Embed Size (px)

Citation preview

PRESENTATION ON

ALTERNATIVE CHANNELS OF

BANKING

ALTERNATIVE CHANNELS

WHAT IS...

Alternative banking, as the name suggest, is the NEWER METHOD OF CARRYING ON BANKING OPERATIONS

DIFFERENT CHANNELS

1. ATM (AUTOMATIC TELLER MACHINE)

2. POS TERMINAL3. INTERNET BANKING4. MOBILE BANKING5. NEFT 6. RTGS7. ECS

ATM (AUTOMATIC TELLER

MACHINES)

Invented in 1960’S by JOHN SHEPHERD-BARRON.

FIRST USED BY BARCLAYS BANK IN 1967.

First ATM in India was set-up in 1987 by HSBC in Mumbai.

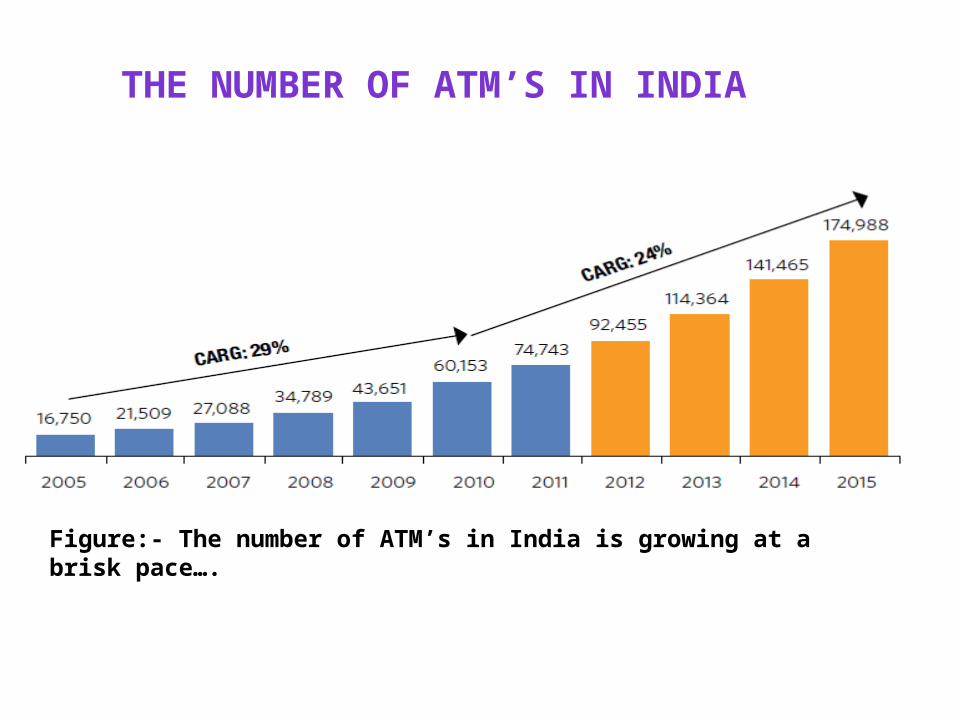

Figure:- The number of ATM’s in India is growing at a brisk pace….

THE NUMBER OF ATM’S IN INDIA

POS TERMINAL (POINT OF SALE)

POS is the place where a retail transaction is completed.

It is the point at which a customer makes a payment to the merchant in exchange for goods or services.

The merchant will also normally issue a receipt for the transaction.

