Embed Size (px)

Citation preview

Funding, equity, valuations

http://startupmba.foundercentric.com

[email protected] foundercentric.com @foundercentric !Mailing list: http://bit.ly/fc-list

Part I Types of funding

3 ways to fund a company

1.Revenue 2.Debt 3.Equity

Revenue

Get paid by your customers

Even if it’s not the long-term plan, it puts you in a stronger position for eventual fund-raising

You don’t depend on anyone else’s approval to build your business

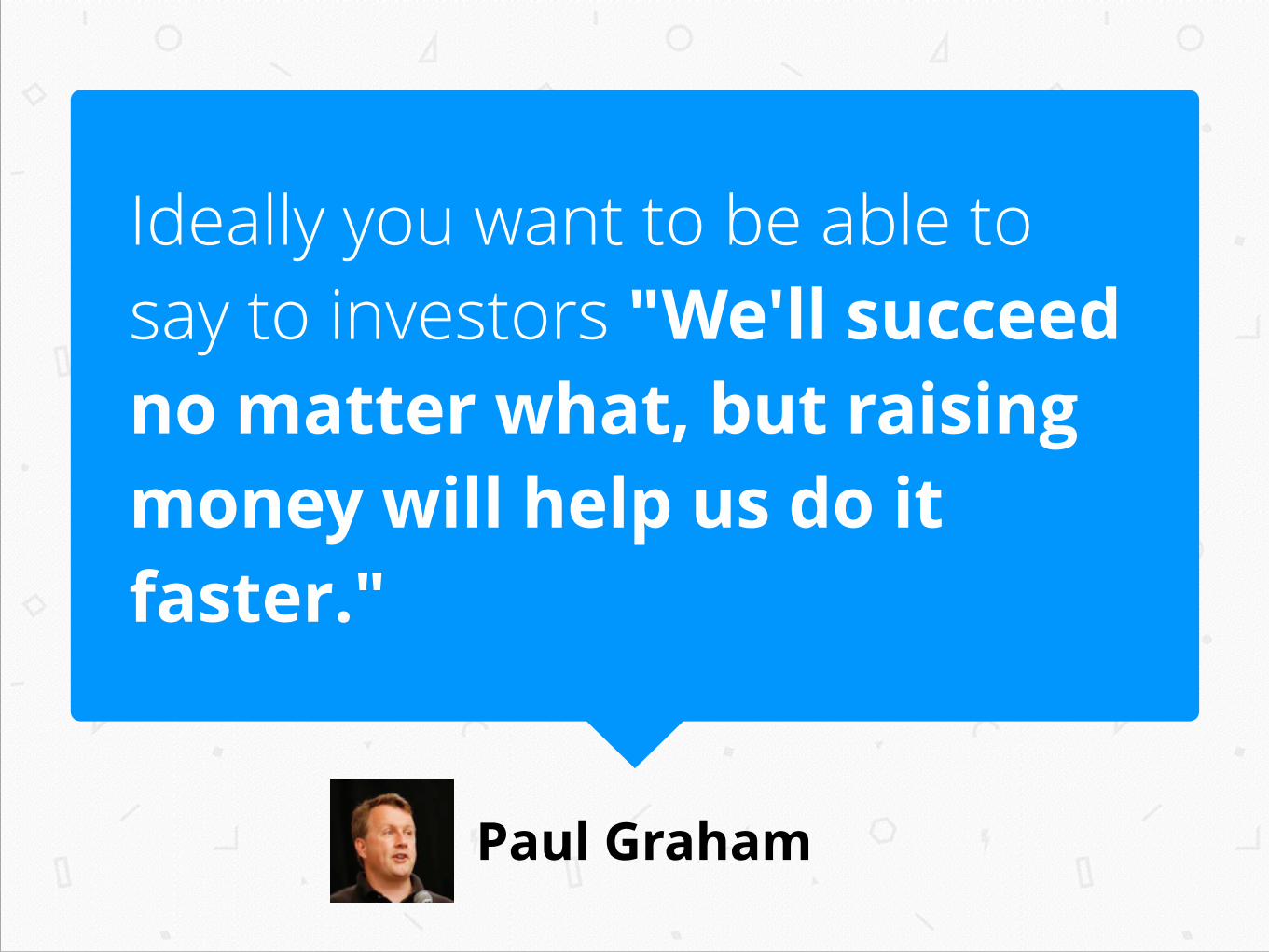

Paul Graham

Ideally you want to be able to say to investors "We'll succeed no matter what, but raising money will help us do it faster."

Debt

Borrow money and promise to pay it back with interest

If the company fails, you’re usually personally liable

Almost always a bad fit (and dangerous) for startups which deal with uncertainty

Equity

Sell a % of your company for cash

If the company fails, you owe nothing

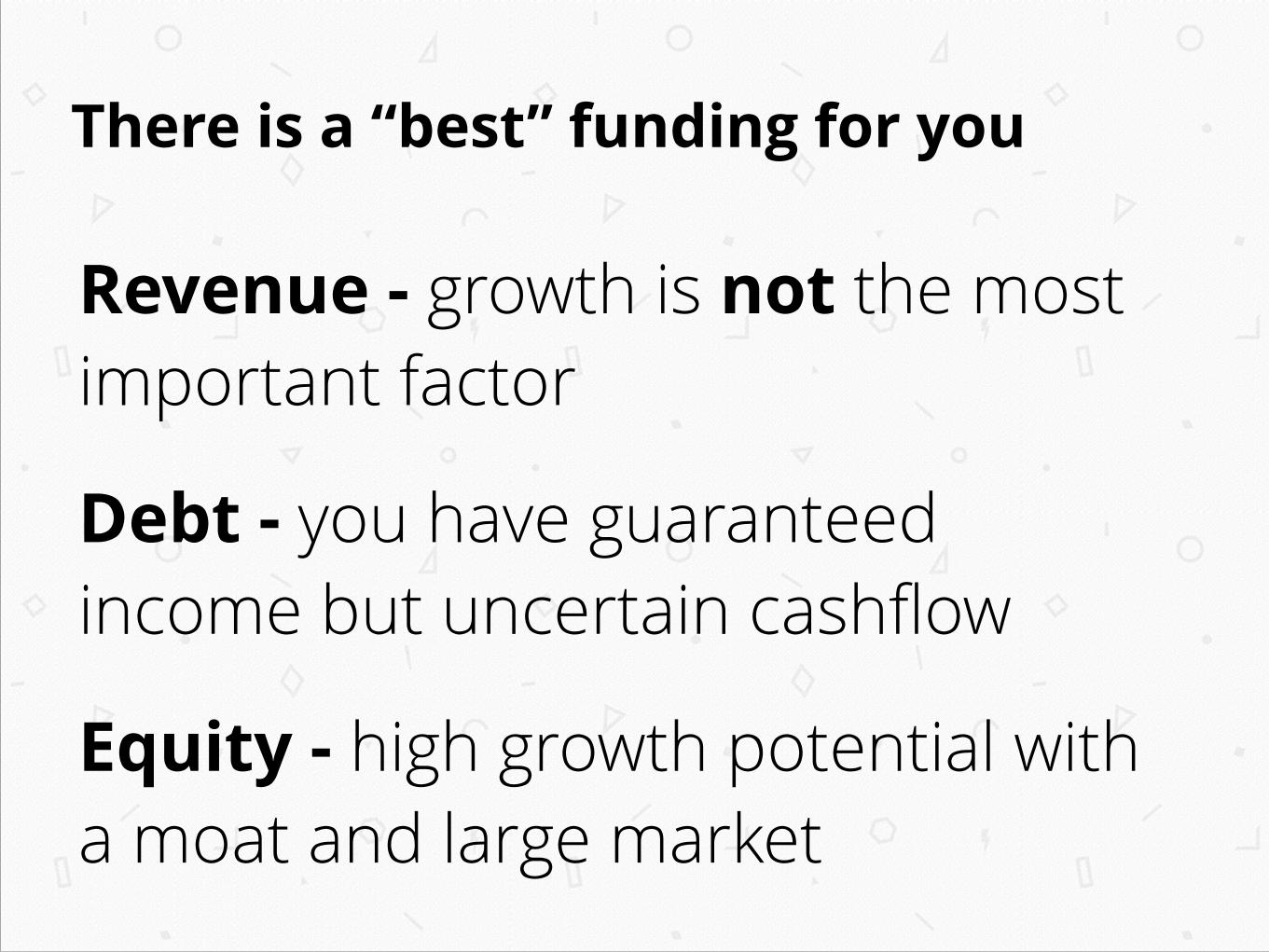

There is a “best” funding for you

Revenue - growth is not the most important factor

Debt - you have guaranteed income but uncertain cashflow

Equity - high growth potential with a moat and large market

Question

Which is best for your business? Revenue, debt, or equity?

