Embed Size (px)

DESCRIPTION

Fundamentals of startup equity with a focus on employe incentive grants, corporate structures and tax liabilities

Citation preview

Startup Equity 101 Primer for Founders and Employees

May 1, 2013by Jamie Lee@jieunjamie

with Ekaterina Mouratova, PLLCwww.mouratovalawfirm.com

Thursday, May 2, 13

Disclaimer

Hi! I’m not an accountant or a lawyer.

The information contained herein and ensuing discussion should NOT be considered tax or legal advice.

The information is intended to help you get familiarized with general concepts in startup finance, which may or may not apply to your situation.

Thank you!

Jamie Lee @jieunjamiejieunjamie.com

Thursday, May 2, 13

Startup Equity: More ART than SCIENCE but still need to ASK questions

Thursday, May 2, 13

Before joining a startup, ask

• Is this the right team and company for my success?

•What is my percentage of ownership?

•What is total company capitalization?

•How long is my vesting schedule?

•What are tax implications?

•What is the estimated valuation at exit?

•What do I need to do when I leave?

Startup Equity: More ART than SCIENCE but still need to ASK questions

Thursday, May 2, 13

Before joining a startup, ask

• Is this the right team and company for my success?

•What is my percentage of ownership?

•What is total company capitalization?

•How long is my vesting schedule?

•What are tax implications?

•What is the estimated valuation at exit?

•What do I need to do when I leave?

Startup Equity: More ART than SCIENCE but still need to ASK questions

If you’re a founder or employee,

•Research market rate salary and equity comp

•Read the partnership and employment agreements

•Negotiate like a business person

•Consult a lawyer or tax accountant (devil’s in the details)

