Embed Size (px)

Citation preview

The Summer Budget

14 July 2015

A viscous and silly budget?

OR

A landmark budget that sought to grasp firmly a number of nettles in the tax and welfare world?

The Highlights (or lowlights)

• The attack on non-doms• The additional main residence nil rate band• Withdrawal of amortisation relief on goodwill• Taxing dividends• Pension changes• Buy to let landlords• The Annual investment Allowance

The attack on non-doms

Long-term non-doms (resident for over 15 of last 20 years) •Taxable on worldwide income and gains• And on benefits from excluded property settlements• Liable to IHT on worldwide assets• Does not affect domicile of children under 15• Applies from 2017/18• No grandfathering; no transitional rules• Consultation later in year• Make gifts now?• Create an excluded property settlement?• Gift to a charitable trust?

The attack on non-doms - 2

Non-doms with UK domicile of origin

• Taxable on worldwide income and gains for any year that they are UK resident • And liable to IHT on worldwide assets if they are resident here• Conservative party message for those who leave the UK to make their fortune abroad:

- Good riddance, we don’t want you back• Tory message to multinationals:

- don’t send back executives who were born here – We would like you to set up a business here but just don’t staff it with Englishmen

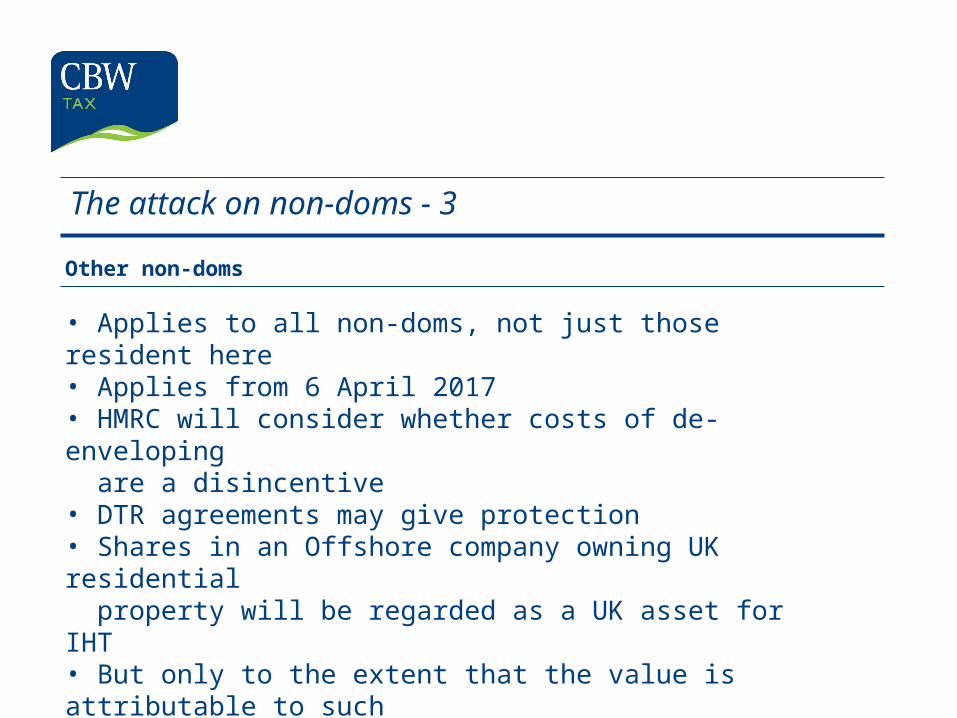

The attack on non-doms - 3

Other non-doms

• Applies to all non-doms, not just those resident here• Applies from 6 April 2017• HMRC will consider whether costs of de-enveloping are a disincentive• DTR agreements may give protection• Shares in an Offshore company owning UK residential property will be regarded as a UK asset for IHT • But only to the extent that the value is attributable to such property

The additional main residence nil rate bandAn extra £175,000 nil rate band so that a married couple can pass on £1 million to their children without IHT

Well, in 2021 that is! The extra amount is being phased in:

• 2017/18 £100,000• 2018/19 125,000• 2019/20 150,000• 2020/21 175,000• 2021/22 onward 175,000 indexed in line

with CPI

The additional main residence nil rate band – 2

The details - 1

• Only available to someone with children• Only available on a gift of the person’s main residence to descendants • Available from 8 July 2015• Can apply to only one house• If a deceased held more than one house the executors can decide which qualifies• It does not need to have been a residence at the date of death• But it must have been one at some time in the period of ownership

