Embed Size (px)

Citation preview

Why Courts Pierce:An Empirical Study of Piercing the Corporate Veil

John H. Mathesont

"The whole problem of the relation between [owners and their]corporations is one that is still enveloped in the mists of metaphor. Metaphorsin law are to be narrowly watched, for starting as devices to liberate thought,they end often by enslaving it. "

"Do you notice anything intellectually disturbing about this [standardpiercing-the-corporate-veil] formulation? That's right; it's vague. It hardlygives you any concrete idea about which conduct does or does not trigger thedoctrine - not enough of an idea, at least, to give you the ability to counselclients in a meaningful way."2

TABLE OF CONTENTS

Introduction.............................3..... ............... 3I. Piercing Doctrine and the Importance of Statistical Analysis...................5II. Methodology and Hypotheses.................................9

A. Case Selection ............................ ............... 10B. Variables .......... l................................1C. Overview of Statistical Methods.........................13

1. Descriptive Statistics..............................132. Logistic Regression..........................13

III. Descriptive Statistics ........................................... 14A. Piercing the Corporate Veil Generally ................. 14B. Court Information ....................................... 17

1. Jurisdiction............... ..................... 172. Court Level .......................... ........... 18

C. Party Information: Type of Plaintiff ........................ 19D. Type of Case: Underlying Cause of Action ...... ........... 20E. Piercing Factors ............................. 29

1. Fraud/Misrepresentation .......... ................. 32

t Law Alumni Distinguished Professor of Law, University of Minnesota Law School; Of Counsel,Kaplan, Strangis and Kaplan, P.A., Minneapolis, Minnesota. I want to thank my excellent researchassistants, Maria de Lourdes B. Dooner, Laurie E. Kellogg, Eric S. Taubel and Emily M. Van Vliet.Any errors or omissions, however, are mine.

1. Berkey v. Third Ave. Ry. Co., 155 N.E. 58, 61 (N.Y. 1926) (Cardozo, J.).2. ROBERT CHARLES CLARK, CORPORATE LAW 38 (1986).

1

Berkeley Business Law Journal Vol. 7, 2010

2. Owner Control/Dominance..........................323. Commingling of Funds.............................334. Undercapitalization...............................335. Non-Functioning.................................346. Overlap........................................357. Unfairness/Injustice...............................358. Non-Existent....................................359. Assumption of Risk...............................36

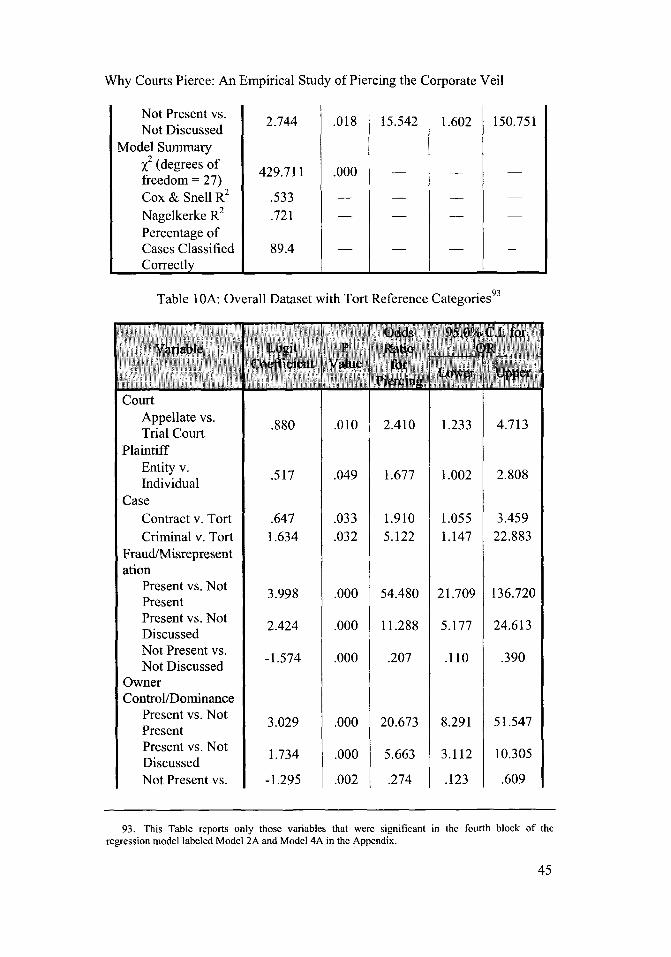

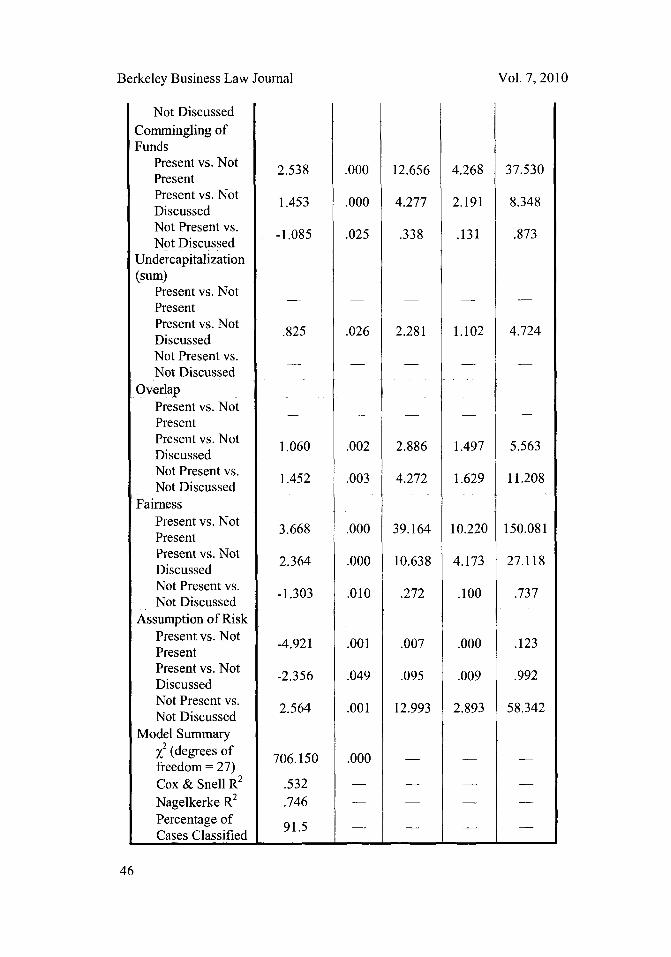

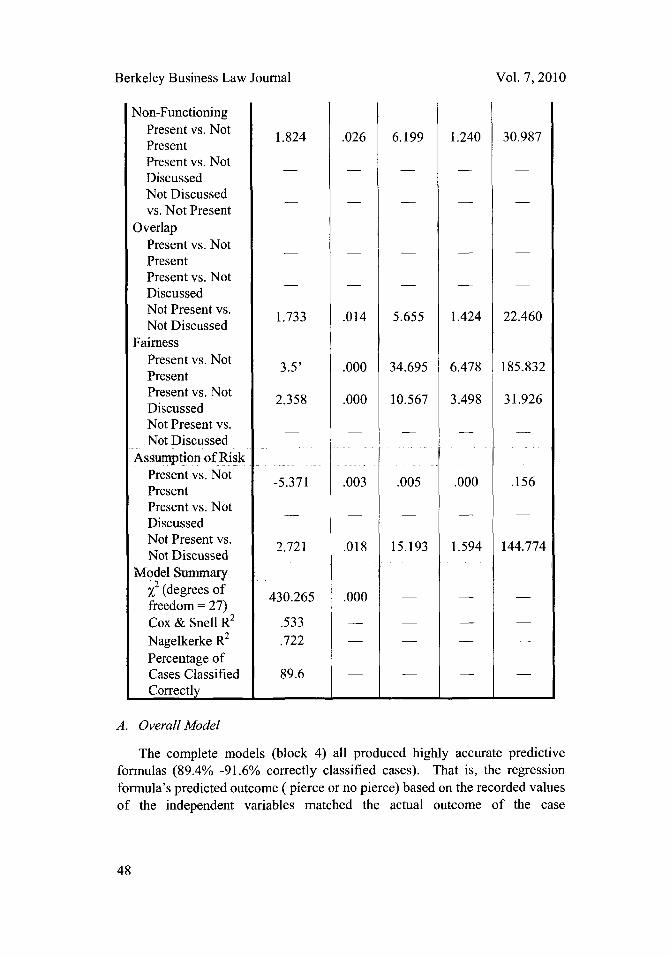

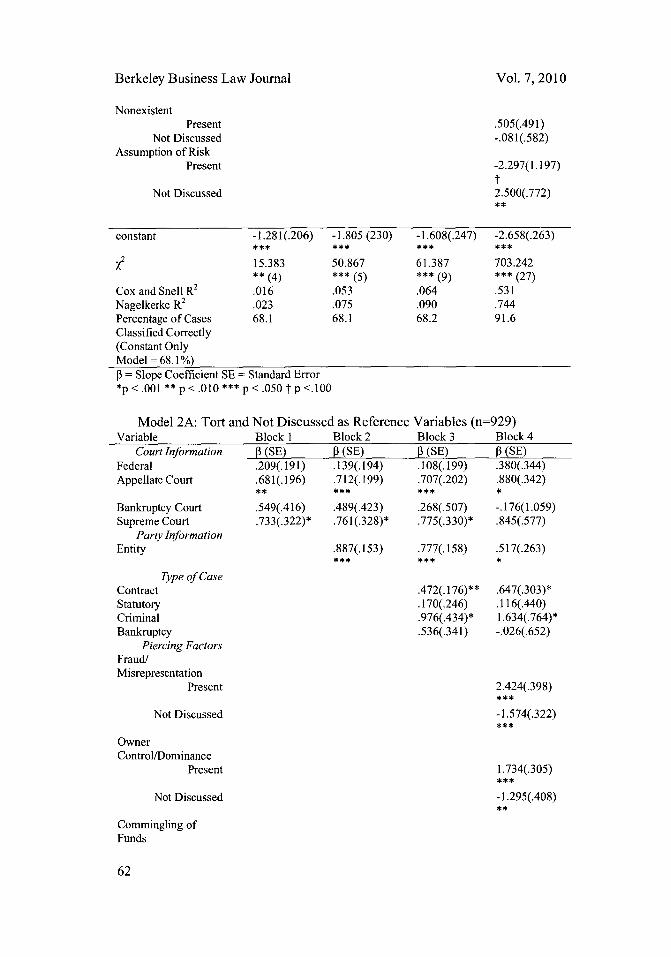

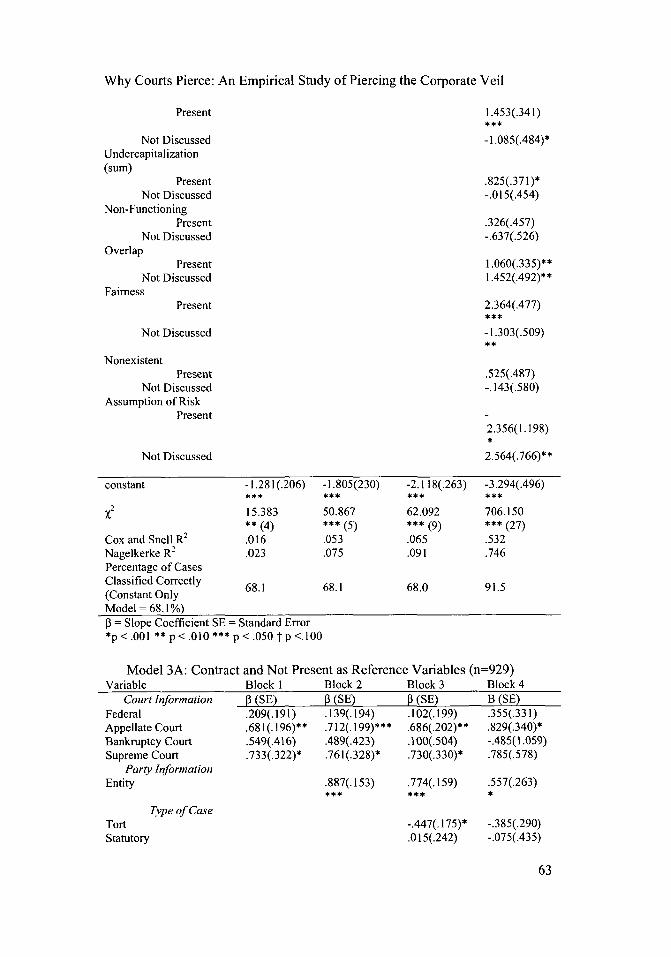

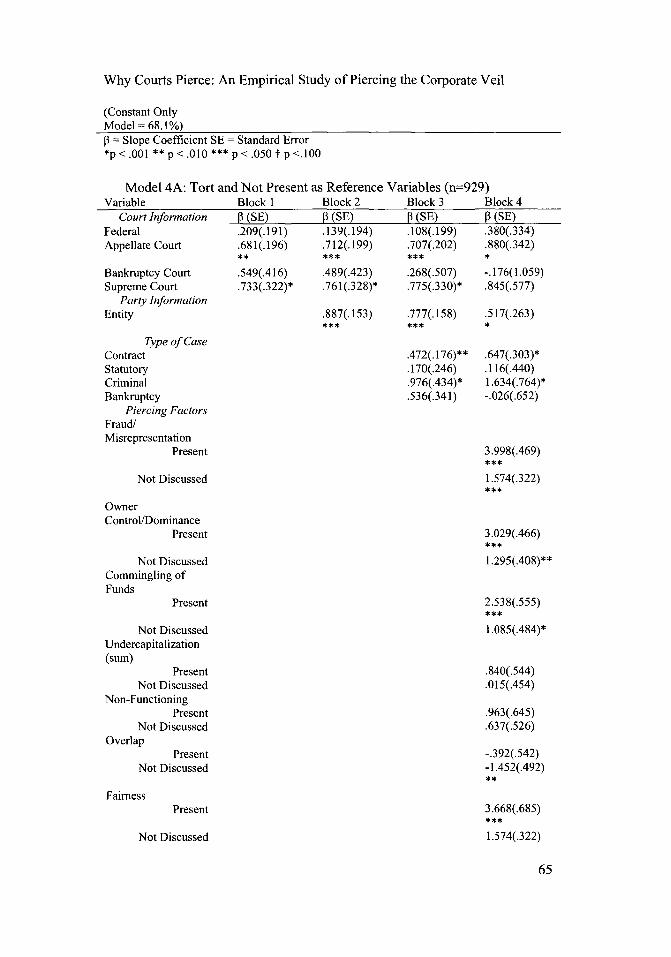

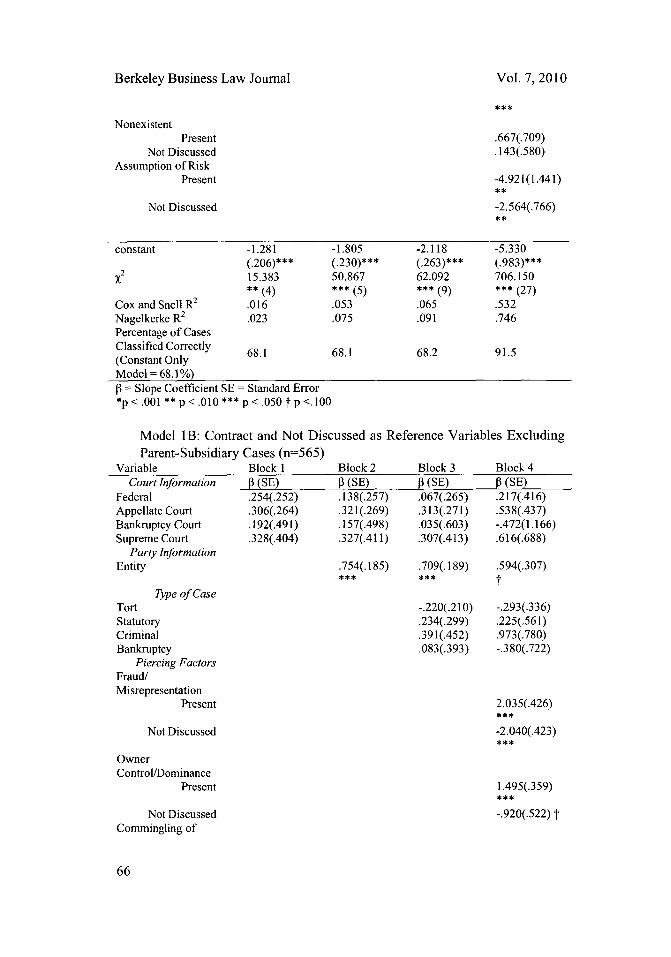

IV. Logistic Regression Analysis.................................36A. Overall Model..................... ................. 48B. Court Information...................................50C. Party Information....................................50D. Type of Claim......................................51E. Piercing Factors.....................................51

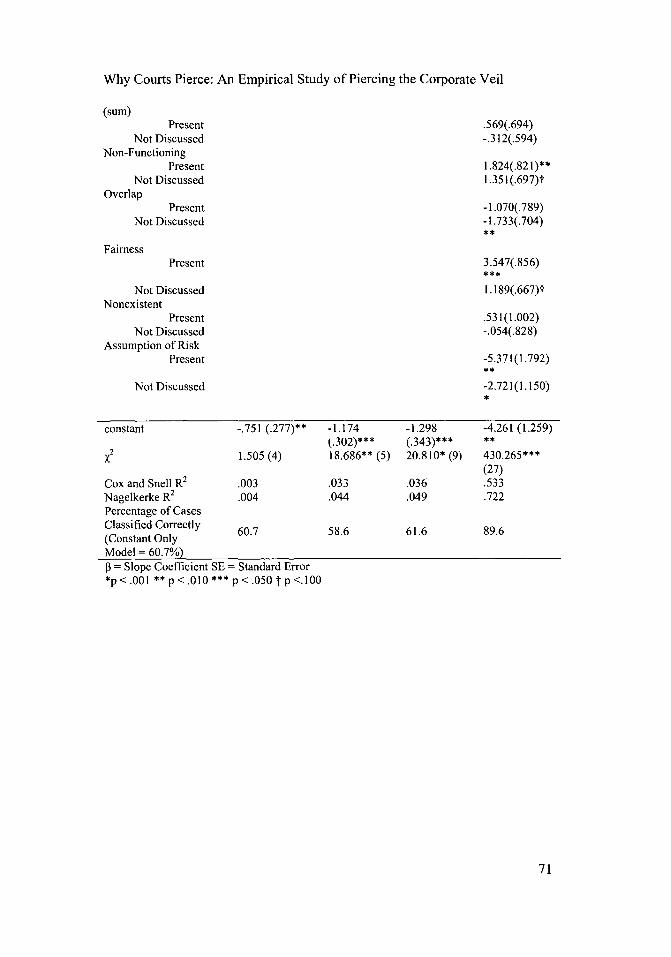

1. Fraud/Misrepresentation............................522. Owner Control/Dominance..........................533. Commingling of Funds.............................544. Undercapitalization...............................555. Non-Functioning................. ................ 556. Overlap........................................567. Fairness........................................568. Non-Existent....................................579. Assumption of the Risk............. .................... 57

Conclusion................................................. 58Appendix. .................................................. 61

2

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

Why Courts Pierce:An Empirical Study of Piercing the Corporate Veil

INTRODUCTION

Limited liability of business owners for the contracts, torts and otherliabilities of their companies has been commonplace for over one hundred andfifty years. This concept of limited liability means that a business owner'spotential personal loss is a fixed amount, namely, the amount invested in thebusiness, usually in the form of stock ownership. Consequently, if the businesssucceeds, the owner obtains the profits, but if the business fails, all of the lossesbeyond the owner's fixed investment are absorbed by others, that is, voluntaryor involuntary creditors,4 or society at large. Although initially applicableprimarily to corporations, new forms of business organizations have appeared,such as limited liability partnerships and limited liability companies, which alsooffer limited liability to their owners.

