Embed Size (px)

Citation preview

Anton Fedorov BURAN VENTURE CAPITAL

tonyfedorov.com

Table of contents

1. Venture Capital overview

What is VC?

Business model

Risks – Reward curve

2. Investment framework

Team

Business Specifics

Market Opportunity

Exit returns

Risk mitigation

3. Lessons learned

2

3

What is Venture capital and why it exists.

Venture capital (VC) is type of funding for a new or growing business which usually involves

high risk financial risks.

Difficult for traditional financiers (banks / capital markets) to fund these firms due to low credible information and low ticket sizes

VC’s address with three key mechanisms:

Sorting: picking the right entrepreneurs.

Controlling: limiting “agency” problems, through

a mixture of incentives and monitoring.

Certifying: developing a tradition of quality and

fair dealings.

What

Why

Venture Capital overview

VС Business / Economic Model

4

Assets

Investments

Entry

Deal sourcing

Due diligence

Decision making

Deal documentation

Value creation

“6-month plan”

Portfolio review:

Budgeting & strategic decision-making

HR

Exit

Decision making

Organizing exit process

Deal documentation

KPIs

Cash-on-cash multiple also known as

multiple of cost

IRR

Liabilities – Limited Partner commitment

Investment team

Track record

Investment philosophy (investment themes, investment approach)

Investment strategy (deal sourcing, structuring, return targets / risk-reward curve)

Fundraising

Key deal metrics with LPs:

Carried interest rate (standard rate 20%)

Hurdle rate (standard rate 8%)

Management fee (standard rate 2%)

Equity – General Partner commitment

“Skin in the game”

Income

statement

Fund & investors Fund managers

Investment income (+) MF income (+)

Investment cost (-) Carry income (+)

Deal expenses (-) Operational expenses (-)

Gross result / IRR

Net income / (loss)MF expense (-)

Carry expense (-)

Net result / IRR

Venture Capital overview

5

Risk – reward curve

100%

30%

10%

1%

3%

Venture Capital overview

VC’s goal is to provide 5-10x gross return over

7-10 years timeframe

To accomplish one must focus not just on

excess returns, but protecting downside

64.8%

25.3%

5.9%2.5% 1.1… 0.4%

32.4%

48.6%

11.3%

4.8%2.1% 0.8%

0-1x 1-5x 5-10x 10-20x 20-50x 50x+

Gross return based of companies '04-'13Simulated returns if losses reduced by 50%

By % of financings in companies going out-of-

business, acquired, or IPO ‘04-’13. N = 21,460 3

Gross realized Multiple range

% o

f finan

cin

gs

Gross return: 7.5%

Cash-on-cash return: 2.1x

Realized

14.7%

3.9x

Simulated:

Targ

et

retu

rns

Risk

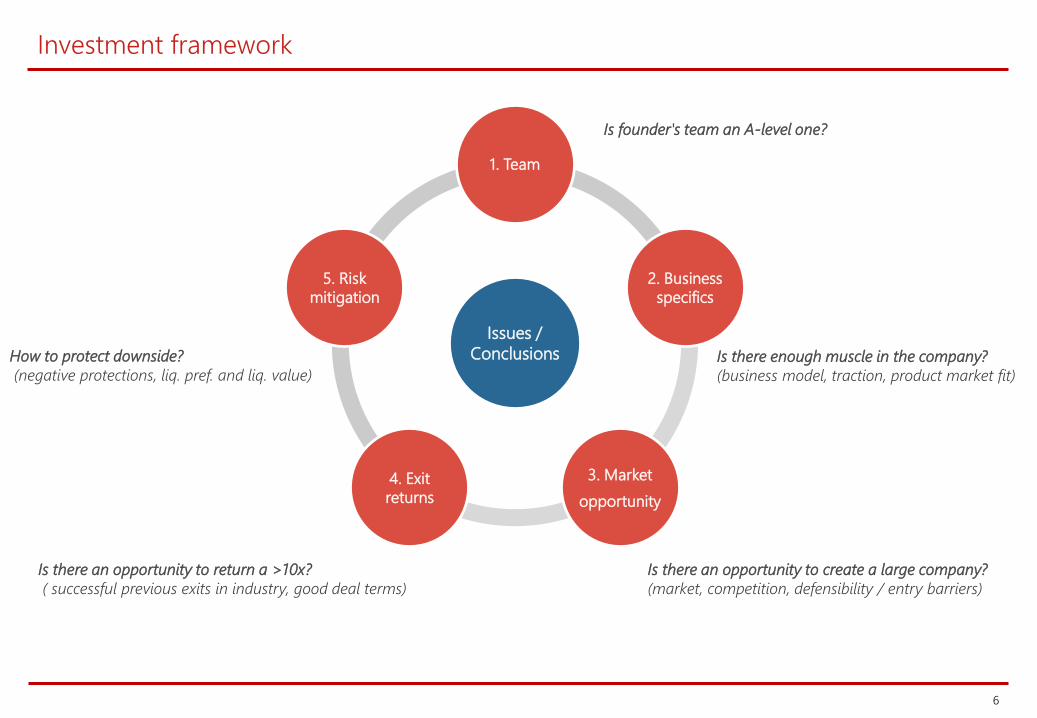

Investment framework

6

Issues /

Conclusions

1. Team

2. Business

specifics

3. Market

opportunity

4. Exit

returns

5. Risk

mitigation

How to protect downside?

(negative protections, liq. pref. and liq. value)

Is founder's team an A-level one?

Is there enough muscle in the company?

(business model, traction, product market fit)

Is there an opportunity to create a large company?

(market, competition, defensibility / entry barriers)

Is there an opportunity to return a >10x?

( successful previous exits in industry, good deal terms)

1. Team:

7

Is founder's team an A-level one?

• Sufficient management team industry expertise

• Serial entrepreneurs

• Founders’ capital contribution US$150k+

• Multiple founders

1

Integrity:

Qualities of Founders:

Reduce asymmetry of

information risk

Goal to accomplish

Reduce founder “flight” risk

Reduce chance of failure

Reduce chance of failure

Scoring questions

Passionate vision:

Experience & expertize:

Leadership:

Commitment.

Cash contribution

Time

Reduce founder “flight” and

asymmetry of information risk

Investment framework

2. Business specifics

8

Scoring questions

• Buran primary investment theme

• First revenues recorded

• Multiple sources of revenue

• Tested and scalable business model

• No external working capital funding required

• Breakeven achievable with Buran investment

2

Business and Financial Metrics

Revenue recurrence (ARR / MRR)

Customer Concentration Risk

Gross margin

LTV (Life Time Value)

CAC

Product and Engagement Metrics

Downloads / Active Users / Customers

Month-on-month (MoM) growth

Net Promoter Score (NPS)

Cohort Analysis / churn:

Gross churn

Net churn

Is there enough muscle in the company?

Company metrics: Threshold levels:

MRR > US$40k

Concertation <15%

margins > 30%

LTV / CAC >4-5x

CAC payback 6-9 months

100’s of paying customers / 100k’s of users

Growth is >2-2.5x y/y, >10-15% M/M

NPS >0

Gross (max): -10% per annum for SaaS or

20% for marketplaces

Net is hopefully negative

Investment framework

• Addressable market size US$100m+

• Market CAGR for next three years 50%+

• #1 position in niche achievable

• Sufficient entry barriers

3

3. Market opportunity

9

Is there an opportunity to create a large company?

