Embed Size (px)

Citation preview

www.hanrickcurran.com.au

Data Analysis for Hanrick Curran

June 2016

2experience. new thinking

What can you learn …

Basic data analysis requirements Using Excel™ Using TeamMate™ Audit implications

4experience. new thinkingexperience. new thinking 4

An understanding of the basics of performing data analysis and computer assisted audit techniques (“CAATs”) is a core part of any auditors toolkit.

Basics

5experience. new thinking

Terminology

Workbook – an excel file with multiple sheets Worksheet – an individual sheet in an excel file Row (record) – a row of data on a worksheet Column (field) – a column of data on a worksheet Table – a part of a worksheet containing data Array – Control totals – details of the file to be imported that

provide certainty that all data has been received / imported

6experience. new thinking

Audit benefits

Data analysis adds to the evidence that we obtain during our audit procedures by enabling us to look at data for the entire population.

This analysis provides additional evidence regarding our audit that is supplemental to our detailed substantive testing.

Data analysis may provide anywhere from minimal to persuasive evidence for the purpose of “Other Substantive Tests”. Of course, this assessment remains a matter of professional judgement.

7experience. new thinking

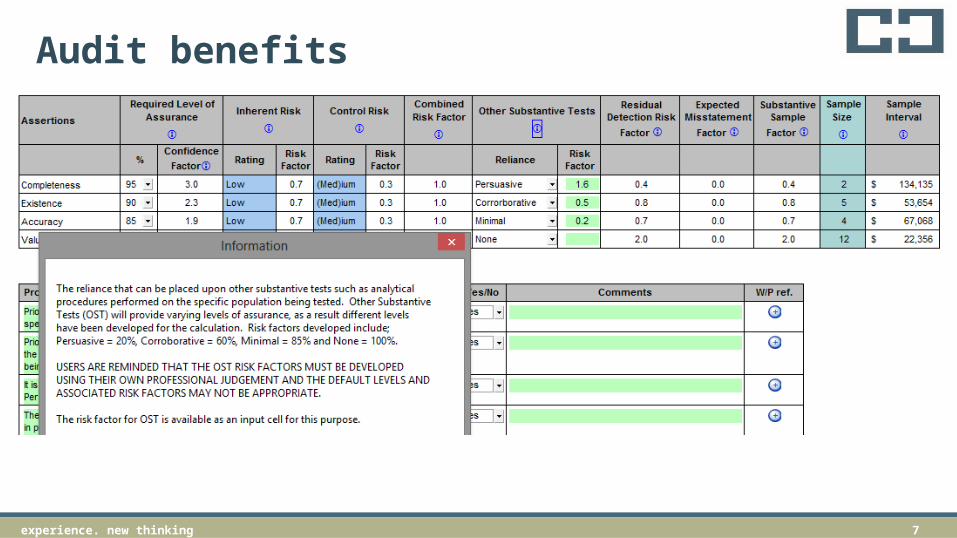

Audit benefits

8experience. new thinking

Getting data from the client Plan your request to the client Set out your needs clearly (email / letter) Allow plenty of time Include a diary reminder

9experience. new thinking

Control totals

When requesting data from clients, have them confirm control totals

Control totals are usually details such as the number of rows / records and the value of a control field (e.g., total payments)

Use the control total to confirm that all records have been correctly imported and that the value of transactions imported agrees with the information provided by the client

10experience. new thinking

Protecting evidence

When analysing data in excel, be careful to maintain the integrity of the information supplied by the client

Work on a copy of the client’s worksheet Keep the original client datafile separate

from the working file Do your backups

11experience. new thinking

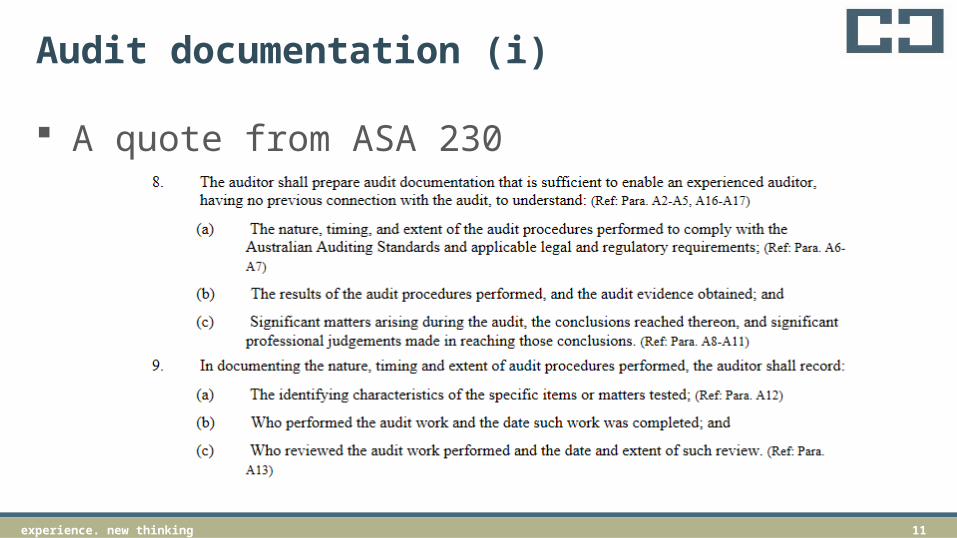

Audit documentation (i)