•Exercise your options early

•Make 83b election ASAP for restricted stock grants

Thursday, May 2, 13

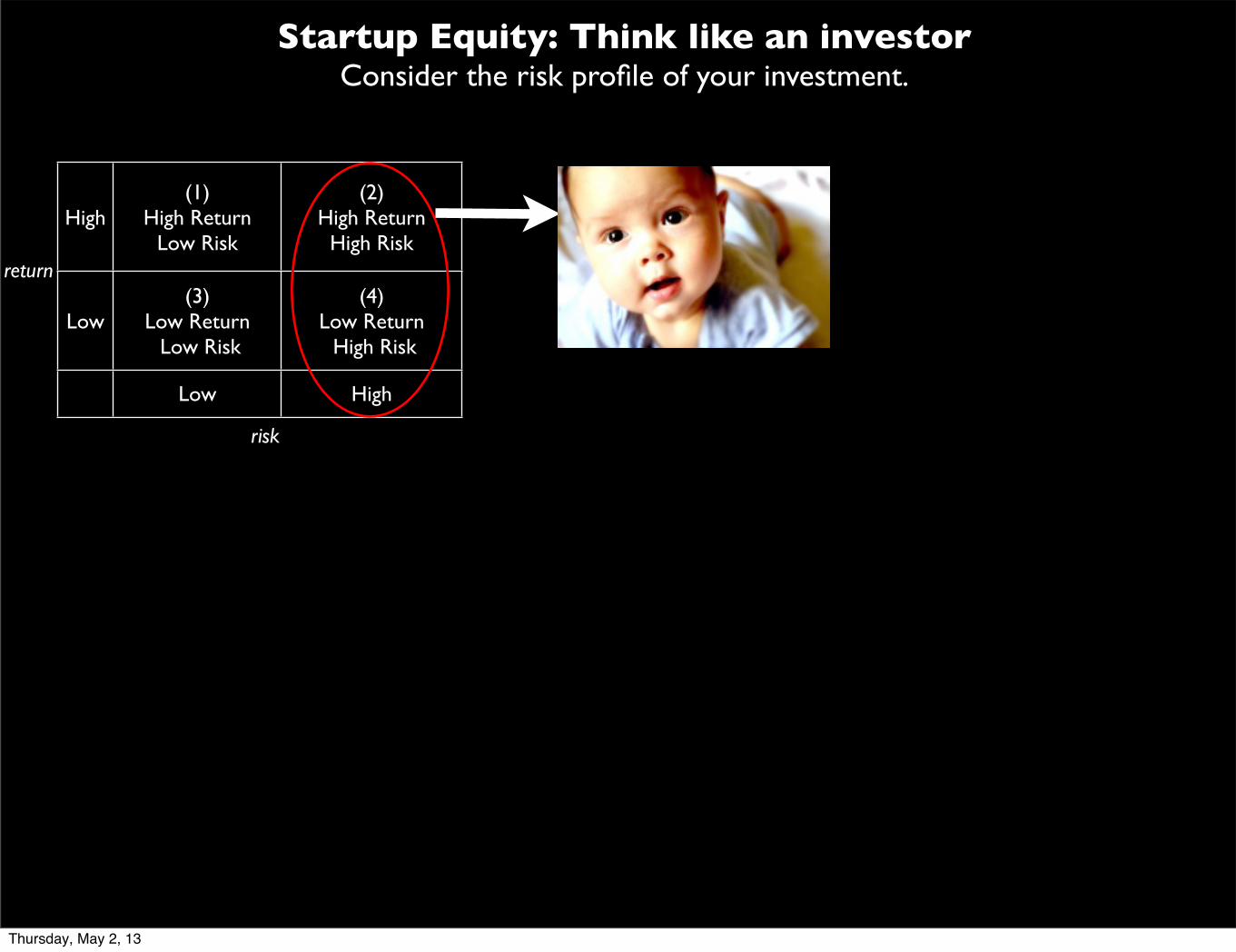

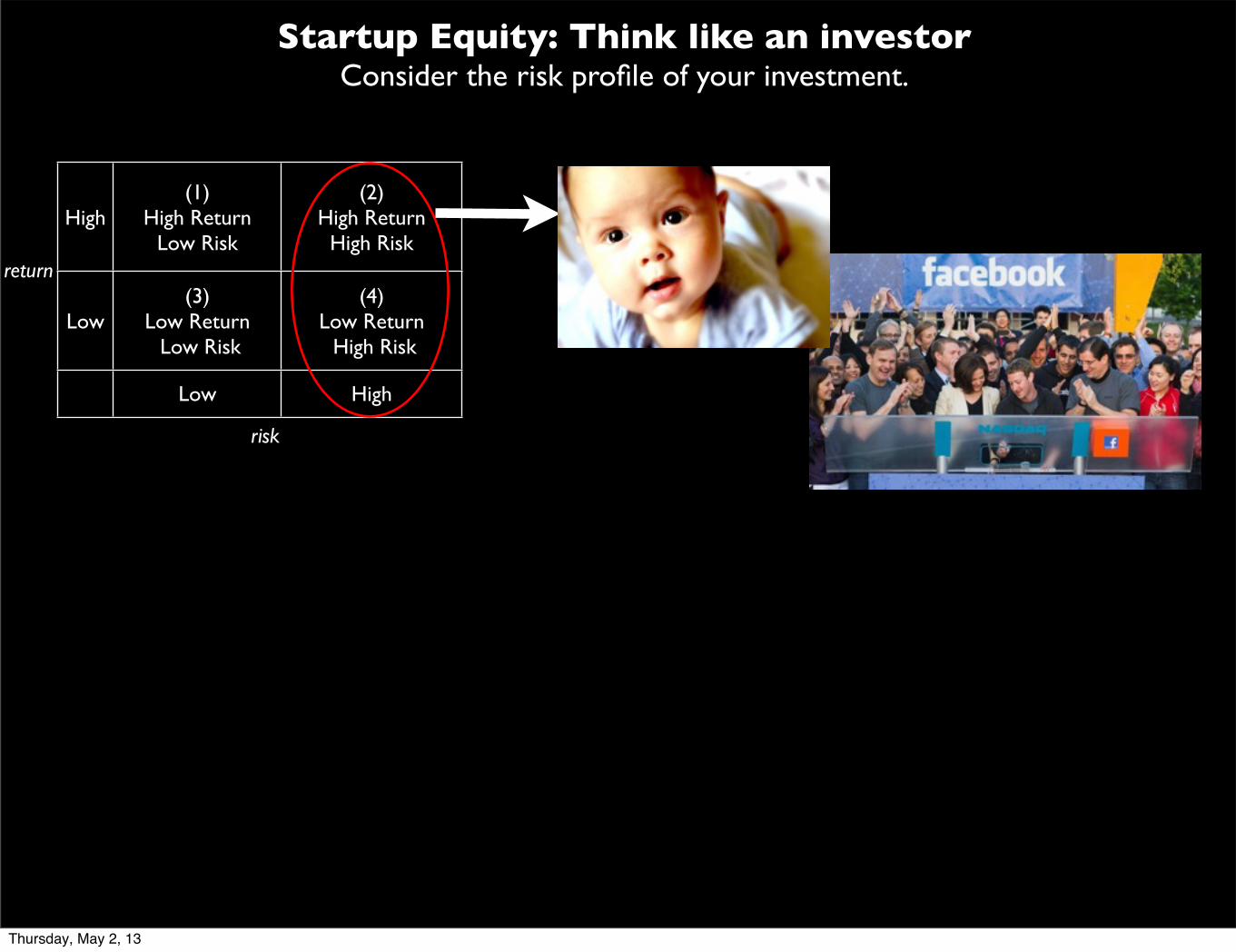

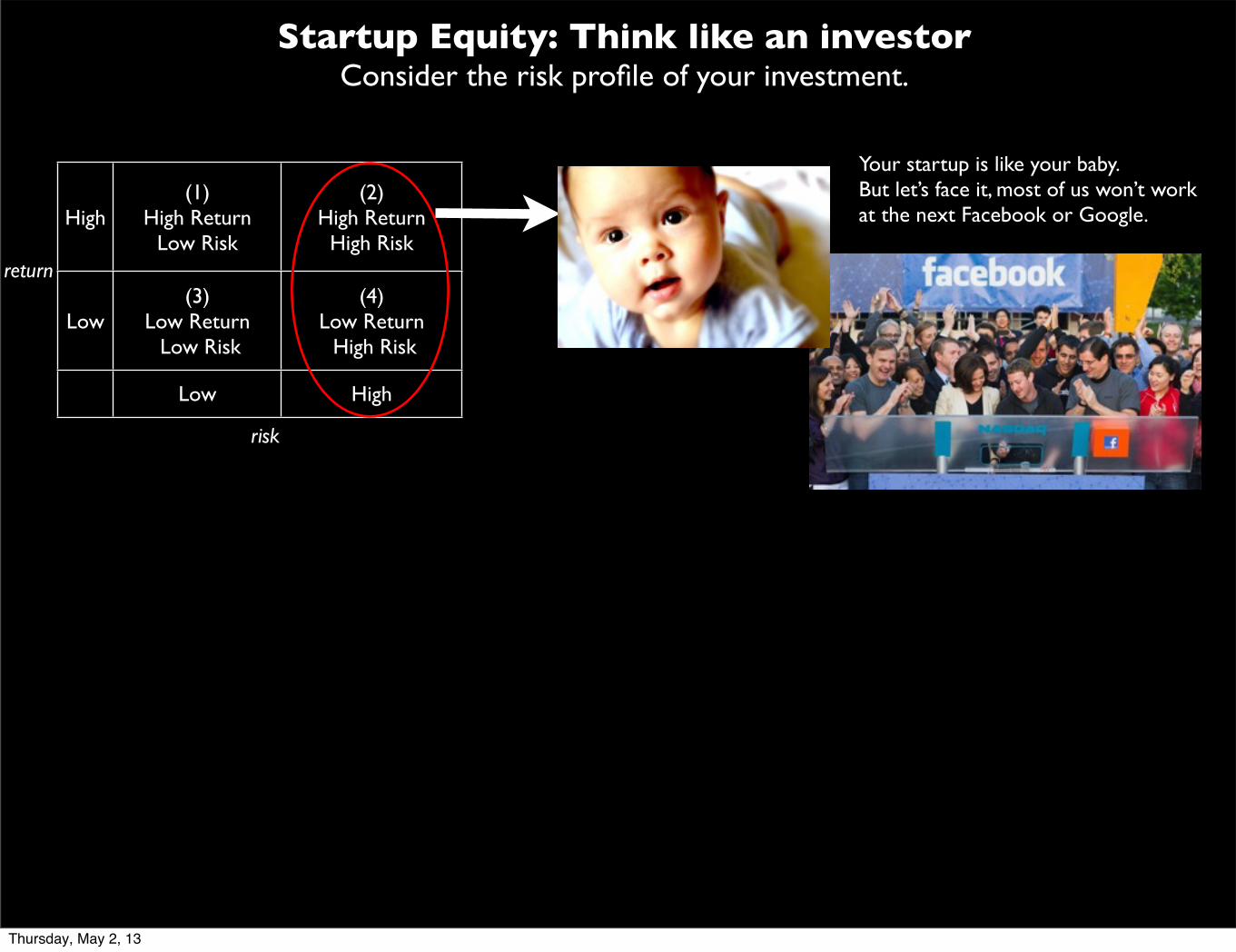

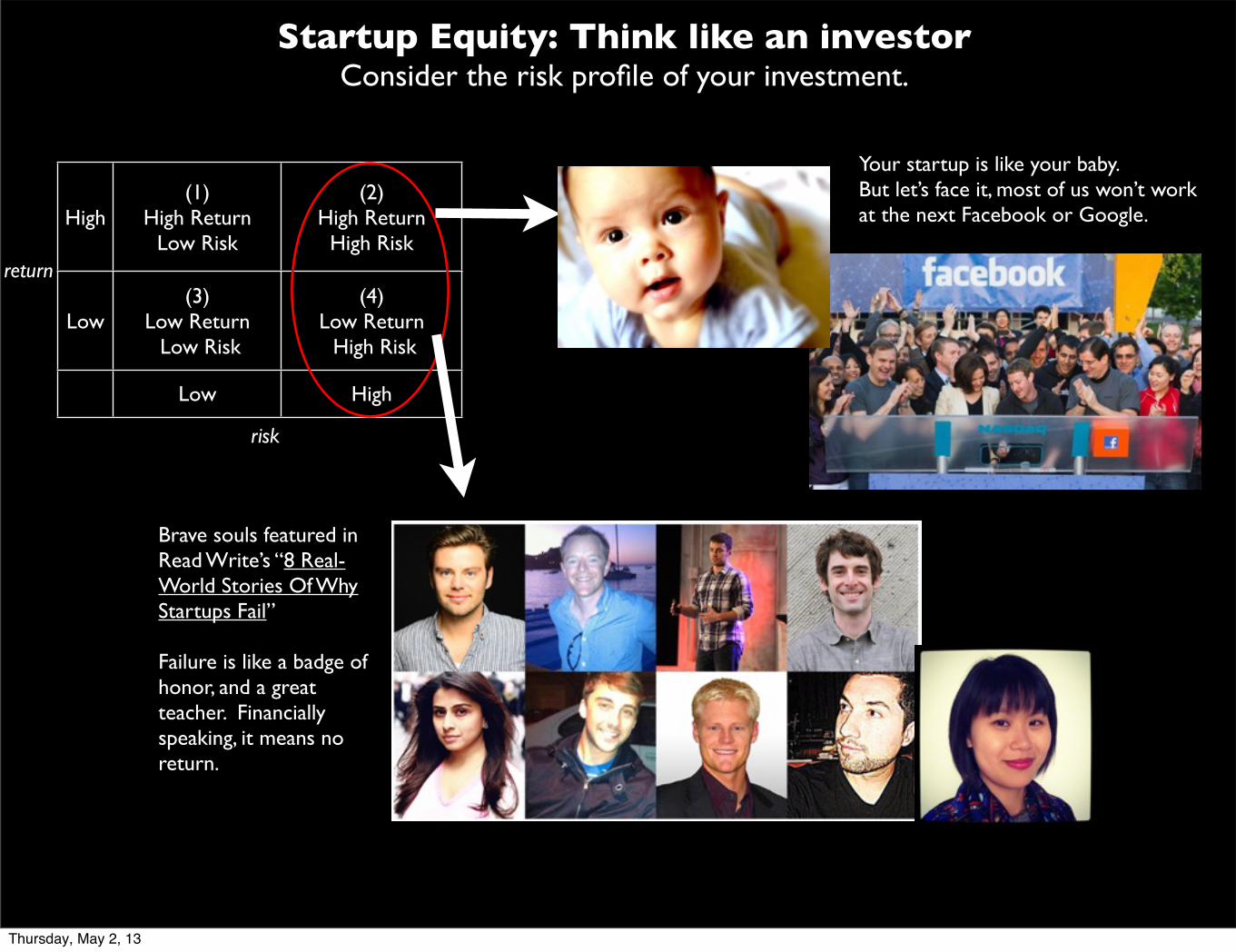

High(1)

High ReturnLow Risk

(2)High Return

High Risk

Low(3)

Low Return Low Risk

(4)Low Return High Risk

Low High

risk

return

Startup Equity: Think like an investorConsider the risk profile of your investment.

Thursday, May 2, 13

High(1)

High ReturnLow Risk

(2)High Return

High Risk

Low(3)

Low Return Low Risk

(4)Low Return High Risk

Low High

risk

return

Startup Equity: Think like an investorConsider the risk profile of your investment.

Thursday, May 2, 13

High(1)

High ReturnLow Risk

(2)High Return

High Risk

Low(3)

Low Return Low Risk

(4)Low Return High Risk

Low High

risk

return

Startup Equity: Think like an investorConsider the risk profile of your investment.

Thursday, May 2, 13

High(1)

High ReturnLow Risk

(2)High Return

High Risk

Low(3)

Low Return Low Risk

(4)Low Return High Risk

Low High

risk

return

Startup Equity: Think like an investorConsider the risk profile of your investment.

Thursday, May 2, 13

High(1)

High ReturnLow Risk

(2)High Return

High Risk

Low(3)

Low Return Low Risk

(4)Low Return High Risk

Low High

risk

return

Startup Equity: Think like an investorConsider the risk profile of your investment.

Thursday, May 2, 13

High(1)

High ReturnLow Risk

(2)High Return

High Risk

Low(3)

Low Return Low Risk

(4)Low Return High Risk

Low High

risk

return

Startup Equity: Think like an investorConsider the risk profile of your investment.

Your startup is like your baby. But let’s face it, most of us won’t work at the next Facebook or Google.

Thursday, May 2, 13

High(1)

High ReturnLow Risk

(2)High Return

High Risk

Low(3)

Low Return Low Risk

(4)Low Return High Risk

Low High

risk

return

Startup Equity: Think like an investorConsider the risk profile of your investment.

Your startup is like your baby. But let’s face it, most of us won’t work at the next Facebook or Google.

Thursday, May 2, 13

High(1)

High ReturnLow Risk

(2)High Return

High Risk

Low(3)

Low Return Low Risk

(4)Low Return High Risk

Low High

risk

return

Startup Equity: Think like an investorConsider the risk profile of your investment.

Your startup is like your baby. But let’s face it, most of us won’t work at the next Facebook or Google.

Thursday, May 2, 13

High(1)

High ReturnLow Risk

(2)High Return

High Risk

Low(3)

Low Return Low Risk

(4)Low Return High Risk

Low High

risk

return

Startup Equity: Think like an investorConsider the risk profile of your investment.

Your startup is like your baby. But let’s face it, most of us won’t work at the next Facebook or Google.

Brave souls featured in Read Write’s “8 Real-World Stories Of Why Startups Fail”

Failure is like a badge of honor, and a great teacher. Financially speaking, it means no return.

Thursday, May 2, 13

High(1)

High ReturnLow Risk

(2)High Return

High Risk

Low(3)

Low Return Low Risk

(4)Low Return High Risk

Low High

risk

return

Startup Equity: Think like an investorConsider the risk profile of your investment.

Your startup is like your baby. But let’s face it, most of us won’t work at the next Facebook or Google.

Brave souls featured in Read Write’s “8 Real-World Stories Of Why Startups Fail”

Failure is like a badge of honor, and a great teacher. Financially speaking, it means no return.

Thursday, May 2, 13

High(1)

High ReturnLow Risk

(2)High Return

High Risk

Low(3)

Low Return Low Risk

(4)Low Return High Risk

Low High

risk

return

Startup Equity: Think like an investorConsider the risk profile of your investment.

Your startup is like your baby. But let’s face it, most of us won’t work at the next Facebook or Google.

Brave souls featured in Read Write’s “8 Real-World Stories Of Why Startups Fail”

Failure is like a badge of honor, and a great teacher. Financially speaking, it means no return.

Yup, that’s me.

Thursday, May 2, 13

Startup Equity: Owning a piece of the pie

Thursday, May 2, 13

Startup Equity: Owning a piece of the pie

Thursday, May 2, 13

Startup Equity: Owning a piece of the pie

Let’s say your startup is like a pizza pie you and your team make from scratch.

Individual slices are owned by different people, but the team’s goal is to grow the pie as a whole.

As more people get involved and invest, your slice may get skinnier, and the pie bigger. This is called dilution.

