Embed Size (px)

Citation preview

Presented by:Presented by:

Presented by:

Tax Accounting: A Regulatory & Tax Perspective

Lakshmanan Balachander, Director, Deloitte Tax LLPPhilip Cusack, Senior Manager, Deloitte & Touche LLP

3 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

Agenda

• Introduction to U.S. Capital Regulations

• U.S. Basel III final rules: Summary

• DTA: Capital treatment under Basel III

• DTA / NOL Planning Considerations

• Practical Implications for Tax Professionals

• Question and Answer

Introduction to U.S.

Capital Regulations

5 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Sets risk and capital management requirements stipulating banks hold sufficient

capital reserves consistent with their risk profile.

• Rules were initially developed in 1988 and have since been implemented (are

being implemented) in most countries, placing internationally active banks on

comparable footing with respect to capital requirements.

• The Basel Accord was formed from guidance provided by the Basel Committee

on Banking Supervision (BCBS)

− Consists of central-banks and banking supervisors of the group of G10

countries (now expanded to G20 countries)

− Looks to promote safety and soundness within the global banking system;

formulates broad supervisory standards and guidelines, and recommends

leading practices

− Expects that authorities of individual member countries will take steps to

implement standards and guidelines through national systems; thus, rules are

somewhat different across jurisdictions, particularly between US and EU

Basel Regulation: Introduction

6 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

• The U.S. Basel III rules (finalized in early 2013), comprehensively overhaul the

regulatory capital framework for banking organizations

• The U.S. Basel III final rules are generally aligned with the Basel Committee on

Banking Supervision (BCBS) guidance - with differences primarily resulting from

Dodd-Frank Act provisions

• Rules effective for the larger US banking institutions as of Jan 1, 2014 and for

smaller banks as of Jan 1 2015

Basel III: A significant milestone for U.S. banks

7 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

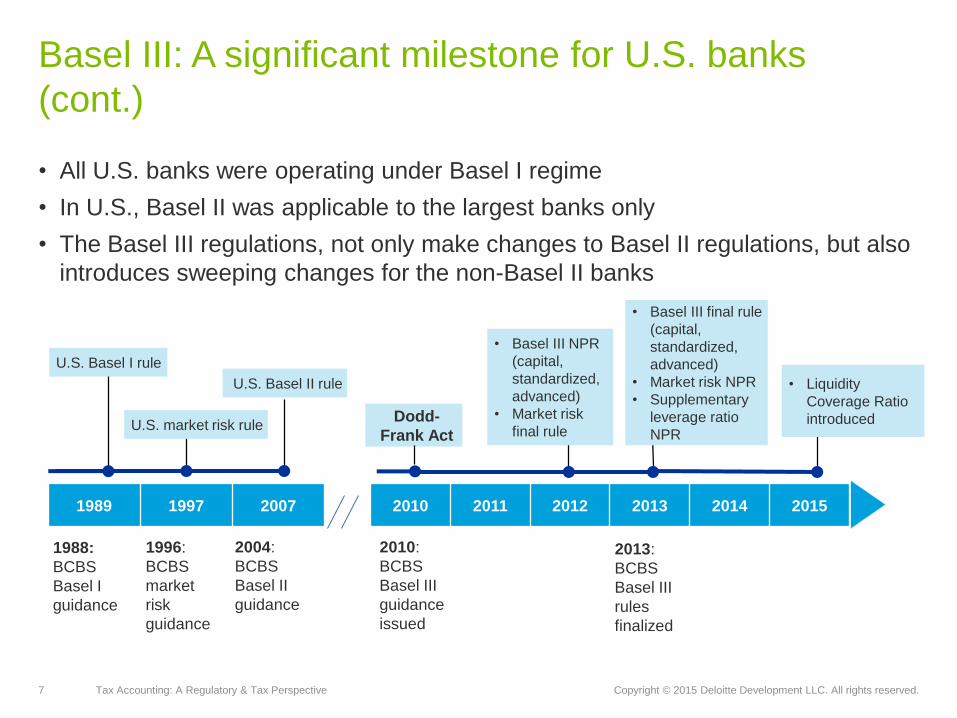

• All U.S. banks were operating under Basel I regime

• In U.S., Basel II was applicable to the largest banks only

• The Basel III regulations, not only make changes to Basel II regulations, but also

introduces sweeping changes for the non-Basel II banks

Basel III: A significant milestone for U.S. banks

(cont.)

