Embed Size (px)

Citation preview

Financial Time Series: Concept and ForecastChainarong Kesamoon, PhD Data Science Thailand [email protected]

Data Science Thailand Meetup #2 6 Nov 2015

Outline:

What is time series?

How to model financial time series?

Forecasting

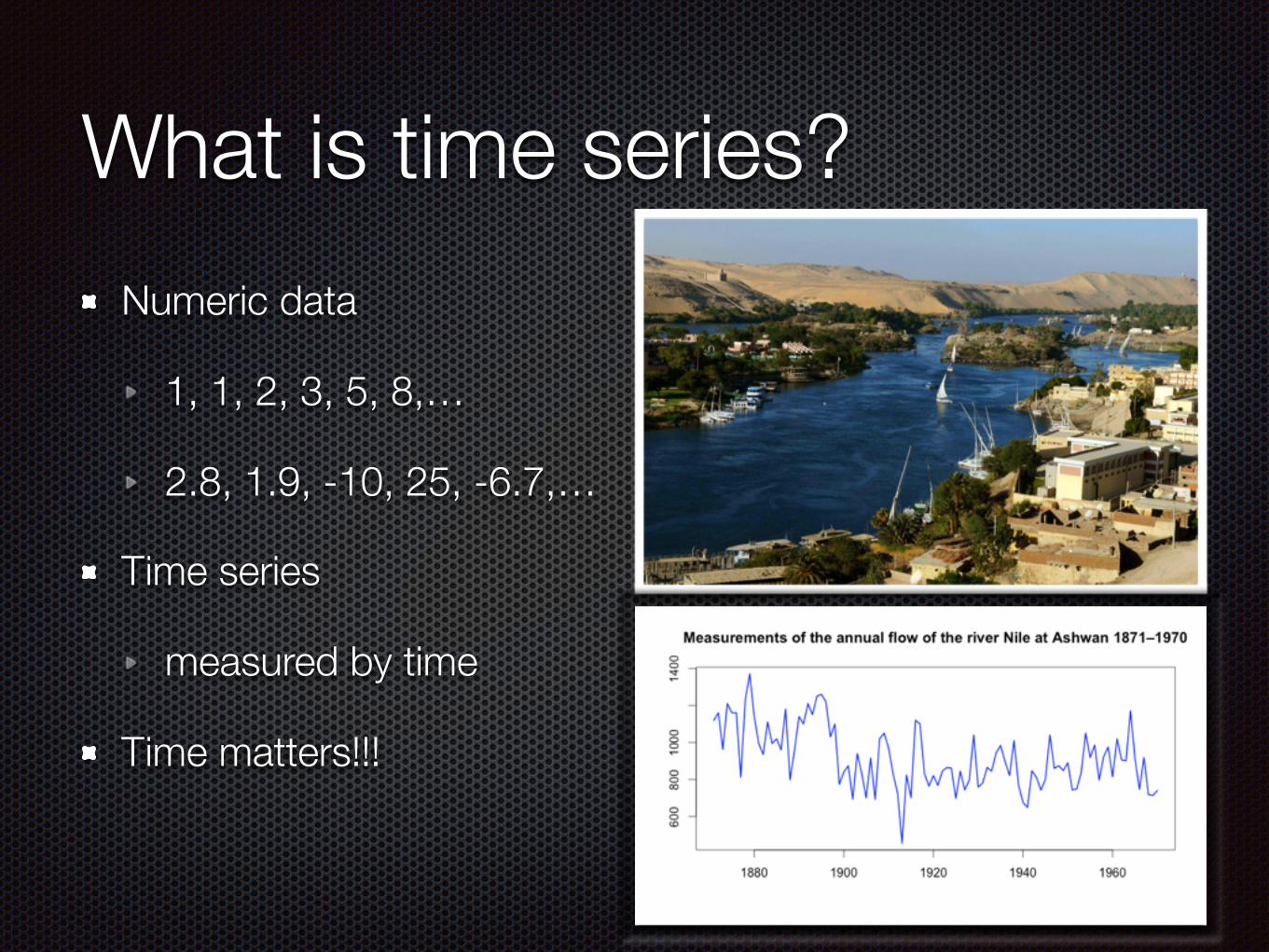

What is time series?Numeric data

1, 1, 2, 3, 5, 8,…

2.8, 1.9, -10, 25, -6.7,…

Time series

measured by time

Time matters!!!

