Embed Size (px)

Citation preview

DEBORAH WEINSWIGMANCHESTER 1

FBIC TOP IDEAS ON GLOBAL RETAIL & TECH

Deborah Weinswig

Executive Director – Head of Global Retail & Technology

Fung Business Intelligence Centre—Global Retail & Technology

DEBORAH WEINSWIGMANCHESTER 2

DEBORAH WEINSWIG • Executive Director and Head of Global Retail & Technology for the Fung Business Intelligence Centre

• Award-winning global retail analyst and a specialist in retail innovation and technology

• Mentor to Silicon Valley accelerators including Alchemist and Plug & Play and New York-based accelerator ERA (Entrepreneurship Roundtable Accelerator)

DEBORAH WEINSWIGMANCHESTER 3

What is FUNG BUSINESS INTELLIGENCE

CENTRE (FBIC)

• Established in 2000 and headquartered in Hong Kong

• FBIC has served as the knowledge bank and think tank for the Fung Group

• Collects and analyzes market data on sourcing, supply chains, distribution and retail

• Provides thought leadership on technology and other key issues

• New York-based Global Retail & Technology Team

• Follows broader retail and technology trends

• Provides advice and consultancy services to colleagues and business partners of the Fung Group

• London-based Research Team

DEBORAH WEINSWIGMANCHESTER 4

AGENDA • Retail Tech Ecosystem

• FBIC Top 10 Retail & Tech Trends

• The State of Global Apparel Retail

• Digital Commerce and Retail in the US

DEBORAH WEINSWIGMANCHESTER

RETAIL TECH ECOSYSTEM

5

DEBORAH WEINSWIGMANCHESTER

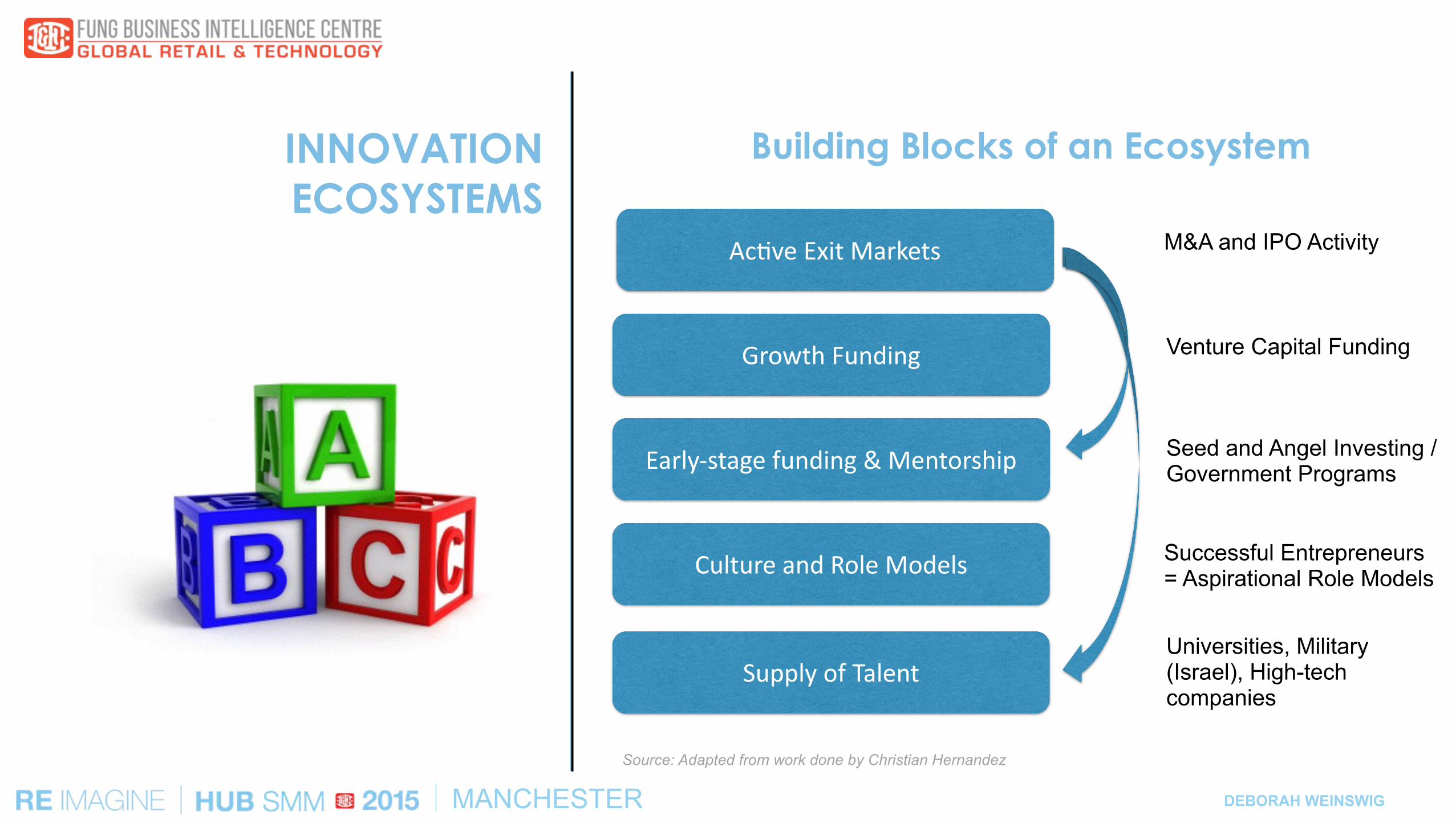

INNOVATION ECOSYSTEMS

Universities, Military (Israel), High-tech companies

Source: Adapted from work done by Christian Hernandez

Supply of Talent

Culture and Role Models

Early-‐stage funding & Mentorship

Growth Funding

Ac?ve Exit Markets

Venture Capital Funding

Seed and Angel Investing / Government Programs

Successful Entrepreneurs = Aspirational Role Models

M&A and IPO Activity

Building Blocks of an Ecosystem

DEBORAH WEINSWIGMANCHESTER

ACCELERATORS

!

Entrepreneurs Roundtable Accelerator in NY

TechStars in Colorado.

TrueStart in London

Cocoon in HK

!

!

The New York Fashion Tech Lab is an accelerator that is a result of a collaboration between the Partnership Fund for New York City, Springboard Enterprises, and major fashion retailers focused on targeting early and growth-stage companies that have developed innovations at the intersection of fashion, retail, and technology. Li & Fung’s PMD Program included startups under NYFTL (Laurianne Listo). GBG also mentored a startup.

