Embed Size (px)

Citation preview

Results of a survey conducted among Polish financial directors (CFOs) during a congress series: CFO of the Year

October 2016

Economy Shifts to a Lower Gear

Dear Reader,Once again, Grant Thornton had the honour to participate in the congress series: CFO of the Year. The opportunity to participate in the series of meetings of CFOs from all over Poland is an extremely valuable experience for us because CFOs, due to their function, are usually responsible for making key decisions in their companies, which indirectly affect the whole economy.

In order to ensure effective care of the financial condition of the company, CFOs need to have a very good understanding of the current economic situation, both in terms of their own business and economy as a whole. Therefore, for the third time, together with Euler Hermes, we decided to ask the participants of the CFO of the Year congress series, which were held in Poznan, Rzeszow, Katowice and Sopot, about their opinion on the economic perspectives for their companies and the entire economy in the next twelve months.

A record number of CFOs (more than 160) participated in the survey, which provided us with excellent material for analysis. And what conclusions can be drawn from the analysis? First of all, a decrease in optimism among CFOs, resulting, among others, from a slowdown in demand and rising payroll costs. However, the number of optimists continues to be higher than the number of pessimists – thus, there is no reason to panic.

Enjoy reading!

Tomasz Wróblewski

Managing Partner

Grant Thornton

A few words from the authorsGrant Thornton

A few words from the authorsEuler Hermes

Dear Reader,For the third time, financial directors attending a congress series: CFO of the Year, replied to the invitation of Grant Thornton and Euler Hermes and expressed their views on the economic outlooks for business in Poland.

Despite differences in the geographic location (different regions of the country) and the diametrically different industries and sectors of operations of the surveyed CFOs, the results gave rise to an interesting, coherent and logical picture. What is more: this picture indicates changes that we may expect in the future.

The CFO environment is well prepared for the current developments and challenges on the market. It has an extraordinary ability to identify risks early in the process, which provides CFOs with more time for adequate response. A perfect example of such ability is the manner in which the level of investment has been adjusted to the uncertain market situation and the whole business environment.

On the other hand, the survey demonstrates that Polish CFOs do not operate conservatively – and similarly to previous years, when they supported development of investment in businesses, they now focus on investment in employees.

This has been confirmed by recent statistics which show that the decreased level of investment is accompanied by the increased utilisation of production capacities of Polish companies. Employment growth is a logical and safe alternative to investments in fixed assets. This also indicates a growing role of CFOs in, and their responsibility for the key competitive advantage – i.e. human capital.

Have a closer look at the results of the survey. They are extremely interesting, and the conclusions will certainly help you in making everyday financial decisions in your companies.

Waldemar Wojtkowiak

Member of the Management Board, CFO

Euler Hermes

Key Conclusions

32 % of survey participants are optimistic about the economic outlooks for the next 12 months. This is a drop by 23 p.p. compared with last year’s survey. In addition, the percentage of CFOs who are pessimistic about the economic future has grown from 5 to 19 percent.

40 % of respondents – i.e. 21 p.p. less than in 2015 – believe that demand for products and services of their companies will grow.

41 % of CFOs – i.e. 15 p.p. more than last year – expect an increase in the average salaries of their employees.

CFOs are much less likely to invest than last year. The percentage of companies planning to purchase fixed assets has dropped from 70 to 59 percent.

