Embed Size (px)

Citation preview

Behavioural Economics in Financial Services: Perspectives and Prospects

A Seminar for Eversheds LLP

• Jim Devlin

• Director: Centre for Risk, Banking and Financial Services

• Professor of Financial Decision Making: Marketing Division

• Nottingham University Business School

• The rise and rise of behavioural economics

• What are the main principles of behavioural economics?

• How do we know this stuff works? Some evidence

• Introduction to applications; A useful tool for policymakers and firms?

• Is there a potential dark side to behavioural economics?

Structure

• Arguably, 10 years ago BE was almost exclusively the preserve of nerdy, academic types mainly working in the area of economic psychology

• Now, the Government has a whole unit focussed on using BE to cure just about any problem one cares to name

• Policymakers are busy working out how to apply BE to their particular area of responsibility (not least the FCA)

Behavioural Economics: The Rise and Rise

• Just about every consultancy has a specialist division in the area

• Companies are busy working out what it all means and how to make money by using it

• Countless seminars are taking place on a weekly basis

• And of course, many of the aforesaid nerdy, academic types are now academic “rock stars” and have written books on the subject that have sold many, many copies

• Why?

Behavioural Economics: The Rise and Rise

• Only natural that things become fashionable at a certain point

• But, as we will come on to see, evidence of BE’s power and potential to influence consumer decision making is strong and consistent

• But that alone does not account for BE’s rise in popularity

• Other factors at play

Behavioural Economics: The Rise and Rise: Why?

• For instance, economists tend to be very well represented in policymaking circles

• Therefore, traditional economic theory and assumptions have tended to dominate policy approaches

• For instance, the recently disbanded Financial Services Authority and its approach….more information and moreconsumer education making “informed, more rational choice” more straightforward and more likely

• But experience has shown that such approaches do not tend to work

Behavioural Economics: The Rise and Rise: Why?

Behavioural Economics: The Rise and Rise: Why?

• Important to understand that BE exists as a counter-point to traditional economic theory

• And the assumption we are essentially rational beings that act as “homo-economicus” (self interested and vested with immense information processing powers)

• A very neat model………but does it account for how we actually behave?

• Increasing realisation that it does not

• Hence alternative approaches required to understand judgments and decision making

Behavioural Economics: The Rise and Rise: Why?

• There is a large body of evidence showing persistent and consistent violations of rationality: As Dan Ariely puts it neatly in the title of his book, we are Predictably Irrational

• This evidence is sizable and robust enough that such departures from rationality cannot be dismissed as mere aberrations

• Hence Behavioural Economics, a relatively recent, multi-disciplinary approach that attempts to explain departures from rationality and actual observed behaviour

Behavioural Economics: What is it all about?

• There are many inconsistencies in our judgments and decision making (known as biases) and these biases are predictable

• We are generally lazy in our thinking and like to take mental short cuts and employ “rules of thumb” (but that sounds too simple so they are known as heuristics in academic work)

• How information and choices are presented to us can have a large impact on our decisions (this is known as framing effects)

Behavioural Economics: What is it all about?

• But just how new is all of this? Not to most marketing practitioners, for instance

• Have been accusations that behavioural economics is little more than glorified common sense and that it merely states the obvious

• But strong evidence base from the research provides depth

• And simplicity does not take away from the potentially profound implications

The evidence: Bias against losses

• We hate losing things roughly twice as much as we like gaining things (known as Loss Aversion)

• “Losses loom larger than gains”• And we use a reference point to evaluate our gains

and losses.• Underpins many important phenomena in

behavioural economics

• The Mug Experiment is just one of many studies that provides empirical backing

The evidence: Bias against losses: The Mug Experiment

Reported in Kahneman, D (2011) Thinking Fast and Slow

• In student classes; random half class given given mugs with University insignia; other half nothing

• People then offered the chance to trade, but buyers had to use their own money

• People had to “name their price”

• Consistently, price required to sell is TWICE that of price buyers are willing to pay

• More of an issue with losing the mug than gaining it!

