Embed Size (px)

Citation preview

Solar Electric Dealers 2004:

Dynamic Markets, Significant Opportunities,

Challenging Threats

Meredith McClintock

Coast Hills Partners

158 Pinon Drive Portola Valley, California 94028

[email protected] (650) 255 -1828

www.coasthillspartners.com

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

Here’s what solar industry leaders are saying about Solar Dealers 2004:

“It is by far the most comprehensive report that I have ever seen about the installation side of our industry… It’s rare that I receive an industry report that I actually download, read through, and highlight.”

-- Barry Cinnamon, President, Akeena Solar

“I found it well researched and informative.” -- Gary T. Gerber, President, Sun Light & Power Company

“…very comprehensive and very well done… [I]t was gratifying to have my assumptions validated with such good data.” -- Tom McCalmont, President, REgrid Power

“Bang on with a host of points… There is ‘coaching’ value in this document.”

-- Louis A. Regaud, Founder, Halus Power Systems

“A trenchant analysis. Useful and provocative. Well done!”

-- David Hughes, President, Affordable Solar Group, LLC

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 2

-- David Hughes, Affordable Solar Group, LLC

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

Contents

I. Executive Summary .......................................................... 6

The Market 6

The Companies 7

The Customers & the Market 8

Competitive Dynamics 10

Pricing & Cost Structure 11

Marketing 12

Recommendations 12

Strategic 12

Policy 14

Further Research 14

II. Acknowledgements........................................................ 16

III. Company Profiles.......................................................... 17

Definition of a Solar Electric Dealer 17

Company Representatives 17

Ages of Companies 18

Revenues 20

Market Segments Served 22

Distribution Channels 23

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 3

Geographic Coverage 25

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

Summary and Conclusions 28

IV. Customer Profiles ......................................................... 29

Residential Customer Attributes 29

Target Residential Customer Motivations 31

Commercial Customer Attributes 35

Target Commercial Customer Motivations 38

The Bay Area Customer Base as Representative 39

Summary and Conclusions 40

V. Market & Trends ............................................................ 42

The Solar Electric Market 42

Business Conditions & Future Expectations 43

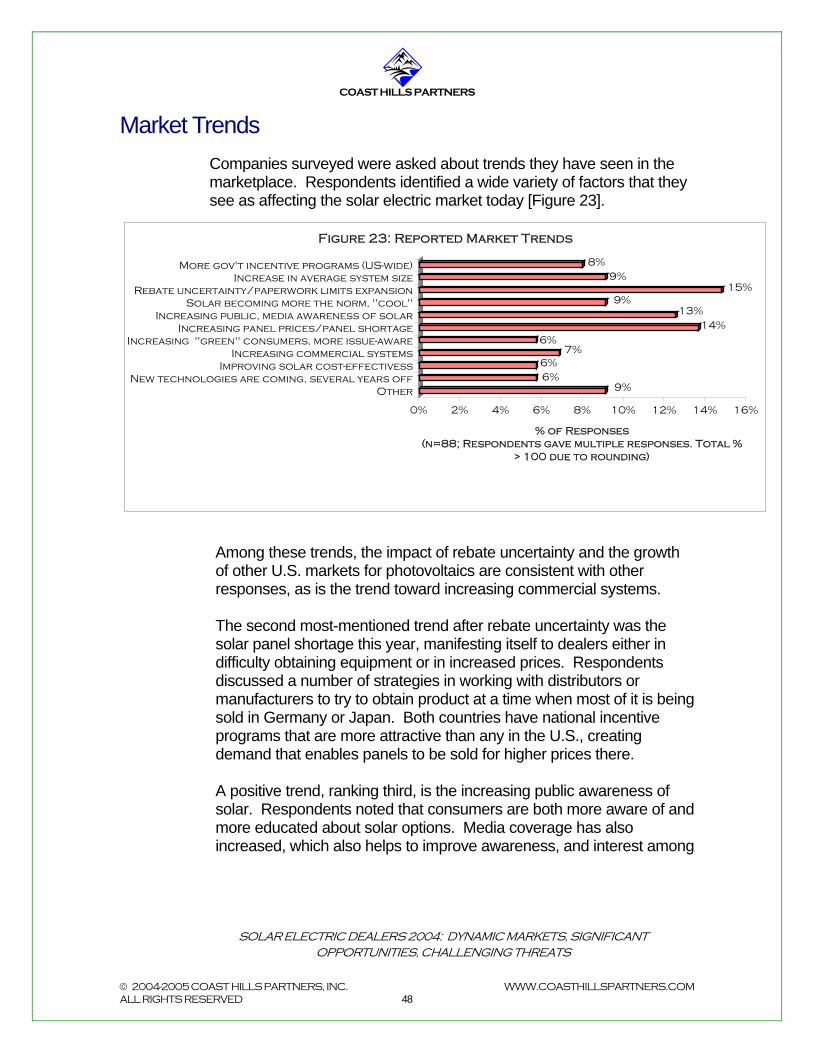

Market Trends 48

Impact of Electricity & Oil Price Volatility on Demand 50

Impact on Businesses if Incentives are Phased Out 52

Opportunities and Threats 53

Summary and Conclusions 56

VI. Company Approaches to Growth ................................. 57

Recent Growth Rates 57

Growth Strategies 60

Summary and Conclusions 65

VII. Competition.................................................................. 66

Competitors Identified by Respondents 66

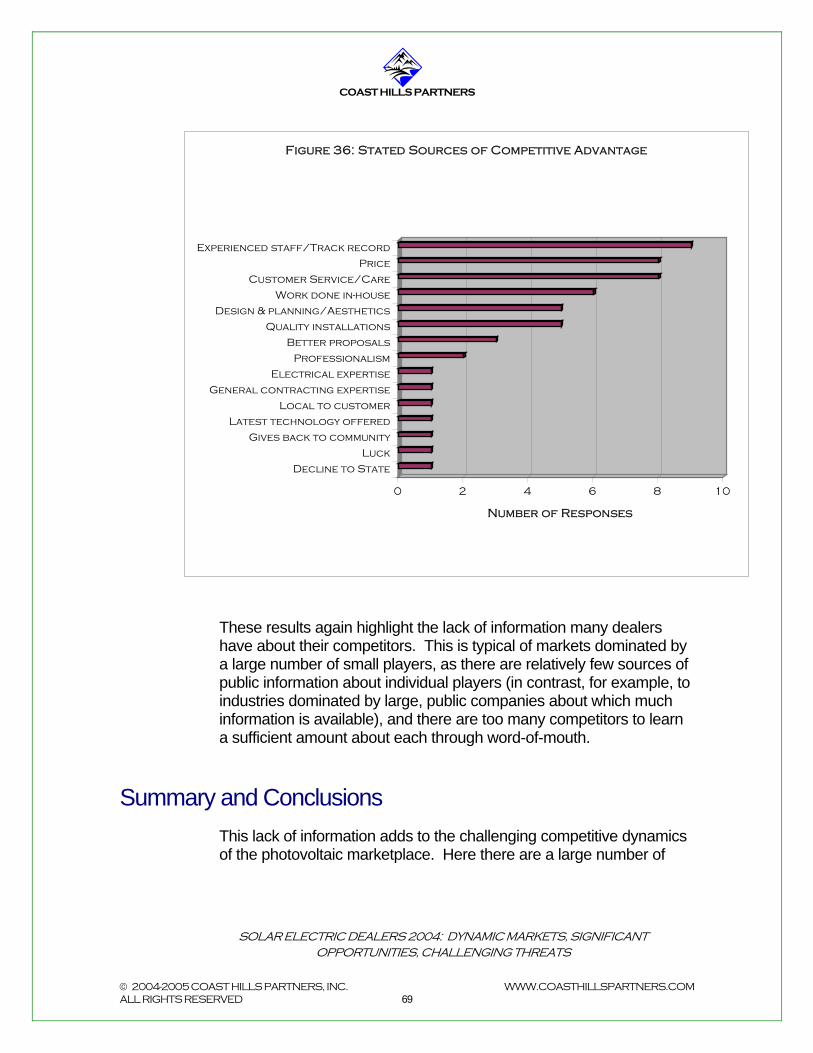

Sources of Competitive Advantage 68

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 4

Summary and Conclusions 69

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

VIII. Pricing & Cost Structure ............................................. 71

Residential Pricing 71

Commercial Pricing 78

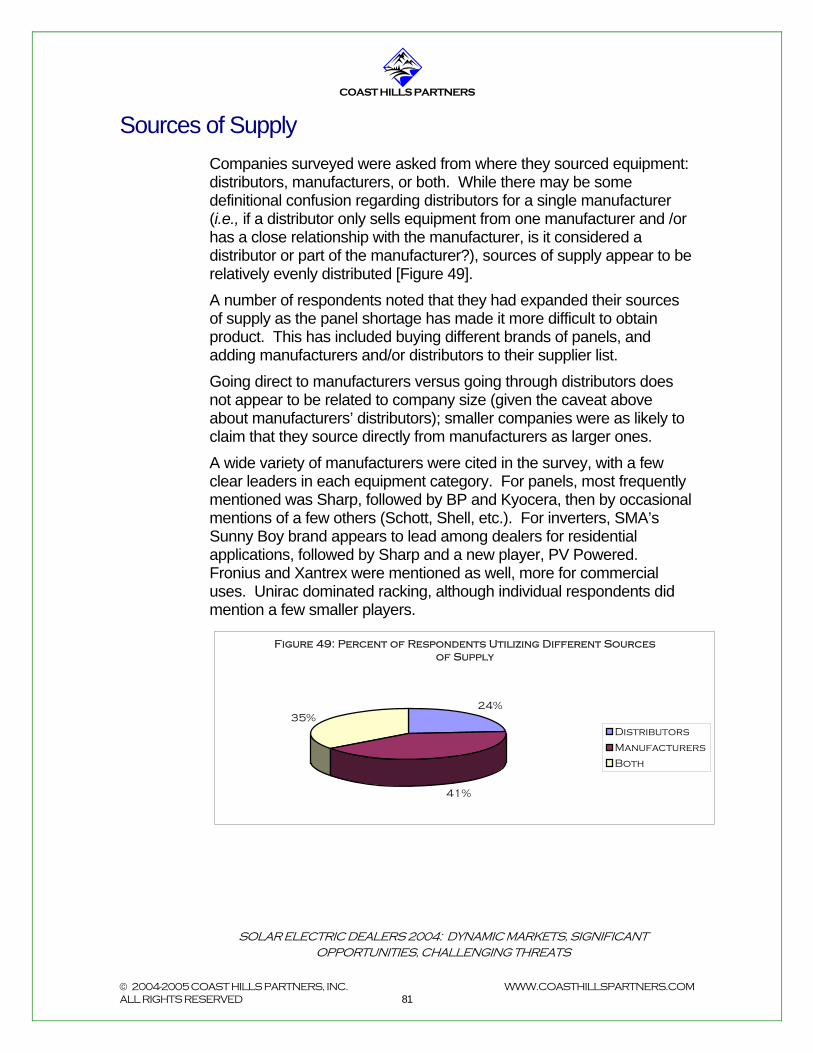

Sources of Supply 81

Revenue Per Employee 82

Contractors 85

Profitability 87

Summary and Conclusions 87

IX. Marketing Strategies & Tactics..................................... 89

Marketing Methods Utilized 89

Sources of New Business 92

Marketing Personnel 94

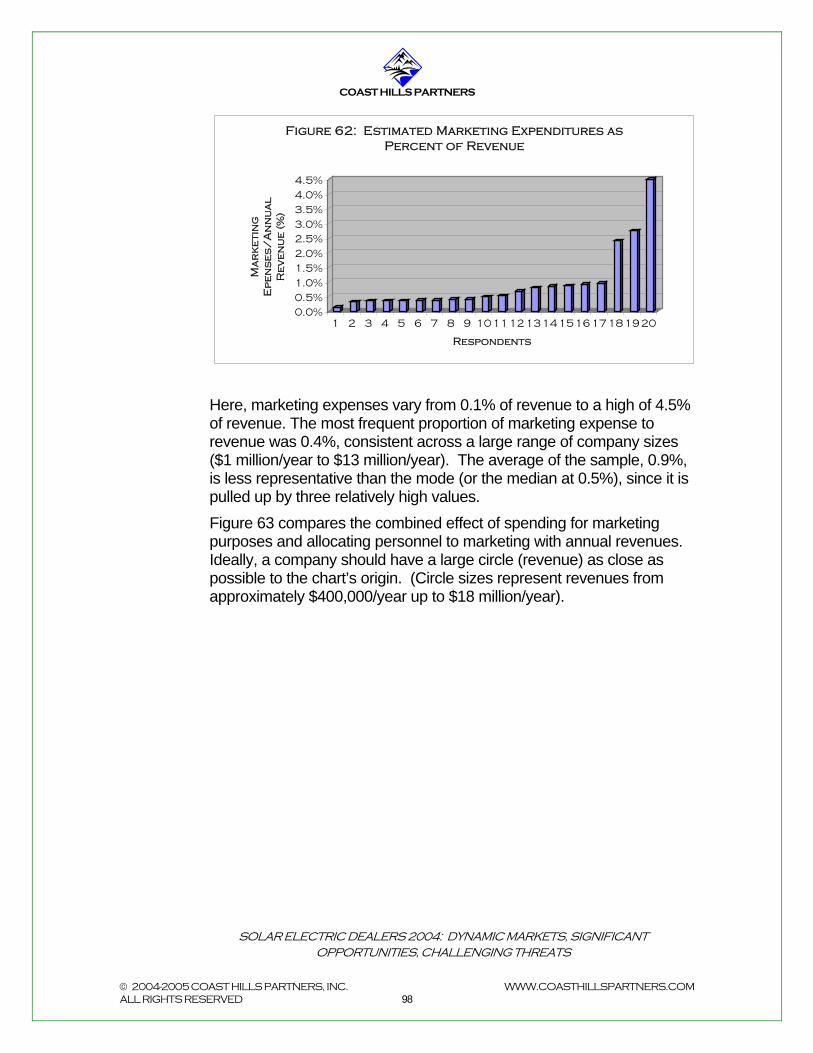

Marketing Expenditures 95

Summary and Conclusions 99

X. Company Motivations .................................................. 101

XI. Conclusion: Findings & Recommendations............... 103

Findings 103

Recommendations 105

Strategic 105

Policy 106

Further Research 107

XII. Study Methodology.................................................... 108

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 5

XIII. About Coast Hills Partners........................................ 114

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

I.

I. Executive Summary

This report analyzes the characteristics of and market dynamics surrounding solar electric dealers in the Greater San Francisco Bay Area. This research should provide insights to photovoltaic dealers seeking benchmarking references, as well as to those companies and organizations that interact with these dealers on a regular basis. Given the size and age of this regional market, it is also reasonable to extrapolate the conclusions here to the developing downstream photovoltaic distribution channel for the U.S.

The Market The market for grid-tied solar electric, or photovoltaic, systems in the Greater San Francisco Bay Area and across the state has exploded over the last six years since the state of California initiated incentives for purchasers of renewable energy systems. Cumulative annual growth rates have averaged over 135% during this period, which has been marked by dramatically increased demand as well as a substantial increase in competition. Coast Hills Partners estimates the total California grid-tied photovoltaic market to be $359 million, and the Greater Bay Area market to be $182 million, in 2004. California is the third largest solar market in the world, and the Greater Bay Area comprises 51% of the overall California market. This area is by far the largest regional market in the U.S., and, on a standalone basis, is the fourth largest solar electric market in the world, behind Japan, Germany, and the rest of Europe. It is also one of the most mature.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 6

