Embed Size (px)

Citation preview

1

Connected Living 2020Future of Smart Homes, Virtual Work, and Connected Cities

2

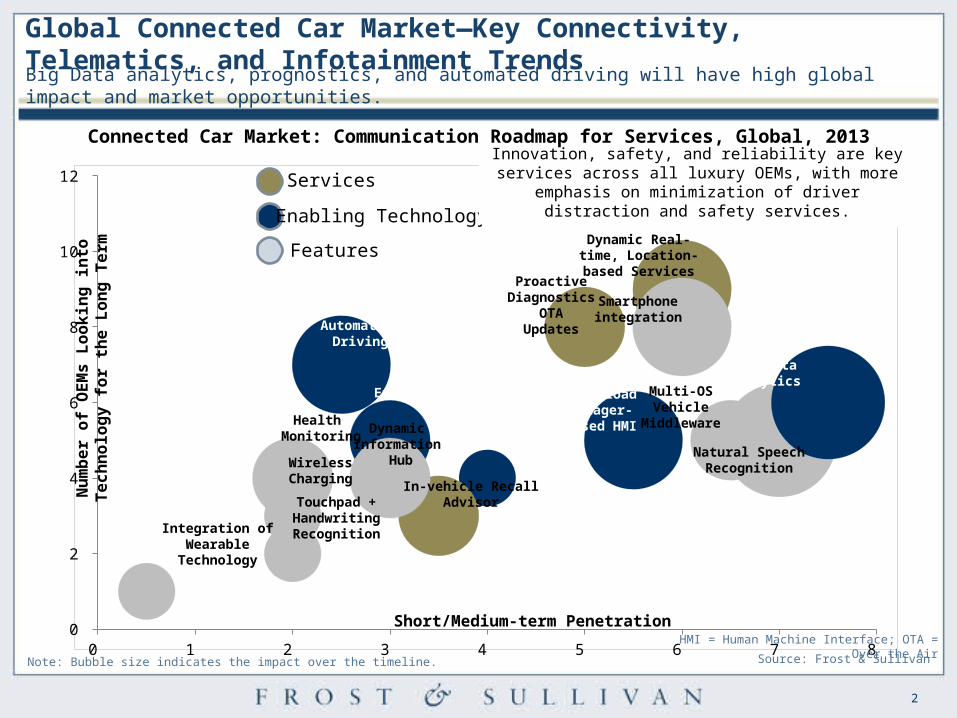

0 1 2 3 4 5 6 7 8 0

2

4

6

8

10

12

Short/Medium-term Penetration

Num

ber o

f OEM

s Lo

okin

g in

toTe

chno

logy

for t

he L

ong

Term

Proactive Diagnostics

OTAUpdates

Dynamic Real-time, Location-based

Services

Big DataAnalytics

Natural Speech Recognition

Multi-OSVehicle

MiddlewareGesture Controls

Automated Driving

In-vehicle RecallAdvisor

Dynamic Information

Hub

Ethernet

Health Monitoring

WirelessCharging

Touchpad + Handwriting RecognitionIntegration of

Wearable Technology

Work load manager-based HMI

Smartphone integration

Services

Features

Enabling Technology

Innovation, safety, and reliability are key services across all luxury OEMs, with more emphasis on minimization of

driver distraction and safety services.

Connected Car Market: Communication Roadmap for Services, Global, 2013

Note: Bubble size indicates the impact over the timeline.

HMI = Human Machine Interface; OTA = Over the Air

Global Connected Car Market—Key Connectivity, Telematics, and Infotainment TrendsBig Data analytics, prognostics, and automated driving will have high global impact and market opportunities.