A quote from ASA 230

12experience. new thinking

Audit documentation (ii)

You need to retain sufficient evidence in your audit workpapers to meet the standards

This does not mean you have to keep the full client records (e.g., payments register)

13experience. new thinkingexperience. new thinking 13

Excel can be used for a large amount of basic data analysis

Excel analysis

14experience. new thinking

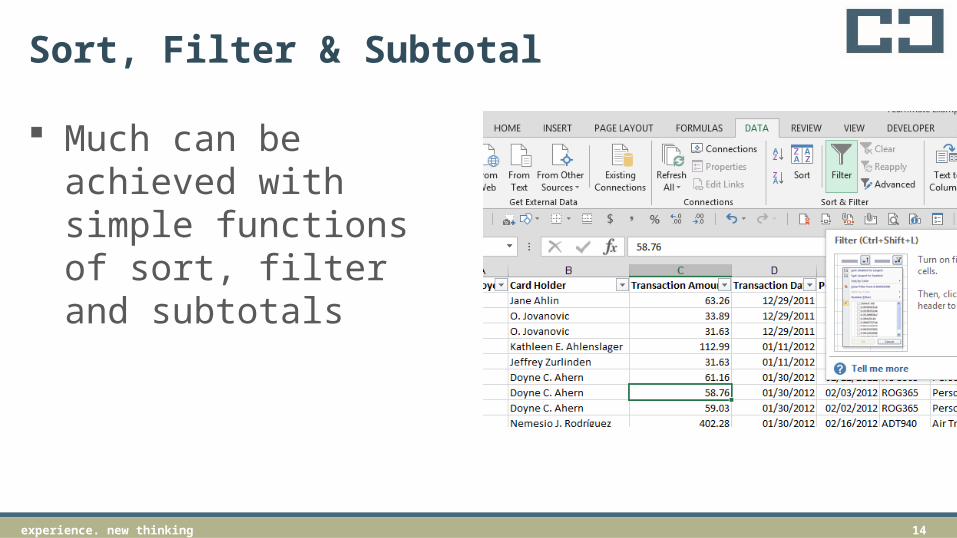

Sort, Filter & Subtotal

Much can be achieved with simple functions of sort, filter and subtotals

15experience. new thinking

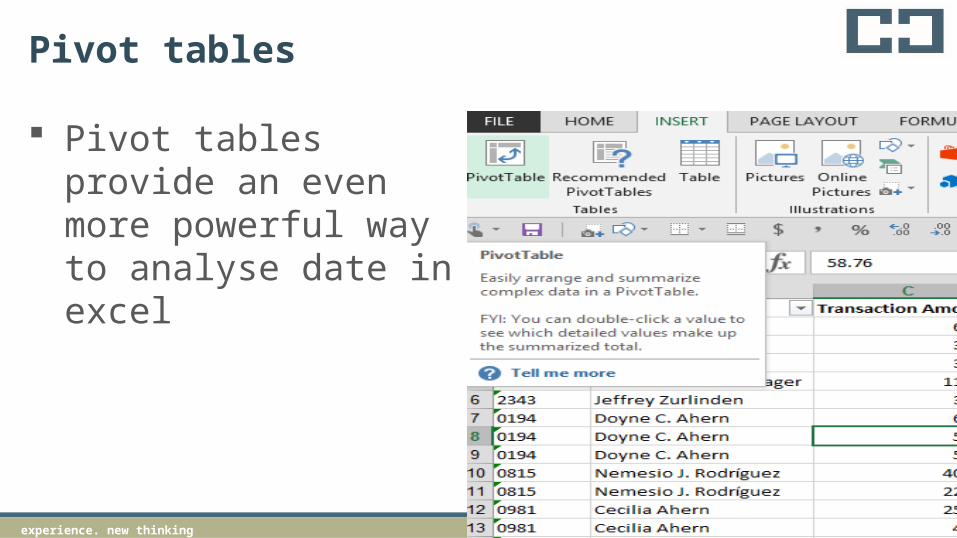

Pivot tables

Pivot tables provide an even more powerful way to analyse date in excel

16experience. new thinking

Vlookup – to join data tables

Vlookup can be used to join data tables Key is to have a common data field (“key”)

