Embed Size (px)

Citation preview

The Council of Community Colleges Page 1

COUNCIL OF COMMUNITY COLLEGES OF JAMAICA

ASSOCIATE DEGREE EXAMINATIONS

SUMMER – 2007 AUGUST

PROGRAMME: BUSINESS STUDIES HOSPITALITY AND TOURISM MANAGEMENT MANAGEMENT INFORMATION SYSTEM INFORMATION TECHNOLOGY LIBRARY TECHNICAL STUDIES

COURSE NAME AND FUNDAMENTALS OF ACCOUNTING CODE: (ACCT 1101) YEAR GROUP: ONE DATE: THURSDAY, AUGUST 16, 2007 TIME: 1: 00 – 4:00 P.M. DURATION: 3 HOURS EXAMINATION TYPE: FINAL

INSTRUCTIONS:

SECTION A: ANSWER ALL QUESTIONS IN THIS SECTION. SECTION B: ANSWER ANY TWO (2) QUESTIONS FROM THIS SECTION.

DO NOT TURN THIS PAGE UNTIL YOU ARE TOLD TO DO SO

ACCT 1101

The Council of Community Colleges of Jamaica Page 2

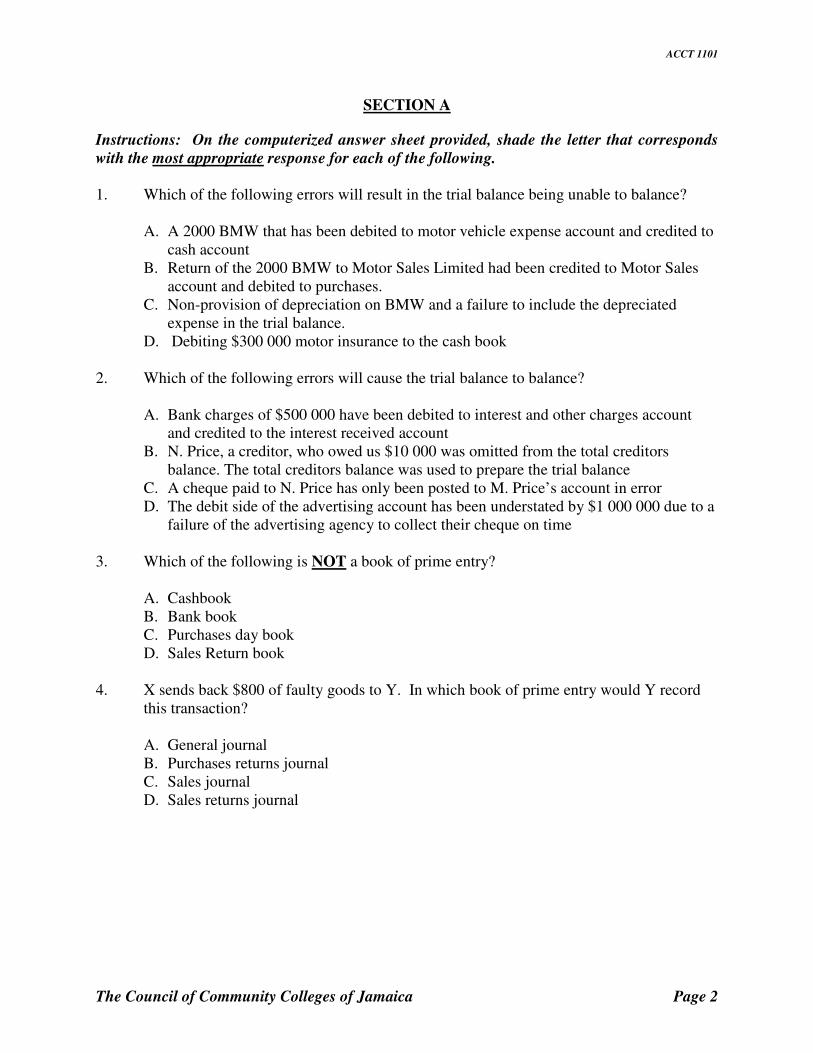

SECTION A

Instructions: On the computerized answer sheet provided, shade the letter that corresponds

with the most appropriate response for each of the following.

1. Which of the following errors will result in the trial balance being unable to balance?

A. A 2000 BMW that has been debited to motor vehicle expense account and credited to cash account

B. Return of the 2000 BMW to Motor Sales Limited had been credited to Motor Sales account and debited to purchases.

C. Non-provision of depreciation on BMW and a failure to include the depreciated expense in the trial balance.

D. Debiting $300 000 motor insurance to the cash book

2. Which of the following errors will cause the trial balance to balance?

A. Bank charges of $500 000 have been debited to interest and other charges account and credited to the interest received account

B. N. Price, a creditor, who owed us $10 000 was omitted from the total creditors balance. The total creditors balance was used to prepare the trial balance

C. A cheque paid to N. Price has only been posted to M. Price’s account in error D. The debit side of the advertising account has been understated by $1 000 000 due to a

failure of the advertising agency to collect their cheque on time 3. Which of the following is NOT a book of prime entry?

A. Cashbook B. Bank book C. Purchases day book D. Sales Return book

4. X sends back $800 of faulty goods to Y. In which book of prime entry would Y record

this transaction?

A. General journal B. Purchases returns journal C. Sales journal D. Sales returns journal

ACCT 1101

The Council of Community Colleges of Jamaica Page 3

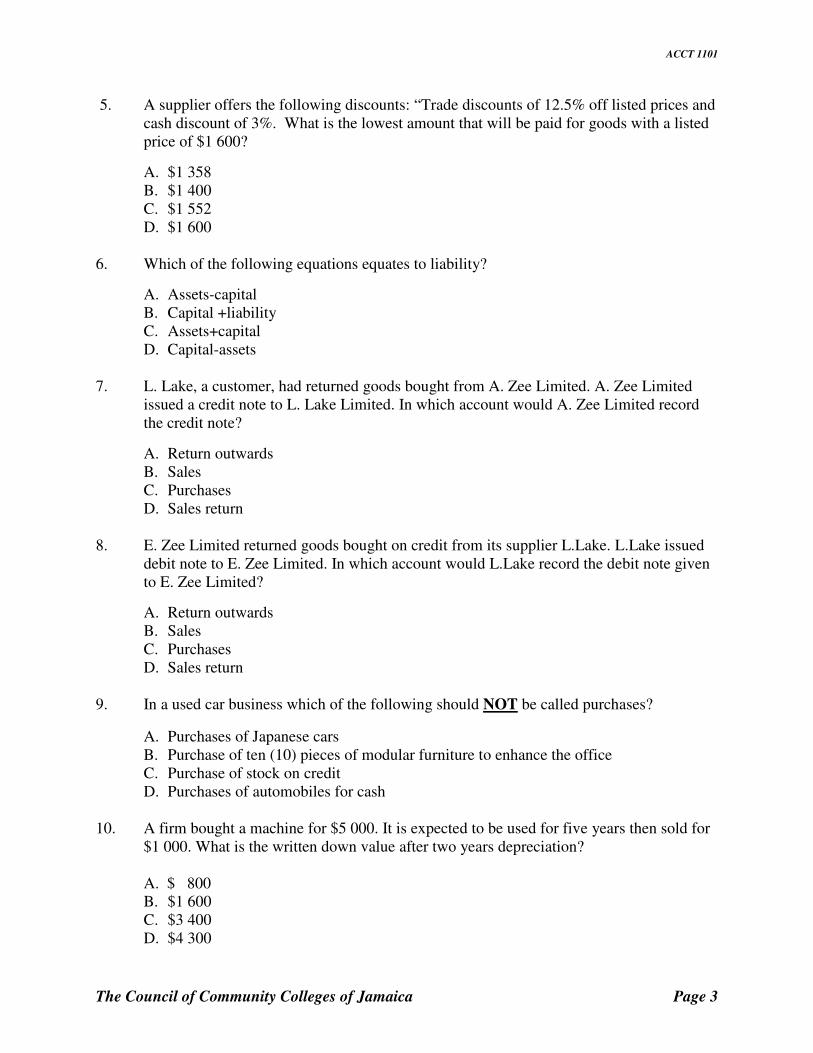

5. A supplier offers the following discounts: “Trade discounts of 12.5% off listed prices and cash discount of 3%. What is the lowest amount that will be paid for goods with a listed price of $1 600?

A. $1 358 B. $1 400 C. $1 552 D. $1 600

6. Which of the following equations equates to liability?

A. Assets-capital B. Capital +liability C. Assets+capital D. Capital-assets

7. L. Lake, a customer, had returned goods bought from A. Zee Limited. A. Zee Limited

issued a credit note to L. Lake Limited. In which account would A. Zee Limited record the credit note?

A. Return outwards B. Sales C. Purchases D. Sales return

8. E. Zee Limited returned goods bought on credit from its supplier L.Lake. L.Lake issued

debit note to E. Zee Limited. In which account would L.Lake record the debit note given to E. Zee Limited?

A. Return outwards B. Sales C. Purchases D. Sales return

9. In a used car business which of the following should NOT be called purchases?

A. Purchases of Japanese cars B. Purchase of ten (10) pieces of modular furniture to enhance the office C. Purchase of stock on credit D. Purchases of automobiles for cash

10. A firm bought a machine for $5 000. It is expected to be used for five years then sold for

$1 000. What is the written down value after two years depreciation?

A. $ 800 B. $1 600 C. $3 400 D. $4 300

ACCT 1101

The Council of Community Colleges of Jamaica Page 4

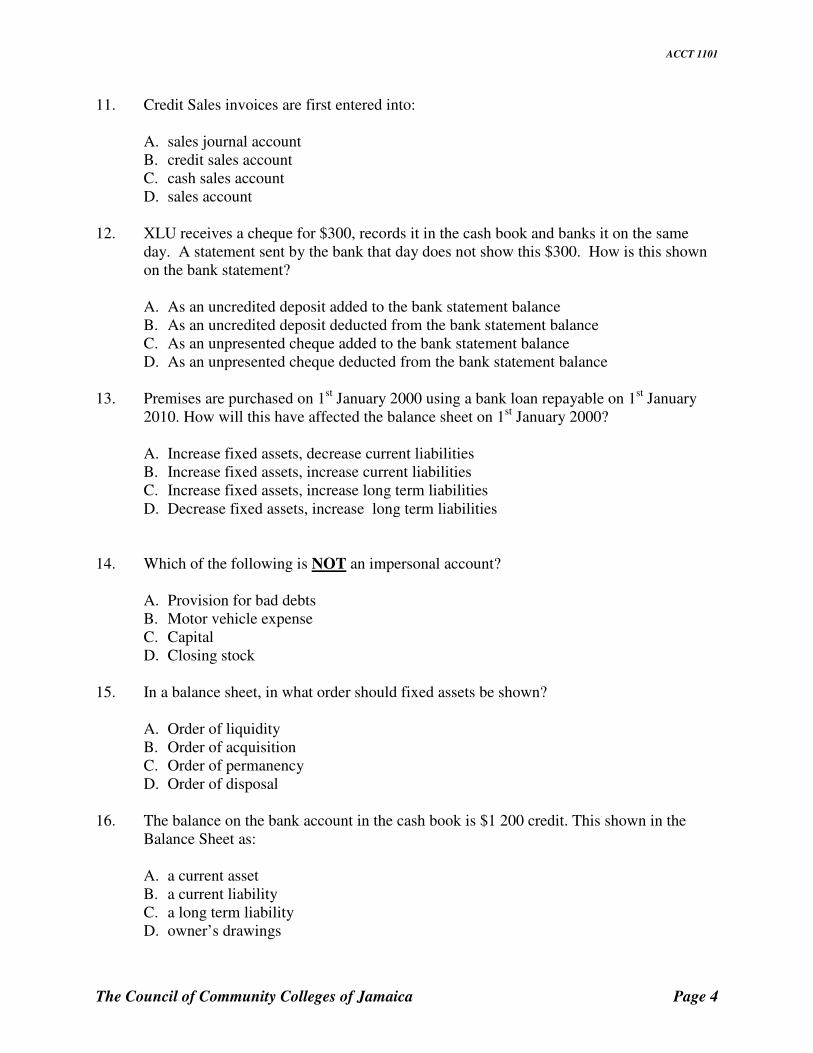

11. Credit Sales invoices are first entered into:

A. sales journal account B. credit sales account C. cash sales account D. sales account

12. XLU receives a cheque for $300, records it in the cash book and banks it on the same

day. A statement sent by the bank that day does not show this $300. How is this shown on the bank statement?

