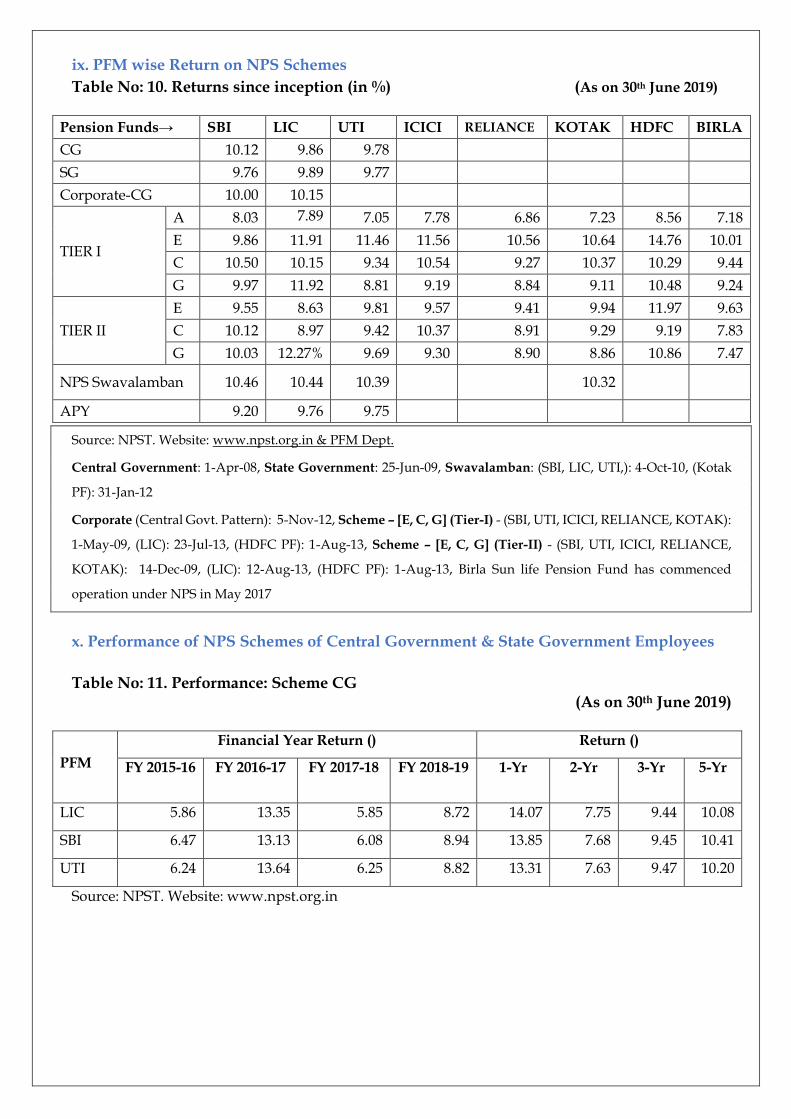

ix. PFM wise Return on NPS Schemes

Table No: 10. Returns since inception (in %) (As on 30th June 2019)

Pension Funds→ SBI LIC UTI ICICI RELIANCE KOTAK HDFC BIRLA

CG 10.12 9.86 9.78

SG 9.76 9.89 9.77

Corporate-CG 10.00 10.15

TIER I

A 8.03 7.89 7.05% 7.78% 6.86% 7.23% 8.56% 7.18%

7.05 7.78 6.86 7.23 8.56 7.18

E 9.86 11.91 11.46 11.56 10.56 10.64 14.76 10.01

C 10.50 10.15 9.34 10.54 9.27 10.37 10.29 9.44

G 9.97 11.92 8.81 9.19 8.84 9.11 10.48 9.24

TIER II

E 9.55 8.63 9.81 9.57 9.41 9.94 11.97 9.63

C 10.12 8.97 9.42 10.37 8.91 9.29 9.19 7.83

G 10.03 12.27% 9.69 9.30 8.90 8.86 10.86 7.47

NPS Swavalamban 10.46 10.44 10.39 10.32

APY 9.20 9.76 9.75

Source: NPST. Website: www.npst.org.in & PFM Dept.

Central Government: 1-Apr-08, State Government: 25-Jun-09, Swavalamban: (SBI, LIC, UTI,): 4-Oct-10, (Kotak

PF): 31-Jan-12

Corporate (Central Govt. Pattern): 5-Nov-12, Scheme – [E, C, G] (Tier-I) - (SBI, UTI, ICICI, RELIANCE, KOTAK):

1-May-09, (LIC): 23-Jul-13, (HDFC PF): 1-Aug-13, Scheme – [E, C, G] (Tier-II) - (SBI, UTI, ICICI, RELIANCE,

KOTAK): 14-Dec-09, (LIC): 12-Aug-13, (HDFC PF): 1-Aug-13, Birla Sun life Pension Fund has commenced

operation under NPS in May 2017

x. Performance of NPS Schemes of Central Government & State Government Employees

Table No: 11. Performance: Scheme CG

(As on 30th June 2019)

PFM

Financial Year Return () Return ()