We’re mostly talking about

equity funding

We’re mainly talking about

equity funding

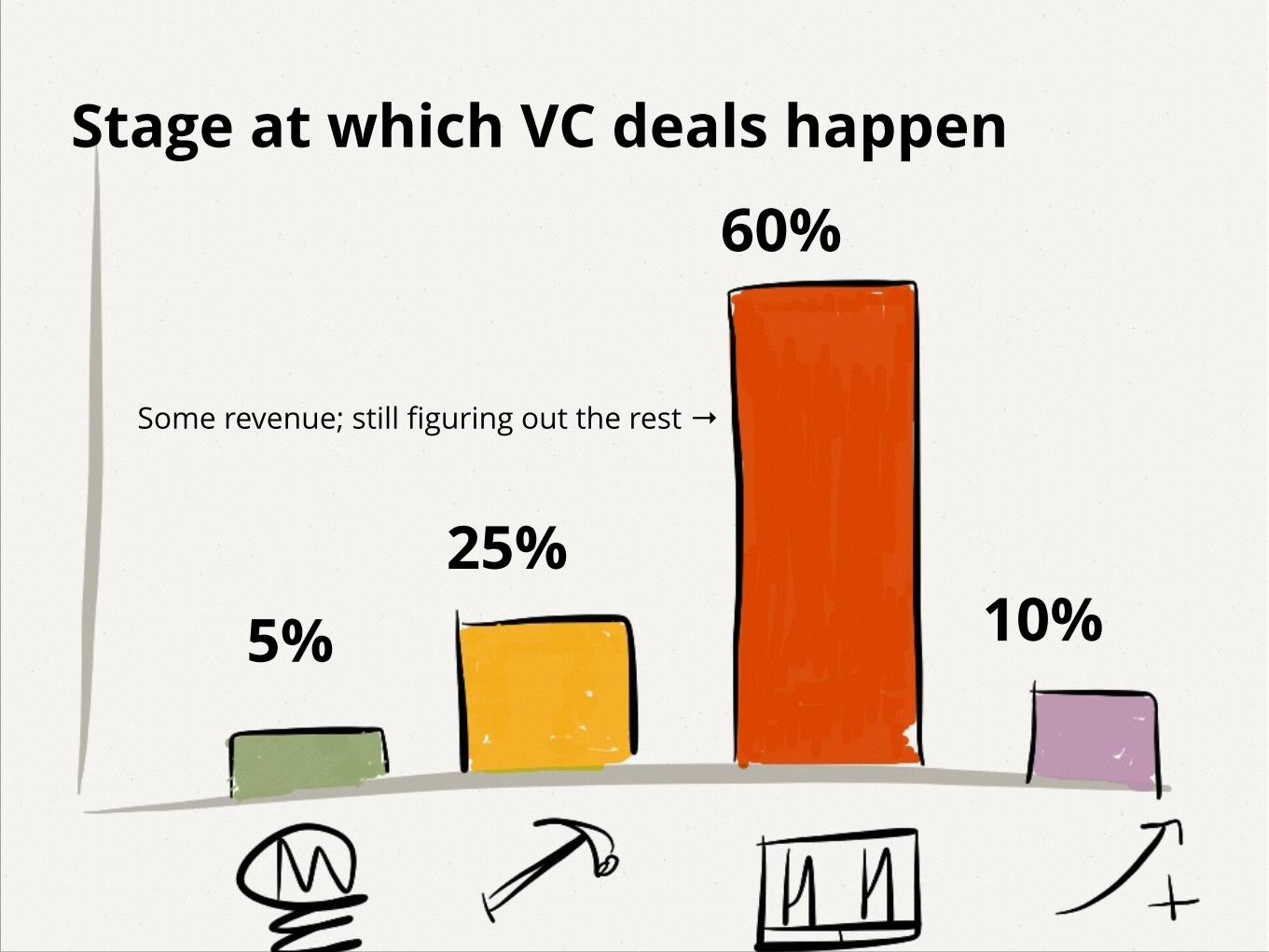

Stage at which VC deals happen

5%25%

60%

10%

Some revenue; still figuring out the rest →

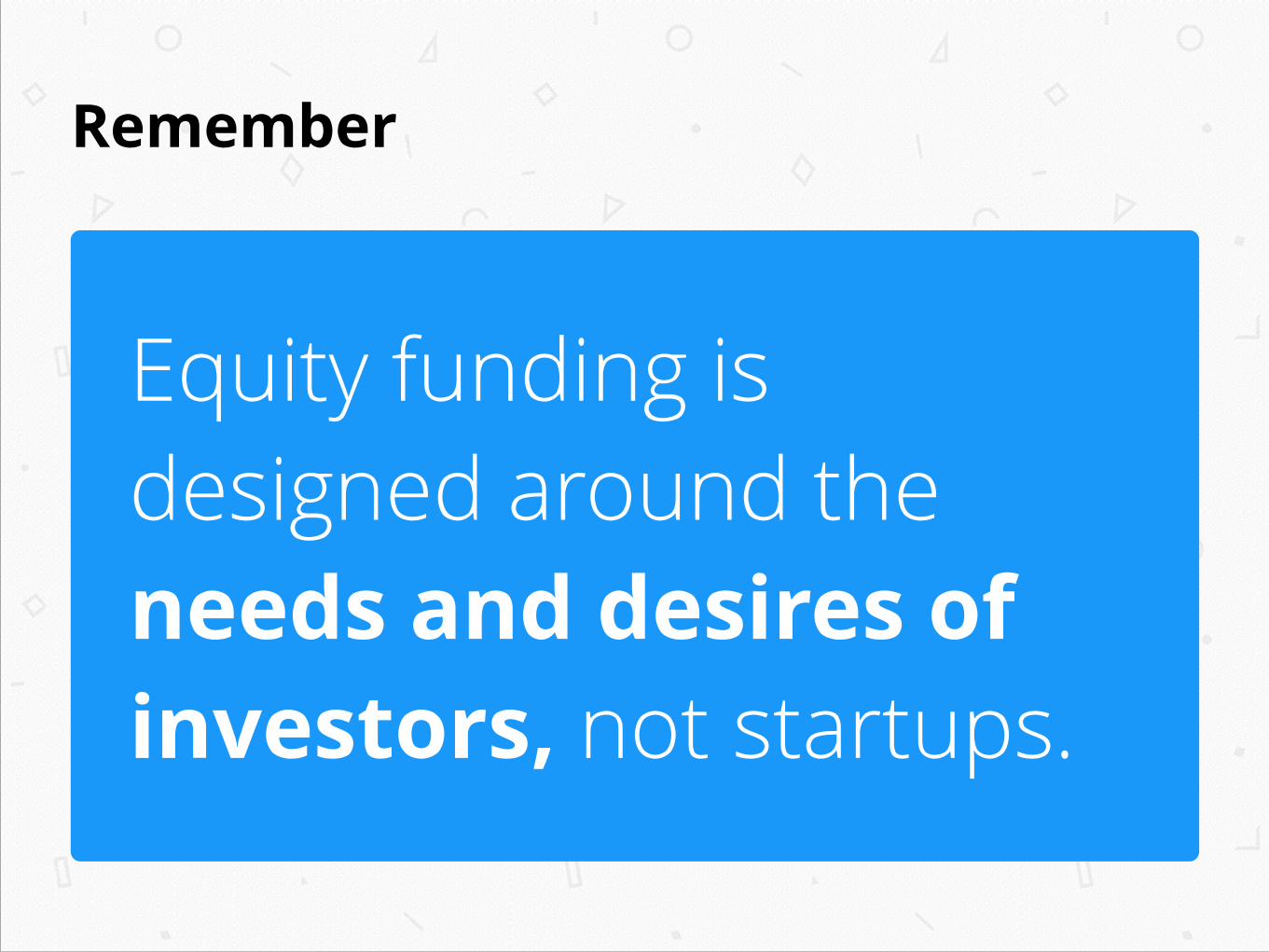

Remember

Equity funding is designed around the needs and desires of investors, not startups.

Question

What do VCs need to see in their investments?

VC investable businesses

1.Big market 2.Defensible moat 3.Ambitious founders 4.10x returns 5. ?

Remember

Investors only get paid if you sell the company, so you’re promising to try and do that

Everyone talks about stock buy-backs;

They don’t happen

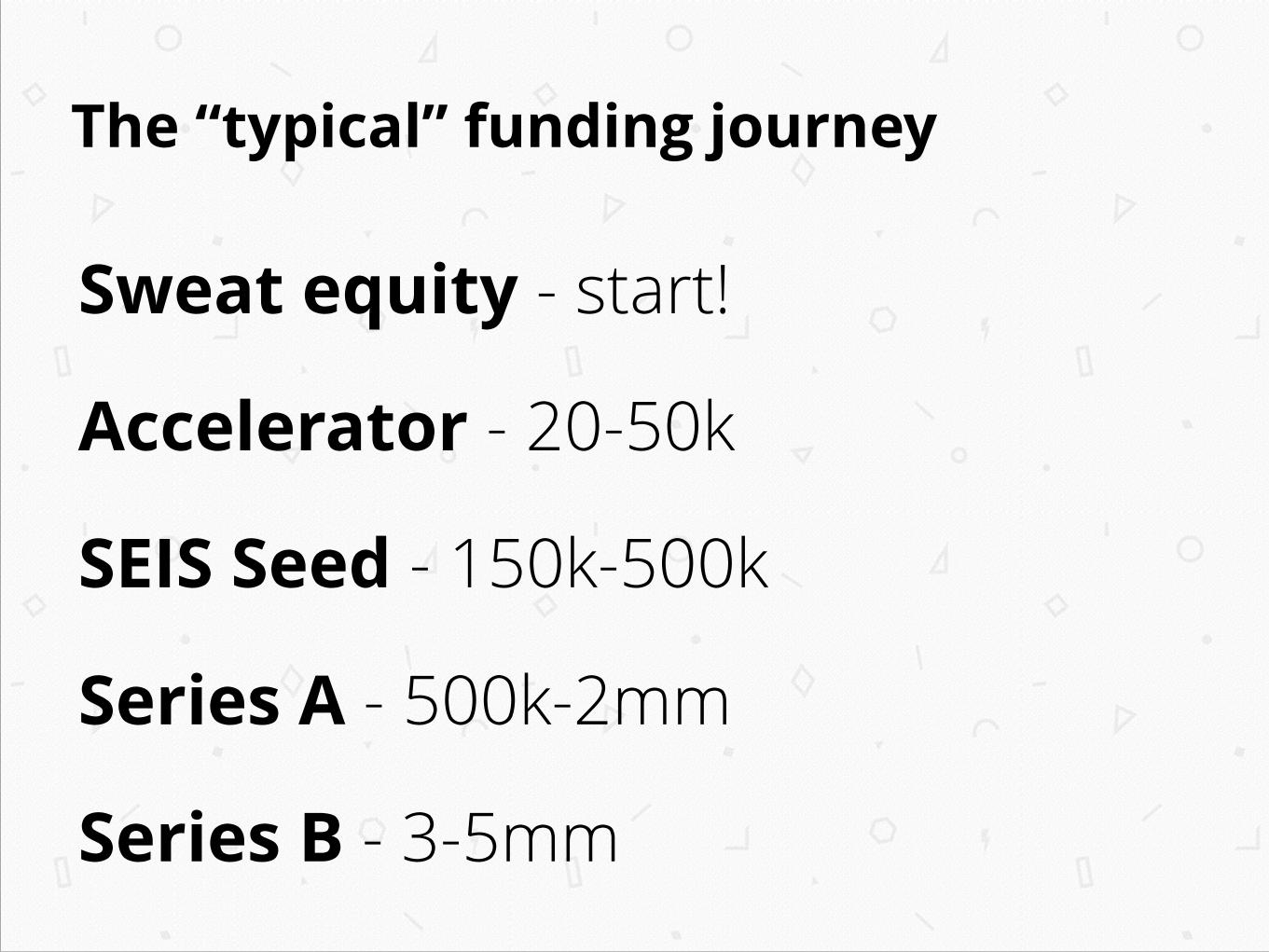

The “typical” funding journey

Sweat equity - start!