A. As an uncredited deposit added to the bank statement balance B. As an uncredited deposit deducted from the bank statement balance C. As an unpresented cheque added to the bank statement balance D. As an unpresented cheque deducted from the bank statement balance

13. Premises are purchased on 1st January 2000 using a bank loan repayable on 1st January 2010. How will this have affected the balance sheet on 1st January 2000?

A. Increase fixed assets, decrease current liabilities B. Increase fixed assets, increase current liabilities C. Increase fixed assets, increase long term liabilities D. Decrease fixed assets, increase long term liabilities

14. Which of the following is NOT an impersonal account?

A. Provision for bad debts B. Motor vehicle expense C. Capital D. Closing stock

15. In a balance sheet, in what order should fixed assets be shown?

A. Order of liquidity B. Order of acquisition C. Order of permanency D. Order of disposal

16. The balance on the bank account in the cash book is $1 200 credit. This shown in the

Balance Sheet as:

A. a current asset B. a current liability C. a long term liability D. owner’s drawings

ACCT 1101

The Council of Community Colleges of Jamaica Page 5

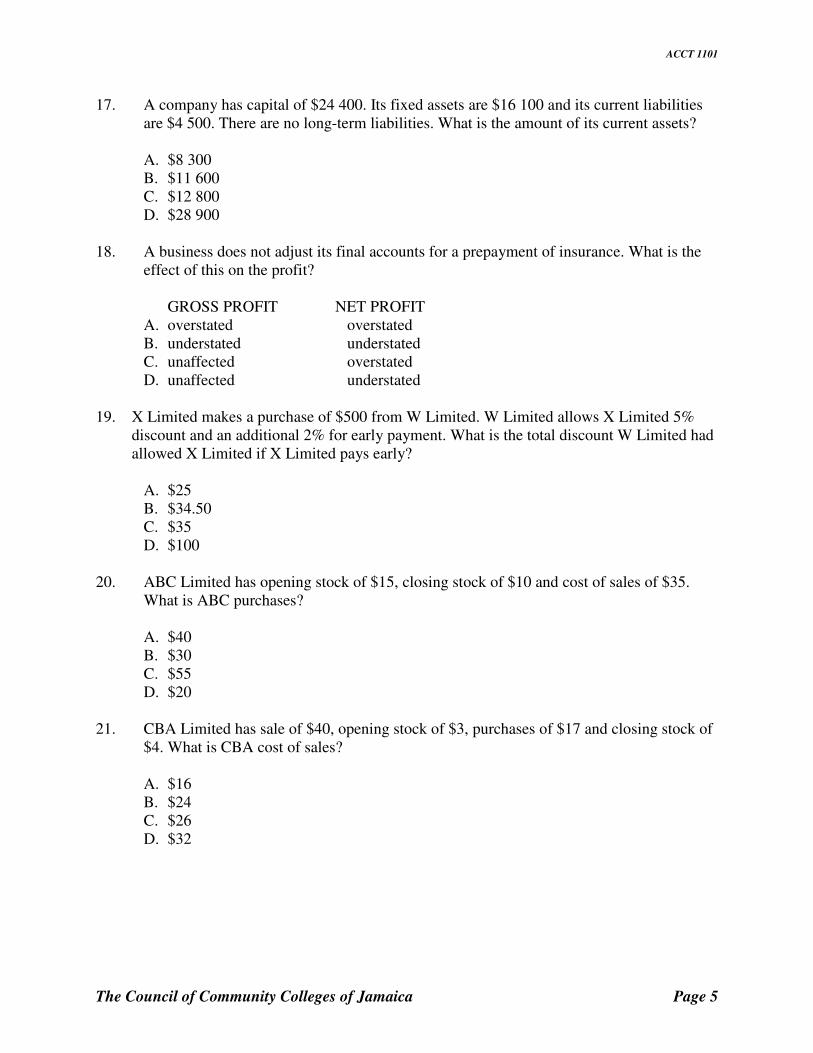

17. A company has capital of $24 400. Its fixed assets are $16 100 and its current liabilities are $4 500. There are no long-term liabilities. What is the amount of its current assets?

A. $8 300 B. $11 600 C. $12 800 D. $28 900

18. A business does not adjust its final accounts for a prepayment of insurance. What is the effect of this on the profit?

GROSS PROFIT NET PROFIT

A. overstated overstated B. understated understated C. unaffected overstated D. unaffected understated

19. X Limited makes a purchase of $500 from W Limited. W Limited allows X Limited 5%

discount and an additional 2% for early payment. What is the total discount W Limited had allowed X Limited if X Limited pays early?

A. $25 B. $34.50 C. $35 D. $100

20. ABC Limited has opening stock of $15, closing stock of $10 and cost of sales of $35.

What is ABC purchases?

A. $40 B. $30 C. $55 D. $20

21. CBA Limited has sale of $40, opening stock of $3, purchases of $17 and closing stock of $4. What is CBA cost of sales?

A. $16 B. $24 C. $26 D. $32

ACCT 1101

The Council of Community Colleges of Jamaica Page 6

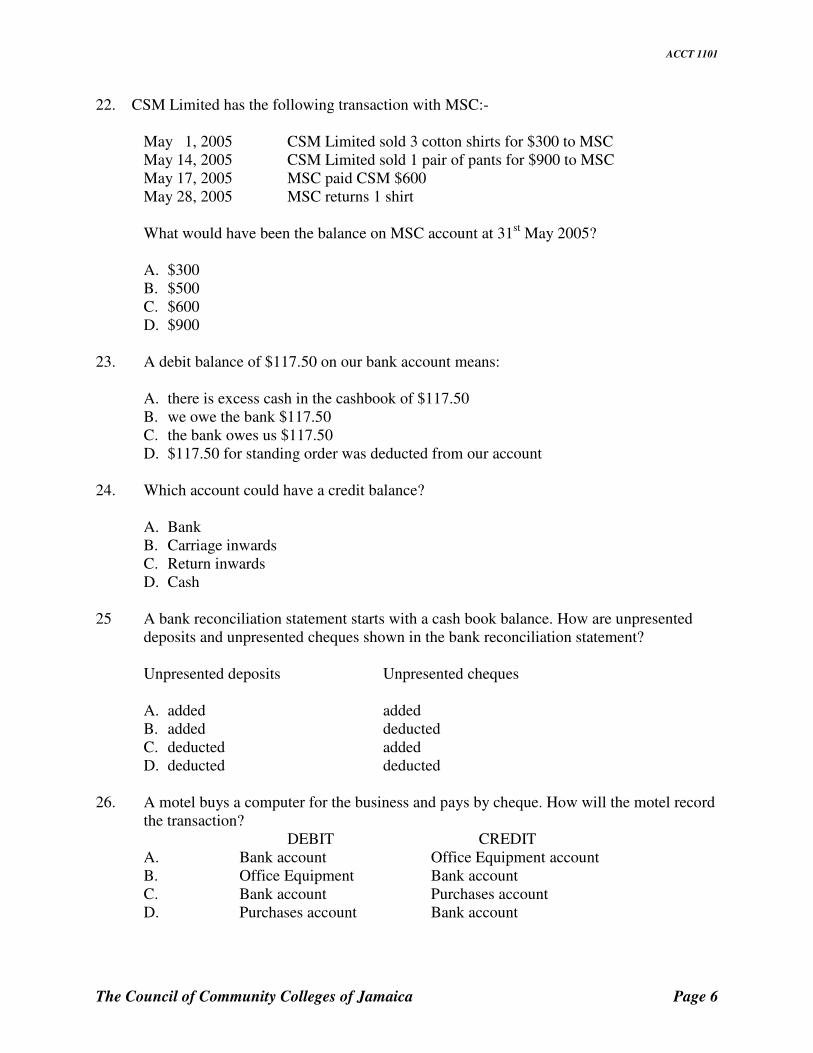

22. CSM Limited has the following transaction with MSC:-

May 1, 2005 CSM Limited sold 3 cotton shirts for $300 to MSC May 14, 2005 CSM Limited sold 1 pair of pants for $900 to MSC May 17, 2005 MSC paid CSM $600 May 28, 2005 MSC returns 1 shirt

What would have been the balance on MSC account at 31st May 2005?

A. $300 B. $500 C. $600 D. $900

23. A debit balance of $117.50 on our bank account means:

A. there is excess cash in the cashbook of $117.50 B. we owe the bank $117.50 C. the bank owes us $117.50 D. $117.50 for standing order was deducted from our account

24. Which account could have a credit balance?

A. Bank B. Carriage inwards C. Return inwards D. Cash

25 A bank reconciliation statement starts with a cash book balance. How are unpresented

deposits and unpresented cheques shown in the bank reconciliation statement?

Unpresented deposits Unpresented cheques

A. added added B. added deducted C. deducted added D. deducted deducted

26. A motel buys a computer for the business and pays by cheque. How will the motel record

the transaction? DEBIT CREDIT

A. Bank account Office Equipment account B. Office Equipment Bank account C. Bank account Purchases account D. Purchases account Bank account

ACCT 1101

The Council of Community Colleges of Jamaica Page 7

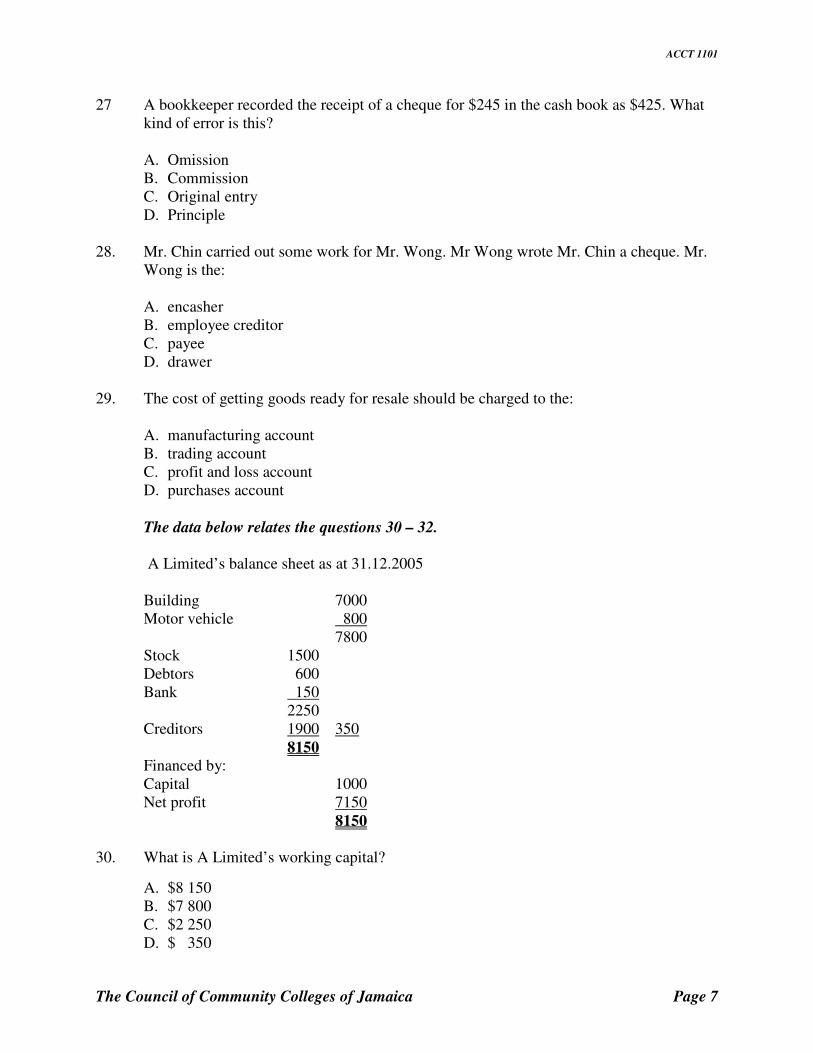

27 A bookkeeper recorded the receipt of a cheque for $245 in the cash book as $425. What kind of error is this?

A. Omission B. Commission C. Original entry D. Principle

28. Mr. Chin carried out some work for Mr. Wong. Mr Wong wrote Mr. Chin a cheque. Mr.

Wong is the:

A. encasher B. employee creditor C. payee D. drawer

29. The cost of getting goods ready for resale should be charged to the:

A. manufacturing account B. trading account C. profit and loss account D. purchases account

The data below relates the questions 30 – 32. A Limited’s balance sheet as at 31.12.2005

Building 7000 Motor vehicle 800

7800 Stock 1500 Debtors 600 Bank 150

2250 Creditors 1900 350

8150 Financed by: Capital 1000 Net profit 7150

8150 30. What is A Limited’s working capital?

A. $8 150 B. $7 800 C. $2 250 D. $ 350

ACCT 1101

The Council of Community Colleges of Jamaica Page 8

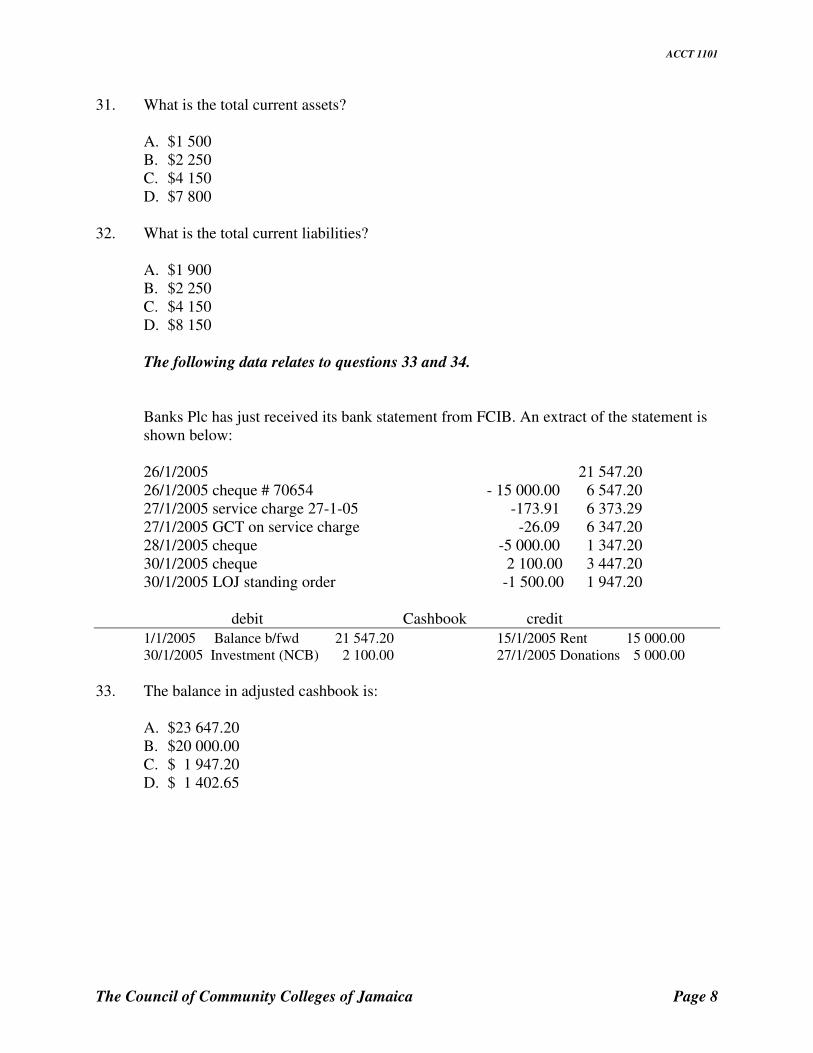

31. What is the total current assets?

A. $1 500 B. $2 250 C. $4 150 D. $7 800

32. What is the total current liabilities?

A. $1 900 B. $2 250 C. $4 150 D. $8 150

The following data relates to questions 33 and 34. Banks Plc has just received its bank statement from FCIB. An extract of the statement is

shown below:

26/1/2005 21 547.20 26/1/2005 cheque # 70654 - 15 000.00 6 547.20 27/1/2005 service charge 27-1-05 -173.91 6 373.29 27/1/2005 GCT on service charge -26.09 6 347.20 28/1/2005 cheque -5 000.00 1 347.20 30/1/2005 cheque 2 100.00 3 447.20 30/1/2005 LOJ standing order -1 500.00 1 947.20

debit Cashbook credit

1/1/2005 Balance b/fwd 21 547.20 15/1/2005 Rent 15 000.00 30/1/2005 Investment (NCB) 2 100.00 27/1/2005 Donations 5 000.00

33. The balance in adjusted cashbook is:

A. $23 647.20 B. $20 000.00 C. $ 1 947.20 D. $ 1 402.65

ACCT 1101

The Council of Community Colleges of Jamaica Page 9

34. Which one of the following must Banks plc use to reconcile the cashbook to the bank balance?

i. GCT charges ii. Investment

iii. LOJ standing order iv. Service charges

A. ii, iii and iv only B. i, ii and iv only C. i, ii and iii only D. i, iii and iv only

35. Which of the following is NOT a valid reason for preparing a bank statement?

A. For control purposes B. To update bank and cash balance C. To ensure that mistakes made by the bank is detected D. To ensure that mistakes have not been made by the firm’s cashier

36. Which of the following entries is INCORRECT?

37. The owner of a business takes goods costing $6 000 from his shop for his own use. What

are the entries necessary for this? DEBIT CREDIT

A Drawings account Purchases account B. Drawings account Stock account C. Purchases account Drawings account D. Stock account Drawings account

38. If bad debts were recovered from J Rowland, what would be the entries?

i. Credit sales account ii. Debit bank account iii. Credit J Rowland account iv. Credit bad debit recovered account

A. i and ii B. ii and iv C. iii and iv D. i and iv

Description Account to be debited Account to be credited

A. Bought motor vehicle on credit for resale

Purchases Trade Creditors

B. Acquired bank loan Bank Loan

C. Paid bank interest by standing order Bank Interest charges

D. Introduced cash into the business Cash Capital

ACCT 1101

The Council of Community Colleges of Jamaica Page 10

39. Depreciation is most accurately defined as the:

A. reduction in the value of an asset over a period of time B. wear and tear associated with an asset over a period of time C. difference between the cost of an asset and its sale or crap proceeds on disposal D. amortisation of an asset over its useful life

40. Willy Nelly, a sole trader, takes $12 000 cash and goods valued at $15 000 for the year. How would we account for these transactions?

A. Debit drawings and credit cash B. Credit cash and debit purchases C. Credit cash and purchases and debit drawings D. Credit capital and debit drawings

41. In order to increase existing provision for doubtful debts:

i. DR. profit and loss ii. CR. provision iii. DR. bad debts iv. CR. debtor’s account

A. i and ii B. ii and iii C. iv and i D. i and iii

42. XYZ has annual credit sales and debtors receipts of $100 000 and $70 000 respectively.

XYZ policy is to make provision for 1% of debtors at its year-end. What is XYZ debtors balance as at the year-end?

A. $20 000 B. $29 300 C. $29 700 D. $30 000

43. At the end of the year it was discovered that the Purchases Returns account had been

undercasted by $160. A Suspense account had been opened. Which entries are required to correct this error?

A. Credit purchases account $160, debit purchases return $160 B. Credit suspense account $160, debit purchases return account $160 C. Debit purchases account $160, credit purchases return account $160 D. Debit suspense account $160, credit purchases return account $160

ACCT 1101

The Council of Community Colleges of Jamaica Page 11

44. Realisation concept states that profit is earned at the time when goods or services which are the subject of sale:

A. are sold or actually converted to money B. have made the transition from seller to customer C. have been replaced by cash or debtor D. have been accepted by the customer and replaced by cash

45. Which of the following statements most accurately explains the going concern concept?

A. It requires us to account for all the business assets and liabilities at the going market

price B. It requires that the business accounts be prepared on the assumption of going market

price for the accounts to be correct C. It requires that the business accounts be prepared on the assumption that the business

will continue in the future D. It requires the business accounts be prepared on the assumption that the assets and

liabilities will be disposed of in the near future 46. Which of the following is NOT a real account?

A. Stock B. Inventories C. Fixtures D. Trade creditors

47. If at 1.1.2005 accumulated provision for doubtful debts is $60 000, provision for bad

debts during the year is $3 000, debtors at 31.12.2005 is $180 000 and the company policy is to provide for provision for doubtful debts using 5% of debtors at year-end, compute the provision for doubtful debts.

A. $3 000 B. $9 000 C. $6 000 D. $12 000

ACCT 1101

The Council of Community Colleges of Jamaica Page 12

48. Which of the following flowcharts most accurately portrays the basic structure of bookkeeping entries?

A. Cash B. Sales Invoices C. Debit and Credit notes D. Purchases invoices

Cash deposit Sales ledger Real and Nominal accounts Purchases Invoices Cashbook Trial Balance Trial Balance Trial Balance Trial balance Profit and Loss Trading, Profit and Loss Profit and Loss Balance sheet Balance sheet Balance sheet Balance sheet

49. In 2000 a business paid $3 000 for electricity. On January 1, 2000, $600 was owed for electricity and on December 31, 2000, $1 300 was owed for electricity. How much is charged for electricity in the Profit and Loss account for 2000?

A. $3 000 B. $3 600 C. $3 700 D. $4 300

50. If the petty cash float is $10 000 and the balance at the end of the month is $1 254, how

much money was spent?