2010 2011 2012 2013 2014 2015

2010:

BCBS

Basel III

guidance

issued

Dodd-

Frank Act

• Basel III NPR

(capital,

standardized,

advanced)

• Market risk

final rule

• Basel III final rule

(capital,

standardized,

advanced)

• Market risk NPR

• Supplementary

leverage ratio

NPR

1989 1997 2007

U.S. Basel I rule

U.S. Basel II rule

2004:

BCBS

Basel II

guidance

1996:

BCBS

market

risk

guidance

1988:

BCBS

Basel I

guidance

U.S. market risk rule

• Liquidity

Coverage Ratio

introduced

2013:

BCBS

Basel III

rules

finalized

8 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

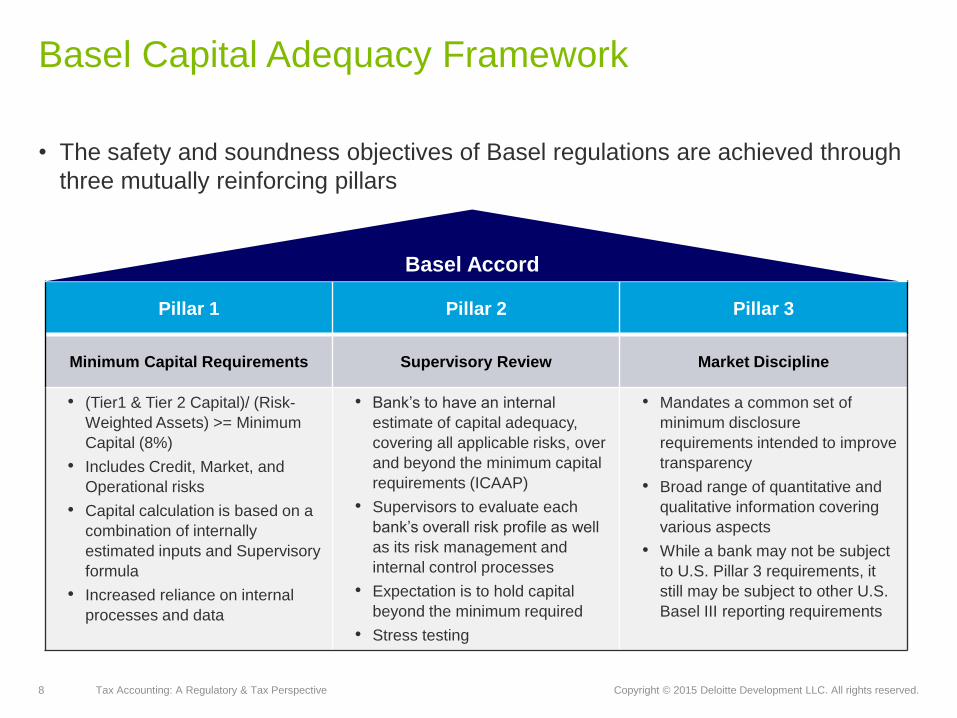

• The safety and soundness objectives of Basel regulations are achieved through

three mutually reinforcing pillars

Basel Capital Adequacy Framework

Pillar 1 Pillar 2 Pillar 3

Minimum Capital Requirements Supervisory Review Market Discipline

• (Tier1 & Tier 2 Capital)/ (Risk-

Weighted Assets) >= Minimum

Capital (8%)

• Includes Credit, Market, and

Operational risks

• Capital calculation is based on a

combination of internally

estimated inputs and Supervisory

formula

• Increased reliance on internal

processes and data

• Bank’s to have an internal

estimate of capital adequacy,

covering all applicable risks, over

and beyond the minimum capital

requirements (ICAAP)

• Supervisors to evaluate each

bank’s overall risk profile as well

as its risk management and

internal control processes

• Expectation is to hold capital

beyond the minimum required

• Stress testing

• Mandates a common set of

minimum disclosure

requirements intended to improve

transparency

• Broad range of quantitative and

qualitative information covering

various aspects

• While a bank may not be subject

to U.S. Pillar 3 requirements, it

still may be subject to other U.S.

