Embed Size (px)

Citation preview

Banking 4.0

Banking in the Fourth Industrial Revolution (Industry 4.0)

2

The Fourth Industrial Revolution is coming

and very few are ready

3

The Fourth Industrial Revolution is comingPowered by Internet of Things applied to the industry, combined with other technologies like BigData, Machine Learning and 3D printing.

Source: Forschungsunion, acatech, Abschlussbericht Arbeitskreis Industrie 4.0

IndustrialInternet of Things

4

Internet of Things is at the center of the revolution

“In the next 10 years, the Internet of Things (IoT) revolution will dramatically alter manufacturing, energy, agriculture, transportation and other industrial sectors of the economy which, together, account for nearly two-thirds of the global gross domestic product (GDP).”

“It will also fundamentally transform how people will work through new interactions between humans and machines.”

Source: World Economic Forum,”Industrial Internet of Things: Unleashing the Potential of Connected Products and Services”

5

Not everything is wearables

Consumer applications have all the media hype and visibility, such as fitness monitors and self-driving cars.

Source: McKinsey, “The Internet of Things: Mapping the value beyond the hype”

But industrial application of IoT in B2B use cases can generate nearly 70 percent of potential value enabled by IoT.

6

Towards a fully networked societyWith an adoption rate five times faster than electricity and telephony

6 devices for each

Smartphone

Where everything is connected, not just consumer devices

7

IoT will change the whole society ...

Source: Texas Instruments, ”The Internet of Things: Opportunities & Challenges”

8

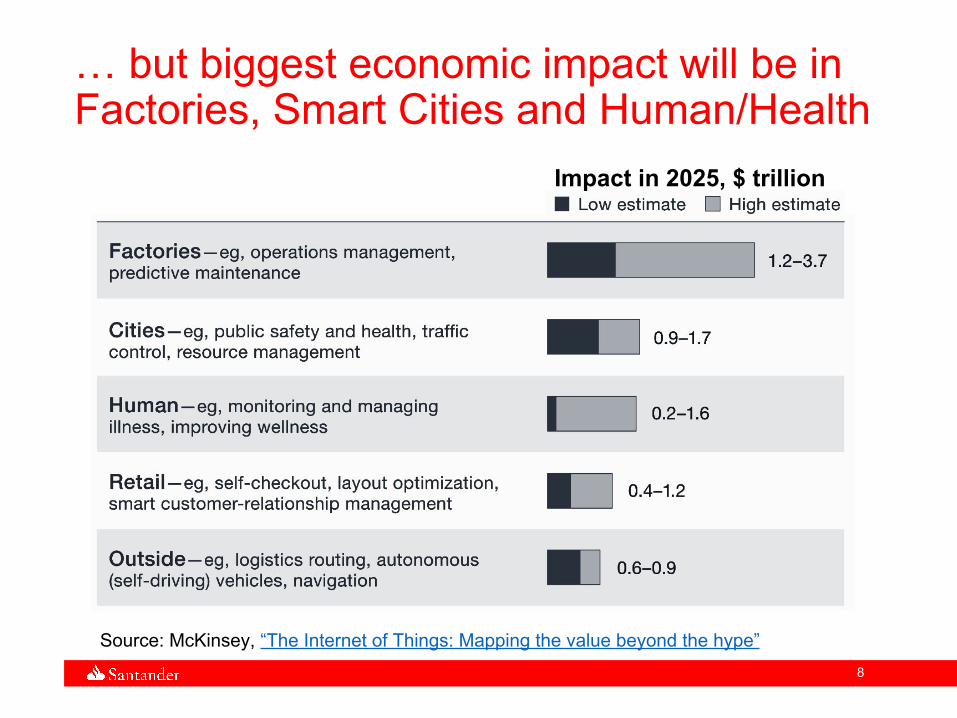

… but biggest economic impact will be in Factories, Smart Cities and Human/Health

Source: McKinsey, “The Internet of Things: Mapping the value beyond the hype”

Impact in 2025, $ trillion

9

Manufacturing has one of the highest multiplier effects on an economy

Manufacturing is an indispensable element of the innovation chain, enabling technological innovations to be applied in goods and services in other sectors like SmartCities or Health, multiplying their societal and economic benefits.