A. $10 000 B. $1 254 C. $8 746 D. $11 254

(Total 50 marks)

ACCT 1101

The Council of Community Colleges of Jamaica Page 13

SECTION B

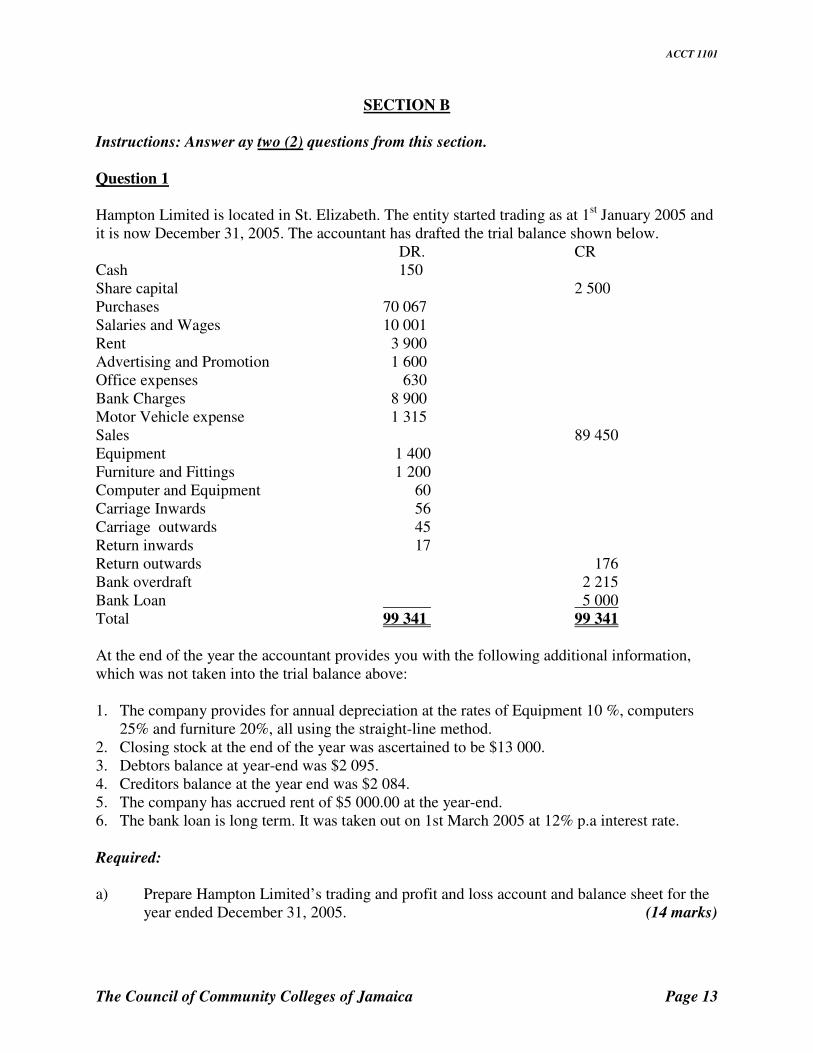

Instructions: Answer ay two (2) questions from this section. Question 1 Hampton Limited is located in St. Elizabeth. The entity started trading as at 1st January 2005 and it is now December 31, 2005. The accountant has drafted the trial balance shown below. DR. CR Cash 150 Share capital 2 500 Purchases 70 067 Salaries and Wages 10 001 Rent 3 900 Advertising and Promotion 1 600 Office expenses 630 Bank Charges 8 900 Motor Vehicle expense 1 315 Sales 89 450 Equipment 1 400 Furniture and Fittings 1 200 Computer and Equipment 60 Carriage Inwards 56 Carriage outwards 45 Return inwards 17 Return outwards 176 Bank overdraft 2 215 Bank Loan 5 000 Total 99 341 99 341

At the end of the year the accountant provides you with the following additional information, which was not taken into the trial balance above: 1. The company provides for annual depreciation at the rates of Equipment 10 %, computers

25% and furniture 20%, all using the straight-line method. 2. Closing stock at the end of the year was ascertained to be $13 000. 3. Debtors balance at year-end was $2 095. 4. Creditors balance at the year end was $2 084. 5. The company has accrued rent of $5 000.00 at the year-end. 6. The bank loan is long term. It was taken out on 1st March 2005 at 12% p.a interest rate.

Required:

a) Prepare Hampton Limited’s trading and profit and loss account and balance sheet for the

year ended December 31, 2005. (14 marks)

ACCT 1101

The Council of Community Colleges of Jamaica Page 14

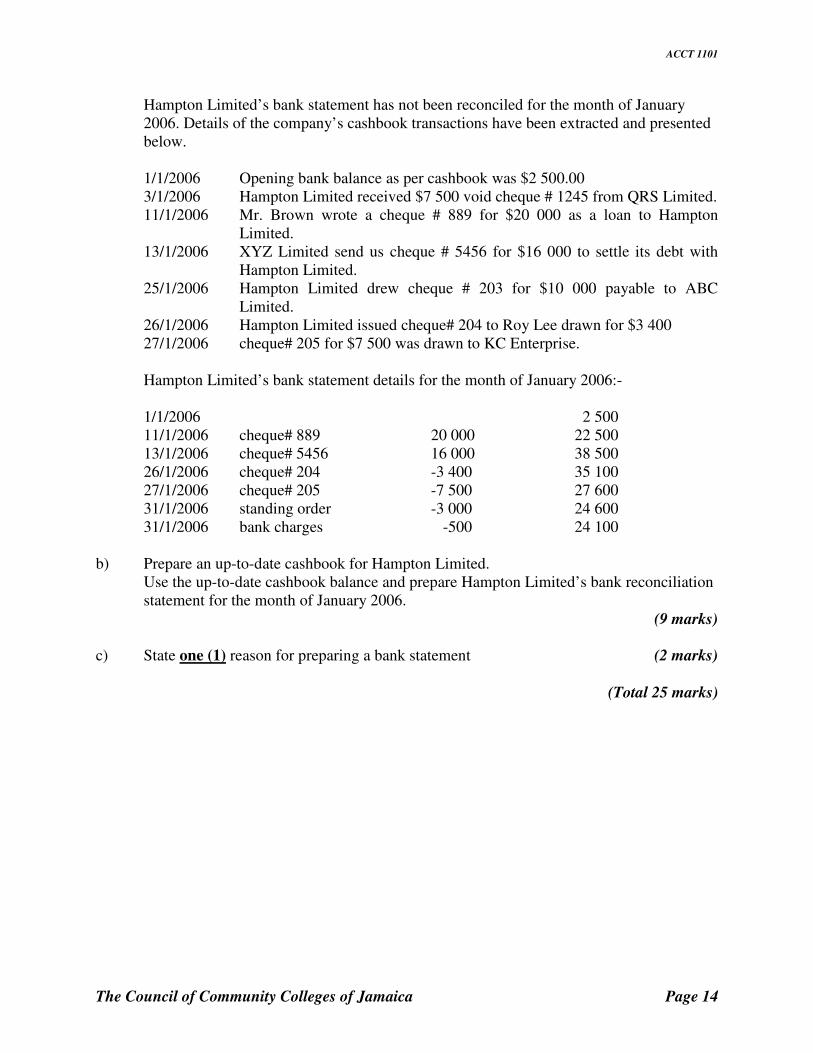

Hampton Limited’s bank statement has not been reconciled for the month of January 2006. Details of the company’s cashbook transactions have been extracted and presented below. 1/1/2006 Opening bank balance as per cashbook was $2 500.00 3/1/2006 Hampton Limited received $7 500 void cheque # 1245 from QRS Limited. 11/1/2006 Mr. Brown wrote a cheque # 889 for $20 000 as a loan to Hampton

Limited. 13/1/2006 XYZ Limited send us cheque # 5456 for $16 000 to settle its debt with

Hampton Limited. 25/1/2006 Hampton Limited drew cheque # 203 for $10 000 payable to ABC

Limited. 26/1/2006 Hampton Limited issued cheque# 204 to Roy Lee drawn for $3 400 27/1/2006 cheque# 205 for $7 500 was drawn to KC Enterprise. Hampton Limited’s bank statement details for the month of January 2006:- 1/1/2006 2 500 11/1/2006 cheque# 889 20 000 22 500 13/1/2006 cheque# 5456 16 000 38 500 26/1/2006 cheque# 204 -3 400 35 100 27/1/2006 cheque# 205 -7 500 27 600 31/1/2006 standing order -3 000 24 600 31/1/2006 bank charges -500 24 100

b) Prepare an up-to-date cashbook for Hampton Limited.

Use the up-to-date cashbook balance and prepare Hampton Limited’s bank reconciliation statement for the month of January 2006.

(9 marks)

c) State one (1) reason for preparing a bank statement (2 marks)

(Total 25 marks)

ACCT 1101

The Council of Community Colleges of Jamaica Page 15

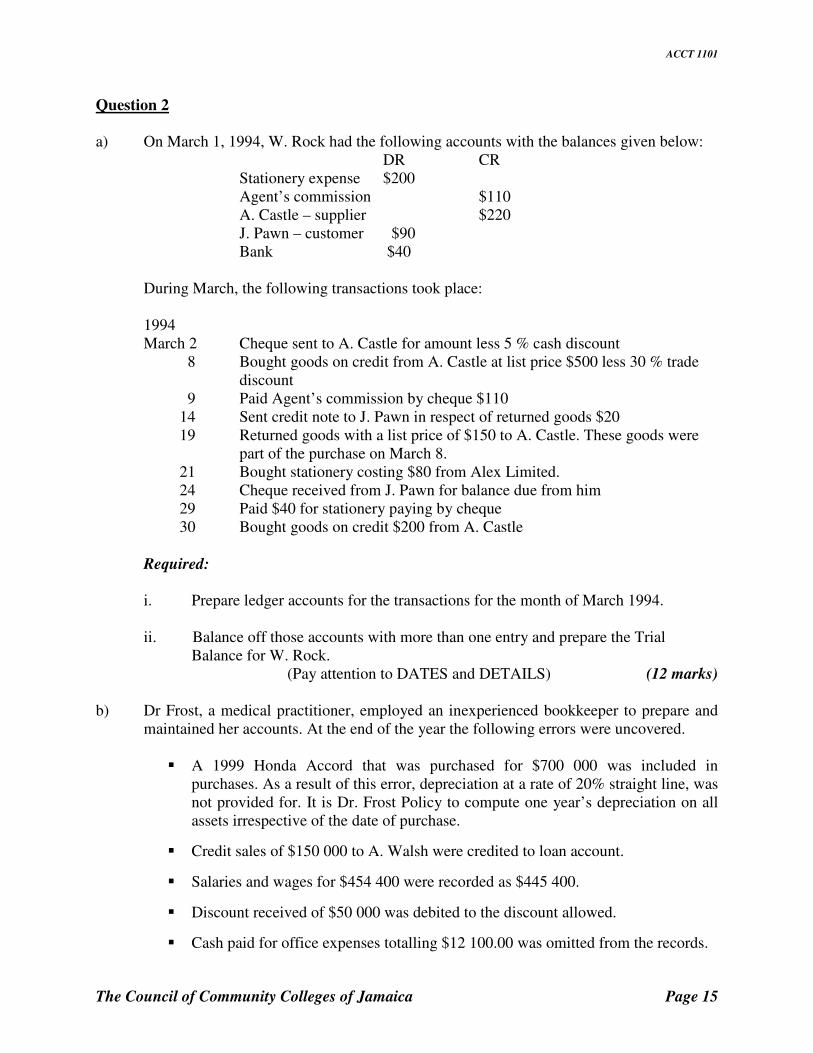

Question 2 a) On March 1, 1994, W. Rock had the following accounts with the balances given below: DR CR Stationery expense $200 Agent’s commission $110 A. Castle – supplier $220 J. Pawn – customer $90 Bank $40 During March, the following transactions took place:

1994 March 2 Cheque sent to A. Castle for amount less 5 % cash discount 8 Bought goods on credit from A. Castle at list price $500 less 30 % trade discount 9 Paid Agent’s commission by cheque $110 14 Sent credit note to J. Pawn in respect of returned goods $20 19 Returned goods with a list price of $150 to A. Castle. These goods were part of the purchase on March 8. 21 Bought stationery costing $80 from Alex Limited. 24 Cheque received from J. Pawn for balance due from him 29 Paid $40 for stationery paying by cheque 30 Bought goods on credit $200 from A. Castle

Required:

i. Prepare ledger accounts for the transactions for the month of March 1994. ii. Balance off those accounts with more than one entry and prepare the Trial Balance for W. Rock. (Pay attention to DATES and DETAILS) (12 marks)

b) Dr Frost, a medical practitioner, employed an inexperienced bookkeeper to prepare and maintained her accounts. At the end of the year the following errors were uncovered.

