Embed Size (px)

Citation preview

CONTENTS

July 2015 Volume 25 No. 7

Page

Thailand Realigns for the Future with IHQ/ITC/SEZ 1

News Bites / BOI Net Applications 2

Industry Focus: Thai Market is Large and Growing Fast 4

The Automotive Summit 6

The 2015 IMD World Competitiveness Scorecard 8

Business Strategy in the Era of ASEAN Economic Community 8

Company Interview: Graeter Pharma 9

Global Prime Office Occupancy Costs 10

BOI’s Missions and Events 11

Thailand Economy-At-A-Glance 12 Continued on P. 3

Thailand Realigns forthe Future with IHQ/ITC/SEZ

In recent years investors have noticed an increase in wage labor in Thailand and the shift of government policies towards attracting more modern industries; industries that are both environmentally sustainable and which support the drive to become an upper income country. While certain businesses, such as in the garment industry, have found neighboring countries to be more competitive and have opted to relocate labor intensive manufacturing facilities, it is true that Thailand still offers them an ideal location for investment in International Headquarters (IHQ) and International Trade Centers (ITC).

The new IHQ/ITC policy, adopted in the closing month of 2014, offers investors in all industries a means of employing the comparative advantages of the sub-region, capitalizing on the best each country has to offer. On 30 June 2015, the Board of Investment held a seminar entitled “Thailand: a Regional Trading and Modern Industry Hub” at the Centara Grand and Bangkok Convention Center at Central World, Bangkok. In his opening remarks to this event and keynote speech, Deputy Prime Minister M.R.Pridiyathorn outlined the evolution towards the IHQ/ITC policy, from the former Regional Operating Headquarters and International Procurement Office policy, and the expanded benefits and relaxed conditions that investors can now enjoy. He underlined the commitment of the new government to the IHQ/ITC policy, as well as the promotion of modern industries, all of which aim to make Thailand an upper income country.

NEWS BITES BOI NET APPLICATIONSThai Agricultural Products for Consumers Worldwide

The Ministry of Transport and the Ministry of Agriculture and Cooperatives on 15 June 2015 signed a memorandum of cooperation to promote Thai agricultural and processed products for consumers worldwide.

Under this cooperation, fresh fruit and vegetables, as well as processed products, from farmers’ organizations and community enterprises would be sent to Thai Airways International for food preparation for passengers. These farm products are certified for their high quality by the Ministry of Agriculture and Cooperatives.

Joint cooperation between the two agencies would promote the strength of Thai food and make Thai products better known among international consumers. Moreover, it would help empower farmers’ organizations and community enterprises, and they would have a new marketing channel. This will add value to the production of Thai fruit and vegetables, as well.

Thai fruit and vegetable exports bring in more than 10 billion baht per year, of which about eight billion baht comes from exports of frozen and dried fruit, while more than one billion baht comes from fresh and frozen vegetables.

U-Tapao to Be Developed as a Commercial Airport

U-Tapao – Rayong – Pattaya International Airport, commonly known as U-Tapao Airport, located in Ban Chang district, Rayong province, will be developed as a commercial airport. It is about 140 kilometers southeast of Bangkok and about a 45-minute drive from Pattaya.

The development project also involves the construction of an “airport link,” connecting Suvarnabhumi, Don Mueang, and U-Tapao with the city of Bangkok in order to cope with the growing air traffic in the future.

The development of U-Tapao Airport is divided into three phases. In the first phase, to be carried out from 2015 to 2017, a new passenger terminal will be constructed together with other facilities. With the new building and the existing passenger terminal, the airport will have the capacity to accommodate three million passengers a year.

National Budget for the 2016 Fiscal Year

The national budget for the 2016 fiscal year has been set at 2.720 trillion baht, representing an increase of 145 billion baht, or 5.6 percent, over that of 2015.

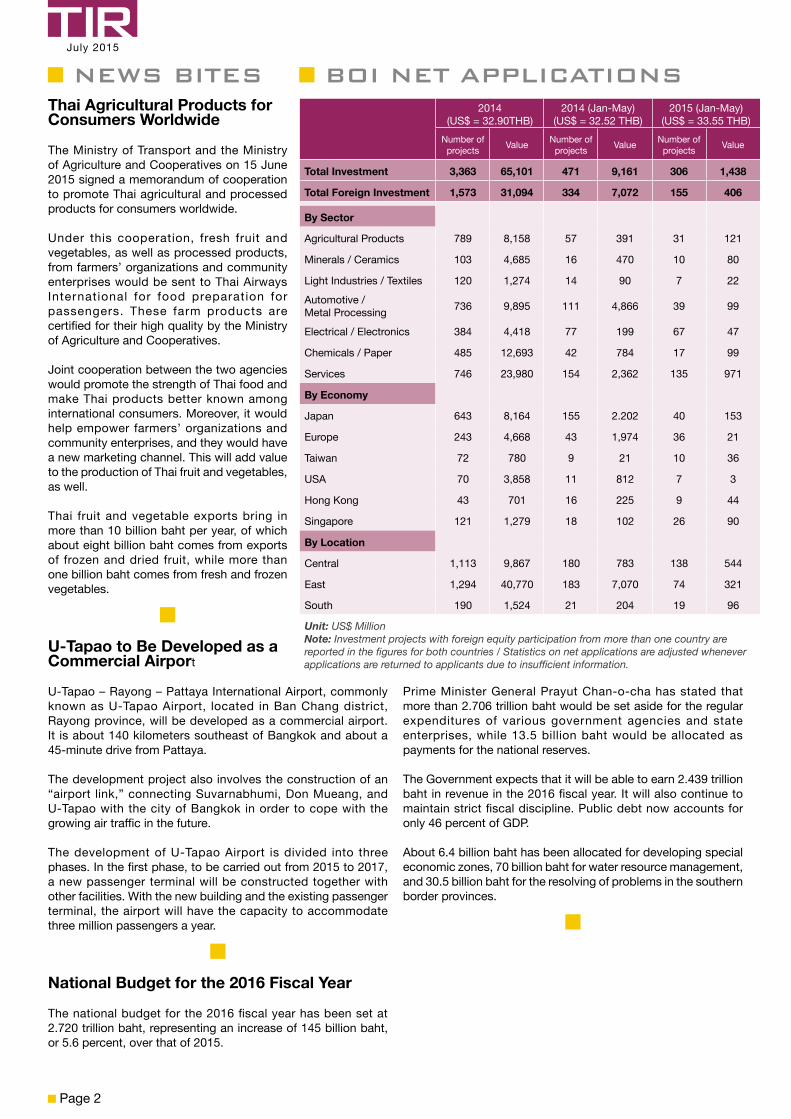

2014(US$ = 32.90THB)