Although limited liability for business owners is common, it is notuncontroverted. From the very beginning, relieving business owners of liabilityfor the operations of the business has had proponents and detractors. In the1800s, Thomas Cooper described corporate limited liability as a "mode ofswindling, quite common and honourable in these United States" and "a fraudon the honest and confiding part of the public." 6 In rhetorical counterpoint,President Nicholas Butler of Columbia University proclaimed limited liabilityas "the greatest single discovery of modem times," and that "[e]ven steam andelectricity are far less important than the limited liability corporation, and theywould be reduced to comparative impotence without it."7 The academic debateover the propriety of limited liability continues unabated.

3. For a discussion of the evolution of business limited liability see John H. Matheson & Brent A.Olson, A Callfor a Unified Business Organization Law, 65 GEO. WASH. L. REV. 1, 5-9 (1996).

4. The classic "voluntary creditor" is a party to a contract with the business. "Involuntary creditor"will be used throughout this article to mean those creditors who did not enter into a debtor-creditorrelationship of their own free will. The clearest example of this category would be a person againstwhom the business committed some tortious act, such as negligent injury of a pedestrian by a companydelivery-truck driver.

5. See John H. Matheson & Raymond B. Eby, The Doctrine of Piercing the Veil in an Era ofMultiple Limited Liability Entities: An Opportunity to Codify the Test for Waiving Owners' Limited-Liability Protection, 75 WASH. L. REV. 147, 157-72 (2000) (discussing the evolution of modem businessforms).

6. THOMAS COOPER, LECTURES ON THE ELEMENTS OF POLITICAL ECONOMY 247 (2nd ed., A.M.Kelley 1971) (1829).

7. NICHOLAS MURRAY BUTLER, WHY SHOULD WE CHANGE OUR FORM OF GOVERNMENT?STUDIES IN PRACTICAL POLITICS 82 (1912).

8. Compare, e.g., Daniel J. Morrissey, Piercing All the Veils: Applying an Established Doctrine toa New Business Order, 32 IOWA I. CORP. L. 529, 533 (2007) (arguing that, because "LLCs and LLPsoffer their members and partners more direct management power than usually afforded shareholders,"

3

Berkeley Business Law Journal

This ambivalence over the propriety of limited business liability is reflectedin the courts in the form of veil piercing. Piercing the corporate veil is a

common law legal doctrine used to break rules of traditional limited liability forowners, and to hold shareholders accountable as though the corporation'saction was the shareholders' own. In deciding whether to pierce the veil, courtslook to sometimes disparate factors and often use unhelpful, conclusorycharacterizations such as "alter ego" and "instrumentality" to describe therelationship between the shareholders and the corporation. 9 While "[p]iercingthe corporate veil is the most litigated issue in corporate law,"' 0 common lawpiercing is complex, inconsistently applied and often poorly understood.

The empirical project presented by this Article is unique. This study is thefirst to empirically examine the distinct question of substantive common lawpiercing of the corporate veil. As a matter of pure hypothesis, one wouldexpect that any common law doctrine should be applied by the courts in aneutral manner, that is, evenhandedly except for variations in factors explicitlyand specifically identified as part of the applicable test. Given thatpresumption, the empirical results of this study, even on a descriptive level, arestartling. Among the statistically significant findings are:

* Courts pierce twice as often to hold individual persons liable thanthey do to hold entities, such as corporations and limited liabilitycompanies (parent-subsidiary piercing), liable.

* Entity plaintiffs are almost twice as likely as individual plaintiffs tosuccessfully pierce the corporate veil.

* Courts are more likely to pierce to enforce a contract claim than toaward recovery to a tort claimant

* The 'kitchen-sink' approach to piercing litigation (adding as manypossible substantive claims as possible) is not as effective asbringing a single claim.

More fundamentally, this Article is the first to apply to substantive piercingthe advanced statistical techniques of quantitative analysis." This study has

there is "greater justification to hold them personally accountable for the obligations of theirbusinesses") and Nina A. Mendelson, A Control-Based Approach to Shareholder Liability for CorporateTorts, 102 COLUM. L. REV. 1203, 1271-79 (2002) (espousing unlimited liability for torts in the singleshareholder and parent-subsidiary context in regard to capacity to control), with Stephen M. Bainbridge,Abolishing LLC Veil Piercing, 2005 U. ILL. L. REv. 77, 79 (2005) ("the case against veil piercing...applies with equal force to LLCs as to corporations.").

9. The failure of courts' attempts to articulate a single test for disregarding the corporate form andholding the owners of a corporation responsible for the business's financial obligations has resulted in anumber of overlapping lists of factors that are passed off as tests. See, e.g., Richard v. Bell Ati. Corp.,946 F. Supp. 54, 61 (D.C. 1996) (setting out four different tests); Laya v. Erin Homes, Inc., 352 S.E.2d93, 98-99 (W. Va. 1986) (listing nineteen factors); Victoria Elevator Co. v. Meriden Grain Co., 283N.W.2d 509, 512 (Minn. 1979) (listing eight factors).

10. Robert B. Thompson, Piercing the Corporate Veil: An Empirical Study, 76 CORNELL L. REV.1036,1036 (1991).

I1. The current database consists of all substantive piercing cases for the relevant period. A

4

Vol. 7, 2010

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

produced a number of key findings brought to light only through theimplementation of logistic regression methodology. Among these findings are:

* Pure descriptive statistics indicate that the relationship betweenplaintiff type (i.e. individual or entity) and claim type (tort,contract, etc.) is statistically significant, as are the relationshipsseparately between plaintiff type and piercing and between claimtype and piercing. This would suggest that either claim type orplaintiff type, or both, would have a statistically significant effecton piercing. However, this does not prove to be true when thesehypotheses are tested in the regression models. That is, eventhough these descriptive statistics tell us when courts pierce, theydo not explain why courts pierce.

* Fraud, owner control, and commingling of funds have the strongestand most predictive relationship with piercing the corporate veil.Indeed, the presence or absence of these factors alone is usuallydispositive of the piercing decision.

* Conversely, factors reflecting the lack of operational formalities,such as non-existence or non-functioning of corporate directors orofficers, are not significantly related to piercing in the regressionmodels.

* While only discussed in 3% of cases, assumption of the risk has alarge impact on incidence of piercing the corporate veil. It is theonly factor that applies to plaintiffs, and when a court finds itpresent the likelihood of a pierce is drastically reduced.

Part I presents a brief discussion of the problems with doctrinal piercingjurisprudence and an explanation of the need for and methods of logisticregression analysis. Part II presents the research design and explains themethodology employed in this study for capturing the relevant data. Part IIIpresents the empirical results of this study in descriptive form. Part IV presentsthe results and analysis of the logistic regression process.

I. PIERCING DOCTRINE AND THE IMPORTANCE OF STATISTICAL ANALYSIS

Commentators have frequently criticized the courts' reliance on conclusoryterms as producing results-oriented decisions when applying the piercingdoctrine.12 From an academic perspective, the courts are vague and

previous study split off a subset of parent-subsidiary cases for separate analysis based on the uniqueissues raised in that context. See John Matheson, The Modern Law of Corporate Groups: An EmpiricalStudy of Piercing the Corporate Veil in the Parent-Subsidiary Context, 87 N.C. L. REV. 1091 (2009).

12. See, e.g., Stephen M. Bainbridge, Abolishing Veil Piercing, 26 IOWA J. CORP. L. 479, 513(2001) ("Judicial opinions in this area tend to open with vague generalities and close with conclusorystatements with little or no concrete analysis in between. There simply are no [sic] bright-line rules fordeciding when courts will pierce the corporate veil.").

5

Berkeley Business Law Journal Vol. 7, 2010

inconsistent, providing little analysis of underlying facts and failing to discussthe policy rationales.' 3 Veil piercing "seems to happen freakishly. Likelightning, it is rare, severe, and unprincipled."1 4

This ad hoc judicial approach to piercing does not diminish the desire ofpractitioners and business owners to understand and predict how courts willrespond to piercing claims. Research that improves understanding of thejudicial application of piercing doctrine offers large practical value because ofthe frequency of piercing litigation and the lack of an easily understood bright-line rule. More fundamentally, disparate judicial results and apparentinconsistencies demonstrate the need for rigorous empirical and statisticalanalysis of actual court results.

A limited amount of previous piercing research has been done, principallyin the form of an article by Professor Robert Thompson in 1990, counting andcategorizing piercing cases up to that time. I5 Thompson categorized casesbased on the absence or presence of certain individual piercing factors. TheThompson study included jurisdictional cases as well as substantive piercingcases, statutory cases as well as common law ones, and reverse piercing casesas well.

13. Stephen Bainbridge has complained that use of veil piercing is "rare, unprincipled, andarbitrary." Id. at 535. See also Davis Millon, Piercing the Corporate Veil, Financial Responsibility,and the Limits of Limited Liability, 56 EMORY L.J. 1305, 1327 (2007) (describing veil-piercing factorsas an "unweighted laundry list"). At times, however, the academics are no clearer. See, e.g., FREDERICKJ. POWELL, PARENT AND SUBSIDIARY CORPORATIONS 9 (1931) (listing 11 factors for application ofinstrumentality rule); Cathy S. Krendl & James R. Krendl, Piercing the Corporate Veil: Focusing theInquiry, 55 DEN. L.J. 1, 52-55 (1978) (a 31 point checklist).

14. Frank H. Easterbrook & Daniel R. Fischel, Limited Liability and the Corporation, 52 U. CHI. L.REV. 89, 89 (1985).

15. The prior empirical work on substantive piercing involved simple descriptive statistics - that is,a counting and categorization of cases, with no quantitative statistical analysis. See, e.g., Thompson,supra note 10, at 1044-47. Professor Thompson subsequently purported to extend his original databasethrough 1996 but once again simply counted and categorized cases. Robert B. Thompson, Piercing theVeil Within Corporate Groups: Corporate Shareholders as Mere Investors, 13 CONN. J. INT'L L. 379,385 (1999). In 2008, two authors, apparently then students, attempted to update Thompson's originalstudy by considering a "random sampling of cases reported in Westlaw from January 1, 1986 throughDecember 31, 1995." Lee C. Hodge & Andrew B. Sachs, Piercing the Mist: Bringing the ThompsonStudy into the 1990s, 43 WAKE FOREST L. REV. 341, 347 (2008). See also Geoffrey Christopher Rapp,Preserving LLC Veil Piercing: A Response to Bainbridge, 31 IOWA J. CORP. L. 1063, 1068-69 (2006)(addressing sixty-one LLC piercing cases from 1997 to 2005).

16. Thompson, supra note 10, at 1044-45. Inclusion of reverse piercing cases is particularlyproblematic, since these cases seek to benefit individual owners by ignoring the corporate veil to providebenefits, not to impose liability. To include them in a database attempting to describe when courtspierce to hold owners liable results in an exaggerated piercing count. Jurisdictional cases should also beexcluded. Piercing in these cases is not a question of the ultimate liability of the owner but ratherwhether the owner can be made a part of the current lawsuit - that is, whether jurisdiction can beexercised over the owner as a matter preliminary to any adjudication of piercing or ultimate liability. Itis generally acknowledged that the courts tend to apply a different and more expansive approach forthose jurisdictional situations. See, e.g., D. Klein & Son, Inc. v. Good Decision, Inc., 147 Fed. App'x.195, 196 (2d Cir. 2005) ("the exercise of personal jurisdiction over an alleged alter ego ... requiresapplication of a 'less onerous standard' than that necessary for equity to pierce the corporate veil forliability purposes under New York law"). These cases were the focus of a separate study. John A.Swain & Edwin E. Aguilar, Piercing the Veil to Assert Personal Jurisdiction Over Corporate Affiliates:

6

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

Although Professor Thompson's study was an important beginning, it wasaimed primarily at simple case counting and categorization. Thus, it sufferedfrom significant statistical limitations. As Professor Fred McChesney noted inhis landmark article identifying the limitations of case counting alone, "thedifficulty of identifying standards in any line of cases . . . may lie as much in

the deficiencies of legal research techniques as in any judicial 'fuzziness."" 7

In that vein, he found prior analytical and empirical work on piercing wanting:Though clearly an advance in the level of corporate law discourse, the rethinking ...carried forward by Thompson is not wholly satisfactory methodologically. Merelycounting cases and sorting them into various pigeonholes according to expressedjudicial rationales (the process used by Thompson for veil-piercing cases and by Frey

18in studying defective incorporation) suffers from . . . deficiencies ... .

One major deficiency of simple case counting and resultant descriptivestatistics is the inability to adequately account for multi-factor tests, such asthose used in veil-piercing cases.19 Several factors or combinations of factorsmay explain case results rather than individual factors. Moreover, casecounting often fails to account for the possible affects of other variables,whereas regression analysis allows for other variables of interest to becontrolled (or held constant). Additionally, any statistical review of a multi-factor judicial analysis may run into the problems of assigning weights to thevarious factors and isolating the separate affects of factors that may operatesimultaneously. While case counting based on individual factors providessome data, it is simply unable to measure the relative strength or interplay ofthose associations. 20

An Empirical Study of the Cannon Doctrine, 84 B.U. L. REV. 445, 446 (2004). Thompson found that, incases involving piercing the veil for jurisdictional purposes, the plaintiffs' success rate was 36.8%.Thompson, supra note 10, at 1060. For venue purposes, however, Thompson found that the plaintiffs'success rate was 58.3%, a higher piercing rate than in the substantive veil piercing cases. See id.

17. Fred S. McChesney, Doctrinal Analysis and Statistical Modeling in Law: The Case ofDefectiveIncorporation, 71 WASH. U.L.Q. 493, 495 (1993). Professor McChesney's article was "the first to usemultiple regression to discern the separate legal reasons for judicial decisions in a purely common-lawdomain." Id. at 519. The statistical techniques McChesney used have been employed subsequently byother authors. See, e.g., Larry A. DiMattco & Bruce Louis Rich, A Consent Theory ofUnconscionability: An Empirical Study ofLaw in Action, 33 FLA. ST. U. L. REV. 1067, 1093-94 (2006).

18. McChesney, supra note 17, at 515.19. Id.20. The Thompson study and those similar to it include only descriptive statistics with no tests for

statistical significance. While Thompson's study shows the distribution of cases and is suggestive ofhow factors effect piercing, his study is not able to compare those findings to determine which has thelarger effect. Indeed, Professor Thompson recognized the limitations of such simple case-countingdescriptive statistics at the time of his study. McChesney, supra note 17, at 515 n.82 ("Thompson isaware of the methodological shortcomings of merely sorting cases, and reports that he is at work on amultiple regression model for the veil-piercing cases."). McChesney's citation is to footnote 62 ofThompson's original article, where Thompson states:

In an additional article in progress, I use this data and a logit analysis, a form of statistical

regression analysis, to test the relationship between a dependent variable, here the court's

decision to pierce the veil, and independent variables here the various factors recorded in the

data set. Not surprisingly, the "conclusory" indicators of alter ego and instrumentality are the

7

Berkeley Business Law Journal

Multiple regression analysis, however, is "a statistical technique that cansolve the problems of calculating the influence of individual case factors,identifying their relative weights, and accounting for the simultaneous presenceof different factors."21 Simply put, case-counting research at best attempts todescribe when, or under what circumstances, a court will pierce the corporateveil. This Article, in contrast, focuses on the question of why courts eitherpierce or do not pierce the corporate veil. 22

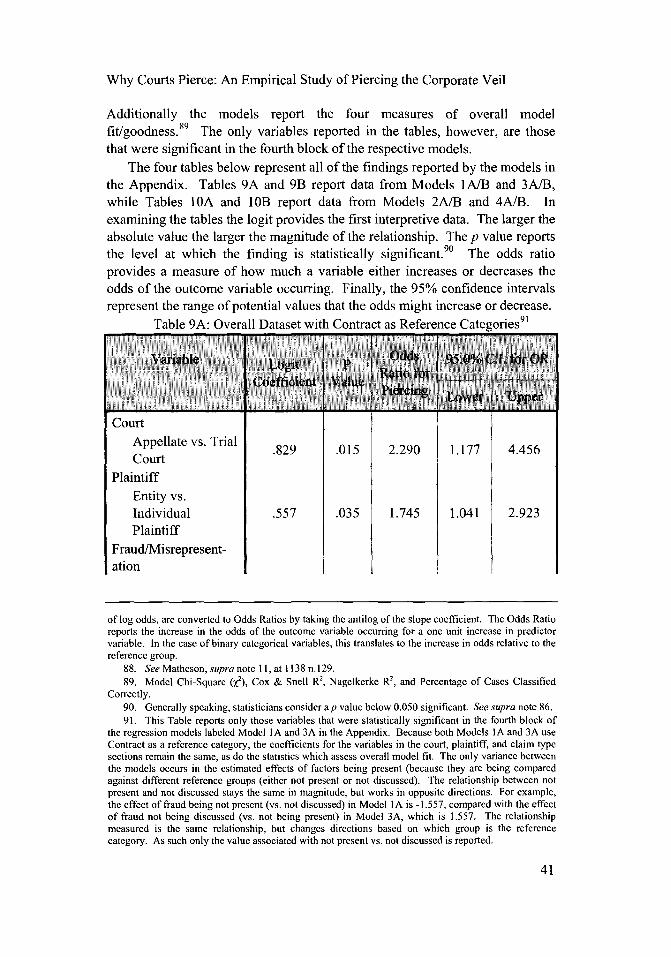

In order to do so, this study employs multiple regression analysis,specifically a logistic model.23 The data generated by a logistic regressionmodel can be used to assess the impact of the independent (predictor) variableson the likelihood of the dependent (outcome) variable occurring, that is,whether a court will pierce. This heightened level of analysis is critical tounderstanding the courts' piercing decisions. Consider one exampledemonstrated in this Article: case counting alone indicates that tort (vs.contract) claims are significantly less successful in achieving a piercing, butthis study empirically demonstrates that, while claim type and piercing areassociated, claim type does not statistically significantly affect the likelihoodthat a court will pierce the corporate veil.24

Given the zero-sum nature of legal disputes, logistic regression can be apowerful tool for practitioner as well as academics. Logistic models generateequations based on known data such that future outcomes can be predicted byapplying the regression equation to new cases. In the models presented belowthe equations generated accurately predicted the court's decision withapproximately 90% accuracy.25 The models presented can be used to make

factors most closely associated with a piercing result. The explanation of that model and theresults are left for another day.

