Embed Size (px)

Citation preview

DAILY REPORT

08th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance

Asian stocks rose modestly on Thursday, taking their cue from gains on Wall Street as the region braced for a re-sumption of trading in the Chinese markets after a week-long break. MSCI's broadest index of Asia-Pacific shares outside Japan tacked on 0.3 percent, supported by South Korea's Kospi rising 0.5 percent and Australian shares climbing 0.9 percent. Japan's Nikkei bucked the trend and lost 0.2 percent on a stronger yen.

Overnight on Wall Street, the S&P 500 soared to a 3-week high thanks to a bounce in biotechnology companies. Ma-terials shares also enjoyed a positive session on the back of gains for precious metals.

Chinese stock markets, which have been hit by wild swings in recent months due to growth and policy worries, re-open later in the session after shutting since the end of September for holidays.

European shares ended slightly higher on Wednesday, giv-ing up earlier gains as a three-day rally appeared to lose momentum, but gains among miners and autos offset a decline in airline stocks. The pan-European FTSEurofirst 300 index pared gains in the last stretch of the session to end up 0.12 percent. The index had earlier gained more than 1 percent to touch its highest level in about one month. Wall Street weighed on European shares while short covering appeared to have come to an end with global economic concerns emerging again. Some investors still expect loose monetary policies to help the rally continue, in spite of weak economic data

Previous day Roundup

Bulls maintained winning streak on Dalal Street as the mar-ket rose for the sixth straight session. The Sensex ended up 102.97 points or 0.4 % at 27035.85. The Nifty was up 24.50 points or 0.3 % at 8177.40. About 1660 shares advanced, 1081 shares declined and 114 shares were unchanged. Meanwhile, oil, metals and auto stocks supported the mar-ket while IT index fell 1.7 % from previous close.

Index stats

The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [up 18.22pts], Capital Goods [up 12.84pts], PSU [up 78.10pts], FMCG [up 19.82Pts], Realty [up 26.53pts], Power [up 24.41pts], Auto [up 243.48Pts], Healthcare [up 31.70Pts], IT [down 188.49pts], Metals [up 197.05pts], TECK [down 87.10pts], Oil& Gas [up 115.92pts].

World Indices

Index Value % Change

D J l 16912.29 +0.73

S&P 500 1995.83 +0.80

NASDAQ 4791.15 +0.90

FTSE 100 6336.35 +0.16

Nikkei 225 18199.14 -0.68

Hong Kong 22337.30 -0.79

Top Gainers

Company CMP Change % Chg

HINDALCO 81.85 6.85 9.13

VEDL 90.70 5.00 5.83

CAIRN 167.60 8.80 5.54

ONGC 260.00 12.65 5.11

TATASTEEL 236.10 8.60 3.78

Top Losers

Company CMP Change % Chg

HCLTECH 820.05 33.55 -3.93

WIPRO 587.30 12.05 -2.01

TCS 2,655.00 45.00 -1.67

BHARTIARTL 343.30 5.55 -1.59

AXISBANK 498.40 8.00 -1.58

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

APOLLOHOSP 1,480.00 -19.00 -1.27

CEATLTD 1,286.00 -13.55 -1.04

GRANULES 154.00 4.70 3.15

JINDALPOLY 472.05 21.65 4.81

JUBILANT 397.00 -0.65 -0.16

JINDALPOLY 472.05 21.65 4.81

JUBILANT 397.00 -0.65 -0.16

Indian Indices

Company CMP Change % Chg

NIFTY 8177.40 +24.50 +0.30

SENSEX 27035.85 +102.97 +0.36

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

- -

DAILY REPORT

08th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

STOCK RECOMMENDATION [CASH] 1. [CASH]

Last session NCLINDIA given sharp up move and finished with 11% gain at life time high of 124.15 where the volume was also increase by 10 time, since EOD candle it bulish Marubozu so we advise to buy it above 125 for target of 128-133-140 with stop loss of 121 MACRO NEWS NTPC-SAIL Power Co gets green nod to expand Durgapur

plant Mutual Funds see Rs 77,000 cr outflow in Sep Crude price can touch $60/ bbl by year-end: Fat Proph-

ets Fund raising via retail NCDs plunges 72% to Rs 1,250 cr Bank of Maha gets nod to raise Rs 394 cr by equity

shares Bajaj Allianz Life ties-up with Dhanlaxmi Bank for distri-

bution of products ONGC sets 280 wells in Jharkhand for coal bed methane Chinese firm starts sourcing Guinea bauxite, sidelining