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

The relative size and maturity of this marketplace, combined with a growing diversity of customer motivations and types, suggest that the Bay Area may serve as a reasonably representative predictor of how other developing photovoltaic markets in the U.S. will behave over the next few years. Even as the market continues to grow, market dynamics are becoming more challenging, as rebates decline and incentives overall are inconsistently supported. Solar electric dealers will have to adapt their strategies in order to thrive as the market evolves.

The Companies Twenty-one solar electric dealers in the Greater Bay Area participated in this study. These companies sell solar photovoltaic systems to residential and/or commercial customers and represent approximately $114 million in total revenue. These companies comprise approximately 37% of the Greater Bay Area market (calculated using revenue from business within the region only). Based on the results of this survey, the typical photovoltaic dealer is a small business, four to six years old, with approximately $4 million in revenues. The company was owner-financed to start and has grown by bootstrapping. The business owner/founder(s) originally entered the business to accomplish environmental and/or energy system goals, in addition to capitalizing on an attractive business opportunity. The majority of the typical dealer’s business is in the residential sector, but projects and revenue from the commercial sector are increasing significantly. The company has about ten employees, each pulling in around $350,000-$400,000/year in sales. These employees include a direct sales force and around 70% of a person devoted to marketing. Contractors are utilized when needed, primarily for electrical, installation, and roofing. The company spends approximately 0.5% of its sales, or $20,000, on marketing, for which it employs a variety of tools and tactics of varying effectiveness.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 7

This typical solar dealer has experienced double- or even triple-digit growth during the past 24 months while the regional market has grown by about 40% per year. The company plans to manage for growth in

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

the future, even though growth expectations, while still positive, are less so than during the recent past: 81% of companies identified business conditions as positive during the past 24 months; 48% expect similar positive conditions over the next 24 months. Future growth is perceived to be limited by supply shortfalls, the challenges of internal growth management, and rebate delays. Company executives are not as familiar as they could be with their competition: who they are, how big they are, and what makes them successful. Most believe their sources of competitive advantage are a combination of experience, customer care, and price; this is problematic since it results in a lack of differentiation among the players. The typical dealer is slightly profitable on a net basis, at an estimated 5%-8% before tax, a somewhat higher rate on average than the rates for general contracting, which run around 3%-5%.

The Customers & the Market The ongoing energy situation today is characterized by high and increasing electric rates, continuing concerns about pollution from fossil fuels and dependence on foreign oil, and extremely slow change in the overall energy generation and distribution system. These factors all fuel increasing demand for photovoltaic systems. Increasing public awareness of solar technology and of environmental issues in general, combined with media coverage, serve to broaden this demand. Although annual rates of increase have slowed from triple digits in 2001, the California market is still expanding at annual rates in the 30-40% range. Future rates of market growth will depend upon incentive levels and volatility, and on the rate of increase in electric rates. In Northern California, electric rates have increased 28% since deregulation in 1996, and additional rate increases have been announced for California in 2005. However, this growth will be cut back if concerns about instability in the state’s renewable energy incentive plans, cited by a third of those surveyed, come to fruition.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 8

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

If the current solar panel shortage persists, it will begin to have greater growth-limiting effects. New manufacturing capacity, in North America and elsewhere, is gradually coming on line, with some scheduled before the end of this year. If sufficient amounts are made available to the U.S. market, this constraint will be relaxed. Residential solar electric customers appear to be driven by three broad motivations:

“Green:” the desire to help the environment and society by switching to a clean, renewable source of energy;

“Economic:” the desire to achieve current and future savings

on electricity expenses; and

“Independence:” the desire to achieve a measure of control over one’s access to power, separate from the current energy infrastructure.

While environmental concerns still play a significant role in motivating solar electric purchases, an increasing number of solar electric customers are seeking positive economic returns as their primary, or a strong secondary, objective, thus expanding the available market. Corroborating this phenomenon is the substantial increase in commercial business now driven by cost-benefit analyses supporting solar adoption.