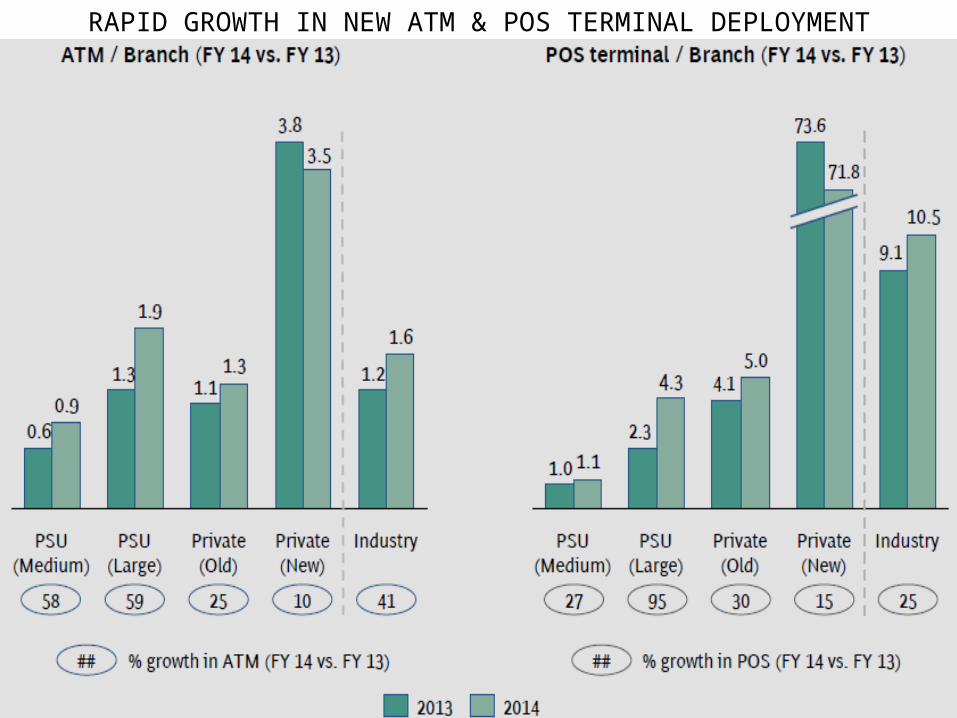

RAPID GROWTH IN NEW ATM & POS TERMINAL DEPLOYMENT

Online banking is an electronic payment system. It enables customers to conduct financial transactions on a website operated by the banks.

Online banking is also referred as Internet banking, e-banking, virtual banking.

INTERNET BANKING

MOBILE BANKING

Mobile banking allows customers to conduct a financial transactions through a mobile device such as a mobile phone or tablet.

The earliest mobile banking services were offered over SMS, a service known as SMS banking.

The Mobile Banking was introduced in 1999.

