Embed Size (px)

Citation preview

Prattle AnalyticsTradable Data From Market Chatter

Using Domain Expertise To Improve Text Analysis

--Evan A. Schnidman

▶ Everyone seems to love mining unstructured data.▶ How much time do you spend on it?

▶ Must impose STRUCTURE to make using that data efficient.

The Era of Big Data

▶ Data is not limited to numerical.

▶ Text is a goldmine of information.

▶ Examples in Finance:

-Corporate Communications

-Regulatory Filings

-Central Bank Communications

▶ Deciphering this information without structure is virtually impossible.

Data is Everywhere

▶ Expertise allows us to impose structure on otherwise messy data.

Domain Expertise

▶ Good Buzzword minus Bad Buzzword == Sentiment

▶ Domain expertise allows for much more refined analysis.

Traditional Sentiment Analysis

▶ Central Bank communications are complex and important▶ Focus today is Federal Reserve

Example: Central Banks

The Briefcase Watch

Traditional Fed Watching

Not Much has Changed

Failed Attempts

▶ Experts are biased and fail to be comprehensive

▶ Simple text analysis dictionaries don’t work for Fed Speak and other complex language

▶ Ex. “modest” v. “moderate”

Necessary Components

▶ Must use expertise to train the system based on whole communications

▶ Market response matters (Hawkish v. Dovish)

Experts in “Fed Speak”

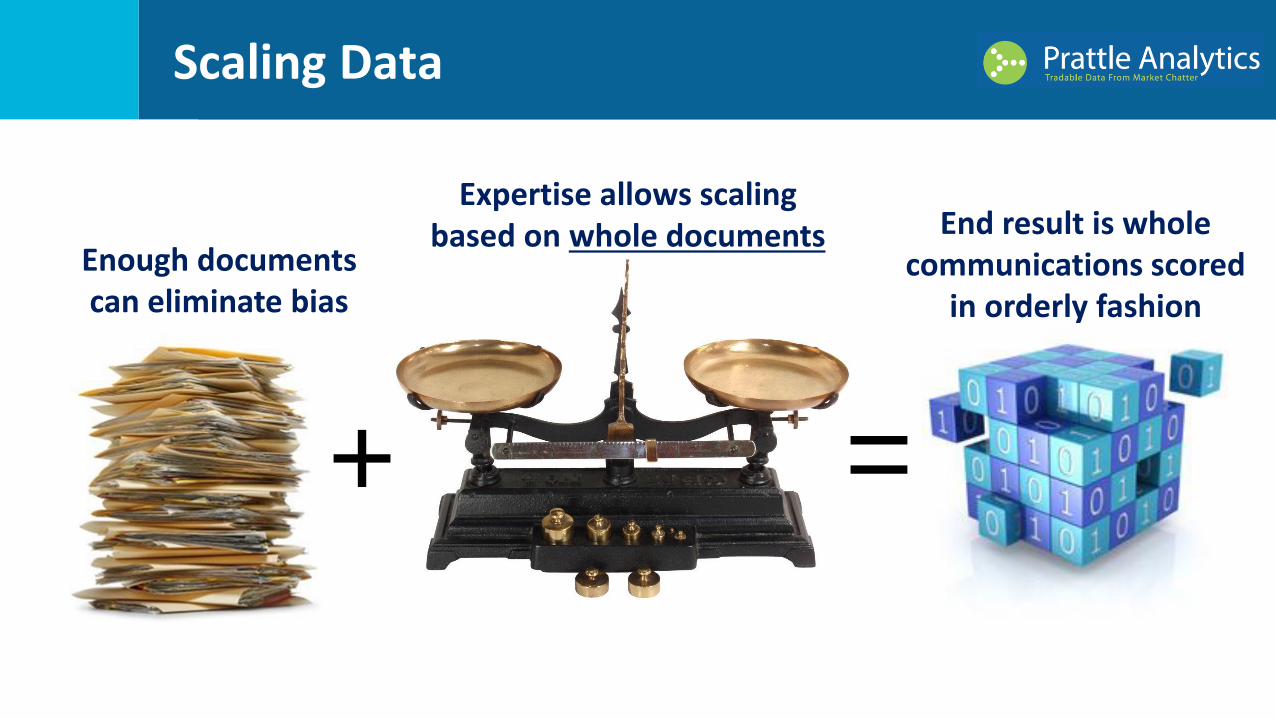

Scaling Data

+ =

Enough documents can eliminate bias

Expertise allows scaling based on whole documents End result is whole

communications scored in orderly fashion

Resulting Data:▶ Comprehensive▶ Unbiased▶ Quantitative▶ Fast

Many Possible Uses▶ Eliminate post-hoc

hedging on CB policy▶ Forecast based on

established correlations▶ Add as a signal in

multifactor model

Qual Turned Quant

Trend matters more than value!

