Embed Size (px)

DESCRIPTION

entry of reliance in telecom sector

Citation preview

PROJECT REPORT

ENTRY OF RELIANCE IN THE TELECOMMUNICATION SECTOR

Submitted by

Amulya Kalia(400907002)

Anupam Garg(400907003)

Karan Garg(400907011)

LMTSOM

THAPAR UNIVERSITY, PATIALA

June 2012

Contents

What is a STRATEGY? .................................................................................................................. 3

What is STRATEGIC MANAGEMENT?...................................................................................... 3

METHODOLOGY FOR SM .......................................................................................................... 4

INDIAN TELECOM SECTOR ...................................................................................................... 5

INDUSTRY ANALYSIS ............................................................................................................... 7

PORTER’S FIVE FORCES MODEL ......................................................................................... 7

STRATEGIES FOR TELECOM SECTOR .............................................................................. 10

SWOT ANALYSIS ................................................................................................................... 14

RELIANCE COMMUNICATIONS ............................................................................................. 15

RCOM STRATEGIES .................................................................................................................. 20

PRICING STRATEGY ............................................................................................................. 20

SALES AND MARKETING STRATEGY: ............................................................................. 21

ADVERTISING: ....................................................................................................................... 21

What is a STRATEGY?

STRATEGY is a method or plan chosen to bring about a desired future, such as achievement of

a goal or solution to a problem.

What is STRATEGIC MANAGEMENT?

STRATEGIC MANAGEMENT analyzes the major initiatives taken by a company's top

management on behalf of owners, involving resources and performance in internal and external

environments. It entails specifying the organization's mission, vision and objectives, developing

policies and plans, often in terms of projects and programs, which are designed to achieve these

objectives, and then allocating resources to implement the policies and plans, projects and

programs.

Strategic Management is all about identification and description of the strategies that managers

can carry so as to achieve better performance and a competitive advantage for their organization.

An organization is said to have competitive advantage if its profitability is higher than the

average profitability for all companies in its industry.

Strategic management can also be defined as a bundle of decisions and acts which a manager

undertakes and which decides the result of the firm’s performance. The manager must have a

thorough knowledge and analysis of the general and competitive organizational environment so

as to take right decisions. They should conduct a SWOT Analysis (Strengths, Weaknesses,

Opportunities, and Threats), i.e., they should make best possible utilization of strengths,

minimize the organizational weaknesses, make use of arising opportunities from the business

environment and shouldn’t ignore the threats. Strategic management is nothing but planning for

both predictable as well as unfeasible contingencies.

Strategic Management is a way in which strategists set the objectives and proceed about attaining

them. It deals with making and implementing decisions about future direction of an organization.

It helps us to identify the direction in which an organization is moving.

Strategic management is a continuous process that evaluates and controls the business and the

industries in which an organization is involved; evaluates its competitors and sets goals and

strategies to meet all existing and potential competitors; and then reevaluates strategies on a

regular basis to determine how it has been implemented and whether it was successful or does it

needs replacement.

Strategic Management gives a broader perspective to the employees of an organization and they

can better understand how their job fits into the entire organizational plan and how it is co-

related to other organizational members. It is nothing but the art of managing employees in a

manner which maximizes the ability of achieving business objectives. The employees become

more trustworthy, more committed and more satisfied as they can co-relate themselves very well

with each organizational task. They can understand the reaction of environmental changes on the

organization and the probable response of the organization with the help of strategic

management. Thus the employees can judge the impact of such changes on their own job and can

effectively face the changes. The managers and employees must do appropriate things in

appropriate manner. They need to be both effective as well as efficient.

One of the major role of strategic management is to incorporate various functional areas of the

organization completely, as well as, to ensure these functional areas harmonize and get together

well. Another role of strategic management is to keep a continuous eye on the goals and

objectives of the organization.