India R-Infra puts cement biz on block Cipla Pact With Biopharm SPA To Set Up JV Co In Algeria Tata Tele wants airwaves freed for 4G services Apollo Health, subsidiary of Apollo Hospitals looks to

raise `500 cr Govt seeks higher profit from Cairn’s Bar-mer hydrocarbon block

DHFL Cuts Home Loan Rates By 20 bps To 9.65% Tech Mahindra In Pact With Transport Systems Catapult

To Deliver Intelligent Mobility Solutions Cairn India Seeks Cut In Cess On Crude As Oil Prices

Halve Man Industries Gets Orders Worth `700 Cr Tata Motors Launches Bolt Hatchback & Sedan In South

Africa

STOCK RECOMMENDATIONS [FUTURE] 1. YESBANK [FUTURE]

From last three trading session YESBANK future trading in narrow range because of index heavyweight not giving big move for that it correct from 760 at last session it finished at 740 with loss of 0.80%, but on EOD chart it following down side trend line whose support at 735 so we advise to buy it near support around 730-735 use stop loss at 715 for target of 750-765+. 2. APOLLO HOSPITAL [FUTURE]

APOLLO HOSPITAL moving near to life time high around 1518 which is it trend line resistance for that it finished with long legged candle at Last session it finished with loss so it is good to sell around 1495-1505 use stop loss at 1525 for tar-get of 1475-1450-1400.

DAILY REPORT

08th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 8,300 84.70 4,74,117 46,20,425

NIFTY CE 8,400 47.60 3,88,366 32,61,100

BANKNIFTY CE 18,000 273.80 48,984 4,56,900

RELIANCE CE 920 21.40 6,221 3,98,250

TATAMOTOR CE 350 9.30 5,142 7,04,500

SBIN CE 250 5.95 4,946 52,08,000

HINDALCO CE 80 4.85 4,692 20,40,000

TATASTEEL CE 240 8.40 4,285 10,83,000

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 8,000 77.00 4,74,409 41,71,625

NIFTY PE 8,100 104.25 3,80,926 39,83,975

BANKNIFTY PE 17,000 200.00 43,055 5,91,875

TATAMOTOR PE 320 6.40 4,359 9,15,500

RELIANCE PE 880 9.85 3,465 3,08,750

RELIANCE PE 900 16.00 3,114 3,74,000

INFY PE 1,140 50.35 2,728 4,30,000

TATASTEEL PE 220 4.05 2,188 9,94,000

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 97585 2200.77 47624 1061.26 984369 22287.1 1139.513

INDEX OPTIONS 268446 7223.67 281692 7438.85 2061365 65205.8 -215.187

STOCK FUTURES 85883 2231.75 98345 2694.44 1784346 46667.1 -462.689

STOCK OPTIONS 70207 1722.27 74685 1841.78 97406 2651.59 -119.512

TOTAL 342.12

STOCKS IN NEWS Reliance ADAG exploring options exit cement business Punj Lloyd bags orders worth Rs 488 crore; shares up

over 6% Tata Steel hopes get Gopalpur SEZ notification in Nov JubilantLife gets USFDA nod for Indomethacin capsules HC restrains Glenmark from anti-diabetes drugs busi-

ness Cairn seeks cut in cess on crude as oil prices halve Tata Motors launches two new brands in South Africa NIFTY FUTURE