Accelerator - 20-50k

SEIS Seed - 150k-500k

Series A - 500k-2mm

Series B - 3-5mm

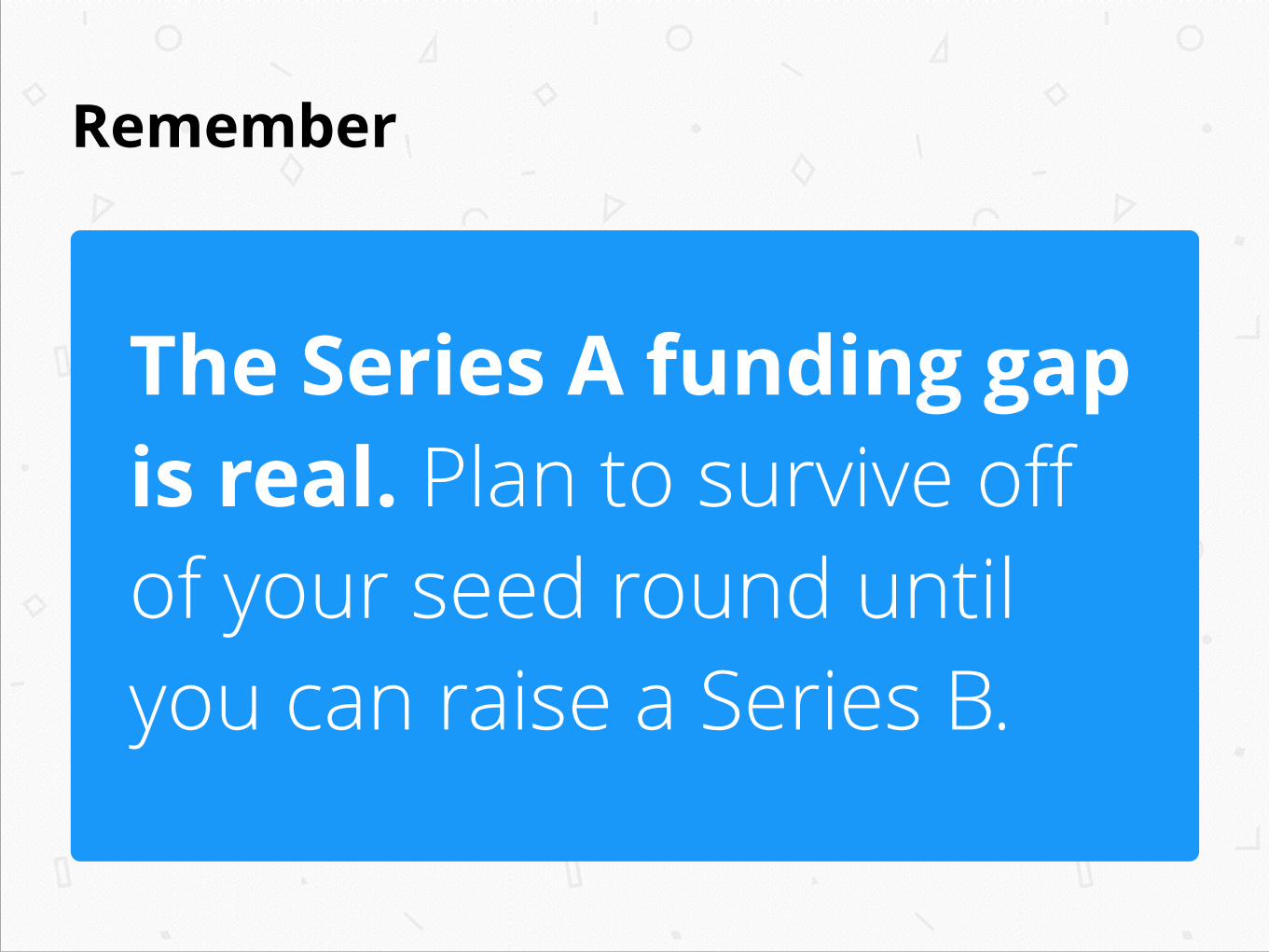

Remember

The Series A funding gap is real. Plan to survive off of your seed round until you can raise a Series B.

You bridge the gaps with sweat equity

Part II Equity

Question

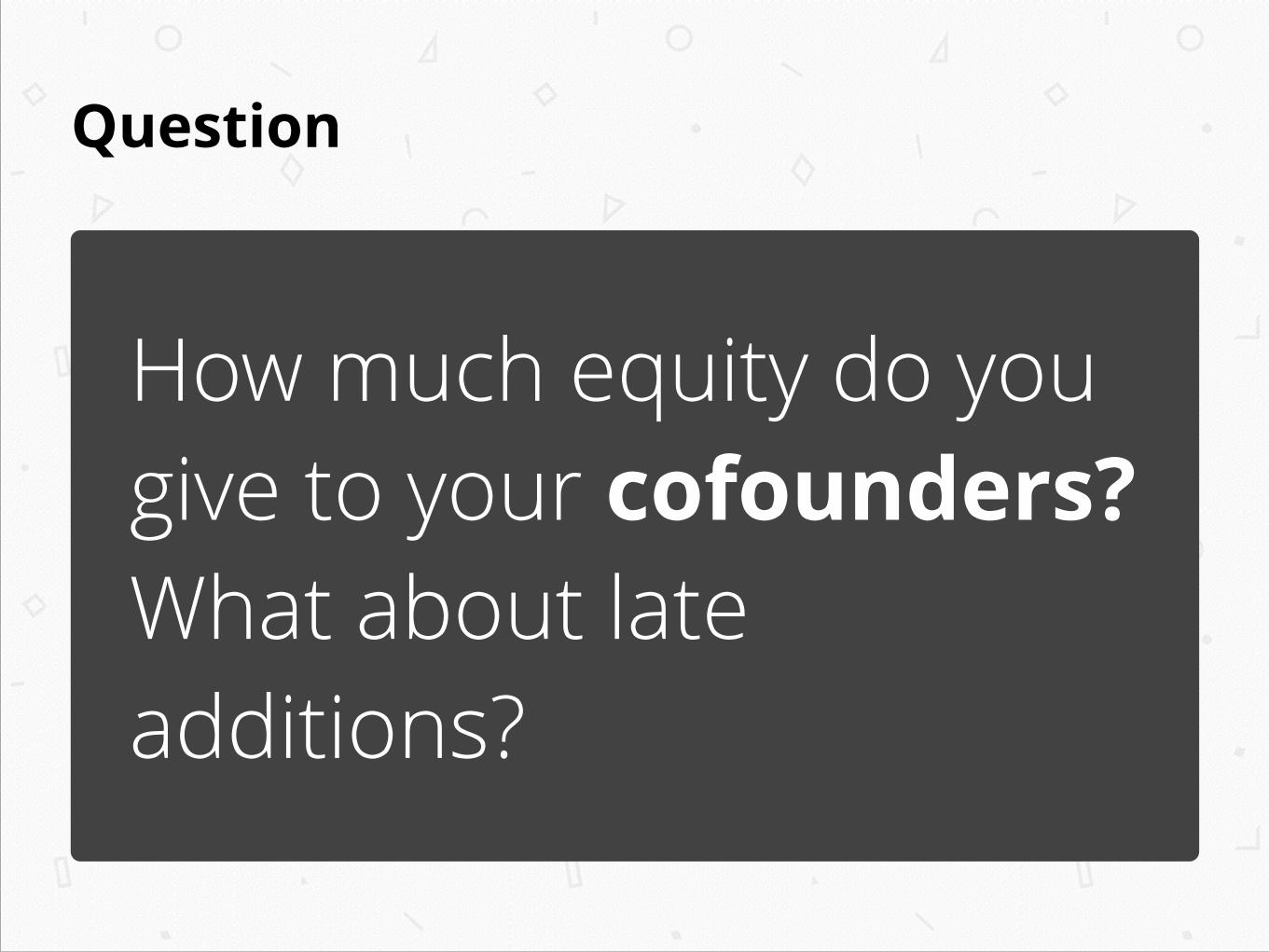

How much equity do you give to your cofounders? What about late additions?

