Embed Size (px)

Citation preview

NATIONAL ASSOCIATION OFELECTRICAL DISTRIBUTORS

Smart Energy Management Systems: Unlocking Opportunities for Growth

EDUCATION &RESEARCH FOUNDATION

EXECUTIVE SUMMARY

The Smart Energy Management System (SEMS) market is an important strategic opportunity for electrical distributors.

While still in the early stages of adoption, US residential and commercial SEMS market exceeds $3.5B today and is forecasted to surpass $8.3B by 2020.

Market growth is underpinned by strong and accelerating customer demand, and driven by improved solution economics for customers, regulatory compliance, and environmental sentiment.

Distributors perceive SEMS as critical to their company’s success; it is an opportunity for both competitive differentiation and to evolve traditional distributor business models.

While most electrical distributors are taking some steps to capitalize on the SEMS opportunity, few believe they are executing against a fully-developed strategy.

•

•

•

•

EDUCATION &RESEARCH FOUNDATION

The SEMS market consists of lighting and HVAC sensing, control, and automation technology

SEMS Market Definition

Drainage Water Reuse System

Elevator Monitoring System

Video MonitoringSystem

Room Access Control System

Disaster Prevention System

Building Energy Management Software

MO

NIT

OR

ING

/ C

ON

TRO

LA

UTO

MA

TIO

NA

CTI

VA

TIO

N

Lighting Control Systems

Controllers

Sensors (occupancy, light)

Batteries

Display Devices

HVAC Control Systems

Controllers

Sensors (temp, humidity, CO2)

Batteries

Display Devices

Other EMS Systems1 (e.g. plug load control)

Controllers

Sensors

Batteries

Display Devices

Smart appliances

SEM

S M

arke

t

Light Bulbs, Light Fixtures, Wiring,

Other

Fans, Condensers, Wiring, Other

Traditional appliances

EDUCATION &RESEARCH FOUNDATION

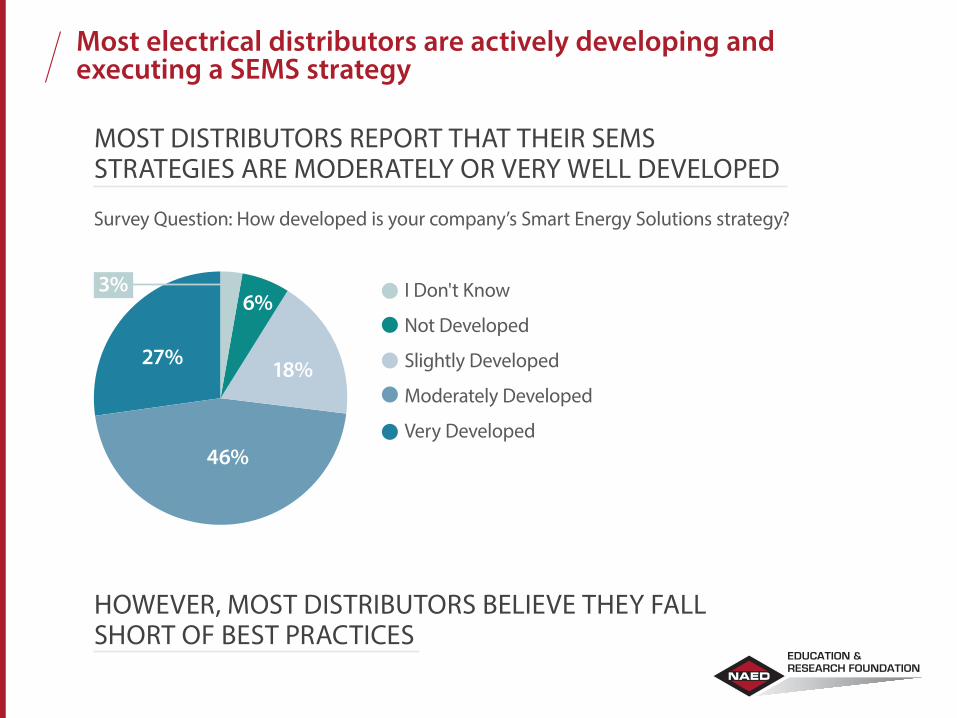

Most electrical distributors are actively developing and executing a SEMS strategy

MOST DISTRIBUTORS REPORT THAT THEIR SEMS STRATEGIES ARE MODERATELY OR VERY WELL DEVELOPED

HOWEVER, MOST DISTRIBUTORS BELIEVE THEY FALL SHORT OF BEST PRACTICES

Survey Question: How developed is your company’s Smart Energy Solutions strategy?

