Embed Size (px)

Citation preview

Hosted by:

John King

Barclays Capital

15 April 2013

The ISG Outsourcing Index, EMEA

First Quarter 2013

Market Data and Insights

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

2

Covering the state of the outsourcing industry for global, commercial contracts.*

Welcome to the 42nd Quarterly ISG Outsourcing Index EMEA

Bernd SchaeferPartner

John Keppel

President & Chief

Marketing Officer

Dr. David Howie

Partner

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

3

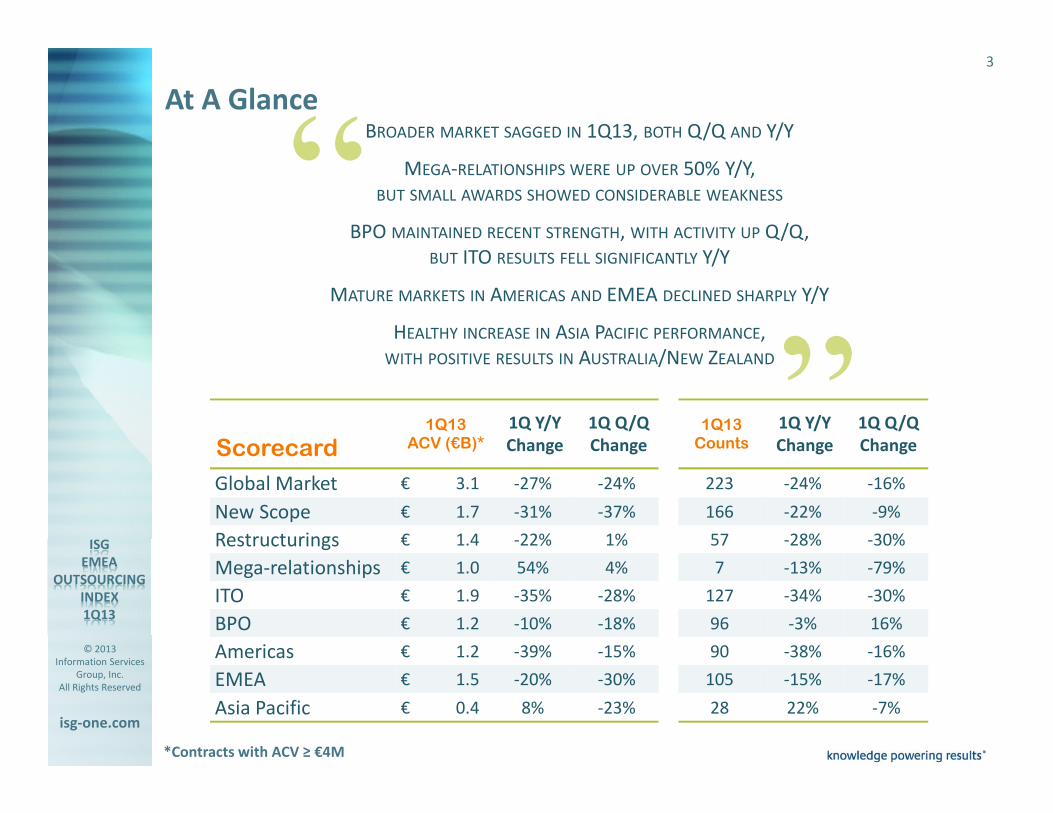

At A Glance

“ “

BROADER MARKET SAGGED IN 1Q13, BOTH Q/Q AND Y/Y

MEGA-RELATIONSHIPS WERE UP OVER 50% Y/Y,

BUT SMALL AWARDS SHOWED CONSIDERABLE WEAKNESS

BPO MAINTAINED RECENT STRENGTH, WITH ACTIVITY UP Q/Q,

BUT ITO RESULTS FELL SIGNIFICANTLY Y/Y

MATURE MARKETS IN AMERICAS AND EMEA DECLINED SHARPLY Y/Y

HEALTHY INCREASE IN ASIA PACIFIC PERFORMANCE,

WITH POSITIVE RESULTS IN AUSTRALIA/NEW ZEALAND

1Q13 1Q Y/Y 1Q Q/Q 1Q13 1Q Y/Y 1Q Q/Q

Scorecard ACV (€B)* Change Change Counts Change Change

Global Market € 3.1 -27% -24% 223 -24% -16%

New Scope € 1.7 -31% -37% 166 -22% -9%

Restructurings € 1.4 -22% 1% 57 -28% -30%

Mega-relationships € 1.0 54% 4% 7 -13% -79%

ITO € 1.9 -35% -28% 127 -34% -30%

BPO € 1.2 -10% -18% 96 -3% 16%

Americas € 1.2 -39% -15% 90 -38% -16%

EMEA € 1.5 -20% -30% 105 -15% -17%

Asia Pacific € 0.4 8% -23% 28 22% -7%

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

4

ACV of just over €4B was down 27% Y/Y and 24% Q/Q. However, the trailing 12-

month ACV was on par with the previous 12 month period, tempering results.

Broader Market ACV (€B)*

New Scope vs. Restructuring ACV(B)*

Broader Market Contract Award Trends