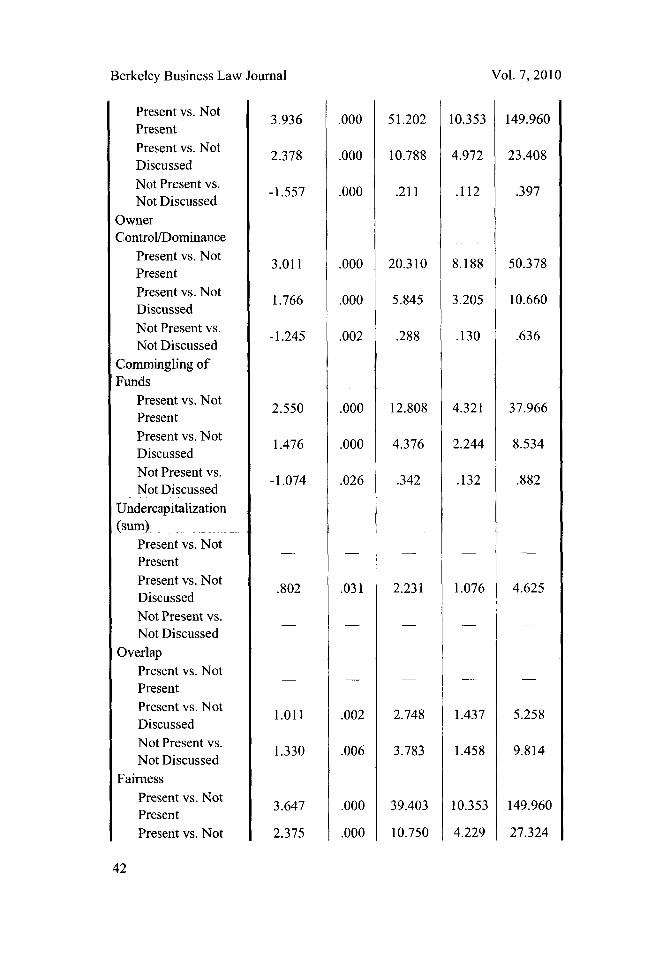

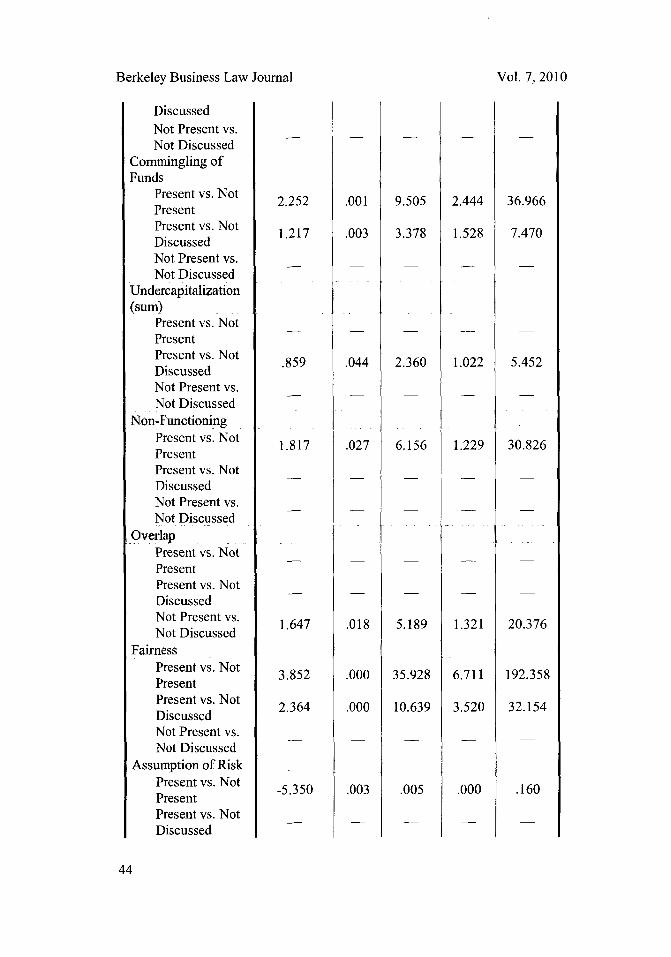

Thompson, supra note 10, at 1046 n.62. Although Thompson recognized the need for a moresophisticated "logit analysis, a form of statistical regression analysis," the supposed "model and theresults" have never been reported. Id.

21. McChesney, supra note 17, at 519.22. "Indeed, as Franklin Fisher has observed, it is difficult to see how anyone could reach

conclusions in legal proceedings involving large-sample, multivariable situations without resort tomultiple regression." Id. at 519-20 (citing Franklin M. Fisher, Multiple Regression in LegalProceedings, 80 COLUM. L. REv. 702, 730 (1980)). See generally Michael 0. Finklestein, RegressionModels in Administrative Proceedings, 86 HARV. L. REV. 1442 (1973) (addressing the use of multipleregression analysis in administrative proceedings); Daniel M. Rubinfeld, Econometrics in theCourtroom, 85 COLUM. L. REV. 1048 (1985) (addressing the use of multiple regression analysis in courtproceedings).

23. Logistic regression is the preferable regression method when the dependent (outcome) variablehas only two response categories. ALAN AGRESTI, AN INTRODUCTION TO CATEGORICAL DATAANALYSIS 103 (1996). For an extended explanation of the technique and benefits of logistic regressionanalysis in a categorical data context see Matheson, supra note I1, at 1133-37.

24. Compare Tables 7.1A and 7.1B with the effect of claim type in Models IA-4A and Models IB-4B in the Appendix.

25. Alternative measures of the effectiveness of the model suggests that the model accounts for 50-75% of the variance in the outcome variable (piercing), or that using the model generated increasespredictive accuracy by 50-75% (over a model with no independent variables). See Model Summary for

8

Vol. 7, 2010

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

strategic litigation decisions, as well as provide valuable insight for attorneysadvising business owners. Findings that show which factors have the largestimpact on the odds of a piercing result can be used to determine which factorsshould be emphasized at trial. Conversely, lawyers will be better able to advisedefendants on whether they should settle by determining which factors are mostlikely to be found at trial and making a more informed risk assessment. Thefindings presented below suggest that when owners are establishing newentities, they need not emphasize operational or corporate formalities in orderto maintain limited liability. 2 6

II. METHODOLOGY AND HYPOTHESES

This project has two primary objectives. The initial goal is to statisticallydescribe the propensities of modem courts for substantive piercing of thecorporate veil. This is the first study to document these judicial proclivities. Inconnection with these descriptive statistics, it is important to explore whetherdifferences in piercing results, such as the level of piercing in cases ofindividual liability as compared to all piercing cases, are statistically significantaccording to accepted quantitative measures of statistical analysis. The secondaim of this study is to move beyond descriptive statistics and explore potentialcausal relationships regarding piercing the veil. These causal relationshipswould inform academic debate and help legal counsel to advise clients based onthe facts in a particular dispute. To that end, the study is designed to test thefollowing major hypotheses involving substantive piercing, among others:

1. Piercing occurs with the same frequency when an entity is theowner (i.e. parent-subsidiary) as when the owners are individuals.

2. Trial courts pierce at the same frequency as appellate courts.3. Courts pierce with the same frequency whether the plaintiff is a

corporate entity or an individual.4. Courts pierce with the same frequency irrespective of the

underlying cause of action, that is, for example, whether a contractclaim is brought as opposed to a tort claim.

5. Each piercing factor identified by the courts is independentlysignificant. That is, the presence of any one factor should beenough to cause a court to pierce.

6. The absence of any single factor will not be enough to prevent acourt from piercing the corporate veil. 27

9

Tables 9A, 9B, 10A, and 10B.26. See discussion infra pp. 55-56 and 59-60.27. The crux of the final two hypotheses is that any factor is sufficient to trigger a pierce, and yet

none is necessary.

Berkeley Business Law Journal Vol. 7, 2010

A. Case Selection

This study employs a database of every case involving piercing in theUnited States from January 1, 1990 to April 1, 2008.28 Cases were selectedusing targeted electronic searches.29 The overall database includes reportedand unreported cases in state and federal courts and every effort was made toinclude only a final decision for a particular case. However, it is important tonote that this database does not account for unreported opinions not availablefrom Westlaw or Lexis, or for cases settled outside of court.

This Article examines substantive piercing for two datasets constructedfrom the database. The first includes all substantive piercing cases.30 Thisdataset was constructed to include all attempts to hold individual owners andparent entities liable, but excludes cases of statutory, reverse, horizontal, andjurisdictional piercing. 31 The second dataset is a sub-dataset that excludesparent-subsidiary piercing. 32 This sub-dataset only includes cases where courts

28. This is the same database from which a subset of parent-subsidiary piercing cases was used inMatheson, supra note 11.

29. The following searches were run for the relevant period:Westlaw searches in ALL STATE and ALL FEDERAL databases. Westlaw Home Page,http://www.westlaw.com.

* SY,DI(pierc! /5 "corporate veil") & da(after 1/l/1990)-yielded 1759 cases* topic(101) /p pierc! /5 "corporate veil" yielded 2275 cases* 101kl.3-yielded 758 cases* 101kl.4-yielded 2519 cases* 101kl.5-yielded 1091 cases* 1OlkI.6-yieldcd 3078 cases* 101kl.7-yielded 1624* Corporate Is "alter ego" (disregard! pierc! Is veil entity form) (single Is business enterprise) &

DA(AFT 1989)-yielded 8739 casesLexis Nexis In-Summary Searches. Lexis Nexis Home Page, http://www.lexisnexis.com.

* (pierc! /5 veil! parent! subsid!)* pierce and corporate veil and (alter ego or instrumentality)

30. Searches constructed for both Lexis and Westlaw resulted in 3,129 piercing cases. However,2,099 of these cases were excluded from the examined database for at least one of the following reasons:the case 1) failed to reach the merits of the piercing issue; 2) had a statutory basis for piercing; 3)pierced to gain jurisdiction over a party; 4) constituted horizontal piercing; or 5) constituted reversepiercing. The remaining 929 cases constitute the overall dataset.

31. This is a significant point of contrast to the Thomspon research, supra note 10, which includesall forms of piercing. Studies involving databases containing all piercing cases are a jumble of variousunrelated situations. They include cases where the legislature has provided a specific statutory testoutside of the common law, such as in environmental litigation. These studies also include bothtraditional single entity piercing as well as corporate group horizontal piercing, where sibling entitiesmay be combined even though the ultimate owners are not held liable. They also capture all forms ofpiercing, including more lenient jurisdictional cases as well as cases that do not truly involve piercing,such as reverse piercing cases that provide benefits to corporate owners, instead of holding them liable.The decision to include only substantive piercing cases in the current project is based in part on thepremise that courts apply different standards for piercing in different piercing contexts. In contrast,examining all groups as one would result in meaningless statistical outcomes.

32. The excluded subset of cases is the subject of a separately published set of statistical findingsfor a parent-subsidiary piercing dataset. See Matheson, supra note I1.

10

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

sought to hold individual owners, not parent corporations, liable.33 In bothdatasets, the relationship between the outcome variable (piercing the corporateveil) and theoretically important predictor variables was analyzed usingdescriptive statistics and logistic regression.

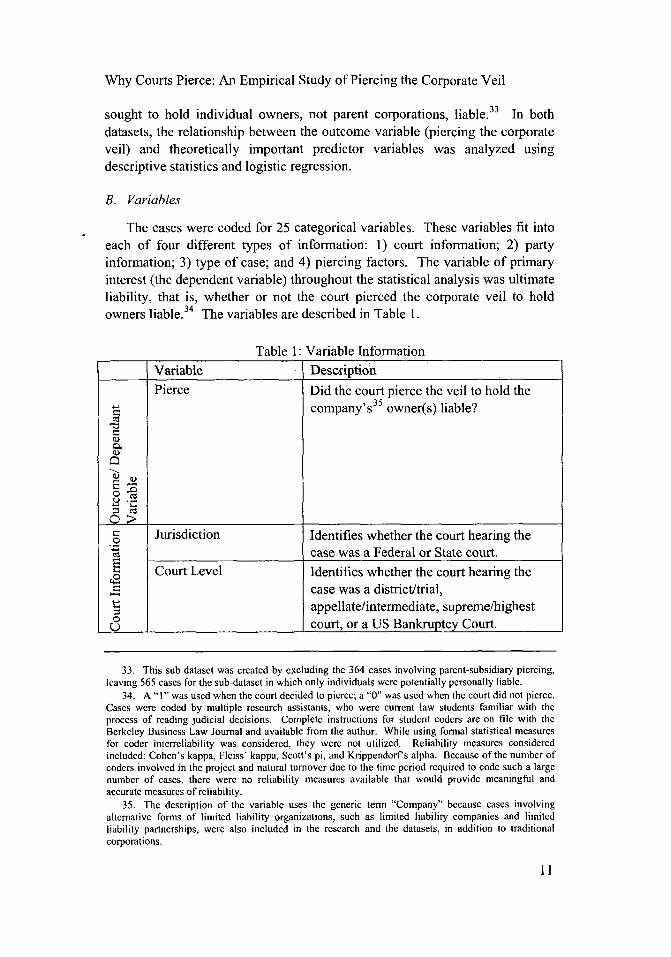

B. Variables

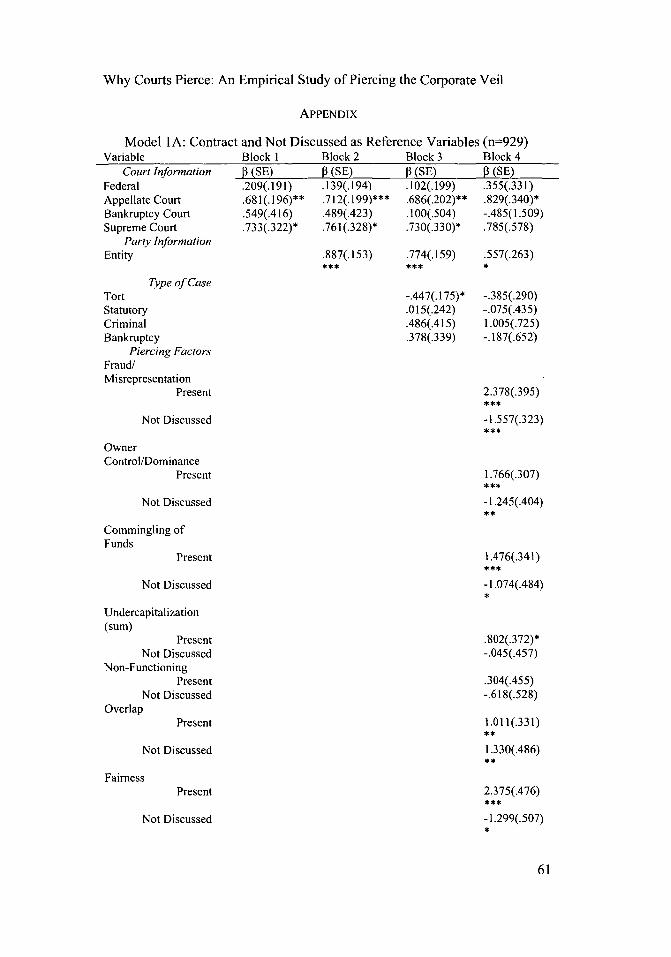

The cases were coded for 25 categorical variables. These variables fit intoeach of four different types of information: 1) court information; 2) partyinformation; 3) type of case; and 4) piercing factors. The variable of primaryinterest (the dependent variable) throughout the statistical analysis was ultimateliability, that is, whether or not the court pierced the corporate veil to holdowners liable. 34 The variables are described in Table 1.

Table 1: Variable InformationVariable Description

Pierce Did the court pierce the veil to hold thecompany's owner(s) liable?

O)

Jurisdiction Identifies whether the court hearing thecase was a Federal or State court.

Court Level Identifies whether the court hearing thecase was a district/trial,appellate/intermediate, supreme/highestcourt, or a US Bankruptcy Court.

33. This sub-datasct was created by excluding the 364 cases involving parent-subsidiary piercing,leaving 565 cases for the sub-dataset in which only individuals were potentially personally liable.