Source: Frost & Sullivan

3

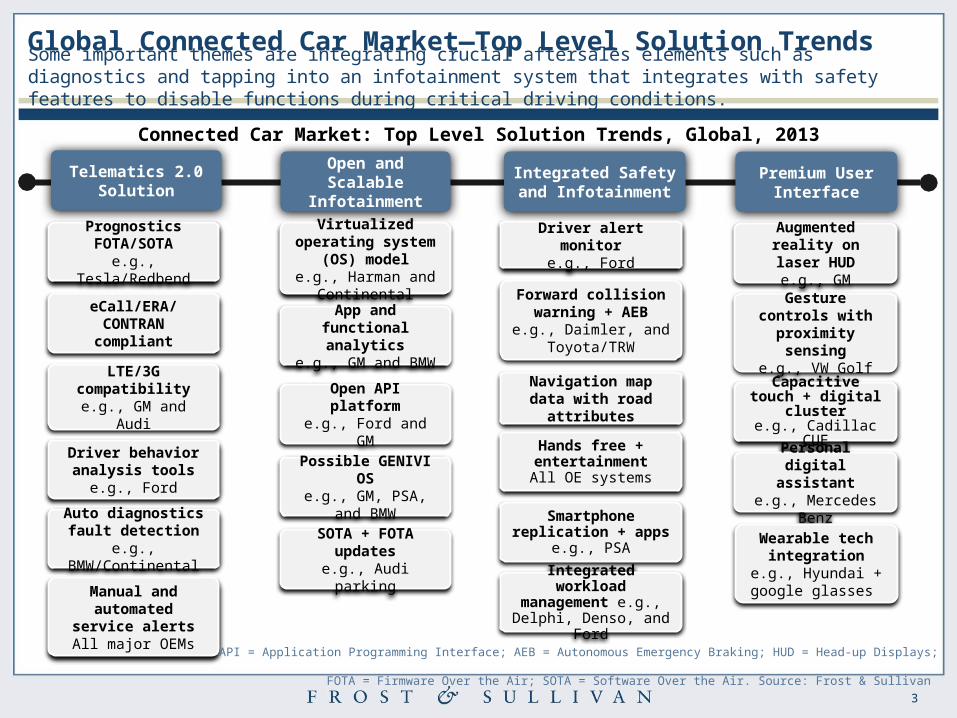

Telematics 2.0 Solution

Open and Scalable Infotainment

Premium User Interface

Integrated Safety and Infotainment

PrognosticsFOTA/SOTA

e.g., Tesla/Redbend

LTE/3G compatibilitye.g., GM and Audi

Driver behavior analysis tools

e.g., Ford

Virtualized operating system (OS) model

e.g., Harman and Continental

App and functional analytics

e.g., GM and BMW

Augmented reality on laser HUD

e.g., GM

Capacitive touch + digital cluster

e.g., Cadillac CUE

Driver alert monitore.g., Ford

Forward collision warning + AEB

e.g., Daimler, and Toyota/TRW

Navigation map data with road attributesOpen API platform

e.g., Ford and GMHands free +

entertainmentAll OE systemsPossible GENIVI OS

e.g., GM, PSA, and BMW

eCall/ERA/CONTRAN compliant

Gesture controls with proximity

sensinge.g., VW Golf

SOTA + FOTA updates

e.g., Audi parking

Auto diagnostics fault detection

e.g., BMW/Continental

Manual and automated service

alertsAll major OEMs

Smartphone replication + apps

e.g., PSA

Integrated workload management e.g.,

Delphi, Denso, and Ford

Personal digital assistant

e.g., Mercedes Benz

Wearable tech integration

e.g., Hyundai + google glasses

Global Connected Car Market—Top Level Solution TrendsSome important themes are integrating crucial aftersales elements such as diagnostics and tapping into an infotainment system that integrates with safety features to disable functions during critical driving conditions.

API = Application Programming Interface; AEB = Autonomous Emergency Braking; HUD = Head-up Displays; FOTA = Firmware Over the Air; SOTA = Software Over the Air. Source: Frost & Sullivan