Broader Market Counts

223 264

292

349

259

Avg of Prior

1Qs

300

1Q134Q3Q2Q1Q124Q3Q2Q1Q114Q3Q2Q1Q10

€ 3.1€ 4.3€ 4.3

€ 4.9

Avg of Prior 1Qs

€ 4.5

1Q134Q3Q2Q1Q124Q3Q2Q1Q114Q3Q2Q1Q10

€ 1.7

€ 2.7 € 2.5

€ 3.2

€ 1.4 € 1.4 € 1.8

€ 1.1

1Q134Q3Q2Q1Q124Q3Q2Q1Q11

New Scope Restructuring

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

5

Mega-relationships, deals with ACV of €80M+, were up 54% Y/Y and 4% Q/Q. Mid to

small sized awards dipped, but the trailing 12-month compare was stable.

Mega-relationships in 8 Quarter Increments

New Scope vs. Restructuring Counts

Broader Market Contract Trends for the Largest Deals

ACV (€B)* by Bands

31

37

48

31

22

13

2Q11 - 1Q13

2Q09 - 1Q11

2Q07 - 1Q09

New Scope Restructuring

1.9

3.23.12.93.7

3.33.12.8

3.8

0.20.70.90.70.90.70.80.4

0.8

1.00.91.21.7

0.6

1.91.4

0.70.5

1Q134Q3Q2Q1Q124Q3Q2Q1Q11

€ 4 - 79M € 40-79M € 80M +

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

6

EMEA ACV of €1.5B was down 32% Q/Q and 21% Y/Y. Restructuring ACV grew

modestly while New Scope ACV fell sharply.

EMEA ACV (€B)*

EMEA New vs. Restructuring ACV(€B)*

EMEA Contract Award Trends

EMEA Counts by ACV Band

€ 1.5 € 2.2 € 2.3

€ 1.9 € 1.9

€ 3.0 € 2.5

€ 1.8 € 2.2

€ 2.8

€ 1.6 € 1.9

€ 2.4

Avg of Prior 1Qs

€ 2.2

1Q134Q3Q2Q1Q124Q3Q2Q1Q114Q3Q2Q1Q10

€ 0.74

€ 1.50

€ 1.31

€ 1.65

€ 0.75

€ 0.70 € 0.60 € 0.55

1Q134Q3Q2Q1Q124Q3Q2Q1Q11

New Scope Restructuring

81916982839796

76

129

212932213731212533

374538432

1Q134Q3Q2Q1Q124Q3Q2Q1Q11

€ 4 - 15M €16 - 79M € 80M +

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

7

The UK and DACH had weak 1Q13 results. However, Nordics and Benelux, held

steady.

