Embed Size (px)

Citation preview

CHAPTER 6

Subsequent-Year Consolidations: General Approach

This chapter presents the last of the material that is crucial to an understanding of intercorporate investments, business combinations, and consolidations. The material in the Appendices to Chapter 6 (parent company investment in non-voting shares and intercompany bond holdings involving premiums or discounts) are additional aspects that are interesting and that occasionally arise in Canadian practice, but are not central concepts of consolidations.

The previous two chapters illustrated intercompany sales of inventory and non-depreciable capital assets, but avoided the additional complexity of intercompany sales of depreciable capital assets. Therefore, this chapter begins with a discussion of such asset transfers.

The second major section presents the general approach to subsequent-year consolidations. The example is of consolidation of a non-wholly owned subsidiary that was acquired in a business combination—the most complex example. Consolidation of wholly owned subsidiaries is simpler, and consolidation of wholly owned subsidiaries that were founded by the parent are simpler still (and much more common). The direct approach to consolidation is used throughout, as in the preceding chapters. The worksheet approach is available on the companion website to this text. Equity basis reporting and consolidated reporting of discontinued operations is also discussed.

Appendix 6A addresses those circumstances where the investee company has outstanding restricted and/or preferred shares in addition to common shares. The treatment of these preferred shares, whether owned by the parent company or by outside interests, on consolidation is discussed. The impact of restricted shares on control and the allocation of earnings is also discussed.

Copyright © 2014 Pearson Canada Inc. 290

Chapter 6 – Subsequent-Year Consolidations: General Approach

Appendix B to Chapter 6, available only online, discusses consolidation of intercompany bond holdings. The Appendix illustrates both the par value and agency approaches to intercompany bond holdings, including the impact on non-controlling interest of each approach. Although the challenges presented by open-market purchases of a related company’s bonds at a premium or discount are intellectually interesting, such transactions are very seldom encountered in Canadian practice. This appendix may be omitted without seriously jeopardizing students’ understanding of consolidations.

Copyright © 2014 Pearson Canada Inc. 291

Chapter 6 – Subsequent-Year Consolidations: General Approach

SUMMARY OF ASSIGNMENT MATERIAL

Case 6-1: International Consolidators Inc.An analyst friend compares the return on equity calculated based on consolidated numbers two years after the acquisition of the subsidiary with the return on equity of the parent and the subsidiary at the time of the acquisition of the latter and concludes that there is no synergy between them. Students are required to adopt the role of the friend of the analyst and are required to first calculate the separate entity financial statements of the parent using the consolidated statements and the separate entity statements of the subsidiary, and second to explain to the friend why consolidation-related adjustments might be clouding the return on equity calculation based on the consolidated statements. Students are also required to explain whether and to what extent the various financial statements truly represent the operations and financial position of the two entities.

Case 6-2: Alright Beverages Ltd.Alright Beverages Ltd. is a multi-topic case that deals primarily with the reporting issues that arise from a series of transactions among related companies. It is a demanding case that requires students to look beyond the surface implications.

Case 6-3: Le GourmandHalf of the issued voting shares of a small company have been purchased by the company’s largest customer. Ownership of the other half of the voting shares is somewhat diffuse and the shareholders are disinterested in the affairs of the company. Has the new owner acquired control? The case requires a discussion of the alternative accounting options and a recommendation. A calculation of net income is also required.

Case 6-4: Constructive Inspirations Inc.This case is quite demanding, especially when assigned as an exam question. It tests students’ understanding of how consolidation-related adjustments relating to a non-wholly owned subsidiary purchased a few years ago impact current net income and ending owners’ equity.

A couple is divorcing amicably, and the divorce settlement requires the valuation of an architectural company run by one of them. Valuation is to be based on the greater of six times net income or ending owners’ equity, both calculated based on IFRS. The architectural company, along with the friends of the architect spouse, owns shares in a supplier of architectural products. The appropriate accounting option to account for this investment has to be recommended. A discussion of the impact of consolidation-related adjustments on net income and owners’ equity respectively is required. The case also requires a discussion of the “fairness” of using IFRS-based financial statements for determining the company’s value.

P6-1 (20 minutes, medium) This problem requires adjustments over a four-year period, ignoring taxes, for an intercompany depreciable capital asset sale. There is a non-controlling interest in the subsidiary, and the sale is upstream.

Copyright © 2014 Pearson Canada Inc. 292

Chapter 6 – Subsequent-Year Consolidations: General Approach

P6-2 (20 minutes, medium)Upstream sale of a 70% depreciated asset by an 80% owned subsidiary. The need to restore the original accumulated depreciation adds a slight twist to the exercise. Eliminations for two non-consecutive years are required.

P6-3 (30 minutes, medium) This problem examines the adjustments required for an unrealized profit in inventory and a gain on the sale of land, both upstream, where there is a 30% non-controlling interest over a two-year period.

P6-4 (30 minutes, medium) Intercompany sales of inventory, land and building between a parent and two subsidiaries (80% and 70% owned). Eliminating entries and NCI effects are required.

P6-5 (20 minutes, medium) Calculation of NCI and consolidated net income four years after acquisition. A good problem for practice at applying the techniques of consolidation without going through an entire set of consolidated statements.

P6-6 (40 minutes, medium) Computation of consolidated net income and retained earnings for a parent and two subsidiaries. The emphasis is on intercompany sales of inventory wherein one subsidiary sells to the parent, which in turn sells to the other subsidiary.

P6-7 (45 minutes, easy)This is a straight-forward exercise on preparing a consolidated statement of financial position five years after acquisition. It is a good practice exercise (or examination question) as it contains no unexpected twists.

P6-8 (20 minutes, medium)Cost versus equity reporting of the investment account five years after purchase. Includes amortization of a FVI on a building.

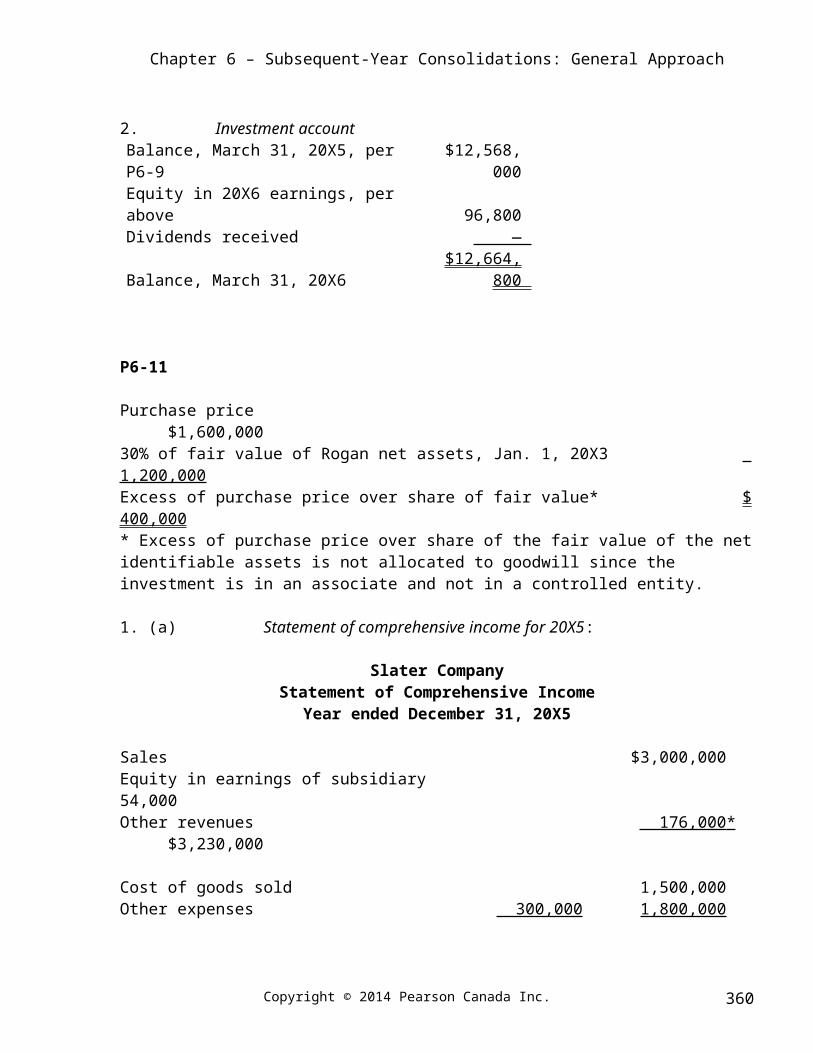

P6-9 (10 minutes, easy)Calculation of equity-basis earnings and investment account one year following acquisition. This problem illustrates equity-basis adjustments for FVI’s, but does not include any intercompany transactions. P6-10 extends this problem for one more year and does include intercompany sales of inventory and unrealized profits.

P6-10 (20 minutes, medium)This is an extension of P6-9 that adds intercompany transactions and unrealized profits. Equity-basis investment income and investment account balance are required, two years after the investment.

Copyright © 2014 Pearson Canada Inc. 293

Chapter 6 – Subsequent-Year Consolidations: General Approach

P6-11 (20 minutes, easy) Cost versus equity reporting of a 30% investment three years after purchase. An equity-basis investor statement of comprehensive income is required, plus determination of the investment account. There are no FVIs or intercompany transactions. P6-12 (60 minutes, medium) This problem involves investments in three other companies, with two reported on the equity basis and one on the cost basis. Discussion of the appropriateness of the cost and equity methods is required. The transactions and the entries required cover a one-year period.

P6-13 (75 minutes, medium)Consolidated SFP amounts (not a full SFP) and equity basis earnings in the subsidiary are required for an 80% subsidiary four years after acquisition. There are several unrealized profits (and one intercompany loss that may be assumed to reflect a decline in recoverable value).

P6-14 (25 minutes, easy) Preparation of a consolidated statement of financial position following upstream sales of inventory and a downstream sale of equipment.