Connected Car Market: Top Level Solution Trends, Global, 2013

4

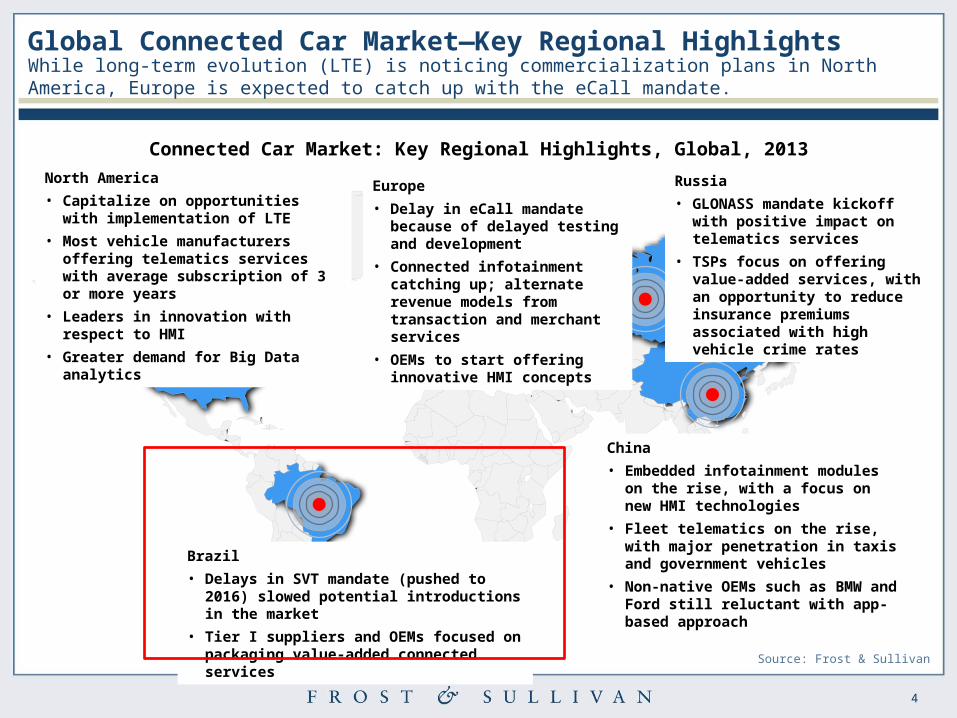

Connected Car Market: Key Regional Highlights, Global, 2013

Global Connected Car Market—Key Regional HighlightsWhile long-term evolution (LTE) is noticing commercialization plans in North America, Europe is expected to catch up with the eCall mandate.

North America• Capitalize on opportunities with

implementation of LTE• Most vehicle manufacturers offering

telematics services with average subscription of 3 or more years

• Leaders in innovation with respect to HMI

• Greater demand for Big Data analytics

Europe• Delay in eCall mandate because

of delayed testing and development

• Connected infotainment catching up; alternate revenue models from transaction and merchant services

• OEMs to start offering innovative HMI concepts

Russia• GLONASS mandate kickoff with

positive impact on telematics services

• TSPs focus on offering value-added services, with an opportunity to reduce insurance premiums associated with high vehicle crime rates

China• Embedded infotainment modules on

the rise, with a focus on new HMI technologies

• Fleet telematics on the rise, with major penetration in taxis and government vehicles

• Non-native OEMs such as BMW and Ford still reluctant with app-based approach

Brazil• Delays in SVT mandate (pushed to 2016)

slowed potential introductions in the market• Tier I suppliers and OEMs focused on

