Embed Size (px)

Citation preview

Marcelo Pereira de CarvalhoCEO - AgriPoint

9 de maio de 2014

What will be the role of Brazil in

the coming years?

AgriPoint

A company in the information business for agricultural sectors, with dairying being the main area.

Our services/products for the dairy sector

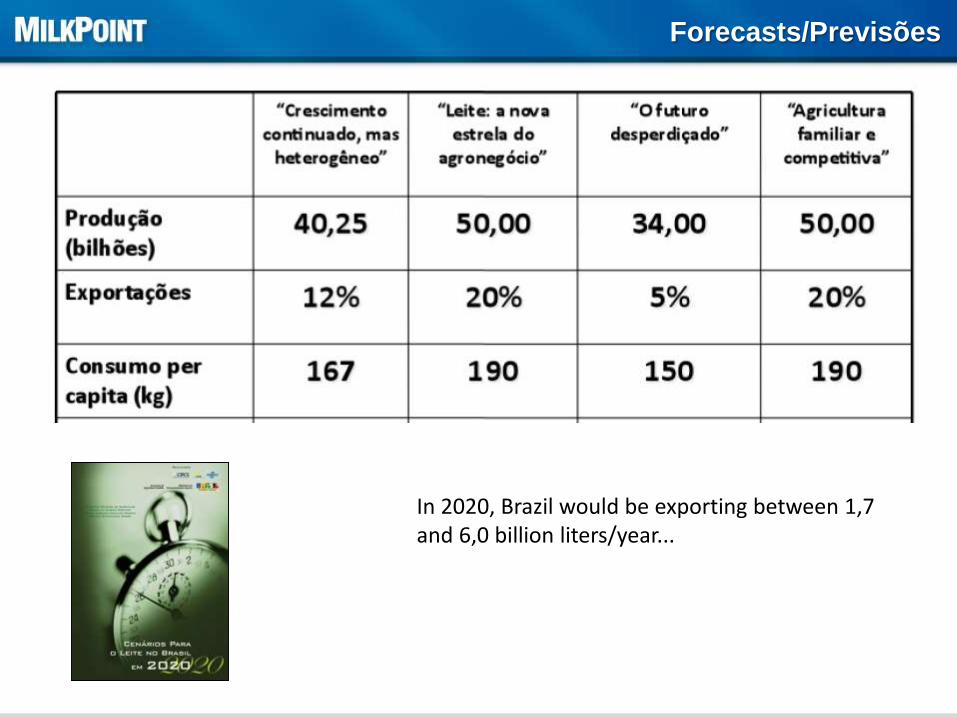

Forecasts/Previsões

Forecasts/Previsões

In 2020, Brazil would be exporting between 1,7 and 6,0 billion liters/year...

It’s not east to make forecasts...

