Embed Size (px)

Citation preview

1

Cautionary Notice

Statements in this presentation which are not purely historical facts or which necessarily depend upon future events,

including statements about forecasted financial performance or other statements about anticipations, beliefs, expectations,

hopes, intentions or strategies for the future, may be forward-looking statements within the meaning of Section 27A of the

Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended. Readers are

cautioned not to place undue reliance on forward-looking statements. All forward-looking statements in this presentation

are based upon information available to Builders FirstSource, Inc. on the date of this presentation. Except as required by

law, Builders FirstSource, Inc. undertakes no obligation to publicly update or revise any forward-looking statements,

whether as a result of new information, future events or otherwise. Any forward-looking statements involve risks and

uncertainties that could cause actual events or results to differ materially from the events or results described in the

forward-looking statements, including risks or uncertainties related to the Company’s revenues and operating results

being highly dependent on, among other things, the homebuilding industry, lumber prices and the economy. Builders

FirstSource, Inc. may not succeed in addressing these and other risks. Further information regarding factors that could

affect our financial and other results can be found in the risk factors section of Builders FirstSource, Inc.’s most recent

Form 10-K filed with the Securities and Exchange Commission. Consequently, all forward-looking statements in this

presentation are qualified by the factors, risks and uncertainties contained therein

Use of Non-GAAP Financial Measures

This presentation includes financial measures and terms not calculated in accordance with accounting principles generally

accepted in the United States (“GAAP”) in order to provide investors with an alternative method for assessing our

operating results in a manner that enables investors to more thoroughly evaluate our current performance as compared to

past performance. We believe these non-GAAP measures provide investors with a better baseline for modeling our future

earnings expectations. Our management uses these non-GAAP measures for the same purpose. We believe that our

investors should have access to the same set of tools that we use in analyzing our results. These non-GAAP measures

should be considered in addition to results prepared in accordance with GAAP, but should not be considered a substitute

for or superior to GAAP results. Our calculations of non-GAAP measures are not necessarily comparable to similarly

titled measures reported by other companies. Schedules that reconcile non-GAAP financial

measures to their GAAP equivalents are included later in this presentation.

Safe Harbor & Non-GAAP Financial Measures

2

Contents

Section 1 Company Overview 3

Section 2 Industry Update 9

Section 3 Investment Highlights 13

Section 4 Financial Overview 19

Section 5 Reconciliation of Non-GAAP Financial Measures 27

Company Overview

4

Prefabricated Components Lumber & Lumber Sheet Other Products & Services

Products include

dimensional lumber,

plywood and oriented

strand board (“OSB”)

Factory-built substitutes

for job side-framing

including floor trusses,

roof trusses, wall

panels, stairs, and

engineered wood

Cabinets, gypsum,

roofing and insulation.

Services include turn-

key framing, shell

construction, design

assistance, and

installation

Windows & Doors Millwork

Manufacturing,

assembly and

distribution of

aluminum and vinyl

windows

Assembly and

distribution of interior

and exterior door units

Distribution of interior

trim, exterior trim,

columns and posts.

Manufacturing of custom

exterior features under

the Synboard™

brand name

Third largest building products provider1 operating in the estimated $129.2 billion single family residential

home construction market2

The Company is a fully-integrated supplier, manufacturer and installer of structural and related building

products

Company Overview

Notes:

1 According to ProSales Magazine among those with manufacturing capabilities, based on 2011 revenues

2 2012 National Association of Home Builder (“NAHB”)

5

Revenue Distribution

Approximately half of BFS sales are from value added product categories — Prefabricated

Components, Millwork and Windows & Doors

Over 20% of sales are related to our installation services

Fiscal Year 2012 March YTD 2013

6

Top 10 customers represented approximately 23% of total sales, with no one customer

exceeding 5% for FY 2012

Customer mix consists of large national homebuilders, regional homebuilders and local

builders

Approximately 15% of sales are related to light commercial and multi-family construction

