Embed Size (px)

Citation preview

Revenue outlook for renewable energyTristan Edis – Director Analysis & Advisory July 2016

Outline

• Number 1 question – How much money will I make in big solar?

• Answer – its complicated and highly uncertain.• The demand is there for projects via Renewable

Energy Target.• Current market prices for power + renewable

certificates (LGCs) should support projects.• But something odd is going on – high prices are not

stimulating long term contracts or new supply.• How could this unfold: Penalty vs LRMC vs

SRMC(price collapse)2

We need lots of new projects!

• RET market bound for severe shortage by 2018

3

Large-scale RET demand-supply balance

We need lots of new projects

• We need an awful lot of capacity and quickly

4

Historical MWs committed versus required to meet RET

Current prices support new supply• Prices heading to shortfall penalty ($92.86)

5

LGC spot price Jan 2015 – April 2016

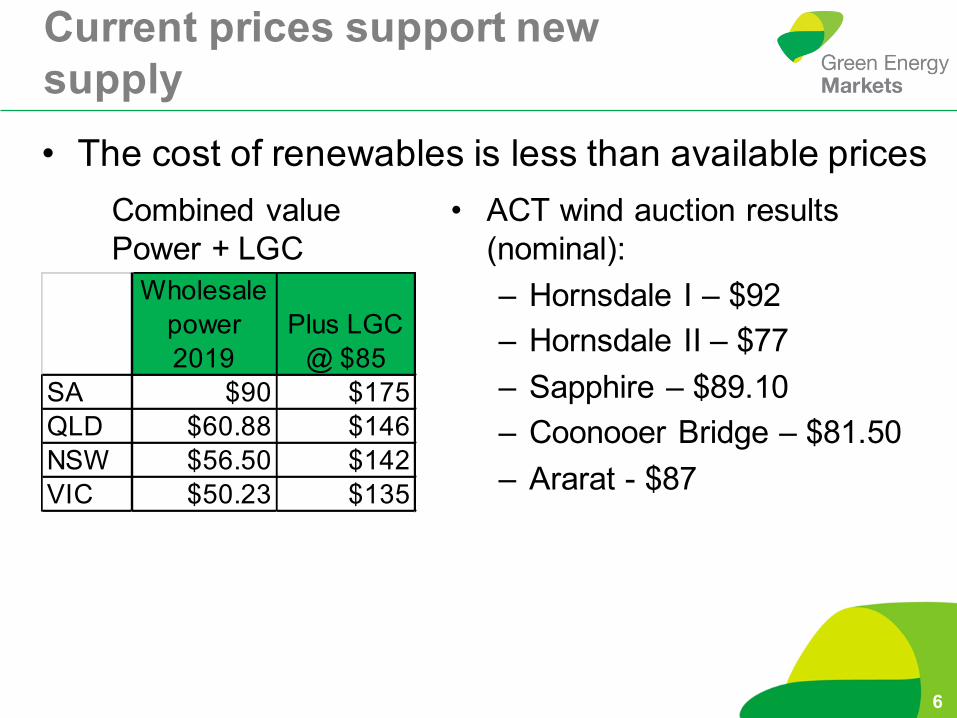

Current prices support new supply• The cost of renewables is less than available prices

6

• ACT wind auction results (nominal):– Hornsdale I – $92– Hornsdale II – $77– Sapphire – $89.10– Coonooer Bridge – $81.50– Ararat - $87

Combined value Power + LGC

Wholesale power 2019

Plus LGC @ $85

SA $90 $175QLD $60.88 $146NSW $56.50 $142VIC $50.23 $135

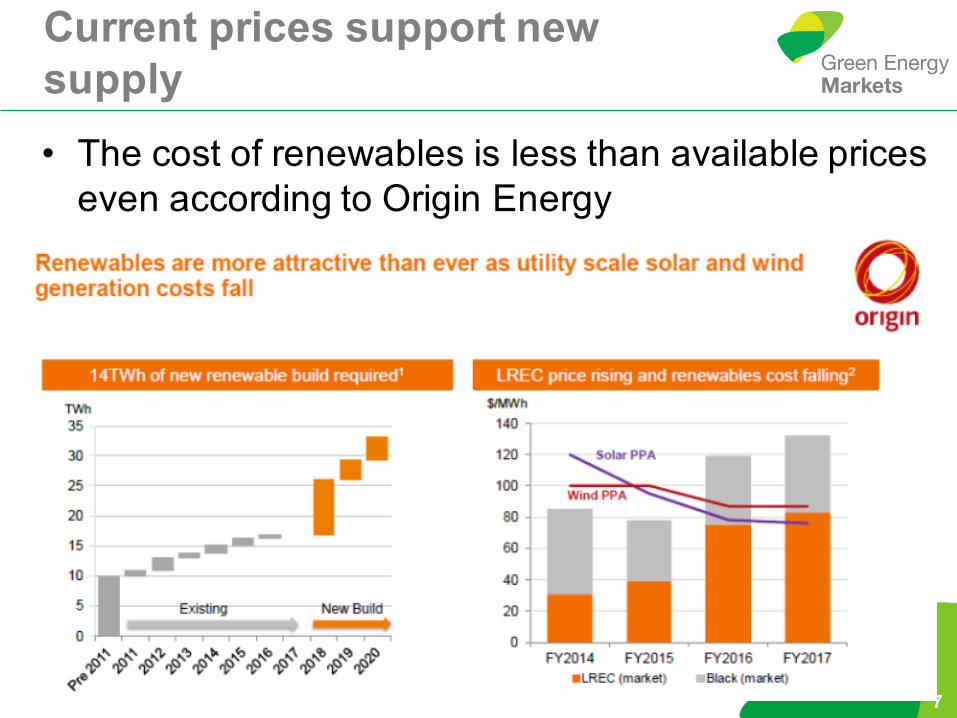

Current prices support new supply• The cost of renewables is less than available prices

even according to Origin Energy

7

Something odd is going on

• There are plenty of available projects so why so few commitments?

