Embed Size (px)

Citation preview

Uncertainty:BusinessasUsualWilliston BasinPetroleum ConferenceDonHrapPresident, Lower48

2

Thefollowing presentation includes forward-looking statements. These statements relatetofuture events, such asanticipated revenues, earnings, business strategies,competitive position orother aspects ofouroperations, operating results ortheindustries ormarkets inwhichweoperate orparticipate ingeneral. Actual outcomesandresults maydiffer materially fromwhatisexpressed orforecast insuch forward-looking statements. These statements arenot guarantees offuture performanceandinvolve certain risks, uncertainties and assumptions thatmayprove tobeincorrect andaredifficult topredict such asoil andgasprices; operational hazards anddrilling risks; potential failure toachieve, and potential delays inachieving expected reserves orproduction levels fromexisting andfuture oil andgasdevelopmentprojects; unsuccessful exploratory activities; unexpected costincreases ortechnical difficulties inconstructing, maintaining ormodifying company facilities;international monetary conditions andexchange controls; potential liability forremedial actions under existing orfuture environmental regulations orfrompending orfuture litigation; limited access tocapital orsignificantly higher costofcapital related toilliquidity oruncertainty in thedomestic orinternational financial markets;general domestic andinternational economic andpolitical conditions, aswellaschanges intax,environmental andother laws applicable toConocoPhillips’ businessandother economic, business, competitive and/or regulatory factors affecting ConocoPhillips’ business generally assetforth in ConocoPhillips’ filings withtheSecurities andExchange Commission (SEC). Wecaution younottoplace undue reliance onourforward- looking statements, which areonly asofthedateofthispresentation orasotherwise indicated, andweexpressly disclaim anyresponsibility forupdating such information.

Useofnon-GAAP financial information – This presentation mayinclude non-GAAP financial measures, which help facilitate comparison ofcompany operatingperformance across periods andwith peercompanies. Anynon-GAAP measures included hereinwill beaccompanied byareconciliation tothenearest correspondingGAAPmeasure onourwebsite atwww.conocophillips.com/nongaap.

Cautionary NotetoU.S. Investors – TheSECpermits oil andgascompanies, intheir filings with theSEC, todisclose only proved, probable andpossible reserves. Weuse theterm"resource" inthis presentation thattheSEC’s guidelines prohibit us fromincluding infilings with theSEC.U.S. investors areurged toconsider closely theoil andgasdisclosures inour Form10-K andother reports and filings with theSEC. Copies areavailable from theSEC andfrom theConocoPhillips website.