EMEA Contract Award Trends Detail

EMEA Sub-region ACV (€B)* EMEA Industry ACV (€B)*

€ 0.72

€ 0.31 € 0.33

€ 0.29

€ 0.03

€ 0.09 € 0.08 € 0.05

€ 0.50

€ 0.22

€ 0.35

€ 0.30

€ 0.04

€ 0.02 € 0.05

€ 0.06

€ -

€ 0.1

€ 0.2

€ 0.3

€ 0.4

€ 0.5

€ 0.6

€ 0.7

€ 0.8

€ 0.9

UK &

Ireland

DACH Nordics Benelux France Southern

Europe

Africa &

Middle

East

E. Europe

& Russia

Prior 5 Like-Qtr Range Prior 5 Like-Qtr Avg 1Q12 1Q13

€ 0.54

€ 0.51

€ 0.34

€ 0.28

€ 0.24

€ 0.10

€ 0.05

€ 0.05

€ 0.37

€ 0.38

€ 0.33

€ 0.18

€ 0.06

€ 0.09

€ 0.06

€ 0.06

Manufacturing

Financial Services

Energy

Travel, Transport,

Leisure

Telecom & Media

Business Services

Retail

Healthcare &

Pharma

Prior 5 Like-Qtr Avg 1Q13

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

8

ITO ACV of €1.1B was down 15% Q/Q and 8% Y/Y. Contract numbers fell to their

lowest point since 4Q 2008.

EMEA ITO Annual ACV (€B)*

EMEA ITO New vs. Restructuring ACV (€B)*

EMEA ITO Contract Award Trends

€ 1.1 € 1.3 € 1.6

€ 1.1 € 1.2

€ 2.3 € 2.0

€ 1.2 € 1.6

€ 2.5

€ 1.2 € 1.7

€ 2.0

Avg of Prior Qs

€ 1.4

1Q134Q3Q2Q1Q124Q3Q2Q1Q114Q3Q2Q1Q10

EMEA ITO Counts

66

84

122

67

Avg of Prior

Qs

91

1Q134Q3Q2Q1Q124Q3Q2Q1Q114Q3Q2Q1Q10

€ 0.55

€ 0.82 € 0.80

€ 1.18

€ 1.10

€ 0.59

€ 0.45 € 0.45 € 0.43

€ 0.92

1Q134Q3Q2Q1Q124Q3Q2Q1Q114Q3Q2Q1Q10

New Scope Restructuring

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

9

While BPO contract numbers remained buoyant in the first quarter, ACV fell due to

the absence of large BPO deals in the region.

EMEA BPO Annual ACV (€B)*

EMEA BPO New vs. Restructuring ACV (€B)*

EMEA BPO Contract Award Trends

EMEA BPO Counts

39 39 39 42

29

Avg of Prior

1Qs

37

1Q134Q3Q2Q1Q124Q3Q2Q1Q114Q3Q2Q1Q10

€ 0.39

€ 0.93

€ 0.66 € 0.77

€ 0.66 € 0.66 € 0.54

€ 0.64 € 0.59

€ 0.30 € 0.41

€ 0.28 € 0.35

Avg of Prior 1Qs

€ 0.53

1Q134Q3Q2Q1Q124Q3Q2Q1Q114Q3Q2Q1Q10

€ 0.21

€ 0.68

€ 0.51 € 0.47

€ 0.25

€ 0.19

€ 0.25

€ 0.15 € 0.12 € 0.10

1Q134Q3Q2Q1Q124Q3Q2Q1Q114Q3Q2Q1Q10

New Scope Restructuring

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

10

The top service providers based on 1Q13 ACV or TTM ACV awarded

Top Service Providers in EMEA

Note: Service providers in alphabetical order; no rankings implied.

Placements based on ACV from commercial contract awards sourced from ISG Contracts Knowledgebase ®.