METHODOLOGY FOR SM

There are many different frameworks and methodologies for strategic planning and

management. While there is no absolute rules regarding the right framework, most follow a

similar pattern and have common attributes. Many frameworks cycle through some variation

on some very basic phases: 1) analysis or assessment, where an understanding of the current

internal and external environments is developed, 2) strategy formulation, where high level

strategy is developed and a basic organization level strategic plan is documented 3) strategy

execution, where the high level plan is translated into more operational planning and action

items, and 4) evaluation or sustainment / management phase, where ongoing refinement and

evaluation of performance, culture, communications, data reporting, and other strategic

management issues occurs.

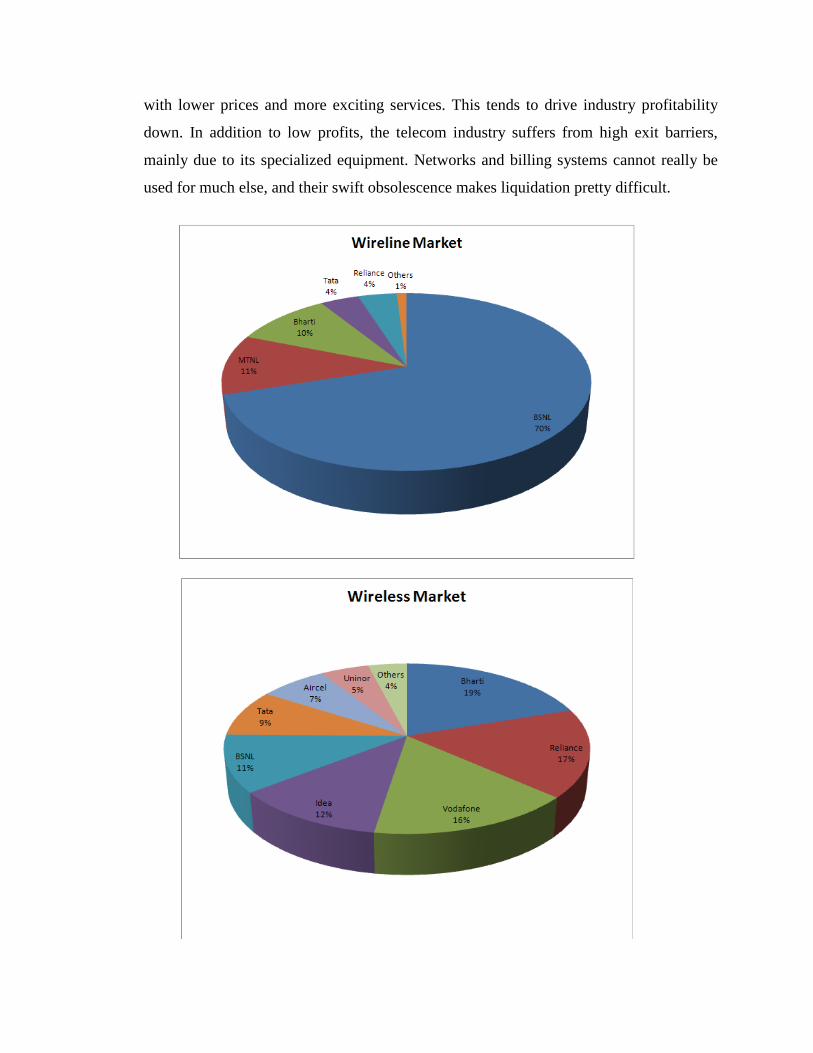

INDIAN TELECOM SECTOR

India has the fastest growing telecom network in the world with its high population and

development potential. Airtel, Vodafone, Idea, Reliance, Tata DoCoMo, BSNL, Aircel, Tata

Indicom, MTNL and Loop Mobile are the major operators in India. However, rural India still

lacks strong infrastructure. India's public sector telecom company BSNL is the 7th largest

telecom company in world.