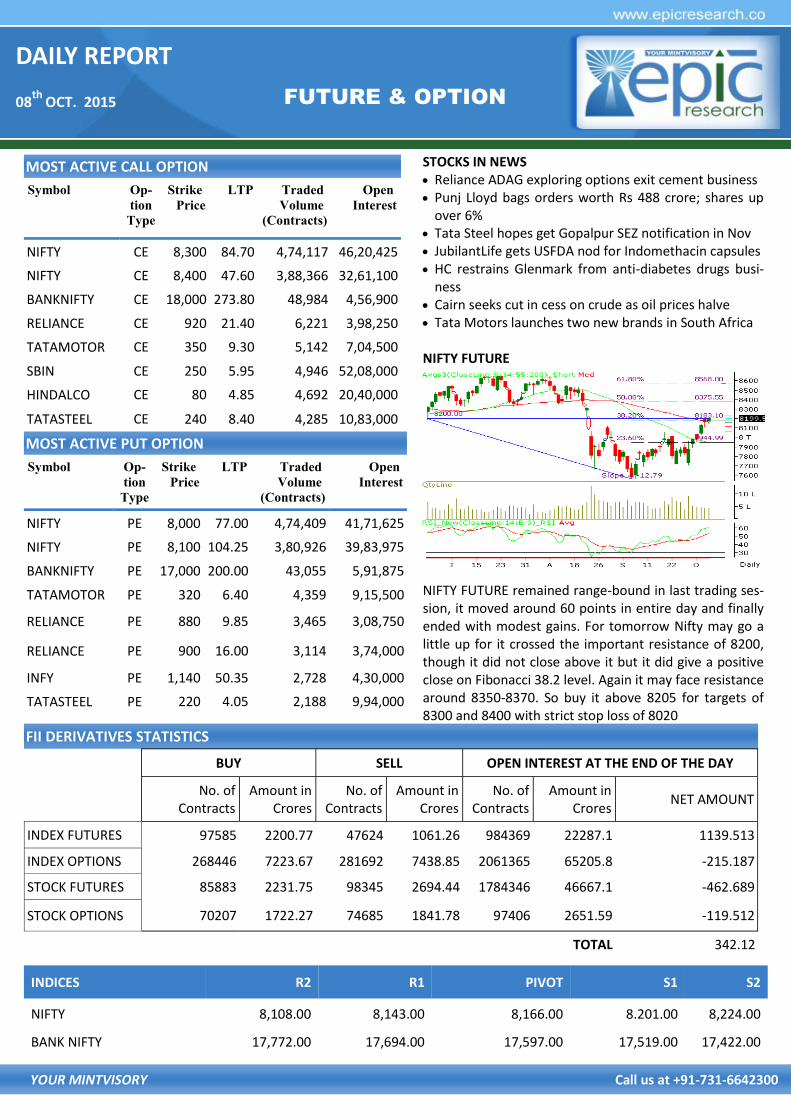

NIFTY FUTURE remained range-bound in last trading ses-sion, it moved around 60 points in entire day and finally ended with modest gains. For tomorrow Nifty may go a little up for it crossed the important resistance of 8200, though it did not close above it but it did give a positive close on Fibonacci 38.2 level. Again it may face resistance around 8350-8370. So buy it above 8205 for targets of 8300 and 8400 with strict stop loss of 8020

INDICES R2 R1 PIVOT S1 S2

NIFTY 8,108.00 8,143.00 8,166.00 8.201.00 8,224.00

BANK NIFTY 17,772.00 17,694.00 17,597.00 17,519.00 17,422.00

DAILY REPORT

08th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RECOMMENDATIONS

GOLD

TRADING STRATEGY:

BUY GOLD OCT ABOVE 26650 TGTS 26730,26820 SL BE-

LOW 26550

SELL GOLD OCT BELOW 26500 TGTS 25420,25330 SL

ABOVE 26600

SILVER

TRADING STRATEGY:

BUY SILVER DEC ABOVE 37700 TGTS 37900,38200 SL BE-

LOW 37400

SELL SILVER DEC BELOW 37300 TGTS 37100,36800 SL

ABOVE 37600

COMMODITY ROUNDUP Gold stayed supported today amid global economic worries, rising geopolitical tensions and a strong undertone in physi-cal demand from the major importers. Equities stayed in afix after recent array of gains as traders eyed rising geopo-litical worries and US economic data showed a mixed pic-ture. Russian and Syrian airstrikes continued to hit ISIS tar-gets. However, the scenario became intense after another violation of Turkish airspace by Russian planes. COMEX Gold futures extended these gains in Asia and currently trade at$1151 per ounce, up 0.40% on the day. However, the MCX Gold futures are trading at Rs26625 per 10 grams, al-most unchanged on the day after hitting highs near Rs 26800 mark. The Indian Rupee gained impressively today, gaining around half a percent to break under65 per US dol-lar mark. Gold speculator and large futures traders in-creased their gold bullish positions higherlast week for a second consecutive week and to the highest level since June The rise in the weekly net speculator positions (+15,520 net contracts) was due to a small gain in the weekly bullish posi-tions by +712 contracts which combined with a large de-crease in the weekly bearish positions by -14,808 contracts. The net speculator contracts are now at the highest bullish position since June 23rd when net positions equaled +95,114 contracts. In the commercial positions for gold on the week, the commercials (hedgers or traders engaged in buying and selling for business purposes) added to their overall bearish positions to a net total position of -73,143 contracts through September 29th. This was a weekly change of -15,915 contracts. The International Copper Study Group (ICSG) has revised its forecasts for copper. From earlier estimate ofsurplus supply in 2016, it has now estimated a deficit for the bellwether base metal, despite slowdown in Chinese demand. In April this year, the industry body had projected surplus in 2015 and slightly lower surplus in 2016, too. The forecasts came after discussions with government delegates and industry advisors from leading copper producing and using countries. Oil headed for its longest rally in almost six months as US industry data showed crude stockpiles fell in the world's biggest consumer. WTI futures rose as much as 2.4% in New York, climbing for a fourth day in the longest advance since April. Inventories dropped by 1.23mn barrels last week. Brent for November settlement rose $1.01 to $52.93 a bar-rel on the London-based ICE Futures Europe exchange. It increased $2.67 to $51.92 on Tuesday. The European benchmark crude was at a premium of $3.32 to WTI.