• The time frame they are done affect our

perceptions and therefore the results

• Many different and uncontrollable variables

• We live in a moment of significant changes

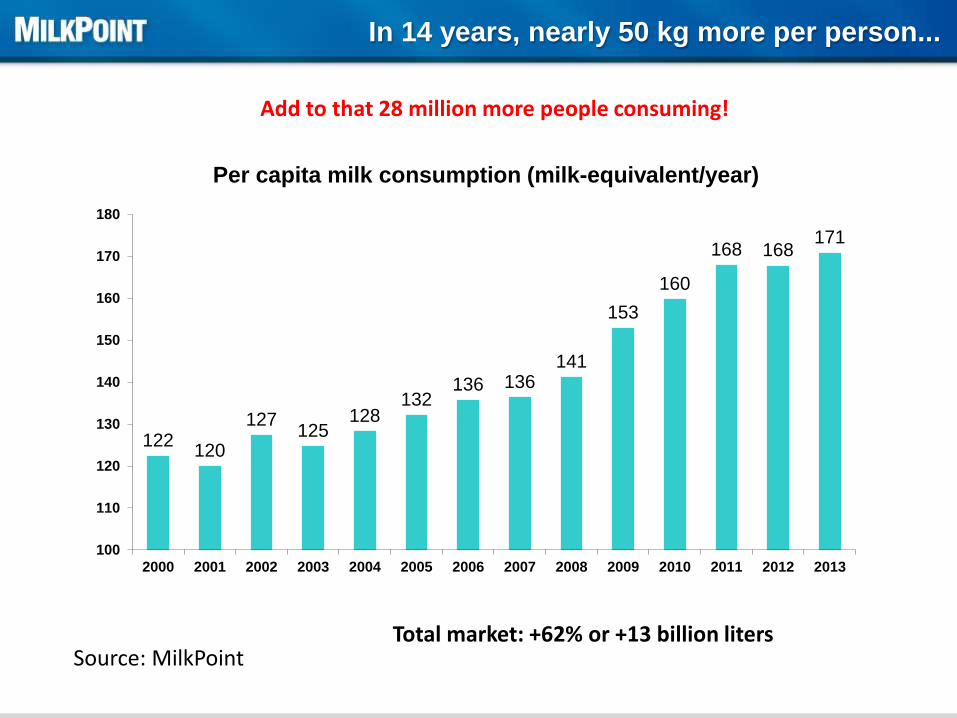

In 14 years, nearly 50 kg more per person...

122120

127125

128132

136 136141

153

160

168 168171

100

110

120

130

140

150

160

170

180

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Per capita milk consumption (milk-equivalent/year)

Source: MilkPoint

Add to that 28 million more people consuming!

Total market: +62% or +13 billion liters

Market growth dynamics

3.12%

2.26%

1.64%1.46%

3.18%3.13%

5.56%

1.34%

1.76%

4.27%

4.42%

5.08%

1.01%

3.38%

4.02%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

1989-2000

2001-2006

2007-2013

Source: MilkPoint

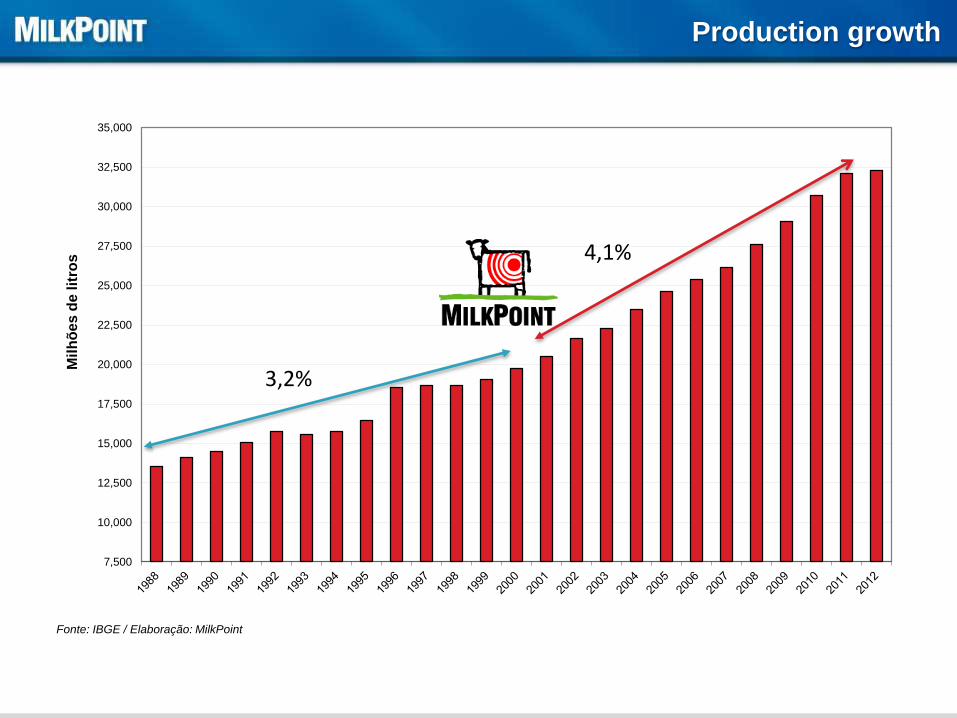

Production growth

7,500

10,000

12,500

15,000

17,500

20,000

22,500

25,000

27,500

30,000

32,500

35,000

Mil

hõ

es d

e lit

ros

Fonte: IBGE / Elaboração: MilkPoint

4,1%

3,2%

How much of our consumption is produced internally

88%

90%

92%

94%

96%

98%

100%

102%

104%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Self-sufficiency Index (production/consumption)