Thursday, May 2, 13

Startup Equity: Owning a piece of the pie

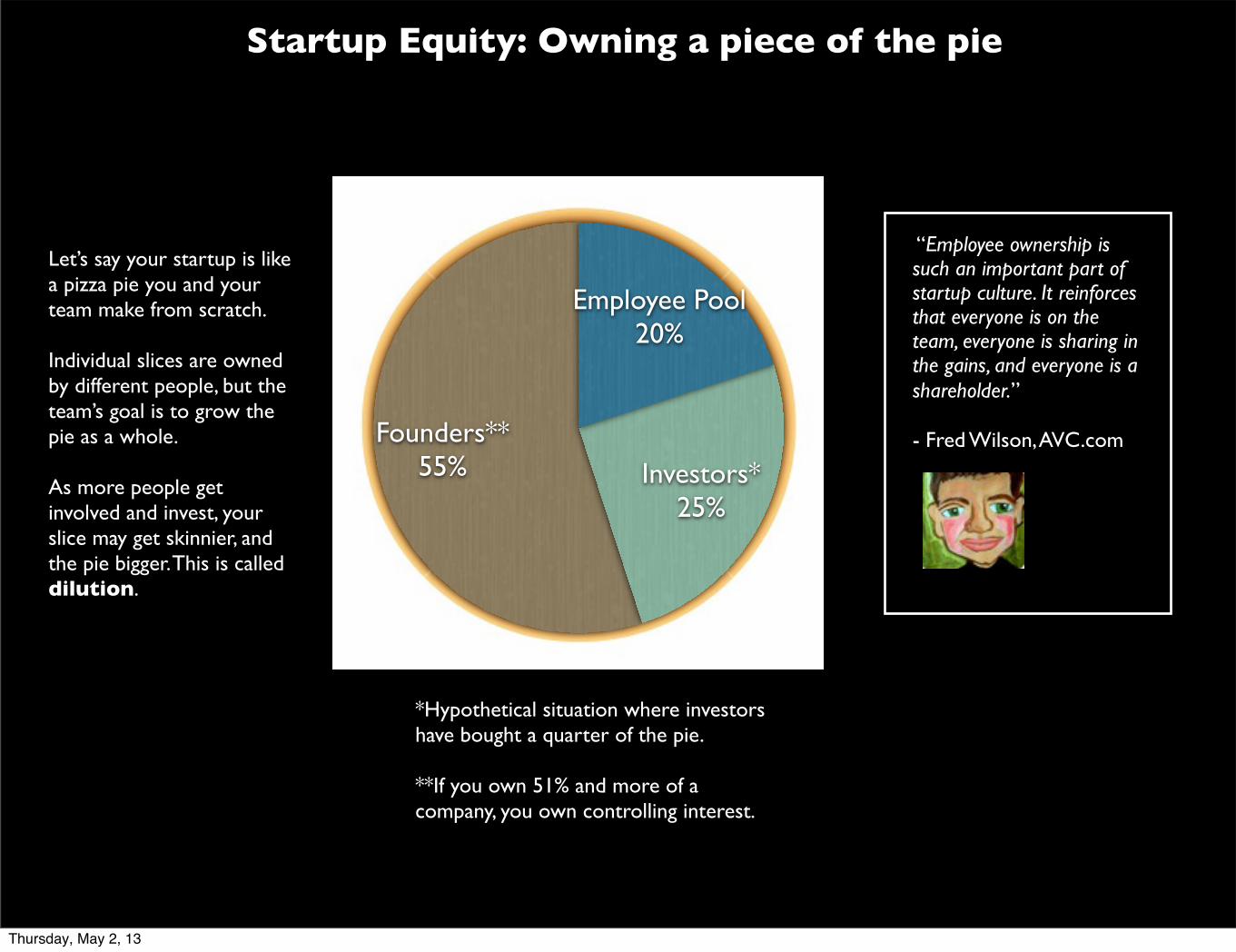

Let’s say your startup is like a pizza pie you and your team make from scratch.

Individual slices are owned by different people, but the team’s goal is to grow the pie as a whole.

As more people get involved and invest, your slice may get skinnier, and the pie bigger. This is called dilution.

“Employee ownership is such an important part of startup culture. It reinforces that everyone is on the team, everyone is sharing in the gains, and everyone is a shareholder.”

- Fred Wilson, AVC.com

Thursday, May 2, 13

Startup Equity: Owning a piece of the pie

Let’s say your startup is like a pizza pie you and your team make from scratch.

Individual slices are owned by different people, but the team’s goal is to grow the pie as a whole.

As more people get involved and invest, your slice may get skinnier, and the pie bigger. This is called dilution.

Founders**55% Investors*

25%

Employee Pool20%

*Hypothetical situation where investors have bought a quarter of the pie.

**If you own 51% and more of a company, you own controlling interest.

“Employee ownership is such an important part of startup culture. It reinforces that everyone is on the team, everyone is sharing in the gains, and everyone is a shareholder.”

- Fred Wilson, AVC.com

Thursday, May 2, 13

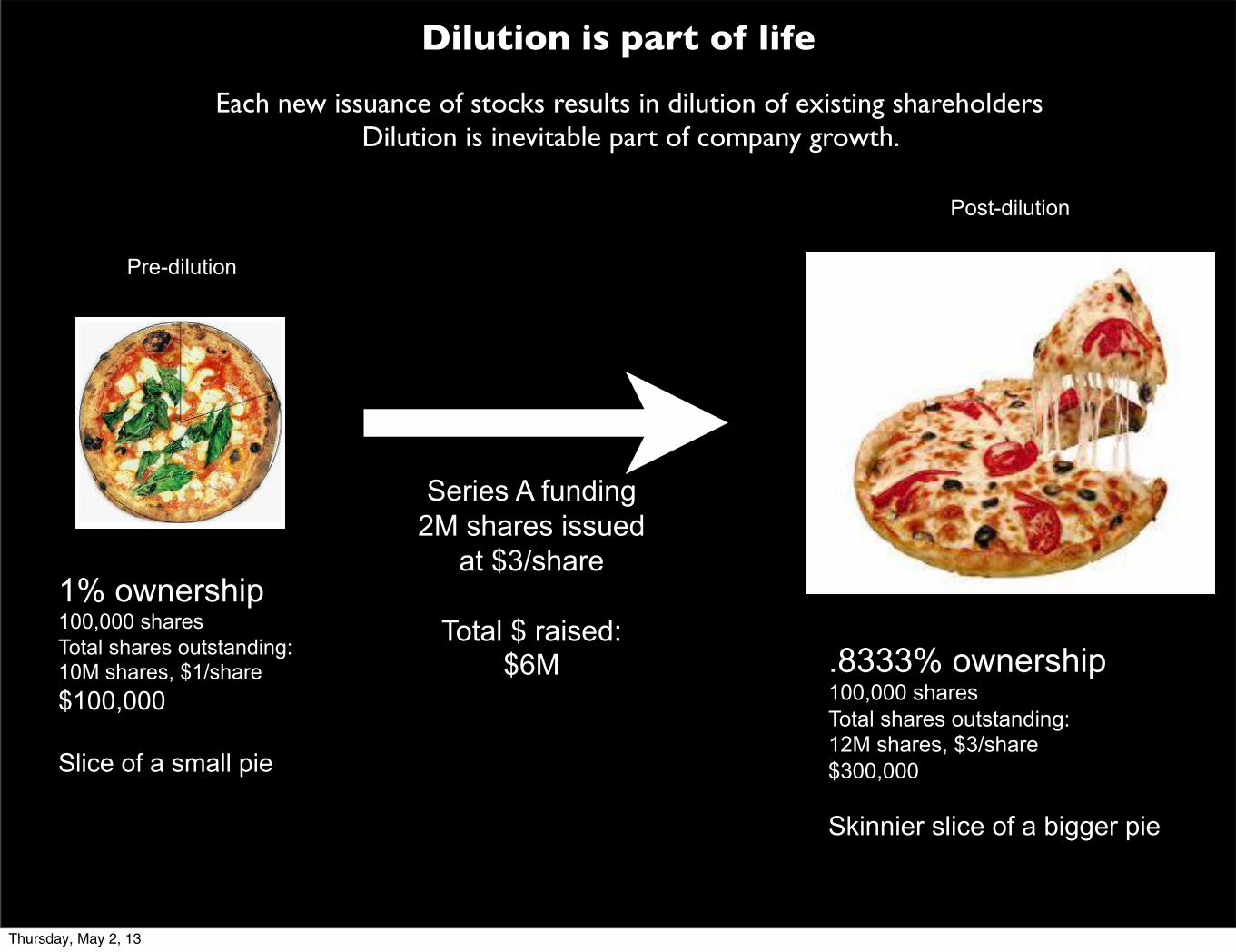

Dilution is part of life

Each new issuance of stocks results in dilution of existing shareholdersDilution is inevitable part of company growth.

Pre-dilution

1% ownership 100,000 shares Total shares outstanding: 10M shares, $1/share $100,000 Slice of a small pie

Series A funding

2M shares issued at $3/share

Total $ raised:

$6M .8333% ownership 100,000 shares Total shares outstanding: 12M shares, $3/share $300,000 Skinnier slice of a bigger pie

Post-dilution

Thursday, May 2, 13

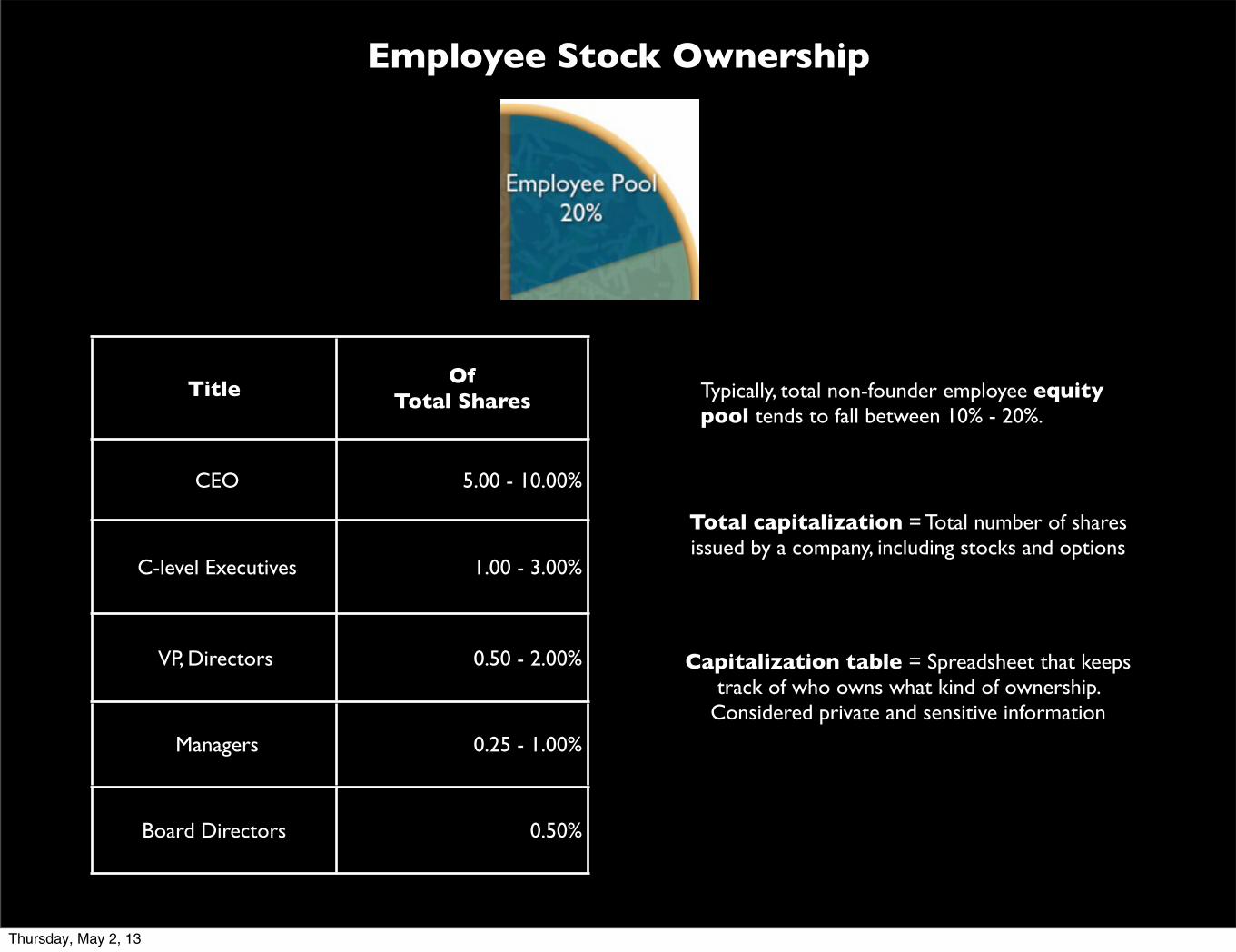

Employee Stock Ownership

Typically, total non-founder employee equity pool tends to fall between 10% - 20%.