7

Growing communities of accelerators and VC firms in the

US, the UK and Hong Kong

DEBORAH WEINSWIGMANCHESTER 8

FBIC TOP 10 RETAIL & TECH TRENDS

DEBORAH WEINSWIGMANCHESTER 9

FBIC TOP 15 RETAIL & TECH TRENDS

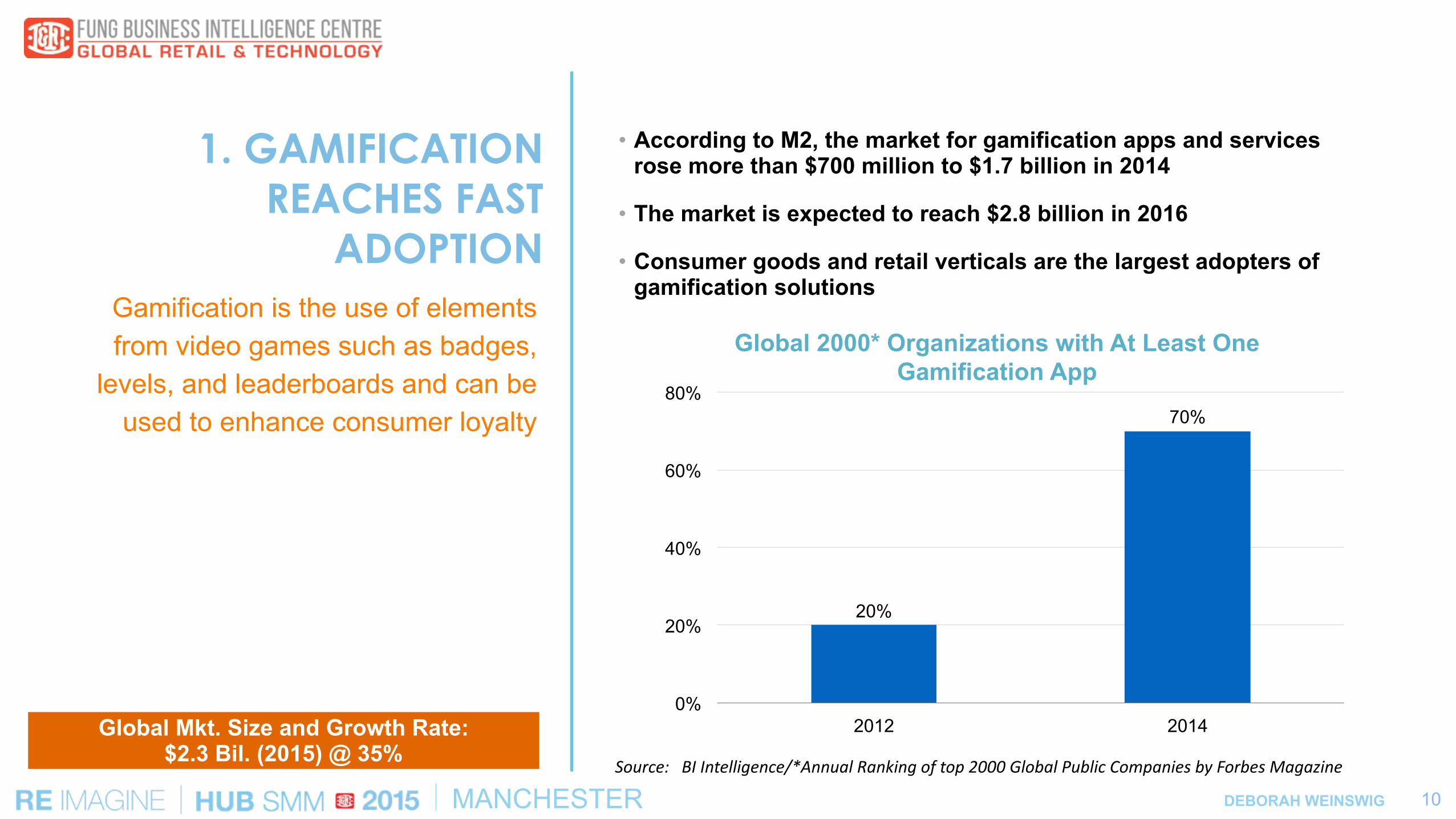

1. GAMIFICATION reaches fast adoption

2. The RENTING ECONOMY– now an option even for apparel

3. The SHARING ECONOMY – UBERIFICATION of services

4. The SUBSCRIPTION ECONOMY – chipping away at brick-and-mortar stores

5. SOCIAL MEDIA becomes a source of consumer data

6. SMARTPHONES are becoming the hub for digital beauty

7. WEARABLE TECH is already here for early adopters

8. BEACONS and location-based marketing

9. NANOTECHNOLOGY

10. 3D PRINTING

DEBORAH WEINSWIGMANCHESTER 10

1. GAMIFICATIONREACHES FAST

ADOPTION

Source: BI Intelligence/*Annual Ranking of top 2000 Global Public Companies by Forbes Magazine

• According to M2, the market for gamification apps and services rose more than $700 million to $1.7 billion in 2014

• The market is expected to reach $2.8 billion in 2016

• Consumer goods and retail verticals are the largest adopters of gamification solutions

Gamification is the use of elements from video games such as badges,

levels, and leaderboards and can be used to enhance consumer loyalty

Global Mkt. Size and Growth Rate: $2.3 Bil. (2015) @ 35%

20%

70%

0%

20%

40%

60%

80%

2012 2014

Global 2000* Organizations with At Least One Gamification App

DEBORAH WEINSWIGMANCHESTER

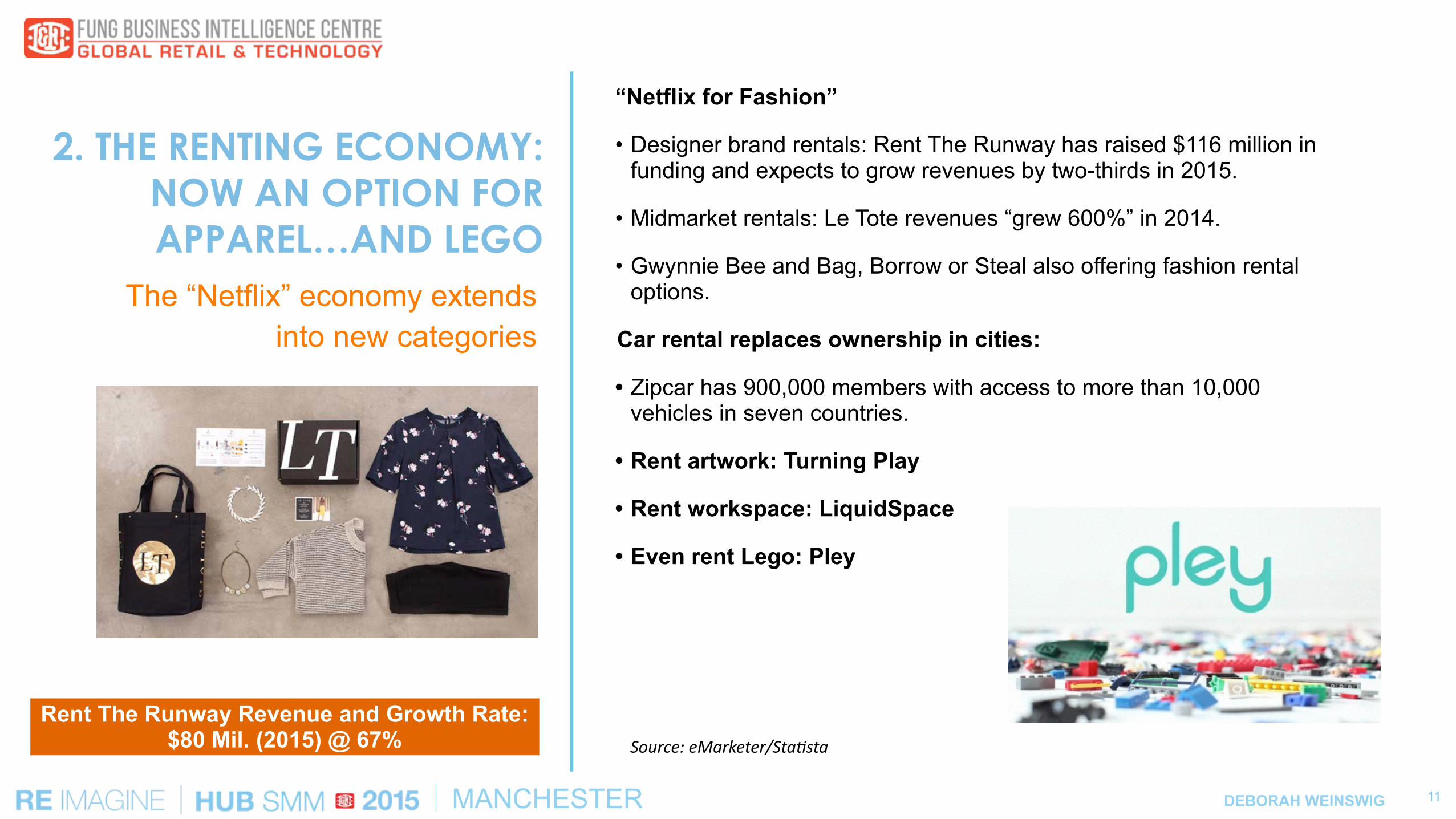

2. THE RENTING ECONOMY: NOW AN OPTION FOR APPAREL…AND LEGO

“Netflix for Fashion”

• Designer brand rentals: Rent The Runway has raised $116 million in funding and expects to grow revenues by two-thirds in 2015.