Typical residential solar electric customers in the Greater Bay Area tend to be affluent, educated, and middle-aged, concerned about the environment and somewhat familiar with technology. These consumers have high electric bills and seek some economic benefit as well as want to “do the right thing” by going solar.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 9

Typical commercial/municipal customers for the dealers in this survey are long-term building occupants or owners, requiring systems between 30kW and 100kW in size. They have cash on hand or the ability to obtain financing to pay for the systems and are seeking positive economic returns from investing in solar. These customers may also seek some collateral benefits as well from solar adoption, such as “green” marketing to their own customers or constituents.

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

In these market conditions, dealers highlight equipment shortages and lack of consistent government support as the two greatest external threats to their business. Supply limitations make it difficult to capitalize on demand, and increased prices due to shortages reduce that demand. Similarly, lack of incentives, inconsistent funding, and unpredictable changes to incentives tend to limit demand growth and make it risky to expand capacity. Dealers almost universally agree with the premises behind the CEC’s planned rebate step-down, with many expressing the desire to be able to operate without incentives, but they acknowledge that the economics are not there just yet. The greatest internal threat cited by survey respondents is the challenge of internal growth management. For any small business, attempting to expand rapidly and/or handle uncertain market conditions is fraught with pitfalls in cash flow management, hiring decisions, and other critical business functions. Solar dealers must rise to these challenges if they are to expand successfully. Top opportunities identified by dealers are, first, the ongoing energy “crisis” (the ever-increasing costs, monetary and otherwise, of fossil fuel dependence), and the growing awareness of solar as an alternative. Second and related is the possibility of more government programs (e.g., at the Federal level) to encourage renewable energy adoption, and third is the increasing availability of new markets, as more states institute incentive programs and more new solar products are introduced.

Competitive Dynamics

The large number of relatively new, small players contributes to an intensely competitive environment made more difficult by limited information flows among the players. As a result, few companies truly understand their source of competitive advantage, and many fail to differentiate themselves from their competitors.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 10

This lack of information adds to the challenging competitive dynamics of the photovoltaic marketplace. The large number of competitors vying for the same types of business, essentially interchangeable products,

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

and potentially uneven rates of market growth going forward all create a potentially unstable competitive situation.

Unless the market continues to expand faster than competitors can meet demand, these conditions point to a likely shakeout in the future. This could be caused by the realization of market threats – loss of incentives or supply interruptions – eliminating weaker players, or by the growth of larger regional players (in the $20 million+ revenue range) with the capability to buy up smaller competitors. In either scenario, companies that have achieved broader customer awareness in their segments will have an advantage in becoming regional leaders or in attracting strong buyout prices. Some players may also find that developing a strong niche position (e.g., leading in the schools segment) is a defensible strategy. Thus, successful branding and differentiation will become crucial competitive marketing strategies.

Pricing & Cost Structure Photovoltaic system pricing has declined slightly overall in California since 1998 (about 5%). Pricing for residential systems typically ranges from $8.72 - $8.80 per AC Watt as rated by the California Energy Commission (CEC), or $7.27 - $7.33 per Standard Test Condition (STC) DC Watt. For commercial and municipal systems, the typical dealer charges $8.00 - $8.29/ CEC Watt, or $6.67 - $6.91/STC Watt. Pricing for the most part indicates no scale effects, except in large commercial systems (>100 kW), projects that few dealers in this study typically win. This lack of scale underscores the need for all dealers to leverage their resources and reduce their cost structures in order to compete effectively in the long run.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 11

The structural environment for solar electric dealers also presents some challenges for manufacturers attempting to introduce new products into this channel. Training must reach personnel in a large number of dispersed organizations, and each dealer must develop a comfort level with the new product, its interoperability, and its track record before being willing to quote it to customers, thus lengthening the time-to-market for many new photovoltaic components.

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

Profitability for solar electric dealers today, suggested to be in the range of 5-8% net before tax, is tight and likely to become more so as competition increases. The ability to achieve scale economies will become increasingly important as the market matures further and competition intensifies. A company’s resulting lower cost structure will improve both profitability and maneuverability.

Marketing Solar electric dealers today utilize a variety of marketing tools, with varied results. These tools include Web-based advertising and a Web site, customer references and referrals, trade shows and industry events, Yellow Page advertisements and some direct mail. Interestingly, the tools most used do not necessarily map to those that bring in the most new business, which are referrals, advertising other than Yellow Pages, and Web presence. While this type of marketing will suffice in the future if demand continues to outpace dealers’ ability to supply solar electric systems, as supply constraints ease and/or competition intensifies, dealers will need to critically evaluate the return on investment for each of their marketing activities. In addition, as the need to differentiate effectively grows with competition, marketing efforts will need to be integrated into a coherent plan to accomplish strategic goals as well as promote sales.

Recommendations Strategic

Solar electric dealers must achieve scale and create sustainable, differentiated positioning. Companies must create reasons for doing business with them that are distinct from their competitors’ and must leverage their resources to a point where scale economies – and therefore lower cost structures -- can be achieved in order to remain competitive.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 12

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

Photovoltaic dealers therefore must:

Develop strategic marketing plans that cost-effectively drive sales while building a distinct, defensible brand and positioning. Carefully track and evaluate the returns on investment for alternative marketing approaches and integrate the best ones into a coordinated plan to drive sales growth, build competitive strength and profitability, and facilitate strategic maneuvers. Position the company based upon an accurate and unique source of competitive advantage.

Grow commercial business as a means of leveraging

sales, purchasing, and delivery resources. The larger deals typical of commercial and municipal opportunities can enable dealers to capture greater revenue per amount of sales effort, and likewise can enable lower unit costs through greater purchasing power and experience curve effects.

Reduce costs wherever possible. Lowering product

delivery cost structure is essential to photovoltaics’ economic viability in the absence of incentives. While the majority of the current cost gap must be closed in manufacturing, every percentage decrease in distribution costs, including dealers’ costs, is an important contribution toward this goal. In addition, lower cost structures improve profitability and competitiveness.

Implement protective strategies, especially smaller players

with less opportunity to develop scale. Developing niche segments with specialized market knowledge and clientele can both differentiate individual dealers and insulate against price pressures in the broader market. In addition, players can potentially increase buying power and reduce product costs through cooperative purchasing organizations or similar sourcing mechanisms.

Become and remain active in the political advocacy

surrounding incentive programs. In short, dealers must participate in the political process to insure that their industry needs are met, or else allow other players to determine their destinies.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 13

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

Policy

Incentive programs have provided an essential catalyst for the photovoltaic market in California. Given where the market stands now and the effects of incentive changes on dealers, the following points are critical to future policy discussions. Government agencies promoting renewable energy sources must:

Ensure that incentive systems remain consistent and predictable. Interruptions in funding or negative, unplanned changes in incentives only serve to undermine growth of the industry the incentives were intended to stimulate.

Take into account global market conditions (e.g.,

unanticipated worldwide supply shortages), as well as slower than anticipated growth in demand, where programs are intended to adjust over time. Positive changes in incentive programs such as these should have a beneficial effect on the industry, so long as the rationale and appropriate future expectations resulting from them are communicated. Alternatively, tie downward adjustments in incentive amounts to total megawattage of installations, or another metric that directly measures industry progress.

Account for the fact that many of the industry

players are very small businesses for which cash flow and timing are critical issues. Emphasize timely return of rebates and set clear expectations for timeframes.

The photovoltaic market in California is ready to take off, which is what the state’s incentive programs are intended to accomplish. It must not be hindered by uncertainties or interruptions. Allowing these to occur simply reduces the return on the public funds invested, and hinders the achievement of renewable energy policy goals.

Further Research

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 14

Additional research in this category will be critical for those players wishing to take leadership positions in the photovoltaic distribution

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

channel. Coast Hills Partners is pursuing further analysis in several important areas. Examples include:

Evaluation and development of effective marketing strategies and tactics

Investigation and creation of strategies to achieve scale

economies or other mechanisms to increase resource leverage in product sourcing and service delivery

Design of operational strategies to improve competitive

advantage and reduce costs

Analysis of additional state markets to determine market potential, target customer attributes, and entry strategies.

For further information or for additional copies of this study please contact Coast Hills Partners:

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 15

www.coasthillspartners.com 1- 650 - 255 -1828

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

II. Acknowledgements

Coast Hills Partners first acknowledges the many solar electric dealers in this study who gave their time to share knowledge and insight about their businesses. Many of the survey respondents’ own questions and suggestions have added depth to this report. Without their participation this study would not have been possible, and for it the author is grateful. Coast Hills Partners is also appreciative of the California Energy Commission’s robust renewable energy library. In addition, we thank Peter Buchanan for outstanding professional consultation, Dr. Leslie Field for her thoughtful review, and Steve Humphreys for peerless logistical and other support, as always.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 16

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

III. Company Profiles

In this section, we provide an overview of solar electric dealers today, based on our survey sample. Company ages, sizes, market segments served, distribution channels and geographic coverage are examined.

Definition of a Solar Electric Dealer A solar electric dealer as defined in this study is a private business that sells solar photovoltaic components and systems to residential and/or commercial and municipal end-customers. The dealer is typically, but is not always, a type of home improvement contractor. Dealers may design and specify photovoltaic systems for clients, or they may merely sell components selected by customers. Similarly, these companies may -- and often do – install these systems for their customers, as well as provide post-installation support where desired. For the purposes of this study, “solar electric” or “photovoltaic” systems refer to grid-tied systems, versus “off-grid” systems, which are not interconnected with the utility’s’ transmission system.