Accenture

AT&T

Atos

BT

Capgemini

CGI

CSC

Evry

HCL

HP

IBM

Infosys

ISS Global A/S

Jones Lang LaSalle

Mahindra Satyam

MITIE

Serco

TCS

T-Systems

Xchanging

Trailing 12 Months

EMEA Top 20

Accenture

AT&T

Capgemini

CGI

Communisis

Evry

Genpact

HCL

HP

Infosys

Lottomatica

Nokia

SQS

Swisscom

TCS

Thales

Tieto

Virtusa

Xchanging

Xerox

1Q13

EMEA Top 20

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

11

Americas ACV of €1.2B was down 39% Y/Y and 15% Q/Q. Americas BPO is up 17%

Y/Y and 50% Q/Q, outperforming the ITO sector for the first time.

Americas ACV (€B)*

Americas New vs. Restructuring ACV(€B)*

Americas Contract Award Trends

Americas ITO vs. BPO ACV (€B)*

€ 0.52

€ 0.99

€ 1.44

€ 0.87

€ 0.72

€ 0.49 € 0.63 € 0.74

1Q134Q3Q2Q1Q124Q3Q2Q1Q11

ITO ACV BPO ACV

€ 1.2€ 1.5€ 1.4€ 1.5

€ 2.1€ 1.8€ 1.6€ 1.4€ 1.6€ 0.9

€ 1.6€ 2.3€ 2.3

Avg of Prior 1Qs

€ 2.0

1Q134Q3Q2Q1Q124Q3Q2Q1Q114Q3Q2Q1Q10

€ 0.62

€ 0.95

€ 0.84

€ 1.11

€ 0.59 € 0.53

€ 1.23

€ 0.50

1Q134Q3Q2Q1Q124Q3Q2Q1Q11

New Scope Restructuring

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

12

The U.S. contributed most to the drop in the Americas ACV, down 43% Y/Y and 24%

Q/Q. Mexico continues to enjoy large-deal activity, boosting the ACV numbers.