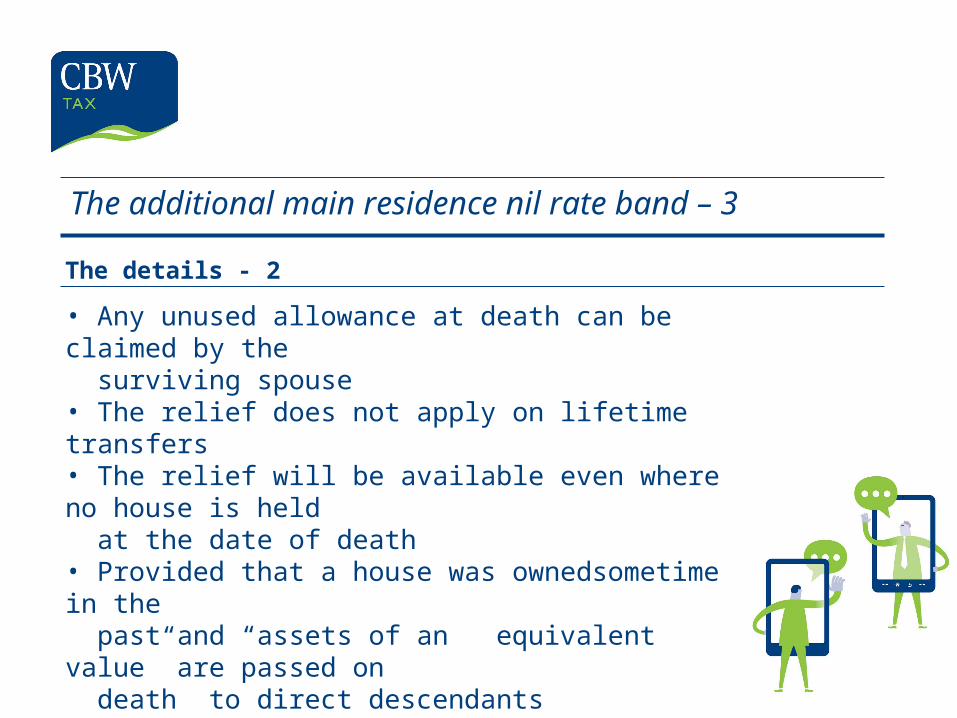

The additional main residence nil rate band – 3

The details - 2

• Any unused allowance at death can be claimed by the surviving spouse• The relief does not apply on lifetime transfers• The relief will be available even where no house is held at the date of death• Provided that a house was owned sometime in the past and “assets of an equivalent value” are passed on death to direct descendants• Descendants includes adopted children and step- children

The additional main residence nil rate band – 4

The details - 3

•The relief is limited to the net value of the property, ie after deducting any mortgage • But it appears that it is deducted before the main nil rate band• The relief is phased out where the net value of the estate (not that of the property) exceeds £2 million• The reduction is £1 for every £2 of the excess, so it does not apply at all to an estate of over £2.35 million

The additional main residence nil rate band – 5

Tough luck on those:

• Who don’t want to give the house to children in case they evict the spouse• Who have dependents other than children• Who leave their money via a will trust?• Who have a large mortgage• Who have not arranged their life assurance so that it bypasses the estate• Who don’t have children

• There will be a consultation paper in September

Withdrawal of corporate amortisation of goodwill

• Mr Osborne thinks that the purchase of a business rather than the company that owns it is done purely for tax avoidance to get relief for amortisation of goodwill• Accordingly companies will no longer be able to amortise purchased goodwill bought after 7 July 2015• Or other “customer-related” assets such as customer lists

Withdrawal of corporate amortisation of goodwill - 2

•The sale proceeds of goodwill will still be taxable as income• The cost can be deducted at the time of sale – but not so as to create a trading loss• Any loss will be treated as a non-trading debit

Withdrawal of corporate amortisation of goodwill - 3

It can still be sensible to buy the company because of:

• Uplift in value of other CGT assets• Capital allowances• Avoids risk of hidden liabilities

Taxing dividends

The new system from 6 April 2016

• Tax credit to be abolished• First £5,000 of dividend will be exempt• Any excess will be taxable at a special rate:

Basic rate taxpayer 7.5%Higher rate taxpayer 32.5%Additional rate taxpayer 38.1%

Taxing Dividends - 2

• Funds the 1% reduction in corporation tax• Big companies and economists will like it• Small companies who pay dividends in lieu of salaries may not• The break even point is around £22,000 of dividend income• Below that you will be better off; above it worse off

Taxing Dividends - 3

• The increase is an effective 7.5% on the excess over £5,000• Arithmetically it is still cheaper in tax terms to pay a dividend than remuneration