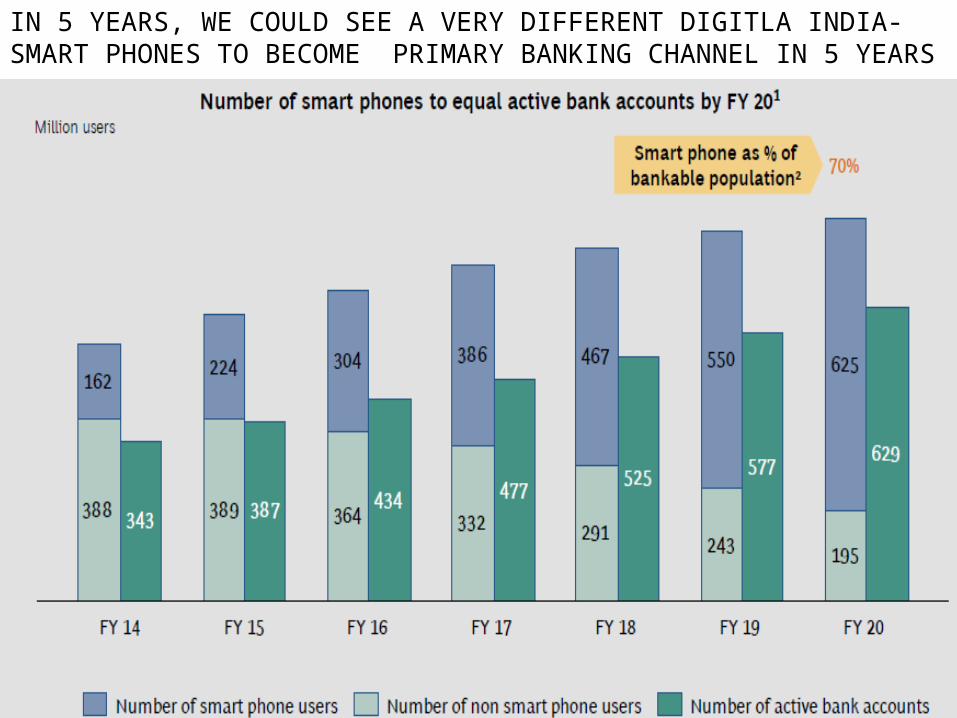

IN 5 YEARS, WE COULD SEE A VERY DIFFERENT DIGITLA INDIA- SMART PHONES TO BECOME PRIMARY BANKING CHANNEL IN 5 YEARS

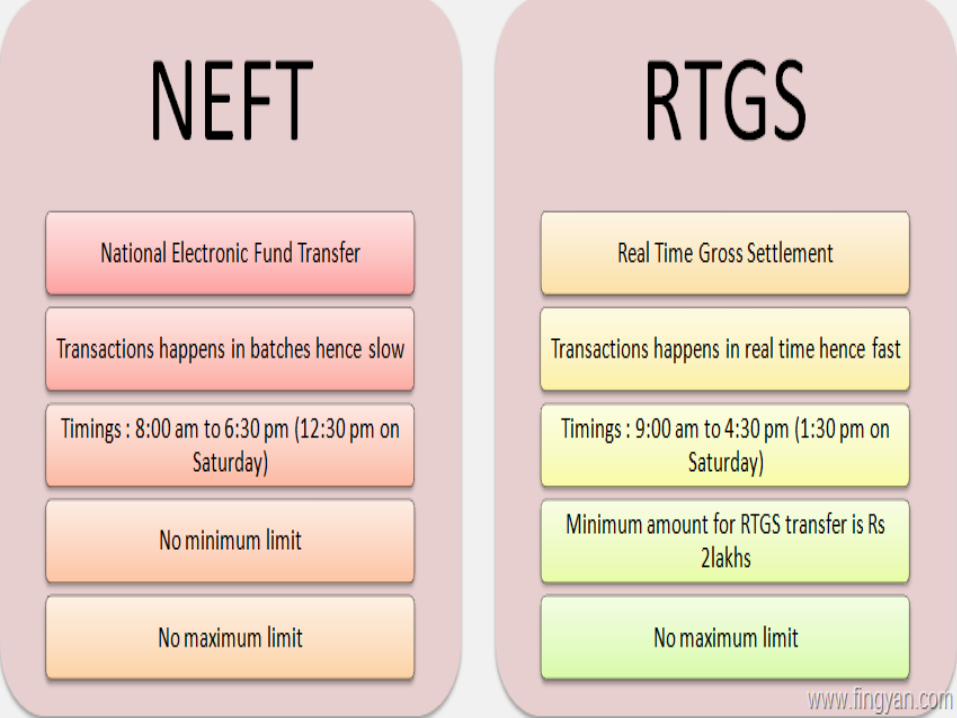

It is one of the most prominent electronic funds transfer systems of India, Started in November 2005.

NEFT is a facility provided by the bank to enable customers to transfer funds easily and securely on a one-to-one basis.

This is a "net" transfer facility which is executed in hourly batches resulting in a time lag.

NEFT(NATIONAL ELECTRONIC FUND

TRANSFER)