CautionaryStatement

Topics

Marketsituation- historicalcontextandprospectsforrecovery

Industryresponsetothedownturn

Importanceoftechnologyandinnovation

Continuingtheenergyrenaissance

Thesupportiveroleofstates

3

MarketSituation

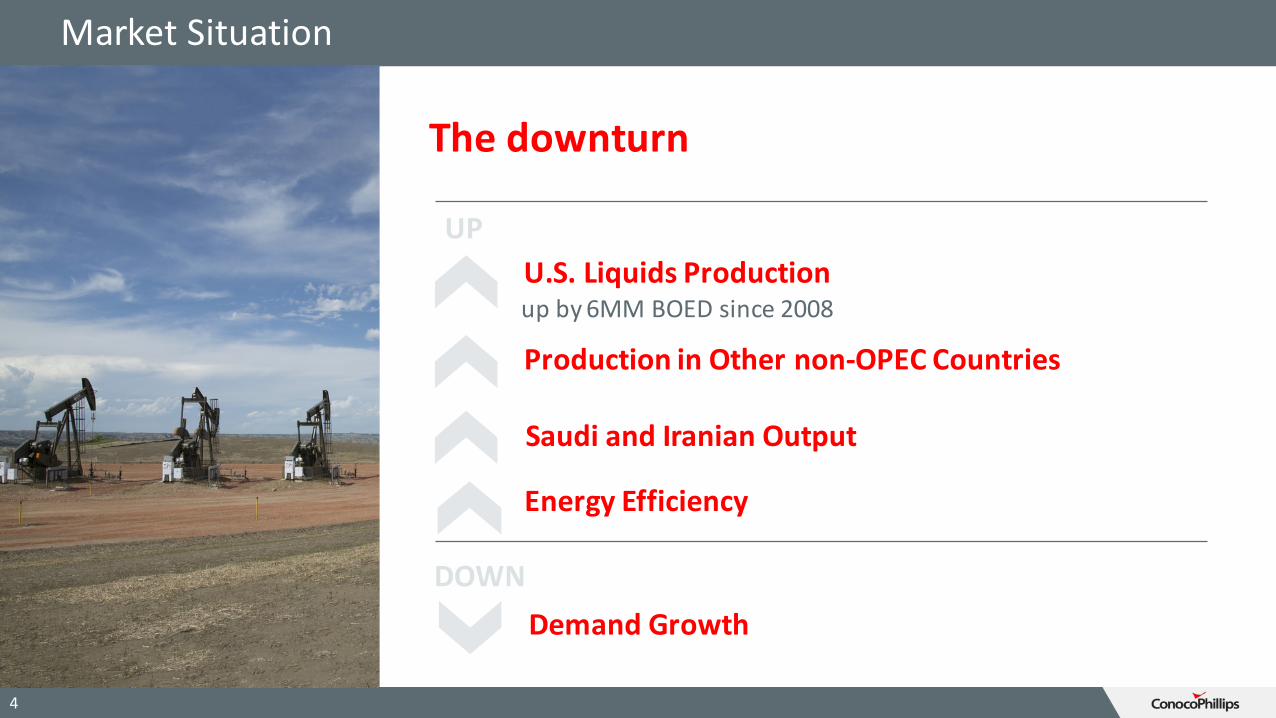

Thedownturn

4

DemandGrowth

EnergyEfficiency

U.S.LiquidsProductionupby6MMBOEDsince2008

UP

DOWN

SaudiandIranianOutput

ProductioninOthernon-OPECCountries

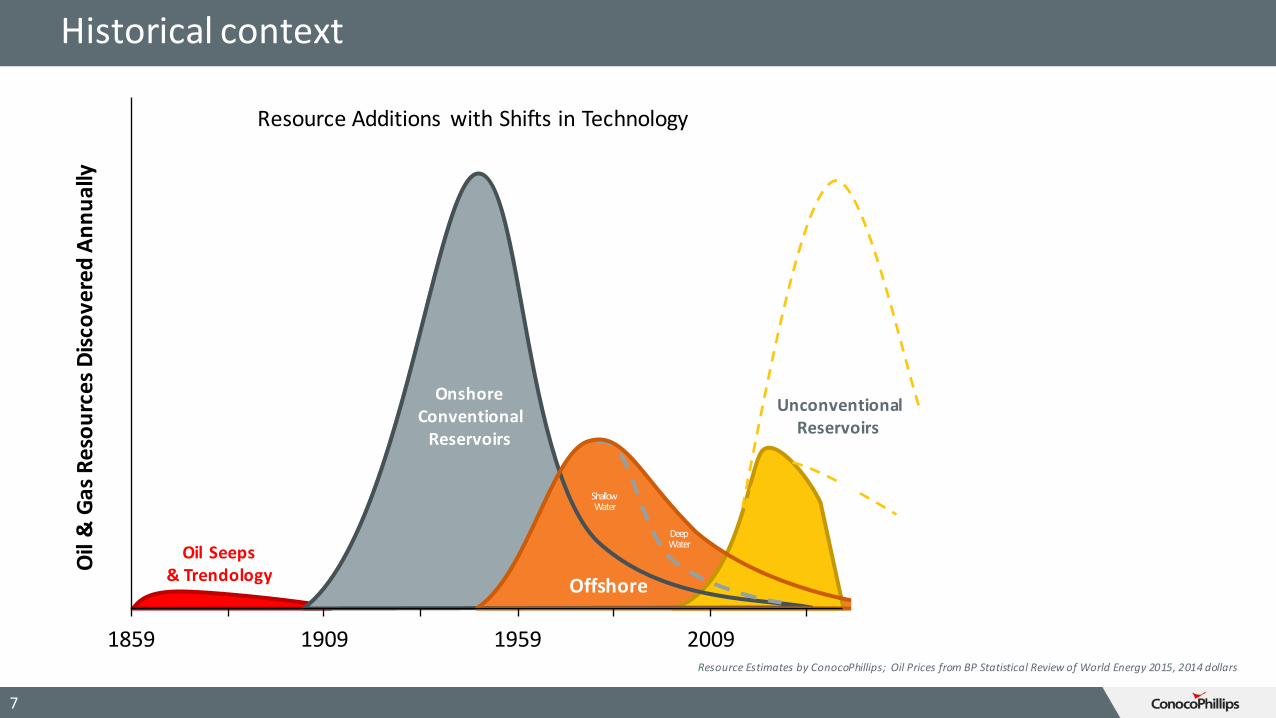

Historicalcontext

5

0

20

40

60

80

100

120

140

1859 1909 1959 2009

OilPrice(2014$pe

rbarrel)

Crudeoilpricesin2014dollarssince1859

Source:Oilpricesfrom2015BPStatisticalReviewofWorldEnergy

6

DatafromBakerHughes

Year-Over-Year Percent Change in U.S. Rig Count

Historicalcontext

ResourceEstimatesbyConocoPhillips;OilPricesfromBPStatisticalReviewofWorldEnergy2015,2014dollars