Source: MilkPoint

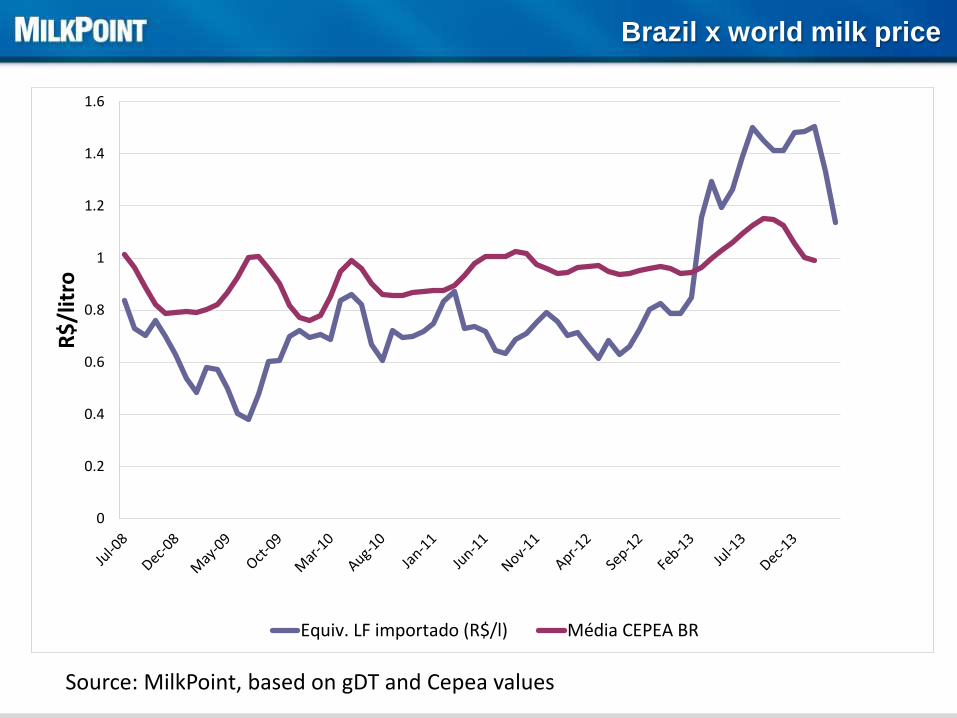

Can Brazil be considered a structural importer?

Brazil x world milk price

Source: MilkPoint, based on gDT and Cepea values

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

R$

/lit

ro

Equiv. LF importado (R$/l) Média CEPEA BR

• Trade policy: 27% tax for WMP distort the

market – will it be kept?

• No clear trend regarding being either a large

importer or a large exporter

• Exchange rates and world prices impact this

status

Brazil’s role regarding dairy trade

• Consumption will growth less in the future

• Production will also growth less in the next

years

What can we expect?