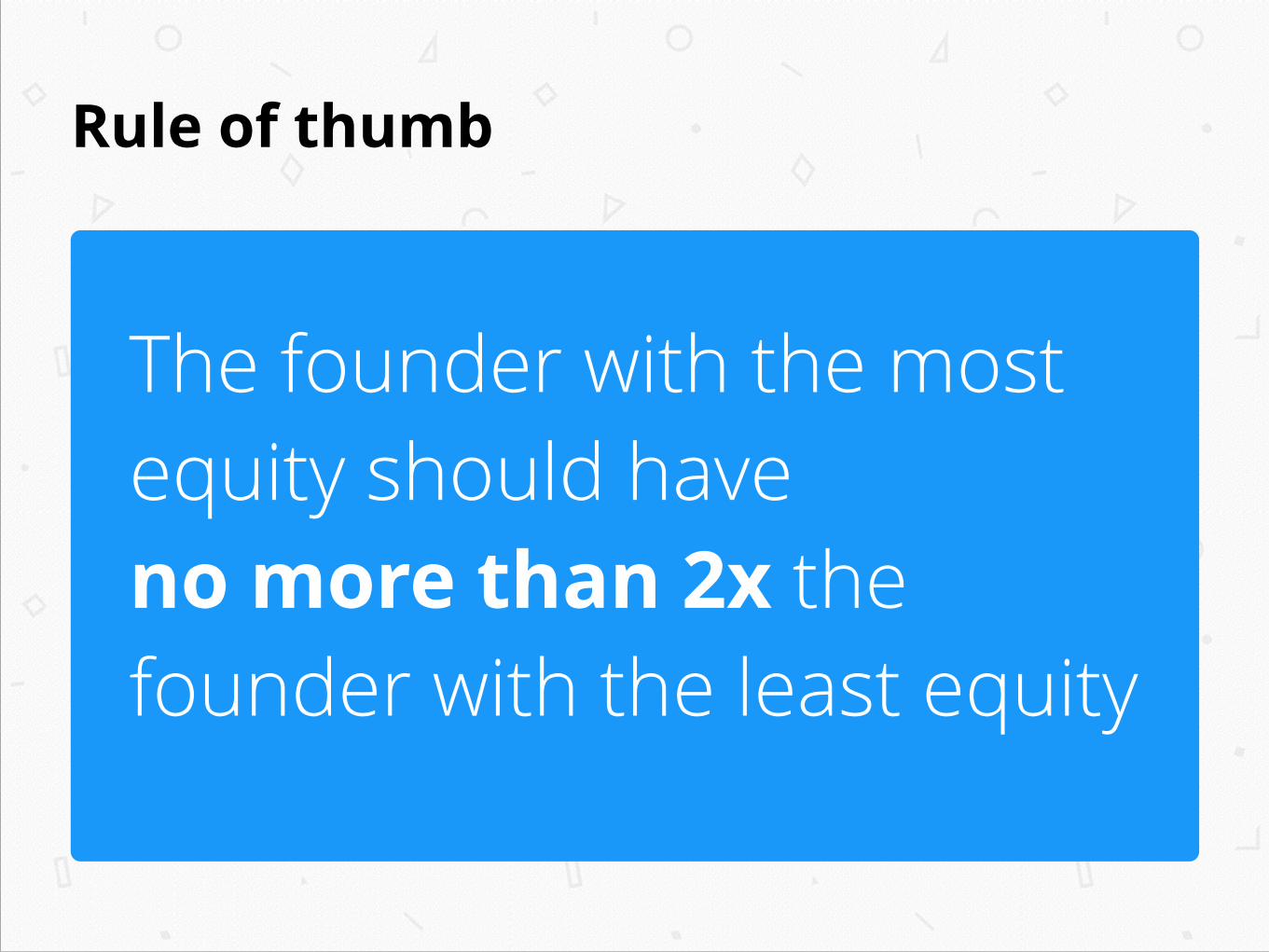

Rule of thumb

The founder with the most equity should have no more than 2x the founder with the least equity

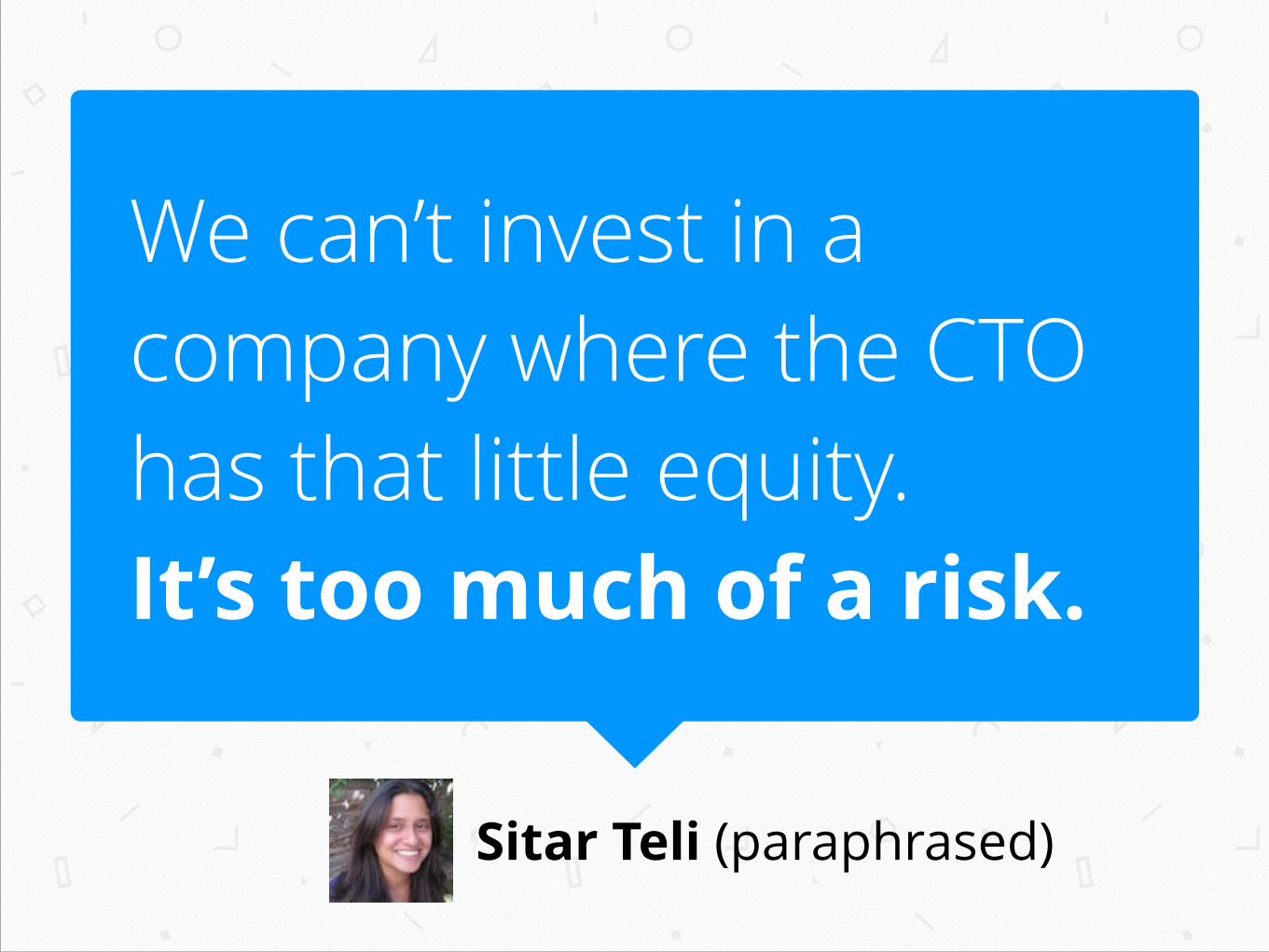

Sitar Teli (paraphrased)

We can’t invest in a company where the CTO has that little equity. It’s too much of a risk.

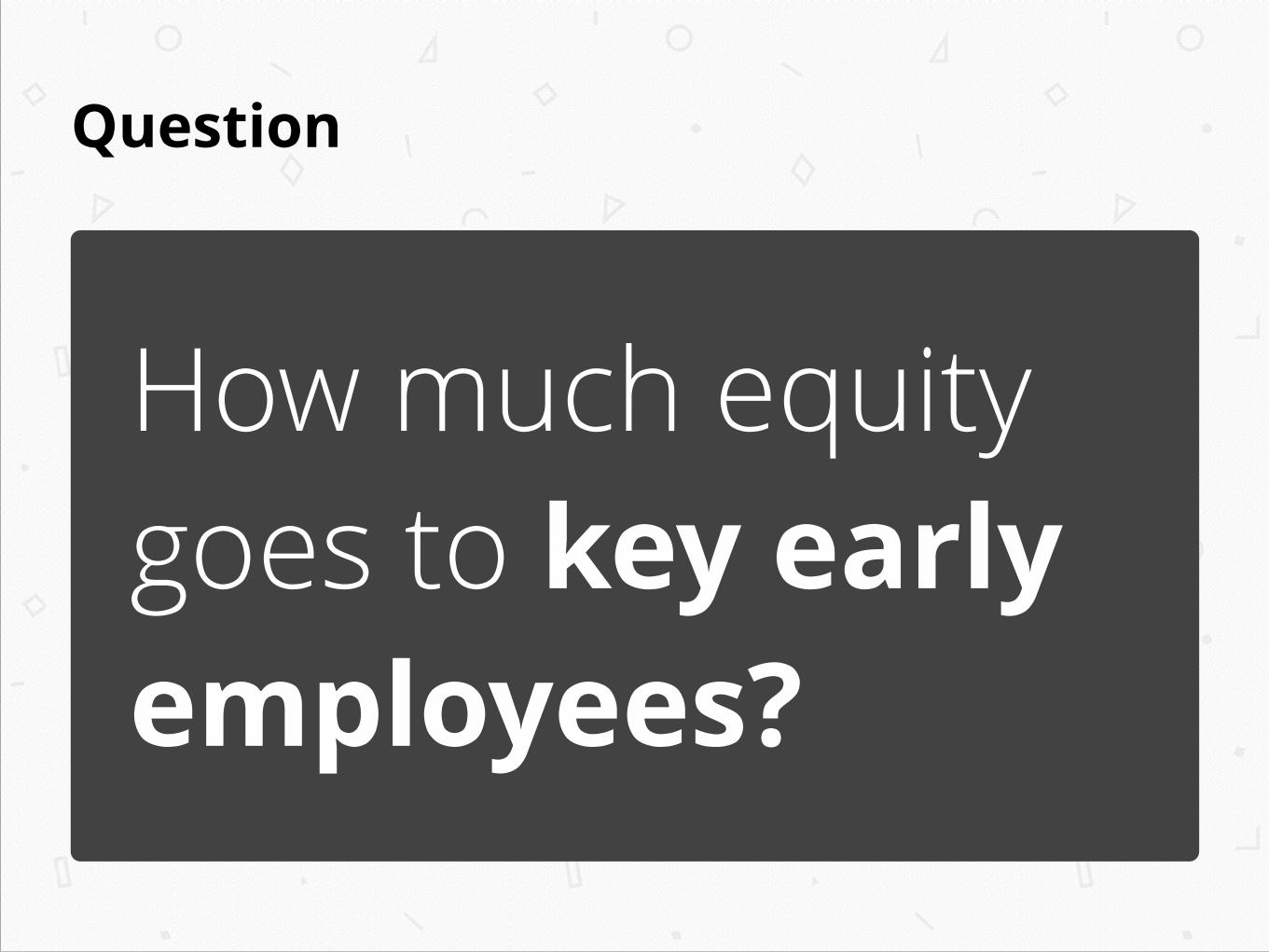

Question

How much equity goes to key early employees?