Basel III reporting requirements

Basel Accord

9 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

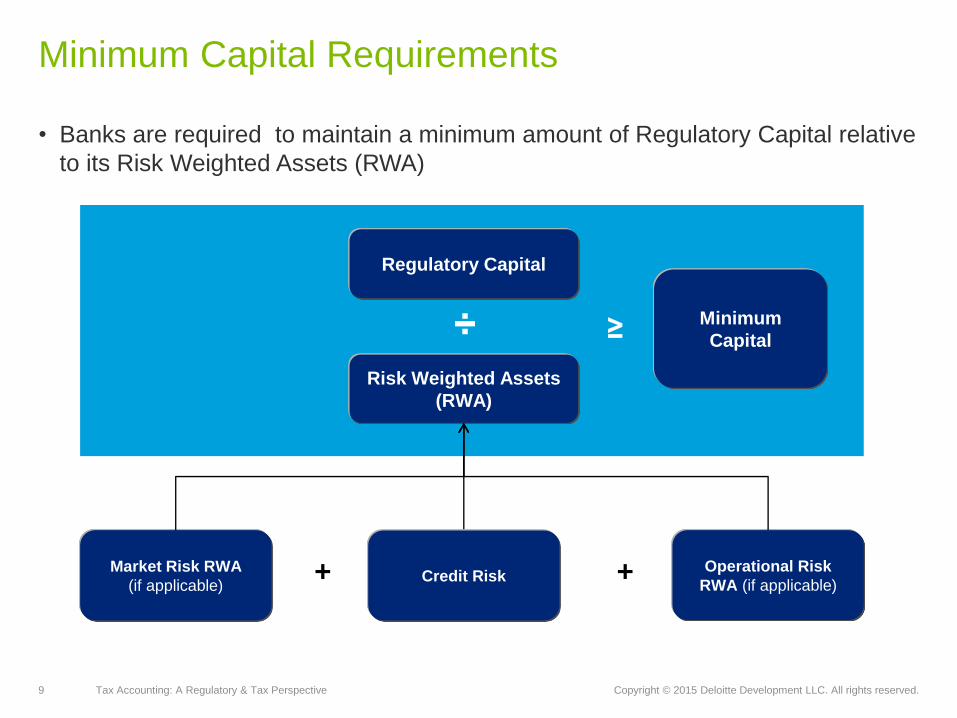

• Banks are required to maintain a minimum amount of Regulatory Capital relative

to its Risk Weighted Assets (RWA)

Minimum Capital Requirements

÷ ≥

Market Risk RWA

(if applicable)

Operational Risk

RWA (if applicable)

Risk Weighted Assets

(RWA)

Regulatory Capital

Minimum

Capital

+ Credit Risk +

10 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

While significant, Basel III is part of the larger regulatory effort to overhaul

risk management

Evolving U.S. banking regulatory landscape

Early remediation

SingleCounterparty

limits

Risk committeeand

governance

Basel III

Volcker rule

Resolutionplan

Stress testingand

capital plan

Liquidityrisk

Disclosureand

reporting

U.S. Basel III final rules:

Summary

12 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

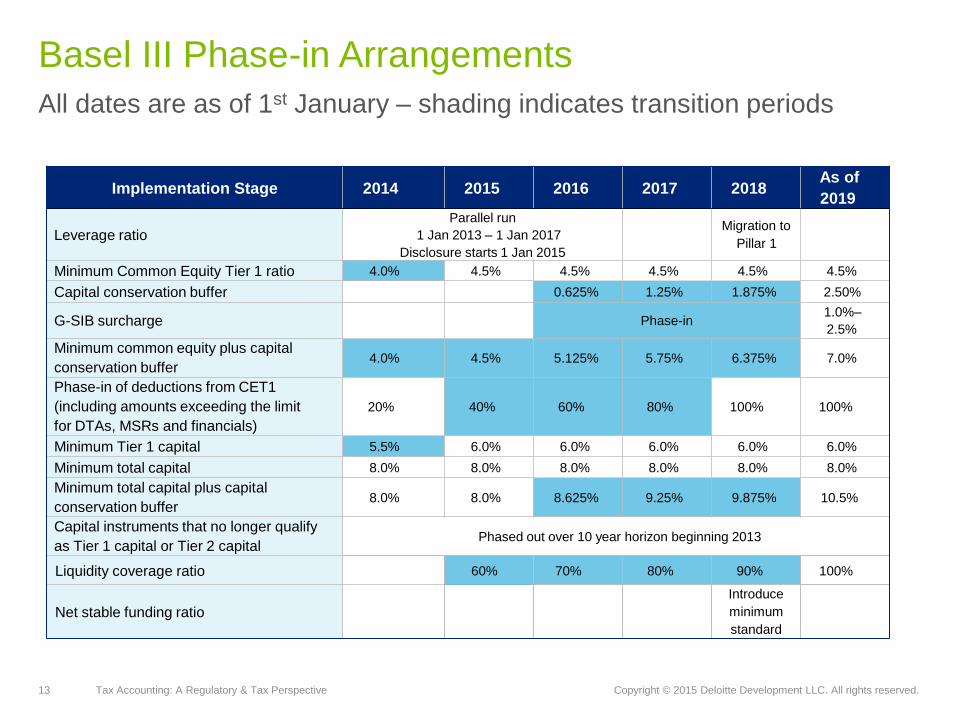

Capital transitions to be completed by 2018; Implementation timelines are

more immediate

Implementation timelines

13 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

Implementation Stage 2014 2015 2016 2017 2018As of

2019

Leverage ratio

Parallel run

1 Jan 2013 – 1 Jan 2017

Disclosure starts 1 Jan 2015

Migration to

Pillar 1

Minimum Common Equity Tier 1 ratio 4.0% 4.5% 4.5% 4.5% 4.5% 4.5%

Capital conservation buffer 0.625% 1.25% 1.875% 2.50%

G-SIB surcharge Phase-in1.0%–

2.5%

Minimum common equity plus capital

conservation buffer4.0% 4.5% 5.125% 5.75% 6.375% 7.0%

Phase-in of deductions from CET1

(including amounts exceeding the limit

for DTAs, MSRs and financials)

20% 40% 60% 80% 100% 100%

Minimum Tier 1 capital 5.5% 6.0% 6.0% 6.0% 6.0% 6.0%

Minimum total capital 8.0% 8.0% 8.0% 8.0% 8.0% 8.0%

Minimum total capital plus capital

conservation buffer8.0% 8.0% 8.625% 9.25% 9.875% 10.5%

Capital instruments that no longer qualify

as Tier 1 capital or Tier 2 capitalPhased out over 10 year horizon beginning 2013

Liquidity coverage ratio 60% 70% 80% 90% 100%

Net stable funding ratio

Introduce

minimum

standard

Basel III Phase-in Arrangements

All dates are as of 1st January – shading indicates transition periods

14 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

Basel III replaces Basel I and modifies Basel II

15 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

Basel III – Snapshot and key takeaways

16 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

Basel III strengthens and simplifies regulatory capital structure

Capital structure

• CET1 is a new category of capital under Basel III

• Most deductions applied to CET1, instead of Tier 1 and Tier 2, increasing the CET1 requirement