that is in both tables

Activity – vlookup on bank account between payroll list and AP list

17experience. new thinking

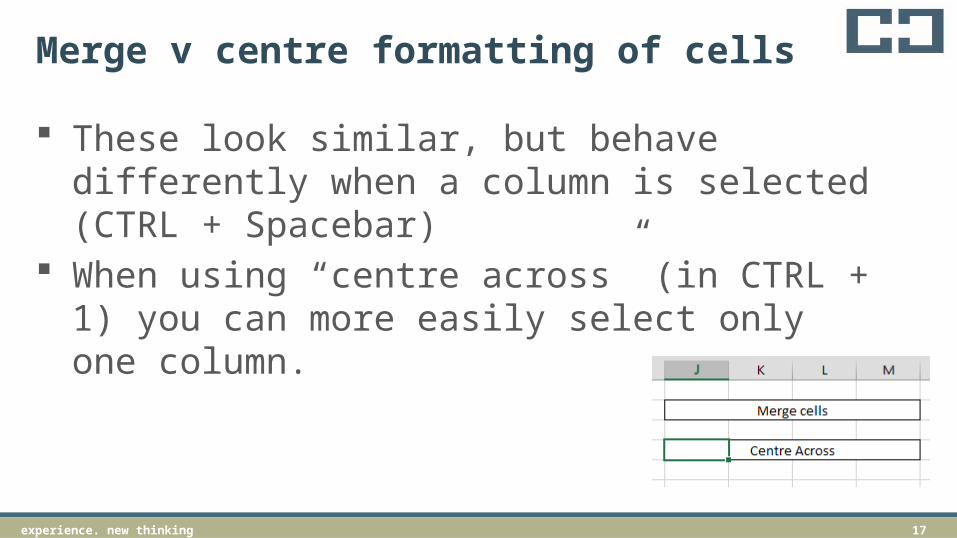

Merge v centre formatting of cells

These look similar, but behave differently when a column is selected (CTRL + Spacebar)

When using “centre across” (in CTRL + 1) you can more easily select only one column.

18experience. new thinking

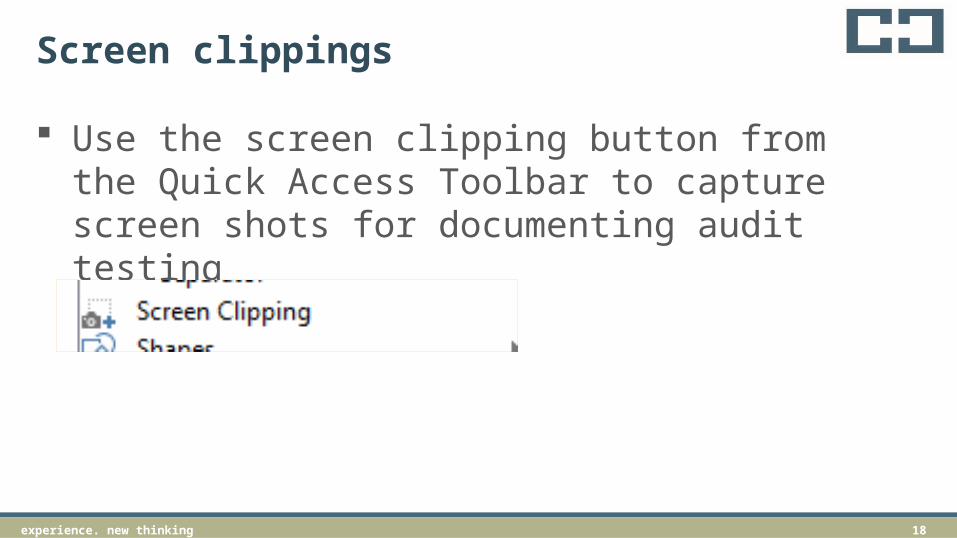

Screen clippings

Use the screen clipping button from the Quick Access Toolbar to capture screen shots for documenting audit testing

19experience. new thinking

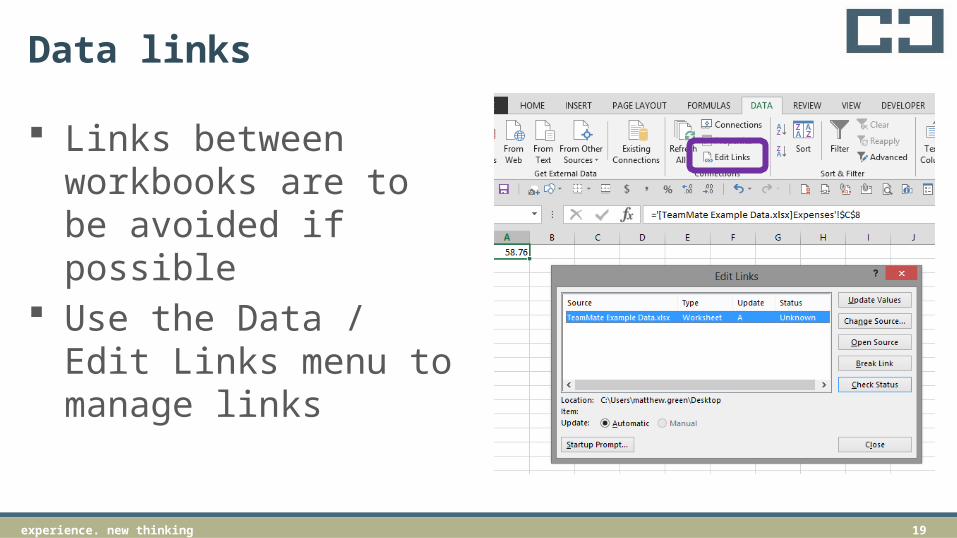

Data links

Links between workbooks are to be avoided if possible

Use the Data / Edit Links menu to manage links

20experience. new thinking

TB editing

TB’s come in many formats, often with the “-” or credit sign at the back of numbers.