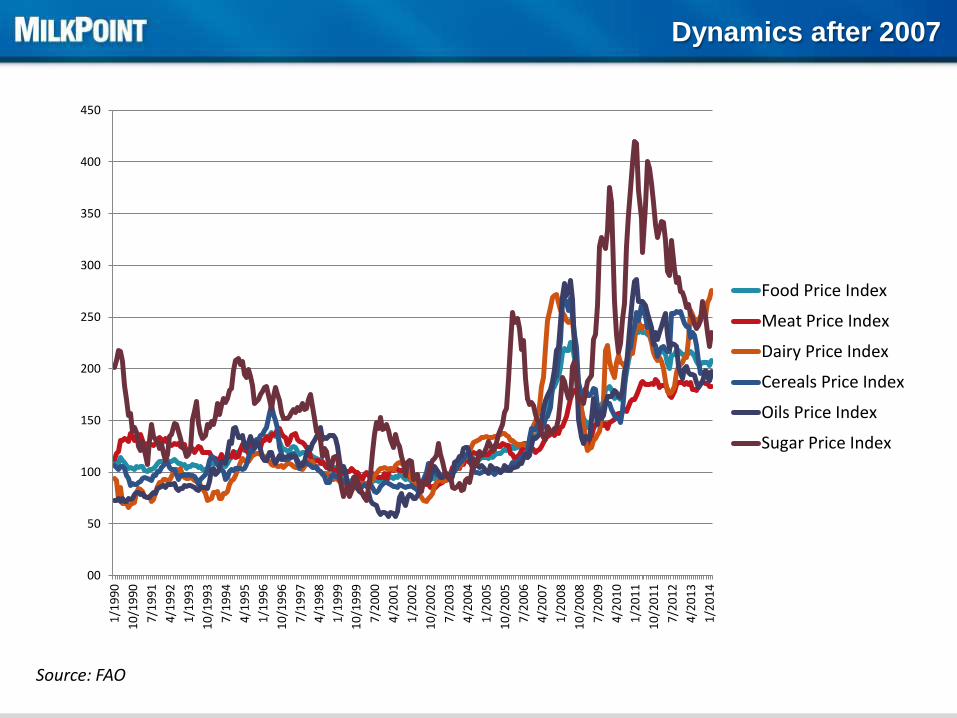

But important changes are happening

Dynamics after 2007

00

50

100

150

200

250

300

350

400

4501

/19

90

10

/19

90

7/1

99

1

4/1

99

2

1/1

99

3

10

/19

93

7/1

99

4

4/1

99

5

1/1

99

6

10

/19

96

7/1

99

7

4/1

99

8

1/1

99

9

10

/19

99

7/2

00

0

4/2

00

1

1/2

00

2

10

/20

02

7/2

00

3

4/2

00

4

1/2

00

5

10

/20

05

7/2

00

6

4/2

00

7

1/2

00

8

10

/20

08

7/2

00

9

4/2

01

0

1/2

01

1

10

/20

11

7/2

01

2

4/2

01

3

1/2

01

4

Food Price Index

Meat Price Index

Dairy Price Index

Cereals Price Index

Oils Price Index

Sugar Price Index

Source: FAO

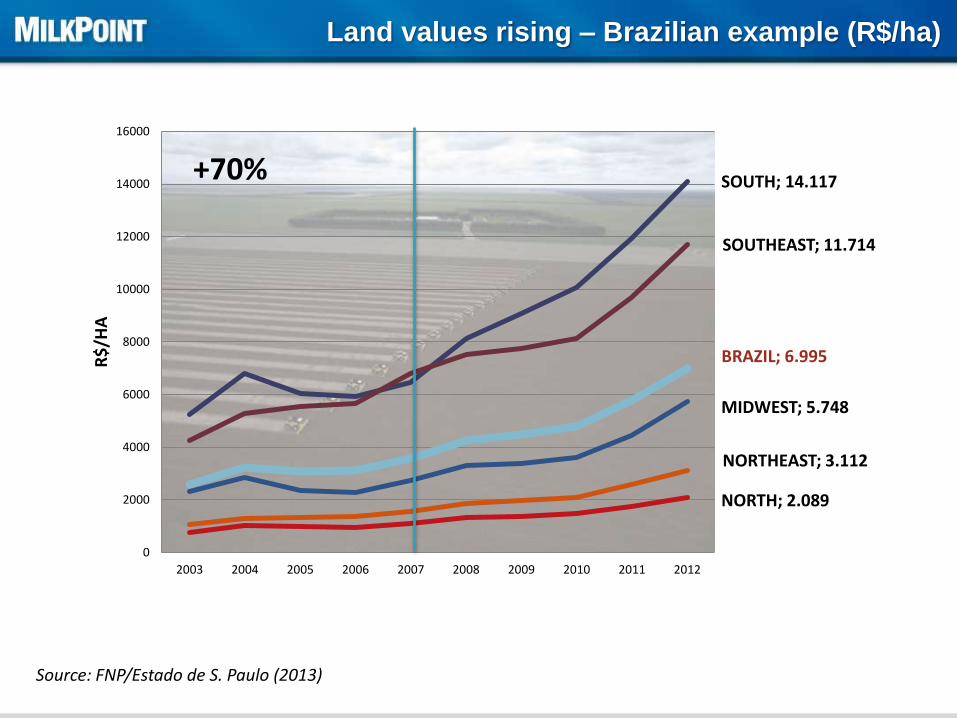

Land values rising – Brazilian example (R$/ha)

Source: FNP/Estado de S. Paulo (2013)