Company Representatives Survey respondents typically represented senior company management, with almost half being CEOs and/or owners of their firms. The next category of respondents, sales or marketing leadership, also were in positions of knowledge about their company’s markets, growth outlook, target customers, and so forth, as were sales personnel in general. Twenty-one companies were interviewed in total.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 17

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

Table 1: Survey Respondents

Ages of Companies The twenty-one companies interviewed ranged widely in age, from under one year to over 40 years [Figure 1]. The median age of responding companies, however, is three to three and a half years, not surprising given the events of 2001. While the original California Energy Commission (CEC) California Emerging Renewables rebate program was launched in 1998, 2001 saw the infamous California energy crisis. The rolling blackouts, Pacific Gas & Electric (PG&E) filing for bankruptcy, and dramatic electric rate increases resulted in widespread consumer outrage -- and a fair amount to emotional fuel to make changes in the system.

0

1

2

3

4

5

6

Number of Companies

1 4 7 10 13 16 19 22 25 28 31 34 37 40

Years

Figure 1: Ages of Businesses Surveyed

In addition, in March 2001, the California Public Utilities Commission instituted the Self Generation Incentive Program, directing utilities to provide financial incentives for large electricity users seeking to install renewable energy systems of 30 kilowatt (kW) or larger. This resulted in creation of PG&E’s attractive rebate program aimed primarily at commercial and municipal customers.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 18

Owner/President/CEO 9 43% Sales/Marketing Director 6 29% Sales 4 19% Other 2 10% TOTAL 21 100%

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

Finally, California instituted a 15% tax credit on purchases of photovoltaic (and wind) systems up to 200 MW, installed between January 1, 2001, and December 31, 2003 – a significant incentive. (The tax credit was reduced to 7.5% for 2004-2005, and is currently planned to sunset in 2006). These three factors combined to make the photovoltaic market more attractive as a business opportunity. Taking a broader view, there was actually a confluence of forces that resulted in almost 60% of sample companies being founded within the last six years:

Establishment of CEC incentives in 1998 dramatically increased the economic feasibility of photovoltaics, enabling it to come out of the realm of remote, non-grid-tied systems (although cost-effectiveness remains a significant issue);

“Y2K” fears in 1998 and 1999 fueled consumer interest in being shielded or independent from large systems such as the electric grid, which were feared to be vulnerable;

Ongoing, increasing environmental awareness in the general population regarding issues such as global warming, air pollution, and habitat preservation has steadily increased the desire for clean energy and the acceptability of “alternative” energy sources;

Finally, the 2001 energy crisis and its reverberations since have helped to sustain and increase the solar electric market. Accordingly, competition has dramatically increased over this time period; some respondents have estimated more than a 10X increase in the number companies participating in the photovoltaic market. The older companies represented in the survey are impressive for their ability to survive: while several had a core business outside of solar prior to entering the photovoltaic market, most have a foundation in early solar technology, such as solar thermal, non-grid-connected solar electric, and so forth. These companies were able to stay in business despite the hostile market conditions of the 1980’s and the1990’s. Not surprisingly, company representatives who have seen some of this history are more sanguine about market conditions today and in the future.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 19

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

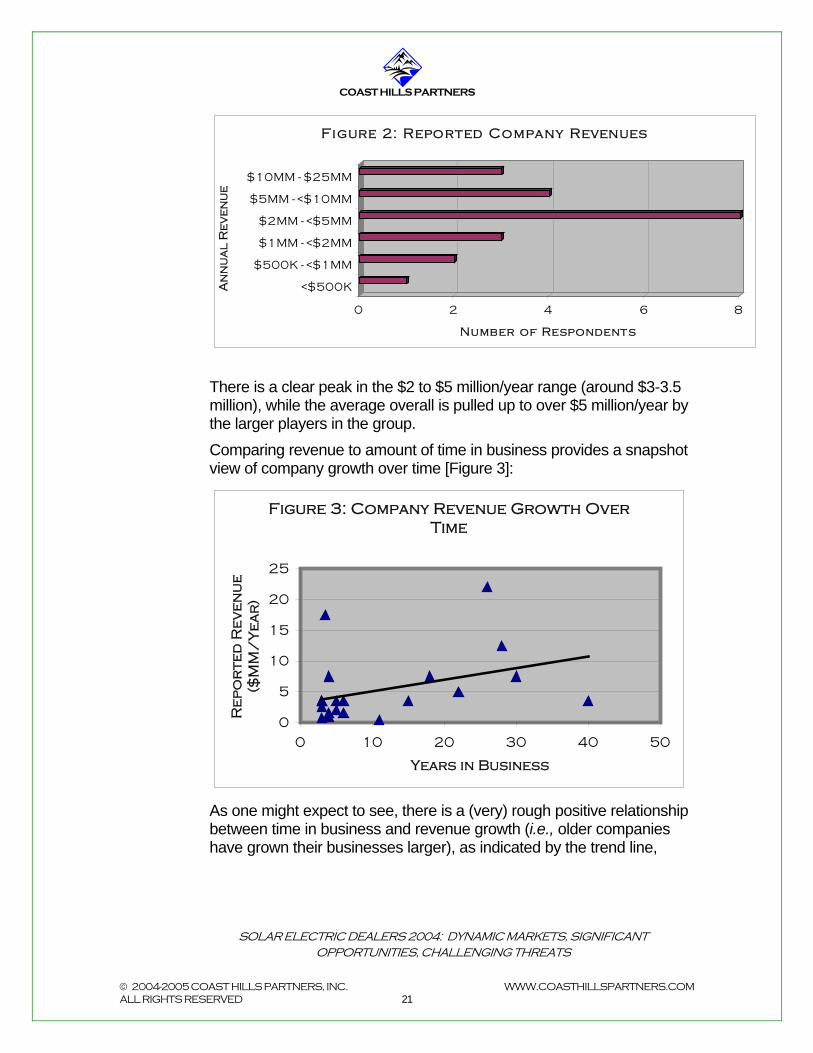

Revenues Company size, measured in annual revenue, also varies widely, although none have broken out of the “small business” size range, defined as $28.5 million/year for the solar industry as a whole in the Small Business Administration’s Size Standards (https://eweb1.sba.gov/naics/dsp_naicsearch2.cfm, description = “solar”). The companies in the survey reported a total of approximately $114 million in sales, estimated for the twelve months of 2004. Analysis of the CEC’s database of renewable energy installations under 30kW in size (http://www.energy.ca.gov/renewables/emerging_renewables/2004-10-1_ERP_Cmptd_Apprvd.XLS) confirms $42.4 million of this revenue. Additional analysis utilizing 2003 data compiled by Solarbuzz (http://www.solarbuzz.com/usgridconnect2004.htm) and updating it for 2004 identifies another $24 million in projects over 30kW. Further Coast Hills Partners analysis of market segments served (below) infers an additional $22 million in sales. Therefore, approximately 80% of reported revenues can be verified or inferred from other information. The remaining 20% can be attributed to additional 2004 business that has not yet been booked, as well as to the fact that many survey respondents preferred to provide their company revenue within a range (e.g., “$2 to $5 million”), as illustrated below [Figure 2]. Looking only at company revenues derived from business sold in Northern California, we estimate that these companies represent approximately 37% of the Northern California market today.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 20

Reported annual company revenues ranged from just under half a million dollars per year to $22 million.

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

0 2 4 6

Number of Respondents

8

<$500K

$500K - <$1MM

$1MM - <$2MM

$2MM - <$5MM

$5MM - <$10MM

$10MM - $25MM

An

nu

al

Re

ve

nu

e

Figure 2: Reported Company Revenues

There is a clear peak in the $2 to $5 million/year range (around $3-3.5 million), while the average overall is pulled up to over $5 million/year by the larger players in the group. Comparing revenue to amount of time in business provides a snapshot view of company growth over time [Figure 3]:

Figure 3: Company Revenue Growth Over Time

0

5

10

15

20

25

0 10 20 30 40 50

Years in Business

Re

po

rte

d R

ev

en

ue

($

MM

/Y

ea

r)

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 21

As one might expect to see, there is a (very) rough positive relationship between time in business and revenue growth (i.e., older companies have grown their businesses larger), as indicated by the trend line,

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

although the many outliers clearly indicate that a variety of growth aspirations and strategies are in play. (Note: the trend lines that appear in some of the analyses in this report are based on simple linear regression analysis, and are intended to illustrate only approximate directional relationships between variables).

Market Segments Served Companies were queried about the solar electric market segments they served: Residential, Commercial/Municipal, Wholesale, or Other Products/Services. The last category could include photovoltaic products other than for standard roof-/ground-mounted systems, other solar segments such as solar thermal systems, or other renewable energy products. The split amongst these segments for the survey sample, in terms of number of systems sold, is shown in Figure 4. The bulk of sample companies currently concentrate sales volume (but not necessarily revenue) in the residential sector, with 71% attributing more than 50% of their sales volume to residential business. That said, almost every company also serving the commercial/municipal market noted that the dollar amounts per sale are much higher on the commercial side, and several noted that their commercial business specifically was increasing dramatically.

Figure 4: Market Segments Served

Wholesale2%

Residential66%

Commercial/Municipal

21%

Other Products/

Services11%

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 22

Only three respondents reported participating significantly in the wholesale solar electric segment. Several companies (33%) are active in other products and services, primarily other photovoltaic or other renewable energy products and services.

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

Respondents provide three basic reasons for participating in these other business areas: Historical: They were already in the other business when they decided to enter the photovoltaic market; Opportunistic: The other market opportunity “came up” and appeared to complement some aspects of their solar electric business; Diversification: The new market segment is insulated from incentive program uncertainties and other photovoltaic market risks. Interestingly, whether or not diversification was part of the business strategy appeared to be unrelated to annual revenue; companies of all sizes were just as likely to pursue multiple markets as not. All diversified respondents did note an increased sense of security from not having all of their business eggs in one basket, so to speak. However, this increased security from risks in one market must be balanced against the internal management risks associated with greater complexity and potentially less focus on the core competencies needed to succeed in one’s chosen market(s). In some cases, enough synergy exists between the different markets that this problem can be minimized. This depends largely upon the skill and expertise of the management involved.