Dwindling optimism of CFOs

Revenues of companies to slow down

Labour costs on the increase

Weakening investment climate

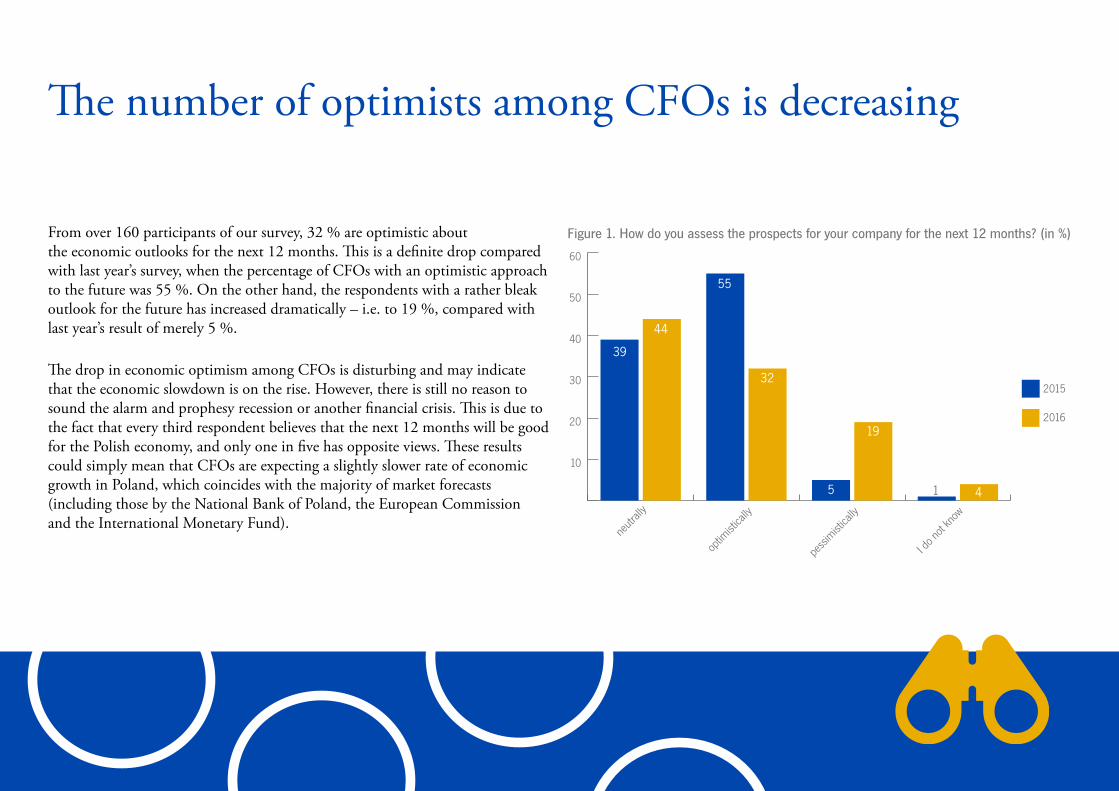

The number of optimists among CFOs is decreasing

Figure 1. How do you assess the prospects for your company for the next 12 months? (in %)

10

20

30

40

50

60

39

44

55

32

5

19

41

2015

2016

neutr

ally

optim

istica

lly

pessi

mistica

lly

I do n

ot kn

ow

From over 160 participants of our survey, 32 % are optimistic about the economic outlooks for the next 12 months. This is a definite drop compared with last year’s survey, when the percentage of CFOs with an optimistic approach to the future was 55 %. On the other hand, the respondents with a rather bleak outlook for the future has increased dramatically – i.e. to 19 %, compared with last year’s result of merely 5 %.

The drop in economic optimism among CFOs is disturbing and may indicate that the economic slowdown is on the rise. However, there is still no reason to sound the alarm and prophesy recession or another financial crisis. This is due to the fact that every third respondent believes that the next 12 months will be good for the Polish economy, and only one in five has opposite views. These results could simply mean that CFOs are expecting a slightly slower rate of economic growth in Poland, which coincides with the majority of market forecasts (including those by the National Bank of Poland, the European Commission and the International Monetary Fund).

The weakening optimism among CFOs may also be seen in the forecasts of demand for products and services of their companies. Currently, 40 percent of respondents believe that such demand will increase over the next 12 months, and only a year ago, this figure stood at 61 %. Moreover, the number of respondents who expect that the demand for products and services of their companies will continue at the current level increased by as many as 19 p.p. (from 29 to 48 %). The positive thing is certainly the fact that only 8 percent of CFOs (compared to 7 percent last year) expect a reduction in demand.

Expecting a decline in demand for their products, CFOs are forced to respond with price reductions. As many as half of the survey participants declare that they have recently experienced increased pressure to reduce prices of products and services of their companies, while only 7 percent of respondents say that the pressure has decreased. Finally, 36 percent of respondents did not feel any pressure to reduce their prices.