Telephony introduced in India in 1882. The total number of telephones in the country stands at

960.9 million, while the overall teledensity has increased to 79.28% as of May 31, 2012 and the

total numbers of mobile phone subscribers have reached 929.37 million as of May 2012. The

mobile teledensity has increased to 76.68% in May 2012. In the wireless segment, 8.35 million

subscribers were added in May 2012. The wire line segment subscriber base stood at 31.53

million.

Indian telecom operators added a staggering 227.27 million wireless subscribers in the 12

months between Mar 2010 and Mar 2011 averaging at 18.94 million subscribers every month. To

put this into perspective, China which currently possesses the world's largest telecommunications

network added 119.2 million wireless subscribers during the same period (March 2010 - March

2011) averaging 9.93 million subscribers every month (a little over half the number India was

adding every month). So, while India might currently be second to China in the total number of

mobile subscribers, India has been adding nearly twice as many subscribers every month until

March 2011. Mobile teledensity increased by almost 18.4 percentage points from Mar 2010 and

Mar 2011 (49.60% to 67.98%) while wire line subscriber numbers fell by a modest 2.2 million.

This frenetic pace of monthly subscriber additions means that the Indian mobile subscriber base

has shown a year on year growth of 43.23%. According to recent reports, India was purported to

overtake China to become the world's largest mobile telecommunications market by the year

2013. It was also predicted that by 2013, the teledensity will shoot up to 75% and the total

mobile subscriber base would be a colossal 1.159 billion.

Rank in world in network size 3rd

Tele density (per hundred populations) 79.28

Telephone connections (In Million)

Fixed 929.37

Mobile 31.53

Total 960.9

INDUSTRY ANALYSIS

PORTER’S FIVE FORCES MODEL

1. Threat of New Entrants. It comes as no surprise that in the capital-intensive telecom

industry the biggest barrier to entry is access to finance. To cover high fixed costs,

serious contenders typically require a lot of cash. When capital markets are generous, the

threat of competitive entrants escalates. When financing opportunities are less readily

available, the pace of entry slows. Meanwhile, ownership of a telecom license can

represent a huge barrier to entry. In addition, it is important to remember that solid

operating skills and management experience is fairly scarce, making entry even more

difficult.

2. Power of Suppliers. At first glance, it might look like telecom equipment suppliers have

considerable bargaining power over telecom operators. Indeed, without high-tech

broadband switching equipment, fiber-optic cables, mobile handsets and billing software,

telecom operators would not be able to do the job of transmitting voice and data from

place to place. But there are actually a number of large equipment makers around. There

are enough vendors, arguably, to dilute bargaining power. The limited pool of talented

managers and engineers, especially those well versed in the latest technologies, places

companies in a weak position in terms of hiring and salaries.

3. Power of Buyers. With increased choice of telecom products and services, the

bargaining power of buyers is rising. Let's face it; telephone and data services do not vary

much, regardless of which companies are selling them. For the most part, basic services

are treated as a commodity. This translates into customers seeking low prices from

companies that offer reliable service. At the same time, buyer power can vary somewhat

between market segments. While switching costs are relatively low for residential

telecom customers, they can get higher for larger business customers, especially those

that rely more on customized products and services.

4. Availability of Substitutes. Products and services from non-traditional telecom

industries pose serious substitution threats. Cable TV and satellite operators now compete

for buyers. The cable guys, with their own direct lines into homes, offer broadband

internet services, and satellite links can substitute for high-speed business networking

needs. Railways and energy utility companies are laying miles of high-capacity telecom

network alongside their own track and pipeline assets. Just as worrying for telecom

operators is the internet: it is becoming a viable vehicle for cut-rate voice calls. Delivered

by ISPs - not telecom operators - "internet telephony" could take a big bite out of telecom

companies' core voice revenues.