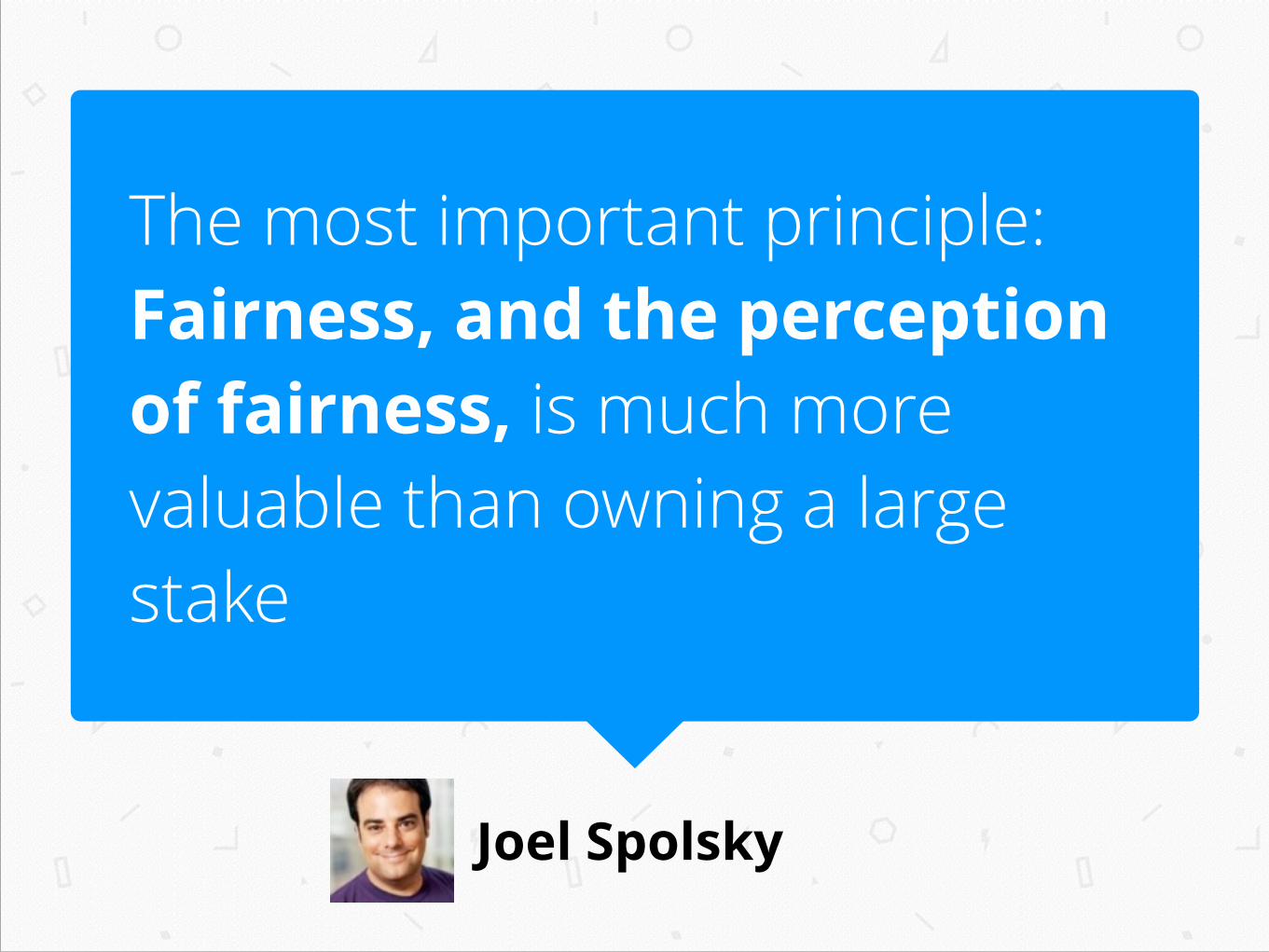

Joel Spolsky

The most important principle: Fairness, and the perception of fairness, is much more valuable than owning a large stake

Question

What do you give an advisor? What do they give you?

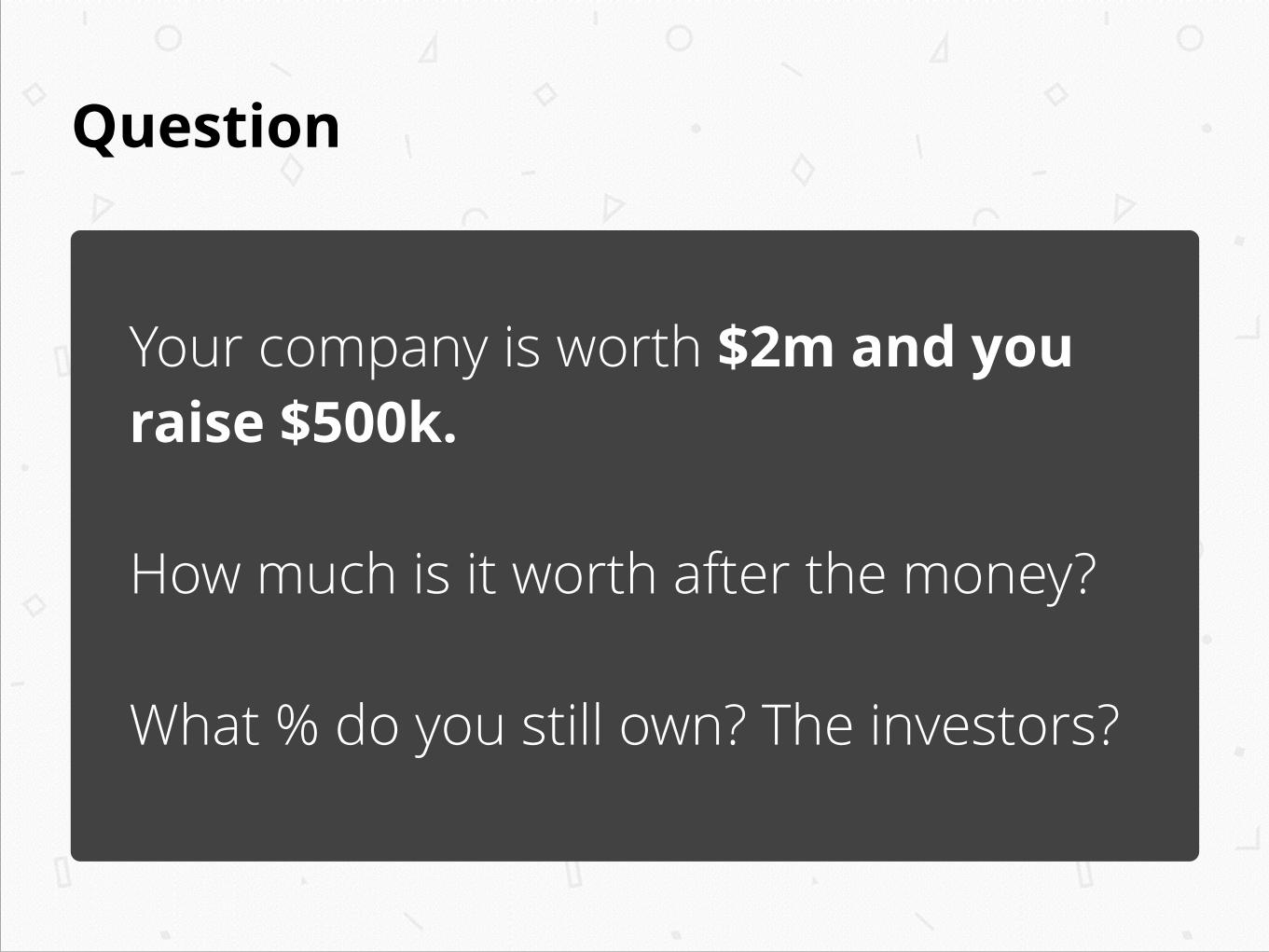

Question

Your company is worth $2m and you raise $500k. !

How much is it worth after the money? !

What % do you still own? The investors?

Question

3 co-founders evenly share a company. They raise 250k on 750k. !

What % and £ does each of them own now? What % of the company have they “given up”?

Run the math!

When investors put cash into a business, your % ownership goes down, but your ££££ ownership stays the same

Part III Valuations

There’s no evidence of what an early-

stage startup will be worth.