packaging value-added connected servicesSource: Frost & Sullivan

5

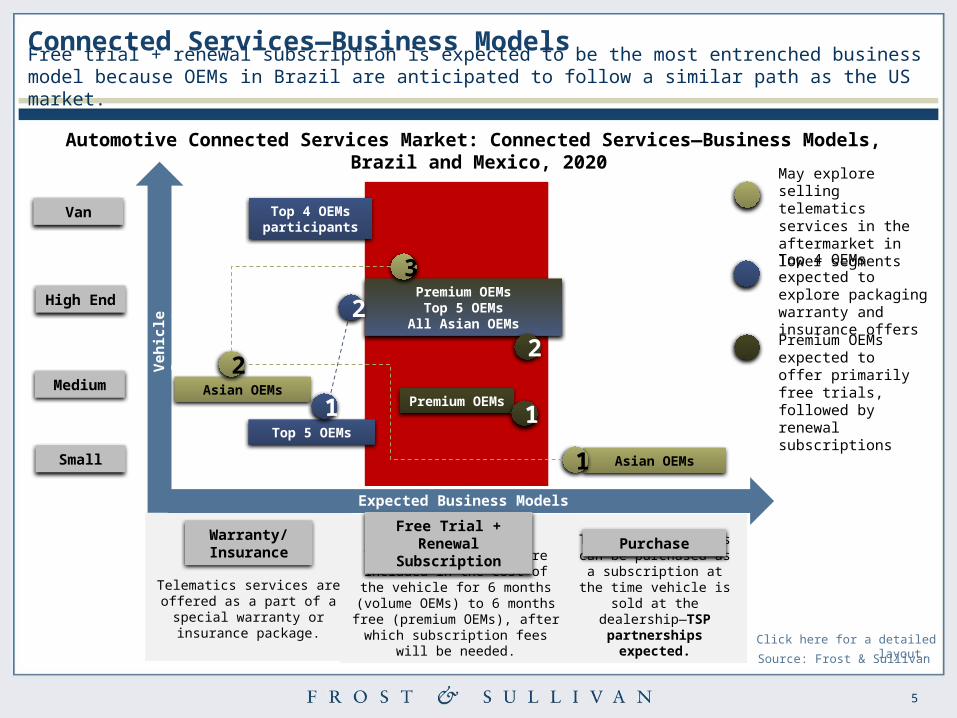

Telematics services can be purchased as a subscription at the time vehicle is sold at

the dealership—TSP partnerships expected.

Telematics services are included in the cost of the vehicle for 6 months (volume OEMs) to 6 months free

(premium OEMs), after which subscription fees will be needed.

Telematics services are offered as a part of a special warranty

or insurance package. Click here for a detailed layout.

Warranty/ Insurance

Free Trial + Renewal Subscription Purchase

Expected Business Models

Vehi

cle

Segm

ent

Small

High End

Van

Top 5 OEMs

Premium OEMsTop 5 OEMs

All Asian OEMs

Asian OEMs

Asian OEMs

Top 4 OEMs participants

Premium OEMs

Medium

1

2

3

1

2

1

2

Automotive Connected Services Market: Connected Services—Business Models, Brazil and Mexico, 2020

Premium OEMs expected to offer primarily free trials, followed by renewal subscriptions

May explore selling telematics services in the aftermarket in lower segments

Top 4 OEMs expected to explore packaging warranty and insurance offers

Connected Services—Business ModelsFree trial + renewal subscription is expected to be the most entrenched business model because OEMs in Brazil are anticipated to follow a similar path as the US market.

Source: Frost & Sullivan

6

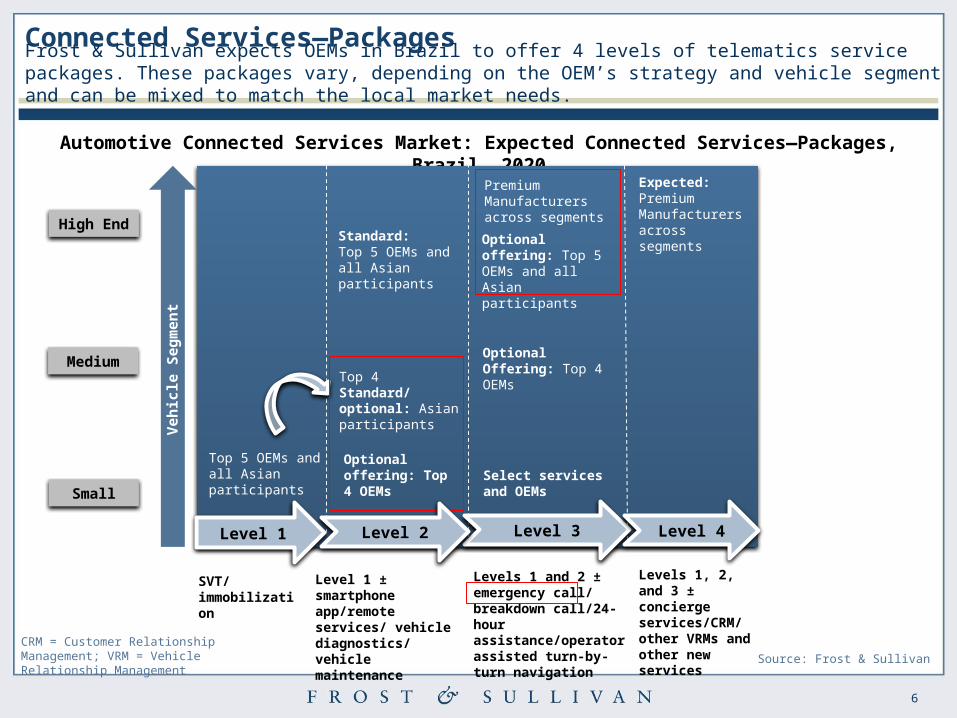

Automotive Connected Services Market: Expected Connected Services—Packages, Brazil, 2020