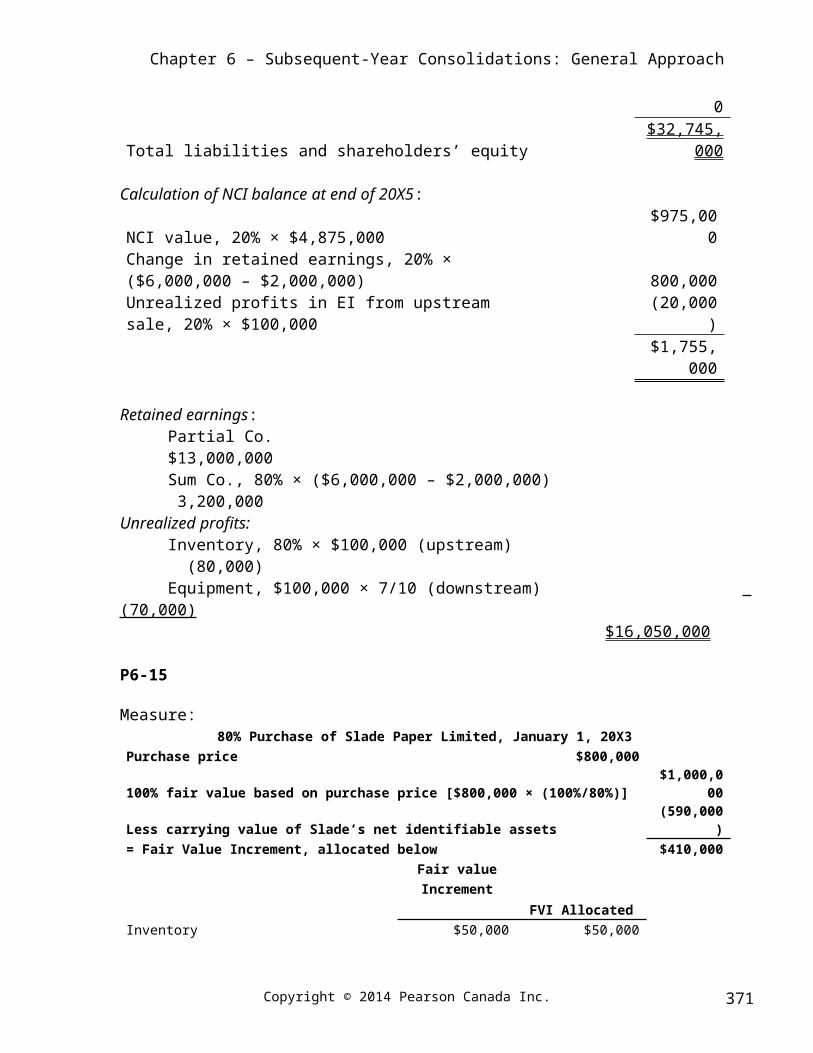

P6-15 (45 minutes, medium)Calculation of the carrying value of goodwill when 80% of the shares have been purchased, preparation of a consolidated statement of comprehensive income three years later, including upstream and downstream unrealized profits and calculation of inventory and non-controlling interest on the statement of financial position three years later.

P6-16 (50 minutes, medium)This problem requires the calculation of consolidated net income and selected SFP amounts two years after the purchase of a 70% interest in a subsidiary. In addition, the journal entry at the time of acquisition is required.

P6-17 (50 minutes, medium)This problem requires the preparation of a consolidated statement of comprehensive income and consolidated statement of retained earnings six years after a 70% purchase, the calculation of consolidated retained earnings at the beginning of the year and an explanation of the treatment of the unrealized profit on an equipment sale. A number of adjustments are required including fair value increments, unrealized profits on inventory (upstream) and a gain on sale of equipment (downstream). This problem also includes an impairment of goodwill.

P6-18 (40 minutes, medium)This problem requires the preparation of a consolidated statement of comprehensive income and the calculation of specific accounts on the consolidated statement of financial position six years after a 70% acquisition. In addition to unrealized upstream inventory profits, this problem incorporates the sale to external parties of a trademark with an unrealized gain.

P6-19 (40 minutes, medium)

Copyright © 2014 Pearson Canada Inc. 294

Chapter 6 – Subsequent-Year Consolidations: General Approach

This problem is similar to P6-16 as it requires the preparation of a consolidated statement of comprehensive income and the calculation of specific accounts on the consolidated statement of financial position four years after a 70% acquisition. There are a number of adjustments including an unrealized profit on an upstream land sale, downstream unrealized inventory profits and a goodwill impairment.

P6-20 (45 minutes, difficult) The challenge in this problem is in preparing the consolidated statement of comprehensive income given a variety of intercompany sales and other intercompany transactions. A challenging and worthwhile problem.

Case 6A-1This case is an adaptation of the comprehensive exam of the 1999 UFE. The students need to consider the impact of an acquisition on the EPS and accounting policies. There is a potential for loss of control depending on the method of financing that is selected for the acquisition. Audit issues also need to be considered.

Case 6A-2It is not always clear just when a joint venture qualifies for joint venture accounting. In this case, a joint venture is described in which one partner does have a majority of the board of directors but is restricted in its control by only 50% voting rights and by a joint venture agreement that requires consent of both co-ventures for substantive alteration of the terms. The case asks students to discuss the appropriateness of using four methods of accounting for the investment.

P6A-1 (40 minutes, easy)This is an exercise in separating the reporting effects of an investment in both common and preferred shares. Equity reporting is assumed rather than consolidation.

P6A-2 (45 minutes, medium)A consolidated statement of financial position is required where the parent owns a portion of the outstanding preferred shares. The purchase price of the subsidiary’s share differs from the redemption value.

P6A-3 (15 minutes, easy)Calculation of the non-controlling interest on the consolidated statement of financial position at the date of acquisition and one year later is required. The subsidiary has preferred and common shares outstanding and the parent owns 80% of the common shares.

P6B-1 (20 minutes, medium) Elimination entry for an intercompany bond investment in a subsidiary, assuming first that the subsidiary is wholly owned, and then that it is 75% owned. Both agency and par value approaches are required.

P6B-2 (30 minutes, medium)

Copyright © 2014 Pearson Canada Inc. 295

Chapter 6 – Subsequent-Year Consolidations: General Approach

Calculation of selected amounts one year after acquisition of an 80% interest, given downstream sales of inventory and land and a purchase of subsidiary bonds by the parent at a premium.

P6B-3 (40 minutes, medium)This problem has two distinct and separable parts: (1) an upstream sale of land and buildings by one subsidiary, and (2) a purchase of another subsidiary’s bonds by the parent. Statement amounts are required (including non-controlling interest in earnings) rather than eliminating entries. The bond aspect requires use of the par-value method.

P6B-4 (50 minutes, medium)A consolidated statement of comprehensive income is required, plus calculation of specified statement of financial position amounts. The bond transaction does not affect non-controlling interest. The fixed asset sale is upstream.

ANSWERS TO REVIEW QUESTIONS

Q6-1: Profits on intercompany sales are unrealized when the merchandise or other assets have not been resold to outside third parties or been consumed by amortization or depreciation.

Q6-2: The unrealized loss on sale of a capital asset at its fair market value may or may not be eliminated on consolidation. The key question is whether the reduced fair market value reflects an impairment in the value of the asset. Under IFRS, an impairment loss exists when the carrying value of the asset exceeds its recoverable value. The recoverable value of an asset represents the higher of its (1) fair value less costs to sell, and (2) value in use. If the original carrying value of the asset still does not exceed the asset’s recoverable value to the consolidated enterprise despite the low resale value, then the loss would be eliminated. If, on the other hand, the resale value is low because the recoverable value of the asset has been impaired, the intercompany loss would not be eliminated.

Q6-3: When assets are sold horizontally between non-wholly owned subsidiaries, the unrealized profit is in the accounts of the selling company. Further, such sales are treated as upstream sales. Therefore, 100% of the unrealized gains has to be eliminated in the consolidated financial statements, allocating 60% to the parent’s owners and the rest, 40%, to the non-controlling interest. Thus, while the consolidated net income should be adjusted to the full extent of the unrealized gain of $20,000, 60% or $12,000 should be allocated to the owners of P and 40%, $8,000 should be allocated to the non-controlling interest.

Q6-4: Equity-basis earnings should be adjusted for the investor company’s share of unrealized profits from sales between significantly influenced investee corporations. In this example, $20,000 of unrealized profit is in the reported net income of IE1, of which IR has a 30% share. Therefore, the adjustment to IR’s share of IE1’s earnings will be $6,000.

Q6-5: The profit on an intercompany sale of a depreciable asset is gradually realized over the productive life of the asset, as the asset is used in the revenue generating activities of the buying

Copyright © 2014 Pearson Canada Inc. 296

Chapter 6 – Subsequent-Year Consolidations: General Approach

company. In accounting terms, the using up of the asset is reflected by depreciation. Therefore, the unrealized profit is realized year-by-year as the asset is depreciated.

Q6-6: If a company sells a long-lived asset that is part of its inventory, either upstream or downstream, it is accounted for as sales revenue with offsetting cost of sales instead of as a gain on sale. The gross profit on the sale would still be considered unrealized.

Q6-7: IAS 38, Intangible Assets, requires disclosure of the gross carrying amount and any accumulated amortization at the beginning and end of each period for each class of intangible assets. Therefore, entities following IFRS will need to keep track of the gross and accumulated amortization amounts separately in different accounts for various classes of intangible assets. Such requirements apply to capital assets as well. Hence, under IFRS, adjustments required upon the sale of an intangible asset with a limited life such as a patent will be the same as the adjustments required on the sale of a capital asset. However, earlier standards did not impose the same disclosure requirements as required under IFRS for intangible assets. Therefore, a separate accumulated amortization amount may not have been maintained in relation to these intangible assets. In such an event, upon the sale of an intangible asset instead of a capital asset, the two amounts for the asset account and the accumulated amortization account would have been netted together.

Q6-8: Consolidated retained earnings is comprised of the parent’s retained earnings, plus the parent’s share of earnings retained by the subsidiary since the date of acquisition (less any unrealized profits of the parent, the parent’s share of any unrealized profits of the subsidiary, and amortization of any fair-value increments, decrements or goodwill).

