Embed Size (px)

Citation preview

How To Get Deals Done

With Bad-Credit Clients

Copyright Sabre Credit Solutions. All Rights Reserved.

What We’ll Cover

•How Credit Laws Work

•How To Help Credit-Challenged Clients

•How To Integrate A High-Quality Credit Restoration Program Into Your Business

Reality•You’ll Get Credit-Challenged

Clients

•Many Times, These Folks Can Be Loan-Ready In Short Order (60-90 Days)

•Many Of Them Are Not Actual Credit Risks

According To A Recent FTC Study, 21% Of

Those Surveyed Had Significant Errors On Their Credit Reports

Reality

•1 Out Of 5 Of Your Clients Are Going To Have Errors On Their Reports

•Total Of 66.9 Million Americans With False Negatives On Their Reports

•Plus - Recovery From The “Great Recession” Has Put Many People Back In The Game Who Had Problems 5 Years Ago

Your Plan

•What Is Your Plan To Help These People?

•If You Turn Them Down, They Will Go Looking For Someone Else

•They’ll Keep Looking Until They Find Someone Who Can Help Them Resolve Their Issues And Get What They Want

Your Plan

•A Basic Understanding Of Credit Law Can Help YOU Be That Person

•It Turns Dead-Deals Into Closed-Deals, And Can Do So Quickly

•Gives You A Distinct Advantage Over Competition

How Credit Works

•FICO Is The Current “Gold Standard” In Lending Risk Assessment

•Point System That Runs From 350 - 850

•Represents A Likelihood On Being Repaid (i.e., 740 Points = 74% Chance Of Being Repaid)

Factors That Matter

•There Are Several Factors That Go Into Score Calculation

•Some Factors Carry More Weight, Some Less

FICO Ingredients•Payment History - Consistency

And Timeliness Of Payments Made

•Amounts Owed - “Utilization Rate” How Much Of A Trade Line Is Being Used?

•Length Of Credit History - Longer Timelines = Greater Statistical Significance = More Trust

FICO Ingredients

•New Credit - Requests For New Credit, Inquiries, Many Accounts In A Short Period Of Time = Greater Risk

•Types Of Credit - Ideal Is A Mix Of Revolving Credit (Credit Cards, Retail Accounts) And Installment Loans (Mortgage, Auto, etc)

What FICO Ignores

•Ethnicity, Religion, Location, Gender, Age

•Salary, Employment History, Occupation

•Self-Initiated Inquiries, Employment Inquiries, Insurance Inquiries

•Child/Family Support Obligations

Law That Matters•State And Federal Government Has

Protections Built Into The Credit System

•These Protections Were In Response To Abuses By The CRA’s (Credit Reporting Agencies)

•You And Your Clients Have Specific Rights As To What Can And Cannot Be Reported

Law That Matters:

1. Fair Credit Billing Act (FCBA) - Focuses On Lender Behavior

2. Fair Credit Reporting Act (FCRA) - Focuses On Credit Reporting Agencies, And The Specifics

Of What Can And Cannot Be Reported

3. Fair Debt Collection Practices Act (FDCPA) - Focuses On Collection Agencies, What Is Lawful

Law That Matters

•These Documents Are Comprised Of Thousands Of Pages Of Legal-Ese

•Case Law Has Tens Of Thousands

•Boil It All Down, And You Get A Simple, Bottom-Line View Of What Matters:

Law That Matters

•All Information Reported Must Be 100% Accurate & Free From Error

•All Information Must Be 100% Verifiable

•By Law, If Information Reported Is Not 100% Accurate And 100% Verifiable, It Must Come Off The Credit Reports

• It Is ILLEGAL To Report Information That Does Not Meet This Criteria

CRA’s•Why Are Such Strong Laws In Place?