FY 2015-16 FY 2016-17 FY 2017-18 FY 2018-19 1-Yr 2-Yr 3-Yr 5-Yr

LIC 5.86 13.35 5.85 8.72 14.07 7.75 9.44 10.08

SBI 6.47 13.13 6.08 8.94 13.85 7.68 9.45 10.41

UTI 6.24 13.64 6.25 8.82 13.31 7.63 9.47 10.20

Source: NPST. Website: www.npst.org.in

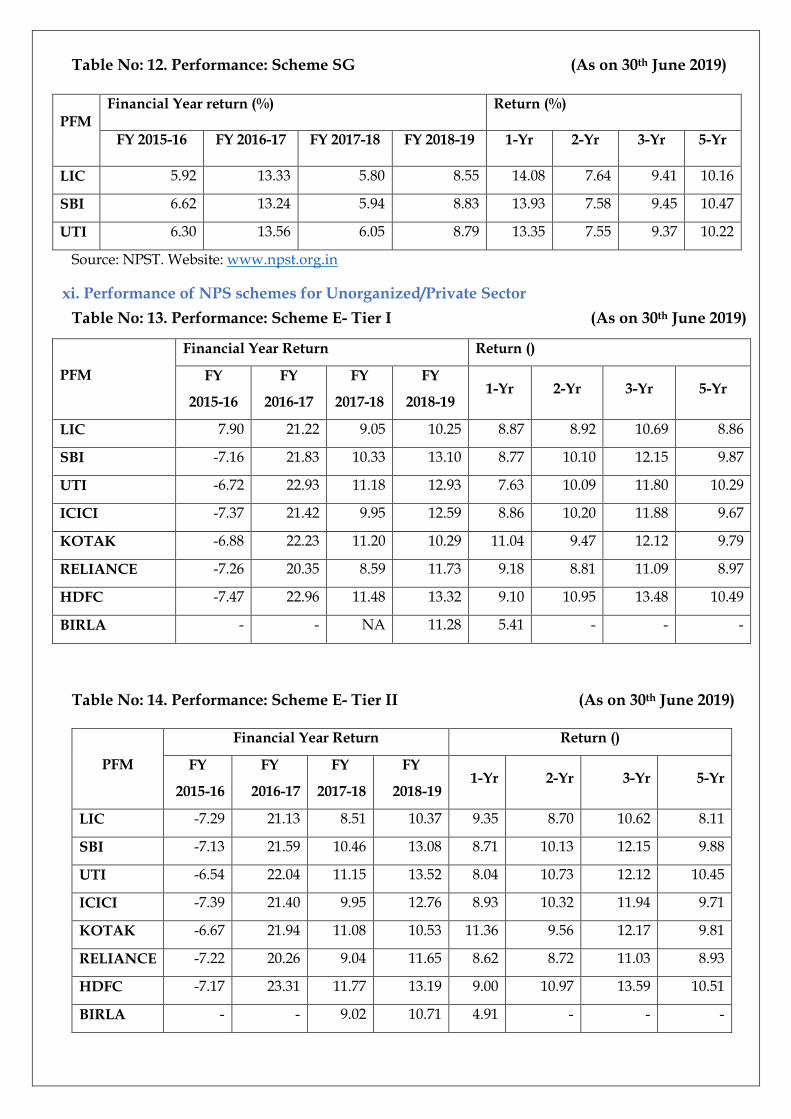

Table No: 12. Performance: Scheme SG (As on 30th June 2019)

PFM Financial Year return (%) Return (%)

FY 2015-16 FY 2016-17 FY 2017-18 FY 2018-19 1-Yr 2-Yr 3-Yr 5-Yr

LIC 5.92 13.33 5.80 8.55 14.08 7.64 9.41 10.16

SBI 6.62 13.24 5.94 8.83 13.93 7.58 9.45 10.47

UTI 6.30 13.56 6.05 8.79 13.35 7.55 9.37 10.22

Source: NPST. Website: www.npst.org.in

xi. Performance of NPS schemes for Unorganized/Private Sector

Table No: 13. Performance: Scheme E- Tier I (As on 30th June 2019)

Table No: 14. Performance: Scheme E- Tier II (As on 30th June 2019)

PFM

Financial Year Return Return ()

FY

2015-16

FY

2016-17

FY

2017-18

FY

2018-19 1-Yr 2-Yr 3-Yr 5-Yr

LIC 7.90 21.22 9.05 10.25 8.87 8.92 10.69 8.86

SBI -7.16 21.83 10.33 13.10 8.77 10.10 12.15 9.87

UTI -6.72 22.93 11.18 12.93 7.63 10.09 11.80 10.29

ICICI -7.37 21.42 9.95 12.59 8.86 10.20 11.88 9.67

KOTAK -6.88 22.23 11.20 10.29 11.04 9.47 12.12 9.79

RELIANCE -7.26 20.35 8.59 11.73 9.18 8.81 11.09 8.97

HDFC -7.47 22.96 11.48 13.32 9.10 10.95 13.48 10.49

BIRLA - - NA 11.28 5.41 - - -

PFM

Financial Year Return Return ()

FY

2015-16

FY

2016-17

FY

2017-18

FY

2018-19 1-Yr 2-Yr 3-Yr 5-Yr

LIC -7.29 21.13 8.51 10.37 9.35 8.70 10.62 8.11

SBI -7.13 21.59 10.46 13.08 8.71 10.13 12.15 9.88

UTI -6.54 22.04 11.15 13.52 8.04 10.73 12.12 10.45

ICICI -7.39 21.40 9.95 12.76 8.93 10.32 11.94 9.71

KOTAK -6.67 21.94 11.08 10.53 11.36 9.56 12.17 9.81

RELIANCE -7.22 20.26 9.04 11.65 8.62 8.72 11.03 8.93

HDFC -7.17 23.31 11.77 13.19 9.00 10.97 13.59 10.51

BIRLA - - 9.02 10.71 4.91 - - -

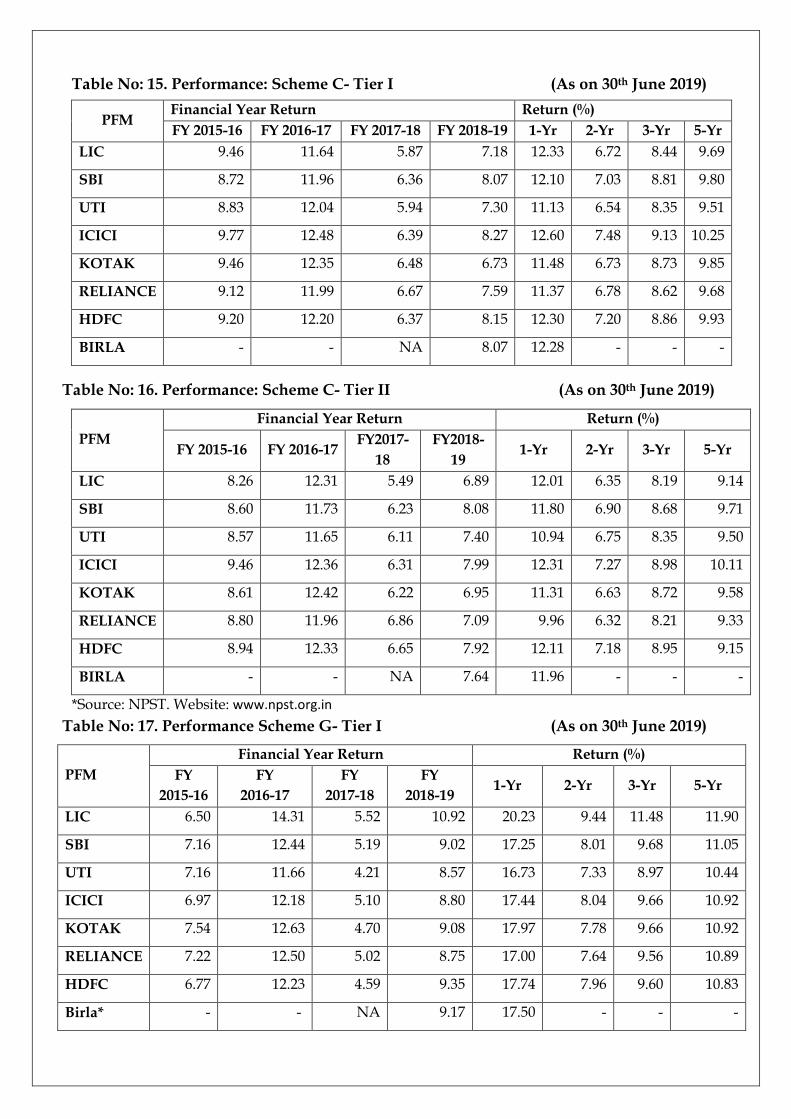

Table No: 15. Performance: Scheme C- Tier I (As on 30th June 2019)