NORTH; 2.089

NORTHEAST; 3.112

MIDWEST; 5.748

SOUTH; 14.117

SOUTHEAST; 11.714

BRAZIL; 6.995

0

2000

4000

6000

8000

10000

12000

14000

16000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

R$

/HA

+70%

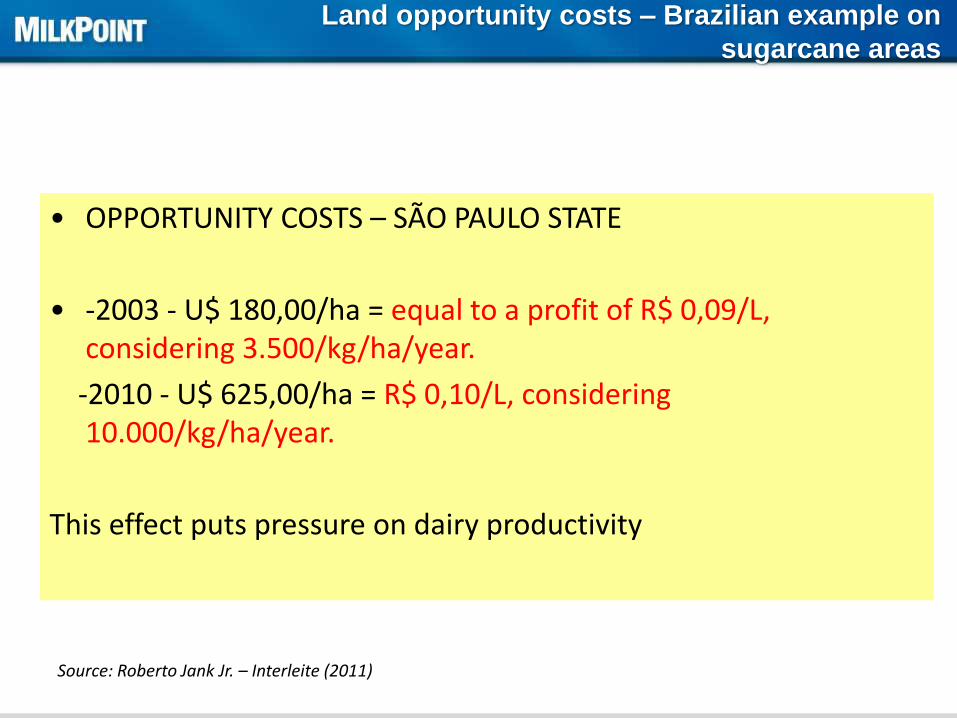

Land opportunity costs – Brazilian example on

sugarcane areas

• OPPORTUNITY COSTS – SÃO PAULO STATE

• -2003 - U$ 180,00/ha = equal to a profit of R$ 0,09/L, considering 3.500/kg/ha/year.

-2010 - U$ 625,00/ha = R$ 0,10/L, considering 10.000/kg/ha/year.

This effect puts pressure on dairy productivity

Source: Roberto Jank Jr. – Interleite (2011)