•Information Reported Is Arguably The Most Important Variable In The Financial Success Of The Consumer Over The Course Of Their Life

•This Information Is Incredibly Important To Consumers, And The CRA’s Have No Financial Motivation To Get It Right

CRA’s•Storing, Organizing, And Selling Of

Financial Information Is Done By The Credit Reporting Agencies, Or Credit Bureaus

•These Are Not Government-Sponsored Organizations

•For-Profit, Billion-Dollar Companies That Make Money Selling Our Information

CRA’s

•Reporting Is Optional, Not Mandatory

•The Laws Are Written In Favor Of Consumers

•The Knowledge Of These Laws Make The Difference In What Your Client Can (Or Cannot) Qualify For

Small Boosts

•Some Clients Will Need A Small Boost (10-30 Points)

•These Types Of Deals Are Easy, And Can Be Accomplished Very Quickly

•Two “Tricks Of The Trade”:

Bump #1

•Utilization Rate Pay-Down

•Pay Down Existing Revolving Trade Lines To 5%-10% Utilization

•30% Of Your Score Is Utilization Rate (Amount Of The Trade Line Utilized)

•Keeping A Low Utilization Rate Creates A Better Risk Profile (Higher Score)

Bump #2•Authorized User

•Get Added To A Credit Card (With Great History) As An Authorized User

•You Don’t Need To Get A Card, Just Be Added On The Account As An Authorized User

Bump #2

•This Immediately Adds All The Positive History Of The Trade Line To The Client’s Reports

•Spouse, Parent, Friend, Etc

•Older And More Positive The Trade Line History, The Better

Challenging Scenarios

•Some Clients Have More Difficult Circumstances

•Foreclosures, Bankruptcies, Collection Accounts, Charge-Off’s, Judgements, Tax Liens, Etc