46%

27% 18%

6% I Don't Know

Not Developed

Slightly Developed

Moderately Developed

Very Developed

3%

EDUCATION &RESEARCH FOUNDATION

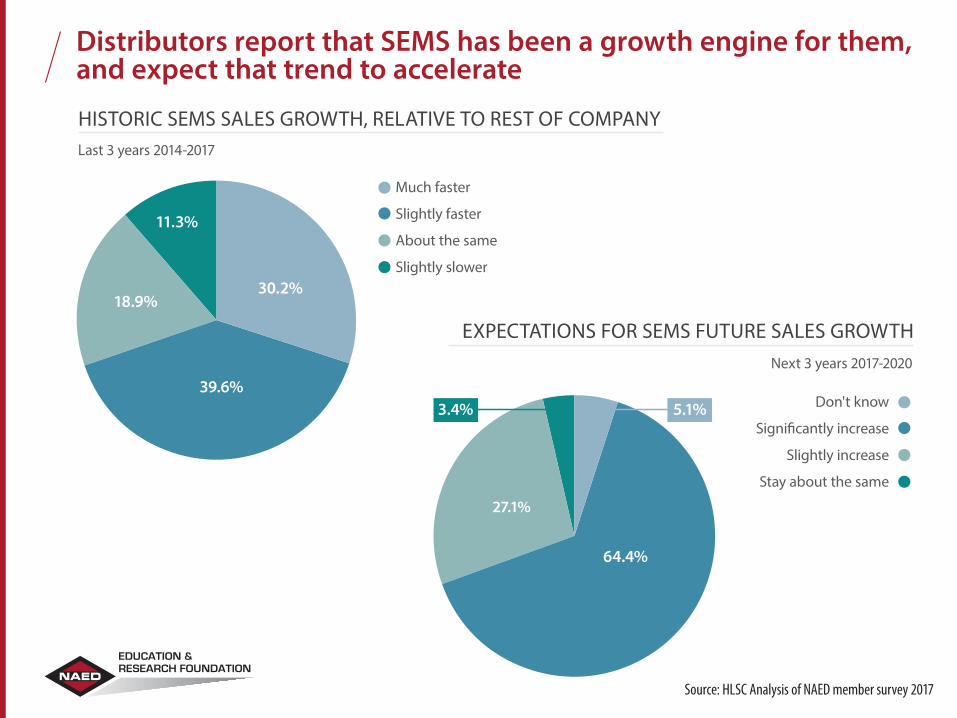

Distributors report that SEMS has been a growth engine for them, and expect that trend to accelerate

18.9%

Much faster

Slightly faster

About the same

Slightly slower

39.6%

30.2%

11.3%

HISTORIC SEMS SALES GROWTH, RELATIVE TO REST OF COMPANYLast 3 years 2014-2017

Source: HLSC Analysis of NAED member survey 2017

EXPECTATIONS FOR SEMS FUTURE SALES GROWTH

Don't know

Significantly increase

Slightly increase

Stay about the same

64.4%

Next 3 years 2017-2020

3.4% 5.1%

27.1%

EDUCATION &RESEARCH FOUNDATION

SEMS Segmentation SEMS are a part of all markets in the electrical distribution channel: residential, commercial and industrial. Due to the extensive scope of the SEMS topic, this study focused on resi-dential and commercial segments. Some of the insights shared in the SEMS survey taken by NAED members are reflected here. The full survey analysis is in Part 1 of Smart Energy Systems: Unlocking Opportunities for Growth.