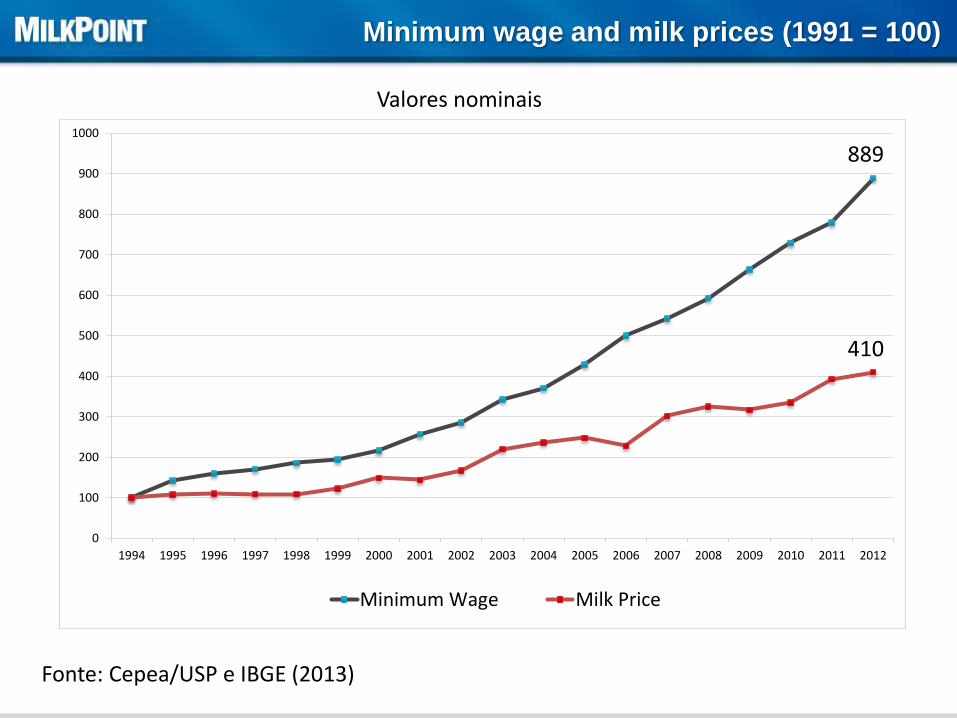

Fonte: Cepea/USP e IBGE (2013)

Minimum wage and milk prices (1991 = 100)

779

393

Valores nominais

0

100

200

300

400

500

600

700

800

900

1000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Minimum Wage Milk Price

410

889

Growing interest on robot milking

Survey on number/profile of dairy producers

• 48 dairy companies

• June/July 2013

• 17,5 million liters/day

• 30% of inspected production

Survey on number/profile of dairy producers

Considering total inspected production

Number of Producers Volume

Ranges liters/day Number % Liters/day %

Up to 250 168.463 67% 14.062.050 23%

250-500 46.637 19% 12.679.935 21%

500-1000 22.668 9,0% 12.432.707 20%

1000-3000 10.821 4,3% 13.668.693 22%

More than 3000 2.194 0,9% 8.357.996 14%

Total 250.782 100% 61.201.381 100%

Average: 249 kg/day

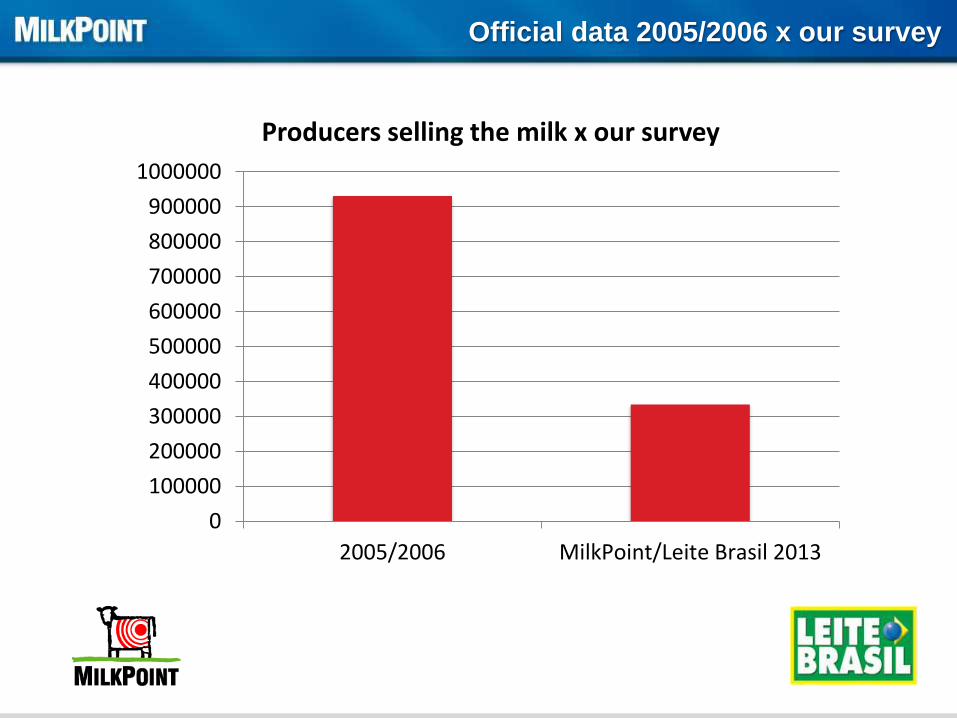

Official data 2005/2006 x our survey

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

2005/2006 MilkPoint/Leite Brasil 2013

Producers selling the milk x our survey

Official data 2005/2006 x our survey

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

2005/2006 MilkPoint/Leite Brasil 2013

Producers selling the milk x our survey

Every 6 minutes a producer left the

business!