Scoring questionsMarket metrics: Threshold levels:

Market Size:

TAM (Total Addressable),

SAM (Served/Serviceable Available),

SOM (Serviceable & Obtainable)

SAM Market growth

HHI of customers

Competition

HHI of competitors

Porter’ 5 Forces analysis

Opportunity timing

Regulatory changes

Technology adoption

UX / Behaviors shifts

SAM >US$100-150m

SOM share 20-30%

in 5-7 years

20-50%

Highly fragmented market

HHI* - Herfindahl-Hirschman Index

Few competitors

Bitcoins

Whatsapp, Youtube, Dropbox, Autonomous driving

Examples:

Dating, Taxi, Snapchat

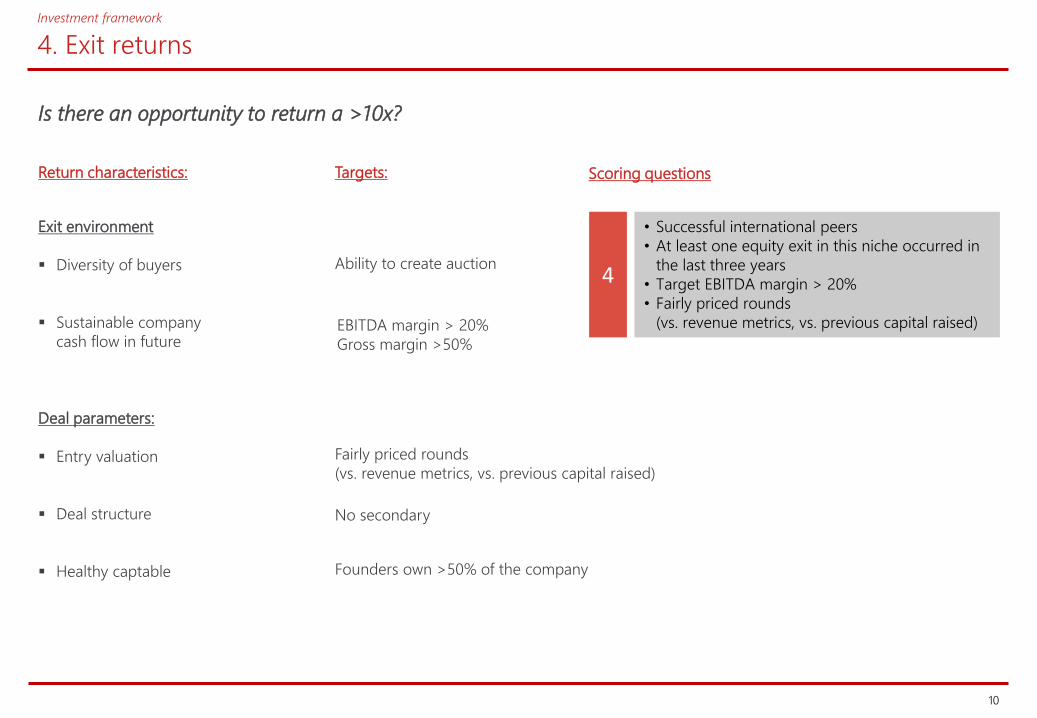

Investment framework

• Successful international peers

• At least one equity exit in this niche occurred in

the last three years

• Target EBITDA margin > 20%

• Fairly priced rounds

(vs. revenue metrics, vs. previous capital raised)

4

4. Exit returns

10

Is there an opportunity to return a >10x?

Scoring questionsReturn characteristics: Targets:

Exit environment

Diversity of buyers

Sustainable company

cash flow in future

Deal parameters:

Entry valuation

Deal structure

Healthy captable

Investment framework

Fairly priced rounds

(vs. revenue metrics, vs. previous capital raised)

No secondary

Founders own >50% of the company

EBITDA margin > 20%

Gross margin >50%

Ability to create auction

5. Risk mitigation

11

How to protect downside?