80% of the EU’s exports are manufactured products. Manufacturing employs around 30M persons in the EU and twice as many in support activities such as logistics.

Sources: European Comission, “Factories of the Future: Multi‐annual roadmap for the contractual PPP under Horizon 2020” and “Factories of the Future: towards competitive EU manufacturing”.World Economic Forum, “The Future of Manufacturing: Driving Capabilities, Enabling Investments”

10

Industry 4.0And beyond

11

Industry 4.0 ecosystem

SuppliersFactory

Logistics Logistics Retailer

Final product

Customer

Social network dataExtended Manufacturing Process

Material flow

Product usage

Smart products

Adaptive logistics

Finance flows in

real-time

Predictive maintenance

Product tracking

New business models

PlatformAn ecosystem of partners provide advanced services to all participants.

Smart Services

All machines with sensors, connected to a cloud platform

12

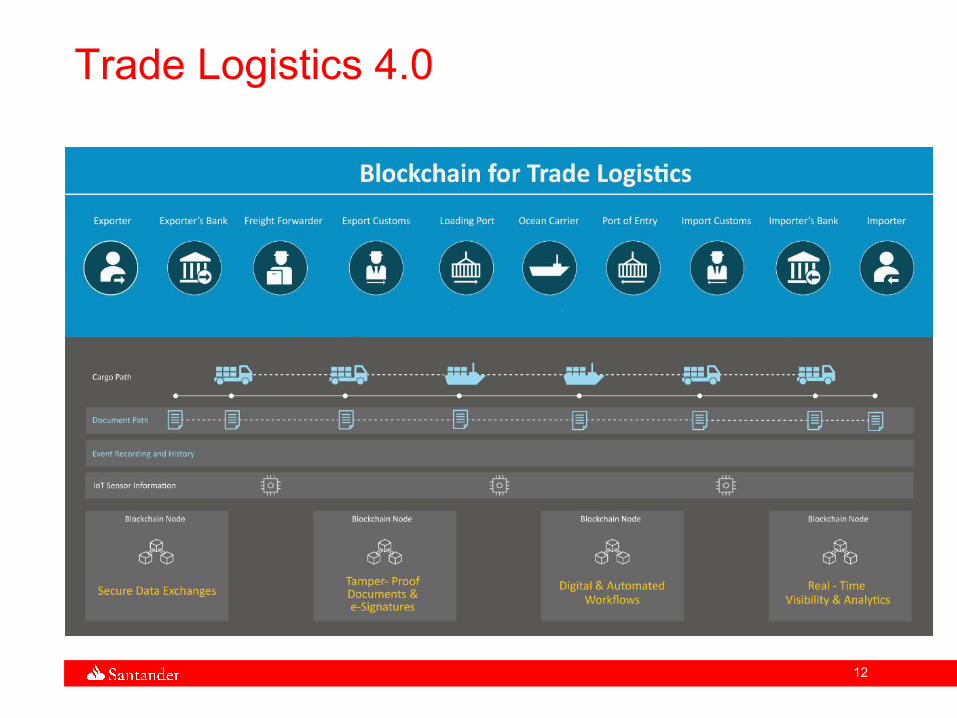

Trade Logistics 4.0

13

Some challenges in Industry 4.0

Which may be opportunities for banks

14

Industry 4.0 ecosystem

SuppliersFactory

Logistics Logistics Retailer

Final product

Customer

Social network dataExtended Manufacturing Process

Material flow

Product usage

Smart products

Adaptive logistics

Finance flows in

real-time

Predictive maintenance

Product tracking

New business models

PlatformAn ecosystem of partners provide advanced services to all participants.