• Additionally, Tier 1 and Tier 2 are simplified, by eliminating various sub-limits in each; and

eligibility criteria are strengthened

New ratio defined for

common equity

Eligibility criteria is

more stringent

Qualifying debt instruments

+/- Regulatory adjustments

Tier 2

Qualifying debt instruments

Tier 3

Common equity

+/- Regulatory adjustments

Common Equity Tier 1

Qualifying debt instruments

Tier 2

Qualifying debt instruments

Additional Tier 1

Eliminated

Eligibility criteria is

more stringent

Common equity

+ Qualifying debt instruments

+/- Regulatory adjustments

Tier 1Adjustments are more

stringent and are made

directly to common equity,

instead of tier 1 and tier 2

8%

6%

4.5%

4%

8%

* Plus:

• Capital buffer: 2.5%

• Counter cyclical buffer: 0-2.5%

• Systemically important financial

institution (SIFI) surcharge: 0-2.5%

Deferred Tax Assets:

Capital Treatment under

Basel III

18 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

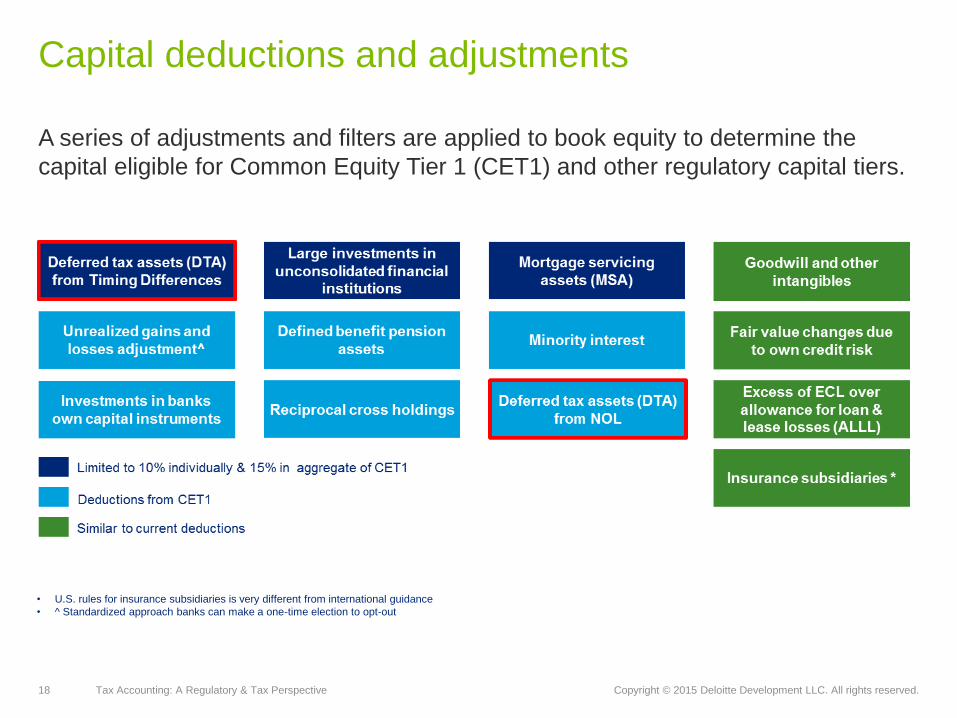

A series of adjustments and filters are applied to book equity to determine the

capital eligible for Common Equity Tier 1 (CET1) and other regulatory capital tiers.

Capital deductions and adjustments

• U.S. rules for insurance subsidiaries is very different from international guidance

• ^ Standardized approach banks can make a one-time election to opt-out

19 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

• A net DTA is allowed to the extent of the lower of:

− 10% of the Total Regulatory Capital

− The amount that can be used in one subsequent year

• A net DTA can be reduced by a carryback prior to applying the above limitation

• DTAs can generally be netted with DTLs

• Certain DTLs in OCI can be either:

− Adjusted out of regulatory capital as a net amount with the OCI item

− Pulled out of OCI and netted against the DTA

DTA Treatment pre-Basel III

20 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

• DTAs that arise from net operating loss and tax credit carry forwards are fully

deducted from CET 1

• DTAs arising from temporary differences that are not absorbed through NOL

carrybacks are included in a bucket with MSRs and Equity in Financial

Institutions

• DTAs not described above:

− Total Limited to 15% of Regulatory Capital

− Each item can not be more than 10% of regulatory capital

− DTAs not deducted will be risk weighted at 100% through 2018

− DTAs not deducted will be risk weighted at 250% beginning in 2019

• Phase-in of the pre-Basel III rules began in 2014

DTA Treatment under Basel III

21 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

• DTLs can be netted against DTAs provided:

− DTAs and DTLs that relate to taxes levied by the same tax authority and are

eligible for offsetting

− DTLs allocated proportionately between DTA arising from NOLs and DTA

arising from temporary differences

• DTLs netted with other assets subject to deduction (Goodwill, Intangibles etc.)

cannot used for netting against DTAs

• AOCI adjustments* must be net of associated tax effects

* i.e. unrealized gains and losses on cash flow hedges for non-fair value items, changes in fair value of liabilities due to changes in the bank’s own credit risk (for an AOCI opt out bank, all other AOCI adjustments)

DTA Treatment under Basel III (cont.)

22 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

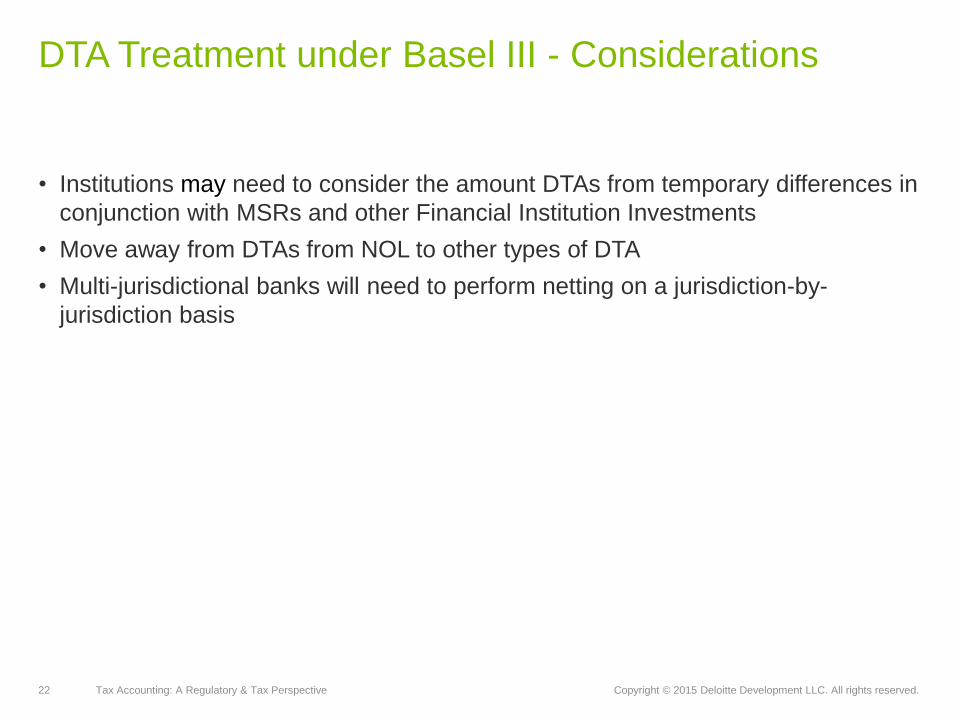

• Institutions may need to consider the amount DTAs from temporary differences in

conjunction with MSRs and other Financial Institution Investments

• Move away from DTAs from NOL to other types of DTA

• Multi-jurisdictional banks will need to perform netting on a jurisdiction-by-

jurisdiction basis

DTA Treatment under Basel III - Considerations

23 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

• There may be an opportunity to utilize DTAs and expiring NOLs by implementing

certain DTA/NOL tax planning.