2014 (Jan-May)(US$ = 32.52 THB)

2015 (Jan-May)(US$ = 33.55 THB)

Number of projects Value Number of

projects Value Number of projects Value

Total Investment 3,363 65,101 471 9,161 306 1,438

Total Foreign Investment 1,573 31,094 334 7,072 155 406

By Sector

Agricultural Products 789 8,158 57 391 31 121

Minerals / Ceramics 103 4,685 16 470 10 80

Light Industries / Textiles 120 1,274 14 90 7 22

Automotive / Metal Processing 736 9,895 111 4,866 39 99

Electrical / Electronics 384 4,418 77 199 67 47

Chemicals / Paper 485 12,693 42 784 17 99

Services 746 23,980 154 2,362 135 971

By Economy

Japan 643 8,164 155 2.202 40 153

Europe 243 4,668 43 1,974 36 21

Taiwan 72 780 9 21 10 36

USA 70 3,858 11 812 7 3

Hong Kong 43 701 16 225 9 44

Singapore 121 1,279 18 102 26 90

By Location

Central 1,113 9,867 180 783 138 544

East 1,294 40,770 183 7,070 74 321

South 190 1,524 21 204 19 96

Unit: US$ MillionNote: Investment projects with foreign equity participation from more than one country are reported in the figures for both countries / Statistics on net applications are adjusted whenever applications are returned to applicants due to insufficient information.

Prime Minister General Prayut Chan-o-cha has stated that more than 2.706 trillion baht would be set aside for the regular expenditures of various government agencies and state enterprises, while 13.5 billion baht would be allocated as payments for the national reserves.

The Government expects that it will be able to earn 2.439 trillion baht in revenue in the 2016 fiscal year. It will also continue to maintain strict fiscal discipline. Public debt now accounts for only 46 percent of GDP.

About 6.4 billion baht has been allocated for developing special economic zones, 70 billion baht for water resource management, and 30.5 billion baht for the resolving of problems in the southern border provinces.

July 2015

Page 2

Continued from P. 1

For one thing, companies that depend on low margin low wage manufacturing can maintain their HQ in Thailand, where Bangkok offers among the lowest cost prime office space in the region, the government offers IHQ/ITC incentives, and a host of other benefits, while shifting their manufacturing to countries with lower wages.

What then, specifically, constitutes an IHQ? It is a company incorporated under Thai law that provides management or technical services, f inancial management, or supporting services such as general management, business planning, and business coordination, procurement of raw materials and parts, research and development of products and other similar activities. It can also include treasury centers and international trading centers.

An investor locating in Thailand qualifies for both BOI and Revenue Department incentives, with each having the same definition of an IHQ. Investors can now get from the Revenue Department, among others, a corporate income tax exemption covering 15 accounting periods, inclusive of corporate income tax exemption for incomes received from overseas affiliated entities; royalties received from associated enterprises incorporated under foreign laws; dividends received from associated enterprises incorporated under foreign laws; capital gains received from the sales of shares in associated enterprises incorporated under foreign laws; income derived from the purchase and sales of goods overseas on the condition that such goods must not be imported into Thailand. In addition, companies are also offered reduced corporate income tax at 10 percent for incomes received from local affiliated entities; 15 percent personal income tax for expatriates; a specific business tax exemption for the gross receipts from lending to associated enterprises; final tax exemption on the interest income on loans to local and overseas affiliated entities, and a final tax exemption on dividends paid to foreign entities. Investors also have the choice to apply for incentives from the Revenue Department alone, BOI’s incentives, or they may apply for both.

It will be recalled that previously Thailand offered attractive benefits under its Regional Operating Headquarters promotion. But the IHQ offers additional expanded incentives, such as the expanded definition of an Associated Enterprise or the lower qualifications that accompany the IHQ promotion. For instance, to qualify for an IHQ a company must provide managerial, technical, supporting services to at least one offshore associated enterprise, not three as in the old plan. Also, under the new IHQ plan if a company fails to meet the qualifications in a given year it is only for that year that the incentive is lost.

An IHQ in Thailand and access to the region’s lower wage emerging economies offers investors the opportunity to capitalize on the best the AEC has to offer.

At the same time, the Thai government, in preparations leading up the AEC, is undertaking a significant investment in infrastructure that will strengthen connectivity and reduce logistics costs, while also putting in place a plan to promote Special Economic Zones along the border. Investments in one of these SEZs will receive maximum incentives and permission to use unskilled foreign labor.

As Deputy Prime Minister Pridiyathorn Devakula noted in his keynote address, if we think beyond our boundary and look to

the sub-region of ASEAN, plus southern China, we have a bigger production base and a greater variety of products. Trading companies can be established to trade in high quality products from Thailand to supply high income markets and lower quality products from newly emerging economies to feed low income countries.

Companies located in Thailand can easily import goods from a neighboring country and sell them to another by utilizing our infrastructure, particularly the road network. To boost this potential, the government has a grand plan to improve the rail network and facilitate cargo transportation

Thailand’s plan aims for 10 SEZs dotted along Thailand’s border with Myanmar, Laos, Cambodia and Malaysia. Already border trade currently accounts for 10 percent of the country’s total exports and is projected to grow by 20-25 percent in 2015.

13 target industries have been identified for the Special Economic Zones: agriculture and fisheries; ceramics; garments, textiles and leather; furnishings and furniture; gems and jewellery; medical equipment, automobiles and parts; electrical appliances and electronics; plastics; pharmaceuticals; logistics; industrial estates and tourism-related. Investments in these industries will qualify for maximum incentives from the BOI including an 8-year corporate income tax exemption, import duty exemption on machinery and raw materials, and an additional 50 per cent reduction on corporate income tax for 5 years. Other incentives include double deductions from the costs of transportation, electricity and water supply for 10 years; an additional 25 per cent cost deduction for installation or construction of facilities and other non-tax incentives.

Thailand is working to ensure that investors can tap into the full potential of the region, with Thailand as a manufacturing base for modern industries and other high-tech manufacturing, while moving less complex labor intensive manufacturing offshore with headquarters remaining in Thailand.

The IHQ/ITC scheme is a bold move to meet the needs of investors and to respond to the changing realities in the region, leaving Thailand well positioned to use its strengths and its geographic location, leaving Thailand still as the place to invest in Southeast Asia.

July 2015

Page 3

INDUSTRY FOCUS

Thai Market is Large and Growing FastAccording to the World Health Organization, the global pharmaceuticals market is worth US$300 billion a year, a figure expected to rise to US$400 billion within three years. The 10 largest drugs companies control over one-third of this market, several with sales of more than US$10 billion a year and profit margins of about 30%. Six are based in the United States and four in Europe.