5. Competitive Rivalry. Competition is "cut throat". The wave of industry deregulation

together with the receptive capital markets of the late 1990s paved the way for a rush of

new entrants. New technology is prompting a raft of substitute services. Nearly

everybody already pays for phone services, so all competitors now must lure customers

with lower prices and more exciting services. This tends to drive industry profitability

down. In addition to low profits, the telecom industry suffers from high exit barriers,

mainly due to its specialized equipment. Networks and billing systems cannot really be

used for much else, and their swift obsolescence makes liquidation pretty difficult.

STRATEGIES FOR TELECOM SECTOR

Scope - Business Portfolio: In the telecom sector, there are a number of ways by which a new

entrant can develop its business portfolio. The key issue is whether the firm wants to be an

integrated or focused player. Reliance Infocom, Bharti Televentures, and Tata Teleservices are

positioning themselves as integrated players, though with differing levels of scope and

commitment, and with desires to have a presence in basic (both wire line and wireless) as well as

national and international long distance. All three companies are laying a fibre optic network

across the country to build backbone infrastructure, though the scale at which Reliance is

building far exceeds that of, say, Tata Teleservices. Bharti's project to connect Chennai and

Singapore through an underground cable shows its commitment to international long distance

market. Reliance additionally has eyes on the data services segment which is slated to exceed the

voice traffic very soon.

Scope-Geographical: Number of geographical sectors where a new entrant to the domestic

telecom sector wishes to be present is also a key decision. The range of choices available can

include local, regional and national. For example, Reliance Infocom, given its big bang

approach, plans to cover all the 18 telecom circles in India. As against this, Bharti seems to be

focussing on south and north Indian circles, Tata Telesrvices in Andhra Pradesh, while smaller

players with limited resources such as HFCL Infotel and Shyam Telecom are concentrating on a

single circle.

Value Propositions: There are essentially three generic strategies, viz. differentiation, cost

leadership and niche, for competing in any industry. This basic concept is applicable in telecom

sector too, though pursuing the niche strategy may not be viable, given the fact that the

boundaries within and across various segments are increasingly getting blurred, possibility of

substitute completion is high (for example Internet telephony can eat into national and

international long distance market and vice versa), bulk of the backbone infrastructure to serve

basic, national long distance and international long distance are common and scale intensive,

benefits of network externalities and positive feedback are real and opportunities for cross

subsidising any niche segment with a view to achieving dominance through predatory pricing is

feasible.

Value Chain Configuration: Configuration of value chain depends on the generic strategy

being pursued and critical capabilities the firm has or proposes to have. If differentiation is the

objective, identification of key value propositions around which the proposed differentiation will

be achieved and capabilities needed to deliver those, will determine which activities will be

performed in-house and which ones will be outsourced but operationally synchronised. For

example, Reliance Infocom, to whom a key value proposition will be to provide customers with

an opportunity to experience and taste their information products and services, proposes to set up

thousands of company owned web stores, where customers can buy mobile phones and

accessories, play online games, hold video-conferences and use Internet. For customers who will

place orders for phones online, deliveries will be made through courier service. They have also

put in place a consumer marketing group to sell the company's products and services as an

FMCG company would do.

Technology Platform: There exist a large number of technological options in telecom field,

each characterised by unique features, complexities, investment requirement, reliability and

maintenance need. Care is needed while selecting a particular technology since such decisions

will have implications for value creation process as well as on cost incurred to create and deliver

the same. Other associated but important issues are problems of lock-ins and switching costs and

flexibility to switch over to next generation technologies without wholesale rejection of legacy

system. In an industry such as telecom where technology is fast changing, service providers will

need to be extra cautious before making irreversible commitment to a particular type or

generation of technology.

Strategic Alliance Partner: When faced with the daunting task of mobilising resources,

technology and marketing capabilities needed to face formidable competitors having all these

inputs, companies lacking these resources to the required degree often enter into strategic

alliances with partners having complementary skills, resources and geographical presence, the

aim being to improve the chance of success in the unfolding industry. The choice of alliance

partners can be critical to future success. A series of strategic alliances, both formal and

informal, have already been entered into in the Indian telecom sector by companies who are

either constrained by shortages of resources or do not have adequate presence in all geographical

markets.