34. A "1" was used when the court decided to pierce; a "0" was used when the court did not pierce.Cases were coded by multiple research assistants, who were current law students familiar with theprocess of reading judicial decisions. Complete instructions for student coders are on file with theBerkeley Business Law Journal and available from the author. While using formal statistical measuresfor coder interreliability was considered, they were not utilized. Reliability measures consideredincluded: Cohen's kappa, Fleiss' kappa, Scott's pi, and Krippendorf's alpha. Because of the number ofcoders involved in the project and natural turnover due to the time period required to code such a largenumber of cases, there were no reliability measures available that would provide meaningful andaccurate measures of reliability.

35. The description of the variable uses the generic term "Company" because cases involvingalternative forms of limited liability organizations, such as limited liability companies and limitedliability partnerships, were also included in the research and the datasets, in addition to traditionalcorporations.

11

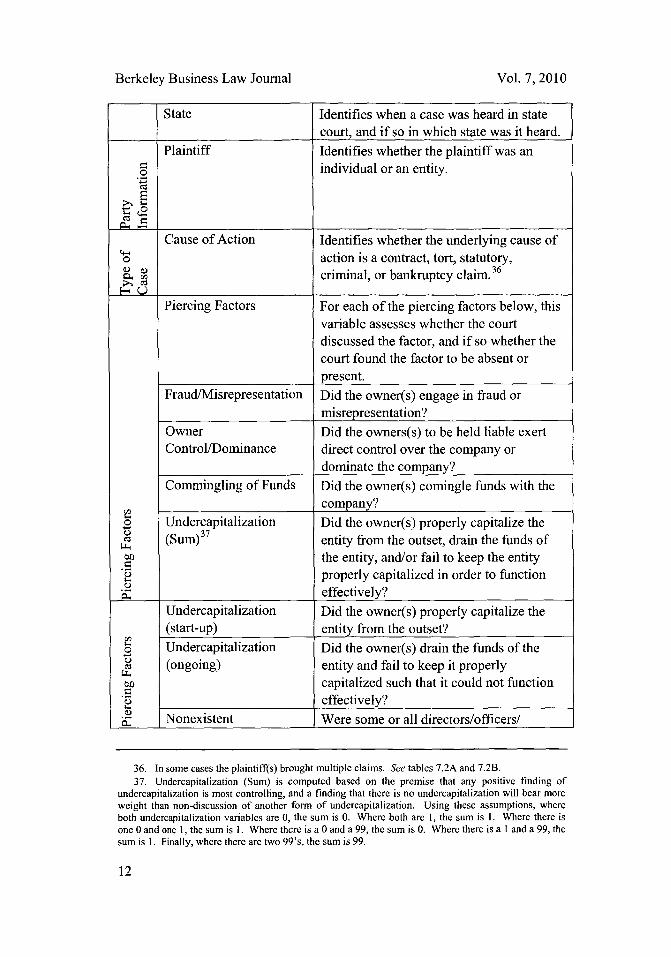

Berkeley Business Law Journal

State Identifies when a case was heard in statecourt, and if so in which state was it heard.

Plaintiff Identifies whether the plaintiff was anindividual or an entity.

0

Cause of Action Identifies whether the underlying cause ofaction is a contract, tort, statutory,criminal, or bankruptcy claim.36

Piercing Factors For each of the piercing factors below, thisvariable assesses whether the courtdiscussed the factor, and if so whether thecourt found the factor to be absent orpresent.

Fraud/Misrepresentation Did the owner(s) engage in fraud ormisrepresentation?

Owner Did the owners(s) to be held liable exertControl/Dominance direct control over the company or

dominate the company?Commingling of Funds Did the owner(s) comingle funds with the

company?'2 Undercapitalization Did the owner(s) properly capitalize the

(Sum)37 entity from the outset, drain the funds ofthe entity, and/or fail to keep the entityproperly capitalized in order to functioneffectively?

Undercapitalization Did the owner(s) properly capitalize the(start-up) entity from the outset?

'2 Undercapitalization Did the owner(s) drain the funds of theLV (ongoing) entity and fail to keep it properly

capitalized such that it could not functioneffectively?

Nonexistent Were some or all directors/officers/

36. In some cases the plaintiff(s) brought multiple claims. See tables 7.2A and 7.2B.37. Undercapitalization (Sum) is computed based on the premise that any positive finding of

undercapitalization is most controlling, and a finding that there is no undercapitalization will bear moreweight than non-discussion of another form of undercapitalization. Using these assumptions, whereboth undercapitalization variables are 0, the sum is 0. Where both are 1, the sum is 1. Where there isone 0 and one 1, the sum is 1. Where there is a 0 and a 99, the sum is 0. Where there is a I and a 99, thesum is 1. Finally, where there are two 99's, the sum is 99.

12

Vol. 7, 2010

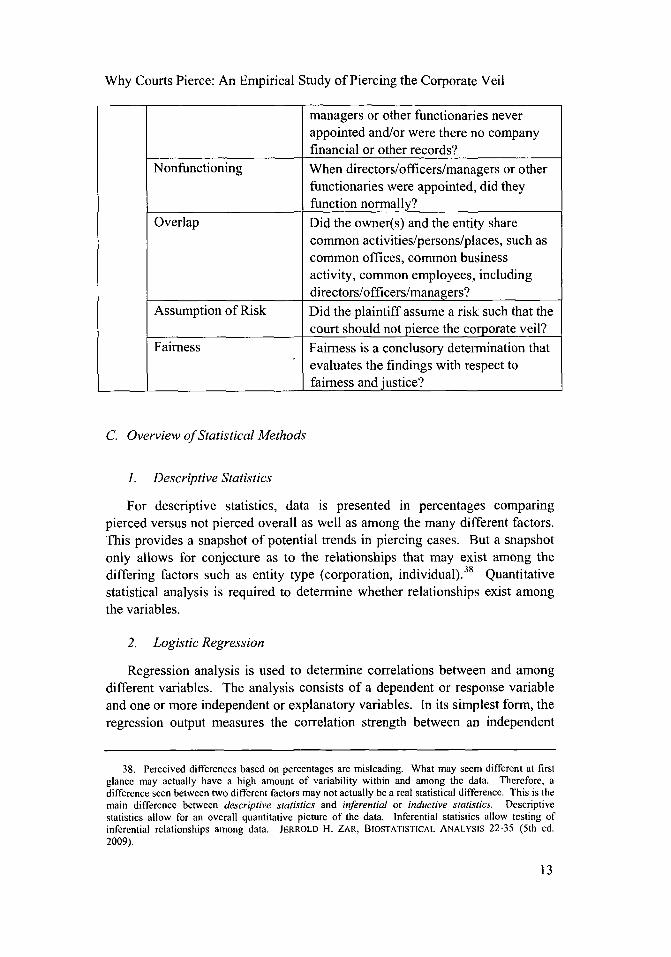

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

managers or other functionaries neverappointed and/or were there no companyfinancial or other records?

Nonfunctioning When directors/officers/managers or otherfunctionaries were appointed, did theyfunction normally?

Overlap Did the owner(s) and the entity sharecommon activities/persons/places, such ascommon offices, common businessactivity, common employees, includingdirectors/officers/managers?

Assumption of Risk Did the plaintiff assume a risk such that thecourt should not pierce the corporate veil?

Fairness Fairness is a conclusory determination thatevaluates the findings with respect tofairness and justice?

C. Overview of Statistical Methods

1. Descriptive Statistics

For descriptive statistics, data is presented in percentages comparingpierced versus not pierced overall as well as among the many different factors.This provides a snapshot of potential trends in piercing cases. But a snapshotonly allows for conjecture as to the relationships that may exist among thediffering factors such as entity type (corporation, individual). Quantitativestatistical analysis is required to determine whether relationships exist amongthe variables.

2. Logistic Regression

Regression analysis is used to determine correlations between and amongdifferent variables. The analysis consists of a dependent or response variableand one or more independent or explanatory variables. In its simplest form, theregression output measures the correlation strength between an independent

38. Perceived differences based on percentages are misleading. What may seem different at firstglance may actually have a high amount of variability within and among the data. Therefore, adifference seen between two different factors may not actually be a real statistical difference. This is themain difference between descriptive statistics and inferential or inductive statistics. Descriptivestatistics allow for an overall quantitative picture of the data. Inferential statistics allow testing ofinferential relationships among data. JERROLD H. ZAR, BIOSTATISTICAL ANALYSIS 22-35 (5th ed.

2009).

13

Berkeley Business Law Journal

variable (e.g. court type) and the dependent variable (e.g. whether a courtpierces). When more than one independent variable exists that can influencethe dependent variable, the tool of choice is multiple regression.

Choosing a statistical method requires an understanding of the limitationsof each method. Our data consist of a dichotomous categorical dependentvariable, meaning that the data fall into one of two qualitative categories-either the court pierces or does not pierce. These types of data are notappropriate for traditional regression analysis as the outcome would lead tononsensical results confounded by weight exerted by only two points.Therefore, to overcome the problems associated with categorical data, the toolof choice is logistic regression. This statistical test determines the amount ofvariance in the dependent variable that can be explained by the independentvariables. Ultimately, the test predicts the odds of an event such as the rate ofpiercing occurring given a set of independent variables.

III. DESCRIPTIVE STATISTICS

A. Piercing the Corporate Veil Generally

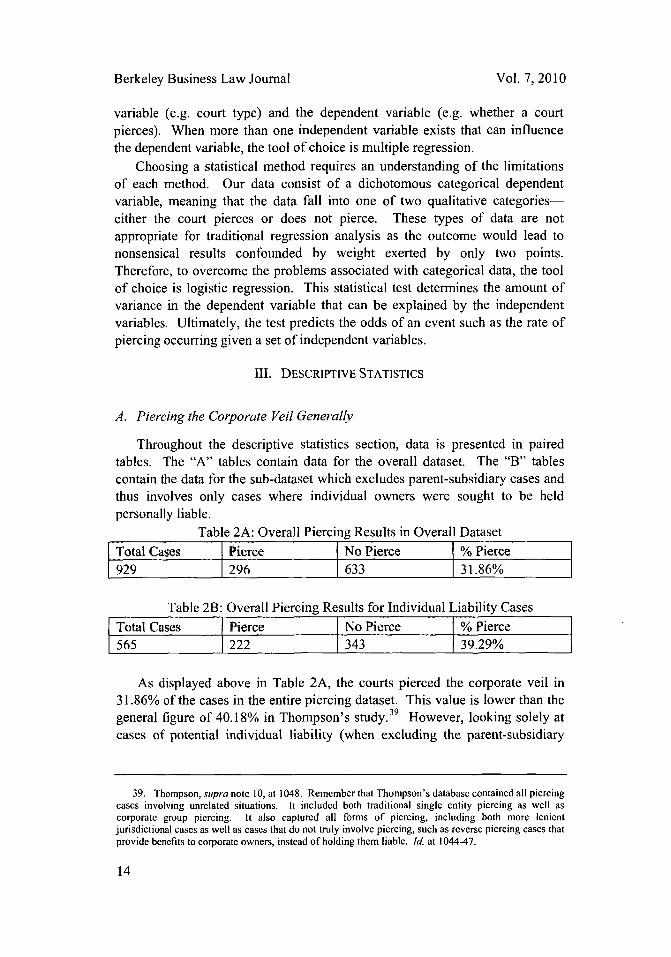

Throughout the descriptive statistics section, data is presented in pairedtables. The "A" tables contain data for the overall dataset. The "B" tablescontain the data for the sub-dataset which excludes parent-subsidiary cases andthus involves only cases where individual owners were sought to be heldpersonally liable.

Table 2A: Overall Piercing Results in Overall DatasetTotal Cases Pierce No Pierce % Pierce929 296 633 31.86%

Table 2B: Overall Piercing Results for Individual Liability CasesTotal Cases Pierce No Pierce % Pierce565 222 343 39.29%

As displayed above in Table 2A, the courts pierced the corporate veil in31.86% of the cases in the entire piercing dataset. This value is lower than thegeneral figure of 40.18% in Thompson's study.39 However, looking solely atcases of potential individual liability (when excluding the parent-subsidiary

39. Thompson, supra note 10, at 1048. Remember that Thompson's database contained all piercingcases involving unrelated situations. It included both traditional single entity piercing as well ascorporate group piercing. It also captured all forms of piercing, including both more lenientjurisdictional cases as well as cases that do not truly involve piercing, such as reverse piercing cases thatprovide benefits to corporate owners, instead of holding them liable. Id. at 1044-47.

14

Vol. 7, 2010

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

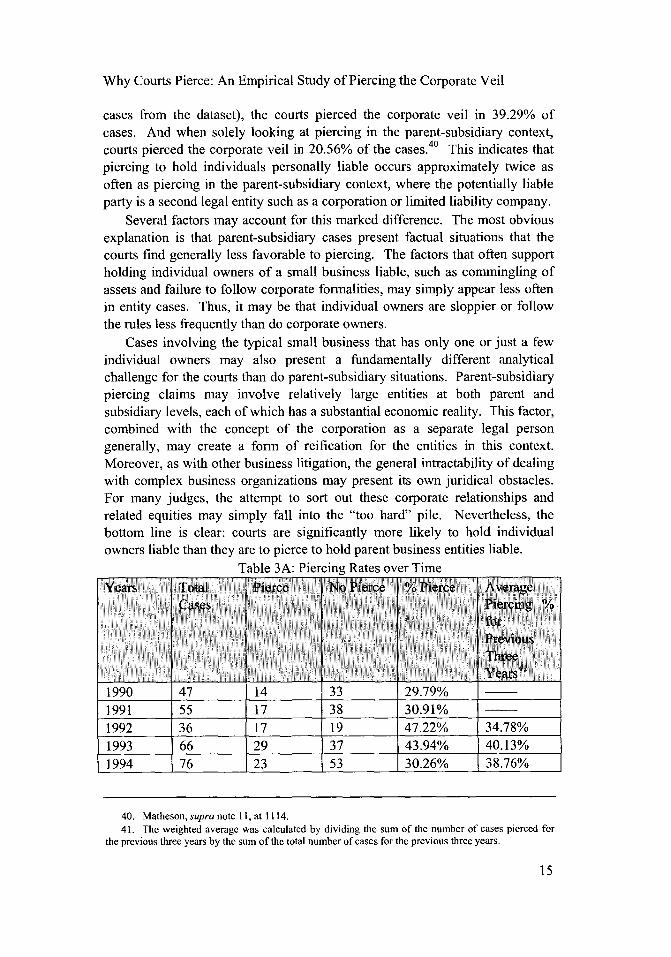

cases from the dataset), the courts pierced the corporate veil in 39.29% ofcases. And when solely looking at piercing in the parent-subsidiary context,courts pierced the corporate veil in 20.56% of the cases. 40 This indicates thatpiercing to hold individuals personally liable occurs approximately twice asoften as piercing in the parent-subsidiary context, where the potentially liableparty is a second legal entity such as a corporation or limited liability company.

Several factors may account for this marked difference. The most obviousexplanation is that parent-subsidiary cases present factual situations that thecourts find generally less favorable to piercing. The factors that often supportholding individual owners of a small business liable, such as commingling ofassets and failure to follow corporate formalities, may simply appear less oftenin entity cases. Thus, it may be that individual owners are sloppier or followthe rules less frequently than do corporate owners.

Cases involving the typical small business that has only one or just a fewindividual owners may also present a fundamentally different analyticalchallenge for the courts than do parent-subsidiary situations. Parent-subsidiarypiercing claims may involve relatively large entities at both parent andsubsidiary levels, each of which has a substantial economic reality. This factor,combined with the concept of the corporation as a separate legal persongenerally, may create a form of reification for the entities in this context.Moreover, as with other business litigation, the general intractability of dealingwith complex business organizations may present its own juridical obstacles.For many judges, the attempt to sort out these corporate relationships andrelated equities may simply fall into the "too hard" pile. Nevertheless, thebottom line is clear: courts are significantly more likely to hold individualowners liable than they are to pierce to hold parent business entities liable.

Thle tA- Piercing Rates over Time

199U '4/ 14 ii -1____ 2 V. / 9"/

1991 55 17 38 30.91% _

1992 36 17 19 47.22% 34.78%1993 66 29 37 43.94% 40.13%1994 76 23 53 30.26% 38.76%

40. Matheson, supra note 11, at 1114.41. The weighted average was calculated by dividing the sum of the number of cases pierced for

the previous three years by the sum of the total number of cases for the previous three years.

15

Berkeley Business Law Journal

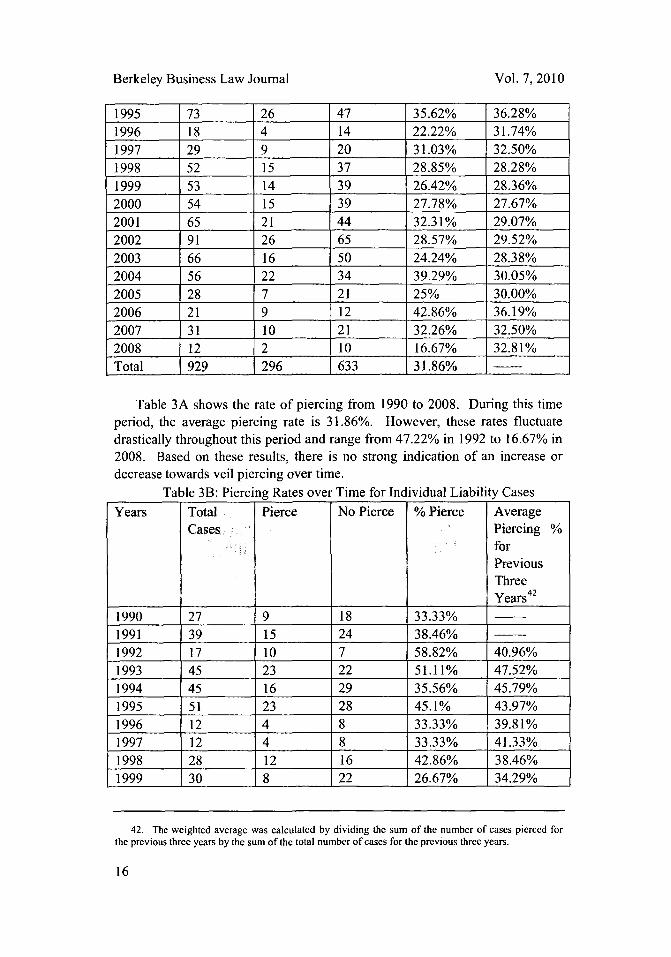

1995 73 26 47 35.62% 36.28%1996 18 4 14 22.22% 31.74%1997 29 9 20 31.03% 32.50%1998 52 15 37 28.85% 28.28%1999 53 14 39 26.42% 28.36%2000 54 15 39 27.78% 27.67%2001 65 21 44 32.31% 29.07%2002 91 26 65 28.57% 29.52%2003 66 16 50 24.24% 28.38%2004 56 22 34 39.29% 30.05%2005 28 7 21 25% 30.00%2006 21 9 12 42.86% 36.19%2007 31 10 21 32.26% 32.50%2008 12 2 10 16.67% 32.81%Total 929 296 633 31.86%

Table 3A shows the rate of piercing from 1990 to 2008. During this timeperiod, the average piercing rate is 31.86%. However, these rates fluctuatedrastically throughout this period and range from 47.22% in 1992 to 16.67% in2008. Based on these results, there is no strong indication of an increase ordecrease towards veil piercing over time.