Q6-9: Ordinarily, any unrealized profit on an upstream intercompany asset sale is deducted from the recorded carrying value of the asset on the parent’s books and from the consolidated retained earnings. However, a subsidiary might sell an asset on which an unamortized fair value increment from the time of the purchase of the subsidiary by the parent exists. In such a case, the unamortized fair value increment reduces the unrealized profit from the viewpoint of the consolidated entity. Therefore, the unrealized profit elimination is not for the amount of profit booked by the subsidiary but is for the difference between the intercompany sales price and the amortized fair value of the asset (i.e. carrying value of the asset from the consolidated perspective). The remaining gain will be offset by the unamortized fair value increment adjustment.

Q6-10: In the year of the sale, any unamortized fair value increment on the asset sold is charged to the gain or loss that has been recorded for the sale. In subsequent years, the charge will be to consolidated retained earnings.

Q6-11: When the equity method is used for recording, the parent’s share of the subsidiary’s earnings is included in the parent’s retained earnings. Since the same amounts also appear in the subsidiary’s retained earnings, the subsidiary’s earnings will be counted twice unless they are adjusted. Therefore, the process of consolidation under the equity method differs from the process under the cost method of recording only in that the equity pick-up of earnings made by the parent

Copyright © 2014 Pearson Canada Inc. 297

Chapter 6 – Subsequent-Year Consolidations: General Approach

must be reversed or eliminated in order to avoid double counting the earnings and the investment account must be eliminated.

Q6-12: The equity-basis balance represents the parent’s share of the amortized fair values of the subsidiary’s net assets as originally acquired, plus the parent’s share of the change in the subsidiary’s net assets since the date of acquisition less/plus any unrealized gains/losses relating to inter-company transactions at year-end.

Q6-13: Under equity basis reporting, the “equity in earnings” captures all of the effects of the relationship between the investor and the investee corporations, without disturbing the basic financial reporting of the activities of the parent or investor corporation. In addition, the “equity in earnings” reflects the change in the investor’s investment account and all changes in net asset values that relate to that account.

CASE NOTES

Case 6-1

Role:First, prepare the separate entity financial statements of ICI and the associated calculations. Second, compare the financial statements prepared by me with the consolidated statements of ICI and the separate entity statements of PTI and explain to my friend how the consolidation-related adjustments may potentially mask the presence of synergy between ICI and PTI. Third, explain to my friend to what extent the separate entity and consolidated financial statements of ICI appropriately reflect the true economic operations and situation of ICI.

Constraints:Since ICI has used IFRS to arrive at its financial statements, all consolidation-related adjustments required under IFRS need to be undone.

Critical Success Factors:Correctly prepare the separate entity FS of ICI and explain to my friend using non-technical language the impact of consolidation-related adjustments on the financial results reported by ICI in its consolidated financial statements. Further explain to my friend to what extent the separate entity and consolidated financial statements of ICI respectively reflect its true economic operations and position.

Users & Objectives:The financial statements and my report are being prepared for the sole use of my friend. My friend is trying to analyze the financial results of ICI from the point of view of an analyst; specifically he is looking to see whether the synergy between ICI and PTI touted by the management of ICI at the time of its acquisition of PTI is indeed present. There are no other users of the financial statements and report prepared by me. However, the financial statements provided to me, the consolidated financial statements of ICI and the separate entity financial statements of PTI were prepared and

Copyright © 2014 Pearson Canada Inc. 298

Chapter 6 – Subsequent-Year Consolidations: General Approach

reported by their respective management and thus may be biased to the extent the respective management teams have tried to meet their objectives keeping in mind the users of their respective financial statements and their objectives.

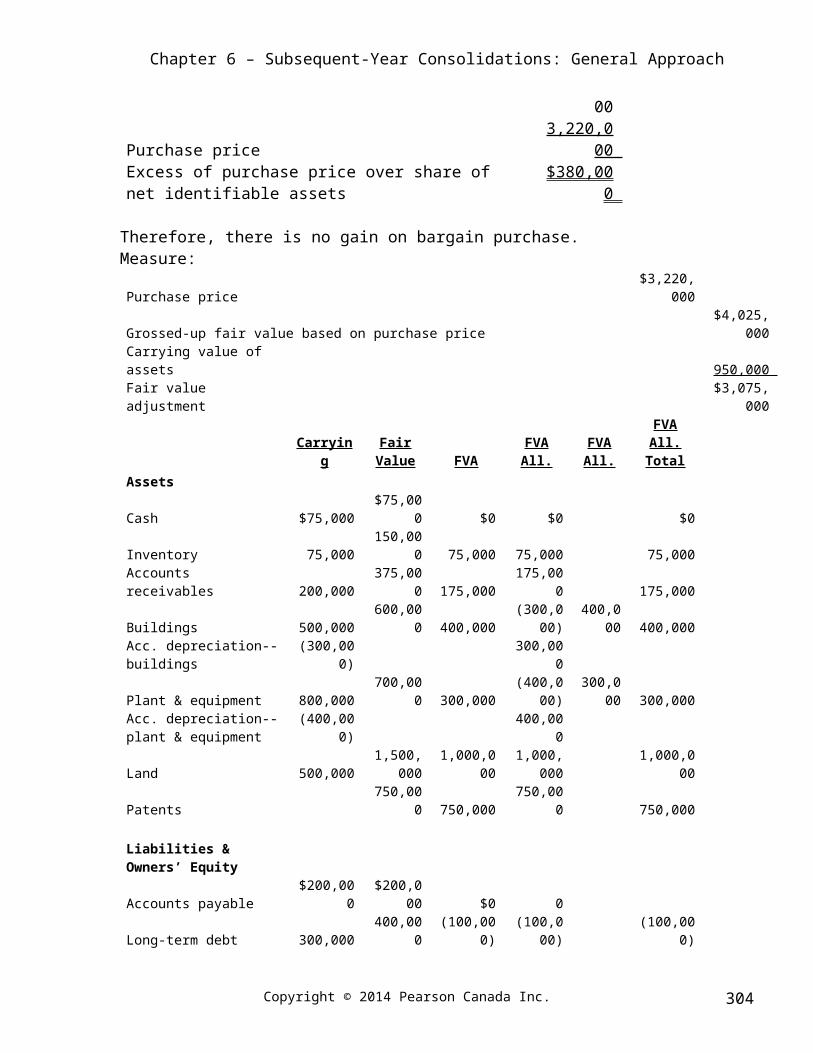

Separate Entity Financial Statements of ICI and Related Calculations:Check to ensure no gain on bargain purchase:Assets $4,150,000 Liabilities 600,000

$3,550,000 80% share 2,840,000 Purchase price 3,220,000 Excess of purchase price over share of net identifiable assets $380,000

Therefore, there is no gain on bargain purchase.Measure:

Purchase price$3,220,00

0

Grossed-up fair value based on purchase price$4,025,00

0

Carrying value of assets 950,000

Fair value adjustment$3,075,00

0

CarryingFair

Value FVA FVA All.FVA All.

FVA All. Total

Assets

Cash $75,000 $75,000 $0 $0 $0

Inventory 75,000 150,000 75,000 75,000 75,000

Accounts receivables 200,000 375,000 175,000 175,000 175,000

Buildings 500,000 600,000 400,000 (300,000)400,00

0 400,000 Acc. depreciation--buildings (300,000) 300,000

Plant & equipment 800,000 700,000 300,000 (400,000)300,00

0 300,000 Acc. depreciation--plant & equipment (400,000) 400,000

Land 500,000 1,500,00

0 1,000,000 1,000,00

0 1,000,000

Patents 750,000 750,000 750,000 750,000

Liabilities & Owners’ Equity

Accounts payable $200,000 $200,000 $0 0

Long-term debt 300,000 400,000 (100,000) (100,000) (100,000)

FVA allocated to net identifiable assets$2,600,00

0

Copyright © 2014 Pearson Canada Inc. 299

Chapter 6 – Subsequent-Year Consolidations: General Approach

Goodwill $475,000

FVA TotalUseful

lifeAmort./

year 20X6 20X7 BalanceInventory $75,000 $75,000 $0 AR 175,000 175,000 0 Buildings 400,000 10 40,000 40,000 40,000 320,000 Plant & Equipment 300,000 10 30,000 30,000 30,000 240,000 Land 1,000,000 1,000,000 Patents 750,000 10 75,000 75,000 75,000 600,000 Long-term Debt (100,000) 10 (10,000) (10,000) (10,000) (80,000)Goodwill 475,000 300,000 175,000

Total $3,075,000 $385,000 $435,000 $2,255,00

0

Eliminate:Eliminate Intercompany Transactions & BalancesDownstream Sales $1,472,900 Upstream Sales 1,499,680 Inter-company dividends 48,000

Eliminate Unrealized Gains:Gross profit percentage on upstream salesGross profit $1,387,204 Revenue 3,749,200

37%

Gross profit percentage on downstream sales (provided) 45%

UpstreamBeginning inventory $100,000 Realized gain 37,000

Ending inventory $150,000 Unrealized gain 55,500

DownstreamBeginning inventory $40,000

Copyright © 2014 Pearson Canada Inc. 300

Chapter 6 – Subsequent-Year Consolidations: General Approach

Realized 18,000

Ending inventory $50,000 Unrealized 22,500

Unrealized and Realized Gain on Upstream Sale of Depreciable Asset:Sale price $200,000 Original cost $200,000 Accumulated depreciation 100,000 Carrying value 100,000 Gain 100,000 Remaining useful live 10 Additional depreciation charged by ICI 10,000

Separate Entity Statements of ICI:

Consolidated SCI of ICI for the Year Ended December 31, 20X7

PTI SE SCI Subtracted Consolidated Adjustments Undone ICI SE SCI

Sales Revenue $6,668,220 $3,749,200 1,472,900 1,499,680 $5,891,600

COGS 2,652,796 2,361,996 1,472,900 1,499,680 37,000 18,000

(55,500) (22,500) 3,240,380

Gross profit $4,015,424 1,387,204 2,651,220

Dividend Income $0 48,000 48,000

Amortization expense 365,000 50,000 (40,000) (30,000) (75,000) 10,000 180,000

Administrative expenses 1,109,404 412,412 10,000 706,992 Selling & marketing expenses 1,643,530 612,500 1,031,030 Loss on impairment of goodwill 300,000 (300,000) 0