DAILY REPORT

08th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

NCDEX ROUNDUP Rising for the third straight day, barley prices went up by another Rs 47 to Rs 1,440 per quintal at futures trade today as participants enlarged positions, tracking a firming trend at the physical market. Persistent rise in barley prices at futures trade was mostly supported by a firming trend at the physical markets on the back of strong demand from-beer and cattle-feed industries against restricted supplies from growing belts. At barley for delivery in April spurted by another Rs 47, or 3.37 per cent, to Rs 1,440 per quintal, with an open interest of 70 lots. The November contract climbed Rs 29.50, or 2.23 per cent, to Rs 1,349.50 per quin-tal, having an open interest of 11,090 lots, while contracts for delivery in October rose Rs 21, or 1.66 per cent, to Rs 1,286.50 per quintal, in an open interest of 9,550 lots. Mentha oil prices were up by 1.03% to Rs 871.50 per kg, largely supported by rising demand in the spot markets. In futures trading at the MCX mentha oil for delivery in Nov gained Rs 8.90, or 1.03%, to Rs 871.50 per kg, with a trading volume of 55 lots. The oil for delivery in October edged up by Rs 8.60, or 1.01%, to Rs 859.40 per kg, with a business turnover of 355 lots. A firming trend at the spot market on pick up in demand amid restricted supplies from Chandausi in UP, mainly influenced mentha oil prices at futures trade. Supported by fall in supplies from growing regions, carda-mom futures rose 0.60% to Rs 817.80 per kg in futures trade today as traders creating speculative positions. Be-sides, firm spot demand influenced cardamom prices. At MCX cardamom for delivery in Nov was up by Rs 4.90, or 0.60%, to Rs 817.80 per kg, with a business turnover of 166 lots. The delivery in Oct also went up by Rs 3.80, or 0.50%, to Rs 763.40 per kg, with a trading volume of 23 lots.

NCDEX INDICES

Index Value % Change

CAETOR SEED 4090 -0.85

CHANA 5002 -2.36

CORIANDER 11455 -0.74

COTTON SEED 1622 +0.25

GUAR SEED 4050 +0.40

JEERA 15810 +0.29

MUSTARDSEED 4634 +0.02

REF. SOY OIL 628.95 +0.21

TURMERIC 7708 +0.16

WHEAT 1579 +0.83

RECOMMENDATIONS

DHANIYA

BUY CORIANDER NOV ABOVE 11760 TARGET 11787 11867

SL BELOW 11733

SELL CORIANDER NOV BELOW 11500 TARGET 11473 11393

SL ABOVE 11527

GUARSGUM

BUY GUARGUM NOVABOVE 8800 TARGET 8850 8920 SL

BELOW 8740

SELL GUARGUM NOVBELOW 8570 TARGET 8520 8450 SL

ABOVE 8630

DAILY REPORT

08th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 65.2571 Yen-100 54.3400

