Embed Size (px)

Citation preview

September 20, 2010

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.

For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report.

* = This Research Report has been partially prepared by analysts employed by non-U.S. affiliates of the member. Please see page 2 for the name of each non-U.S. affiliate contributing to this Research Report and the names of the analysts employed by each contributing affiliate.

+= Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to NASD/NYSE restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

M O R G A N S T A N L E Y B L U E P A P E R

The China Files US Corporates and China’s Megatransition

China is still the next big thing. China is poised for a “megatransition” between now and 2020—from leading producer of globally distributed goods to the world’s largest market for consumer and industrial products. For multinationals and investors seeking exposure, size is only part of the story. Competitive landscapes in specific industries are becoming more complex, reflecting the powerful secular trends (which we call the “megatrends”) driving the megatransition: demographics, urbanization, infrastructure, social security network, consumer financing, and education.

We identify 16 US companies best positioned for the opportunities we see in China. A team of 33 contributors—our China strategy team along with industry analysts from the US and China for 16 industries— systematically reviewed the landscape of each industry, evaluating companies’ current position, growth strategy, and competitive headwinds. Their top picks are Nike, Wynn Resorts, Yum! Brands, Procter & Gamble, Pfizer, Medtronic, Yahoo!, Apple, Marvell, Dow Chemical, Mosaic, General Dynamics, Emerson Electric, Caterpillar, FedEx, and Diana Shipping.

Winning strategies of multinationals in China should feature two elements, we think: 1) a shift to franchise-building (establishing brands and distribution/service networks) over revenue generation (maximizing short-term sales); and 2) a preference for integration (making China a second home market) over localization (treating China like another foreign market).

M O R G A N S T A N L E Y R E S E A R C H G L O B A L

China Strategy

Jerry Lou [email protected] +852 2848-6511 Morgan Stanley Asia Limited+

Allen Gui [email protected] +86 21 2326-0036 Morgan Stanley Asia Limited+

US & China Research Teams See page 2 for the authors of this report*

M O R G A N S T A N L E Y R E S E A R C H

2

September 20, 2010The China Files

China Team

Charlie Chan1 Technology +852 2848-5636 [email protected]

Grace Chen2 Technology +886 2 2730-2890 [email protected]

Jeremy Chen2 Autos, Building & Construction, Chemicals, Consumer, Fertilizer, Mid Cap +886 2 2730-2876 [email protected]

Praveen Choudhary1 Gaming, Multi-Industry +852 2848-5068 [email protected]

Allen Gui1 Strategist +86 21 2326-0036 [email protected]

Lin He1 Leisure & Lodging, Mid Cap +86 21 2326-0016 [email protected]

Richard Ji1 Internet Services, Media +852 2848-6926 [email protected]

Bin Li1 Healthcare +852 2239-7596 [email protected]

Jerry Lou1 Strategist +852 2848-6511 [email protected]

Bill Lu1 Technology +852 2848-5214 [email protected]

Jasmine Lu1 Technology +852 2239-1348 [email protected]

Angela Moh1 Consumer +852 2848-5405 [email protected]

Wee-Kiat Tan1 Coal, Oil & Gas +852 2848-7488 [email protected]

Helen Wen1 Capital Goods, Utilities +852 2848-5438 [email protected]

Edward Xu1 Transportation +852 2239-1521 [email protected]

Kate Zhu1 Automobiles, Building & Construction, Capital Goods +852 2848-6843 [email protected]

US Team

Vincent Andrews3 Food, Agricultural Chemicals +1 (212) 761 3293 [email protected]

Scott Davis3 Electrical Equipment & Industrial Conglomerates +1 (212) 761 7670 [email protected]

Sanjay Devgan3 Semiconductors +1 (415) 576 2382 [email protected]

Scott Devitt3 Internet & Consumer Software +1 (212) 761 3365 [email protected]

John Glass3 Restaurants +1 (617) 856 8752 [email protected]

William Greene3 Freight Transportation +1 (212) 761 8017 [email protected]

Katy Huberty3 Systems and PC Hardware +1 (212) 761 6249 [email protected]

Chi H. Lee3 Apparel and Footwear +1 (415) 576 8738 [email protected]

David R. Lewis3 Medical Technology +1 (415) 576 2324 [email protected]

Paul Mann3 US Chemicals +1 (212) 761 3865 [email protected]

Mary Meeker3 Internet & Consumer Software +1 (212) 761 8042 [email protected]

Dara Mohsenian3 Household & Personal Care +1 (212) 761 6575 [email protected]

David Risinger3 Large Cap & Specialty Pharmaceuticals +1 (212) 761 6494 [email protected]

Ole Slorer3 Commodity Shipping +1 (212) 761 6198 [email protected]

Mark Strawn3 Gaming & Lodging +1 (212) 761 4990 [email protected]

Robert Wertheimer3 Electrical Equipment & Industrial Conglomerates +1 (212) 761 6334 [email protected]

Heidi Wood3 Aerospace & Defense +1 (212) 761 4407 [email protected]

1Morgan Stanley Asia Limited+ 2Morgan Stanley Taiwan Limited+ 3Morgan Stanley & Co. Incorporated

M O R G A N S T A N L E Y R E S E A R C H

3

September 20, 2010The China Files

Table of Contents

The China Landscape .............................................................................................................................................................. 4

US Multinationals' Winning Strategies in China......................................................................................................................... 10

What’s Your China Plan? US Top Picks.................................................................................................................................... 13

Market Overviews / Top Picks

Apparel.................................................................................................................................... Angela Moh / Chi H. Lee 14

Casinos & Gaming .................................................................................................. Praveen Choudhary / Mark Strawn 16

Restaurants.................................................................................................................................... Lin He / John Glass 18

HPC ............................................................................................................................... Angela Moh / Dara Mohsenian 20

Pharmaceuticals......................................................................................................................... Bin Li / David Risinger 22

Medical Devices ......................................................................................................................... Bin Li / David R. Lewis 24

Internet............................................................................................................. Richard Ji / Mary Meeker /Scott Devitt 26

Tech Hardware................................................................................................. Jasmine Lu / Grace Chen / Katy Huberty 28

Semis ................................................................................................................ Bill Lu / Charlie Chan / Sanjay Devgan 31

Chemicals ............................................................................................................................ Wee-Kiat Tan / Paul Mann 33

Agrichemicals.............................................................................................................. Jeremy Chen / Vincent Andrews 35

Aerospace & Defense ................................................................................................................ Allen Gui / Heidi Wood 37

Industrials................................................................................................................ Kate Zhu / Helen Wen/ Scott Davis 39

Machinery .......................................................................................................................... Kate Zhu / Rob Wertheimer 41

Transportation .................................................................................................................. Edward Xu / William Greene 43

Shipping .................................................................................................................................... Edward Xu / Ole Slorer 45

Runners-Up.............................................................................................................................................................................. 47

Appendix: Morgan Stanley US China Exposure Basket .......................................................................................................... 52

Morgan Stanley is acting as financial advisor to Bristol-Myers Squibb in relation to the announced tender offer to acquire ZymoGenetics, Inc ("ZymoGenetics"), as announced on September 7, 2010. The proposed acquisition is subject to the successful tender offer for the shares of ZymoGenetics and other closing conditions. This report and the information provided herein is not intended to (i) provide advice with respect to whether to tender ZymoGenetics shares, (ii) serve as an endorsement of the proposed transaction, or (iii) result in the procurement or exchange of a security by a security holder. Bristol-Myers Squibb has agreed to pay fees to Morgan Stanley for its financial services, including transaction fees that are subject to the consummation of the proposed transaction. Please refer to the notes at the end of this report.

M O R G A N S T A N L E Y R E S E A R C H

4

September 20, 2010The China Files

The China Landscape: Megatrends and Megatransition

Megatrends: From producer to consumer economy. Several secular trends are forcing a “megatransition” in China as the country evolves from one of the world’s foremost producers of globally distributed goods into a leading consumer. The trends driving this growth, as we see it, are the seismic shifts in China’s demographics; the country’s continued urbanization; the ongoing development of a world-class infrastructure; the expansion of a comprehensive public security network; positive consumer financing developments; and the benefits of an educated workforce in an ever-improving industrial workplace.