Income tax expense 209,098 62,458 146,640Net income and comprehensive income $388,392 249,834 634,558

Allocated to:

Shareholders of ICI $667,125

Non-controlling interest $21,267

Statement of Changes in Equity—Retained Earnings Section

Cons. ICI SE ICI

BRE parent $1,386,732 1,598,460 Net income attributable to shareholders of ICI 427,125 634,558

Dividends for the year (200,000) (200,000)

Copyright © 2014 Pearson Canada Inc. 301

Chapter 6 – Subsequent-Year Consolidations: General Approach

Ending RE $1,613,857 2,033,018

SFP as of December 31, 20X7

Cons. ICI PTI SE Consolidated Adjustments Undone ICI SE

Assets

Cash $515,202 $252,184 $263,018

Inventory 252,000 80,000 55,500 22,500 250,000

Accounts receivables 555,000 225,000 330,000

Buildings 2,100,000 500,000 300,000 (400,000) 1,500,000 Acc. depreciation—buildings (990,000) (340,000) (300,000) 80,000 (870,000)

Plant & equipment 2,700,000 600,000 400,000 (300,000) 2,200,000 Acc. depreciation--plant & equipment (1,540,000) (360,000) (400,000) 60,000 (20,000) 100,000 (1,440,000)

Land 3,250,000 800,000 (1,000,000) 1,450,000

Patents 600,000 (750,000) 150,000 0

Investment in PTI 0 3,220,000 3,220,000

Goodwill 175,000 (475,000) 300,000 0

TOTAL ASSETS $7,617,202 $1,757,184 $6,903,018 Liabilities & Owners’ Equity

Accounts payable $422,510 $172,510 $250,000

Long-term debt 655,000 175,000 (100,000) 20,000 400,000

Contributed capital 4,220,000 500,000 4,220,000

Retained earnings 1,613,857 909,674 2,033,018

NCI 705,835 0 TOTAL LIABILITIES & OWNERS' EQUITY $7,617,202 $1,757,184 $6,903,018

Copyright © 2014 Pearson Canada Inc. 302

Chapter 6 – Subsequent-Year Consolidations: General Approach

Independent Calculation of SE Beginning RE of ICI (not required):Beg. SE RE ICI $1,598,460

Beg. RE PTIEnding RE $909,674 Less income for the year (249,834)Add dividends declared for the year 60,000 Beg. RE 719,840 RE at acquisition 450,000 Change in RE 269,840 Less FVA amortization 20X6 (385,000)Less gain on sale of P&E (100,000)Add realization of gain 10,000 Unrealized gain beginning upstream (37,000)Adj. change RE of PTI (242,160)ICI's share (193,728)Unrealized gain beginning downstream (18,000)Consolidated Beg. RE ICI $1,386,732

Independent Calculation of SE Ending RE of ICI:RE Ending $2,033,018 Less Unrealized gain ending (22,500)

RE Ending 909,674 RE acquisition (450,000)Change in RE 459,674 Less FVA amortization 20X6 (385,000)Less FVA amortization 20X7 (435,000)Less Unrealized gain ending (55,500)Less unrealized gain P&E (80,000)Adj. change in RE (495,826)Parent's share (396,661)Consolidated End RE ICI $1,613,857

Analysis of Financial Statements & Report to Friend:I have calculated different returns on equity measures based on the separate entity financial statements of ICI and PTI respectively, and alternate returns on equity measures based on the consolidated financial statements of ICI. While these different measures can be used to compare the performance of ICI and PTI in 20X7 with their performance at the time of the acquisition of

Copyright © 2014 Pearson Canada Inc. 303

Chapter 6 – Subsequent-Year Consolidations: General Approach

PTI, it is important to understand that such comparison may not necessarily shed light on the presence or absence of synergy between ICI and PTI.

Return of Equity of PTI in 20X7Owners' equity $1,409,674 Net income 249,834Return on equity 17.72%

Consolidated Return on Equity of ICI in 20X7 (provided):Total owners' equity including NCI equity $6,539,692Consolidated net income and comprehensive income 388,392Return on equity 5.94%

Alternate Consolidated Return on Equity of ICI in 20X7 Excluding NCI:Owners' equity excluding NCI equity $5,833,857 Net income attributable to shareholders of ICI 427,125

7.32%

Return of Equity of ICI in 20X7:Owners' equity $6,253,018 Net income 634,558Return on equity 10.15%

The provided returns on equity of PTI and ICI at the time of acquisition are 20.42% and 10.69% respectively. In comparison, the returns on equity of PTI and ICI for 20X7, as calculated above, are 17.72% and 10.15%. Thus, both returns on equity in 20X7 are lower than their comparatives at the time of acquisition. However, notice that both these returns of equity are far above the alternate returns on equity calculated based on the consolidated numbers, 5.94% and 7.32%. In short, the returns on equity based on the separate entity financial statements of PTI and ICI are not as bad as those based on the consolidated financial statements. The reasons for this disparity are: The loss of $300,000 recognized in the consolidated SCI relating to the impairment of the

goodwill arising from the acquisition of PTI, The fair value adjustment amortization of $135,000 relating to the identifiable net assets of

PTI on the consolidated SCI in 20X7, The unrealized gains present in the ending inventories of PTI and ICI relating to the inter-

company sales of inventory between them being higher by $23,000 compared to the unrealized gains in the beginning inventories of the two companies.

Note that these additional expenses/adjustments do not show up on the separate entity financial statements of PTI. Thus, comparing the consolidated results with the results of PTI at the time of its acquisition, based on its separate entity statements at that time, is incorrect. Nevertheless, note that the consolidated adjustments highlighted above are done for genuine reasons. When one company controls another, the consolidated statements should represent only the results of those transactions that exist between the consolidated entity and outside entities. Otherwise, a

Copyright © 2014 Pearson Canada Inc. 304

Chapter 6 – Subsequent-Year Consolidations: General Approach

consolidated entity can very easily inflate the results presented in the consolidated statements by suitably structuring inter-company transactions.Additional consolidation-related adjustments include the elimination of upstream as well as downstream sales between ICI and PTI. Such sales represent 28.53% of the total sales of ICI and PTI. Thus intercompany sales represent a significant proportion of the total sales of the two entities and indicate the presence of strong links and potential synergy between them. It is not clear whether such inter-company transactions existed prior to the acquisition of PTI and ICI. This opens up the question of why ICI acquired PTI in the first place. ICI may have acquired PTI to consolidate the market for the products of the two companies, or to fend off a competitor from acquiring PTI. ICI may have perceived that the market for its products is slowly drying up or the profit margins are being squeezed, and thus might have purchased PTI to prevent further erosion of its market share or profitability. If that was the aim of acquiring PTI, the acquisition may indeed have achieved its desired purpose despite the subsequent decrease in the return on equity.Therefore, it is not clear why the management of ICI decided to take an impairment loss of $300,000 in relation to the goodwill arising from the acquisition of PTI. While the separate entity returns on equity of PTI and ICI in 20X7 are no doubt lower than their counterparts at the time of the acquisition of PTI, the differences between them do not appear to be that large so as to warrant writing off the goodwill. There may be many different reasons for such a decrease, some of which were already pointed out earlier. Further, the recent downturn in the economy may be temporarily depressing the returns of the two companies. In such an event I think writing off the goodwill may not be warranted. On the other hand, and notwithstanding the previous reasons, the decrease in the returns on equity may indeed indicate a permanent decrease in the profitability of the two companies, meaning that the expected synergy has not occurred. Therefore, if the goodwill was paid in relation to the expected synergy it is appropriate to write-off the portion of the goodwill that has no future value. The performance of the combined entity with those of other companies in the same industry may provide some clues on this issue. However, such comparison has to be done with caution, since, as we have already seen, the method and type of accounting adopted by individual companies can have a significant impact on their returns, thereby making an one-on-one comparison of their results with those of other companies difficult if not impossible.Another reason for exercising caution while using consolidated SFP numbers is the fact that the consolidated SFP includes the net assets of ICI at their carrying values, while including the net assets of PTI at their fair values at the time of PTI’s acquisition less related amortization. This is like trying to add apples to oranges. Thus, it is really difficult to make sense of any ratios that you might obtain based on the consolidated numbers. Consequently, it is incorrect to compare the return on equity calculated based on the consolidated statements of ICI at the end of 20X7 to the returns on equity at the time of acquisition and conclude that there is no synergy between ICI and PTI.In summary, it is premature to conclude based on the decrease in the return on equity of the two companies subsequent to the acquisition of PTI that synergy between them is absent.

True Picture of the Operations and Financial Position of ICI and PTI:None of the financial statements provide a true picture of the operations and economic situation of ICI and PTI at the end of 20X7. Accounting based SFPs report the carrying values of a significant portion of the net assets of entities most often than not at their historical values, not at their fair values. For example, it looks as if the fair values of the net assets of ICI including its land holdings at the end of 20X7 are significantly higher than their carrying values on its separate entity SFP.

Copyright © 2014 Pearson Canada Inc. 305

Chapter 6 – Subsequent-Year Consolidations: General Approach

PTI’s assets including its significant land holding may also have similarly increased in value since the time of its acquisition in 20X5. However, such increases are not reported on the any of the financial statements, separate entity or consolidated. Since land appears to represent a significant portion of the net assets of PTI and ICI, the consolidated and separate entity SFPs may be significantly misreporting the true values of the net assets of both companies at the end of 20X7. Consequently, if returns from holding land represent a significant source of returns for both companies, such returns will not be shown on the separate entity or consolidated SCIs of the two companies. In summary, both the returns and the financial positions of ICI and PTI may not be correctly reflected in their respective separate entity and consolidated financial statements. This misrepresentation can be alleviated partially if both companies use the revaluation method of accounting for reporting their assets on their financial statements.

Case 6-2: Alright Beverages Ltd.

