Embed Size (px)

Citation preview

Todd Creeger

President Australia-West

SEAAOC, 20 August 2014

Leveraging our LNG advantage

in a global market

Cautionary Statement The following presentation includes forward-looking statements. These statements relate to future events, such as anticipated revenues, earnings, business strategies, competitive position or other aspects of our operations or operating results or the industries or markets in which we operate or participate in general. Actual outcomes and results may differ materially from what is expressed or forecast in such forward-looking statements. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that may prove to be incorrect and are difficult to predict such as oil and gas prices; operational hazards and drilling risks; potential failure to achieve, and potential delays in achieving expected reserves or production levels from existing and future oil and gas development projects; unsuccessful exploratory activities; unexpected cost increases or technical difficulties in constructing, maintaining or modifying company facilities; international monetary conditions and exchange controls; potential liability for remedial actions under existing or future environmental regulations or from pending or future litigation; limited access to capital or significantly higher cost of capital related to illiquidity or uncertainty in the domestic or international financial markets; general domestic and international economic and political conditions, as well as changes in tax, environmental and other laws applicable to ConocoPhillips’ business and other economic, business, competitive and/or regulatory factors affecting ConocoPhillips’ business generally as set forth in ConocoPhillips’ filings with the Securities and Exchange Commission (SEC). We caution you not to place undue reliance on our forward-looking statements, which are only as of the date of this presentation or as otherwise indicated, and we expressly disclaim any responsibility for updating such information. Use of non-GAAP financial information – This presentation may include non-GAAP financial measures, which help facilitate comparison of company operating performance across periods and with peer companies. Any non-GAAP measures included herein will be accompanied by a reconciliation to the nearest corresponding GAAP measure in an appendix. Cautionary Note to U.S. Investors – The SEC permits oil and gas companies, in their filings with the SEC, to disclose only proved, probable and possible reserves. We use the term "resource" in this presentation that the SEC’s guidelines prohibit us from including in filings with the SEC. U.S. investors are urged to consider closely the oil and gas disclosures in our Form 10-K and other reports and filings with the SEC. Copies are available from the SEC and from the ConocoPhillips website.