Activity– for TB(1) and TB(2), use the functions to manipulate the data to prepare a TB for importing to CaseWare

21experience. new thinking

TB editing - exampleSteps to fix the TB Use TeamMate / ASAP-Utilities ? (see http://www.asap-utilities.com /) Sort the TB on the balance numbers In the next column over, copy the numbers into the new column, leave the

debit numbers alone For the credit numbers, include a formula “= - (main number)” On the main numbers, highlight the credit numbers and use CTRL + H to

access “find and replace” Find the minus sign (-) and replace with nothing For the new column of numbers (which should now add to zero), copy the

column and use paste values (ALT-H-V-V) paste the values into the sheet Delete the column with the original numbers and import to CaseWare TB

module

22experience. new thinkingexperience. new thinking 22

TeamMate is the data analysis software that we have selected for our auditors. This software works as an add-in to Excel and should be used as the basis for our data analysis during audit assignments.We have other tools available, which include IDEA and Spreadsheet Detective.

TeamMate

23experience. new thinking

Append / join sheets

Join sheets - Joins two sheets together, based on a common matching column, e.g. common bank test, inventory for NPV testing. (Activity)

Append sheets - Joins multiple sheets that all have the same column structure together. For example, where you have separate reports for each sales person, each warehouse, etc. that you wish to combine into one report. (Activity)

24experience. new thinking

Manipulate fields

An available tool inside TeamMate that can be used for data manipulation

Can be used for all sorts of different actions and is well worth exploring

Highlights : Normalize fields – tool to standardize fields Debit and credit columns – splits/ combines Dr and Cr columns

(example) Merge wrap and autofit – combines those functions from Excel into one

(example)

25experience. new thinking

Stratify

Used to obtain information regarding the characteristics of a data set

Should be run on all files as a preliminary activity with the objective of understanding the nature of the population under investigation

Activity – stratify the expenses listing

26experience. new thinking

Extract (duplicates / gaps / sample) Can be used to extract relevant data from a population (e.g.,

duplicates, gaps or samples) Gaps extraction - Identifies for gaps in a sequence of numbers or

partly numeric references, such as missing invoices or journals. Duplicates extraction - Extracts duplicate records, based on up to

3 fields you specify. Can be used to isolate specific transactions/records for further

investigation

Activity – review the Payables for duplicates, extract gaps in General journal listing

27experience. new thinking

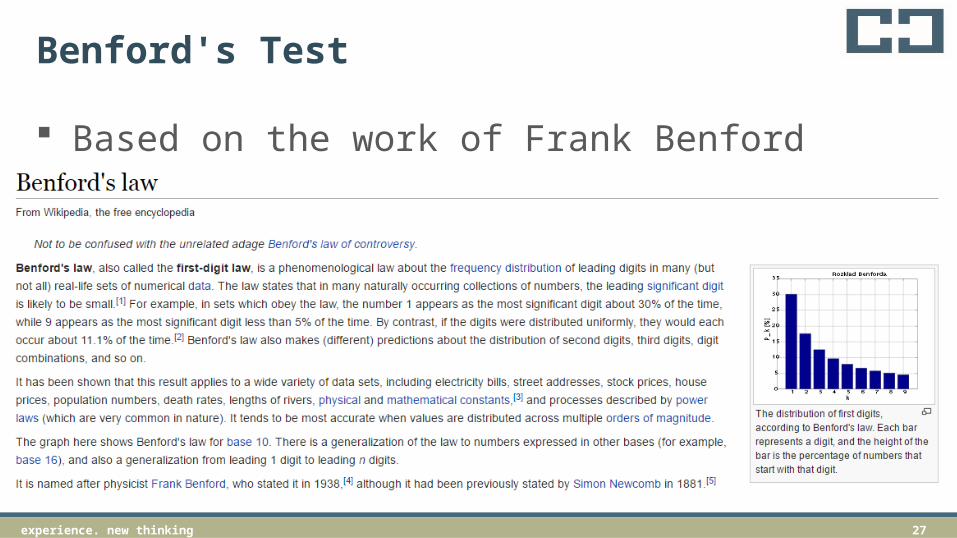

Benford's Test

Based on the work of Frank Benford

28experience. new thinking

Benford's Test

Benford’s test should be run on all data sets to identify any anomalous transactions that may warrant further investigation

Activity – run Benford’s on the expenses listing

29experience. new thinking

Outliers

Used to extract records from a data set that are at the edge of the normal distribution

Can be used to extract records more than X times the average or standard deviation

30experience. new thinking

Sampling

Sampling is used to extract records for further analysis as part of detailed substantive testing

Various types of sampling can be undertaken (refer additional slides)

31experience. new thinking

Sampling - MUS

Our preferred method for sample selection is the use of a MUS (Monetary Unit Sample).

A MUS sample is preferred because of the effectiveness of the audit testing that results and the efficiency of the sample selection (e.g., all ‘high value’ items will be selected).

32experience. new thinking

Sampling MUS – activity

Using materiality of $4,000 generate a MUS sample for the expenditure file

33experience. new thinking

Random sample - Extracts a number of randomly sampled items from your population.

Systematic sample - Extracts every ‘nth’ item from the population.