Objectives of the Case

This case deals with a number of issues, but the basic focus is on the reporting implications of transactions among a family of related companies, including revenue recognition, adjustments for unrealized profits, and reporting long-term installment purchase contracts. The required for the case can be expanded to include income tax issues.

Objectives of Financial Reporting

The company is publicly held, and thus is IFRS-constrained. It also has debt financing (bank loans). There is a bonus scheme for at least some of management, including the management of Concentrated Vending Ltd. (CVL). There is explicit mention of tax deferral as an objective. Therefore, the reporting objectives would include the following: 1. Performance evaluation 2. Tax deferral3. Cash flow prediction 4. Profit maximization

Note that there may be different priorities for these objectives in the different reporting units. The relative ranking of objectives shown above is essentially for the consolidated enterprise. For CVL as a separate entity, however, profit maximization may move into first or second place due to the bonus arrangement with the managers of CVL. If the other 30% of CVL is not publicly held, then performance evaluation may not be an important objective for CVL.

Accounting and Reporting Issues

Copyright © 2014 Pearson Canada Inc. 306

Chapter 6 – Subsequent-Year Consolidations: General Approach

Sales by VSL to Local Operators

VSL is selling the machines on an easy-payment plan to local operators. The sales contract includes implicit interest. The alternatives for recognizing revenue include the following:

1. Recognize the present value of the payments, discounted at a market rate of interest for conditional sales contracts. The interest would be recognized over the life of the sales contracts on an effective yield basis. This alternative would cause recognition of at least some profit above the $5,000 cost of the machines to VSL at the time the contract starts. This alternative permits the earliest recognition of revenue. An allowance for doubtful contracts would have to be set up. Given the lack of any track record for these contracts, there may be considerable uncertainty associated with this alternative. If an allowance cannot be estimated, this method would not be appropriate.

2. Discount the payments to the cost of the machines to VSL of $5,000 each. Revenue would be recognized only in the form of interest as the contract matures. Revenue would be recognized later in this alternative than in the former alternative, but it would also tend to delay income taxes, as was considered desirable.

3. Discount the payments to the cost of the machines to CVL of $3,000 each. This alternative would work on a consolidated basis, but not very well on a separate-entity basis for VSL. On the other hand, there may be no need for separate-entity statements for VSL as it is a wholly-owned subsidiary of ABL. This alternative would also solve the unrealized-profit problem on consolidation, as will be discussed in the following section.

4. Recognize revenue on a cost-recovery basis. This is the most conservative approach and it would delay recognition (and taxes) the longest. It is not advantageous for fulfilling the other reporting objectives, however.

Sales by CVL to VSL

From the viewpoint of CVL as a separate entity, there is no problem with recording the sales when they occur. However, there is some question as to the permanence of those sales. If VSL cannot unload all of the machines that it takes, will CVL be required to accept them back? Are returns estimable? VSL is already expecting to hold 1,200 machines in inventory at the end of the year, almost 20% of the total purchases. There is a suggestion of profit manipulation for the benefit of CVL (or its managers). Of course, the intercompany profit will have to be eliminated upon consolidation.

A less obvious unrealized-profit issue arises from the sale of the machines by VSL to the local operators. To the extent that the revenue from the outside sales has not been recognized, then that portion of the intercompany profit per machine must also be eliminated. Therefore, there is a degree of interaction between the revenue recognition policy for sales by VSL and the realization of profit by CVL within the consolidated reports of ABL.

Sales by ABL to Bottlers

Copyright © 2014 Pearson Canada Inc. 307

Chapter 6 – Subsequent-Year Consolidations: General Approach

The bottlers in major cities are wholly owned subsidiaries of ABL. ABL sells the syrups to the bottlers, presumably at a profit. Revenue could be recognized by ABL (as a separate entity) when the syrup is sold, or only when the syrup has been used and the product sold by the bottler. As a separate entity, profit should probably be recognized when the syrup is sold by ABL. For consolidated reporting, however, unrealized profits on syrup held by the bottlers should be eliminated, if material in aggregate.

Business Combination

The acquisition of CVL by ABL should be reported by the acquisition method. If the fair values of the net assets acquired were greater than the purchase price paid by ABL, then the negative goodwill would have to be recognized as a gain from a bargain purchase. Although the price paid by ABL was well below the proportionate carrying value, it is possible that the fair value of the net assets was even lower, thereby resulting in goodwill. Although the presence of goodwill is unlikely given that CVL was in financial difficulty, a bargain purchase still could have occurred. If there is goodwill, it must be tested for impairment on an annual basis.

Inventory Valuation

The case mentions that CVL’s current cost to manufacture the machines is “significantly lower than in previous years.” This comment should trigger examination of CVL’s finished goods inventory to see if there are machines in stock that are being carried at higher than replacement cost. If so, a partial write-down may be appropriate if net realizable value has also declined.

Operating Segment Reporting

The additional sales by CVL to VSL will increase CVL’s revenues. Operating segments reporting may therefore be appropriate. Management may argue, however, that the machine sale is just a part of an integrated soft drink enterprise, and that the production and distribution of soft drinks (including the manufacture of the vending machines) is a dominant industry segment that comprises over 75% of the company’s revenue, profit, and assets.

Note: Segment reporting is discussed extensively in Chapter 7. However, most students will have been exposed to segment reporting in Intermediate Accounting and therefore should be familiar with the broad outlines of segment reporting requirements.

Case 6-3: Le Gourmand

Objectives of the Case

Copyright © 2014 Pearson Canada Inc. 308

Chapter 6 – Subsequent-Year Consolidations: General Approach

This case asks the student to examine the evidence in a business combination and determine what method of reporting is appropriate for the acquirer. It also requires the calculation of net income.

Objectives of Financial Reporting

Le Gourmand is an incorporated company, as indicated by the name (Le Gourmand Inc). It appears to be owned by one shareholder, Francois LeClerc, whose main concern regarding the combination with Ombre Wines is the cash flow from dividends. Le Gourmand has no long term debt outstanding; its only financing is from short term creditors. Accordingly, unless a bank or other user requires financial statements in accordance with IFRS, IFRS does not appear to be mandatory, and the choice of accounting policy should be based on LeClerc’s needs, not on what is required under IFRS. Accounting Standards for Private Enterprises (ASPE) are an option for Le Gourmand.

Alternative Accounting Policy Choices

Le Gourmand Inc. has purchased 50% of the outstanding voting shares (3,000 of 6,000 issued common shares) of Ombre Wines Ltd. This is not a majority of the outstanding voting shares, but may be sufficient to elect a majority of the Board of Directors and to control the operations of Ombre Wines. The evidence must be examined. Under IAS 27, Consolidated and Separate Financial Statements, control exists when one entity has the power to direct the financing and operating activities of another entity to derive benefits from that entity.

While the ownership of a majority of voting shares is usually evidence of control, control can exist when there is ownership of 50% or less of the voting shares, combined with: (1) an irrevocable agreement with other shareholders conferring their voting rights to the enterprise, or (2) ownership of rights, options, warrants, convertible debt, convertible non-voting equity or other instruments, which, if converted, would result in the enterprise owning a majority voting interest. Further, the existence of de facto control by a minority shareholder should also be considered in the absence of formal arrangements which would give it majority of the voting rights. For example, control is possible when the ownership of the balance of shares is dispersed and such owners have not organized themselves in such a manner as to exercise more voting shares than the minority shareholder.

Francois LeClerc’s expectation of future dividends implies that LeClerc intends to hold the shares for a long time. It also indicates that he expects to be able to control or at least influence the declaration of dividends, thus control or influence the company. LeClerc purchased most of the Ombre Wines trading shares, further indicating his desire for control. The fact that he only purchased 50%, when there were more than 50% trading (since some shares were still available to the public) indicates that LeClerc felt that 50% was enough to obtain control. He may have based this on the following: (1) Le Gourmand was Ombre Wines’ largest customer, and (2) although the founders of the company are still active, their children are selling their interests and do not plan to take over the business. Thus, there is evidence that Le Gourmand has acquired control of Ombre Wines.

Copyright © 2014 Pearson Canada Inc. 309

Chapter 6 – Subsequent-Year Consolidations: General Approach

The common shares held by the original founders and their families must be less than 50%. However, the original founders own the preferred shares of the company and could potentially acquire the 1,000 common shares that have not been issued, unless LeClerc is in a position to block the issue of such shares. This would effectively block Le Gourmand’s control of the company. Further evidence of control by Le Gourmand, or lack of control on the part of the original owners, needs to be gathered before it can be concluded that Le Gourmand has control.

If Le Gourmand could show control, consolidation would be the appropriate accounting policy for reporting its investment in Ombre Wines under IFRS. However, under ASPE, LeClerc can also elect to account for an investment subject to control using either the cost or equity methods. If control cannot be exercised, the equity method would be appropriate. Here, LeClerc could elect to use the cost method if ASPE are adopted. Le Gourmand’s 20X5 net income would be identical under the consolidation and equity methods. The cost method would not be appropriate under IFRS since Le Gourmand has more than a passive interest. As mentioned above, however, the owner, Francois LeClerc, could elect the cost method under ASPE, or accept a qualified or adverse report. It is possible that Francois may want to minimize his bookkeeping costs and therefore choose the method that is the least costly.