▶ Alpha across asset classes, not just Fixed Income▶ Mitigates downside risk, especially with Equities.

▶ Beats Buy and Hold and Trend Following ▶ Low correlation to commonly used strategies▶ Better performance with FOREX because both sides of currency pair trade.

Backtested Data

Graph Courtesy

of Mavenomics

▶ Method translates across wide variety of financially important texts▶ Regulatory and shareholder documents for individual equities▶ Other regulatory information (Dodd-Frank, FDA, EPA etc.)

Other Applications

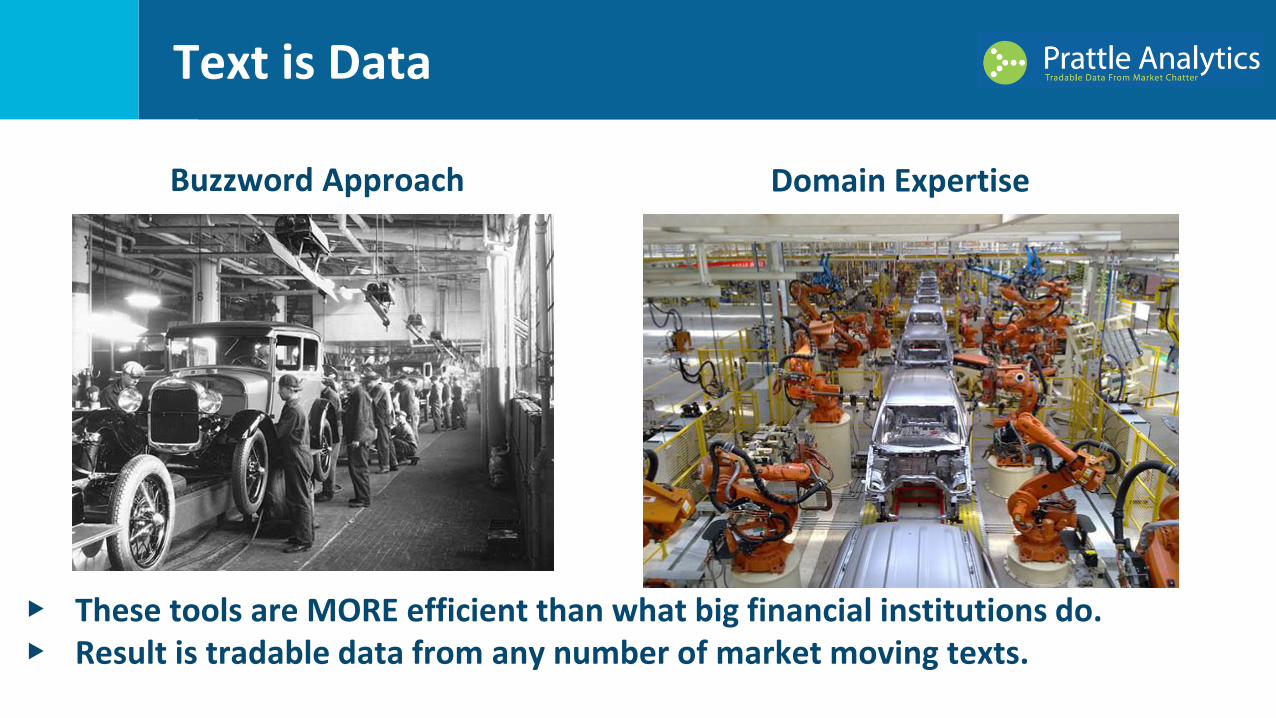

▶ These tools are MORE efficient than what big financial institutions do.▶ Result is tradable data from any number of market moving texts.

Text is Data

Buzzword Approach Domain Expertise

U.S. Federal Reserve European Central Bank Bank of EnglandBank of Canada Bank of Japan Reserve Bank of Australia Bank of Korea Reserve Bank of India Swedish Riksbank

Reserve Bank of New Zealand Central Bank of MexicoCentral Bank of BrazilCentral Bank of RussiaSouth African Reserve Bank Bank of IsraelCentral Bank of TurkeyCentral Bank of TaiwanSwiss National Bank