The evidence: Bias against losses: The Mug Experiment

Reported in Kahneman, D (2011) Thinking Fast and Slow

• Third group added who don’t name a price for buying and selling, but can choose either the mug or an amount of money and state what amount of money is equally desirable to the mug; results:

• Sellers $7.12, Choosers $3.12, Buyers $2.87

• Gap between sellers and choosers is particularly remarkable, as either can go home with the mug or the money and face what should be the same choice!

The evidence: Bias for the status quo and default option:

• People have a tendency to stick with current choices/patterns of behaviour

• An exaggerated preference for the status quo which is really just inertia

• It involves less mental effort• Colloquially known as the “whatever” phenomenon• Relatedly, most people also go with the “default

option” rather than make a more considered choice• These biases are arguably intuitively obvious

• But how do we know that they are so predictable and prevalent

The evidence: Bias for the status quo and default option:

Reported in Thaler, R and Sunstein, C (2008) Nudge: Improving Decisions about Health Wealth

and Happiness

• Study conducted in the late 1980s on the pension plan of many college professors in the US

• After initial asset allocation decision, median number of changes over a lifetime was ZERO

• In the whole of their working life, more than half of all scheme members made no changes whatsoever

The evidence: Bias for the status quo and default option:

Reported in Thaler, R and Sunstein, C (2008) Nudge: Improving Decisions about Health Wealth

and Happiness

• Separate study participants were given a scenario where they inherited some money as cash and were given four investment options (moderate risk company, high risk company, treasury bills, bonds)

• When told that the inherited money was a mixture of cash and stocks of moderate risk many more chose to stick with this option and % ending up in moderate risk assets much higher

• Overall, compelling evidence

The evidence: Heuristics Reported in Kahneman, D (2011) Thinking Fast

and Slow

• Mental shortcuts abound, we can only cover some of the most important

• Anchoring and Adjustment: our tendency to make judgements by adjusting from some reference point, which can even be arbitrary

• Far easier to provide evidence/illustrate than explain!

The evidence: Heuristics Reported in Kahneman, D (2011) Thinking Fast

and Slow

• Two Professors in the US once rigged a “wheel of fortune” marked 1-100, but that would only stop at 10 or 65• Groups of students stood in front of it whilst it was spun

and wrote down the number at which it stopped• They were then asked “What is your best guess of the % of

African nations in the US?”

• Average estimates for those who saw the wheel stop at• The number 10 = 25%• The number 65 = 45%

• Exposure to a totally irrelevant number influenced their guess

• One of the most robust and reliable results in behavioural economics

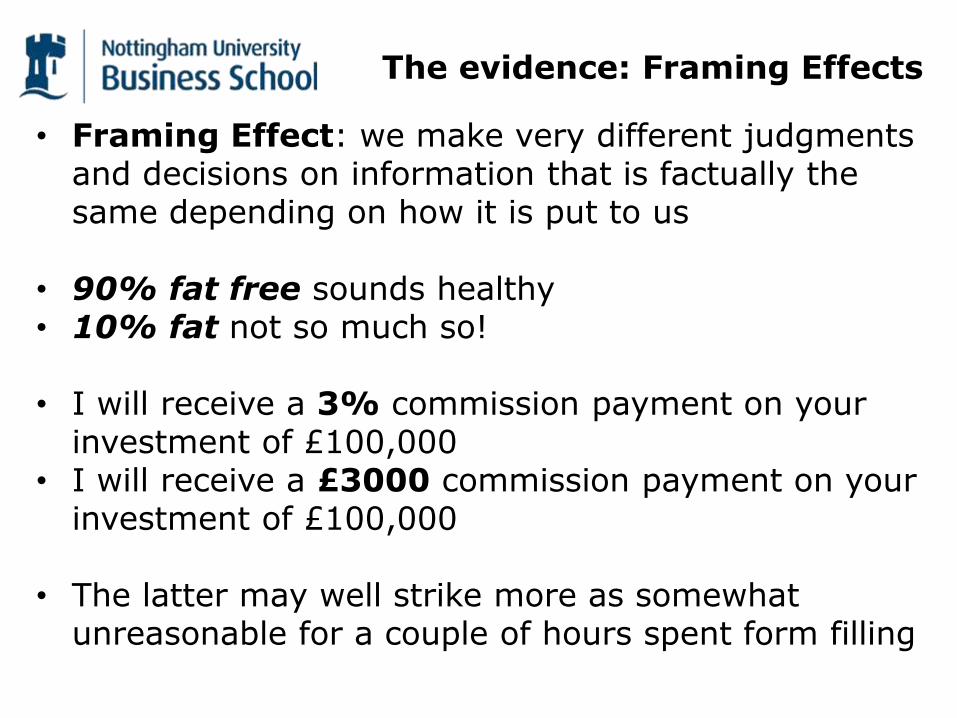

The evidence: Framing Effects

• Framing Effect: we make very different judgments and decisions on information that is factually the same depending on how it is put to us