Table 3B: Piercing Rates over Time for Individual Liability CasesYears Total Pierce No Pierce % Pierce Average

Cases Piercing %forPreviousThreeYears 42

1990 27 9 18 33.33%1991 39 15 24 38.46%1992 17 10 7 58.82% 40.96%1993 45 23 22 51.11% 47.52%1994 45 16 29 35.56% 45.79%1995 51 23 28 45.1% 43.97%1996 12 4 8 33.33% 39.81%1997 12 4 8 33.33% 41.33%1998 28 12 16 42.86% 38.46%1999 30 8 22 26.67% 34.29%

42. The weighted average was calculated by dividing the sum of the number of cases pierced forthe previous three years by the sum of the total number of cases for the previous three years.

16

Vol. 7, 2010

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

2000 26 12 14 46.15% 38.10%2001 40 16 24 40.00% 37.50%2002 62 19 43 30.65% 36.72%2003 43 13 30 30.23% 33.10%2004 36 17 19 47.22% 34.75%2005 19 5 14 26.32% 35.71%2006 5 4 1 80.00% 43.33%

2007 18 10 8 55.56% 45.24%

2008 10 2 8 20.00% 48.48%Total 565 222 343 39.29%

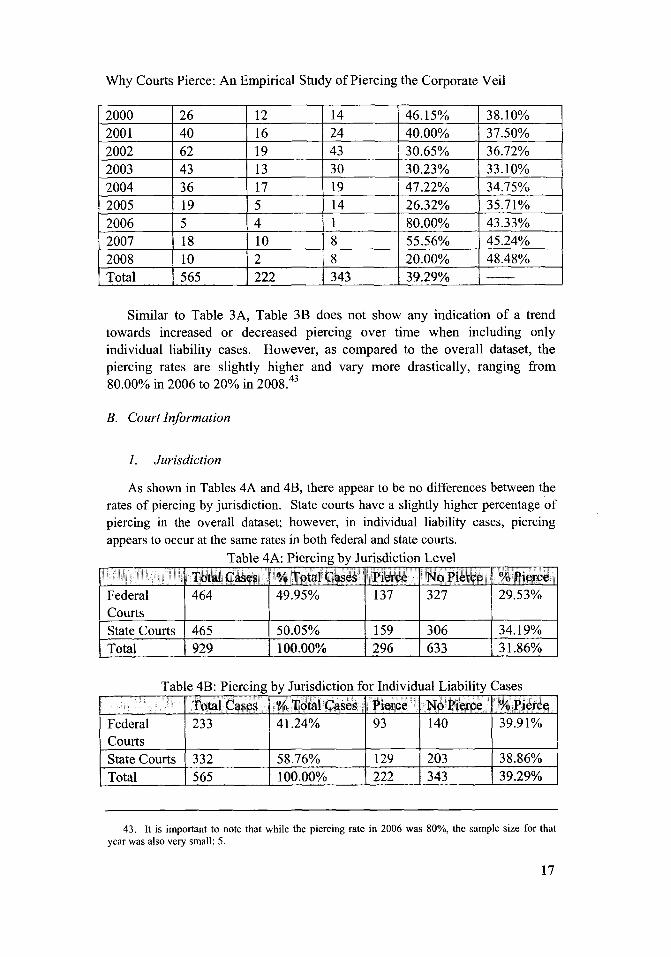

Similar to Table 3A, Table 3B does not show any indication of a trendtowards increased or decreased piercing over time when including onlyindividual liability cases. However, as compared to the overall dataset, thepiercing rates are slightly higher and vary more drastically, ranging from80.00% in 2006 to 20% in 2008.43

B. Court Information

1. Jurisdiction

As shown in Tables 4A and 4B, there appear to be no differences between therates of piercing by jurisdiction. State courts have a slightly higher percentage ofpiercing in the overall dataset; however, in individual liability cases, piercingappears to occur at the same rates in both federal and state courts.

Table 4A: Piercing by Jurisdiction Level

Total Cases % Total Cases Pierce No Pierce % Pierce

Federal 464 49.95% 137 327 29.53%Courts

State Courts 465 50.05% 159 306 34.19%Total 929 100.00% 296 633 31.86%

Table 4B: Piercing by Jurisdiction for Individual Liability Cases

Total Cases % Total Cases Pierce No Pierce % PierceFederal 233 41.24% 93 140 39.91%Courts

State Courts 332 58.76% 129 203 38.86%Total 565 100.00% 222 343 39.29%

43. It is important to note that while the piercing rate in 2006 was 80%, the sample size for thatyear was also very small: 5.

17

Berkeley Business Law Journal

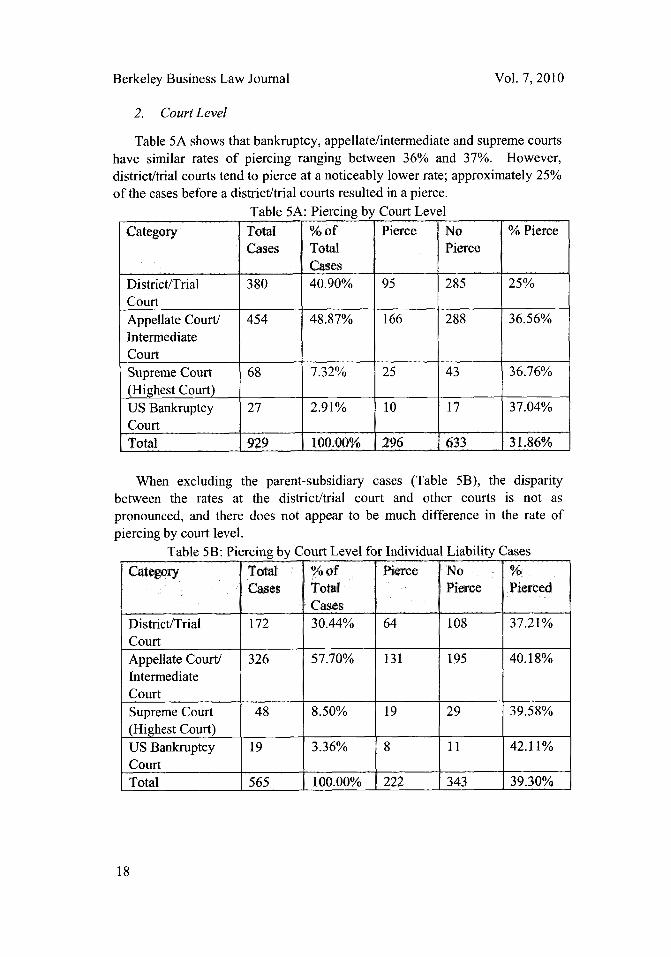

2. Court Level

Table 5A shows that bankruptcy, appellate/intermediate and supreme courtshave similar rates of piercing ranging between 36% and 37%. However,district/trial courts tend to pierce at a noticeably lower rate; approximately 25%of the cases before a district/trial courts resulted in a pierce.

Table 5A: Piercing by Court LevelCategory Total % of Pierce No % Pierce

Cases Total PierceCases

District/Trial 380 40.90% 95 285 25%CourtAppellate Court/ 454 48.87% 166 288 36.56%IntermediateCourtSupreme Court 68 7.32% 25 43 36.76%(Highest Court)US Bankruptcy 27 2.91% 10 17 37.04%Court I I

Total 929 100.00% 296 633 31.86%

When excluding the parent-subsidiary cases (Table 5B), the disparitybetween the rates at the district/trial court and other courts is not aspronounced, and there does not appear to be much difference in the rate ofpiercing by court level.

Table 5B: Piercing by Court Level for Individual Liability CasesCategory Total % of Pierce No %

Cases Total Pierce PiercedCases

District/Trial 172 30.44% 64 108 37.21%Court

Appellate Court/ 326 57.70% 131 195 40.18%IntermediateCourtSupreme Court 48 8.50% 19 29 39.58%(Highest Court)

US Bankruptcy 19 3.36% 8 11 42.11%Court I I I I I

Total 565 100.00% 222 343 39.30%

18

Vol. 7, 2010

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

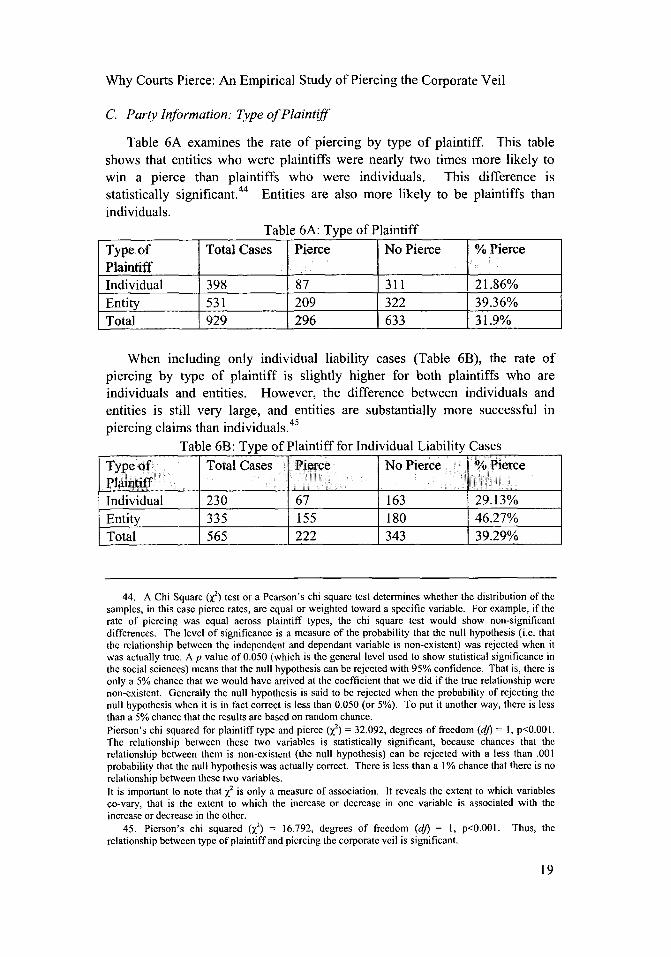

C. Party Information: Type of Plaintiff

Table 6A examines the rate of piercing by type of plaintiff. This tableshows that entities who were plaintiffs were nearly two times more likely towin a pierce than plaintiffs who were individuals. This difference isstatistically significant.44 Entities are also more likely to be plaintiffs thanindividuals.

Table 6A: Type of Plaintiff

Type of Total Cases Pierce No Pierce % PiercePlaintiff

Individual 398 87 311 21.86%Entity 531 209 322 39.36%Total 929 296 633 31.9%

When including only individual liability cases (Table 6B), the rate ofpiercing by type of plaintiff is slightly higher for both plaintiffs who areindividuals and entities. However, the difference between individuals andentities is still very large, and entities are substantially more successful inpiercing claims than individuals. 45

Table 6B: Type of Plaintiff for Individual Liability CasesType of Total Cases Pierce No Pierce % PiercePlaintiff

Individual 230 67 163 29.13%Entity 335 155 180 46.27%Total 565 222 343 39.29%

44. A Chi Square (X2) test or a Pearson's chi square test determines whether the distribution of thesamples, in this case pierce rates, are equal or weighted toward a specific variable. For example, if therate of piercing was equal across plaintiff types, the chi square test would show non-significantdifferences. The level of significance is a measure of the probability that the null hypothesis (i.e. thatthe relationship between the independent and dependant variable is non-existent) was rejected when itwas actually true. A p value of 0.050 (which is the general level used to show statistical significance inthe social sciences) means that the null hypothesis can be rejected with 95% confidence. That is, there isonly a 5% chance that we would have arrived at the coefficient that we did if the true relationship werenon-existent. Generally the null hypothesis is said to be rejected when the probability of rejecting thenull hypothesis when it is in fact correct is less than 0.050 (or 5%). To put it another way, there is lessthan a 5% chance that the results are based on random chance.Pierson's chi squared for plaintiff type and pierce (x2) = 32.092, degrees of freedom (dj) = 1, p<0.001.The relationship between these two variables is statistically significant, because chances that therelationship between them is non-existent (the null hypothesis) can be rejected with a less than .001probability that the null hypothesis was actually correct. There is less than a 1% chance that there is norelationship between these two variables.It is important to note that X2 is only a measure of association. It reveals the extent to which variablesco-vary, that is the extent to which the increase or decrease in one variable is associated with theincrease or decrease in the other.

45. Pierson's chi squared (x) 16.792, degrees of freedom (d) = 1, p<0.001. Thus, therelationship between type of plaintiff and piercing the corporate veil is significant.

19

Berkeley Business Law Journal

D. Type of Case: Underlying Cause ofAction

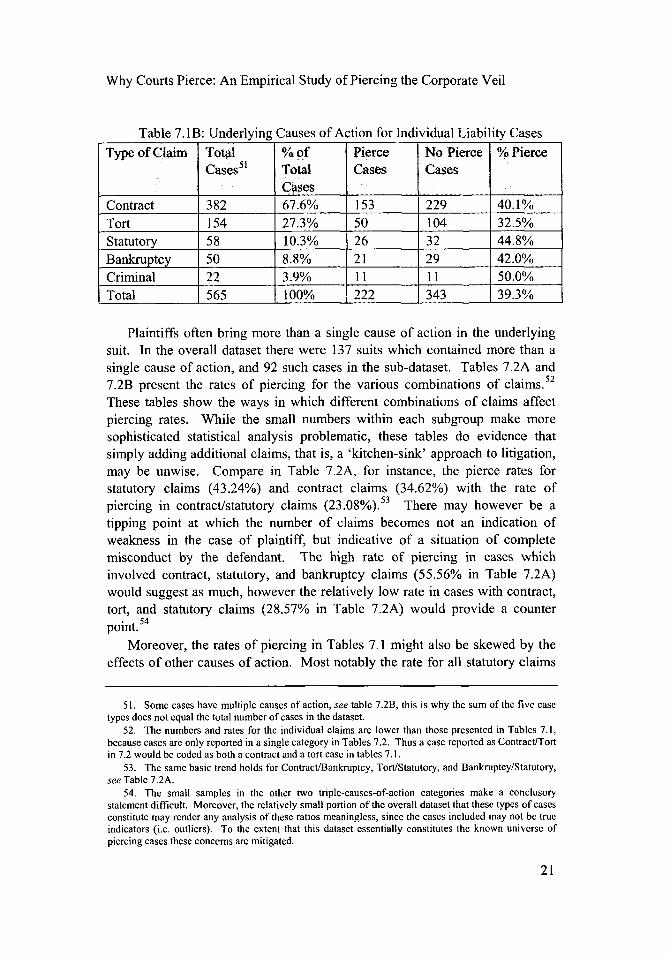

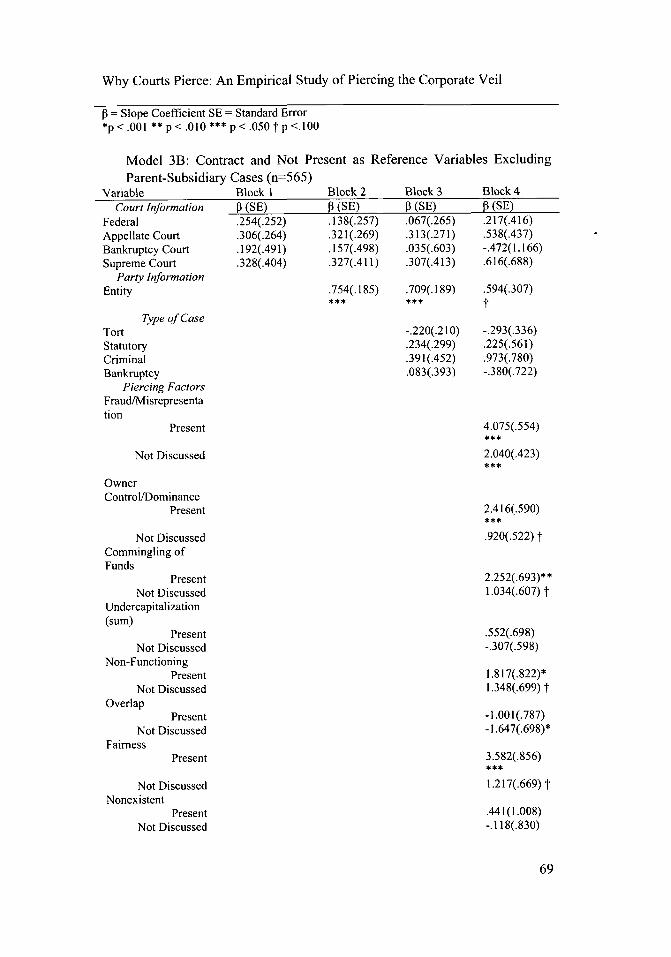

Tables 7.1A and 7.1B analyze cases by underlying cause of action.46 Inboth tables, the rate of piercing is much higher in contract cases than in tortcases. This is consistent with Professor Thompson's finding that courts piercemore often in contract cases than in tort cases.47 It is also interesting to notethat the gap between the rate of piercing in contract versus tort cases appears todecrease when looking only at cases of potential individual liability. In theoverall dataset both tort claims and contract claims have a statisticallysignificant relationship with piercing the corporate veil, however, therelationships between piercing and bankruptcy, criminal, and statutory claimsare not statistically significant.48 In the subset of data that involves onlypotential individual liability cases; only tort claims are statisticallysignificant. 49

Table 7.1A: Underlying Causes of ActionType of Claim Total ON o f Pierce No Pierce % Pierce

Cases 0 Total Cases CasesCases

Contract 598 64.4% 213 385 35.6%Tort 289 31.1% 63 226 21.8%Statutory 105 11.3% 32 73 30.5%Bankruptcy 63 6.8% 25 38 39.7%Criminal 26 2.8% 12 14 46.2%Total 929 100% 296 633 31.86%

46. While there is some overlap between causes of action, the number of cases with multiple causesof action is relatively insubstantial compared to the total number of cases. There are 152 more causes ofaction than cases for Table 7.1 A. Recognizing that some cases may have more than two causes ofaction, there is overlap in a maximum of 16% of the cases. In Table 7.IB, there are 101 more causes ofaction than cases. Therefore there is overlap between causes of action in a maximum of 18% of thecases.