Nonetheless, there is rapid growth in the market and research environment in emerging economies, leading to a gradual migration of economic and research activities from Europe to these fast-growing markets. Furthermore, Southeast Asia is a growing pharmaceutical market. The member states of ASEAN have taken initial steps towards seeking more harmonized regulation of their respective pharmaceutical and medical-device industries. With a population of more than 600 million, this market represents another rapidly growing emerging market. In general, the market has become more attractive in recent years as wages have risen and country governments have made healthcare sector growth a priority.

Looking at Thailand specifically, the market is dominated by generic drugss in terms of volume. The new medicines are coming up and showing good efficacy over the old generics, yet the country still needs to import a lot of products. There are two main international contract manufacturers – OLIC (owned by Fuji Pharma) and Zuellig Pharma – and multinationals engage in re-packing or contract manufacture through these two main companies. However, local manufacturers have been growing very fast for the last 5 years as they can produce drugs much cheaper and the market has started to shift in favor of any company that gives the lowest price.

The Thai market is large and growing fast, with the government remaining the biggest client for the industry. Previously, 60 % of the market share used to go to hospitals and 40% to the OTC (over-the-counter) or drugstore market. With the introduction of the 30-baht scheme, it appears that market distribution has shifted with 70% for hospitals and 30% for OTCs (drugstores).

In the past, contract manufacturing was not an area that interested local manufacturers due to the propriety of know how. Consequently, multinationals went directly to the two main international contract manufacturers in Thailand. Today, the situation is different and contract manufacturing is viewed as an enormous opportunity with the looming inauguration of the AEC and its attendant opening of the ASEAN market. It means much more investment will flow into Thailand as pharmaceutical companies can export throughout the ASEAN region. As a result, interest in contract manufacturing has been expressed not only by local pharmaceutical industry but also by multinationals that are re-considering their own investments in ASEAN. Opportunities are emerging, and the Board of Investment (BOI) now is making an effort to invite pharmaceutical companies to invest in Thailand.

Regarding the GMP standards, the local industry has learned and improved greatly in the last five years. The Thai FDA applied

for PIC/S membership so the entire local industry now has to comply with the PIC/S GMP. Moreover, the Thai Pharmaceutical Manufacturers Association conducts PIC/S GMP training sessions. Some 20 companies have entered the program and 10 of them has been approved by the Thai FDA. It is worth mentioning that in Thailand, the market is based on government tenders and with the newly implemented GMP standards; the products of local manufacturers are not different from those of the multinationals.

Thai products have been exported to neighboring countries for decades. The market share of Thai pharmaceuticals is being challenged more and more by emerging countries like Indonesia and Malaysia. On the other hand, the Thai pharmaceutical industry has been expanding every year when compared to neighboring countries. When considering the country’s strengths, Thailand is the best location for investment and its market is set to experience more growth with the implementation of GMP standards and ASEAN’s economic integration.

There are two main bodies of law applicable to drugs in Thailand. The first, the law of patents, relates to the intellectual property protection of new drugs, while the second body of law, principally codified in the Drug Act 1967 (BE 2510) and subsequent amendments, sets out a regulatory regime for the supervision of drug production, importation, sale and marketing of drugs in Thailand.

The sale of drugs and medicines in Thailand is supervised by FDA, which functions under the Ministry of Public Health. Part of the FDA’s mandate is to supervise pharmaceuticals in accordance with the Drug Act. In fact, the Drug Control Division of the Thai FDA has responsibility for drug licensing, inspection, registration and post-market surveillance, in line with the various rules and supplementary ministerial regulations promulgated to govern the FDA approval process. New drugs must be registered and approved before being sold on the open market. The Trade Secrets Act also comes into play when it involves the implementation of regulations that deal specifically with confidential clinical safety data that has been submitted to the FDA during the regulatory approval process.

Likewise, for new drug applications, the ASEAN Common Technical Requirements and Dossier are accepted. At present, licenses do not have an expiration date. What’s more, import and manufacturing licenses are valid for one calendar year and need to be renewed annually.

July 2015

Page 4

Continued on P. 6

Interestingly, Thailand has been part of the ASEAN Consultative Committee on Standards and Quality (ACCSQ) since1992. Then in 1999, the Pharmaceutical Product Working Group (PPWG) was formed as part of the ACCSQ. Regulatory harmonization is expected to benefit pharmaceutical companies that are looking to launch a new product in several countries simultaneously, as it reduces drug registration costs and approval times.

Since 1 January 2009, one of the main aims of the ACCSQ-PPWG has been to create a harmonized scheme among ASEAN member states to standardize and regulate the production and distribution of pharmaceuticals. The convergence of standards and regulations aims to ensure the free flow of cheap, quality, safe medicinal drugs in the region, through the reduction of trade barriers and an increase in cooperation between ASEAN members. The ASEAN Common Technical Dossier (ACTD) is another important legal instrument as it ensures the homogenization of quality, safety and efficacy of administrative data and product information for pharmaceuticals across the ASEAN region.

Worth mentioning, Thailand has a universal health insurance structure that provides at least basic care to all Thai citizens. This system is divided into three programs. The Civil Servant Medical Benefit Scheme gives approximately 7 million government workers excellent healthcare benefits. The Social Security Scheme covers about 10 million private sector workers and is based on an employer contribution system. Finally, the Universal Coverage Scheme provides free basic healthcare coverage to the remaining 50 million Thais.

As a percentage of total government expenditures, the Thai government spends 14% of the budget on healthcare, more than many developed European countries. In addition, hospitals purchase about 75% of all medicinal drugs fabricated and sold locally in Thailand, usually on the basis of generic tenders or negotiated contracts for brand name pharmaceuticals.

Without a doubt, Thailand’s pharmaceutical industry is one of the largest and most developed in Southeast Asia, with projections that it will have the eighth largest pharmaceutical market in the Asia Pacific region in 2016. The country’s unique universal medical scheme and its position as a hub of regional distribution have formed a highly attractive market. As the Thai population grows, urbanizes, becomes more affluent, ages and is increasingly sedentary, demand for better healthcare will increase. Equally significant, the Thai generic sector is growing, especially in the public sector, where the government has encouraged its use over patented drugs in order to cut costs. For instance, Greater Pharma has recently launched its first generic inhaler drug for the treatment of osteoporosis, making it the first company in Southeast Asia to manufacture successfully a generic version of this drug.

The number of Thai domestic drug companies has been growing quickly over the past decade. The government is now funding more R&D, encouraging the local drug industry to move up the value chain. In 2014, pharmaceutical exports were valued at 13.85 billion baht and were shipped primarily to other Southeast Asian countries like Vietnam, Cambodia, Philippines and Myanmar. The government, with the recent introduction of biotech parks and attractive tax incentives, also promotes biotechnology. Medical tourism is another priority for Thailand. The country’s almost 1,500 hospitals see more than 2.1 million foreign patients annually.