Growth in demand to slow down

Figure 2. What developments in the demand for your products and services do you expect in the next 12 months (in %)

Figure 3. How do you assess the current price levels in your industry, and the pressure to reduce them? (in %)

10

20

30

40

50

60

70

61

40

29

48

7 8 2 4

2015

2016

it will

grow

it will

not c

hang

e

it will

drop

I do n

ot kn

ow

10

20

30

40

5050

36

7 6

it has

increa

sed

it con

tinue

s

at the

same l

evel

it has

decre

ased

it is q

uite t

he op

posite

:

in my in

dustr

y,

price

s are

growing

Only every third respondent expects greater profitability of his/her company in the next 12 months. This is approx. 11 p.p. less than in the previous survey. In addition, there has been a significant decline in the difference between the percentage of CFOs expecting an increase in sales profitability and the percentage of CFOs expecting it to decrease. In 2015, the difference was less than 28 p.p., and now it has declined to merely 8.4 p.p. Approximately 40 % of respondents do not foresee any changes to profitability.

Not surprisingly, by analogy to last year, there has been a decrease in the percentage of CFOs who expect growing revenues from the domestic market and exports. The percentage of these CFOs continues to be greater than the percentage of CFOs expecting a decline in such revenues, yet the disparity has decreased. In this year’s edition of the survey, 48 % of respondents expect their company to generate more revenue in the domestic market, and 52 % expect an improvement in their export revenues. As compared with the previous year and the 2014 survey, this is a decrease by 13 and 2 p.p. and 19 and 13 p.p. respectively.

Unsatisfactory profitability

Figure 4. Do you think that over the next 12 months profitability will (in %) Figures 5. and 6. What developments in the domestic market and export revenues do you expect in the next 12 months (in %)

domestic market exports

4034

26

continue at the same level

grow

decrease

48they

will growthey will drop

35

17

they will continue at the same level

52

38

10they will drop

they will continue at the same level

they will grow

Another possible factor contributing to deteriorated sentiments of CFOs is the situation on the labour market in Poland. 41 % of survey participants, i.e. 15 p.p. more than last year, expect that over the next 12 months salaries in their companies will grow faster than the rate of inflation. CFOs realise that in order to keep the most qualified employees, i.e. those generating the greatest added value for the company, they will have to offer them better financial conditions. Thus, CFOs expect that in addition to decreasing revenues, labour costs will rise as well. As a result, they believe that profitability of their businesses in the nearest future will be under double pressure – both in terms of revenues and costs.

It is worth noting that there has been a decline in the percentage of CFOs who expect salaries to grow at a pace similar to the rate of inflation. This option has been chosen by 30 % of respondents - 18 p.p. less than last year. However, it is hardly surprising given the deflation which has become more pronounced in Poland since the last survey. This means that if salaries were to grow at the rate of inflation, in practice, their nominal value would have to decrease, which is rarely practiced in Polish companies. 28 % of CFOs say that salaries will remain at the current level.

Payroll costs on the rise

Figure 7. In the next 12 months, do you expect that average employee salaries will (in %)

10

20

30

40

50

26

41

48

3026 28

0 1

2015

2016

grow fa

ster th

an

the ra

te of

inflat

ion

grow at

the s

ame p

ace

as th

e rate

of in

flatio

n

not b

e inc

rease

d at a

ll

be re

duce

d

Fewer CFOs plan investments

Figure 8. In the next 12 months, do you intend to increase expenditure on (in %):

10

20

30

40

50

60

70

80

2015

2016

74

61

70

59

48 48

13

23

13

5

new m

arket

entrie

s

new m

achin

ery

and e

quipm

ent

resea

rch an

d deve

lopmen

t

acqu

isition

of

compa

nies i

n Pola

nd

acqu

isition

of ot

her

compa

nies a

broad

The slightly worse sentiment among CFOs is also shown in the analysis of their investment plans for the next 12 months. Although the majority of surveyed CFOs intend to increase their capital expenditures, especially those related to entering new markets or purchasing new machinery and equipment, the percentage of such CFOs has dropped by 13 p.p. (from 74 to 61 %) and 11 p.p. (from 70 to 59 %) respectively.