•These Take A More Focused Approach, And Require More Expertise To Resolve

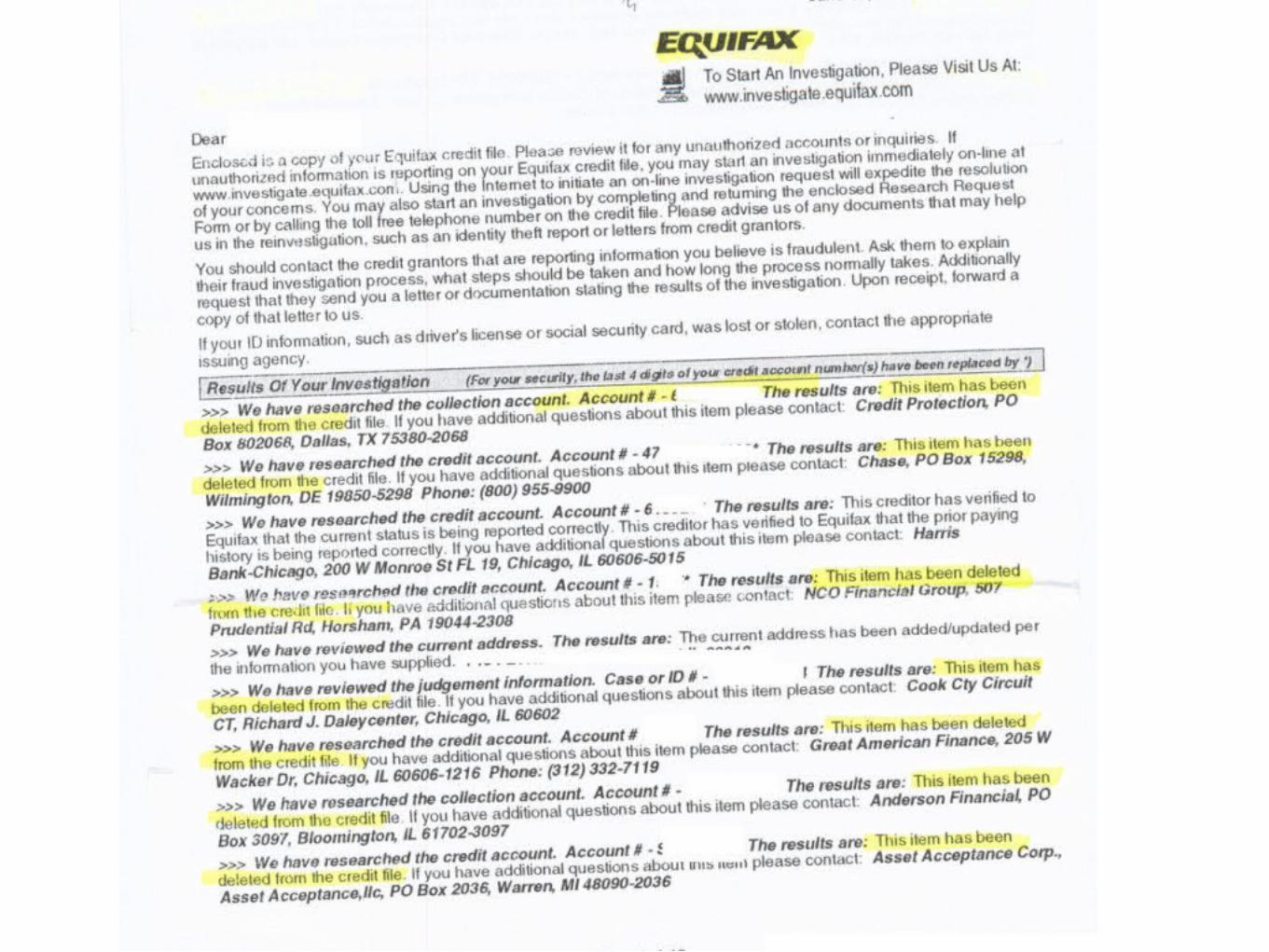

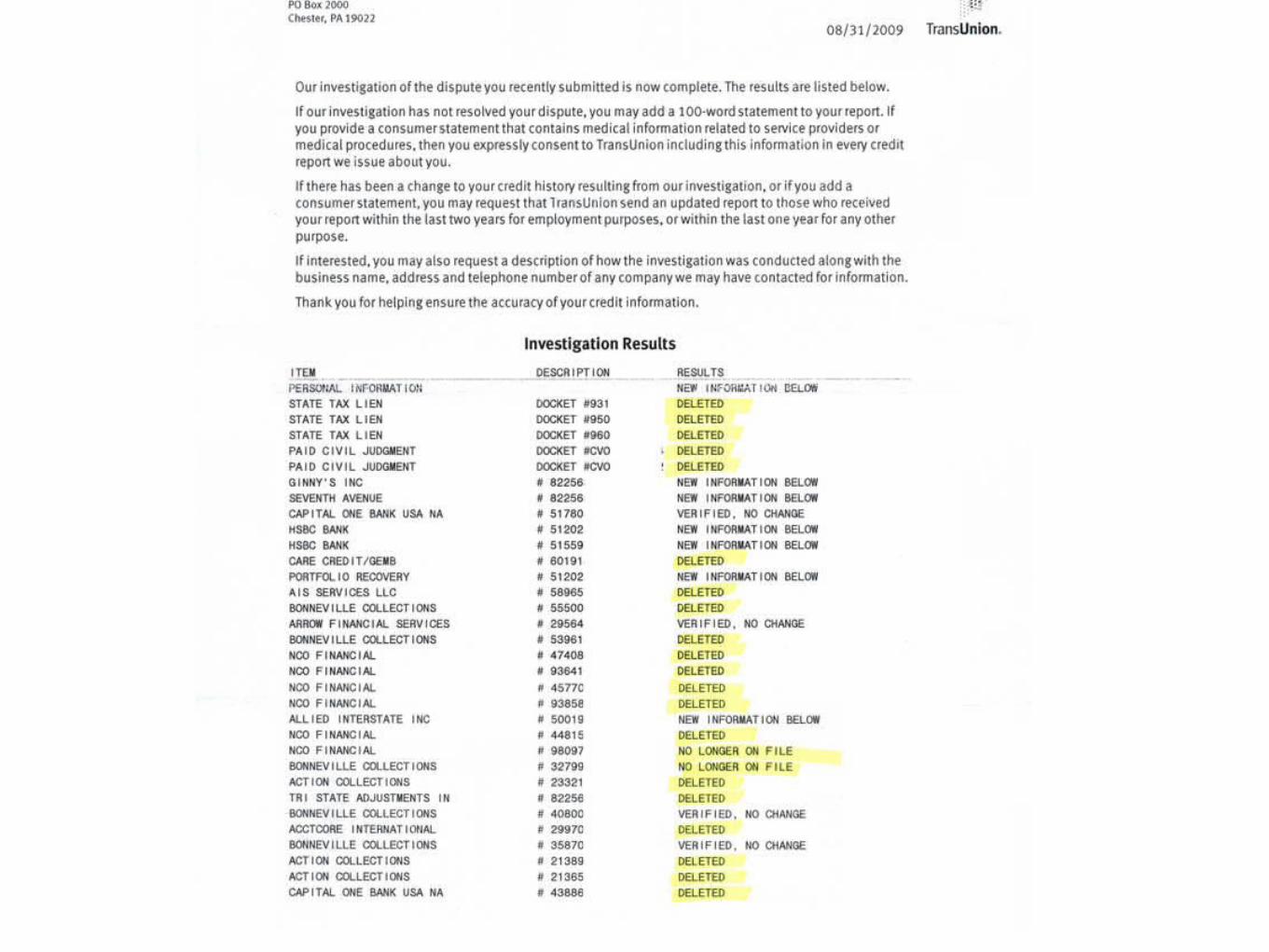

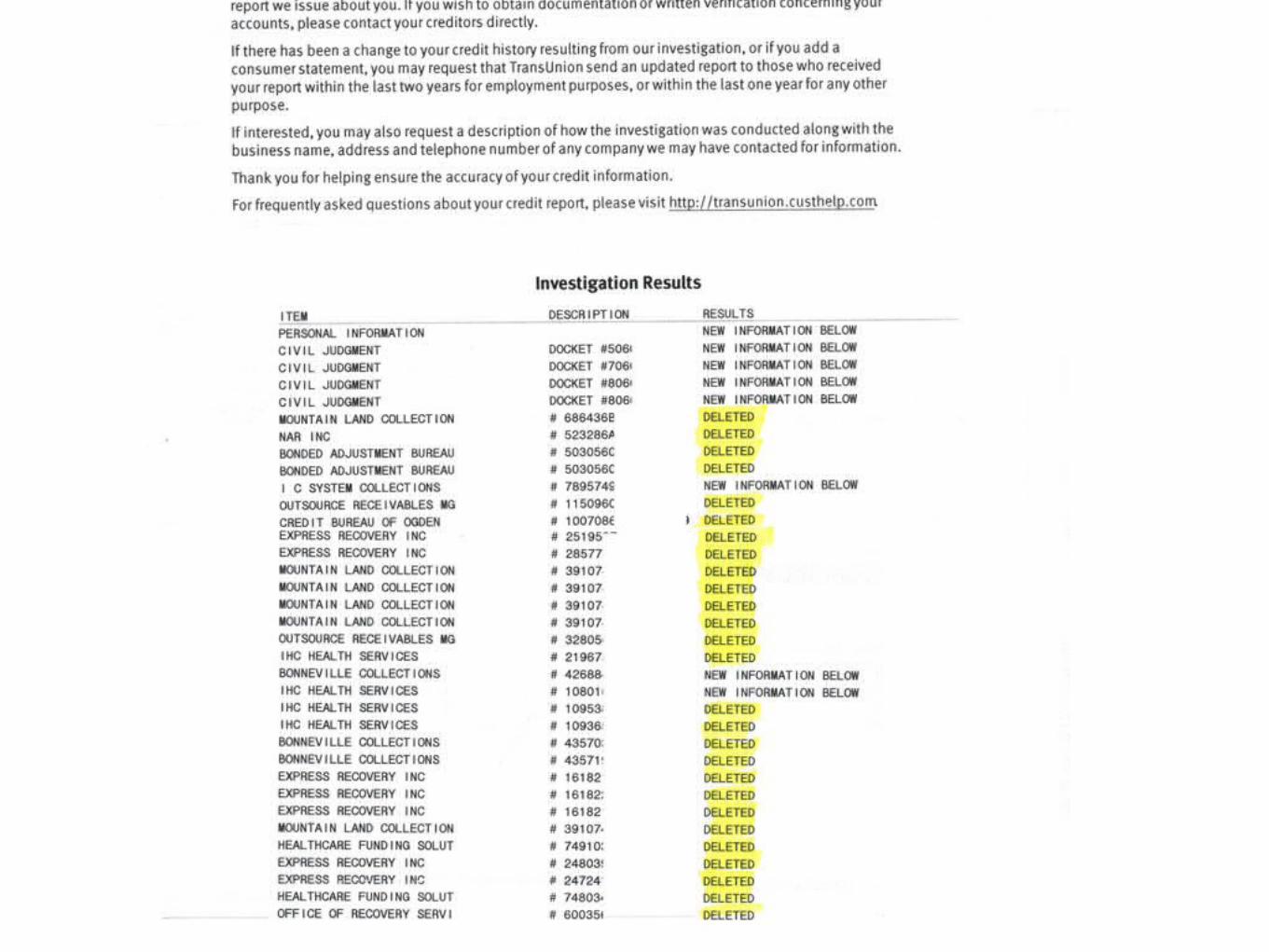

Why Credit Repair

•In These Cases, It’s Good To Have A Credit-Repair Firm As An Option For Your Clients

•It Helps You And Your Clients Multiple Ways:

Why Credit Repair

•Takes The Client Off The Market (If Turned Down By You, They Will Continue Shopping Until They Find Someone Who Can Help)

•Professionally Represents Your Clients In Resolving Credit-Bureau Issues

•Makes Your Marketing Dollars Go Further (More ROI)

Why Sabre•Our Firm Is A “Brand Partner” For

You

•Goal Is To Get A Client Qualified Quickly, And Turn Them Back To You

•Documented, Industry-Leading Results

Why Sabre•Generally, We Can Get 5 Out Of 10

Of Your Bad-Credit Clients Loan-Ready Within The First 60-90 Days Of Our Program

•Goal Is To Get A Client Qualified Quickly, And Turn Them Back Your Way To Complete Their Transaction

•Examples Of Client Results:

How Sabre Works

•As Your Credit Repair And Restoration Firm, We Work To Get Your Client Loan-Ready ASAP

•Co-Branded Back Office System Ensures You Stay “Top Of Mind”