Distribution Channels Survey respondents reported two types of distribution channels: direct sales and Internet sales with affiliate installers [see Figure 5]. The direct sales model is the most prevalent, with 86% of companies utilizing this channel, as well as the most traditional: a company representative meets directly with sales prospects, makes the proposal and shepherds the opportunity through to a close.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 23

The Internet approach utilizes a Web site enabled for e-commerce, so that customers can order photovoltaic equipment directly from the Web site or over the phone. In one case a paper catalog is also used. Equipment is then shipped directly to the customer, who can then choose to work with an affiliated installer to complete the installation.

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

0

5

10

15

20

Nu

mb

er

of

R

es

po

nd

en

ts

Direct Sales Internet Sales w/Affiliate Installers

Figure 5: Distribution Channels Utilized

The Internet sales model affords greater geographical reach, and attracts a demographic of knowledgeable and/or do-it-yourselfer customers. Lower equipment prices are a significant draw in most cases, as are advertised large selections, lower overhead, and so forth. Possible downsides for the consumer include shipping costs, support, and the tax implications of rebates if the dealer does not process them. These can be, but are not always, addressed by the dealer. Two apparent downsides for the dealer are the lack direct customer contact in the field and of control over the final installation. These can be addressed, however, with limited site visits after extensive phone consultation, and with affiliates that have a significant stake in the success of the dealer (e.g., affiliates that are shareholders of the dealer). The economics of these two types of distribution present a number of trade-offs. Direct sales represent the most expensive form of distribution. Sales personnel are paid to track prospects and present proposals, a time-consuming process in which a large percentage will not come to fruition. However, it also affords the greatest control over the sale and is particularly useful in complex, high-value sales. While it is more expensive, the conversion rate of prospects to closed sales is probably higher.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 24

Internet-based sales offer the possibility of much lower distribution costs, through fewer and sometimes less well-compensated personnel, lower expenses (e.g., no travel expenses, less hard-copy collateral, no remote sales offices), and sometimes less post-sale service. These

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

advantages are reduced as Internet dealers add services to compete with the higher customer touch of direct sales dealers. Although the close rate may be lower with this model, costs of the distribution channel are lower, too. Which model is ultimately “best” will depend upon how well individual players execute their respective distribution strategies, and requires further analysis of the specifics of the solar electric marketplace, not covered in this report.

Geographic Coverage All participating companies in the survey serve the “Greater Bay Area,” an area defined loosely as centered around San Francisco, extending north to Sonoma and Napa counties; east to Solano and Contra Costa counties; and south through Santa Clara and Santa Cruz counties [see map, Figure 7]. Company locations are distributed around the Greater Bay Area, with a slight emphasis on the South and East Bay regions in number of companies [Table 2], although not in revenue. Locations are either headquarters or local outposts if the company is based elsewhere.

Table 2: Company Locations Within the Great Bay Area Region Number of

Companies Percentage of Companies

Percentage of Reported Revenue

South Bay 8 38% 31%

East Bay 6 29 23

North Bay 4 19 39

Peninsula 2 9 4

Outside of Bay Area 1 5 3

TOTAL 21 100% 100%

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 25

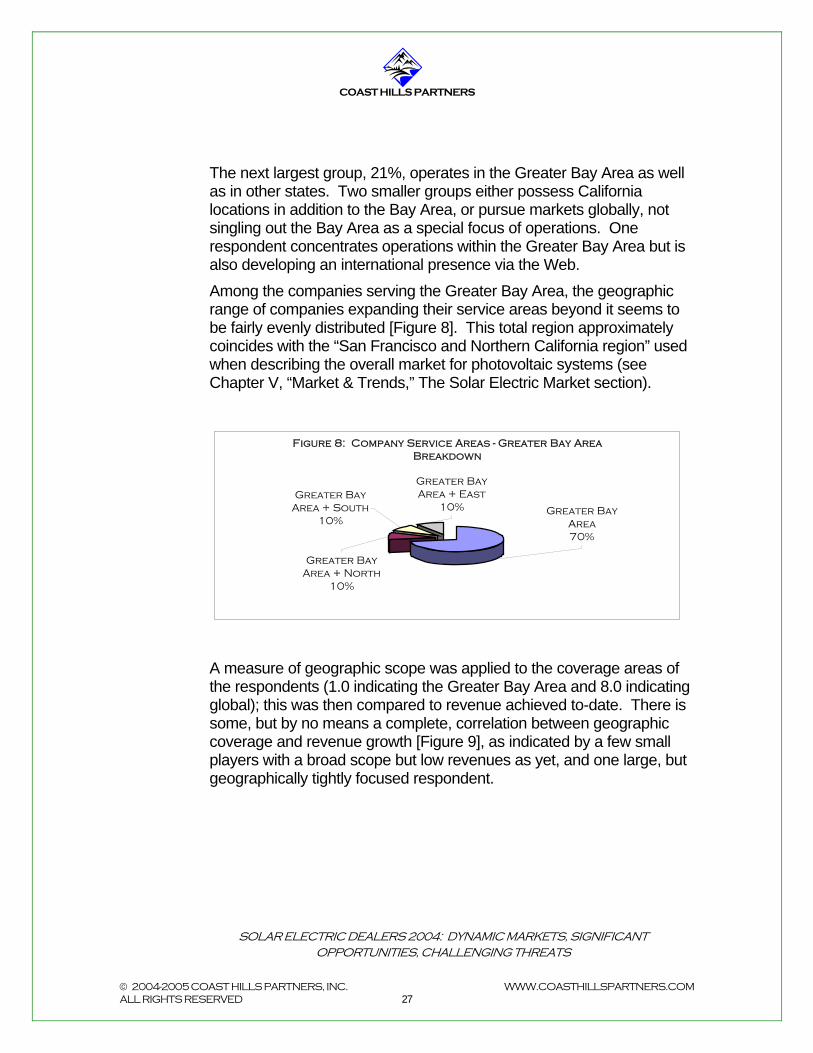

Slightly over one third (36%) of companies concentrated their business in the Greater Bay Area as defined. A superset of this group, 49%, serves either the Greater Bay Area alone or this plus some extension

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

beyond it (e.g., serving into Yolo or San Joaquin counties). See Figure 8. Interestingly, few companies (with one significant exception) noted doing a great deal of business within the city of San Francisco itself. Several noted challenges in competing for municipal contracts or in gaining building approvals for residential systems.

Figure 7: Geographic Ranges of Companies Surveyed

Greater Bay Area + other

California13%

Greater Bay Area + other state(s)

21%

Global13%

Greater Bay Area + International

4%

Greater Bay Area 49%

Figure 8: The Greater Bay Area

Map Source: The CA Gen Web Project, 2004

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 26

Greater bay Area counties: San Francisco, San Mateo, Santa Cruz, Santa Clara, Alameda, Contra Costa, Solano, Napa, Sonoma

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

The next largest group, 21%, operates in the Greater Bay Area as well as in other states. Two smaller groups either possess California locations in addition to the Bay Area, or pursue markets globally, not singling out the Bay Area as a special focus of operations. One respondent concentrates operations within the Greater Bay Area but is also developing an international presence via the Web. Among the companies serving the Greater Bay Area, the geographic range of companies expanding their service areas beyond it seems to be fairly evenly distributed [Figure 8]. This total region approximately coincides with the “San Francisco and Northern California region” used when describing the overall market for photovoltaic systems (see Chapter V, “Market & Trends,” The Solar Electric Market section).

Figure 8: Company Service Areas - Greater Bay Area Breakdown

Greater Bay Area + South

10%

Greater Bay Area + East

10%

Greater Bay Area + North

10%

Greater Bay Area70%

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 27

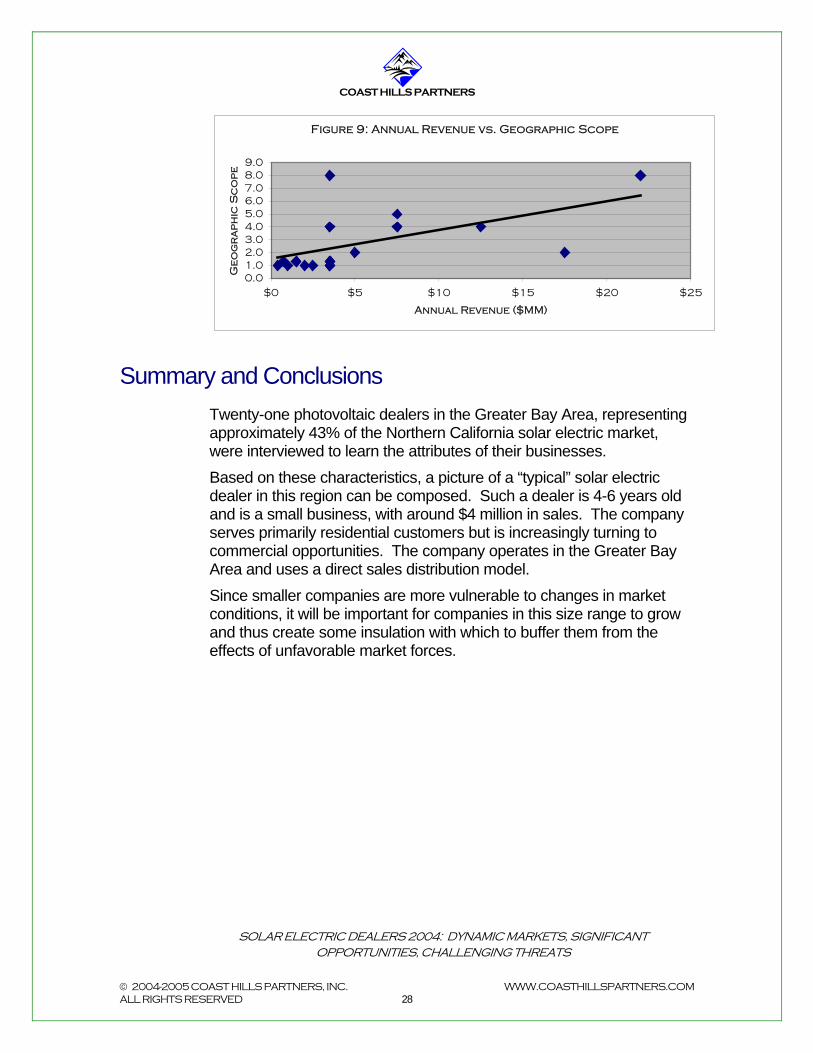

A measure of geographic scope was applied to the coverage areas of the respondents (1.0 indicating the Greater Bay Area and 8.0 indicating global); this was then compared to revenue achieved to-date. There is some, but by no means a complete, correlation between geographic coverage and revenue growth [Figure 9], as indicated by a few small players with a broad scope but low revenues as yet, and one large, but geographically tightly focused respondent.