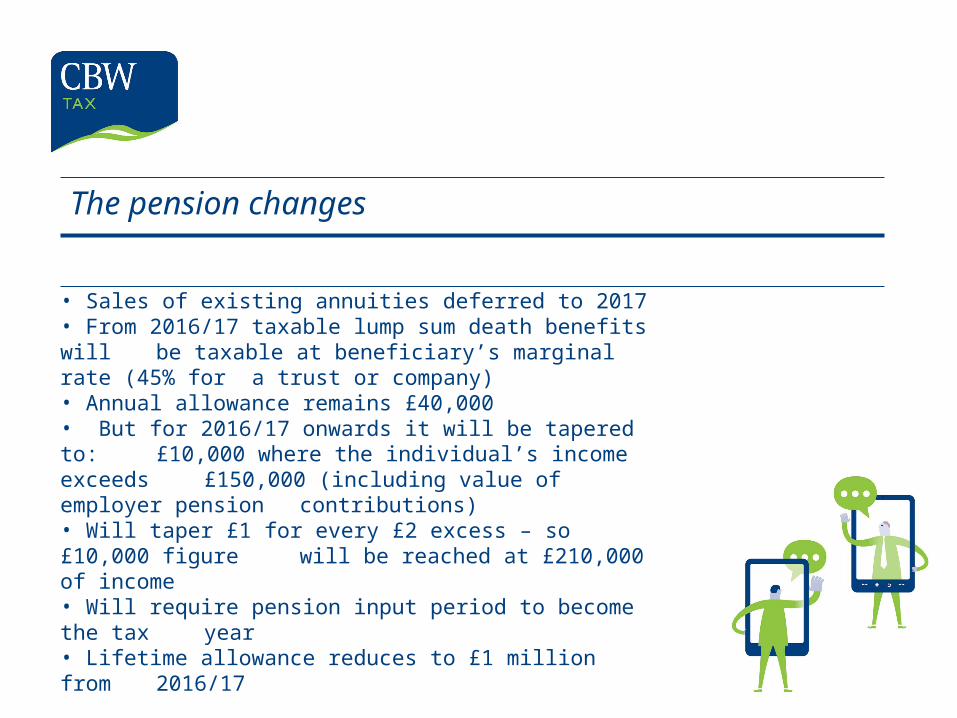

The pension changes

• Sales of existing annuities deferred to 2017• From 2016/17 taxable lump sum death benefits will be taxable at beneficiary’s marginal rate (45% for a trust or company)• Annual allowance remains £40,000• But for 2016/17 onwards it will be tapered to: £10,000 where the individual’s income exceeds £150,000 (including value of employer pension contributions)• Will taper £1 for every £2 excess – so £10,000 figure

will be reached at £210,000 of income• Will require pension input period to become the tax year• Lifetime allowance reduces to £1 million from2016/17

Letting residential property

Tax relief for interest etc

• Interest relief (and for other financing costs) at basic rate only• Applies only to residential property• Position on mixed property is unclear• Reduction will be phased in:

2016/17 full relief2017/18 full relief on 75% (effective rate 35%)2018/19 full relief on 50% (effective rate 30%)2019/20 full relief on 25% (effective rate 25%)2020/21 relief at 20% only

Letting residential property - 2

Wear and tear allowance

• The 10% notional wear and tear allowance on furnished lettings will not apply after 2015/16• Instead landlord can deduct actual cost of replacing furnishings