Obstacles: Environmental concerns and finite resources. We foresee two primary impediments to China’s growth in the upcoming decade: The country’s fragile environment and the decreasing availability of resources. To sustain growth, it is essential that China address its environmental policies and reduce its current level of dependence on energy and certain commodities.

Megatransition. We believe that by 2020 China will triple its nominal GDP to account for 14% of the world economy, more than double its fixed asset investment and more than triple consumer spending. We also see exciting opportunities at the micro level: China’s “baby boomers” will predominate among consumers; urban populations will expand by 300 million people; wages will more than quadruple; and consumer credit will surge rapidly.

Megatrends

China is entering a new phase of economic growth, one where rebalancing and reform will stimulate domestic consumption, effect industrial improvements, and spark global interest in the possibilities of China’s economy, the second -largest in the world. Behind this optimistic view of China lie several specific drivers—what we call “megatrends.”

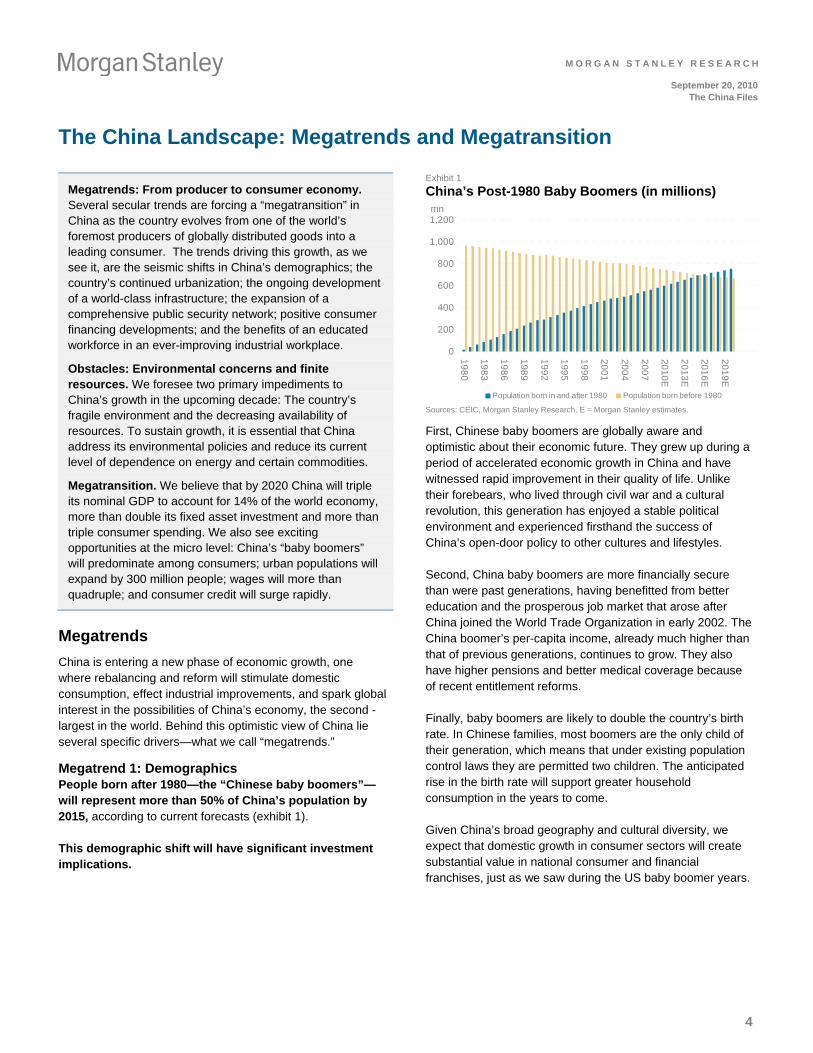

Megatrend 1: Demographics People born after 1980—the “Chinese baby boomers”—will represent more than 50% of China’s population by 2015, according to current forecasts (exhibit 1).

This demographic shift will have significant investment implications.

Exhibit 1

China’s Post-1980 Baby Boomers (in millions)

0

200

400

600

800

1,000

1,200

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

E

20

13

E

20

16

E

20

19

E

mn

Population born in and after 1980 Population born before 1980 Sources: CEIC, Morgan Stanley Research, E = Morgan Stanley estimates.

First, Chinese baby boomers are globally aware and optimistic about their economic future. They grew up during a period of accelerated economic growth in China and have witnessed rapid improvement in their quality of life. Unlike their forebears, who lived through civil war and a cultural revolution, this generation has enjoyed a stable political environment and experienced firsthand the success of China’s open-door policy to other cultures and lifestyles.

Second, China baby boomers are more financially secure than were past generations, having benefitted from better education and the prosperous job market that arose after China joined the World Trade Organization in early 2002. The China boomer’s per-capita income, already much higher than that of previous generations, continues to grow. They also have higher pensions and better medical coverage because of recent entitlement reforms.

Finally, baby boomers are likely to double the country’s birth rate. In Chinese families, most boomers are the only child of their generation, which means that under existing population control laws they are permitted two children. The anticipated rise in the birth rate will support greater household consumption in the years to come.

Given China’s broad geography and cultural diversity, we expect that domestic growth in consumer sectors will create substantial value in national consumer and financial franchises, just as we saw during the US baby boomer years.

M O R G A N S T A N L E Y R E S E A R C H

5

September 20, 2010The China Files

Another powerful demographic trend to consider is China’s aging population. As a result of China’s population control policies from the late 1970s, at some point between 2015 and 2020 the number of new retirees will outpace the number of new laborers (exhibit 2). This shift in China’s labor market will open up market opportunities for automation and machinery applications in manufacturing, transforming the industry’s current labor-intensive business model into a capital-intensive one.

Exhibit 2

China Dependent Ratio Evolution China Dependent Ratios - MS estimates

0%

35%

70%

105%

140%

19

50

19

60

19

70

19

80

19

90

20

00

20

10

20

20

20

30

20

40

20

50

Total dependent ratio (TDR) Elderly dependent ratio (EDR)

Child dependent ratio (CDR) Notes: CDR = number of children and youth (aged 0-19) as percentage of working population (aged 20-59); EDR = elderly population (aged 60+) as percentage of working population (aged 20-59); TDR = CDR+EDR. Sources: UN, Morgan Stanley Research.

The shift also will increase workers’ value—and bargaining power—in the labor market, which will directly push up labor’s share of GDP, as we have seen in Japan (exhibit 3). We forecast that China nominal GDP will triple by 2020 and that labor’s share of GDP will normalize to 22% (at current average developing country levels), which implies an increase in absolute wages (in renminbi terms) of more than four times (exhibits 4 and 5).

Exhibit 3

Japan: Labor’s Share of GDP versus Dependent Ratio

41%

43%

45%

47%

49%1

98

5

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

50%

52%

54%

56%

Total dependency ratio Labor cost as % of GDP (right) Note: Dependent ratio is plotted using UN data reported every five years Sources: UN, CEIC, Morgan Stanley Research.

Exhibit 4

China Labor as Percentage of GDP versus Other Countries

0% 10% 20% 30% 40% 50% 60% 70%

Denmark

Germany

Japan

Australia

Norway

Luxembourg

New Zealand

Mexico

Thailand

China

Sources: CEIC, OECD, Morgan Stanley Research.

Exhibit 5

China Wage Forecasts

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

2005 2007 2009 2011 2013 2015 2017 2019

billions Rmb

0%

5%

10%

15%

20%

25%

30%

35%Total wages Total labor cost as % of GDP (right)

Sources: CEIC, Morgan Stanley Research.

China’s aging population also will create investment opportunities in financial services such as life insurance and mutual funds, and in healthcare, medical devices, and the pharmaceutical industry.

Megatrend 2: Urbanization Our economist Qing Wang expects urbanization to remain China’s main growth driver over the next 10 years (exhibit 6). Wang also holds that the rapid urbanization of the previous decade will remain or even accelerate as we enter the next decade, lifting China’s urbanization ratio to the level of developed countries, from the current 47% to 63% in the long-term. In fact, as part of its initiative to support urbanization in midsize and small cities—particularly in the inland provinces—the Chinese government recently decided to speed up the reform of the household registration system. This reform seeks to equalize rural and urban citizens’ entitlements to pension, education, and other social benefits so that migrant workers from rural areas can more easily relocate to urban areas.