PFM Financial Year Return Return (%)

FY 2015-16 FY 2016-17 FY 2017-18 FY 2018-19 1-Yr 2-Yr 3-Yr 5-Yr

LIC 9.46 11.64 5.87 7.18 12.33 6.72 8.44 9.69

SBI 8.72 11.96 6.36 8.07 12.10 7.03 8.81 9.80

UTI 8.83 12.04 5.94 7.30 11.13 6.54 8.35 9.51

ICICI 9.77 12.48 6.39 8.27 12.60 7.48 9.13 10.25

KOTAK 9.46 12.35 6.48 6.73 11.48 6.73 8.73 9.85

RELIANCE 9.12 11.99 6.67 7.59 11.37 6.78 8.62 9.68

HDFC 9.20 12.20 6.37 8.15 12.30 7.20 8.86 9.93

BIRLA - - NA 8.07 12.28 - - -

Table No: 16. Performance: Scheme C- Tier II (As on 30th June 2019)

PFM

Financial Year Return Return (%)

FY 2015-16 FY 2016-17 FY2017-

18

FY2018-

19 1-Yr 2-Yr 3-Yr 5-Yr

LIC 8.26 12.31 5.49 6.89 12.01 6.35 8.19 9.14

SBI 8.60 11.73 6.23 8.08 11.80 6.90 8.68 9.71

UTI 8.57 11.65 6.11 7.40 10.94 6.75 8.35 9.50

ICICI 9.46 12.36 6.31 7.99 12.31 7.27 8.98 10.11

KOTAK 8.61 12.42 6.22 6.95 11.31 6.63 8.72 9.58

RELIANCE 8.80 11.96 6.86 7.09 9.96 6.32 8.21 9.33

HDFC 8.94 12.33 6.65 7.92 12.11 7.18 8.95 9.15

BIRLA - - NA 7.64 11.96 - - -

*Source: NPST. Website: www.npst.org.in

Table No: 17. Performance Scheme G- Tier I (As on 30th June 2019)

PFM

Financial Year Return Return (%)

FY

2015-16

FY

2016-17

FY

2017-18

FY

2018-19 1-Yr 2-Yr 3-Yr 5-Yr

LIC 6.50 14.31 5.52 10.92 20.23 9.44 11.48 11.90

SBI 7.16 12.44 5.19 9.02 17.25 8.01 9.68 11.05

UTI 7.16 11.66 4.21 8.57 16.73 7.33 8.97 10.44

ICICI 6.97 12.18 5.10 8.80 17.44 8.04 9.66 10.92

KOTAK 7.54 12.63 4.70 9.08 17.97 7.78 9.66 10.92

RELIANCE 7.22 12.50 5.02 8.75 17.00 7.64 9.56 10.89

HDFC 6.77 12.23 4.59 9.35 17.74 7.96 9.60 10.83

Birla* - - NA 9.17 17.50 - - -

*Inception date 08.05.2017, Source: NPST. Website: www.npst.org.in

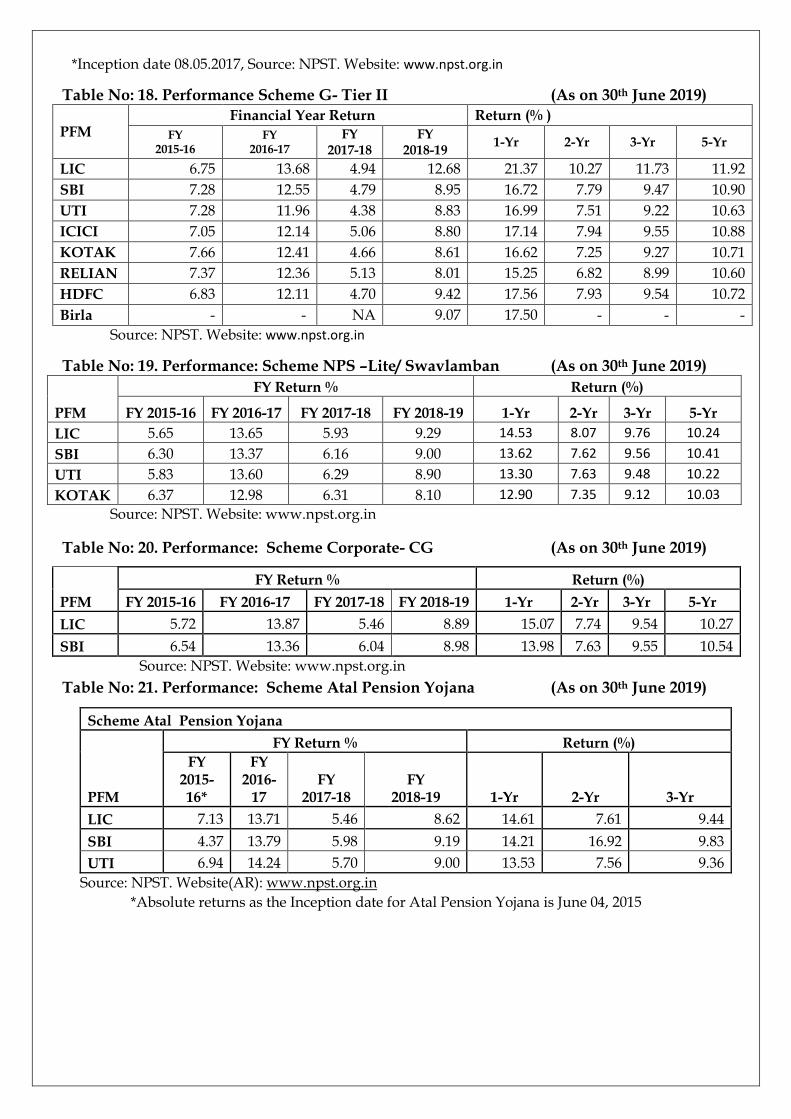

Table No: 18. Performance Scheme G- Tier II (As on 30th June 2019)

PFM Financial Year Return Return (% )

FY 2015-16

FY 2016-17

FY 2017-18

FY 2018-19

1-Yr 2-Yr 3-Yr 5-Yr

LIC 6.75 13.68 4.94 12.68 21.37 10.27 11.73 11.92

SBI 7.28 12.55 4.79 8.95 16.72 7.79 9.47 10.90

UTI 7.28 11.96 4.38 8.83 16.99 7.51 9.22 10.63

ICICI 7.05 12.14 5.06 8.80 17.14 7.94 9.55 10.88

KOTAK 7.66 12.41 4.66 8.61 16.62 7.25 9.27 10.71

RELIAN 7.37 12.36 5.13 8.01 15.25 6.82 8.99 10.60

HDFC 6.83 12.11 4.70 9.42 17.56 7.93 9.54 10.72

Birla - - NA 9.07 17.50 - - -

Source: NPST. Website: www.npst.org.in

Table No: 19. Performance: Scheme NPS –Lite/ Swavlamban (As on 30th June 2019)

PFM

FY Return % Return (%)