Project Overview

3

ConocoPhillips Australia & Timor-Leste Portfolio

4

Australia Pacific LNG

CSG to LNG project in Queensland

Constructing 2 x 4.5 MTPA trains, first LNG mid-2015

ConocoPhillips operator of downstream LNG facility on Curtis Island

5

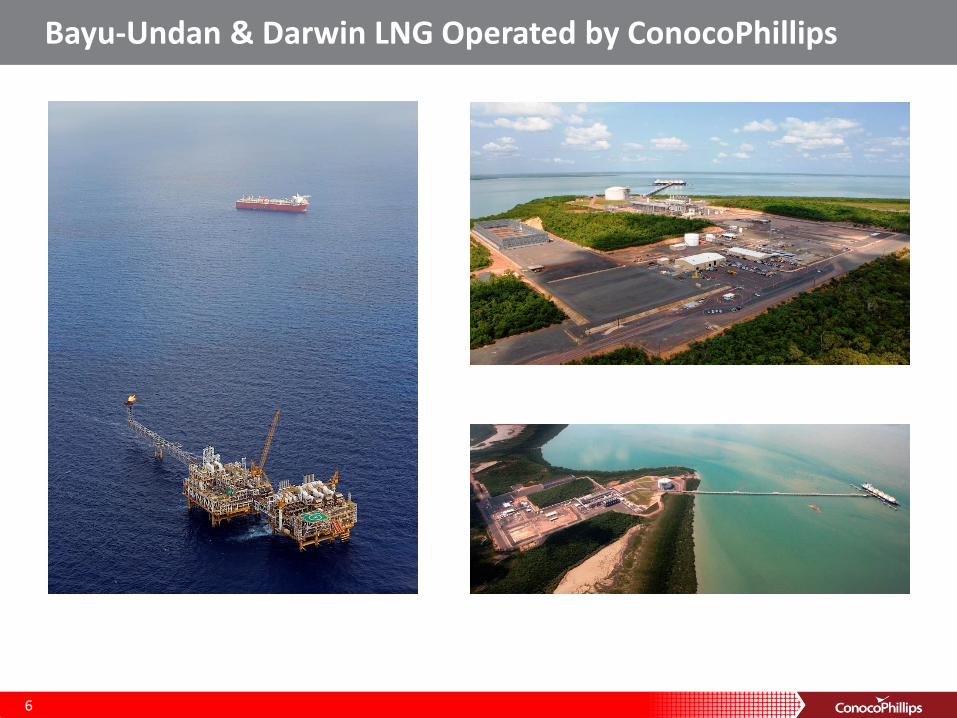

Bayu-Undan & Darwin LNG Operated by ConocoPhillips

6

ConocoPhillips Exploration & Appraisal Programs

Understanding reservoir & assessing commerciality

Greater Poseidon fields Exploration, Browse Basin

Ten wells since 2001

Caldita-Barossa fields Appraisal, Bonaparte Basin

Three wells 2014/15

7

Potential Development Options

Offshore processing facilities and back-fill Darwin LNG

Floating LNG

Offshore processing facilities and expansion Darwin LNG

JV partners appraising/exploring across northern Australia

8

Setting the Scene

9

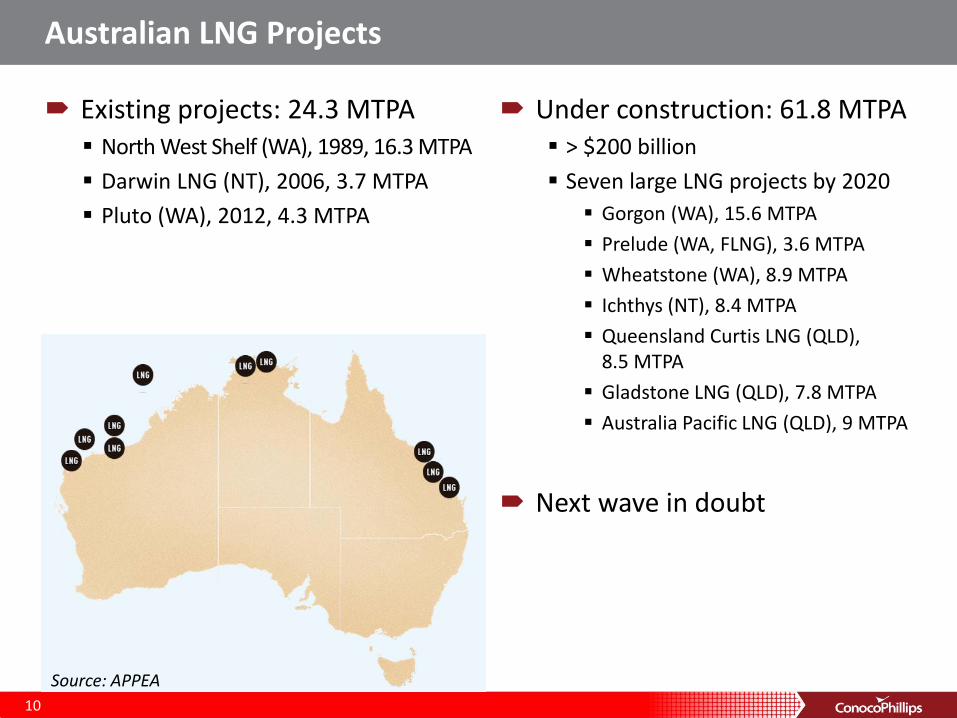

Australian LNG Projects

Existing projects: 24.3 MTPA North West Shelf (WA), 1989, 16.3 MTPA

Darwin LNG (NT), 2006, 3.7 MTPA

Pluto (WA), 2012, 4.3 MTPA