Our Customers

7

BFS has operations in 33 markets in 9 states primarily in the southern and eastern regions of the United States

BFS is in 16 of the nation’s

top 50 Metropolitan Statistical

Areas (as ranked by single

family housing permits)

Approximately 45% of 2012

U.S. housing permits were

issued in states in which BFS

operates

53 distribution centers and 44

manufacturing facilities, some

of which are co-located

Geographic Footprint

North East

Emmitsburg Frederick

Port of Rocks

Hagerstown

Manassas

Culpeper

Washington

Hillsborough

High Point

Bristol

Piney Flats Kingsport

Johnson City

Knoxville Asheville

Hendersonville

Brevard Cashiers

Blairsville

Gainsville

Atlanta

LaGrange

Columbus

CherryPoint

Edisto Island

Johns Island

Charleston

Pawleys Island

Columbia

Sumter Goose Creek

Conway Loris

Florence

Anderson

Seneca Greenville

Spartanburg

Cowpens

Charlotte

Aberdeen

Fayetteville

Southport

Wilmington Wilmington

Nashville

Chelsea

Shelby

Auburn

Jacksonville Freeport

Tampa

Bunnell

Orlando

West Palm Beach

Dallas Headquarters

Lewisville

Arlington

Grand Prairie

Houston

San Antonio

Austin

Apex

Clarksville

8

Strong Market Position

BFS is the third largest building products provider in an estimated

$129.2 billion single family residential construction market1

Building Products Suppliers with Manufacturing Capabilities

Note:

1 2012 NAHB

Pro Distributor % Change

ProBuild Holdings $2,838 $3,045 -6.8%

84 Lumber 1,278 1,378 -7.2%

Builders FirstSource 779 700 11.3%

Stock Building Supply 735 818 -10.1%

BMC 631 570 10.7%

Carter Lumber 557 535 4.2%

US LBM 429 270 59.3%

Harvey Building Products 400 n/m n/m

McCoy’s Building Supply 380 377 0.6%

Golden State Lumber 213 212 0.4%

Source: ProSales Magazine, 2011 & 2010

2011 Pro Segment

Sales ($mm)

2010 Pro Segment

Sales ($mm)

Industry Update

10

Recent downturn in residential new construction market is without precedent since World War II

Since 2008, housing starts have been well below the long term trend of 1.5 million total starts and

1.1 million single family starts.

Overbuild/Underbuild

New Construction Market Trends

11

The residential new construction market has experienced a substantial downturn in recent

years as a result of the recession

The downturn resulted in the largest decline in housing starts since the Great Depression

falling by 73% from the 2005 peak to the current trough

Building products sales have had a corresponding decline

Trends that will drive a recovery in U.S. housing demand include:

Low interest rates, the aging of housing stock, and population growth due to

immigration and birthrates exceeding death rates

The National Association of Home Builders (“NAHB”) is predicting that 2013 U.S.

single family housing starts will grow approximately 24% from 2012, with

approximately 664,000 single family housing starts predicted

NAHB predicts single family housing starts will increase to 855,000 in 2014,

representing a 29% increase over the 2013 forecast

The Macro Environment

BFS is well positioned to take advantage of anticipated renewed demand

12

Commodity Price Trends

Commodity prices have steadily increased since the beginning of the 2012. Higher commodity prices

will typically result in increased gross profit dollars and improved EBITDA flow through.