M O R G A N S T A N L E Y R E S E A R C H

6

September 20, 2010The China Files

Exhibit 6

China Rate of Urbanization

0

10

20

30

40

50

60

70

80

1949 1969 1989 2009 2029 2049 2069

US in 1840

US in 1960

Share of urban population (%)

China US in 1900

Artificially suppressed

Sources: CEIC, Morgan Stanley Research.

We also see signs that China is planning to enhance its public services network as the country’s urban areas expand (see Megatrend 4).

This powerful urbanization trend will positively affect both capital formation and personal consumption, leading to long-term opportunities in sectors like capital goods, building materials, property, utilities, and basic materials. Consumer franchises will likely benefit as well. Urbanization also is a strong engine for creating wealth, bringing new consumers to the marketplace. If, in the long run, urbanization reaches 63% of China’s 1.4 billion people, 300 million additional consumers will see their spending power increase substantially. The main beneficiaries of this trend will be the consumer staples and personal care sectors, along with household product companies that sell “black and white goods,” such as TVs, video players, refrigerators, and air conditioners.

Megatrend 3: Infrastructure China has made tremendous strides in developing its infrastructure, but there is room for more economic expansion and rebalancing. Specifically, the country needs to further develop its national high-speed rail and highway grids, ultra-high-voltage power transmission network, nuclear power plants, gas distribution grid, and sewage and solid waste treatment facilities.

Plans for infrastructure development are already in place: China intends to lengthen its total rail network from 86,000 kilometers to 120,000 by 2015, and at least 60% of this system will be electrified, up from 40%. China’s high-speed passenger rail system will reach 16,000 kilometers in length from the current 3,500 kilometers by 2015, at which point China will operate one of the most extensive high-speed rail networks in the world. And within five years China’s total roadway capacity—now at 70% of US capacity—will surpass that of the US.

Megatrend 4: Completion of Public Services Network China’s high rate of personal savings stems from individuals’ concerns about retirement without a comprehensive, government-sponsored social security system in place (exhibit 7). We believe that an aggressive reform and funding of the country’s pension, healthcare, and education systems would go a long way to unleashing domestic demand and that planned reforms of China’s entitlement programs over the next decade will push consumer growth beyond levels previously seen.

Exhibit 7

High Savings Rate Equals Consumption Potential

0% 10% 20% 30% 40% 50% 60%

US

UK

Germany

Korea

Japan

China

Source: Country Statistics, Morgan Stanley Research.

Beijing is already well on its way to reforming the social security system: More than 90% of rural households already participate in the new Rural Cooperative Medicare system (which offers only basic medical coverage), and within the next five years all urban populations should participate in a government health plan, as compared with 60% now (exhibit 8). By 2015 all citizens in urban areas will be enrolled in a state-sponsored pension plan, and those in rural areas will be enrolled by 2020 (exhibit 9).

M O R G A N S T A N L E Y R E S E A R C H

7

September 20, 2010The China Files

Exhibit 8

Expansion of Medical Insurance Coverage

0

20

40

60

80

100

1999 2001 2003 2005 2007 2009 2011E 2013E

%

% of urban population covered % to rural population covered Sources: MoH, Morgan Stanley Research. E = Morgan Stanley estimates.

Exhibit 9

Overview of China’s Pension Schemes

Urban employee

pension Rural social

pension

Rollout date Early 1990s Early 1990s

Total population* (mil.) 450 500

Covered population** (mil.) 234 60

Current coverage (%) 52 12

Target coverage 100% by ~2015 ~20% in 2010;

100% by 2020

Funding source (%) 30/70, employee/employer 50/50, resident/government

Monthly pension payout (est.) 20%-50% local avg. wage 100-150 Rmb

Current avg. monthly cost

of living (Rmb)

1,600 450

Monthly pension payout vs.

current monthly cost of living***

(%)

48

28

*Working and retired population. **As of 2009. ***As example only. Percentage varies based on pre-retirement wages. Sources: Government data, Morgan Stanley Research.

Megatrend 5: Consumer Finance Consumer finance in China lags that of developed economies such as the US and Europe: Total credit spending in China is about 10% of consumers’ total expenditure, compared with around 50% in more developed economies. Thus, as consumer credit becomes more accessible in China consumer spending will increase.

A thriving internet environment makes online shopping possible and so drives consumer credit. Since China has the highest number of internet users in the world—390 million—we see substantial upside for online settlement and credit cards as e-commerce continues to develop in China. Today about 20% of Chinese internet users shop online, far below the rate in developed countries, which is about 60%. Should online shopping penetration rise to 50%, there could be as many as 120 million additional credit card users in China (today there are about 150 million cardholders).

As credit use grows, consumer credit reports are becoming more useful in China, where the central bank has kept credit records on 600 million individuals and more than 6 million corporations since 1997. This credit tracking will make further consumer credit extension easier and will enhance credit protection efforts—a major concern. To combat identity theft and fraud—two ills that have plagued China’s credit industry in the past—China started using second-generation identification cards in 2004, making identify theft and fraud almost impossible today.

We estimate that China’s consumer credit spending as a percentage of total consumption will meet the world average of 40% by 2020, boosting consumers’ purchasing power by a dramatic 30%—and this is before taking into account the reduction in personal savings and improved wages across China.

Megatrend 6: Industrial Upgrades In the early 1990s—when China started to rise as a global producer—only 3% of its working population had college degrees. This lack of educated laborers forced Chinese companies to adopt a low-quality, mass-produced approach to their businesses. But this scenario is changing rapidly.

Today, approximately 10% of China’s work force has a college degree (exhibit 11), and Chinese companies are changing their business models to make a place for this better-educated worker. Soon, China’s cheap and low-value-add approach to production will become obsolete as a younger, college-educated population enters the workforce.

We estimate that by 2020 some 35% of China’s workforce will be college educated. This level will match that of the US today, where we see a strong correlation between education and the value added of manufacturing (exhibit 10).

Exhibit 10

US Manufacturing Value-Added versus Education

22%

24%

26%

28%

30%

32%

34%

36%

38%

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

US

$ b

n

Percentage of college graduates in total employment (left) GDP - Manufacturing value added (right)

Sources: CEIC, Morgan Stanley Research.

M O R G A N S T A N L E Y R E S E A R C H

8

September 20, 2010The China Files

Exhibit 11

China Baby Boomers Receive Better Education

Sources: CEIC, Morgan Stanley Research.

Obstacles to Growth

As China heads toward the megatransition that these megatrends portend, the country will doubtless face obstacles to its ongoing growth. It must therefore adjust its growth model to address these obstacles if it hopes to continue on a trajectory of expansion. The two main obstacles to ongoing growth are environmental issues and the availability of certain resources.

Environmental issues China, the world’s top carbon emitter, accounts for approximately 21% of global carbon emissions—and its emissions liability is growing faster than that of any other nation. Further industrialization, growing urbanization, and rising disposable income will drive up energy consumption in the coming decade, and the rate of carbon emissions will multiply unless China makes a concerted effort to alter its current growth model (exhibit 12).

Exhibit 12

China Carbon Emissions

R2 = 0.7058

-5

0

5

10

15

20

25

-10,000 - 10,000 20,000 30,000 40,000 50,000 60,000

Per capita GDP (US$)

CO

2 e

mis

sio

n p

er

cap

, to

ns

US

EU25

CanadaAustralia

UK

Japan

Korea

India

China

China 2020e -efforts taken

GDP/CO2 curve

China 2020e - BAU*

Note: Size of bubble measures each country’s emissions, 2005 data. BAU—Business as usual. Sources: CAIT, Morgan Stanley Research. E=Morgan Stanley estimates.

Curbing carbon emission has become part of China’s national priorities, especially after the Copenhagen Summit last year. At the summit, Premier Wen committed to “reducing carbon emissions per unit of GDP by 40% to 45%, by 2020, from the 2005 level.”

China’s strategy to reduce carbon emissions—different from that of developed countries—will be to develop less carbon-intensive businesses and new energy sources, with an eye toward reducing marginal carbon emission per dollar. China’s secondary focus will be to reduce carbon emissions in existing production processes and streamline consumption.