Although almost 80% of the drug companies operating in Thailand are local firms, imported pharmaceuticals make up a significant portion of the market by value. More than US$1.1 billion worth of drug products are imported each year. Actually, in 2014, Thailand imported 62.93 billion baht in pharmaceutical products. The major sources of these imports were companies based in Switzerland, United States, France, Germany, Spain, and India, which together accounted for about 44% of all imported drug sales. Prominent foreign pharmaceutical manufacturers and distributors operating in Thailand include Meji, Baxter,

Mega Lifesciences, Linaria, Otsuka, Sanofi, Pfizer, Merck, Novartis and GlaxoSmithKline.

Foreign pharmaceutical companies generally employ several large Thai contract manufacturers either to re-package their imported drugs or to produce locally. Industry experts agree there is room for growth for the Thai healthcare business when the AEC opens. Apart from hospital serv ices hav ing internat ional standards, Thailand is developing biopharmaceutical products and medical devices to reduce reliance on imports.

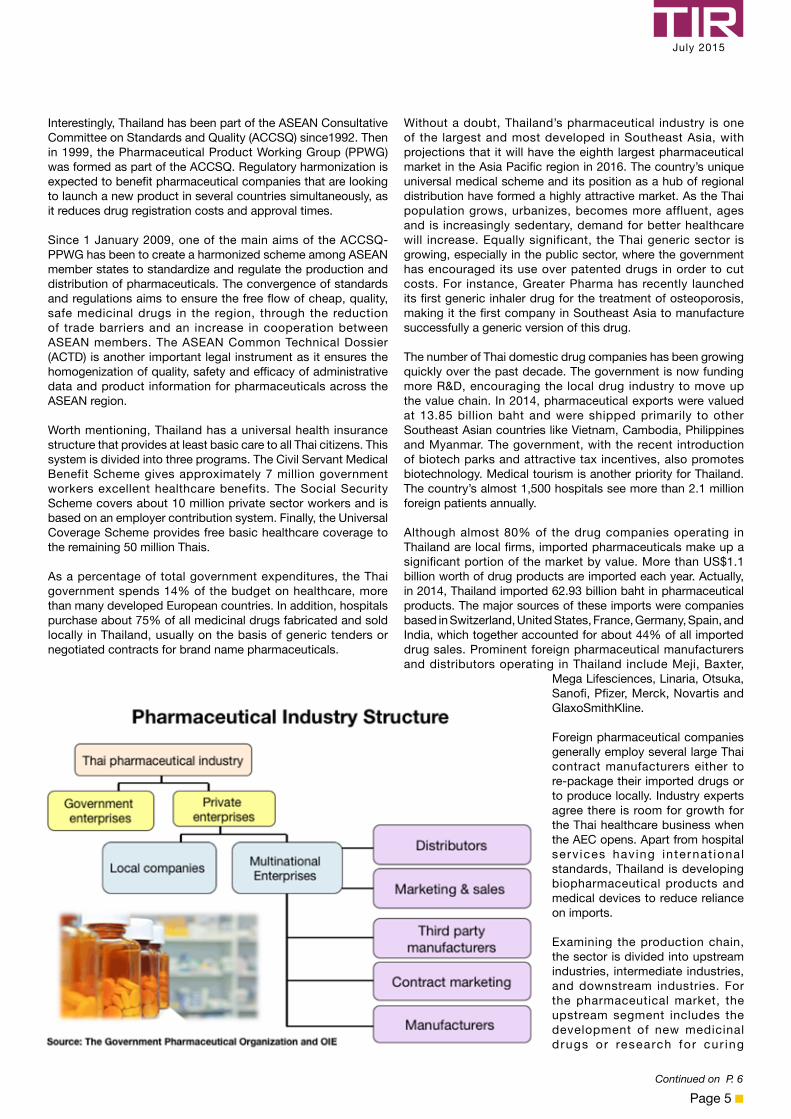

Examining the production chain, the sector is divided into upstream industries, intermediate industries, and downstream industries. For the pharmaceutical market, the upstream segment includes the development of new medicinal drugs or research for cur ing

July 2015

Page 5

Continued from P. 5

The Automotive Summit

The Automotive Summit is a major event for the automotive industry in ASEAN by delivering knowledge on testing technology and automotive and auto parts testing standards after the inauguration of the ASEAN Economic Community (AEC). Many leading auto parts manufacturers, operators, and engineers from around the world attended this event to exchange ideas and to network with government officials, company executives,

business leaders, and automakers. Furthermore, insights were provided on the performance of the ASEAN Consultative Committee for Standards and Quality (ACCSQ) and on progress made on the ASEAN Mutual Recognition Arrangement on Type Approval for Automotive Products (ASEAN AP MRA).

Under the theme of “ASEAN…The Emerging Automotive Hub of the World”, the Automotive Summit took place on 24-25 June 2015 at BITEC, as part of the “Automotive Manufacturing 2015” exhibition. The Thailand Automotive Institute and Reed Tradex organized the conference.

Motor vehicles are a technological invention that is related directly to the welfare and safety of both the driver and society in general. Accordingly, motor vehicles and automotive parts must be produced in a strictly measured manner thereby ensuring excellence throughout the entire manufacturing process. In this regard, automotive testing technology must develop along with testing standards, in order to conform with changes in the auto industry and consumer market.

In the past, national governments would create and implement automotive and auto parts testing standards with varying degrees of rigidity but with the same purpose: To control the quality of products that are imported and sold in their respective countries as well as to protect consumers. Nowadays, governments pursue development and prosperity through economic integration as

emerging illnesses. Meanwhile, the midstream segment includes production of active ingredients and requires the use of the latest technology and the input of substantial capital investment. This is done usually through a joint venture. Lastly, the downstream segment includes the production of finished medicines.

With a robust chemicals industry and great biodiversity to support pharmaceutical manufacturing, Thailand provides many benefits for foreign companies looking to fabricate or source their products in Thailand – including a skilled workforce, strong medical training, a friendly regulatory environment and a well-established infrastructure. Thailand has applied for membership in the Pharmaceutical Inspection Cooperation Scheme (PICS), so Good Manufacturing Practice (GMP) standards meet international benchmarks. The government also offers incentives like tax holidays and reduced import duties for equipment to foreign pharmaceutical investors.

To be specific, the new seven-year BOI investment promotion strategy (2015-2021) contains two industry-related activities. First, there is 6.9 – Active pharmaceutical ingredients (APIs) under Group A2. The condition for Activity 6.9 is that it must be for production of active or raw materials of APIs. Group A2 activities carry an eight-year CIT exemption with cap as well as an exemption of import duty on machinery/raw materials along with other non-tax incentives.