• Midmarket rentals: Le Tote revenues “grew 600%” in 2014.

• Gwynnie Bee and Bag, Borrow or Steal also offering fashion rental options.

Car rental replaces ownership in cities:

• Zipcar has 900,000 members with access to more than 10,000 vehicles in seven countries.

• Rent artwork: Turning Play

• Rent workspace: LiquidSpace

• Even rent Lego: Pley

11

Source: eMarketer/StaDsta

The “Netflix” economy extends into new categories

Rent The Runway Revenue and Growth Rate: $80 Mil. (2015) @ 67%

DEBORAH WEINSWIGMANCHESTER 12

3. THE SHARING ECONOMY:

UBERFICATION OF SERVICES

• Uber is the most visible player (and driver) of the “sharing economy”

• Changing consumer mindsets will challenge retailers

• Opportunities for retailers: How much is convenience worth?

Uber Revenue and Growth Rate: $10 Bil. (2015) @ 300%

DEBORAH WEINSWIGMANCHESTER

4. THE SUBSCRIPTION ECONOMY:

CHIPPING AWAY AT BRICK-AND-MORTAR

• Consumers love the convenience and dependability of the service

• Retailers love subscription models as a source of recurring revenue

• Consumers find value in avoiding the drudgery of shopping for everyday commodity items

• Birchbox opened first store in New York’s SoHo in July 2014

13

Global Mkt. Size and Growth Rate: $3 Bil. (2015) @ 30%

Due to their convenience, value, and variety, subscription

businesses are slowly nibbling away at retailers’ businesses

DEBORAH WEINSWIGMANCHESTER 14

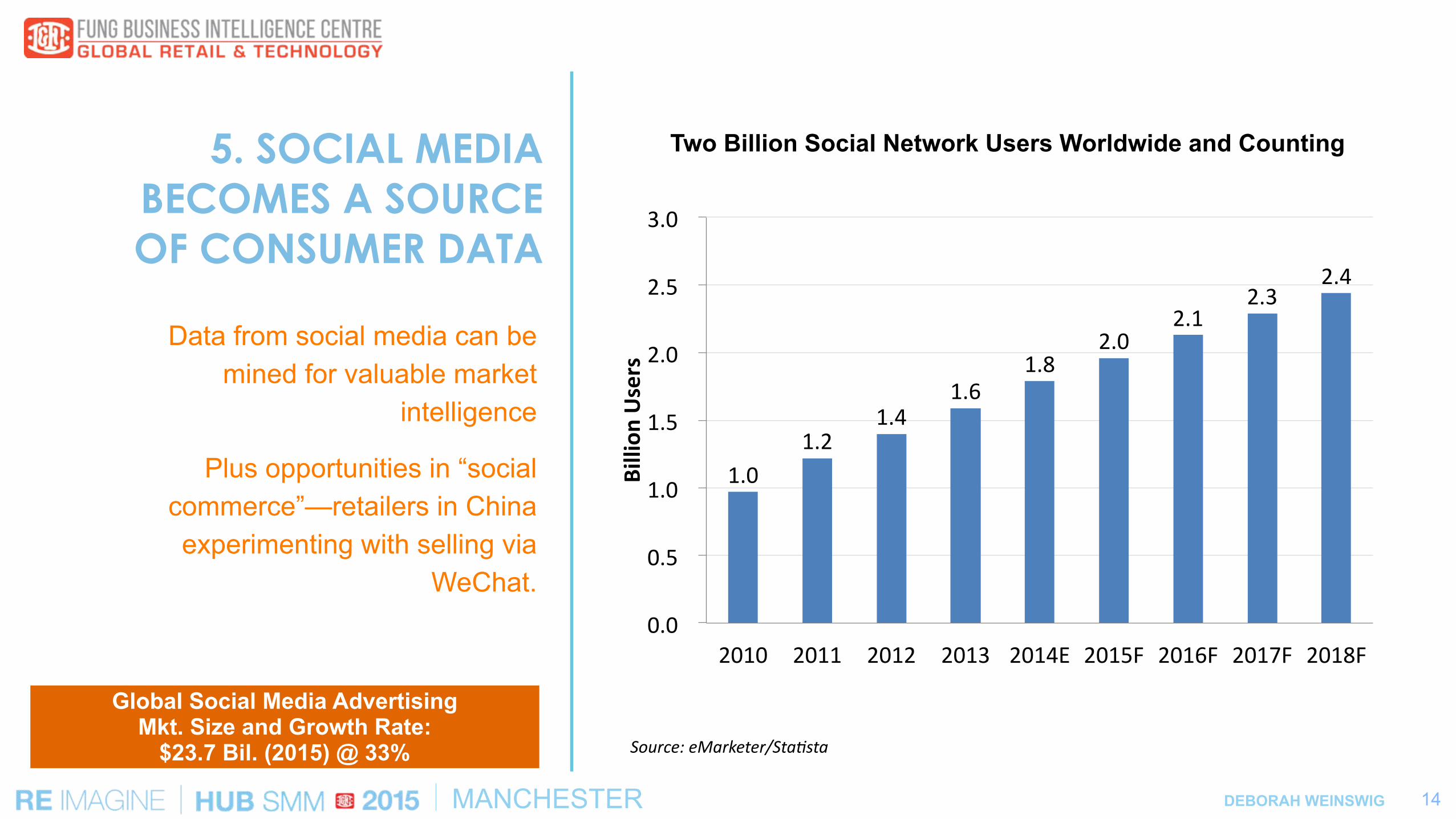

5. SOCIAL MEDIA BECOMES A SOURCE OF CONSUMER DATA

Source: eMarketer/StaDsta

Two Billion Social Network Users Worldwide and Counting

Data from social media can be mined for valuable market

intelligence

Plus opportunities in “social commerce”—retailers in China experimenting with selling via

WeChat.

Global Social Media Advertising Mkt. Size and Growth Rate:

$23.7 Bil. (2015) @ 33%

1.0$1.2$

1.4$1.6$

1.8$2.0$

2.1$2.3$

2.4$

0.0$$

0.5$$

1.0$$

1.5$$

2.0$$

2.5$$

3.0$$

2010$ 2011$ 2012$ 2013$ 2014E$ 2015F$ 2016F$ 2017F$ 2018F$Billion

&Users&

DEBORAH WEINSWIGMANCHESTER 15

6. SMARTPHONES ARE BECOMING THE HUB FOR DIGITAL BEAUTY

Several digital technologies are being applied to beauty, including:

• Facial recognition and mapping

• Color matching

• Augmented reality

• Smartphone appsSmartphones are becoming for digital hub for digitally trying on and visualizing beauty products

Tapping the growing, $400 billion global beauty market (2014).