Legal Structure: An important choice for a firm planning to make a big foray into the Indian

telecom sector in is the kind of legal structure it should have, to drive its strategy and business

plan. For example - should it have separate legal entities for servicing wire line, wireless and

data services? Should it have an independent company for running the backend infrastructure

and a separate outfit for providing the information and related services? Should the long distance

(both national and international) be kept separate from basic services? Questions like these and

similar others are very common in telecom sector and the choice will differ from company to

company. Each of these options will have different legal, financial and organizational

implications and individual companies will need to make decisions in this regard, keeping in

view the big picture they have and also the administrative implications.

Mode of Entry: In India, different telecom operators followed different entry strategies for

entering different segments of the industry, based on their respective assessment of how the

chosen route would provide specific advantages like lowering the cost of and time of entry and

access to markets being targeted. Both Hutchison and Bharti entered the Calcutta cellular market

through acquiring existing operators, who originally entered the industry through green field

project using technical know-how from overseas collaborators but could not run the business as

they did not have the deep pockets.

Timing of Entry And Roll Out: In case of a fast changing industry such as telecom which is

characterized by availability of variety of technologies and standards and evolving regulations,

timing of entry and roll out is a major strategic decision. Too early an entry involving

irreversible commitments may turn out to be wrong while delayed entry may mean lost

opportunities. In information goods industry, it is generally perceived that early movers get

advantage over late entrants and such advantages are difficult to overcome once these accrue to

the first movers.

Subsequent to the entry of various new players into the cellular market, each making major

financial, technological and organizational commitments, the Government made a number of

policy changes such as allowing the incumbent public sector unit to offer cellular services

without paying the steep license fee, change of fee structure from fixed licensed fee concept to

revenue sharing concept and most importantly allowing the basic service providers to offer

limited mobility, all of which may put a downward pressure on future profitability of cellular

segment. During this period, there were also developments on the technology front and

advantages and disadvantages of GSM and CDMA technologies particularly with regard to voice

quality, roaming facility and broadband services in relation to cellular services became clearer.

Pace of execution: The speed at which a project will be executed is a major decision that can

have important cost implications. It is well known that longer the execution time more will be

the overall cost of the project. The delay will also imply loss of opportunity to use the

investments being made. In case of the telecom industry, where investments involved are very

high and there is also the necessity to delay consciously the actual commencement of project

execution for reasons discussed in the previous section, the importance of high speed execution

cannot be overemphasized. Reliance Group, which is known for its rapid project execution

capabilities (they had put up a 30 million ton grass root refinery involving an investment of US$

4 billion in just 14 months in late 90's) could afford to delay taking a final decision on

technology and project scope because of their confidence and capability to execute any mega

project rapidly.