So you make it up as a combination of necessity plus comparisons

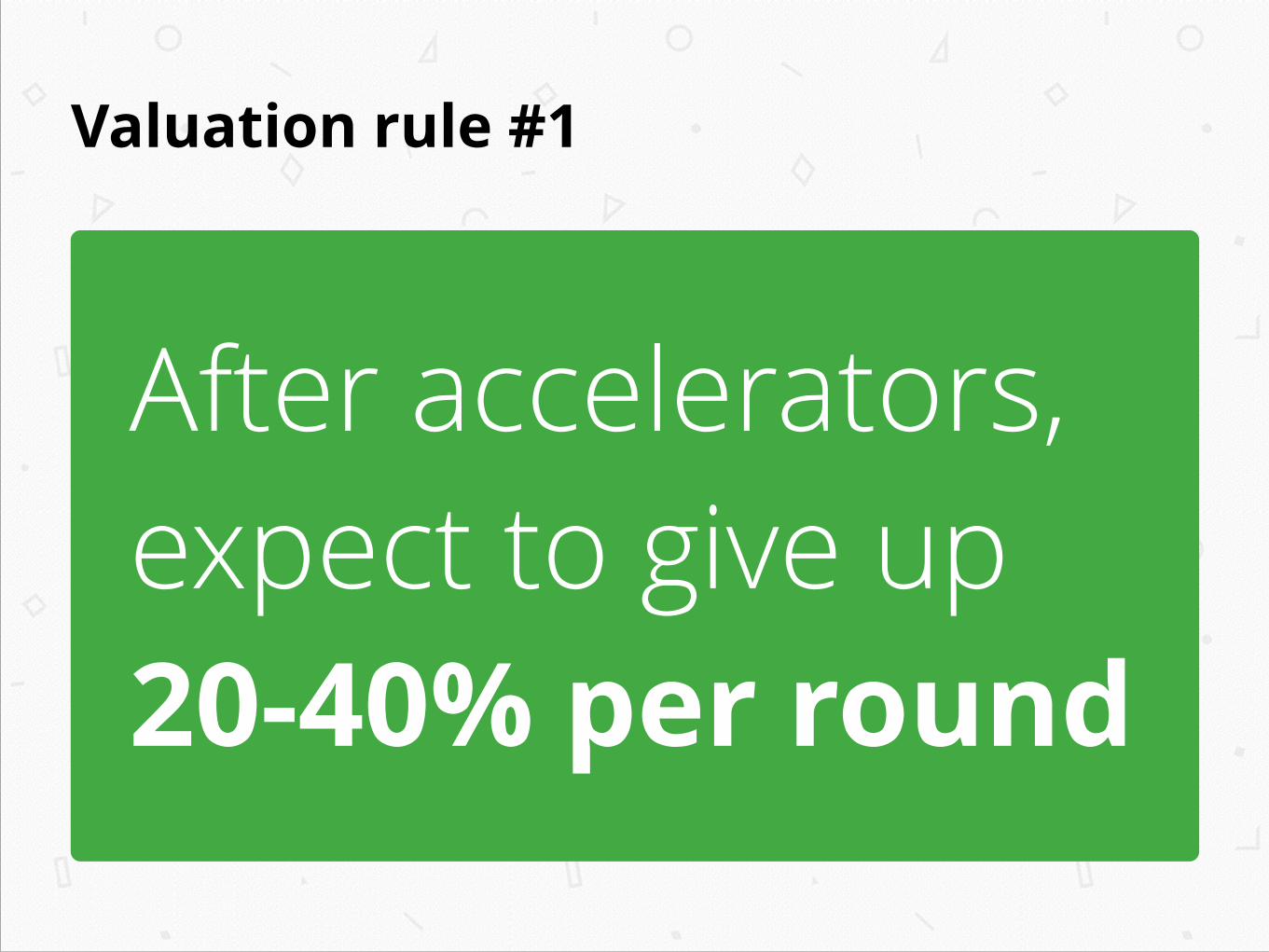

Valuation rule #1

After accelerators, expect to give up 20-40% per round

Don Dodge

Don't worry about giving up too much equity at an early stage. If the company is successful you will be very rich. If it isn't successful then holding 60% versus 30% won't matter.

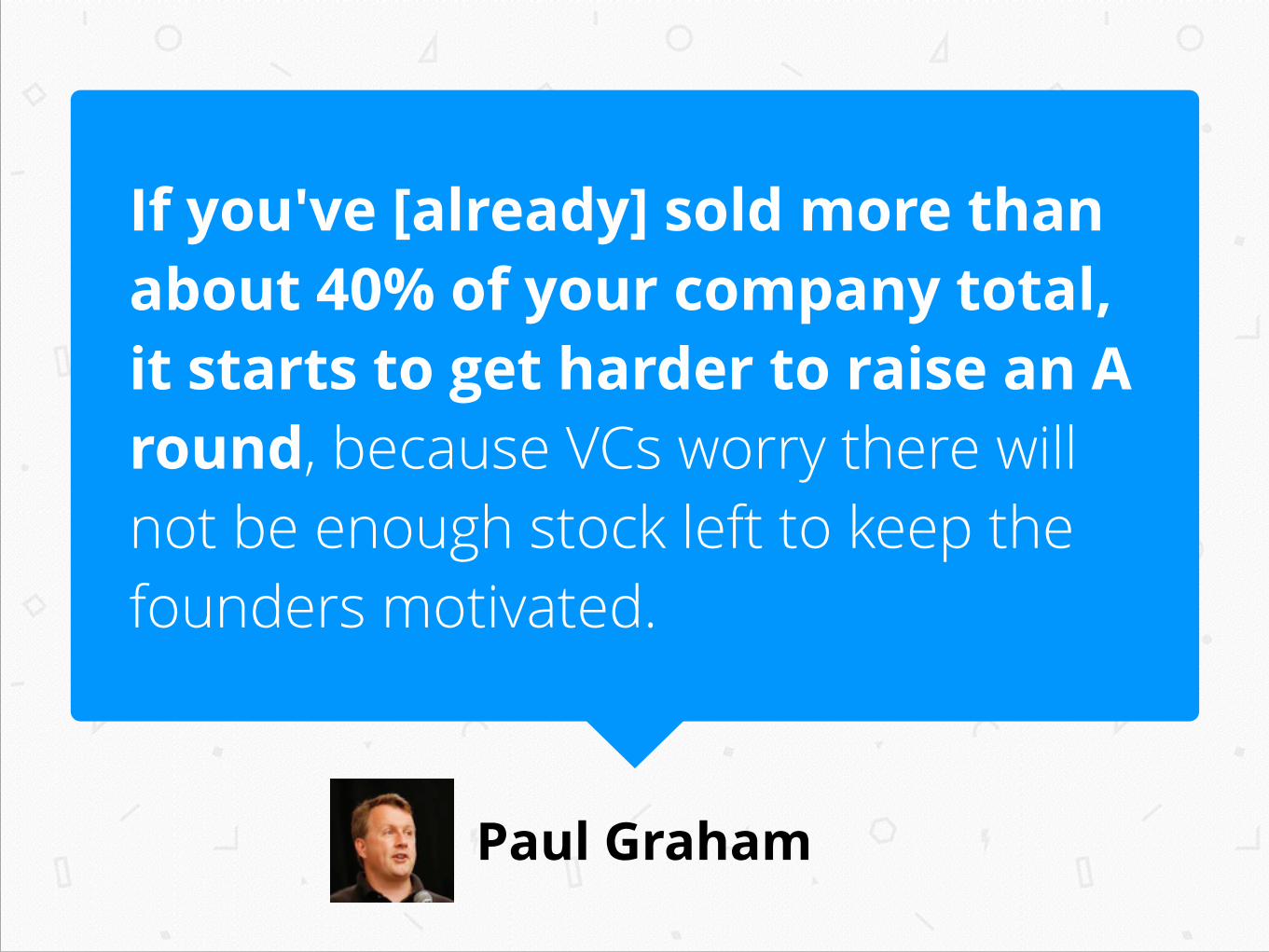

Paul Graham

If you've [already] sold more than about 40% of your company total, it starts to get harder to raise an A round, because VCs worry there will not be enough stock left to keep the founders motivated.

Question

What is the danger of a sky-high valuation? (remember the 10x exit rule)

Valuation rule #2

Raise enough money for 12-24 months

Question

Why raise for so much time?