Stratified sample – Stratifies data and select a random sample from each strata band

Other types of sampling

34experience. new thinking

Activity on Revenue analytics

Year-on-year analytical review with TeamMate

35experience. new thinking

If you want to explore more, visit video demonstrations website:

http://www.topcaats.com/resources/demonstrations/

36experience. new thinking

AUDIT EVIDENCEUnderstanding the requirements of ASA 500

37experience. new thinking

ASA 500 – audit evidence

4. The objective of the auditor is to design and perform audit procedures in such a way as to enable the auditor to obtain sufficient appropriate audit evidence to be able to draw reasonable conclusions on which to base the auditor’s opinion.

Audit Training - Sampling - June 2013

38experience. new thinking

ASA 500 – audit evidence 5(b). Appropriateness means the measure of the

quality of audit evidence; that is, its relevance and its reliability in providing support for the conclusions on which the auditor’s opinion is based.

5(e) Sufficiency means the measure of the quantity of audit evidence. The quantity of the audit evidence is affected by the auditor’s assessment of the risks of material misstatement and also by the quality of such audit evidence.

Audit Training - Sampling - June 2013

39experience. new thinking

ASA 500 – audit evidence9. When using information produced by the entity, the

auditor shall evaluate whether the information is sufficiently reliable for the auditor’s purposes, including as necessary in the circumstances:(a) Obtaining audit evidence about the accuracy and

completeness of the information; and(b) Evaluating whether the information is sufficiently

precise and detailed for the auditor’s purposes.

“ASIC’s Top 10 issues for auditors includes a failure to apply professional scepticism and document work.

Audit Training - Sampling - June 2013

40experience. new thinking

ASA 500 – Requirements for audit evidence11. if:

(a) audit evidence obtained from one source is inconsistent with that obtained from another; or

(b) the auditor has doubts over the reliability of information to be used as audit evidence,

the auditor shall determine what modifications or additional to audit procedures are necessary to resolve the matter, and shall consider the effect of the matter, if any, on other aspects of the audit.

Audit Training - Sampling - June 2013

41experience. new thinking

ASA 500 – Requirements for audit evidence A2. … procedures to obtain audit evidence can include

Inspection Observation Confirmation Re-calculation Re-performance Analytical procedures Enquiry

Audit Training - Sampling - June 2013

42experience. new thinking

ASA 500 – Requirements for audit evidence A52. … The means available to the

auditor for selecting items for testing are:(a) selecting all items (100% testing)(b) selecting specific items(c) audit sampling

Testing

All items

Specific items

Sampling

Audit Training - Sampling - June 2013

43experience. new thinking

AUDIT SAMPLINGUnderstanding the requirements of ASA 530

44experience. new thinking

ASA 530 – Requirements for audit sampling 5(a). Audit sampling means the application of audit

procedures to less than 100% of items within a population of audit relevance such that all sampling units have a chance of selection in order to provide the auditor with a reasonable basis on which to draw conclusions about the entire population.

5(b) Population means the entire set of data from which a sample is selected and about which the auditor wishes to draw conclusions.

Audit Training - Sampling - June 2013

45experience. new thinking

ASA 530 – Requirements for audit sampling 5(c). Sampling risk means the risk that the

auditor’s conclusions based on a sample may be different from the conclusion if the entire population were subjected to the same audit procedure.

5(d) Non-sampling risk means the risk that the auditor reaches an erroneous conclusion for any reason not related to sampling risk.

Audit Training - Sampling - June 2013

46experience. new thinking

ASA 530 – Requirements for audit sampling 5(e). Anomaly means a misstatement or

deviation that is demonstrably not representative of misstatements or deviations in a population.

Audit Training - Sampling - June 2013

47experience. new thinking

ASA 530 – Requirements for audit sampling 5(g). Statistical sampling means an approach to

sampling that has the following characteristics:(i)Random selection of sample items; and(ii)The use of probability theory to evaluate

sample results, including measurement of sampling risks.

A sampling approach that does not have characteristics (i) and (ii) is considered non-statistical sampling.

Audit Training - Sampling - June 2013

48experience. new thinking

ASA 530 – Requirements for audit sampling 5(i). Tolerable misstatement means a monetary amount

set by the auditor in respect of which the auditor seeks to obtain an appropriate level of assurance that the monetary amount set by the auditor is not exceeded by the actual misstatement in the population.

“Typically this would be the amount determined as materiality, specifically the performance materiality, or a lower amount.

Audit Training - Sampling - June 2013

49experience. new thinking

ASA 530 – Requirements for audit sampling12. The auditor shall investigate the nature and cause of any deviations or

misstatements identified, and evaluate their possible effect on the purpose of the audit procedure and on other areas of the audit

13. In the extremely rare circumstances when the auditor considers a misstatement or deviation discovered in a sample to be an anomaly, the auditor shall obtain a high degree of certainty that such misstatement or deviation is not representative of the population. The auditor shall obtain this degree of certainty by performing additional audit procedures to obtain sufficient appropriate evidence that the misstatement or deviation does not affect the remainder of the population.

Audit Training - Sampling - June 2013

50experience. new thinking

Sample selection methods (ASA 530.App 4)(a) Random selection (applied through random number generators or random number

tables)

Audit Training - Sampling - June 2013

51experience. new thinking

Sample selection methods (ASA 530.App 4) (b) Systematic selection, in which the number of sampling units in the

population is divided by the sample size to give a sampling interval, for example 50, and having determined a starting point within the first 50, each 50th sampling unit thereafter is selected. Although the starting point may be determined haphazardly, the sample is more likely to be truly random if it is determined by use of a computerised random number generator or random number tables. When using systematic selection, the auditor would need to determine that sampling units within the population are not structured in such a way that the sampling interval corresponds with a particular pattern in the population.