Global Digital Beauty Mkt. Size and Growth Rate:

$50 Bil. (2015) @ 20%

DEBORAH WEINSWIGMANCHESTER

7.WEARABLE TECH IS ALREADY HERE FOR

EARLY ADOPTERS

• Wearable tech has existed for centuries: wristwatches, hearing aids, pacemakers, and headphones

• Advances in electronics, miniaturization, and sensors are making these devices wearable and inexpensive

• Smartwatches are here today … for early adopters

• Health and wellness as well as industrial are huge future applications for wearables

• "Moore's law" is the observation that, over the history of computing hardware, the number of transistors in a dense integrated circuit doubles approximately every two years.

Moore’s Law and advances in sensors and manufacturing are

putting intelligent networked devices into the consumer arena

Global Mkt. Size and Growth Rate: $2 Bil. (2015) @ 40%

16

DEBORAH WEINSWIGMANCHESTER 17

8. BEACONS AND LOCATION-BASED

MARKETING

• What is a beacon?

• Ideal solution for improving in-store retail experience

• 2016 is expected to be the Year of the Beacon

• US installed base expanding rapidly, but consumer response is key to further penetration

Beacon-Influenced Retail Sales Mkt. Size and Growth Rate:

$41 Bil. (2015) @ 100+% Source: Bi Intelligence, Feb. 9, 2015

$41.0

$444.0

2015 2016

Beacon-Influenced In-Store Retail Sales ($ Billion)

DEBORAH WEINSWIGMANCHESTER

9. NANOTECH …IN TEXTILES

• Nanotechnology can make textiles multifunctional and enable the manufacture of smart fabrics

• Nanomaterials give textiles properties such as windproofing and waterproofing, wrinkle and stain prevention, electrostatic protection, and odor resistance

Global Mkt. Size and Growth Rate: $568 Mil. (2015) @ 25%

Nanotech gives textiles increased performance and additional

properties such as wind- and waterproofing

18

DEBORAH WEINSWIGMANCHESTER

… AND IN BEAUTY• Nanotechnology and nanomaterials are used in moisturizers, hair-care

products, make-up and sunscreen

MAIN USES:

• UV filters—some nanoparticles act as UV filters; some particles transmit light, and consumes equate clear products with being natural and clean

• Delivery vehicles—liposomes and niosomes are used for cosmetic delivery

• Encapsulation—polymer capsules used to transport vitamins

Global Mkt. Size and Growth Rate: $270 Mil. (2015) @ 20%

Nanomaterials are used in cosmetics, haircare, sunscreen,

and anti-aging products

19

DEBORAH WEINSWIGMANCHESTER

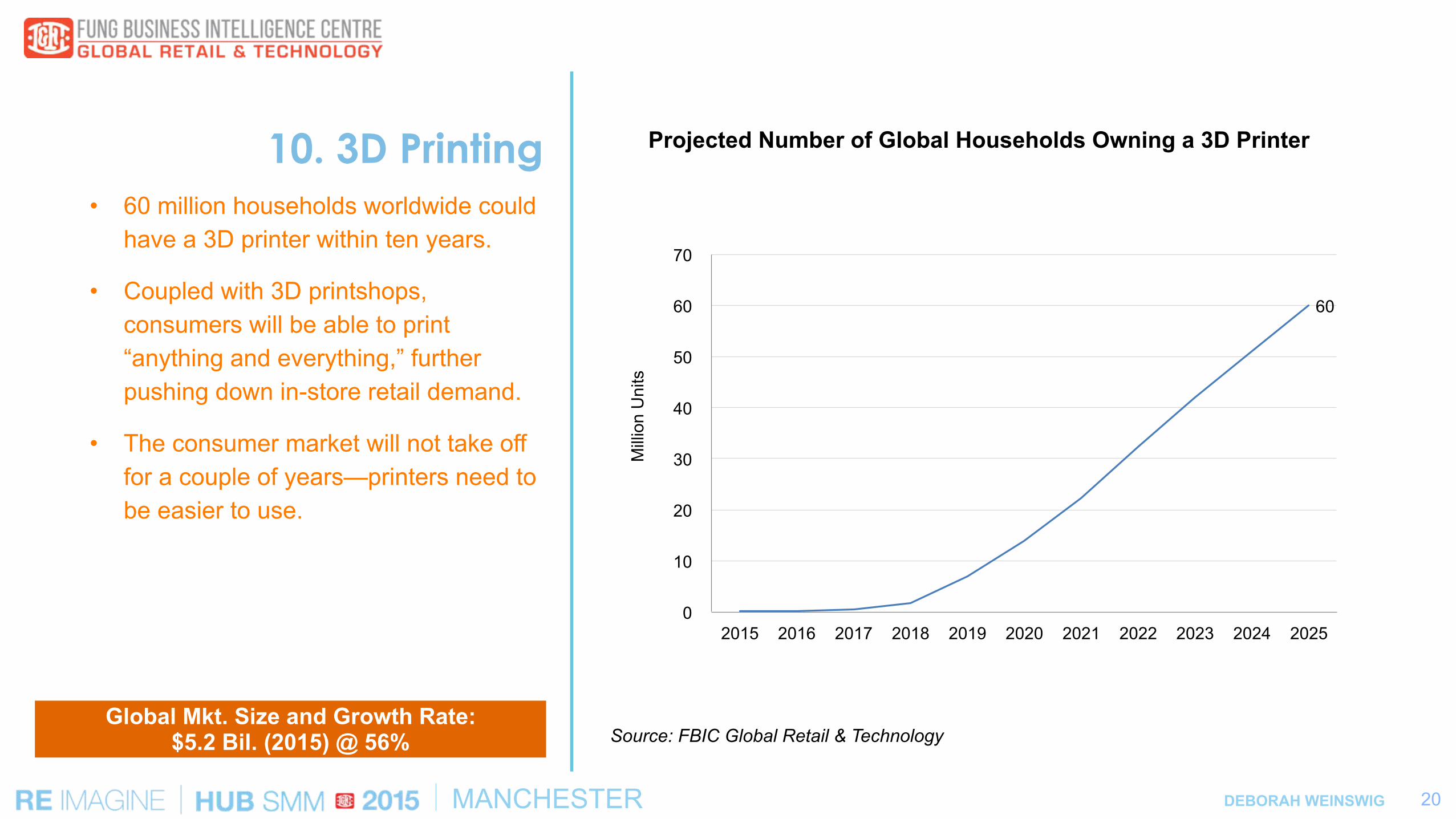

10. 3D Printing Projected Number of Global Households Owning a 3D Printer

• 60 million households worldwide could have a 3D printer within ten years.

• Coupled with 3D printshops, consumers will be able to print “anything and everything,” further pushing down in-store retail demand.

• The consumer market will not take off for a couple of years—printers need to be easier to use.