Measure Step:

Purchase price of 50% of the shares of Ombre$207,00

0Imputed value of 100% of Ombre based on purchase price $414,000Carrying value of net identifiable assets:Preferred shares $20,000Common shares 137,000Retained earnings 170,000Net assets 327,000Less: Preferred shares (20,000)

Dividends in arrears (2004 - $20,000 × 0.06) (1,200)(305,800

)

Fair Market Value IncrementsInvestment land 20,000Factory land 15,000Grape press 4,000 (39,000)Goodwill @ 100% $69,200

Copyright © 2014 Pearson Canada Inc. 310

Chapter 6 – Subsequent-Year Consolidations: General Approach

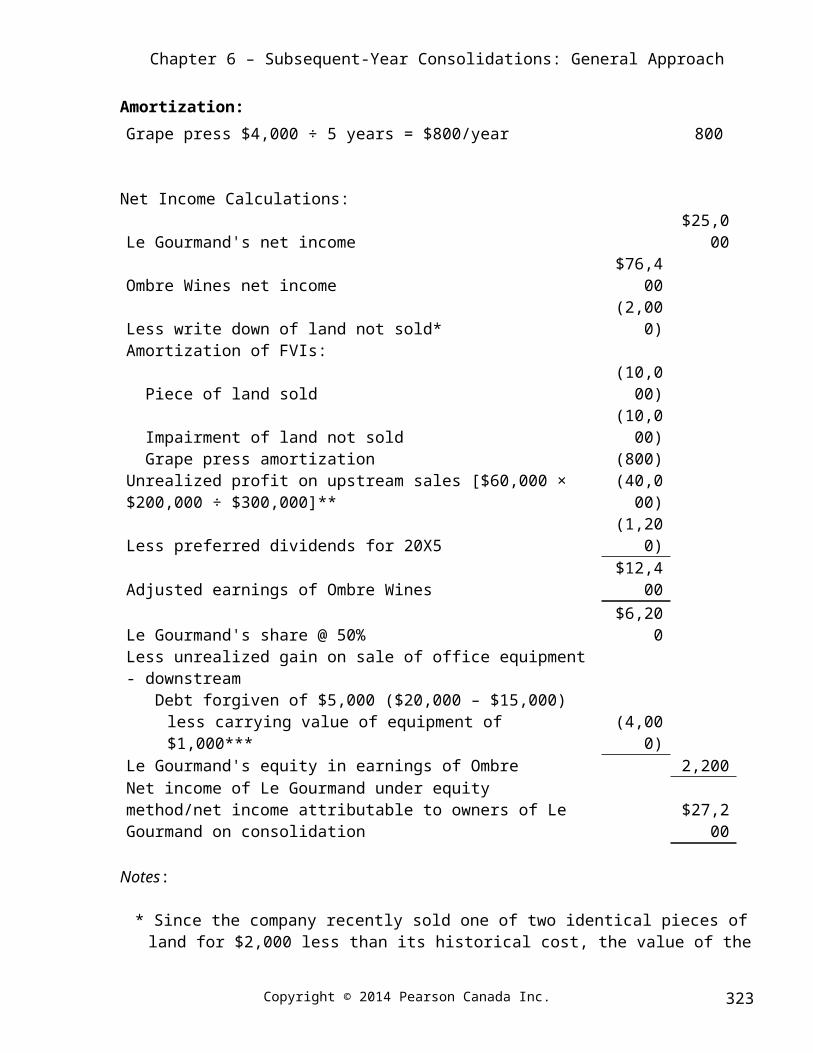

Amortization:

Grape press $4,000 ÷ 5 years = $800/year 800

Net Income Calculations:

Le Gourmand's net income$25,00

0Ombre Wines net income $76,400Less write down of land not sold* (2,000)Amortization of FVIs:

Piece of land sold(10,000

)

Impairment of land not sold(10,000

) Grape press amortization (800)

Unrealized profit on upstream sales [$60,000 × $200,000 ÷ $300,000]**(40,000

)Less preferred dividends for 20X5 (1,200)Adjusted earnings of Ombre Wines $12,400Le Gourmand's share @ 50% $6,200Less unrealized gain on sale of office equipment - downstream Debt forgiven of $5,000 ($20,000 – $15,000) less carrying value of

equipment of $1,000*** (4,000)Le Gourmand's equity in earnings of Ombre 2,200Net income of Le Gourmand under equity method/net income attributable to owners of Le Gourmand on consolidation

$27,200

Notes:

* Since the company recently sold one of two identical pieces of land for $2,000 less than its historical cost, the value of the land still held is questionable and should be written down. However, there is a fair value increment of $20,000 on the land. Since one piece of land has been sold, $10,000 should be included in the loss on sale and the other $10,000 should be written down as it is impaired.

** There is no adjustment for the unrealized profit at the beginning of the year as the parties were at arm's length at that time.

*** As the office equipment was transferred at year-end, amortization for 20X5 would have been charged.

Copyright © 2014 Pearson Canada Inc. 311

Chapter 6 – Subsequent-Year Consolidations: General Approach

Case 6-4: Constructive Inspirations Inc.

Overview

Accounting Experts LLP (AE) has been engaged by Jennifer and Johnnie to provide advice on the accounting alternatives available under IFRS for valuing CI. Specifically, such choices will be used to prepare CI’s financial statements, which will be used to value CI in relation to Jennifer's and Johnnie's divorce settlement. While Jennifer will continue to own CI, assets equal to the value of CI will be transferred to Johnnie as part of the divorce settlement. The value of CI will be equal to six times the net income of CI in 20X9 or equal to the ending owners’ equity of CI in 20X9, whichever amount is higher.

CI appears to have been in existence for quite some time. Forty percent of the shares of CEDS were also purchased by CI three years ago on Jan. 1 20X7. Therefore, general purpose financial statements must have been generated in the past aimed at providing financial information about CI and its investments to various users, including employees and the bank. The bank in any case will want to look at the separate entity financial statements of CI. The investors in CEDS will mainly focus on the FS of CEDS, not those of CI. Accounting Experts has not been engaged to provide advice relating to these general purpose statements. Rather, the advice is specific to the calculation of net income and owners’ equity to be used to value CI for the purpose of the divorce settlement between Jennifer and Johnnie.

Therefore, the present report will focus only on the accounting alternatives to be used for preparing the special purpose financial statements needed for valuing CI. These financial statements will not be available to other users of CI’s general purpose financial statements. Such users and their objectives are irrelevant for the purpose of this report and thus will not be considered here.

Constraints

Jennifer and Johnnie have agreed that IFRS for public entities have to be used as long as the end results are logical. Thus, for the purpose of this report IFRS is a constraint unless the results therefrom are not logical.

Critical Success Factor

Critical success factors that affect the long-run success of CI are irrelevant here since this report is not being provided for preparing the general purpose financial statements of CI.However, it is critical to us that our advice is found acceptable by both Jennifer and Johnnie. Both of them are long-term clients of AE, and we would like to keep both as our clients in the future as well. However, this factor is not a CSF that applies to CI, rather it is critical to AE in maintaining its long-term relationship between it and Jennifer and Johnnie respectively.

Copyright © 2014 Pearson Canada Inc. 312

Chapter 6 – Subsequent-Year Consolidations: General Approach

Users’ Objectives

Jennifer:Everything else being equal, Jennifer would like those accounting choices that will reduce both the net income of CI in 20X9 and the owners’ equity of CI at the end of 20X9. This will reduce the value of CI and therefore the value of the assets that will be transferred to Johnnie.

Johnnie:Everything else being equal, Johnnie will have objectives that are exactly the opposite of Jennifer's. He would prefer those accounting alternatives and choices that will increase both the net income of CI in 20X9 and the owners’ equity of CI at the end of 20X9. At worst, he would like a fair evaluation of NI of 20X9 and OE at end of 20X9, such that he obtains a fair value of CI.

Ranking of Users and Objectives

The divorce settlement has been amicable so far. Therefore, it is reasonable to assume that both Jennifer and Johnnie would like to continue to keep it that way. Thus, neither party would want to be unfair or appear unfair to the other party. However, as pointed out above, everything else being equal, each would like those accounting alternatives that cater to their objectives.

Both Jennifer and Johnnie are important and long-term clients of AE. Therefore, it appears prudent for AE not to be seen to be biased towards one over the other while providing their advice. Further, AE has a fiduciary duty to both of them. Given the above, it appears reasonable to provide advice that fairly reflects the economic situation of CI. Towards this end, the most appropriate alternative under IFRS for public entities will be provided for each relevant accounting issue. Non-IFRS alternatives will be considered only when all IFRS alternatives are found to be unsuitable.

Accounting Issues and Alternatives

Net Income versus Owners’ Equity

A fair value for CI can be based on either an income or cash-flow approach, wherein, the future income or cash-flow is discounted to present value terms, or based on the fair value of the existing assets and liabilities of CI as at the end of 20X9. Jennifer and Johnnie have agreed to value CI based on six times the NI of 20X9 or the ending owners’ equity of CI. Thus, while the former measure appears to be roughly approximating the income approach of valuation, the latter, based on owners’ equity, appears to be approximating the financial position basis of valuation. However, both figures are historical cost based and do not necessarily reflect the impact of present values or of future operations. For example, on the SCI, amortization and depreciation values are historical cost based. Similarly, on the SFP, the assets and liabilities are valued at their historical cost. Further, the assets and liabilities on the SFP of CI at the end of 20X9 may not accurately represent the income generating potential of CI in the future. One glaring example is the value of Jennifer to CI. Some of these problems can be mitigated by using the replacement model for measuring the assets and liabilities of CI. This is discussed in further detail in the next section.

Copyright © 2014 Pearson Canada Inc. 313

Chapter 6 – Subsequent-Year Consolidations: General Approach

Cost versus Revaluation Model of Valuing Assets of CI and CEDS

IFRS allows the use of either the cost or the revaluation model to value the assets of an entity. Potentially a more accurate value of CI can be obtained by using the revaluation model to measure assets such as property, plant and equipment and intangible assets. While such revaluation can increase owners’ equity (assuming asset values are increasing), thereby increasing the value of CI, it will also lead to higher amortization expenses on the SCI. Revaluation gains are not taken to net income except to the extent of revaluation losses taken to net income in prior periods. On the whole, however, following the revaluation model will lead to a higher valuation of CI, since such value is based on the higher of six times NI or owners’ equity.

Since revaluation amounts are not available at this time, the discussion in the latter sections assumes the use of the cost model.

CEDSCI owns 40% of the shares of CEDS and one of its employees is on the BOD of CEDS. However, the other 15 owners of CEDS, who are friends of Jennifer, have, via a written agreement, given CI the authority to make operating and investing decisions in relation to CEDS. Further, CEDS also appears to be a supplier of supplies to CI. CI’s employees are also working for CEDS. Finally, CI did not charge a management fee to CEDS.