• 90% fat free sounds healthy• 10% fat not so much so!

• I will receive a 3% commission payment on your investment of £100,000

• I will receive a £3000 commission payment on your investment of £100,000

• The latter may well strike more as somewhat unreasonable for a couple of hours spent form filling

The evidence: Framing Effects

• Even professionals influenced by framing

• Some doctors told that an operation was associated with a 90% survival rate

• Others that the same operation was associated with a 10% mortality rate

• Former group more likely to recommend the operation even though outcomes are factually identical

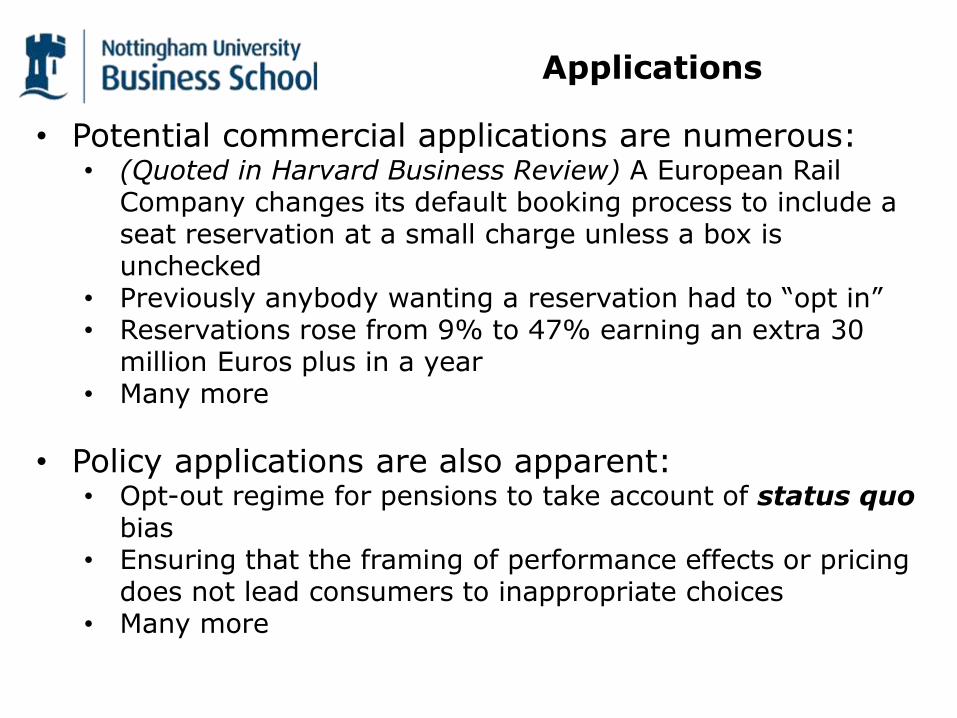

Applications

• Potential commercial applications are numerous:• (Quoted in Harvard Business Review) A European Rail

Company changes its default booking process to include a seat reservation at a small charge unless a box is unchecked