TitleOf

Total Shares

CEO 5.00 - 10.00%

C-level Executives 1.00 - 3.00%

VP, Directors 0.50 - 2.00%

Managers 0.25 - 1.00%

Board Directors 0.50%

Total capitalization = Total number of shares issued by a company, including stocks and options

Capitalization table = Spreadsheet that keeps track of who owns what kind of ownership.

Considered private and sensitive information

Thursday, May 2, 13

Set you expectations right

$ Cash Comp

Equity CompAt a smaller, younger, startup with less funding

$ Cash Comp

Equity Comp

At a bigger, more established company after several rounds of fundraising

Thursday, May 2, 13

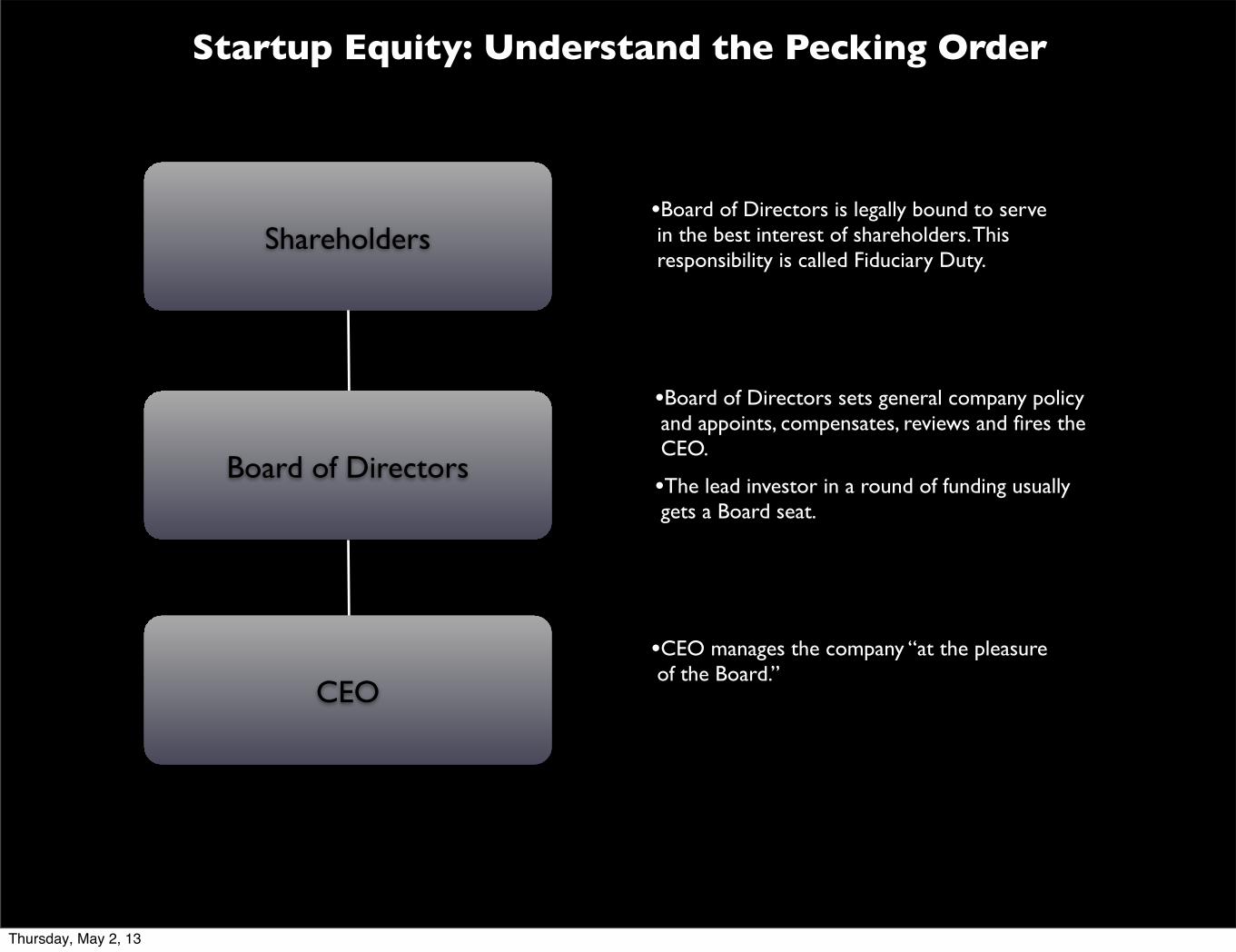

Startup Equity: Understand the Pecking Order

Shareholders

Board of Directors

CEO

•Board of Directors is legally bound to serve in the best interest of shareholders. This responsibility is called Fiduciary Duty.

•Board of Directors sets general company policy and appoints, compensates, reviews and fires the CEO.

•The lead investor in a round of funding usually gets a Board seat.

•CEO manages the company “at the pleasure of the Board.”

Thursday, May 2, 13

Startup Equity: Common vs. Preferred

Who

gets them?

What

kind of rights?

When

are they issued?

Why

are they issued?

How

about IPO?

Founders, employees, some board members

Outside investors such as VCs

At incorporation and at the discretion of the Board of Directors

When investors buy company shares. They usually pay a premium over Common for Preferred. Named Series A, B, C, D, etc.

To retain and motivate employees, in lieu of cash bonus, aka “Sweat Equity”

To raise capital for company growth, etc.aka “Cash Equity”

To attend shareholder meetings Can include board seat, Preference, or the right to get paid before common, right of first refusal, anti-dilution rights, right to convert to Common

Equal footing as Preferred Shares Preferred rights go away

Thursday, May 2, 13

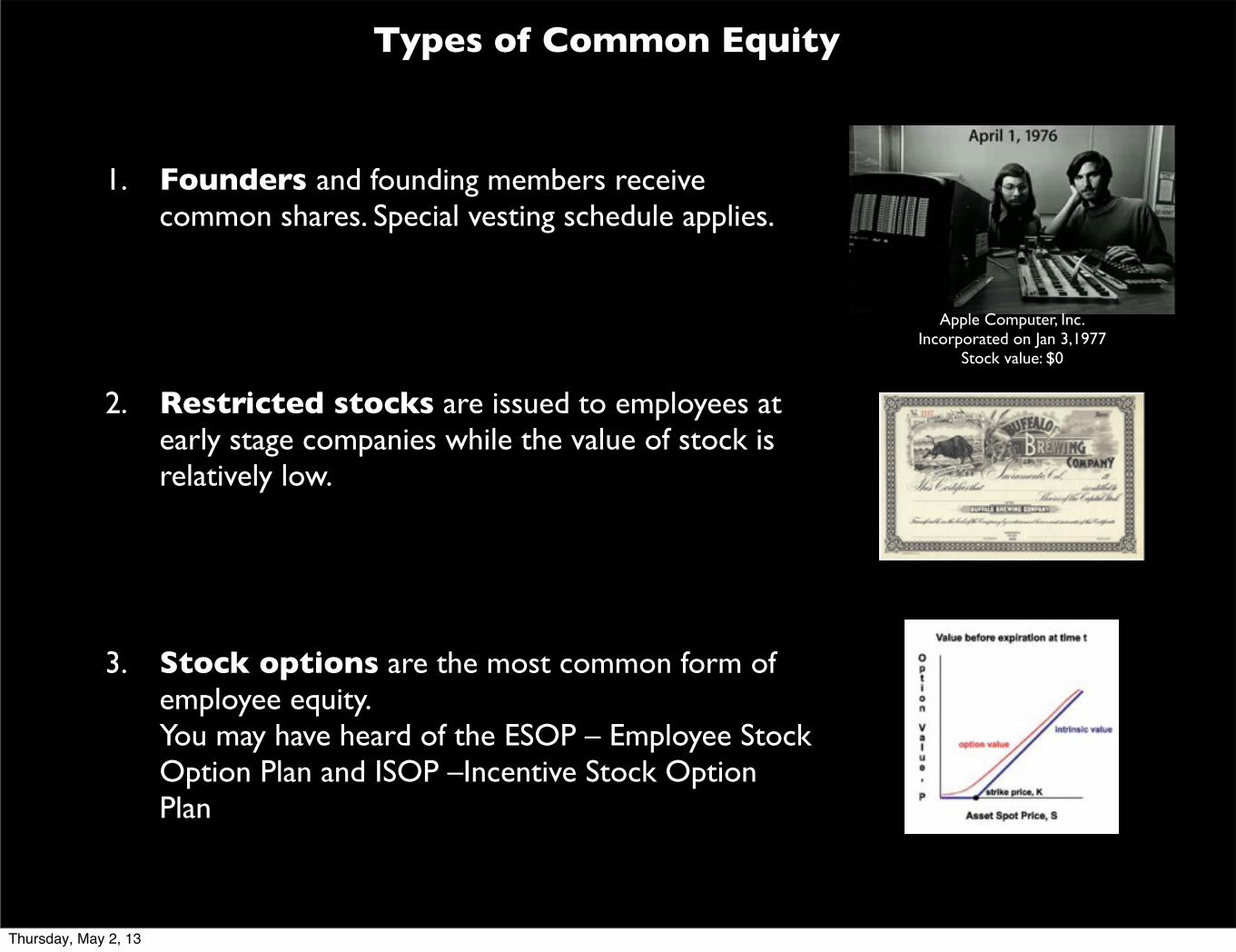

1. Founders and founding members receive common shares. Special vesting schedule applies.

2. Restricted stocks are issued to employees at early stage companies while the value of stock is relatively low.

3. Stock options are the most common form of employee equity. You may have heard of the ESOP – Employee Stock Option Plan and ISOP –Incentive Stock Option Plan