Investment Highlights

14

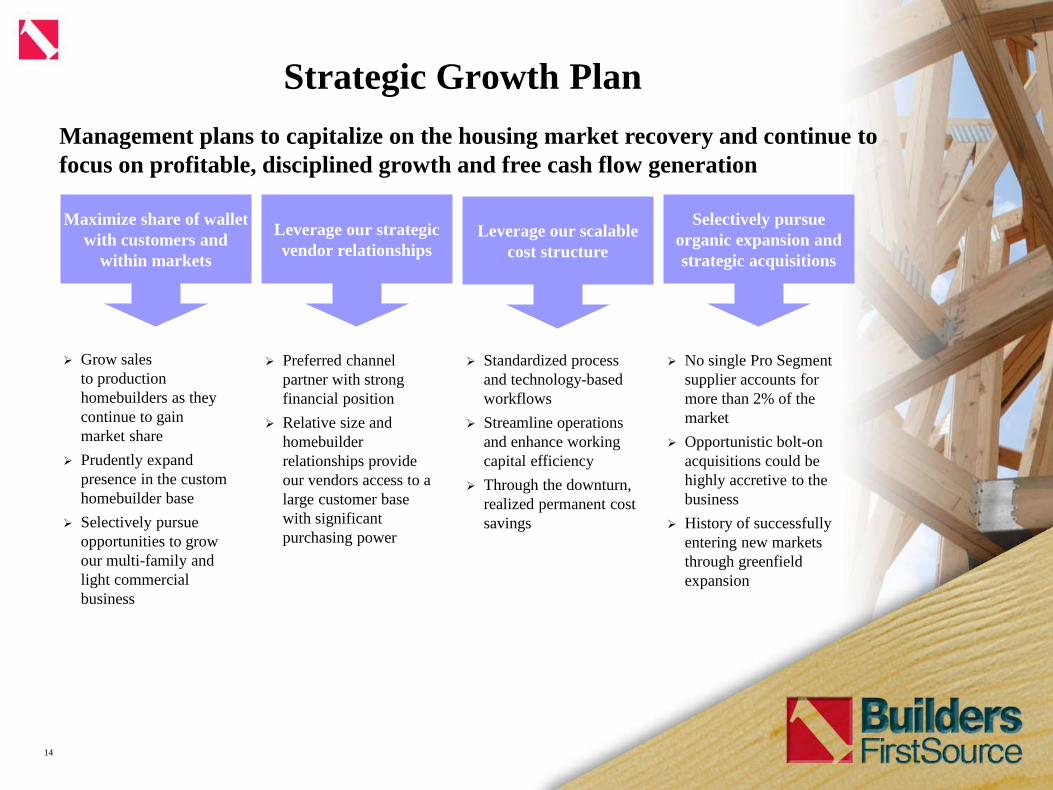

Strategic Growth Plan

Management plans to capitalize on the housing market recovery and continue to

focus on profitable, disciplined growth and free cash flow generation

Maximize share of wallet

with customers and

within markets

Leverage our strategic

vendor relationships

Leverage our scalable

cost structure

Selectively pursue

organic expansion and

strategic acquisitions

Grow sales

to production

homebuilders as they

continue to gain

market share

Prudently expand

presence in the custom

homebuilder base

Selectively pursue

opportunities to grow

our multi-family and

light commercial

business

Preferred channel

partner with strong

financial position

Relative size and

homebuilder

relationships provide

our vendors access to a

large customer base

with significant

purchasing power

Standardized process

and technology-based

workflows

Streamline operations

and enhance working

capital efficiency

Through the downturn,

realized permanent cost

savings

No single Pro Segment

supplier accounts for

more than 2% of the

market

Opportunistic bolt-on

acquisitions could be

highly accretive to the

business

History of successfully

entering new markets

through greenfield

expansion

15

Fully Integrated Distribution Platform

BFS has an integrated business model that differentiates it from

competitors that operate with a decentralized collection of facilities

Network of 53 distribution centers and 44 manufacturing facilities, some which are co-

located

Size of facilities tailored to each market to meet customer needs

Offering large-scale, full-service branches in larger markets and smaller, more tailored

facilities in secondary markets

Highly customized, proprietary information technology system drives internal efficiencies

allowing the Company to respond rapidly to customers and reduce their costs

BFS operates and owns the source code to its enterprise resource planning (“ERP”)

computer system that is tailored to the building supply industry in addition to laser

technology that facilitates precision, speed and efficiency in the manufacturing process

16

Due to the breadth of its product offering (65,000 SKUs), BFS functions as a “one-stop shop”