List of Central Banks

Tree Maps

Tree Maps

Courtesy of

Mavenomics

Forecasting

Backtesting

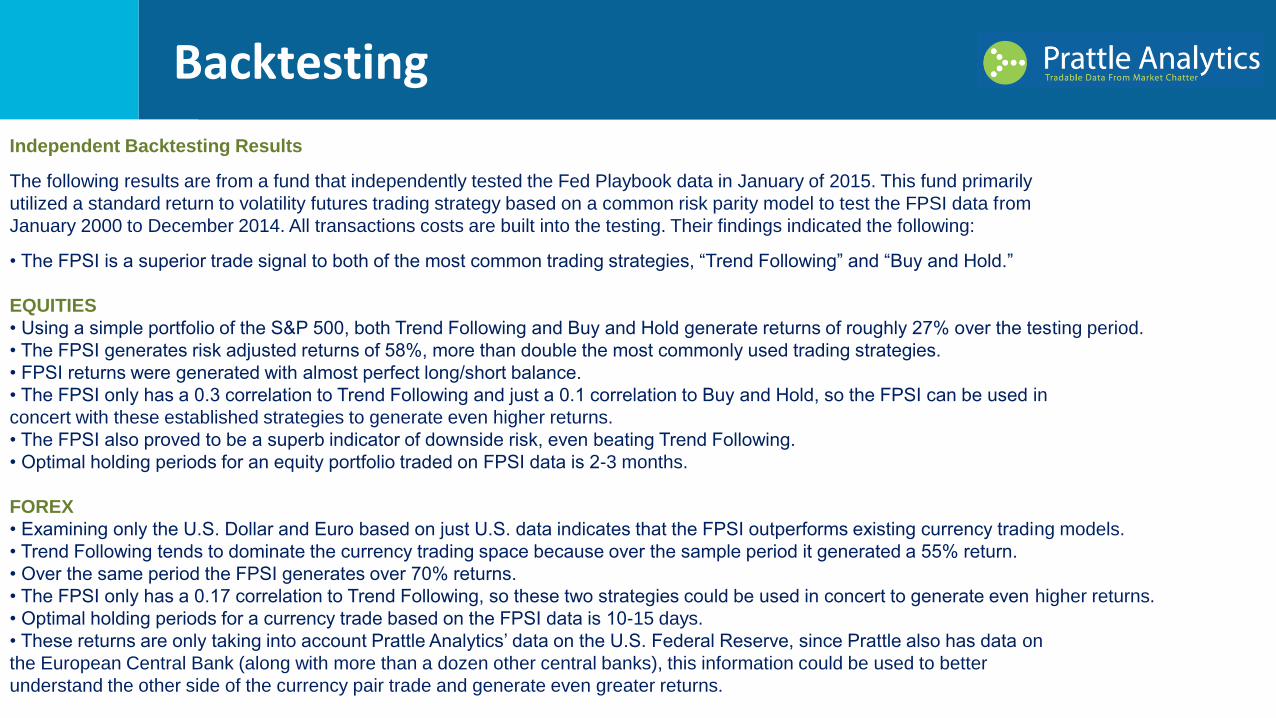

Independent Backtesting Results

The following results are from a fund that independently tested the Fed Playbook data in January of 2015. This fund primarily

utilized a standard return to volatility futures trading strategy based on a common risk parity model to test the FPSI data from

January 2000 to December 2014. All transactions costs are built into the testing. Their findings indicated the following:

• The FPSI is a superior trade signal to both of the most common trading strategies, “Trend Following” and “Buy and Hold.”

EQUITIES

• Using a simple portfolio of the S&P 500, both Trend Following and Buy and Hold generate returns of roughly 27% over the testing period.

• The FPSI generates risk adjusted returns of 58%, more than double the most commonly used trading strategies.

• FPSI returns were generated with almost perfect long/short balance.

• The FPSI only has a 0.3 correlation to Trend Following and just a 0.1 correlation to Buy and Hold, so the FPSI can be used in

concert with these established strategies to generate even higher returns.

• The FPSI also proved to be a superb indicator of downside risk, even beating Trend Following.

• Optimal holding periods for an equity portfolio traded on FPSI data is 2-3 months.

FOREX

• Examining only the U.S. Dollar and Euro based on just U.S. data indicates that the FPSI outperforms existing currency trading models.

• Trend Following tends to dominate the currency trading space because over the sample period it generated a 55% return.

• Over the same period the FPSI generates over 70% returns.

• The FPSI only has a 0.17 correlation to Trend Following, so these two strategies could be used in concert to generate even higher returns.

• Optimal holding periods for a currency trade based on the FPSI data is 10-15 days.

• These returns are only taking into account Prattle Analytics’ data on the U.S. Federal Reserve, since Prattle also has data on

the European Central Bank (along with more than a dozen other central banks), this information could be used to better

understand the other side of the currency pair trade and generate even greater returns.

Prattle AnalyticsTradable Data From Market Chatter

Using Domain Expertise To Improve Text Analysis

--Evan A. [email protected]