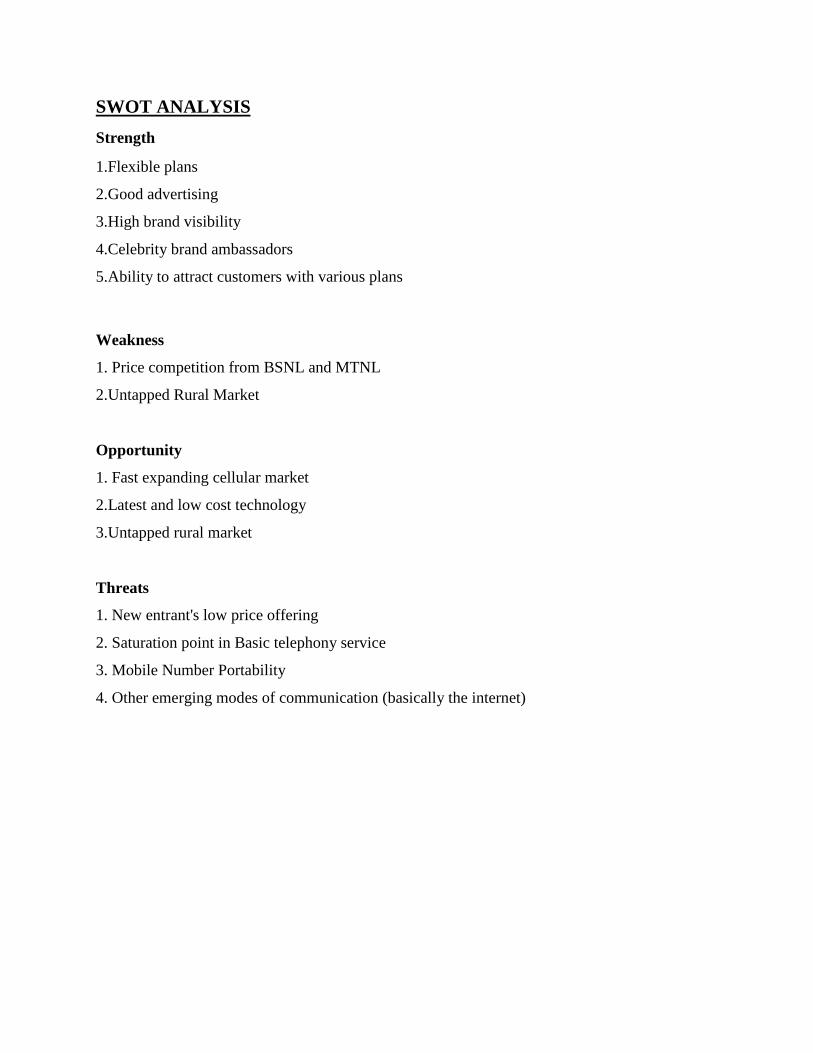

SWOT ANALYSIS

Strength

1.Flexible plans

2.Good advertising

3.High brand visibility

4.Celebrity brand ambassadors

5.Ability to attract customers with various plans

Weakness

1. Price competition from BSNL and MTNL

2.Untapped Rural Market

Opportunity

1. Fast expanding cellular market

2.Latest and low cost technology

3.Untapped rural market

Threats

1. New entrant's low price offering

2. Saturation point in Basic telephony service

3. Mobile Number Portability

4. Other emerging modes of communication (basically the internet)

RELIANCE COMMUNICATIONS Reliance Communications Ltd. (commonly called RCOM) is an Indian broadband and

telecommunications company headquartered in Navi Mumbai, India. RCOM is India's second

largest telecom operator, only after Bharti Airtel. It is world's 15th largest mobile phone

operator with over 150 million subscribers. Established in 2004, it is a subsidiary of the Reliance

Group. The company has five segments: Wireless segment includes wireless operations of the

company; broadband segment includes broadband operations of the company; Global segment

include national long distance and international long distance operations of the company and the

wholesale operations of its subsidiaries; Investment segment includes investment activities of the

Group companies, and Other segment consists of the customer care activities and direct-to-

home (DTH) activities.