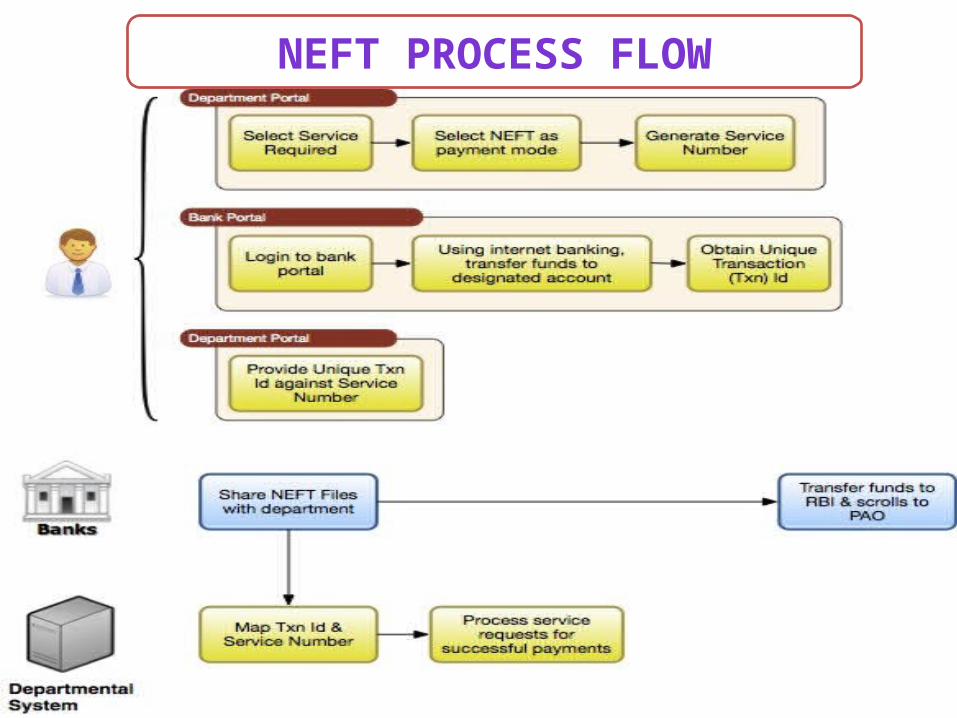

NEFT PROCESS FLOW

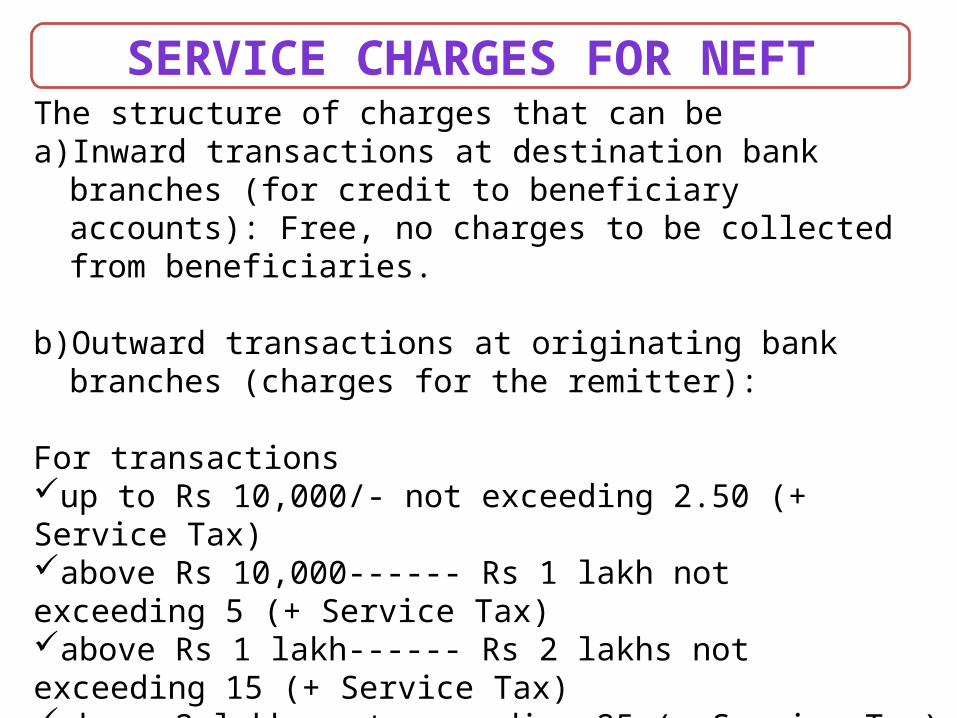

SERVICE CHARGES FOR NEFTThe structure of charges that can bea) Inward transactions at destination bank branches (for

credit to beneficiary accounts): Free, no charges to be collected from beneficiaries.

b)Outward transactions at originating bank branches (charges for the remitter):

For transactionsup to Rs 10,000/- not exceeding 2.50 (+ Service Tax)above Rs 10,000------ Rs 1 lakh not exceeding 5 (+ Service Tax)above Rs 1 lakh------ Rs 2 lakhs not exceeding 15 (+ Service Tax)above 2 lakhs not exceeding 25 (+ Service Tax)

RTGSREAL TIME GROSS

SETTLEMENT Real time= continuous settlement.