8

Megawatts of projects in development versus requirement

Required capacity

Something odd is going on

9

Retailers and other liable parties net LGC position to 2020

Searching for explanations

• Forget economics, think fear & power:– Fear of ghost of Abbott– Little finance available for projects w/o PPA.– Some retailers not deemed credit-worthy counter parties

by banks.– Credit worthy retailers not the ones hurt by penalty.– Retailer concern about impact of new supply on their

other generation assets.– Retailer fear they’ll be out of the money as solar costs

drop further.– Even slight oversupply leads to LGC price collapse.

10

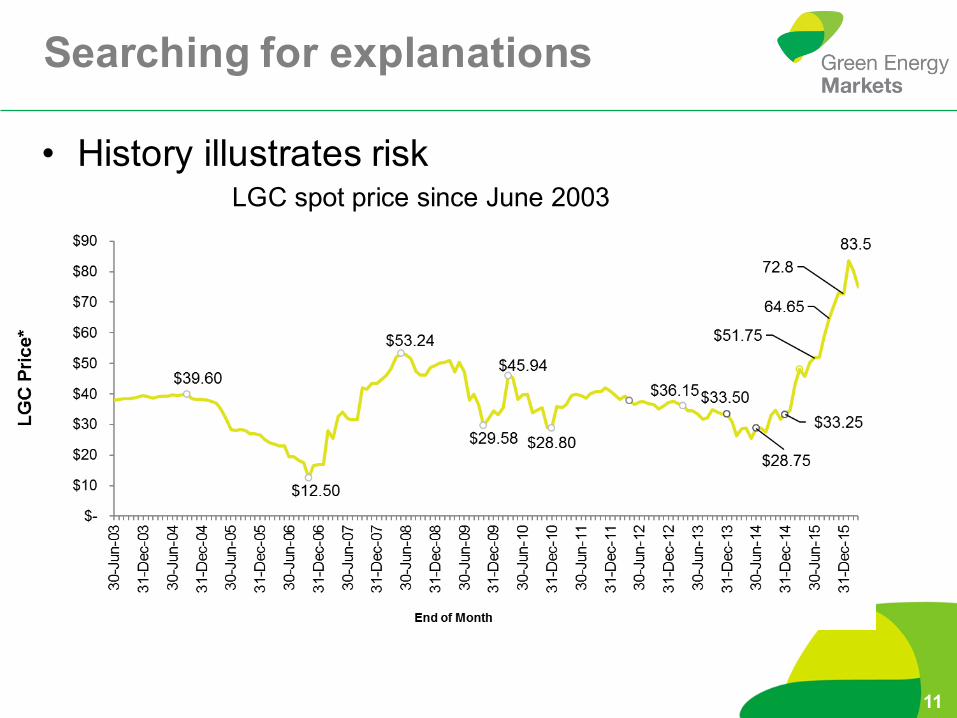

Searching for explanations

• History illustrates risk

11

LGC spot price since June 2003

What’s it mean for $$$

• Bad news if you are expecting a power retailer to underwrite your project

• Great news if you can get finance to go merchant• But how long can it last?

– Can power retailers and bankers constrain supply and hold back fundamental economics?

– Will state governments usurp power retailers providing long-term offtakes.

– Senate make up and role of Xenophon?– Power lobby success in getting media to blame SA power

problems on renewables.– Turnbull commitment to 2030 emission reduction target.

12

Some conceivable scenarios

• The love child of Abbott - $40 compensation• Victim of success – price collapse to option on new

policy• Killed by kindness – New non-RET support policy

drives:– Oversupply; or – Increase in wholesale power prices

• Do we need to also shut down coal, not just support renewables?– Theoretically: NO– Practically - maybe

13

What would we know?

• Green Energy Markets produces analysis on supply, demand and prices in Australia’s major carbon abatement certificate markets.

• CEO - Ric Brazzale: – Former head of Australia’s industry association for clean

energy sector beginning in the 1990’s when the Renewable Energy Target was conceived.

• Tristan Edis:– Climate Spectator, Grattan Institute, EY, Clean Energy

Council, Australian Government Greenhouse Office• Subscribers include power co’s, developers,

equipment suppliers and government.14

How we can help – market intelligence• Monthly updates on LGC and STC supply and price• Quarterly detailed reviews of committed supply and

demand• Quarterly reviews of who has got the LGCs, who

needs them, who’s buying and who’s selling.• Quarterly review of price drivers and future

pathways for LGCs

15