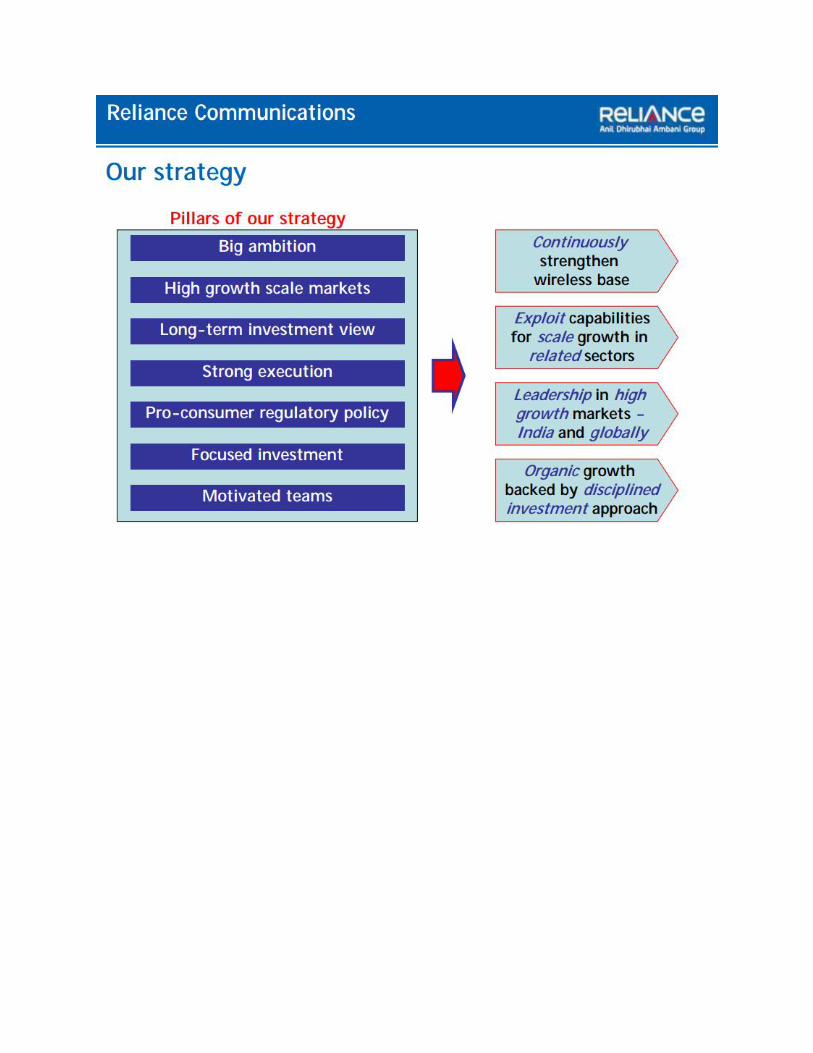

VISION

-By 2015, be amongst the top 3 most valued Indian companies,

-Providing Information, Communication & Entertainment services, and being the industry

benchmark in

-Customer Experience, Employee Centricity and Innovation

MISSION

Create world-class benchmarks by:

Meeting and exceeding Customer expectations with a segmented approach

Establishing, re-engineering and automating Processes to make them customer centric,

efficient and effective

Incessant offering of Products and Services that are value for money and excite customers

Providing a Network experience that is best in the industry

Building Reliance into an iconic Brand which is benchmarked by others and leads industry

in Intention to Purchase and Loyalty

Developing a professional Leadership team that inspires, nurtures talent and propagates

RCOM Values by personal example

RCOM STRATEGIES

PRICING STRATEGY

“My vision is to provide the latest telecommunication facilities to every Indian at the price of a

post card” – Dhirubhai Ambani.

“A monthly telecom spend of Rs 2503 ($5.6) would usher in a telecom revolution in India. At

that rate, the telecom market will be around 600 million lines,” said B D Khurana, former group

President and CEO, Reliance Infocomm.

Reliance Infocomm challenged conventional cost structures in the telecommunications industry.

Historically, telecommunication services have been the privilege of a small section of society.

Reliance Infocomm broke this mould with a tariff that is the most ambitious ever listed by a

telecom company in India. It aimed for prices as low as the cheapest alternative – the postcard.

While other operators aimed for the value market, Reliance Infocomm realized that there is a

market in driving volumes and aimed at creating a completely new market. “According to

estimates, there are around 320 million households with an annual income of Rs 1.5 lakh

($3,333). Out of that, half are in rural area with similar purchasing power. And this segment is

expected to grow to 478 million by 2007 and to 602 million by 2010” commented BD Khurana,

former group President and CEO, Reliance Infocomm, hinting about the market that Reliance

infocomm aimed to capture.