All of the above indicate that under IFRS, CI has control over the operating and investment decisions of CEDS. Therefore, the investment is CEDS has to be accounted for as a business combination. Consequently, the financial statements of CEDS have to be consolidated with those of CI using the acquisition method. Under the acquisition method, both CI’s share as well as the share of the other 15 owners (NCI) has to be accounted at their fair value at the time of acquisition.

However, we do not presently have sufficient information to carry out a full consolidation of CEDS’ FS with those of CI. In fact, such consolidation may not be required for the purpose of this report since the issue of importance is the impact of the accounting alternatives on the net income of CI in 20X9 and the owners’ equity of CI in 20X9. Therefore, the following discussion will restrict itself to the consolidation-related accounting adjustments required under IFRS for the various issues relating to CEDS.

Fair Value of CEDS and Fair Value Increments at the Time of Acquisition

The balance of the FVI of $100,000 has been allocated to goodwill. This indicates that there is no gain on bargain purchase. Consequently, the initial accounting for CEDS will not impact the net income of CI nor its owners’ equity. The acquisition method allows for the use of either the entity method or the parent-company extension method. The difference between the two methods affects valuation of goodwill and valuation of NCI. Neither will affect the NI for 20X9 or owners’ equity at the end of that year.

Copyright © 2014 Pearson Canada Inc. 314

Chapter 6 – Subsequent-Year Consolidations: General Approach

Furthermore, the FVI allocated to inventory and patent will also not affect either net income or owners’ equity at the time of acquisition. However, post-acquisition, both amounts will have the following impact on net income of 20X9 and owners’ equity:

FVI allocated to inventoryThere is a fair value decrement of $50,000 in relation to inventory. Inventories are assumed to be sold in the very next year after acquisition. From the consolidated perspective the true cost of the inventory is less by the FVD of $50,000, compared to the cost shown on the separate entity FS of CEDS.

Therefore, the consolidated COGS would have been reduced by the $50,000 FVD in 20X7. This would have increased the net income of that year by $50,000. 40% of the $50,000 increase, i.e., $20,000 is attributable to CI, while the remaining 60% or $30,000 is attributable to the NCI. Since consolidation related adjustments do no carryover to later periods, suitable consolidation related adjustments have to be made in later years to capture the cumulative impact of previous years’ consolidation adjustments. Therefore, in 20X9, focusing just on CI’s portion, an adjustment to increase beginning owners’ equity of CI by $20,000 will have to be made. This adjustment will carry over to ending owners’ equity, increasing it by $20,000. Thus, the value of CI for the purpose of the divorce settlement will go up by $20,000 consequent to this adjustment.

FVI allocated to patentThe FVI allocated to patent is equal to $100,000. The patent had a further useful life of 10 years at the time of the acquisition of CEDS by CI. Therefore, in its consolidated statements CI will make consolidation adjustments to amortize the FVI of $100,000 over this 10-year period. Therefore, the FVI amortization in 20X7 and 20X8 would have been $10,000 per year. A further $10,000 amortization of this FVI will be made in 20X9 as well.

While the $10,000 amortization of FVI in 20X9 will decrease the CI’s consolidated net income by $10,000, CI’s share is only $4,000. Therefore, this will decrease the ending owners’ equity of CI in 20X9 by that amount. In addition, the cumulative impact of the adjustments relating to the amortization of the FVI in previous years on CI’s ending retained earnings in 20X9 will be a negative $8,000. Therefore, in total, the amortization of the FVI relating to the patent over the three-year 20X7-20X9 period will have a negative impact of $12,000 on ending owners’ equity in 20X9. Therefore, for the purpose of the divorce settlement the cumulative impact of the FVI amortization over the three-year period will be to decrease the value of CI by $12,000. In contrast, the impact of the FVI amortization in 20X9 on the value of CI (using net income) for the purpose of the divorce settlement will be greater, decreasing it by 6 × $4,000 or $24,000.

Impairment of GoodwillIt is assumed that the $100,000 FVI allocated to goodwill represents 100% of the value of goodwill. Therefore, of the impairment loss of $20,000 relating to goodwill in 20X8, only $8,000 is attributable to CI. Therefore, the related cumulative adjustment in 20X9 will reduce the beginning and thus the ending retained earnings of 20X9 by $8,000 and as a consequence the value of CI for the purpose of the divorce settlement by $8,000.

Management Fees

Copyright © 2014 Pearson Canada Inc. 315

Chapter 6 – Subsequent-Year Consolidations: General Approach

CI did not charge management fees to CEDS since 20X7. IFRS require all intercompany transactions be eliminated while preparing consolidated statements, since these statements represent the financial status of all the entities forming part of the consolidated group as one single economic entity. Therefore, even if CI had originally charged management fees to CEDS, such management fees would have been eliminated at the consolidated level for 20X9. No elimination is required for the management fees in earlier years. Therefore, failure of CI to charge management fees to CEDS does not have any impact on either the 20X9 net income attributable to CI or to the owners’ equity of CI.

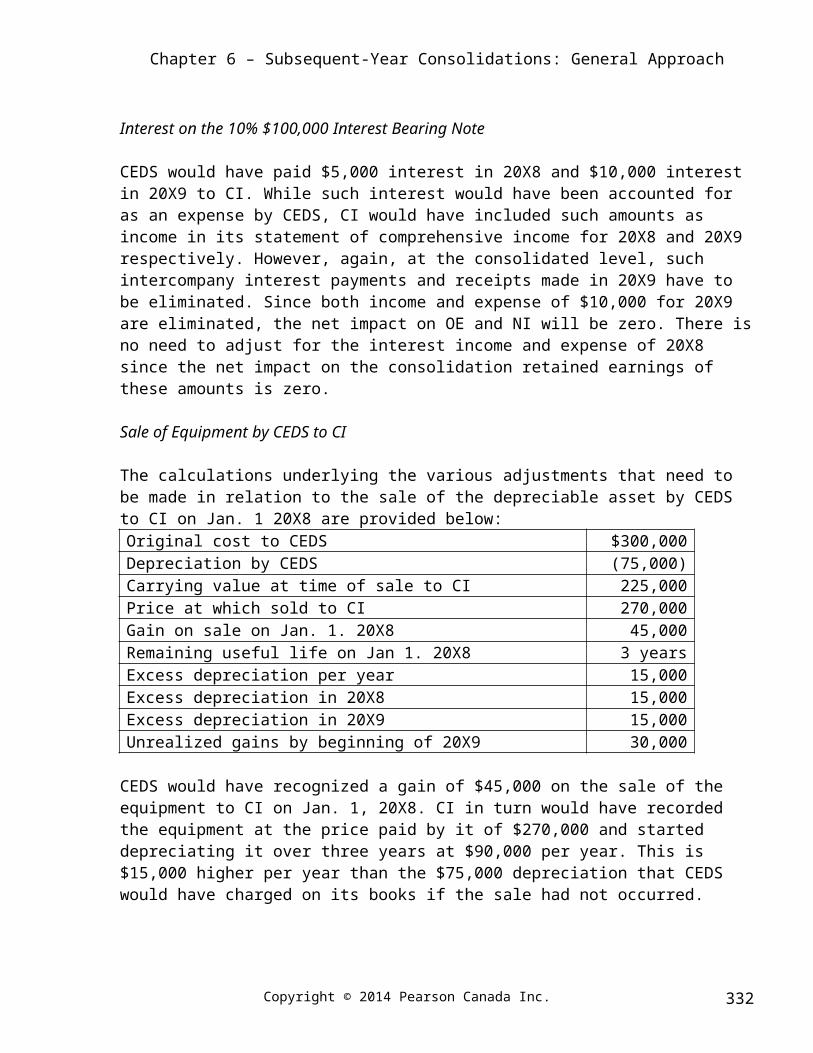

Interest on the 10% $100,000 Interest Bearing Note

CEDS would have paid $5,000 interest in 20X8 and $10,000 interest in 20X9 to CI. While such interest would have been accounted for as an expense by CEDS, CI would have included such amounts as income in its statement of comprehensive income for 20X8 and 20X9 respectively. However, again, at the consolidated level, such intercompany interest payments and receipts made in 20X9 have to be eliminated. Since both income and expense of $10,000 for 20X9 are eliminated, the net impact on OE and NI will be zero. There is no need to adjust for the interest income and expense of 20X8 since the net impact on the consolidation retained earnings of these amounts is zero.

Sale of Equipment by CEDS to CI

The calculations underlying the various adjustments that need to be made in relation to the sale of the depreciable asset by CEDS to CI on Jan. 1 20X8 are provided below:Original cost to CEDS $300,000Depreciation by CEDS (75,000)Carrying value at time of sale to CI 225,000Price at which sold to CI 270,000Gain on sale on Jan. 1. 20X8 45,000Remaining useful life on Jan 1. 20X8 3 yearsExcess depreciation per year 15,000Excess depreciation in 20X8 15,000Excess depreciation in 20X9 15,000Unrealized gains by beginning of 20X9 30,000

CEDS would have recognized a gain of $45,000 on the sale of the equipment to CI on Jan. 1, 20X8. CI in turn would have recorded the equipment at the price paid by it of $270,000 and started depreciating it over three years at $90,000 per year. This is $15,000 higher per year than the $75,000 depreciation that CEDS would have charged on its books if the sale had not occurred.

From a consolidated perspective no sale has actually occurred. Therefore, the adjustment in 20X9 to capture the cumulative impact of the consolidation-related adjustments made in 20X8 would be to eliminate the remaining unrealized gain of $30,000 ($45,000 – $15,000) at the beginning of 20X9. Specifically, the equipment account would be decreased by $30,000 while reducing

Copyright © 2014 Pearson Canada Inc. 316

Chapter 6 – Subsequent-Year Consolidations: General Approach

beginning retained earnings by 40% of that amount, i.e. $12,000 and reducing NCI by the remaining 60% or $18,000. Another adjustment is also required to eliminate the excess depreciation of $15,000 in 20X9. This adjustment will increase the net income attributable to CI by $15,000 × 40% or $6,000, while increasing the net income attributable to NCI by the remaining amount of $9,000.