Source: FBIC Global Retail & Technology

20

Global Mkt. Size and Growth Rate: $5.2 Bil. (2015) @ 56%

60

0

10

20

30

40

50

60

70

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 M

illio

n U

nits

DEBORAH WEINSWIGMANCHESTER

THE STATE OF GLOBAL APPAREL RETAIL

21

DEBORAH WEINSWIGMANCHESTER 22

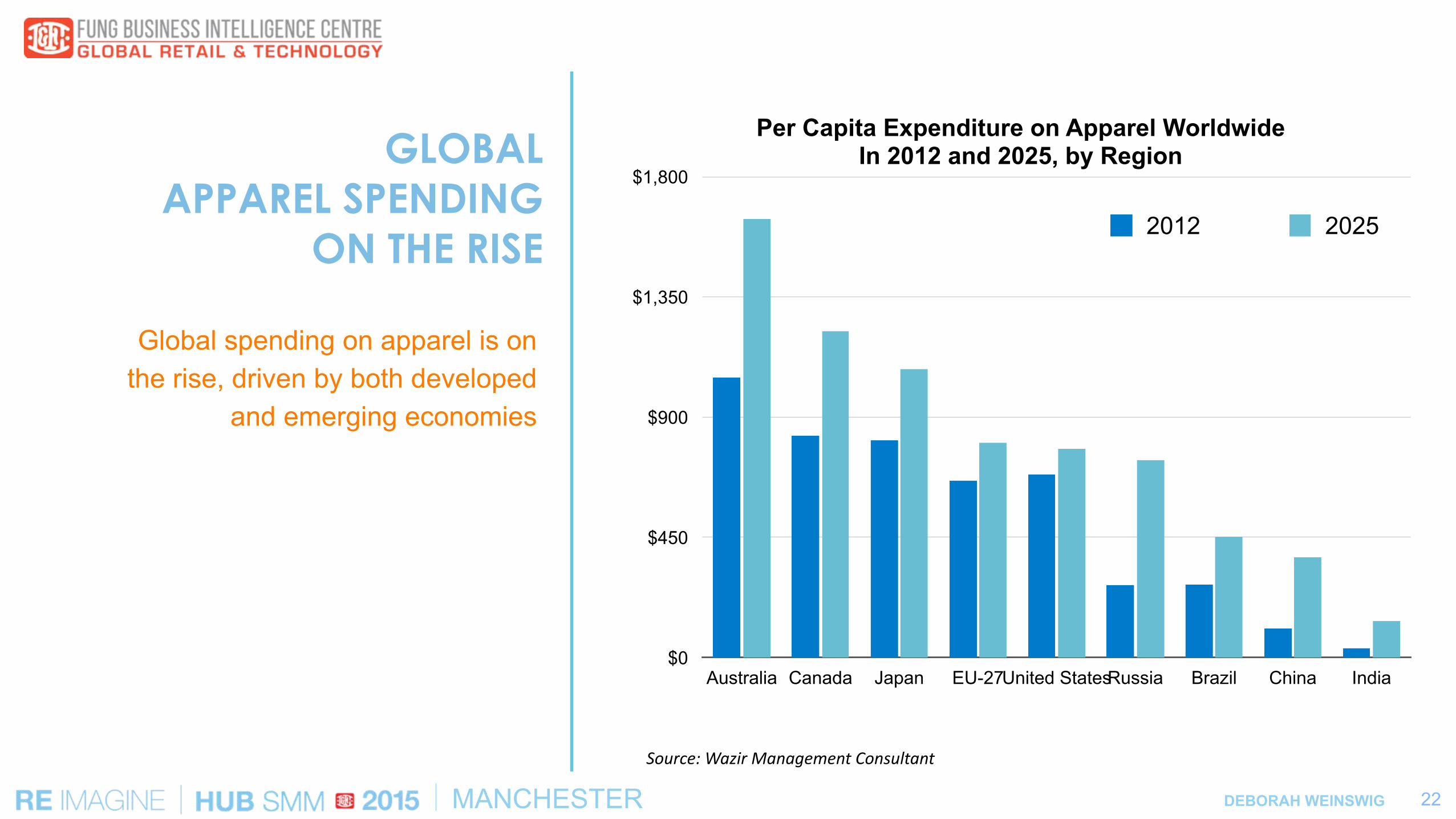

GLOBAL APPAREL SPENDING

ON THE RISE

$0

$450

$900

$1,350

$1,800

Australia Canada Japan EU-27United StatesRussia Brazil China India

2012 2025

Per Capita Expenditure on Apparel Worldwide In 2012 and 2025, by Region

Source: Wazir Management Consultant

Global spending on apparel is on the rise, driven by both developed

and emerging economies

DEBORAH WEINSWIGMANCHESTER

Company

Sales Growth YoY

Total Sales ($ Mil.) *

Gross Margin

US Store Count 2014

US % of Total Stores 2014

Total Global Stores 2014

Total Global Stores 2013

Store # Growth

H&M 18% 20,352 58.8% 356 10% 3,511 3,132 12%

Inditex 11% 21,066 58.3% 55 0.8% 6,683 6,340 5%

17% 8,067 N/A O NM 278 253 10%

Uniqlo 21% 10,043 50.6% 42 1.4% 3,015 2,449 23%

INTERNATIONAL INVADERS SET TO

THRIVE IN US

23

Selected International Brands (FY2014)

• H&M focuses store expansion in US and China markets

• Primark plans 8 US stores by 2016

• Uniqlo will open 5 US stores in spring/summer 2015

Source: Company reports * Sales translated to USD from reporting currency according to EOP FX rates

DEBORAH WEINSWIGMANCHESTER

PRIMARK ARRIVES AT DOWNTOWN CROSSING,

BOSTON THIS FALL

24

• Primark has secured a total of eight properties with the equivalent of 500,000 sq. ft. of retail space (about equal to Zara’s US exposure).

• The semi-disposable clothing with a convincing fashion edge drives weekly visits by Primark’s loyal shoppers—it doesn’t sell online.

• TJX Companies CEO Carol Meyrowitz, on TJX May 19 conference call:

“So I've said it many times. We love being next to Primark and fast fashion because it really just drives the traffic along with the other off-pricers, so it just creates a mecca for us.”

DEBORAH WEINSWIGMANCHESTER

A TWO-TIERED ECONOMY

A widening bifurcation between low and high income households

drives the success of value retailers, fast fashion and off-price retailers as well as luxury brands

while mid-tier retailers suffer.

25

Neiman Marcus Saks

Nordstrom Bloomingdale’s

Macy’s Dillard’s

SVU (former Albertsons Stores) Kroger Kohl’s

Safeway JCPenny

Drugstores (CVS/WAG) Clubs (BJ/COST/Sam’s Club)

Target Walmart

Kmart/Sears Dollar Stores

SVU (Sav-A-Lot)

DEBORAH WEINSWIGMANCHESTER

... AND DEPARTMENT STORES TESTING

OFF-PRICE FORMAT

• Kohl’s will open a single store selling returned items in Cherry Hill, NJ in early June 2015

• Macy’s discount chain “Macy’s Backstage” will open four stores in greater New York City area in fall 2015

26

!

Department stores are offering below-retail prices through off-price chains

Both Kohl’s and Macy’s are opening off-price stores this year

DEBORAH WEINSWIGMANCHESTER

AND INTERNET PURE PLAYS ARE BOOMING

• Zalando: 26% sales growth to €2.2 billion in 2014.

• ASOS: 27% sales growth to £976 million in 2014.

• Zulily: 73% sales growth to $1.2 billion in 2014.

• Amazon 1Q sales up another 15%. Amazon now growing its offer in fashion, its “fastest-growing category”.