The Annual Investment Allowance

On most plant and machinery

• Increases/reduces to £200,000 for expenditure from 1 January 2016

• This is described as a permanent increase

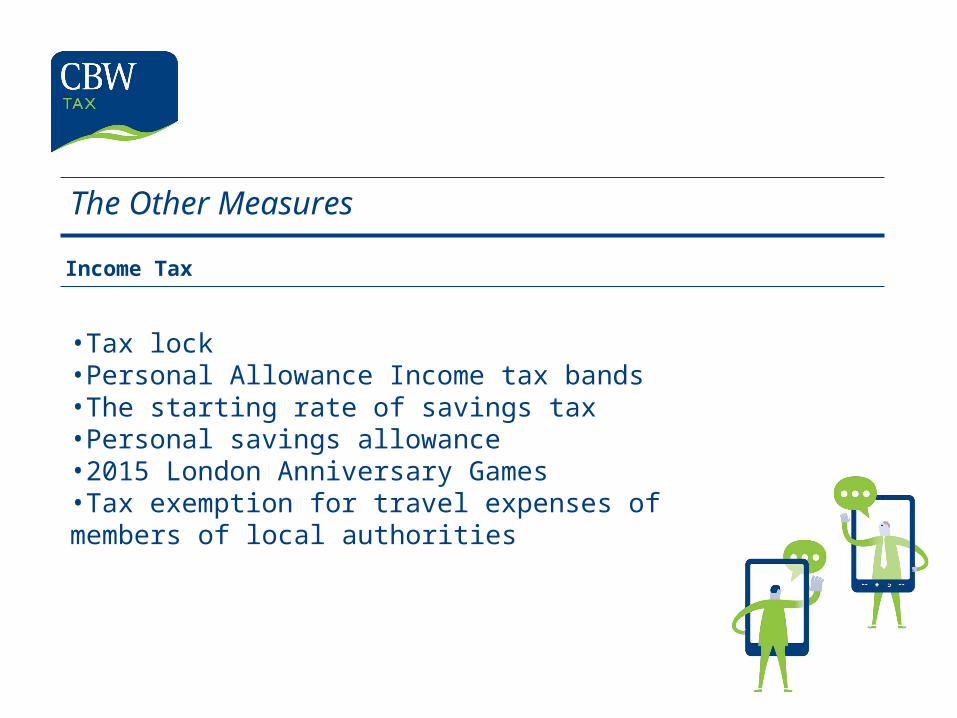

The Other Measures

Income Tax

•Tax lock •Personal Allowance Income tax bands •The starting rate of savings tax •Personal savings allowance •2015 London Anniversary Games •Tax exemption for travel expenses of members of local authorities

The Other Measures

Income Tax - 2

•Review of employee benefits and expenses •Employment intermediaries and tax relief for travel and subsistence •Rent a room relief •Amendments to tax-advantaged venture capital schemes •Sporting testimonials •Extension of averaging period for farmers

The Other Measures

Corporation tax

•Rates •Modernising the taxation of corporate debt •Payment dates •Research and development tax credits:

• universities • and charities

•Simplifying the link company requirements

The Other Measures

Corporation Tax - 2

•Controlled Foreign Company: Loss restriction •Bank corporation tax surcharge •Bank levy reform •Restructuring tax relief for banks’ compensation payments •Scottish Savings Bank •Updating bank definitions

The Other Measures

Capital Gains Tax

• Carried interests of investment managers

The Other Measures

Inheritance Tax

•Nil rate band •Emigration •Simplifying changes on trusts •Pilot trusts •Claims for conditional exemption •Life interest of surviving spouse •Appointment to surviving spouse •Late payment interest

The Other Measures

Administration

•Direct recovery of tax debts •Simplification of HMRC debtor and creditor interest rates •Tackling offshore evasion •Tackling the hidden economy •Additional compliance resources for HMRC

The Other Measures

Other Taxes

• National Insurance: Employment Allowance • Insurance premium tax: Rate increase • Aggregates levy: Exemption re-instated • Climate Change Levy: Green relief withdrawn • Vehicle Excise Duty: New system from 1 April 2017

Robert Maas

Tax Consultant & Tax Expert Robert is a giant in the tax world. He is widely regarded as one of the leading tax practitioners in the UK and is a long-standing tax commentator. He has authored extensively on tax and is always a draw card speaker. The announcement that Robert had won the 2013 Lifetime Achievement Award was met with a standing ovation. Robert is well-loved and much respected – with good reason.

Amongst other roles, Robert is a member of the Technical Committee of the ICAEW Tax Faculty.

t: +44 (0)20 7309 [email protected]

Thomas Adcock

Tax Partner Thomas is a specialist in helping businesses to understand the tax implications of their actions. He works closely with entrepreneurs to manage their tax liability when engaging in property deals, M&A, re-organisations, growth, international deals or when simply looking to improve their tax efficiency.

He also works with ambitious and successful individuals who wish to build, spend or share their personal wealth tax efficiently.

t: +44 (0)20 7309 [email protected]

Andy White

Tax Partner Advising clients on their strategic tax affairs is Andy’s specialist area. He combines his deep technical knowledge and creativity to deliver real taxation solutions that advance clients’ commercial and personal interests.

With 30 years’ general practice experience, including advising on flotation's, MBOs and secondary buyouts, Andy makes an excellent advisor to most businesses experiencing rapid growth or considering strategic changes.

t: +44 (0)20 7309 [email protected]

CBW66 Prescot Street London E1 8NN

t: + 44 (0)20 7309 3800 f: + 44 (0)20 7309 3801

e: [email protected]: cbw.co.uk

Where are we?

can

can