SVT/ immobilization

Level 1 ± smartphone app/remote services/ vehicle diagnostics/ vehicle maintenance

Levels 1 and 2 ± emergency call/breakdown call/24-hour assistance/operator assisted turn-by-turn navigation

Levels 1, 2, and 3 ± concierge services/CRM/ other VRMs and other new services

Vehi

cle

Segm

ent

Small

High End

Medium

Top 5 OEMs and all Asian participants

Premium Manufacturers across segments

Level 1 Level 3 Level 4

Top 4Standard/optional: Asian participants

Optional offering: Top 4 OEMs

Optional Offering: Top 4 OEMs

Expected: Premium Manufacturers across segmentsOptional offering: Top

5 OEMs and all Asian participants

Level 2

Standard:Top 5 OEMs and all Asian participants

Connected Services—PackagesFrost & Sullivan expects OEMs in Brazil to offer 4 levels of telematics service packages. These packages vary, depending on the OEM’s strategy and vehicle segment and can be mixed to match the local market needs.

CRM = Customer Relationship Management; VRM = Vehicle Relationship Management Source: Frost & Sullivan

Select services and OEMs

7

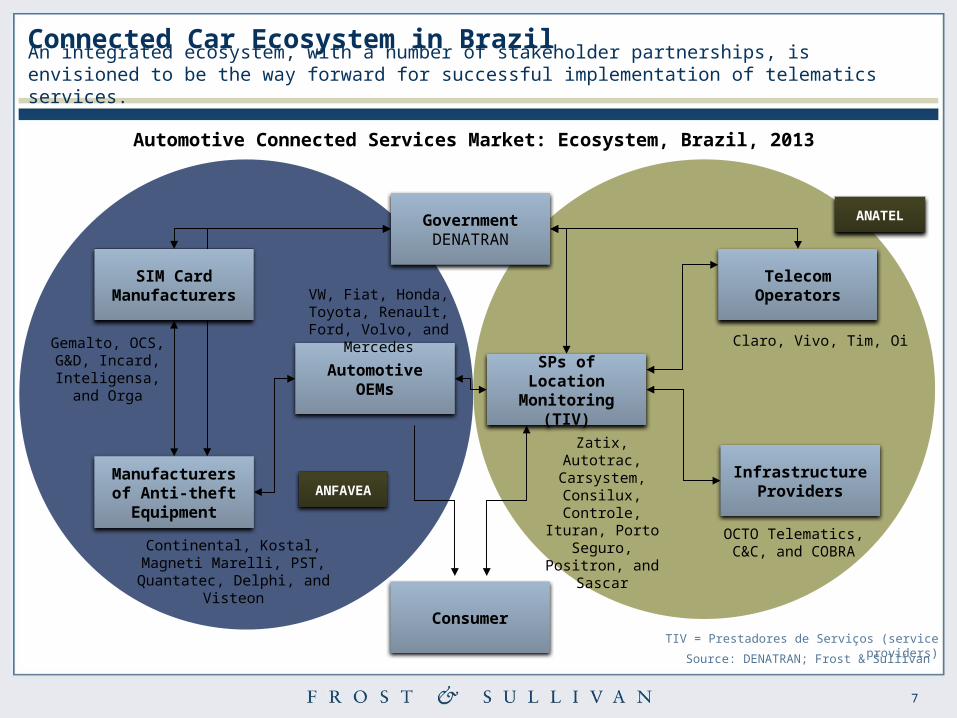

Manufacturers of Anti-theft

Equipment

Automotive OEMs SPs of Location Monitoring (TIV)

Infrastructure Providers

Telecom Operators

Consumer

GovernmentDENATRAN

SIM Card Manufacturers

Gemalto, OCS, G&D, Incard,

Inteligensa, and Orga

Continental, Kostal, Magneti Marelli, PST, Quantatec,

Delphi, and Visteon

VW, Fiat, Honda, Toyota, Renault, Ford, Volvo,

and MercedesClaro, Vivo, Tim, Oi

OCTO Telematics, C&C, and COBRA

Zatix, Autotrac, Carsystem,

Consilux, Controle, Ituran, Porto

Seguro, Positron, and Sascar

ANATEL

ANFAVEA

Automotive Connected Services Market: Ecosystem, Brazil, 2013

TIV = Prestadores de Serviços (service providers)

Connected Car Ecosystem in BrazilAn integrated ecosystem, with a number of stakeholder partnerships, is envisioned to be the way forward for successful implementation of telematics services.