SALES AND MARKETING STRATEGY:

Reliance targeted internally as it looked around for the first set of customers. Officials of

Reliance Infocomm realized that an employee base of more than 50,000 and a shareholder base

of about 3.3 million was the best place to start as far as customers are concerned. Every

employee was offered 10 connections at a discounted rate. While the normal monthly charges

would be Rs.600 ($13.3), for the employees it was offered at Rs.500 ($11.1). Many employees

bought Reliance connections for many of their relatives and friends. During the annual general

meeting the Reliance Chairman offered shareholders a discount package. The company offered

Rs.850 ($18.9) discount on initial payments on subscription per connection. In addition, the

shareholders were offered free usage worth Rs.100 ($2.2) for the next six months. This amounted

to a total discount of Rs.1,450 ($32.2) per connection. In addition the shareholders were

encouraged to promote Reliance Infocomm connections among their circle of influence. If a

shareholder subscribed to two connections, he or she would get free usage worth Rs.100 ($2.2)

per connection for the next 12 months, in addition to the Rs.850 ($18.9) per connection discount.

This amounted to a total discount of Rs.4,100 ($91.1) for two connections.

ADVERTISING:

Advertising was definitely a marketing strategy which complemented the unconventional

channels of Reliance Infocomm. The Reliance mobile brand was branded as IndiaMobile to cash

in on patriotic feelings. Bundling of handsets along with the service – a first time in India –

allowed Reliance Infocomm to resort to a co-branding exercise with the handset makers. The

Reliance Infocomm brand name embossed on every handset gave it a unique mileage, while the

costs of many of the advertisements were discounted since they were borne together with the

handset makers. A mega advertising campaign was launched across the media to mark the

launch. The blitzkrieg coincided with the world cup cricket tournament. This ensured that

practically the whole of India was watching and listening. The main theme of the first campaign

built on the vision of Reliance Infocomm in bringing the power of telecommunications to every

common person. This campaign helped educating people on the importance of

telecommunication services. The next set of campaigns talked about the innovative product

features, which differentiated Reliance Infocomm from competitors. The advertisements

announced that Reliance IndiaMobile was 'Kabhi mobile, kabhi computer' (Sometimes Mobile,

Sometimes Computer). In the subsequent campaigns Reliance started riding on movies and

cricket as a theme. Overall three things emerge from the way Reliance handled the media. Firstly

Reliance built a huge public relations exercise around the launch of the product. The public

relations gave much leverage to the advertising and gave rise to a word of mouth campaign.

Secondly Reliance Infocomm utilized every media vehicle effectively. Literally it advertised on

every single TV channel available and every single newspaper available, thus making sure that

the product was being promoted across India – a nation very much divided by language and

market conditions. At the peak Reliance Infocomm booked about 5,000 spots in 40 TV channels,

1 million sq ft of spaceon hoardings across the country and inserted ads in over 70 publications

in national and regional languages. Thirdly, Reliance Infocomm relied on the passions of India,

while framing advertisements. The campaigns that had an emotional note to them, piggy backed

on Cricket and Bollywood (equivalent of Hollywood in India) – two main themes of India, thus

effectively connecting to almost every Indian. For marketing promotions Reliance again

followed unconventional strategies. The mobile service was promoted aggressively through

every single marketing channel. Huge signages were put up in front of every gas station, office

space in addition to the prime spots booked all across the nation. The bulk purchase of signages

ensured that the cost was low compared to the competitors. Reliance Infocomm also utilized

their telecom towers by putting up glow sign boards on them, which lit up during the night – an

innovative but cost effective strategy since most of the towers were in highly populated and

visible areas.

![THE BUSINESS STRATEGY OF CONNOISSEURS TECHNOLOGIES PRIVATE LIMITED [SERVICE PROVIDER OF RELIANCE TELECOM] WITH SPECIAL REFERENCE TO SALES STRATEGY, AT AGARTALA](https://img.dokumen.tips/doc/110x75/577ccfae1a28ab9e78904aae/the-business-strategy-of-connoisseurs-technologies-private-limited-service.jpg)