Second, there is 7.12.2 – R&D activity and/or manufacturing of biopharmaceutical agents using biotechnology under Group A1. The conditions for Activity 7.12.2 are that the projects must use modern biotechnology approved by the National Science and Technology Development Agency (NSTDA) or the Thailand Centre of Excellence for Life Sciences (TCELS). Furthermore, projects located in a science and technology park promoted by the BOI or one that is approved by the BOI will receive an additional 50% reduction in corporate income tax for five years after the end of its corporate tax exemption period. Group A1 activities carry an eight-year CIT exemption without cap as well as an exemption of import duty on machinery/raw materials along with other non-tax incentives.

As Thailand has developed into the medical hub of Asia, its pharmaceutical market also has experienced significant growth. Thailand’s cost-effective and high-quality manufacturing base has been a key driver in attracting foreign pharmaceutical companies. In recent years, the increasing numbers of medical tourists, an aging population, and high levels of health awareness among the Thai population have boosted the country’s pharmaceutical image. Plus, Thailand currently produces 25 active pharmaceutical ingredients, including sodium chloride, camphor, and menthol. Nevertheless, most active ingredients are imported from manufacturers overseas, leaving sizable room for new pharmaceutical investors.

July 2015

Page 6

clear targets and schedules for harmonization of standards and align national standards among ASEAN member states.

More relevant to the automotive industry in Southeast Asia, there is the ASEAN AP MRA. During the panel session, it was mentioned that the burgeoning trend of eco-car manufacturing possesses the potential to advance the growth and expansion of the entire enterprise in ASEAN. Nonetheless, for this sunrise sector to flourish, both in a supply and demand sense, product harmonization is critical and this outcome can be actualized through the acceptance of a compulsory MRA. To streamline economic integration, enhance overall productivity, and improve supply chain efficiency, additional testing must not take place after a product has passed the testing standards of one ASEAN

member and exported to another ASEAN market.

A mutual recognition arrangement (MRA) is a policy instrument that is designed to promote economic integration and increased trade between participants, particularly between countries. These goals are achieved by reducing regulatory impediments to the movement of goods and services. In fact, MRAs facilitate trade because they smooth the negotiation process between governments. Each country has its own rules, standards, and procedures. If trade is to flow freely between countries then agreement has to be reached on synchronizing the various national regulatory regimes. MRAs are the mechanism that is used to reach such an agreement.

Additionally, the panel discussants pointed out that the ASEAN automotive industry is geared towards customer satisfaction and ready to engage in more innovation. Still, government support at the national level, as demonstrated through market-friendly policies, is essential. For instance, the inclusion of “smart technologies” into automobiles has now become standard practice but the industry is exploring ways to expand this development. Such advances, however, require the involvement of the public sector – government – to create the most conducive business environment through the enactment of suitable laws that facilitate investment as well as upgrade the country’s human resource base.

Finally, raising ASEAN competitiveness is vital, so augmenting the marketing profile of the region, as a whole, must be put into action. ASEAN comprises a population greater than the European Union, a young and tech-savvy public, and a marketplace with plenty of room for growth, as motorization rates continue to remain low. Yet there are certain policy challenges that both ASEAN and individual national governments must confront and address, like concentration on labor-intensive manufacturing segments, and limited economies of scale and high cost bases.

the creation of a single large market increases competitiveness. With the imminent launch of the AEC, steps have been taken to review automotive and auto part testing standards of each member state in order to settle by mutual agreement their various regulatory differences and avoid unnecessary obstacles to future economic activity.

From the onset of the seminar, there was a focus on the importance of raising testing standards, inspection procedures, quality systems, and R&D investment. Such a region-wide approach would be beneficial to ASEAN members as it would stimulate modernization of the industry, improve human resource development, and foster market expansion. Likewise, during the presentations, a number of issues were highlighted. For instance, many parts of the world have formed regional communities and common markets, hence obligating firms to adapt to rapid technological changes in the industry and consumer trends. At the moment, there exists a demand for cars that are of higher performance and more fuel-efficient. With this in mind, the integration of Southeast Asia’s automotive industry, through the establishment of the AEC, will reduce manufacturing costs and spur innovation.

Speaker after speaker stressed that harmonization of standards – from national to regional and from regional to international – was essential for the success of the AEC. The audience was reminded that the key aspirations of the AEC revolve around it becoming a single market and production base, a highly competitive economic zone, a community of equitable economic development, and a region fully integrated into the global economy. Keep in mind that the AEC strives to further the free flow of goods, services, and investments as well as to boost the greater flow of capital and skilled labor within the regional grouping. However, these targets will not be achieved unless national laws that concern product standards and quality are not synchronized. Enter the ACCSQ. Its purpose is to set

July 2015

Page 7

The 2015 IMD World Competitiveness Scorecard

The 2015 IMD World Competitiveness Scorecard has been released with Thailand ranking 30th, of 61 economies covered. The most competitive this year is the United States and the least is reported to be Venezuela. Among the ASEAN countries included in the ranking, Thailand places 3rd, and ahead of several industrialized countries within the European Union. Thailand is reported to have improved in government efficiency, business efficiency and infrastructure.

In its press release issued on releasing the 2015 results, IMD notes that the ranking is “A question of business efficiency” with a commonality that among the best ranked countries “nine countries from the top 10 are also listed as top 10 of the business efficiency factor.”

IMD goes on to say that “Business efficiency focuses on the

extent to which the national environment encourages enterprises to perform in an innovative, profitable and responsible manner. It is assessed through indicators related to productivity such as the labor market, finance, management practices and the attitudes and values that characterize the business environment.”

TIR would like to note here that the new BOI policies that went into effect at the start of this year aim to achieve just that: performance in an innovative, profitable and responsible manner. Likewise, the new IHQ/ITC policy adopted by the government further streamlines Thailand’s capacity to become a trading hub within the forthcoming AEC.

With the appropriate government policies now in place and a government committed to improving the business environment, the future competitiveness of Thailand remains right.

Business Strategy in the Era of ASEAN Economic CommunityOn July 6, 2015, Nikkei Inc. and Thailand Board of Investment jointly hosted the Bangkok Nikkei Forum 2015: “Business Strategy in the era of ASEAN Economic Community Thailand, major manufacturing hub for Japan”. Prime Minister Prayut Chan-o-cha presided over the forum and mentioned that the ASEAN Economic Community (AEC) will lead to cooperation in various aspects. Business opportunities will widen and the Thai cabinet has given priority to strengthening the nation’s infrastructure, regulations and systems to support and facilitate business operations. Also, the government will proceed with the digital economy and promote Thailand to be an International Business Center to enhance the competitive capacity and strengthen the country. Recently, the cabinet made an announcement to promote Special Economic Zones (SEZs) along the border with neighboring countries. The Prime Minister expects that trade and investment between Thailand and its neighbors will become more robust due to the SEZ policy and with the transportation and logistics system plan, including road, rail, water, and air, which will increase the competitive capacity and reduce logistics costs from 2016 on.