FY 2015-16 FY 2016-17 FY 2017-18 FY 2018-19 1-Yr 2-Yr 3-Yr 5-Yr

LIC 5.65 13.65 5.93 9.29 14.53 8.07 9.76 10.24

SBI 6.30 13.37 6.16 9.00 13.62 7.62 9.56 10.41

UTI 5.83 13.60 6.29 8.90 13.30 7.63 9.48 10.22

KOTAK 6.37 12.98 6.31 8.10 12.90 7.35 9.12 10.03

Source: NPST. Website: www.npst.org.in

Table No: 20. Performance: Scheme Corporate- CG (As on 30th June 2019)

Source: NPST. Website: www.npst.org.in

Table No: 21. Performance: Scheme Atal Pension Yojana (As on 30th June 2019)

Source: NPST. Website(AR): www.npst.org.in

*Absolute returns as the Inception date for Atal Pension Yojana is June 04, 2015

PFM

FY Return % Return (%)

FY 2015-16 FY 2016-17 FY 2017-18 FY 2018-19 1-Yr 2-Yr 3-Yr 5-Yr

LIC 5.72 13.87 5.46 8.89 15.07 7.74 9.54 10.27

SBI 6.54 13.36 6.04 8.98 13.98 7.63 9.55 10.54

Scheme Atal Pension Yojana

PFM

FY Return % Return (%)

FY 2015-16*

FY 2016-

17 FY

2017-18 FY

2018-19 1-Yr 2-Yr 3-Yr

LIC 7.13 13.71 5.46 8.62 14.61 7.61 9.44

SBI 4.37 13.79 5.98 9.19 14.21 16.92 9.83

UTI 6.94 14.24 5.70 9.00 13.53 7.56 9.36

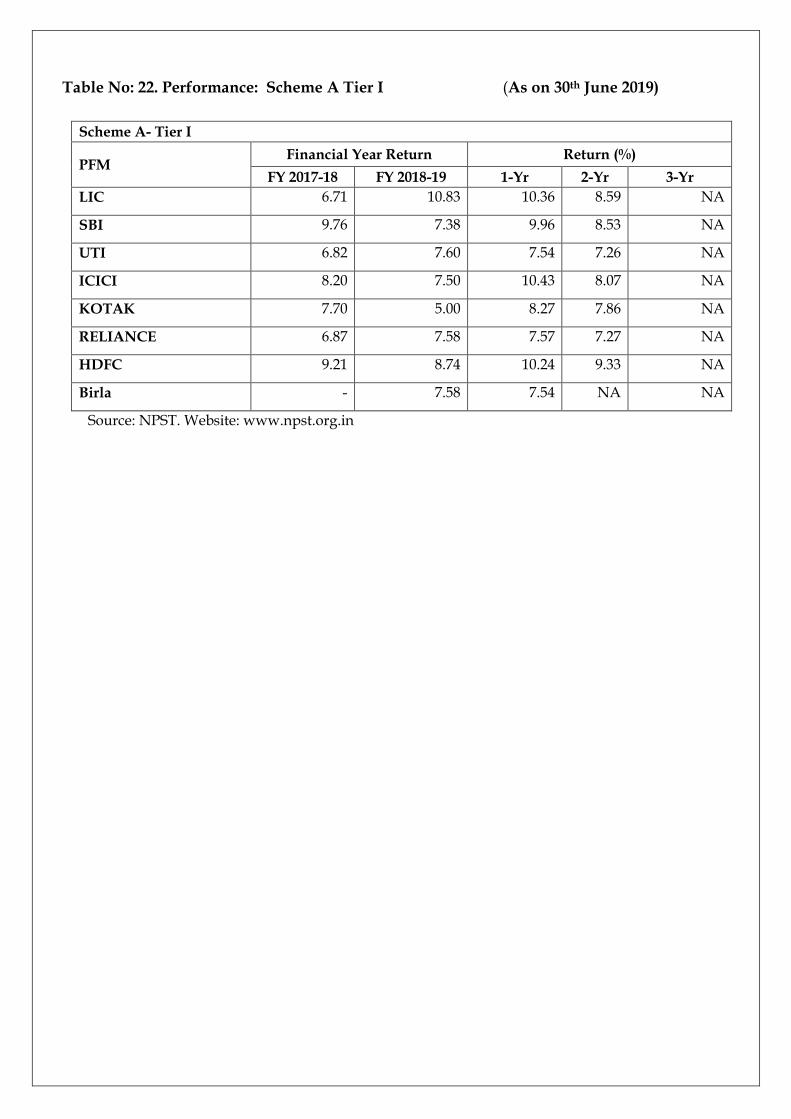

Table No: 22. Performance: Scheme A Tier I (As on 30th June 2019)

Scheme A- Tier I

PFM Financial Year Return Return (%)

FY 2017-18 FY 2018-19 1-Yr 2-Yr 3-Yr

LIC 6.71 10.83 10.36 8.59 NA

SBI 9.76 7.38 9.96 8.53 NA

UTI 6.82 7.60 7.54 7.26 NA

ICICI 8.20 7.50 10.43 8.07 NA

KOTAK 7.70 5.00 8.27 7.86 NA

RELIANCE 6.87 7.58 7.57 7.27 NA

HDFC 9.21 8.74 10.24 9.33 NA

Birla - 7.58 7.54 NA NA

Source: NPST. Website: www.npst.org.in

Section 6: Circulars

Circulars/Notices/Guidelines Issued/Advisory

The detailed Circulars/Notices/Guidelines Issued/Advisory may be referred at PFRDA’s website

Date of Circular Circular Number Subject

17-June-2019 PFRDA/2019/13/REG-POP/1 Format for Annual Certificate for Point of Presence as per PFRDA(POP) Regulation, 2018

In the above circular, a reference is invited to the notification of PFRDA (Point of Presence)

Regulations,2018, and in terms regulation no. 11(d) and regulation number 29(2) of said regulations, all

registered POPs are required to submit Annual certificate to the Authority. The prescribed format for the

Annual Certificate can be accessed through PFRDA website in the referred circular.

Section 7: International section Extracts from: https://www.bloomberg.com/news/articles/2019-06-19/australia-to-fix-flaws-in-world-s-fourth-biggest-pension-pool

Australia to Fix Flaws in World's Fourth-Biggest Pension Pool

Australia’s government said it’s committed to tackling structural flaws in the nation’s A$2.8 trillion ($1.9 trillion) pensions industry that have eroded retirement savings and cost people billions of dollars in unnecessary fees.

The government will try again to stop the common practice of young workers automatically being charged for life insurance through their pension plans, Senator Jane Hume, the new assistant minister for superannuation, financial services and financial technology, told a Bloomberg conference Thursday. It will also work to ensure people are given better options for drawing down their savings when they reach retirement.

“There are several challenges with the way our superannuation system is operating,” Hume said. “Our focus must be on improving the efficiency of the system, lowering costs and promoting informed member choice and competition.”