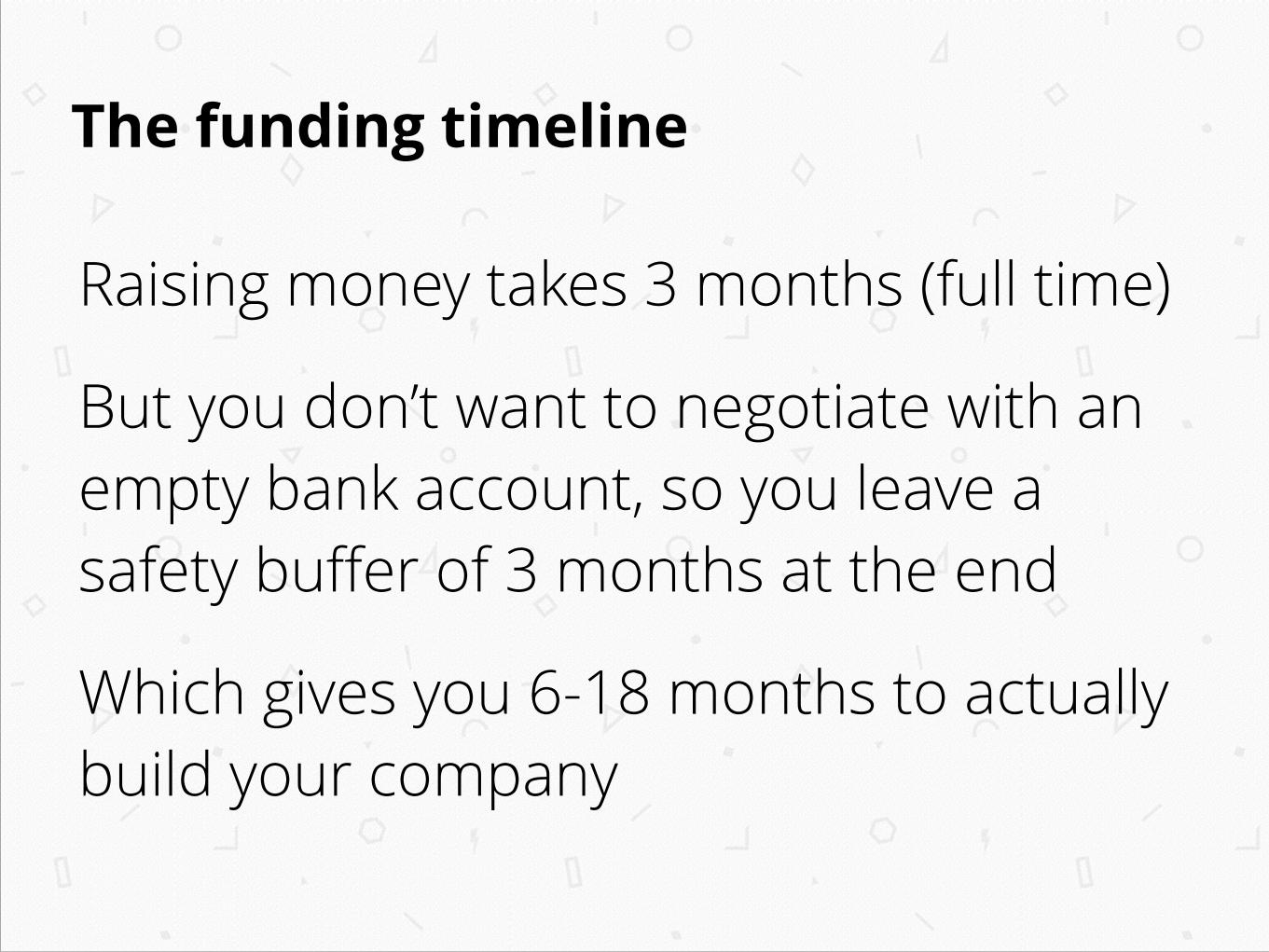

The funding timeline

Raising money takes 3 months (full time)

But you don’t want to negotiate with an empty bank account, so you leave a safety buffer of 3 months at the end

Which gives you 6-18 months to actually build your company

So what’s your valuation?

(Or rather, your valuation range)

Figuring out your valuation

1.Figure out 12 and 24 month budgets 2.Work out a valuation for each based

on 20% and 40% dilution 3.You’ve now got the four “corners” of

your valuation range 4.Negotiate inside those ranges based

on your strength vs. peers

Figuring out your valuation

In other words, if you’re strong, you can either negotiate toward the 20% (less equity) or the 24 months (more runway)

Paul Graham

One of the things that surprises founders most about fundraising is how distracting it is. When you start fundraising, everything else grinds to a halt.

Part IV Practicalities

Stephen Rapoport

I said, “I’m not raising money right now. But I will be in 3 months. What are you scared of and where would we need to be for you to be excited?”

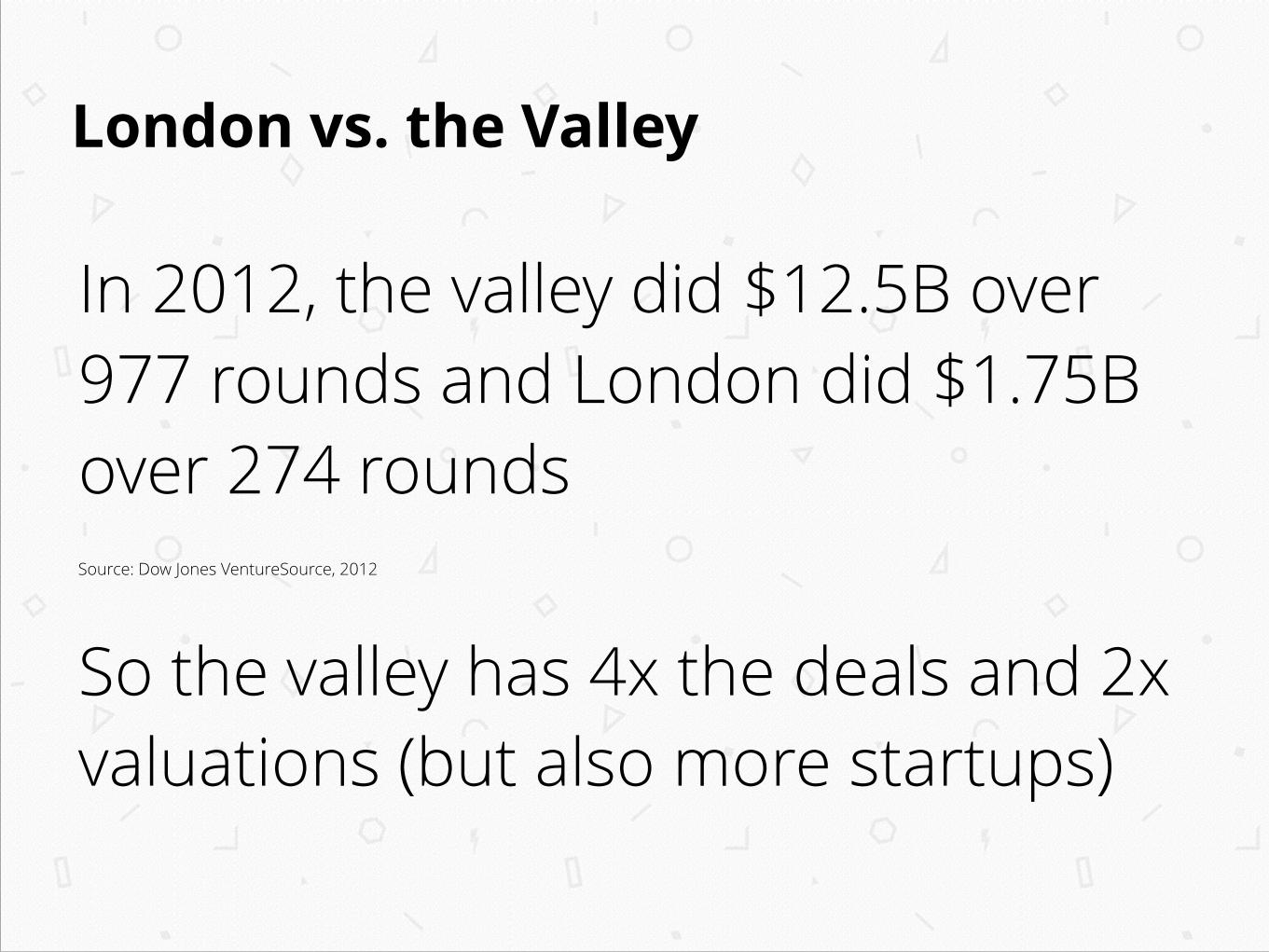

London vs. the Valley

In 2012, the valley did $12.5B over 977 rounds and London did $1.75B over 274 rounds Source: Dow Jones VentureSource, 2012

So the valley has 4x the deals and 2x valuations (but also more startups)

Do your investor Due Dil

• f6s.com (accelerators) • angel.co (angels & VCs globally) • capitallist.co (London angels) • thefunded.com (investor ratings)

Some final tips

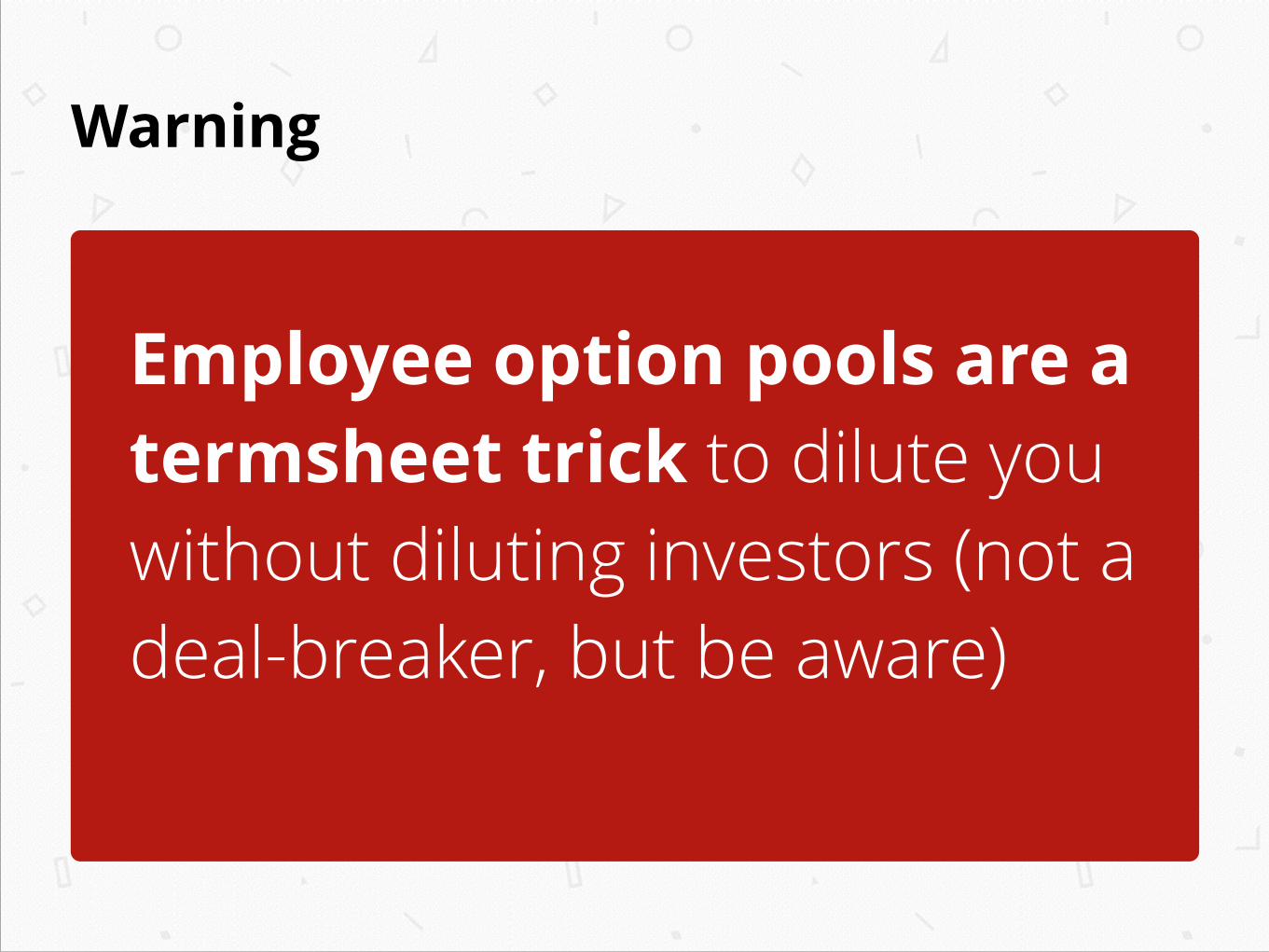

Warning

Employee option pools are a termsheet trick to dilute you without diluting investors (not a deal-breaker, but be aware)