Homebuilders value the convenience and efficiency of using one supplier throughout building process

BFS provides customers with a full range of services including professional installation, turn-key

framing and shell construction and design

BFS’s salespeople are typically trained homebuilders who understand the challenges that might be

encountered at the job site

Just-in-time delivery of just the right amount of product

Value-added advice and consultation on engineering, building codes and other building matters

BFS acts as both a supplier and advisor to the homebuilding customer

Supplier to

Homebuilders

Trusted Consultant

Full Offering of Manufactured Products and

Construction Services

17 17

Experienced Management Team

Lou Davis Vice President – Manufacturing

Morris E. Tolly Senior Vice President – Operations

Floyd F. Sherman President and CEO

Chad Crow Senior Vice President and CFO

13 years of industry experience

Prior experience: Director of Accounting at Pier One Imports and five

years experience with PriceWaterhouse

Over 40 years of industry experience

Prior experience: Area Manager at Pelican Companies, Inc.

Over 40 years of industry experience

Prior experience: Chairman & CEO of Triangle Pacific / Armstrong

Flooring

Area VPs

Over 40 years of industry experience

Prior experience: Manufacturing management positions with Wickes, Inc.,

Fabricon, Inc., National Homes Corp

Average BFS tenure of 20 years

Donald F. McAleenan Senior VP and General Counsel

20 years of industry experience

Prior experience: VP & Deputy General Counsel of Fibreboard, Asst

General Counsel of AT&E, nine years as a securities lawyer

18

Summary

Experienced

Management

Team

Sustained

investment

through the cycle

Fully-integrated

industry-leading

IT system

Comprehensive

value-added

approach to

customer service

Market

Leadership in

Attractive

Fragmented

Markets

Differentiating factors that will enhance BFS’s ability to take advantage of housing

recovery

Financial Overview

20

Review of 2012 Operating Results

Sales for 2012 were 37.4% higher than 2011 primarily driven by volume, and to a lesser extent,

commodity price inflation

U.S. single family housing starts (South region) were up only 23.1% over the same period

U.S. single family units under construction (South region) were up only 7.7% over the same

period

Combination of these data points, indicate market share gains

Gross margin decreased slightly from 20.3% in 2011 to 20.0% in 2012. Increased sales volume was

offset by intra-quarter commodity lumber price inflation relative to quarterly customer pricing

commitments. Higher than expected sales volume resulted in us replacing inventory during the latter

half of the quarters at higher costs.

Selling, general, and administrative expenses have been monitored closely by management and as a

percentage of sales decreased from 24.2% in 2011 to 20.4% in 2012 (excluding stock compensation

expense)

FY 2012 Adjusted EBITDA improved $21.4 million – $6.4 million compared to ($15.0) million in

2011

21

After declines in 2007-2009, revenues stabilized in 2010 then grew 11% in 2011 and 37% in 2012

Historical margins demonstrate the potential for expansion from current margins as the business

builds toward historical scale and leverages a leaner cost structure

Proven ability to conserve capital through tight working capital management and reduced capital

spending

Summary Financial Performance

$mm except Sales per SF Start 2005 2006 2007 2008 2009 2010 2011 2012

South Region Single Family Housing Starts1

831,300 756,500 539,500 323,600 232,100 247,200 229,200 282,100

South region sales per SF start $2,572 $2,728 $2,722 $3,066 $2,921 $2,833 $3,399 $3,795