A government-commissioned review earlier this year found the superannuation system, which invests the mandatory retirement savings of Australians, was beset by a litany of problems including high fees, multiple accounts and chronic under-performance by some funds. Further to that, a yearlong inquiry into the financial services industry uncovered misconduct that has hammered the reputation of some funds.

Hume, who worked in banking, finance and funds management before entering parliament, said the government had already acted on many of the recommendations of the Productivity Commission and the inquiry led by Kenneth Hayne.

Under laws coming into force next month, the tax office will have greater powers to help people consolidate low-balance or inactive accounts; fees will be capped on accounts with A$6,000 or less, and exit fees will be barred. The Productivity Commission inquiry found one third of all superannuation accounts are unintended, costing A$2.6 billion in unnecessary fees and insurance each year.

Further, the prudential regulator in April was given greater powers to take action against under-performing funds before members suffer significant harm. That includes civil penalties for fund directors and trustees for breaching their obligations to act in the best interests of their members.

Hume outlined further steps the government will take, including trying again to pass legislation that ends default insurance for under-25s or on low balance accounts. That legislation was blocked in parliament earlier this year.

There is currently “very little guidance on how retirees should draw down their savings when they reach retirement,” Hume said. Funds will be required to develop a retirement income strategy, and the government is “also exploring ways of expanding the range of retirement income products available.”

A review of the capabilities of the prudential regulator is almost complete, and the government is also planning a review of the retirement income system -- a recommendation of the Productivity Commission.

“This is a crucial time for financial services in Australia,” Hume said. “A lot is happening already and a lot more needs to happen, because financial services are the arterial veins of our economy.”

Current market enticing more U.K. plans to let liabilities go https://www.pionline.com/print/current-market-enticing-more-uk-plans-let-liabilities-go

More U.K. trustees are finding they can afford to insure their defined benefit plan liabilities as More U.K. trustees are finding they can afford to insure their defined benefit plan liabilities as funding levels remain high, longevity expectations have declined and insurers' fees have come down.

Consultants advising on buy-in and buyout deals said insurers' growing capacity to take on larger transactions compared with a few years ago has lured more trustees to the market with hopes of securing a buy-in while pricing remains attractive.

According to Aon PLC, the U.K. pension risk transfer market is set to break a record in 2019, reaching more than £30 billion ($38 billion). Data from consultant Hymans Robertson LLP show that deals completed in 2018 equaled £24 billion, doubling from £12.2 billion in 2017 and increasing 137% since 2016.

In the past few months, there have been several £1 billion-plus transactions:

Rolls-Royce, Goodwood, England, insured £4.1 billion in liabilities of its £13 billion Rolls-Royce U.K. Pension Fund through a buyout with Legal & General Assurance Society in June. Marks and Spencer PLC, London, completed £1.4 billion of buy-ins with Pension Insurance Corp. and Phoenix Life for its £10.5 billion Marks and Spencer Pension Scheme in May. Commerzbank, London, insured £1.2 billion in liabilities for its Dresdner Kleinwort Pension Plan through a buy-in with PIC in April.

A combination of factors has improved insurers' position, allowing them to adjust fees. In the past, insurers shunned taking on the liabilities of deferred participants - those who stopped accruing benefits but are yet to start receiving their pension - due to higher capital requirements they faced under Solvency II regulation. Instead they focused on buy-in deals.

Through a buy-in, plan sponsors can insure a proportion of their plan's liabilities that corresponds with a set of benefits that are due to be received by retired participants. Conversely, a buyout deal includes securing the benefits of deferred as well as retired participants.

However, recent revisions of mortality figures and a growing number of participants choosing to transfer out of defined benefit into defined contribution plans boosted the certainty of outcomes for insurers. Life expectancy in the U.K. has been declining since 2014, according to World Bank data.

£70 billion transferred

Richard Wellard, partner and risk transfer specialist at Hymans Roberston in London, pointed out that since 2015 when the U.K. introduced the pension freedoms regulation, there have been more than £70 billion of benefits transferred by participants out of DB funds and into DC plans.

Mr. Wellard said the volume of transfers out of defined benefit funds has increased the affordability of insuring the benefits that are left in the plans for trustees. "It generally costs trustees less to pay a transfer value (of benefits) if a member chooses to transfer their benefits than it does to insure those benefits if the member remains in the pension scheme," he said.

In turn, sources said plan sponsors in 2019 spent about 5% less on a full buyout and around 20% less on a buy-in than in previous years. "Pricing is as good as it has ever been," said David Ellis, U.K. leader, bulk pensions insurance advisory at mercer in London, which advised on the Rolls-Royce deal.

"Many companies don't want to hold off (insuring liabilities) if they can afford it," he added.

John Baines, partner in Aon's risk settlement group in London, said a "few years ago it was quite risky for insurers to write large transactions because if they had failed they couldn't readily use the assets elsewhere, because there weren't many other large deals in the market."

Mr. Baines expects more megadeals sized at between £3 billion and £4 billion to emerge as a result of insurers' eagerness to take on the liabilities and improved financial positions.

Insurers are expected to secure £14 billion worth of deals in the first half of 2019, Mr. Ellis noted. "(And) first half of the year is usually more quiet," he added. Building on the £14 billion, Mercer expects £30 billion or more for the full year, he said.

Mr. Baines noted that for plan sponsors it can be more affordable to do a buyout than to stay invested in low-yielding assets such as government bonds, as it removes the risk of having to make uncertain levels of pension contributions in the future. Still, sources are questioning if buy-ins or buyouts will remain cheaper for trustees as insurers begin to struggle to source relevant assets such as long-dated credit, for example, 15-year corporate bonds.

Aon's Mr. Baines said: "I don't see it in 2019 but beyond 2020 we could start to see a capacity constraint."

David Salter, partner at Lane Clark & Peacock LLP in London, who advised on the Commerzb "There is a global competition for assets to back liabilities," Mr. Ellis said.

The U.S. buyout market is simultaneously booming. Corporate pension plan buyout sales for the first quarter totaled about $4.7 billion, the highest first quarter in 30 years, according to LIMRA Secure Retirement Institute's quarterly survey. Buyout sales were $10.5 billion in the fourth quarter of 2018, according to LIMRA.

Compressed credit spreads Russell Lee, head of client solutions, pension risk transfer at Legal & General Group PLC, said in the last 12 months credit spreads have compressed. "We have a pipeline of bulk annuity transactions for the next two to three years, but some schemes may have unrealistic views about the pricing that is achievable," he said. Aon's Mr. Baines said: "I don't see it in 2019 but beyond 2020 we could start to see a capacity constraint."

David Salter, partner at Lane Clark & Peacock LLP in London, who advised on the Commerzbank deal, said "we are seeing a place where supply and demand start to balance each other out."