We expect that China’s energy structure in the coming decade will evolve away from coal and toward clean and/or renewable sources of energy. In our view, this evolution of China’s energy structure will be the most effective way to reduce carbon emissions, cutting them by at least 51% by 2020. Further reductions will come from improved efficiency at thermal plants (a 37% reduction) and at industrial sites (mainly within the cement industry, with a 12% reduction).

Resource constraints Today, China consumes a significant share of the global supply of commodities and energy. Given China’s high rate of growth, this rate of consumption cannot continue over the long term (exhibit 13).

Exhibit 13

China Percentage of Total Global Commodities Consumption, 2008 - 2009

20% 25% 30% 35% 40% 45% 50%

Copper

Aluminum

Zinc

Lead

Tin

Coal

Sources: CEIC, Factiva, Morgan Stanley Research.

Today, China competes for these limited resources with other growing economies in a global market vastly different from the one that it entered as the dominant emerging economy in 1993. Since then, more countries have started to develop—Brazil, Russia, and India, for example—and now demonstrate considerable demand for the same resources as China.

If China and other emerging economies keep growing at current speeds without reducing their energy and commodity dependency, prices for these resources may move beyond

-

5,000

10,000

15,000

20,000

25,000

1949 1959 1969 1979 1989 1999 2009

millions

China - College students per million of population

baby boomers

M O R G A N S T A N L E Y R E S E A R C H

9

September 20, 2010The China Files

what China can afford, triggering an economic slowdown in the country.

The Megatransition: China by 2020

As the first decade of the 21st century winds down, China stands ready to make a megatransition, from the world’s factory to an economic powerhouse on the global stage. The megatrends we identified, while facing some constraints, are the push and pull factors to help China achieve such a megatransition.

At macro levels, we believe that by 2020:

China’s GDP share in the world economy will grow to 14% from the current 8%.

China’s domestic FAI will keep growing at 11.0% CAGR, or more than double.

China’s private consumption will grow at 12.6% CAGR, or more than triple.

China will have made its currency, the renminbi, freely convertible and its capital account open.

China will become one of the largest outbound investors, in both financial direct investment and world capital markets.

At micro levels, we believe that by 2020:

China baby boomers—those born after 1980—will represent 45% of the workforce and be the dominant consumer.

China will have deepened its urbanization ratio to 63%, having added 300 million to its urban population, an increase of 50% from today.

China’s labor cost-to-GDP ratio will go up to 30%, with wages more than quadrupling.

China will complete a comprehensive social security network, covering the majority of its population, with health insurance for the entire population of 1.3 billion and pension coverage for 0.8 billion employed workers.

Of Chinese workers, 35% will have college degrees.

China will have developed a comprehensive consumer finance industry, driven by advances in e-commerce and credit reporting. The credit consumption ratio could rise to 40% from today’s 10%.

China will have in place a nationwide, world-class infrastructure, from ports to airports, highways to high-speed rail lines, and power grids to gas distribution networks.

Also see “China Economics: Chinese Economy Through 2020: Not

Whether but How Growth Will Decelerate”, by Qing Wang, 19

September 2010.

M O R G A N S T A N L E Y R E S E A R C H

10

September 20, 2010The China Files

US Multinationals’ Winning Strategies in China

China’s challenge. China’s rising stature in the world economy will pose a critical challenge to multinationals in the coming decade: how to remain competitive globally in the face of China’s rapid growth.

Protectionist concerns. Despite the growing consensus that China is becoming more protectionist, we believe that multinationals’ success in China will be the market’s choice, not the government’s choice.

Two factors that will contribute to multinationals’ winning strategy. By adopting a franchise approach rather than focusing on short-term sales, multinationals will fare well in China. Also, if multinationals integrate their current products and operations into the Chinese market they will win over China’s buying public.

Three opportunities for US multinationals. We have seen that US multinationals can find a competitive advantage by making the most of opportunities related specifically to the consumers’ boom, anticipated industrial upgrades, and demand for materials.

China’s Challenge

The challenge for multinationals in the coming decade is clear: If China’s economy comes to represent 14% of global GDP by 2020, as our China economist Qing Wang estimates, multinationals need to think about how they can benefit strategically from China’s advancement (exhibit 14). In 2009, Asia made up only 5.2% of S&P 500 sales, and the China portion is surely lower than that, though we do not know by how much. With this in mind, China’s significance as an overseas market will undoubtedly increase over time, offering an opportunity that US multinationals cannot ignore. In short, a multinational today cannot remain truly multinational in the coming decade without a proper China strategy.

Exhibit 14

China Economy Size in the World

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2000 2002 2004 2006 2008 2010E 2012E 2014E

2%

4%

6%

8%

10%

12%

14%

China GDP as % of World (right) China GDP US$ bn Sources: IMF, Morgan Stanley Research. E = IMF estimates.

Exhibit 15

Foreign Companies’ Share in China Industry Value Added

5%

10%

15%

20%

25%

30%

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

Source: CEIC, Morgan Stanley Research

We believe that China also stands to gain from multinationals’ presence in the region. At present, only a few large multinationals operate in the country, limiting China’s opportunities for cultural and technology exchanges (exhibit 15). There are no official data available regarding foreign companies’ share of Chinese GDP, but our rough math shows that they are still under-represented. First, foreign companies accounted for 28% of industrial sales in 2009. Given that foreign companies' contribution to primary and tertiary industries is almost negligible, we estimate foreign companies’ share of GDP would be slightly higher than 13% (secondary industry was about 46% of GDP in 2009). The upside to this share is, in our view, quite significant.

How Big a Concern Is Protectionism?

Contrary to the view that China is becoming more protectionist, a development that might limit multinationals’ upside in China, we see it differently. We believe that business success is the market’s choice, not the government’s choice, and that US multinationals will succeed in China in the long term. Our rationale: More important than any government initiative is China’s growing need for marketing expertise and technology, and the multinationals have them.

Multinationals, especially consumer brands from the US and Europe, are experienced in building franchises. Chinese companies will need to develop expertise in this area if they hope to compete in China’s geographically broad, culturally diverse, highly stratified marketplace, where foreign companies can leverage expertise from their home markets to great success. We expect that as the Chinese market continues to expand in the coming decade, the China

M O R G A N S T A N L E Y R E S E A R C H

11

September 20, 2010The China Files

consumer will welcome multinationals that can adapt to regional differences.

Multinationals, especially industrial firms, have invested significantly in technological development over the last two decades. Chinese companies will likely seek to build alliances with multinationals that are more technologically advanced; these new business relationships will help eliminate existing barriers to trade and will ease multinationals’ entry into the market.

There are many great success stories of foreign companies in China. To name a few—none of which was the government’s choice:

Nike generates 10% of their sales from China, holding the top premier sportswear brand position in Tier 1 and Tier 2 cities;

Yum! Brands now operates 3,500 restaurants in China and has seen profits grow at 30% CAGR in the past five years, making it one of the top players in the catering business and far ahead of most local players;

Procter & Gamble holds 13% of the household and personal care market, and is the largest H/PC company in China among both local and foreign players;

China is already the fourth largest market for Emerson Electric, contributing 12% to its total revenue; and

China has contributed to about 30% of Dow Chemical’s sales since 2008.

These stories illustrate how well the market economy is working in China, how China’s decision to build a market economy paved the way for its current economic success. In order for this success to continue, however, the market must determine which goods and services it prefers.

Two Factors for Success

Market experience and technology are what multinationals can offer to the China market, but these two contributions do not guarantee multinationals’ success there over the next decade. We believe that before all else, multinationals need to devise a clear, long-term strategy in China.

Most multinationals employ two strategies in China: They maximize sales revenue—often by running parallel brands and business lines—and they try to localize operations, from production to service and support. While we do not fault this model, we believe these strategies can be improved.

We see opportunity in moving from a revenue model to a franchise model. A franchise model relies on an extensive network of sales and services for long-term, sustainable

growth. A franchise model also requires a centralized decision-making process about branding, sales, marketing, and relationships management.

Multinationals with multiple brands and business lines could benefit from adopting this model, in our view, beginning with the implementation of a unified marketing and branding strategy. They then could consolidate their sales networks to avoid internal competition and inconsistent handling of clients. They might also consolidate the management of different business lines’ clients, government relations, and marketing.