Examples

Financial Time Series

Stock prices

Market index

Money Exchange rates

gold, oil

Typical data set source: Google Finance

We would like to know:

Tomorrow prices!!!

Chance of profit or loss

Future value of our money

That’s all about “Return & Risk”

Return

Today’s return=today’s price - yesterday’s price

Percentage return = Today’s return/yesterday’s price

Log return = log(today’s price) - log(yesterday’s price)

know return then we also know price

Better analyze returns than prices

Let’s analyze!

CorrelationPositive correlation :

More experience, more salary

Where there’s a will, there’s a way.

Negative correlation:

The higher the Doy, the lower the temperature.

The more one works, the less free time one has.

No correlation:

The color of your shirt, the color of my shoes.

Coefficient of Correlationmpg Miles/(US) gallon

cyl Number of cylinders

disp Displacement (cu.in.)

hp Gross horsepower

drat Rear axle ratio

wt Weight (lb/1000)

qsec 1/4 mile time

vs V/S

am Transmission (0 = automatic, 1 = manual)

gear Number of forward gears

carb Number of carburetors

Correlation between returns on different days

Can we forecast the return?Imagine you have tossed a normal coin ten times, last five outcomes were all head.

Do you expect that the next outcome would be head?

If there is no correlation, the next outcome would be like tossing a coin.

Seem hopeless T__T

H T T H

T H H H

H H

1 2 3 4

5 6 7 8

9 10 11

?

Efficient Market Hypothesis A financial economist and passionate defender of the efficient markets hypothesis (EMH) was walking down the street with a friend. The friend stops and says, "Look, there's a $20 bill on the ground."

The economist turns and says, "Boy, this must be our lucky day! Better pick that up quick because the market is so efficient it won't be there for very long. Finding a $20 bill lying around happens so infrequently that it would be foolish to spend our time searching for more of them. Certainly, after assigning a value to the time spent in the effort, an 'investment' in trying to find money lying on the street just waiting to be picked up would be a poor one. I am also certainly not aware of lots of people, if any, getting rich mining beaches with metal detectors."

When he had finished they both look down and the $20 bill was gone!

source: http://www.etf.com/sections/features/123.html

Let’s try another way

Why squared return?The variance of return is calculated from squared returns.

Why variance? What is it?

Variance is the degree of variation

High variance => high volatility=> high risk

Volatility is forecastable

High risk, high return (but return can be either + or - )

Major Stylized Facts for Return

I. The distribution of returns is not normal, it has a high peak and fat tails.

II. There is almost no correlation between returns for different days.

III. There is positive correlation between squared returns on nearby days, likewise for absolute returns.

Time series modelsGeneral time series models:

MA : moving average

AR : autoregressive

ARMA : autoregressive moving average

ARIMA, ARFIMA,…

Financial time series models:

EWMA : exponentially weighted moving average

(G)ARCH : (generalized) autoregressive conditional heteroskedastic

SV : stochastic volatility

Asset pricing model

Black-Scholes model

Robert F. Engle Tim BollerslevNobel Prize in Economic Sciences 2003

GARCH modelGeneralized AutoRegressive Conditional Heteroskedasticity Modelrt+1 = µ+ �t+1✏t+1

�2t+1 = ! + ↵(rt � µ)2 + ��2

t

where ✏t+1 ⇠ N(0, 1)

ExamplesGARCH volatility forecasting

Using data up to 5 Nov 2015Date Return SD6 Nov 0 0.3847 Nov 0 0.3908 Nov 0 0.3969 Nov 0 0.401

10 Nov 0 0.40711 Nov 0 0.41212 Nov 0 0.41613 Nov 0 0.421

"When Professors Scholes and Merton and I invested in warrants, Professor Merton lost the most money. And I lost the least”

– Fischer Black –

Nobel Prize in Economic Sciences1997: Fischer Black, Myron Scholes, and Robert

Merton

Challenging, isn’t it?Financial time series is challenging as it is quite difficult to forecast.

Multivariate time series is also of interest, but it is even more difficult to model multiple time series together.

Most financial models were created some years ago, at the time that less data were available.

Nowadays, we can access more and more data, that would be a good opportunity to explore and create better models for financial market.

–Chainarong Kesamoon

“Moltes Gracies”