• Previously anybody wanting a reservation had to “opt in”• Reservations rose from 9% to 47% earning an extra 30

million Euros plus in a year• Many more

• Policy applications are also apparent:• Opt-out regime for pensions to take account of status quo

bias• Ensuring that the framing of performance effects or pricing

does not lead consumers to inappropriate choices• Many more

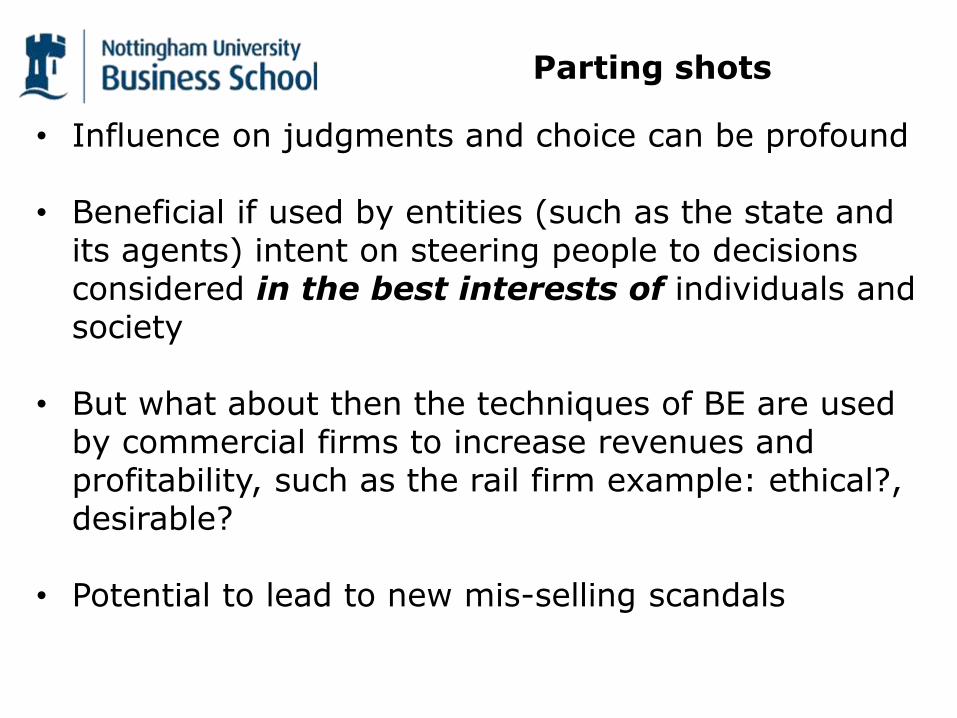

Parting shots

• Influence on judgments and choice can be profound

• Beneficial if used by entities (such as the state and its agents) intent on steering people to decisions considered in the best interests of individuals and society

• But what about then the techniques of BE are used by commercial firms to increase revenues and profitability, such as the rail firm example: ethical?, desirable?

• Potential to lead to new mis-selling scandals

Behavioural Economics and Competition Law

Implications for Enforcement

Adam Ferguson, Eversheds LLP

6 May 2014

Overview

• Is there a role for competition law in addressing problems created by behavioural biases and heuristics?

• What impact could behavioural economics have on competition law enforcement?

• Should regulators design remedies to account for behavioural biases?

• What are the threats and opportunities for financial services businesses?