Source: DENATRAN; Frost & Sullivan

8

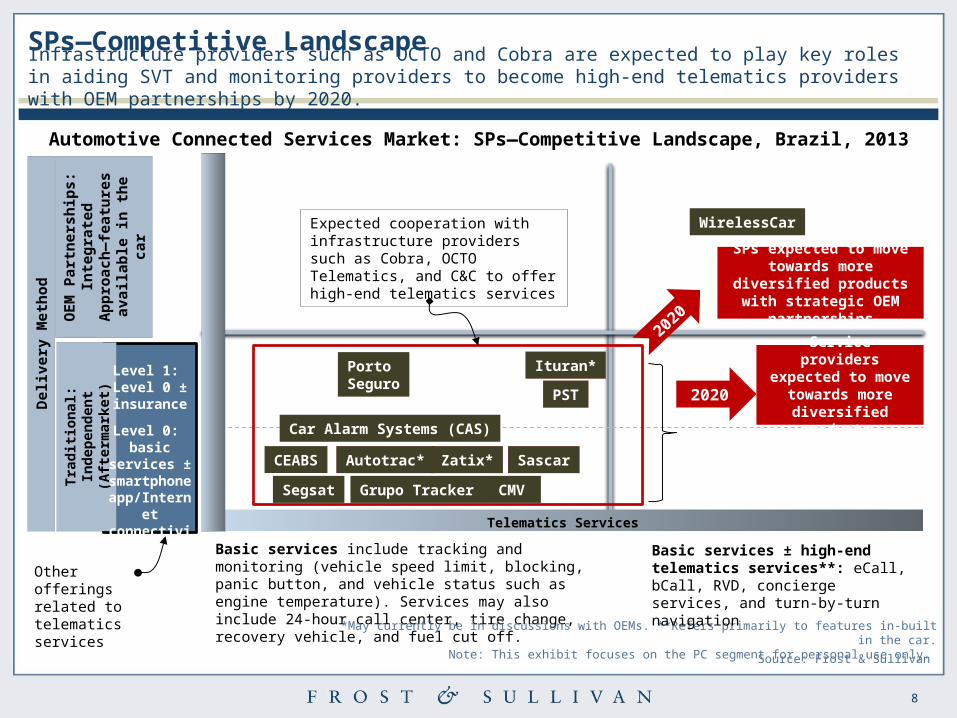

Telematics Services

Automotive Connected Services Market: SPs—Competitive Landscape, Brazil, 2013

Basic services include tracking and monitoring (vehicle speed limit, blocking, panic button, and vehicle status such as engine temperature). Services may also include 24-hour call center, tire change, recovery vehicle, and fuel cut off.

Trad

ition

al: I

ndep

ende

nt

(Afte

rmar

ket)

OEM

Par

tner

ship

s:

Inte

grat

ed A

ppro

ach—

feat

ures

ava

ilabl

e in

th

e ca

r

*May currently be in discussions with OEMs. **Refers primarily to features in-built in the car.Note: This exhibit focuses on the PC segment for personal use only.

Level 1: Level 0 ± insurance

Level 0: basic

services ± smartphone app/Internet connectivity

Ituran*Porto Seguro

Zatix* SascarAutotrac*CEABS

Segsat

WirelessCar

Basic services ± high-end telematics services**: eCall, bCall, RVD, concierge services, and turn-by-turn navigation

Car Alarm Systems (CAS)

Del

iver

y M

etho

d

Other offerings related to telematics services

PST

Grupo Tracker

2020

SPs expected to move towards more diversified products with strategic

OEM partnerships

Service providers expected to move

towards more diversified products

2020

CMV

Expected cooperation with infrastructure providers such as Cobra, OCTO Telematics, and C&C to offer high-end telematics services

SPs—Competitive LandscapeInfrastructure providers such as OCTO and Cobra are expected to play key roles in aiding SVT and monitoring providers to become high-end telematics providers with OEM partnerships by 2020.

Source: Frost & Sullivan