Indeed, many large firms have used the franchise model to achieve success in China—GE, Emerson, and Proctor & Gamble, for instance. These companies all came to China early in its rise, to be sure, but even though they also ran multiple business lines and/or brands, they centralized their branding, marketing, distribution, and relationships management operations from their start here. We believe this approach is crucial for companies hoping to establish a long-term business in China.

We also see opportunity in moving from a localization model to an integration model. Given the size of the Chinese market, we think multinationals would be well served to view China as a secondary home market, or even as a second headquarters, rather than as just another foreign market. Using a localization model, multinationals typically do two things: They bring products from their home market into China and localize the production, and they employ local workers. This could be improved upon, we think, by adapting to regional differences and integrating foreign products and services in that way. To accomplish this, multinationals could offer different products and/or services that appeal specifically to the Chinese consumer and work through existing institutional and operational structures to improve system efficiency and reduce bureaucratic delays.

Unfortunately, although there are many good examples of foreign firms’ localization, we have found very few that are good at integration. On the product-offering side, P&G and Unilever are the two rare examples of foreign firms that understand the differences in the China market and design broad lines of products specifically for this market. Clearly, these companies have been very successful in China.

At the corporate structure level, an example of integration is even harder to find. Most multinationals have their Asian headquarters outside of China, even in instances where a company derives most of its revenue from China. IBM, GE, GM, and Honeywell are the few exceptions, having moved their regional headquarter to China in the past decade. Managing from a distance is not the optimal model, in our view. China is not just a big market, it is a quickly growing and

M O R G A N S T A N L E Y R E S E A R C H

12

September 20, 2010The China Files

changing market. It is impossible to manage a China business efficiently from an offshore headquarters using a remote control. Given the difficulty of managing from afar and the importance of China to multinationals, we believe that most multinationals should build a second global headquarter in this country.

Three Categories of Opportunity for US Firms

We group the China opportunities into three general categories. The first two categories represent companies that will benefit from the direct opportunities offered by China’s consumer boom and industrial upgrades. Taken together, these two direct opportunities create a third, indirect opportunity—a demand for materials, from which companies in the third category will benefit (exhibit 16).

Although foreign companies today make up more than 20% of China’s gross industrial output, most of these foreign companies are concentrated in low value-added businesses such as OEM factories. We believe that the greater upside potential for foreign companies, especially the US companies, lies in the franchise-critical consumer sectors and technology-intensive capital goods sectors. This view is consistent with our analysts’ findings as well.

Some examples of foreign companies in sectors underrepresented in China are:

Pfizer, which captures only 2% of the market, even though it’s the largest foreign pharmaceutical company in China;

Starbucks, which has only 400 outlets in China, even though it has been growing at a rate of 15%-20% per year. China’s contribution to Starbucks’ group sales is almost negligible; and

Caterpillar, which generates only 5%-7% of sales from China, the largest machinery market in the world.

US firms in general are competitive in technology and experienced in franchise-building, which gives them certain advantages at the micro level. With these advantages in mind, in the consumers category, we believe US companies are more competitive in household consumption (apparel, HPC, computer hardware, semiconductors, and air freight & logistics); culture and leisure (internet, casinos & gaming, and restaurants); and healthcare (healthcare supplies and pharmaceuticals). In the industrial upgrade category, US companies are more competitive in aerospace & defense, industrial conglomerates, and machinery. US companies also have opportunities in selective material and related sectors, such as fertilizers & agrichemicals and chemicals, as well as marine.

Exhibit 16

US Companies’ China Opportunity Map

machinery

Consumer Boom

Industrial Upgrade

Materials

restaurants

household consumption

apparel

HPC

tech hardware

semis

transportation

culture and leisure

internet

casinos & gaming

medical deviceshealthcare

pharmaceuticals

shipping

chemicals

agrichemicals

aero space & defense

industrials

Source: Morgan Stanley Research.

M O R G A N S T A N L E Y R E S E A R C H

13

September 20, 2010The China Files

What’s Your China Plan? US Top Picks

The secular growth dynamics of the Chinese market don’t leave US companies with much of a choice. If China’s rate of economic growth and the potential of its various industry sectors are anywhere close to what analysts forecast, the difference between playing in the game and sitting on the sidelines will be big enough to affect companies’ earnings and valuation multiples relative to their peers’.

Given this macro reality, the question for US companies today simply becomes: What’s your China plan?1

In this next section, we asked our US industry analysts to identify the companies in their coverage universe that are best positioned to participate in the secular growth dynamics that our China strategist Jerry Lou describes in the introduction, “The China Landscape: Megatrends and Megatransition.” For each of the industry sectors discussed in this report, our local China industry experts provide the relevant market overview as well.

A full-blown competitive analysis would involve an in-depth study of current market shares, projected market sizes, and various competitive strategies across industry sectors and global peer companies. Such an analysis is outside the scope of this report and is best accomplished at the industry sector level. Instead, we have asked our analysts to qualitatively assess their top picks along three simple but distinct dimensions, with the understanding that any one or all of these can determine a company’s success in new markets.

Exposure Today Some US companies have already established a beachhead in China and can claim China as their third- or even second-largest regional market. Other foreign companies may hold a dominant position in the Chinese market, even though China operations contribute a relatively small percentage to their global sales. All of these companies have significant exposure to the Chinese market, with all of the opportunity and risk that this exposure entails.

We must stress that what works elsewhere does not necessarily work in China. Therefore, the extent to which US companies have gained market share in China reflects their ability to overcome barriers to entry related to:

Aligning products and pricing with local client preferences;

Identifying and cooperating with the right distribution partners; and

Understanding how to navigate a complex new market via formal and informal networks.

1This topic of US corporate strategy in China has received recent attention in

the financial press. See, for example, “Divided by a Two-Track Economy: Foreign Demand Buoys Some U.S. Firms, but Others Face Wary Consumers at Home,” The Wall Street Journal, September 7, 2010.

What this means is that beyond the headline revenue number, market share in China is directly related to experience and access in the region. Companies eager to do business in China—like our top picks—cannot underestimate the significance of this point.

Strategy Even companies with a strong foothold in China must continue to assess their positioning there as market conditions change. Conversely, because the Chinese market is ever changing, even a company with little exposure in China today may become a dominant player there tomorrow.

Therefore, it is imperative that we understand the strategies of the companies our analysts have chosen. How focused is management on the Chinese market? What investments are being made and what alliances forged? Taken in sum, the answers to these questions lead us to the likely winners in the region.

Some of our top picks may actually have a smaller presence in China when compared to some of their American peers. However, we predict that within five years the strategies that these companies employ will prove to succeed in China’s rapidly evolving market.

Competition We believe that even with the significant exposure and the credible strategies of some of our top picks, a company can be overcome by local and foreign competition. To address this concern, we have asked our analysts to provide a brief assessment of the competitive headwinds for each of their top picks.

As mentioned, a full-blown analysis of the competitive landscape is beyond the scope of this introductory, cross-sector China Files report and is best addressed at the industry sector level. Such an analysis would be necessary, however, to gain a more in-depth understanding of the challenges that might confront a US corporate operating in China.

To be able to track the performance of our top picks and runners-up as the China growth theme unfolds, and for investors wishing to participate in the theme via these US stocks, we created a US-China Exposure basket2 (Bloomberg ticker <MSMSCHX>; see Appendix for constituents).

2 The information contained herein has been prepared solely for informational purposes and is not a solicitation of any offer to buy or sell any security or any other financial instrument or to participate in any trading strategy. Products and trades of this type may not be appropriate for each investor. Please consult with you legal and tax advisors before making any investment decision. Please contact your Morgan Stanley sales representative for more details.