27

DEBORAH WEINSWIGMANCHESTER 28

DIGITAL COMMERCE AND RETAIL IN THE US

DEBORAH WEINSWIGMANCHESTER 29

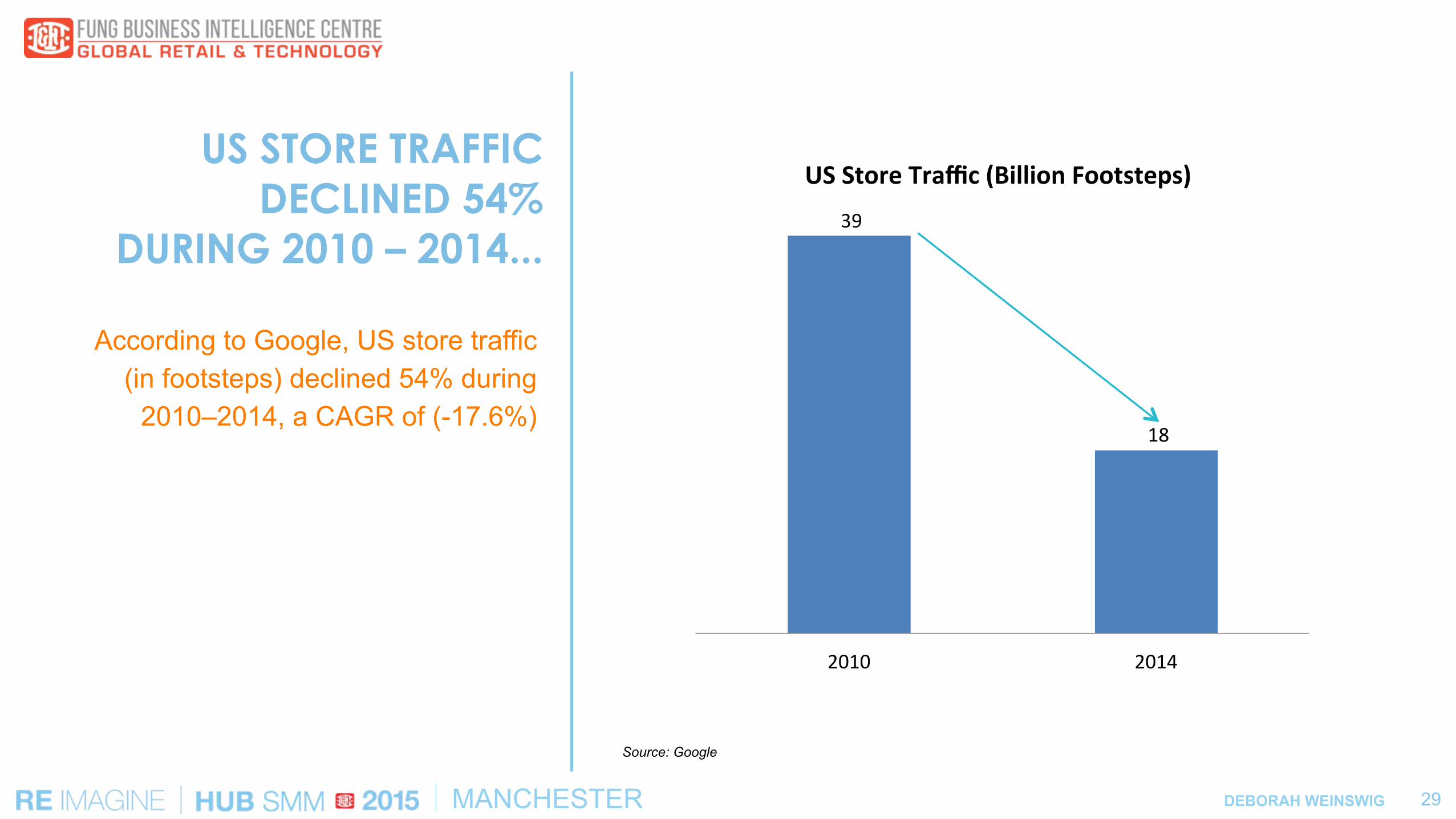

US STORE TRAFFIC DECLINED 54%

DURING 2010 – 2014...

According to Google, US store traffic (in footsteps) declined 54% during

2010–2014, a CAGR of (-17.6%)

!39!!

!18!!

2010! 2014!

US#Store#Traffic#(Billion#Footsteps)##

Source: Google

DEBORAH WEINSWIGMANCHESTER 30

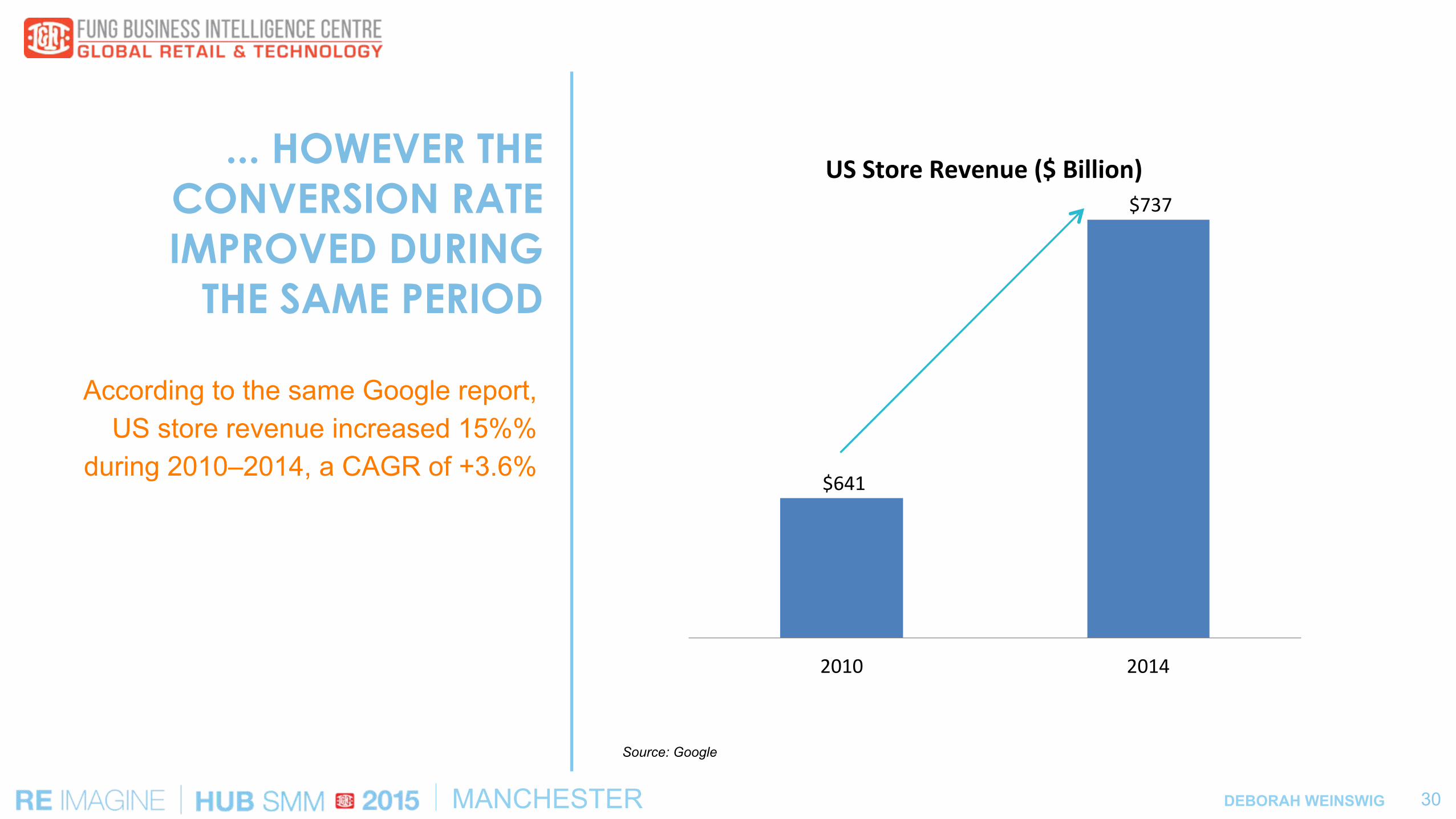

... HOWEVER THE CONVERSION RATE IMPROVED DURING

THE SAME PERIOD

!$641!!

!$737!!

2010! 2014!