Audit Training - Sampling - June 2013

52experience. new thinking

Sample selection methods (ASA 530.App 4)(c) Monetary Unit Sampling is a type of value-weighted selection (as described in

Appendix 1) in which sample size, selection and evaluation results in a conclusion in monetary amounts.

“Also known as Dollar Unit Sampling (DUS) or Constant Monetary Amount (CMA) sampling.

Audit Training - Sampling - June 2013

53experience. new thinking

Sample selection methods (ASA 530.App 4) (d) Haphazard selection, in which the auditor selects the sample without

following a structured technique. Although no structured technique is used, the auditor would nonetheless avoid any conscious bias or predictability (for example, avoiding difficult to locate items, or always choosing or avoiding the first or last entries on a page) and thus attempt to ensure that all items in the population have a chance of selection. Haphazard selection is not appropriate when using statistical sampling.

Audit Training - Sampling - June 2013

54experience. new thinking

Sample selection methods (ASA 530.App 4) (e) Block selection involves selection of a block(s) of contiguous items from

within the population. Block selection cannot ordinarily be used in audit sampling because most populations are structured such that items in a sequence can be expected to have similar characteristics to each other, but different characteristics from items elsewhere in the population. Although in some circumstances it may be an appropriate audit procedure to examine a block of items, it would rarely be an appropriate sample selection technique when the auditor intends to draw valid inferences about the entire population based on the sample.

Audit Training - Sampling - June 2013

55experience. new thinking

DETERMINING A SAMPLE SIZEUsing the ICAA Audit Manual

56experience. new thinking

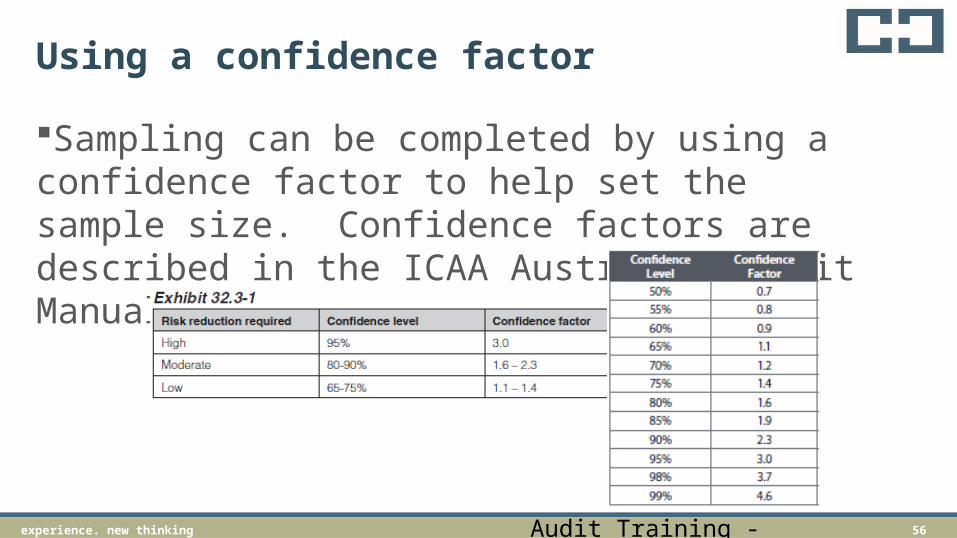

Using a confidence factor

Sampling can be completed by using a confidence factor to help set the sample size. Confidence factors are described in the ICAA Australian Audit Manual (p.497)

Audit Training - Sampling - June 2013

57experience. new thinking

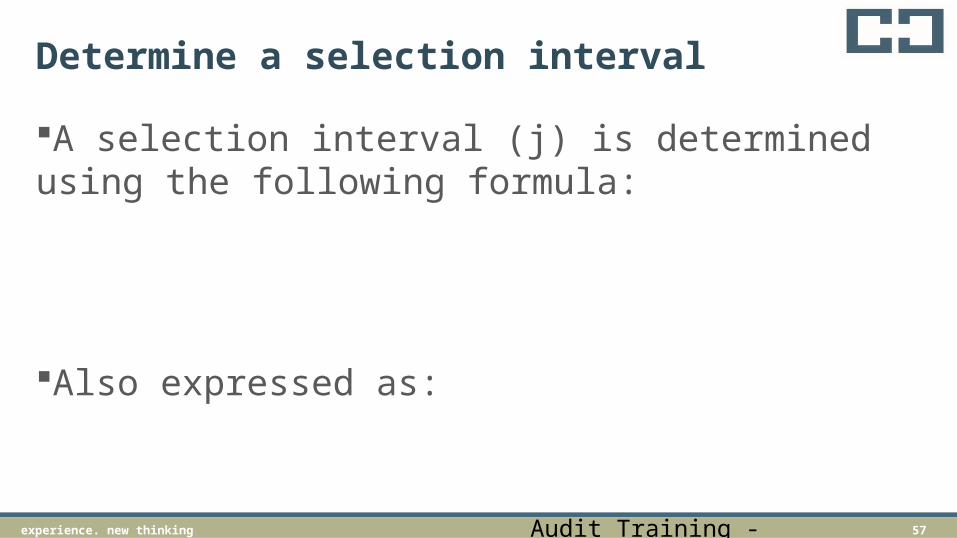

Determine a selection interval

A selection interval (j) is determined using the following formula:

Also expressed as:

Audit Training - Sampling - June 2013

58experience. new thinking

Determine a sample size

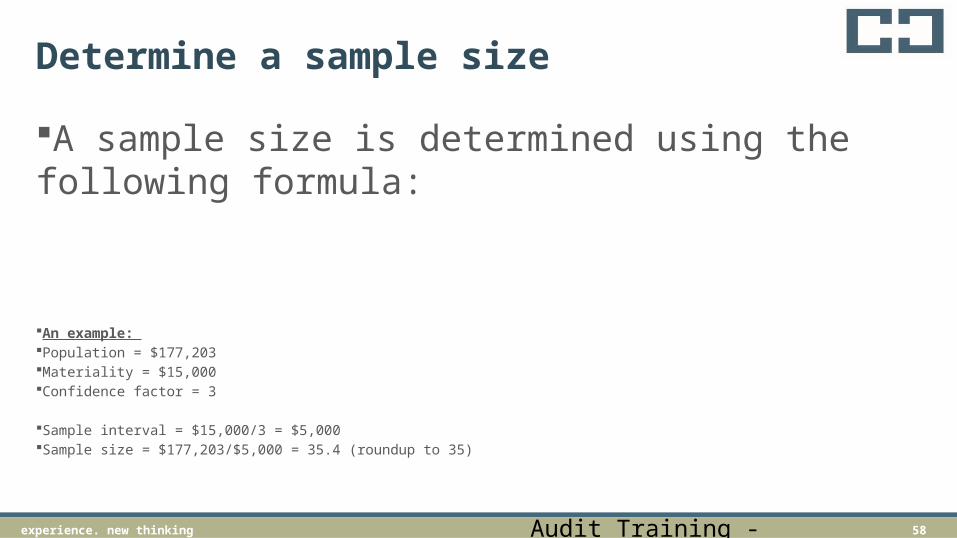

A sample size is determined using the following formula:

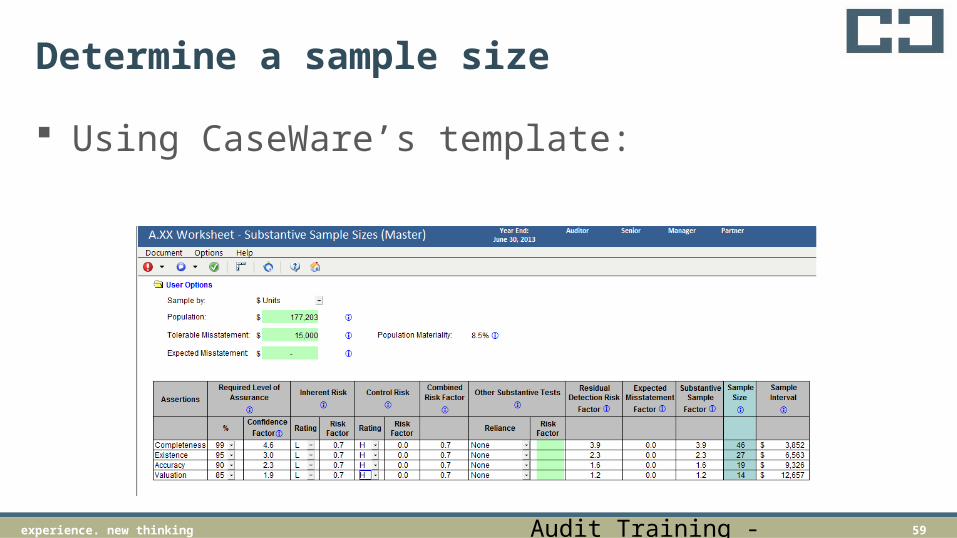

An example: Population = $177,203Materiality = $15,000Confidence factor = 3

Sample interval = $15,000/3 = $5,000Sample size = $177,203/$5,000 = 35.4 (roundup to 35)

Audit Training - Sampling - June 2013

59experience. new thinking

Determine a sample size

Using CaseWare’s template:

Audit Training - Sampling - June 2013

60experience. new thinking

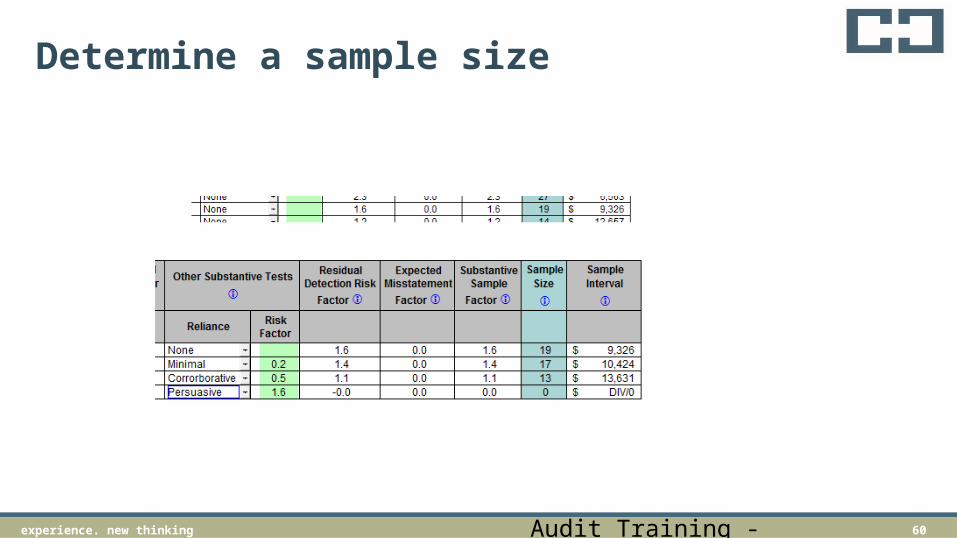

Determine a sample size

Audit Training - Sampling - June 2013

61experience. new thinking

How do I select a confidence factor?

“professional judgement.

Audit Training - Sampling - June 2013

62experience. new thinking

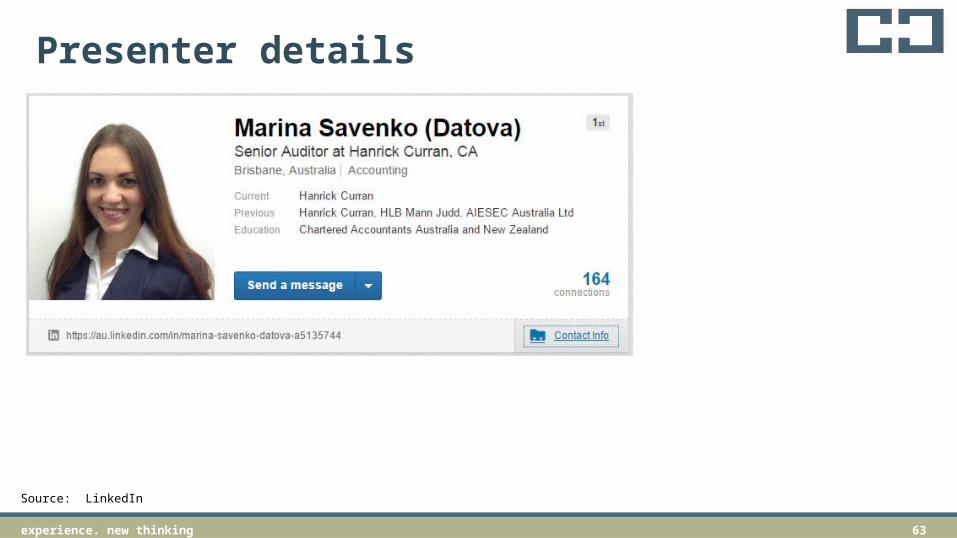

Presenter details

Source: LinkedIn

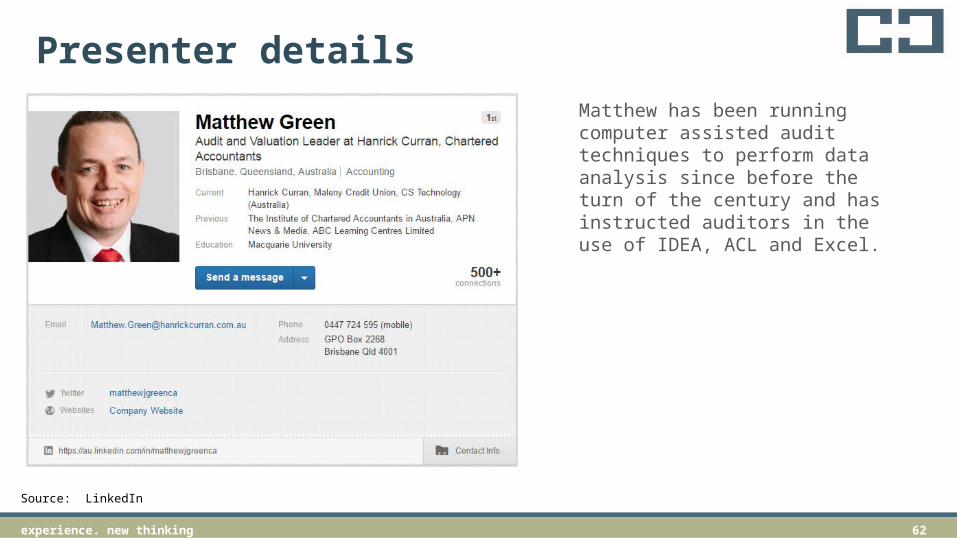

Matthew has been running computer assisted audit techniques to perform data analysis since before the turn of the century and has instructed auditors in the use of IDEA, ACL and Excel.

63experience. new thinking

Presenter details

Source: LinkedIn

Thank you

www.hanrickcurran.com.au

Hanrick Currant. (07) 3218 3900f. (07) 3218 3901e. [email protected]

Level 11307 Queen StreetBrisbane Qld 4000

GPO Box 2268Brisbane Qld 4001