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

Figure 9: Annual Revenue vs. Geographic Scope

0.01.02.03.04.05.06.07.08.09.0

$0 $5 $10 $15 $20 $25

Annual Revenue ($MM)

Ge

og

ra

ph

ic S

co

pe

Summary and Conclusions Twenty-one photovoltaic dealers in the Greater Bay Area, representing approximately 43% of the Northern California solar electric market, were interviewed to learn the attributes of their businesses. Based on these characteristics, a picture of a “typical” solar electric dealer in this region can be composed. Such a dealer is 4-6 years old and is a small business, with around $4 million in sales. The company serves primarily residential customers but is increasingly turning to commercial opportunities. The company operates in the Greater Bay Area and uses a direct sales distribution model.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 28

Since smaller companies are more vulnerable to changes in market conditions, it will be important for companies in this size range to grow and thus create some insulation with which to buffer them from the effects of unfavorable market forces.

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

IV. Customer Profiles

Survey respondents provided a wealth of information regarding their target customers, both residential and commercial. Company representatives were asked to describe the key characteristics of their target customers, and, while each description was different, some common themes emerged. For analytical purposes, these customer characteristics have been divided into customer attributes and customer motivations – attributes being aspects of who the customers are, and motivations being the reasons they are interested in solar. First we’ll take a look at residential customers, then commercial/municipal ones.

Residential Customer Attributes For residential customer attributes, respondents shared a wide variety of characteristics that they believed define their target customers [see Figure 10]. Although many attributes appear here, even after some have been aggregated, there are some clear commonalities. From this data, and in descending order of importance, the target residential customer for photovoltaic systems appears to be:

Environmentally concerned. While not a passionate environmentalist, the target customer is aware of environmental issues and concerned about the environment.

Affluent. Target customers are typically mid- to upper-middle class and are able to consider purchases in the range of solar electric system costs.

Comfortable and familiar with technology.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 29

Educated, typically global thinkers. This factor may co-vary with affluence and/or environmental concern.

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

Over 40 years old, and/or retirees. This could co-vary with affluence, as affluent people tend to be older (or, younger people are less likely to have amassed wealth since they have had fewer years in which to do it – dot-com boom notwithstanding).

4%4%

2%10%10%

2%2%

6%22%

4%2%

16%6%

12%

0% 5% 10% 15% 20% 25%

% of Responses

Technology savvyHigh electric use

AffluentAgricultural producers

ProfessionalsEnvironmentally concerned

Small % = environmentalists Need quality, value, service

Alt. fuel vehicle ownersOver 40 &/or retirees

Educated/ global thinkersLiberal

Know someone w/ solarNOT an environmentalist

Figure 10: Target Residential Customer Attributes

There was also agreement across a number of respondents that only a small percentage of customers are passionate, or “hard-core” environmentalists. As a broad characterization (or perception amongst dealers), hard-core environmentalists typically buy small systems, either due to inability to pay for larger ones or having relatively small electric usage to begin with. Other respondents noted that a certain, possibly increasing, percentage of customers are specifically not environmentalists. Rather, they are interested in solar because of its economic benefits and/or the degree of independence it provides from one’s utility and the overall power system.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 30

The same number of respondents identified high electric power consumption as an important target customer attribute. While a prospective customer does not have to have exorbitant electric bills to benefit from solar, higher bills do increase the likely benefit and hence the motivation to purchase. They also indicate some degree of affluence, which also predisposes toward a solar purchase.

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

In identifying these attributes, almost all respondents opted not to mention some basic prerequisites for a prospective customer, presumably because these are assumed. These prerequisites include:

Prospect has sufficient sun exposure Prospect is typically a homeowner Prospect has sufficient financial resources Prospect has more than minimal electric usage.

The average size of residential system sold by respondents is approximately 4.6 kW. The size of system most frequently sold to residential customers (the mode of the sample) is also between 4.5 and 5.0 kW.

Target Residential Customer Motivations For target customers with the attributes described above, motivations to purchase a photovoltaic system appear to divide into three major themes:

“Green,” or environmentally motivated; Economic, primarily driven by the desire for savings; and Independence, driven by anger at one’s electric utility and

desire to have some control over power generation and access Figure 11 shows the relative frequency of customer motivations cited:

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 31

43%34%

23%

0%

10%

20%

30%

40%

50%

% o

f

Re

sp

on

se

s

(n=

44

)

Green Economic Independence

Figure 11: Relative Frequency of Customer Motivational Themes

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

The most prevalently cited motivations fell into the “Green” theme [Figure 12]:

Figure 12: "Green" Motivations for Buying Solar

Willing to pay small

economic penalty

5%

Do the Right Thing

(Enviro/Soci0- conscience)

69%

Politico-environmental motive (often

small systems)21%

Aware of oil issues/want to

reduce oil dependence

5%

The majority of reasons cited for interest in solar fall under the umbrella of wanting to “do the right thing,” meaning the customer seeking to do his/her part to reduce dependence on fossil fuels and their attendant side effects, particularly of pollution and global warming. Next off are those customers motivated by more pure environmentalist thinking. These are often politically motivated; solar electric may not actually make economic sense for them; and they typically purchase smaller systems. Finally, some customers appear to be motivated by oil issues: concern about dependence on foreign oil and its environmental and political implications for society. In all of these, some respondents noted, some customers motivated by green reasons can be willing to take a small economic penalty for going solar. In other words, they may fare about the same or a little worse than by sticking with their utility, but they are willing to nonetheless bear the expense of installing a photovoltaic system in order to achieve other environmental and social benefits.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 32

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

The next most-often cited set of motivations, the “Economic” theme, is increasingly prevalent amongst target customers, according to respondents. As solar has become more affordable, and conventional electric rates have increased, there is a positive economic trade-off to going solar for more consumers (although this is partially mitigated by declining rebates). See Figure 13.

Figure 13: Economic Motivations to Buy Solar

Add value to house

7% Want to reduce bills53%

Lock in Energy costs20%

Seek good ROI20%

The first three stated categories are slightly different presentations of the same basic economic motivation, which is to reduce household energy costs. It was noted by some respondents that the desire to lock in energy costs, and thus be insulated from future rate increases, is particularly evident among retirees (due to fixed incomes). The fourth category, the desire to add value to one’s house, is most likely a secondary motivation behind a primary economic or other reason for interest in solar, as presumably a consumer would not purchase a system immediately in advance of selling the home.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 33

Ironically, the focus on return on investment (ROI) can be a limiting factor for solar sales as well. Many consumers resist payback periods that hover around a decade, according to respondents. One company representative noted with frustration that some consumers were unwilling to purchase a solar electric system because they felt that a 10-year payback period was too long, but these same consumers had no problem buying the latest large SUV (which of course has no return on investment, and an infinite payback period). A marketing challenge, for sure.