47. Thompson, supra note 10, at 1058.48. Pierson's chi squared (X2) for contract claims in table 7.1A= 10.909, degrees of freedom (d)=

1, p<0.01 0 . Pierson's chi squared (?) for tort claims in table 7.1A = 19.567, degrees of freedom (dj)=1, p<0.001.

49. Pierson's chi squared (X2) for tort claims in table 7.2A = 4.134, degrees of freedom (d) = 1,p< 0 .0 5 0 .

50. Some cases have multiple causes of action, see table 7.2A, this is why the sum of the five casetypes does not equal the total number of cases in the dataset.

20

Vol. 7, 2010

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

Table 7.1B: Underlying Causes of Action for Individual Liability CasesType of Claim Total % of Pierce No Pierce % Pierce

Cases5' Total Cases CasesCases

Contract 382 67.6% 153 229 40.1%Tort 154 27.3% 50 104 32.5%Statutory 58 10.3% 26 32 44.8%Bankruptcy 50 8.8% 21 29 42.0%Criminal 22 3.9% 11 11 50.0%Total 565 100% 222 343 39.3%

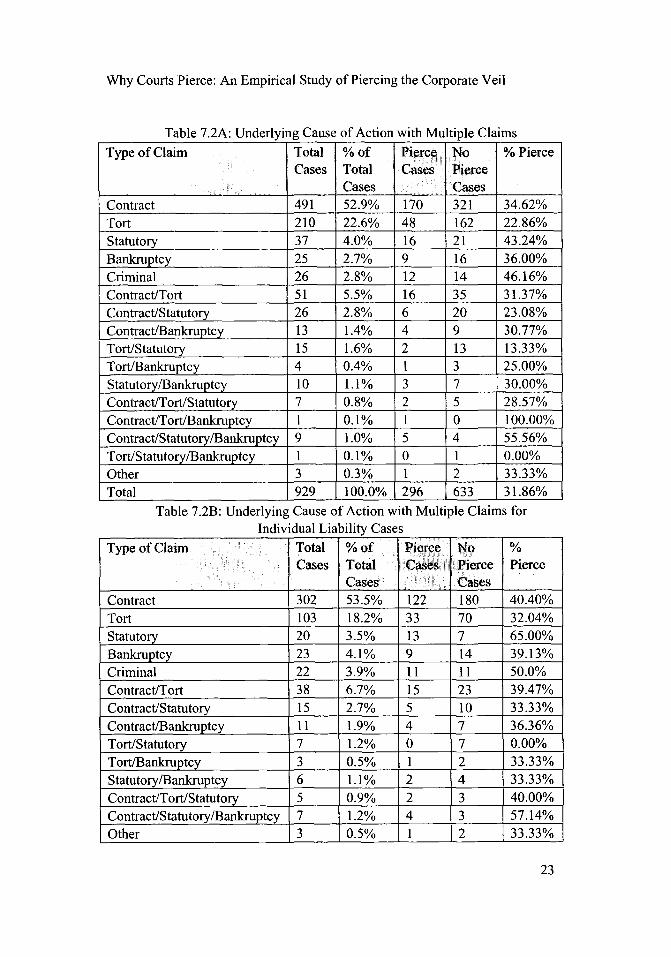

Plaintiffs often bring more than a single cause of action in the underlyingsuit. In the overall dataset there were 137 suits which contained more than asingle cause of action, and 92 such cases in the sub-dataset. Tables 7.2A and7.2B present the rates of piercing for the various combinations of claims. 52

These tables show the ways in which different combinations of claims affectpiercing rates. While the small numbers within each subgroup make moresophisticated statistical analysis problematic, these tables do evidence thatsimply adding additional claims, that is, a 'kitchen-sink' approach to litigation,may be unwise. Compare in Table 7.2A, for instance, the pierce rates forstatutory claims (43.24%) and contract claims (34.62%) with the rate ofpiercing in contract/statutory claims (23.08%).53 There may however be atipping point at which the number of claims becomes not an indication ofweakness in the case of plaintiff, but indicative of a situation of completemisconduct by the defendant. The high rate of piercing in cases whichinvolved contract, statutory, and bankruptcy claims (55.56% in Table 7.2A)would suggest as much, however the relatively low rate in cases with contract,tort, and statutory claims (28.57% in Table 7.2A) would provide a counterpoint. 54

Moreover, the rates of piercing in Tables 7.1 might also be skewed by theeffects of other causes of action. Most notably the rate for all statutory claims

51. Some cases have multiple causes of action, see table 7.2B, this is why the sum of the five casetypes does not equal the total number of cases in the dataset.

52. The numbers and rates for the individual claims are lower than those presented in Tables 7.1,because cases are only reported in a single category in Tables 7.2. Thus a case reported as Contract/Tortin 7.2 would be coded as both a contract and a tort case in tables 7.1.

53. The same basic trend holds for Contract/Bankruptcy, Tort/Statutory, and Bankruptcy/Statutory,see Table 7.2A.

54. The small samples in the other two triple-causes-of-action categories make a conclusorystatement difficult. Moreover, the relatively small portion of the overall dataset that these types of casesconstitute may render any analysis of these ratios meaningless, since the cases included may not be trueindicators (i.e. outliers). To the extent that this dataset essentially constitutes the known universe ofpiercing cases these concerns are mitigated.

21

Berkeley Business Law Journal Vol. 7, 2010

as represented in Table 7.1 is 30.5%, however, when those claims that include astatutory claim and an additional claim(s) are removed the rate jumps to46.16%. This effect is most exaggerated in the incidents of statutory/tortclaims, where only 13.33% of cases result in a pierce. The lowered rate ofpiercing in statutory cases in Table 7.1A then may be a result of the lesssuccessful tort claims. That is, it seems plausible that the tort claimpredominates over the statutory claim. The difference in rates may also beexplainable in terms of the type of plaintiff (see Tables 7.3A-B, 7.4A-B and7.5A-B). The ratio of entity-to-individual plaintiffs for statutory claims is 2-1(25-12, see Tables 7.5A and 7.4A respectively) while the ratio of entity-to-individual plaintiffs for tort/statutory claims is 2-3 (6-9, see Tables 7.5A and7.4A respectively). The decrease in success from statutory claims tostatutory/tort claims may be caused by the increased likelihood of an individualplaintiff bringing a statutory/tort claim.55

Due to the correlation between type of claim and plaintiff type the twovariables were tested for potential multicollinearity. 56 Type of plaintiff wassignificantly correlated with tort claims (Pearson's correlation of -.278 with apvalue of 0.000), contract (Pearson's correlation of .237 with ap value of 0.000),and bankruptcy claims (Pearson's correlation of .078 with ap value of 0.018).Diagnostic statistics suggested that while the variables were highly correlatedthey were within acceptable tolerance levels for collinearity.57

55. For a discussion of why this theory, casting plaintiff type as driving the effects of claim type, isproblematic see infra pp. 27-29.

56. Multicollinearity is a data problem that arises when independent variables are highly correlated.This is a problem for regression analysis because the model attempts to discern the effects of eachindependent variable while controlling for the effects of the other variables. When two, or more,variables are highly correlated the model will not be able to accurately predict how a specific variablewill impact the outcome variable because the model won't be able to disentangle the effects of thecollinear variables. While multicollincarity does not affect the magnitude and direction of therelationship it does inflate the standard errors making it more difficult to achieve statistical significance.PAUL D. ALLISON, LOGISTICAL REGRESSION USING SAS@: THEORY AND APPLICATION § 3.5 (1999),available at http://proquest.safaribooksonline.com/9781580253529.

57. Tolerance for contract is 0.437 with a variance inflation factor (VIF) of 2.399, tolerance for tortis 0.449 with VIF of 2.225, and tolerance for bankruptcy is 0.852 with VIF of 1.173. Multicollinearityin logistic models can be diagnosed by running the model as a linear regression, even though the binaryoutcome variable violates an assumption of linear regression. This is not a problem, because the twokey diagnostic measurements (tolerance and variance inflation factor) are constructed by regressing theindependent variables on each other, and the outcome variable is not included. The first measure foreach variable, tolerance, is constructed by taking the R2 of the regression in which that variable was theoutcome variable and subtracting one. A low tolerance is associated with the presence ofmulticollincarity, because this would mean that the other variables were able to predict the outcome ofthe tested variable. The implication of this finding is that the test variable does not need to be in themodel because the remaining independent variables account for its affects. Like all statistics, there isnot a hard and fast number at which it can be said that the tolerance is so low that multicollinearity ispresent. A tolerance below .40, however, should raise concerns. Id. The second statistic, VIF, is ameasure of "how inflated the variance of the coefficient is, compared to what it would be if the variablewere uncorrelated with any other variable in the model." Id. (internal quotations omitted).

22

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

Table 7.2A: Underlying Cause of Action with Multiple ClaimsType of Claim Total % of Pierce No % Pierce

Cases Total Cases PierceCases Cases

Contract 491 52.9% 170 321 34.62%Tort 210 22.6% 48 162 22.86%Statutory 37 4.0% 16 21 43.24%Bankruptcy 25 2.7% 9 16 36.00%Criminal 26 2.8% 12 14 46.16%Contract/Tort 51 5.5% 16 35 31.37%Contract/Statutory 26 2.8% 6 20 23.08%Contract/Bankruptcy 13 1.4% 4 9 30.77%Tort/Statutory 15 1.6% 2 13 13.33%Tort/Bankruptcy 4 0.4% 1 3 25.00%Statutory/Bankruptcy 10 1.1% 3 7 30.00%Contract/Tort/Statutory 7 0.8% 2 5 28.57%Contract/Tort/Bankruptcy 1 0.1% 1 0 100.00%Contract/Statutory/Bankruptcy 9 1.0% 5 4 55.56%Tort/Statutory/Bankruptcy 1 0.1% 0 1 0.00%Other 3 0.3% 1 2 33.33%Total 929 100.0% 296 633 31.86%

Table 7.2B: Underlying Cause of Action with Multiple Claims forIndividual Liability Cases

Type of Claim Total % of Pierce No %Cases Total Cases Pierce Pierce

Cases CasesContract 302 53.5% 122 180 40.40%Tort 103 18.2% 33 70 32.04%Statutory 20 3.5% 13 7 65.00%Bankruptcy 23 4.1% 9 14 39.13%Criminal 22 3.9% 11 11 50.0%Contract/Tort 38 6.7% 15 23 39.47%Contract/Statutory 15 2.7% 5 10 33.33%Contract/Bankruptcy 11 1.9% 4 7 36.36%Tort/Statutory 7 1.2% 0 7 0.00%Tort/Bankruptcy 3 0.5% 1 2 33.33%Statutory/Bankruptcy 6 1.1% 2 4 33.33%Contract/Tort/Statutory 5 0.9% 2 3 40.00%Contract/Statutory/Bankruptcy 7 1.2% 4 3 57.14%Other 3 0.5% 1 2 33.33%

23

Berkeley Business Law Journal

Total 565 100.0% 222 343 39.29%Table 7.3A: Type of Plaintiff and Underlying Cause of Action

Type of Claim Total # Ind. P % Ind. # Entity P % EntityCases58 Cases P Cases P

Contract 598 204 34.1% 394 65.9%Tort 289 182 63.2% 106 36.8%Statute 105 48 45.7% 57 54.3%Bankruptcy 63 18 28.6% 45 71.4%Criminal 26 10 38.5% 16 61.5%Total 929 398 42.8% 531 57.2%

Table 7.3B: Type of Plaintiff and Underlying Cause of ActionType of Claim Total # Md. P % Id. Entity P % Entity

Cases59 Cases P Cases PContract 382 144 37.7% 238 62.3%Tort 154 89 57.8% 65 42.2%Statute 58 16 27.6% 42 72.4%Bankruptcy 50 15 30% 35 70%Criminal 22 8 36.4% 14 63.6%Total 565 230 40.7% 335 59.3%

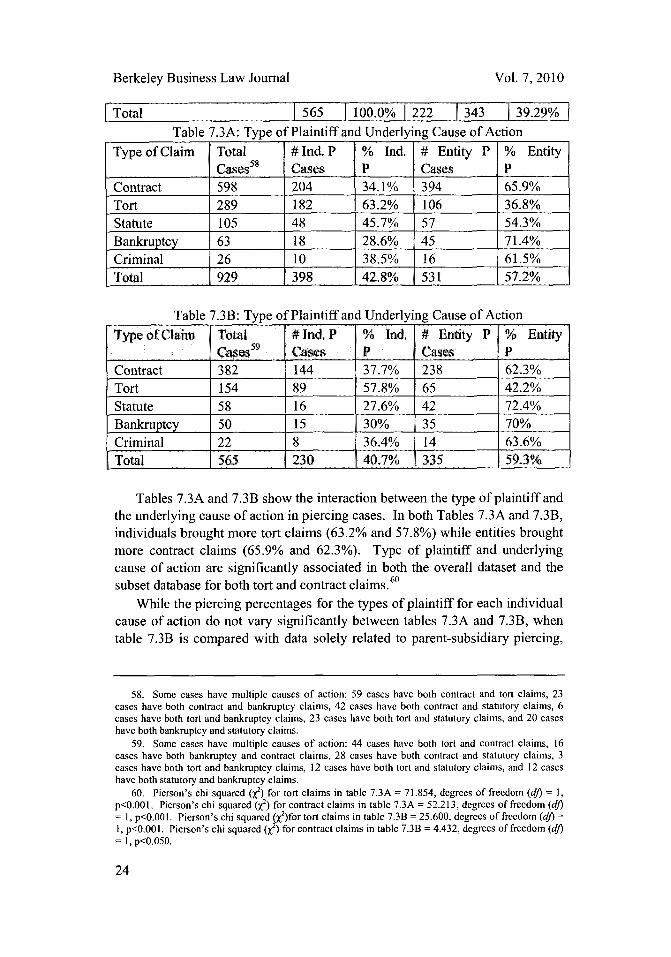

Tables 7.3A and 7.3B show the interaction between the type of plaintiff andthe underlying cause of action in piercing cases. In both Tables 7.3A and 7.3B,individuals brought more tort claims (63.2% and 57.8%) while entities broughtmore contract claims (65.9% and 62.3%). Type of plaintiff and underlyingcause of action are significantly associated in both the overall dataset and thesubset database for both tort and contract claims.60

While the piercing percentages for the types of plaintiff for each individualcause of action do not vary significantly between tables 7.3A and 7.3B, whentable 7.3B is compared with data solely related to parent-subsidiary piercing,

58. Some cases have multiple causes of action: 59 cases have both contract and tort claims, 23cases have both contract and bankruptcy claims, 42 cases have both contract and statutory claims, 6cases have both tort and bankruptcy claims, 23 cases have both tort and statutory claims, and 20 caseshave both bankruptcy and statutory claims.

59. Some cases have multiple causes of action: 44 cases have both tort and contract claims, 16cases have both bankruptcy and contract claims, 28 cases have both contract and statutory claims, 3cases have both tort and bankruptcy claims, 12 cases have both tort and statutory claims, and 12 caseshave both statutory and bankruptcy claims.

60. Pierson's chi squared (X) for tort claims in table 7.3A = 71.854, degrees of freedom (dj) = 1,p<0.001. Pierson's chi squared (X2) for contract claims in table 7.3A = 52.213, degrees of freedom (dj)= 1, p<0.001. Pierson's chi squared (X2)for tort claims in table 7.3B = 25.600, degrees of freedom (d)=1, p<0.001. Pierson's chi squared (X) for contract claims in table 7.3B = 4.432, degrees of freedom (dj)= 1, p<0.050.