"Insurers are starting to choose which transactions they want to quote on. They can afford to be picky," he said. To deal with the constraint, insurers have been expanding their investible universe and getting creative with the types of assets that could be used to match pension liabilities they take on, including infrastructure debt. "(Illiquid) assets are attractive only if the price is right," Mr. Lee said. However, larger deals for sponsors with more complex defined benefit arrangements could take longer to complete. "The decision on the Commerzbank deal was taken in the middle of last year. A buy-in was a targeted focus over a number of years as the plan became fully funded," Mr. Salter said. But, "more generally, plans have just realized that buyout is affordable as pricing has improved," he said, adding that trustees could wait between three to four months to get a deal.

Section 8: Events International Yoga Day celebration

The fifth International Day of Yoga (IDY) was organized on 21st June 2019 in PFRDA. Two certified

yoga instructors provided yoga training for the staff members. The yoga session was actively

participated by more than 60 staff members. The event was successfully accomplished.”

Yoga embodies unity of mind and body; thought and action; restraint and fulfilment; harmony between

man and nature; a holistic approach to health and well-being.

Trainers performing Asana.

PFRDA staff members performing Asana.

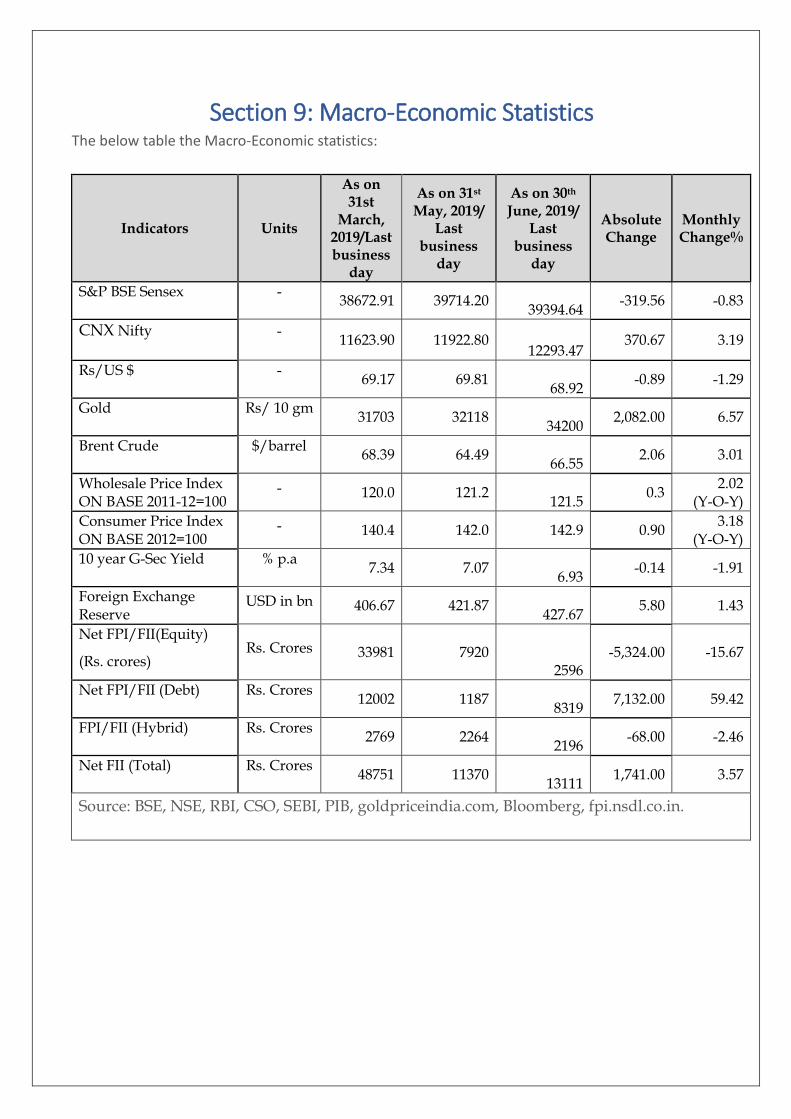

Section 9: Macro-Economic Statistics The below table the Macro-Economic statistics:

Indicators Units

As on 31st

March, 2019/Last business

day

As on 31st May, 2019/

Last business

day

As on 30th June, 2019/

Last business

day

Absolute Change

Monthly Change%

S&P BSE Sensex - 38672.91 39714.20

39394.64 -319.56 -0.83

CNX Nifty - 11623.90 11922.80

12293.47 370.67 3.19

Rs/US $ - 69.17 69.81

68.92 -0.89 -1.29

Gold Rs/ 10 gm 31703 32118

34200 2,082.00 6.57

Brent Crude $/barrel 68.39 64.49

66.55 2.06 3.01

Wholesale Price Index ON BASE 2011-12=100

- 120.0 121.2 121.5

0.3 2.02

(Y-O-Y)

Consumer Price Index ON BASE 2012=100

- 140.4 142.0 142.9 0.90 3.18

(Y-O-Y)

10 year G-Sec Yield % p.a 7.34 7.07

6.93 -0.14 -1.91

Foreign Exchange Reserve

USD in bn 406.67 421.87 427.67

5.80 1.43

Net FPI/FII(Equity)

(Rs. crores)

Rs. Crores 33981 7920 2596

-5,324.00 -15.67

Net FPI/FII (Debt) Rs. Crores 12002 1187

8319 7,132.00 59.42

FPI/FII (Hybrid) Rs. Crores 2769 2264

2196 -68.00 -2.46

Net FII (Total) Rs. Crores 48751 11370

13111 1,741.00 3.57

Source: BSE, NSE, RBI, CSO, SEBI, PIB, goldpriceindia.com, Bloomberg, fpi.nsdl.co.in.