� A 1999 Honda Accord that was purchased for $700 000 was included in

purchases. As a result of this error, depreciation at a rate of 20% straight line, was not provided for. It is Dr. Frost Policy to compute one year’s depreciation on all assets irrespective of the date of purchase.

� Credit sales of $150 000 to A. Walsh were credited to loan account.

� Salaries and wages for $454 400 were recorded as $445 400.

� Discount received of $50 000 was debited to the discount allowed.

� Cash paid for office expenses totalling $12 100.00 was omitted from the records.

ACCT 1101

The Council of Community Colleges of Jamaica Page 16

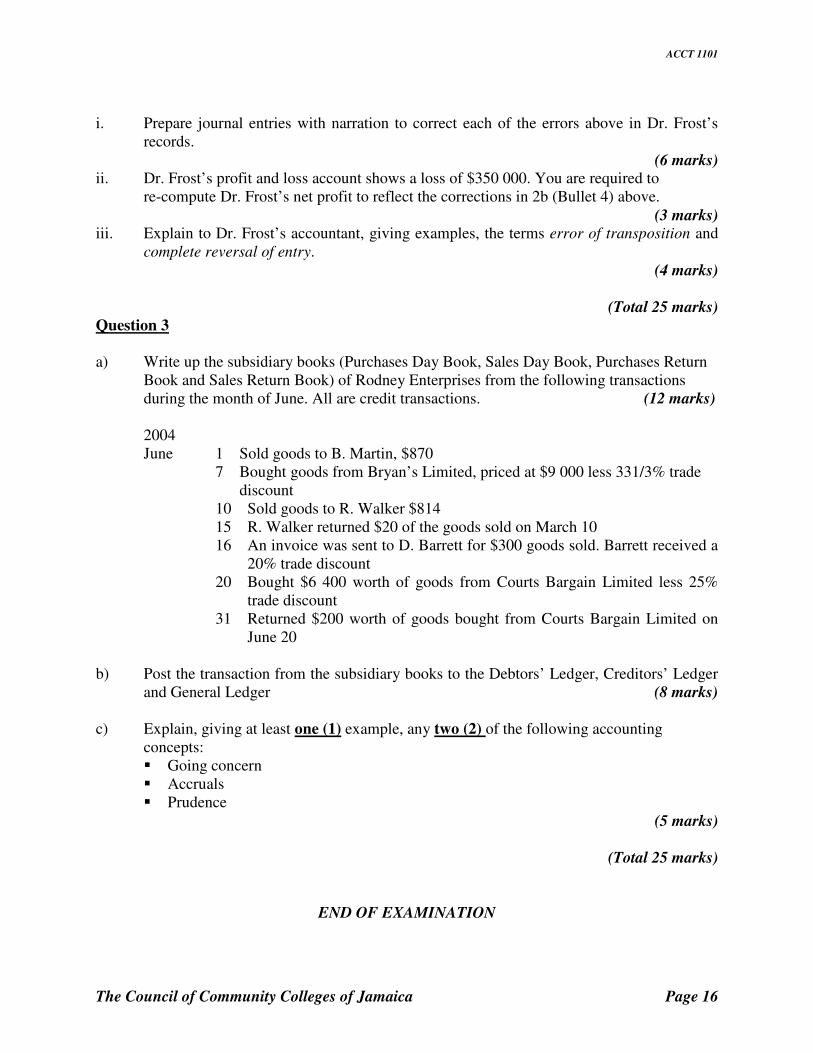

i. Prepare journal entries with narration to correct each of the errors above in Dr. Frost’s

records. (6 marks)

ii. Dr. Frost’s profit and loss account shows a loss of $350 000. You are required to re-compute Dr. Frost’s net profit to reflect the corrections in 2b (Bullet 4) above.

(3 marks) iii. Explain to Dr. Frost’s accountant, giving examples, the terms error of transposition and

complete reversal of entry. (4 marks)

(Total 25 marks)

Question 3 a) Write up the subsidiary books (Purchases Day Book, Sales Day Book, Purchases Return

Book and Sales Return Book) of Rodney Enterprises from the following transactions during the month of June. All are credit transactions. (12 marks)

2004 June 1 Sold goods to B. Martin, $870

7 Bought goods from Bryan’s Limited, priced at $9 000 less 331/3% trade discount

10 Sold goods to R. Walker $814 15 R. Walker returned $20 of the goods sold on March 10 16 An invoice was sent to D. Barrett for $300 goods sold. Barrett received a

20% trade discount 20 Bought $6 400 worth of goods from Courts Bargain Limited less 25%

trade discount 31 Returned $200 worth of goods bought from Courts Bargain Limited on

June 20 b) Post the transaction from the subsidiary books to the Debtors’ Ledger, Creditors’ Ledger

and General Ledger (8 marks) c) Explain, giving at least one (1) example, any two (2) of the following accounting

concepts: � Going concern � Accruals � Prudence

(5 marks)

(Total 25 marks)

END OF EXAMINATION

ACCT 1101

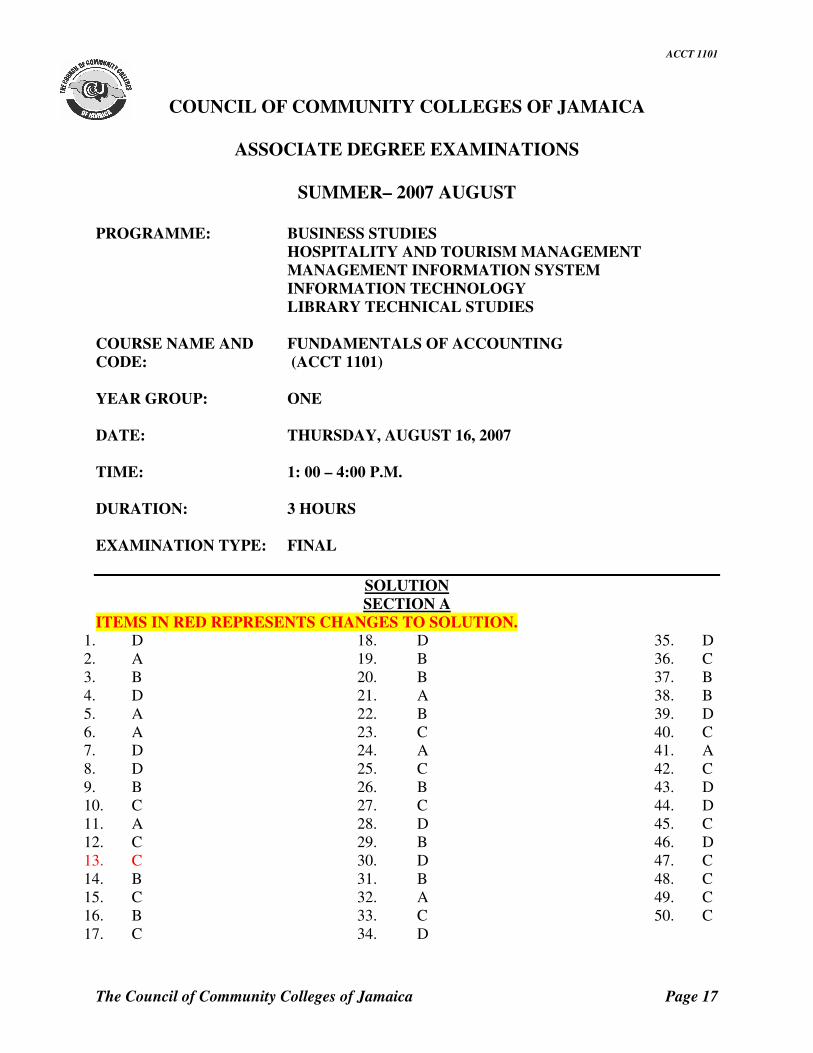

The Council of Community Colleges of Jamaica Page 17

COUNCIL OF COMMUNITY COLLEGES OF JAMAICA

ASSOCIATE DEGREE EXAMINATIONS

SUMMER– 2007 AUGUST

PROGRAMME: BUSINESS STUDIES HOSPITALITY AND TOURISM MANAGEMENT MANAGEMENT INFORMATION SYSTEM INFORMATION TECHNOLOGY LIBRARY TECHNICAL STUDIES

COURSE NAME AND FUNDAMENTALS OF ACCOUNTING CODE: (ACCT 1101) YEAR GROUP: ONE DATE: THURSDAY, AUGUST 16, 2007 TIME: 1: 00 – 4:00 P.M. DURATION: 3 HOURS EXAMINATION TYPE: FINAL

SOLUTION SECTION A

ITEMS IN RED REPRESENTS CHANGES TO SOLUTION.1. D 2. A 3. B 4. D 5. A 6. A 7. D 8. D 9. B 10. C 11. A 12. C 13. C 14. B 15. C 16. B 17. C

18. D 19. B 20. B 21. A 22. B 23. C 24. A 25. C 26. B 27. C 28. D 29. B 30. D 31. B 32. A 33. C 34. D

35. D 36. C 37. B 38. B 39. D 40. C 41. A 42. C 43. D 44. D 45. C 46. D 47. C 48. C 49. C 50. C

The Council of Community Colleges Page 18

(50 marks)

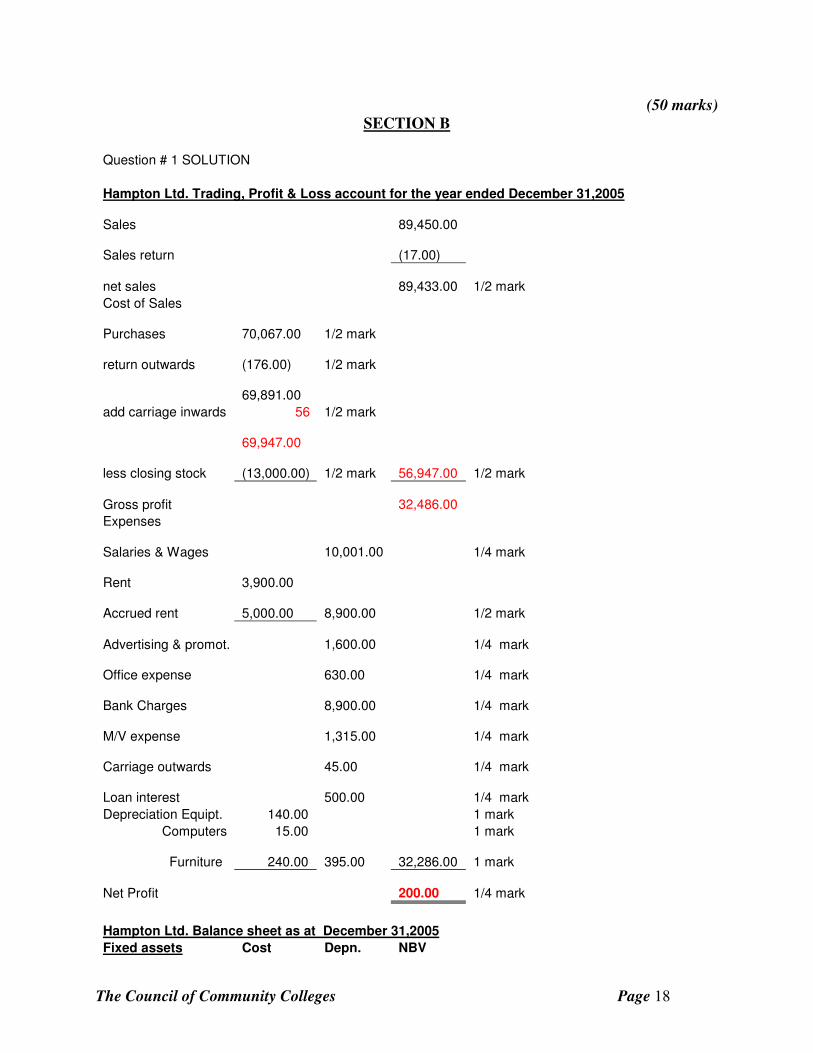

SECTION B Question # 1 SOLUTION

Hampton Ltd. Trading, Profit & Loss account for the year ended December 31,2005

Sales 89,450.00

Sales return (17.00)

