Embed Size (px)

Citation preview

Financial Accounting

1

Lecture – 13

Recap

• Analysis and Recording of transactions

• Preparation of ledger accounts

• Calculation of ledger balance

• Preparation of trial balance

• Preparation of a basic profit and loss and balance sheet

Financial Accounting

2

Lecture – 13

Areas Covered in This Lecture

• Different types of vouchers

• Carrying of balance from one period to the next period

• Recording the transaction of February and preparation of trial balance

Financial Accounting

3

Lecture – 13

Voucher

• Specific format

• Control of transactions

• Serial numbered

Financial Accounting

4

Lecture – 13

Types of Voucher

• Receipt voucher

• Payment voucher

• Journal voucher

Financial Accounting

5

Lecture – 13

Receipt Voucher

• Receipt voucher is used to record receipt of cash or cheque

• Receipt vouchers can be further divided into Cash Receipt and Bank Receipt vouchers

Financial Accounting

6

Lecture – 13

Receipt Voucher

Name of the Organization

Bank Receipt / Cash Receipt OR Receipt Voucher

Date: No:

Cash / Bank code: Description / Title:

Description /

Title of Account

Code

#

Credit

Amount

Total:

Narration:

Prepared By: Checked by:

Financial Accounting

7

Lecture – 13

Payment Voucher

• Payment voucher is used to record a payment of cash or cheque

• Payment vouchers can be further divided into Cash Payment and Bank Payment vouchers

Financial Accounting

8

Lecture – 13

Payment Voucher

Name of the Organization

Bank Payment / Cash Payment OR Payment Voucher

Date: No:

Cash / Bank code: Description / Title:

Description /

Title of Account

Code

#

Credit

Amount

Total:

Narration:

Prepared By: Checked by:

Financial Accounting

9

Lecture – 13

Journal Voucher

• Journal voucher is used to record transactions that do not effect cash and bank account

Financial Accounting

10

Lecture – 13

Journal Voucher

Name Of Organization

Journal Voucher

Date: No:

Description Code

#

Debit

Amount

Credit Amount

Total:

Narration:

Prepared By: Checked by:

Financial Accounting

11

Lecture – 13

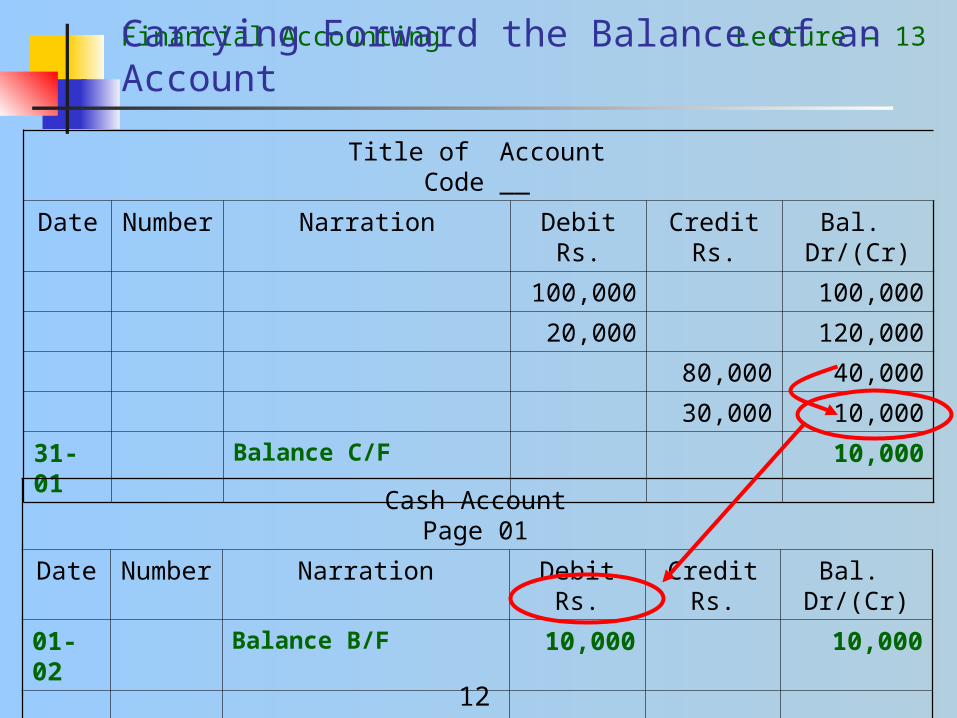

Carrying Forward the Balance of an Account

Title of Account Account Code 01

Debit Side Credit Side

Date No. Narration Dr. Rs. Date No. Narration Cr. Rs.

100,000 80,000

20,000 30,000

31-01 Balance C/F 10,000

120,000 120,000

Title of Account Account Code 01

Debit Side Credit Side

Date No. Narration Dr. Rs. Date No. Narration Cr. Rs.