Euro 73.4664 GBP 99.5301

CURRENCY

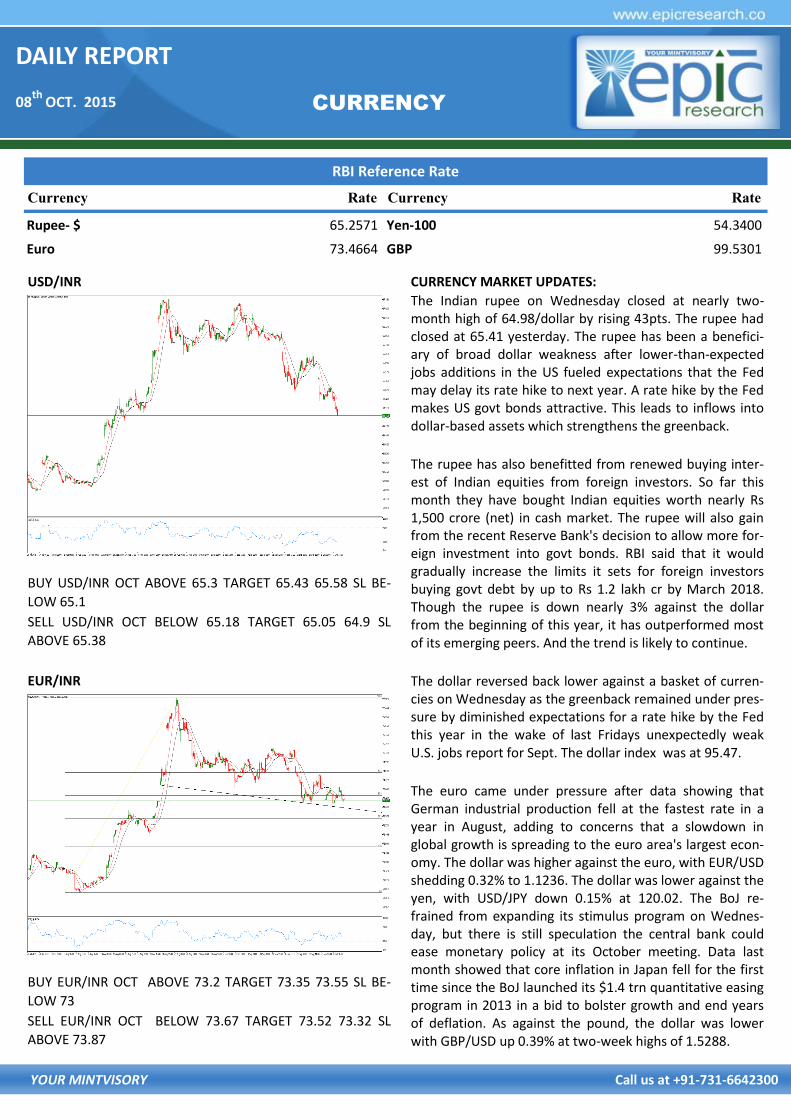

USD/INR

BUY USD/INR OCT ABOVE 65.3 TARGET 65.43 65.58 SL BE-

LOW 65.1

SELL USD/INR OCT BELOW 65.18 TARGET 65.05 64.9 SL

ABOVE 65.38

EUR/INR

BUY EUR/INR OCT ABOVE 73.2 TARGET 73.35 73.55 SL BE-

LOW 73

SELL EUR/INR OCT BELOW 73.67 TARGET 73.52 73.32 SL

ABOVE 73.87

CURRENCY MARKET UPDATES:

The Indian rupee on Wednesday closed at nearly two-month high of 64.98/dollar by rising 43pts. The rupee had closed at 65.41 yesterday. The rupee has been a benefici-ary of broad dollar weakness after lower-than-expected jobs additions in the US fueled expectations that the Fed may delay its rate hike to next year. A rate hike by the Fed makes US govt bonds attractive. This leads to inflows into dollar-based assets which strengthens the greenback.

The rupee has also benefitted from renewed buying inter-est of Indian equities from foreign investors. So far this month they have bought Indian equities worth nearly Rs 1,500 crore (net) in cash market. The rupee will also gain from the recent Reserve Bank's decision to allow more for-eign investment into govt bonds. RBI said that it would gradually increase the limits it sets for foreign investors buying govt debt by up to Rs 1.2 lakh cr by March 2018. Though the rupee is down nearly 3% against the dollar from the beginning of this year, it has outperformed most of its emerging peers. And the trend is likely to continue.

The dollar reversed back lower against a basket of curren-cies on Wednesday as the greenback remained under pres-sure by diminished expectations for a rate hike by the Fed this year in the wake of last Fridays unexpectedly weak U.S. jobs report for Sept. The dollar index was at 95.47.