Scoring questionsRisk mitigation:

Portfolio diversification:

Minority protective provisions:

Board seat

Reps and warranties

Covenants

Pre- and post-closing conditions

Anti-dilution provisions

Liquidity rights / transfer provisions (tag, drag,

pre-emptions, ROFR, CoC)

Information rights

Indemnities (protection if rights are breached)

• Investment size between US$500-5,000k

• Liquidation preference over 1x

• Liquidation value over BVC investment size

• Board seat and minority protective provisions

• Positive feedback from industry experts

5

Investment framework

Liquidation value:

Liquidation preference > hurdle rate

Important pieces:

Title to the shares

Level of indebtedness

intellectual property

Fraud is a real issue. Protections: due diligence,

personal guarantees, funding in installments.

The only real levers that we have are:

1. Funding schedule and triggers

2. Instigate management changes

3. Forcing a default or an exit

Main consequences:

Follow investment strategy

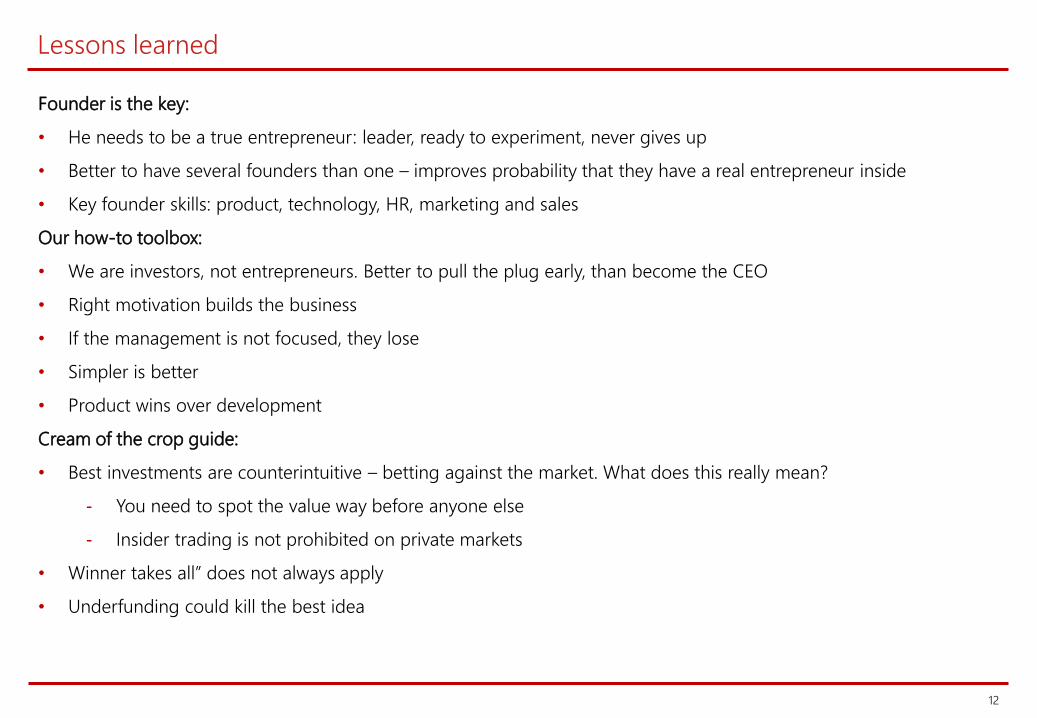

Lessons learned

12

Founder is the key:

• He needs to be a true entrepreneur: leader, ready to experiment, never gives up

• Better to have several founders than one – improves probability that they have a real entrepreneur inside

• Key founder skills: product, technology, HR, marketing and sales

Our how-to toolbox:

• We are investors, not entrepreneurs. Better to pull the plug early, than become the CEO

• Right motivation builds the business

• If the management is not focused, they lose

• Simpler is better

• Product wins over development

Cream of the crop guide:

• Best investments are counterintuitive – betting against the market. What does this really mean?

- You need to spot the value way before anyone else

- Insider trading is not prohibited on private markets

• Winner takes all” does not always apply

• Underfunding could kill the best idea

13

Thank you