The same number of respondents as last year – 48 percent – have plans to increase their spending on research and development. This could mean that CFOs are becoming increasingly aware of the importance of innovation in the process of building competitiveness of a company, and therefore, intend to devote a larger portion of their budgets to R&D.

28 % of respondents declare their willingness to increase spending on the acquisition of other businesses. This number has increased by 2 p.p. as compared to last year, however, the structure of such acquisitions is slightly different. Last year, the same number of respondents, i.e. 13 %, planned acquisition of both Polish and foreign companies. In this year’s edition of the report – 23 % of CFOs have declared their plans to acquire domestic companies, but only 5 % have stated their interest in the acquisition of foreign businesses. Thus, the results went back to the 2014 status.

Surprisingly, despite the decreasing demand for products and services, and a lower percentage of financial directors declaring an increase in capital expenditure, the demand for new employees continues at a high level. The percentage of CFOs planning to increase employment is slightly growing – currently, as many as 41 percent of CFOs plan to increase the number of employees in their companies in the next twelve months – i.e. 4 p.p. more than last year. What is more, for the first time in the three-year history of our report, the number of companies planning to attract new workers is greater than the number of companies intending to maintain their employment at the current level. Only a year ago, the intention to maintain a stable number of employees was declared by every second respondent, but this year, the number has increased to 37 percent. Moreover, only 13 % of respondents – i.e. the same number as in 2015 – have plans to reduce their employment figures.

Greater demand for employees

Figure 9. In the next 12 months, does your company plan to (in %):

10

20

30

40

50

37

41

49

37

13 139

1

2015

2016

increa

se

emplo

ymen

t

keep

emplo

ymen

t

at the

same l

evel

reduc

e

emplo

ymen

t

I do n

ot kn

ow

In comparison with previous years, CFOs have demonstrated less optimism. Several factors have contributed to the deterioration in the sentiments of CFOs. The participants of our survey expect that in the next 12 months, the growth in the demand for their products and services will slow down, which is reflected in their profitability and revenue forecasts, also showing less optimism than last year. As a result of such slightly weaker economic outlooks, there is a smaller percentage of CFOs whose companies have plans for new market entries or more spending on new machinery and equipment. The situation on the labour market is also conducive to such economic outlooks. CFOs expect an increase in the payroll costs, which puts profitability of their companies under pressure, both in terms of revenues and costs.

Despite such deteriorated sentiment among CFOs, there is still no reason to sound the alarm. Among CFOs, there are still more optimists than pessimists, which could simply mean that the respondents expect a slightly slower rate of economic growth in Poland. This is further corroborated by forecasts of such institutions as the National Bank of Poland and the International Monetary Fund.

Summary

ContactSurvey information

This report has been prepared on the basis of more than 160 surveys distributed and collected during four editions of the CFO of the Year congress, which were held in Poznan, Sopot, Katowice and Rzeszow in May 2016.

The congress series is a unique event of this type in Poland, integrating the environments of CFOs and board members responsible for financial matters in their organisations.

These meetings are always devoted to the most current issues faced by managers of Polish companies.

For more congress information go to:

http://dyrektorfinansowyroku.pl/

Jacek KowalczykMarketing and PR Director

Grant Thornton T +48 22 205 4841 M +48 505 024 168 E [email protected]

The nature of information contained in this document is only general and illustrative. It does not create any commercial or tax, legal, accounting or any other professional advisory relationship. Prior to any action, please contact your professional advisor for advice tailored to your individual needs.

Grant Thornton Frąckowiak Sp. z o.o. Sp. k. have made their best efforts in order to ensure that the information contained herein is complete, true and based on reliable sources. However, Grant Thornton Frąckowiak Sp. z o.o. Sp. k. shall not be liable for any errors or omissions in such information or any errors arising from its invalidity. Furthermore, Grant Thornton Frąckowiak Sp. z o.o. Sp. k. shall not be liable for consequences of any action resulting from the use of such information.

Grzegorz BłachnioResearch & Communication

Euler Hermes T +48 22 385 49 19 M +48 601 056 830 E [email protected]