The euro came under pressure after data showing that German industrial production fell at the fastest rate in a year in August, adding to concerns that a slowdown in global growth is spreading to the euro area's largest econ-omy. The dollar was higher against the euro, with EUR/USD shedding 0.32% to 1.1236. The dollar was lower against the yen, with USD/JPY down 0.15% at 120.02. The BoJ re-frained from expanding its stimulus program on Wednes-day, but there is still speculation the central bank could ease monetary policy at its October meeting. Data last month showed that core inflation in Japan fell for the first time since the BoJ launched its $1.4 trn quantitative easing program in 2013 in a bid to bolster growth and end years of deflation. As against the pound, the dollar was lower with GBP/USD up 0.39% at two-week highs of 1.5288.

DAILY REPORT

08th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

CALL REPORT

S T O

PERFORMANCE UPDATES

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

07/10/15 NCDEX DHANIYA OCT. BUY 11580 11607-11687 11553 BOOKED PROFIT

07/10/15 NCDEX DHANIYA OCT. SELL 11483 11456-11376 11510 BOOKED FULL PROFIT

07/10/15 NCDEX GUARGUM OCT. BUY 8530 8580-8650 8470 BOOKED FULL PROFIT

07/10/15 NCDEX GUARGUM OCT. SELL 8200 8150-8080 8260 NOT EXECUTED

07/10/15 MCX GOLD OCT. BUY 26800 26880-26970 26700 NOT EXECUTED

07/10/15 MCX GOLD OCT. SELL 26600 25520-25430 26700 BOOKED FULL PROFIT

07/10/15 MCX SILVER DEC. BUY 37500 37700-38000 37200 NOT EXECUTED

07/10/15 MCX SILVER DEC. SELL 37200 37000-36700 37500 SL TRIGGERED

07/10/15 USD/INR OCT. BUY 65.70 65.83-65.98 65.50 NOT EXECUTED

07/10/15 USD/INR OCT. SELL 65.55 65.42-65.27 65.75 BOOKED FULL PROFIT

07/10/15 EUR/INR OCT. BUY 73.70 73.85-74.05 73.50 BOOKED PROFIT

07/10/15 EUR/INR OCT. SELL 73.45 73.30-73.10 73.65 BOOKED PROFIT

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

07/10/15 NIFTY FUTURE SELL 8180-8200 8100-8000 8350 CALL OPEN

07/10/15 IBREALEST FUTURE BUY 71.5 73-75 70.50 BOOKED PROFIT

07/10/15 CEAT FUTURE BUY 1310 1325-1340 1299 SL TRIGGERED

07/10/15 GRANULES CASH BUY 151 154-157 148 BOOKED PRFOIT

06/10/15 NIFTY FUTURE SELL 8180-8200 8080-7950 8350 CALL OPEN

06/10/15 PFC FUTURE BUY 247-252 258-264 241 SL TRIGGERED

06/10/15 MOTHERSON SUMI CASH BUY 235-240 250-255 215 CALL OPEN

DAILY REPORT

08th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any responsibility (or

liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere efforts have been made to present the

right investment perspective. The information contained herein is based on analysis and up on sources that we consider reliable. This material is for per-

sonal information and based upon it & takes no responsibility. The information given herein should be treated as only factor, while making investment

decision. The report does not provide individually tailor-made investment advice. Epic research recommends that investors independently evaluate par-

ticular investments and strategies, and encourages investors to seek the advice of a financial adviser. Epic research shall not be responsible for any trans-

action conducted based on the information given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projec-

tions shown are not necessarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change

without notice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone who is

browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either the site or its owners

or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this disclaimer. All Rights Reserved. Investment

in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the completeness thereof. We are not responsible for any

loss incurred whatsoever for any financial profits or loss which may arise from the recommendations above epic research does not purport to be an invi-

tation or an offer to buy or sell any financial instrument. Our Clients (Paid or Unpaid), any third party or anyone else have no rights to forward or share

our calls or SMS or Report or Any Information Provided by us to/with anyone which is received directly or indirectly by them. If found so then Serious

Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, OCT. 05

10 AM ISM NONMANUFACTURING INDEX SEPT. 57.5% 59.0%

TUESDAY, OCT. 06

8:30 AM TRADE DEFICIT AUG. -$48.1 BLN -$41.9 BLN

WEDNESDAY, OCT. 07

3 PM CONSUMER CREDIT AUG. -- $19 BLN

THURSDAY, OCT. 08

8:30 AM WEEKLY JOBLESS CLAIMS OCT. 3 271,000 277,000

2 PM FOMC MINUTES SEPT. 17

FRIDAY, OCT. 09

8:30 AM IMPORT PRICE INDEX SEPT. -- -1.8%

10 AM WHOLESALE INVENTORIES AUG. -- -0.1%