US#Store#Revenue#($#Billion)##

According to the same Google report, US store revenue increased 15%%

during 2010–2014, a CAGR of +3.6%

Source: Google

DEBORAH WEINSWIGMANCHESTER 31

THERE IS AN INCREDIBLE DIGITAL

OPPORTUNITY …

93%

Sales will be Offline

70%

Sales will be digitally influenced

Source: Google

Retailers need to embrace the Internet and digital in the future, as nearly all sales will be offline

and the vast majority will be digitally influenced

DEBORAH WEINSWIGMANCHESTER 32

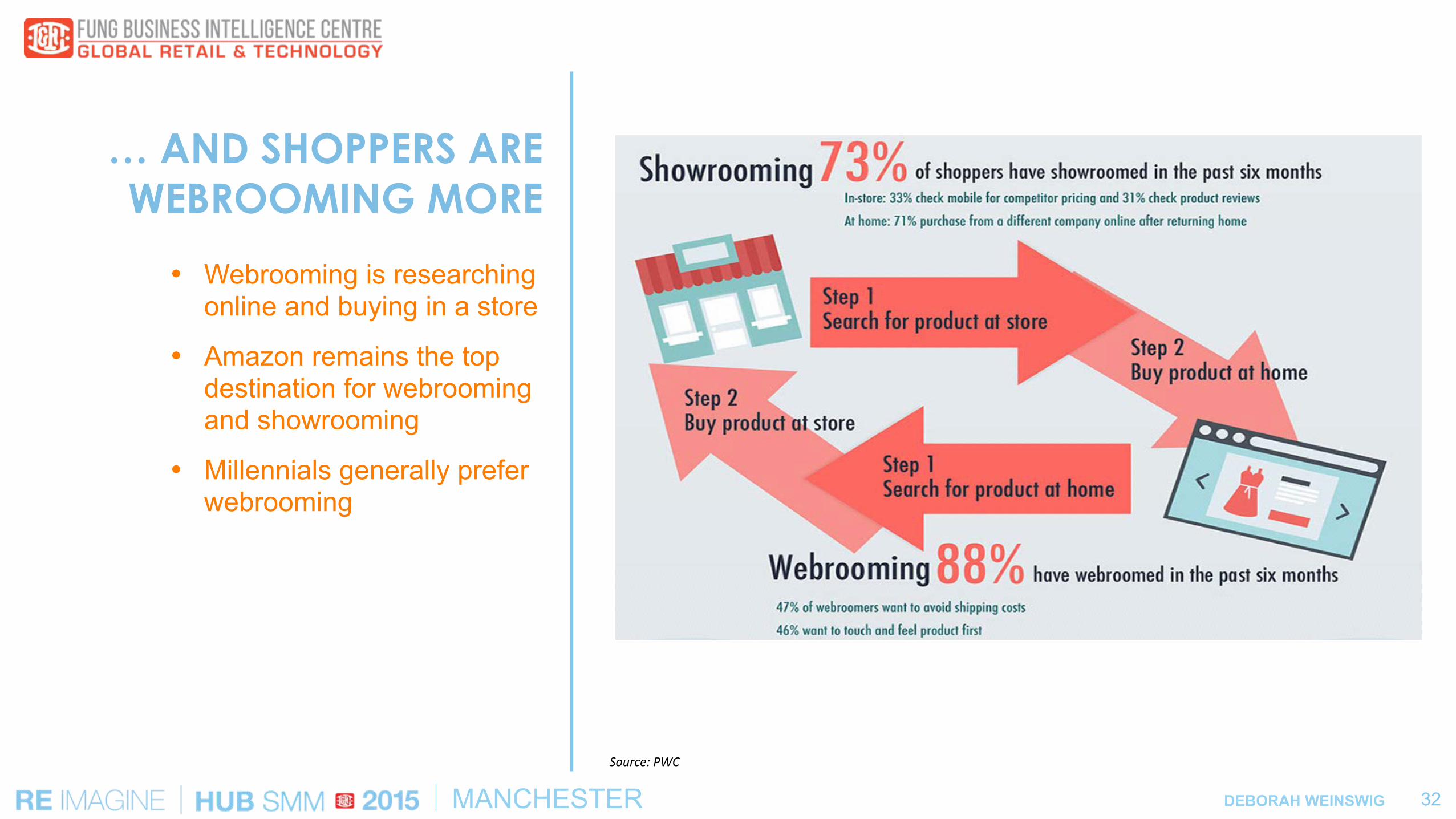

… AND SHOPPERS ARE WEBROOMING MORE

Source: PWC

� Webrooming is researching online and buying in a store

� Amazon remains the top destination for webrooming and showrooming

� Millennials generally prefer webrooming

DEBORAH WEINSWIGMANCHESTER 33

LUXURY CONTINUES TO

UNDERPERFORM

Source:SpendingPulse/Mastercard Advisors

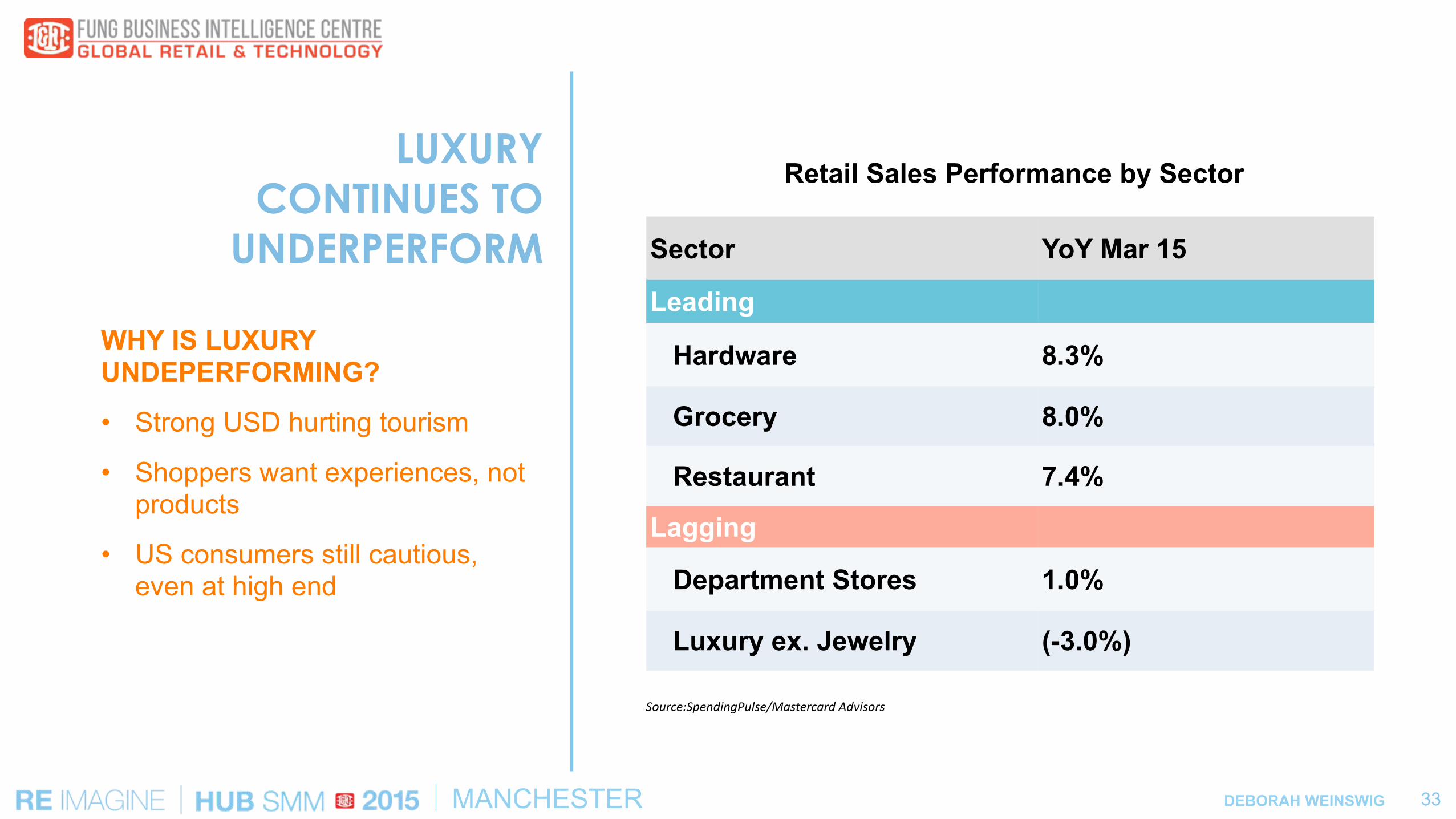

WHY IS LUXURY UNDEPERFORMING?