BOI Secretary-General Mrs. Hirunya Sujinai also stated that SEZs policy will build new business opportunities for the Japanese

investors. With its strategic location, Japanese investors can easily access production inputs from various locations through the Greater Mekong Subregion Economic Corridors (GMS). She also mentioned that entrepreneurs who invest in Thailand are eligible for the highest BOI activity-based incentives, including an 8-year CIT exemption, and additional benefits for projects creating value added, or through merit-based Incentives such as research and development, product and packaging design, advanced technology training, development of local suppliers. Moreover, projects located in 20 provinces with lowest per capita income and projects located in industrial estates or promoted industrial zones are eligible for more privileges.

There were over 400 Japanese attendants at the forum, mostly senior executives. Presently, Japanese entrepreneurs in industries such as automotive, electronics and electrical appliances, finance, insurance, wholesale and retail trade are the major investors in Thailand and ASEAN.

Thailand, at the crossroads of the AEC, is prepared for the changing economic environment and continues to offer investors the place to invest.

July 2015

Page 8

Continued on P. 10

COMPANY INTERVIEW

Greater PharmaEstabl ished in 1967, Greater Pharma manufactures qual i ty pharmaceutical products and m a k e s a v a i l a b l e a f f o rd a b l e medicine to Thai consumers. Since then, it has evolved into one of Thailand’s premier pharmaceutical manufacturers with capabilities in drug research and development. The company is GMP compliant and also has been awarded ISO 9001 and ISO/IEC 17025 certification. It currently manufactures mostly generic pharmaceutical products and is moving into increasingly complex manufacturing processes.

The history of Greater Pharma Co., Ltd. spans back to 1932 with the founding of a modest grocery shop by Mr. Lieng Tengamnuay on Maharaj Road in the Tha Prachan area of Bangkok. It became a fully-fledged drugstore in 1956. Adapting to world market trends, Greater Pharma during the mid-1960s started to engage in the production of generic products as well as the repackaging of imported pharmaceutical products and medicinal consumer products.

Not long ago, the Thailand Investment Review newsletter team had the chance to visit Greater Pharma’s facility in Bangkok Noi and interview Mr. Chernporn Tengamnuay, managing director. A number of questions and topics were covered that provided an in-depth look into the operations and future plans of the company.

Greater Pharma is a pioneering Thai pharmaceutical business. According to Mr. Tengamnuay, the company’s overriding goal is to manufacture quality products at an affordable price for consumers in Thailand. Its strict quality standards and modern techniques and equipment ensure product safety and manufacturing efficiency. A leader in the production of pharmaceuticals, herbal food supplements and cosmetics, it was reported in August 2014 that Greater Pharma set up a joint venture with Laos-based Viengthong Pharma for the creation of an herbal products facility in Vientiane, Laos. Interestingly, the project receives grant funding from the Dutch government within the context of its Private Sector Investment program.

The company concentrates on the Thai market but also engages in exports, particularly in the ASEAN region. As Mr. Tengamnuay pointed out, imports comprise of 90% of the raw material for the production of pharmaceuticals. If raw materials were to be manufactured locally then costs could be reduced and productivity rates improved. For Mr. Tengamnuay, his aspiration for the company is to turn out a finished product that consists of 60-70% local content within a decade. Its product coverage encompasses allergy care, herbal/traditional products, OTCs (over-the-counter), pediatric consumer health, sports nutrition, vitamins and dietary supplements, and weight management.

Having received a BOI license for general herbal products and pharmaceuticals and biotechnology, Greater Pharma always is searching for new markets and opportunities to explore. To

illustrate the company’s reach and progress within the industry, Mr. Tengamnuay commented on cooperation with Siriraj Hospital in the development of an allergy vaccine (house dust mite). This is an example of technology transfer and this partnership has been ongoing for more than five years already. Yet the project required intensive investment and product marketing. Nonetheless, he indicated that such collaboration is necessary for Greater Pharma to remain ahead of the curve, as it is the first company in Thailand that applied and received a license for biopharmaceuticals. As a result, Greater Pharma must broaden its horizons regarding product research and development as well as product commercialization.

Mr. Tengamnuay remarked that the industry is growing with a consumer base that comprises ever more of an ageing population and the inclusion of not only the rural/urban poor but also the working class. Consequently, there is market expansion potential across ASEAN. In order to enhance the competitiveness of the company, Greater Pharma is pursuing joint research with institutes and universities on biopharmaceuticals, which he opines is the next level, particularly nanomedicine or the medical application of nanotechnology.

Besides the Siriraj Medical School of Mahidol University, other partners include the National Science and Technology Development Agency (NSTDA), National Innovation Agency (NIA), National Center for Genetic Engineering and Biotechnology (BIOTEC), National Nanotechnology Center (NANOTEC), and Thailand Institute of Scientific and Technological Research (TISTR). Greater Pharma also has membership in several associations such as the Thai Pharmaceutical Manufacturers Association (TPMA), Franco-Thai Chamber of Commerce (FTCC), Federation of Thai Industries (FTI), and the International Society of Pharmaceutical Engineering (ISPE).

“Greater Pharma’s key success factors are our continuous commitment and enthusiasm to transform the company into the lead Thai pharmaceutical manufacturer of high quality drugs and healthcare products”, declared Mr. Tengamnuay. He added that Greater Pharma aims to compete in the global market and looks to achieve this through the training of its people, adherence to international standards (e.g. PIC/S), and the acquisition of modern manufacturing techniques.

The Pharmaceutical Inspection Convention and Pharmaceutical Inspection Co-operation Scheme (jointly referred to as PIC/S) are two international instruments between countries and pharmaceutical inspection authorities that deal with the observance and enforcement of Good Manufacturing Practices.

Greater Pharma aims to invest heavily in the advancement of its current manufacturing capacity to facilitate the production of consumer goods in addition to its pharmaceutical products. This initiative is to prepare itself in response to the larger market size created by free trade agreements in Southeast Asia as the competitive landscape is predicted to become fierce. In addition, a considerable new online marketing campaign on Facebook will be developed to enhance its existing profile within the industry.