Gross settlement= settlement of funds transfer instructions occurs individually.

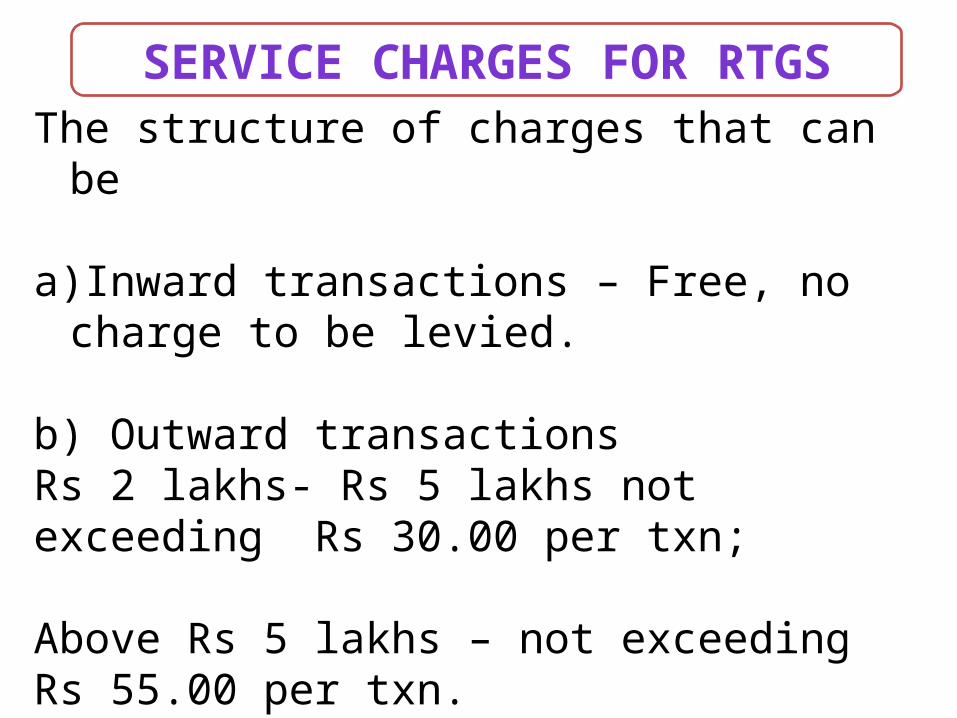

SERVICE CHARGES FOR RTGS

The structure of charges that can be

a)Inward transactions – Free, no charge to be levied.

b) Outward transactions Rs 2 lakhs- Rs 5 lakhs not exceeding Rs 30.00 per txn;

Above Rs 5 lakhs – not exceeding Rs 55.00 per txn.

ECS is an electronic mode of payment / receipt for transactions that are repetitive and periodic in nature.

ECS is used by institutions for making bulk payment of amounts towards distribution of dividend, interest, salary, pension, etc., or for bulk collection of amounts towards telephone, electricity, water dues, tax collections, loan installment repayments, periodic investments in mutual funds, insurance premium etc.

ECS facilitates bulk transfer of money from one bank account to many bank accounts or vice versa.

ECS (ELECTRONIC CLEARING SERVICE)