Types of Common Equity

Apple Computer, Inc.Incorporated on Jan 3,1977

Stock value: $0

Thursday, May 2, 13

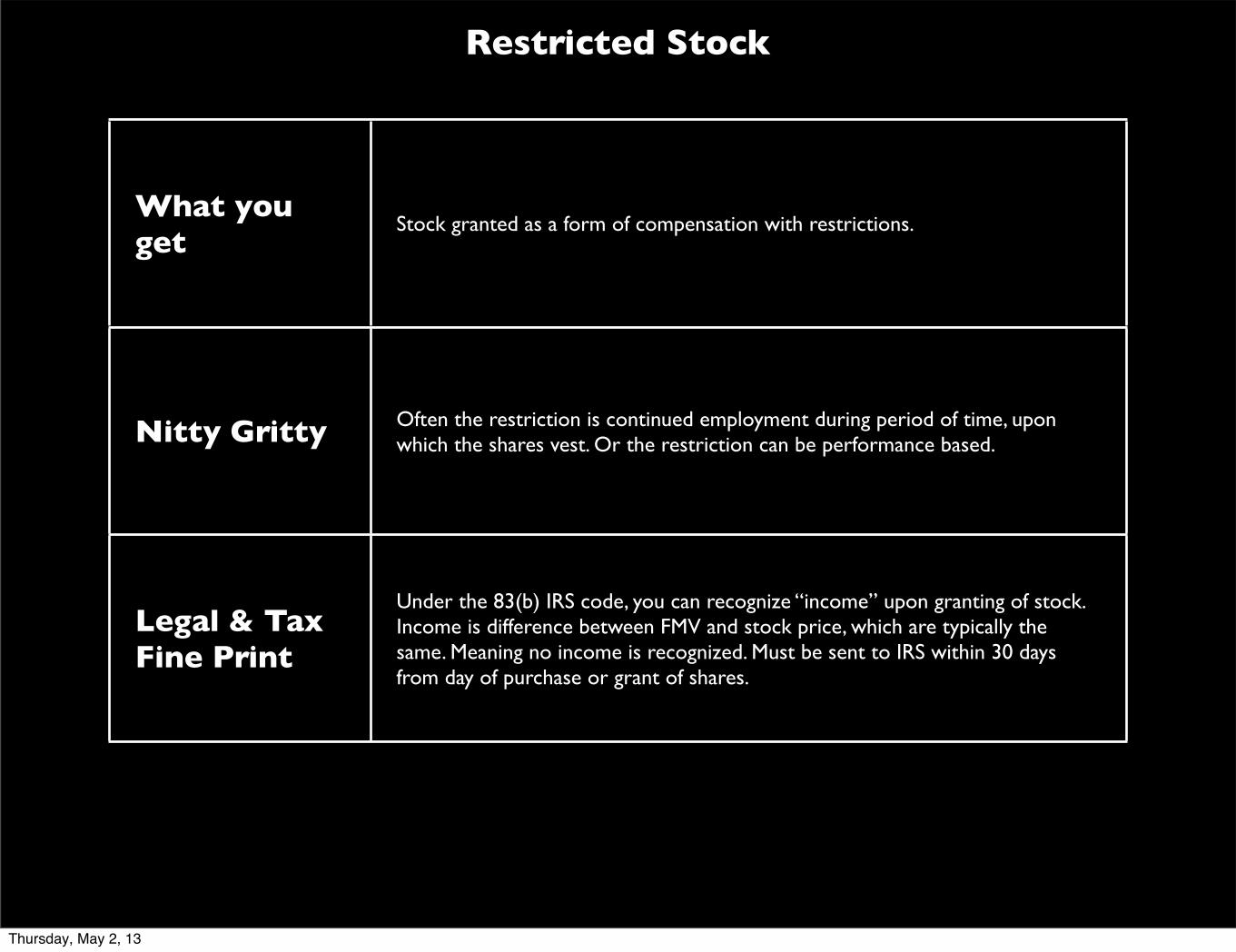

Restricted Stock

What you get

Stock granted as a form of compensation with restrictions.

Nitty Gritty Often the restriction is continued employment during period of time, upon which the shares vest. Or the restriction can be performance based.

Legal & Tax Fine Print

Under the 83(b) IRS code, you can recognize “income” upon granting of stock. Income is difference between FMV and stock price, which are typically the same. Meaning no income is recognized. Must be sent to IRS within 30 days from day of purchase or grant of shares.

Thursday, May 2, 13

Vesting Schedule

4 year vesting with 1 year cliff is common.

1 year cliff means you don’t vest during the 1st year. If you leave during this period, you leave with no equity.

Unvested equity may be repurchased by the company and returned to the employee pool.

Idea is to avoid a “hit and run” situation and to retain talented employees.

Oops

27.1%

+1 mo.

Day 1 1st year 2nd year 3rd year 4th year

0% 25% 50% 75% 100%

0 2,5002,710

5,000 7,500 10,000Vested Shares

Generally, option strike price will not change throughout vesting schedule.

Thursday, May 2, 13

Thursday, May 2, 13

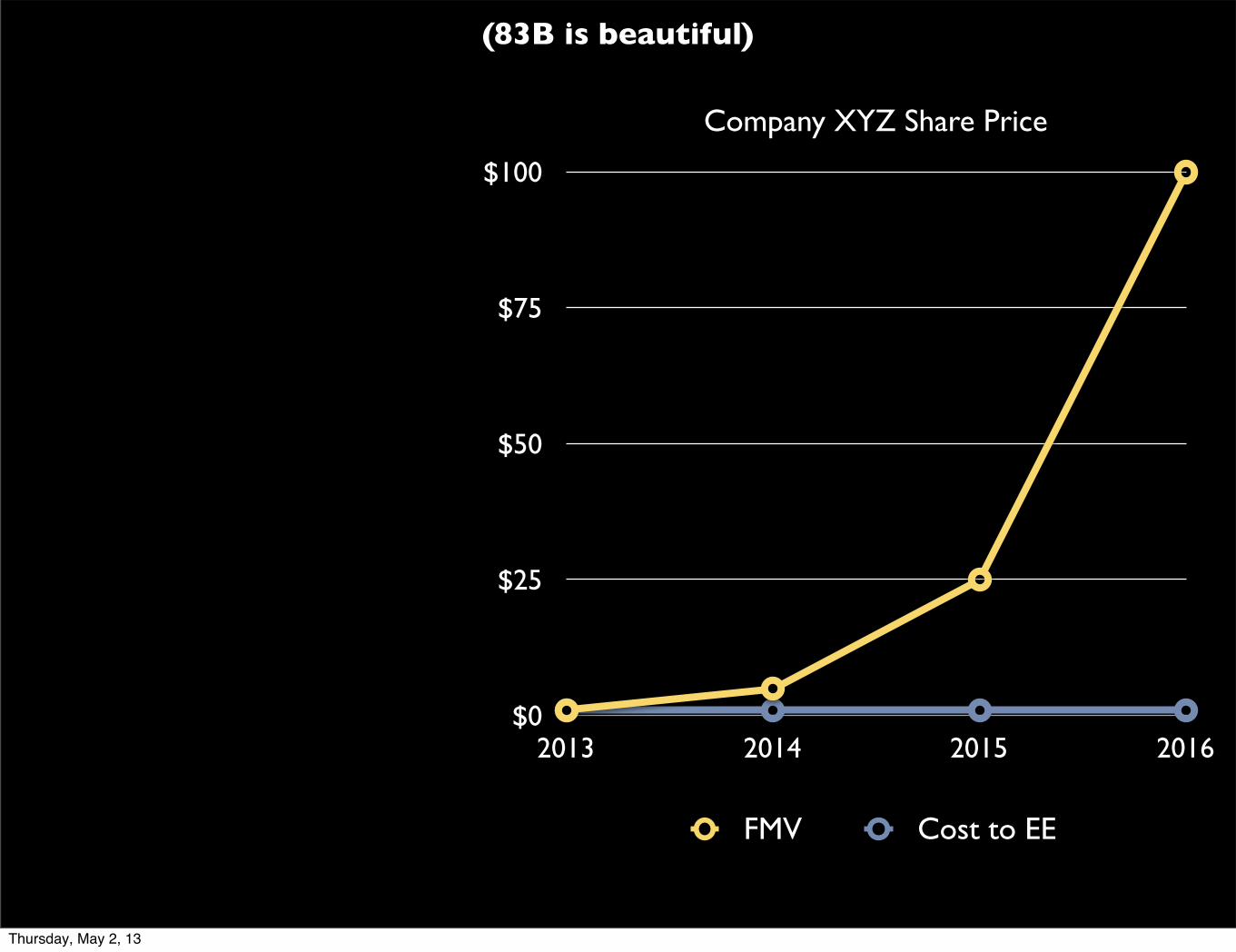

(83B is beautiful)

Thursday, May 2, 13

FMV Cost to EE

(83B is beautiful)

Thursday, May 2, 13

$0

$25

$50

$75

$100

2013 2014 2015 2016

Company XYZ Share Price

FMV Cost to EE

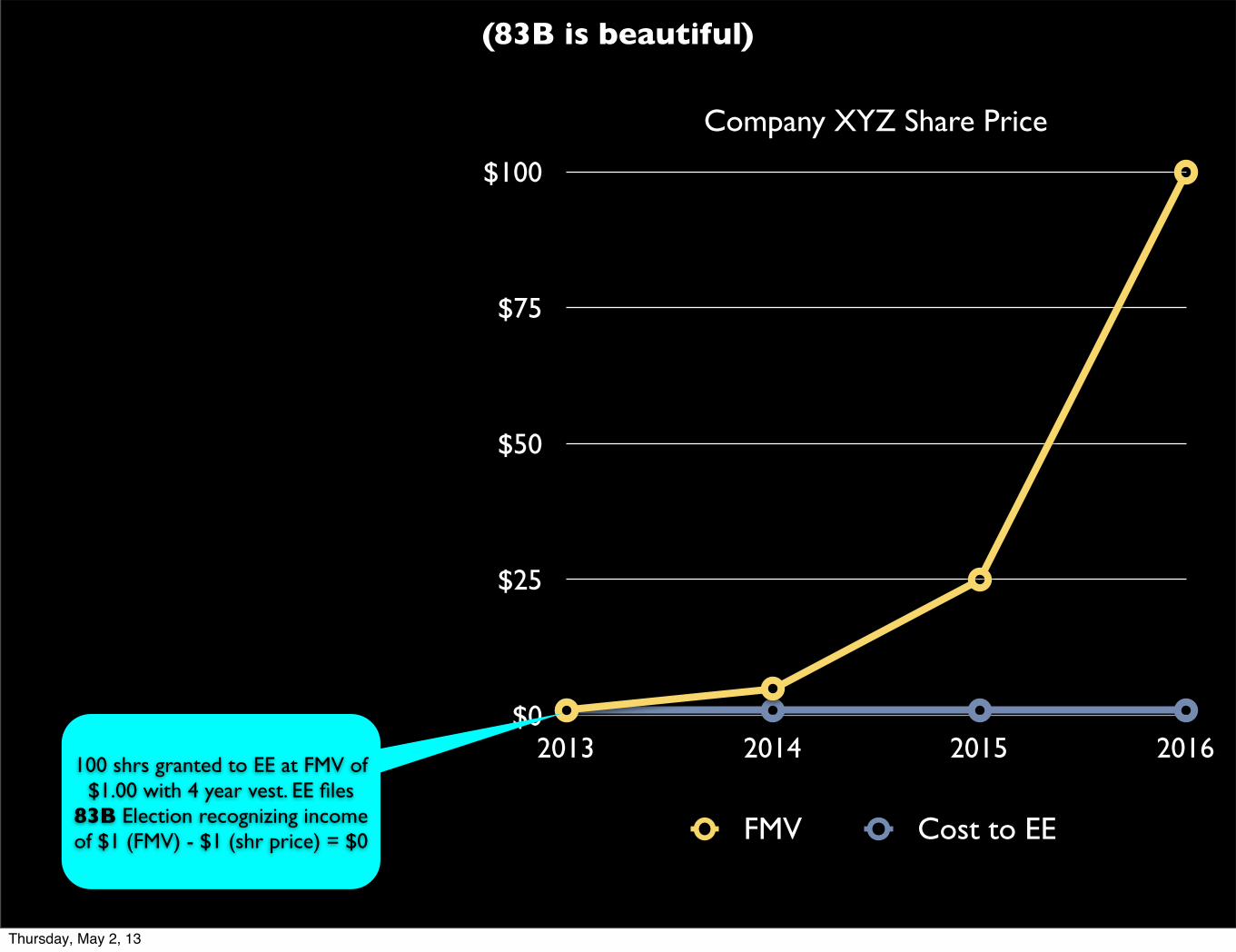

(83B is beautiful)

Thursday, May 2, 13

$0

$25

$50

$75

$100

2013 2014 2015 2016

Company XYZ Share Price

FMV Cost to EE

100 shrs granted to EE at FMV of $1.00 with 4 year vest. EE files

83B Election recognizing income of $1 (FMV) - $1 (shr price) = $0

(83B is beautiful)