Oil Seeps&Trendology

OnshoreConventionalReservoirs

DeepWater

ShallowWater

1859 1909 1959 2009

UnconventionalReservoirs

Oil&GasResou

rcesDisc

overed

Ann

ually

Offshore

ResourceAdditions withShiftsinTechnology

7

Historicalcontext

Oil Seeps&Trendology

OnshoreConventionalReservoirs

Offshore

DeepWater

ShallowWater

Oil&GasResou

rcesDisc

overed

Ann

ually

0

20

40

60

80

100

120

140

1859 1909 1959 2009

OilPrice($perbarrel)

ResourcesD

iscoveredAn

nually

UnconventionalReservoirs

High

Low

Geologicshortage

IncreasedCompetition

AutomobileDemand

IranianRevolution

Limitedaccess+Chinademand

GlobalFinacialCrisis

GlobalCommodity PricesPricesin1800setequalto100

Drivers:1.TechnologyAdvances/ProductivityImprovements2.ResourceAbundance

ResourceEstimatesbyConocoPhillips;OilPricesfromBPStatisticalReviewofWorldEnergy2015,2014dollars;CommodityPricesdatafromBMO CapitalMarketsEconomicResearch.Graphexcerptedfrom“PlayingtoWin”byLafleyandMartin

8

Historicalcontext

9

ResponsetoLowerforLongerPriceEnvironment

Reducecosts

Reducespending

Greaterefficiency

Focusonbestresources

ThePossibleUpturn

10

MarketStrengthens• Lowpricesstimulatedemand• Productioncurtailedbycapitalcuts

AlternativeScenarios

MarketStrengthensFaster• Geopolitical supplydisruption

• OPECproduction decline

Lowerfor(even)Longer• Weakerdemandgrowth

• Moreproduction (Iran/Iraq)