As the world changes, new technology is always introduced

July 2015

Page 9

Continued from P. 9

and developed, similarly so is the production process. Greater Pharma always implements new modern machinery and manufacturing technology. A team of highly qualified and well-experienced personnel staffs the facility, and quality is built-in into its products by design. Starting with vendor approval, analysis of raw materials, in-process checks and finished product analysis, the company’s stringent approach to quality ensures that its products meet international specifications. Greater Pharma manufactures almost all drug dosage forms, covering tablets, capsules, liquid orals, powders, creams and ointments. Separate sections have been established for the manufacture of penicillin groups, non-penicillin groups and steroids, to ensure against cross contamination.

Even though production for its own sales is the primary activity, Greater Pharma also manufactures licensed products for other international enterprises and this is testament to the high quality standard of drugs manufactured by the company.

Greater Pharma has a well-equipped Quality Control Laboratory for thorough testing of its products at all stages of manufacturing and the performing of stability studies to ensure quality during storage. Awarded a GMP Certificate by the Thai Food and Drug Administration, its modern manufacturing methods and strict quality control regime comply fully with WHO standards.

Turning to the topic of the company’s workforce, Mr. Tengamnuay stated that his team possesses the necessary skills and qualifications to compete in the market. With 600 employees, Greater Pharma always has been at the forefront of the local pharmaceutical industry. His staff revolves a core of pharmacists, engineers, chemists, and lab technicians. In order to keep up with the competition training courses, which meet the criteria set up by the ISO system, are provided to all personnel to upgrade their skills and knowledge. Universities, machine suppliers, and government agencies (e.g. TFDA) offer additional training sessions. More universities in Thailand have opened programs/majors in pharmacy. Still, the Thai university system overall requires further development with regards to the

technical aspect of the industry. “We can develop our human resources step-by-step and to meet the labor demands of the industry”. From labor-intensive to knowledge-intensive, the pharmaceutical industry obligates companies to become R&D-oriented.

When asked about the AEC, Mr. Tengamnuay was quick to reply, “ASEAN is our market already”. Thai pharmaceutical firms, in general, and Greater Pharma, specifically, adhere to the guidelines set forth by the ASEAN Consultative Committee on Standards and Quality as it deals with the same format of registration. Similarly, the Thai government has embraced the ASEAN standard. However, Mr. Tengamnuay mentioned that the BOI must support the local pharmaceutical industry. It is essential to attract MNCs to invest and establish themselves in Thailand as pharmaceuticals are a high technology product, a comprehensive, long-term strategy is required. Still, the launching of the AEC will result in increased competition and Greater Pharma will have to deal with the obstacles placed by regional protectionism. Nonetheless, the company’s relationship with the BOI is strong and goes back years, in fact, Greater Pharma has been a BOI-promoted company since 2006. With all the challenges evident on the horizon, the industry needs more BOI privileges to progress.

Greater Pharma has strived to establish itself as the leading healthcare provider in Thailand. Under the guidance of Mr. Tengamnuay, the company has played an important role in the development of both the Thai pharmaceutical and healthcare industries, with a product line that ranges from generic drugs, OTCs, functioning food supplements, to anti-aging products. It uses the latest manufacturing and laboratory testing technology, and it follows standard quality management systems such as ISO 9001:2008, GMP, and ISO/IEC 17025. Greater Pharma has continued to improve and develop its products to meet international standards in order to provide the best quality products at an affordable price both in Thailand and in the global marketplace.

Global Prime OfficeOccupancy Costs

CBRE has issued its report on the Global Prime Office Occupancy Costs, listing the top three most expensive locations being in London, Hong Kong and Beijing, in that order. In Asia, 12 of 31 locations listed in the report had an increase in costs of more than 1 percent.

According to CBRE, Bangkok is ranked 105 of 127 cities surveyed in the first quarter for overall occupancy costs for Grade A office space, with the average Grade A CBD rents in the city increasing by 3.2 percent year-over-year to THB 859 per sq.m. per month.

CBRE tracks occupancy costs for Grade A or prime office space in 127 markets around the globe. Of the top 50 ‘most expensive’ markets, Asia Pacific had the most number of markets featured, with 20 markets ranked.

July 2015

Page 10

BOI Secretary General Hirunya Suchinai gave a speech on “Business Strategy in the Era of ASEAN Economic Community (AEC) – Thailand, major manufacturing hub for Japan” at the “Seminar: Bangkok Nikkei Forum” which was held on 6 July 2015 at Conrad Hotel Bangkok.

Mr. Dean Matlack, Commercial Attaché at the U.S. Embassy (Bangkok) and Ms. Christine Brown, Director for Southeast Asia & Pacific Affairs, Office of the United States Trade Representative from Washington D.C. visited OSOS on 8 July 2015 to discuss with Ms. Ajarin Pattanapanchai, Senior Executive Investment Advisor of BOI, the investment promotion policy for International Headquarters (IHQ), International Trading Center (ITC) and Special Economic Zones (SEZs).

H.E. M.R. Pridiyathorn Devakula, Deputy Prime Minister of the Kingdom of Thailand and Mr. Gregory So, Secretary for Commerce and Economic Development of the Hong Kong Special Administrative Region, witnessed an MOU signing between BOI and Invest Hong Kong at the roadshow trip to Hong Kong during which BOI organized signing ceremony and a seminar on “Thailand: A Regional Trading and Modern Industry Hub”, 25 June 2015 at Shangri-la hotel.

H.E. M.R. Pridiyathorn Devakula, Deputy Prime Minister of the Kingdom of Thailand, presided over the opening ceremony for the expansion of OSOS services to cover information and consultation services for investors interested in investing in International Headquarters (IHQ), International Trading Centers (ITC), and in Special Economic Zones (SEZs), on 9 July 2015 at Chamchuri Square Building, Bangkok.

Mr. Jesada Sornsurk, Executive Director of Investment Development Assistance Bureau, together with Ms. Sonklin Ploymee, Director of BOI Unit for Industrial Linkages Development, and Mr. Salil Wisalswadi, BOI Tokyo Director, led a business delegation from 22 -28 June 2015 to the M-Tech Tokyo 2015 Exhibition. The mission included business matching with companies from Yokohama and Shimane in Automotive, Electronic & Electrical, and Machinery Industries.

BOI Executive Director of Regional Investment and Economic Centre, Eastern Region, Mr. Chanin Khaochan, together with Ms. Kanokporn Chotipal, BOI Mumbai Director, gave a presentation on “Investing in Thailand and using Thailand as a base for ASEAN business” to the BOI seminar conducted on 24 June 2015 at S.L. Kirloskar International Convention Centre Complex, Pune, during an investment promotion mission to India from 22-26 June 2015.