Thursday, May 2, 13

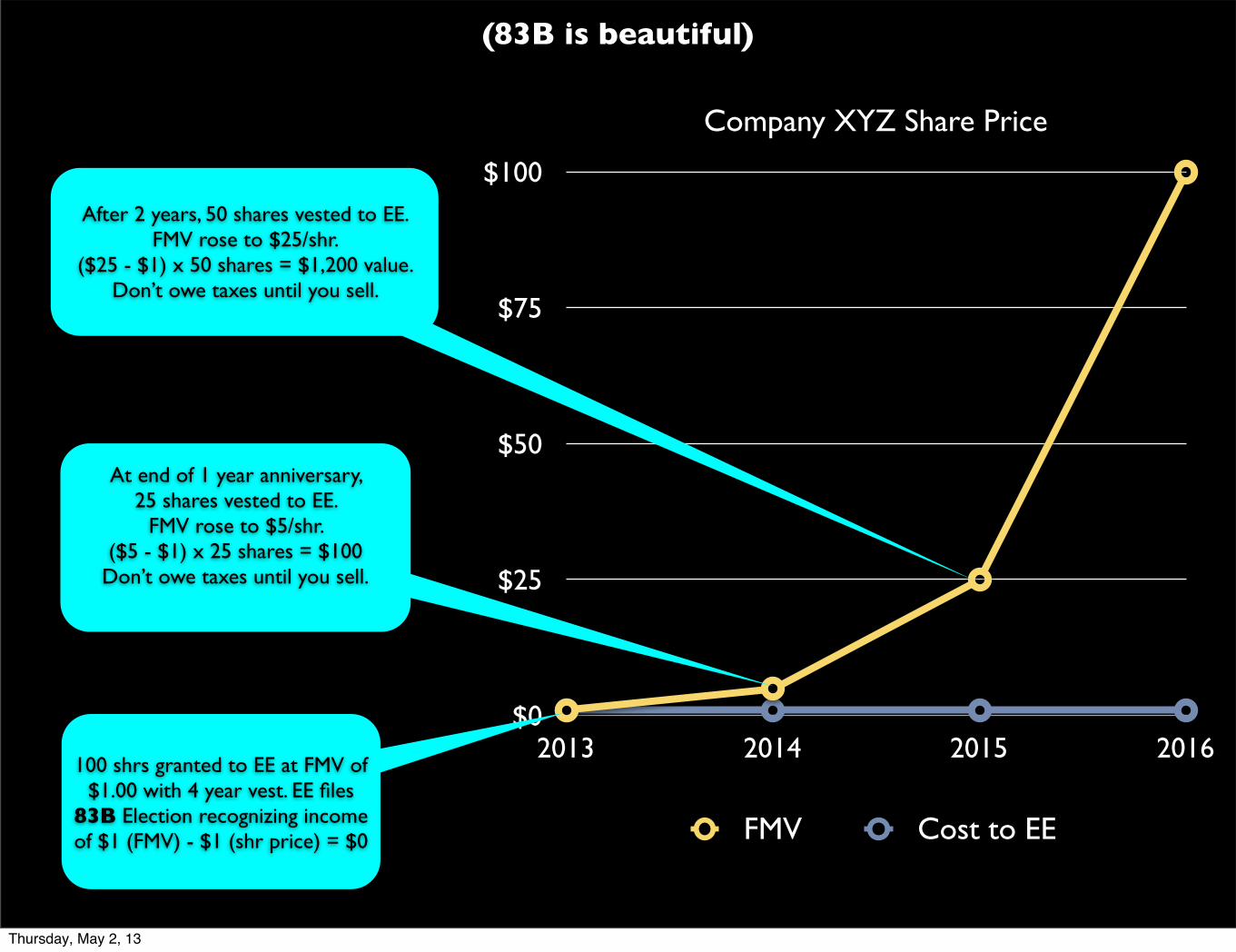

$0

$25

$50

$75

$100

2013 2014 2015 2016

Company XYZ Share Price

FMV Cost to EE

100 shrs granted to EE at FMV of $1.00 with 4 year vest. EE files

83B Election recognizing income of $1 (FMV) - $1 (shr price) = $0

At end of 1 year anniversary, 25 shares vested to EE.

FMV rose to $5/shr. ($5 - $1) x 25 shares = $100

Don’t owe taxes until you sell.

(83B is beautiful)

Thursday, May 2, 13

$0

$25

$50

$75

$100

2013 2014 2015 2016

Company XYZ Share Price

FMV Cost to EE

100 shrs granted to EE at FMV of $1.00 with 4 year vest. EE files

83B Election recognizing income of $1 (FMV) - $1 (shr price) = $0

At end of 1 year anniversary, 25 shares vested to EE.

FMV rose to $5/shr. ($5 - $1) x 25 shares = $100

Don’t owe taxes until you sell.

After 2 years, 50 shares vested to EE. FMV rose to $25/shr.

($25 - $1) x 50 shares = $1,200 value. Don’t owe taxes until you sell.

(83B is beautiful)

Thursday, May 2, 13

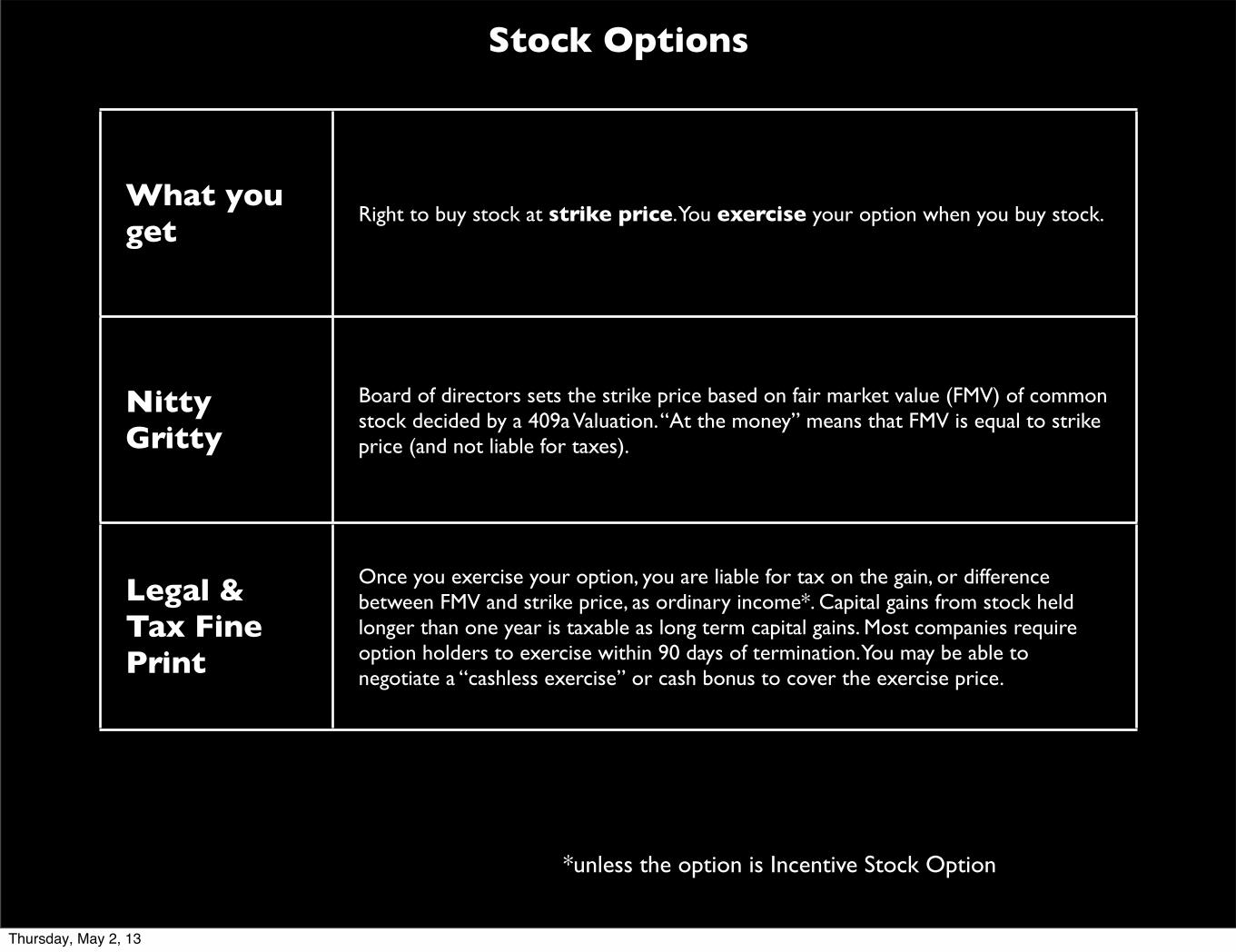

Stock Options

What you get

Right to buy stock at strike price. You exercise your option when you buy stock.

Nitty Gritty

Board of directors sets the strike price based on fair market value (FMV) of common stock decided by a 409a Valuation. “At the money” means that FMV is equal to strike price (and not liable for taxes).

Legal & Tax Fine Print

Once you exercise your option, you are liable for tax on the gain, or difference between FMV and strike price, as ordinary income*. Capital gains from stock held longer than one year is taxable as long term capital gains. Most companies require option holders to exercise within 90 days of termination. You may be able to negotiate a “cashless exercise” or cash bonus to cover the exercise price.

*unless the option is Incentive Stock Option

Thursday, May 2, 13

Incentive Stock Option

Incentive stock options (ISOs), are a type of employee stock option that can be granted only to employees and confer a U.S. tax benefit.

The tax benefit is that on exercise the individual does not have to pay ordinary income tax (nor employment taxes) on the difference between the exercise price and the fair market value of the shares issued (however, the holder may have to pay U.S. alternative minimum tax instead).

Instead, if the shares are held for 1 year from the date of exercise and 2 years from the date of grant, then the profit (if any) made on sale of the shares is taxed as long-term capital gain. Long-term capital gain is taxed in the U.S. at lower rates than ordinary income.*