Americas Contract Award Trends Detail

Americas Sub-region ACV (€B)* Americas Industry ACV (€B)*

€ 1.85

€ 1.08

€ -

€ 0.5

€ 1.0

€ 1.5

€ 2.0

€ 2.5

US

€ 0.19

€ 0.01

€ 0.02

€ -

€ 0.08

€ 0.02

€ 0.00

€ 0.08

€ -

€ 0.02

€ 0.04

€ 0.06

€ 0.08

€ 0.10

€ 0.12

€ 0.14

€ 0.16

€ 0.18

€ 0.20

Canada Brazil Other

LatAm

Mexico

Prior 5 Like-Qtr Range Prior 5 Like-Qtr Avg 1Q12 1Q13

€ 0.53

€ 0.30

€ 0.22

€ 0.20

€ 0.25

€ 0.10

€ 0.09

€ 0.09

€ 0.16

€ 0.28

€ 0.43

€ 0.09

€ 0.16

€ 0.02

€ 0.05

€ 0.07

Manufacturing

Financial Services

Telecom & Media

Business Services

Healthcare &

Pharma

Retail

Energy

Travel, Transport,

Leisure

Prior 5 Like-Qtr Avg 1Q13

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

13

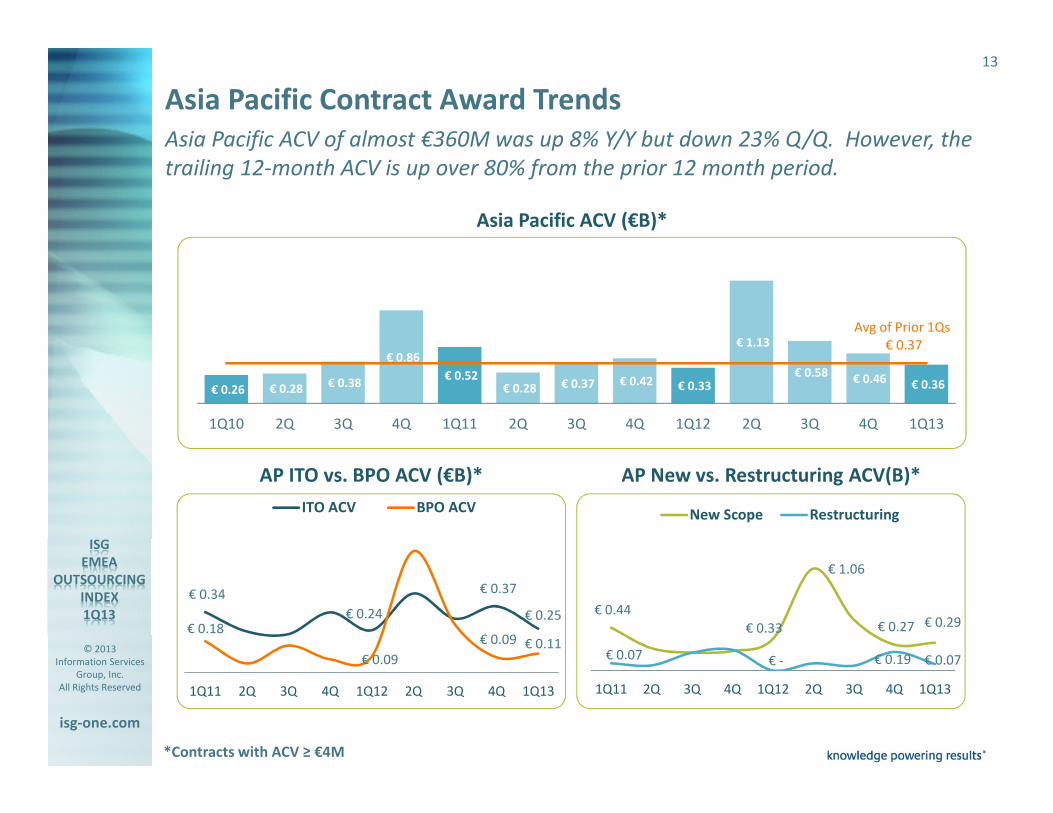

Asia Pacific ACV of almost €360M was up 8% Y/Y but down 23% Q/Q. However, the

trailing 12-month ACV is up over 80% from the prior 12 month period.

Asia Pacific ACV (€B)*

AP New vs. Restructuring ACV(B)*

Asia Pacific Contract Award Trends

AP ITO vs. BPO ACV (€B)*

€ 0.25

€ 0.37

€ 0.24

€ 0.34

€ 0.11 € 0.09

€ 0.09

€ 0.18

1Q134Q3Q2Q1Q124Q3Q2Q1Q11

ITO ACV BPO ACV

€ 0.29 € 0.27

€ 1.06

€ 0.33

€ 0.44

€ 0.07 € 0.19 € -€ 0.07

1Q134Q3Q2Q1Q124Q3Q2Q1Q11

New Scope Restructuring

€ 0.36 € 0.46 € 0.58

€ 1.13

€ 0.33 € 0.42 € 0.37 € 0.28 € 0.52

€ 0.86

€ 0.38 € 0.28 € 0.26

Avg of Prior 1Qs

€ 0.37

1Q134Q3Q2Q1Q124Q3Q2Q1Q114Q3Q2Q1Q10

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

14

Australia/New Zealand and Japan posted positive results due to several large

awards. Energy and Travel & Transport were up over historical averages.