24

Vol. 7, 2010

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

there are larger differences. For instance, in the piercing dataset excludingparent-subsidiary piercing, the individuals brought 57.8% of tort cases while inparent-subsidiary cases they brought 70% of tort cases.6

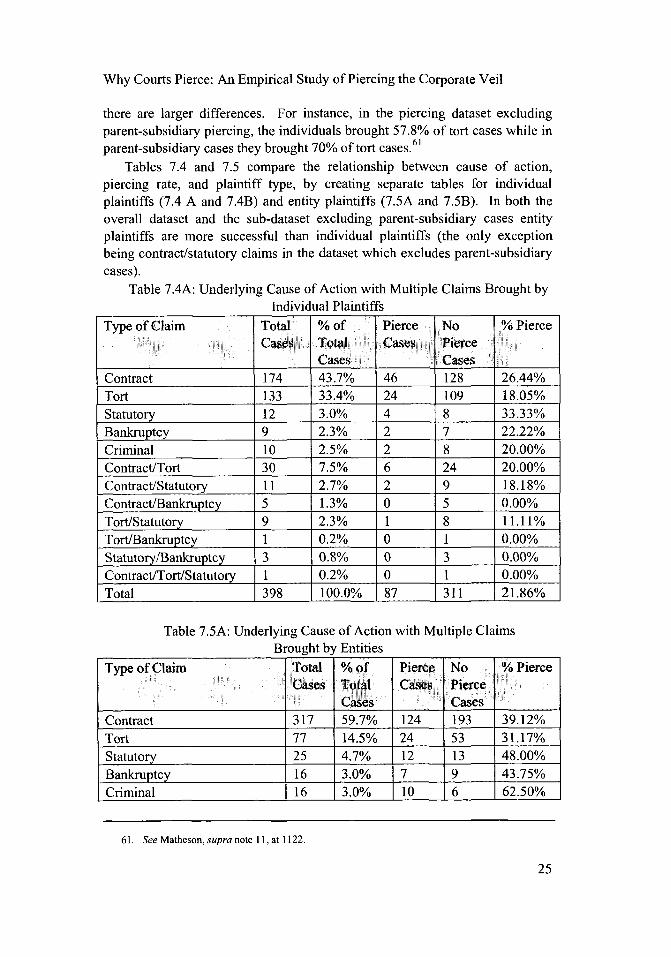

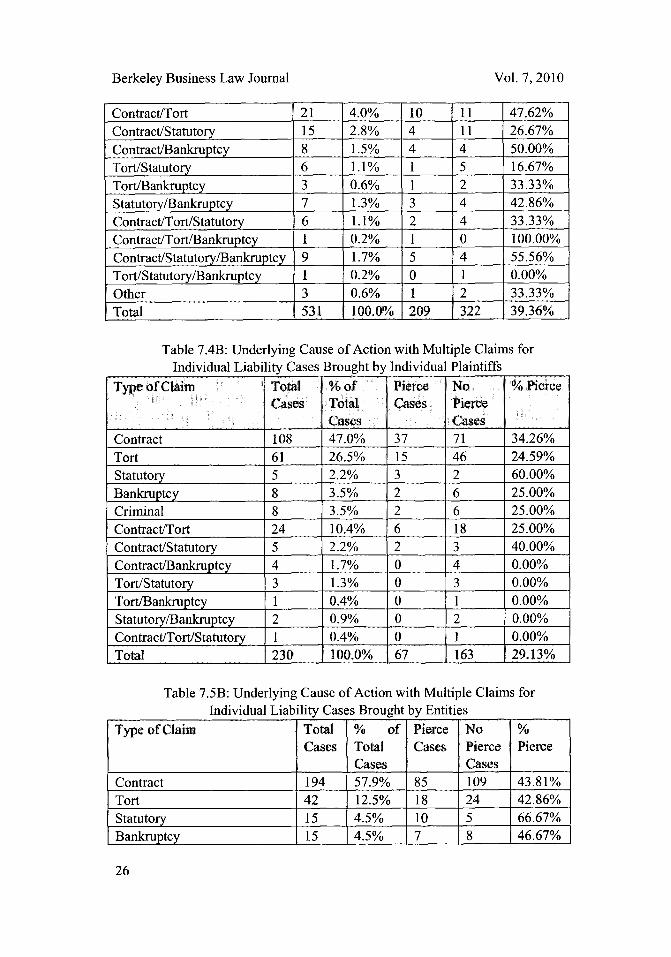

Tables 7.4 and 7.5 compare the relationship between cause of action,piercing rate, and plaintiff type, by creating separate tables for individualplaintiffs (7.4 A and 7.4B) and entity plaintiffs (7.5A and 7.5B). In both theoverall dataset and the sub-dataset excluding parent-subsidiary cases entityplaintiffs are more successful than individual plaintiffs (the only exceptionbeing contract/statutory claims in the dataset which excludes parent-subsidiarycases).

Table 7.4A: Underlying Cause of Action with Multiple Claims Brought byIndividual Plaintiffs

Type of Claim Total % of Pierce No % PierceCases Total Cases Pierce

Cases Cases

Contract 174 43.7% 46 128 26.44%Tort 133 33.4% 24 109 18.05%Statutory 12 3.0% 4 8 33.33%Bankruptcy 9 2.3% 2 7 22.22%Criminal 10 2.5% 2 8 20.00%

Contract/Tort 30 7.5% 6 24 20.00%Contract/Statutory 11 2.7% 2 9 18.18%Contract/Bankruptcy 5 1.3% 0 5 0.00%Tort/Statutory 9 2.3% 1 8 11.11%Tort/Bankruptcy 1 0.2% 0 1 0.00%Statutory/Bankruptcy 3 0.8% 0 3 0.00%Contract/Tort/Statutory 1 0.2% 0 1 0.00%Total 398 100.0% 87 311 21.86%

Table 7.5A: Underlying Cause of Action with Multiple ClaimsBrought by Entities

Type of Claim Total % of Pierce No % PierceCases Total Cases Pierce

Cases CasesContract 317 59.7% 124 193 39.12%Tort 77 14.5% 24 53 31.17%Statutory 25 4.7% 12 13 48.00%Bankruptcy 16 3.0% 7 9 43.75%Criminal 16 3.0% 10 6 62.50%

61. See Matheson, supra note 11, at 1122.

25

Berkeley Business Law Journal

Contract/Tort 21 4.0% 10 11 47.62%Contract/Statutory 15 2.8% 4 11 26.67%Contract/Bankruptcy 8 1.5% 4 4 50.00%Tort/Statutory 6 1.1% 1 5 16.67%Tort/Bankruptcy 3 0.6% 1 2 33.33%Statutory/Bankruptcy 7 1.3% 3 4 42.86%Contract/Tort/Statutory 6 1.1% 2 4 33.33%Contract/Tort/Bankruptcy 1 0.2% 1 0 100.00%Contract/Statutory/Bankruptcy 9 1.7% 5 4 55.56%Tort/Statutory/Bankruptcy 1 0.2% 0 1 0.00%Other 3 0.6% 1 2 33.33%Total 531 100.0% 209 322 39.36%

Table 7.4B: Underlying Cause of Action with Multiple Claims forIndividual Liability Cases Brought by Individual Plaintiffs

Type of Claim Total % of Pierce No % PierceCases Total Cases Pierce

SCases CasesContract 108 47.0% 37 71 34.26%Tort 61 26.5% 15 46 24.59%Statutory 5 2.2% 3 2 60.00%Bankruptcy 8 3.5% 2 6 25.00%Criminal 8 3.5% 2 6 25.00%Contract/Tort 24 10.4% 6 18 25.00%Contract/Statutory 5 2.2% 2 3 40.00%Contract/Bankruptcy 4 1.7% 0 4 0.00%Tort/Statutory 3 1.3% 0 3 0.00%Tort/Bankruptcy 1 0.4% 0 1 0.00%Statutory/Bankruptcy 2 0.9% 0 2 0.00%Contract/Tort/Statutory 1 0.4% 0 1 0.00%Total 230 100.0% 67 163 29.13%

Table 7.5B: Underlying Cause of Action with Multiple Claims forIndividual Liability Cases Brought by Entities

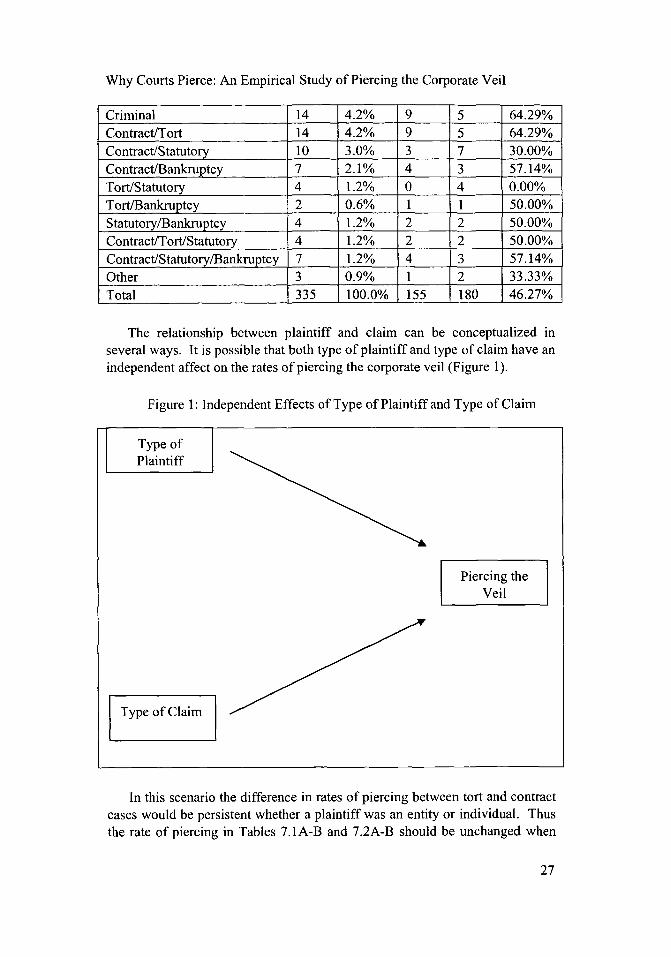

Type of Claim Total % of Pierce No %Cases Total Cases Pierce Pierce

Cases CasesContract 194 57.9% 85 109 43.81%Tort 42 12.5% 18 24 42.86%Statutory 15 4.5% 10 5 66.67%Bankruptcy 15 4.5% 7 8 46.67%

26

Vol. 7, 2010

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

Criminal 14 4.2% 9 5 64.29%Contract/Tort 14 4.2% 9 5 64.29%Contract/Statutory 10 3.0% 3 7 30.00%Contract/Bankruptcy 7 2.1% 4 3 57.14%Tort/Statutory 4 1.2% 0 4 0.00%Tort/Bankruptcy 2 0.6% 1 1 50.00%Statutory/Bankruptcy 4 1.2% 2 2 50.00%Contract/Tort/Statutory 4 1.2% 2 2 50.00%Contract/Statutory/Bankruptcy 7 1.2% 4 3 57.14%Other 3 0.9% 1 2 33.33%Total 335 100.0% 155 180 46.27%

The relationship between plaintiff and claim can be conceptualized inseveral ways. It is possible that both type of plaintiff and type of claim have anindependent affect on the rates of piercing the corporate veil (Figure 1).

Figure 1: Independent Effects of Type of Plaintiff and Type of Claim

Type ofPlaintiff

Type of Claim

In this scenario the difference in rates of piercing between tort and contractcases would be persistent whether a plaintiff was an entity or individual. Thusthe rate of piercing in Tables 7.1A-B and 7.2A-B should be unchanged when

27

Piercing theVeil

Berkeley Business Law Journal

plaintiff type is introduced. The rates of piercing reported in Tables 7.4A-Band 7.5A-B however show that there is some interaction between the type ofclaim brought and the type of plaintiff bringing the claim.

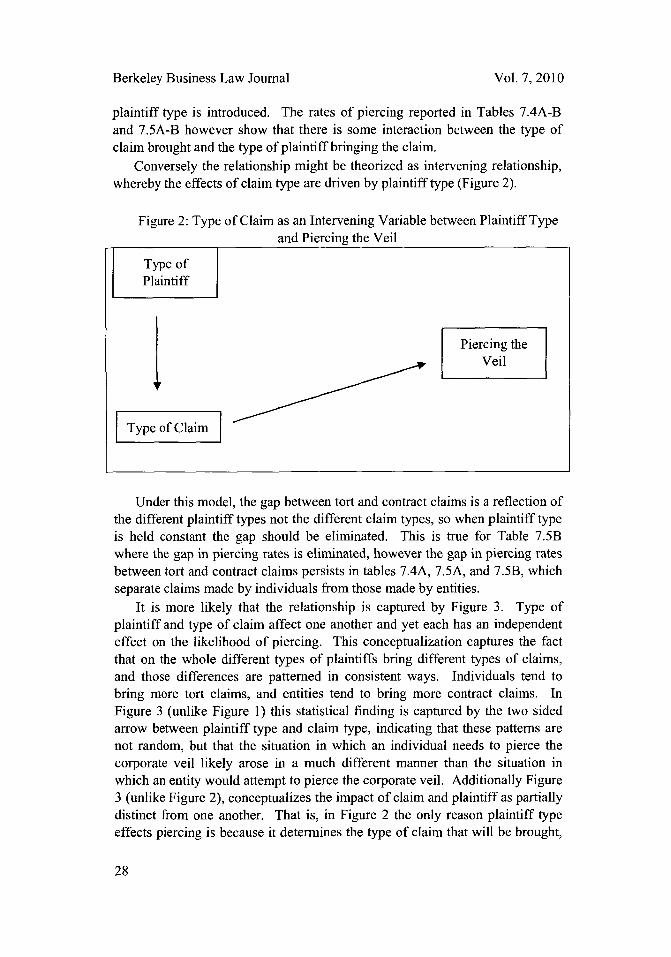

Conversely the relationship might be theorized as intervening relationship,whereby the effects of claim type are driven by plaintiff type (Figure 2).

Figure 2: Type of Claim as an Intervening Variable between Plaintiff Typeand Piercing the Veil

Type ofPlaintiff

Piercing theVeil

Type of Claim

Under this model, the gap between tort and contract claims is a reflection ofthe different plaintiff types not the different claim types, so when plaintiff typeis held constant the gap should be eliminated. This is true for Table 7.5Bwhere the gap in piercing rates is eliminated, however the gap in piercing ratesbetween tort and contract claims persists in tables 7.4A, 7.5A, and 7.5B, whichseparate claims made by individuals from those made by entities.

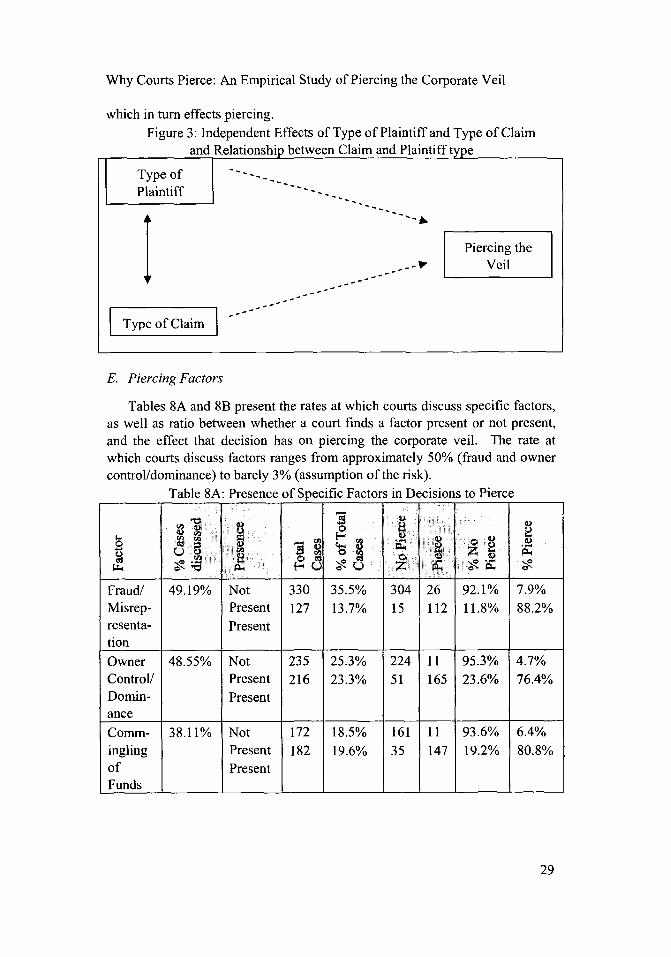

It is more likely that the relationship is captured by Figure 3. Type ofplaintiff and type of claim affect one another and yet each has an independenteffect on the likelihood of piercing. This conceptualization captures the factthat on the whole different types of plaintiffs bring different types of claims,and those differences are patterned in consistent ways. Individuals tend tobring more tort claims, and entities tend to bring more contract claims. InFigure 3 (unlike Figure 1) this statistical finding is captured by the two sidedarrow between plaintiff type and claim type, indicating that these patterns arenot random, but that the situation in which an individual needs to pierce thecorporate veil likely arose in a much different manner than the situation inwhich an entity would attempt to pierce the corporate veil. Additionally Figure3 (unlike Figure 2), conceptualizes the impact of claim and plaintiff as partiallydistinct from one another. That is, in Figure 2 the only reason plaintiff typeeffects piercing is because it determines the type of claim that will be brought,

28

Vol. 7, 2010

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

which in turn effects piercing.