U.S. Single Family Housing Starts1

1,715,800 1,465,300 1,046,100 622,000 445,000 471,100 430,500 534,600

U.S. sales per SF start $1,246 $1,408 $1,404 $1,595 $1,523 $1,487 $1,810 $2,003

Total Revenue $2,138.1 $2,063.5 $1,468.4 $992.0 $677.9 $700.3 $779.1 $1,070.7

% growth -3.5% -28.8% -32.4% -31.7% 3.3% 11.2% 37.4%

Gross Profit $543.4 $544.8 $363.2 $215.5 $142.4 $131.8 $157.9 $214.6

% margin 25.4% 26.4% 24.7% 21.7% 21.0% 18.8% 20.3% 20.0%

Operating Expenses2

$388.6 $401.5 $341.9 $280.0 $201.4 $194.1 $193.0 $222.3

% revenue 18.2% 19.5% 23.3% 28.2% 29.7% 27.7% 24.8% 20.8%

Adjusted EBITDA3

$172.7 $169.9 $53.2 ($32.4) ($35.1) ($43.6) ($15.0) $6.4

% margin 8.1% 8.2% 3.6% -3.3% -5.2% -6.2% -1.9% 0.6%

Capex4

$29.7 $27.2 $10.1 $8.2 $2.1 $9.0 $4.8 $10.4

% revenue 1.4% 1.3% 0.7% 0.8% 0.3% 1.3% 0.6% 1.0%

Net Working Capital as % of Revenue5

10.0% 10.4% 11.6% 12.2% 10.2% 9.3% 10.0% 10.0%

Notes:

1 Source: U.S. Census

2 2005 operating expenses adjusted to exclude $35.5mm anti-dilution payment to stock option holders

3 See Adjusted EBITDA reconciliation on page 28

4 2005 and 2006 capex includes expansion expenditures.

5 Calculated as monthly average of net working capital divided by total annual revenue

Fiscal Year

22

Recent Quarterly Performance

Recent quarterly performance demonstrates strong revenue trends with six

consecutive quarters of revenue growth greater than 30%

Q2 Q3 Q4 2012 2012 2012 2012 2013

$mm except Sales per SF Start 2011 2011 2011 Q1 Q2 Q3 Q4 Q1

South Region Single Family Housing Starts1

63,800 61,700 51,600 62,000 77,200 78,100 65,300 79,000

South region sales per SF start $3,235 $3,520 $3,734 $3,539 $3,522 $3,736 $4,404 $4,047

U.S. Single Family Housing Starts1

123,400 117,700 99,900 105,500 151,100 150,100 128,600 135,200

U.S. sales per SF start $1,673 $1,845 $1,929 $2,080 $1,799 $1,944 $2,236 $2,365

Total Revenue $206.4 $217.2 $192.7 $219.4 $271.9 $291.8 $287.6 $319.7

% growth y-o-y -2.4% 20.4% 31.0% 34.7% 31.7% 34.3% 49.2% 34.7%

Gross Profit $42.8 $44.4 $39.3 $45.1 $53.7 $57.7 $58.1 $62.3

% margin 20.7% 20.4% 20.4% 20.6% 19.7% 19.8% 20.2% 19.5%

Operating Expenses $49.0 $50.2 $47.1 $50.8 $55.0 $58.7 $57.8 $61.1

% revenue 23.7% 23.1% 24.4% 23.2% 20.2% 20.1% 20.1% 19.1%

Adjusted EBITDA2

($1.3) ($0.7) ($3.3) ($2.1) $2.1 $3.0 $3.4 $5.4

% margin -0.6% -0.3% -1.7% -1.0% 0.8% 1.0% 1.2% 1.7%

Capex $1.1 $1.1 $2.1 $1.7 $2.3 $5.2 $1.2 $1.0

% revenue 0.5% 0.5% 1.1% 0.8% 0.8% 1.8% 0.4% 0.3%

Notes:

1 Source: U.S. Census

2 See Quarterly Adjusted EBITDA reconciliation on page 29

23

Market Share Gains

Consistent growth in sales per single-family housing start indicates market share

gains

24

Sales & Adjusted EBITDA Trends

Consistent sales and adjusted EBITDA growth

Six straight quarters of y/o/y sales growth greater than 30%

Nine straight quarters of y/o/y adjusted EBITDA improvement

25

March YTD 2013 Update

Sales for Q1 2013 were $319.7 million, a 45.7% increase over sales of $219.4 million for Q1 2012

Sales growth estimated to be driven by volume (29.7%) and price (16.0%)

U.S. single family housing starts (South region) were up only 27.4% over the same period

U.S. single family units under construction (South region) were up only 23.2% over the same

period

Gross margin was 19.5% for Q1 2013 compared to 20.6% for Q1 2012. Increased sales volume was

offset by intra-quarter commodity lumber price inflation relative to quarterly customer pricing

commitments.