Asia Pacific Contract Award Trends Detail

Asia Pacific Sub-region ACV (€B)* AP Industry ACV (€B)*

€ 0.08

€ 0.05

€ 0.11

€ 0.03

€ 0.06

€ -

€ 0.12

€ 0.07

€ 0.14

€ 0.01 € 0.01

€ -

€ 0.05

€ 0.10

€ 0.15

€ 0.20

€ 0.25

ANZ India and

South Asia

Japan ASEAN Greater

China

South Korea

Prior 5 Like-Qtr Range Prior 5 Like-Qtr Avg 1Q12 1Q13

€ 0.09

€ 0.09

€ 0.07

€ 0.04

€ 0.02

€ 0.02

€ 0.01

€ 0.001

€ 0.01

€ 0.07

€ 0.05

€ 0.08

€ 0.13

€ 0.00

€ 0.00

€ -

Telecom &

Media

Manufacturing

Financial

Services

Travel,

Transport,

Leisure

Energy

Business

Services

Retail

Healthcare &

Pharma

Prior 5 Like-Qtr Avg 1Q13

Special Topic for First Quarter 2013

John KeppelPresident & Chief

Marketing Officer

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

16

Western-heritage Providers

Leading Providers Experience Shift in Market Share

13%

12%

ACV

Awards

Awards

ACV

Market Share Shifts 2009 - 2012

India-heritage Providers

9%

7%

CAGR Disparity

2005 - 2012

India-heritage

�32%

�16%

�7%�0.4%

Western-heritage

2005 2009 2012

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

17

3Make New Inroads into the Global Public Sector Markets

13%

Opportunities and Challenges for Short-term Growth

Continue Winning in the MatureUK and US Restructuring Markets

4%

20%

2005 2009 2012

Increase European Market Sharevia Enhanced Offshore Value Prop

India-heritage Restructuring ACV Market Share

1

7%

2005-08 2009-12

Capitalize on BPO Growth via Investment in Vertical Solutions

India-heritage EuropeanACV Market Share

India-heritage BPO ACVMarket Share

16%

36%

2005 2009 2012

$$$$

4

2

$$$$ $$$

Investment Investment

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

18

Staying Ahead: What got you here will not get you there.

Long-term, the best defense may be a good offense, a challenge for western

providers with high overhead, India-heritage providers need long-term growth

engines to stay on trajectory.

Capturing the Expected Growth in the Mid-Market� India-heritage Providers have proven offshoring credentials

� Western providers have started to create dedicated mid-market organizations

Lower Cost of Switching Puts Everybody on Notice � Equal threat to all providers, no matter their heritage

� Incumbency advantage disappearing as transitions become less painful

ITO ChallengeGet familiar with the new buyers of emerging technologies, who sit outside

the CIO’s organization.

BPO Challenge Pay for performance, rather than for bodies, is becoming the norm. Pricing

based on labor mark-up is becoming less attractive.€

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

19

� Market continues to struggle to regain traction with soft spots in ACV

smaller deal space and in New Scope

� ITO performance is weak and BPO remains the bright spot

� Trailing 12 months is encouraging and the Mega-relationship market

was strong

� EMEA New Scope activity fell unexpectedly but restructurings rose.

Financial Services was off and BPO ACV fell while contract awards

remained strong

� Americas saw decline in the US market and a low number of ITO

contracts. BPO gains rise above ITO in the region.

� Asia Pacific held steady, with ACV and activity increasing Y/Y, and

positive results in Australia/New Zealand.

� Keep expectations in check for 2Q13 with softness in the overall market

� Positive signs point to a healthier outlook for the full year

� Strength in BPO

� Positivity in the emerging markets in the last 12 months

� Impact of timing on deal flow should eventually rebound

1Q13 ISG Outsourcing Index Summary and Outlook

summarymarket

outlookmarket

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

20

Please contact us with your questions and comments.