M O R G A N S T A N L E Y R E S E A R C H

14

September 20, 2010The China Files

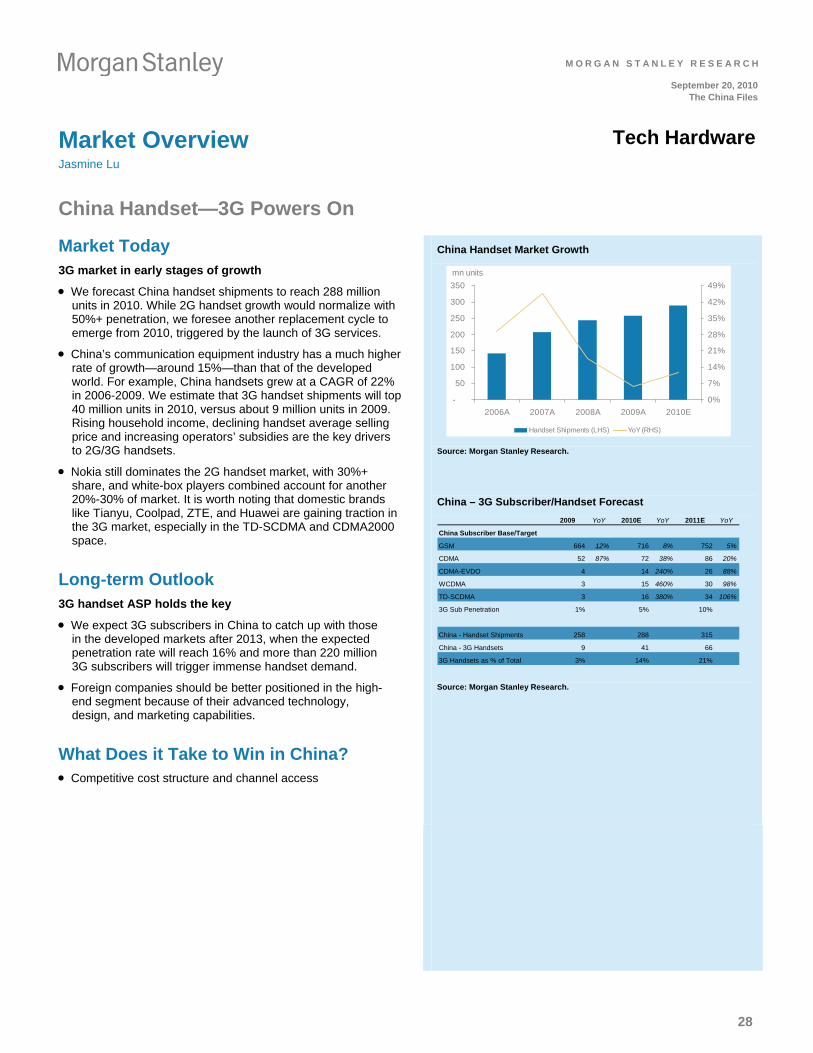

Market Overview ApparelAngela Moh

Rosier Outlook Ahead

Market Today

Exciting growth delivered

The sportswear industry experienced rapid growth from 2002 to 2008, with a CAGR of between 30% and 35%. Even so, per-capita consumption is still at a low level when compared to that of developed counties.

The apparel market in China remains fragmented, with the high-end/premium apparel market mostly dominated by international brands.

The three main drivers of the apparel industry are heightened fashion and brand awareness, higher incomes, and the swelling of the urban population and middle class.

Foreign firms have a strong foothold in the luxury/sports apparel and footwear segments.

Long-term Outlook

Better than expected

We expect solid growth across all segments of the apparel and footwear industries as a result of the secular boom of domestic consumption in China.

In the sportswear segment specifically, we project growth at a CAGR of 15%-20% during 2008-2013, driven by a higher sports participation rate, an increase in disposable income and ongoing urbanization. We also see significant potential in the lower-tier cities for this segment.

Apparel and Footwear Consumption in China

0 6 13 20

63

119133 137

176

211233

0

50

100

150

200

250

Ind

ia

Ch

ina

Ch

ina

(Ad

just

ed

)

Sin

ga

po

re

Jap

an

Ko

rea

Fra

nce

U.K

.

Ge

rma

ny

U.S

.

Ca

na

da

US$

Source: Morgan Stanley Research.

Per Capita Consumption of Sportswear by Country

Apparel and Footwear Consumption in China

-

500

1,000

1,500

2,000

2,500

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

E

2010

E

2011

E

2012

E

2013

E

Rmb bn

2008-13CAGR = 14%

1998-08 CAGR = 11%

Source: Morgan Stanley Research.

What Does it Take to Win in China?

Branding, design, marketing, and distribution

M O R G A N S T A N L E Y R E S E A R C H

15

September 20, 2010The China Files

Top Pick: Nike ApparelNKE, $76.56

Chi H. Lee

Growth Without Equity Dilution Comments from management

Exposure Today A doubling of sales within five years

Nike enjoys strong brand recognition across both footwear and apparel in China and is positioned more as a lifestyle brand than as a pure athletic brand. Its products are not commoditized, which allows for a strong price premium that we think is sustainable in Tier 1 and Tier 2 cities.

Nike currently generates about 10% of total sales ($1.7 billion) from China, making this the third -largest market after North America (35%) and Europe (26%), but ahead of Japan (6%) and Brazil (estimated at about 5%). We expect Nike to double its current sales over the next five years, equal to a CAGR of about 15% per year.

Nike is currently the premier brand in both Tier 1 and Tier 2 cities. Its growth trajectory relies on increasing in share lower-tier cities, which will require greater utilization of the lower ends of its price band. The company is not aiming to compete on price with local competitors—Li Ning and Anta—which currently dominate the lower-tier cities, but some competitor convergence is likely as Nike increases its penetration in the lower tiers and the local players migrate upwards.

Strategy Competitor convergence—increasing penetration in lower-tier cities

Nike’s reputation as a premier brand is not under threat in China. The company will continue to push retail expansion in lower tier cities, principally through key licensing partners, and will begin to push growth in the Converse brand in 2011 as a directly operated business (currently licensed).

Competition Enough room for domestic and foreign competitors to grow

The market may remain skeptical of Nike’s longer-term growth trajectory, even as it acknowledges the company’s growing presence in lower-tier cities. Nike’s distribution partners will continue to add stores and square footage in these cities, and we think Nike can successfully avoid the inventory problems suffered during the Beijing Olympics (point-of-sale infrastructure is improving). And while local producers do offer some competition, we do not see them posing any serious contest to multinationals’ sales within developed markets over the next five years. Finally, Nike operates one of the most diversified sourcing bases within footwear, providing some offset to rising Chinese cost and currency pressures, like wage inflation and labor constraints.

“I’ve made it clear to our leadership team that we will not leave any key growth opportunities untapped. China is a great example….We are the leading force in this incredible market and we’ll leverage that position to exceed our current market revenue of 1.7 billion. And that’s just with the NIKE brand.… When we stay connected to consumers and focused on our key growth opportunities, I’m confident we’ll manage through the uncertainties of the global economy to deliver continued momentum and another strong year.”1

Mark Parker, President and CEO

1FactSet, 4Q2009 earnings call transcript.

M O R G A N S T A N L E Y R E S E A R C H

16

September 20, 2010The China Files

Market Overview Casinos & GamingPraveen Choudhary

Leveraged Macro Play

Market Today

A special gaming zone for the whole country

Macau, a special administration region of China, is the only place in the country where gaming is legal. Macau gaming industry revenue grew at 27% CAGR from 2003-2009 on the strength of Hong Kong and China GDP and a robust tourist industry.

So far, Macau revenue growth has remained unaffected by the slowdown in loan growth and property prices in the wake of government-imposed austerity measures.

At 70% of total revenue, the VIP sector is much larger in size and shows better growth than the mass business segment. Still, the VIP segment is more volatile, riskier, and vulnerable to any downturn. The mass business is more resilient and less volatile and generates a higher margin for the operators. Thus we prefer the mass business segment over the VIP segment.

Foreign companies operate in both the VIP and the mass business segments. Wynn Macau concentrates more on the VIP side, with 74% of its second-quarter gross revenue generated by the VIP segment. Sands China, by contrast, concentrates more on mass and non-gaming businesses, with 53% of gross revenue from the VIP segment for the same time period.

Long-term Outlook

Expecting normalized but stable growth

In the long term, the sustainable growth rate should be around 10%-15% for the Macau gaming industry.

The VIP business in Macau could be negatively affected by the licensing of new junkets in Singapore, but the mass business segment should enjoy more stable and resilient growth.

What Does it Take to Win in China?

The execution of expansion plans

Macau Gaming Revenue versus Visitation

-40%

-20%

0%

20%

40%

60%

80%

100%

Jan-08 Jun-08 Nov-08 Apr-09 Sep-09 Feb-10 Jul-10

Gaming Revenue YoY % Visitation YoY %

Sources: DSEC, Morgan Stanley Research.