Thus, the cumulative impact on the ending retained earnings of CI would be to decrease it by $12,000 – $6,000 or $6,000. Consequently, for the purpose of the divorce settlement the value of CI will be reduced by $6,000. In contrast, if the net income of 20X9 is used to value CI, the value of CI will in fact increase by $6,000 × 6 or $36,000. Clearly, in this case, diametrically different results will ensue depending on which amount is used to value CI, net income of CI in 20X9 or ending retained earnings of CI in 20X9.

Inter-company Sale of Inventory

Under IFRS, gains on inter-company sales of inventory are deemed to be unrealized as long as the inventory remains within the consolidated group. Therefore, such unrealized gains are required to be eliminated while preparing consolidated financial statements.

Unrealized gains exist in both the beginning as well as the ending inventory of CI in 20X9. Beginning inventories are assumed to have been sold during the year, and therefore are assumed to have been realized during the year. The following calculations provide the amount of unrealized gains present in the opening and closing inventories respectively, and CI’s share of such gains:

Beginning Inventory Ending Inventory Inter-company sale 80,000 90,000 Proportion remaining unsold 0.2 0.3 Inventory remaining unsold 16,000 27,000 Profit proportion 0.4 0.4 Unrealized profit 6,400 10,800 CI’s ownership proportion 0.4 0.4 CI’s share of unrealized profit 2,560 4,320 Impact on 20X9 Ending RE None (4,320)Impact on 20X9 CI NI share 2,560 (4,320)

Of the unrealized gains present in the opening inventory, $2,560 is attributable to CI. Since this unrealized gain would have been eliminated in 20X8, to capture the impact of that adjustment the corresponding cumulative adjustment in 20X9 will reduce opening retained earnings by that amount. However, to reflect the fact that the gain was realized in 20X9 the COGS of 20X9 will also be reduced by that amount. The overall impact on ending retained earnings will therefore be zero. Therefore, while ending owners’ equity remains unaffected by these changes and thus does not affect the value of CI, the increase in profit in 20X9 will mean that the value of CI based on the net income amount will increase by 6 × $2,560 or $15,360.

Copyright © 2014 Pearson Canada Inc. 317

Chapter 6 – Subsequent-Year Consolidations: General Approach

The consolidation-related adjustment relating to the unrealized gain in the ending inventory will decrease profit by $4,320 and therefore the ending retained earnings. The impact on the value of CI for the divorce settlement will therefore be (1) if based on net income, a decrease of 6 × $4,320 or $25,920, or (2) if based on ending owners’ equity, a decrease of $4,320.

No dividends have been declared by CEDS from the time of its acquisition by CI. That means that the separate entity FS of CI would not have included any portion of the operating results of CEDS in any of the three years 20X7-20X9. However, the consolidated FS of CI should not only include the results from the operations of CI but also the operating results of CEDS as well. This difference will affect both the ending owners’ equity as well as the net income of 20X9.

Since the impact of the other consolidation-related adjustments were discussed previously, we can now focus solely on the impact of the consolidation-related adjustment relating to CEDS’ operations, without any adjustments. CEDS’ change in retained earnings since its acquisition by CI until the beginning of 20X9 will be added to that of CI to the extent of CI’s ownership of CEDS. The remaining 60% will be adjusted against the NCI balance. The impact will either be negative or positive depending on the nature of the change in retained earnings of CEDS during the period.

The individual items of the statement of comprehensive income of CEDS are also included line-by-line in the consolidated statement of comprehensive income of CI. The result will be the same as adding the net income of CEDS to the net income of CI. Thus, the consolidated income will either increase or decrease depending on whether CEDS had a net loss or net income during 20X9. CI’s portion will be apportioned to CI, and will suitably increase or decrease ending retained earnings.

Thus, the operations of CEDS will influence the value of CI either through its influence on the net income of CI in 20X9 or through its impact on the ending retained earnings of CI. We will need to obtain these details from Jennifer to be able to quantify the impact.

The table below summarizes the impact of the various known adjustments relating to CEDS on the value of CI calculated based on (1) net income in 20X9 and (2) the ending owners’ equity at the end of 20X9:

Net IncomeOwners' Equity

FVI allocated to inventory 0 20,000FVI allocated to patent (24,000) (12,000)Impairment of goodwill 0 (8,000)Inter-company sale of equipment 36,000 (6,000)Unrealized gains in opening inventory 15,360 0Unrealized gains in ending inventory (25,920) (4,320)Net income of CEDS Unknown UnknownSum of known amounts 1,440 (10,320)

It is clear that the adjustments will have a negative impact on the value of CI if ending owners’ equity in 20X9 is used for such valuation. As opposed to this, the impact of using NI is marginally

Copyright © 2014 Pearson Canada Inc. 318

Chapter 6 – Subsequent-Year Consolidations: General Approach

positive. However, we do not have full details on the net income and owner's equity amounts related to CEDS. Therefore, we are unable at this time to conclude which of the two figures will lead to either a lower or higher value for CI.

Fairness of Using IFRS-based Financial Statements to Value CI

IFRS has, over the years, been moving more towards a fair-value basis of accounting and away from the historical basis of accounting. While monetary assets and liabilities are reported at their fair values on the SFP, many non-monetary assets like inventories are also reported at fair values. In addition, IFRS also allows the use of the revaluation model of valuating assets such as property, plant and equipment and intangible assets. Thus, the impact of the historical basis of accounting, which does not appropriately reflect fair values, is reduced. Nonetheless, accounting is backward looking and may not appropriately reflect the future operations of CI. It may be argued that CI should be valued based on its future potential and not on its past performance.

Further, under IFRS, the results of the operations of CEDS have to be included in the financial statements of CI either by including CI’s equity in the earnings of CEDS or by consolidation. It is not clear what Jennifer and Johnnie mean by the fair value of CI. Do they intend for CI’s value to include the value of CEDS as well? If not, CEDS will form part of the other assets which Johnnie will get. Excluding CEDS from the value of CI most probably will decrease the amount which Johnnie will get as part of the divorce settlement.

Finally, the criterion of fairness is a bit nebulous. Should the value of CI also include the value of Jennifer to it? Under IFRS, the value of Jennifer to CI cannot be recognized as an identifiable intangible asset. In any case, it is not clear that CI’s value should be based on its future operations. Maybe the value of CI should be based only on the fair values of the existing assets and liabilities of CI and that of CEDS attributable to CI.

SOLUTIONS TO PROBLEMS

P6-1

The various adjustments (rounded to the nearest dollar) are being provided in journal entry format below:

20X2:Gain on sale of fixtures $45,000

Fixtures $45,000

Accumulated depreciation 8,000Depreciation expense 8,000

Copyright © 2014 Pearson Canada Inc. 319

Chapter 6 – Subsequent-Year Consolidations: General Approach

The net impact of the above adjustments on net income will be to decrease it by $40,000. Of this amount, 30%, i.e. $12,000 is attributable to the NCI, while the rest belongs to the owners of the parent.

20X3:Retained earnings, opening 28,000 NCI 12,000Accumulated depreciation 8,000

Fixtures 48,000

Accumulated depreciation 8,000Depreciation expense 8,000

The decrease in the depreciation expense of $8,000 will increase net income by that amount. Of this amount, $2,400 is attributable to the NCI, while the rest is attributable to the owners of the parent.

20X4:Retained earnings, opening 22,400 NCI 9,600Accumulated depreciation 16,000

Fixtures 48,000

Accumulated depreciation 8,000Depreciation expense 8,000

Again, the decrease in depreciation expense of $8,000 will increase net income by that amount. Of this amount, $2,400 is attributable to the NCI, while the rest is attributable to the owners of the parent.

20X5:Retained earnings, opening 16,800NCI 7,200Accumulated depreciation 24,000

Fixtures 48,000

Accumulated depreciation 667Depreciation expense 667

(assuming 1 month’s depreciation is taken)

Fixtures 48,000Accumulated depreciation 24,667

Copyright © 2014 Pearson Canada Inc. 320

Chapter 6 – Subsequent-Year Consolidations: General Approach

Gain on sale of fixtures 23,333

The overall impact of the above entries on net income will be to increase it by $22,666. 30%, i.e. $6,800 is attributable to the NCI, while the rest is attributable to the owners of the parent.

P6-2

a. 20X3:Gain on sale of building $1,740,000

Accumulated depreciation $560,000

Buildings1,180,00

0

(Eliminates the gain, reduces the building to its cost to Sub, and restores the accumulated depreciation.)

The elimination of the gain on sale of building amount of $1,740,000 will decrease net income by that amount. Therefore, 20% of that amount, or $348,000, should be attributed to the NCI.

NCI (SFP) 348,000NCI in earnings of Sub (SCI) 348,000

(20% of the unrealized gain of $1,560,000.)

Accumulated depreciation 290,000Depreciation expense 290,000

[($1,980,000/6) – (800,000/20)]The decrease in depreciation expense of $290,000 will increase net income by that amount. Therefore, 20% or $58,000 should be attributed to the NCI:

NCI in earnings of Sub (SCI) 58,000NCI (SFP) 58,000

(20% of depreciation adjustment.)

b. 20X5:Accumulated depreciation (3 × 290,000) 870,000Retained earnings 0.80[1,740,000 – (2 × 290,000)] 928,000NCI (SFP) 0.20 × [1,740,000 – (2 × 290,000)] 232,000

Depreciation expense 290,000Accumulated depreciation 560,000Buildings 1,180,00

Copyright © 2014 Pearson Canada Inc. 321

Chapter 6 – Subsequent-Year Consolidations: General Approach

0

The decrease in depreciation expense of $290,000 will increase net income by that amount. Therefore, 20% or $58,000 should be attributed to the NCI.

NCI in earnings of Sub (SCI) 58,000NCI (SFP) 58,000

(20% of depreciation adjustment.)

P6-3

1. Eliminating entries, 20X4: Sales $800,000

Cost of goods sold $800,000

Cost of goods sold 80,000Inventory 80,000

Accounts payable 500,000Accounts receivable 500,000

Gain on sale of land 80,000Land 80,000

Interest revenue 13,000Interest expense 13,000

Note payable 273,000Note receivable 273,000

Eliminating entries 2005:

Retained earnings, opening 56,000 NCI 24,000

Cost of goods sold 80,000