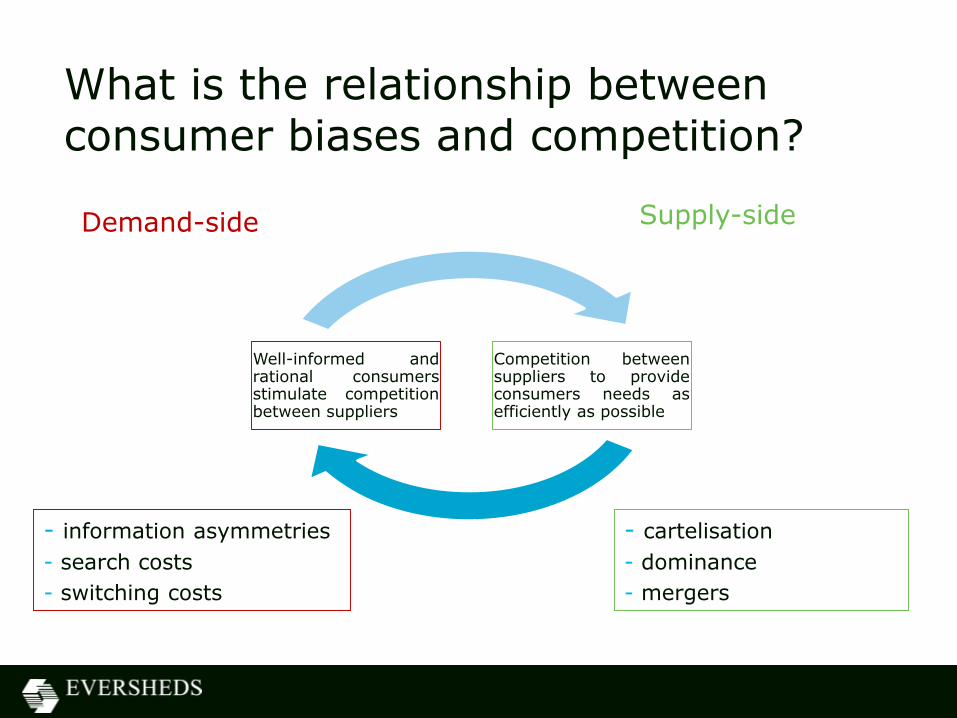

What is the relationship between consumer biases and competition?

Competition betweensuppliers to provideconsumers needs asefficiently as possible

Well-informed andrational consumersstimulate competitionbetween suppliers

Demand-side Supply-side

- cartelisation

- dominance

- mergers

- information asymmetries

- search costs

- switching costs

The UK markets regime

• Traditional antitrust tools not designed to address issues on the demand side...

• However, the Enterprise Act 2002:

– enables the Competition and Markets Authority (CMA) to intervene where it is concerned that any feature of a market leads to an adverse effect on competition (AEC); and

– if there is an AEC, to remedy it

The UK markets regime

• For example, Competition Commission’s Issues Statement in Payday Lending identifies two features which may lead to an AEC:

– market concentration

– impediments to switching

• In that context the CMA is considering the role of present bias and over-confidence

Impact of BE: better understanding of demand-side harms

• For example in relation to tying and bundling cases:

– when viewed entirely rationally, tying may appear to create only minimal switching costs

– however, default bias and endowment effects may make market foreclosure more likely than might appear to be the case

• Microsoft – Windows/Media Player

Impact on selection of cases?

• BE casts light on gravity of demand side phenomena

• For example:

– the risk and gravity of increased search costs resulting from drip or complex pricing may be more prevalent because of reference dependence and/or framing effects

• Therefore, the prevalence of biases may make for a stronger case for intervention

• Also, the CMA now has the ability to look at features on cross-market basis

What does BE mean for remedies?

• Traditional anti-trust tools identify, punish, deter and facilitate reparation

• In market investigations, CMA must ensure any remedy is:

– comprehensive

– effective

– proportionate

• Critical that regulators are aware of behavioural biases to ensure remedies are effective and have no unintended consequences

What does BE mean for remedies?

• Awareness of BE will affect remedy design

– more information / more choice will not necessarily enhance competition

– the impact of consumer education may be limited

• Regulators have and will take consumer biases into account (contrast the Microsoft Media Player and Internet Explorer cases)

• Need for more intensive remedies stage to allow for input from behavioural psychologists and test efficacy of remedies?

• Can this be accommodated in the shorter statutory timetable for market investigations?

Threats and opportunities

• Businesses exploiting consumer biases are at greater risk of intervention

• Insights of BE are not the sole preserve of regulators

• Businesses must ensure competition authorities:

– do not misapply their consumer regulatory powers without full rigours of market investigation

– take account of behavioural biases where this militates against intervention and in formulating remedies

For example…

• Allowance for over-confidence and aggression –when assessing the weight to attach to evidence in internal documents

• Could vengeful rather than rational behaviour counteract attempts to exploit consumers?

Conclusions

• There is a role for competition law in addressing behavioural biases

• BE is already having and will continue to impact competition law enforcement

• Businesses need to familiarise themselves with the insights of behavioural economics

– to protect against the risk of intervention

– to better anticipate the outcome of regulatory intervention

– to ensure regulatory outcomes are fair and proportionate

Are any of us immune?

• Which location is rainier

– Manchester or

– Weston-super-Mare?

• Even regulators are susceptible to biases and heuristics

For more information please contact:

David SaundersPartner - Financial Institutions sectorT: 0845 497 3647E: [email protected]

or visit:

www.eversheds.com/financialinstitutions

www.twitter.com/EvershedsFI