IMPORTANCE OF

DIFFERNET CHANNELS

OF BANKING

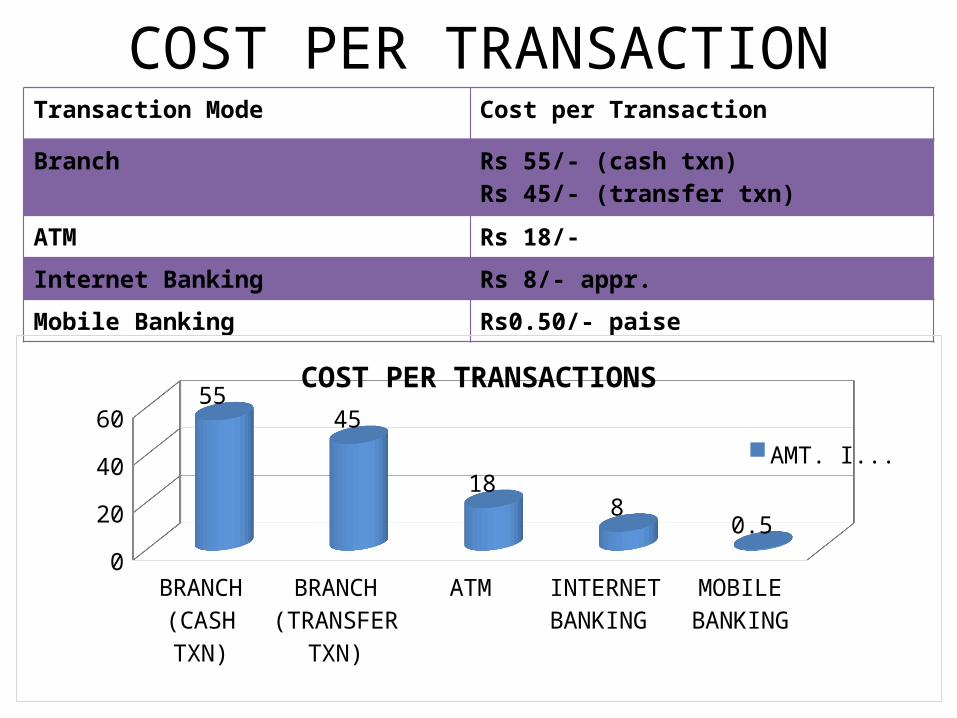

COST PER TRANSACTIONTransaction Mode Cost per Transaction

Branch Rs 55/- (cash txn)Rs 45/- (transfer txn)

ATM Rs 18/-

Internet Banking Rs 8/- appr.

Mobile Banking Rs0.50/- paise

BRANCH (CASH TXN)

BRANCH (TRANSFER

TXN)

ATM INTERNET BANKING

MOBILE BANKING

0

20

40

6055

45

188

0.5

COST PER TRANSACTIONS

AMT. IN RS.

IMPACT OF TECHNOLOGY

IN PRODUCTIVITY OF

BRANCH SALES

TECHNOLOGY CAN ALSO INCREASE PRODUCTIVITY OF BRANCH SALES

MASSIVE GROWTH IN DIGITAL TRANACTIONS FOLLOWED BY ATM/CDM-TOMORROW’S WINNERS IN DEPOSITS WILL NEED TO MASTER DIGITAL TRANSACTIONS

CASH RELATED AND CHEQUE TRANSACTIONS DOMINATE CASA- RAPID PHASE OUT CASH RELATED AND CHEQUE TRANSACTION WILL HASTEN DIGITAL REVOLUTION