BOI’S MISSIONS AND EVENTS

July 2015

Page 11

THAILAND ECONOMY-AT-A-GLANCE

Source: Stock Exchange of Thailand

Source: Bank of ThailandSET Monthly Closing Values

International Reserves / Short-term Debt (%)

Exchange Rate Trends

Industrial Capacity Utilization (%)

Head Office, Office of the Board of Investment 555 Vibhavadi-Rangsit Road, Chatuchak, Bangkok 10900, ThailandTel: +66 (0) 2553 8111 Fax: +66 (0) 2553 8316 Website: www.boi.go.th E-mail: [email protected] Board of Investment, Beijing Office Royal Thai Embassy No.40 Guang Hua Road, Beijing, 100600, P.R.China Tel: (86-10) 6532-4510 Fax: (86-10) 6532-1620 E-mail: [email protected]

FRANKFURTThailand Board of Investment, Frankfurt OfficeBethmannstr. 58, 5.OG60311 Frankfurt am Main Federal Republic of Germany Tel: (49 69) 92 91 230Fax: (49 69) 92 91 2320E-mail: [email protected]

GUANGZHOUThailand Board of Investment, Guangzhou OfficeRoyal Thai Consulate-General GuangzhouNo.36 Youhe Road, Haizhu District, Guangzhou, P.R.C 510310 Tel: +8620 8385 8988 Ext. 220-225 +8620 8387 7770 (Direct Line)

Fax: +8620 8387 2700 E-mail: [email protected]

LOS ANGELES Thailand Board of Investment, Los Angeles Office Royal Thai Consulate-General 611 North Larchmont Boule-vard, 3rd Floor, Los Angeles, CA 90004 USA Tel: (1-323) 960 1199Fax: (1-323) 960 1190E-mail: [email protected]

MUMBAIThailand Board of Investment,Mumbai OfficeRoyal Thai Consulate-General,Express Tower, 12th Fl., Barrister Rajni Patel Marg, Nariman Point, Mumbai, Maharashtra 400021 Republic of India Tel: (9122) 2204 1589-90 Fax: (9122) 2282 1071E-mail: [email protected]

NEW YORKThailand Board of Investment, New York Office 7 World Trade Center, 34th Floor, Suite F, 250 Green-wich Street, New York, NY 10007Tel: (1-212) 422 9009Fax: (1-212) 422 9119E-mail: [email protected]

OSAKAThailand Board of Investment, Osaka Office Royal Thai Consulate-General, Osaka, Bangkok Bank Bldg. 7th Floor , 1-9-16 Kyutaro-Machi, Chuo-Ku, Osaka 541-0056 Japan Tel: (81-6) 6271-1395 Fax: (81-6) 6271-1394E-mail: [email protected]

PARISThailand Board of Investment, Paris Office Ambassade Royale de Thailande, 8, Rue Greuze75116 Paris, FranceTel: (33 1) 5690 2600 (33 1) 5690 2601Fax: (33 1) 5690 2602E-mail: [email protected]

SEOULThailand Board of Investment, Seoul Office#1804, 18th Floor, Koryo Daeyeongak Center,97 Toegye-ro, Jung-gu, Seoul, 100-706, Korea Tel: (822) 319-9998 Fax: (822) 319-9997E-mail: [email protected]

SHANGHAIThailand Board of Investment, Shanghai OfficeRoyal Thai Consulate-General15 F., Crystal Century Tower, 567 Weihai Road, Shanghai, 200041, P.R.China Tel: (86-21) 6288-9728, (86-21) 6288-9729 Fax: (86-21) 6288-9730E-mail: [email protected]

STOCKHOLMThailand Board of Investment, Stockholm OfficeStureplan 4C 4th Floor 114 35 Stockholm, Sweden Tel: +46 (0)8 463 1158 +46 (0)8 463 1172 +46 (0)8 463 1174 to 75 Fax: +46 (0)8 463 1160 E-mail: [email protected]

SYDNEYThailand Board of Investment, Sydney Office 234 George Street, Sydney, Suite 101, Level 1,New South Wales 2000, Australia Tel: +61-2-9252-4884 Fax: +61-2-9252-4882E-mail: [email protected]

TAIPEIThailand Board of Investment, Taipei Office Taipei World Trade Center 3rd Floor, Room 3E39-40, No.5, Xin-Yi Road, Sec.5Taipei 110, Taiwan, R.O.C. Tel: (886) 2-23456663Fax: (886) 2-23459223 E-mail: [email protected]

TOKYOThailand Board of Investment, Tokyo Office Royal Thai Embassy8th Fl., Fukuda Building West,2-11-3 Akasaka, Minato-ku, Tokyo 107-0052 JapanTel: (81 3) 3582 1806Fax: (81 3) 3589 5176E-mail: [email protected]

Facts about ThailandPopulation (2014) 65 millionASEAN Population 625 millionLiteracy Rate 96%Minimum Wage 300 Baht/day

GDP (2014) US$ 404.8 billionGDP per Capita (2014) US$ 6,041.1 GDP Growth (2014) 0.9%GDP Growth (2015, projected) 3.0-4.0 %Export Growth (2014) -0.3%Export Growth (2015, projected) 0.2%

Trade Balance (2014) US$ 24.6 billionCurrent Account Balance (2014) US$ 13.1 billionInternational Reserves (2014) US$ 157.1 billionCapacity Utilization (2014) 60.48%Manufacturing Production Index (2014) 168.2Core Inflation (2015, projected) 1.59Headline Inflation (2015, projected) 1.89Consumer Price Index (June 2015) 106.64 (2011=100)

Corporate Income Tax 10-20%Withholding Tax 0-15%Value Added Tax 7%

June Average Exchange RatesUS$1 = 33.73 baht€1 = 37.86 baht£1 = 52.52 baht100 ¥ = 27.28 bahtCNY1 = 5.44 baht

Top 10 Exports 2015 (Jan-May)

Product Share Value (US$ bn)

1 Motor cars, parts and accessories 11.74 10.42

2 Automatic data processing machines and parts thereof

8.17 7.25

3 Precious stones and jewellery 5.04 4.47

4 Polymers of ethylene, propylene, etc in primary forms

3.89 3.45

5 Refine fuels 3.64 3.23

6 Rubber products 3.40 3.01

7 Electronic integrated circuits 3.34 2.96

8 Chemical products 3.21 2.84

9 Machinery and parts thereof 3.13 2.78

10 Iron and steel and their products 2.54 2.25

Total 88.69Source: Ministry of Commerce

Source: Bank of Thailand

Source: Bank of Thailand BOI

July 2015

Page 12

![Investment Opportunities in Thailand - boi.go.thEdited] PPT for SG 120917_EN as of... · Investment Opportunities in Thailand Mrs. Hirunya Suchinai Secretary General Thailand Board](https://img.dokumen.tips/doc/110x75/5a79235d7f8b9a00168da346/investment-opportunities-in-thailand-boigoth-edited-ppt-for-sg-120917en-as.jpg)