•We Make You Money Three Ways

How Sabre Works

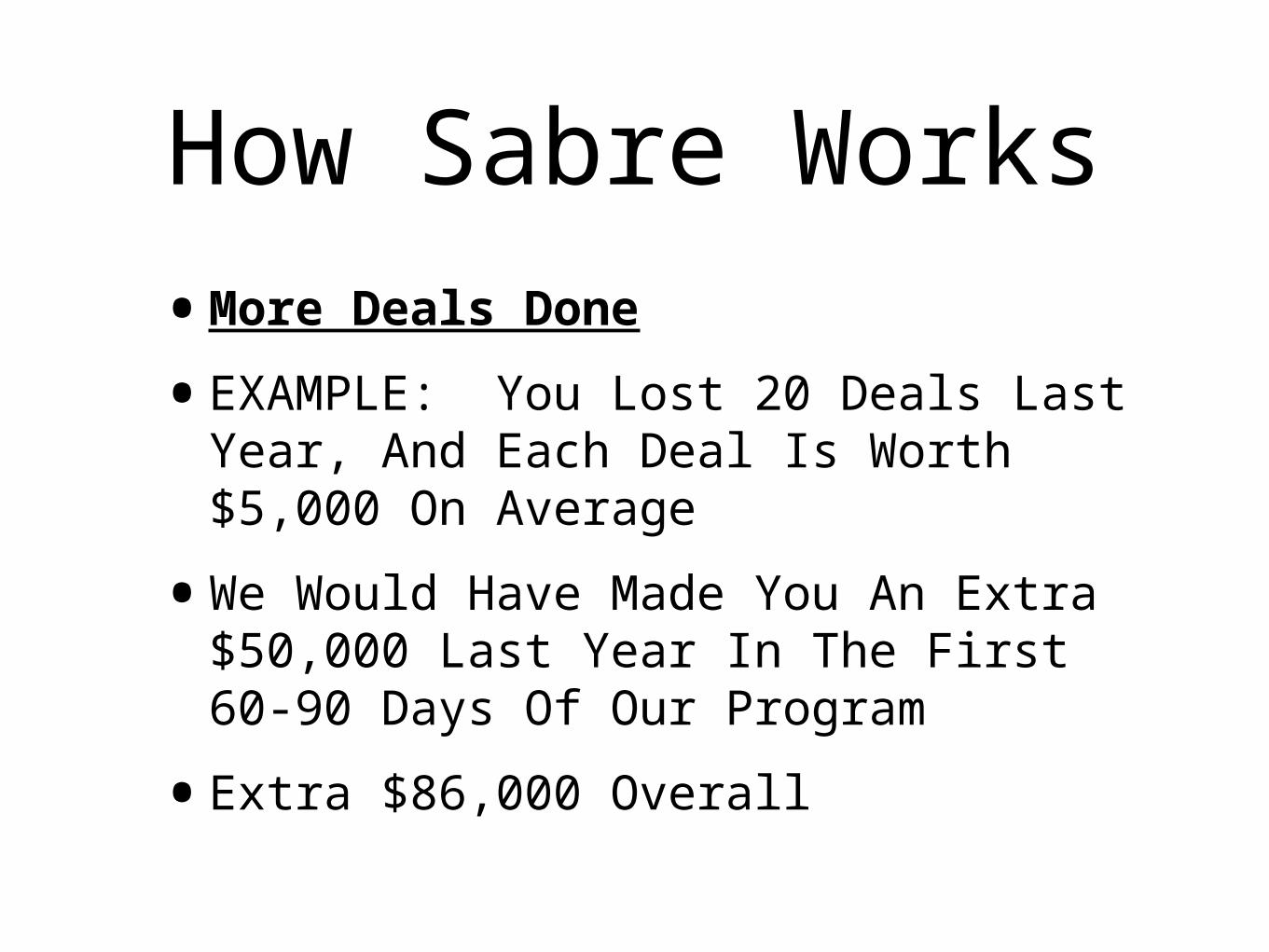

•More Deals Done

•Do The Math - How Many Deals Did You Turn Away Last Year Because Of Credit Issues?

•What’s An Average Deal Worth To You?

How Sabre Works•More Deals Done

•EXAMPLE: You Lost 20 Deals Last Year, And Each Deal Is Worth $5,000 On Average

•We Would Have Made You An Extra $50,000 Last Year In The First 60-90 Days Of Our Program

•Extra $86,000 Overall

How Sabre Works

•Direct Referral Fees

•We Pay You $50 For Every Client You Refer That Does Business With Us

•You’re Not Going To Get Rich Off Referral Fees

•An Extra $1,000 - $2,000 Does Make For A Nice Christmas Bonus :)

How Sabre Works

•Indirect Referral Fees

•We Pay You $25 For Every Client Your Referral Partners Send Us

•Colleagues, Competitors, etc

•Creates A Passive Stream Of Income For You

How Sabre Works•Indirect Referral Fees

•Say You Know 10 People In Your Industry That Needs A Credit Repair Firm As A Partner

•Same Math (20 Deals Lost Last Year)

•Makes You An Extra $5,000 In Hands-Off, Passive Income

How Sabre Works

•You Get A Branded Marketing System (Customizable & Optional)

•Back Office Tracking And Monitoring System (See Items Repaired In Real-Time)

•Check Stats, Review Client Progress

How Sabre Works

•Our Program Is Affordable To Your Clients, And Helps Them Get What They Want & Need

•No Long-Term Contracts, Cancel At Any Time

•Win/Win/Win Scenario (You, The Client, And Sabre)

How Sabre Works

•Questions? Drop Us A Line: [email protected]

•Speak With Your Representative About Further Details And Implementation