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

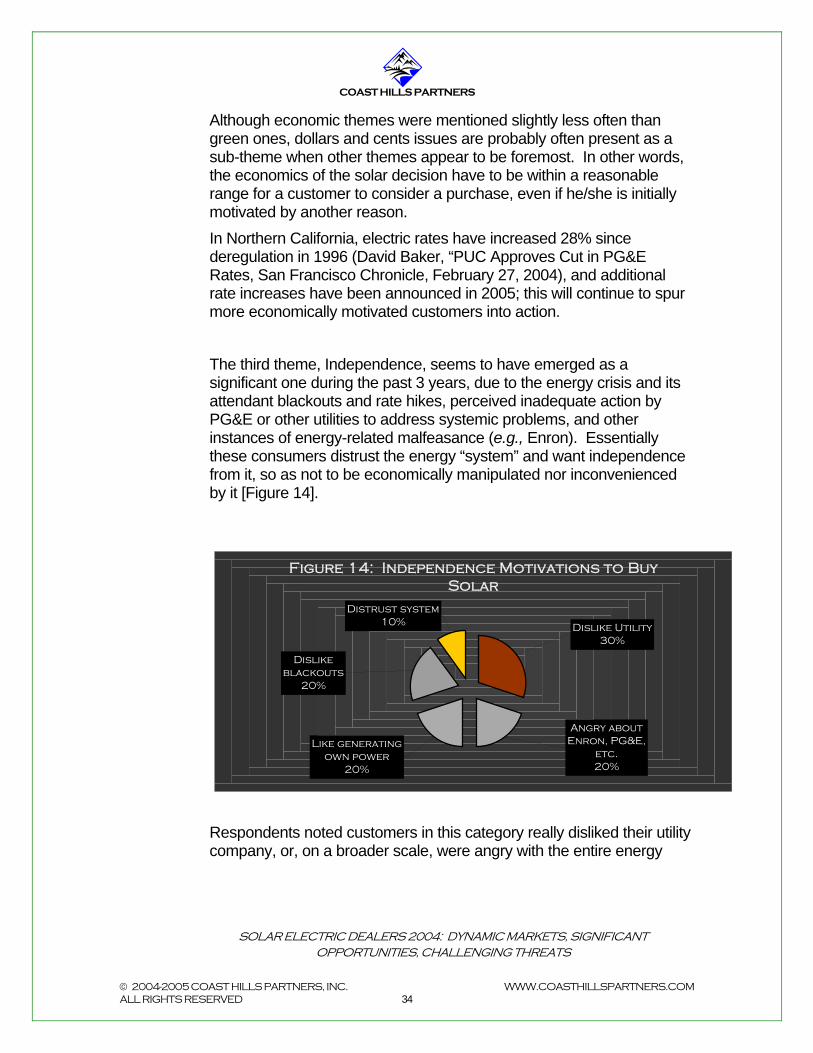

Although economic themes were mentioned slightly less often than green ones, dollars and cents issues are probably often present as a sub-theme when other themes appear to be foremost. In other words, the economics of the solar decision have to be within a reasonable range for a customer to consider a purchase, even if he/she is initially motivated by another reason. In Northern California, electric rates have increased 28% since deregulation in 1996 (David Baker, “PUC Approves Cut in PG&E Rates, San Francisco Chronicle, February 27, 2004), and additional rate increases have been announced in 2005; this will continue to spur more economically motivated customers into action. The third theme, Independence, seems to have emerged as a significant one during the past 3 years, due to the energy crisis and its attendant blackouts and rate hikes, perceived inadequate action by PG&E or other utilities to address systemic problems, and other instances of energy-related malfeasance (e.g., Enron). Essentially these consumers distrust the energy “system” and want independence from it, so as not to be economically manipulated nor inconvenienced by it [Figure 14].

Figure 14: Independence Motivations to Buy Solar

Dislike blackouts

20%

Like generating own power

20%

Angry about Enron, PG&E,

etc.20%

Dislike Utility30%

Distrust system10%

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 34

Respondents noted customers in this category really disliked their utility company, or, on a broader scale, were angry with the entire energy

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

system and what has transpired over the past few years in California, specifically citing Enron, blackouts, or the failed system in general. These consumers seek to have more control over their own power generation, both to protect themselves from a broken system and to deny the players in that system any economic benefit from their households. Interestingly, it is these target customers who were most likely to identify themselves specifically as non-environmentalists. This may be due to the fact that there is a new demographic with a more conservative mindset (which is sometimes, although not always, associated with less interest in environmental issues) drawn to solar because it is an available way of removing oneself partially or completely from an energy system which does not support the interests of the little guy. Of course, while it is useful to divide customer motivations into these three analyzable groups, in reality motivations expressed by target customers are probably often mixed across categories. For example, someone desiring to “Do the right thing” environmentally may decide to purchase once the economic case has been made that solar is affordable and beneficial. Similarly, economic and independence motivations are probably strongly linked: much of the anger at utilities stems from high bills and rate increases.

Commercial Customer Attributes

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 35

Respondents provided data about target commercial and municipal customers, but in general with less detail with less consensus among respondents. When aggregated, commercial and municipal customer characteristics did show some commonalities [Figure 15].

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 36

0% 5% 10% 15% 20% 25% 30% 35% 40%

% of Respondents Identifying(Responses greater than 100%)

Landlord/Long-term building occupantHigh power usage/Need >30kW system

Profitable business with CashSchools

Housing complexesMunicipal buildings

Some consumer contactMedium-sized business

Owners with solar residences

Figure 15: Target Commercial & Municipal Customer Attributes

Respondents identified several specific business segments as good target customers for solar electric systems:

Housing complexes Municipal buildings (although some respondents have chosen

not to pursue this segment due to the frequently lower margins, longer timeframes, and other requirements)

Schools (in many cases private schools, which do not have the cumbersome public budgeting process)

“Big box” retail (included in “long-term building occupant” in Fig. 15] The most frequently reported commercial customer attribute, according to respondents, was being either a landlord or a long-term building occupant. This makes obvious sense, since those businesses with short-term building leases would be unwilling to make a long-term investment in something like solar for that building space. Those with longer time horizons are better able to take advantage of the long-term benefits of solar. The next most-frequently cited attributes, being a profitable business and being a high power user, sound obvious but do represent some nuances in the commercial market. Unprofitable businesses are clearly not going to invest in something like solar (nor would they make good business risks for dealers), but profitable ones also need to possess sufficient cash-on-hand or have access to financing in order to be

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

viable customers. Low margin businesses with low cash flow are therefore not likely to make good candidates. Non-profits create an interesting dilemma in this regard. Respondents reported a great deal of interest from the non-profit sector, and some reported completing installations for large non-profits. However, many smaller non-profits that do not possess strong endowments just cannot muster the financial resources to go solar, unless they organize a fund-raising campaign to do so. Qualifying non-profit prospects thus is a very important part of the sales process. Relatively high power usage makes sense as a target customer attribute, since the higher the current usage the more rapid the payback, and businesses in particular seek rapid returns on their solar investments. In addition, potential customers requiring more than a 30kW system make good targets because this size pushes them into the PG&E rebate tier, which is much more attractive on a per-Watt basis (currently $4.50/Watt) than the CEC rebates ($3.00/Watt until January, 2005, when they will decline again). This assumes that the PG&E rebate fund continues to be replenished annually and waiting lists do not become too long. Companies with some consumer contact as well as an economic justification for going solar can reap the additional benefit of being able to utilize “green” marketing tactics, highlighting their clean energy production as a means of building consumer loyalty. Finally, an attractive attribute cited by at least one respondent is that the target be a medium sized business. In this case “medium” is a subjective term, but the concept is finding commercial entities that are big enough to benefit from solar and able to pay, but are not so big that the sales process is overly bureaucratic or lengthy, the headquarters is remote, and so forth. The average commercial system sold by respondents is approximately 55 kW. If we remove outliers on the top and bottom of the reported range, the average is a perhaps more realistic 36 kW for this sample. (The 55kW average was influenced by one very high reported average commercial system size). The median and mode of reported system sizes is between 30 and 40kW, with a range of 20-70 kW, plus one very high response at 200 kW.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 37

There are two reasons way the average commercial system size appears relatively small. One is simply sample variance: the dealers

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

responding to the survey may have concentrated less on commercial (although that is changing, according to a number of them), and therefore have not sold a repeated number of large (>100kW) systems. Second, several respondents mentioned PowerLight (not surveyed) as a major competitor in the commercial arena, along with the fact that PowerLight tends to target larger (>100kW) deals. PowerLight’s behavior may have created an “umbrella” under which smaller competitors in the commercial marketplace can carve out successful positions without often running up against this large player.

Target Commercial Customer Motivations Commercial and municipal customer motivations essentially boil down to economic reasoning, with the one cited exception being that municipal customers sometimes desire to make a political statement or set an example for residents by adopting solar. Figure 16 illustrates how these motivations split out:

Figure 16: Target Commercial Customer Motivations

Political statement (Municipal)

7%

Educate others

7%

"Green" marketing

7%

Want to insulate vs. increasing

rates13%

Seek 3-7 year ROI26%

Seek overall economic

benefit20%

EconomicBenefit

93%

Save money now20%

In addition to the pure economic return received from solar, some commercial/municipal customers are able to achieve additional, collateral benefits, such as “green” marketing to consumers, education

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 38

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

in the case of schools or some non-profits, as well as the aforementioned political statement or setting of an example, which is all the more powerfully made when the municipality can clearly demonstrate that solar is the right thing to do both economically and environmentally.

The Bay Area Customer Base as Representative While the San Francisco Bay Area certainly has its points of uniqueness compared to other major metropolitan areas in the U.S., it is nonetheless increasingly able to serve as a representative market for photovoltaics when forecasting market behavior and trends. The Greater Bay Area is the largest regional photovoltaic market in the U.S. California makes up an enormous 80% of the current United States photovoltaic market; more than 50% of this comes from the region just surrounding the Greater Bay Area. This market has been actively growing since 1998, making it one of the oldest in the U.S. as well. The large number of customers, plus the relative maturity of the market here, all contributes to the Greater Bay Area’s usefulness in forecasting behavior in other state and regional markets. Commercial customers, primarily motivated by economic benefits, behave no differently in the Bay Area than in the rest of the country in this respect. As more and more states adopt renewable energy incentive programs, the economic equation for more businesses will dictate converting to solar or another renewable energy source just as it does in Northern California.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 39

Similarly, as electric rates increase and more incentive programs are instituted, the economic equation for consumers in other regions becomes more and more similar to the one in the Bay Area. In addition, as general environmental awareness continues to grow, taking action for environmental reasons becomes both more common and less of a political statement. Doing the right thing for the environment becomes a civic-minded thing to do instead of something radical, as has become the case with recycling. This combination of increasing economic similarity and the mainstreaming of environmental awareness reduces the importance o f the Bay Area’s specific socio-political demographics.

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

The increasing diversity of motivations in the Bay Area suggests a broadening of the solar electric market to include a wider variety of customer types, which most likely tends to push the Bay Area’s customer profile further in the direction of the average for the country as a whole. This factor plus the size and age of this photovoltaics market relative to other markets in the U.S. suggests that we can look to the Bay Area to draw implications about the future behavior and trends in these newer markets.

Summary and Conclusions Typical residential solar electric customers in the Greater Bay Area tend to be affluent, educated, and middle-aged, concerned about the environment and are probably somewhat familiar with technology. These consumers have high electric bills and seek some economic benefit as well as want to “do the right thing” by going solar.