*straight out of Wikipedia

Thursday, May 2, 13

Thursday, May 2, 13

$0

$15

$30

$45

$60

$75

$90

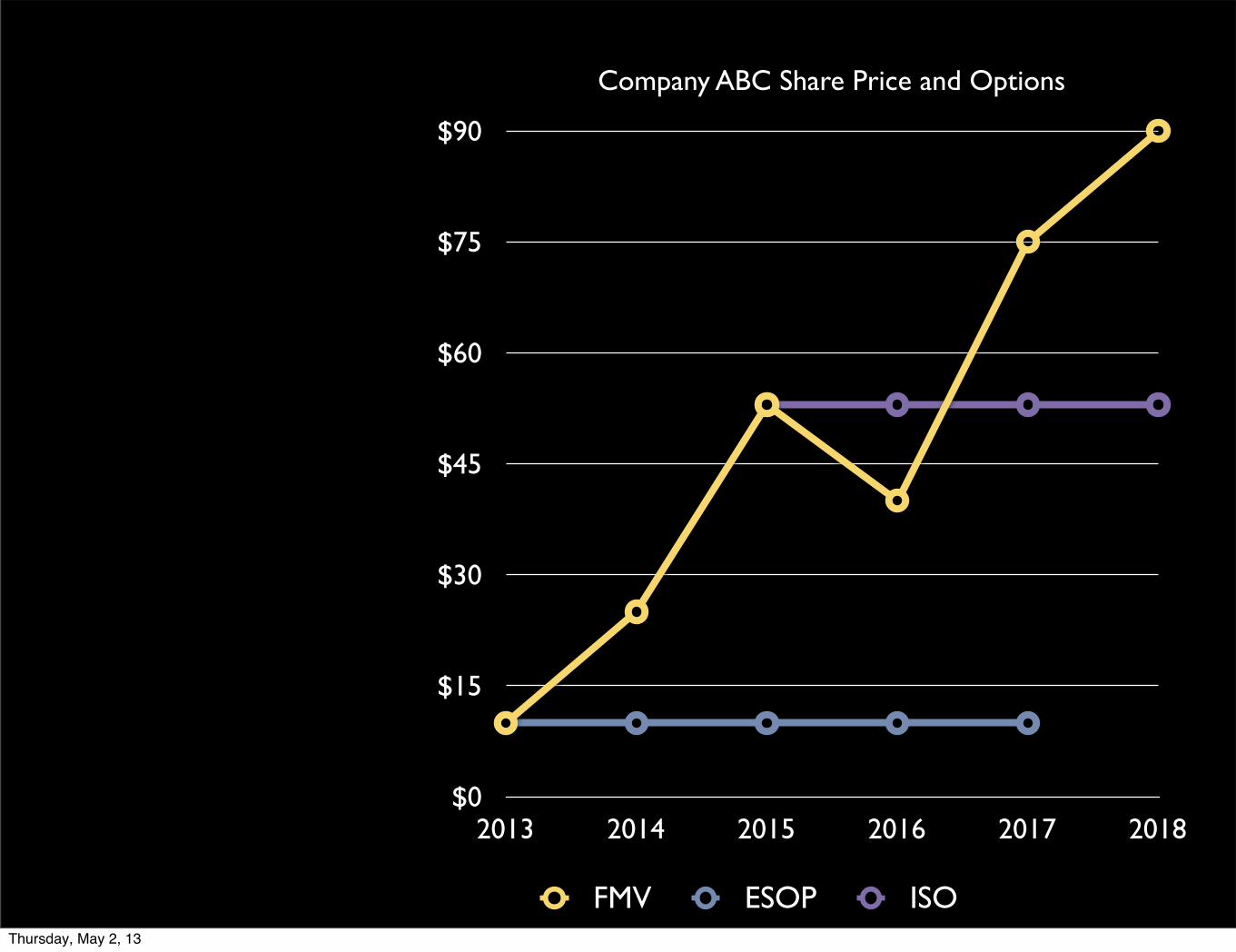

2013 2014 2015 2016 2017 2018

Company ABC Share Price and Options

FMV ESOP ISOThursday, May 2, 13

$0

$15

$30

$45

$60

$75

$90

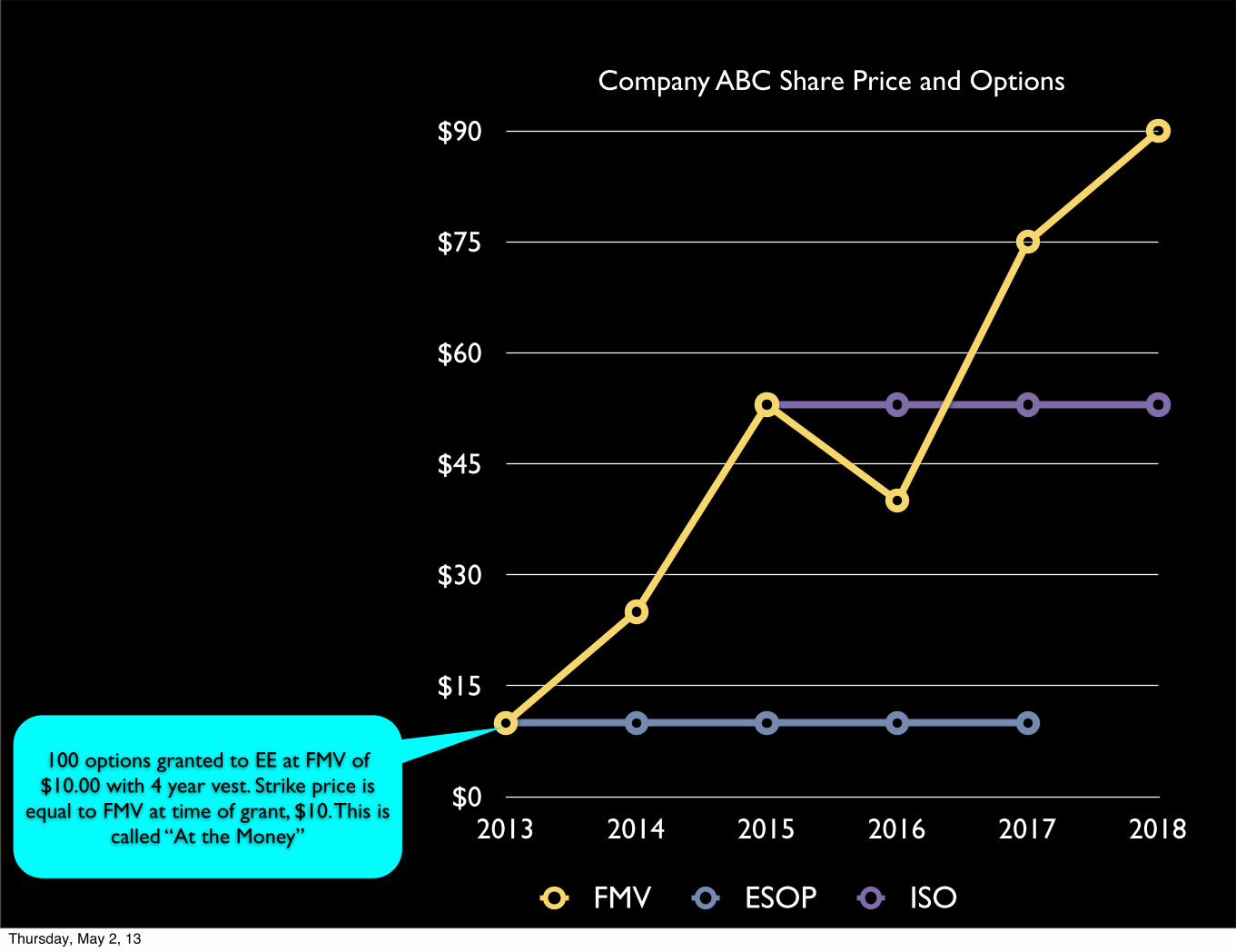

2013 2014 2015 2016 2017 2018

Company ABC Share Price and Options

FMV ESOP ISO

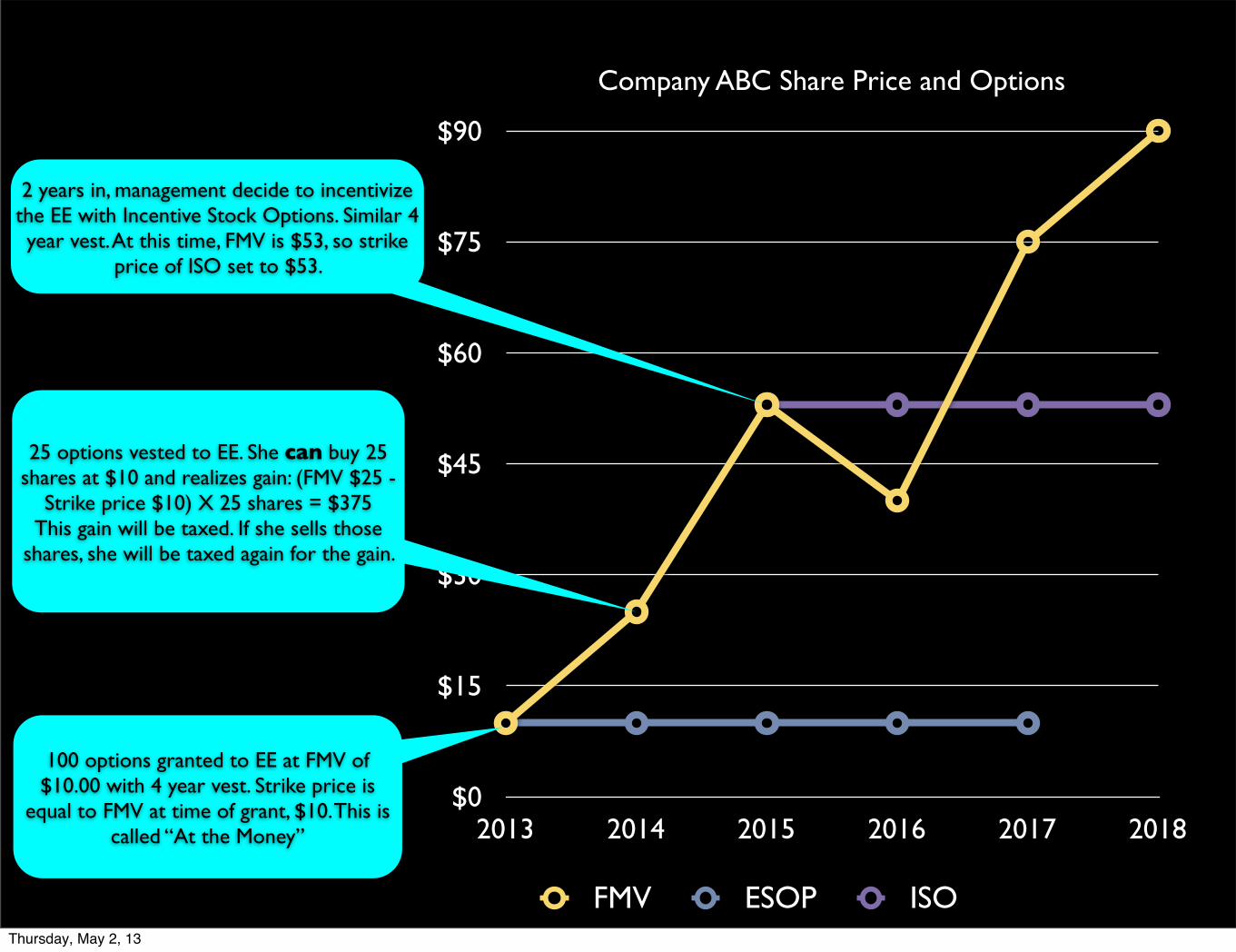

100 options granted to EE at FMV of $10.00 with 4 year vest. Strike price is

equal to FMV at time of grant, $10. This is called “At the Money”

Thursday, May 2, 13

$0

$15

$30

$45

$60

$75

$90

2013 2014 2015 2016 2017 2018

Company ABC Share Price and Options

FMV ESOP ISO

100 options granted to EE at FMV of $10.00 with 4 year vest. Strike price is

equal to FMV at time of grant, $10. This is called “At the Money”

25 options vested to EE. She can buy 25 shares at $10 and realizes gain: (FMV $25 -

Strike price $10) X 25 shares = $375This gain will be taxed. If she sells those

shares, she will be taxed again for the gain.

Thursday, May 2, 13

$0

$15

$30

$45

$60

$75

$90

2013 2014 2015 2016 2017 2018

Company ABC Share Price and Options

FMV ESOP ISO

100 options granted to EE at FMV of $10.00 with 4 year vest. Strike price is

equal to FMV at time of grant, $10. This is called “At the Money”

25 options vested to EE. She can buy 25 shares at $10 and realizes gain: (FMV $25 -

Strike price $10) X 25 shares = $375This gain will be taxed. If she sells those

shares, she will be taxed again for the gain.

2 years in, management decide to incentivize the EE with Incentive Stock Options. Similar 4 year vest. At this time, FMV is $53, so strike

price of ISO set to $53.