• Population income raised and unemployment rate fell steadily to

less that 5% higher consumption but also labor and sucession

challenges in farms

• Higher land opportunity costs improve productivity or leave

• Investments in processing capacity aiming domestic market

and exports

• Import tax shielded (to some extent) Brazilian market to what was

happening in the world artificially high internal prices

• But production lagged behind consumption market were tight

and industries were pressured

Dynamics after 2007

0.500

0.600

0.700

0.800

0.900

1.000

1.100

1.200

1.300

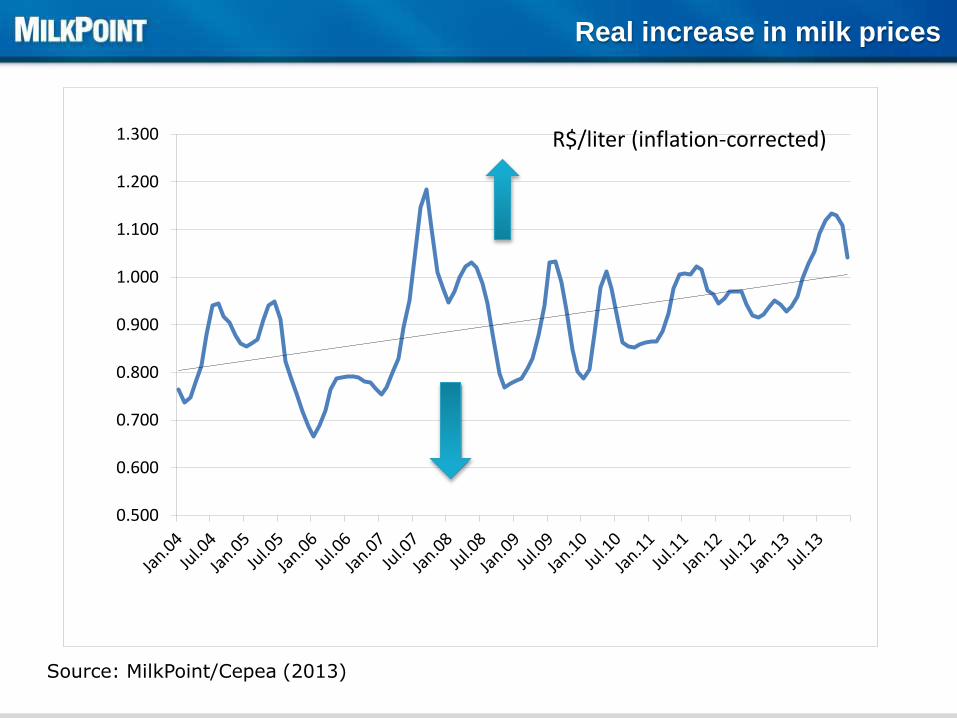

Real increase in milk prices

Source: MilkPoint/Cepea (2013)

R$/liter (inflation-corrected)

• Averages hide a big range in prices received by dairy farmers

• Within the same region, there may be producers getting R$

0,80/liter up to R$ 1,30/liter

– Volume

– Quality

– Influence, etc

• Are they in the same business?

• Efficient large farmers do have a good business!

Dynamics after 2007

Top 100 grew nearly 10% in 2013

New investments going on – Southeast Brazil

New investments going on – Midwest Brazil

New investments going on – Northeast Brazil

Progressive producers – South Brazil

Midwest Brazil

South Brazil

Small producers with family labour also growing

Small producers with family labour also growing

•How long it will last for?

But...