Under construction: 61.8 MTPA > $200 billion

Seven large LNG projects by 2020

Gorgon (WA), 15.6 MTPA

Prelude (WA, FLNG), 3.6 MTPA

Wheatstone (WA), 8.9 MTPA

Ichthys (NT), 8.4 MTPA

Queensland Curtis LNG (QLD), 8.5 MTPA

Gladstone LNG (QLD), 7.8 MTPA

Australia Pacific LNG (QLD), 9 MTPA

Next wave in doubt

10

Source: APPEA

Australia’s LNG Advantage

11

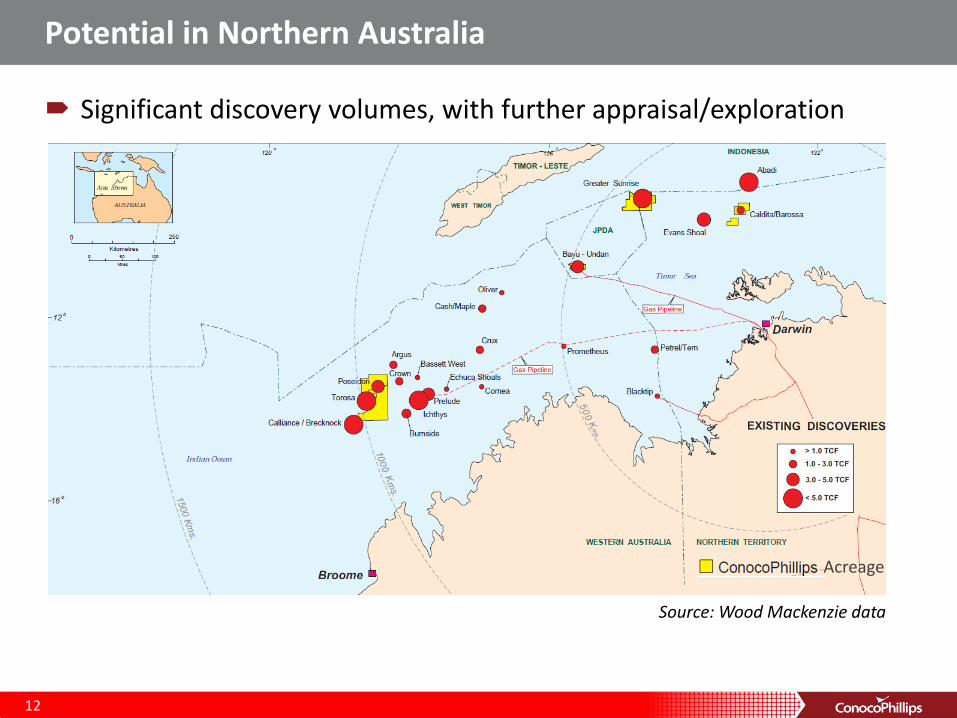

Potential in Northern Australia

Significant discovery volumes, with further appraisal/exploration

12

Source: Wood Mackenzie data

Acreage

Source: WA Department of Mines & Petroleum and EnergyQuest (July 2013) *Source: EIA World Shale Gas and Oil Resource Assessment 2013

Australia’s Advantage

Stable fiscal and regulatory regime

Close to LNG customers

Skilled and experienced workforce

Existing infrastructure

Abundant discovered and proved resources

13

Liquefaction Capacity v LNG Demand (Source: Wood Mackenzie 2014)

14

If probable, possible and speculative capacity is built, we may see potential LNG oversupply (affecting Australia)