Learn More

--- Media Contacts ---

► John Keppel

President & Chief Marketing Officer

+44 (0)7879 432 212

blog.isg-one.com

► Denise Colgan

Marketing Director, EMEA, ISG

+44 1737 371523

► Louise Fernley

Cohn & Wolfe for ISG

+44 207 331 5365

First Quarter 2013

© 2013

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M

22

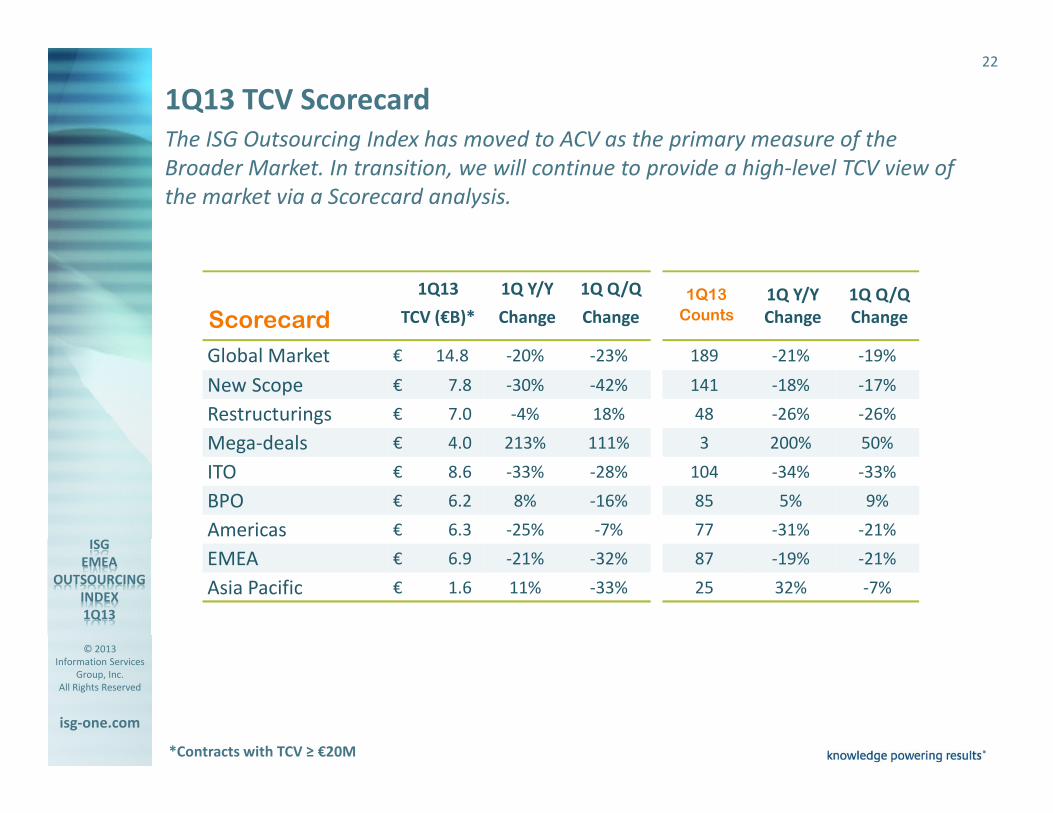

The ISG Outsourcing Index has moved to ACV as the primary measure of the

Broader Market. In transition, we will continue to provide a high-level TCV view of

the market via a Scorecard analysis.

1Q13 TCV Scorecard

*Contracts with TCV ≥ €20M

1Q13 1Q Y/Y 1Q Q/Q Counts Change Change

189 -21% -19%

141 -18% -17%

48 -26% -26%

3 200% 50%

104 -34% -33%

85 5% 9%

77 -31% -21%

87 -19% -21%

25 32% -7%

1Q13 1Q Y/Y 1Q Q/Q

Scorecard TCV (€B)* Change Change

Global Market € 14.8 -20% -23%

New Scope € 7.8 -30% -42%

Restructurings € 7.0 -4% 18%

Mega-deals € 4.0 213% 111%

ITO € 8.6 -33% -28%

BPO € 6.2 8% -16%

Americas € 6.3 -25% -7%

EMEA € 6.9 -21% -32%

Asia Pacific € 1.6 11% -33%

www.isg-one.com

Information Services Group is a leading technology insights, market intelligence and advisory services company, serving more

than 450 clients around the world to help them achieve operational excellence. ISG supports private and public sector

organizations to transform and optimize their operational environments through research, benchmarking, consulting and

managed services, with a focus on information technology, business process transformation, program management services and

enterprise resource planning. Clients look to ISG for unique insights and innovative solutions for leveraging technology, the

deepest data source in the industry, and more than five decades of experience of global leadership in information and advisory

services. Based in Stamford, Conn., the company has more than 800 employees and operates in 21 countries.

knowledge powering results®