net sales 89,433.00 1/2 mark

Cost of Sales

Purchases 70,067.00 1/2 mark

return outwards (176.00) 1/2 mark

69,891.00

add carriage inwards 56 1/2 mark

69,947.00

less closing stock (13,000.00) 1/2 mark

56,947.00 1/2 mark

Gross profit 32,486.00

Expenses

Salaries & Wages 10,001.00 1/4 mark

Rent 3,900.00

Accrued rent 5,000.00

8,900.00 1/2 mark

Advertising & promot. 1,600.00 1/4 mark

Office expense 630.00 1/4 mark

Bank Charges 8,900.00 1/4 mark

M/V expense 1,315.00 1/4 mark

Carriage outwards 45.00 1/4 mark

Loan interest 500.00 1/4 mark

Depreciation Equipt. 140.00 1 mark

Computers 15.00 1 mark

Furniture 240.00 395.00

32,286.00 1 mark

Net Profit 200.00 1/4 mark

Hampton Ltd. Balance sheet as at December 31,2005

Fixed assets Cost Depn. NBV

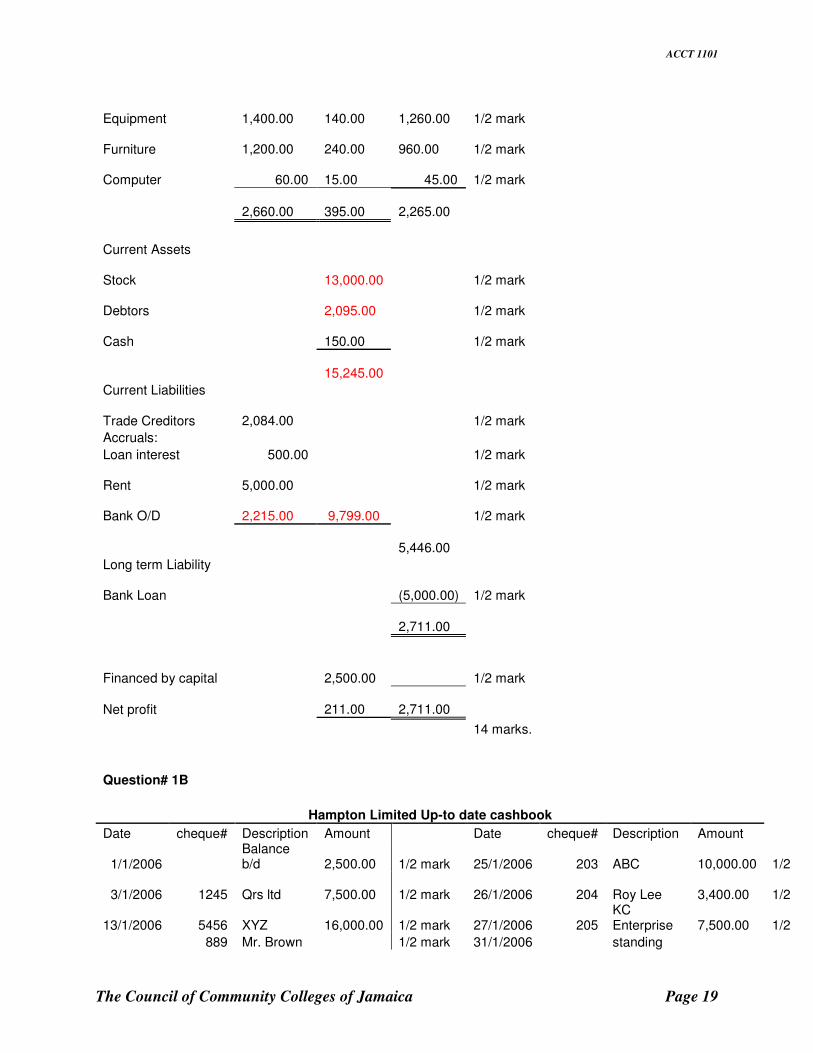

ACCT 1101

The Council of Community Colleges of Jamaica Page 19

Equipment 1,400.00

140.00

1,260.00 1/2 mark

Furniture 1,200.00

240.00

960.00 1/2 mark

Computer 60.00 15.00 45.00 1/2 mark

2,660.00

395.00

2,265.00

Current Assets

Stock 13,000.00 1/2 mark

Debtors 2,095.00 1/2 mark

Cash 150.00 1/2 mark

15,245.00

Current Liabilities

Trade Creditors 2,084.00 1/2 mark

Accruals:

Loan interest 500.00 1/2 mark

Rent 5,000.00 1/2 mark

Bank O/D 2,215.00 9,799.00 1/2 mark

5,446.00

Long term Liability

Bank Loan (5,000.00) 1/2 mark

2,711.00

Financed by capital 2,500.00 1/2 mark

Net profit 211.00

2,711.00

14 marks.

Question# 1B

Hampton Limited Up-to date cashbook

Date cheque# Description Amount Date cheque# Description Amount

1/1/2006 Balance b/d

2,500.00 1/2 mark 25/1/2006 203 ABC

10,000.00

1/2

3/1/2006 1245 Qrs ltd 7,500.00 1/2 mark 26/1/2006 204 Roy Lee

3,400.00

1/2

13/1/2006 5456 XYZ 16,000.00 1/2 mark 27/1/2006 205

KC Enterprise

7,500.00

1/2

889 Mr. Brown 1/2 mark 31/1/2006 standing

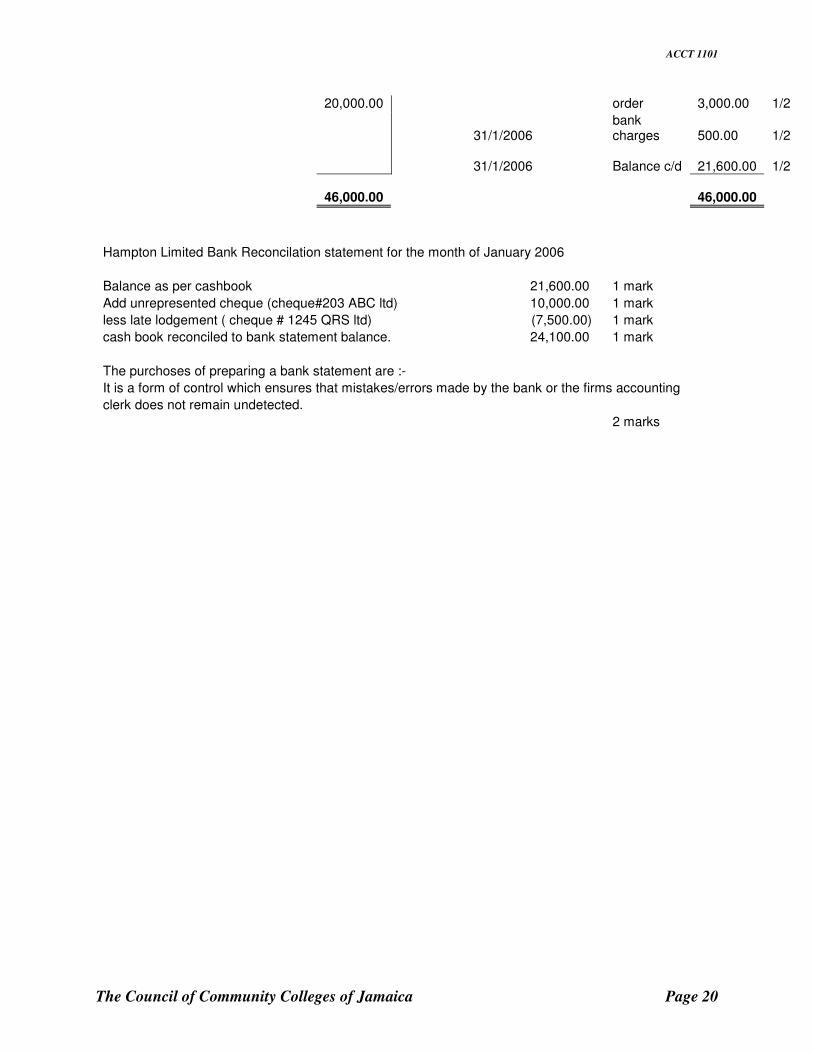

ACCT 1101

The Council of Community Colleges of Jamaica Page 20

20,000.00 order 3,000.00 1/2

31/1/2006 bank charges

500.00

1/2

31/1/2006 Balance c/d 21,600.00

1/2

46,000.00

46,000.00

Hampton Limited Bank Reconcilation statement for the month of January 2006

Balance as per cashbook 21,600.00 1 mark

Add unrepresented cheque (cheque#203 ABC ltd) 10,000.00 1 mark

less late lodgement ( cheque # 1245 QRS ltd) (7,500.00) 1 mark

cash book reconciled to bank statement balance. 24,100.00 1 mark

The purchoses of preparing a bank statement are :-

It is a form of control which ensures that mistakes/errors made by the bank or the firms accounting

clerk does not remain undetected.

2 marks

ACCT 1101

The Council of Community Colleges of Jamaica Page 21

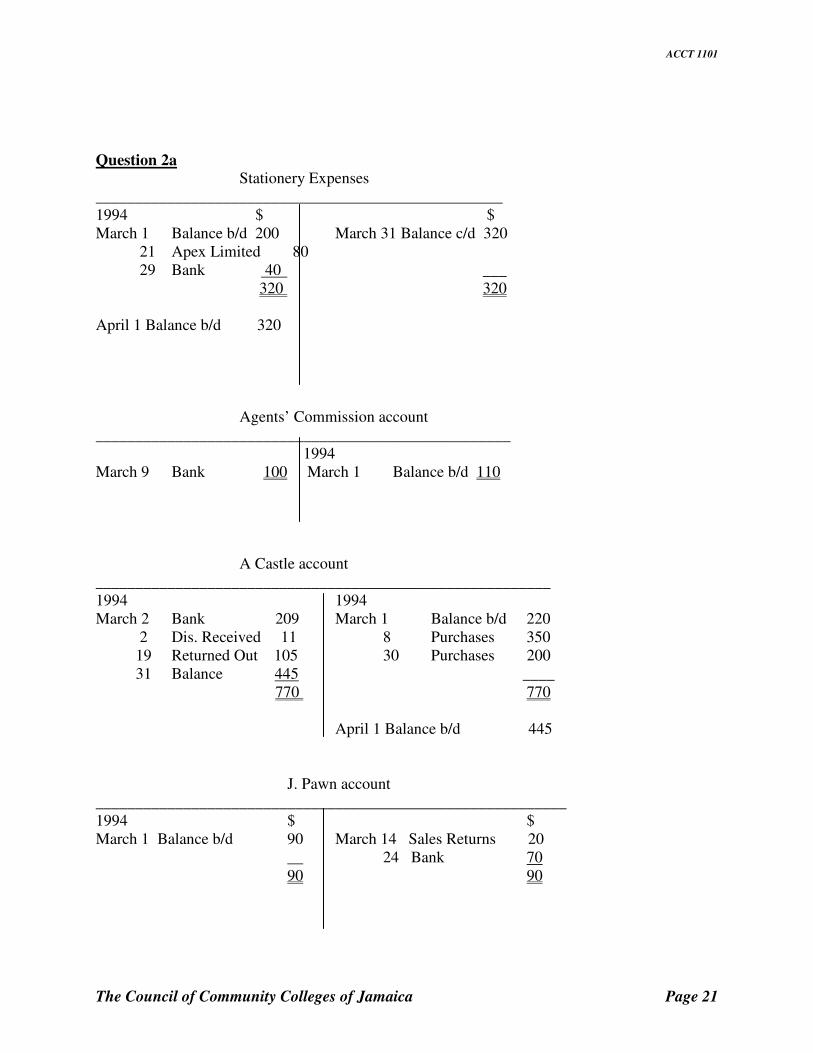

Question 2a Stationery Expenses ___________________________________________________ 1994 $ $ March 1 Balance b/d 200 March 31 Balance c/d 320 21 Apex Limited 80 29 Bank 40 ___ 320 320 April 1 Balance b/d 320 Agents’ Commission account ____________________________________________________ 1994 March 9 Bank 100 March 1 Balance b/d 110 A Castle account _________________________________________________________ 1994 1994 March 2 Bank 209 March 1 Balance b/d 220 2 Dis. Received 11 8 Purchases 350 19 Returned Out 105 30 Purchases 200 31 Balance 445 ____ 770 770 April 1 Balance b/d 445 J. Pawn account ___________________________________________________________ 1994 $ $ March 1 Balance b/d 90 March 14 Sales Returns 20 __ 24 Bank 70 90 90