Mass Business versus VIP Market

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

May-08 Oct-08 Mar-09 Aug-09 Jan-10 Jun-10

VIP Roll Mass Revenue

Growth YoY %

Source: Morgan Stanley Research.

M O R G A N S T A N L E Y R E S E A R C H

17

September 20, 2010The China Files

Top Pick: Wynn Resorts Casinos & Gaming WYNN, $90.28

Mark Strawn

WYNN brings Las Vegas to Macau Comments from management

Exposure Today

Gaming market opens up

Three years after the liberalization of the gaming industry in Macau, in 2006 WYNN opened its first casino in the region. Like the local competition but unlike Las Vegas Sands, its main foreign competitor, WYNN focuses almost exclusively on the VIP segment of the casino business, which accounts for 75% of total revenue in the $20-billion Macau gaming market. Over the 12 months ending June 30, 2010, 77% of WYNN’s $2.7 billion of casino revenues in Macau came from the VIP segment.

WYNN currently derives 70% of its revenue and 75% of its EBITDA from Macau (the remainder comes from Las Vegas). WYNN generates the highest returns on invested capital—50%, as compared with the industry average of 21%—and the highest operating metrics (EBITDA per gaming table and EBITDA per square foot of development) in Macau.

Year to date, overall gaming revenues in Macau are up 67% and VIP revenues 85% in response to three recent changes in the region’s gaming industry: the improved availability of credit for VIP players; the opening of additional casinos in Macau, including WYNN’s Encore hotel in April 2010; and the removal of travel restrictions from China into Macau in late 2009. Longer term, as year-over-year comparisons get tougher, we expect the Macau gaming market to grow at a rate of 10%-15% per year. The major drivers will be continued economic growth in China, rising disposable incomes, an expanding middle class, and China’s commitment to making Macau the leisure hub of the Pan Pearl River Delta.

Strategy

Expansion in Cotai

With a relatively clean balance sheet (1.1x net debt) and strong free cash flow generation ($700 million per year), the next step in WYNN’s development plan likely will be a major project in Macau’s Cotai district, which resembles the Las Vegas Strip in Nevada. We expect an announcement later this year of a WYNN Cotai project costing more than $2.75 billion, with completion expected in 2014.

Competition

Courting the VIP segment

WYNN competes almost exclusively in the VIP segment of Macau, where it has the second highest market share (behind the local incumbent, SJM Holdings.) While this has been an extremely profitable strategy to date, we believe growth will decelerate, with the mass casino segment becoming the fastest growing segment of the business starting in 2011. We believe future casino projects on Cotai and infrastructure developments throughout the Pan Pearl River Delta will increase the appeal of and facilitate travel to Macau.

The major risks for all Macau operators include government intervention (such as travel and currency restrictions between China and Macau) and slowing economic growth in China.

“The Asian market is very, very aware of the top brands, and that’s why we’re so meticulous in making sure that we meet that demand. For example, it is nonproductive for us to appeal to the low-end market in China because the government does not encourage the low-end of China to go to Macau. They don’t mind if people who can afford it go and gamble, but they’re sensitive to people who can’t afford it going across the border to Macau. That’s why they pulled back on the visas. But for those people in Hong Kong and South China from Taiyuan and Shanghai who can afford the good life, there’s no stigma attached to that in China, and there are so many of them.” 1

Stephen Wynn, Chairman and

CEO

1FactSet, 1Q2010 earnings call transcript.

M O R G A N S T A N L E Y R E S E A R C H

18

September 20, 2010The China Files

Market Overview RestaurantsLin He

Dining Out in China

Market Today

Strong but fragmented

China’s restaurant industry has posted robust growth, outpacing nominal GDP and consumer expenditure growth.

From 2000 to 2008, the share of restaurant food as a percentage of the total food budget for Chinese urban residents climbed from 14.7% to 20.6%. For rural residents, this ratio climbed from 2002’s 10.6% to 2007’s 13.7%. By means of comparison, in 2008 restaurant food accounted for about 47% of total food expenditures in the US.

Current growth topped 20% during the 1990-2008 period. We attribute this to rising per-capita income, a faster-paced lifestyle, and a demographic shift to smaller families.

Foreign brands like KFC and McDonald’s are the leading players in the fast food segment, with market share of 17.6% and 6.1%, respectively, in consumer food service in 2009.

Long-term Outlook

Moving into the fast lane

China’s Ministry of Commerce projected 16.5% CAGR for the industry for the time period of 2009-2013.

Although independent outlets still dominate China’s restaurant industry, chain brands will grow much more quickly than will non-chained restaurants.

We believe that foreign brands will continue to lead in the fast food segment because of their existing presence in the sector, economies of scale, and strong logistical capabilities.

What Does it Take to Win in China?

Standardized operations, strong brand awareness, and rapid expansion through franchising

Industry Revenue Growth

-

500

1,000

1,500

2,000

2,500

3,000

3,500

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10e

13e

(Rmb bn)

90-08: 21.1% CAGR

09-13e: 16.5% CAGR

Sources: China Statistical Year Book, Morgan Stanley Research. E=China Cuisine Association estimates and Mofcom.

GDP and Total Consumer Spending

0%

10%

20%

30%

40%

50%

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Nominal GDP YoY Growth Restaurant Industry Revenue YoY GrowthTotal Consumer expenditure YoY

Sources: China Statistical Year Book, Morgan Stanley Research.

M O R G A N S T A N L E Y R E S E A R C H

19

September 20, 2010The China Files

Top Pick: Yum! Brands RestaurantsYUM, $45.92

John Glass

YUM Defines Food-Service Market in China Comments from management

Exposure Today

The industry standard

For more than two decades, YUM has set the standard for food service operations in China. Building on a reputation for innovation and expansion, the company has developed a broad supply chain and distribution network that allows faster unit growth and higher store returns than peers over time. China contributed 31% of total company revenues in 2009, second only to the US, at 41%. Within five years, we expect China will be YUM’s largest market, generating more than 50% of revenues and between 45%-50% of operating profits.

YUM operates more than 3,500 restaurants in mainland China; in 2009 these restaurants generated operating margins of 20%. YUM’s operating profit has grown on average about 30% each year over the last five years. From here, YUM’s primary profit growth driver will remain the expansion of its store base, with same-store sales growth and G&A leverage as secondary drivers. Currently, YUM is opening around 475 new stores per year; we look for this pace to continue over the next five years, at approximately 2,400 stores, with sales expected to grow around 15% CAGR.

Strategy

New stores, new services

China is management’s primary geographic focus. With average unit volumes at more than $1.2 million and margins of 20%, YUM can open new restaurants with a cash payback of within two to three years. The company plans to expand its Pizza Hut Home Service and a Chinese quick service restaurant chain, East Dawning, with 21 stores currently, and it has a 27% stake in Little Sheep, a Chinese hot pot concept. Additional growth opportunities may exist through day-part expansion (breakfast and late-night service) and new product categories, like fountain and hot beverages.

“Our strategy is to have the leading brands in every significant category. What we’re trying to do is build every one of our brands into power brands so [that] we compete effectively. And as the buying power of the consumer increases, which it will inevitably do, we will be able to take advantage of it.”

1

“When you step back and look at where we’re at with China, it’s pretty difficult to imagine a better scenario. We couldn’t be happier, and we just keeping growing talent like you can’t believe there. That’s one of those intangibles that you can’t see. But our talent level is better, our operations continue to be best-in-class, [and] we’re leveraging the asset throughout the day. We’re in one thousand stores in home delivery, one thousand stores in 24-hour service—we’re just getting started.” 1

David Novak, Chairman, CEO

and President

Competition

A breakaway leader

YUM has world-class infrastructure, with its own food distribution system, and one of the largest real estate and construction teams anywhere in the world—two competitive advantages. McDonald’s, YUM’s primary competitor in China, is less than half of YUM’s size, and the market can easily accommodate both. The strengthening renminbi offers a benefit to earnings, with inputs sourced locally and profits denominated in US dollars. We estimate that every 1% appreciation of the renminbi is worth $0.01 per share of EPS annually (our 2010 EPS estimate is $2.50). Exogenous risks such as political restrictions on property building, which would limit planned unit expansion, or a health scare (for example, the 2006 avian flu outbreak), could significantly affect YUM’s growth plans.