• These planning approaches may be implemented in the form of:

− Certain elections and other miscellaneous items

− Accounting method changes

− Counterintuitive acceleration of revenue and deferral of expense

DTA/NOL Planning Opportunities

24 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

• A taxpayer may elect to capitalize certain costs in the year they are incurred, as

opposed to deducting these costs which may provide an opportunity to increase

income for a particular year. Some of these elections include but are not limited

to:

− Capitalization of employee compensation and overhead under 1.263(a)-

2T(f)(2)(iv)

− Capitalization of costs under section 1.266-1 – Under section 266, a taxpayer

may elect to capitalize taxes and carrying charges related to real or personal

property.

− Election to capitalize research and experimentation costs under section 59(e)

• Other elections and miscellaneous items include:

− Electing out of bonus depreciation

− Inclusion of disputed receivables in income

− Changes to accrued bonus, vacation and sick pay plan

Elections and other misc. items

25 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

Filing a Form 3115, Application for Change in Method of Accounting, for the

method changes listed above, may result in an increase in taxable income to offset

pre-existing NOLs. An accounting method change can either be classified as an

automatic or advanced consent. The following are examples of accounting method

changes that may be effectuated by filing a Form 3115:

• Automatic method changes:

− Direct reallocation method

− Full inclusion method

− Capitalization of software development costs

− Timing of liabilities

• Advanced Consent method changes:

− Accrual method to cash method for self-insured medical, worker’s

compensation, and retiree medical benefits

− Expense to amortization for certain non-deductible prepaid expenses

Accounting Method Changes

26 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Carryback just DTAs, or DTAs net of DTLs

• Two year carryback application (periods used, AMT)

• Blended state tax rates

• State temporary differences

• Intra-entity transfers and the deferred tax impact

• Resolution VAs, APB 23

• Recovery VAs, APB 23

Basel III Marketplace Discussions

Practical Implications

for Tax Professionals

28 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Largest financial institutions have been required to do annual “stress tests”

− Annual process with the Federal Reserve to determine capital adequacy in

financial institutions under various scenarios

− Started in 2009 for the 18 largest financial institutions (originally called SCAP)

− In 2013 another 12 financial institutions; over $50B in assets

− Capital rules eventually apply to all financial institutions

• Implications for Tax Professionals

− Participation in a rigorous process in assembling projections

◦ Income statement

◦ Balance sheet

◦ Coordination with Treasury, Finance, other parties

− Critical to understand tax related capital calculations

◦ Very important to have broader understanding of how certain other items are treated

in the capital calculation and how they relate to tax calculations

CCAR / DFAST Process

29 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Implications for Tax Professionals (cont.)

− Deliverables

◦ Calculation of effective tax rate

◦ Calculation of estimated current tax payable

◦ Carryback capacity

◦ AMT/Business credit limitation

− Estimation of temporary differences and impact on DTA/DTL

− Calculation of estimated DTA that may be relevant for capital calculation

◦ Grossed up DTA’s / DTL’s

◦ Carryback analysis

◦ Carryforward identification

◦ Allocation of DTL’s to various DTA’s

− Documentation

CCAR / DFAST Process (cont.)

30 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Implications for Tax Professionals (cont.)

− Other considerations

◦ Technology

◦ Process integrity

◦ Coordination with other reporting

◦ Tax return / estimated taxes

◦ Required scenarios and timing

◦ Role of advisors

• Federal Reserve Methodology

− “Black Box”

◦ Simplifying tax rate assumptions used

◦ Potential distortion of capital levels

CCAR / DFAST Process (cont.)

31 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

GAAP

• Heightened expectations

• Materiality

• Capital ratio disclosures

Regulatory

• DFAST / CCAR

• Call reports

• Legal entity integrity

External Reporting

32 Tax Accounting: A Regulatory & Tax Perspective Copyright © 2015 Deloitte Development LLC. All rights reserved.

This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting,

business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for

such professional advice or services, nor should it be used as a basis for any decision or action that may affect your

business. Before making any decision or taking any action that may affect your business, you should consult a qualified

professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this presentation.

About this presentation

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities.

DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see

www.deloitte.com/about for a detailed description of DTTL and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte

LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Member of Deloitte Touche Tohmatsu Limited