Smart Services

All machines with sensors, connected to a cloud platform

15

A lot of sensors, actuators and extended communications require a lot of investment

Some companies have already invested in sensors and comms, but for most SMEs they still have to invest a lot.

Everything is connected to a shared platform: the factory, suppliers, logistics providers and retailers, and also the customer products.This allows to have a real-time holistic view of the manufacturing process.

16

Risk of lack of integration

If each participant implements its own solution, they are not integrated and it is difficult to perform global optimization and provision of services.

17

All entities participating in the value chain are connected to a common platform

It may not be a traditional “Data Lake”, but instead a virtual decentralized infrastructure, like the Industrial Data Space.Or the MIT Enigma.

It aggregates data from all participants:● Supports new data value

chains● Linking providers and data

users● Supports the development

of new value added data services.

18

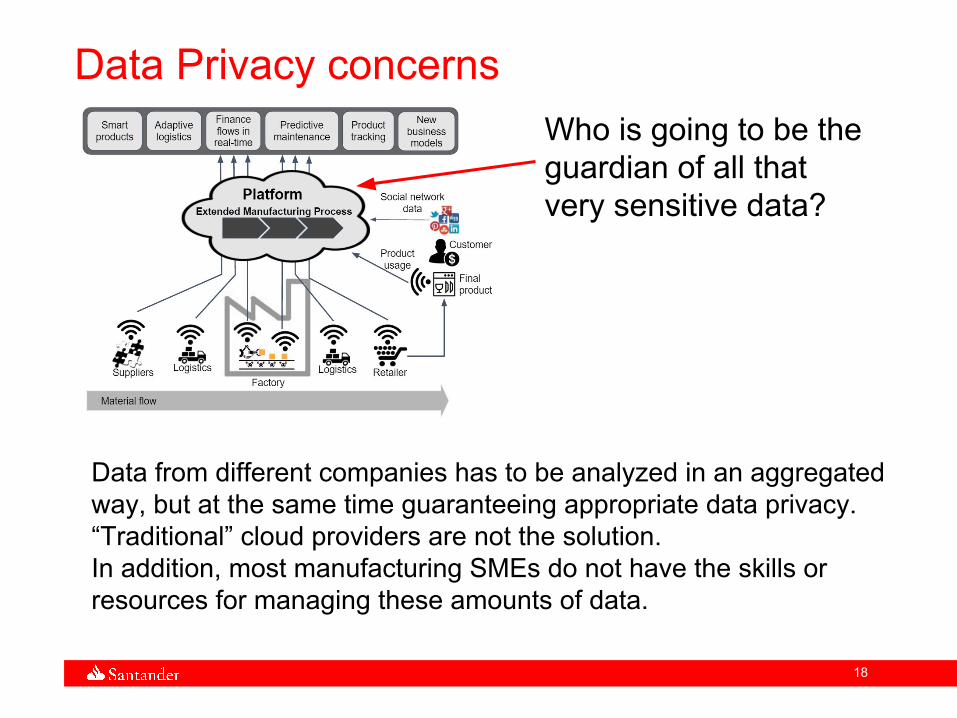

Data Privacy concerns

Data from different companies has to be analyzed in an aggregated way, but at the same time guaranteeing appropriate data privacy.“Traditional” cloud providers are not the solution.In addition, most manufacturing SMEs do not have the skills or resources for managing these amounts of data.

Who is going to be the guardian of all that very sensitive data?

19

Data Privacy is one of the main challenges

Source: Altimeter Group, “Consumer Perceptions of Privacy in the Internet of Things” (2015)

Consumers’ top privacy concerns with IoT are data selling, storage, access, and the ability to be identified individually.Q: Rate your level of privacy concerns across each of the following ways companies interact with your data

Age groups

20

But banks are (still) well positioned

Which type of company do you trust most with securely managing your data on your behalf?

Despite the reputational damage from the financial crisis, banks hold a fundamentally trusted position in society, as the stewards of assets and commerce.