Thursday, May 2, 13

$0

$15

$30

$45

$60

$75

$90

2013 2014 2015 2016 2017 2018

Company ABC Share Price and Options

FMV ESOP ISO

100 options granted to EE at FMV of $10.00 with 4 year vest. Strike price is

equal to FMV at time of grant, $10. This is called “At the Money”

25 options vested to EE. She can buy 25 shares at $10 and realizes gain: (FMV $25 -

Strike price $10) X 25 shares = $375This gain will be taxed. If she sells those

shares, she will be taxed again for the gain.

2 years in, management decide to incentivize the EE with Incentive Stock Options. Similar 4 year vest. At this time, FMV is $53, so strike

price of ISO set to $53.

When FMV falls under strike price, it’s called “under water”

Thursday, May 2, 13

Startup Equity RECAP: More ART than SCIENCE but still need to ASK and do the MATH

Thursday, May 2, 13

Startup Equity RECAP: More ART than SCIENCE but still need to ASK and do the MATH

Before joining a startup, ask

• Is this the right team and company for my success?

•What is my percentage of ownership?

➡ # shares you own / total shares issued

•How long is my vesting schedule?

➡ 4 years with 1 year cliff is standard

•What are tax implications?

➡Restricted stock: make 83B elections

➡Option holders: liable for capital gains at exercise and when sold

•What is total company capitalization?

•What is the estimated valuation at exit?

•What do I need to do when I leave?

If you’re a founder or prospective employee,

•Research market rate salary and equity comp

➡See appendices for references

•Read the partnership and employment agreements

•Negotiate like a business person

•Consult a lawyer or tax accountant

Thursday, May 2, 13

Startup Equity: More ART than SCIENCE but still need to do the MATH

1) Ownership = # Shares Granted to You Total Capitalization

Formulas Example

1) 1% = 0.1M Shares Granted10M Total Shares Outstanding

2) Dilution Factor = (# Your Future Shares + Future Investor Shares)

Total Cap. + # Your Future + Future Investor Shares

2) 0.17% = (0.05M +2M) (10M+0.1M+2M)

1% - 0.17% = 0.83% New Ownership

3) Your Payday at Exit* = (Your Ownership X Company Exit Price)

– (Total Exercise Price)

3) $99K* = (0.83% X $30M) - ($150K)

*Assuming $1 strike price, BEFORE taxes, very rough est.

Thursday, May 2, 13

Sources- Andy Payne, Startup Equity for Employees: http://www.payne.org/index.php/Startup_Equity_For_Employees

- Brad Feld, Blog archive on Term Sheets:

http://www.feld.com/wp/archives/2005/08/term-sheet-series-wrap-up.html

- Chris Dixon, The One Number You Should Know About Your Equity http://cdixon.org/2009/08/27/the-one-number-you-should-know-about-your-equity-grant/

- Fred Wilson, MBA Monday Series on Equity: http://www.avc.com/a_vc/2010/09/employee-equity.html

http://www.avc.com/a_vc/2008/11/restricted-stoc.html

- How Stuff Works, Stock Options:

http://money.howstuffworks.com/personal-finance/financial-planning/stock-options1.htm

- Infochachkie, What The Heck Are My Startup Stock Options Worth?! Seven Questions You Should Ask Before Joining A Startup: http://infochachkie.com/options/

- Paul Graham, Equity Equation: http://paulgraham.com/equity.html

- Pop History of DIg, Apple Rising: 1976 - 1985: http://www.pophistorydig.com/?tag=apple-computer-ipo

- Startup Company Lawyer, What is an 83b Election?

http://www.startupcompanylawyer.com/2008/02/15/what-is-an-83b-election/

- Wealthfront, Manage Your Tech Career: https://blog.wealthfront.com/startup-employee-equity-compensation/

- Wealthfront, The 12 Crucial Questions About Stock Options: https://blog.wealthfront.com/stock-options-package-valuation/

- Wikipedia, Restricted Stock: http://en.wikipedia.org/wiki/Restricted_stock

Thank you!Thursday, May 2, 13

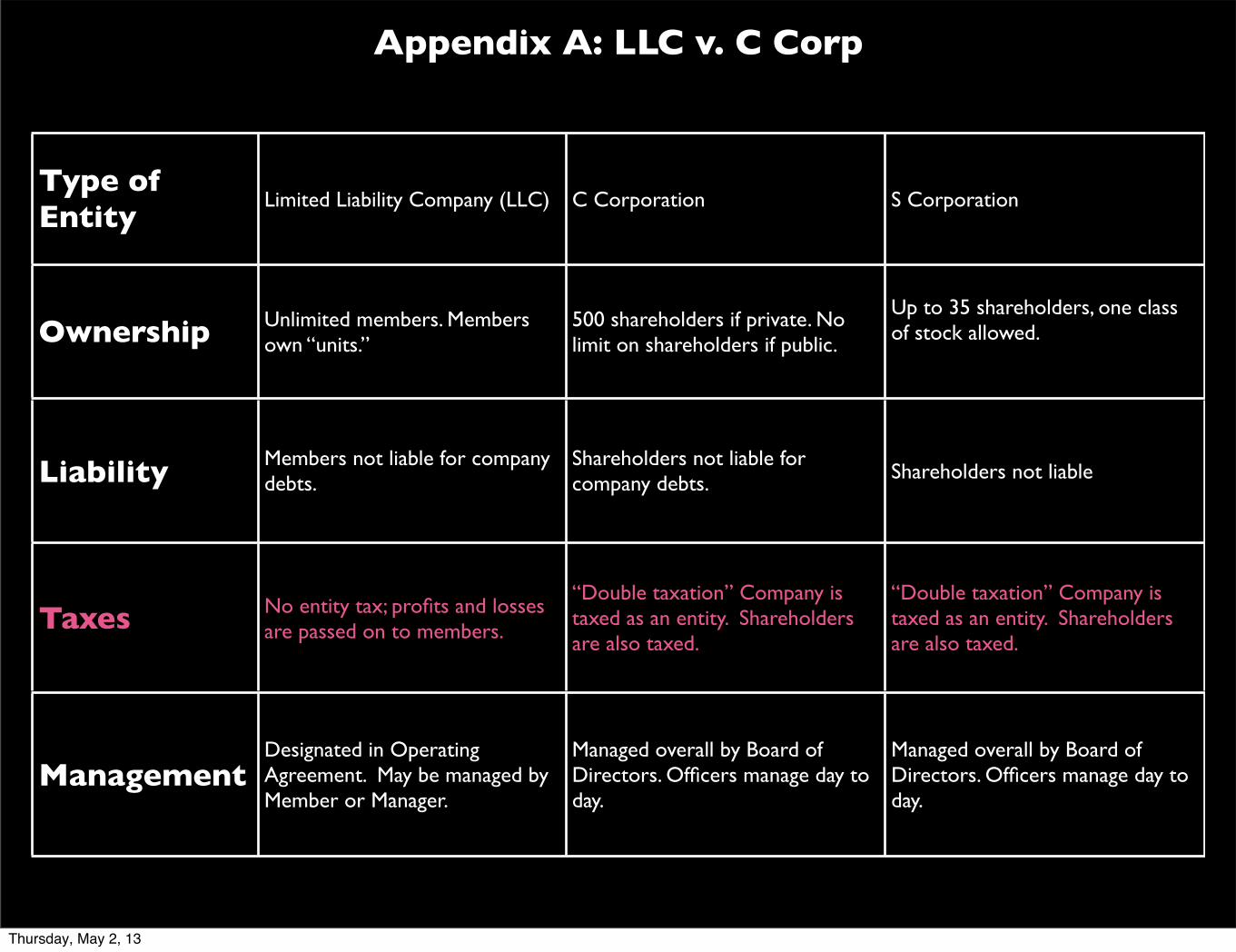

Appendix A: LLC v. C Corp

Thursday, May 2, 13

Appendix A: LLC v. C Corp

Type of Entity

Limited Liability Company (LLC) C Corporation S Corporation

Ownership Unlimited members. Members own “units.”

500 shareholders if private. No limit on shareholders if public.

Up to 35 shareholders, one class of stock allowed.

Liability Members not liable for company debts.

Shareholders not liable for company debts. Shareholders not liable

Taxes No entity tax; profits and losses are passed on to members.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

ManagementDesignated in Operating Agreement. May be managed by Member or Manager.

Managed overall by Board of Directors. Officers manage day to day.

Managed overall by Board of Directors. Officers manage day to day.

Thursday, May 2, 13

Appendix A: LLC v. C Corp

Type of Entity

Limited Liability Company (LLC) C Corporation S Corporation

Ownership Unlimited members. Members own “units.”

500 shareholders if private. No limit on shareholders if public.

Up to 35 shareholders, one class of stock allowed.

Liability Members not liable for company debts.

Shareholders not liable for company debts. Shareholders not liable

Taxes No entity tax; profits and losses are passed on to members.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

ManagementDesignated in Operating Agreement. May be managed by Member or Manager.

Managed overall by Board of Directors. Officers manage day to day.

Managed overall by Board of Directors. Officers manage day to day.

Thursday, May 2, 13

Appendix A: LLC v. C Corp

Type of Entity

Limited Liability Company (LLC) C Corporation S Corporation

Ownership Unlimited members. Members own “units.”

500 shareholders if private. No limit on shareholders if public.

Up to 35 shareholders, one class of stock allowed.

Liability Members not liable for company debts.

Shareholders not liable for company debts. Shareholders not liable

Taxes No entity tax; profits and losses are passed on to members.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

ManagementDesignated in Operating Agreement. May be managed by Member or Manager.

Managed overall by Board of Directors. Officers manage day to day.

Managed overall by Board of Directors. Officers manage day to day.

Thursday, May 2, 13

Appendix A: LLC v. C Corp

Type of Entity

Limited Liability Company (LLC) C Corporation S Corporation

Ownership Unlimited members. Members own “units.”

500 shareholders if private. No limit on shareholders if public.

Up to 35 shareholders, one class of stock allowed.

Liability Members not liable for company debts.

Shareholders not liable for company debts. Shareholders not liable

Taxes No entity tax; profits and losses are passed on to members.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

ManagementDesignated in Operating Agreement. May be managed by Member or Manager.

Managed overall by Board of Directors. Officers manage day to day.

Managed overall by Board of Directors. Officers manage day to day.

Thursday, May 2, 13

ACME, LLCAnnual net profit: $100M

No corp tax

Appendix B: LLC Tax Passthrough

•Members taxed for ACME’s profit (or loss) proportionately•Members receive K1 tax form (and tax assistance from entity, depending on terms of agreement)

A:10%$10M

B:10%$10M

C:80%$80M

Tax Liability Tax Liability

Thursday, May 2, 13

ACME, Inc.Annual profit: $100M

Corp tax: $35M Net profit: $65M

dividends paid out to shareholders(taxed on individual level)

Appendix C: C Corp “Double Taxation”

•Both ACME, Inc. and shareholders taxed •No tax assistance from entity to shareholders

dividends dividends

Thursday, May 2, 13

Appendix D: Recommended Online Resources

• Check out Anonymous Startup Salaries, Stock Options and Equity on Ackwire.com

• Check out Fred Wilson’s Cap Table Template on Google Docs

Thursday, May 2, 13

Appendix E: Recommended Online Resources

• Check out Patrick McKenzie’s Salary Negotiation: Make More Money, Be More

• Check out David Weekly’s An Intro to Stock Options

Thursday, May 2, 13

![Startup Advice 101 [FRENCH]](https://img.dokumen.tips/doc/110x75/555dff97d8b42a3f618b5325/startup-advice-101-french.jpg)