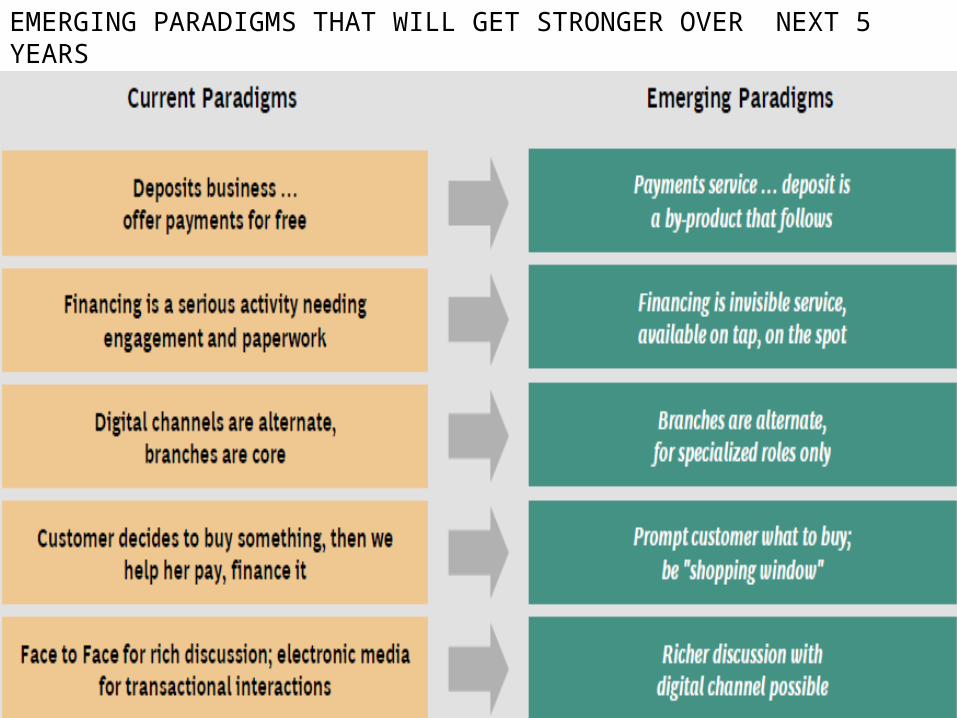

EMERGING PARADIGMS IN NEXT 5 YEARS

EMERGING PARADIGMS THAT WILL GET STRONGER OVER NEXT 5 YEARS

LOW ENGAGEMENT OF

CUSTOMERS ON

DIGITAL CHANNELS

75% RETAIL CUSTOMERS NOT USING CASH-LESS CHANNELS

LOW ENGAGEMENT AND ACTIVATION OF RETAIL CUSTOMERS ON DIGITAL CHANNELS

TRANSFORMATION OF BHARAT TO INDIA WITH THE HELP OF

DIFFERENT CHANNELS OF

BANKING

BHARAT VS. INDIA- SEMI URBAN/RURAL % GROWTH FASTER IN RETAIL/AGRI/MSME

MAKING THIS HAPPEN

WHAT WILL IT TAKE

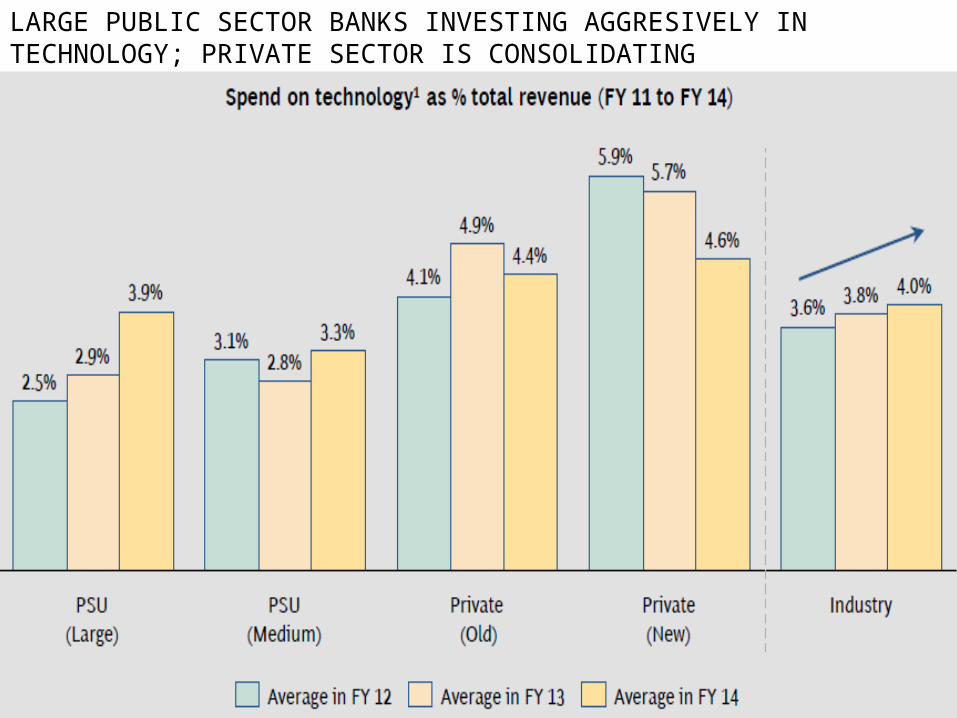

LARGE PUBLIC SECTOR BANKS INVESTING AGGRESIVELY IN TECHNOLOGY; PRIVATE SECTOR IS CONSOLIDATING