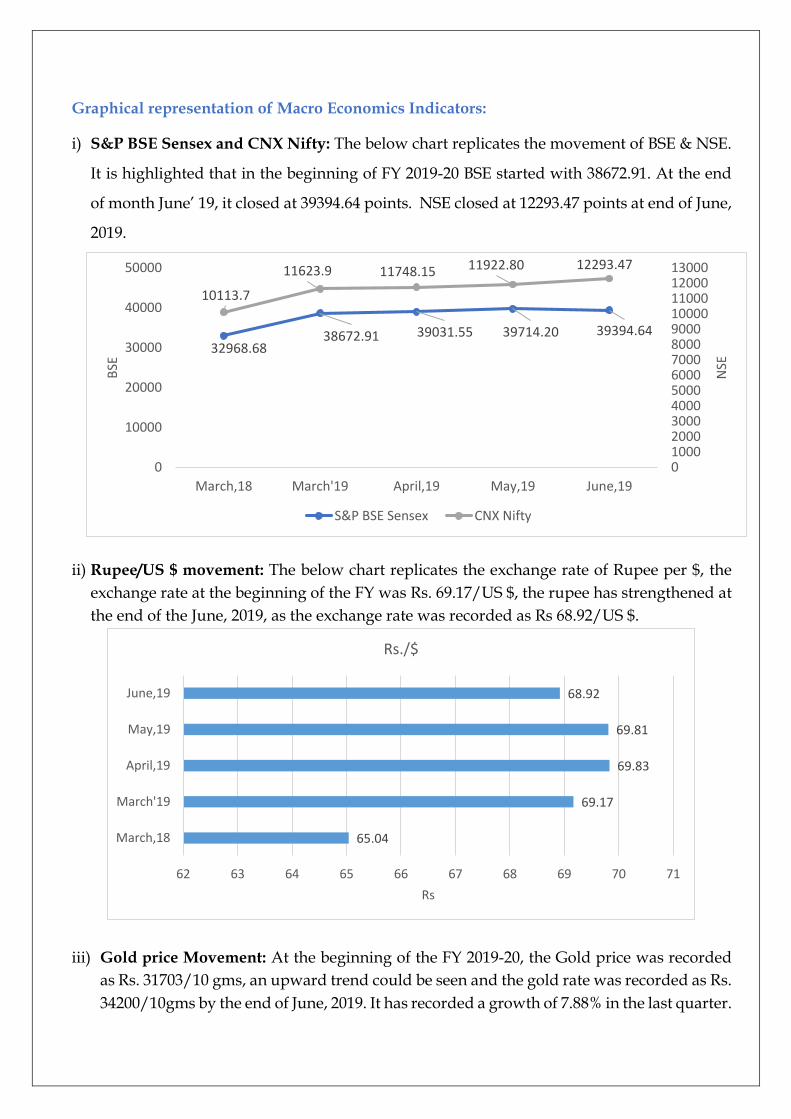

Graphical representation of Macro Economics Indicators:

i) S&P BSE Sensex and CNX Nifty: The below chart replicates the movement of BSE & NSE.

It is highlighted that in the beginning of FY 2019-20 BSE started with 38672.91. At the end

of month June’ 19, it closed at 39394.64 points. NSE closed at 12293.47 points at end of June,

2019.

ii) Rupee/US $ movement: The below chart replicates the exchange rate of Rupee per $, the

exchange rate at the beginning of the FY was Rs. 69.17/US $, the rupee has strengthened at

the end of the June, 2019, as the exchange rate was recorded as Rs 68.92/US $.

iii) Gold price Movement: At the beginning of the FY 2019-20, the Gold price was recorded

as Rs. 31703/10 gms, an upward trend could be seen and the gold rate was recorded as Rs.

34200/10gms by the end of June, 2019. It has recorded a growth of 7.88% in the last quarter.

32968.6838672.91 39031.55 39714.20 39394.64

10113.7

11623.9 11748.15 11922.80 12293.47

010002000300040005000600070008000900010000110001200013000

0

10000

20000

30000

40000

50000

March,18 March'19 April,19 May,19 June,19

NSE

BSE

S&P BSE Sensex CNX Nifty

65.04

69.17

69.83

69.81

68.92

62 63 64 65 66 67 68 69 70 71

March,18

March'19

April,19

May,19

June,19

Rs

Rs./$

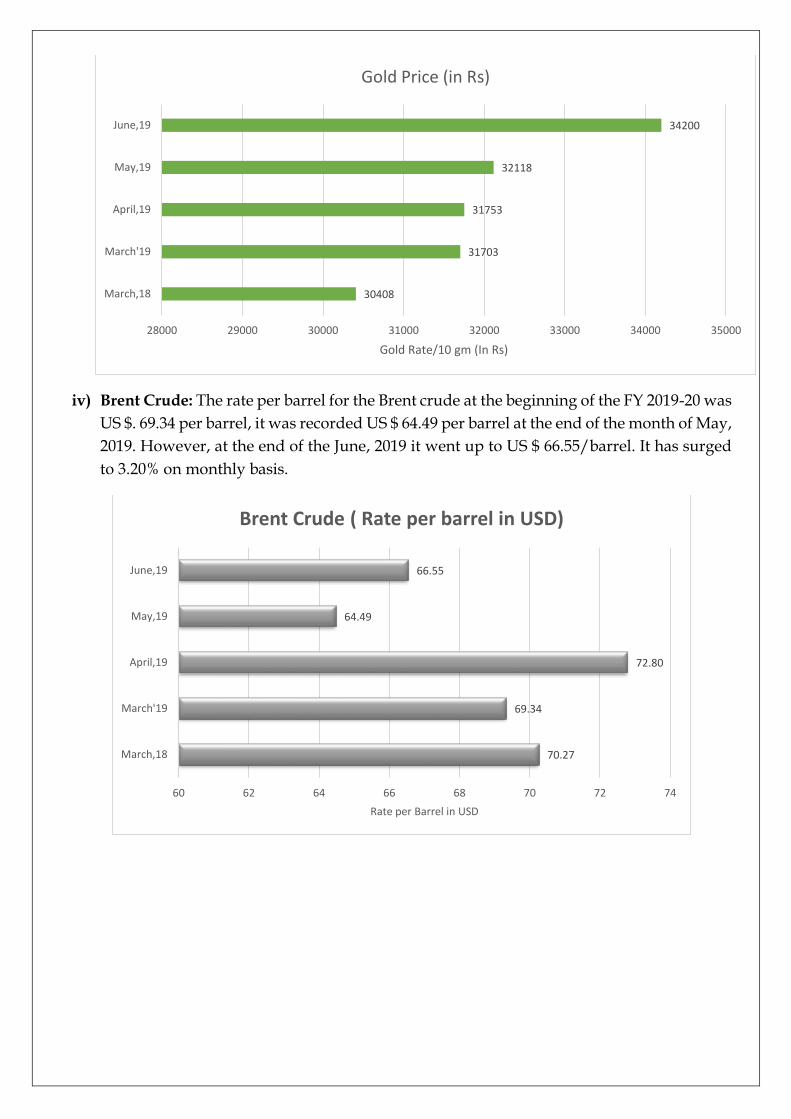

iv) Brent Crude: The rate per barrel for the Brent crude at the beginning of the FY 2019-20 was

US $. 69.34 per barrel, it was recorded US $ 64.49 per barrel at the end of the month of May,

2019. However, at the end of the June, 2019 it went up to US $ 66.55/barrel. It has surged

to 3.20% on monthly basis.