01-02 Balance B/F 10,000

Financial Accounting

12

Lecture – 13

Carrying Forward the Balance of an Account

Title of AccountCode __

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

100,000 100,000

20,000 120,000

80,000 40,000

30,000 10,000

31-01 Balance C/F 10,000

Cash AccountPage 01

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

01-02 Balance B/F 10,000 10,000

Financial Accounting

13

Lecture – 13

No. Date Particulars

20--

01 Feb 02 Deposited Rs. 25,000 in bank

02 Feb 02 Expense accrued last month reduced by Rs. 5,000

03 Feb 05 Expense accrued last month paid through cheque Rs. 15,000

04 Feb 06 Received Rs. 14,000 cash from Mr. B (debtor)

05 Feb 07 Discount given to Mr. B. Rs. 1,000

Financial Accounting

14

Lecture – 13

No. Date Particulars

20--

06 Feb 10 Goods purchased on credit from Mr. A Rs. 60,000

07 Feb 12 Goods sold on credit to Mr. B Rs. 95,000

08 Feb 15 Placed Rs. 75,000 in fixed deposit

09 Feb 17 Paid to Mr. A Rs. 25,000 through cheque

10 Feb 20 Received cash from Mr. B. Rs. 75,000

11 Feb 28 Salaries accrued Rs. 5,000

12 Feb 28 Expenses accrued Rs. 15,000

Financial Accounting

15

Lecture – 13

Ali Traders

Trial Balance As On January 31, 20--

Title of Account Code Dr. Rs. Cr. Rs.

Cash Account 01 35,000

Bank Account 02 130,000

Capital Account 03 200,000

Furniture Account 04 15,000

Vehicle Account 05 50,000

Purchases Account 06 60,000

Mr. A (Creditor) 07 15,000

Sales 08 95,000

Mr. B (Debtor) 09 15,000

Salaries 10 5,000

Expenses 11 20,000

Expenses Payable 12 20,000

Total 330,000 330,000

Financial Accounting

16

Lecture – 13

01 – Deposited Rs. 25,000 in Bank

Bank AccountCode 02

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 130,000 130,000

Feb 02 01 Cash deposited 25,000 155,000

Cash AccountCode 01

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 35,000 35,000

Feb 02 01 Cash deposited 25,000 10,000

Financial Accounting

17

Lecture – 13

02 – Expense Accrued Last Month Reduced by Rs. 5,000

Expenses AccruedCode 12

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 20,000 (20,000)

Feb 02 02 Expenses payable reduced 5,000 (15,000)

Expense AccountCode 11

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 20,000 20,000

Feb 02 02 Expenses payable reduced 5,000 15,000

Financial Accounting

18

Lecture – 13

03 – Expense Accrued Last Month Paid Through Cheque Rs. 15,000

Expenses AccruedCode 12

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 20,000 (20,000)

Feb 02 02 Expenses payable reduced 5,000 (15,000)

Feb 05 03 Expenses payable paid 15,000 0

Bank AccountCode 02

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 130,000 130,000

Feb 02 01 Cash deposited 25,000 155,000

Feb 05 03 Expenses payable paid 15,000 140,000

Financial Accounting

19

Lecture – 13

04 – Received Rs. 14,000 Cash From Mr. B (Debtor)

Mr. BCode 09

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 15,000 15,000

Feb 06 04 Cash received from B 14,000 1,000

Cash AccountCode 01

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 35,000 35,000

Feb 02 01 Cash deposited 25,000 10,000

Feb 06 04 Cash received from B 14,000 24,000

Financial Accounting

20

Lecture – 13

05 – Discount Given to Mr. B. Rs. 1,000

Mr. BCode 09

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 15,000 15,000

Feb 06 04 Cash received from B 14,000 1,000

Feb 07 05 Discount given to B 1,000 0

discount AccountCode 13

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 0 0

Feb 07 05 Discount given to B 1,000 10,000

Financial Accounting

21

Lecture – 13

06 – Goods Purchased on Credit From Mr. A Rs. 60,000.

Mr. ACode 07

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 15,000 (15,000)

Feb 10 06 Credit purchases from B 60,000 (75,000)

Purchases AccountCode 06

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 60,000 60,000

Feb 10 06 Credit purchases from B 60,000 120,000

Financial Accounting

22

Lecture – 13

07 – Goods Sold on Credit to Mr. B Rs. 95,000.

SalesCode 08

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 95,000 (95,000)

Feb 12 07 Credit sale to B 95,000 (190,000)

Mr. BCode 09

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 15,000 15,000

Feb 06 04 Cash received from B 14,000 1,000

Feb 07 05 Discount given to B 1,000 0

Feb 12 07 Credit sale to B 95,000 95,000

Financial Accounting

23

Lecture – 13

08 – Placed Rs. 75,000 in Fixed Deposit

Fixed DepositCode 14

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 0 0

Feb 15 08 Fixed deposit placed 75,000 75,000

Bank AccountCode 02

Date Number Narration Debit Rs. Credit Rs. Bal. Dr/(Cr)

Feb 01 Balance B/F 130,000 130,000

Feb 02 01 Cash deposited 25,000 155,000

Feb 05 03 Expenses payable paid 15,000 140,000

Feb 15 08 Fixed deposit placed 75,000 65,000