Figure 3: Independent Effects of Type of Plaintiff and Type of Claimand Relationship between Claim and Plaintiff type

Type of

Plaintiff

Piercing theI VeilType of Claim

E. Piercing Factors

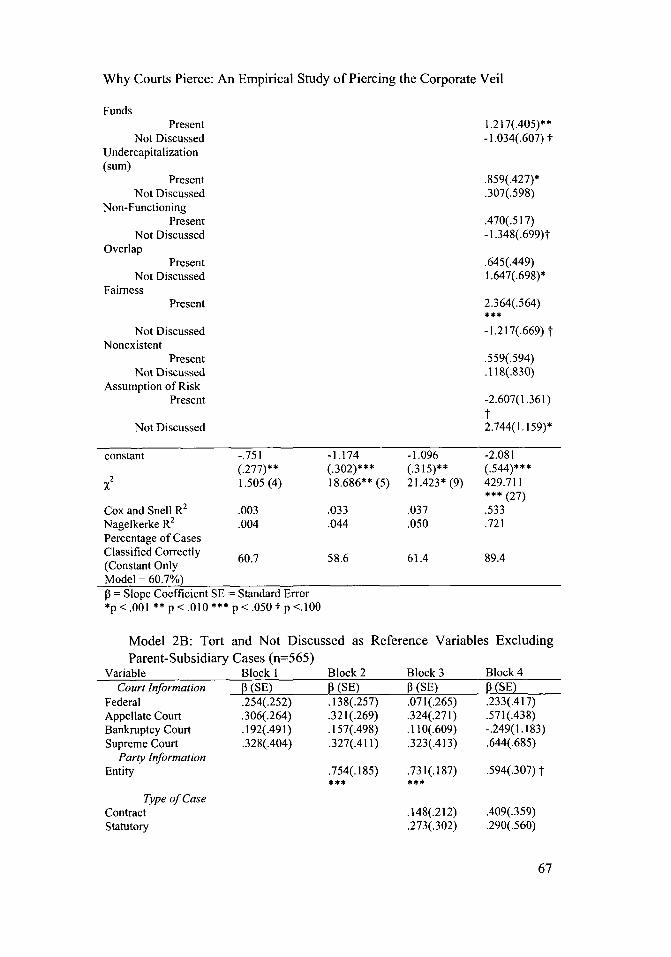

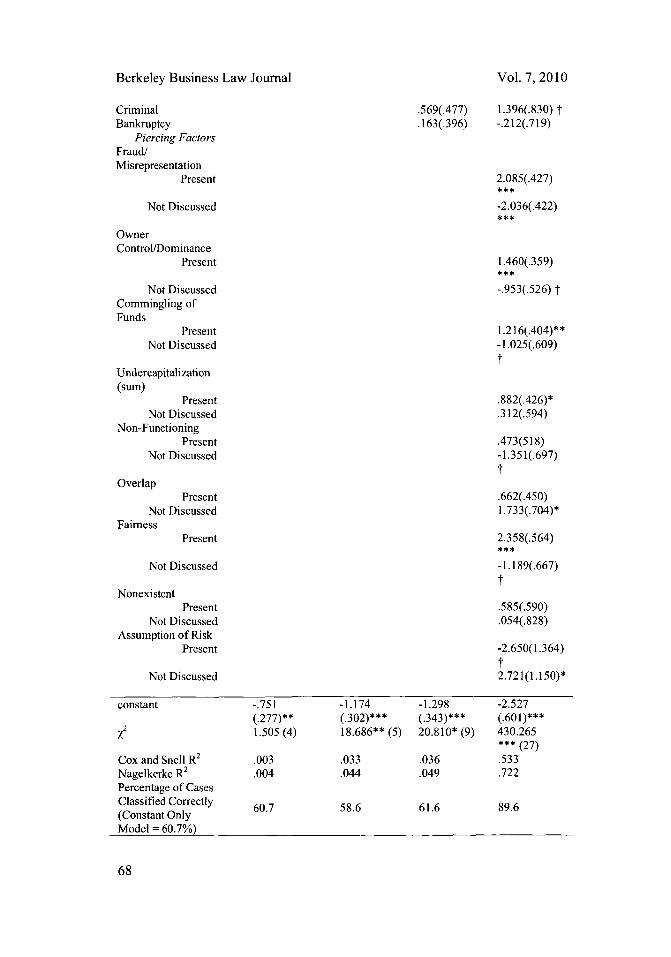

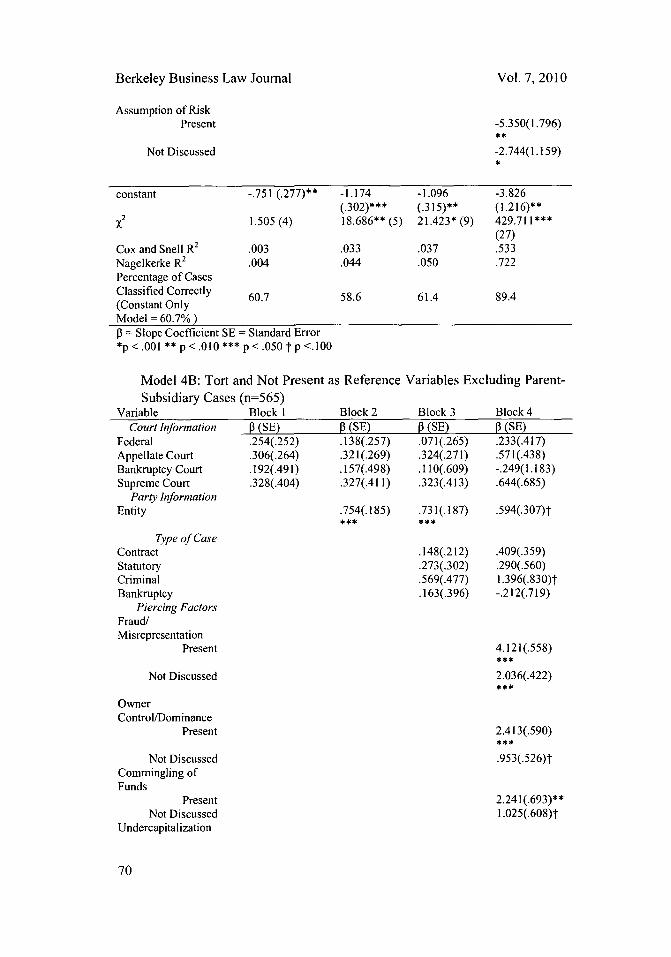

Tables 8A and 8B present the rates at which courts discuss specific factors,as well as ratio between whether a court finds a factor present or not present,and the effect that decision has on piercing the corporate veil. The rate atwhich courts discuss factors ranges from approximately 50% (fraud and ownercontrol/dominance) to barely 3% (assumption of the risk).

Table 8A: Presence of Specific Factors in Decisions to Pierce

20

Fraud/ 49.19% Not 330 35.5% 304 26 92.1% 7.9%Misrep- Present 127 13.7% 15 112 11.8% 88.2%resenta- Presenttion

Owner 48.55% Not 235 25.3% 224 11 95.3% 4.7%Control/ Present 216 23.3% 51 165 23.6% 76.4%Domin- Presentance

Comm- 38.11% Not 172 18.5% 161 11 93.6% 6.4%ingling Present 182 19.6% 35 147 19.2% 80.8%of PresentFunds

29

Berkeley Business Law Journal

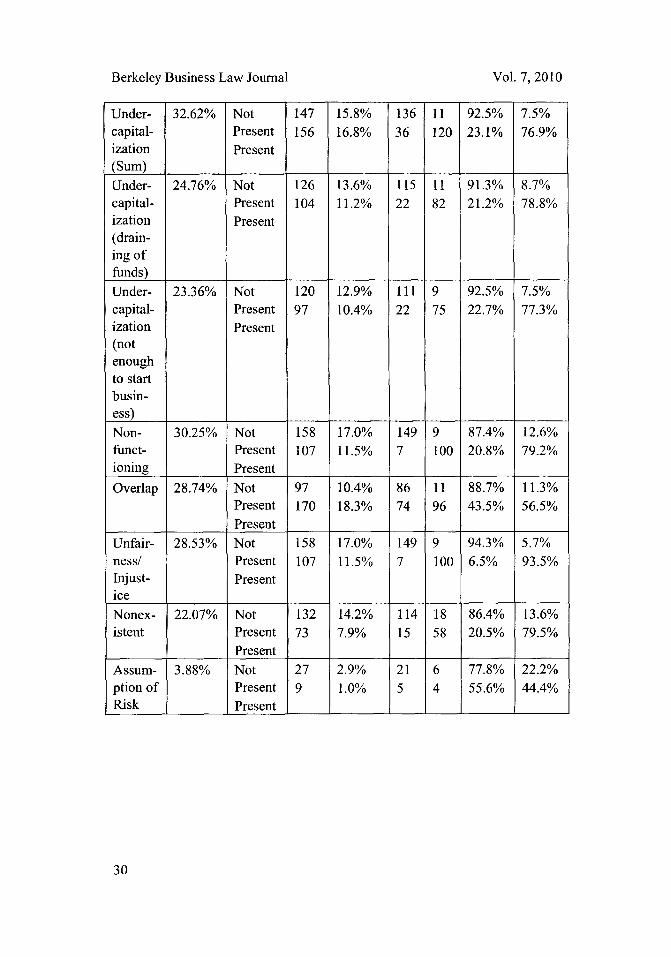

Under- 32.62% Not 147 15.8% 136 11 92.5% 7.5%capital- Present 156 16.8% 36 120 23.1% 76.9%ization Present(Sum)

Under- 24.76% Not 126 13.6% 115 11 91.3% 8.7%capital- Present 104 11.2% 22 82 21.2% 78.8%ization Present(drain-ing offunds)Under- 23.36% Not 120 12.9% 111 9 92.5% 7.5%capital- Present 97 10.4% 22 75 22.7% 77.3%ization Present(notenoughto startbusin-ess)

Non- 30.25% Not 158 17.0% 149 9 87.4% 12.6%funct- Present 107 11.5% 7 100 20.8% 79.2%ioning Present

Overlap 28.74% Not 97 10.4% 86 11 88.7% 11.3%Present 170 18.3% 74 96 43.5% 56.5%Present

Unfair- 28.53% Not 158 17.0% 149 9 94.3% 5.7%ness/ Present 107 11.5% 7 100 6.5% 93.5%Injust- PresenticeNonex- 22.07% Not 132 14.2% 114 18 86.4% 13.6%istent Present 73 7.9% 15 58 20.5% 79.5%

PresentAssum- 3.88% Not 27 2.9% 21 6 77.8% 22.2%ption of Present 9 1.0% 5 4 55.6% 44.4%Risk Present

30

Vol. 7, 2010

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

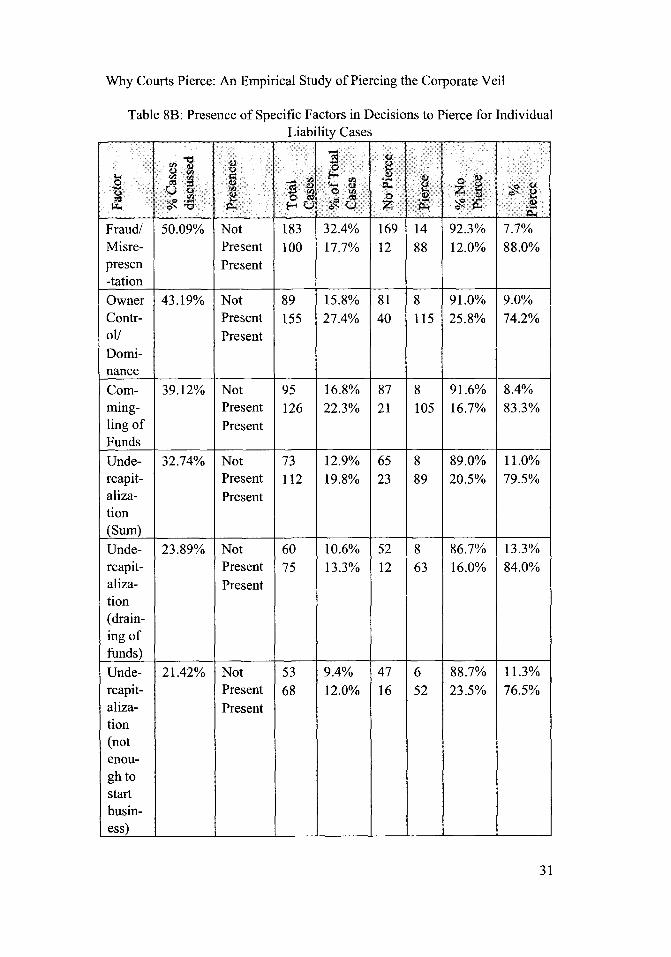

Table 8B: Presence of Specific Factors in Decisions to Pierce for IndividualLiability Cases

Fraud/ 50.09% Not 183 32.4% 169 14 92.3% 7.7%Misre- Present 100 17.7% 12 88 12.0% 88.0%presen Present-tation

Owner 43.19% Not 89 15.8% 81 8 91.0% 9.0%Contr- Present 155 27.4% 40 115 25.8% 74.2%ol/ PresentDomi-nance

Com- 39.12% Not 95 16.8% 87 8 91.6% 8.4%ming- Present 126 22.3% 21 105 16.7% 83.3%ling of PresentFunds

Unde- 32.74% Not 73 12.9% 65 8 89.0% 11.0%reapit- Present 112 19.8% 23 89 20.5% 79.5%aliza- Presenttion(Sum)Unde- 23.89% Not 60 10.6% 52 8 86.7% 13.3%reapit- Present 75 13.3% 12 63 16.0% 84.0%aliza- Presenttion(drain-ing offunds)

Unde- 21.42% Not 53 9.4% 47 6 88.7% 11.3%rcapit- Present 68 12.0% 16 52 23.5% 76.5%aliza- Presenttion(notenou-gh tostartbusin-ess)

31

Berkeley Business Law Journal

Non- 31.15% Not 93 16.5% 80 13 86.0% 14.0%funct- Present 83 14.7% 17 66 20.5% 79.5%ioning PresentOver- 19.29% Not 38 6.7% 31 7 81.6% 18.4%lap Present 71 12.6% 22 49 31.0% 69.0%

PresentUnfai- 26.55% Not 70 12.4% 65 5 92.9% 7.1%mess/ Present 80 14.2% 5 75 6.3% 93.8%Injust- PresenticeNone- 20.71% Not 61 10.8% 51 10 83.6% 16.4%xistent Present 56 9.9% 10 46 17.9% 82.1%

Present

Assu- 3.89% Not 15 2.7% 12 3 80.0% 20.0%mption Present 7 1.2% 5 2 71.4% 28.6%of PresentRisk

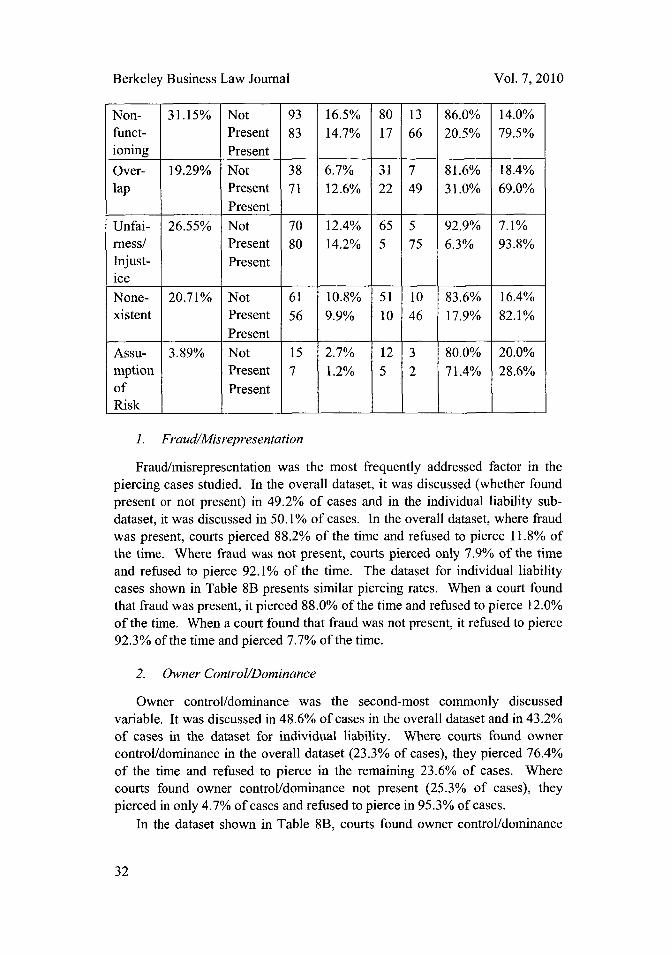

1. Fraud/Misrepresentation

Fraud/misrepresentation was the most frequently addressed factor in thepiercing cases studied. In the overall dataset, it was discussed (whether foundpresent or not present) in 49.2% of cases and in the individual liability sub-dataset, it was discussed in 50.1% of cases. In the overall dataset, where fraudwas present, courts pierced 88.2% of the time and refused to pierce 11.8% ofthe time. Where fraud was not present, courts pierced only 7.9% of the timeand refused to pierce 92.1% of the time. The dataset for individual liabilitycases shown in Table 8B presents similar piercing rates. When a court foundthat fraud was present, it pierced 88.0% of the time and refused to pierce 12.0%of the time. When a court found that fraud was not present, it refused to pierce92.3% of the time and pierced 7.7% of the time.

2. Owner Control/Dominance

Owner control/dominance was the second-most commonly discussedvariable. It was discussed in 48.6% of cases in the overall dataset and in 43.2%of cases in the dataset for individual liability. Where courts found ownercontrol/dominance in the overall dataset (23.3% of cases), they pierced 76.4%of the time and refused to pierce in the remaining 23.6% of cases. Wherecourts found owner control/dominance not present (25.3% of cases), theypierced in only 4.7% of cases and refused to pierce in 95.3% of cases.

In the dataset shown in Table 8B, courts found owner control/dominance

32

Vol. 7, 2010

Why Courts Pierce: An Empirical Study of Piercing the Corporate Veil

present in 27.4% of all cases in the sub-dataset and not present in 15.8% ofcases. Where courts found it to be present, they pierced 74.2% of the time,refusing to pierce the remaining 25.8% of the time. Where courts found ownercontrol/dominance not present, they refused to pierce in 91.0% of cases andpierced in only the remaining 9.0% of cases.

3. Commingling of Funds

In the overall dataset, courts discussed commingling of funds in over a thirdof the cases (38.1%). Courts discussed commingling in a similar proportion inthe individual liability dataset (39.1%). In the overall dataset in Table 8A,commingling was found to be present in 19.6% of the cases, and when it waspresent, the court pierced 80.8% of the time and refused to pierce only 19.2%of the time. When commingling was found not to be present in 18.5% of thecases, courts refused to pierce in 93.6% of the cases and pierced in 6.4% of thecases.

In the dataset shown in Table 8B, courts found commingling in 22.3% ofcases. In 83.3% of those cases courts pierced whereas in 16.7% of those casesthey declined to hold owners liable. In the 16.8% of cases where a court foundthat there was no commingling, it refused to pierce 91.6% of the time andpierced only 8.4% of the time.

4. Undercapitalization

Undercapitalization is discussed in three variables below: (1)Undercapitalization (not enough to start a business); (2) Undercapitalization(draining of funds); and (3) Undercapitalization (Sum). 62 Undercapitalization(Sum) was created during the analysis process. Because a court does notalways distinguish which type of undercapitalization is being discussed,Undercapitalization (Sum) eliminates difficulties posed by this lack of clarityby combining the two variables. 63

In the overall dataset shown in Table 8A, insufficient funds to start abusiness are discussed in 24.8% of the cases. Where it is discussed, the courtfound that it was present in 13.6% of cases, but not present in 11.2% of cases.Of the cases where the court found insufficient funds to start a business, itpierced in 77.3% of cases and refused to pierce in 22.7% of cases. Where thecourt found that there were not insufficient funds to start the business, it refusedto pierce in 92.5% of those cases and pierced in 7.5% of those cases.

In the dataset where liability was sought to be imposed on individualowners, shown in Table 8B, the court discussed insufficiency of funds in 21.4%

62. Table 1.63. See supra note 38.

33

Berkeley Business Law Journal

of cases. Where the court found that the funds were insufficient (12% ofcases), it pierced 76.5% of the time and refused to pierce 23.5% of the time.Where the court found that the funds were not insufficient (9.4% of cases), itpierced only 11.3% of the time and refused to pierce in 88.7% of cases.