27.1%

End customers decide if and how to include SEMS in their retrofit plans

Architects & Engineers specify

types of SEMS to be included

in project

4

Contractors perform detailed engineering

and decide what types of SEMS will be

included in project

5

6

NEW

CO

NST

RUC

TIO

NRE

TRO

FIT

DIY Retrofit

Custom Single-Family Homes and

Large Retrofits

1

New Tract and Multi-Family

Homes

2

3

Residential SegmentBy type of home and project

Commercial SegmentBy project type and decision maker

EDUCATION &RESEARCH FOUNDATION

Residential SEMS segment is substantially smaller than commercial, but is growing at a rapid pace

27.1%

RESIDENTIAL SEGMENT COMPRISES <15% OF MARKET…

Residential

Commercial

2015

3.1

0.5

3.5

2020

7.1

1.2

8.3North America, USD Billion

19%

EDUCATION &RESEARCH FOUNDATION

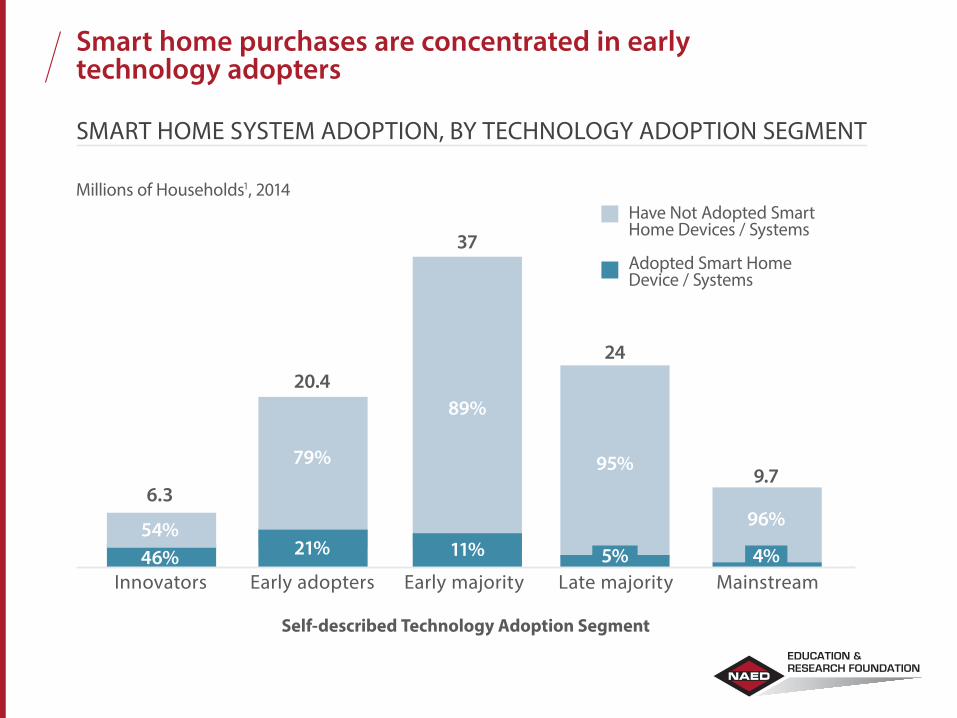

Smart home purchases are concentrated in early technology adopters

SMART HOME SYSTEM ADOPTION, BY TECHNOLOGY ADOPTION SEGMENT

Have Not Adopted Smart Home Devices / Systems

Adopted Smart Home Device / Systems

Innovators Early adopters Early majority Late majority Mainstream

Millions of Households1, 2014

54%

6.3

46%

79%

20.4

21%

89%

37

11%

95%

24

5%

96%

9.7

4%

Self-described Technology Adoption Segment

EDUCATION &RESEARCH FOUNDATION

Commercial segment represents a $3.1B opportunity, and is concentrated in new construction projects

COMMERCIAL SEGMENT COMPRISES 85%+ OF SEMS MARKET…

Residential

Commercial

2015

3.1

0.5

3.6

2020

7.1

1.2

8.3North America, USD Billion

18%

EDUCATION &RESEARCH FOUNDATION

As Electrical Distributors look to advance their SEMS business, addressing key barriers to adoption will be essential

COMMERCIAL SEMS ADOPTION BARRIERS (AVERAGE RATING)

Upfront costs too high

End customers unaware of benefits

Architects/ Engineers lack technical knowledge

Architects/ Engineers unaware of benefits

Savings potential too low

Integration challenges

Security concerns

Technology not yet sufficiently developed

Other

Despite cost declines and increasing benefits of rapidly evolving SEMS solutions, greater education and awareness will be critical to driving commercial adoption.

NoImpact

LittleImpact

ModerateImpact

HighImpact

EDUCATION &RESEARCH FOUNDATION

Download the full report at naed.org/sems

EDUCATION &RESEARCH FOUNDATION