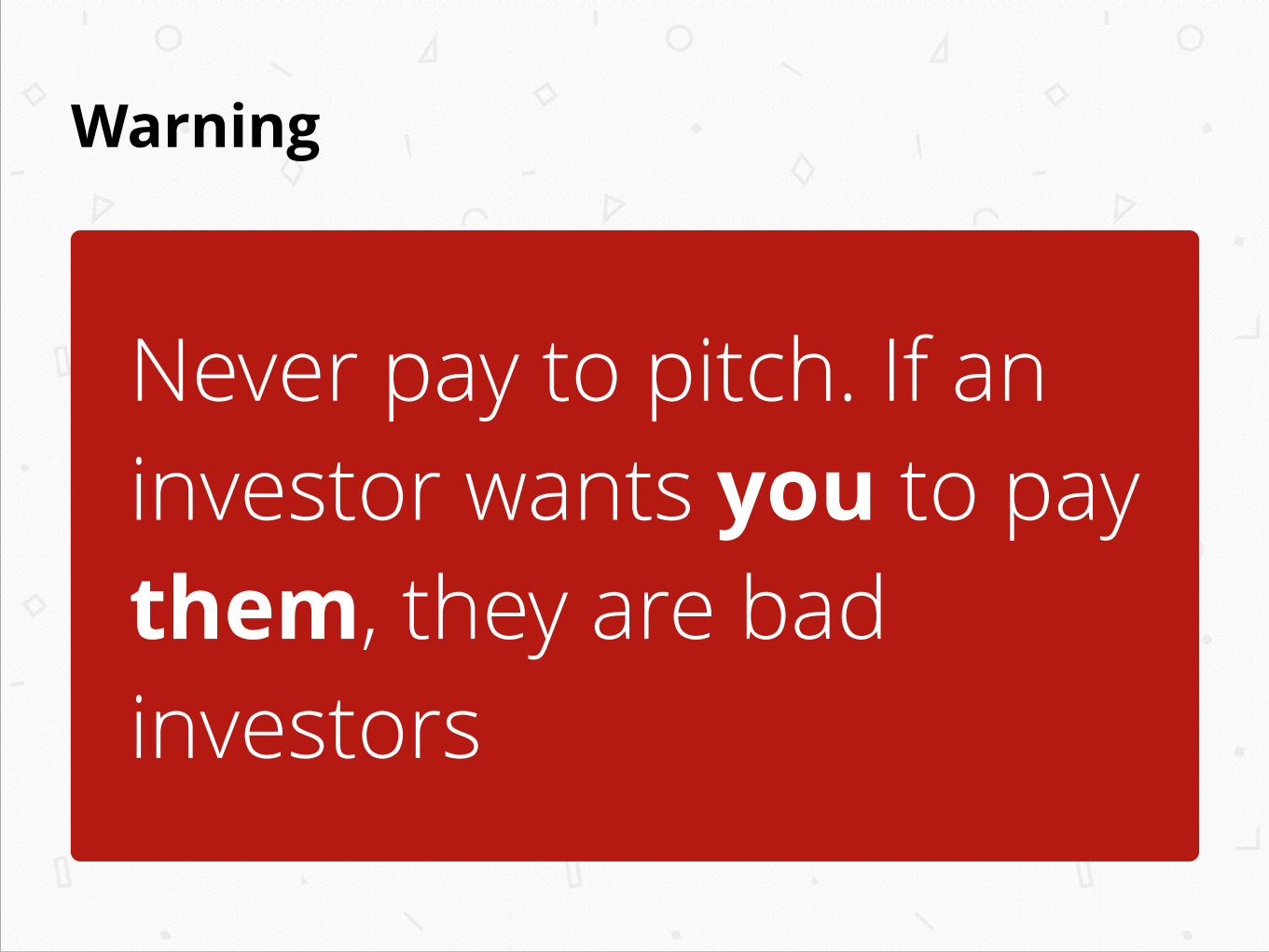

Warning

Never pay to pitch. If an investor wants you to pay them, they are bad investors

Warning

Don’t do deals with investors who propose “participation preferred” or “ratchets”

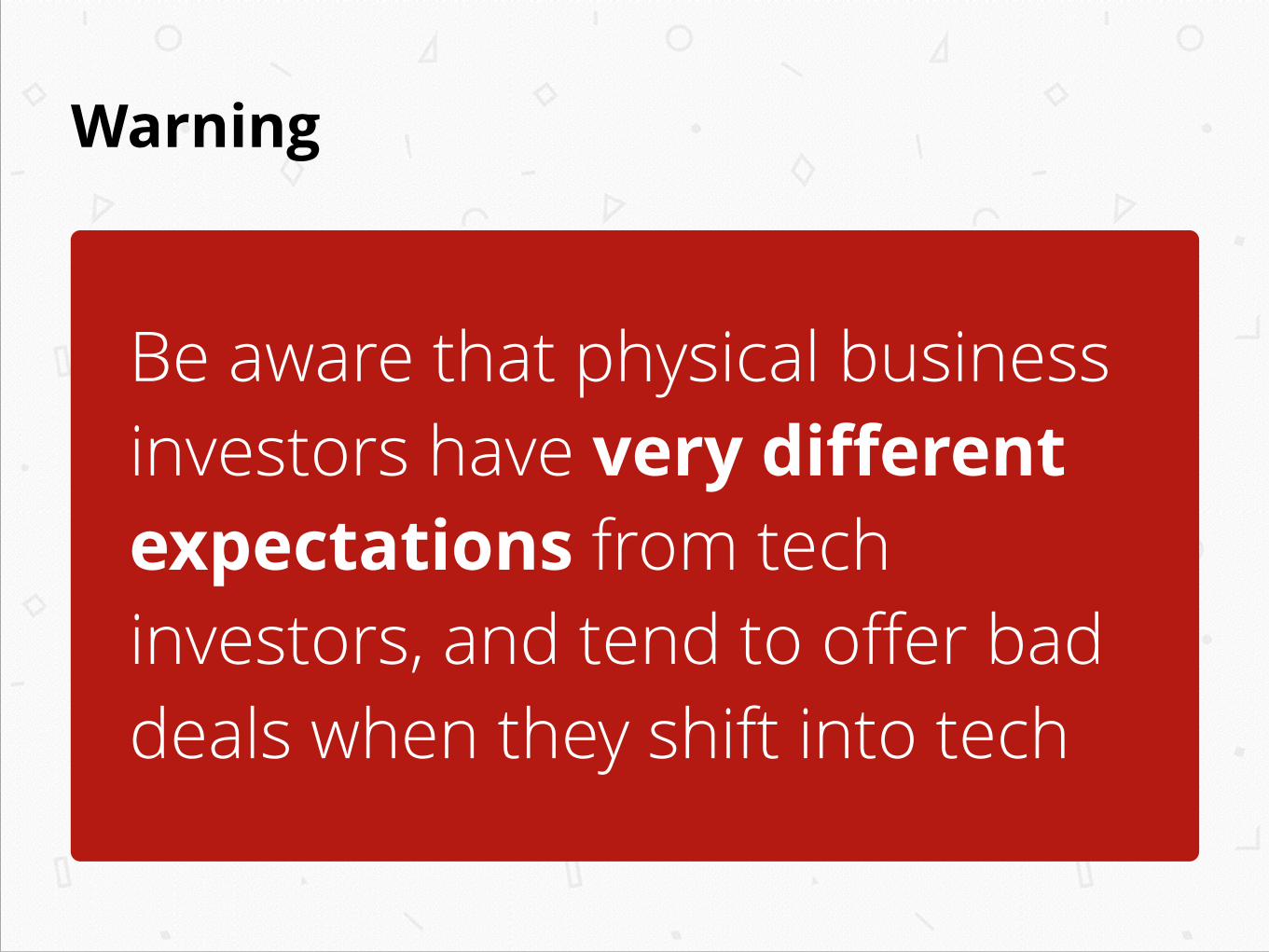

Warning

Be aware that physical business investors have very different expectations from tech investors, and tend to offer bad deals when they shift into tech

Tip

Keep negotiation simple by focusing only on pre-money valuation and the amount they’re putting in

Tip

Search online for founder-friendly boilerplate and bring your own term sheet to resolve the rest of the terms

Tip

Close a strong lead investor ASAP (e.g. cash in bank), and then fill in the rest as a rolling round

Tip

Cold emails to investors don’t work. You need warm intros.

Paul Graham

And read this: paulgraham.com/fr.html

Thanks! Questions?