At March 31, 2013, our LTM Adjusted EBITDA had improved $7.5 million – $5.4 million

compared to ($2.1) million for the same period in 2012

26

Capital Structure Summary

$mm 3/31/2013 Coupon Maturity Call Provisions

Cash & Cash Equivalents $117.7

Term Loan *

225.0 L+950 bps (2% Libor floor) Sep-15 Interest make-whole through Dec 2014

Second-lien Floating Rate Notes 139.7 L+1000 bps (3% Libor floor) Feb-16 Currently callable at 100

Other debt 4.0

Total Debt 368.7

Stockholders' Equity 37.1

Total Capitalization 405.8

Net Debt $251.0

* Financing also includes a stand-alone LC facility that provides for the issuance of up to $10mm letters of credit and a sub-facility that

provides for the issuance of up to $15mm letters of credit

Reconciliation of

Non-GAAP Financial Measures

28

Adjusted EBITDA Reconciliation

$mm 2005 2006 2007 2008 2009 2010 2011 2012

Net Income (Loss) $48.6 $68.9 ($23.8) ($139.5) ($61.9) ($95.5) ($65.0) ($56.9)

Reconciling Items:

Depreciation & amortization 16.9 20.4 22.4 20.8 17.9 15.4 14.0 11.1

Interest expense 47.2 28.7 27.7 25.6 27.0 31.7 24.9 45.1

Income tax expense (benefit) 27.0 43.3 (4.3) (17.7) (30.8) (1.1) 2.2 0.6

(Income) loss from discontinued operations, net of tax (3.6) 2.3 21.1 18.9 5.0 1.2 0.4 2.4

Asset impairments - - 0.4 46.9 0.5 0.8 - 0.0

Stock compensation expense 0.0 4.1 7.0 8.5 2.9 4.3 4.6 3.6

Litigation settlement - - - - - (1.2) - (0.6)

Transaction costs - - 1.1 2.8 3.2 (0.0) 1.2 -

Facility closure costs 0.8 0.6 0.1 1.2 1.2 0.6 2.5 1.0

Anti-dilution payment to stock option holders 35.5 - - - - - - -

Other 0.2 1.6 1.5 (0.1) (0.0) 0.2 0.2 (0.0)

Adjusted EBITDA $172.7 $169.9 $53.2 ($32.4) ($35.1) ($43.6) ($15.0) $6.4

Fiscal Year

29

Quarterly Adjusted EBITDA Reconciliation

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

$mm 2011 2011 2011 2012 2012 2012 2012 2013

Net Loss ($15.5) ($11.6) ($16.7) ($19.2) ($12.1) ($13.6) ($12.0) ($11.8)

Reconciling Items:

Depreciation & amortization 3.5 3.4 3.5 2.9 2.5 2.9 2.9 2.8

Interest expense 5.7 5.3 8.1 13.1 10.5 10.6 11.0 12.5

Income tax expense (benefit) 1.7 0.3 0.3 0.2 0.1 0.0 0.2 0.3

Loss from discontinued operations, net of tax 0.1 0.1 0.1 0.1 0.1 1.3 1.0 0.2

Stock compensation expense 0.9 1.7 0.9 0.8 0.9 0.9 1.0 1.3

Transaction costs 0.3 - - - 0 0 - -

Facility closure costs 1.9 0.1 0.4 0.1 0.1 0.7 0.1 0.1

Other 0.1 (0.0) 0.1 0.0 (0.0) 0.0 (0.6) (0.0)

Adjusted EBITDA ($1.3) ($0.7) ($3.3) ($2.1) $2.1 $3.0 $3.4 $5.4