• Strong USD hurting tourism

• Shoppers want experiences, not products

• US consumers still cautious, even at high end

Retail Sales Performance by Sector

Sector YoY Mar 15

Leading

Hardware 8.3%

Grocery 8.0%

Restaurant 7.4%

Lagging

Department Stores 1.0%

Luxury ex. Jewelry (-3.0%)

DEBORAH WEINSWIGMANCHESTER 34

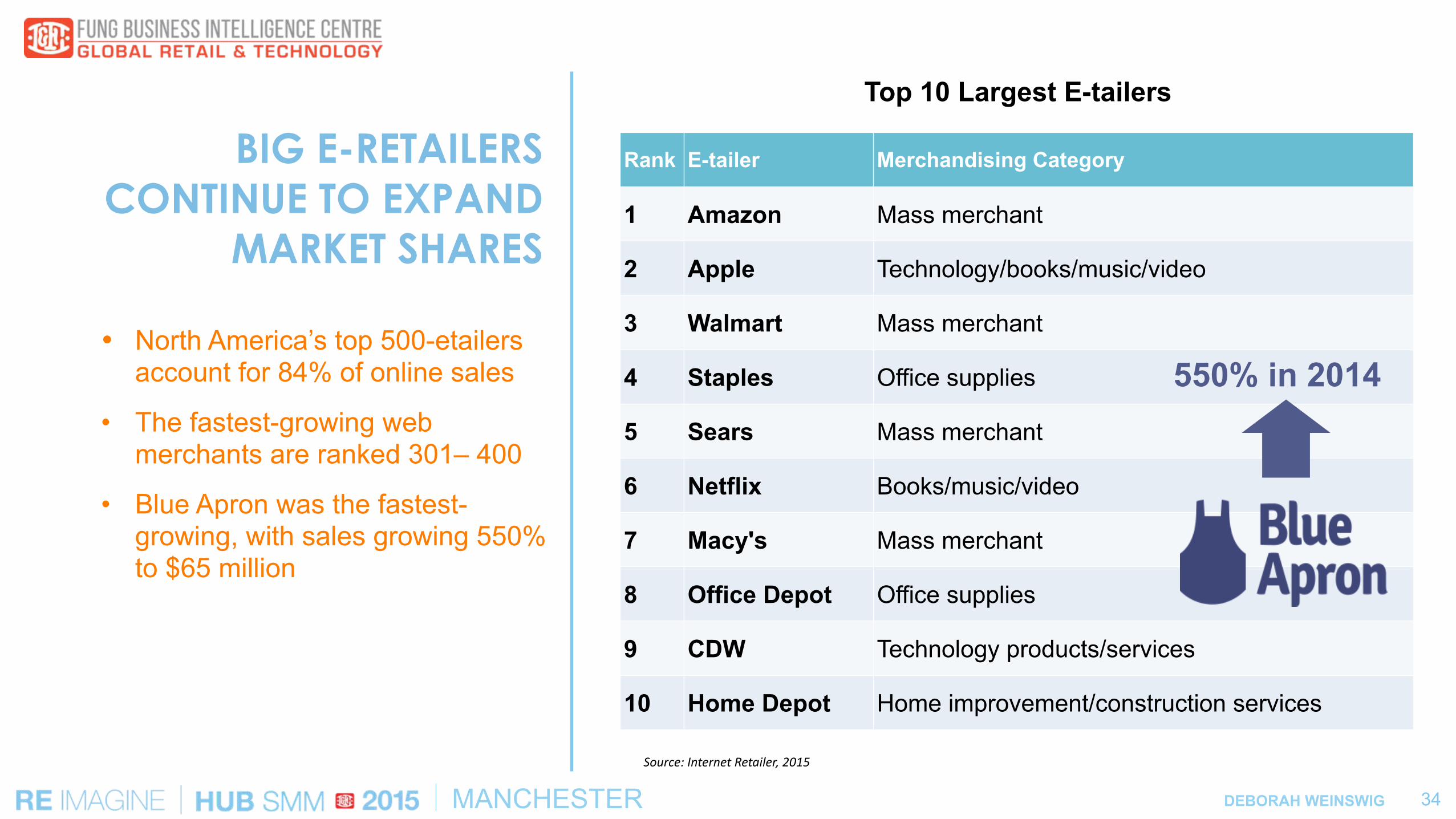

BIG E-RETAILERS CONTINUE TO EXPAND

MARKET SHARES

Source: Internet Retailer, 2015

� North America’s top 500-etailers account for 84% of online sales

• The fastest-growing web merchants are ranked 301– 400

• Blue Apron was the fastest-growing, with sales growing 550% to $65 million

Rank E-tailer Merchandising Category

1 Amazon Mass merchant

2 Apple Technology/books/music/video

3 Walmart Mass merchant

4 Staples Office supplies

5 Sears Mass merchant

6 Netflix Books/music/video

7 Macy's Mass merchant

8 Office Depot Office supplies

9 CDW Technology products/services

10 Home Depot Home improvement/construction services

550% in 2014

Top 10 Largest E-tailers

DEBORAH WEINSWIGMANCHESTER

RETAIL REAL ESTATE SUPPLY CONDITIONS

1Q ANNOUNCED STORE CLOSURES

Store closures concentrated in home entertainment and apparel, which were 96% of 1Q announcements.

Space associated with 3,558 announced closings represents 0.1% of

total inventory of US retail space.

Retailer Segment No. of Closings

RadioShack Home Entertainment 1,784

Wet Seal Apparel 338

Deb Shops Apparel 287

Body Central Apparel 256

Cache Apparel 153

Jones NY Apparel 127

The Children’s Place Apparel 125

Chico’s Apparel 120

Izod Apparel 120

Fresh & Easy Grocery Stores 50

Selected Store Closures 1Q2015

Source: : ICSC Research PNC Real Estate Research

35

DEBORAH WEINSWIGMANCHESTER

GAP PLANS FURTHER NORTH AMERICAN STORE

RATIONALIZATION FOR GAP BRAND

• Another 175 North American Gap stores are scheduled to close, 140 in 2015, representing approximately $300 million in sales.

• Gap’s North American Store fleet will consist of approximately 800 stores upon completion

• Full price locations will decline to about 500 stores and the remainder Gap Factory and Gap Outlets.

• its June 16 Analyst Day, management’s focus on driving product acceptance doesn’t comport with the structural competitive environment.

• The real threat to Gap is the rise of deep value retailers using more efficient supply chains and store models that is driving industry prices and profits lower.

36

DEBORAH WEINSWIGMANCHESTER 37

THANK YOU