Residential solar electric customers appear to be driven by three broad motivations:

“Green:” the desire to help the environment and society by switching to a clean, renewable source of energy;

“Economic:” the desire to achieve current and future savings on electricity expenses; and

“Independence:” the desire to achieve a measure of control over one’s access to power, separate from the current energy infrastructure. While environmental concerns still play a significant role in motivating photovoltaic purchases, an increasing number of solar electric customers are seeking positive economic returns as their primary, or a strong secondary, objective, thus expanding the available market.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 40

Typical commercial/municipal customers for the dealers in this survey are long-term building occupants or owners, requiring systems between 30kW and 100kW in size. They have cash on hand or the ability to obtain financing to pay for the systems and are seeking positive economic returns from investing in solar. These customers may also

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

seek some collateral benefits as well from solar adoption, such as “green” marketing to their own customers or constituents.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 41

The broadening of the photovoltaic market beyond purely environmentally driven residential customers and the growth of the commercial/municipal market bodes well for continuing market expansion. This increasing diversity of customer motivations and types also suggests that the Bay Area may be a reasonable predictor of solar market development in other major U.S. metropolitan regions, as solar adoption becomes less dependent upon the sociopolitical demographics of Northern California and more so upon broad-based, politically neutral motivations.

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

V. Market & Trends

After discussing the characteristics of target customers, we now analyze the overall market and its effect on solar electric dealers. Survey respondents were interviewed about perceived business conditions and expectations, market trends, impact on the industry from certain events, and opportunities and threats for their businesses going forward.

The Solar Electric Market California is the third largest solar market in the world today, partly as a result of the incentives created by the state to encourage the industry’s growth (Starr, Thomas, Bonneville Environmental Foundation, 2004. http://www.californiasolarcenter.org/pdfs/forum/ Solar04-PerfBasedIncent-Pub.pdf). This market’s dramatic growth has been a boon to solar electric dealers, although, ironically, the very success of these programs has created challenges as well. The California photovoltaic market is projected to reach approximately $359 million in 2004, up from $339 million, according to Coast Hills Partners analysis of CEC and other data (see Chapter III, Company Profiles, Revenues section). The California market as a whole grew 34% from 2003 to 2004, with the region surrounding and including the Greater Bay Area growing slightly faster, at 41% (see Chapter VI, Company Approaches to Growth). This region, the primary marketplace for most of the surveyed companies, comprises 51% of the total California market, or $182 million [Figure 17].

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 42

As noted previously, since California makes up a whopping 80% of the U.S. solar electric market, San Francisco and Northern California thus make up 40% of the total U.S. photovoltaic market. This is both the largest regional market in the United States, as well as a substantial market from a worldwide perspective. Analysis of 2003 data from Solarbuzz (http://www.solarbuzz.com/marketbuzz2004-intro.htm) shows that, if broken out separately, the Northern California region

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

would rank 4th in global market size, behind Japan, Germany, and the rest of Europe.

Business Conditions & Future Expectations A clear majority of survey respondents (81%) reported either a substantial improvement in business conditions over the past 24 months or at least some overall improvement [Figure 18], which is consistent with overall market growth. The remainder reported a variety of conditions, ranging from neutral (no change in business conditions in this time period, or some positive change & some negative change) to slightly negative. Negative assessments were all attributed to the declining rebates in California. These have resulted in lower margins for some; lower volumes for others as they see some consumers being priced out of the market by higher net system costs. Others have looked to markets in other states where the incentives are more attractive (e.g., New Jersey). Although these other state markets are relatively tiny today, some dealers are betting that growth there will pick up, similar to growth in California from 2001 to present.

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 43

N

S

Figure 17: 2004 California Solar Electric Market by Regions

Total = $359 Million

San Francisco &

Northern California

51%

Los Angeles &

Central California

37%

San Diego11%

Other California

1%

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

1111

611

0 2 4 6 8 10 12

Number of Respondents

Improved significantly

ImprovedIncreased volume, some decreased

marginStayed same

Improvement out of state; decline in CA

Worsened somewhat

Figure 18: Business Conditions, Last 24 months

Expectations for the future show a similar pattern, although they are not so predominantly optimistic [Figure 19]. The major factor cited behind this change is the instability of California rebate programs. While the existence of the programs and the fact that they are being utilized by so many end-customers is certainly tremendous for dealers, the success of these incentives have sown the seeds of volatility, as program funds have been used faster than expected. Respondents noted that the unexpectedly large drop in the per-Watt rebate in January, 2004, ($.60/Watt instead of the expected $.20/Watt) created a great deal of uncertainty about the predictability of the CEC program going forward. Some respondents felt that this was too large a drop for the market to bear at that stage in its development, particularly as panel shortages have reduced or eliminated the price reductions that were expected to occur as more solar systems were sold. In addition, at the time of the survey, the CEC program was in danger of running out of money if the Governor did not sign A.B. 135, authorizing additional funds to be used this year (it was subsequently signed). Respondents compared the uncertainty and the possible impact if the bill were not signed to a similar, previous situation when the fund ran dry and no rebate checks were signed for a few months. Solar dealers were faced with cash flow crunches in some cases, a fall-

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 44

Positive 81%

Neutral 14%

Negative 5%

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

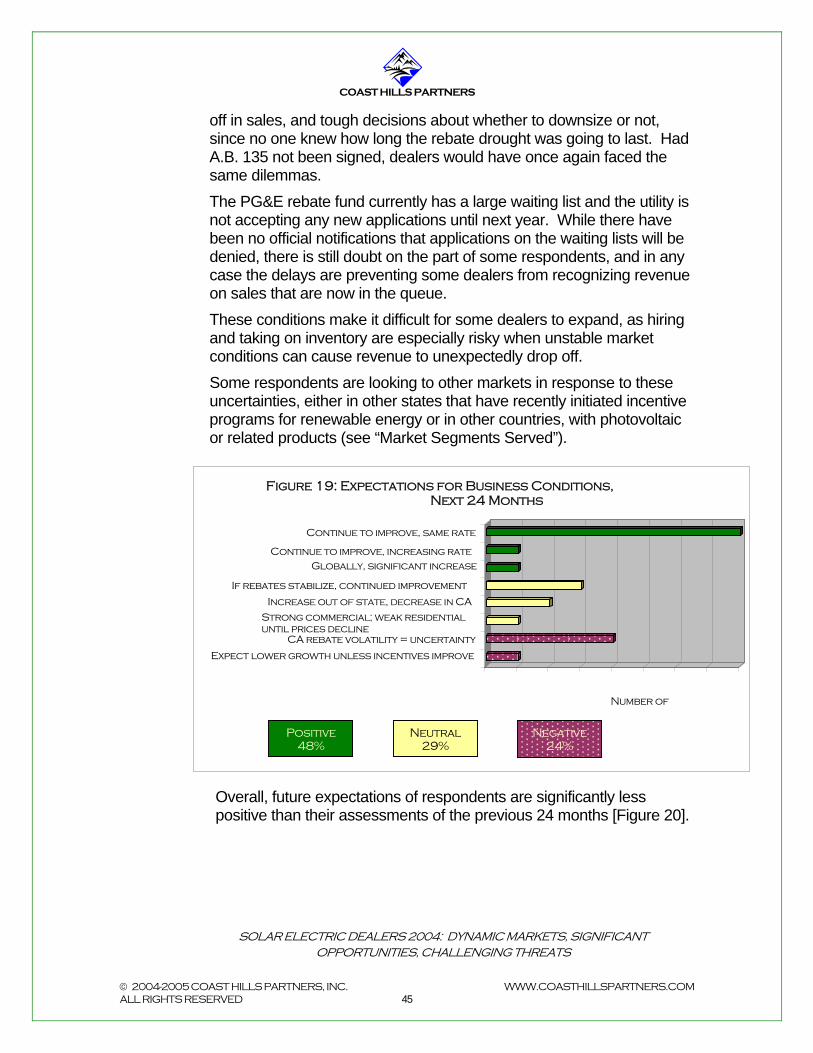

off in sales, and tough decisions about whether to downsize or not, since no one knew how long the rebate drought was going to last. Had A.B. 135 not been signed, dealers would have once again faced the same dilemmas. The PG&E rebate fund currently has a large waiting list and the utility is not accepting any new applications until next year. While there have been no official notifications that applications on the waiting lists will be denied, there is still doubt on the part of some respondents, and in any case the delays are preventing some dealers from recognizing revenue on sales that are now in the queue. These conditions make it difficult for some dealers to expand, as hiring and taking on inventory are especially risky when unstable market conditions can cause revenue to unexpectedly drop off. Some respondents are looking to other markets in response to these uncertainties, either in other states that have recently initiated incentive programs for renewable energy or in other countries, with photovoltaic or related products (see “Market Segments Served”).

Figure 19: Expectations for Business Conditions, Next 24 Months

Continue to improve, same rate

Continue to improve, increasing rateGlobally, significant increase

If rebates stabilize, continued improvement

Increase out of state, decrease in CA

Strong commercial; weak residential until prices decline

CA rebate volatility = uncertainty

Expect lower growth unless incentives improve

Number of

Positive 48%

Neutral Negative 24% 29%

Overall, future expectations of respondents are significantly less positive than their assessments of the previous 24 months [Figure 20].

© 2004-2005 COAST HILLS PARTNERS, INC. WWW.COASTHILLSPARTNERS.COM ALL RIGHTS RESERVED 45

COAST HILLS PARTNERS

SOLAR ELECTRIC DEALERS 2004: DYNAMIC MARKETS, SIGNIFICANT OPPORTUNITIES, CHALLENGING THREATS

5%14%

81%

24%

29%

48%

0%

20%

40%

60%

80%

100%

% o

f

Re

sp

on

se

s

Previous 24months

FutureExpectations

Figure 20: Perceptions of Business Conditions, Past & Future

Positive

Neutral

Negative