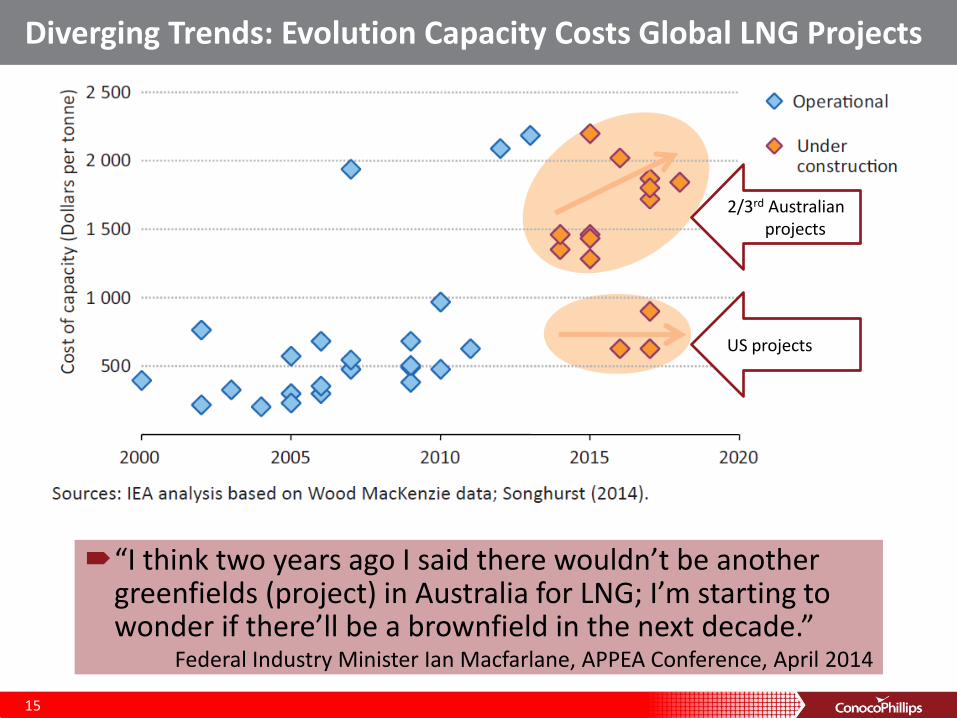

Diverging Trends: Evolution Capacity Costs Global LNG Projects

15

“I think two years ago I said there wouldn’t be another greenfields (project) in Australia for LNG; I’m starting to wonder if there’ll be a brownfield in the next decade.”

Federal Industry Minister Ian Macfarlane, APPEA Conference, April 2014

2/3rd Australian projects

US projects

Leveraging our Advantage

16

Brownfield Development

Use existing infrastructure to reduce capital costs

Leverage operations best practice e.g. experienced operator, skilled workforce, existing construction and operator relationships

17

ConocoPhillips Example of Brownfields Advantage

Darwin LNG Cost advantage of tying into

existing infrastructure

Permitted for 10 MTPA

Expansion land available

Australia Pacific LNG Cost advantage of tying into existing

infrastructure

Permitted for 18 MTPA

Land available for 2 additional trains

Leverage Operations Best Practice Strong relationships with train

construction companies

Experienced operator ConocoPhillips Optimized Cascade© Process

Regional Infrastructure

18

Technological Innovation

Complement not replace existing options

One Australian project committed: Shell Prelude Project

Preferred development option: Woodside Browse & Sunrise Projects

Opportunity to position Australia as a global FLNG hub Centre of excellence: operations, maintenance, supply chain and support

19

Potential Business Risk: External Influencers

Environmental groups/NGOs Ideologically oppose non-renewable energy sources

Influence policy setting by public opinion: NSW and VIC moratoriums

Case Study: Queensland Genuine community engagement

4,000+ signed access agreements

Peak petroleum industry body estimates economic benefits 30,000+ new jobs Private sector investment $60b+

20

Source: Ruth Alice White, via ClimateHoward

Resources Do Not Equal Development

Policy makers must think big Stable fiscal regimes attract global

investment

Cutting approval timelines

Sound regulation based on prudent scientific fact is vital

Remain open to innovative technology such as FLNG

Laws should promote investment

Domestic gas reservation policies deter investment

Support industry investment in training

21

Resources Do Not Equal Development

Industry must act responsibly Continuously improve safety and

environmental performance

Continuously improve technologies, processes and safeguards

Better inform & engage stakeholders

Commit to local content that builds capacity & economic participation

Collaborative training approach Commitment to an industry-wide

skills training and development

Work together to increase skill pool including diversity

22

Summary

Australia has delivered world class LNG projects

Australia’s advantage Close to LNG customers

Existing infrastructure

Highly experienced workforce

Abundant resources

Challenged to remain cost competitive in a global marketplace

Addressing challenges Brownfield developments

Innovative technology – FLNG

Investment decisions need certainty Stable fiscal settings

Sound regulatory policy

Industry must remain committed to transparency and sustainability

23

Follow ConocoPhillips at:

Conventional Gas Resources, Proven Basins & Infrastructure

25

Source: Geoscience Australia, 2014 Australian Energy Resource Assessment (Second Edition)

Analysis suggests that multiple LNG supply sources could be competitive into Asian markets

“I think two years ago I said there wouldn’t be another greenfields (project) in Australia for LNG; I’m starting to wonder if there’ll be a brownfield in the next decade.”

Federal Industry Minister Ian Macfarlane, APPEA Conference, April 2014.

Delivered Cost of LNG to Japan

26

Source: Wood Mackenzie, LNG Tool H1 ’14