• Inventoriesdecline• PricesStrengthen

11

FiveCharacteristicsforSuccess

Diverseportfoliowithlowcostofsupply

Baseoflow-declineproducingproperties

Flexibleshort-cyclecapitalprojects

Strongbalancesheet

Continuousimprovementwithflawlessexecution

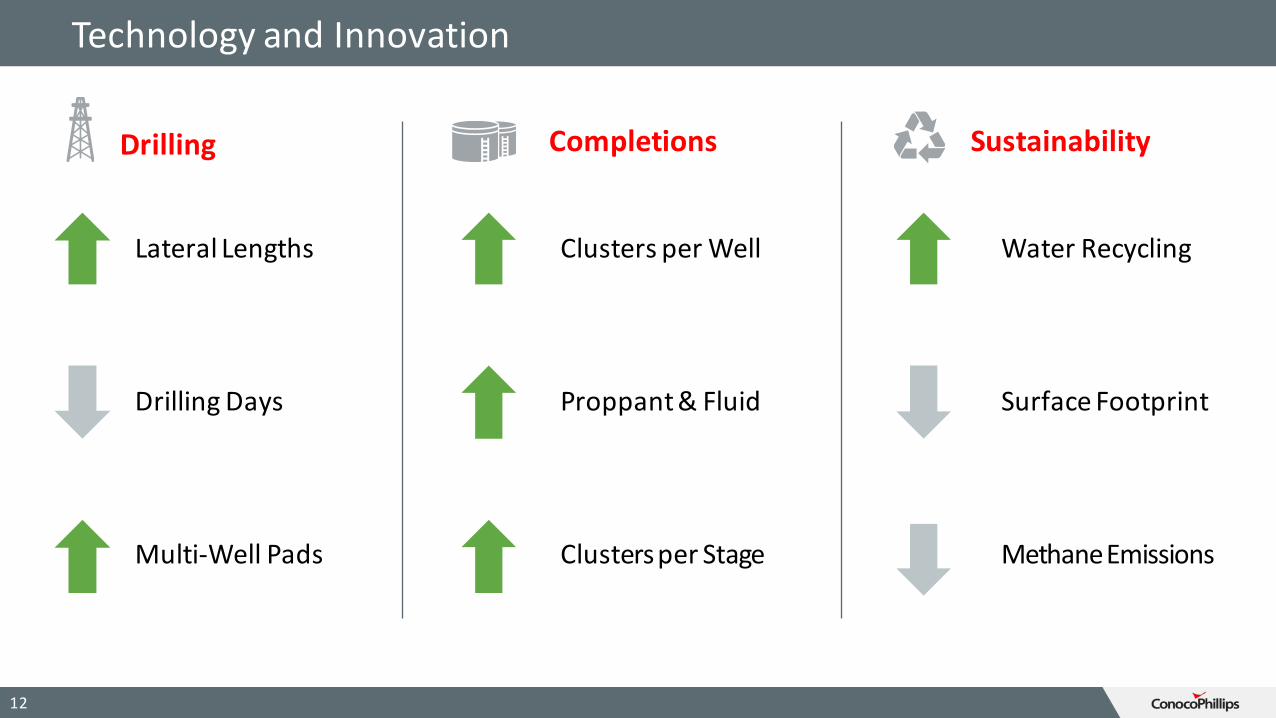

TechnologyandInnovation

12

LateralLengths

DrillingDays

Multi-WellPads

Drilling Completions

ClustersperWell

Proppant&Fluid

ClustersperStage

Sustainability

WaterRecycling

SurfaceFootprint

MethaneEmissions

13

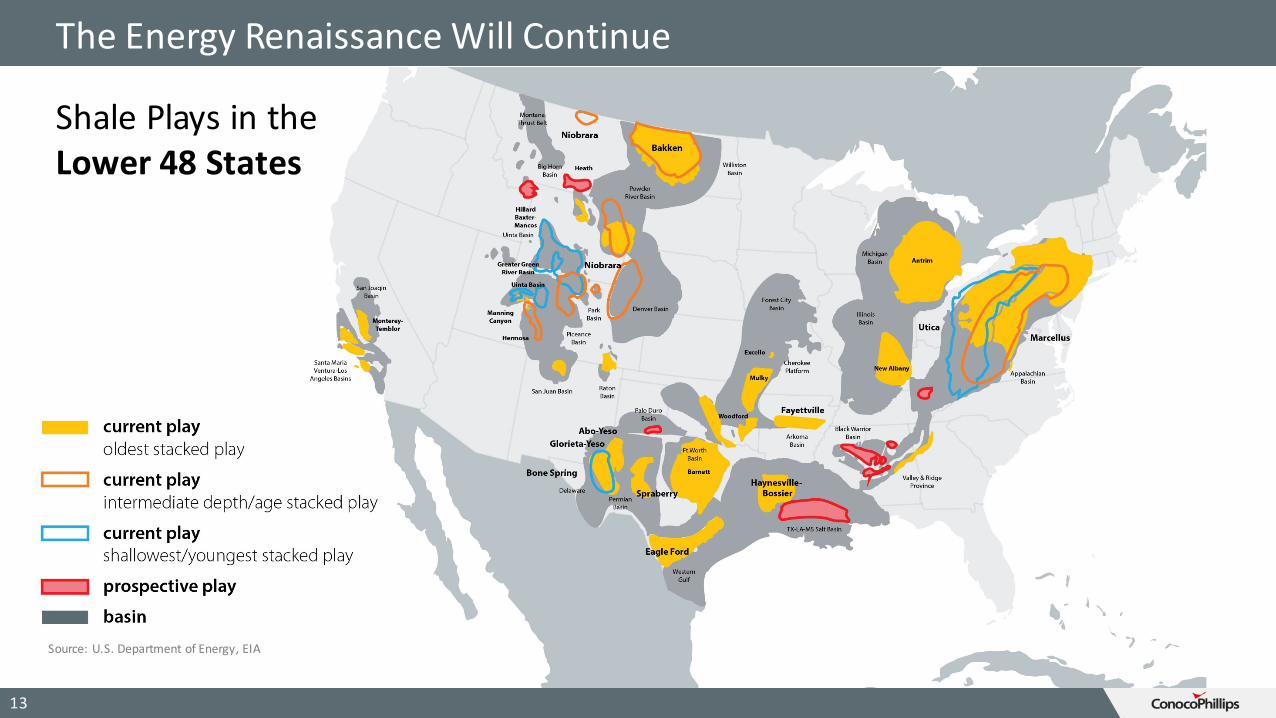

TheEnergyRenaissanceWillContinue

Source:U.S.DepartmentofEnergy,EIA

ShalePlaysintheLower48States

14

BenefitsoftheEnergyRenaissance

EnergyScarcitytoAbundance

AffordableEnergyPrices

JobCreation9.8millionjobs

Environmental

HighlyRegulatedIndustryatLocal,State&FederalLevels

U.S.OnshoreOilandNaturalGasRegulations

15

StateRole• Designfitforpurposeregulation• Ongoingconsultationwith

industry• Soundcostbenefitanalysis• Pragmaticimplementationdesign

IndustryRole• Leveragetechnology• Lowercostandimprove

efficiency• Improveenvironmental

performance

16

Summary

Downturnhashithard

Fundamentalssupportarecovery

U.S.resourcepotentialremainsstrong

Technologyandinnovationareincreasinglyimportant

Statescanhelpfosterpragmaticregulation