30408

31703

31753

32118

34200

28000 29000 30000 31000 32000 33000 34000 35000

March,18

March'19

April,19

May,19

June,19

Gold Rate/10 gm (In Rs)

Gold Price (in Rs)

70.27

69.34

72.80

64.49

66.55

60 62 64 66 68 70 72 74

March,18

March'19

April,19

May,19

June,19

Rate per Barrel in USD

Brent Crude ( Rate per barrel in USD)

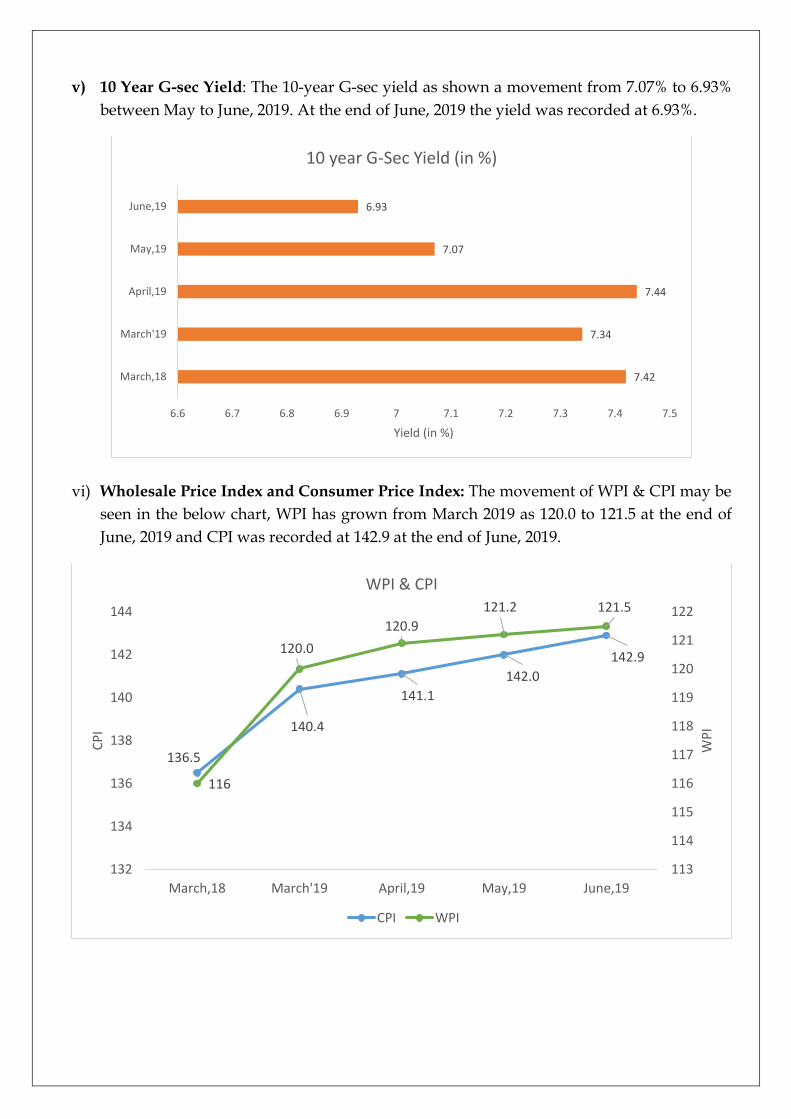

v) 10 Year G-sec Yield: The 10-year G-sec yield as shown a movement from 7.07% to 6.93%

between May to June, 2019. At the end of June, 2019 the yield was recorded at 6.93%.

vi) Wholesale Price Index and Consumer Price Index: The movement of WPI & CPI may be

seen in the below chart, WPI has grown from March 2019 as 120.0 to 121.5 at the end of

June, 2019 and CPI was recorded at 142.9 at the end of June, 2019.

7.42

7.34

7.44

7.07

6.93

6.6 6.7 6.8 6.9 7 7.1 7.2 7.3 7.4 7.5

March,18

March'19

April,19

May,19

June,19

Yield (in %)

10 year G-Sec Yield (in %)

136.5

140.4

141.1

142.0

142.9

116

120.0

120.9

121.2 121.5

113

114

115

116

117

118

119

120

121

122

132

134

136

138

140

142

144

March,18 March'19 April,19 May,19 June,19

WP

I

CP

I

WPI & CPI

CPI WPI

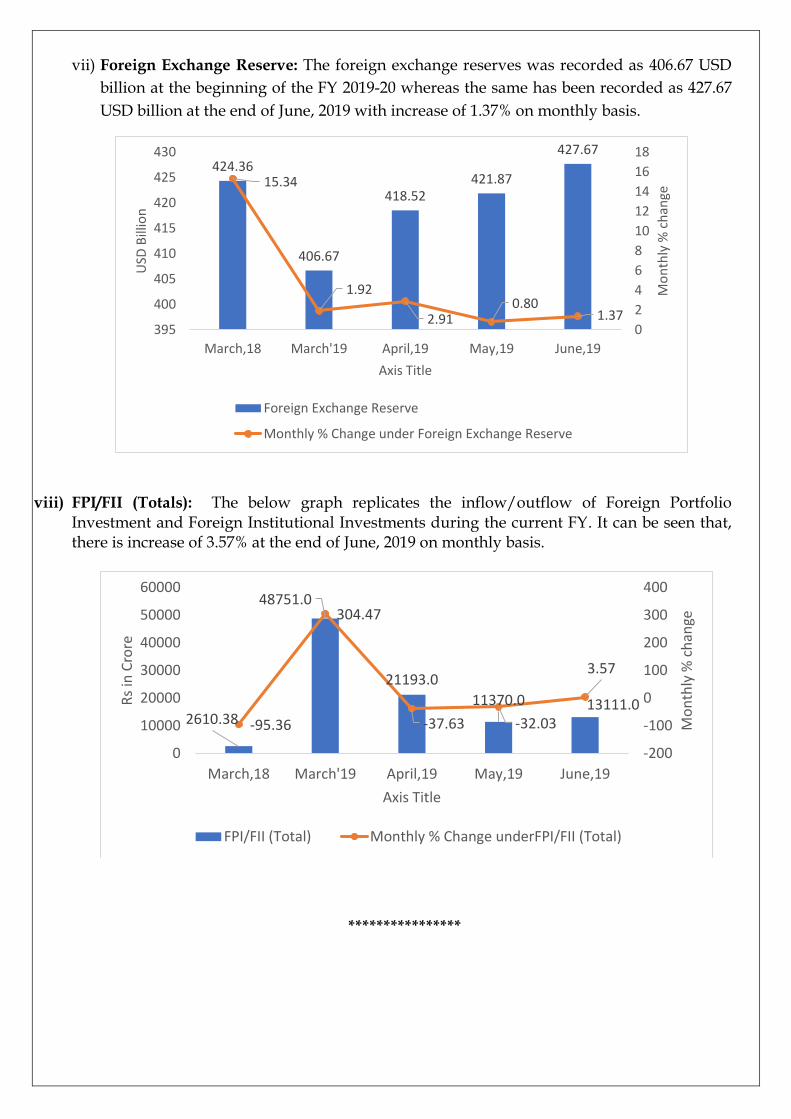

vii) Foreign Exchange Reserve: The foreign exchange reserves was recorded as 406.67 USD

billion at the beginning of the FY 2019-20 whereas the same has been recorded as 427.67

USD billion at the end of June, 2019 with increase of 1.37% on monthly basis.

viii) FPI/FII (Totals): The below graph replicates the inflow/outflow of Foreign Portfolio Investment and Foreign Institutional Investments during the current FY. It can be seen that, there is increase of 3.57% at the end of June, 2019 on monthly basis.

****************

424.36

406.67

418.52421.87

427.67

15.34

1.92

2.910.80

1.370

2

4

6

8

10

12

14

16

18

395

400

405

410

415

420

425