ACCT 1101

The Council of Community Colleges of Jamaica Page 22

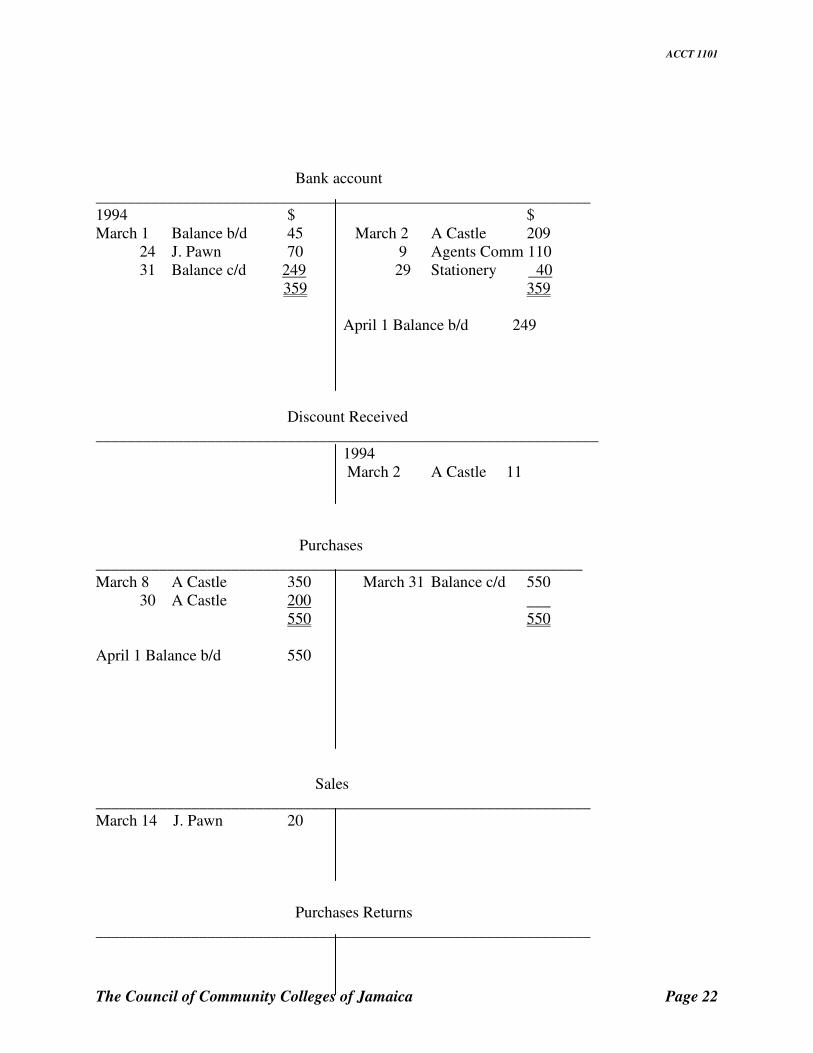

Bank account ______________________________________________________________ 1994 $ $ March 1 Balance b/d 45 March 2 A Castle 209 24 J. Pawn 70 9 Agents Comm 110 31 Balance c/d 249 29 Stationery 40 359 359 April 1 Balance b/d 249 Discount Received _______________________________________________________________ 1994 March 2 A Castle 11 Purchases _____________________________________________________________ March 8 A Castle 350 March 31 Balance c/d 550 30 A Castle 200 ___ 550 550 April 1 Balance b/d 550 Sales ______________________________________________________________ March 14 J. Pawn 20

Purchases Returns ______________________________________________________________

ACCT 1101

The Council of Community Colleges of Jamaica Page 23

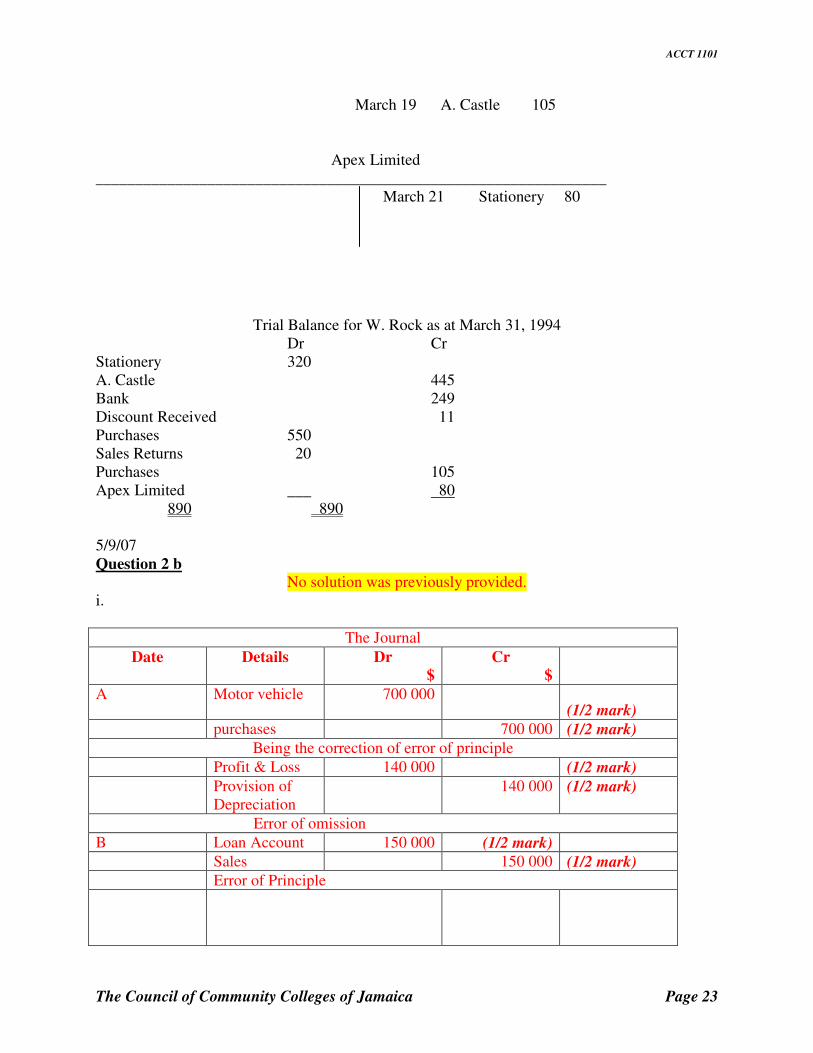

March 19 A. Castle 105 Apex Limited ________________________________________________________________ March 21 Stationery 80

Trial Balance for W. Rock as at March 31, 1994 Dr Cr Stationery 320 A. Castle 445 Bank 249 Discount Received 11 Purchases 550 Sales Returns 20 Purchases 105 Apex Limited ___ 80

890 890 5/9/07 Question 2 b

No solution was previously provided. i.

The Journal

Date Details Dr $

Cr $

A Motor vehicle 700 000 (1/2 mark)

purchases 700 000 (1/2 mark) Being the correction of error of principle

Profit & Loss 140 000 (1/2 mark) Provision of

Depreciation 140 000 (1/2 mark)

Error of omission

B Loan Account 150 000 (1/2 mark)

Sales 150 000 (1/2 mark) Error of Principle

ACCT 1101

The Council of Community Colleges of Jamaica Page 24

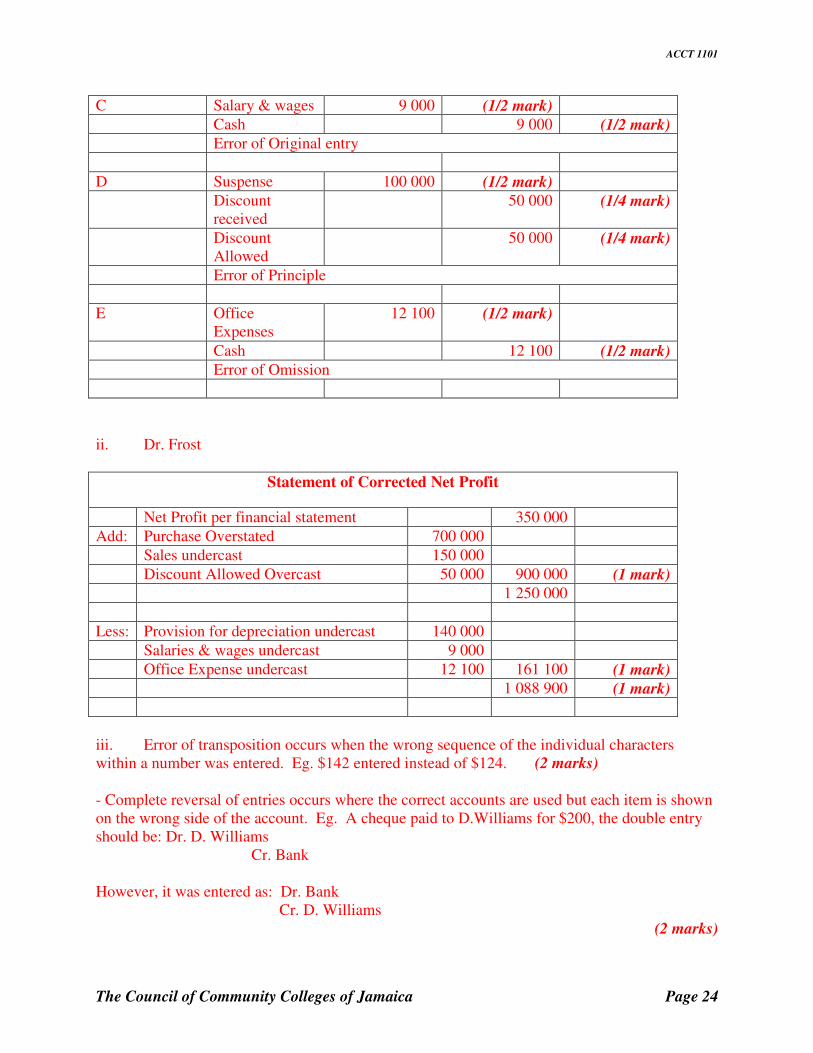

C Salary & wages 9 000 (1/2 mark)

Cash 9 000 (1/2 mark) Error of Original entry

D Suspense 100 000 (1/2 mark)

Discount received

50 000 (1/4 mark)

Discount Allowed

50 000 (1/4 mark)

Error of Principle

E Office Expenses

12 100 (1/2 mark)