1FactSet, 2Q2010 earnings call transcript.

M O R G A N S T A N L E Y R E S E A R C H

20

September 20, 2010The China Files

Market Overview HPCAngela Moh

Foreign Dominance to Continue

Market Today

Foreign players already claim dominant positions

China's household and personal care industry has enjoyed solid growth over the past 10 years; CAGRs for the years 1998-2008 range from 5% to 10%, depending on the category.

Markets are still far from saturation, though: Per-capita consumption of many product categories remains very low, compared with that in more developed countries.

Industry growth could accelerate over the next three to five years, supported by sustained per-capita income growth, continued urbanization, premiumization (consumers trading up for better quality), and enhanced distribution, with retail companies gradually tapping into low-tier cities.

Foreign players have been very successful in HPC markets due to advertising and marketing efforts. Local players are also strong in select categories due to a more comprehensive distribution network.

Long-term Outlook

Stable, rapid growth

We expect 10%-15% annual growth rates for leading players in HPC markets in the next decade.

Foreign players will continue dominate many sub-segments, but local rivals are rising quickly in a few niche fields such as natural products based on traditional Chinese herbs.

What Does it Take to Win in China?

Marketing, branding, and distribution

Hair Care: China Market Growth

Retail Sales of Hair Care Products in China

-

10,000

20,000

30,000

40,000

50,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

E

2011

E

2012

E

2013

E

2014

E

Rmb mn

1999-09 CAGR = 8.9%

2009-14 CAGR = 10.4%

Source: Morgan Stanley Research.

Skin Care: China Market Growth

Retail Sales of Skin Care Products in China

-

20

40

60

80

100

120

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

E

2010

E

2011

E

2012

E

2013

E

Rmb bn

1998-08 CAGR = 16.8%

2008-13 CAGR = 14.8%

Source: Morgan Stanley Research.

M O R G A N S T A N L E Y R E S E A R C H

21

September 20, 2010The China Files

Top Pick: Procter & Gamble HPCPG, $61.11

Dara Mohsenian

Procter & Gamble Already a Dominant Player Comments from management

Exposure Today

A major product leader

Procter & Gamble holds a 13% share of the household and personal care market and is the largest consumer products company in China. PG is the market leader in 11 of its 12 product categories within the region.

Overall, PG has grown at a 5% CAGR over the last five years, and over the next five years we expect a 4% CAGR. Today China is PG’s second biggest market, but it only accounts for around 6% of total sales, well behind the US, at 39%. We expect sales to grow from $5 billion to $8 billion by 2015, which would equal about 8% of total company sales.

We estimate that the Chinese household and personal care segment will grow at an 11% CAGR over the next five years. Three cultural shifts will contribute to this growth: consumer preference for premium products as income levels rise, consumer preference for natural and organic products in reaction to concerns about product safety, and product-driven changes in personal habits.

Strategy

More options on the menu

PG will continue to roll out new products as the market becomes more receptive (see bullet 3 above). Management sees significant potential to expand horizontally by introducing more product categories in the region as appropriate for the rising economic power of the Chinese consumer (PG is currently underpenetrated in several categories in China, such as home care and consumer health). PG has already invested heavily in infrastructure (like distribution) and is preparing to diversify its product offerings into lower-end price segments so as to offer a complete portfolio of products to Chinese consumers.

Competition

Room to expand

PG’s overall HPC market share is disproportionately low in China because of its narrower range of product offerings. The company is preparing to access this untapped potential through its improved infrastructure and a stronger focus on the region. Per capita consumption of PG products in China is about $3 annually, below the BRIC’s weighted average rate of $4 and much lower than the $20 rate in Mexico, or the even higher rate developed markets—$110 in the US. For perspective, if PG were able to close the personal care consumer gap for its products between China and Brazil, it would add a total estimated 15% to its current top-line. PG faces stiff competition in China from Colgate (in oral care), L’Oreal and Unilever (in beauty/personal care), and SC Johnson (in home care), and from strong local companies in paper products, consumer health, and fabric care.

“The biggest opportunity we have is to get all of our categories into all of our countries around the world. We have about 36 product categories, and we’re in all those categories in the United States, where we’ve been for 172 years. But in countries like China, where we lead, we’re in just over a dozen—probably about 16. So we have work to do to adapt those categories for the Chinese market.” 1

Bob McDonald, Chairman, President, and CEO

“Some companies may take the attitude that China is a growth market where they need to build a position for tomorrow, thinking that eventually they could raise profitability to target levels. This is not what we are trying to accomplish in China. We have set adequate, definable profit objectives for ourselves and believe that from both a strategic and an organizational focus this is the best way to take on the cost challenge involved in serving the mid-tier consumer segment in China. Tough profit objectives force you to get your cost structure competitive.” 2

Laurent Philippe, President for Greater China

1FactSet, 4Q2010 (FY) earnings call transcript.

2McKinsey Quarterly, “Understanding the Chinese Consumer,” July 2004.

M O R G A N S T A N L E Y R E S E A R C H

22

September 20, 2010The China Files

Market Overview PharmaceuticalsBin Li

Visible Fast Growth Ahead

Market Today

A counter-cyclical growth industry

We saw a 21% CAGR for the overall healthcare market during the last six years, versus a global average of 9%.

China’s aging population drives demand. In 2007 China had 107 million citizens aged 65 and above, versus 88 million in 2000, for a CAGR of 2.8%. Another driver is China’s rising income level, especially in urban areas, and greater access to insurance (we expect full coverage of China’s 1.3 billion people by 2020).

Multinational healthcare companies are actively seeking partnerships with Chinese companies, although the regulatory environment favors local players. Competition is intense in low-/mid-end products.

Long-term Outlook

Fast growth sustainable

Industry growth could reach a CAGR of more than 20% in the next five years, well above the estimated global average of 5%.

We expect that China’s healthcare reform will increase the country’s pharmaceutical user base and medical spending per capita. The government also plans to allocate more resources to underserved rural areas and nonworking classes and provide more affordable healthcare services to a broader population.

Multinationals should choose to enter partnerships with strong local players.

What Does it Take to Win in China?

Distribution and technology

Industry Sales Trend

0

200

400

600

800

1,000

2004 2005 2006 2007 2008E

0%

5%

10%

15%

20%

25%

30%

China Pharmaceuticals Sales (RMB bn) YOY (%)

Source: Morgan Stanley Research.

Industry Margin Trend

0%

10%

20%

30%

40%

50%

2004 2005 2006 2007 2008E

Gross Margin% Net Margin% Source: Morgan Stanley Research.

M O R G A N S T A N L E Y R E S E A R C H

23

September 20, 2010The China Files

Top Pick: Pfizer PharmaceuticalsPFE, $17.27

David Risinger

Major Commitment to Build Presence Comments from management

Exposure Today

Top foreign pharmaceutical company in China

Pfizer is the largest foreign pharmaceutical company in China, and China is one of Pfizer’s priority markets. We estimate PFE’s 2010 China sales will be about $2 billion, or approximately 3% of its global sales. China’s pharmaceutical market—estimated at about $40 billion in 2010—is highly fragmented, however, and Pfizer has captured only about 2% of it. To increase its market share, the company plans to expand its presence in the region from the 2009 level of about 2,300 sales reps in 177 cities to 3,300 sales reps in 272 cities in 2010 and 5,400 sales reps in 360 cities by 2012. Pfizer also plans to extend its research and development capabilities in China: The company has operated one manufacturing facility in Dalian since 1989 and a research hub in Shanghai since 2005; to these Pfizer will add a new clinical R&D center in Wuhan to support its global clinical programs. Pfizer estimates that the China pharmaceutical market will grow to about $100 billion by 2015, at which point it will become Pfizer’s third-largest market.

Strategy

Adapt to China’s unique business environment

PFE plans to drive incremental organic growth by focusing on core brands and new product launches. Chronic diseases common in the US and Europe (for example, high cholesterol, hypertension, and diabetes) are increasing in China due to a richer diet and more sedentary lifestyle. To address these conditions and others, Pfizer offers blockbuster drugs that we expect to be major drivers of growth in China: Lipitor for cholesterol, Norvasc for high blood pressure, and the Prevnar-13 vaccine for pneumococcal disease.