While the public gives low ratings to the industry as a whole on matters of trust*, their opinions about the banks they actually do business with are far more favorable**.

Sources:*Edelman, “2016 Edelman Trust Barometer”**Accenture, “2015 North America Consumer Digital Banking Survey - Banking Shaped by the Customer”

Bank

Payments provider

Mobile networkOnline retailer

Consumer technologyBroadband internetSocial media

21

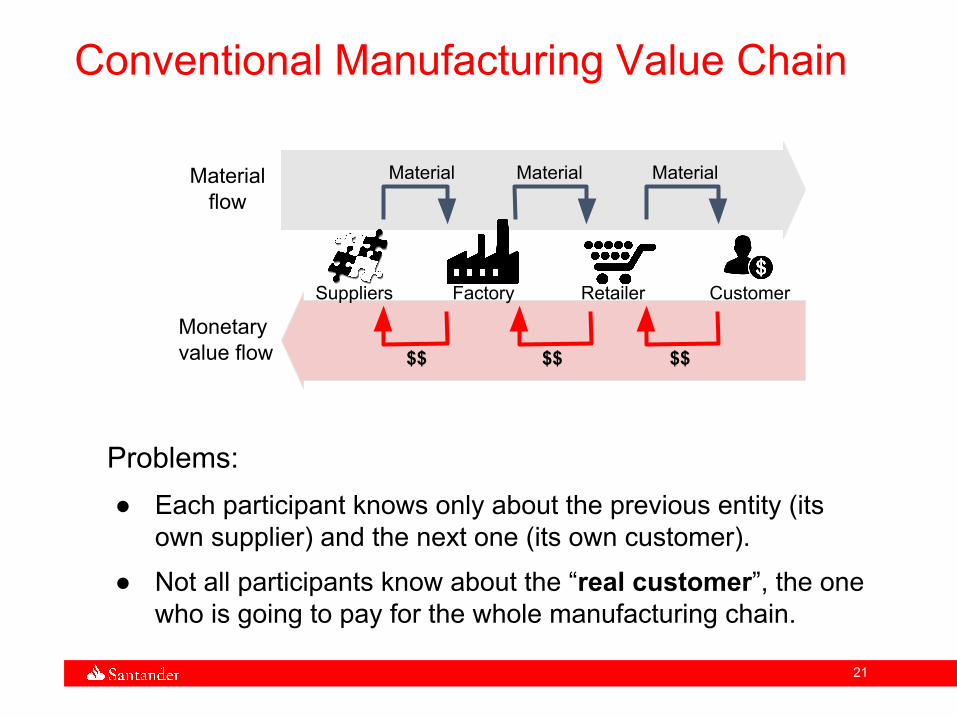

Conventional Manufacturing Value Chain

Factory Retailer CustomerSuppliers

$$ $$ $$

Material Material MaterialMaterial flow

Monetary value flow

Problems:● Each participant knows only about the previous entity (its

own supplier) and the next one (its own customer).

● Not all participants know about the “real customer”, the one who is going to pay for the whole manufacturing chain.

22

New business models for new finance flows

Flow of materials, value and information are different and in real-time.

They require new ways of payments and financing that will have to be bundled with the services provided by new ecosystem platforms.

New products and services offered both to individual entities and to the Platform as a whole

23

Autonomous, pull economy

Highly automated, flexible production and fulfilment networks

Continuous demand-sensing

Monetary flows

24

Conclusion

The Fourth Industrial Revolution is comingWorld 4.0 will radically alter the flows of value among the participants in the new economy, and will require new ways of payments and financing.

The challenge for banks is to determine new business models beyond the purely financial services, and new partnerships, as the world economy evolves first to an outcome-based economy and eventually to a pull-based economy.

“Our mission is to help people and businesses prosper”

Nuestra misión es contribuir al progreso de las personas y de las empresas.

Nuestra cultura se basa en la creencia de que todo lo que hacemos debe ser

Gracias