Real retail prices for a mix of dairy products

0.00

0.50

1.00

1.50

2.00

2.50

3.00

1.9

.06

1.1

1.0

6

1.1

.07

1.3

.07

1.5

.07

1.7

.07

1.9

.07

1.1

1.0

7

1.1

.08

1.3

.08

1.5

.08

1.7

.08

1.9

.08

1.1

1.0

8

1.1

.09

1.3

.09

1.5

.09

1.7

.09

1.9

.09

1.1

1.0

9

1.1

.10

1.3

.10

1.5

.10

1.7

.10

1.9

.10

1.1

1.1

0

1.1

.11

1.3

.11

1.5

.11

1.7

.11

1.9

.11

1.1

1.1

1

1.1

.12

1.3

.12

1.5

.12

1.7

.12

1.9

.12

1.1

1.1

2

1.1

.13

1.3

.13

1.5

.13

1.7

.13

1.9

.13

1.1

1.1

3

Composto Varejo Composto Indústria ProdutorFonte: CEPEA, MilkPoint; Elaboração: MilkPoint

R$/liter – inflation corrected

Industry lost margin to producers and retailers

0.93

0.86 0.86

0.95 0.94

1.04

0.760.78 0.77

0.670.62

0.71

0.610.64

0.590.64

0.71

0.75

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

2008 2009 2010 2011 2012 2013

% Produtor

% Indústria

% Varejo

Fonte: CEPEA e MilkPoint (2013)

Inflation-corrected values for a mix of UHT, pasteurized, powder milk and cheese

Some relevant processors facing problems

Solvency problems

Coop sold 50% to Vigor -JBS

Board authorized to sell dairy assets

New players studying Brazil, but only a minor deal ocurred

What to expect?

• Large price ranges will continue

• This, coupled with opportunity costs, will lead to a

structural change in production

• Many will leave the business, but production will keep

growing

• How many will be producing milk in 10 years? Good

question!

• Production will grow less – 2-3% in average, compared

to >4% from 2007-2013

• Brazil will still be an opportunistic exporter and a minor

importer, unless...

• Import taxes are removed (if so, the change will be more

dramatic and faster!)

What to expect?

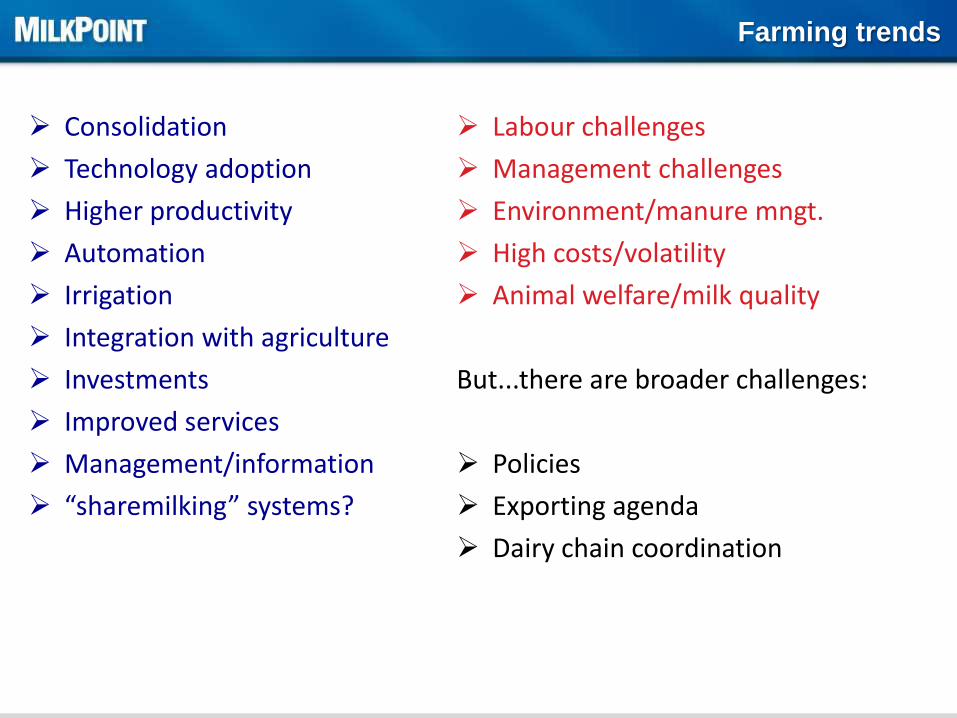

Farming trends

Consolidation

Technology adoption

Higher productivity

Automation

Irrigation

Integration with agriculture

Investments

Improved services

Management/information

“sharemilking” systems?

Labour challenges

Management challenges

Environment/manure mngt.

High costs/volatility

Animal welfare/milk quality

But...there are broader challenges:

Policies

Exporting agenda

Dairy chain coordination