Cash 12 100 (1/2 mark) Error of Omission

ii. Dr. Frost

Statement of Corrected Net Profit

Net Profit per financial statement 350 000

Add: Purchase Overstated 700 000

Sales undercast 150 000

Discount Allowed Overcast 50 000 900 000 (1 mark)

1 250 000

Less: Provision for depreciation undercast 140 000

Salaries & wages undercast 9 000

Office Expense undercast 12 100 161 100 (1 mark)

1 088 900 (1 mark)

iii. Error of transposition occurs when the wrong sequence of the individual characters within a number was entered. Eg. $142 entered instead of $124. (2 marks) - Complete reversal of entries occurs where the correct accounts are used but each item is shown on the wrong side of the account. Eg. A cheque paid to D.Williams for $200, the double entry should be: Dr. D. Williams Cr. Bank However, it was entered as: Dr. Bank Cr. D. Williams

(2 marks)

ACCT 1101

The Council of Community Colleges of Jamaica Page 25

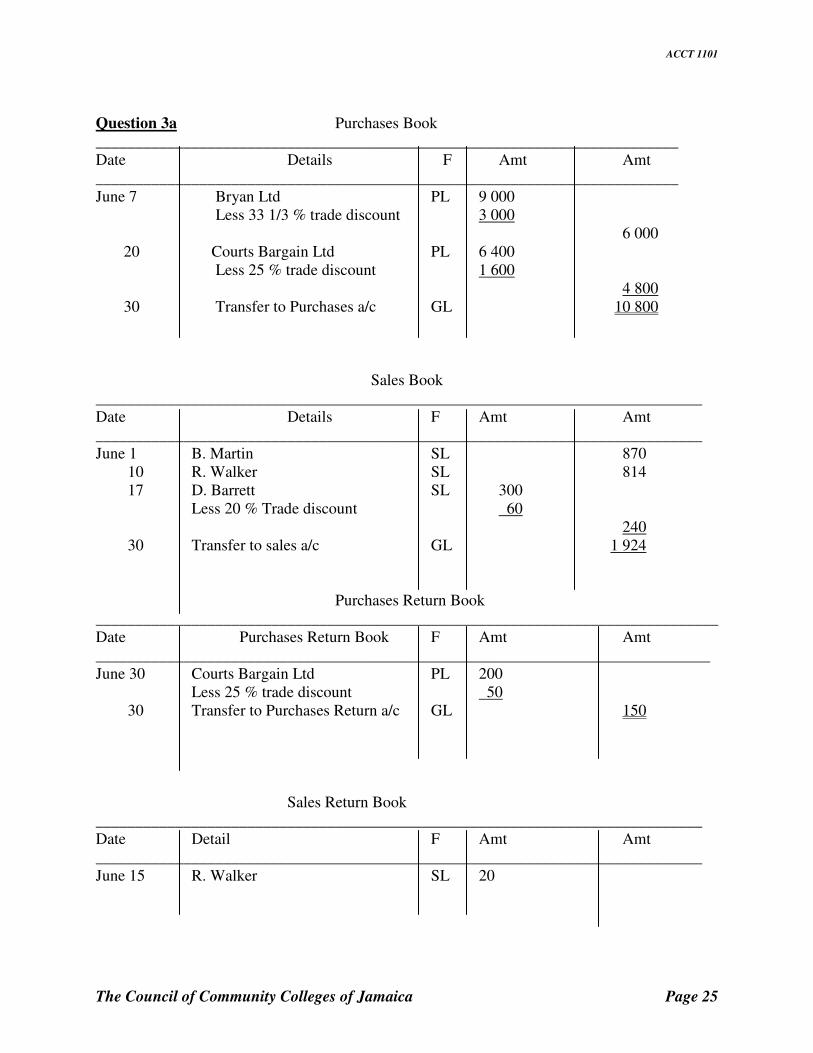

Question 3a Purchases Book _________________________________________________________________________ Date Details F Amt Amt _________________________________________________________________________ June 7 Bryan Ltd PL 9 000 Less 33 1/3 % trade discount 3 000 6 000 20 Courts Bargain Ltd PL 6 400 Less 25 % trade discount 1 600 4 800 30 Transfer to Purchases a/c GL 10 800

Sales Book ____________________________________________________________________________ Date Details F Amt Amt ____________________________________________________________________________ June 1 B. Martin SL 870 10 R. Walker SL 814 17 D. Barrett SL 300 Less 20 % Trade discount 60 240 30 Transfer to sales a/c GL 1 924 Purchases Return Book ______________________________________________________________________________ Date Purchases Return Book F Amt Amt _____________________________________________________________________________ June 30 Courts Bargain Ltd PL 200 Less 25 % trade discount 50 30 Transfer to Purchases Return a/c GL 150 Sales Return Book ____________________________________________________________________________ Date Detail F Amt Amt ____________________________________________________________________________ June 15 R. Walker SL 20

ACCT 1101

The Council of Community Colleges of Jamaica Page 26

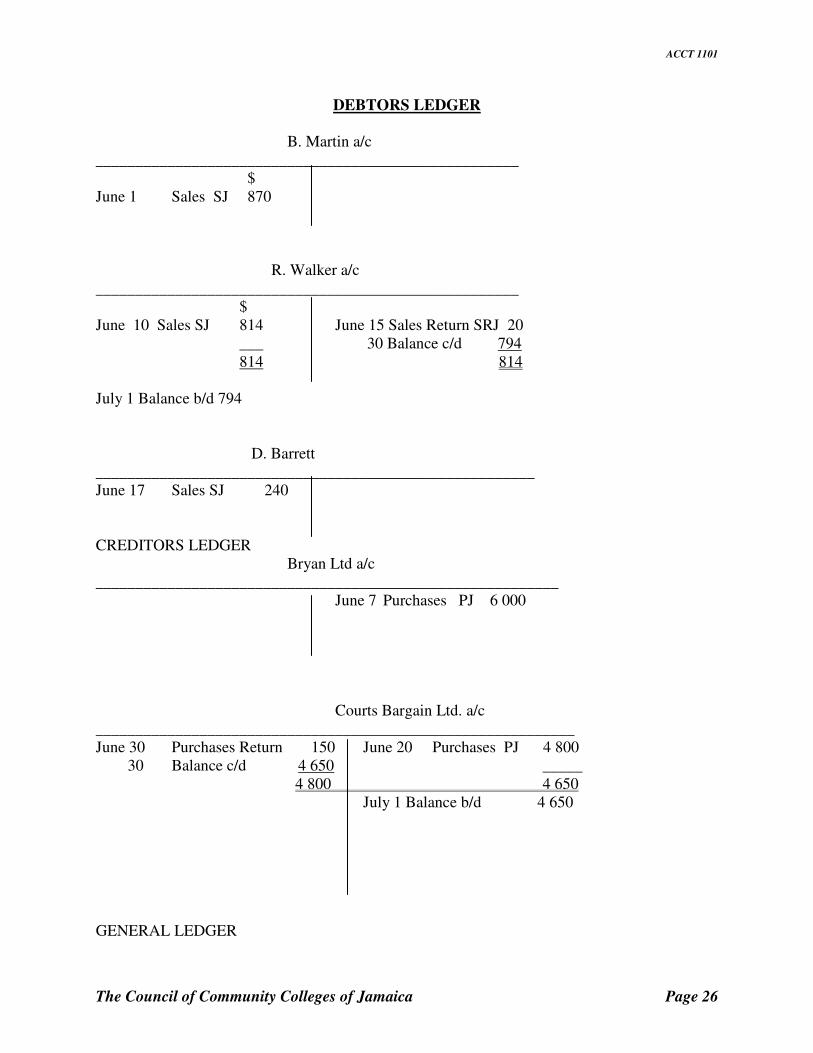

DEBTORS LEDGER B. Martin a/c _____________________________________________________ $ June 1 Sales SJ 870

R. Walker a/c _____________________________________________________ $ June 10 Sales SJ 814 June 15 Sales Return SRJ 20 ___ 30 Balance c/d 794 814 814 July 1 Balance b/d 794 D. Barrett _______________________________________________________ June 17 Sales SJ 240 CREDITORS LEDGER Bryan Ltd a/c __________________________________________________________ June 7 Purchases PJ 6 000 Courts Bargain Ltd. a/c ____________________________________________________________ June 30 Purchases Return 150 June 20 Purchases PJ 4 800 30 Balance c/d 4 650 _____ 4 800 4 650 July 1 Balance b/d 4 650

GENERAL LEDGER

ACCT 1101

The Council of Community Colleges of Jamaica Page 27

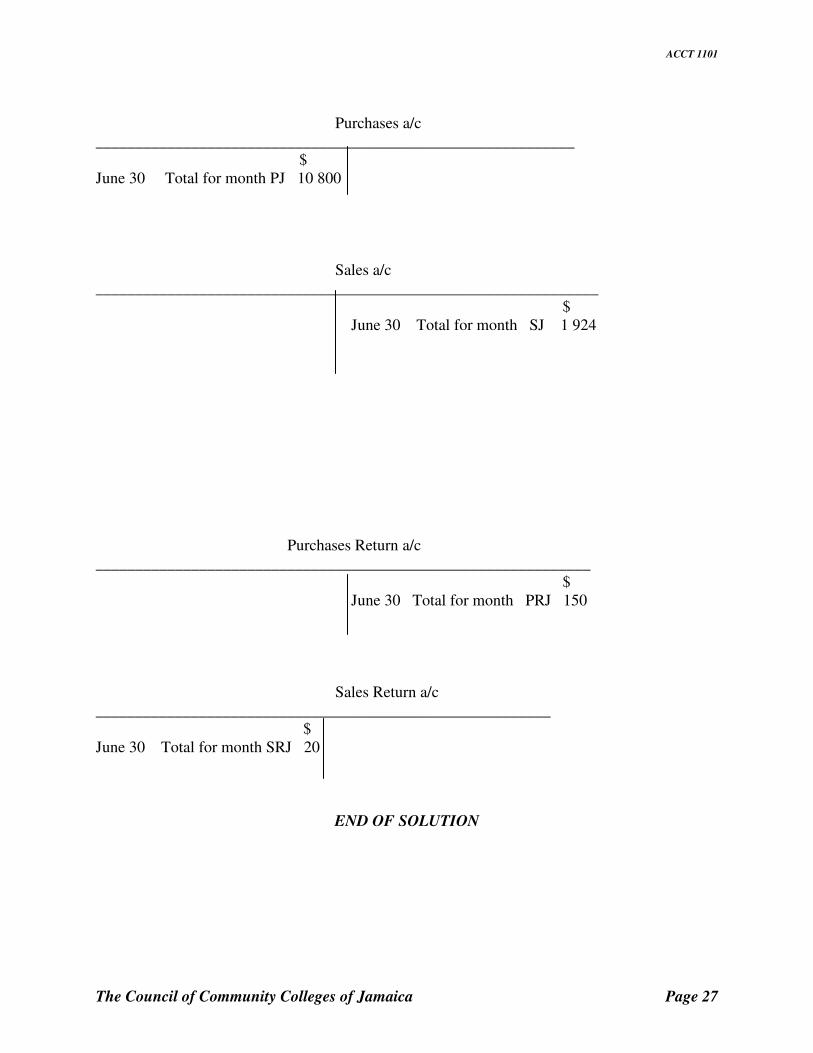

Purchases a/c ____________________________________________________________ $ June 30 Total for month PJ 10 800 Sales a/c _______________________________________________________________ $ June 30 Total for month SJ 1 924 Purchases Return a/c ______________________________________________________________ $ June 30 Total for month PRJ 150 Sales Return a/c _________________________________________________________ $ June 30 Total for month SRJ 20

END OF SOLUTION